Embed Size (px)

Citation preview

PERFECT COMPETITION

-Featuring Milk Market-

Subject: Microeconomic

Lecturer: Ms. Trần Thị Minh Ngọc

Date: August 10th, 2013

Group members:

Trần Nguyên Phương

Huỳnh Minh Quân

Nguyễn Quang Tuấn

Trương Ngọc Lan Thanh

Nguyễn Minh Nguyên

Contents• Theory of Perfect

Competition

• Features of Milk

products

Theory: Definition

Perfect Competition (which is sometimes known as

“Pure Competition”) is a type of market

characterized by:

•A very large number of small producers or sellers,

•A standardized, homogeneous product

•The inability of individual sellers to influence price

•The free entry and exit of sellers in the market

unnecessary nonprice actions.

Theory: Definition

(1) Buyers and sellers are too numerous and too small to have any degree of individual control over prices

(2) All buyers and sellers seek to maximize their profit (income)

(3) Buyers and seller can freely enter or leave the market

(4) All buyers and sellers have access to information regarding availability, prices, and quality of goods being traded

(5) All goods of a particular nature are homogeneous, hence substitutable for one another.

Theory: Getting to know

Generally, a perfectly competitive market exists

when every participant is a "price taker", and no

participant influences the price of the product it

buys or sells.

Theory: Getting to knowSpecific characteristics may include:• Infinite buyers and sellers – An infinite number of consumers with the willingness and ability to buy the product at a certain price, and infinite producers with the willingness and ability to supply the product at a certain price.

• Zero entry and exit barriers – A lack of entry and exit barriers makes it extremely easy to enter or exit a perfectly competitive market.

• Perfect factor mobility – In the long run factors of production are perfectly mobile, allowing free long term adjustments to changing market conditions.

• Perfect information - All consumers and producers are assumed to have perfect knowledge of price, utility, quality and production methods of products.

Theory: Getting to know

• Zero transaction costs - Buyers and sellers do not incur costs in making an exchange of goods in a perfectly competitive market.

• Profit maximization - Firms are assumed to sell where marginal costs meet marginal revenue, where the most profit is generated.

• Homogenous products - The qualities and characteristics of a market good or service do not vary between different suppliers.

• Non-increasing returns to scale - The lack of increasing returns to scale (or economies of scale) ensures that there will always be a sufficient number of firms in the industry.

• Property rights - Well defined property rights determine what may be sold, as well as what rights are conferred on the buyer.

Theory: Getting to know

Examples of markets in perfect competition areextremely rare. Numerous markets in the retail,service and agricultural sectors approach perfectcompetition best. But, in the agricultural sector,government support price programs distort themarket mechanism. Notwithstanding the lack ofgood examples, this form of market is importantbecause of its.

Features of Milk Products

Q: Why Milk Market is considered as the Perfect Competition?

A: Because a Milk Market assumes:

•Infinite buyers and producers

•Buyers and sellers are well informed

•Even though there are exceptions in Milk identical (organic, 1%, reduced fat etc.), different companies do not produce different "types" of milk

•There are no major barriers preventing the free market to enter/exit.

NUMBER OF FIRMS

• Theory

The very large number of firms in perfect competition implies that each individual firm is very small in comparison to the total market. Indeed, if one firm were to become significantly large, it would dominate the market and competition would be eliminated or at least diminished.

• Feature

In the milk production segment of agriculture, farms are usually small. They are especially small compared to the size of the entire market for milk. Note that the milk distributors are occasionally large, but not the productive farms.

STANDARDIZED PRODUCT• Theory

The product in perfect competition is said to be standardized(or homogeneous)=> It does not make any difference to customers which specific firm sells the product: It is absolutely identical. This is the main distinction between perfect competition and monopolistic competition: once some differences can be recognized by customers, firms acquire power over these customers.

• Feature

Milk is a uniform and homogeneous product. It is not possible to make a distinction between the milk of one farm and another. Thegovernment has indeed set standards of quality, fat content and cleanliness.

