Embed Size (px)

Citation preview

China Natural Gas Market StatusChina Natural Gas Market Status and Outlook

Duan ZhaofangCNPC ETRI

2017.11.08·Beijing

CNPC ETRI

中国石油集团经济技术研究院| Page 1

IEEJ:November 2017 © IEEJ 2017

Outline

I China Natural Gas Market Status

II China Natural Gas Market Outlook

中国石油集团经济技术研究院| Page 2

IEEJ:November 2017 © IEEJ 2017

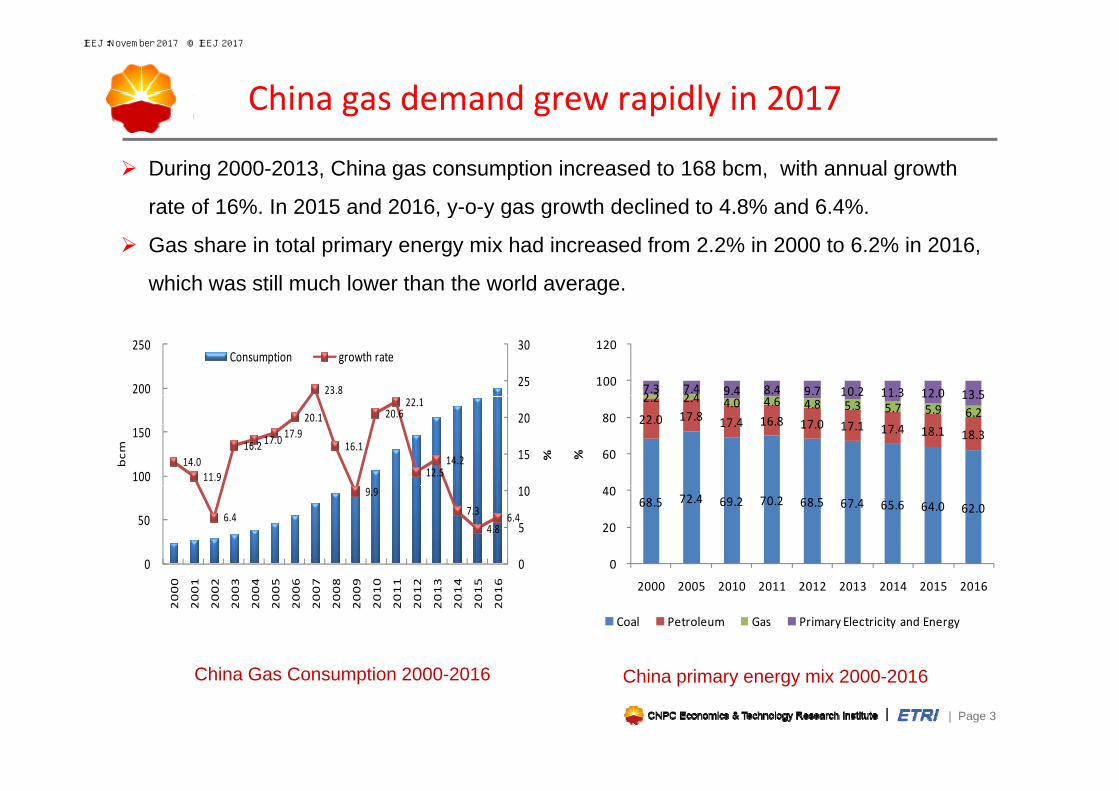

China gas demand grew rapidly in 2017

During 2000-2013, China gas consumption increased to 168 bcm, with annual growth

rate of 16%. In 2015 and 2016, y-o-y gas growth declined to 4.8% and 6.4%. , y y g g

Gas share in total primary energy mix had increased from 2.2% in 2000 to 6.2% in 2016,

which was still much lower than the world average.

