Embed Size (px)

Citation preview

2011 SEAISI Singapore Conference &

May 23, 2011

Chief Executive Officer, POSCO

Joon-Yang Chung

POSCO’s Regional Strategies

toward Southeast Asian Steel Industries

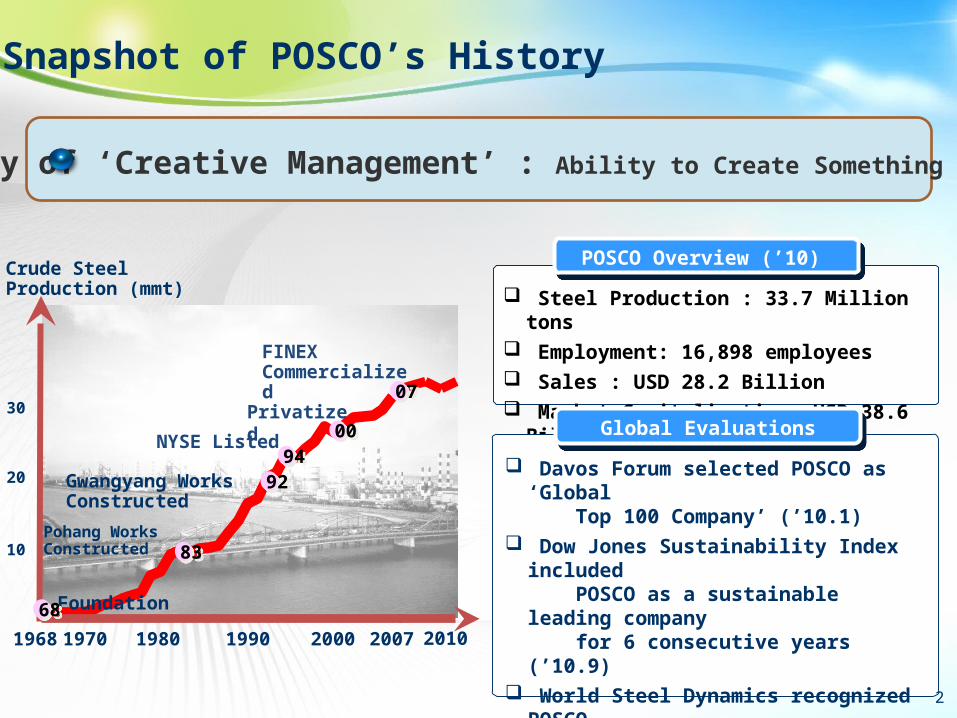

History of ‘Creative Management’ : Ability to Create Something from Scratch

POSCO Overview (’10) POSCO Overview (’10)

Steel Production : 33.7 Million tons Employment: 16,898 employees Sales : USD 28.2 Billion Market Capitalization: USD 38.6 Billion (‘11.5)

Global EvaluationsGlobal Evaluations

Davos Forum selected POSCO as ‘Global Top 100 Company’ (’10.1)

Dow Jones Sustainability Index included POSCO as a sustainable leading company for 6 consecutive years (’10.9)

World Steel Dynamics recognized POSCO for the world’s best competitiveness (WSD, ‘10)

Fortune Magazine's “most admired company” (metal category, ’11.3)

1980 1990 2007200019701968

30

20

10

Foundation

Pohang WorksConstructed

Privatized

NYSE Listed

Gwangyang WorksConstructed

FINEX Commercialized

8383

92929494

0000

0707

6868

2010

Crude Steel Production (mmt)

Snapshot of POSCO’s History

1 2

Key Issues for Global Steel IndustryⅠⅠ

Potential of South-east Asian Steel IndustryⅡⅡ

POSCO in South-east AsiaⅢⅢ

Concluding RemarksⅣⅣ

3

① Challenges and Opportunities on Environment

Emerging new paradigm of “Low Carbon and Green Growth”

Climate Change / Green Growth were key issues of Seoul G20 Business Summit, 2010

Low Carbon and

Green Growth

Low Carbon and

Green Growth

Post-Ky-

oto

National Act for Green GrowthGreen

Business

Demand for De-creasing energy usage

CO 2 R

e-

duction

Environment: the biggest challenge and core of competitiveness for steel industry

Regulations: Post-Kyoto Regime, National Act for Green Growth, etc.

