Embed Size (px)

Citation preview

1

PART 2

Basic Concepts and techniques

2

CHAPTER 4

Audit Objectives, Procedures, and Working Papers

3

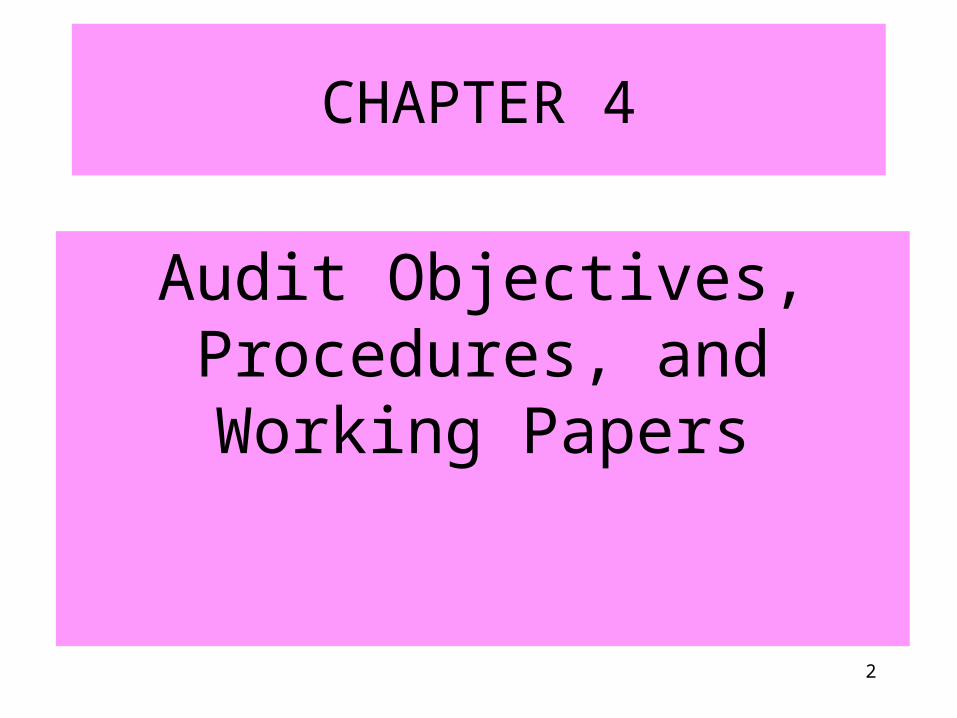

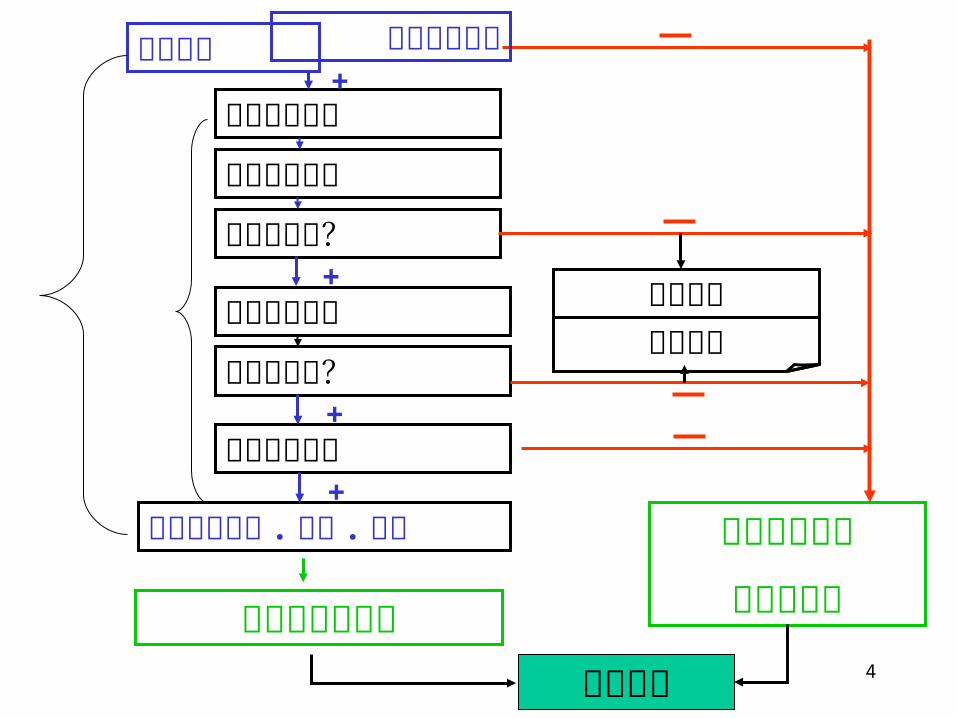

审计报告

计划阶段

实施阶段

报告阶段

4

调查内部控制

记录内部控制

评价健全性?

年度计划

执行符合测试

评价符合性?

