Embed Size (px)

Citation preview

Cash, Receivables & Marketable Securities

SH

Cash, Receivables & Marketable Securities

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

1

CURRENT ASSETS (流動資産)

代表的な資産は

Cash (現金)

Marketable Securities (有価証券)

Accounts Receivable (売掛金)

Notes Receivable (手形)

Inventories (商品在庫)

Prepaid expenses (前払い費用)

1. Cash で重要なのは:

Definition, Cash Equivalents, Bank Reconciliation

2. Marketable Securities で重要なのは:

他社の株や社債を投資目的で購入している場合の会計処理です。特に株式の場合、カテゴリー

は持株比率により 3 つあります。

持株比率 0~20%:このカテゴリーが Marketable Securities と呼び、Cost method で処理

します。Asset 1 でまさに学びます。

20~50%:Equity Method (持分法), 税効果会計と連結の Topic で学習します。

50%以上の持株比率:連結。Consolidations.

3. Accounts Receivable では:

Bad Debts Expense (貸倒費用) の計上法がポイントになります。

4. Notes Receivable では:

現在価値です。日本人受験生が苦手とする Topic です。

5. Inventories では:

なんといっても Pricing でしょう。いろんな Method で 12 月 31 日の Inventory 残高を算出しま

す。

6. Prepaid expenses は Non-Factor だね!いくつか過去問題が問題集に出ていたりしますが、3

年に 1 回、1 問でるかな―?

総括:

CPA の試験では 1~5 が満遍なく出題されます。難しい Topic ではないのでグイグイ覚えていきまし

ょう。

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

2

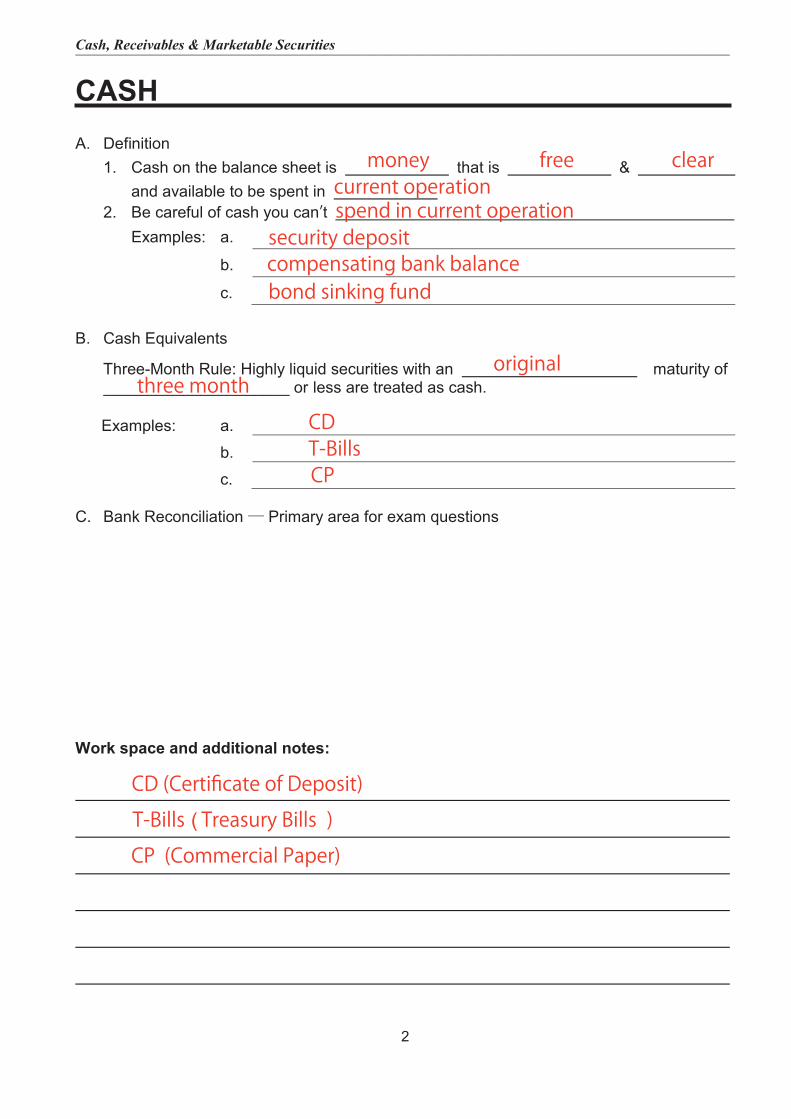

CASHA. Definition

1. Cash on the balance sheet is that is & and available to be spent in

2. Be careful of cash you can’t Examples: a.

b.

c.

B. Cash Equivalents

Three-Month Rule: Highly liquid securities with an maturity of _____________________ or less are treated as cash.

Examples: a.

b.

c.

C. Bank Reconciliation ― Primary area for exam questions

Work space and additional notes:

money free clearcurrent operationspend in current operation

security depositcompensating bank balancebond sinking fund

originalthree month

CDT-BillsCP

CD (Certificate of Deposit)

( Treasury Bills ) T-Bills

CP (Commercial Paper)

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

3

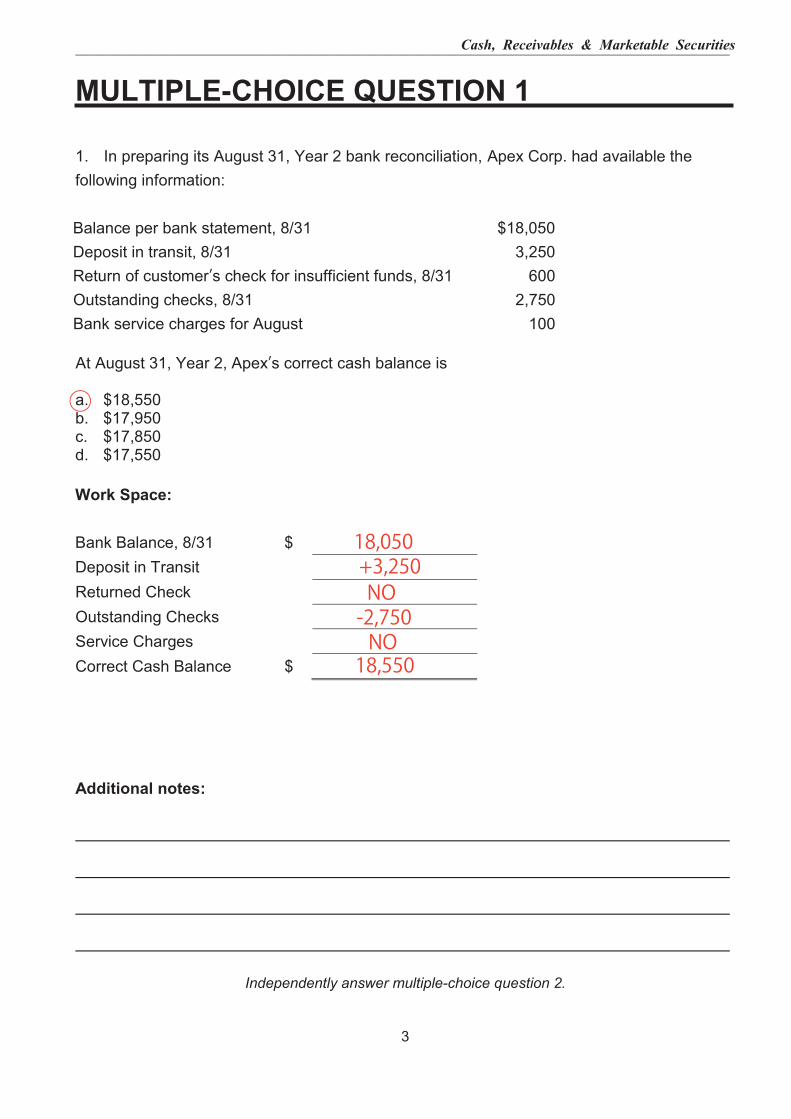

MULTIPLE-CHOICE QUESTION 1 1. In preparing its August 31, Year 2 bank reconciliation, Apex Corp. had available the following information:

Balance per bank statement, 8/31 $18,050 Deposit in transit, 8/31 3,250 Return of customer’s check for insufficient funds, 8/31 600 Outstanding checks, 8/31 2,750 Bank service charges for August 100

At August 31, Year 2, Apex’s correct cash balance is

a. $18,550 b. $17,950 c. $17,850 d. $17,550 Work Space: Bank Balance, 8/31 $ Deposit in Transit Returned Check Outstanding Checks Service Charges Correct Cash Balance $ Additional notes:

Independently answer multiple-choice question 2.

○

18,050+3,250NO

-2,750NO

18,550

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

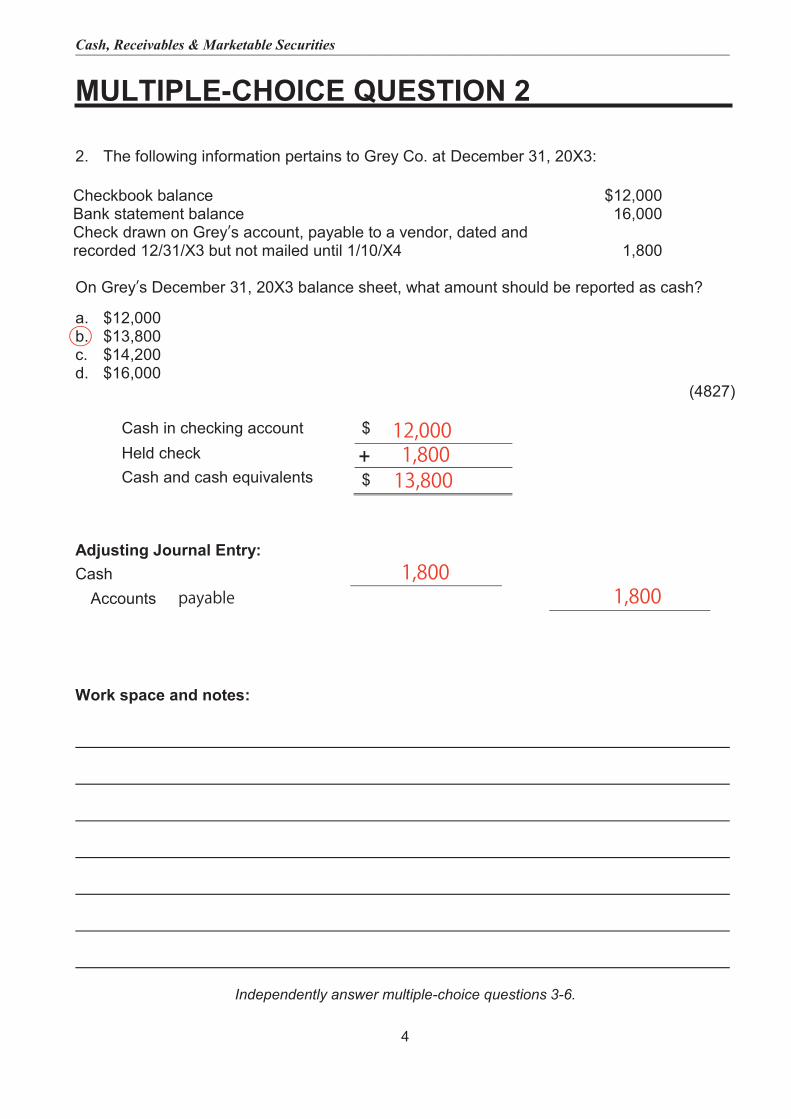

4

MULTIPLE-CHOICE QUESTION 2 2. The following information pertains to Grey Co. at December 31, 20X3: Checkbook balance $12,000 Bank statement balance 16,000 Check drawn on Grey’s account, payable to a vendor, dated and recorded 12/31/X3 but not mailed until 1/10/X4 1,800 On Grey’s December 31, 20X3 balance sheet, what amount should be reported as cash? a. $12,000 b. $13,800 c. $14,200 d. $16,000

(4827)

Cash in checking account $ Held check Cash and cash equivalents $

Adjusting Journal Entry: Cash Accounts Work space and notes:

Independently answer multiple-choice questions 3-6.

○

12,000+ 1,800

13,800

payable1,800

1,800

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

5

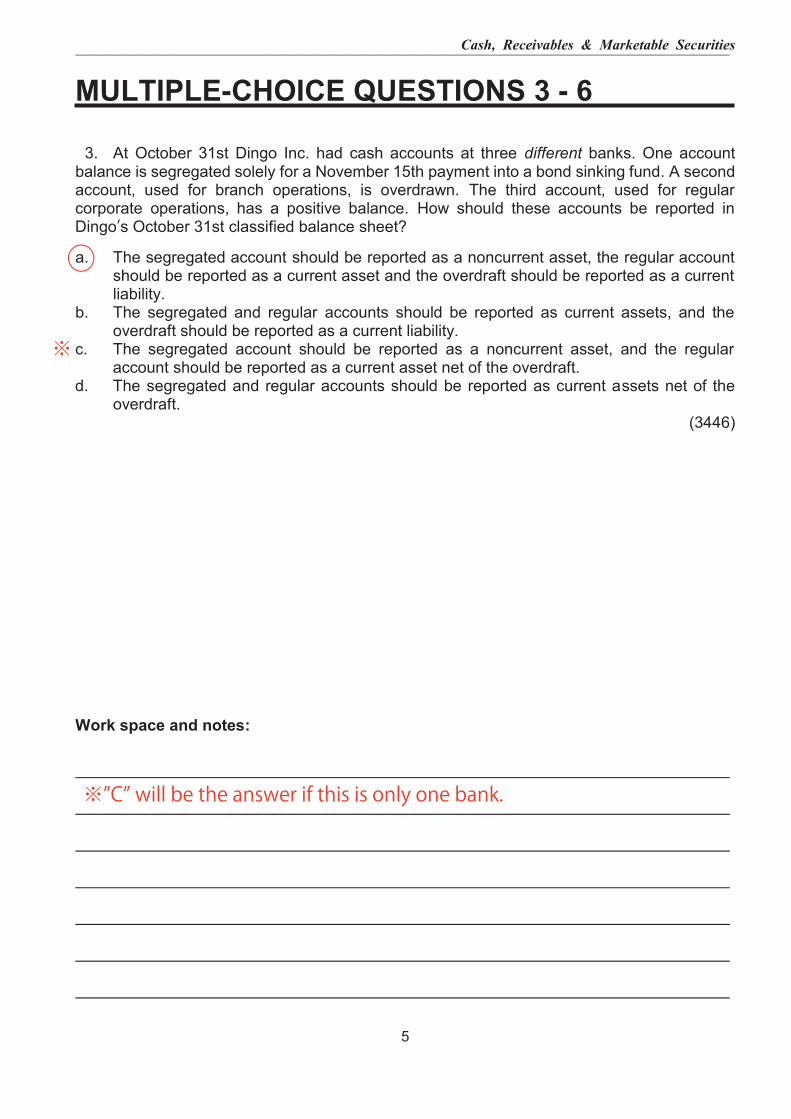

MULTIPLE-CHOICE QUESTIONS 3 - 6

3. At October 31st Dingo Inc. had cash accounts at three different banks. One accountbalance is segregated solely for a November 15th payment into a bond sinking fund. A second account, used for branch operations, is overdrawn. The third account, used for regular corporate operations, has a positive balance. How should these accounts be reported in Dingo’s October 31st classified balance sheet?

a. The segregated account should be reported as a noncurrent asset, the regular accountshould be reported as a current asset and the overdraft should be reported as a currentliability.

b. The segregated and regular accounts should be reported as current assets, and theoverdraft should be reported as a current liability.

c. The segregated account should be reported as a noncurrent asset, and the regularaccount should be reported as a current asset net of the overdraft.

d. The segregated and regular accounts should be reported as current assets net of theoverdraft.