23.8 25

30

200

250 Consumption growth rate

2 2 2 47.3 7.4 9.4 8.4 9.7 10.2 11.3 12 0 13 5

100

120

14.0 11.9

16.2 17.0 17.9

20.1

16.1

20.6 22.1

12.5 14.2 15

20

100

150

%bcm

22.0 17.8 17.4 16.8 17.0 17.1 17.4 18.1 18.3

2.2 2.4 4.0 4.6 4.8 5.3 5.7 5.9 6.2

10.2 11.3 12.0 13.5

60

80

%

6.4

9.9 7.3

4.8 6.4

0

5

10

0

50 68.5 72.4 69.2 70.2 68.5 67.4 65.6 64.0 62.0

0

20

40

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016 2000 2005 2010 2011 2012 2013 2014 2015 2016

Coal Petroleum Gas Primary Electricity and Energy

中国石油集团经济技术研究院| Page 3

China Gas Consumption 2000-2016 China primary energy mix 2000-2016

IEEJ:November 2017 © IEEJ 2017

China gas demand grew rapidly in 2017

China gas consumption has increased by 17% y-o-y for the first 9 months of 2017.

• Economic development:GDP grew by 6.9% y-o-y for Q1&Q2,6.8% for Q3

Gas consuming industries’(Steel, glass, chemical) markets

improved.

• Policy:Coal-to-gas projects surged driven by environmental policies

• Price:Alternative fuels prices increased

• Transmission line maintenance in Yangtze River Delta; less hydropower generation

25

30

60

70

10

15

20

25

30

40

50

60

%bcm

5

0

5

10

0

10

20

30

‐5 0

Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3

2010 2011 2012 2013 2014 2015 2016 2017

中国石油集团经济技术研究院| Page 4

Consumption Growth rate

IEEJ:November 2017 © IEEJ 2017

Domestic gas supply capacity kept growing

During 2000-2015, domestic gas production increased from 27 bcm to 132 bcm, with

average annual growth rate of 11%.g g

In 2016, domestic gas production grew by 1.6% y-o-y. • Total shale gas output raised to 7.9 bcm.

• CBM production was 4.5 bcm.

• Coal-based synthetic gas production was 1.6 bcm.

18.4 19.0 18.7 18 3 20160

7 9

11.5

18.4 18.3

16.0

11.2 9.4

8 1 101214161820

80

100

120

140

160

%m

Domestic gas production and total

gas supply (including coal-based

synthetic gas) grew by 10 9% and 7.9 7.7 7.2 6.2 6.6 6.5

8.1

4.7

1.6

0246810

0

20

40

60

80 %bc

synthetic gas) grew by 10.9% and

10.8% y-o-y for the first 9 months of

2017.00

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

production growth rate

中国石油集团经济技术研究院| Page 5

China gas production 2000~2016

IEEJ:November 2017 © IEEJ 2017

Gas import growth rebounded greatly

Driven by lower import prices and delivery of new contracts, gas imports increased by19.1% y-o-y in 2016, with foreign dependence rate reaching 37%.

PNG imports: 38.4 bcm, grew by 13.3% y-o-y

LNG imports: 26.06 MT(27.3 bcm), grew by 32.6% y-o-y

China gas imports reached 57 6 bcm for the first 9 months of 2017 increased by 21% y-o-yChina gas imports reached 57.6 bcm for the first 9 months of 2017, increased by 21% y o y

PNG 31.5 bcm, grew by 7.7% y-o-y

LNG 33.3 bcm, grew by 35% y-o-y

321.7

250

300

350

60

70

80

Papua New Guinea8.2%

others4.4%

Nigeria1.0%

USA0.8%

126.9

84 7100

150

200

250

20

30

40

50

%bcm

Australia45.9%

Indonesia10 7%

Malaysia9.9%

8 %

14.8

65.6 84.7

35.0 25.0 12.3 3.5 19.1

0

50

0

10

20

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Qatar19.1%

10.7%

中国石油集团经济技术研究院| Page 6China gas import growth rate 2006~2016China LNG import sources in 2016Total Import Volume Growth Rate

IEEJ:November 2017 © IEEJ 2017

Infrastructure construction is moving forward steadily

Pipeline: natural gas trunk pipelines totaled over 70000 km

LNG terminals: 12 in operation, current import capacity 52.8 MTA by 2016.p , p p y y