评价控制风险

确定审计范围 . 方法 . 时间

有限实质性审计

全面账项基础

实质性审计

鉴定缺陷管理建议

+

+

+

+

审计报告

审计计划

内控评价

预测控制概况

5

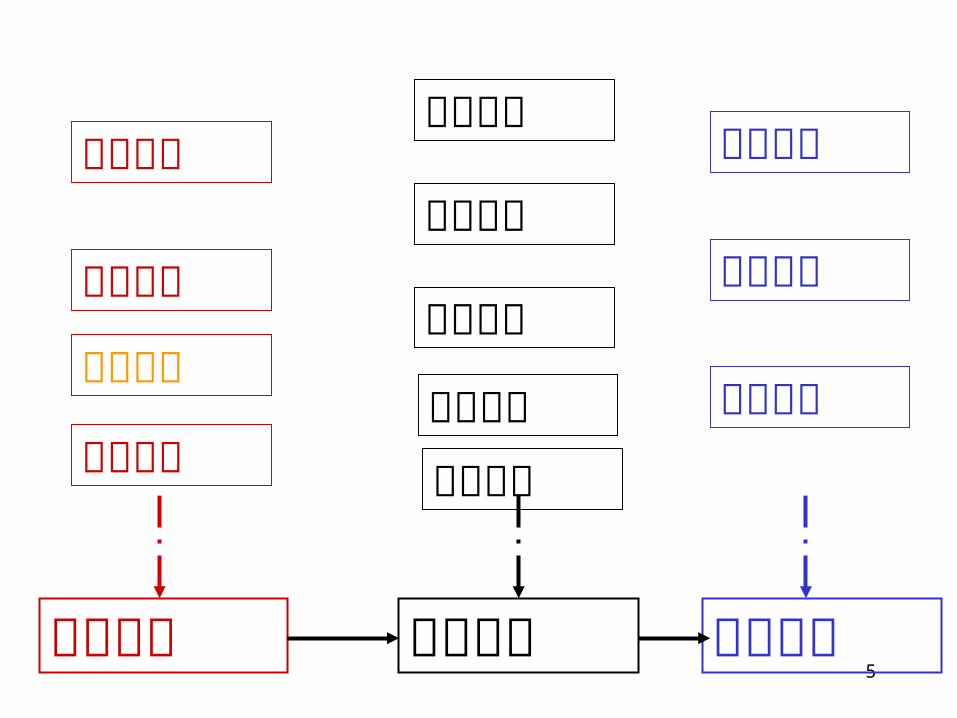

审计方案

审计委托

审计线索

审计方法

审计范围

审计证据

审计结果

审计意见

审计报告

审计计划 审计实施 审计报告

审计约定

内控评价

工作底稿

6

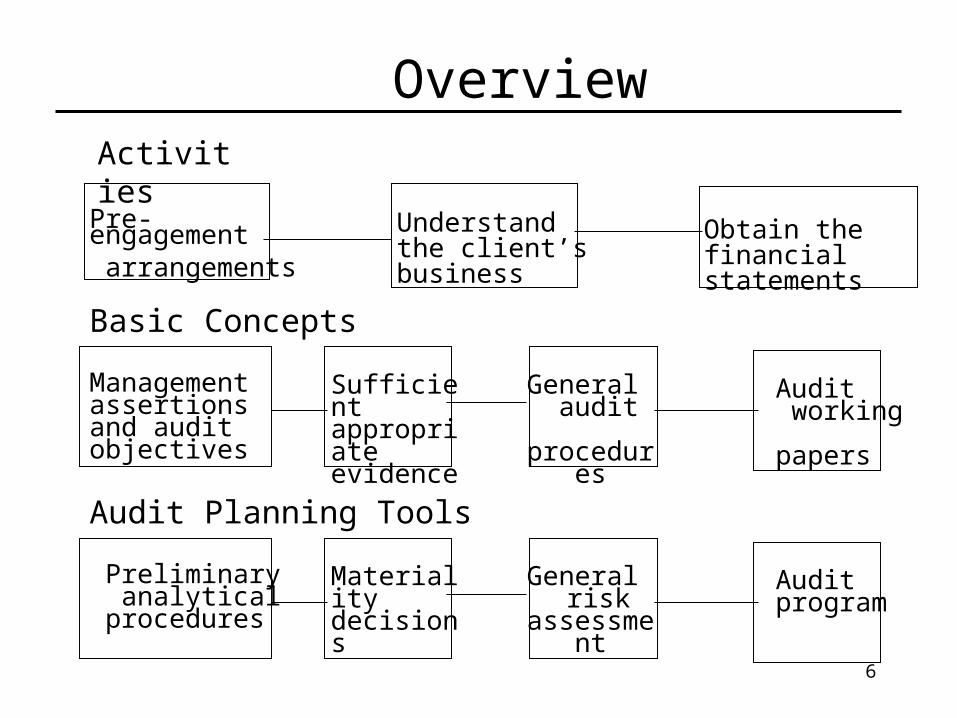

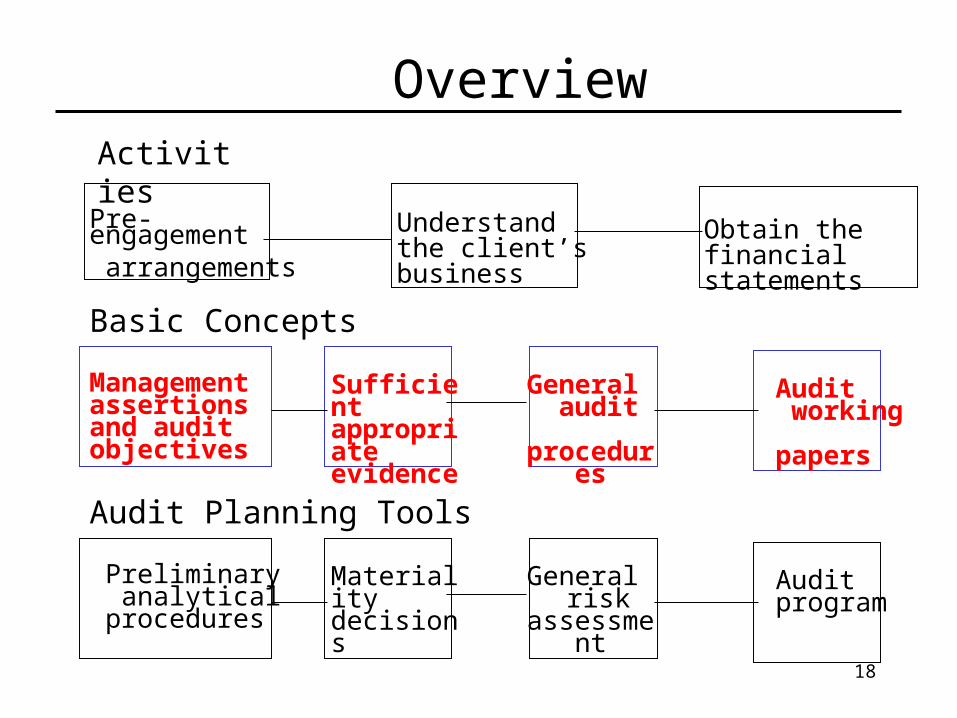

Pre-engagement arrangements

Activities

Understand the client’s business

Obtain the financial statements

Sufficient appropriate evidence

General audit

procedures

Audit working papers

Management assertions and audit objectives

Basic Concepts

Materiality decisions

General risk

assessment

Audit program

Preliminary analytical procedures

Audit Planning Tools

Overview

7

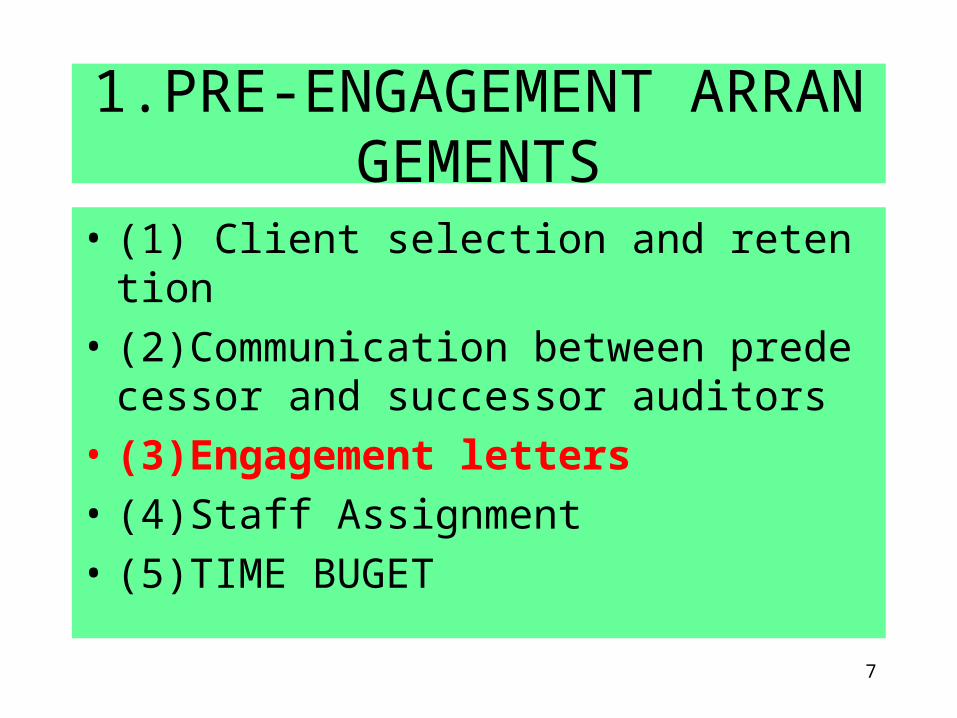

1.PRE-ENGAGEMENT ARRANGEMENTS

• (1) Client selection and retention

• (2)Communication between predecessor and successor auditors

• (3)Engagement letters

• (4)Staff Assignment

• (5)TIME BUGET

8

