Embed Size (px)

Citation preview

© C

opyright ION

A T

echnologies 2002

Chris Horn, ChairmanIONA TechnologiesJune 2002

Dublin as a Knowledge City?

Ireland as a Knowledge Enterprise ?

© C

opyright ION

A T

echnologies 2002

National Propensity to Innovate

• Swift, Beckett, O’Casey, Connelly, Yeats, Wilde, Friel, Yeats, Doyle..

• Boyle, Kelvin, Walton, Hamilton, Tyndell…

• The Chieftans, Christy Moore, Riverdance..

• Planxty, Clanad , The Corrs, The Cranberries..

• Thin Lizzy, Boomtown Rats, Van Morrison, Paul Brady, U2 …

• Jack Charlton, Mick McCarthy..

A culture of shared learning and experience,

co-operation for the world stage

© C

opyright ION

A T

echnologies 2002

Ireland has gained world wide recognition as the Celtic Tiger, based on our remarkable ability to ride the surge in high technology industries, from computers to software to to medical devices to pharmaceuticals. However, with the emergence of the Eastern Europe cubs and the Chinese Dragon, we need to move on...

Ireland - a report card

3

• World’s Most Global Economy

• Exports are 88% of GDP

• UK still our primary trade partner

• More US imports than elsewhere in EU

• 20 Years Ago - High Quality, Low Cost, Medium Technical Competence

• Now - High Quality, Medium Cost, High Technical Competence -- and High Reputation

© C

opyright ION

A T

echnologies 2002

The Plain People of Ireland

• How does technology bring employment, social cohesion and

high quality of life to those at lower end of economic scale ?

• What is the tangible benefit of ICT to me ?

– The Digital Hub project

– “At the moment this project seems to have little more vision than to be

Temple Bar with PCs”

• Public finances are a car crash just about to happen…

• WHY invest in ICT, broadband infrastructure…. ?

– when we have falling tax revenues, imminent benchmarking, woeful health

services, poor transport infrastructure, falling educational quality….

– where are the votes in the 2007 election ?….– (Aren’t there bigger issues ? Like what is the future of Ireland ????)

© C

opyright ION

A T

echnologies 2002

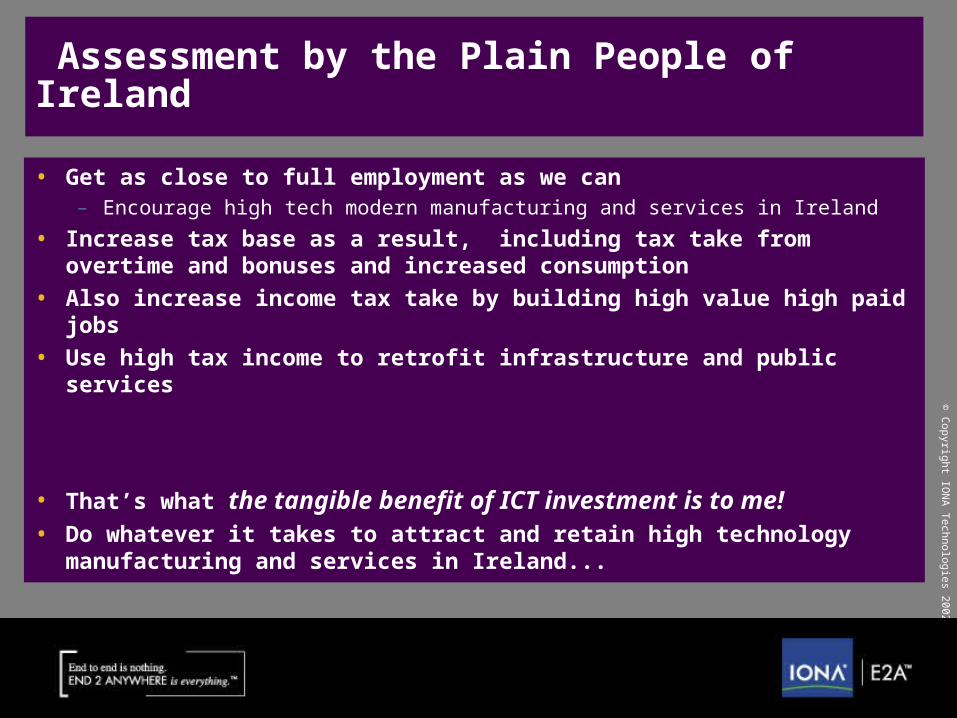

Assessment by the Plain People of Ireland

• Get as close to full employment as we can– Encourage high tech modern manufacturing and services in Ireland