3 new terminals under construction, + 1 for extension, total capacity will exceed 68 MTA

Tangshan(in 2013,6.5MT/a)Dalian phaseI (in 2011,3MT/a)PhaseII(under contruction,3MT/a)

Nanjiang(in 2013,2.2MT/a)

Nanggang(under construction,3MT/a)

Rudong Phase I(in 2011,3.5MT/a)Phase II(under construction,3MT/a)

Yangshan(in 2009 3MT/a)

Qingdao(in 2014,3MT/a)

Zhoushan(Under construction,3MT/a)

Qidong(in 2017,0.60MT/a)

Putian(in 2008,6.3MT/a)

Yangshan(in 2009,3MT/a)Ningbo phase I(in 2012,3MT/a)Phase II(under construction,3MT/a)

中国石油集团经济技术研究院| Page 7Beihai(in 2016,3MT/a)

Zhuhai(in 2013,3.5MT/a)

Dapeng(in 2006,6.80MT/a);Diefyu(under construction,4MT/a)

Jieyang(in 2017,2MT/a)

Yangpu (in 2014,3MT/a)

IEEJ:November 2017 © IEEJ 2017

Gas market reform accelerated—gas price liberalization

A

Average city-gate prices 2.09(lower

by 16 7%)

gas price liberalizationNegotiable city gate price with fertilizer producers; city-gate

prices liberalization trial in Fujian2016 11Non-residential city-gate prices decreasedby 0.7 RMB/CM; Negotiable non-

2015.11

Average city-gate

prices2.51

by 16.7%) 2016.11

Average city-gateresidential city gate price within price caps since 2016.11 (20% higher than the base prices)

2015.4

2014Average city-gate

g y gprices

Existing:2.47Incremental:2.96

Incremental gas city-gate prices decreased by 0.44 RMB/CM;

Existing gas city-gate ri in r d b

2014g y gprices

Existing:2.09Incremental:2.96 2017.8

The notification of lowering non-residential city gate prices

Existing gas city-gate prices increased by 0 4 RMB/CM

prices increased by 0.04 RMB/CM.

Two prices got in linewith each other.

2013Non-residential city gate prices were lowered by 0.1 RMB/CM since September 1st 2017

non residential city gate prices

2017 9Regulation from wellhead to city gate; 0.4 RMB/CMprice cap for existing gas,