(3446)

Work space and notes:

※”C” will be the answer if this is only one bank.

※

○

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

6

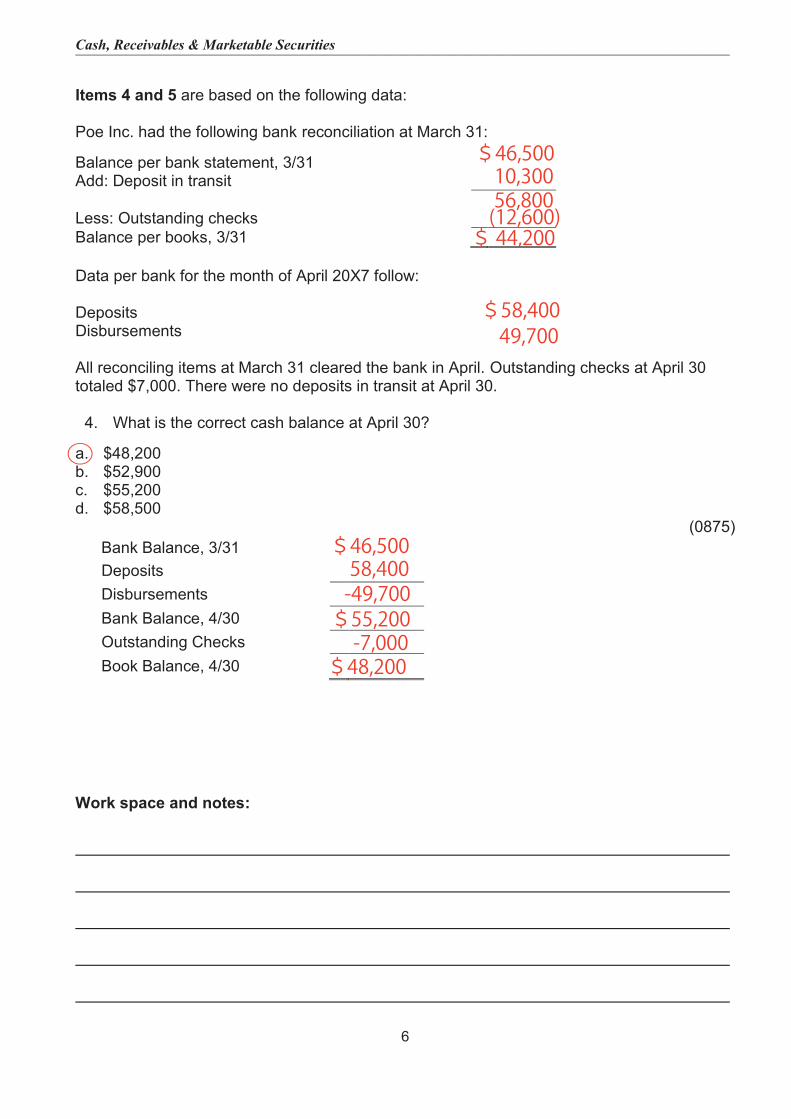

Items 4 and 5 are based on the following data:

Poe Inc. had the following bank reconciliation at March 31:

Balance per bank statement, 3/31 Add: Deposit in transit

Less: Outstanding checks Balance per books, 3/31

Data per bank for the month of April 20X7 follow:

Deposits Disbursements

All reconciling items at March 31 cleared the bank in April. Outstanding checks at April 30 totaled $7,000. There were no deposits in transit at April 30.

4. What is the correct cash balance at April 30?

a. $48,200b. $52,900c. $55,200d. $58,500

(0875) Bank Balance, 3/31 DepositsDisbursementsBank Balance, 4/30 Outstanding ChecksBook Balance, 4/30

Work space and notes:

○

$46,50010,30056,800(12,600)

$ 44,200

$58,40049,700

$46,50058,400-49,700

$55,200-7,000

$48,200

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

7

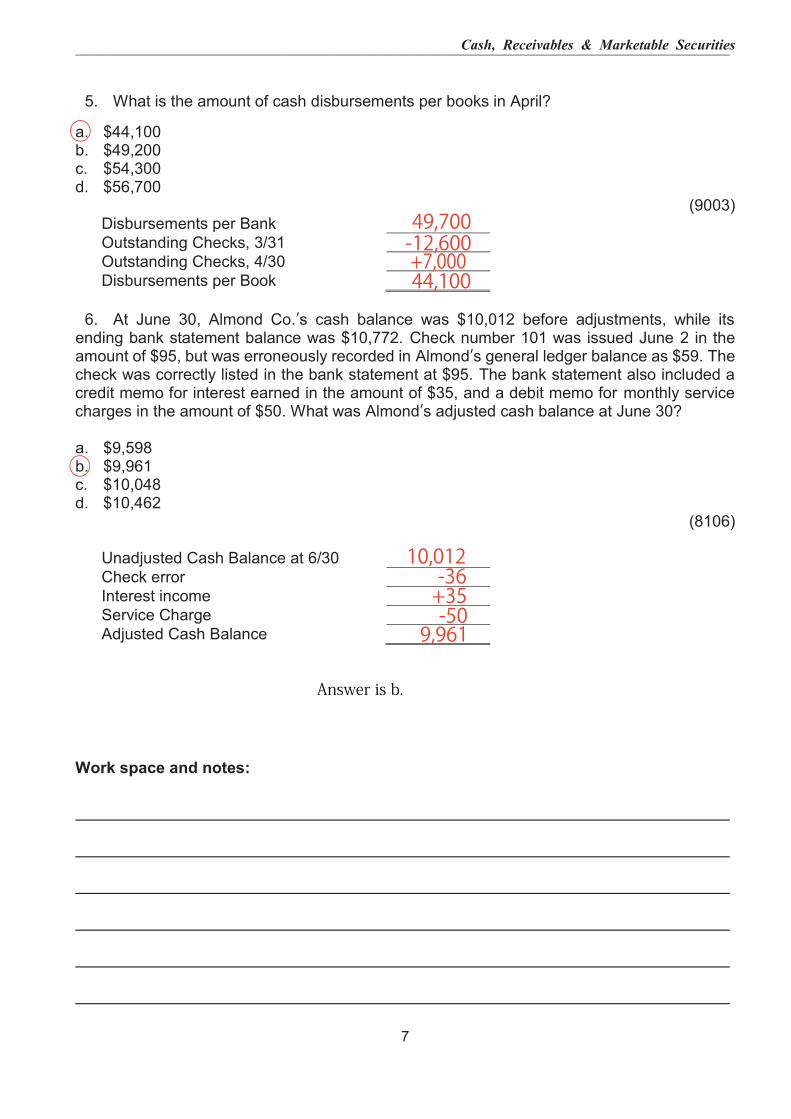

5. What is the amount of cash disbursements per books in April?

a. $44,100b. $49,200c. $54,300d. $56,700

(9003) Disbursements per Bank Outstanding Checks, 3/31 Outstanding Checks, 4/30 Disbursements per Book

6. At June 30, Almond Co.’s cash balance was $10,012 before adjustments, while itsending bank statement balance was $10,772. Check number 101 was issued June 2 in the amount of $95, but was erroneously recorded in Almond’s general ledger balance as $59. Thecheck was correctly listed in the bank statement at $95. The bank statement also included a credit memo for interest earned in the amount of $35, and a debit memo for monthly service charges in the amount of $50. What was Almond’s adjusted cash balance at June 30?

a. $9,598b. $9,961c. $10,048d. $10,462

(8106)

Unadjusted Cash Balance at 6/30 Check error Interest income Service Charge Adjusted Cash Balance

Work space and notes:

49,700-12,600+7,00044,100

○

10,012-36+35-50

9,961

Answer is b.

○

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

8

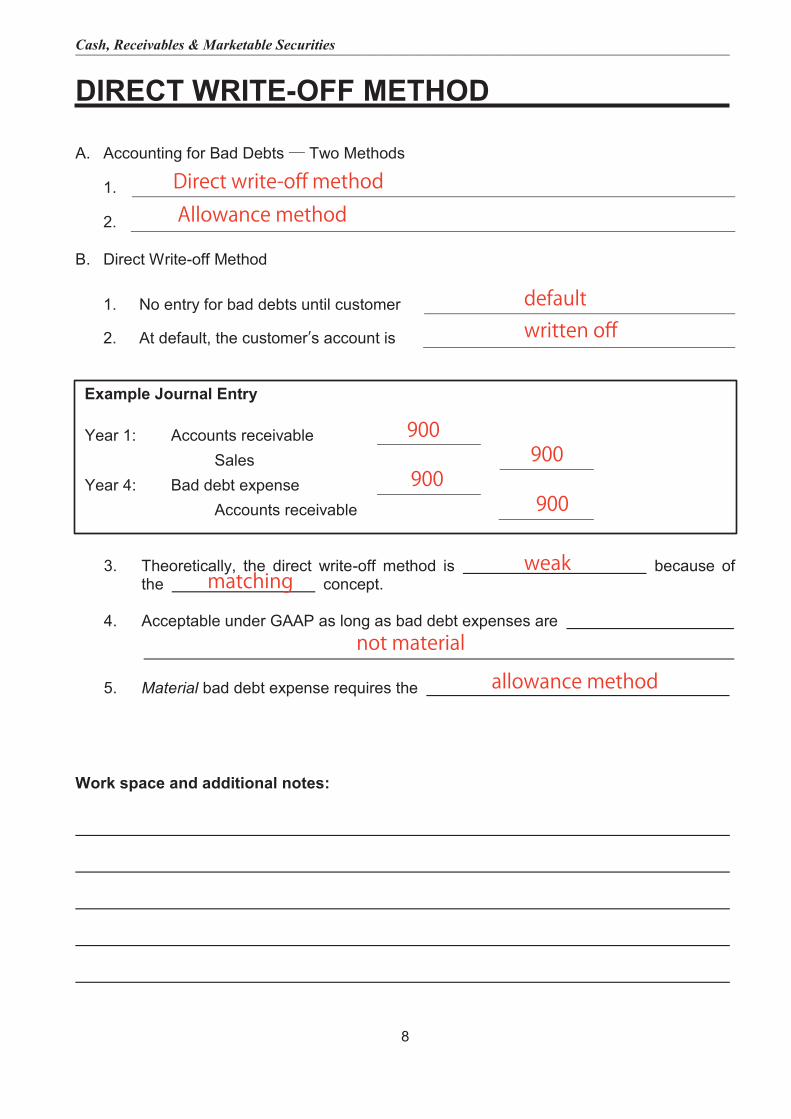

DIRECT WRITE-OFF METHOD

A. Accounting for Bad Debts ― Two Methods

1.

2.

B. Direct Write-off Method

1. No entry for bad debts until customer

2. At default, the customer’s account is

Example Journal Entry

Year 1: Accounts receivable Sales

Year 4: Bad debt expense Accounts receivable

3. Theoretically, the direct write-off method is because of the concept.

4. Acceptable under GAAP as long as bad debt expenses are

5. Material bad debt expense requires the

Work space and additional notes:

Direct write-off methodAllowance method

defaultwritten off

900

900900

900

weakmatching

not material

allowance method

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

9

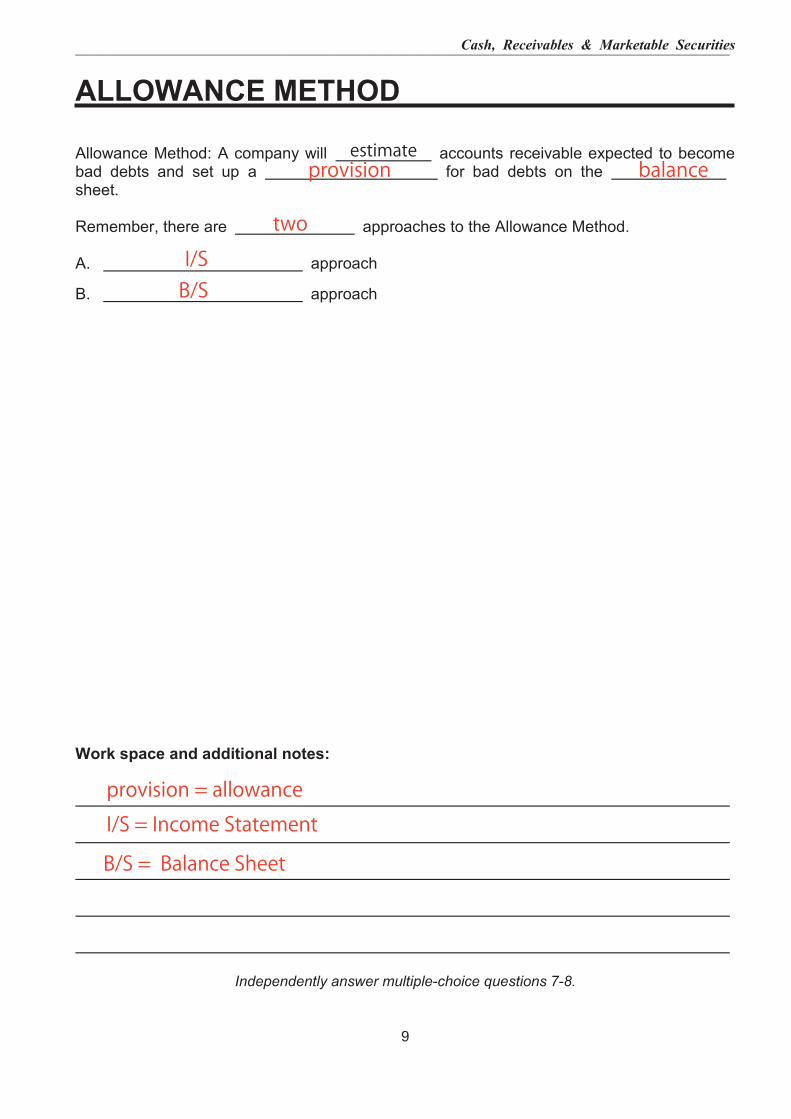

ALLOWANCE METHOD Allowance Method: A company will accounts receivable expected to become bad debts and set up a for bad debts on the a sheet. Remember, there are approaches to the Allowance Method. A. approach

B. approach Work space and additional notes:

Independently answer multiple-choice questions 7-8.