• EU adapted its Emission Trading Scheme in 2005 Challenges: Demand for Decreasing Energy Usage and for CO2 Reduction

• The steel industry accounts for 4~5% of total global CO2 gas emissions – IEA

4

POSCO, for Global Green Growth Leader

Invest 700 million USD by 2015to improve energy efficiencyvia by-product gas combined cycle power plant, etc.

Invest 700 million USD by 2015to improve energy efficiencyvia by-product gas combined cycle power plant, etc.

Improvement ofEnergy EfficiencyImprovement of

Energy Efficiency

Development of New CO2 reduction

Steel Process

Development of New CO2 reduction

Steel Process

Development ofHydrogen

Steelmaking

Development ofHydrogen

Steelmaking

H2

Very-high-temperature Reactor (VHTR)

FOG, SNG

-Improve energy efficiency of current processes by heat recovery and re-use

Coke Dry Quenching

-Develop innovative steelmaking processes to save energy

• POSBOP (POSCO Basic Oxygen Process)

- Innovative steelmaking process with lower energy intensity

• CEM -Energy saving of reheating step by connecting two separate processes

-Hydrogen replaces coal as a reducing material

-Dramatic reduction of CO2 emission

Enforcing Steel Competitiveness through Improvement of Energy Efficiency and Breakthrough Technology

5

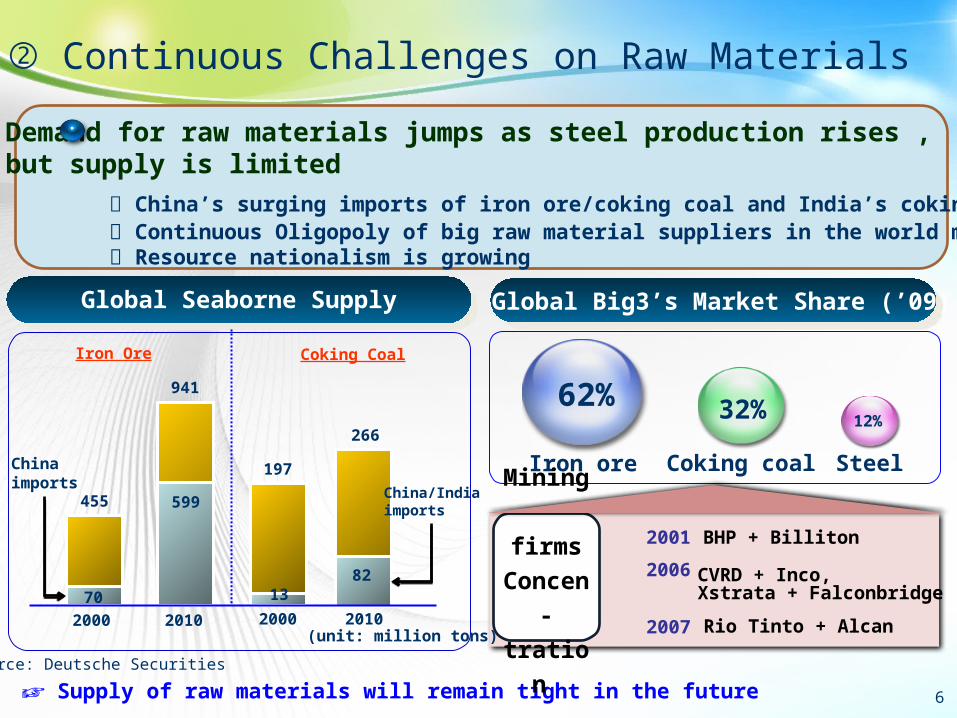

② Continuous Challenges on Raw Materials

Demand for raw materials jumps as steel production rises , but supply is limited

China’s surging imports of iron ore/coking coal and India’s coking coal

☞ Supply of raw materials will remain tight in the future

Continuous Oligopoly of big raw material suppliers in the world market

Global Big3’s Market Share (’09)