PRICE TAKER• Theory

The firms in perfect competition have no power over price: they have to sell at the going market price. The firms in perfect competition are said to be price takers. Should a firm attempt to raise the price by the smallest possible amount, customers would not buy from it because they could buy the same product from other firms. Lowering the price is also not necessary because the firm can already sell all its output at the going price.

• Feature

A milk producer who would try to raise his/her revenues by increasing the price for milk, would find the company collecting the milk in that region unwilling to buy his/her milk any longer. One individual farmer is thus unable to affect the price of milk in the entire market.

ENTRY AND EXIT

• ENTRY Should demand be above the minimum of average total cost, pureprofit would exist for firms in perfect competition. This profit would attract new firms to the industry. Such entry of new firms is not impeded by any entry barriers in industries in perfect competition. The new firms would increase the total market supply and drive the price down. The lower price pushes the demand for each firm down toward or even below the equilibrium minimum average total cost point.

• EXIT Should the demand be below the minimum of average total cost, losses of firms would force some firms to leave the industry. As firms leave, a decreasing total supply pushes price back up. The increasing price lifts the demand curves for individual firms upward toward or even above the equilibrium point. Firms departure or entry will continue until the price settles to be just equal to minimum average cost.

NON-PRICE ACTION

• Theory

Non-price actions such as advertising, service after sale or warranty, are not necessary in perfect competition because the firm can already sell all its output at the going price, and incurring additional expense would only make it unprofitable (Non-price action for the entire industry may however be useful).

• Feature

A single milk producer cannot possibly influence the consumption of milk at large, and needs not advertise. An association of milk producers or a large milk distributor may, however, be in a position to use advertisement effectively.

DEMAND

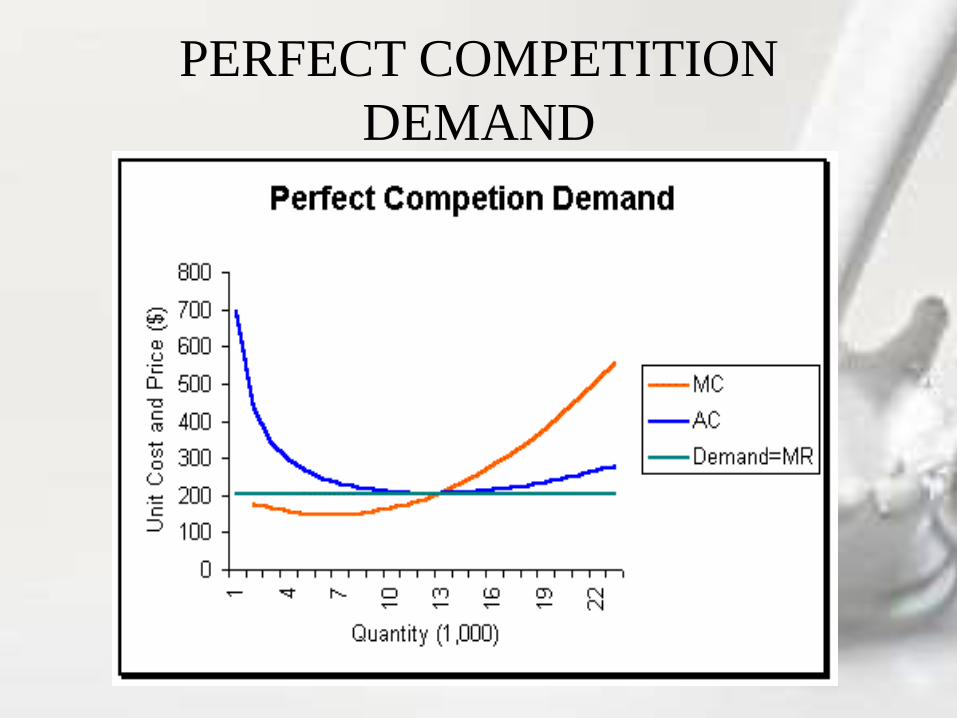

• TheoryThe demand of firms in perfect competition is perfectly elastic(i.e., the smallest possible price change results in avirtually infinite quantity change). Such demand is represented graphically by a horizontal demand curve: no matter what quantity is sold, the price is the same, and it is the going price in the market.