estimateprovision balance

two

I/SB/S

provision = allowance

I/S = Income Statement

B/S = Balance Sheet

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

10

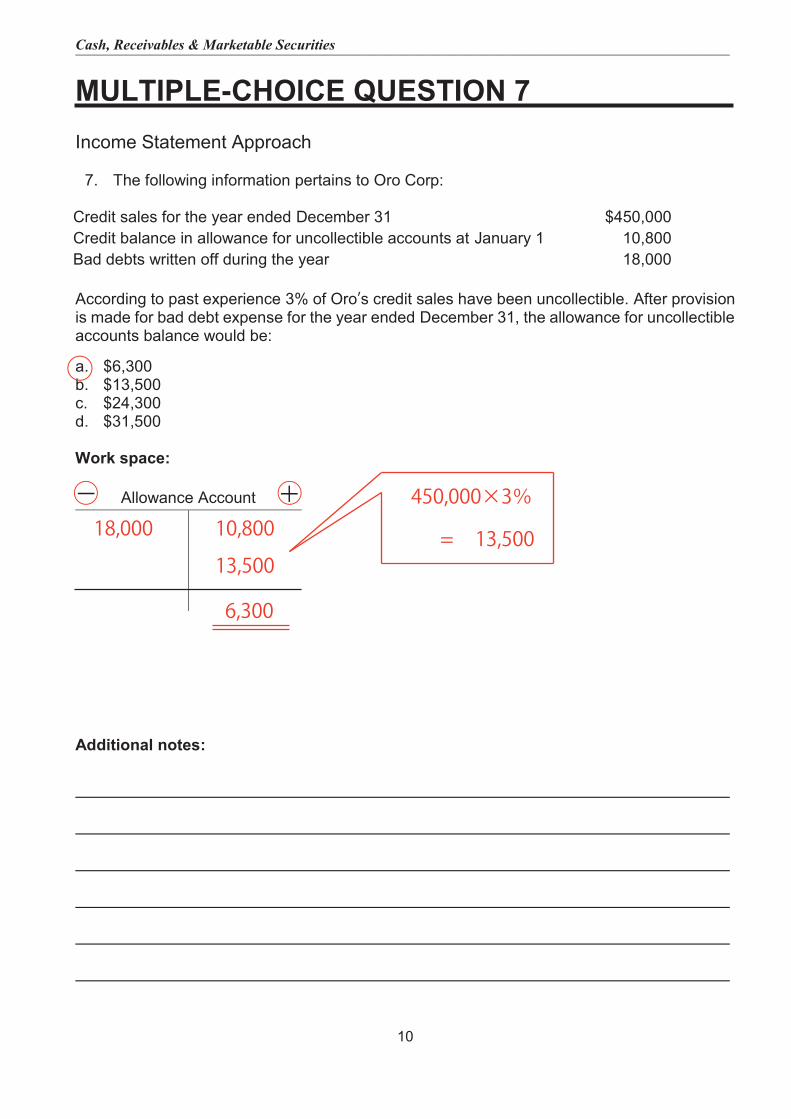

MULTIPLE-CHOICE QUESTION 7Income Statement Approach

7. The following information pertains to Oro Corp:

Credit sales for the year ended December 31 $450,000 Credit balance in allowance for uncollectible accounts at January 1 10,800 Bad debts written off during the year 18,000

According to past experience 3% of Oro’s credit sales have been uncollectible. After provisionis made for bad debt expense for the year ended December 31, the allowance for uncollectible accounts balance would be: a. $6,300b. $13,500c. $24,300d. $31,500

Work space:

Allowance Account

Additional notes:

- +

○

○○18,000 10,800

13,500

6,300

450,000×3%

= 13,500

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

11

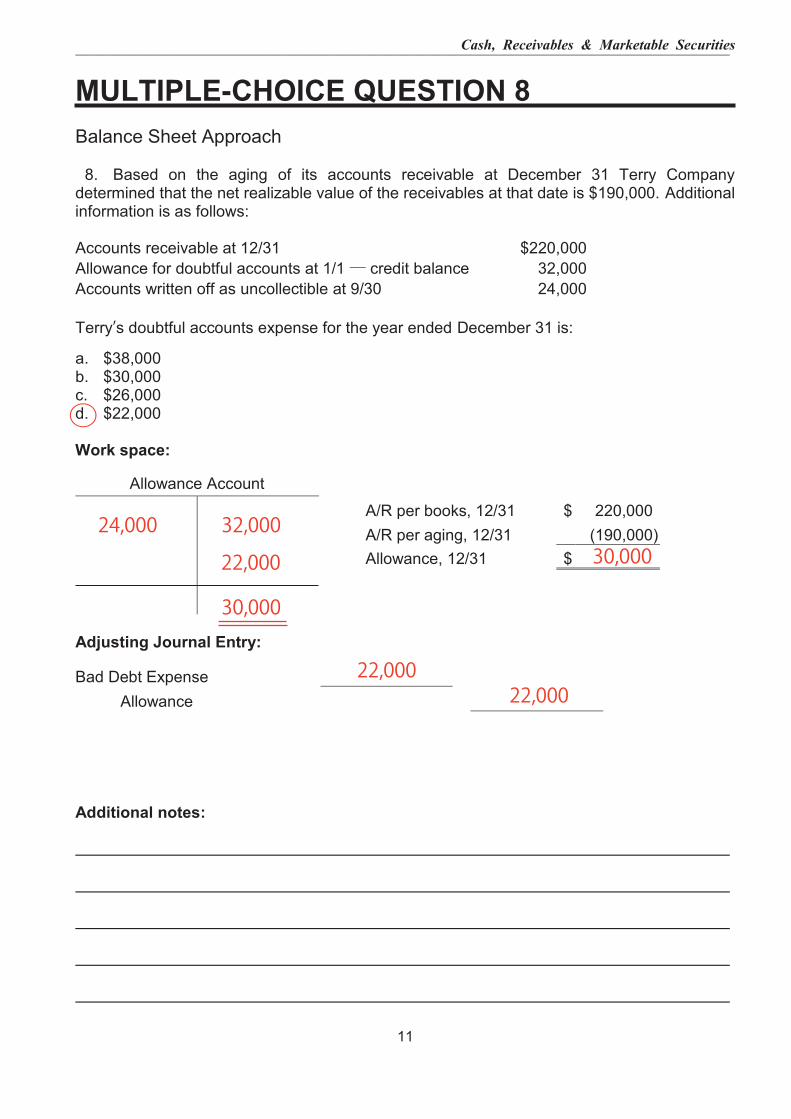

MULTIPLE-CHOICE QUESTION 8 Balance Sheet Approach

8. Based on the aging of its accounts receivable at December 31 Terry Company determined that the net realizable value of the receivables at that date is $190,000. Additional information is as follows: Accounts receivable at 12/31 $220,000 Allowance for doubtful accounts at 1/1 ― credit balance 32,000 Accounts written off as uncollectible at 9/30 24,000 Terry’s doubtful accounts expense for the year ended December 31 is: a. $38,000 b. $30,000 c. $26,000 d. $22,000 Work space:

Allowance Account A/R per books, 12/31 $ 220,000

A/R per aging, 12/31 (190,000) Allowance, 12/31 $

Adjusting Journal Entry:

Bad Debt Expense

Allowance Additional notes:

24,000 32,00030,000

30,000

22,00022,000

22,000

○

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

12

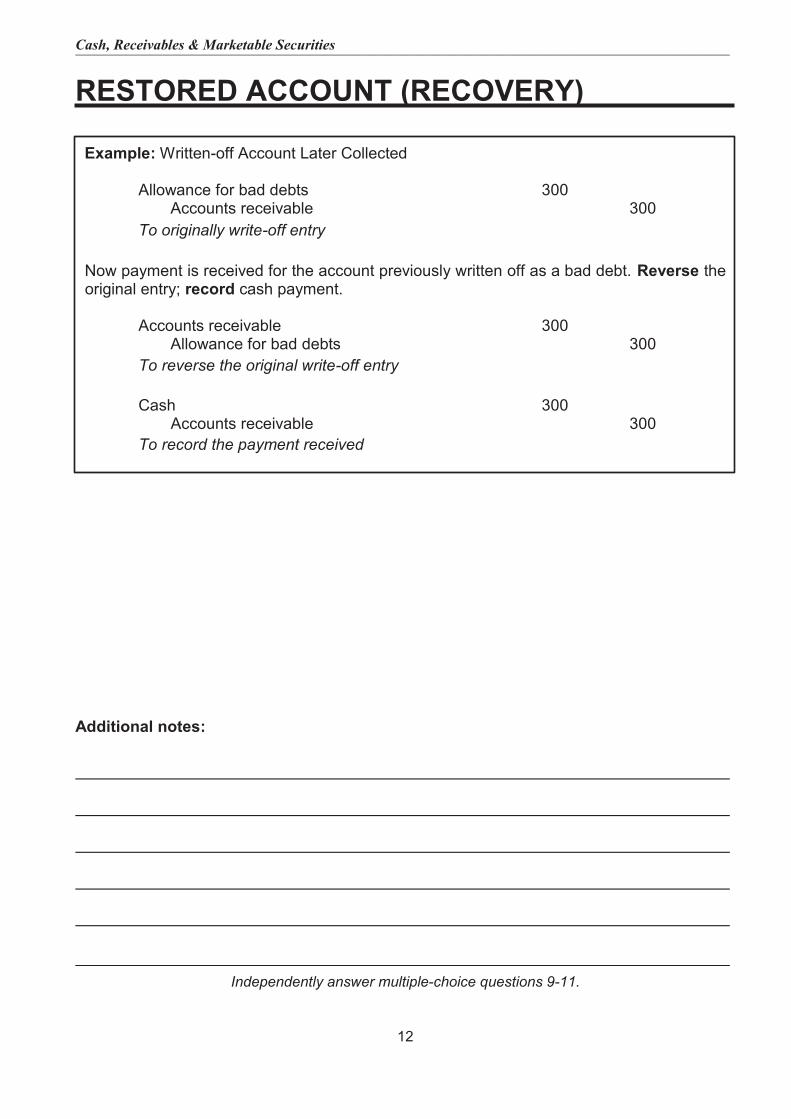

RESTORED ACCOUNT (RECOVERY)

Example: Written-off Account Later Collected

Allowance for bad debts 300 Accounts receivable 300

To originally write-off entry

Now payment is received for the account previously written off as a bad debt. Reverse the original entry; record cash payment.

Accounts receivable 300 Allowance for bad debts 300

To reverse the original write-off entry

Cash 300 Accounts receivable 300

To record the payment received

Additional notes:

Independently answer multiple-choice questions 9-11.

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

13

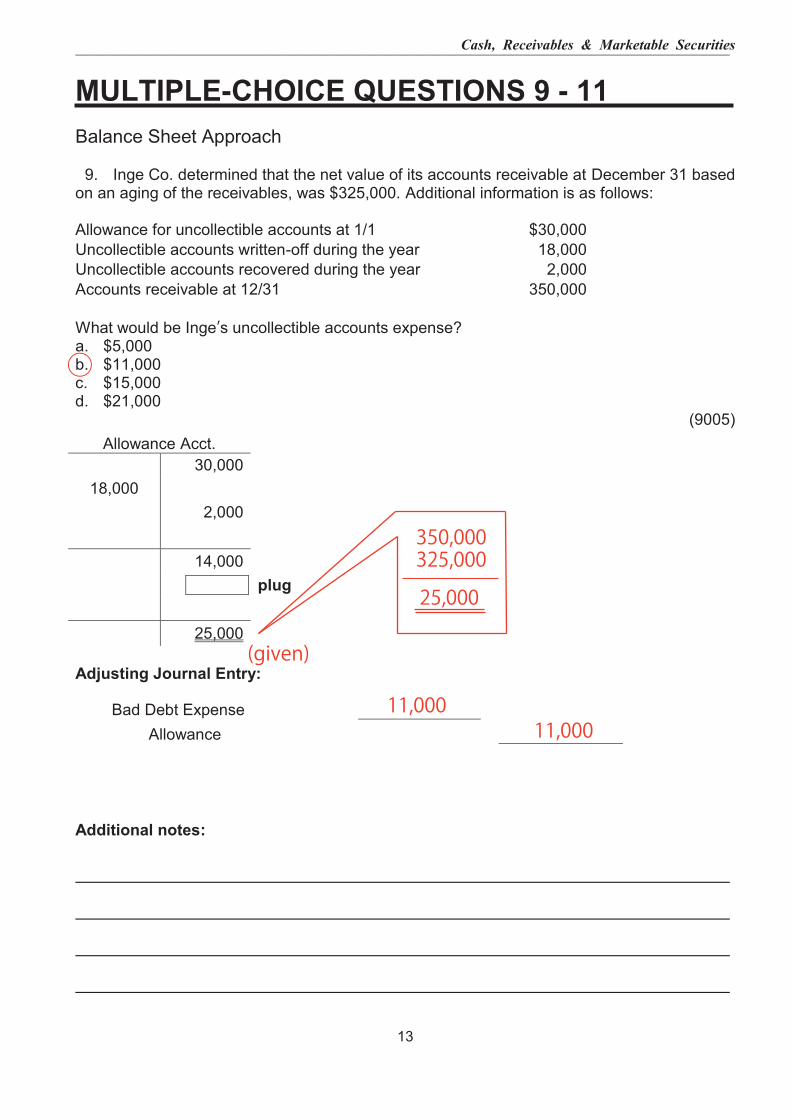

MULTIPLE-CHOICE QUESTIONS 9 - 11Balance Sheet Approach

9. Inge Co. determined that the net value of its accounts receivable at December 31 basedon an aging of the receivables, was $325,000. Additional information is as follows:

Allowance for uncollectible accounts at 1/1 $30,000 Uncollectible accounts written-off during the year 18,000 Uncollectible accounts recovered during the year 2,000 Accounts receivable at 12/31 350,000

What would be Inge’s uncollectible accounts expense?a. $5,000b. $11,000c. $15,000d. $21,000

(9005) Allowance Acct.

30,000 18,000

2,000

14,000 A aaaa plug

25,000

Adjusting Journal Entry:

Bad Debt Expense Allowance

Additional notes:

○

350,000325,000

25,000

11,00011,000

(given)

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

14

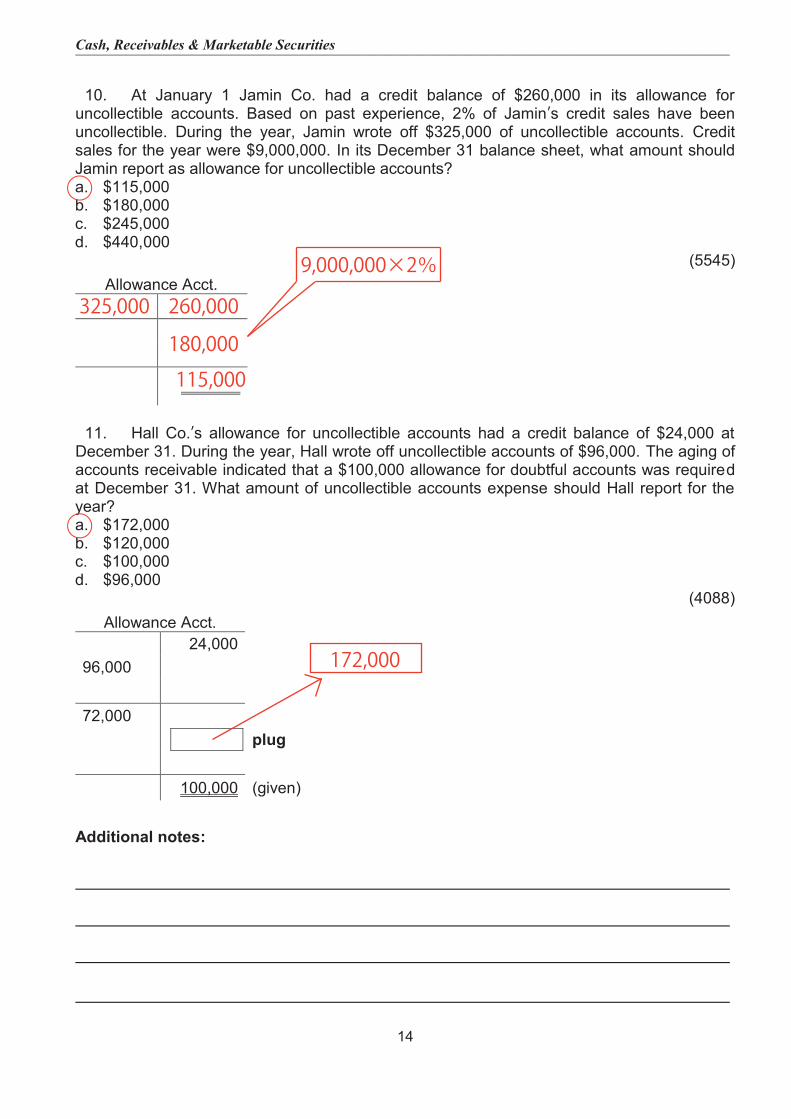

10. At January 1 Jamin Co. had a credit balance of $260,000 in its allowance for

uncollectible accounts. Based on past experience, 2% of Jamin’s credit sales have been uncollectible. During the year, Jamin wrote off $325,000 of uncollectible accounts. Credit sales for the year were $9,000,000. In its December 31 balance sheet, what amount should Jamin report as allowance for uncollectible accounts? a. $115,000 b. $180,000 c. $245,000 d. $440,000

(5545) Allowance Acct.