Iron ore Coking coal Steel

BHP + Billiton

CVRD + Inco,Xstrata + Falconbridge

Rio Tinto + Alcan

2001

2006

2007

Mining

firms

Concen-

tration

62% 32% 12%

Global Seaborne Supply

20002000 2010

455

941

599

70

Chinaimports

197

266

2010

8213

China/Indiaimports

Iron Ore Coking Coal

Source: Deutsche Securities

(unit: million tons)

Resource nationalism is growing

6

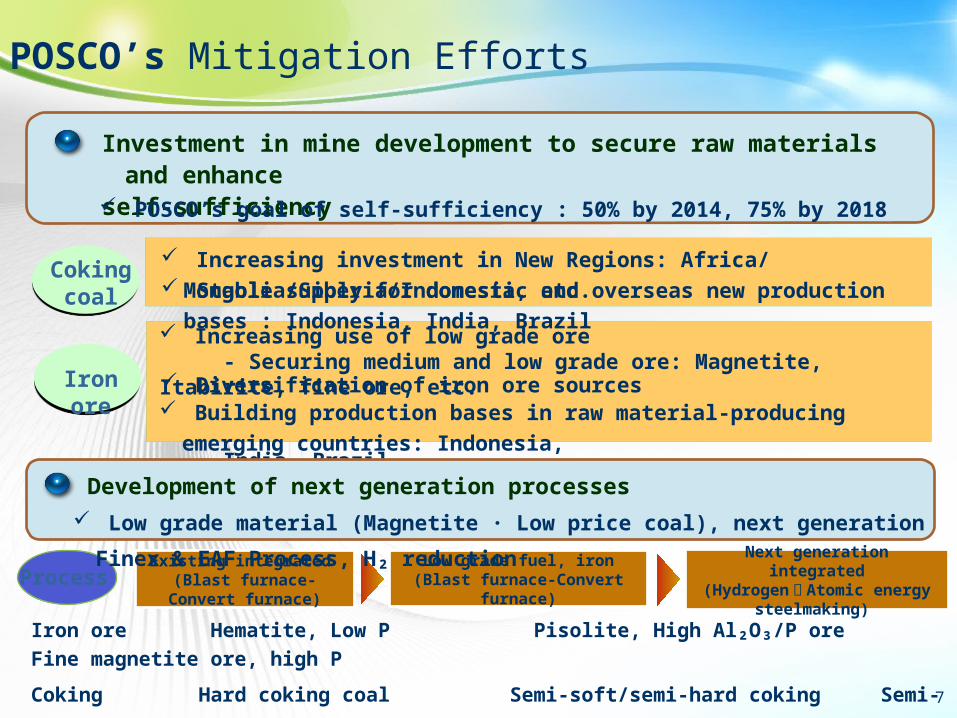

POSCO’s Mitigation Efforts

Investment in mine development to secure raw materials and enhance self-sufficiency

Increasing use of low grade ore - Securing medium and low grade ore: Magnetite, Itabirite, fine ore, etc.

