Embed Size (px)

Citation preview

2017 ANNUAL FINANCIAL RESULTS13 FEBRUARY 2018

1

Certain statements made in this presentation constitute forward-looking statements. Forward-looking

statements are typically identified by the use of forward-looking terminology such as ‘believes’, ‘expects’,

‘may’, ‘will’, ‘could’, ‘should’, ‘intends’, ‘estimates’, ‘plans’, ‘assumes’ or ‘anticipates’ or the negative thereof or

other variations thereon or comparable terminology, or by discussions of, e.g. future plans, present or future

events, or strategy that involve risks and uncertainties. Such forward-looking statements are subject to a

number of risks and uncertainties, many of which are beyond the company's control and all of which are

based on the company's current beliefs and expectations about future events. Such statements are based

on current expectations and, by their nature, are subject to a number of risks and uncertainties that could

cause actual results and performance to differ materially from any expected future results or performance,

expressed or implied, by the forward-looking statement. No assurance can be given that such future results

will be achieved; actual events or results may differ materially as a result of risks and uncertainties facing the

company and its subsidiaries. The forward-looking statements contained in this presentation speak only as

of the date of this presentation and the company undertakes no duty to, and will not necessarily, update any

of them in light of new information or future events, except to the extent required by applicable law or

regulation.

DISCLAIMER

2

IMPRESSIVE PERFORMANCE ACROSS THE BOARD

Safety:

fatality free and

improvement across

all metrics

Operations:

increased productivity

and efficiency

Financials:

benefit from

performance and price

Capital allocation:

strong

balance sheet

Strategy:

transformation to

full potential

Outlook:

delivering

stakeholder value

3

TRCFR improvement from 0.78

0.65

Total recordable cases

20%

Lost time injuries

0.17LTIFR improvement from 0.28

43%

High potential incidents

FATALITY FREE

Fatalities

0

46%

FY17FY16

4

EBITDA

R19.6bn

6%

Production

45Mt

8%

SOLID OPERATING AND FINANCIAL PERFORMANCE

FY17FY16

HEPS

R30.47

12%

Attributable free

cash flow

R12.3bn

10%

5

EBITDA IMPROVEMENT DUE TO EFFICIENCY AND PRODUCTIVITY GAINS

18 410 18 275

19 5584 985 (4 063)

(1 073)(272) 288

2 133(850)

FY16 Price Currency Inflation Royalties Shipping Total afternon-controllables

Volume Opex FY17

Operational performance

(135) 1 283

Rm

(1%) 7%

6

Communities

R107mdirect social

investment

SIGNIFICANT VALUE SHARED

Suppliers

R520mhost community

suppliers

R9.4bnprocurement from

HDSA businesses

Government

R5.9bnincome tax

R1.2bnroyalties

Employees

R4.2bnsalaries and

benefits

Shareholders

R10bnowners of Kumba

R3.1bnempowerment

partners

MARKET OVERVIEW

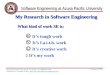

8

0

200

400

600

800

1000

1200

1400

1600

1800

2011 2012 2013 2014 2015 2016 2017

Global seaborne iron ore supply2 (Wmt)

Rio Vale BHP FMG RoW

CAGR

0

50

100

150

200

400

600

800

1000

2011 2012 2013 2014 2015 2016 2017N

et e

xp

ort

s

Ste

el p

rod

uction

China crude steel production & net exports1 (Mt)