11. Hall Co.’s allowance for uncollectible accounts had a credit balance of $24,000 at

December 31. During the year, Hall wrote off uncollectible accounts of $96,000. The aging of accounts receivable indicated that a $100,000 allowance for doubtful accounts was required at December 31. What amount of uncollectible accounts expense should Hall report for the year? a. $172,000 b. $120,000 c. $100,000 d. $96,000

(4088) Allowance Acct.

24,000 96,000 72,000 Aa aa plug 100,000 (given)

Additional notes:

○

325,000 260,000

180,000

115,000

9,000,000×2%

172,000

○

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

15

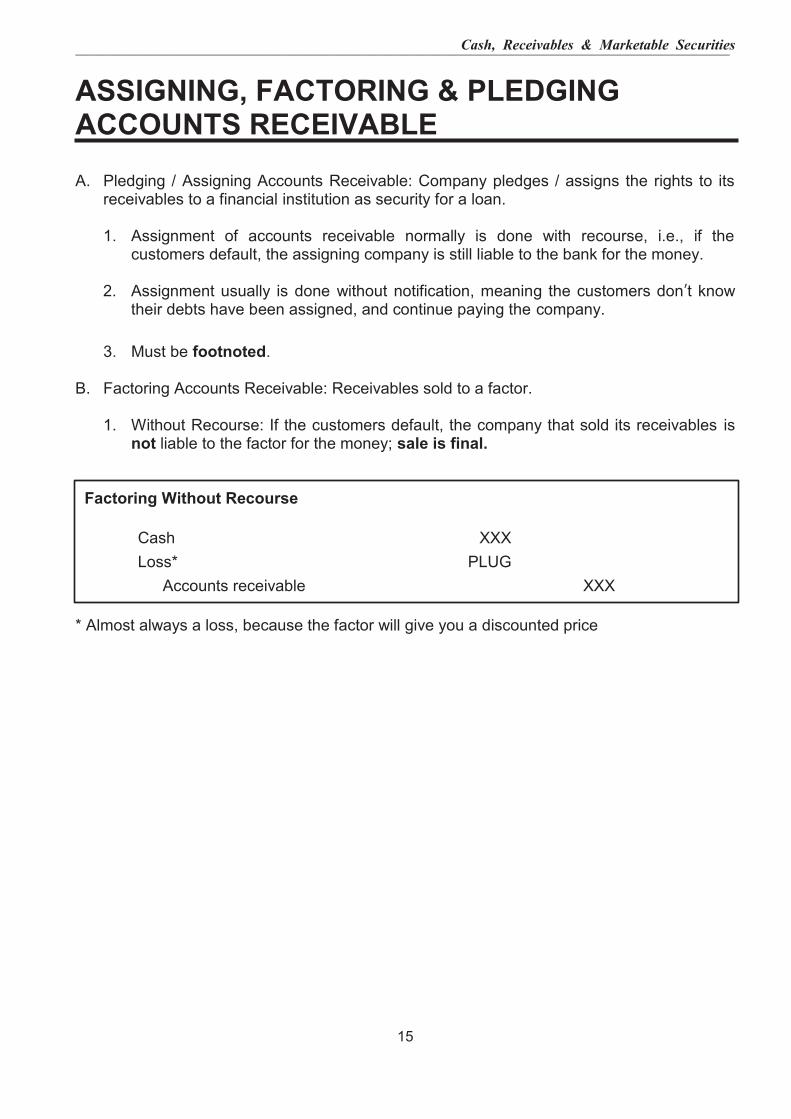

ASSIGNING, FACTORING & PLEDGING ACCOUNTS RECEIVABLE

A. Pledging / Assigning Accounts Receivable: Company pledges / assigns the rights to its

receivables to a financial institution as security for a loan. 1. Assignment of accounts receivable normally is done with recourse, i.e., if the

customers default, the assigning company is still liable to the bank for the money.

2. Assignment usually is done without notification, meaning the customers don’t know their debts have been assigned, and continue paying the company.

3. Must be footnoted. B. Factoring Accounts Receivable: Receivables sold to a factor.

1. Without Recourse: If the customers default, the company that sold its receivables is

not liable to the factor for the money; sale is final.

Factoring Without Recourse

Cash XXX Loss* PLUG Accounts receivable XXX

* Almost always a loss, because the factor will give you a discounted price

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

16

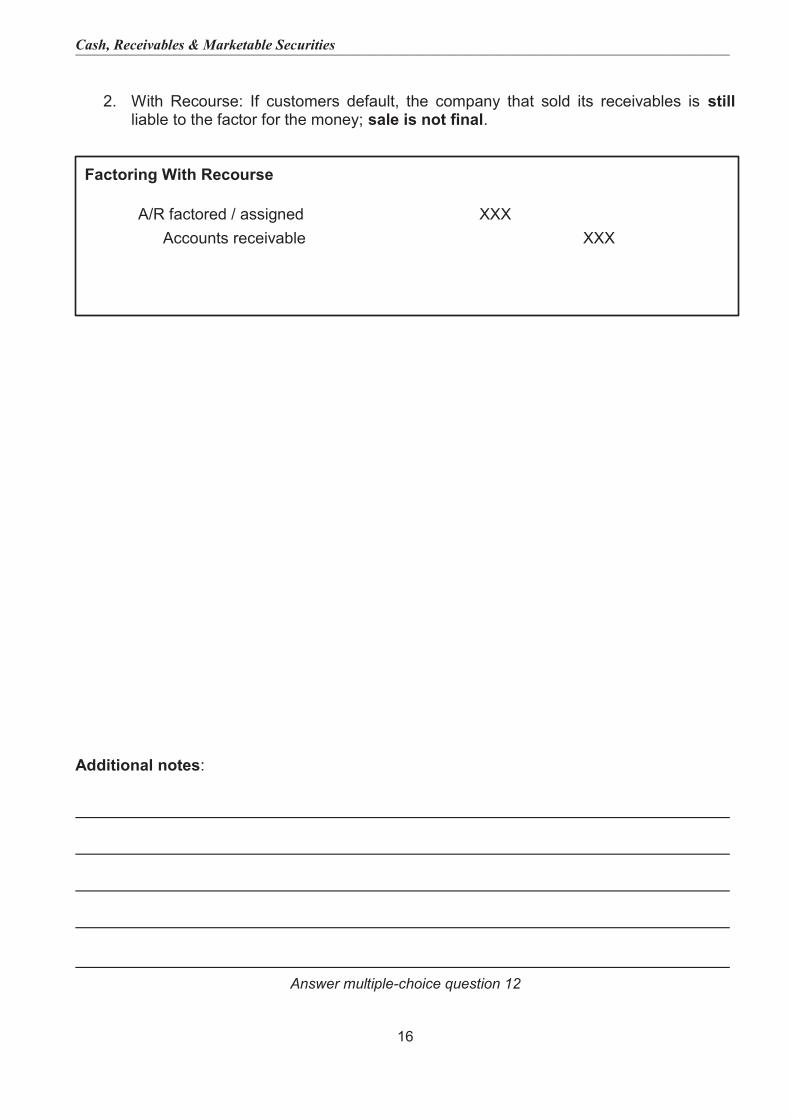

2. With Recourse: If customers default, the company that sold its receivables is still

liable to the factor for the money; sale is not final.

Factoring With Recourse

A/R factored / assigned XXX Accounts receivable XXX

Additional notes:

Answer multiple-choice question 12

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

17

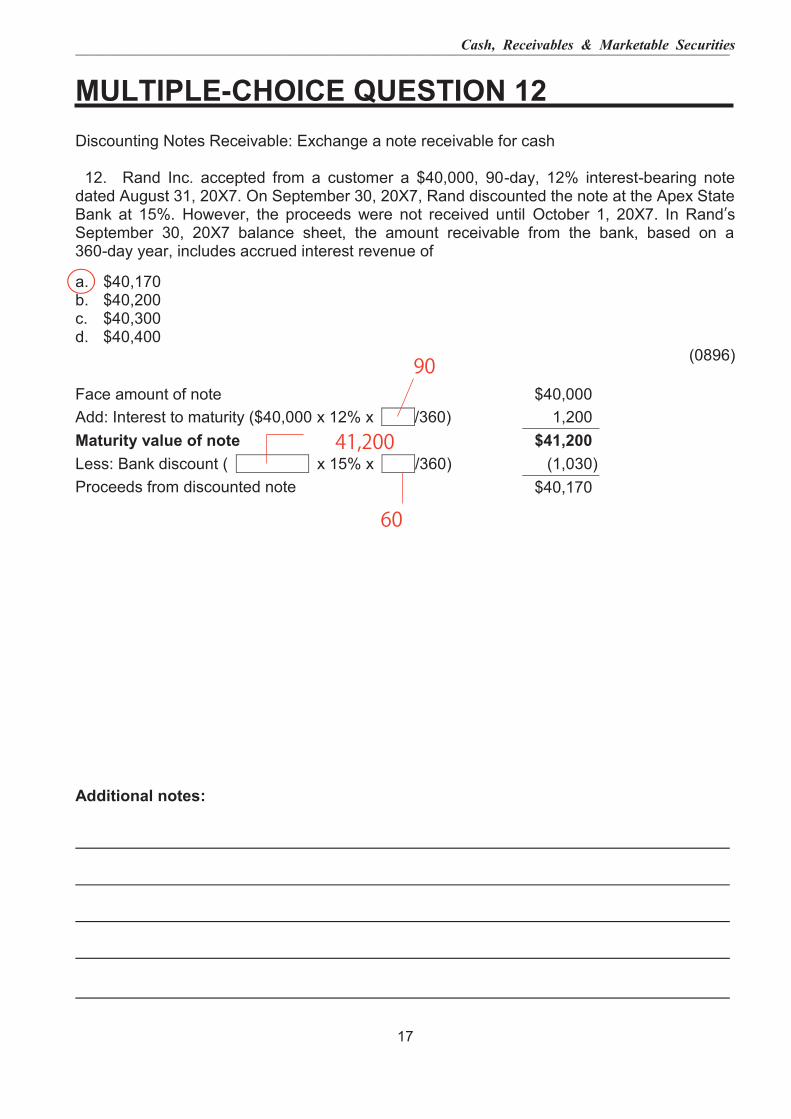

MULTIPLE-CHOICE QUESTION 12Discounting Notes Receivable: Exchange a note receivable for cash

12. Rand Inc. accepted from a customer a $40,000, 90-day, 12% interest-bearing notedated August 31, 20X7. On September 30, 20X7, Rand discounted the note at the Apex State Bank at 15%. However, the proceeds were not received until October 1, 20X7. In Rand’sSeptember 30, 20X7 balance sheet, the amount receivable from the bank, based on a 360-day year, includes accrued interest revenue of

a. $40,170b. $40,200c. $40,300d. $40,400

(0896)

Face amount of note $40,000 Add: Interest to maturity ($40,000 x 12% x /360) 1,200 Maturity value of note $41,200

x 15% x /360) (1,030) $40,170

Less: Bank discount ( Proceeds from discounted note

Additional notes:

○

90

41,200

60

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

18

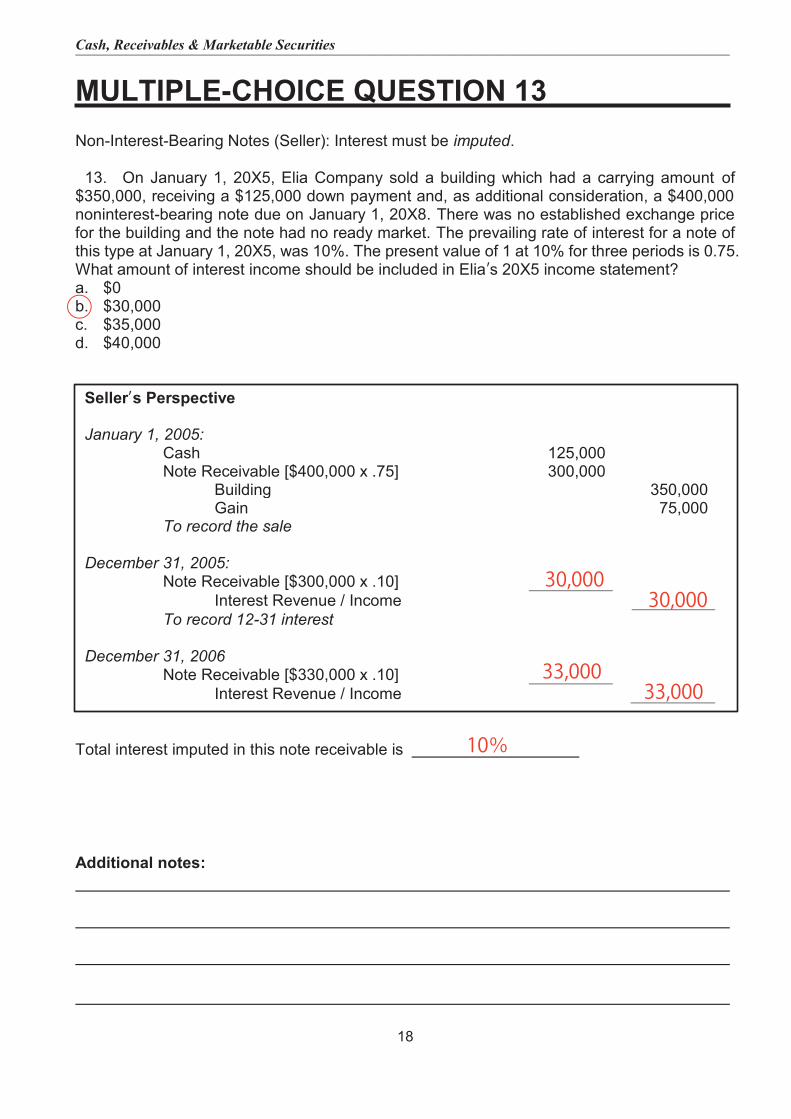

MULTIPLE-CHOICE QUESTION 13Non-Interest-Bearing Notes (Seller): Interest must be imputed.