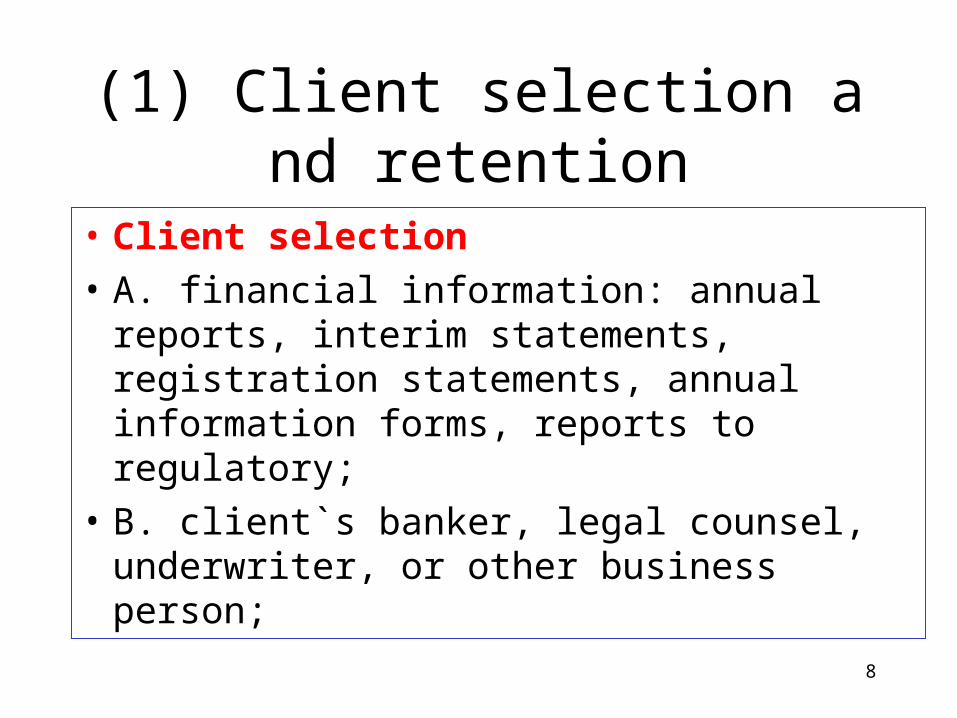

(1) Client selection and retention

• Client selection

• A. financial information: annual reports, interim statements, registration statements, annual information forms, reports to regulatory;

• B. client`s banker, legal counsel, underwriter, or other business person;

9

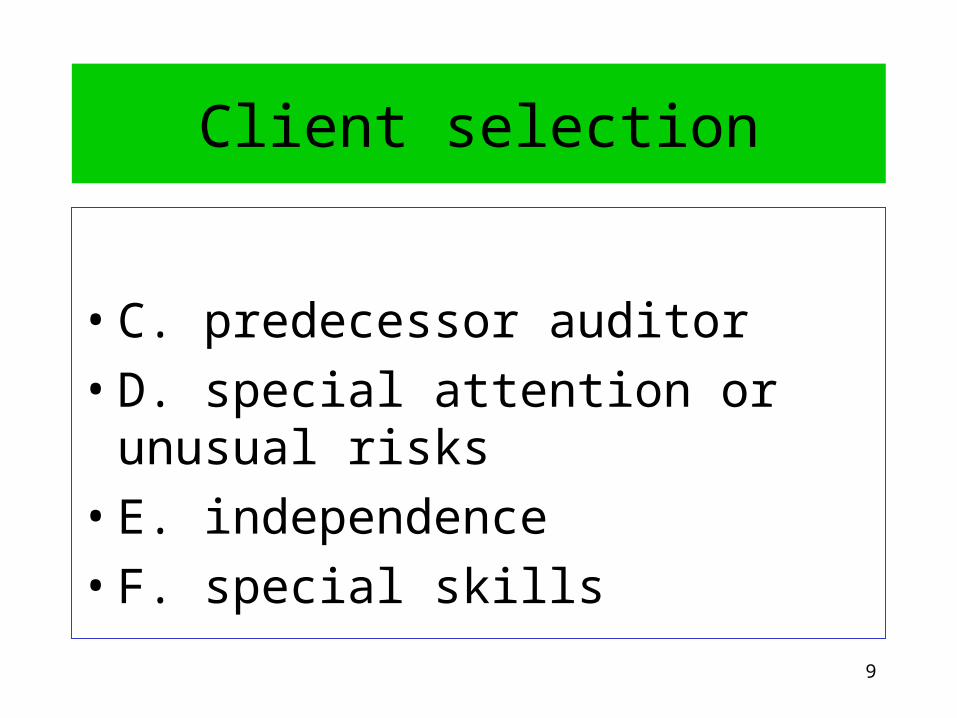

Client selection

• C. predecessor auditor

• D. special attention or unusual risks

• E. independence

• F. special skills

10

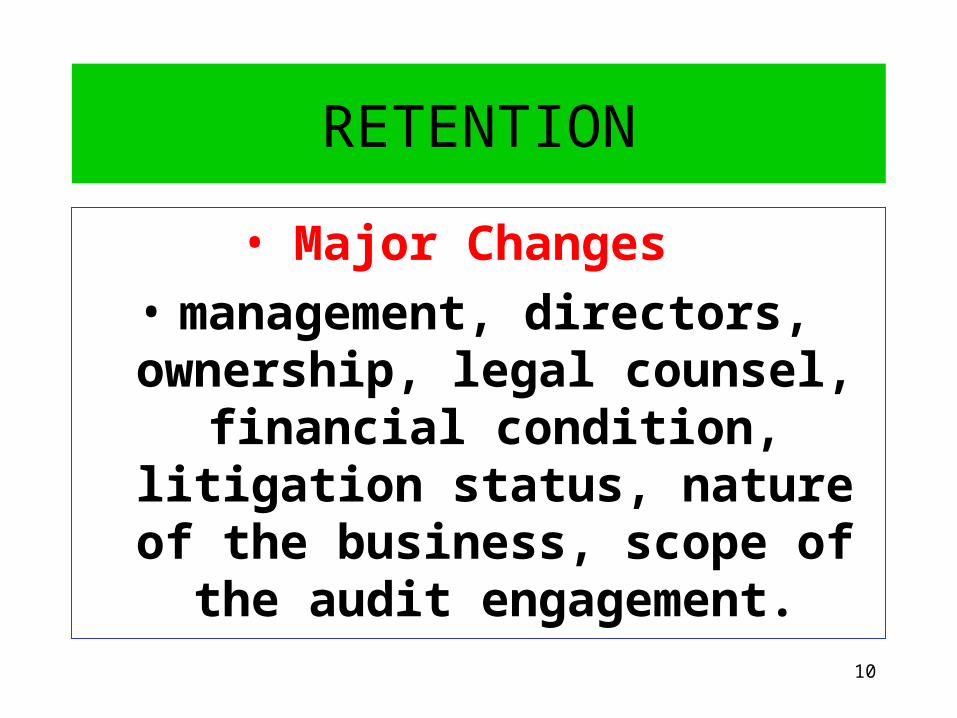

RETENTION

• Major Changes

• management, directors, ownership, legal counsel,

financial condition, litigation status, nature of the business,

scope of the audit engagement.

11

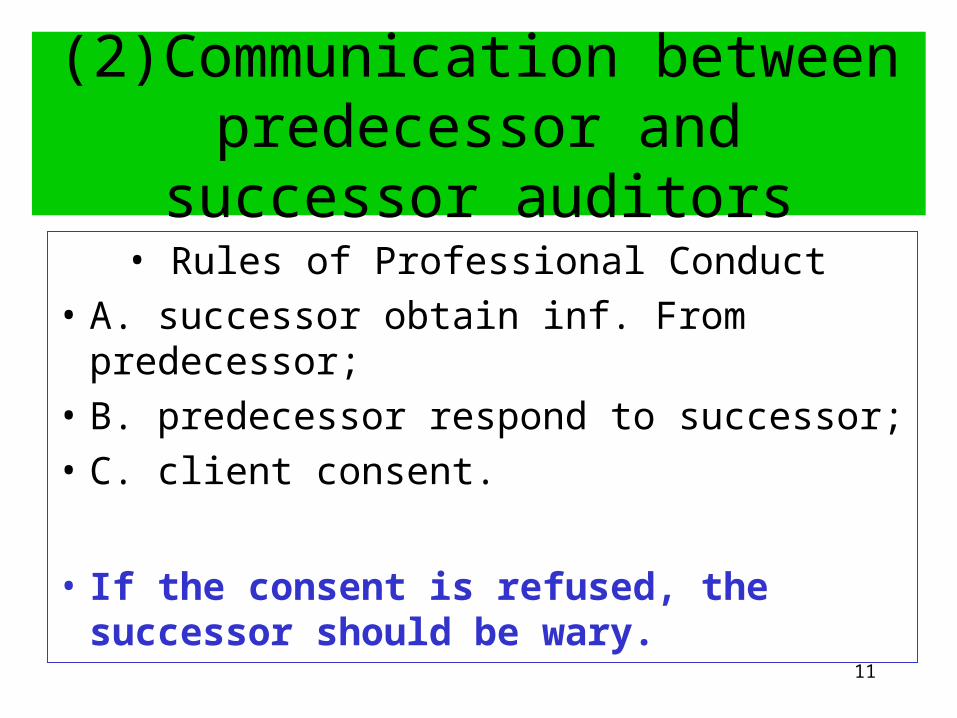

(2)Communication between predecessor and successor auditors

• Rules of Professional Conduct

• A. successor obtain inf. From predecessor;

• B. predecessor respond to successor;

• C. client consent.

• If the consent is refused, the successor should be wary.

12

(3)Engagement letters

• Scope

• GAAS

• Plan

• Fee

• P109 exhibit 4-1

13

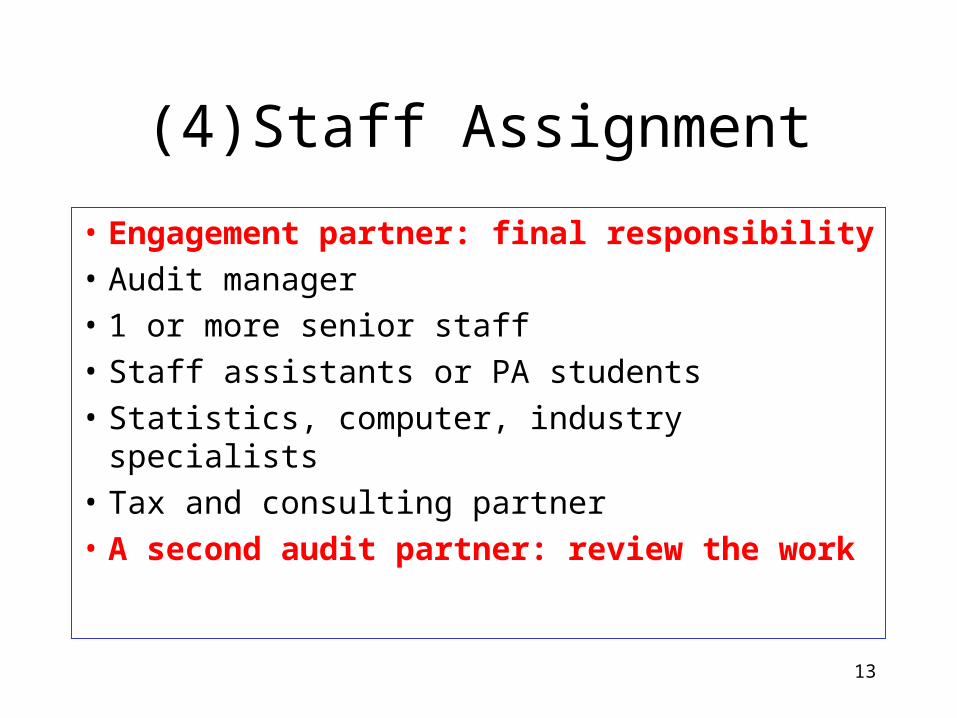

(4)Staff Assignment

• Engagement partner: final responsibility

• Audit manager

• 1 or more senior staff

• Staff assistants or PA students

• Statistics, computer, industry specialists

• Tax and consulting partner

• A second audit partner: review the work

14

(5)time budget

• Interim audit work:

• before the balance sheet date

• Year-end audit work:

• before and after the balance sheet date

15

2.Understanding the client`s business

(1)methods and sources of information

• A.enquiry, including prior working papers

• B. observation

• C. study

16

(2) other aspects of understanding the business

• A. First-time audit: balance sheet

• reliable account balances

• B. internal auditors: internal control

• C. analysis

• D.specialists

17

3.Management`s financial statement

• A.CYCLE• revenue and collection• acquisition and expenditure• production and conversion• finance and investment• B.FINANCIAL STATEMENTS• C.NOTES• P116, 117 E4-2A/B

18

Pre-engagement arrangements

Activities

Understand the client’s business

Obtain the financial statements

Sufficient appropriate evidence

General audit

procedures

Audit working papers

Management assertions and audit objectives

Basic Concepts

Materiality decisions

General risk

assessment

Audit program

Preliminary analytical procedures

Audit Planning Tools

Overview

19

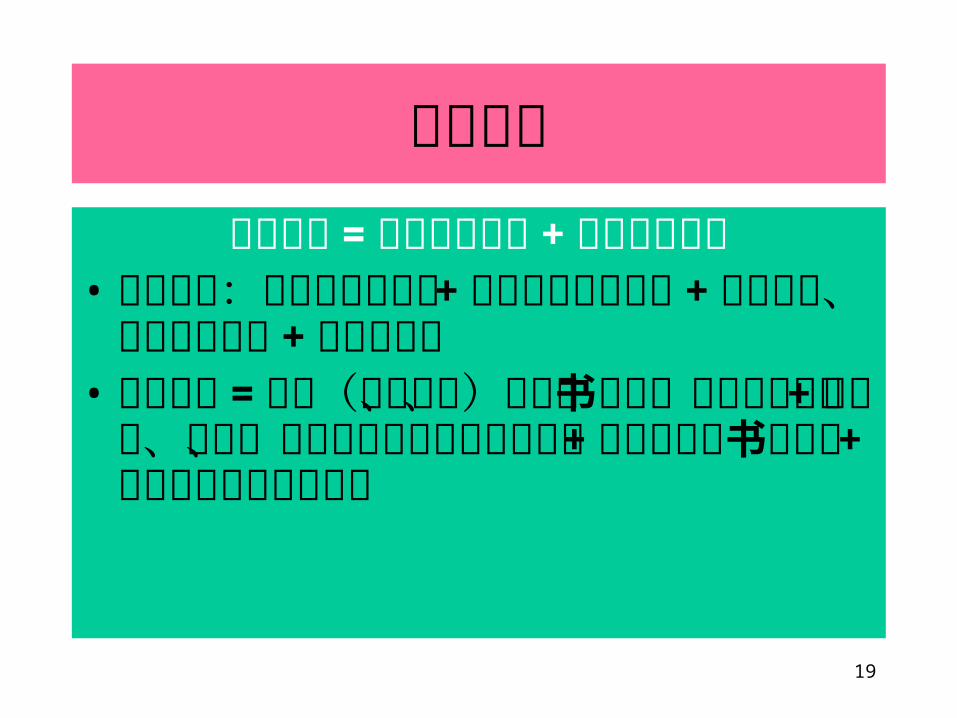

审计等式审计证据 = 客户会计资料 + 审计确认信息

• 会计资料:原始登记记录簿 + 总帐及辅助分类帐 + 成本分配、计算及调节单 +会计手册等

• 确认信息 = 文件(包括支票、发票、合同书及会议记录) + 由询问、观察、检查及实地考查获得的资料 + 确认及其他书面证明 + 审计师获得的其他资料

20

Management`s financial statement

• A.CYCLE• revenue and collection• acquisition and expenditure• production and conversion• finance and investment• B.FINANCIAL STATEMENTS• C.NOTES• P116, 117 E4-2A/B

21

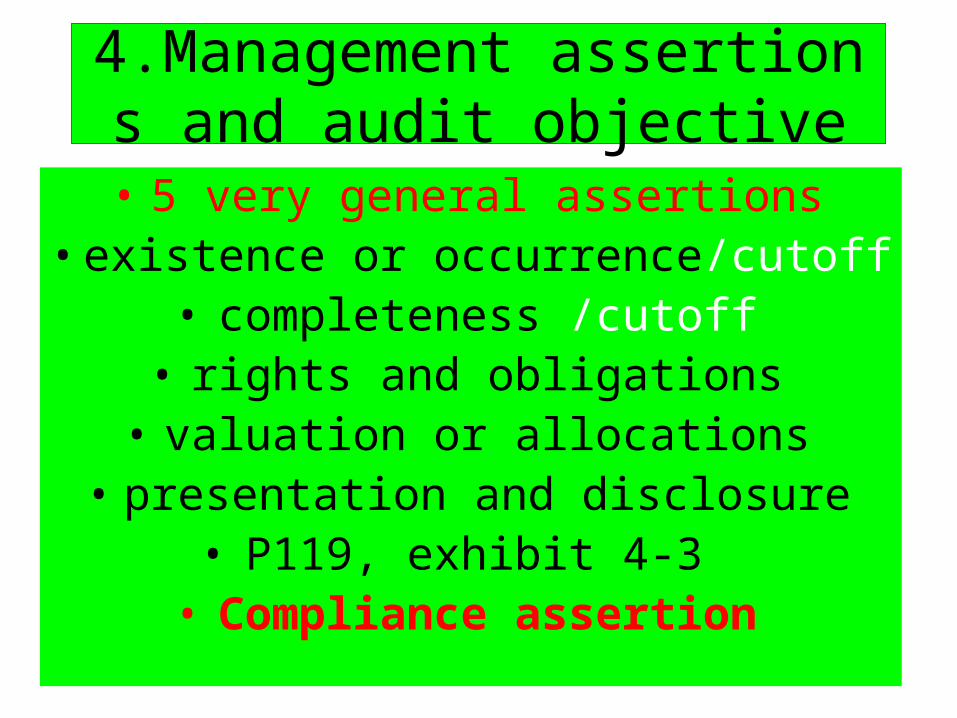

4.Management assertions and audit objective

• 5 very general assertions• existence or occurrence/cutoff

• completeness /cutoff• rights and obligations

• valuation or allocations• presentation and disclosure

• P119, exhibit 4-3 • Compliance assertion

22

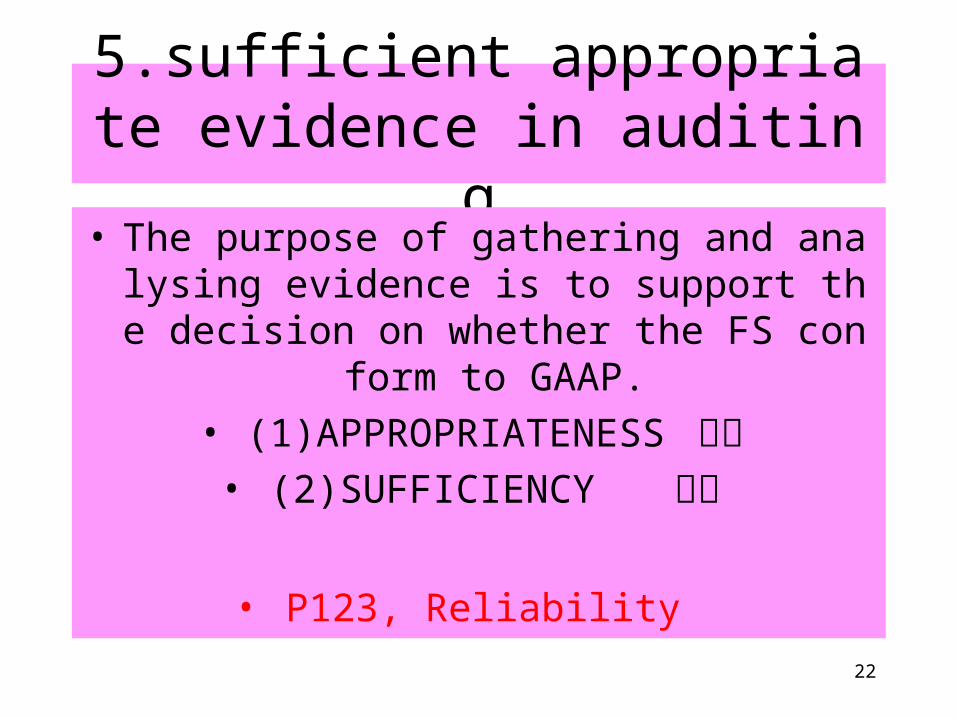

5.sufficient appropriate evidence in auditing

• The purpose of gathering and analysing evidence is to support the decision on whether

the FS conform to GAAP.

• (1)APPROPRIATENESS 品质• (2)SUFFICIENCY 数量

• P123, Reliability

23

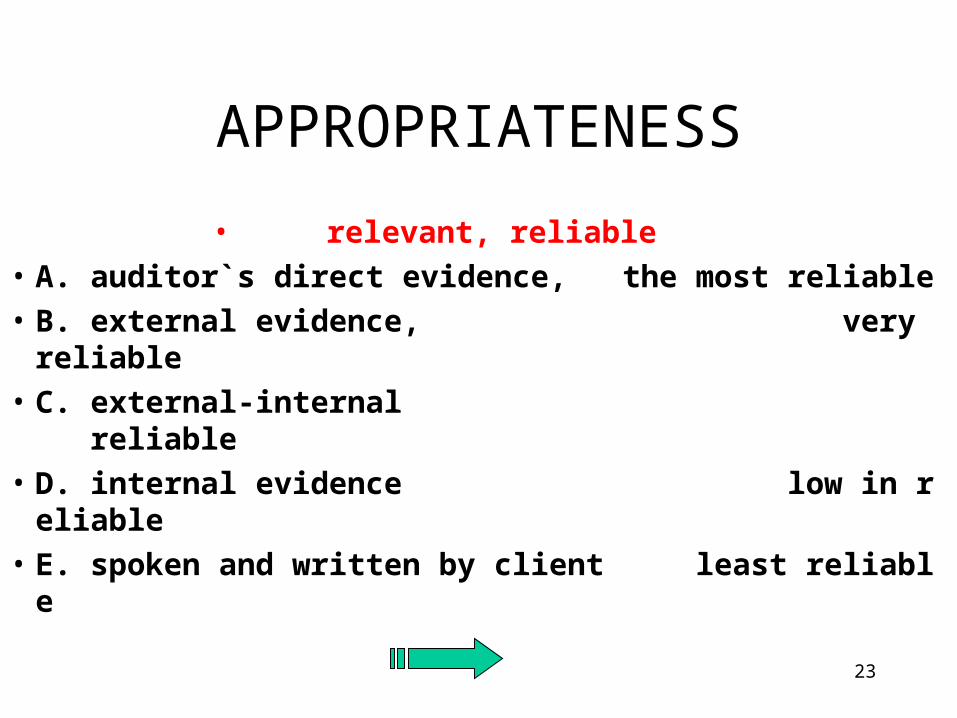

APPROPRIATENESS

• relevant, reliable

• A. auditor`s direct evidence, the most reliable

• B. external evidence, very reliable

• C. external-internal reliable

• D. internal evidence low in reliable

• E. spoken and written by client least reliable

24

6.general audit techniques

• (1)computation

• (2)observation

• (3)confirmation 确认,函证• (4)enquiry 询问• (5)inspection

• (6)analysis

• P125, E4-4

25

审计并非重复会计过程通过检测有选择性的主要会计数据

获得和评估证据以证实财务报表的可信程度

26

(1)computation

Auditor`s calculations

27

(2)observation

Physical observation, inspection

28

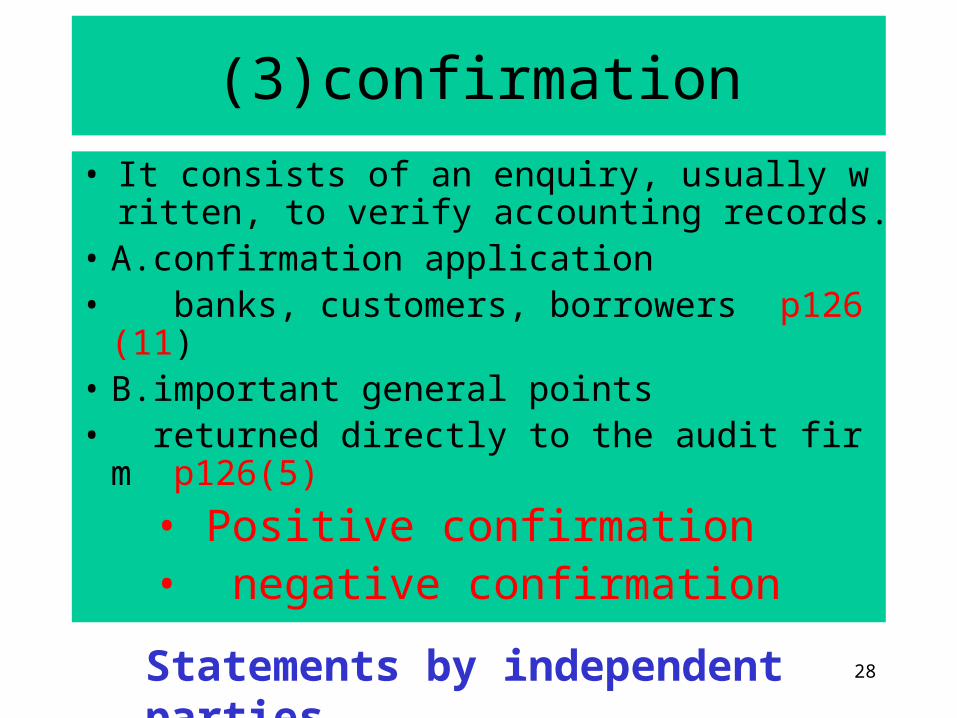

(3)confirmation

• It consists of an enquiry, usually written, to verify accounting records.

• A.confirmation application • banks, customers, borrowers p126(11)• B.important general points • returned directly to the audit firm p126(5)

• Positive confirmation • negative confirmation

Statements by independent parties

29

(4)enquiry

•

Statements by client personnel

30

(5)inspection

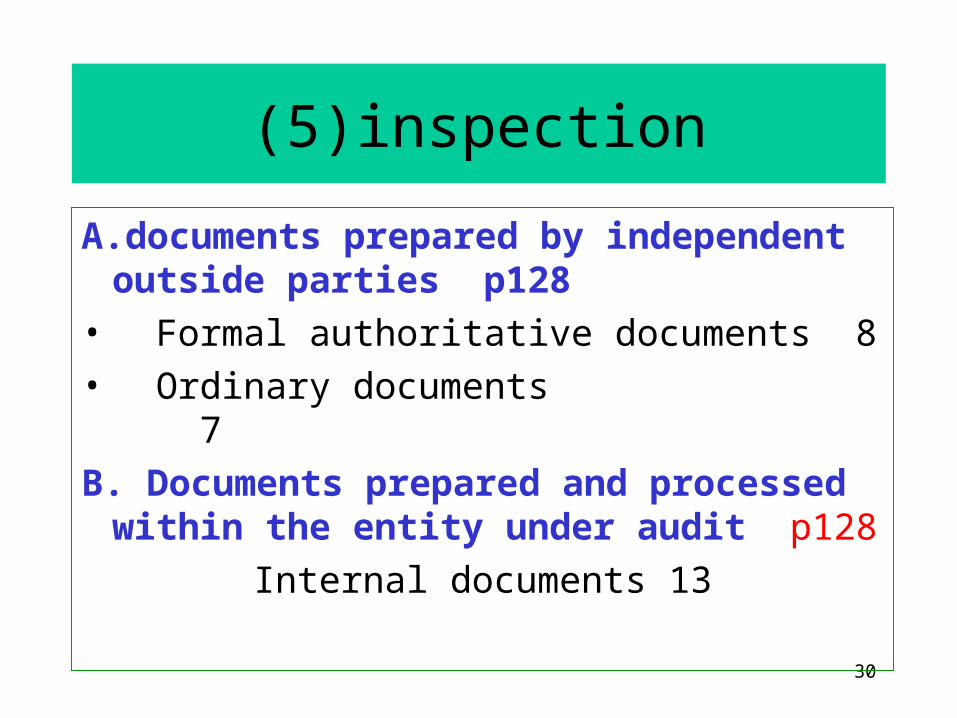

A.documents prepared by independent outside parties p128

• Formal authoritative documents 8

• Ordinary documents 7

B. Documents prepared and processed within the entity under audit p128

Internal documents 13

31

(5)inspection

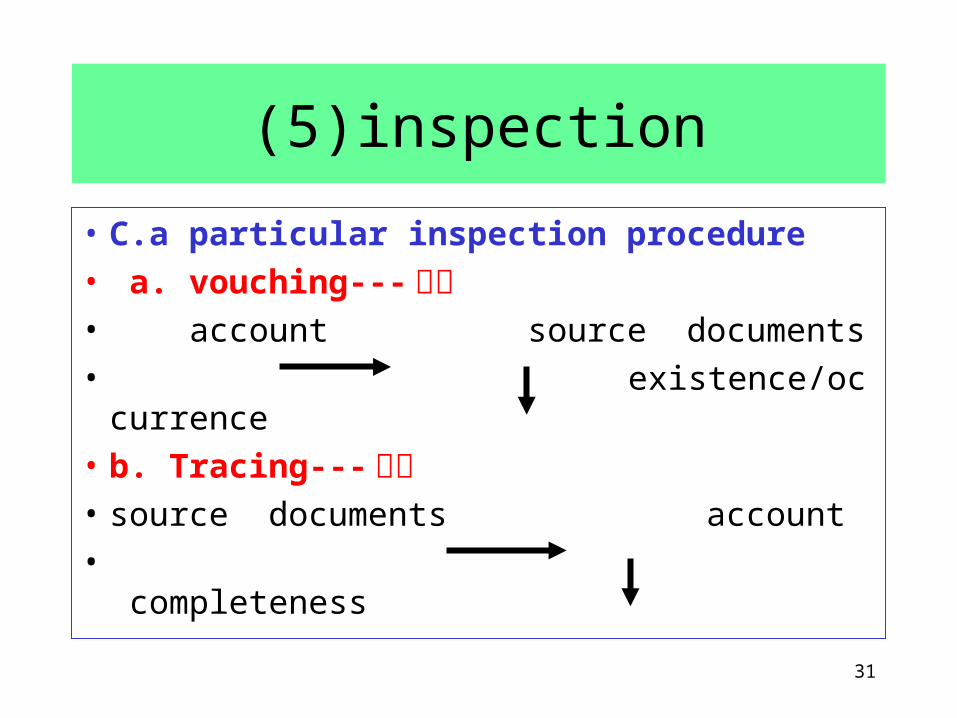

• C.a particular inspection procedure

• a. vouching--- 逆查• account source documents

• existence/occurrence

• b. Tracing--- 顺查• source documents account

• completeness

32

(5)inspection

• c.scanning— 审阅• Looking for anything unusual

• Does not produce direct evidence

• Raise questions for which other evidence must be obtained

• 重点: 数量上重大 性质上可疑

33

奇异现象 奇异的数字; 奇异的时间; 奇异的地点; 奇异的交易频率; 奇异的往来单位;奇异的业务内容;