Steel production Net exports

1. Crude steel equivalent, 2. Vale, 9M17 annualised.Source: World Steel Association, GTIS

HIGHER STEEL PRODUCTIONBUT SLOWER IRON ORE SUPPLY EXPANSION

7.8% 3.6%

9

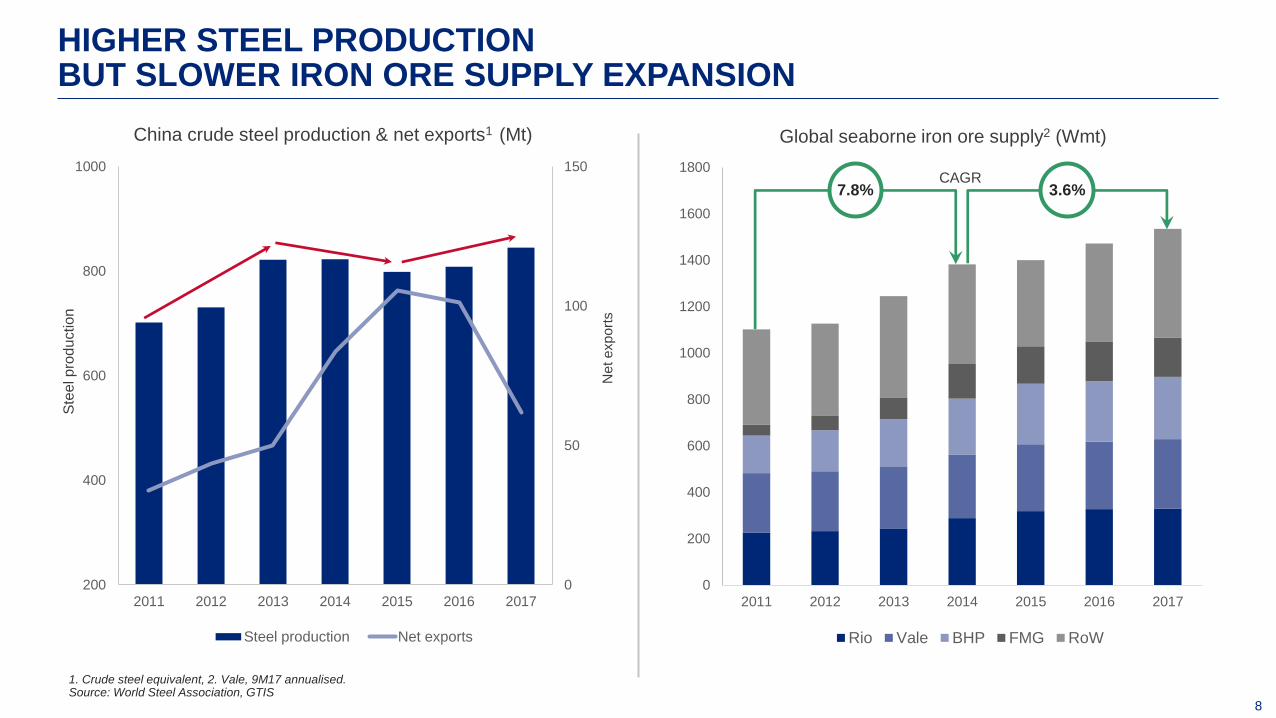

STEEL AND IRON ORE PRICES DIVERGED

30

50

70

90

110

130

150

200

250

300

350

400

450

500

550

600

650

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

Iro

n o

re p

rice

($

/dm

t C

FR

Qin

gd

ao

)

Bill

et p

rice

($

/t)

Steel and iron oreprices in China

China billet ($/t) Platts 62 index ($/t)

Source: Platts

Platts

IODEX

average ($/t)97 56 58 71 76

9%

10%

11%

12%

13%

14%

15%

16%

17%

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

Lu

mp

% o

f to

tal p

ort

sto

cks (

%)

Pla

tts lu

mp

pre

miu

m (

$/d

mtu

)

Relationship between Platts lump premium and port stocks in China

Platts lump premium ($/dmtu) Lump % of total stocks

Platts lump

premium

average

($/dmtu)

0.17 0.14 0.15 0.15 0.12

10

(20)

(15)

(10)

(5)

-

5

10

15

20

25

30

Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17 Jul-17 Dec-17

$/t

Platts index premium and discount ($/dmt)

Platts 65/Platts 62 premium Platts 58 (low Al)/Platts 62 discount

0

5

10

15

20

25

30

150

200

250

300

350

400

450

500

550

600

650

Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17 Jul-17 Dec-17

P6

5/P

62

diffe

ren

tial (

$/t)

Bill

et p

rice

($

/t)

China steel price and high grade premiums

China billet ($/t) Platts 65/Platts 62 differential ($/t)

Source: Platts

RECORD MILL PROFITABILITY BUOYING DEMAND FOR PREMIUM ORES

11

71

(12)

59

3

7

2

71

Platts 62 indexCFR China

Saldanha -Qingdao freight

Platts 62 indexFOB Saldanha

Fe premium Lump premium Marketingpremium

AchievedFOB 2017 price

$/dmt

REALISED FOB PRICE AT US$71/t

Source: Kumba Marketing

2%

China

63%

Japan &

Korea

17%

EU/MENA

18%

Export sales geographical split

India &

other Asia

13.9

15.2

2016 2017

Ex-China sales (Mt)

12

5

2925

2

66

Peer 1 Peer 2 Peer 3 Peer 4 Kumba

2017 Lump:Fine (%), Peer comparison

Source: Market Intelligence, Company Reports, Woodmac

63.9

60.8 60.7

57.7

64.1

Peer 1 Peer 2 Peer 3 Peer 4 Kumba

2017 average Fe content (%), Peer comparison

71

58 (est)