Iron ore

Increasing investment in New Regions: Africa/Mongolia/Siberia/Indonesia, etc.Coking coal

POSCO’s goal of self-sufficiency : 50% by 2014, 75% by 2018

Stable supply for domestic and overseas new production bases : Indonesia, India, Brazil

Diversification of iron ore sources Building production bases in raw material-producing emerging countries: Indonesia, India, Brazil

Development of next generation processes

Iron ore Hematite, Low P Pisolite, High Al₂O₃/P ore Fine magnetite ore, high P

Coking Hard coking coal Semi-soft/semi-hard coking Semi-soft/semi-

hard coking coal (Low Ash/S/P) coal (high Ash/S/P) coal, Ultra-low price coal

ProcessExisting integrated (Blast furnace-Con-

vert furnace)

Low grade fuel, iron(Blast furnace-Convert

furnace)

Next generation inte-grated

(Hydrogen ㆍ Atomic en-ergy steelmaking)

Low grade material (Magnetite · Low price coal), next generation Finex & EAF Process, H₂ reduction

7

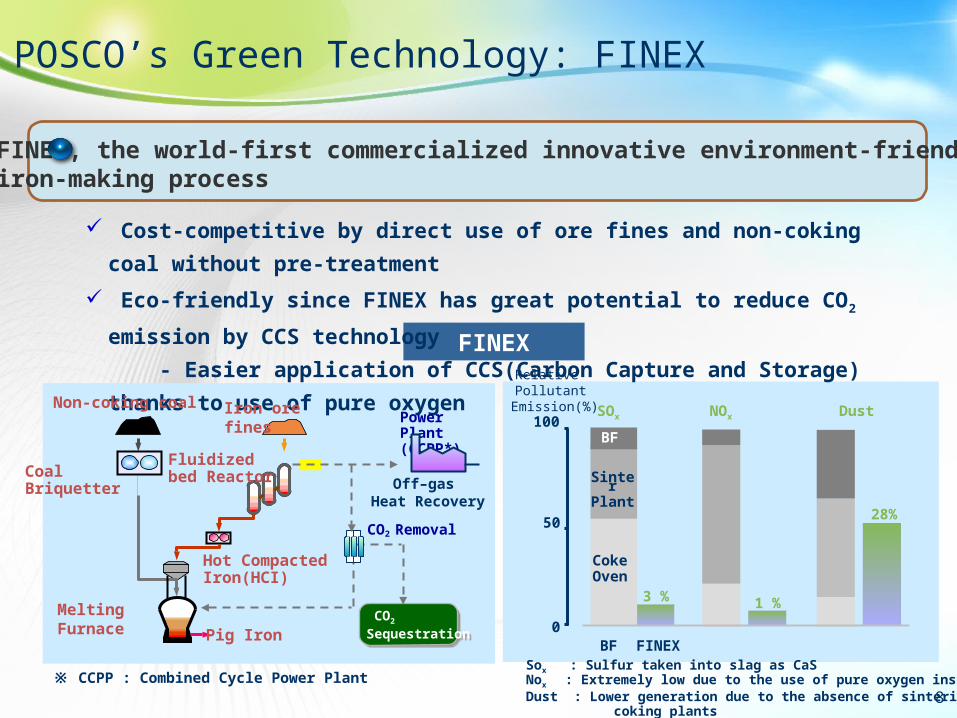

POSCO’s Green Technology: FINEX

FINEX

FINEX, the world-first commercialized innovative environment-friendlyiron-making process

Cost-competitive by direct use of ore fines and non-coking coal without pre-treatment

Eco-friendly since FINEX has great potential to reduce CO2 emission by CCS technology

- Easier application of CCS(Carbon Capture and Storage) thanks to use of pure oxygen

Iron ore finesNon-coking coal

CoalBriquetter

Fluidized bed Reactor

Hot Compacted Iron(HCI)

Pig Iron

MeltingFurnace

Power Plant(CCPP*)

CO2 Removal

CO2

Sequestration

CO2

Sequestration

Off–gas Heat Recovery

※ CCPP : Combined Cycle Power Plant

BF FINEX

NOx Dust

0

50

100

CokeOven

SinterPlant

BF

3 % 1 %

28%

SOx

Relative Pollutant

Emission(%)

Sox : Sulfur taken into slag as CaSNox : Extremely low due to the use of pure oxygen instead of airDust : Lower generation due to the absence of sintering and coking plants