0.4 RMB/CM 2017.9Market-oriented gas pricing

through trading hubs

中国石油集团经济技术研究院| Page 8

g g ,incremental gas prices linked to alternative fuels

IEEJ:November 2017 © IEEJ 2017

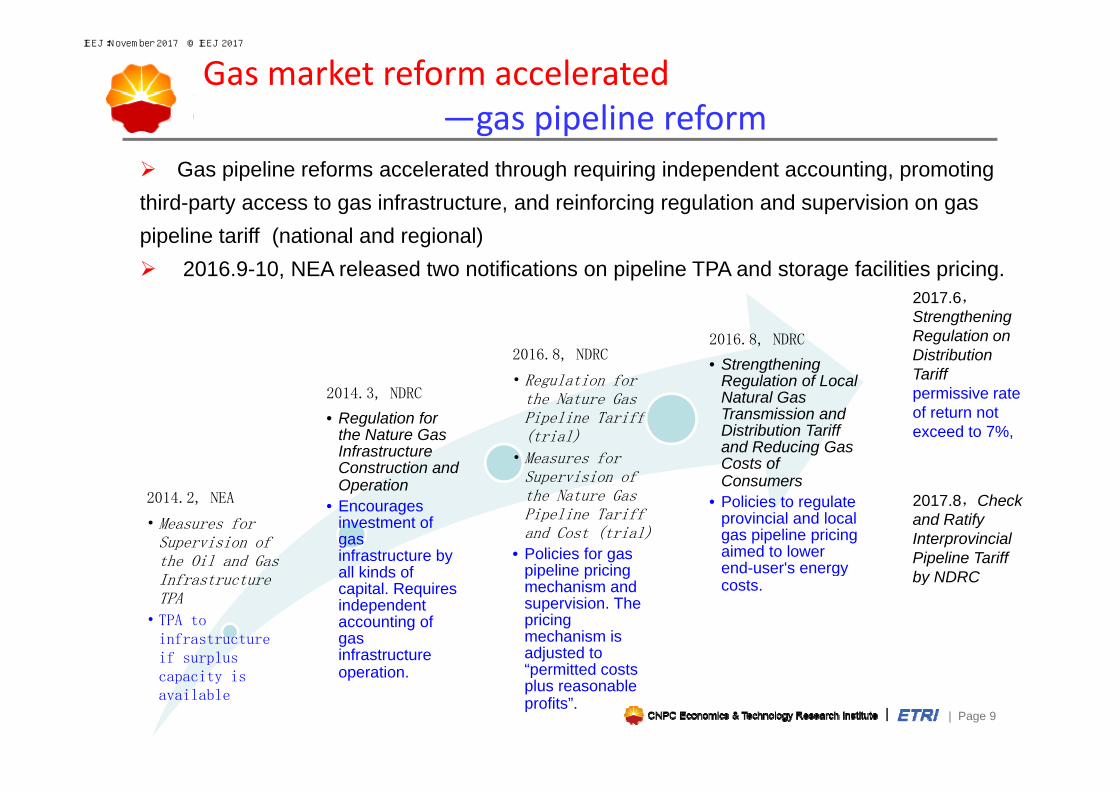

Gas market reform accelerated—gas pipeline reform

Gas pipeline reforms accelerated through requiring independent accounting, promoting third-party access to gas infrastructure, and reinforcing regulation and supervision on gas

gas pipeline reform

pipeline tariff (national and regional) 2016.9-10, NEA released two notifications on pipeline TPA and storage facilities pricing.

2017.6,

2014 3 NDRC

2016.8, NDRC

• Regulation for th N t G

2016.8, NDRC

• Strengthening Regulation of Local Natural Gas

StrengtheningRegulation onDistributionTariffpermissive rate2014.3, NDRC

• Regulation for the Nature Gas Infrastructure Construction and Operation

the Nature Gas Pipeline Tariff (trial)

• Measures for Supervision of

Natural Gas Transmission and Distribution Tariff and Reducing Gas Costs of Consumers

permissive rate of return not exceed to 7%,

2014.2, NEA

• Measures for Supervision of the Oil and Gas I f

Operation• Encourages

investment of gas infrastructure by all kinds of

the Nature Gas Pipeline Tariff and Cost (trial)

• Policies for gas pipeline pricing

Consumers• Policies to regulate

provincial and local gas pipeline pricing aimed to lower end-user's energy

2017.8,Check and Ratify Interprovincial Pipeline Tariff by NDRCInfrastructure

TPA

• TPA to infrastructure if surplus

all kinds of capital. Requires independent accounting of gas infrastructure

pipeline pricing mechanism and supervision. The pricing mechanism is adjusted to “ itt d t

gycosts. by NDRC

中国石油集团经济技术研究院| Page 9

capacity is available

operation. “permitted costs plus reasonable profits”.

IEEJ:November 2017 © IEEJ 2017

Gas market reform accelerated—establishment of gas trading exchange

Shanghai Petroleum and Gas Exchange formally started operation in November 2016

Trading volumes in 2016 reached 30 5 bcm (bilateral) PNG 27 9 bcm LNG 1 75 MT

establishment of gas trading exchange

Trading volumes in 2016 reached 30.5 bcm (bilateral), PNG 27.9 bcm, LNG 1.75 MT

LNG and PNG bidding started in July and September of 2017

More gas trading hubs are emerging in Chongqing, Xinjiang etc.

中国石油集团经济技术研究院| Page 10

IEEJ:November 2017 © IEEJ 2017

Gas market reform accelerated— increasing number of new players

Private companies including Guanghui, ENN etc are participating into LNG business.