• Increase tax base as a result, including tax take from overtime and bonuses and increased consumption

• Also increase income tax take by building high value high paid jobs

• Use high tax income to retrofit infrastructure and public services

• That’s what the tangible benefit of ICT investment is to me!• Do whatever it takes to attract and retain high technology

manufacturing and services in Ireland...

© C

opyright ION

A T

echnologies 2002

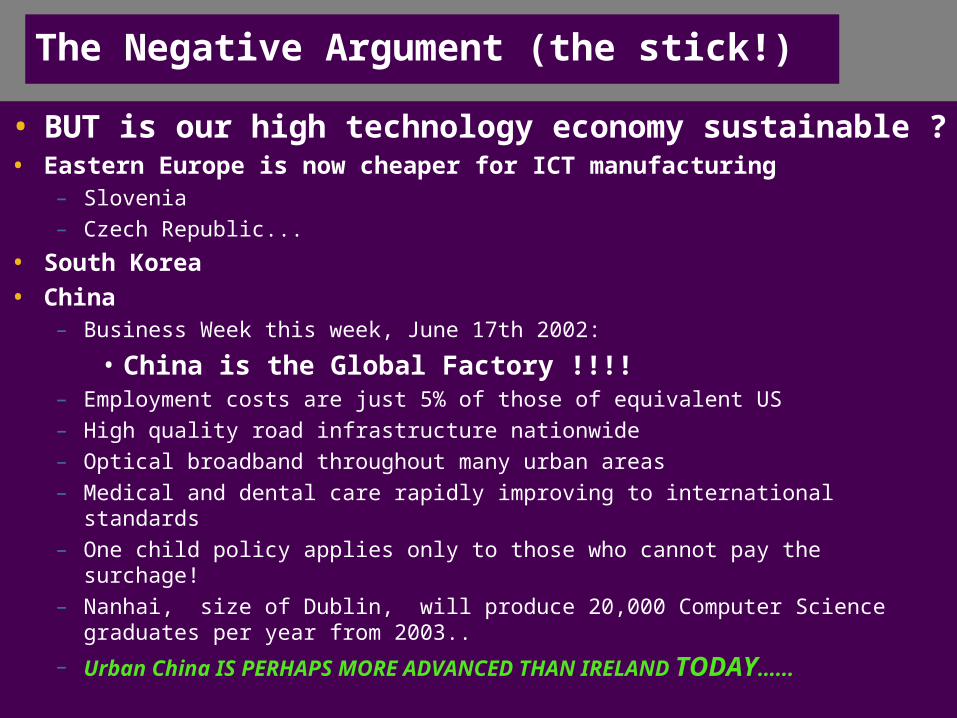

The Negative Argument (the stick!)

• BUT is our high technology economy sustainable ?• Eastern Europe is now cheaper for ICT manufacturing

– Slovenia

– Czech Republic...

• South Korea

• China– Business Week this week, June 17th 2002:

• China is the Global Factory !!!!– Employment costs are just 5% of those of equivalent US

– High quality road infrastructure nationwide

– Optical broadband throughout many urban areas

– Medical and dental care rapidly improving to international standards

– One child policy applies only to those who cannot pay the surchage!

– Nanhai, size of Dublin, will produce 20,000 Computer Science graduates per year from 2003..

– Urban China IS PERHAPS MORE ADVANCED THAN IRELAND TODAY…...

© C

opyright ION

A T

echnologies 2002

Previous Low Cost ICT manufacturing centres

• Remember Spain as a centre for foreign direct investment in ICT manufacturing ?– Where are the Spanish ICT manufacturing centres going today..

• Remember Taiwan as a centre for foreign direct investment in ICT manufacturing ?– Where are the Taiwanese ICT manufacturing centres going today..