13. On January 1, 20X5, Elia Company sold a building which had a carrying amount of$350,000, receiving a $125,000 down payment and, as additional consideration, a $400,000 noninterest-bearing note due on January 1, 20X8. There was no established exchange price for the building and the note had no ready market. The prevailing rate of interest for a note of this type at January 1, 20X5, was 10%. The present value of 1 at 10% for three periods is 0.75. What amount of interest income should be included in Elia’s 20X5 income statement?a. $0b. $30,000c. $35,000d. $40,000

Seller’s Perspective

January 1, 2005: Cash 125,000 Note Receivable [$400,000 x .75] 300,000

Building 350,000 Gain 75,000

To record the sale

December 31, 2005: Note Receivable [$300,000 x .10]

Interest Revenue / Income To record 12-31 interest

December 31, 2006 Note Receivable [$330,000 x .10]

Interest Revenue / Income

Total interest imputed in this note receivable is

Additional notes:

○

30,00030,000

33,00033,000

10%

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

19

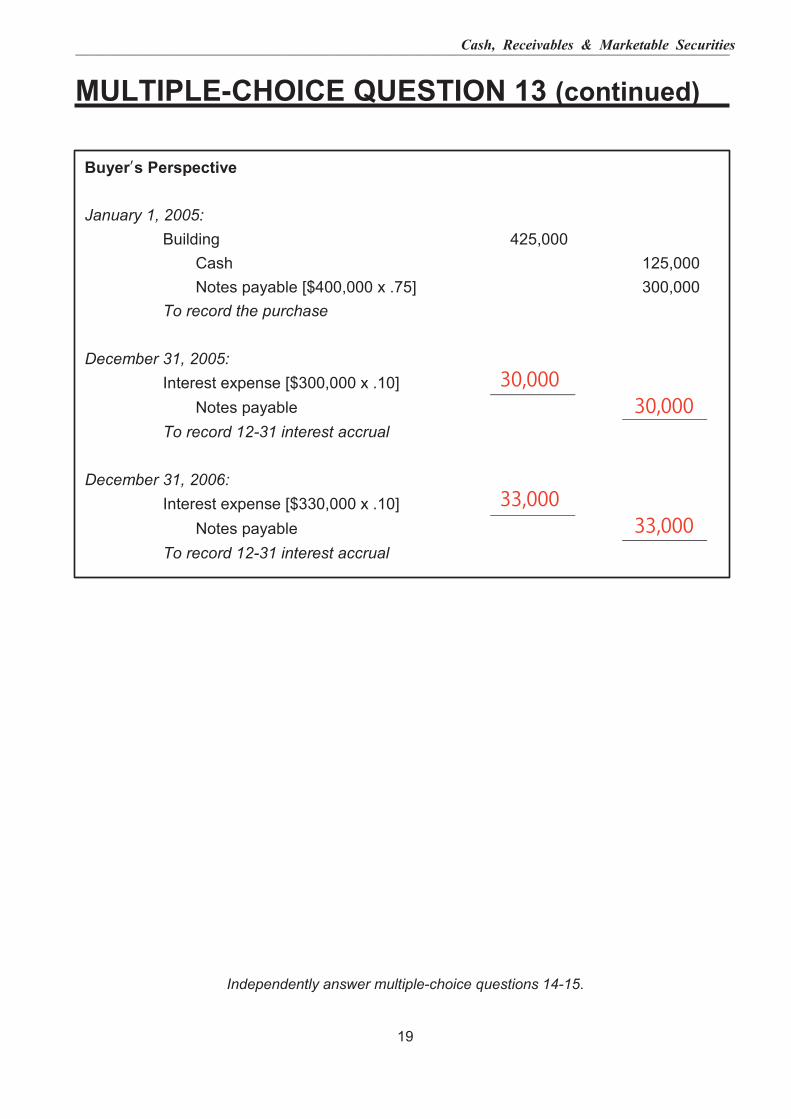

MULTIPLE-CHOICE QUESTION 13 (continued)

Buyer’s Perspective January 1, 2005: Building 425,000 Cash 125,000 Notes payable [$400,000 x .75] 300,000 To record the purchase December 31, 2005: Interest expense [$300,000 x .10] Notes payable To record 12-31 interest accrual December 31, 2006: Interest expense [$330,000 x .10] Notes payable To record 12-31 interest accrual

Independently answer multiple-choice questions 14-15.

30,00030,000

33,00033,000

Cash, Receivables & Marketable Securities

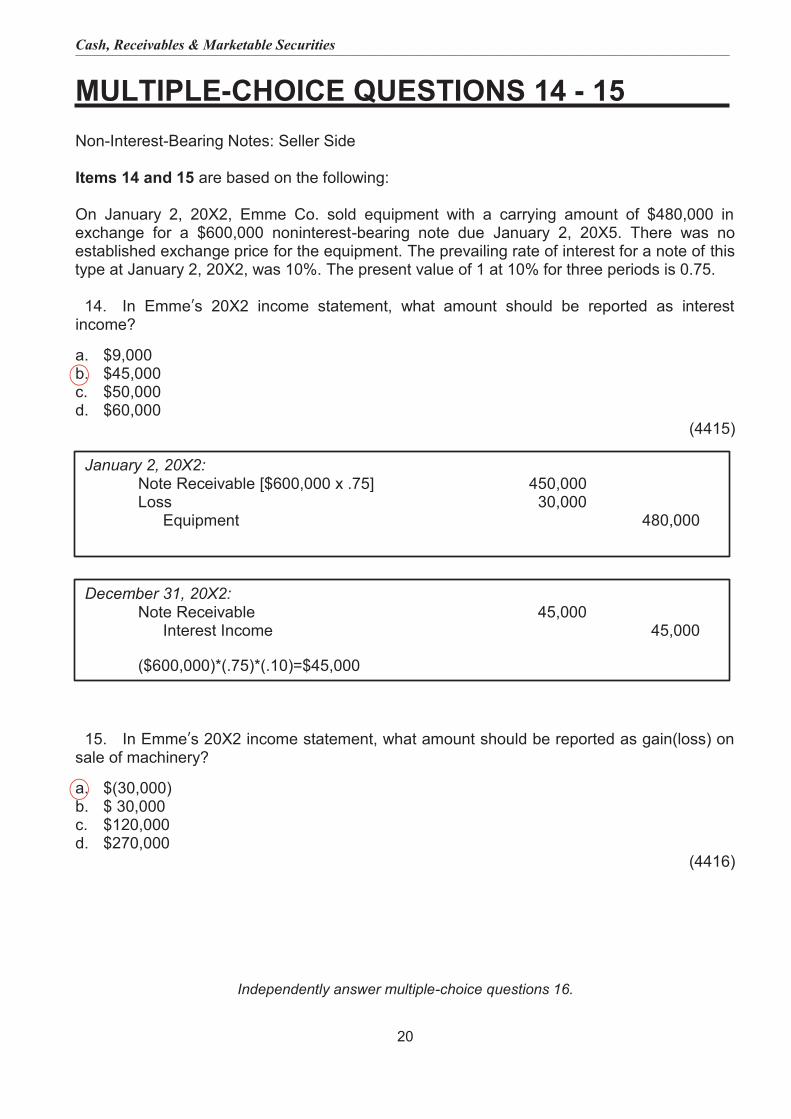

20

MULTIPLE-CHOICE QUESTIONS 14 - 15 Non-Interest-Bearing Notes: Seller Side Items 14 and 15 are based on the following: On January 2, 20X2, Emme Co. sold equipment with a carrying amount of $480,000 in exchange for a $600,000 noninterest-bearing note due January 2, 20X5. There was no established exchange price for the equipment. The prevailing rate of interest for a note of this type at January 2, 20X2, was 10%. The present value of 1 at 10% for three periods is 0.75.

14. In Emme’s 20X2 income statement, what amount should be reported as interest income?

a. $9,000 b. $45,000 c. $50,000 d. $60,000

(4415)

January 2, 20X2: Note Receivable [$600,000 x .75] 450,000 Loss 30,000 Equipment 480,000

December 31, 20X2:

Note Receivable 45,000 Interest Income 45,000

($600,000)*(.75)*(.10)=$45,000

15. In Emme’s 20X2 income statement, what amount should be reported as gain(loss) on sale of machinery?

a. $(30,000) b. $ 30,000 c. $120,000 d. $270,000

(4416)

Independently answer multiple-choice questions 16.

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

21

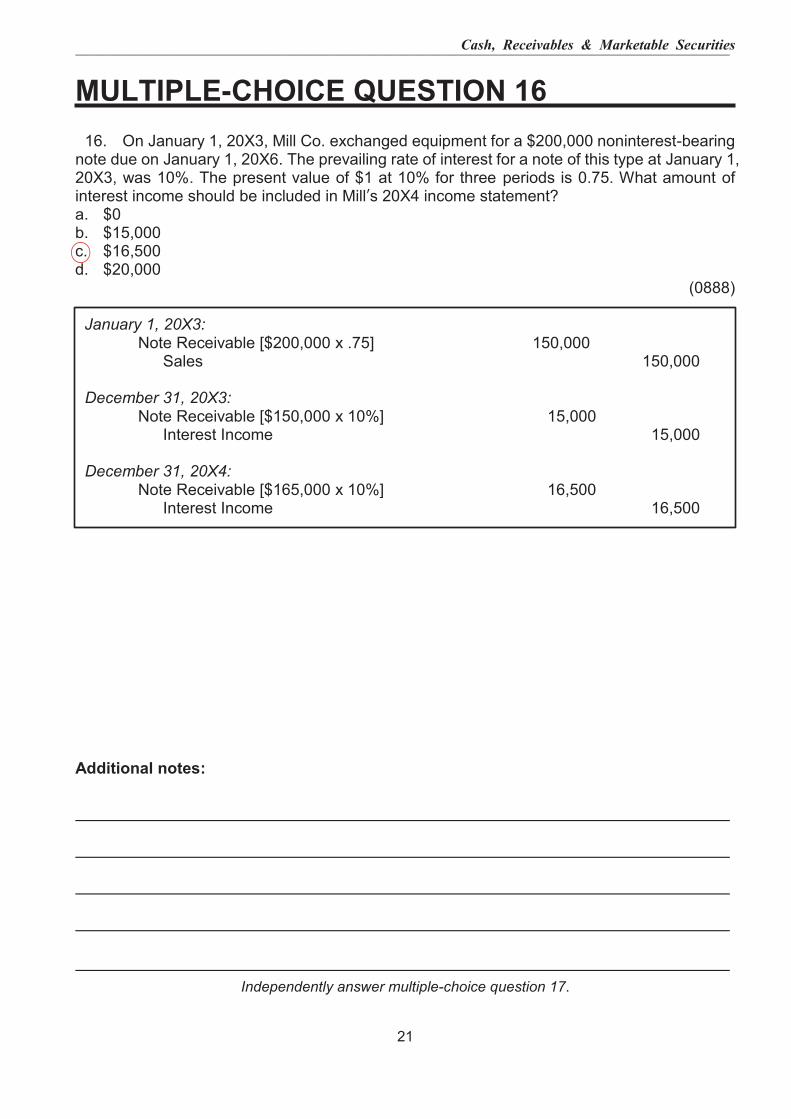

MULTIPLE-CHOICE QUESTION 16

16. On January 1, 20X3, Mill Co. exchanged equipment for a $200,000 noninterest-bearing note due on January 1, 20X6. The prevailing rate of interest for a note of this type at January 1, 20X3, was 10%. The present value of $1 at 10% for three periods is 0.75. What amount of interest income should be included in Mill’s 20X4 income statement? a. $0 b. $15,000 c. $16,500 d. $20,000

(0888)

January 1, 20X3: Note Receivable [$200,000 x .75] 150,000 Sales 150,000

December 31, 20X3:

Note Receivable [$150,000 x 10%] 15,000 Interest Income 15,000

December 31, 20X4:

Note Receivable [$165,000 x 10%] 16,500 Interest Income 16,500

Additional notes:

Independently answer multiple-choice question 17.

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

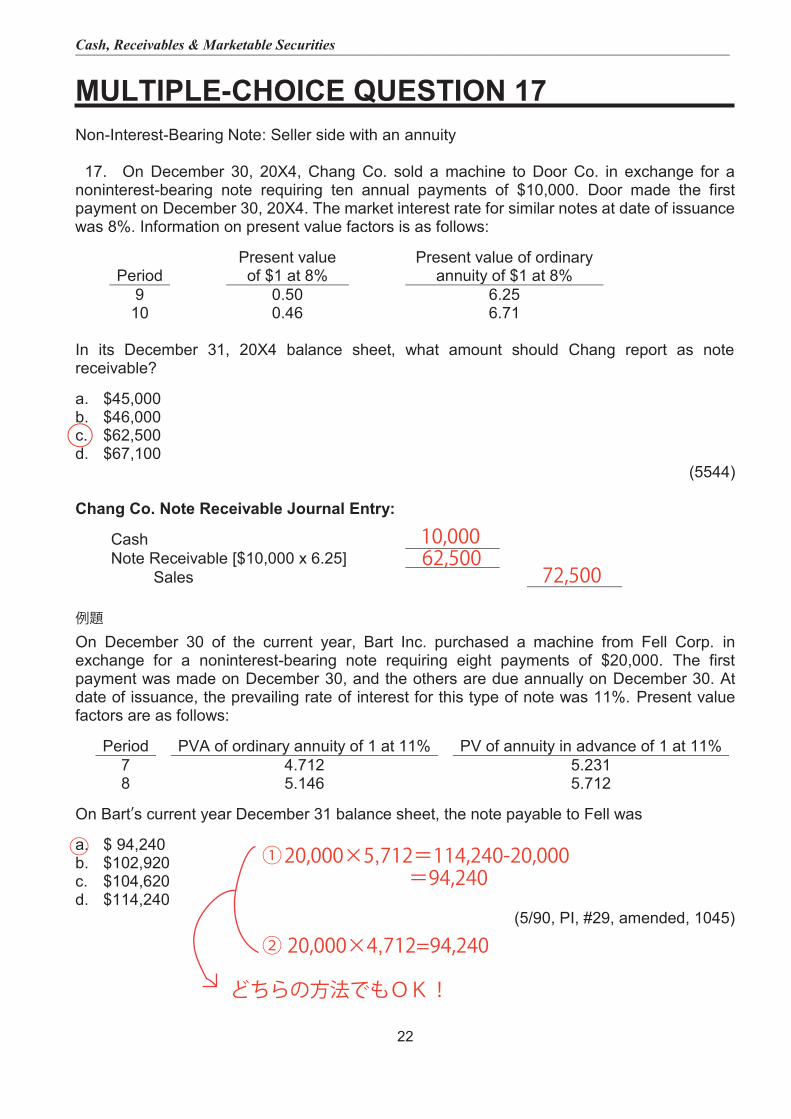

22

MULTIPLE-CHOICE QUESTION 17Non-Interest-Bearing Note: Seller side with an annuity

17. On December 30, 20X4, Chang Co. sold a machine to Door Co. in exchange for anoninterest-bearing note requiring ten annual payments of $10,000. Door made the first payment on December 30, 20X4. The market interest rate for similar notes at date of issuance was 8%. Information on present value factors is as follows:

Period Present value of $1 at 8%

Present value of ordinary annuity of $1 at 8%

9 0.50 6.25 10 0.46 6.71

In its December 31, 20X4 balance sheet, what amount should Chang report as note receivable?

a. $45,000b. $46,000c. $62,500d. $67,100

(5544)

Chang Co. Note Receivable Journal Entry:

Cash Note Receivable [$10,000 x 6.25]

Sales

例題 On December 30 of the current year, Bart Inc. purchased a machine from Fell Corp. in exchange for a noninterest-bearing note requiring eight payments of $20,000. The first payment was made on December 30, and the others are due annually on December 30. At date of issuance, the prevailing rate of interest for this type of note was 11%. Present value factors are as follows:

Period PVA of ordinary annuity of 1 at 11% PV of annuity in advance of 1 at 11% 7 4.712 5.231 8 5.146 5.712

On Bart’s current year December 31 balance sheet, the note payable to Fell was

a. $ 94,240b. $102,920c. $104,620d. $114,240

(5/90, PI, #29, amended, 1045)

○

10,00062,500

72,500

○ 20,000×5,712=114,240-20,000 =94,240

20,000×4,712=94,240

①

②

どちらの方法でもOK!