65

64

41

Kumba

Peer 1

Peer 2

Peer 3

Peer 4

2017 achieved price ($/dmt, FOB), Peer comparison

KUMBA’S COMPETITIVE ADVANTAGE

OPERATIONAL OVERVIEW

14

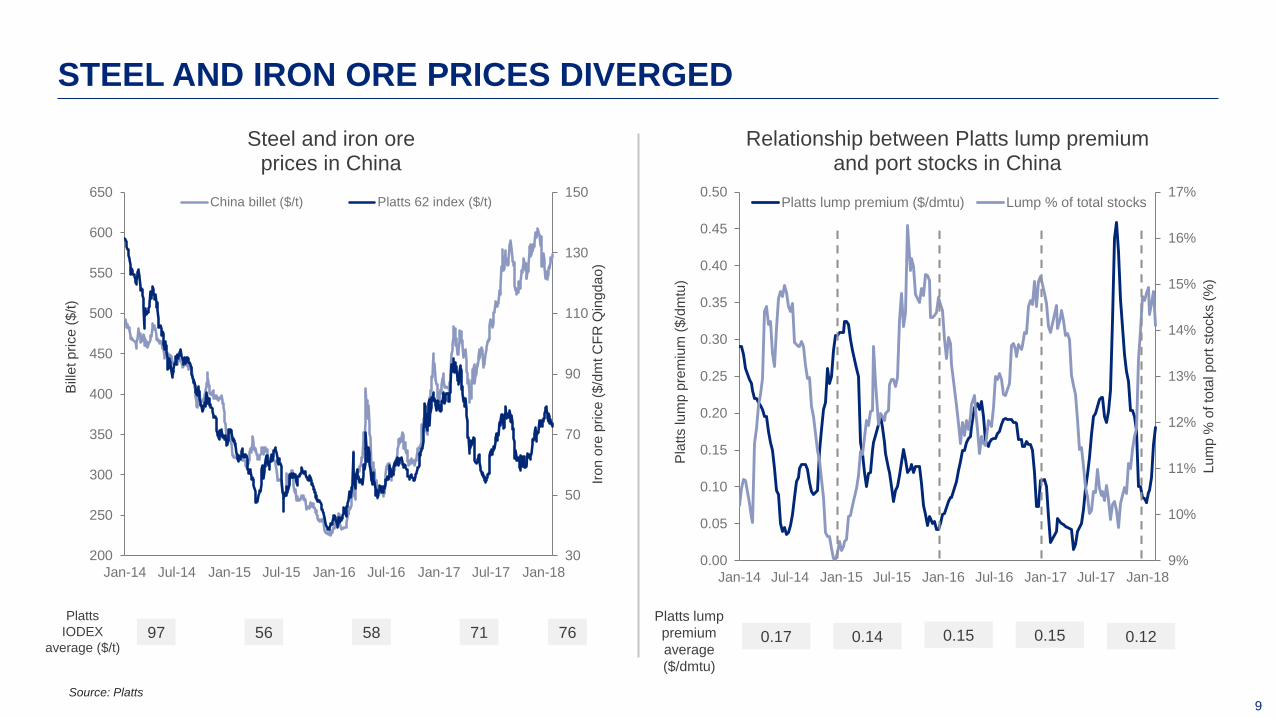

SISHEN PERFORMANCE UNDERPINNED BY IMPROVED PRODUCTIVITY

61% reduction in high potential

incidents

Waste up 18% to 162Mt driven by

efficiencies

Production up 10% to 31.1Mt from

higher plant throughput and yields28.4

31.1

FY16 FY17

Sishen production (Mt)

137

162

FY16 FY17

Sishen waste (Mt)

10%18%

Strip

ratio3.3 4.3

15

OPERATING MODEL – STRUCTURED APPROACH FOR IMPROVEMENT

Highlights

62% productivity improvement on Sishen fleet

31% increase in direct operating hours

4100 shovels tempo up 63% from 1H16

Effective planning and scheduling

80% improvement in sequencing of activities

Each task planned and scheduled in detail

Use data to improve scheduling and execution capability

(schedule effectiveness)

Work management - controlled execution

Monitor schedule completion per task

Measuring scheduled work vs unscheduled work

Sishen fleet productivity (kt/day)

379 474 529

613

1H16 2H16 1H17 2H17

3.0 3.5 4.04.9

1H16 2H16 1H17 2H17

Sishen pre-strip shovel tempo (kt/h)

62%

63%

16

KOLOMELA CONTINUES STRONG PERFORMANCE

154 days of zero harm

Waste increased 11% to 55.6Mt

Production up 9% to 13.9Mt

Improved performance due to plant

and equipment efficiencies 12.7

13.9

FY16 FY17

Kolomela production (Mt)

50.2

55.6

FY16 FY17

Kolomela waste (Mt)

9%11%

Strip

ratio3.7 3.4

17

36.7 40.5 38.145.3

1H16 2H16 1H17 2H17

14.015.7 15.9 16.5

1H16 2H16 1H17 2H17

1. Truck direct operating hours (DOH): Time equipment is operational, performing production and non-production activities

Significant improvement from 1H16 to 2H17

23% increase in DSO plant production

− Improved DOH and tempo

− Improved reliability

18% increase in truck DOH

Strategy in place to achieve further improvements

OPERATIONAL EFFICIENCIES FROM OPERATING MODEL

18%

Kolomela DSO product (kt/day)

Truck DOH1 performance (hours/day)

Operating Model “go-live” APC roll-out

23%

18

LOGISTICS PERFORMANCE REFLECTS HIGHER PRODUCTION

39.8

42.0

FY16 FY17

Railed to port (Mt)

38.7

41.6

FY16 FY17

Total shipped (Mt)

42.5

44.9

FY16 FY17

Total sales (Mt)

6% 7% 6%

FINANCIAL OVERVIEW

20

Revenue increased 14% to R46bn

EBITDA of R19.6bn up 6%

Headline earnings of R9.7bn up 12%

Capex of R3.1bn supports production

Attributable free cash flow of R12.3bn up 10%

2017 dividend of R30.97 per share

− Final: R15.00 per share

− Interim: R15.97 per share

FINANCIAL PERFORMANCE HIGHLIGHTS

11.82

27.3030.47

FY15 FY16 FY17

HEPS (R/share)

11.9

18.4 19.6

FY15 FY16 FY17

EBITDA (Rbn)1

1. Excluding impairment reversal/charges

65%

158%

21

REVENUE GROWTH FROM STRONGER PRICES AND HIGHER VOLUMES

Revenue increased by 14%

Realised average FOB export price rose 11% to $71/t (FY16: $64/t)

9% stronger average R/$ exchange rate of R13.30 (FY16: R14.69)

Total sales up 6% to 44.9Mt: export sales up 2.5Mt, domestic sales down 0.1Mt

38 020

41 975

2 747

4 404 5 930 2 133 1 657

(4 108)

FY16 Price Currency Volume Shipping FY17

Rm

Mining operations Shipping

46 379

40 767

22

16 3

30 (28)

(30)

296 287

FY16 Inflation Costescalation

Miningvolume

Productionvolume

Deferred stripping FY17

R/t

Unit cash cost

6% (9%)

1

SISHEN: IMPROVED UNIT COST THROUGH OPERATING EFFICIENCIES

CPI of 5.3%

Cost escalation due to higher diesel price

Mining cost driven by increased volumes

Higher capitalisation of deferred stripping cost driven by increased strip ratio

1. Excluding impact of deferred stripping on unit cost FY17: R30/t (FY16: R3/t)

23

11 5

43 (21)

(2)

201

237

FY16 Inflation Costescalation

Miningvolume

Productionvolume

Deferred stripping FY17

R/t

Unit cash cost

8% 9%

1

KOLOMELA: UNIT COST DRIVEN BY PLANT FEEDSTOCK

CPI of 5.3%

Cost escalation due to higher fuel prices

Increased mining cost due to higher volumes and modular plant feedstock

1. Excluding impact of deferred stripping on unit cost FY17: R18/t (FY16: R18/t)

24

29

40

1 15

4

FY16 Controllable costs Price impact Freight Currency FY17

Non-controllable costs up $10/t

− Freight rates up $5/t

− Stronger currency adding $4/t

− Lower market premium of $1/t

BREAKEVEN - CONTROLLABLE COSTS CONTAINED

Breakeven price up $11/t from FY16 average

Controllable costs up $1/t driven by:

− higher mining volumes, increased deferred

stripping and cost escalation

− offset by improved efficiencies, overhead savings

and higher production

Platts 62% Breakeven Price ($/t)

$1 $10

Controllables Non-controllables

25

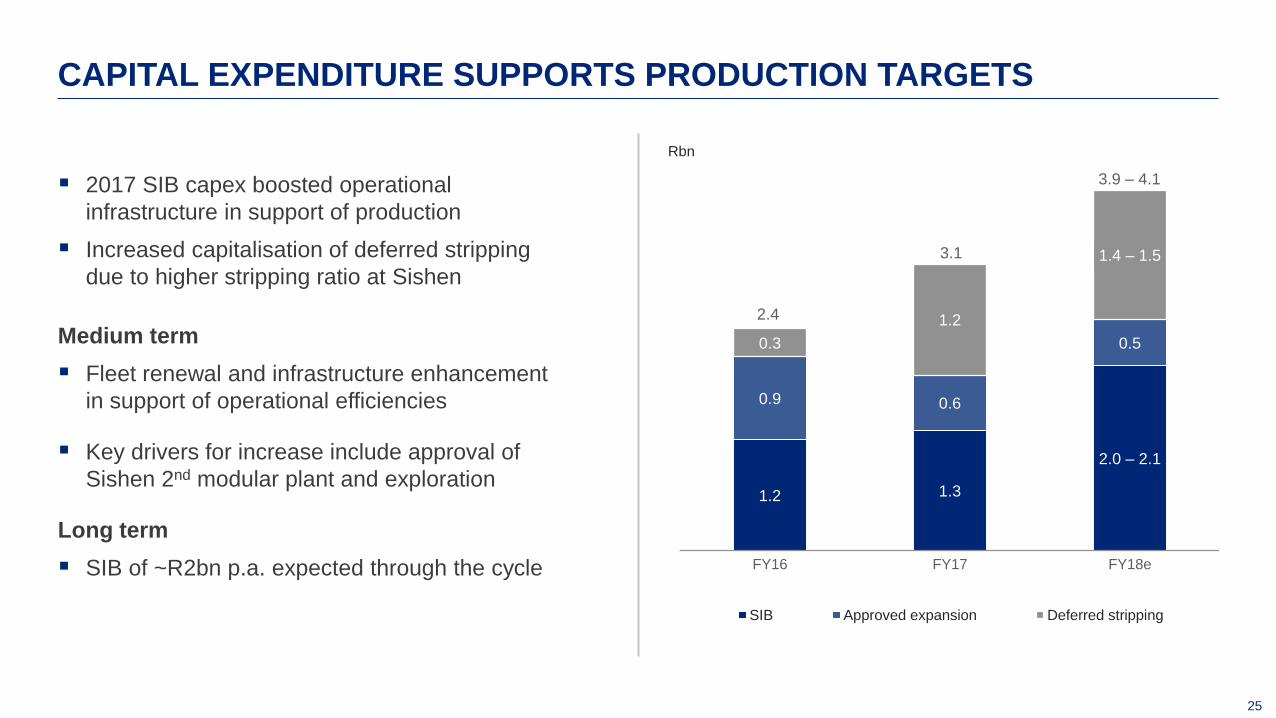

1.2 1.3

2.0 – 2.1

0.9 0.6

0.50.3

1.2

1.4 – 1.5

FY16 FY17 FY18e

Rbn

SIB Approved expansion Deferred stripping

2017 SIB capex boosted operational

infrastructure in support of production

Increased capitalisation of deferred stripping

due to higher stripping ratio at Sishen

Medium term

Fleet renewal and infrastructure enhancement

in support of operational efficiencies

Key drivers for increase include approval of

Sishen 2nd modular plant and exploration

Long term

SIB of ~R2bn p.a. expected through the cycle

CAPITAL EXPENDITURE SUPPORTS PRODUCTION TARGETS

3.9 – 4.1

2.4

3.1

26

13 874

7 5426 165

22 432

461

(5 883)

(3 074) 516

(5 114)

(4 831)

(1 559)

(1 502)

2016 Cash generatedfrom operations

Net financeincome

Tax paid Capex Other Interim2017 dividend

(incl. minorities)

2017 Final 2017dividend

(incl. minorities)

Pro-formacash retained

Rm

Kumba shareholders Minorities

(6 743)

(6 333)

Strong cash generation of R22.4bn

Cash balance of R13.9bn at 31 Dec 2017

STRONG, FLEXIBLE BALANCE SHEET

Final dividend R15.00 per share

Returning R13.1bn to shareholders

125%

27

ENHANCING RETURNS FOR ALL STAKEHOLDERS

Additional margin

extraction from entire

value chain

Free cash flow

generation after

sustaining capex

Disciplined capital

allocation to sustain

and grow core assets

Return of excess

capital unless value

accretive investment

opportunities identified

Strict cost stewardship

across the business

STRATEGY

29

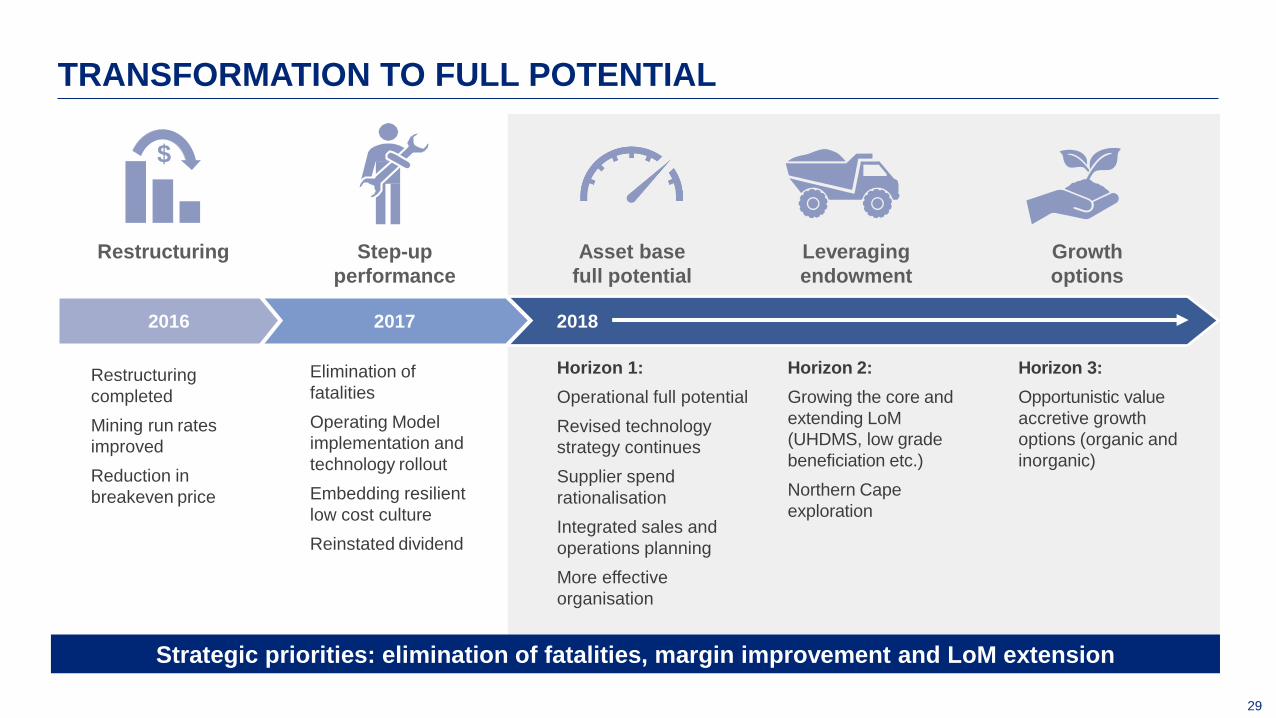

TRANSFORMATION TO FULL POTENTIAL

Step-up

performance

Asset base

full potential

Leveraging

endowment

Horizon 1:

Operational full potential

Revised technology

strategy continues

Supplier spend

rationalisation

Integrated sales and

operations planning

More effective

organisation

Restructuring

completed

Mining run rates

improved

Reduction in

breakeven price

Elimination of

fatalities

Operating Model

implementation and

technology rollout

Embedding resilient

low cost culture

Reinstated dividend

Horizon 2:

Growing the core and

extending LoM

(UHDMS, low grade

beneficiation etc.)

Northern Cape

exploration

Horizon 3:

Opportunistic value

accretive growth

options (organic and

inorganic)

Restructuring

2018

$

20172016

Strategic priorities: elimination of fatalities, margin improvement and LoM extension

Growth

options

30

HORIZON 1: OPTIMISING OUR ASSETS

OEEs1 still below best

practices (e.g. 40-60%

gap on shovels tempos)

Focusing on specific

efficiency drivers

Total expenditure ~R28bn

(over 1 500 suppliers and

service providers to be

consolidated)

Recent step change in the

predictability of production

Leaner organisation post 2016

restructurings

Improvements in safety

Continued focus on loading

and hauling practices and

tempos

Processing throughput and

quality (Fe content and

lump:fine ratio)

Supplier consolidation and

terms negotiations

Closer partnerships with

strategic suppliers

Demand controls and

development of tools to

analyse and reduce further

consumption

Specifications review with

TCO2 approach

Continued efforts to improve

operations and ensure

consistent product quality

Greater integration of sales

and operations planning to

respond to market dynamics

Curr

ent

situation

2018 p

riorities

Reinforce core skills and

capabilities

Fit-for-purpose and effective

organisation

Greater agility to accelerate

decision-making and execution

Strong leadership and winning

culture

Operationalfull potential

Externalspend

Integrated sales & operations planning

More effective organization

1. OEE: Overall Equipment Effectiveness

2. TCO: Total Cost of Ownership

31

HORIZON 2: INVESTING TO GROW THE CORE

Northern Cape

full potential

Conceptual3-10 years

Pre-feasibility2–3 years

ConstructionCompleted

Sishen

DMS upgrade to UHDMS

Leveraging proven UHDMS

technology

~2Mtpa over LoM

Low capex

High margin

Sishen

2nd Modular UHDMS plant

Reprocessing of remaining JIG

discard stream material

~0.6Mtpa over LoM

Low capex

High margin

Sishen and Kolomela

UHDMS modular plants

Sishen:

Reprocessing of JIG

discard material

~0.7Mtpa product

Low opex

High margin

Kolomela:

Processing of B grade material

~0.7Mtpa product

Low grade beneficiation options

On mine exploration

Near mine exploration potential

LoM extension, maintaining high returns and product quality

GUIDANCE

33

Production: 30 – 31Mt in 2018

Waste: 170 – 180Mt in 2018

Unit costs: R295 to R305 in 2018

Strip ratio: to exceed 4 in 2018, LoM ~4

LoM: 13 years

Production: ~14Mt in 2018

Waste: 55 – 57Mt in 2018

Unit costs: R240 to R250 in 2018

Strip ratio: to exceed 3.5 in 2018, LoM ~4

LoM: 14 years

GUIDANCE

Sishen Kolomela

Total production (Mt)

44 – 45Total sales (Mt)

44 – 45Capex (Rbn)

3.9 – 4.1

34

UNLOCKING FULL POTENTIAL

Safe, efficient

and productive

operations

Sound

financial

discipline

Well positioned

for long term

sustainability

QUESTIONS

ANNEXURES

37

Mt FY17 FY16 % change 2H17 1H17 % change

Railed to port (incl. Saldanha Steel) 42.0 39.8 6 21.2 20.8 2

Sishen mine (incl. Saldanha Steel) 28.5 26.8 6 14.1 14.4 (2)

Kolomela mine 13.5 13.0 4 7.1 6.4 11

Total sales 44.9 42.5 6 23.7 21.2 12

Export 41.6 39.1 6 22.1 19.5 13

Domestic 3.3 3.4 (3) 1.6 1.7 (6)

Total ore shipped 41.6 38.7 7 22.1 19.5 13

CFR (shipped by Kumba) 28.6 27.3 5 15.9 12.7 25

FOB (shipped by customers) 13.0 11.4 14 6.2 6.8 (9)

Finished product inventory 4.3 3.5 23 4.3 4.4 (2)

ANNEXURE 1:LOGISTICS PERFORMANCE REFLECTS HIGHER PRODUCTION

38

1. Including Thabazimbi2. Excluding the impairment reversal in 2017/charge in 2016

ANNEXURE 2:ROBUST OPERATING MARGIN AND HEALTHY CASH GENERATION

Rm FY171 FY161 % change 2H171 1H171 % change

Revenue 46 379 40 767 14 24 879 21 500 16

Operating expenses (25 058) (25 451) 2 (11 205) (13 853) 19

Operating profit 21 321 15 316 39 13 674 7 647 79

Operating margin (%)2 36 38 (2) 36 36 -

Profit for the period 16 133 11 144 45 10 135 5 998 69

Equity holders of Kumba 12 335 8 621 43 7 749 4 586 69

Non-controlling interest 3 798 2 523 51 2 386 1 412 69

Effective tax rate (%) 25 26 (1) 27 23 4

Cash generated from operations 22 432 17,218 30 10 706 11 726 (9)

39

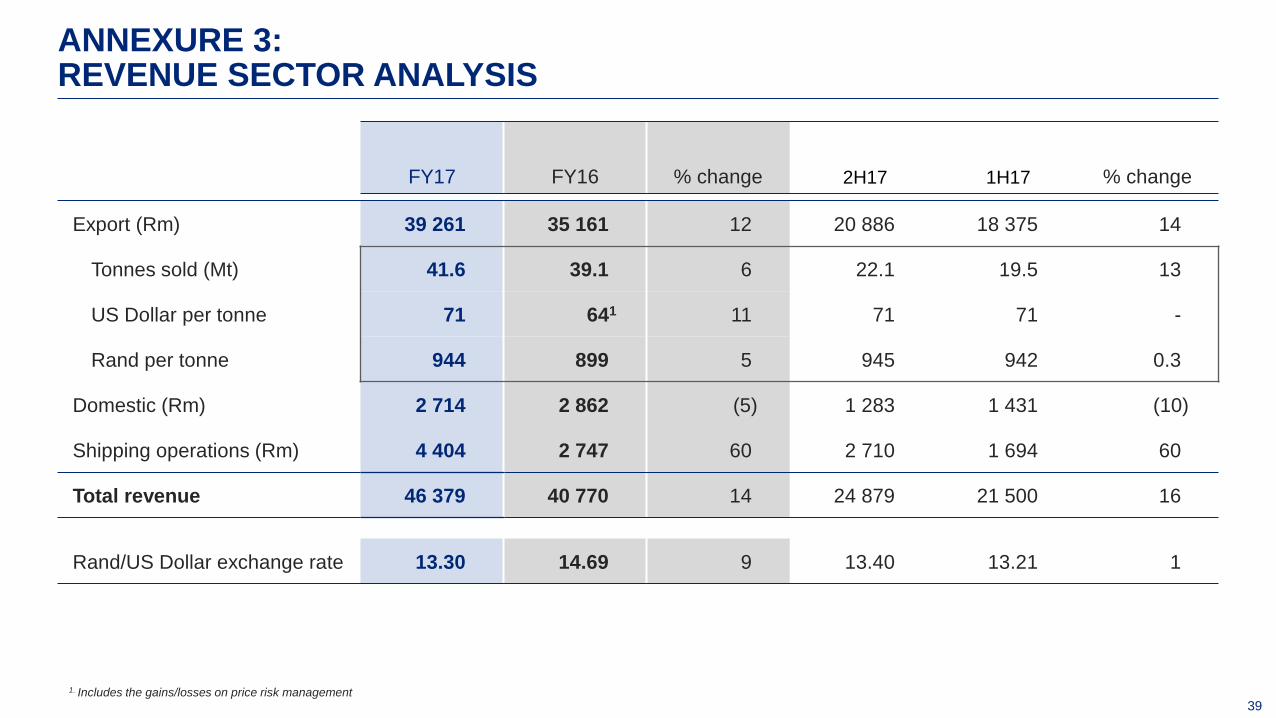

FY17 FY16 % change 2H17 1H17 % change

Export (Rm) 39 261 35 161 12 20 886 18 375 14

Tonnes sold (Mt) 41.6 39.1 6 22.1 19.5 13

US Dollar per tonne 71 641 11 71 71 -

Rand per tonne 944 899 5 945 942 0.3

Domestic (Rm) 2 714 2 862 (5) 1 283 1 431 (10)

Shipping operations (Rm) 4 404 2 747 60 2 710 1 694 60

Total revenue 46 379 40 770 14 24 879 21 500 16

Rand/US Dollar exchange rate 13.30 14.69 9 13.40 13.21 1

ANNEXURE 3:REVENUE SECTOR ANALYSIS

1. Includes the gains/losses on price risk management

40

15 965

18 307

3 117

4 486

1 206470 1 505

1 369436

(839)

5 379

5 815

FY16 Mining operations Stockmovement

Deferred stripping Escalation,non-cash and forex

Shipping Selling anddistribution

FY17

Rm

Mining operations Shipping Selling and distribution

24 461

1

Mining

2 342Logistics

1 805

28 608

1. Excluding the mineral royalty, impairment reversal

ANNEXURE 4:OPERATING EXPENDITURE DRIVEN BY VOLUME GROWTH

41

ANNEXURE 5:AGGREGATE OPERATING EXPENDITURE

Rm FY17 FY16 % change 2H17 1H17 % change

Cost of goods sold 18 306 15 965 15 9 521 8 785 8

Cost of goods produced 16 588 15 160 9 8 435 8 153 3

Production costs 16 360 15 470 6 8 704 7 656 14

Sishen mine 11 164 11 372 (2) 5 828 5 336 9

Kolomela mine 4 708 3 888 21 2 597 2 111 23

Thabazimbi mine 94 195 (52) (10) 104 (110)

Other 394 15 2 527 289 105 175

Inventory movement WIP 228 (310) 174 (269) 497 154

A grade (69) 118 (158) (69) - 100

B grade 297 (428) 169 (200) 497 (140)

Inventory movement finished product 231 300 (23) 215 16 1 244

Corporate support and studies 1 123 1 074 5 673 450 50

Forex and other 364 (569) 164 198 166 19

Mineral royalty 1 239 986 26 591 648 (9)

Impairment charge/(reversal) (4 789) 4 100 (4 789) - 100

Selling and distribution 5 816 5 379 8 3 157 2 659 19

Shipping operations 4 486 3 117 44 2 725 1 761 55

Operating expenses 25 058 25 451 (2) 11 205 13 853 (19)

42

(3)(30) (18) (18)

46 53 32 31

10 10

4 4

12 13

14 15

44 58

28 27

64

59

68 96

43

50

26

30

80

74

47

52

Sishen mineFY16

Sishen mineFY17

Kolomela mineFY16

Kolomela mineFY17

Deferred stripping Other Energy Drilling and blasting Maintenance Outside services Fuel Labour

296

287

201

237

ANNEXURE 6:SISHEN AND KOLOMELA MINES’ UNIT CASH COST STRUCTURE (R/t)

43

16 17 15 12

3 3 2 2

4 4 66

15 1813

10

21 19 31 38

14 1612 12

27 23 21 20

Sishen mineFY16

Sishen mineFY17

Kolomela mineFY16

Kolomela mineFY17

Other Energy Drilling and blasting Maintenance Outside services Fuel Labour

ANNEXURE 7:SISHEN AND KOLOMELA MINES’ UNIT CASH COST STRUCTURE (%)

44

Rm 2016 2017

12 months

31 Dec 2018

Forecast

Approved expansion 856 575 ~500

Deferred stripping 321 1 194 1 400 – 1 500

Sishen 88 942 1 200 – 1 300

Kolomela 233 252 ~200

SIB Sishen 875 793 1 300 – 1 400

SIB Kolomela 301 507 ~700

Total capital expenditure 2 353 3 069 3 900 – 4 100

ANNEXURE 8:CAPITAL EXPENDITURE ANALYSIS

45

Change per unit of key operational drivers, each tested independently

Sensitivity analysis Unit change EBITDA impact

Currency (Rand/US$) R0.10/US$ R300m

Export Price (US$/t) US$1.00/t R535m

Volume (kt) 100kt R65m

Breakeven price impact

Currency (Rand/US$) R1.00/US$ US$2.75/t

(400)

(380)

(265)

400

380

265

-500 -400 -300 -200 -100 0 100 200 300 400 500

Currency

Export price

Export volume

Sensitivity analysis (1% change) – EBITDA impact (Rm)

Source: WSA, Kumba market intelligence, GTIS Based on 4M16 data

ANNEXURE 9:SENSITIVITY ANALYSIS

1% change to key operational drivers, each tested independently