8

Key Issues for Global Steel IndustryⅠⅠ

Potential of South-east Asian Steel IndustryⅡⅡ

POSCO in South-east AsiaⅢⅢ

Concluding RemarksⅣⅣ

9

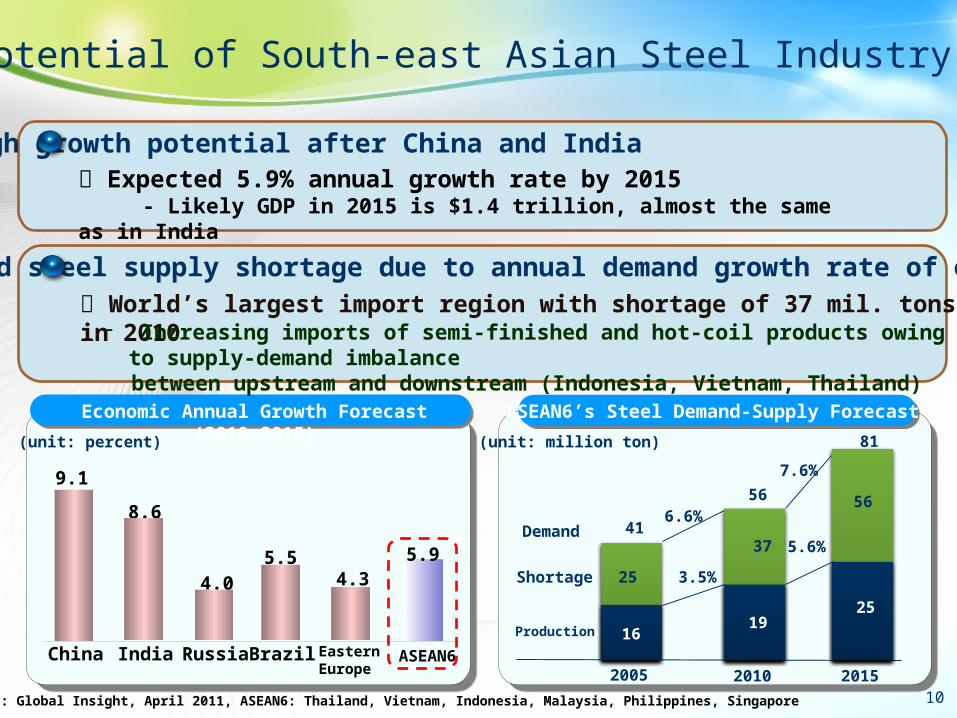

Potential of South-east Asian Steel Industry

Expected steel supply shortage due to annual demand growth rate of over 7.6% World’s largest import region with shortage of 37 mil. tons in 2010

Source: Global Insight, April 2011, ASEAN6: Thailand, Vietnam, Indonesia, Malaysia, Philippines, Singapore

China India Russia Brazil EasternEurope

ASEAN6

9.1

8.6

4.05.5

4.35.9

Economic Annual Growth Forecast (2010~2015)

High growth potential after China and India Expected 5.9% annual growth rate by 2015 - Likely GDP in 2015 is $1.4 trillion, almost the same as in India

- Increasing imports of semi-finished and hot-coil products owing to supply-demand imbalance between upstream and downstream (Indonesia, Vietnam, Thailand)

ASEAN6’s Steel Demand-Supply Forecast

56

2010

19

37

81

2015

25

56

Production

Shortage

Demand

16

41

2005

25

6.6%

7.6%

3.5%

5.6%

(unit: million ton)(unit: percent)