• Feature

Nationwide, the demand for milk is likely to be down-sloping, that is inversely related to price. But for a single milk producer, it is given by the price the farmer can receive: the going market price. It does not change, no matter what quantity the farmer produces. Thus demand is horizontal.

PERFECT COMPETITION

DEMAND

PROFIT MAXIMIZATION & LOSS

MAXIMIZATION

• A firm must seek to sell a volume of output

where its total revenue exceeds its total cost by

the largest amount possible; that is, its profit is

the maximum.

• If a firm fails to derive a profit, it may

nevertheless seek, in the short run, to produce at

that level of sales where the difference between

its cost and its revenue, i.e., its loss, is minimum.

CLOSE DOWN DECISION &

BREAK-EVEN POINT

• CLOSE DOWN DECISIONIf a firm has revenues that are insufficient to cover even its fixed costs in the short run, the firm must close down.

• BREAK-EVEN POINTThe volume of output where total revenue is equal to total cost is known as the break-even point. A firm must be beyond its break-even point in order to be maximizing its profit.

MARGINAL REVENUE

MARGINAL COST RULE• MARGINAL REVENUE, MARGINAL COST RULEProducing at the level of output where marginal revenue equalsmarginal cost is equivalent to profit maximization. Indeed, ifone less unit were to be produced, profit would be smaller by theexcess of marginal revenue over marginal cost for that lastunit. If one more unit were to be produced, profit would also besmaller, this time by the excess of marginal cost over marginalrevenue.

MR = Change in total revenue/ one unit change in output

• MARGINAL REVENUE, MARGINAL COSTThe marginal revenue = marginal cost rule is applicable to loss minimization as well as profit maximization. However, if marginal revenue intersects marginal cost below average variable cost, it means that revenues are not sufficient to cover fixed costs and the firm should close down.

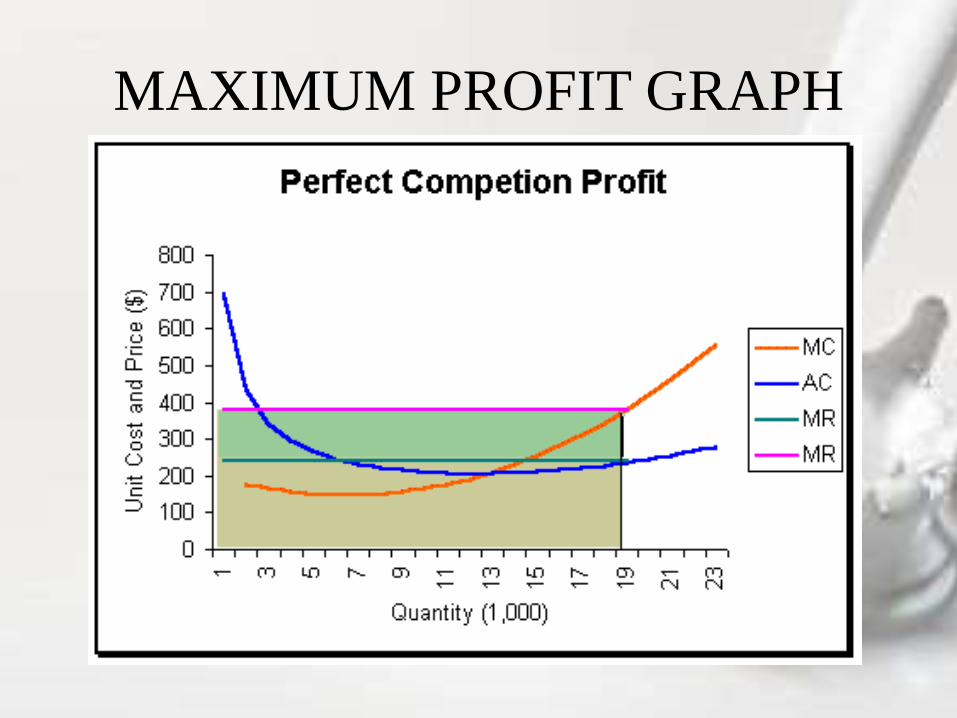

MAXIMUM PROFIT

• MAXIMUM PROFITThe maximum profit is obtained by first determining the levelof output for which marginal revenue equals marginal cost (thusprofits cannot possibly be increased). Then determining:1- total revenue given by price multiplied by quantity2- total cost given by average total cost multiplied by quantity3- the difference between 1 and 2 above is the profit (or loss).