• Remember Singapore as a centre for foreign direct investment in ICT manufacturing ?– How has Singapore survived the loss of much of its high technology

manufacturing to elsewhere in Asia ?

© C

opyright ION

A T

echnologies 2002

Our Vulnerabilities

• Geographic Position is distant from most consumer markets• Geographic Position is distant from most manufacturing

centres• Our cost base is now high compared to emerging, high quality,

alternatives• We don’t offer a huge domestic market• Our broadband infrastructure is poor• Our transport infrastructure is poor• Our health and education systems are under stress• Our public finances are limited• Our complacency

Other locations can offer good tax advantages and grants, well qualified, English language competent, good quality of life, and sometimes a huge domestic market….

© C

opyright ION

A T

echnologies 2002

Some of previous presentations

• Dublin Chamber of Commerce e-City report, December 2001– Available from the Chamber web site at www.dubchamber.ie– Dublin ranks moderately, and is falling behind, as an international e-City– Report currently being updated for 2002

• E-Logistics, Farmleigh, March 2002, the new Bush Administration– The threat of Eastern Europe and Asia (especially China) on our manufacturing– The Microsoft X-box example– The opportunity to counter this by making Ireland the global e-logistics centre– How and Why we should proactively outsource to Eastern Europe and Asia

• IMI, Killarney, April 2002: – The dilemma for Innovators and Entrepreneurs - Customer Satisfaction vs Technology Capability– How technology often exceeds customer need, leading to industry disruption– The dilemma for National Policy Makers - Industry Requirements for continued Inward Investment in a

location, vs. National Capability and Cost– The need for focus on Innovation, the role of outsourcing out of Ireland, and the need to globally

compete

© C

opyright ION

A T

echnologies 2002

Farmleigh: Our leverage points

• Testing and Diagnosis– opportunity to innovate, and further improve and automate

• Manufacturing Competence– world class for computer products

• Product Development Centers– indigenous sector buoyant; foreign multinationals weak

• Euro – Clearer Procurement alternatives; cross border efficiencies increasing

• Customer Contact and Care– Exploit call centres further

• Financial Services Center– eCommerce Billing & Support

• Supply Chain Command Centers– Services Aggregation & Management

© C

opyright ION

A T

echnologies 2002

Farmleigh: The Opportunity for Ireland ?

Given• Our widely respected competence in IT manufacturing

• The trust and respect held in us by US parents– Our spiritual closeness to Boston - as well as Berlin

• Our world class engineers

• The emergence of High Quality, Low Cost, Medium Technical Competence centres elsewhere

• Enterprise Ireland’s encouragement and active assistance to the indigenous sector to outsource to lower cost centres overseas

– In contrast to the IDA focus on inward manufacturing investment!

© C

opyright ION

A T

echnologies 2002

Farmleigh: Our opportunity

• We should not rely on manufacturing in Ireland for our future– Manufacturers in this country are going to move abroad

– We need to create new jobs to replace the inevitable vacuum

• We should innovate new products and services– By understanding products designed abroad and learning

– By research, innovation and entrepreneurship

• We should have them manufactured as cheaply as possible, without compromising quality– We want to exploit foreign low cost manufacturing centres ourselves

• We should have them distributed to global markets as appropriate, as cheaply as possible, without compromising channel quality– We want to exploit foreign distribution channels ourselves

– We want products manufactured close to the markets in which they are sold

© C

opyright ION

A T

echnologies 2002

ConsolesDevelop & TestCustomer CareSupply Chain MgmtFinance MgmtSoftware ManufactureOn Line Hosting

Distribution VendorFront End Call CentreGermany

Authorized Replicator UK

Authorized ReplicatorGermany

Xbox ConsoleManufactureHungary

Xbox ConsoleManufacture(Motherboard)Austria

Xbox PeripheralsFar East

1st PartySoftware

Peripherals

Repair & Refurb UK

Repair & RefurbGermany

Fighting back: The Xbox Case

Courtesy Microsoft Ireland

© C

opyright ION

A T

echnologies 2002

Farmleigh Proposal - Ireland as the global e-logistics command centre

• Commit to (US) Parents to fulfil manufacturing and distribution

• At lowest cost, keeping quality high– Allows parent to focus on core competencies of product research and

development; marketing; business development; and customer care

• Decide what -- if any!!! - subsystems and components to manufacture in Ireland

• Decide where to undertake final assembly, test and repair diagnosis - probably Ireland, and upskill Irish staff