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

23

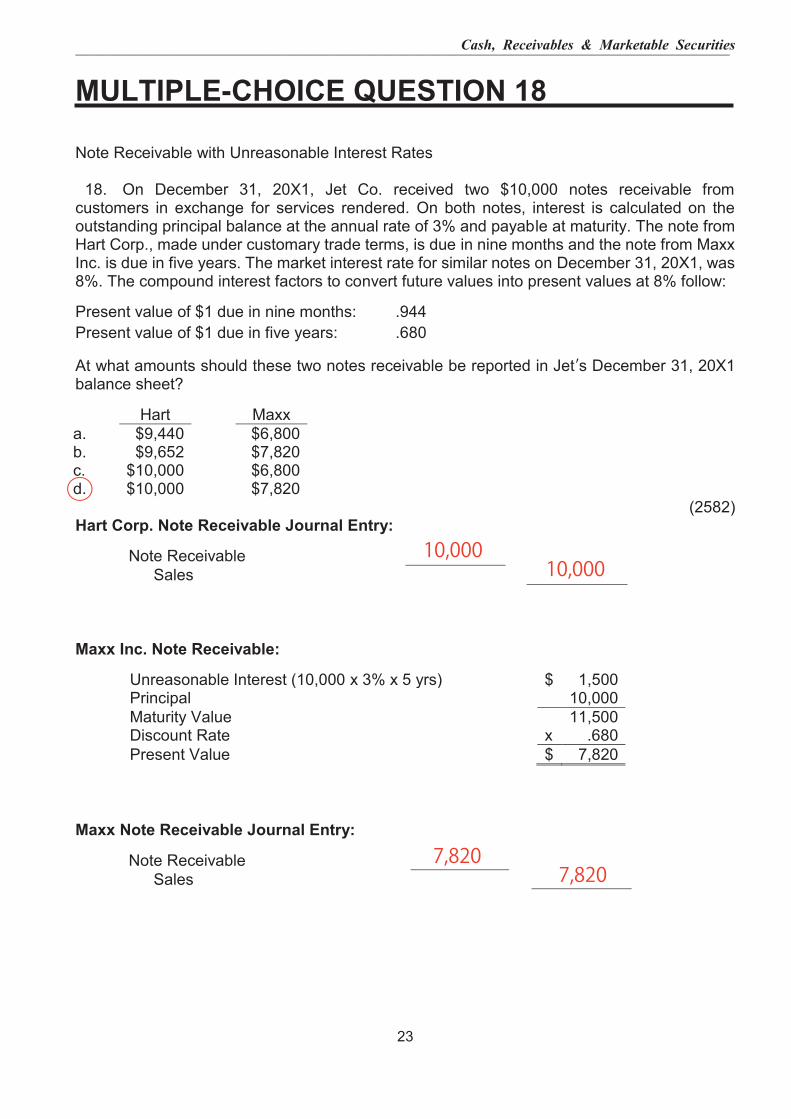

MULTIPLE-CHOICE QUESTION 18

Note Receivable with Unreasonable Interest Rates

18. On December 31, 20X1, Jet Co. received two $10,000 notes receivable fromcustomers in exchange for services rendered. On both notes, interest is calculated on the outstanding principal balance at the annual rate of 3% and payable at maturity. The note from Hart Corp., made under customary trade terms, is due in nine months and the note from Maxx Inc. is due in five years. The market interest rate for similar notes on December 31, 20X1, was 8%. The compound interest factors to convert future values into present values at 8% follow:

Present value of $1 due in nine months: .944 Present value of $1 due in five years: .680 At what amounts should these two notes receivable be reported in Jet’s December 31, 20X1balance sheet?

Hart Maxx a. $9,440 $6,800 b. $9,652 $7,820 c. $10,000 $6,800 d. $10,000 $7,820

(2582) Hart Corp. Note Receivable Journal Entry:

Note Receivable Sales

Maxx Inc. Note Receivable:

Unreasonable Interest (10,000 x 3% x 5 yrs) $ 1,500 Principal 10,000 Maturity Value 11,500 Discount Rate x .680 Present Value $ 7,820

Maxx Note Receivable Journal Entry:

Note Receivable Sales

○

10,00010,000

7,8207,820

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

24

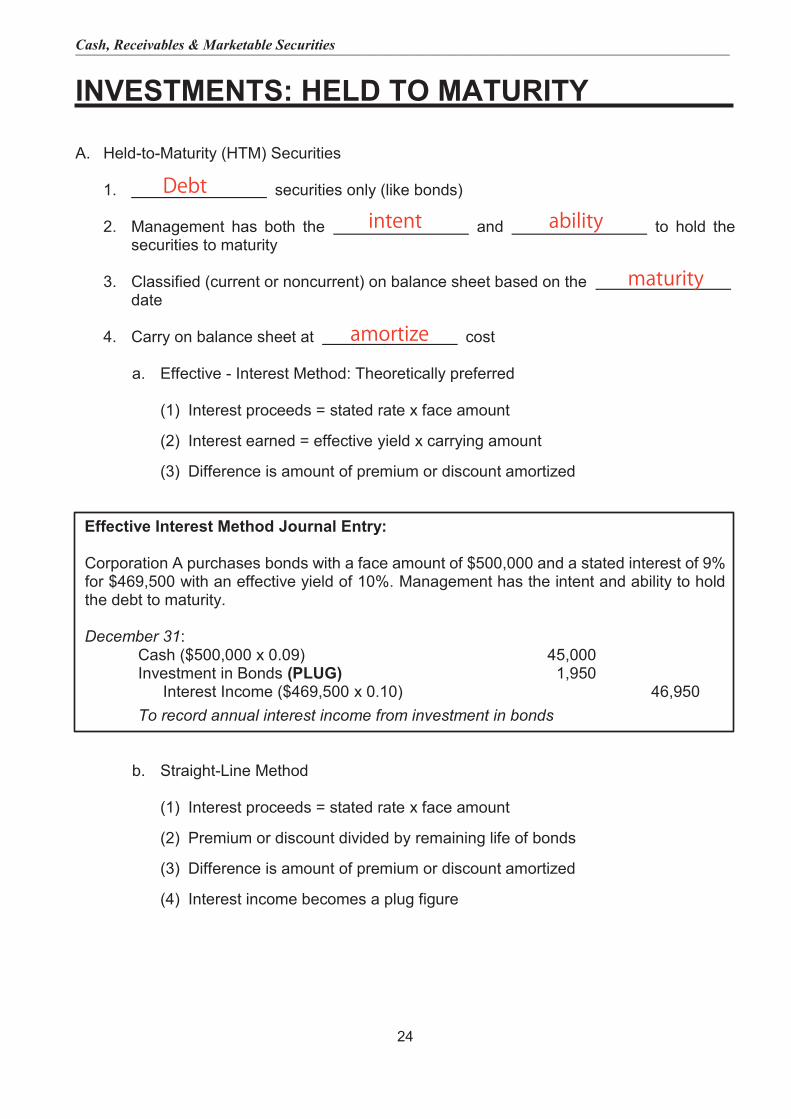

INVESTMENTS: HELD TO MATURITY

A. Held-to-Maturity (HTM) Securities

1. securities only (like bonds)

2. Management has both the and to hold the securities to maturity

3. Classified (current or noncurrent) on balance sheet based on the date

4. Carry on balance sheet at cost

a. Effective - Interest Method: Theoretically preferred

(1) Interest proceeds = stated rate x face amount

(2) Interest earned = effective yield x carrying amount

(3) Difference is amount of premium or discount amortized

Effective Interest Method Journal Entry:

Corporation A purchases bonds with a face amount of $500,000 and a stated interest of 9% for $469,500 with an effective yield of 10%. Management has the intent and ability to hold the debt to maturity.

December 31: Cash ($500,000 x 0.09) 45,000 Investment in Bonds (PLUG) 1,950

Interest Income ($469,500 x 0.10) 46,950 To record annual interest income from investment in bonds

b. Straight-Line Method

(1) Interest proceeds = stated rate x face amount

(2) Premium or discount divided by remaining life of bonds

(3) Difference is amount of premium or discount amortized

(4) Interest income becomes a plug figure

Debt

intent ability

maturity

amortize

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

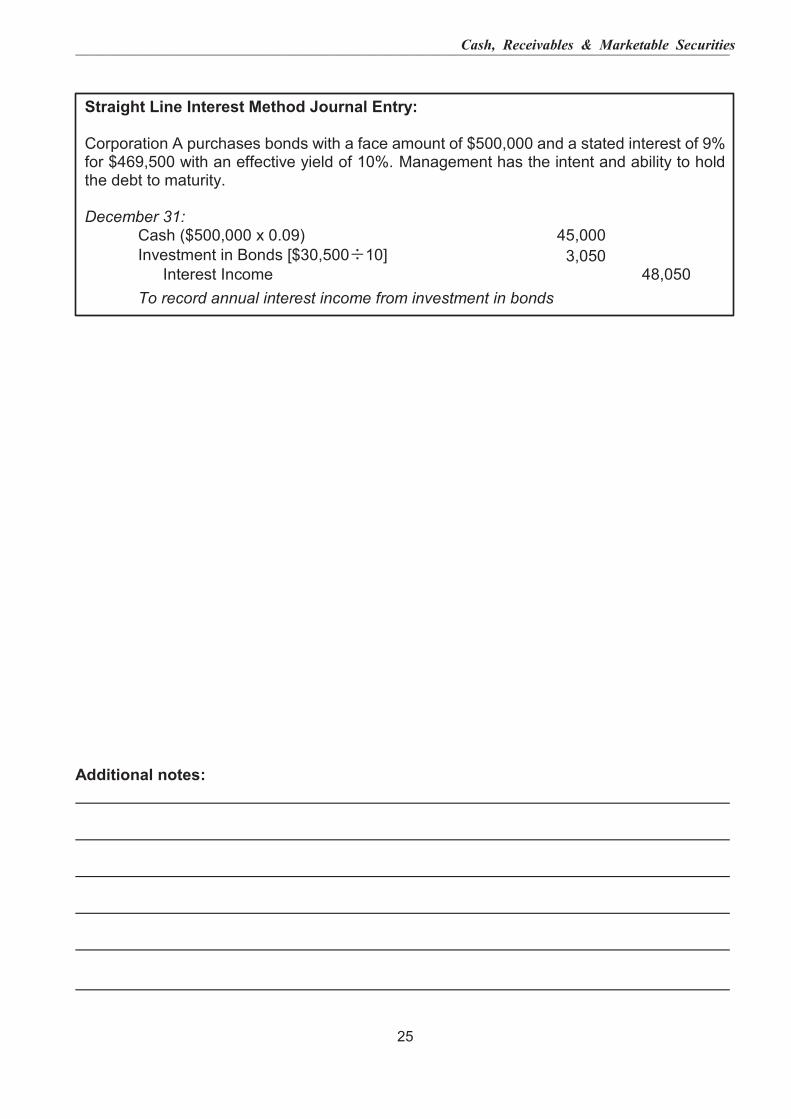

25

Straight Line Interest Method Journal Entry:

Corporation A purchases bonds with a face amount of $500,000 and a stated interest of 9% for $469,500 with an effective yield of 10%. Management has the intent and ability to hold the debt to maturity.

December 31: Cash ($500,000 x 0.09) 45,000 Investment in Bonds [$30,500÷10] 3,050

Interest Income 48,050 To record annual interest income from investment in bonds

Additional notes:

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

26

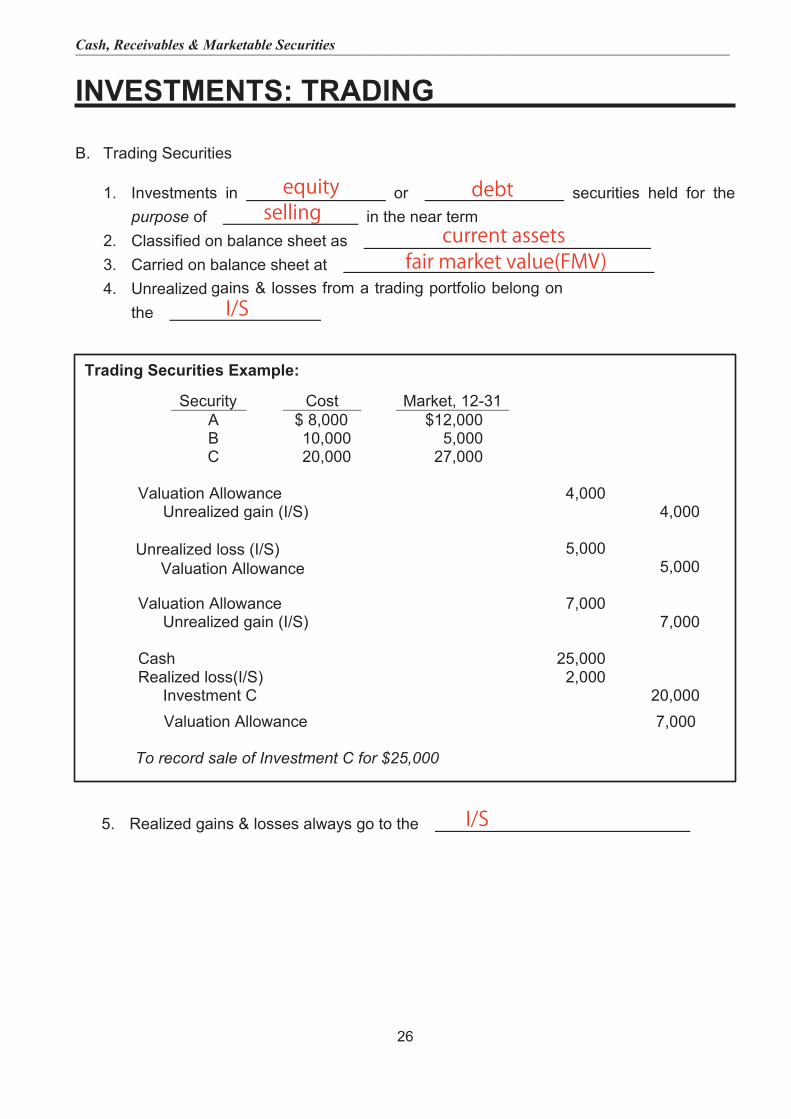

INVESTMENTS: TRADING

B. Trading Securities

1. Investments in or securities held for the purpose of in the near term

2. Classified on balance sheet as 3. Carried on balance sheet at 4. Unrealized gains & losses from a trading portfolio belong on

the

Trading Securities Example:

Security Cost Market, 12-31 A $ 8,000 $12,000 B 10,000 5,000 C 20,000 27,000

Valuation Allowance 4,000 Unrealized gain (I/S) 4,000

5,000 5,000

Valuation Allowance 7,000 Unrealized gain (I/S) 7,000

Cash 25,000 Realized loss(I/S) 2,000

Investment C 20,000

To record sale of Investment C for $25,000

5. Realized gains & losses always go to the

equity debtselling

current assetsfair market value(FMV)