10

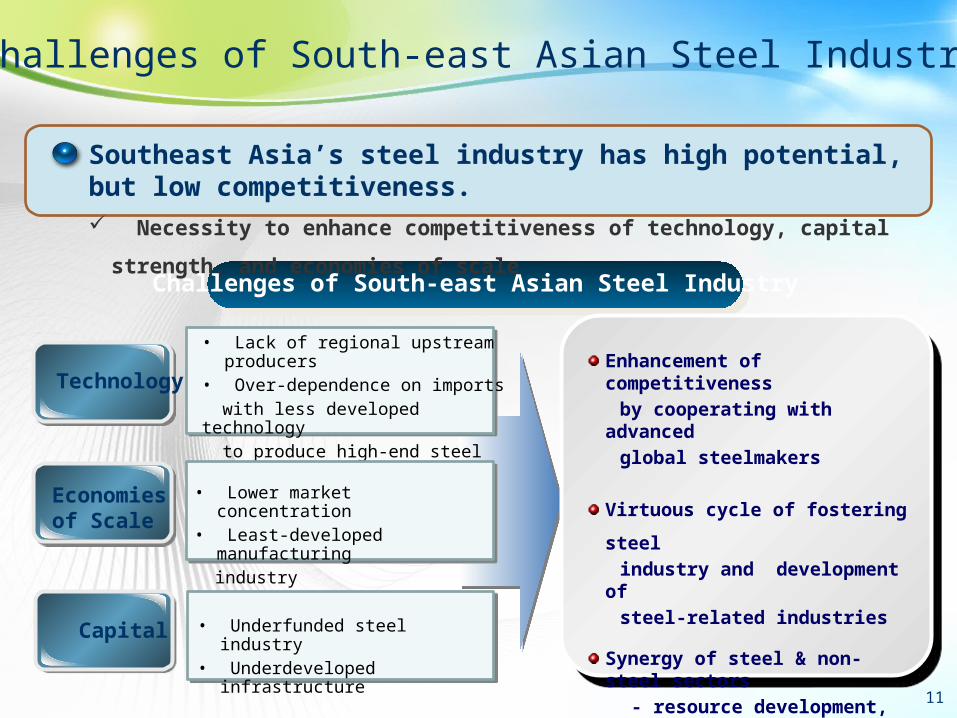

Southeast Asia’s steel industry has high potential, but low competitiveness. Necessity to enhance competitiveness of technology, capital strength, and economies of scale

Challenges of South-east Asian Steel Industry

TechnologyEnhancement of competitiveness

by cooperating with advanced

global steelmakers

Virtuous cycle of fostering

steel industry and development

of steel-related industries

Synergy of steel & non-steel sectors

- resource development, infrastructure expansion

• Lack of regional upstream producers• Over-dependence on imports with less developed technology to produce high-end steel