Huadian, ENN, Beijing Gas, Guanghui have signed LNG importing contracts; ENN

increasing number of new players

showed interests to take 11.7% stakes of Santos, making it the largest shareholder of

the Australian company; Beijing Gas purchased 20% stakes of Rosneft in VChNG.

LNG importing contracts signed by Chinese buyers 2008-2016

中国石油集团经济技术研究院| Page 11

LNG importing contracts signed by Chinese buyers 2008 2016

IEEJ:November 2017 © IEEJ 2017

Challenges met by China gas market

Responsibility and emergency system for gas peak shaving are called for. As

l h d k ll d bcoal to gas switching drives gas consumption peak-valley difference bigger ,

inadequate gas peak shaving capacity is becoming a prominent problem. China

has 18 underground gas storages by 2016, with working gas 6.1 Bcm, accounting

for 3% of gas consumption.

Price regulation confines gas supply capacity.Foreign countries underground gas storage facilities

6

Country

Numberof

storagesWorkinggas Bcm

Maximumwithdrawal

volumes Bcm/d

Gasconsumptio

n Bcm

% of gas consumptio

n

S 400 133 3 34 759 4 1 63

4

5

6

ubic m

eter

US 400 133.7 3.34 759.4 17.6 Russia 24 69.6 0.74 409.2 17.0

Ukraine 13 32.2 0.29 38.4 83.9 Germany 53 24.6 0.64 70.9 34.7 Canada 61 23.2 0.36 104.2 22.3 0

1

2

g i g i

Yuan/cu

Italy 12 17 0.33 56.8 29.9 France 13 12.2 0.27 35.9 34.0

Netherlands 5 10.2 0.22 32.1 31.8 Austria 9 8.2 0.09 7.8 105.1

Australia 7 6.4 0.02 29.2 21.9Beijing

Shanghai

Nanjing

Xining

Urumch

i

Guangzh

ou

residential industrial fuel CNG for vehicle

中国石油集团经济技术研究院| Page 12

Australia 6.4 21.9

End user gas prices by major city

IEEJ:November 2017 © IEEJ 2017

Outline

I China Natural Gas Market Status

II China Natural Gas Market Outlook

中国石油集团经济技术研究院| Page 13

IEEJ:November 2017 © IEEJ 2017

Policies to promote China’s gas industry

Central government

Plan:Natural Gas 13th Five Year plan Energy 13th Five Year Plan Long TermPlan:Natural Gas 13 Five Year plan, Energy 13 Five Year Plan, Long Term

Oil and Gas Pipeline Network Planning

Price:Notifications on Strengthening Regulation on Distribution Tariff,

Lowering Non-residential City Gate Prices, etc

Environment:Air Pollution Control Action Plan for Beijing-Tianjin-Hebei

Area 2017-2018 etc.

Utilization:Suggestion of Promoting Gas Utilization, etc.

Others: Some Suggestions on Deepening Oil and Gas Industry Reform etcOthers: Some Suggestions on Deepening Oil and Gas Industry Reform, etc.

Local government

Actively carried out planning, policies on prices and utilizations.

中国石油集团经济技术研究院| Page 14

IEEJ:November 2017 © IEEJ 2017

Huge potential market

Strategic Action Plan for Energy Development, Natural Gas 13th Five Year

Plan Energy 13th Five Year Plan Suggestion of Promoting Gas UtilizationPlan, Energy 13 Five Year Plan ,Suggestion of Promoting Gas Utilization

targeted 10% by 2020 and 15% by 2030 for gas share in primary energy

consumption.