• MAXIMUM PROFIT GRAPHSince maximum profit is the excess of total revenue over total cost, it is shown graphically as the area by which the total revenue rectangle exceeds the total cost rectangle. The height of total revenue rectangle is the price received by the firm, and the width is the optimum quantity (where MR=MC). The height of total cost rectangle is average total cost (on ATC curve), and the width is the optimum quantity.

MAXIMUM PROFIT GRAPH

SUPPLY CURVE• SHORT RUN SUPPLY CURVE

The short run supply curve of firms in perfect competition is the

up-sloping portion of the marginal cost curve (above the average

variable cost intersection). Indeed, a firm determines its optimum

volume of sales by taking the intersection of marginal revenue

and marginal cost. The marginal revenue is also the price it

receives. Thus supplier's price-quantity combinations are given

by the marginal cost up-sloping portion.

• LONG RUN SUPPLY CURVE

The long run supply curve for an industry in perfect competition

is perfectly elastic (that is horizontal) in constant-cost industries

and up-sloping in increasing-cost industries. Whether an industry

is constant-cost or increasing-cost is determined by the presence

of adequate or insufficient resources.

LONG RUN PERFECT

EQUILIBRIUM

The long run equilibrium for firms in perfect

competition is where demand (and marginal

revenue which is identical to it) is tangent to the

minimum of average total cost (where marginal

cost also intersects average total cost). At that

point, there is no profit or loss for the firm. (Note

that there is no pure or economic profit, but

normal profit must still be covered).

ECONOMIC EFFECT &

PRODUCTIVE EFFICIENCY• PERFECT COMPETITION ECONOMIC EFFECTPerfect competition is seen as an ideal or optimum form ofmarket because of its very beneficial economic effect forsociety, which comes from- allocative efficiency, and- productive efficiency.But there are a few shortcomings nevertheless.

• PRODUCTIVE EFFICIENCYThe productive efficiency of perfect competition can be observedin the long run equilibrium point of all firms in the industry,which is at the minimum of average total cost. This means thatall firms are forced to cut their costs and utilize the bestavailable technology in order to have their minimum averagetotal cost no higher than that of all the other firms in theindustry. There is also no under or over utilized capacity.

ALLOCATIVE EFFICIENCY &

SHORTCOMINGS

• ALLOCATIVE EFFICIENCYThe allocative efficiency in perfect competition comes from thefact that the quantity produced by each firm is just that forwhich the price paid by society is equal to the cost ofadditional resources (marginal cost). More could not possiblybe obtained for a lower price. The resources are also the mostefficiently allocated among industries since firms will bid forthese resources up to the price consumers want to pay for them.

• PERFECT COMPETITION SHORTCOMINGSIn spite of its beneficial economic effect, perfect competitionfails to- provide any correction for income distribution inequity,- generate any public goods since there is not profit,- stimulate technological progress because of lack of profits,- offer diversity in products since these are standardized.

SUMMARY

As mentioned above, the perfect competition model, if interpreted as applying also to short-period or very-short-period behavior, is approximated only by markets of homogeneous products produced and purchased by very many sellers and buyers, usually organized markets for agricultural products or raw materials.

In real-world markets, assumptions such as perfect information cannot be verified and are only approximated in organized double-auction markets where most agents wait and observe the behavior of prices before deciding to exchange.

REFERENCES

• http://www.businessdictionary.com/definition/

perfect-competition

• https://en.wikipedia.org/wiki/Perfect_competiti

on

• http://www.investopedia.com/terms/p/perfectc

ompetition.asp

• http://www.economicsonline.co.uk/Business_e

conomics/Perfect_competition.html