• Obtain competitive pricing based on volume purchasing through global procurement

• Actively monitor quality and delivery management

© C

opyright ION

A T

echnologies 2002

• Pro-actively manage supply chain and end delivery in real-time– the e-logistics command centre

– real time tracking of inventory and components

• Share competence and supply chain expertise amongst companies based in Ireland– National asset of current “best practice” international suppliers

– Build a network of international procurement offices for leveraging global buying power and ensuring access to limited allocation components

– Formally and periodically evaluate suppliers for quality, delivery, flexibility, price and responsiveness

– Enterprise Ireland has head start here….

Farmleigh Proposal - Ireland as the global e-logistics command centre

© C

opyright ION

A T

echnologies 2002

Research

• Our Universities and Institutes generally have high reputation– We sometimes do not realise how good we are !

• Publicly funded research is now very positive– Science Foundation Ireland

– Programme for Research in Third Level Institutions (PRTLI)

• Competition for research funds between Universities has been intense

• And needs to STOP– Duplicate capital expenditures

– Poor sharing of ideas, stimuli, experiences and results

– Weakens the Quality of Irish Research

• Perhaps SFI Centres Programme will help…– But we must not confuse Education with Research

© C

opyright ION

A T

echnologies 2002

Innovation

• Usually innovative products result from systematic exploitation of

new combinations of existing technological principles

• Revolutionary new products are difficult to sell!

• Innovation is generally considered difficult

• In fact the bigger challenge in the Irish context is commercialisation

of the innovation

– very small domestic market, difficult to test market a new product locally

© C

opyright ION

A T

echnologies 2002

Exploitation

• Europe in general yields great science, but poorly succeeds in commercialisation

• Need to build practical business models for commercialisation of academic research.– And we must not confuse Research and Commercialisation

• We should not view our Indigenous and the Foreign companies as necessarily in competition to exploit Irish research– We want to build wealth in the Economy

– Indigenous and Foreign companies can fruitfully co-operate -- recall Sun Microsystems’ 1993 investment in IONA

© C

opyright ION

A T

echnologies 2002

Proposal - Ireland as a Focus for Collaborative Research and Exploitation

• Establish focussed research centres– Cross university, cross sectorial

– Full time research staff -- no specific academic duties

– Full time Director and Board of Directors

– Board of Directors guide specific research objectives

– Centre publishes general results, but builds IPR

– Builds international reputation, attracts best in class researchers

– Funding:• Public funding

– Return to the tax payer is FDI, and social cohesion from research objectives

• IPR Licensing

– SFI on the way to establishing these...

© C

opyright ION

A T

echnologies 2002

Proposal - Ireland as a Focus for Collaborative Research and Exploitation

• Two categories: Basic Research and Applied Research Centres

• Basic Research - as last slide BUT no sponsoring companies!

• Applied Research:– Companies can join Applied Research Centre - centre becomes a research consortium

• Annual membership fee

• Investment in kind via equipment, software

– Each member company (regardless of size) has one Board seat• Recall: Board directs research objectives

– Each member company can second one staff member for research • minimum of six months commitment...

– Companies can contribute IPR to centre, with prior Board approval• all such IPR is licensible to all member companies at favourable rates

– Companies can exploit IPR generated by centre at favourable rates• Non founder member companies pay additional fee

• Non founder member companies require Board approval to join

• Non members can license IPR as per basic research centres

© C

opyright ION

A T

echnologies 2002

National Propensity to Innovate

• Ireland is tiny on the world stage

• We need to help each other and co-operate by sharing best practices

• We can develop best in world manufacturing management

• We can develop best in world academic research

• We can develop best in world innovation and commercialisation

A culture of shared learning and experience,

co-operation for the world stage

© C

opyright ION

A T

echnologies 2002

IONA TechnologiesNasdaq: IONA