It is estimated that gas consumption will be 400 bcm by 2020 and 600 bcm by

2030.15.0 16

10.0 10

12

14

2.2 2.4 4.0

5.9

4

6

8%

2.2

0

2

2000 2005 2010 2015 2020 2030

中国石油集团经济技术研究院| Page 15

Share of gas in primary energy mix – planned goals by 2020 and 2030

IEEJ:November 2017 © IEEJ 2017

Key orientation of China gas demand

The major gas consuming sectors in China are city gas (40%), industrial (30%) , power

generation (15%) and chemical (15%)g ( ) ( )

Suggestion of Promoting Gas Utilization distributed by 13 national departments pointed

out four key utilization areas for gas: cities and towns, power generation, industrial fuels and

transportation.

• Distributive ti

• Residentialt i t generation

• Peak generation• Cogeneration

customers in town and rural areas

• Clean heating innorthern areas.

City and Power generatiC ty a d

towns generation

• Gas-fueled• Coal-to-gas in

Transportation

Industrial fuels

中国石油集团经济技术研究院| Page 1616

Gas-fueledvehicles

• Gas-fueled ships

Coal-to-gas inindustrial sector

IEEJ:November 2017 © IEEJ 2017

Gas supply capacity will increases steadily

It is expected that the supply capacity will be 340 bcm in 2020, with 220 bcm domestic

gas, and 120 bcm imported gas.

Supply capacity will be as much as 590 bcm in 2030, with domestic production of 390 bcm

and 200 bcm imported gas.

600

700 LNG import Pipeline import SNG

Shale gas CBM Conventional gas

20

130

70

400

500

m

16

50

30

80

4

34

65

27

60

200

300 bcm

95 124 170

240 4 4 1 4

34 13

0

100

2010 2015 2020 2030

中国石油集团经济技术研究院| Page 17

2010 2015 2020 2030

IEEJ:November 2017 © IEEJ 2017

Gas supply capacity will increases steadily

Shale gas technically recoverable resources totaled at 21.8 Tcm by 2015,

according to Ministry of Land and Resourcesaccording to Ministry of Land and Resources.

Major exploration and production companies include Sinopec, CNPC, Yanchang

Petroleum Group.

NEA’s Shale Gas Planning (2016-2020) targets shale gas production to reach

30 Bcm by 2020 and 80-100 Bcm by 2030.

Resource base:richresource and industrial

basePolicy:supportive national

Fiscal subsidies:0.4 RMB/CM 2012-2015,0.3 RMB/CM 2016 2018 0 2Policy:supportive national

development strategy and policy, independent mine

type

RMB/CM 2016-2018;0.2 RMB/CM 2019-2020

Lack of developmenttechnology for deep shale gas:exploration depth of

Investment intensive:Shale gas exploration andproduction requires huge

it l i t d l l d

中国石油集团经济技术研究院| Page 18

current technology < 3500meters

capital input and long lead time, thus makes investment risky

IEEJ:November 2017 © IEEJ 2017

Gas supply capacity will increases steadily

CBM has been developed steadily with surface production reaching 4.5 Bcm in 2016;

Surface production will lead future CBM growth as a result of increasing coal Surface production will lead future CBM growth as a result of increasing coal

mines closing down.

CBM production is expected to mount 24 Bcm by 2020, with surface production

reaching 10 Bcm (utilization rate > 90%) and coal mine methane production

reaching 140 Bcm (utilization rate > 50%).

F bl di i20

Favorable condition:

Supportive policy: subsidy standard

raises from 0.2 RMB/CM to 0.3 RMB/CM

d i 13th Fi Pl i d

15 S urface developm ent D ow nhole extraction

during 13th Five-year Plan period.

Restraining factors:

Mine rights, geological conditions, 7.2 7.6

9.2 9.9 12.6

13.3 13.6 12.8

5

10

bcm

technology and equipments, reform

process.

0.0 0.1 0.4 0.8 1.0 1.6 2.3 2.6 3.0 3.7 4.4 4.5 2.3 2.5

4.7 5.8

7.2

0 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

中国石油集团经济技术研究院| Page 19China CBM production 2005-2016

IEEJ:November 2017 © IEEJ 2017

Thank You

CNPC Economics & Technology Research Institute, ETRI

中国石油集团经济技术研究院| Page 20

IEEJ:November 2017 © IEEJ 2017

Contact: [email protected]