I/S

I/S

Valuation Allowance 7,000

Unrealized loss (I/S) Valuation Allowance

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

27

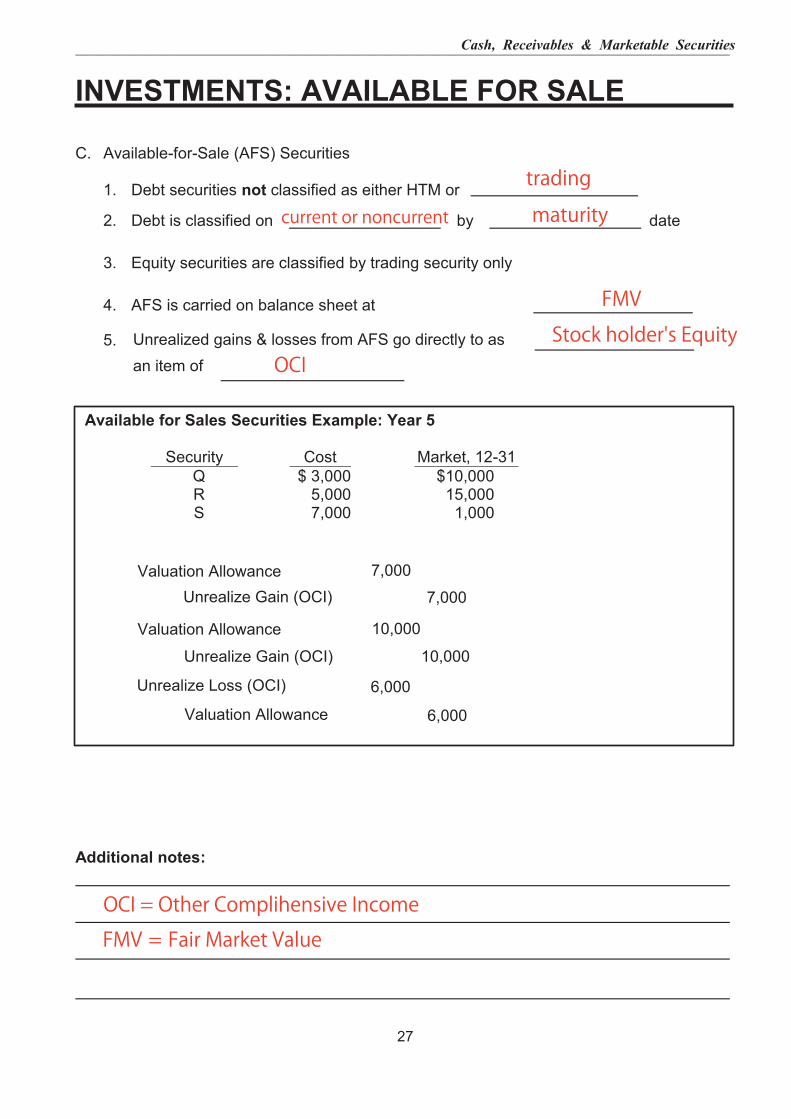

INVESTMENTS: AVAILABLE FOR SALE

C. Available-for-Sale (AFS) Securities

1. Debt securities not classified as either HTM or

2. Debt is classified on by date

3. Equity securities are classified by trading security only

4. AFS is carried on balance sheet at

5. Unrealized gains & losses from AFS go directly to asan item of

Available for Sales Securities Example: Year 5

Security Cost Market, 12-31 Q $ 3,000 $10,000 R 5,000 15,000 S 7,000 1,000

7,000 Unrealize Gain (OCI)

Additional notes:

trading

current or noncurrent maturity

FMV

OCI = Other Complihensive Income

FMV = Fair Market Value

Valuation Allowance 7,000

Valuation Allowance 10,000

Unrealize Gain (OCI) 10,000

Unrealize Loss (OCI) 6,000

Valuation Allowance 6,000

OCI

Stock holder's Equity

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

28

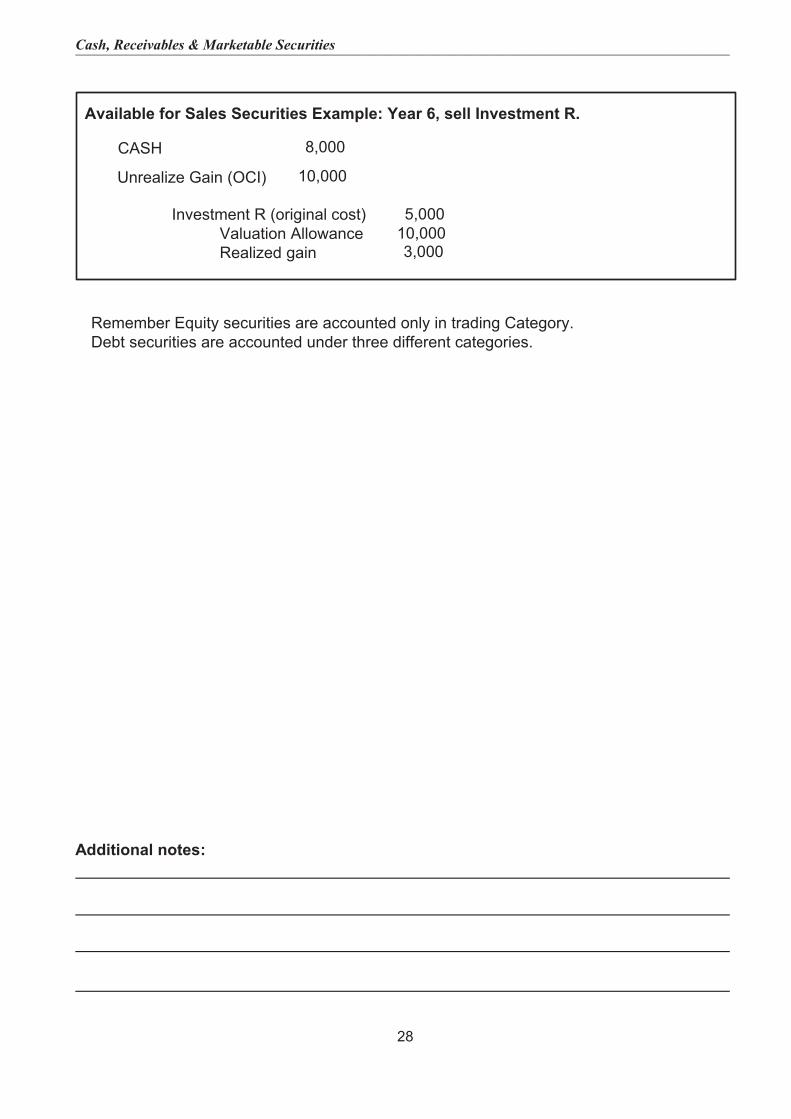

Available for Sales Securities Example: Year 6, sell Investment R.

CASH 8,000

10,000

5,000 Investment R (original cost) Valuation Allowance Realized gain 3,000

Additional notes:

Unrealize Gain (OCI)

10,000

Remember Equity securities are accounted only in trading Category.Debt securities are accounted under three different categories.

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

29

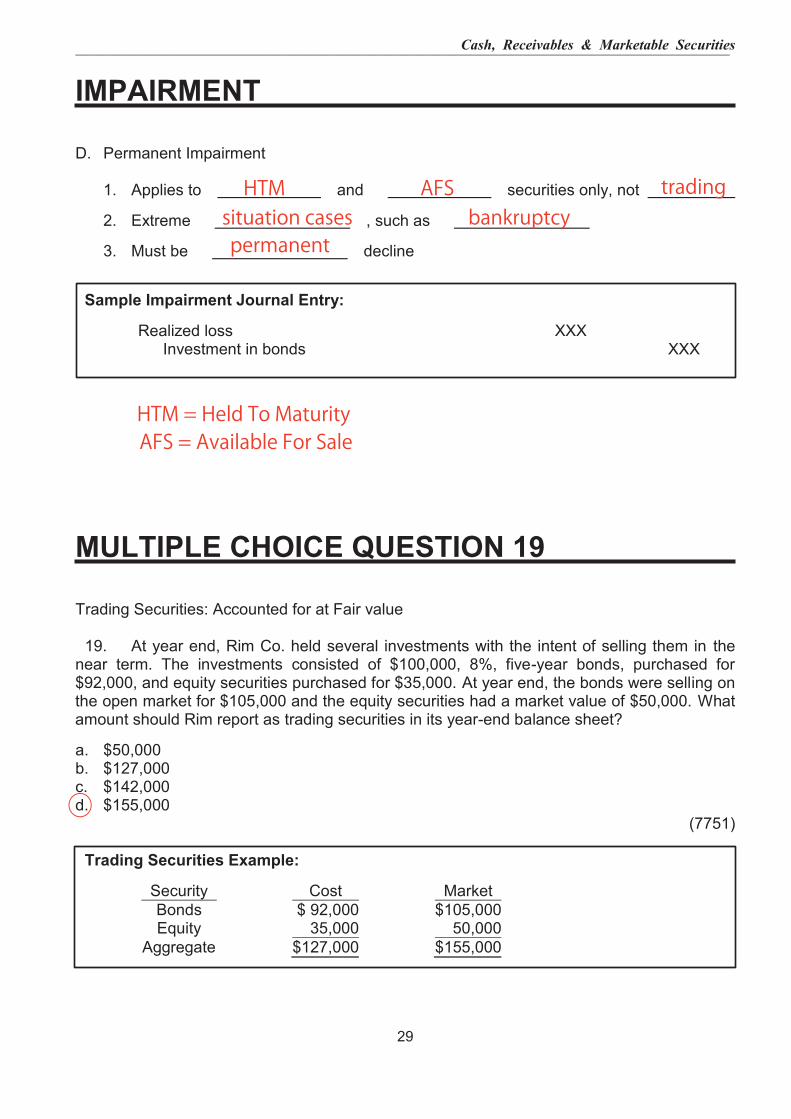

IMPAIRMENT

D. Permanent Impairment

1. Applies to and securities only, not

2. Extreme , such as

3. Must be decline

Sample Impairment Journal Entry:

Realized loss XXX Investment in bonds XXX

MULTIPLE CHOICE QUESTION 19

Trading Securities: Accounted for at Fair value

19. At year end, Rim Co. held several investments with the intent of selling them in thenear term. The investments consisted of $100,000, 8%, five-year bonds, purchased for $92,000, and equity securities purchased for $35,000. At year end, the bonds were selling on the open market for $105,000 and the equity securities had a market value of $50,000. What amount should Rim report as trading securities in its year-end balance sheet?

a. $50,000b. $127,000c. $142,000d. $155,000

(7751)

Trading Securities Example:

Security Cost Market Bonds $ 92,000 $105,000 Equity 35,000 50,000

Aggregate $127,000 $155,000

HTM AFS tradingsituation cases bankruptcypermanent

○

HTM = Held To MaturityAFS = Available For Sale

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

30

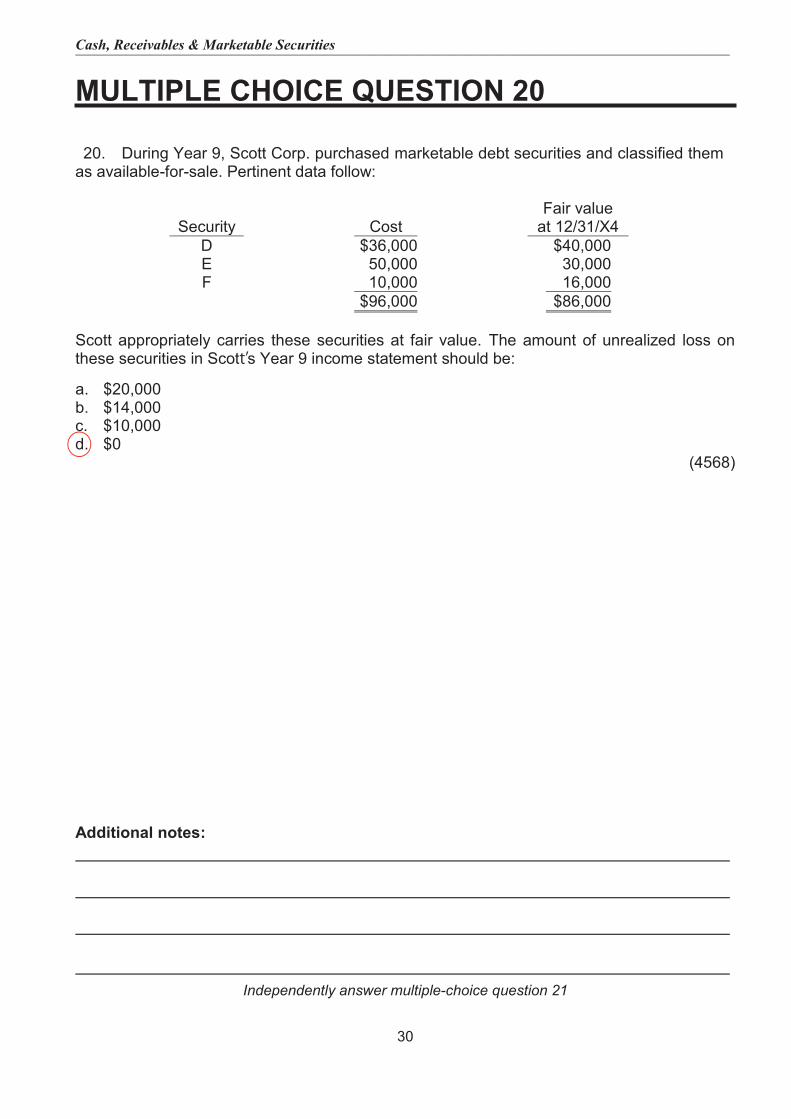

MULTIPLE CHOICE QUESTION 20

20. During Year 9, Scott Corp. purchased marketable debt securities and classified themas available-for-sale. Pertinent data follow:

Security Cost

Fair value at 12/31/X4

D $36,000 $40,000 E 50,000 30,000 F 10,000 16,000

$96,000 $86,000

Scott appropriately carries these securities at fair value. The amount of unrealized loss on these securities in Scott’s Year 9 income statement should be:

a. $20,000b. $14,000c. $10,000d. $0

(4568)

Additional notes:

Independently answer multiple-choice question 21

○

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

31

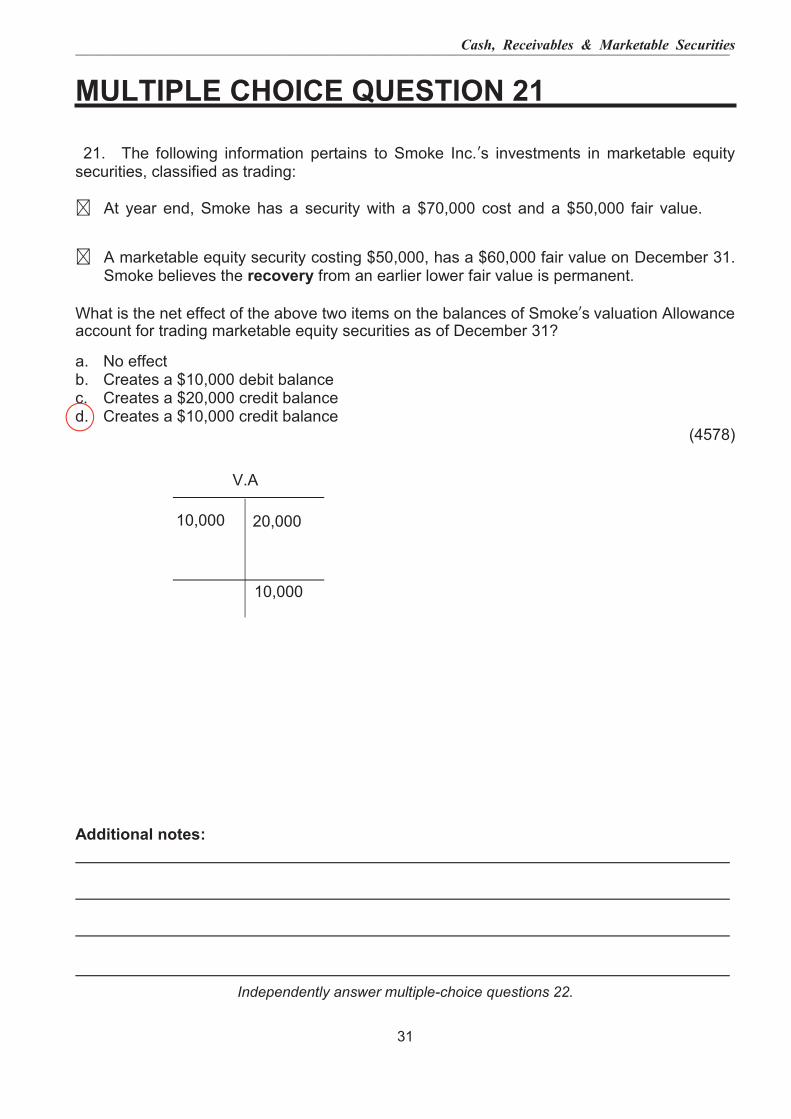

MULTIPLE CHOICE QUESTION 21

21. The following information pertains to Smoke Inc.’s investments in marketable equitysecurities, classified as trading:

At year end, Smoke has a security with a $70,000 cost and a $50,000 fair value.