Capital • Underfunded steel industry• Underdeveloped infrastruc-

ture

Economiesof Scale

• Lower market concentration• Least-developed manufacturing industry

Challenges of South-east Asian Steel Industry

11

Key Issues for Global Steel IndustryⅠⅠ

Potential of South-east Asian Steel IndustryⅡⅡ

POSCO in South-east AsiaⅢⅢ

Concluding RemarksⅣⅣ

12

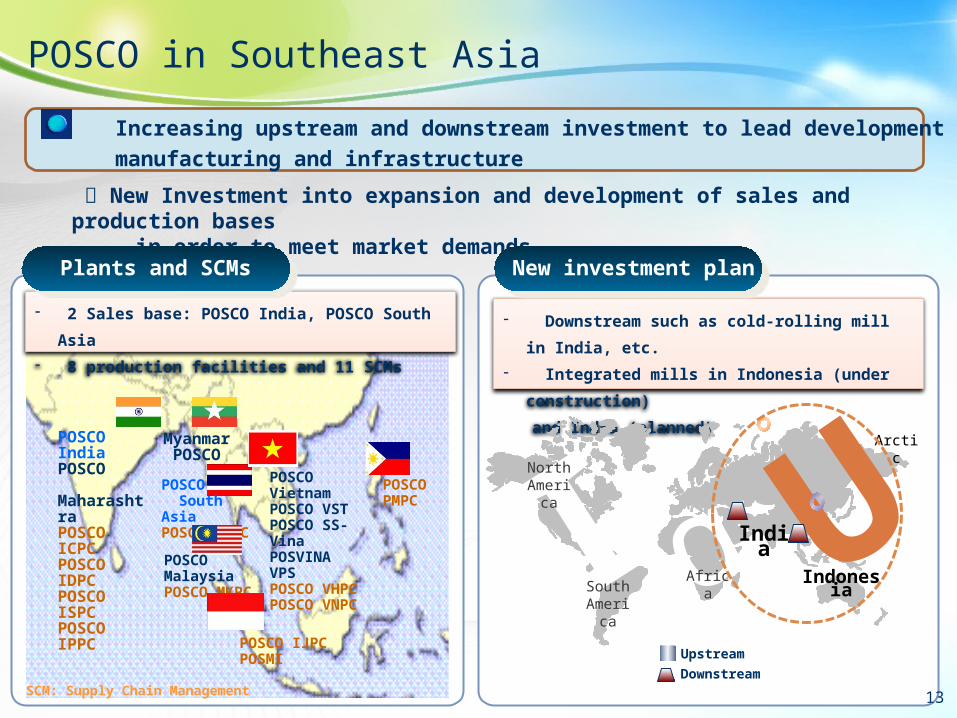

Increasing upstream and downstream investment to lead development of

manufacturing and infrastructure

New Investment into expansion and development of sales and production bases in order to meet market demands

POSCO IndiaPOSCO MaharashtraPOSCO ICPCPOSCO IDPCPOSCO ISPCPOSCO IPPC

Myanmar POSCO

POSCO South AsiaPOSCO TBPC

POSCO VietnamPOSCO VSTPOSCO SS-VinaPOSVINAVPSPOSCO VHPCPOSCO VNPC

POSCO PMPC

POSCO MalaysiaPOSCO MKPC

POSCO IJPCPOSMI

- 2 Sales base: POSCO India, POSCO South

Asia

- 8 production facilities and 11 SCMs

SCM: Supply Chain Management

POSCO in Southeast Asia

- Downstream such as cold-rolling mill in India,

etc.

- Integrated mills in Indonesia (under construction)

and India (planned)

Arctic

UIndia

IndonesiaINorth

America

South America

αAfrica

Upstream

Downstream

Plants and SCMs New investment plan

13

Win-Win strategy with local steelmakers and contribution to domestic

economic growth

- Location : Cilegon in Banten

- Partner : Krakautau (PT.KS)

- Share : POSCO 70%, PT.KS 30%

- Capacity in Phase 1 : Slab 1.5 mil. tons,

Steel plate 1.5 mil.

tons

- Construction Period : 2010-2013

PT.KS-POSCO JVC

Integrated Mill JVC in Indonesia

Contribution to boost competitiveness of steel and related industries

Contribution to boost competitiveness of steel and related industries

Stable supply of slabs to KS

Building development base for related industries and increasing productivity

Economic Ripple Effects Economic Ripple Effects

Win-Win Strategy

PT.KS-POSCO JVC in Indonesia

production inducement worth 600 trillion Rp Creation of 1.5 mil of new jobs

14

Key Issues for Global Steel IndustryⅠⅠ

Potential of South-east Asian Steel IndustryⅡⅡ

POSCO in South-east AsiaⅢⅢ

Concluding RemarksⅣⅣ

15

POSCO expects rapid growth in SEA’s economic growth potential

Concluding Remarks

SEA’s growing economy will need quantitative and qualitative

advancement of steel as demand is expected to rapidly increase.

POSCO is setting up SEA “production bases” with local partners,

utilizing world-class Operational Expertise and Green Technology to

satisfy local steel demands

POSCO’s SEA strategy is to ultimately contribute to the economic

development of South-east Asia as a whole, through investment in

regional steel production.

Collaboration between POSCO and SEA regional steel producers creates

many opportunities for cooperation and high synergy, with ideal

combination of technology, capital, markets and labor.

16