奇异的物流方向;奇异的科目对应;奇异的人员变动;奇异的指标变动。

• 如精确到“角、分”的固定资产, 3 年以上的应收账款,从服装企业采购钢材,损益金额巨幅增减,会计人员变动频繁等。

34

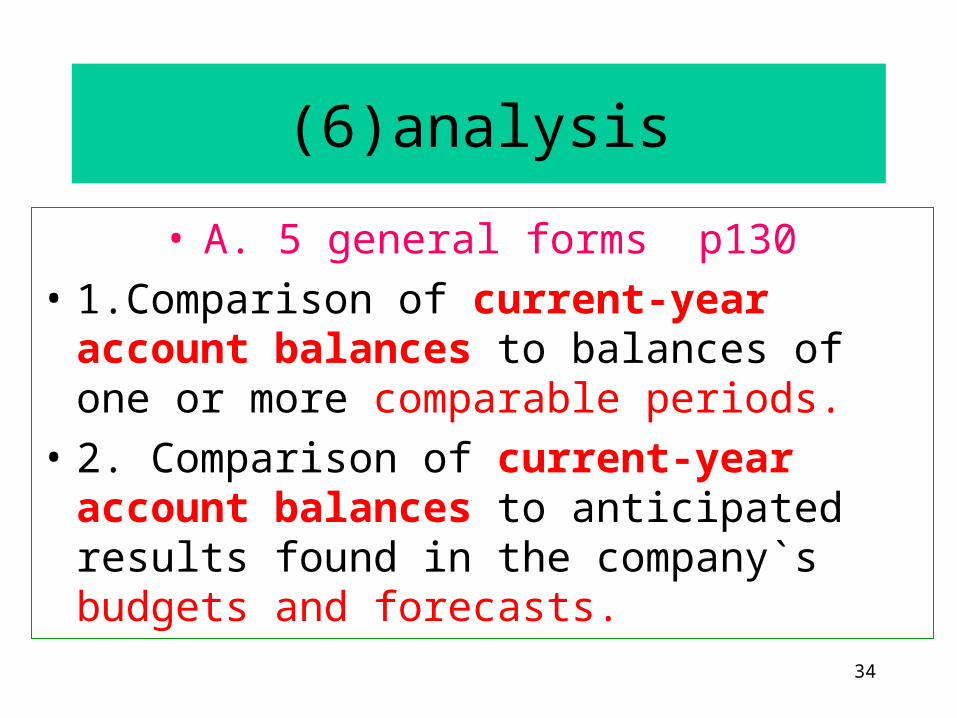

(6)analysis

• A. 5 general forms p130

• 1.Comparison of current-year account balances to balances of one or more comparable periods.

• 2. Comparison of current-year account balances to anticipated results found in the company`s budgets and forecasts.

35

5 general forms

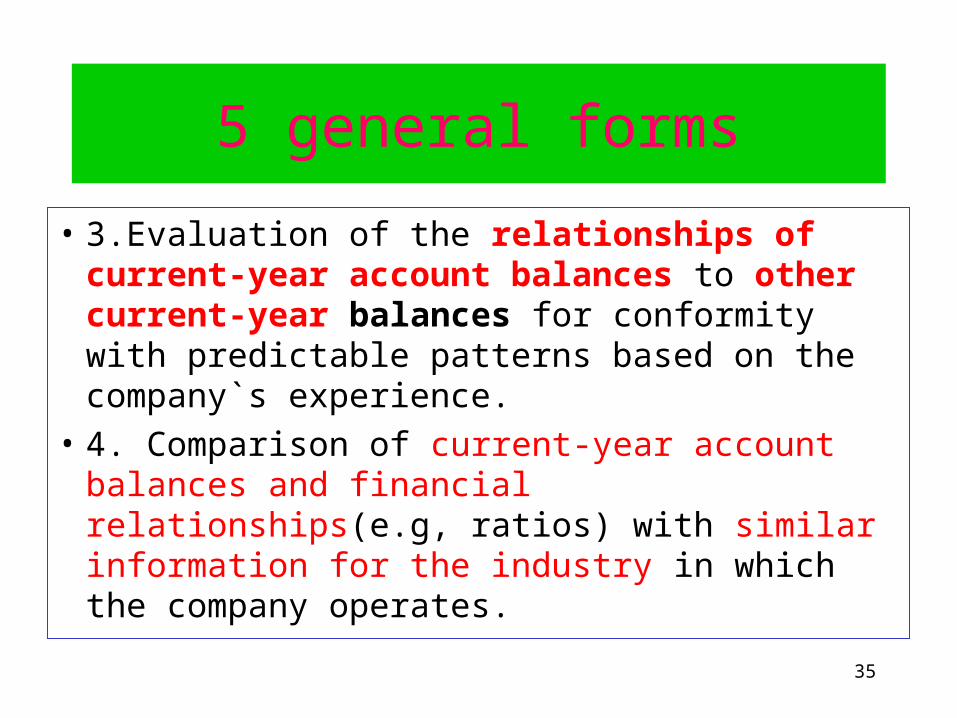

• 3.Evaluation of the relationships of current-year account balances to other current-year balances for conformity with predictable patterns based on the company`s experience.

• 4. Comparison of current-year account balances and financial relationships(e.g, ratios) with similar information for the industry in which the company operates.

36

• 5.Study of the relationships of current-year account balances with relevant nonfinancial information

• ( e.g, physical production statistics).