A marketable equity security costing $50,000, has a $60,000 fair value on December 31. Smoke believes the recovery from an earlier lower fair value is permanent.

What is the net effect of the above two items on the balances of Smoke’s valuation Allowanceaccount for trading marketable equity securities as of December 31?

a. No effectb. Creates a $10,000 debit balancec. Creates a $20,000 credit balanced. Creates a $10,000 credit balance

(4578)

Additional notes:

Independently answer multiple-choice questions 22.

○

V.A

10,000 20,000

10,000

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

32

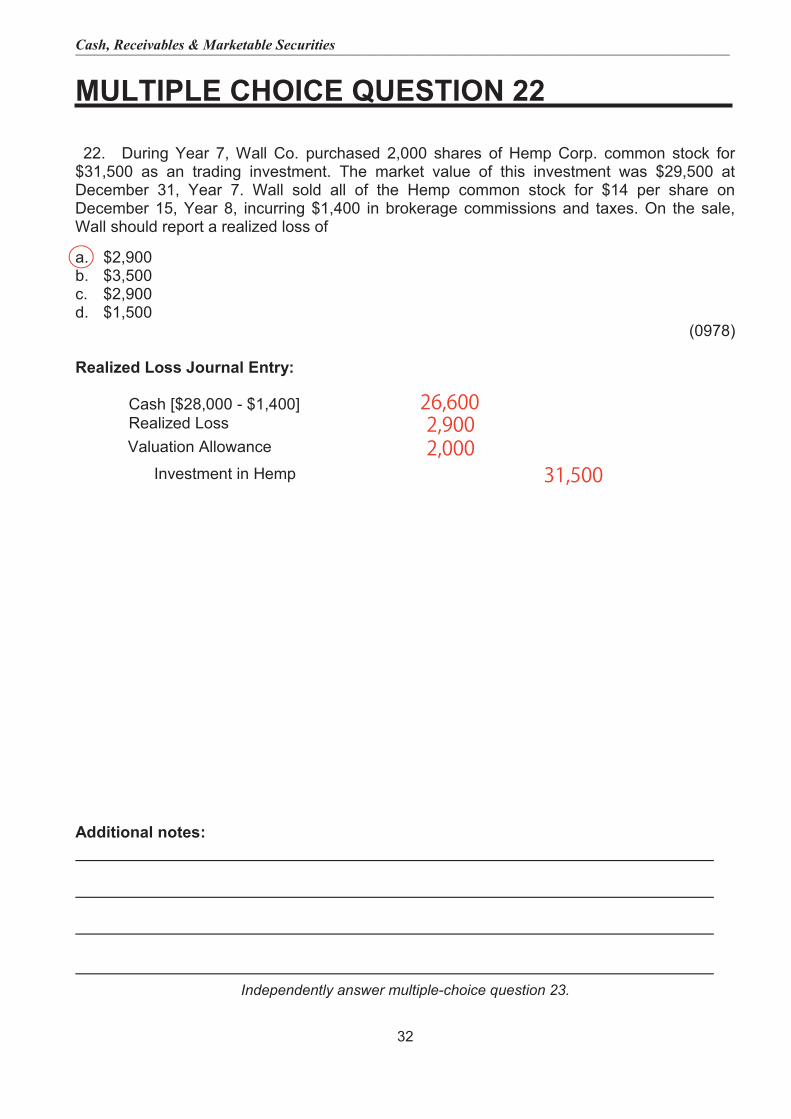

MULTIPLE CHOICE QUESTION 22

22. During Year 7, Wall Co. purchased 2,000 shares of Hemp Corp. common stock for$31,500 as an trading investment. The market value of this investment was $29,500 at December 31, Year 7. Wall sold all of the Hemp common stock for $14 per share on December 15, Year 8, incurring $1,400 in brokerage commissions and taxes. On the sale, Wall should report a realized loss of

a. $2,900b. $3,500c. $2,900d. $1,500

(0978)

Realized Loss Journal Entry:

Cash [$28,000 - $1,400] Realized Loss

Investment in Hemp

2,900

Additional notes:

Independently answer multiple-choice question 23.

26,600

31,500

○

Valuation Allowance 2,000

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

33

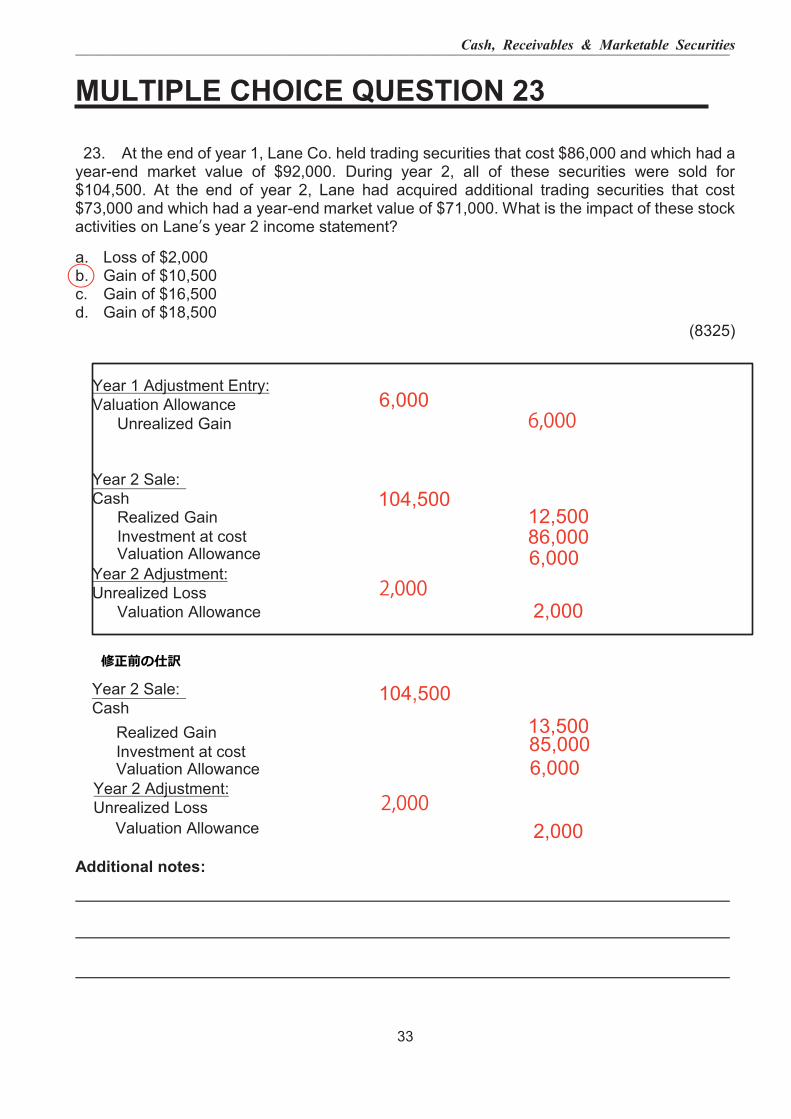

MULTIPLE CHOICE QUESTION 23

23. At the end of year 1, Lane Co. held trading securities that cost $86,000 and which had ayear-end market value of $92,000. During year 2, all of these securities were sold for $104,500. At the end of year 2, Lane had acquired additional trading securities that cost $73,000 and which had a year-end market value of $71,000. What is the impact of these stock activities on Lane’s year 2 income statement?

a. Loss of $2,000b. Gain of $10,500c. Gain of $16,500d. Gain of $18,500

(8325)

Year 1 Adjustment Entry: Valuation Allowance

Unrealized Gain

Year 2 Sale: Cash

Realized Gain Investment at cost

Year 2 Adjustment: Unrealized Loss

Valuation Allowance

Additional notes:

○

6,0006,000

12,50086,000

2,0002,000

Valuation Allowance 6,000

104,500

Year 2 Sale: Cash

Realized Gain Investment at costValuation Allowance

104,50013,50085,0006,000

修正前の仕訳

Year 2 Adjustment: Unrealized Loss

Valuation Allowance 2,000

2,000

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

34

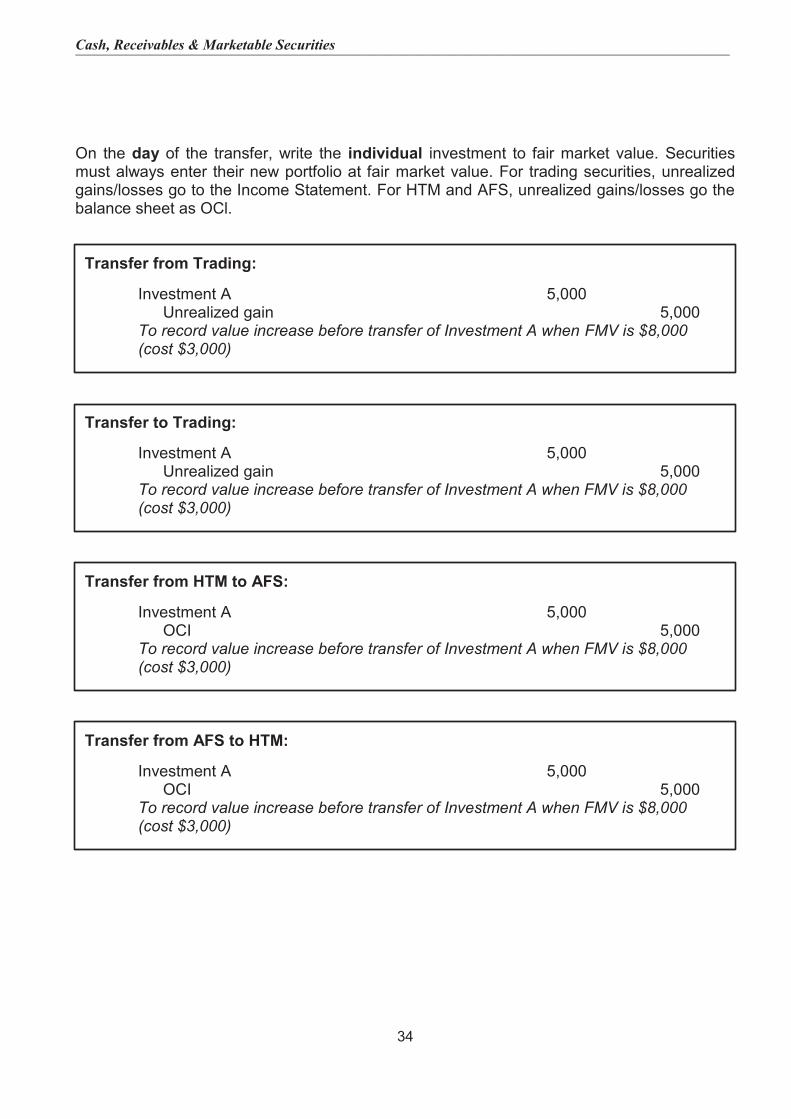

On the day of the transfer, write the individual investment to fair market value. Securities must always enter their new portfolio at fair market value. For trading securities, unrealized gains/losses go to the Income Statement. For HTM and AFS, unrealized gains/losses go the balance sheet as OCl.

Transfer from Trading:

Investment A 5,000 Unrealized gain 5,000

To record value increase before transfer of Investment A when FMV is $8,000 (cost $3,000)

Transfer to Trading:

Investment A 5,000 Unrealized gain 5,000

To record value increase before transfer of Investment A when FMV is $8,000 (cost $3,000)

Transfer from HTM to AFS:

Investment A 5,000 OCI 5,000

To record value increase before transfer of Investment A when FMV is $8,000 (cost $3,000)

Transfer from AFS to HTM:

Investment A 5,000 OCI 5,000

To record value increase before transfer of Investment A when FMV is $8,000 (cost $3,000)

Cash, Receivables & Marketable Securities ‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

35

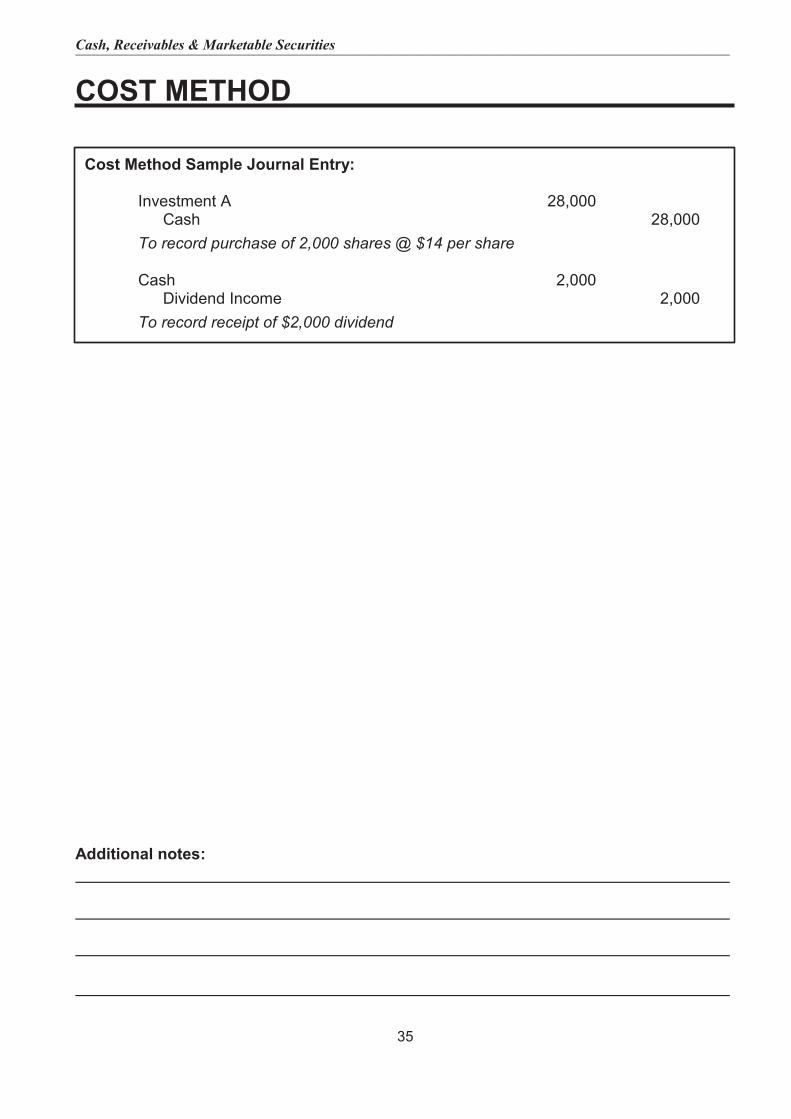

COST METHOD

Cost Method Sample Journal Entry:

Investment A 28,000 Cash 28,000 To record purchase of 2,000 shares @ $14 per share

Cash 2,000 Dividend Income 2,000

To record receipt of $2,000 dividend

Additional notes: