Embed Size (px)

Citation preview

March 2, 2012 British Columbia Utilities Commission 6th Floor, 900 Howe Street Vancouver, BC V6Z 2N3 Attention: Ms. Alanna Gillis, Acting Commission Secretary Dear Ms. Gillis: Re: Application for Approval of a Capital Expenditure Schedule, Rate Design and

Rates Established in an Operating and Maintenance Agreement between FortisBC Energy Inc. (“FEI” or the “Company”) and the Strata Corporation of Tsawwassen Springs Development to Provide Thermal Energy Services (“TES”) (the “Application”)

Tsawwassen Springs Development (the “Development”) is a four-phased residential development. FEI entered into an Operating and Maintenance Agreement (the “Service Agreement”) with the developer of the Development to own, operate, and maintain only four Loop Field Systems (“LFS”), each of which is a component of the ground heat pump geo-exchange energy system serving each phase of the Development. The contract has been assigned to the strata corporation (the “Strata Corporation”) which now owns the Development and the energy systems except the LFS. The LFS for the first phase of the Development is now operational.

In Order No. G-9-12 under paragraph 2, the Commission directed:

“A CPCN proceeding is not required for the following four AES projects: Tsawwassen Springs, Camden Green, Glen Valley and Gorman School”.

Further in the Reasons for Decision attached as Appendix A to Order No. G-9-12, on page 4 of 8, regarding the four identified projects the Commission Panel noted:

“where construction was started well in advance of the Order, and outside of the 30 day period that is described in section 45(5) of the Act, the Commission Panel agrees that no CPCN is required.”

With this Application, FEI is seeking, pursuant to section 44.2 of the Utilities Commission Act (the “Act”), for acceptance of a capital expenditure schedule. Although FEI has filed the “Loop Field System Purchase and Sale Agreement” entered into between FEI and the developer (the “Purchase and Sale Agreement), FEI does not request approval or acceptance from the Commission for this agreement. The Purchase and Sale Agreement is provided to demonstrate and support the calculation of capital expenditures requested.

FEI is also seeking pursuant to sections 59-61 of the Act, Commission approval of the rate design and rates established in the Service Agreement as “just and reasonable.” As

Diane Roy Director, Regulatory Affairs - Gas FortisBC Energy Inc.

16705 Fraser Highway Surrey, B.C. V4N 0E8 Tel: (604) 576-7349 Cell: (604) 908-2790 Fax: (604) 576-7074 Email: [email protected] www.fortisbc.com Regulatory Affairs Correspondence Email: [email protected]

B-1

March 2, 2012 British Columbia Utilities Commission Application for Approval of Operating and Maintenance Agreement for TES between FEI and the Strata Corporation of Tsawwassen Springs Development Page 2

demonstrated in the Application, the rate (termed “Monthly Fee” in the Service Agreement) designed for the Development accords with basic cost of service ratemaking principles that recover a “fair and reasonable charge” for the service to be provided to the Strata Corporation.

Regulatory Review Process

In Orders No. G-1-12 and G-9-12, the Commission has decided that a Certificate of Public Convenience and Necessity (“CPCN”) is not required for this Application. As FEI stated in the “Submissions of FEU Regarding Interim CPCN Threshold” in the AES Inquiry, the procedural process to review an application under a provision of the Act should be determined in a manner that is commensurate with the size and scope of the projects at issue. For this Application, FEI proposes that the regulatory review consists of the Commission and the registered interveners filing written comments on the Application. FEI will then address concerns raised in written comments through a written submission. FEI submits that this approach is appropriate and efficient for this Application for the following reasons.

First, the cost of service rates provided for in the Service Agreement and for which FEI seeks approval are based on the cost-of-service model and cost inputs set forth in section 12A of FEI’s General Terms and Conditions that were approved in FEI’s 2010-2011 Revenue Requirements Application. Although the Commission has made GT&C 12A interim by Order No. G-223-11, the interim nature of 12A should not affect the approval of the Application. The rates designed in this Application follow the cost-of-service rate design principles and allow FEI to recover costs for providing service to the Strata Corporation during the contract period.

Second, the size of the project subject to this Application is rather small. The capital expenditures for the Loop Field Systems to be owned and operated by FEI are approximately $1.2 million, reflecting the aggregate cost of all four Loop Field Systems to be installed at the Development.

Third, the energy systems that will be installed will be completely within the Development lands and will not have any direct impacts on others.

Fourth, FEI’s natural gas customers will not be adversely impacted by the thermal energy service provided to the Strata Corporation because all costs and revenues will be recorded in the TES Deferral Account and will not be recovered from the natural gas class of service customers.

Fifth, this service differs from the service that FEI proposes to provide to the Delta School District, where FEI will own and operate all of the thermal energy equipment, purchase all of the energy necessary to produce thermal energy, meter the thermal energy deliveries for billing purposes and set rates on an annual basis to reflect changes in the cost of service. Rather, the rates for this service are set according to a cost of service forecast for the term of the contract for FEI to own and operate only one component of the thermal energy equipment. As a result, the service and rates for this Application are inherently simpler and therefore, review may be abbreviated in comparison. Further, since this Application follows GT&C 12A, which is now interim, there is little or nothing of precedential value in this

March 2, 2012 British Columbia Utilities Commission Application for Approval of Operating and Maintenance Agreement for TES between FEI and the Strata Corporation of Tsawwassen Springs Development Page 3

Application other than as it relates to the other three projects FEI developed under GT&C12A and will be submitting shortly to the Commission.

Finally, an inquiry into FEI’s “alternative energy services” is underway. Some broader or policy-type issues relevant to FEI’s provision of thermal energy services have been canvassed thoroughly in that process. Although some of these issues may be relevant to the present Application, they should not be re-addressed here.

In light of these considerations, FEI submits that the process described above is appropriate for the review of this Application.

Confidentiality

FEI requests that the Commission keep the following appendices confidential in accordance with the Commission’s Practice Directive related to Confidential Filings:

(a) Appendix A – Operating & Maintenance Agreement

(b) Appendix B – Purchase and Sale Agreement

However, after the approval of the Application, Appendix A can become part of the public record for this Application.

The particular rationale for keeping each specific document confidential is as follows.

Service Agreement (Appendix A)

The general terms of the Service Agreement are described in Section 2.3.1 of the Application. FEI submits that this Service Agreement should be kept confidential until this Application is approved by the Commission. The terms and conditions of the Agreement reveal the parties’ agreed upon positions after negotiation. Should this Application not be approved, FEI will be in the situation where it may need to enter into re-negotiation with the Strata Corporation. In the event that the Strata Corporation may wish to consider other providers of thermal energy service (competitors of FEI) during the re-negotiation, FEI would be prejudiced by a competitor who has access to those contractual terms and gain an unfair advantage over FEI in future negotiations. This represents a substantial risk of harm to FEI.

Once the contracts are approved, the concern discussed above no longer exists. Thus, the contracts can then be made public.

Purchase and Sale Agreement (Appendix B)

The general terms of the Purchase and Sale Agreement are described in section 3 of the Application. FEI submits that the Purchase and Sale Agreement should be kept confidential on the basis that it contains commercially sensitive information, and there is a reasonable expectation of prejudice to FEI if this information is made public. The Purchase and Sale Agreement contains information relevant to the business model/arrangement that FEI has developed for owning and operating thermal energy systems employed in residential strata developments. FEI has spent time developing this business model that is unique to this Development but also may be used in similar projects. FEI believes that disclosure of such

March 2, 2012 British Columbia Utilities Commission Application for Approval of Operating and Maintenance Agreement for TES between FEI and the Strata Corporation of Tsawwassen Springs Development Page 4

commercially sensitive information can unduly harm FEI’s competitive and negotiations in future similar business negotiations and transactions.

Moreover, the public interest in the transparency of the regulatory process and FEI’s charged rates will not be impaired. As stated above, the Service Agreement will become public when this Application is approved. As mentioned above, the relevant portion of the Purchase and Sale Agreement is the purchase price for the Loop Field Systems, which has been disclosed in the Application.

FEI submits that the proper approach to considering confidentiality requests of this nature is to balance between the commercial interest being compromised, on the one hand, and the interests of those seeking disclosure of the document on the other hand. FEI does not object to customer group interveners such as the British Columbia Public Interest Advocacy Centre on behalf of the British Columbia Old Age Pensioners Organization et al (“BCOAPO”) and the Commercial Energy Consumers Association of British Columbia (“CEC”) and environmental interveners such as the BC Sustainable Energy Association (“BCSEA”), who are not competitors of FEI or currently negotiating with FEI for TES projects, being provided with these appendices upon executing standard form undertakings of confidentiality. However, for the reasons set out above, FEI does not believe that any of these documents should be provided to its competitors, such as Corix Utilities Inc. This ensures that those parties who represent the interests of ratepayers, and broader public interests, have access to the full record of the proceeding, and diminishes concerns regarding transparency in the regulatory process.

FEI therefore requests the Commission hold the information in the above identified Appendices confidential in accordance with the Commission’s Practice Directive related to Confidential Filings. FEI believes that there is more than adequate non-confidential information in the Application to permit a transparent review process for all concerned interveners. Furthermore, those parties with non-competitive, public interest concerns with the Application can have access to the full record upon executing standard undertakings of confidentiality, and as a result FEI’s requests for confidentiality should be granted.

If you require further information or have any questions regarding this submission, please contact Gareth Jones at (250) 380-5792.

Yours very truly, FORTISBC ENERGY INC. Original signed by: Shawn Hill

For: Diane Roy Attachments cc: Registered Parties to the FEU 2012-2013 RRA Proceeding Registered Parties to the AES Inquiry Proceeding

FortisBC Energy Inc.

Application for Approval of a Capital Expenditure Schedule and Rate

Design and Rates Established in an Operating and Maintenance Agreement

to Provide Thermal Energy Services for Tsawwassen Springs Development

March 2, 2012

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

Page i

Table of Contents

1 Request for Approval ......................................................................................... 1

1.1 Thermal Energy Service ........................................................................................ 1

1.2 Capital Expenditures of $1.184 Million ................................................................... 1

1.3 Rates for Service ................................................................................................... 2

2 General Terms and Conditions Section 12A .................................................... 3

2.1 System Used at the Development .......................................................................... 3

2.1.1 Geo-Exchange System ............................................................................................ 3

2.1.2 Operating Characteristics ........................................................................................ 5

2.2 Ownership of LFS .................................................................................................. 5

2.2.1 Selection and construction of Geo-Exchange ......................................................... 5

2.2.2 Ownership of the Subsurface Loop fields ................................................................ 6

2.3 Cost of Service Model ............................................................................................ 7

2.3.1 Rate and Other Key Terms of Service Agreement .................................................. 7

2.3.2 Cost of Service Recovery ........................................................................................ 7

2.4 Projected Energy Consumption/Number of Customers .......................................... 9

2.5 Costs ....................................................................................................................10

2.5.1 Capital Cost, Rate Base & Depreciation Expense ................................................ 11

2.5.2 Return on Investment ............................................................................................ 13

2.5.3 Operating and Maintenance (O&M) Expenses ...................................................... 13

2.5.4 Applicable Taxes ................................................................................................... 14

3 Conclusion ........................................................................................................ 16

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

Page ii

List of Appendices

A – Operating & Maintenance Agreement (Service Agreement) CONFIDENTIAL

B – Loop Field System Purchase and Sale Agreement (Purchase Agreement) CONFIDENTIAL

C – Financial Schedules

Schedule 1 - Rate Design & Thermal Energy Services Deferral Account

Schedule 2 - Revenue Requirement

Schedule 3 - Rate Base

Schedule 4 - Income Tax Expense

Schedule 5 - Discounted Cash Flow Analysis.

D – Evidence in Support of Equity Risk Premium

E – Draft Order

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

Page 1

1 REQUEST FOR APPROVAL

1.1 Thermal Energy Service

Pursuant to section 12A of FortisBC Energy Inc. (“FEI”) General Terms and Conditions (“GT&C

12A”) and Order No. G-141-09 issued by the British Columbia Utilities Commission (“BCUC” or

the “Commission”), FEI intends to provide Thermal Energy Service (“TES”) to the Tsawwassen

Springs Development (the “Development”), by owning, operating and maintaining four geo-

exchange loop field systems (“LFS”), one for each phase of the Development, and charging a

rate for the service. The provision of thermal energy service for each of the four phases of the

Development is administered through one Operating and Maintenance Agreement (the “Service

Agreement”, attached confidentially as Appendix A) between FEI and the Strata Corporation

(owners of Strata Plan BCS41181, also being referred to as the “Strata”) (the “Application”).

Each LFS will provide thermal energy and deliver it to the Strata by connecting to equipment

that the Strata will own and operate. Further, the Strata will own the mechanical equipment that

causes the circulation of the water/glycol mixture in each LFS that FEI owns and operates and

will be responsible for purchasing any electricity or natural gas necessary to operate their

equipment. FEI will not be metering the thermal energy that FEI provides through each LFS

and delivers to the Strata.

This service differs from the service that FEI proposes to provide to the Delta School District,

where FEI will own and operate all of the thermal energy equipment, purchase all of the energy

necessary to produce thermal energy and meter the thermal energy deliveries for billing

purposes.

1.2 Capital Expenditures of $1.184 Million

FEI requests that the Commission accept capital expenditures of $1.184 million pursuant to

section 44.2 of the Utilities Commission Act (“UCA”). The amount reflects the cost to purchase

all four LFS’s, plus 10 percent capitalization of the purchase price for each LFS. Although FEI

does not require or request Commission acceptance of the Loop Field System Purchase and

Sale Agreement entered between FEI and the developer (the “Purchase and Sale Agreement”),

attached confidentially as Appendix B, it is filed in support of the calculation of capital

expenditure amounts requested. Further details regarding the capital expenditures are in

section 2.5.1.

1 The Service Agreement was originally executed between FEI and TGCC Management LLP, the developer, and

was subsequently assigned to the owners of Strata Plan BCS4118.

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

Page 2

Section 44.2 of the Act requires the Commission to consider the applicable of British Columbia’s

energy objectives, which are defined in Section 2 of the Clean Energy Act. The requested

capital expenditures are for geo-exchange systems, which, in turn, advance British Columbia’s

energy objectives by:

• using innovative geothermal energy technology that supports energy conservation and

efficiency through the use of a renewable resource;

• reducing BC greenhouse gas emissions through the use of a renewable resource; and

• encouraging the switching from one kind of energy source or use to another that

decreases greenhouse gas emissions in British Columbia.

All of this will, in turn, benefit British Columbians in general, whether or not they currently

receive services from FEI.

Moreover, there is no risk to FEI’s natural gas customers as the services contemplated in the

Service Agreement are related to FEI’s thermal energy class of service. As approved in

Commission Order No. G-141-09, costs and revenues related to provision of thermal energy

services will be separately tracked and accounted for.

This Application is consistent with the 2010 Long Term Resource Plan (“LTRP”) filed by the

FortisBC Energy Utilities (comprised of FortisBC Energy Inc., FortisBC Energy (Vancouver

Island) Inc. and FortisBC Energy (Whistler) Inc.) as an application for a specific project that

supports British Columbia’s energy objectives as described above. This Application is also

consistent with the stated intention of FEI to initially apply for approval of rates on a project-by-

project basis.

1.3 Rates for Service

FEI also requests that the Commission approve the proposed rate design and rates as they are

set out in the Service Agreement (termed as “Monthly Fee” in the Agreement, being referred to

here as the “Rate” or “Rates”) pursuant to sections 59-61 of the UCA and in accordance with

Commission Order No. G-9-12. The Rates that FEI proposes to charge for this service are just

and reasonable as they will recover the cost of service relating to the ownership and operation

of each LFS only during the term of the Service Agreement. This is further explained in section

2.5.1 below.

Phase 1 LFS has been constructed and is owned and operated by FEI; however, FEI is not yet

collecting Rates as contemplated under the Service Agreement until FEI receives the requested

approval.

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 3

2 GENERAL TERMS AND CONDITIONS SECTION 12A

FEI submits that the terms of the Service Agreement satisfy the requirements of GT&C 12A.

The discussion below follows GT&C 12A.

2.1 System Used at the Development

2.1.1 GEO-EXCHANGE SYSTEM

The Development is using a geo-exchange system to provide each of the strata lots with the

majority of their thermal energy needs for space heating and cooling by utilizing heat pumps that

access thermal energy from the ground. The GT&C 12A.1 describes geo-exchange systems as

follows:

“Geo-exchange systems, also referred to as geo-thermal systems, earth exchange systems or ground and water source heat pumps, utilize the latent heat energy contained in near surface layers of the earth, ground water and surface water. A subsurface piping system contains a liquid that absorbs heat from the surrounding material and delivers it to a central heat exchanger. High efficiency heat pumps convert this latent energy into hot water or steam contained in a separate piping system that can then deliver the heat energy to where it is required for space heating and hot water uses. Centralized equipment is usually contained within specifically designed mechanical room that serves the entire development. The heat exchanger is reversed to provide space cooling, removing heat from the building(s) and returning it to the subsurface substrate.”

In this instance, there will be four geo-exchange systems in total, each providing the thermal

energy requirements for each of the four phases of the Development. Each geo-exchange

system will have a LFS and will also incorporate a natural gas boiler, which the Strata will own

as part of the mechanical equipment, to supplement the peak heating loads and to supplement

domestic hot water loads in order to minimize capital costs and rates.

Figure 1 below shows the system at the Development.

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 4

Figure 1: Ground Source Heat Pump System (“GSHP System”)

The subsurface piping or geo-exchange loop fields consist of high density polyethylene piping

that circulates a water/glycol mixture (“Agent”). This Agent either absorbs or rejects heat to or

from the earth as necessary depending on the operating mode of the heat pumps throughout

the Development.

LFS for phase 1 for the Development has already been successfully installed and FEI is

currently operating the LFS. This LFS consists of 54 boreholes at depths of approximately 75

meters each and a common header to connect to the heat pumps.

The remaining 3 phases of the Development will each require a similar LFS.

The mechanical room for each phase of the Development contains pumps for circulating the

flow of the Agent in the LFS, a centralized heat pump for the pre-heating of domestic hot water

and a natural gas boiler to supplement peak thermal energy demands.

The Agent, after circulating through the LFS, enters a header in the mechanical room and then

travels via a building loop to each of the suites where individual heat pumps then supply the

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 5

final thermal energy demands. In the heating season, the LFS extracts heat from the earth into

the Agent for use by the heat pumps and in the cooling season, the LFS rejects heat into the

earth from the building loop system. During peak demand conditions, the natural gas boiler

provides additional heat to the Agent prior to distribution through the building loop to the heat

pumps.

2.1.2 OPERATING CHARACTERISTICS

Ground source heat pump energy systems use electricity to run the pumps that circulate the

Agent through the piping in the earth where the transfer of energy occurs and to run the heat

pumps that either increase or decrease the temperature of the Agent in order to produce usable

thermal energy. At the depth of 100 meters, the ground in the Vancouver area is approximately

10°C regardless of the ambient temperature. This enables ground source heat pumps to

operate at high efficiency levels even during peak demand periods when the ambient air

temperature is low. The relative stability of the temperatures at these depths means that a

vertical borehole, closed loop field and ground source heat pump can provide high efficiency

space heating and cooling under all weather conditions. While it is possible to design these

systems to meet all of the peak day demands, use of a supplementary natural gas boiler helps

to minimize the overall capital costs, without adding significantly to the GHG emissions.

Nonetheless, since it is possible to extract or inject energy from or to the earth, this is free

renewable energy. This explains why heat pumps have efficiency ratings that can exceed

300%.

2.2 Ownership of LFS

2.2.1 SELECTION AND CONSTRUCTION OF GEO-EXCHANGE

The developer chose to meet the energy requirements of its Development with a geo-exchange

thermal energy system as a marketing initiative for the project and to meet their sustainability

commitments to the Corporation of Delta. The developer also sought a hybrid solution

comprised of geo-exchange and natural gas boilers to ensure a competitive rate to the final

customers of the system. By adding gas boilers to the energy system, the capacity of the LFS

could be optimized so that it operates at a higher utilization rates over the course of the year

thus reducing the unit costs of the thermal energy it provides. In this manner, the geo-exchange

thermal energy system will provide up to 90% of the overall energy required for space heating,

with the natural gas boilers providing the remaining 10%. FEI does not own the boilers and is

only providing the energy that comes from the LFS.

Given the advantages of having the developer’s general contractor oversee the work related to

the drilling of the boreholes and other construction activities, the developer and FEI decided to

have the developer construct each LFS as part of their overall Development, and that FEI will

purchase the LFS at a fixed price once it has been commissioned. In this manner, the capital

costs of the Development, including the geo-exchange thermal energy systems, were reduced,

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 6

and construction and cost risks have been assumed by the developer. This approach enhanced

the marketability of the Development and also ensured that the Rate that FEI will charge is

stable and predictable for the Strata Corporation.

The design of the first LFS was performed by certified personnel at the developer’s direction.

FEI reviewed the design and was satisfied that the LFS would be compatible with the other

components of the GSHP System.

After the successful commissioning of the LFS in phase 1 was completed in Q2, 2011 and an

occupancy permit was obtained for that phase, FEI purchased the LFS from the developer

under the Purchase and Sale Agreement.

FEI will purchase each LFS for each phase of the Development following a similar process.

The expected completion date for the remainder of the phases is as follows:

Phase 2: Projected Completion Q3, 2013 Phase 3: Projected Completion Q3, 2014 Phase 4: Projected Completion Q3, 2015

2.2.2 OWNERSHIP OF THE SUBSURFACE LOOP FIELDS

FEI will own, operate and maintain each LFS for each phase of the Development. FEI’s

ownership is up to the point at which each LFS enters the respective mechanical room. The

Strata will own all additional equipment related to the GSHP System in the mechanical rooms

and throughout the buildings. Each strata lot owner will then own the equipment located within

their suite, namely the heat pump.

FEI will charge the Strata Corporation a Rate for owning, operating and maintaining each of the

four LFS components of the energy systems. Details of services to be provided in terms of

operation and maintenance are outlined in Schedule C of the Service Agreement.

It is important to note that FEI is only responsible for providing thermal energy from the LFS,

and is not responsible for the ownership, operation and maintenance of the mechanical room

equipment, building loop or the in-suite heat pumps. Further, FEI is not responsible for

acquiring the natural gas or electricity necessary to operate the geo-exchange systems.2

Therefore, the Rate in the Service Agreement does not recover the costs of any of these

components; rather, the Rate relates to the ownership and operation of one component of each

thermal energy system and recovers only the cost of owning and operating the LFS.

2 FEI and the Strata are in negotiation for FEI to provide maintenance services for other components of

the energy system. This will be a separate agreement if one is reached.

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 7

2.3 Cost of Service Model

2.3.1 RATE AND OTHER KEY TERMS OF SERVICE AGREEMENT

The Rate for each LFS for each phase of the Development is on a monthly basis and is set out

in Schedule D of the Service Agreement as follows:

Phase 1: $1,800 ($21,600 per year) plus applicable taxes Phase 2: $2,800 ($33,600 per year) plus applicable taxes Phase 3: $2,800 ($33,600 per year) plus applicable taxes Phase 4: $1,800 ($21,600 per year) plus applicable taxes

The Rate above is cumulative based on the number of LFS owned and operated by FEI at the

time of billing. For example, once the LFS for phases 1 and 2 are operative, the Rate would be

$4,600 per month ($1,800 plus $2,800). The monthly Rate will also be increased annually by

the greater of the percentage change during the preceding twelve (12) months in Statistics

Canada All Items Consumer Price Index for Vancouver, and two (2%) percent. Further, the

Rate is fixed and cannot be changed without the consent of all parties.

For each of the four phases of the Development, the Service Agreement provides for a term of

25 years running from the date that the particular phase is placed in service, subject to renewal

or renegotiation. As a result, there is not one, but four “terms” of the contract, each running

from the in-service date of the LFS and lasting 25 years.

At the end of the 25 year contractual term with respect to each phase of the Development, the

Service Agreement states that FEI and the Strata Corporation can either renew or renegotiate

the term and other conditions to extend the Agreement. Failing such extension arrangement,

the Strata Corporation must purchase the LFS from FEI for a price equal to twenty percent

(20%) of the initial purchase price paid by FEI. As shown below in section 2.5.1 (Table 3), the

end of term purchase amount is reflected in the LFS cost of service.

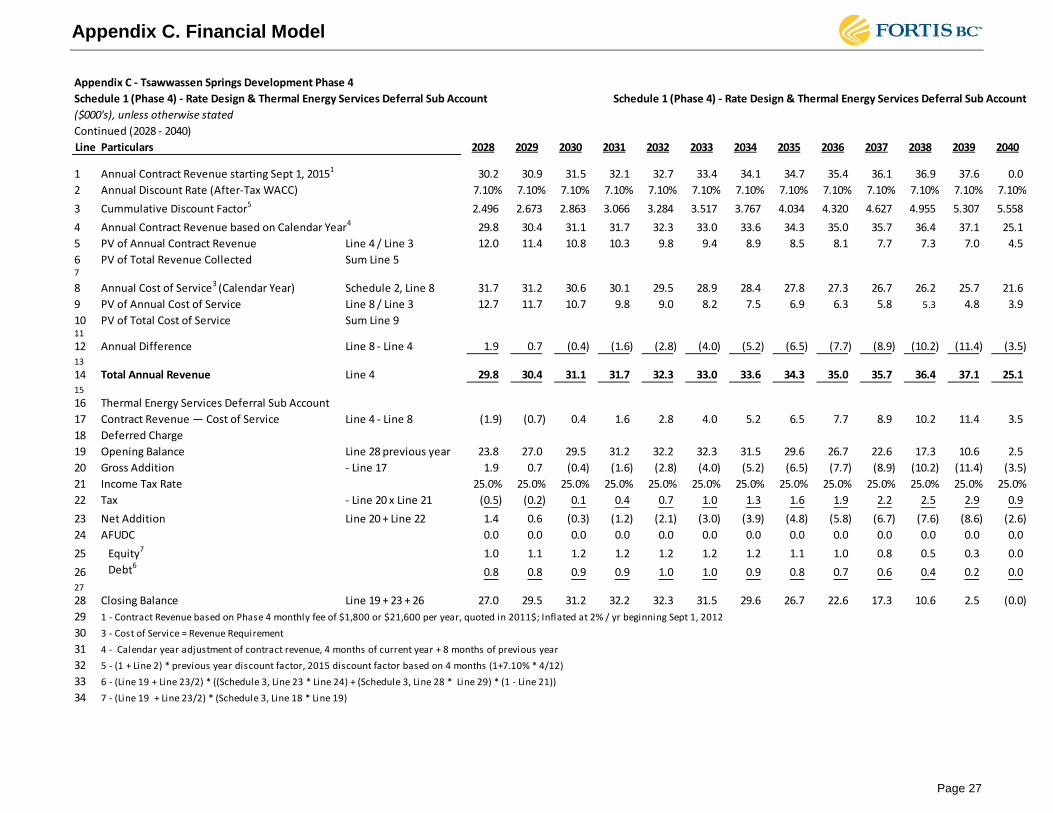

2.3.2 COST OF SERVICE RECOVERY

FEI designed the Rate according to a cost of service forecast model that conforms to the

requirements of GT&C 12A and Order G-141-09. GT&C 12A states:

“All applications by Customers for service using an alternative energy extension will be

subject to review using a cost of service model. The cost of service model will determine

the rate that a customer will pay for the service associated with the alternative energy

extension. Service will be provided under the terms and conditions of the Service

Agreement between FortisBC Energy and the Customer.”

As mentioned above, the Rate for each phase is termed as a Monthly Fee. Each of the monthly

Rates is for owning and operating the LFS for each phase and is designed to fully recover the

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 8

cost of service for that phase. That is, the four monthly rates cumulatively recover the cost of

service for all the phases in aggregate. Accordingly, the present value of total revenue from

rates for each phase, and for all phases in total, over the term of the contract equals the present

value of the total cost of service over the same time period. In this manner, the discounted cash

flows for each LFS demonstrate that each LFS investment will generate sufficient revenues to

recover its cost of service over the term of the Service Agreement.

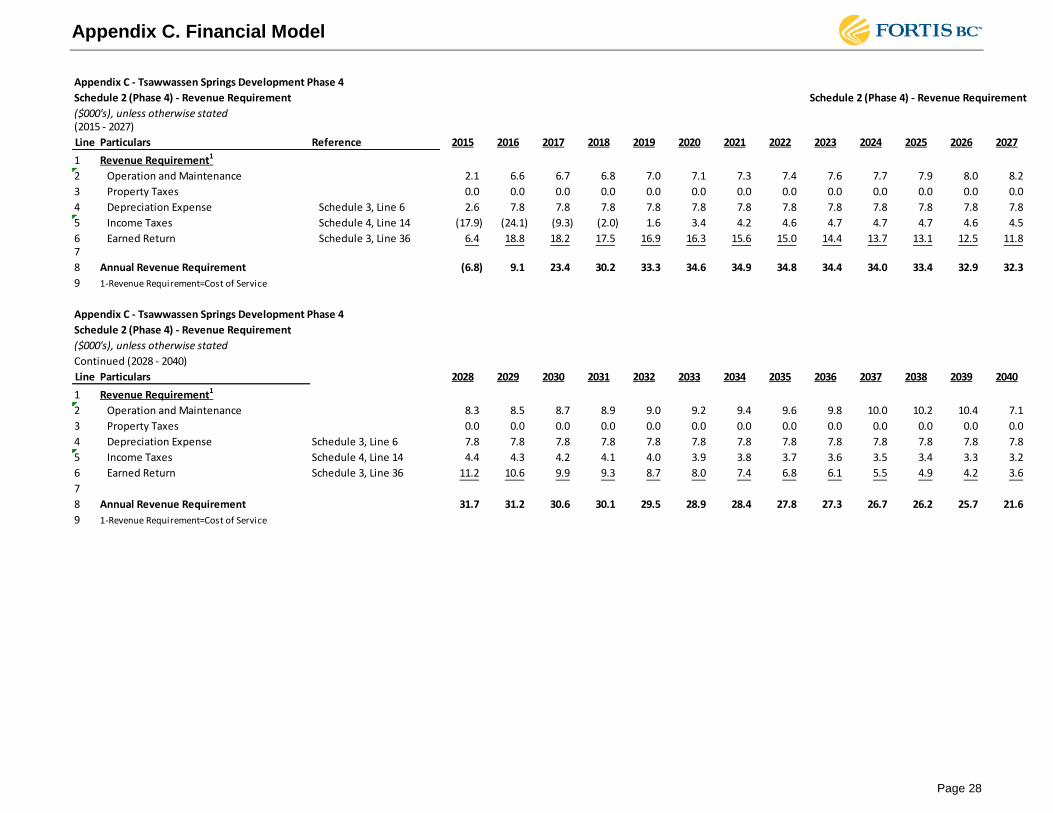

The cost of service is primarily determined by the capital cost of the LFS and the on-going

maintenance costs. The annual cost of service revenue requirements related to the LFS will

display a downward trend over time due to depreciation of the rate base. Should the Rate be

based on a traditional cost of service approach, energy costs at the outset of the term will be

higher and will be declining over time. This is not an attractive rate design for the developer. As

a result, FEI and the developer agreed to levelize the cost of service in order to smooth out the

rate over time, while ensuring that the Rates in aggregate still recover the cost of service over

the term of the Service Agreement. This adjustment provides a smoother rate that reduces

what would have been high upfront costs payable by the Strata Corporation.

Figure 2 below illustrates the difference between a rate derived from a traditional utility cost of

service (dashed line) and that derived from a levelized approach (solid line).

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 9

Figure 2: Cost of Service and Contract Revenue

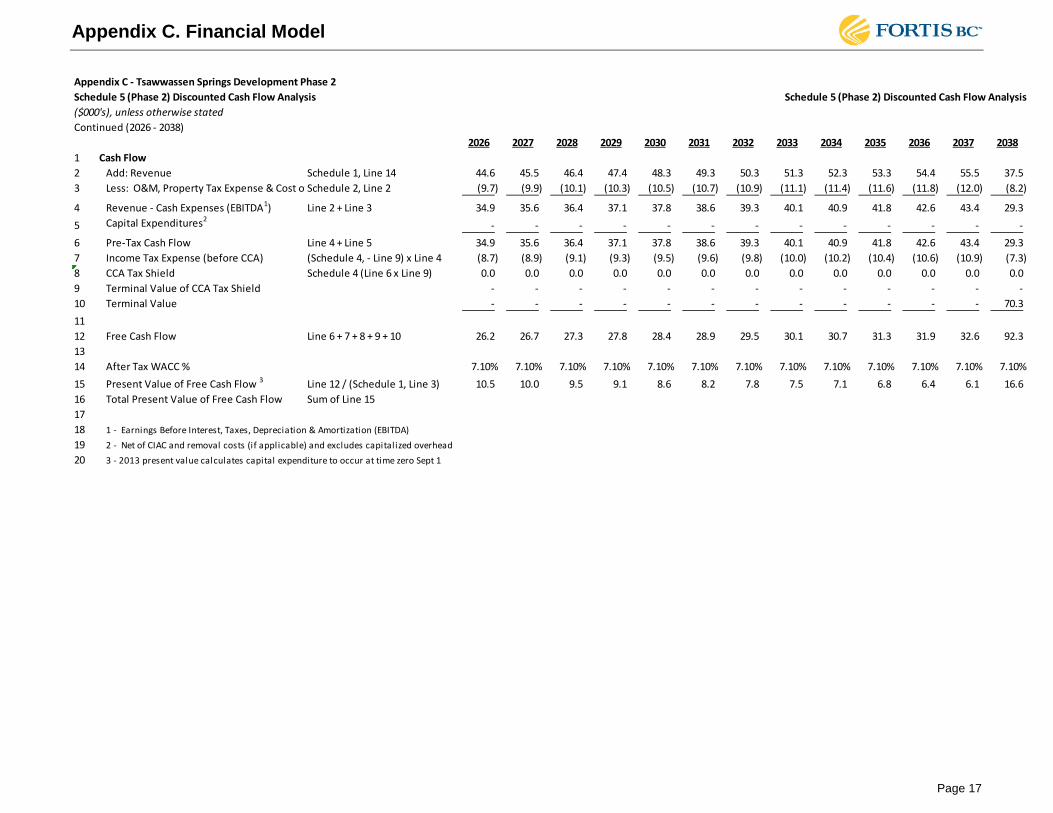

FEI will capture variances between the calculated cost of service and the actual revenues from

Rates in the Thermal Energy Services Deferral Account (the “TES Deferral Account”)

established pursuant to Commission Order No. G-141-09. FEI will also track revenues and

costs relating to this specific project and the Service Agreement via an Internal Order number

(the “IO number”) within the TES Deferral Account. In the initial years of service, the Rate is set

at a level lower than the cost of service; however, the relationship reverses starting

approximately in the year 2026 of the contract term (Appendix C, Schedule 1 - Phase 1), so that

the accumulated balance in the TES Deferral Account in respect of this Development is zero at

the end of the contract term.

2.4 Projected Energy Consumption/Number of Customers

Tsawwassen Springs Development is a residential strata development, consisting of four

phases, totalling 296 fee simple strata lots. However, there will be a single customer for FEI,

the Strata. The phasing plans for the development are as follows:

-

5

10

15

20

25

30

35

40

'00

0$

Year

Cost of Service & Contract Revenue - Contract Years

Cost of Service - Contract Year

Contract Revenue - Contract Year

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 10

Phase 1: 55 apartment style strata lots - four-storey wood framed building

Phase 2: 93 apartment style strata lots - six-storey concrete building

Phase 2: 93 apartment style strata lots - six-storey concrete building

Phase 4: 55 apartment style strata lots - four-storey wood framed building

The Rate that FEI is proposing to charge the Strata is based directly on the cost or purchase

price of the LFS and reflects the cost of service to the Strata over the term of the Service

Agreement. The Strata Corporation allocates the Rate to each of the strata lot (condo) owners

based on unit entitlement. Thus, the energy consumption estimate and the number and type of

thermal appliances do not have bearing on the Rate or its calculation and thus do not impact the

cost of service model, which is more fully explained below.

2.5 Costs

While only phase 1 of the Development is currently complete, FEI has provided separate

financial schedules for all four phases of the Development. Each of the phases includes costs

as set out in GT&C 12A.5:

(a) the full labour, material, and other costs necessary to serve the new Customers less

any contributions in aid of construction by the Customers or third parties, grants, tax

credits, or non-financial factors offsetting the full costs that are deemed to be acceptable

by the British Columbia Utilities Commission;

(b) the appropriate allocation of FortisBC Energy's overheads associated with the

construction of the alternative energy extension;

(c) depreciation expense related to the capital equipment associated with the alternative

energy extension; and

(d) the incremental operating and maintenance expenses necessary to serve the

Customers.

In addition to the costs identified, the cost of service model will include applicable taxes

and the appropriate return on investment as approved by the British Columbia Utilities

Commission.

Each above listed element will be explained further below. The financial schedules that support

the Rates in all four phases are contained in Appendix C. For each phase of the Development,

the schedules are organized as follows:

Schedule 1 - Rate Design & Thermal Energy Services Deferral Account

Schedule 2 - Revenue Requirement

Schedule 3 - Rate Base

Schedule 4 - Income Tax Expense

Schedule 5 - Discounted Cash Flow Analysis.

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 11

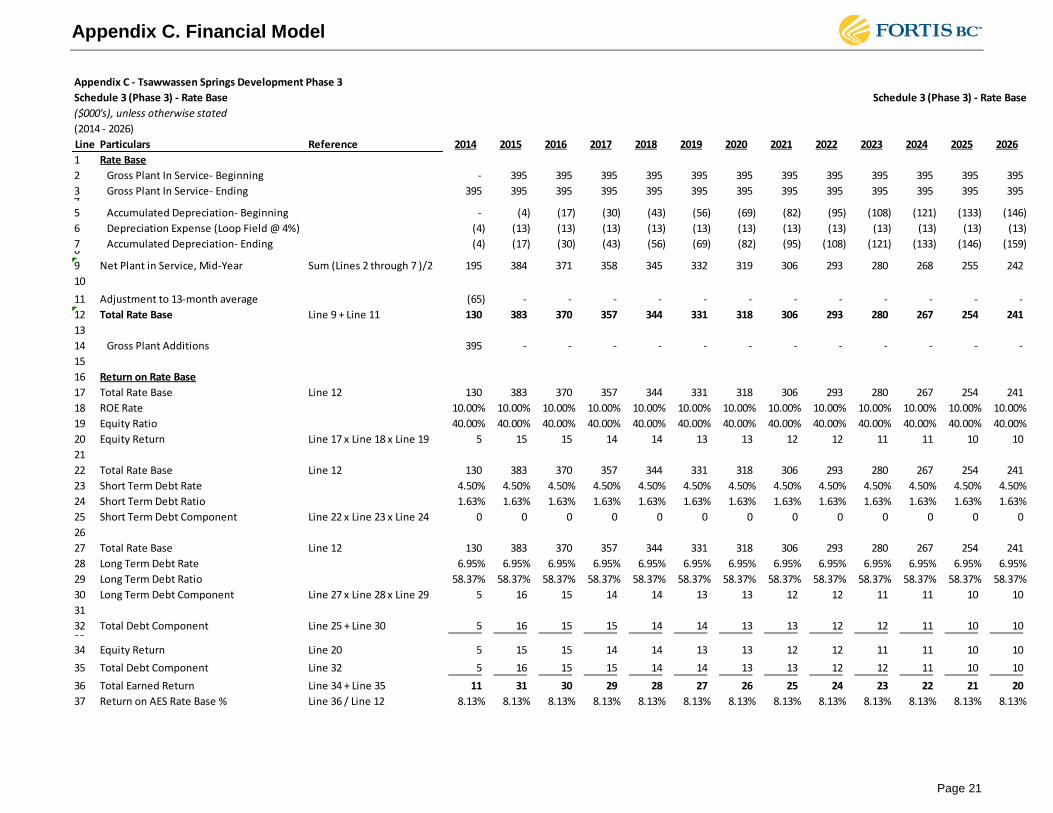

2.5.1 CAPITAL COST, RATE BASE & DEPRECIATION EXPENSE

FEI entered into the Purchase and Sale Agreement with the developer for the purchase of the

four LFS’s. The Purchase and Sale Agreement sets out the pre-determined purchase price for

each LFS in respect of each phase of the Development, as illustrated in Table 1:

Table 1: Purchase Price of LFS

Purchase Price of LFS

2011$ Phase 1 Phase 2 Phase 3 Phase 4 Total

LFS Purchase Price $200,000 $338,000 $338,000 $200,000 $1,076,000

The purchase price of the LFS for phase 1 was based on the installed cost of the system for that

phase and reflects the size of the LFS that has been engineered. The purchase price for the

LFS for phases 2 and 3 was calculated based on the LFS cost for phase 1 adjusted to reflect

the additional square footage of buildings 2 and 3. The LFS purchase price for building 4 is the

same as that of building 1 as the building size of both buildings is identical.

The purchase price to be paid for each LFS, other than for phase 1, will be escalated each year

by the greater of 2% or the rate of inflation. This annual price adjustment to the purchase prices

of the LFS for phases 2, 3 and 4 is the only adjustment that is applicable to the future purchase

prices of the LFS.

The total purchase price for the four loop field systems is $1.076 million. No contribution in aid

of construction has been provided by the developer.

FEI has capitalized 10 percent of the purchase price of each LFS, totalling $107,600. The 10%

is a fixed percentage that FEI has used to represent the project development costs that are to

be capitalized. The development costs related to this Development are for activities spanning

the period from early 2010 to completion of the fourth LFS expected in 2015.

Thus, the capital expenditure of $1.184 million for which FEI seeks acceptance of represents

the sum of the purchase price of $1.076 million, and 10 percent of the purchase price that is to

be capitalized in respect of development costs, as shown in Table 2 below.

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 12

Table 2: Capital Expenditures for which Acceptance is being Sought

Rate Base Summary

2011$ Phase 1 LFS Phase 2 LFS Phase 3 LSF Phase 4 LFS Total

Direct Capital (LFS Purchase Price)

$200,000 $338,000 $338,000 $200,000 $1,076,000

FEI Development Costs (capitalized)

$20,000 $33,800 $33,800 $20,000 $107,600

Total Addition to Rate Base

$220,000 $371,800 $371,800 $220,000 $1,183,600

There is no addition of AFUDC respecting the purchase price for each LFS as FEI will purchase

the LFS from the developer at approximately the same time as the equipment is put into service.

The total rate base addition for all four loop field systems will be $1,183,600, plus any inflation

adjustments. The capital to be depreciated for all four Loop Field Systems is $968,400, as

shown on the last line item in Table 3 below.

Table 3: Depreciable Rate Base Summary

Rate Base Summary and Depreciation

2011$ Phase 1

LFS Phase 2

LFS Phase 3

LFS Phase 4

LFS Total

Rate Base $220,000 $371,800 $371,800 $220,000 $1,183,600

End of Term Buy-Out $40,000 $67,600 $67,600 $40,000 $215,200

Capital to be Depreciated $ 180,000 $ 304,200 $ 304,200 $ 180,000 $968,400

At the end of the 25 year contractual term with respect to each phase of the Development, if the

Service Agreement is not extended, the Strata Corporation must purchase the LFS from FEI for

a price equal to twenty percent (20%) of the initial purchase price paid by FEI. The line item

“Capital to be Depreciated” in the above table represents the portion of the “Total Capital Cost

added to Rate Base” that will be depreciated over the term of the contract so that the remaining

un-depreciated capital at the end of contract matches the end of term buy-out amount.

For example, for phase 1 the amount of capital to be depreciated over the contract term is

$180,000; this amount is equal to the initial rate base capital ($220,000) less the end of term

buy-out amount ($40,000). This approach ensures that assets will not be stranded at the end of

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 13

the contract term. In the event that the Service Agreement is extended, FEI would design a rate

structure to ensure that all capital assets were fully depreciated over the renewal period.

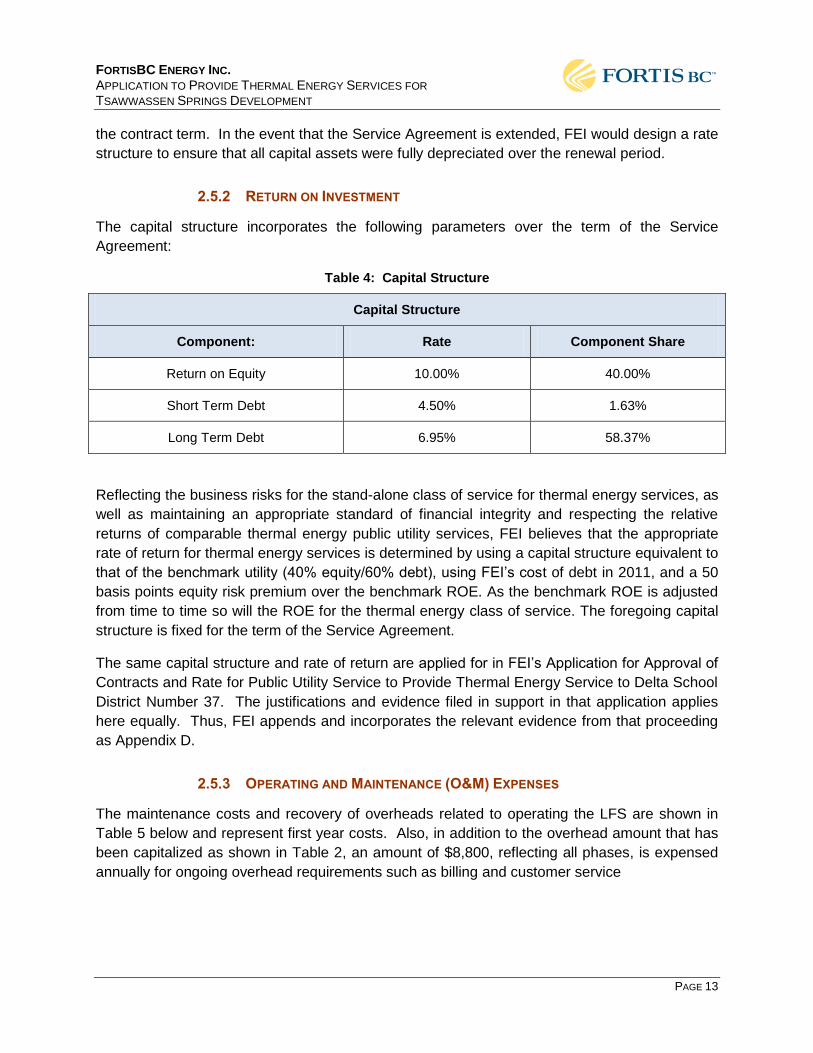

2.5.2 RETURN ON INVESTMENT

The capital structure incorporates the following parameters over the term of the Service

Agreement:

Table 4: Capital Structure

Capital Structure

Component: Rate Component Share

Return on Equity 10.00% 40.00%

Short Term Debt 4.50% 1.63%

Long Term Debt 6.95% 58.37%

Reflecting the business risks for the stand-alone class of service for thermal energy services, as

well as maintaining an appropriate standard of financial integrity and respecting the relative

returns of comparable thermal energy public utility services, FEI believes that the appropriate

rate of return for thermal energy services is determined by using a capital structure equivalent to

that of the benchmark utility (40% equity/60% debt), using FEI’s cost of debt in 2011, and a 50

basis points equity risk premium over the benchmark ROE. As the benchmark ROE is adjusted

from time to time so will the ROE for the thermal energy class of service. The foregoing capital

structure is fixed for the term of the Service Agreement.

The same capital structure and rate of return are applied for in FEI’s Application for Approval of

Contracts and Rate for Public Utility Service to Provide Thermal Energy Service to Delta School

District Number 37. The justifications and evidence filed in support in that application applies

here equally. Thus, FEI appends and incorporates the relevant evidence from that proceeding

as Appendix D.

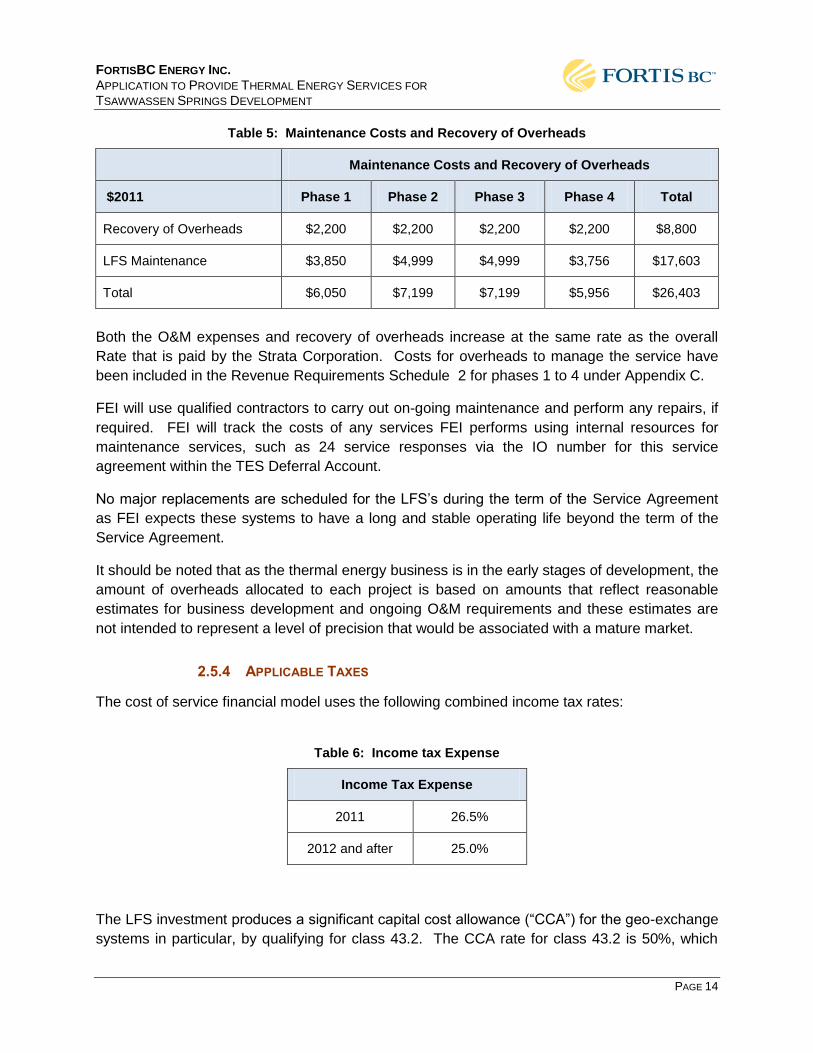

2.5.3 OPERATING AND MAINTENANCE (O&M) EXPENSES

The maintenance costs and recovery of overheads related to operating the LFS are shown in

Table 5 below and represent first year costs. Also, in addition to the overhead amount that has

been capitalized as shown in Table 2, an amount of $8,800, reflecting all phases, is expensed

annually for ongoing overhead requirements such as billing and customer service

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 14

Table 5: Maintenance Costs and Recovery of Overheads

Maintenance Costs and Recovery of Overheads

$2011 Phase 1 Phase 2 Phase 3 Phase 4 Total

Recovery of Overheads $2,200 $2,200 $2,200 $2,200 $8,800

LFS Maintenance $3,850 $4,999 $4,999 $3,756 $17,603

Total $6,050 $7,199 $7,199 $5,956 $26,403

Both the O&M expenses and recovery of overheads increase at the same rate as the overall

Rate that is paid by the Strata Corporation. Costs for overheads to manage the service have

been included in the Revenue Requirements Schedule 2 for phases 1 to 4 under Appendix C.

FEI will use qualified contractors to carry out on-going maintenance and perform any repairs, if

required. FEI will track the costs of any services FEI performs using internal resources for

maintenance services, such as 24 service responses via the IO number for this service

agreement within the TES Deferral Account.

No major replacements are scheduled for the LFS’s during the term of the Service Agreement

as FEI expects these systems to have a long and stable operating life beyond the term of the

Service Agreement.

It should be noted that as the thermal energy business is in the early stages of development, the

amount of overheads allocated to each project is based on amounts that reflect reasonable

estimates for business development and ongoing O&M requirements and these estimates are

not intended to represent a level of precision that would be associated with a mature market.

2.5.4 APPLICABLE TAXES

The cost of service financial model uses the following combined income tax rates:

Table 6: Income tax Expense

Income Tax Expense

2011 26.5%

2012 and after 25.0%

The LFS investment produces a significant capital cost allowance (“CCA”) for the geo-exchange

systems in particular, by qualifying for class 43.2. The CCA rate for class 43.2 is 50%, which

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 15

produces a significant tax benefit in the early years of the project. Income tax costs have been

included in the Revenue Requirements Schedule 2 (phases 1-4) under Appendix C.

There is currently no property tax charge that FEI must pay related to the ownership and

operation of LFS and FEI does not expect property taxes to be levied on the LFS. Accordingly,

FEI has made no provision for the payment of property taxes.

FORTISBC ENERGY INC. APPLICATION TO PROVIDE THERMAL ENERGY SERVICES FOR TSAWWASSEN SPRINGS DEVELOPMENT

PAGE 16

3 CONCLUSION

The developer of the Development has determined to install a GSHP System to meet the

majority of the energy needs at the Development. FEI has reached an agreement to own,

operate, and maintain the LFS of the GSHP System. FEI is seeking acceptance of the capital

cost for $1.184 million, which includes the purchase prices of the four loop field systems and the

amount of capitalized development costs, before any inflationary adjustments.

FEI is also seeking approval of the Rates and rate design applicable to the Development. This

Rate will recover the LFS cost of service, including an appropriate amount for ongoing overhead

expenses, over the term of the Service Agreement.

FEI respectfully requests that the Commission grant the orders sought in this Application. A

draft order is attached as Appendix E.

Appendix A

OPERATING & MAINTENENACE AGREEMENT (SERVICE AGREEMENT)

FILED CONFIDENTIALLY

Appendix B

LOOP FIELD SYSTEM PURCHASE AND SALE AGREEMENT (PURCHASE AGREEMENT)

FILED CONFIDENTIALLY

Appendix C

FINANCIAL SCHEDULES

Appendix C. Financial Model

Page 1

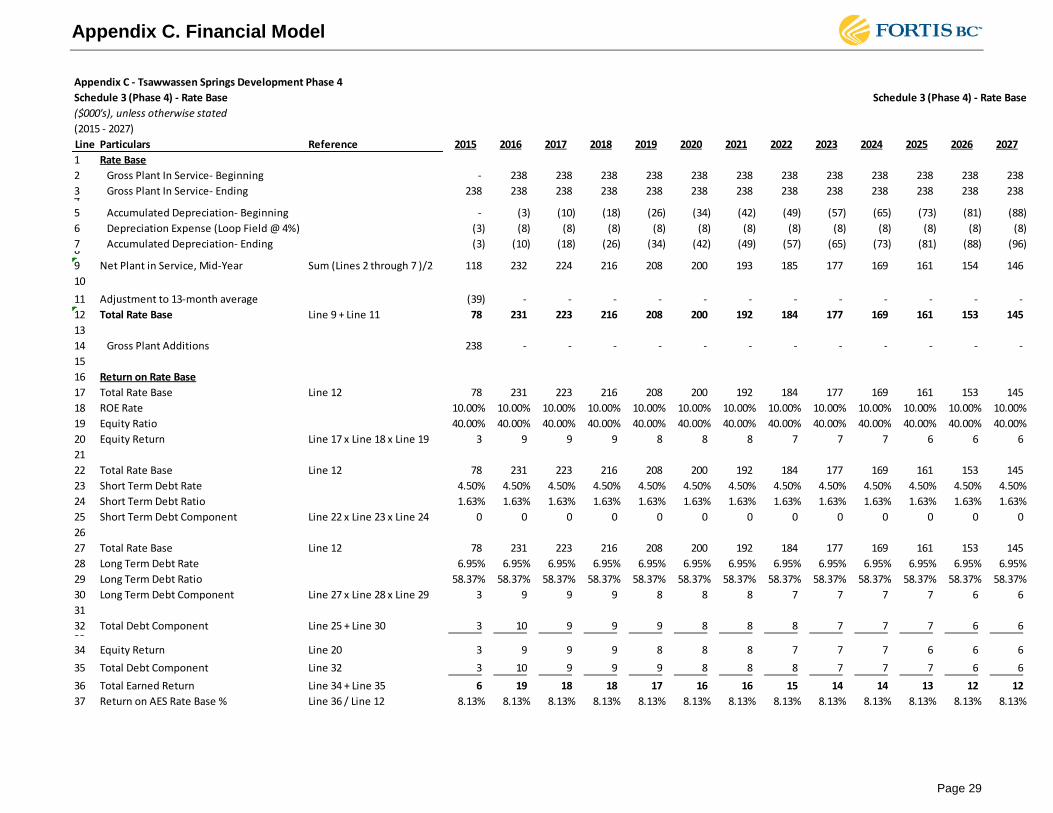

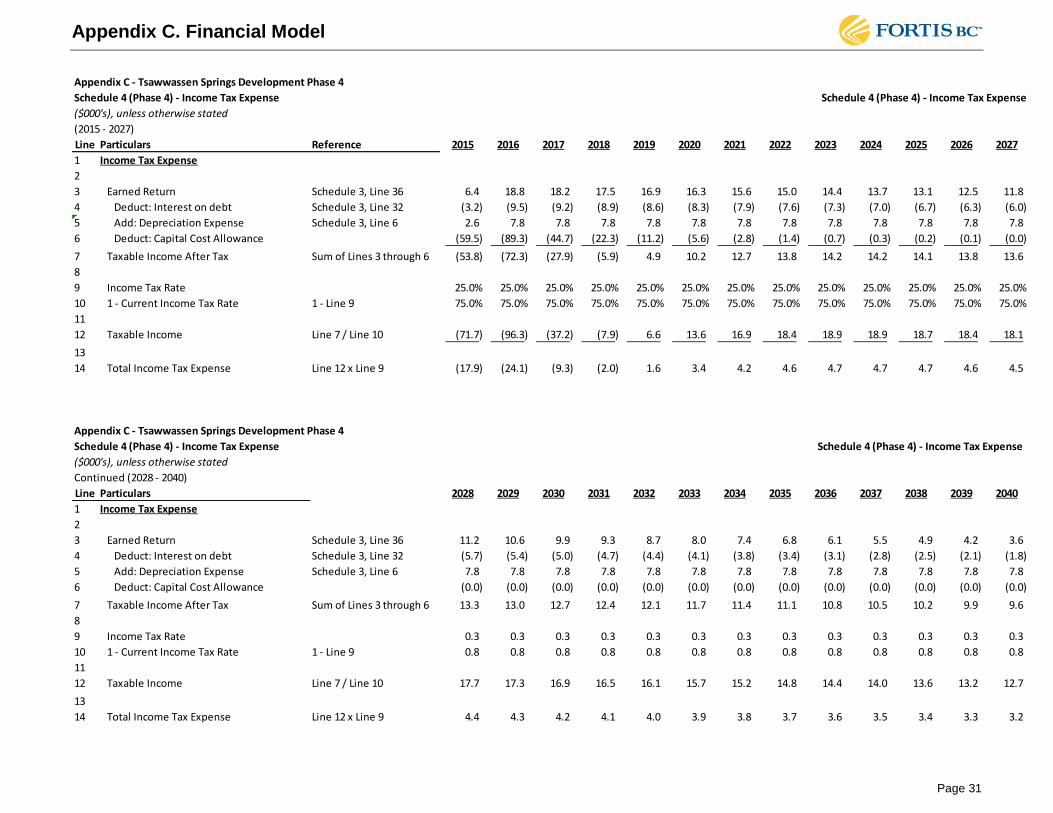

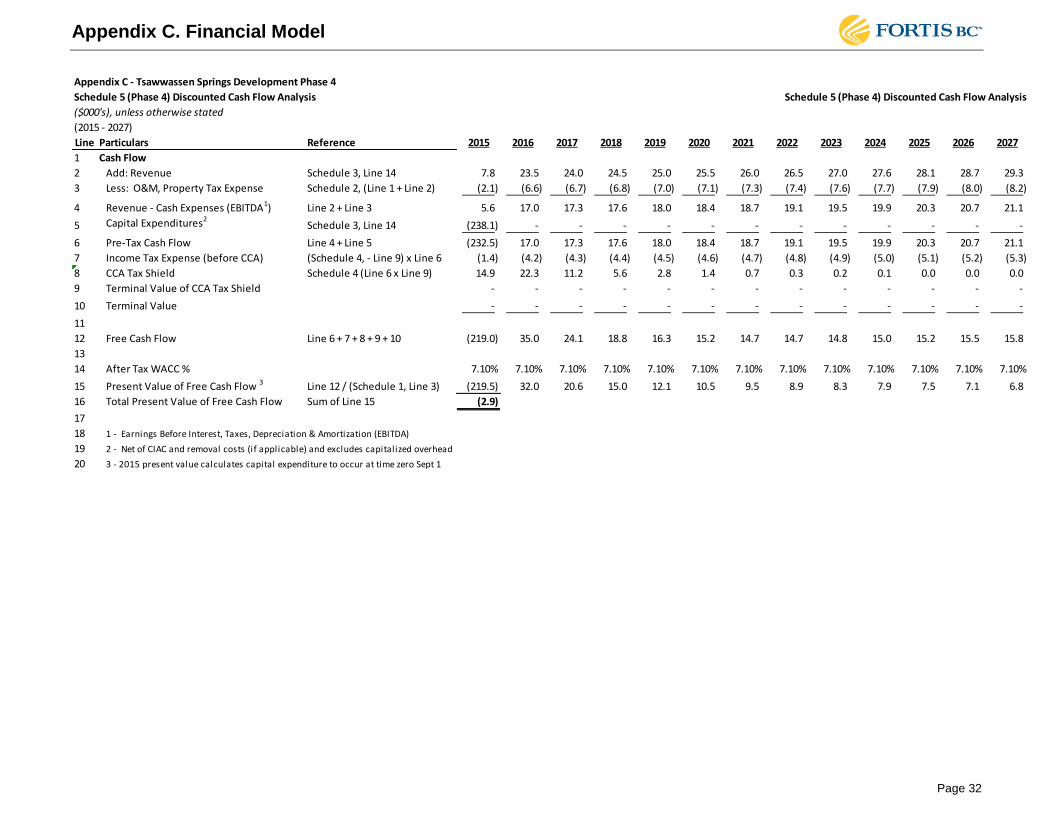

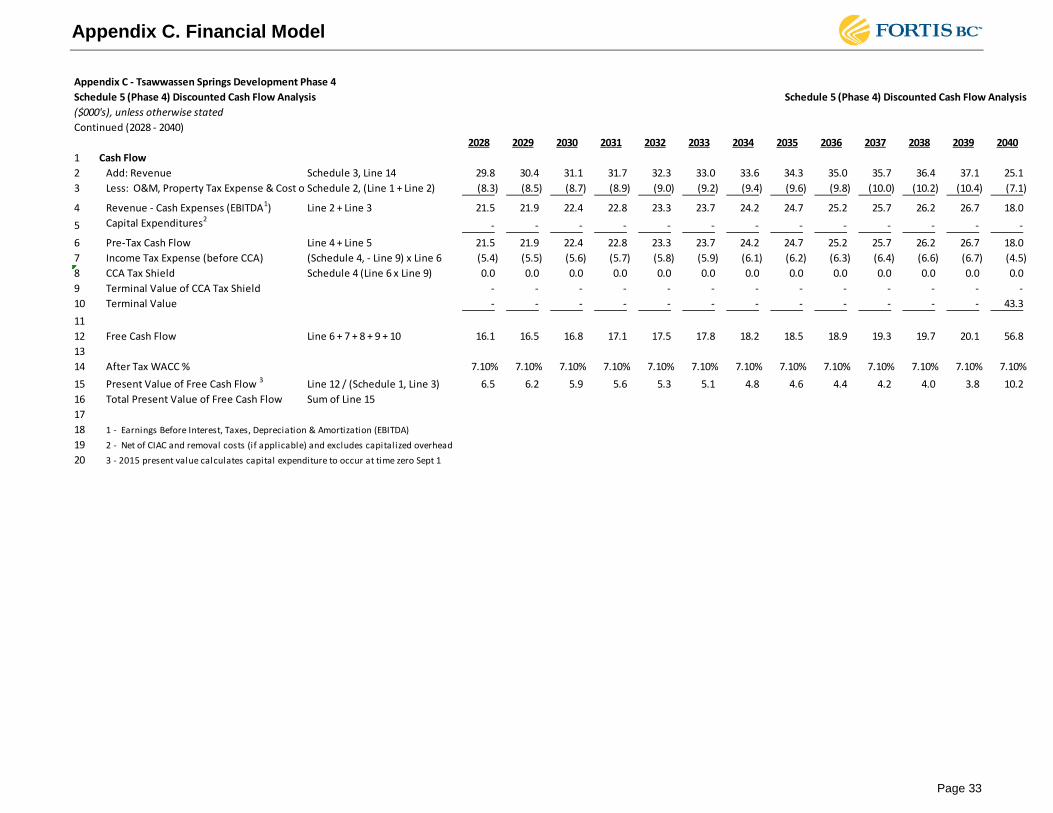

Appendix C List of Schedules Phase 1 - Start Sept 1, 2011 Schedule 1 (Phase 1) - Rate Design & Thermal Energy Services Deferral Sub Account Schedule 2 (Phase 1) - Revenue Requirement Schedule 3 (Phase 1) - Rate Base Schedule 4 (Phase 1) - Income Tax Expense Schedule 5 (Phase 1) - Discounted Cash Flow Analysis Phase 2 – Start Sept 1, 2013 Schedule 1 (Phase 2) - Rate Design & Thermal Energy Services Deferral Sub Account Schedule 2 (Phase 2) - Revenue Requirement Schedule 3 (Phase 2) - Rate Base Schedule 4 (Phase 2) - Income Tax Expense Schedule 5 (Phase 2) - Discounted Cash Flow Analysis Phase 3 – Start Sept 1, 2014 Schedule 1 (Phase 3) - Rate Design & Thermal Energy Services Deferral Sub Account Schedule 2 (Phase 3) - Revenue Requirement Schedule 3 (Phase 3) - Rate Base Schedule 4 (Phase 3) - Income Tax Expense Schedule 5 (Phase 3) - Discounted Cash Flow Analysis Phase 4 – Start Sept 1, 2015 Schedule 1 (Phase 4) - Rate Design & Thermal Energy Services Deferral Sub Account Schedule 2 (Phase 4) - Revenue Requirement Schedule 3 (Phase 4) - Rate Base Schedule 4 (Phase 4) - Income Tax Expense Schedule 5 (Phase 4) - Discounted Cash Flow Analysis

Appendix C. Financial Model

Page 2

Appendix C - Tsawwassen Springs Development Phase 1

Schedule 1 (Phase 1) - Rate Design & Thermal Energy Services Deferral Sub Account Schedule 1 (Phase 1) - Rate Design & Thermal Energy Services Deferral Sub Account

($000's), unless otherwise stated

(2011 - 2023)

Line Particulars Reference 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

1 Annual Contract Revenue starting Sept 1, 2011121.6 22.0 22.5 22.9 23.4 23.8 24.3 24.8 25.3 25.8 26.3 26.9 27.4

2 Annual Discount Rate (After-Tax WACC) 7.04% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10%

3 Cummulative Discount Factor51.023 1.096 1.174 1.257 1.346 1.442 1.544 1.654 1.771 1.897 2.032 2.176 2.330

4 Annual Contract Revenue based on Calendar Year47.2 21.7 22.2 22.6 23.1 23.5 24.0 24.5 25.0 25.5 26.0 26.5 27.0

5 PV of Annual Contract Revenue Line 4 / Line 3 7.0 19.8 18.9 18.0 17.1 16.3 15.5 14.8 14.1 13.4 12.8 12.2 11.6

6 PV of Total Revenue Collected Sum Line 5 2997

8 Annual Cost of Service3 (Calendar Year) Schedule 2, Line 8 (7.6) 8.5 21.7 28.0 30.9 32.0 32.4 32.2 31.9 31.5 31.0 30.5 30.0

9 PV of Annual Cost of Service Line 8 / Line 3 (7.4) 7.7 18.5 22.3 22.9 22.2 21.0 19.5 18.0 16.6 15.3 14.0 12.9

10 PV of Total Cost of Service Sum Line 9 29911

12 Annual Difference Line 8 - Line 4 (14.8) (13.3) (0.5) 5.4 7.8 8.5 8.3 7.8 6.9 6.0 5.0 4.0 2.9 13

14 Total Annual Revenue Line 4 7.2 21.7 22.2 22.6 23.1 23.5 24.0 24.5 25.0 25.5 26.0 26.5 27.0

15

16 Thermal Energy Services Deferral Sub Account17 Contract Revenue — Cost of Service Line 4 - Line 8 14.8 13.3 0.5 (5.4) (7.8) (8.5) (8.3) (7.8) (6.9) (6.0) (5.0) (4.0) (2.9)

18 Deferred Charge

19 Opening Balance Line 28 previous year - (11.3) (22.2) (24.1) (21.8) (17.4) (12.1) (6.6) (1.2) 4.0 8.9 13.3 17.3

20 Gross Addition - Line 17 (14.8) (13.3) (0.5) 5.4 7.8 8.5 8.3 7.8 6.9 6.0 5.0 4.0 2.9

21 Income Tax Rate 26.5% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0%

22 Tax - Line 20 x Line 21 3.9 3.5 0.1 (1.4) (2.1) (2.3) (2.2) (2.1) (1.8) (1.6) (1.3) (1.1) (0.8)

23 Net Addition Line 20 + Line 22 (10.9) (9.7) (0.4) 3.9 5.7 6.3 6.1 5.7 5.1 4.4 3.7 2.9 2.2

24 AFUDC

25 Equity7 (0.2) (0.6) (0.9) (0.9) (0.8) (0.6) (0.4) (0.2) 0.1 0.2 0.4 0.6 0.7

26 Debt6(0.2) (0.5) (0.7) (0.7) (0.6) (0.4) (0.3) (0.1) 0.0 0.2 0.3 0.5 0.6

27

28 Closing Balance Line 19 + 23 + 26 (11.3) (22.2) (24.1) (21.8) (17.4) (12.1) (6.6) (1.2) 4.0 8.9 13.3 17.3 20.7

29 1 - Contract Revenue based on Phase 1 monthly fee of $1,800 or $21,600 per year; Inflated at 2% / yr beginning Sept 1, 2012

30 3 - Cost of Service = Revenue Requirement

31 4 - Calendar year adjustment of contract revenue, 4 months of current year + 8 months of previous year

32 5 - (1 + Line 2) * previous year discount factor, 2011 discount factor based on 4 months (1+7.04% * 4/12)

33 6 - (Line 19 + Line 23/2) * ((Schedule 3, Line 23 * Line 24) + (Schedule 3, Line 28 * Line 29) * (1 - Line 21))

34 7 - (Line 19 + Line 23/2) * (Schedule 3, Line 18 * Line 19)

Appendix C. Financial Model

Page 3

Appendix C - Tsawwassen Springs Development Phase 1

Schedule 1 (Phase 1) - Rate Design & Thermal Energy Services Deferral Sub Account Schedule 1 (Phase 1) - Rate Design & Thermal Energy Services Deferral Sub Account

($000's), unless otherwise stated

Continued (2024 - 2036)

Line Particulars 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036

1 Annual Contract Revenue starting Sept 1, 20111 27.9 28.5 29.1 29.7 30.2 30.9 31.5 32.1 32.7 33.4 34.1 34.7 0.0

2 Annual Discount Rate (After-Tax WACC) 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10%

3 Cummulative Discount Factor,5 2.496 2.673 2.863 3.066 3.283 3.516 3.766 4.033 4.320 4.626 4.954 5.306 5.557

4 Annual Contract Revenue based on Calendar Year4 27.6 28.1 28.7 29.3 29.8 30.4 31.1 31.7 32.3 33.0 33.6 34.3 23.2

5 PV of Annual Contract Revenue Line 4 / Line 3 11.0 10.5 10.0 9.5 9.1 8.7 8.2 7.9 7.5 7.1 6.8 6.5 4.2

6 PV of Total Revenue Collected Sum Line 57

8 Annual Cost of Service3 (Calendar Year) Schedule 2, Line 8 29.5 28.9 28.4 27.9 27.4 26.9 26.4 25.9 25.4 24.9 24.4 23.9 20.1

9 PV of Annual Cost of Service Line 8 / Line 3 11.8 10.8 9.9 9.1 8.3 7.6 7.0 6.4 5.9 5.4 4.9 4.5 3.6

10 PV of Total Cost of Service Sum Line 911

12 Annual Difference Line 8 - Line 4 1.9 0.8 (0.3) (1.4) (2.5) (3.6) (4.7) (5.8) (7.0) (8.1) (9.3) (10.4) (3.1) 13

14 Total Annual Revenue Line 4 27.6 28.1 28.7 29.3 29.8 30.4 31.1 31.7 32.3 33.0 33.6 34.3 23.2

15

16 Thermal Energy Services Deferral Sub Account

17 Contract Revenue — Cost of Service Line 4 - Line 8 (1.9) (0.8) 0.3 1.4 2.5 3.6 4.7 5.8 7.0 8.1 9.3 10.4 3.1

18 Deferred Charge

19 Opening Balance Line 28 previous year 20.7 23.6 25.9 27.6 28.5 28.6 27.9 26.3 23.8 20.1 15.4 9.5 2.2

20 Gross Addition - Line 17 1.9 0.8 (0.3) (1.4) (2.5) (3.6) (4.7) (5.8) (7.0) (8.1) (9.3) (10.4) (3.1)

21 Income Tax Rate 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0%

22 Tax - Line 20 x Line 21 (0.5) (0.2) 0.1 0.4 0.7 0.9 1.2 1.5 1.8 2.1 2.5 2.8 0.8

23 Net Addition Line 20 + Line 22 1.4 0.6 (0.2) (1.0) (1.8) (2.6) (3.5) (4.3) (5.1) (6.0) (6.8) (7.7) (2.3)

24 AFUDC 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

25 Equity7 0.9 1.0 1.0 1.1 1.1 1.1 1.0 1.0 0.8 0.7 0.5 0.2 0.0

26 Debt60.7 0.7 0.8 0.8 0.9 0.8 0.8 0.7 0.7 0.5 0.4 0.2 0.0

27

28 Closing Balance Line 19 + 23 + 26 23.6 25.9 27.6 28.5 28.6 27.9 26.3 23.8 20.1 15.4 9.5 2.2 (0.0)

29 1 - Contract Revenue based on Phase 1 monthly fee of $1,800 or $21,600 per year; Inflated at 2% / yr beginning Sept 1, 2012

30 3 - Cost of Service = Revenue Requirement

31 4 - Calendar year adjustment of contract revenue, 4 months of current year + 8 months of previous year

32 5 - (1 + Line 2) * previous year discount factor, 2011 discount factor based on 4 months (1+7.04% * 4/12)

33 6 - (Line 19 + Line 23/2) * ((Schedule 3, Line 23 * Line 24) + (Schedule 3, Line 28 * Line 29) * (1 - Line 21))

34 7 - (Line 19 + Line 23/2) * (Schedule 3, Line 18 * Line 19)

Appendix C. Financial Model

Page 4

Appendix C - Tsawwassen Springs Development Phase 1

Schedule 2 (Phase 1) - Revenue Requirement Schedule 2 (Phase 1) - Revenue Requirement

($000's), unless otherwise stated(2011 - 2023)

Line Particulars Reference 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

1 Revenue Requirement1

2 Operation and Maintenance 2.0 6.2 6.3 6.4 6.5 6.7 6.8 6.9 7.1 7.2 7.4 7.5 7.7

3 Property Taxes 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

4 Depreciation Expense Schedule 3, Line 6 2.4 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2

5 Income Taxes Schedule 4, Line 14 (17.9) (22.3) (8.6) (1.8) 1.5 3.1 3.9 4.2 4.4 4.4 4.3 4.3 4.2

6 Earned Return Schedule 3, Line 36 5.9 17.4 16.8 16.2 15.6 15.0 14.4 13.8 13.3 12.7 12.1 11.5 10.97

8 Annual Revenue Requirement (7.6) 8.5 21.7 28.0 30.9 32.0 32.4 32.2 31.9 31.5 31.0 30.5 30.0

9 1-Revenue Requirement=Cost of Service

Appendix C - Tsawwassen Springs Development Phase 1

Schedule 2 (Phase 1) - Revenue Requirement

($000's), unless otherwise stated

Continued (2024 - 2036)

Line Particulars 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036

1 Revenue Requirement1

2 Operation and Maintenance 7.8 8.0 8.1 8.3 8.5 8.6 8.8 9.0 9.2 9.4 9.5 9.7 6.6

3 Property Taxes 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

4 Depreciation Expense Schedule 3, Line 6 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2

5 Income Taxes Schedule 4, Line 14 4.1 4.0 3.9 3.8 3.7 3.6 3.5 3.4 3.3 3.2 3.1 3.0 2.9

6 Earned Return Schedule 3, Line 36 10.3 9.8 9.2 8.6 8.0 7.4 6.8 6.2 5.7 5.1 4.5 3.9 3.3

7

8 Annual Revenue Requirement 29.5 28.9 28.4 27.9 27.4 26.9 26.4 25.9 25.4 24.9 24.4 23.9 20.1

9 1-Revenue Requirement=Cost of Service

Appendix C. Financial Model

Page 5

Appendix C - Tsawwassen Springs Development Phase 1

Schedule 3 (Phase 1) - Rate Base Schedule 3 (Phase 1) - Rate Base

($000's), unless otherwise stated

(2011 - 2023)

Line Particulars Reference 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

1 Rate Base

2 Gross Plant In Service- Beginning - 220 220 220 220 220 220 220 220 220 220 220 220

3 Gross Plant In Service- Ending 220 220 220 220 220 220 220 220 220 220 220 220 220 4

5 Accumulated Depreciation- Beginning - (2) (10) (17) (24) (31) (38) (46) (53) (60) (67) (74) (82)

6 Depreciation Expense (Loop Field @ 4%) (2) (7) (7) (7) (7) (7) (7) (7) (7) (7) (7) (7) (7)

7 Accumulated Depreciation- Ending (2) (10) (17) (24) (31) (38) (46) (53) (60) (67) (74) (82) (89) 8

9 Net Plant in Service, Mid-Year Sum (Lines 2 through 7 )/2 109 214 207 200 192 185 178 171 164 156 149 142 135

10

11 Adjustment to 13-month average (36) - - - - - - - - - - - -

12 Total Rate Base Line 9 + Line 11 72 214 206 199 192 185 178 170 163 156 149 142 134

13

14 Gross Plant Additions 220 - - - - - - - - - - - -

15

16 Return on Rate Base

17 Total Rate Base Line 12 72 214 206 199 192 185 178 170 163 156 149 142 134

18 ROE Rate 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00%

19 Equity Ratio 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00%

20 Equity Return Line 17 x Line 18 x Line 19 3 9 8 8 8 7 7 7 7 6 6 6 5

21

22 Total Rate Base Line 12 72 214 206 199 192 185 178 170 163 156 149 142 134

23 Short Term Debt Rate 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50%

24 Short Term Debt Ratio 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63%

25 Short Term Debt Component Line 22 x Line 23 x Line 24 0 0 0 0 0 0 0 0 0 0 0 0 0

26

27 Total Rate Base Line 12 72 214 206 199 192 185 178 170 163 156 149 142 134

28 Long Term Debt Rate 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95%

29 Long Term Debt Ratio 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37%

30 Long Term Debt Component Line 27 x Line 28 x Line 29 3 9 8 8 8 7 7 7 7 6 6 6 5

31

32 Total Debt Component Line 25 + Line 30 3 9 9 8 8 8 7 7 7 6 6 6 6 33

34 Equity Return Line 20 3 9 8 8 8 7 7 7 7 6 6 6 5

35 Total Debt Component Line 32 3 9 9 8 8 8 7 7 7 6 6 6 6

36 Total Earned Return Line 34 + Line 35 6 17 17 16 16 15 14 14 13 13 12 12 11

37 Return on AES Rate Base % Line 36 / Line 12 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13%

Appendix C. Financial Model

Page 6

Appendix C - Tsawwassen Springs Development Phase 1

Schedule 3 (Phase 1) - Rate Base Schedule 3 (Phase 1) - Rate Base

($000's), unless otherwise stated

Continued (2024 - 2036)

Line Particulars 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036

1 Rate Base

2 Gross Plant In Service- Beginning 220 220 220 220 220 220 220 220 220 220 220 220 220

3 Gross Plant In Service- Ending 220 220 220 220 220 220 220 220 220 220 220 220 220 4

5 Accumulated Depreciation- Beginning (89) (96) (103) (110) (118) (125) (132) (139) (146) (154) (161) (168) (175)

6 Depreciation Expense (Loop Field @ 4%) (7) (7) (7) (7) (7) (7) (7) (7) (7) (7) (7) (7) (7)

7 Accumulated Depreciation- Ending (96) (103) (110) (118) (125) (132) (139) (146) (154) (161) (168) (175) (182) 8

9 Net Plant in Service, Mid-Year Sum (Lines 2 through 7 )/2 128 120 113 106 99 92 84 77 70 63 56 48 41 10

11 Cash Working Capital (0) (0) (0) (0) (0) (0) (0) (0) (0) (0) (0) (0) (0)

12 Total Rate Base Line 9 + Line 11 127 120 113 106 98 91 84 77 70 62 55 48 41 13

14 Gross Plant Additions - - - - - - - - - - - - - 15

16 Return on Rate Base

17 Total Rate Base Line 12 127 120 113 106 98 91 84 77 70 62 55 48 41

18 ROE Rate 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00% 10.00%

19 Equity Ratio 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 40.00%

20 Equity Return Line 17 x Line 18 x Line 19 5 5 5 4 4 4 3 3 3 2 2 2 2

21

22 Total Rate Base Line 12 127 120 113 106 98 91 84 77 70 62 55 48 41

23 Short Term Debt Rate 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50% 4.50%

24 Short Term Debt Ratio 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63% 1.63%

25 Short Term Debt Component Line 22 x Line 23 x Line 24 0 0 0 0 0 0 0 0 0 0 0 0 0

26

27 Total Rate Base Line 12 127 120 113 106 98 91 84 77 70 62 55 48 41

28 Long Term Debt Rate 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95% 6.95%

29 Long Term Debt Ratio 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37% 58.37%

30 Long Term Debt Component Line 27 x Line 28 x Line 29 5 5 5 4 4 4 3 3 3 3 2 2 2

31

32 Total Debt Component Line 25 + Line 30 5 5 5 4 4 4 3 3 3 3 2 2 2

33

34 Equity Return Line 20 5 5 5 4 4 4 3 3 3 2 2 2 2

35 Total Debt Component Line 32 5 5 5 4 4 4 3 3 3 3 2 2 2

36 Total Earned Return Line 34 + Line 35 10 10 9 9 8 7 7 6 6 5 4 4 3

37 Return on AES Rate Base % Line 36 / Line 12 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13% 8.13%

Appendix C. Financial Model

Page 7

Appendix C - Tsawwassen Springs Development Phase 1

Schedule 4 (Phase 1) - Income Tax Expense Schedule 4 (Phase 1) - Income Tax Expense

($000's), unless otherwise stated

(2011 - 2023)

Line Particulars Reference 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

1 Income Tax Expense

2

3 Earned Return Schedule 3, Line 36 5.9 17.4 16.8 16.2 15.6 15.0 14.4 13.8 13.3 12.7 12.1 11.5 10.9

4 Deduct: Interest on debt Schedule 3, Line 32 (3.0) (8.8) (8.5) (8.2) (7.9) (7.6) (7.3) (7.0) (6.7) (6.4) (6.1) (5.8) (5.5)

5 Add: Depreciation Expense Schedule 3, Line 6 2.4 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2

6 Deduct: Capital Cost Allowance (55.0) (82.5) (41.3) (20.6) (10.3) (5.2) (2.6) (1.3) (0.6) (0.3) (0.2) (0.1) (0.0)

7 Taxable Income After Tax Sum of Lines 3 through 6 (49.7) (66.8) (25.8) (5.5) 4.6 9.4 11.7 12.7 13.1 13.1 13.0 12.8 12.5

8

9 Income Tax Rate 26.5% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0%

10 1 - Current Income Tax Rate 1 - Line 9 73.5% 75.0% 75.0% 75.0% 75.0% 75.0% 75.0% 75.0% 75.0% 75.0% 75.0% 75.0% 75.0%

11

12 Taxable Income Line 7 / Line 10 (67.6) (89.0) (34.4) (7.3) 6.1 12.6 15.6 17.0 17.4 17.5 17.3 17.0 16.7

13

14 Total Income Tax Expense Line 12 x Line 9 (17.9) (22.3) (8.6) (1.8) 1.5 3.1 3.9 4.2 4.4 4.4 4.3 4.3 4.2

Appendix C - Tsawwassen Springs Development Phase 1

Schedule 4 (Phase 1) - Income Tax Expense Schedule 4 (Phase 1) - Income Tax Expense

($000's), unless otherwise stated

Continued (2024 - 2036)

Line Particulars 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036

1 Income Tax Expense

2

3 Earned Return Schedule 3, Line 36 10.3 9.8 9.2 8.6 8.0 7.4 6.8 6.2 5.7 5.1 4.5 3.9 3.3

4 Deduct: Interest on debt Schedule 3, Line 32 (5.3) (5.0) (4.7) (4.4) (4.1) (3.8) (3.5) (3.2) (2.9) (2.6) (2.3) (2.0) (1.7)

5 Add: Depreciation Expense Schedule 3, Line 6 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2 7.2

6 Deduct: Capital Cost Allowance (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.0)

7 Taxable Income After Tax Sum of Lines 3 through 6 12.3 12.0 11.7 11.4 11.1 10.8 10.6 10.3 10.0 9.7 9.4 9.1 8.8

8

9 Income Tax Rate 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3

10 1 - Current Income Tax Rate 1 - Line 9 0.8 0.8 0.8 0.8 0.8 0.8 0.8 0.8 0.8 0.8 0.8 0.8 0.8

11

12 Taxable Income Line 7 / Line 10 16.4 16.0 15.6 15.2 14.8 14.5 14.1 13.7 13.3 12.9 12.5 12.2 11.8

13

14 Total Income Tax Expense Line 12 x Line 9 4.1 4.0 3.9 3.8 3.7 3.6 3.5 3.4 3.3 3.2 3.1 3.0 2.9

Appendix C. Financial Model

Page 8

Appendix C - Tsawwassen Springs Development Phase 1

Schedule 5 (Phase 1) Discounted Cash Flow Analysis Schedule 5 (Phase 1) Discounted Cash Flow Analysis

($000's), unless otherwise stated

(2011 - 2023)

Line Particulars Reference 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

1 Cash Flow

2 Add: Revenue Schedule 1, Line 14 7.2 21.7 22.2 22.6 23.1 23.5 24.0 24.5 25.0 25.5 26.0 26.5 27.0

3 Less: O&M Schedule 2, (Line 2) (2.0) (6.2) (6.3) (6.4) (6.5) (6.7) (6.8) (6.9) (7.1) (7.2) (7.4) (7.5) (7.7)

4 Revenue - Cash Expenses (EBITDA1) Line 2 + Line 3 5.2 15.6 15.9 16.2 16.5 16.9 17.2 17.5 17.9 18.2 18.6 19.0 19.4

5 Capital Expenditures2Schedule 3, Line 14 (220.0) - - - - - - - - - - - -

6 Pre-Tax Cash Flow Line 4 + Line 5 (214.8) 15.6 15.9 16.2 16.5 16.9 17.2 17.5 17.9 18.2 18.6 19.0 19.4

7 Income Tax Expense (before CCA) (Schedule 4, - Line 9) x Line 4 (1.4) (3.9) (4.0) (4.1) (4.1) (4.2) (4.3) (4.4) (4.5) (4.6) (4.7) (4.7) (4.8)

8 CCA Tax Shield Schedule 4 (Line 6 x Line 9) 14.6 20.6 10.3 5.2 2.6 1.3 0.6 0.3 0.2 0.1 0.0 0.0 0.0

9 Terminal Value of CCA Tax Shield - - - - - - - - - - - - -

10 Terminal Value - - - - - - - - - - - - -

11

12 Free Cash Flow Line 6 + 7 + 8 + 9 + 10 (201.6) 32.3 22.2 17.3 15.0 13.9 13.5 13.5 13.6 13.8 14.0 14.3 14.5

13

14 After Tax WACC % 7.04% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10%

15 Present Value of Free Cash Flow 3 Line 12 / (Schedule 1, Line 3) (202.0) 29.5 18.9 13.8 11.1 9.7 8.8 8.1 7.7 7.3 6.9 6.6 6.2

16 Total Present Value of Free Cash Flow Sum of Line 15 (2.9)

17

18 1 - Earnings Before Interest, Taxes, Depreciation & Amortization (EBITDA)

19 2 - Net of CIAC and removal costs (if applicable) and excludes capitalized overhead

20 3 - 2011 present value calculates capital expenditure to occur at time zero Sept 1

Appendix C. Financial Model

Page 9

Appendix C - Tsawwassen Springs Development Phase 1

Schedule 5 (Phase 1) Discounted Cash Flow Analysis Schedule 5 (Phase 1) Discounted Cash Flow Analysis

($000's), unless otherwise stated

Continued (2024 - 2036)

2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036

1 Cash Flow

2 Add: Revenue Schedule 1, Line 14 27.6 28.1 28.7 29.3 29.8 30.4 31.1 31.7 32.3 33.0 33.6 34.3 23.2

3 Less: O&M Schedule 2, (Line 2) (7.8) (8.0) (8.1) (8.3) (8.5) (8.6) (8.8) (9.0) (9.2) (9.4) (9.5) (9.7) (6.6)

4 Revenue - Cash Expenses (EBITDA1) Line 2 + Line 3 19.8 20.1 20.5 21.0 21.4 21.8 22.2 22.7 23.1 23.6 24.1 24.6 16.5

5 Capital Expenditures2- - - - - - - - - - - - -

6 Pre-Tax Cash Flow Line 4 + Line 5 19.8 20.1 20.5 21.0 21.4 21.8 22.2 22.7 23.1 23.6 24.1 24.6 16.5

7 Income Tax Expense (before CCA) (Schedule 4, - Line 9) x Line 4 (4.9) (5.0) (5.1) (5.2) (5.3) (5.5) (5.6) (5.7) (5.8) (5.9) (6.0) (6.1) (4.1)

8 CCA Tax Shield Schedule 4 (Line 6 x Line 9) 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

9 Terminal Value of CCA Tax Shield - - - - - - - - - - - - -

10 Terminal Value - - - - - - - - - - - - 40.0

11

12 Free Cash Flow Line 6 + 7 + 8 + 9 + 10 14.8 15.1 15.4 15.7 16.0 16.4 16.7 17.0 17.4 17.7 18.1 18.4 52.4

13

14 After Tax WACC % 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10%

15 Present Value of Free Cash Flow 3 Line 12 / (Schedule 1, Line 3) 5.9 5.7 5.4 5.1 4.9 4.7 4.4 4.2 4.0 3.8 3.6 3.5 9.4

16 Total Present Value of Free Cash Flow Sum of Line 15

17

18 1 - Earnings Before Interest, Taxes, Depreciation & Amortization (EBITDA)

19 2 - Net of CIAC and removal costs (if applicable) and excludes capitalized overhead

20 3 - 2011 present value calculates capital expenditure to occur at time zero Sept 1

Appendix C. Financial Model

Page 10

Appendix C - Tsawwassen Springs Development Phase 2

Schedule 1 (Phase 2) - Rate Design & Thermal Energy Services Deferral Sub Account Schedule 1 (Phase 2) - Rate Design & Thermal Energy Services Deferral Sub Account

($000's), unless otherwise stated

(2013 - 2025)

Line Particulars Reference 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

1 Annual Contract Revenue starting Sept 1, 2013135.0 35.7 36.4 37.1 37.8 38.6 39.4 40.2 41.0 41.8 42.6 43.5 44.3 45.2

2 Annual Discount Rate (After-Tax WACC) 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10%

3 Cummulative Discount Factor51.024 1.096 1.174 1.257 1.347 1.442 1.545 1.654 1.772 1.897 2.032 2.176 2.331 2.496

4 Annual Contract Revenue based on Calendar Year411.7 35.2 35.9 36.6 37.3 38.1 38.9 39.6 40.4 41.2 42.1 42.9 43.8 44.6

5 PV of Annual Contract Revenue Line 4 / Line 3 11.4 32.1 30.6 29.1 27.7 26.4 25.2 24.0 22.8 21.7 20.7 19.7 18.8 17.9

6 PV of Total Revenue Collected Sum Line 5 483

7

8 Annual Cost of Service3 (Calendar Year) Schedule 2, Line 8 (12.1) 11.7 34.8 45.9 50.9 52.9 53.3 53.1 52.4 51.6 50.7 49.7 48.7 47.7

9 PV of Annual Cost of Service Line 8 / Line 3 (11.8) 10.7 29.7 36.5 37.8 36.7 34.5 32.1 29.6 27.2 24.9 22.8 20.9 19.1

10 PV of Total Cost of Service Sum Line 9 483

11

12 Annual Difference Line 8 - Line 4 (23.7) (23.5) (1.1) 9.3 13.5 14.8 14.5 13.4 12.0 10.4 8.6 6.8 5.0 3.1

13

14 Total Annual Revenue Line 4 11.7 35.2 35.9 36.6 37.3 38.1 38.9 39.6 40.4 41.2 42.1 42.9 43.8 44.6 15

16 Thermal Energy Services Deferral Sub Account17 Contract Revenue — Cost of Service Line 4 - Line 8 23.7 23.5 1.1 (9.3) (13.5) (14.8) (14.5) (13.4) (12.0) (10.4) (8.6) (6.8) (5.0) (3.1)

18 Deferred Charge

19 Opening Balance Line 28 previous year - (18.4) (38.0) (41.5) (37.2) (29.4) (20.0) (10.1) (0.4) 8.9 17.5 25.5 32.6 38.7

20 Gross Addition - Line 17 (23.7) (23.5) (1.1) 9.3 13.5 14.8 14.5 13.4 12.0 10.4 8.6 6.8 5.0 3.1

21 Income Tax Rate 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0%

22 Tax - Line 20 x Line 21 5.9 5.9 0.3 (2.3) (3.4) (3.7) (3.6) (3.4) (3.0) (2.6) (2.2) (1.7) (1.2) (0.8)

23 Net Addition Line 20 + Line 22 (17.8) (17.6) (0.8) 6.9 10.2 11.1 10.9 10.1 9.0 7.8 6.5 5.1 3.7 2.3

24 AFUDC

25 Equity7 (0.4) (1.1) (1.5) (1.5) (1.3) (1.0) (0.6) (0.2) 0.2 0.5 0.8 1.1 1.4 1.6

26 Debt6(0.3) (0.8) (1.2) (1.2) (1.0) (0.7) (0.5) (0.2) 0.1 0.4 0.6 0.9 1.1 1.2

27

28 Closing Balance Line 19 + 23 + 26 (18.4) (38.0) (41.5) (37.2) (29.4) (20.0) (10.1) (0.4) 8.9 17.5 25.5 32.6 38.7 43.9

29 1 - Contract Revenue based on Phase 2 monthly fee of $2,800 or $33,600 per year; Inflated at 2% / yr beginning Sept 1, 2012

30 3 - Cost of Service = Revenue Requirement

31 4 - Calendar year adjustment of contract revenue, 4 months of current year + 8 months of previous year

32 5 - (1 + Line 2) * previous year discount factor, 2013 discount factor based on 4 months (1+7.10% * 4/12)

33 6 - (Line 19 + Line 23/2) * ((Schedule 3, Line 23 * Line 24) + (Schedule 3, Line 28 * Line 29) * (1 - Line 21))

34 7 - (Line 19 + Line 23/2) * (Schedule 3, Line 18 * Line 19)

Appendix C. Financial Model

Page 11

Appendix C - Tsawwassen Springs Development Phase 2

Schedule 1 (Phase 2) - Rate Design & Thermal Energy Services Deferral Sub Account Schedule 1 (Phase 2) - Rate Design & Thermal Energy Services Deferral Sub Account

($000's), unless otherwise stated

Continued (2026 - 2038)

Line Particulars 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038

1 Annual Contract Revenue starting Sept 1, 20131 45.2 46.1 47.0 48.0 48.9 49.9 50.9 51.9 53.0 54.0 55.1 56.2 0.0

2 Annual Discount Rate (After-Tax WACC) 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10% 7.10%

3 Cummulative Discount Factor5 2.496 2.673 2.863 3.066 3.284 3.517 3.767 4.034 4.320 4.627 4.955 5.307 5.558

4 Annual Contract Revenue based on Calendar Year4 44.6 45.5 46.4 47.4 48.3 49.3 50.3 51.3 52.3 53.3 54.4 55.5 37.5

5 PV of Annual Contract Revenue Line 4 / Line 3 17.9 17.0 16.2 15.4 14.7 14.0 13.3 12.7 12.1 11.5 11.0 10.5 6.7

6 PV of Total Revenue Collected Sum Line 5

7

8 Annual Cost of Service3 (Calendar Year) Schedule 2, Line 8 47.7 46.7 45.7 44.7 43.7 42.7 41.8 40.8 39.8 38.8 37.9 36.9 31.9

9 PV of Annual Cost of Service Line 8 / Line 3 19.1 17.5 16.0 14.6 13.3 12.2 11.1 10.1 9.2 8.4 7.6 7.0 5.7

10 PV of Total Cost of Service Sum Line 9

11

12 Annual Difference Line 8 - Line 4 3.1 1.2 (0.7) (2.6) (4.6) (6.5) (8.5) (10.5) (12.5) (14.5) (16.5) (18.6) (5.6)

13

14 Total Annual Revenue Line 4 44.6 45.5 46.4 47.4 48.3 49.3 50.3 51.3 52.3 53.3 54.4 55.5 37.5

15

16 Thermal Energy Services Deferral Sub Account

17 Contract Revenue — Cost of Service Line 4 - Line 8 (3.1) (1.2) 0.7 2.6 4.6 6.5 8.5 10.5 12.5 14.5 16.5 18.6 5.6

18 Deferred Charge

19 Opening Balance Line 28 previous year 38.7 43.9 47.9 50.7 52.3 52.5 51.1 48.1 43.4 36.8 28.1 17.3 4.1

20 Gross Addition - Line 17 3.1 1.2 (0.7) (2.6) (4.6) (6.5) (8.5) (10.5) (12.5) (14.5) (16.5) (18.6) (5.6)

21 Income Tax Rate 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0%

22 Tax - Line 20 x Line 21 (0.8) (0.3) 0.2 0.7 1.1 1.6 2.1 2.6 3.1 3.6 4.1 4.6 1.4

23 Net Addition Line 20 + Line 22 2.3 0.9 (0.5) (2.0) (3.4) (4.9) (6.4) (7.9) (9.4) (10.9) (12.4) (13.9) (4.2)

24 AFUDC 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

25 Equity7 1.6 1.8 1.9 2.0 2.0 2.0 1.9 1.8 1.5 1.3 0.9 0.4 0.1

26 Debt61.2 1.4 1.5 1.5 1.6 1.5 1.5 1.4 1.2 1.0 0.7 0.3 0.1

27

28 Closing Balance Line 19 + 23 + 26 43.9 47.9 50.7 52.3 52.5 51.1 48.1 43.4 36.8 28.1 17.3 4.1 (0.0)

29 1 - Contract Revenue based on Phase 2 monthly fee of $2,800 or $33,600 per year; Inflated at 2% / yr beginning Sept 1, 2012

30 3 - Cost of Service = Revenue Requirement

31 4 - Calendar year adjustment of contract revenue, 4 months of current year + 8 months of previous year

32 5 - (1 + Line 2) * previous year discount factor, 2013 discount factor based on 4 months (1+7.10% * 4/12)

33 6 - (Line 19 + Line 23/2) * ((Schedule 3, Line 23 * Line 24) + (Schedule 3, Line 28 * Line 29) * (1 - Line 21))

34 7 - (Line 19 + Line 23/2) * (Schedule 3, Line 18 * Line 19)

Appendix C. Financial Model

Page 12

Appendix C - Tsawwassen Springs Development Phase 2

Schedule 2 (Phase 2) - Revenue Requirement Schedule 2 (Phase 2) - Revenue Requirement

($000's), unless otherwise stated(2013 - 2025)

Line Particulars Reference 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

1 Revenue Requirement1

2 Operation and Maintenance 2.5 7.6 7.8 7.9 8.1 8.3 8.4 8.6 8.8 9.0 9.1 9.3 9.5

3 Property Taxes 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0