• B.the sources of information is very important p131

5 general forms

Data interrelationships

37

审计方法体系

•

参见:《税收财务物价违纪与检查处理》

第一篇第四章

38

7.Effectiveness of audit procedure

• P134, E4-6, Summary of misstatements

• P134, E4-7, Initial events that identified adjustments

39

8. Audit working papers

• (1)permanent file papers

• (2)audit administrative papers

• (3)audit evidence papers

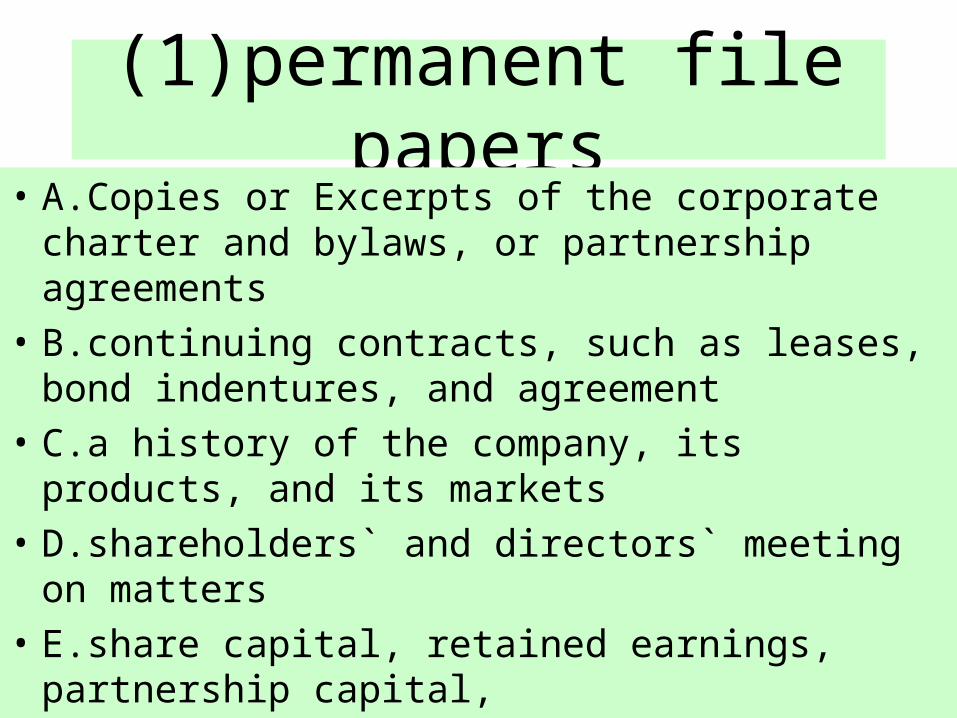

40

(1)permanent file papers• A.Copies or Excerpts of the corporate charter and

bylaws, or partnership agreements

• B.continuing contracts, such as leases, bond indentures, and agreement

• C.a history of the company, its products, and its markets

• D.shareholders` and directors` meeting on matters

• E.share capital, retained earnings, partnership capital,

41

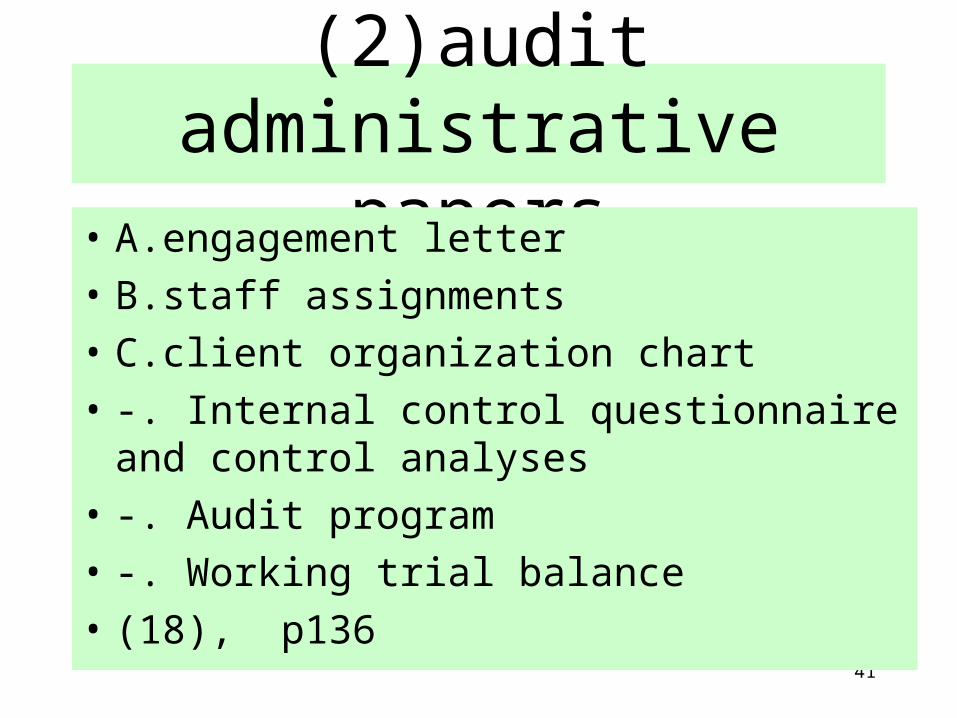

(2)audit administrative papers

• A.engagement letter

• B.staff assignments

• C.client organization chart

• -. Internal control questionnaire and control analyses

• -. Audit program

• -. Working trial balance

• (18), p136

42

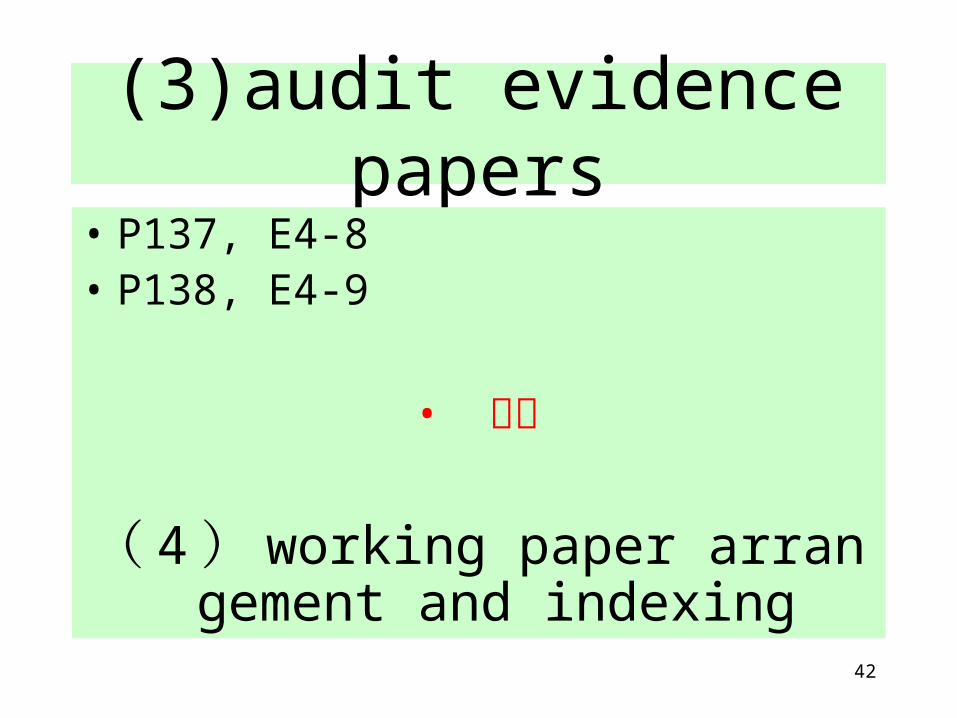

(3)audit evidence papers• P137, E4-8• P138, E4-9

• 样本

( 4 ) working paper arrangement and indexing

43

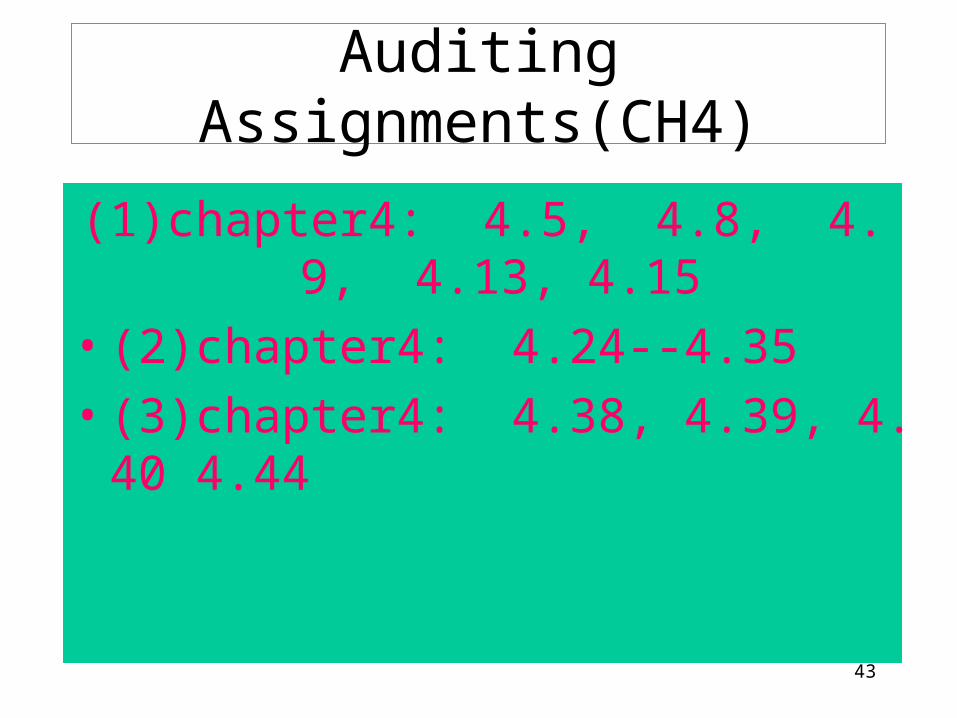

Auditing Assignments(CH4)

(1)chapter4: 4.5, 4.8, 4.9, 4.13, 4.15

• (2)chapter4: 4.24--4.35

• (3)chapter4: 4.38, 4.39, 4.40 4.44

44