Embed Size (px)

Citation preview

Administering Your Firm's

Retirement Plan in a Changing

Environment

Presented by

Ginger Brennan, FINRA Series 6,7,24,

FM11

4/3/2017

1:45 PM - 2:45 PM

The handouts and presentations attached are copyright and trademark

protected and provided for individual use only.

1

www.abaretirement.comwww.abaretirement.com2017

CN0124-30496-0219D

Administering Your Firm’s Retirement Plan

in a Changing Environment

ABA Retirement Funds Program

Ginger Brennan

Monday, April 3rd | 1:45pm – 2:45pm

2ABA Retirement Funds Program Presentation

Important information

Please read the Program Disclosure Document (April 2016) carefully before

investing. The Program Disclosure Document contains important information

about the Program and investment options. For email inquiries contact us at

Registered representative of and securities offered through Voya Financial

Partners, LLC (Member SIPC).

Voya Financial Partners is a member of the Voya family of companies (“Voya”).

Voya, the ABA Retirement Funds, The Mercer Trust Company, and TD

Ameritrade Inc. are separate, unaffiliated entities, and not responsible for one

another’s products and services.

2

3ABA Retirement Funds Program Presentation

Agenda

Introduction

Benefits and responsibilities of

sponsoring a workplace retirement plan

Plan type selection and responsibilities

Overview of ABA Retirement Funds

Key takeaways Senior Vice President

National Director of

Sales and Marketing

ABA Retirement Funds Program

Registered representative of Voya Financial

Partners, LLC (Member SIPC)

Ginger Brennan

4ABA Retirement Funds Program Presentation

Introduction

The decision to sponsor a workplace retirement plan generates benefits

as well as responsibilities.

Selection of plan type &

features

Selection of providers

Fiduciary role

Administration and

Maintenance

Responsibilities

Pre-tax income directed to a

long-term savings vehicle on a

tax-deferred basis

Attract and retain talented

employees

Do a good thing for your

employees

Employer tax deduction

Benefits

Workplace

Retirement

Plan

3

5ABA Retirement Funds Program Presentation

Tax-deferred, long-term savings

In the example below we show you the retirement plans of Sarah and Adam who saved the same amount monthly but started at different times.

Benefits

25 30 35 40 45 50 55 60 65

Sarah’s 15-year

head start produced

$974,000 more in

savings than Adam.

That’s the power of

starting early.

Sarah starts saving at 25, she invests $1,000 a month for 25 years. At 50 years of age

Sarah stops contributing to her savings and relies only on the power of compounding for

the next 15 years. The result is a retirement nest egg of nearly $1,700,000 at age 65.

Adam decides to put off starting his retirement savings until the age of 40. His total after

25 years of continuous $1,000 a month contributions is nearly $698,000.

Note: This example uses a 6% annual return on investment, and because of the tax deferred

nature of retirement accounts the power of compounding is impactful because there are no

taxes to be paid on interest and dividends that could otherwise deplete assets each year. For

illustration purposes only.

$2M

$1.5M

$1M

$500K

$0

SarahAge 25

Adam retires with$697,876 at age 65

At age 50, Sarah stops contributing and relies only on the power of

compounding for the next 15 years.Sarah retires with

$1,672,501at age 65

AdamAge 40

Sara’s Saving

Adam’s Saving Years

25 35 40 45AGE50 55 65

6ABA Retirement Funds Program Presentation

Attract and retain talented employees

When asked to rank the importance of 11

factors relating to job opportunities, survey

respondents placed salary, benefits (including

health insurance and 401(k) programs) and

opportunities for professional growth and

advancement at the top of the list.1

Companies that emphasize

better benefits and use them to

attract and retain high caliber

staff add 7.3 percent in

additional profit to their

bottom line.2

1Generation Y. What millennial workers want: How to attract and retain Gen Y Employees; Robert Half International and Yahoo! Hotjobs.com, 20082The Human Capital Edge: 21 People Management Practices Your Company Must Implement (or Avoid) to Maximize Shareholder Value; by Bruce N. Pfau, PhD, Ira T. Kay, PhD, Watson

Wyatt Worldwide, 2001

Benefits

4

7ABA Retirement Funds Program Presentation

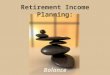

Doing good for your employees Benefits

Pensions have been cut

In 1985, 90% of

companies offered

traditional pensions

plans. By 2012,

that number fell to

just 11%1

In 1998, only 10%

of companies

offered only a DC

plan. This number

is now 70%1

In the legal community

9 out of 10 lawyers are in firms with fewer than

ten attorneys2

Only 17.3% of Companies with fewer

than ten employees sponsor a retirement

plan3

1“Retirement Plan Types of Fortune 100 Companies in 2012,” Towers Watson, Insider October 20122The Lawyer Statistical Report, American Bar Foundation, 2012 edition3Employee Benefit Research Institute estimates from the 2011 March Current Population Survey

8ABA Retirement Funds Program Presentation

Employer tax deduction Benefits

Employer contributions are deductible on

the employer’s federal income tax return

to the extent that the contributions do not

exceed the limitations described in section

404 of the Internal Revenue Code.Refer to Publication 560, Retirement Plans for

Small Business (SEP, SIMPLE, and Qualified

Plans), for more information about deduction

limitations.

You may be able to claim a tax

credit for part of the ordinary and

necessary costs of starting a SEP,

SIMPLE, or qualified plan. The credit equals 50% of the cost to set

up and administer the plan and educate

employees about the plan, up to a

maximum of $500 per year for each of

the first 3 years of the plan.

5

9ABA Retirement Funds Program Presentation

Selection of plan type and features

Pla

n T

yp

es

What type of

plan is right

for your firm?

Defined

Benefit

Cash

Balance

Plan

Money

PurchaseSEP IRA SIMPLE

Pla

n S

tra

teg

ies

What plan

strategy

meets your

objectives?

Safe Harbor

Maximize contributions

while reducing

limitations associated

with testing

Social Sec. Integration

Formula awards higher-

paid employees with a

larger percentage of

their compensation

Cross-tested

Different employee

groups defined and

separate contributions

to each group are made

Pla

n F

eatu

res

What plan

features will

make your

plan unique?

Eligibility & Vesting

Investment Options &

Trading Restrictions

Match &

Match Structure

Distribution & Rollover

Options

Automatic Features &

QDIA

Self-Directed

Brokerage Service

TIPDoes your plan include an advice offering?

TIPIf your strategy is to maximize tax deferred contributions, look into adding a Cash Balance plan to your 401(k)

Profit

Sharing /

401(k)

This example was designed for educational purposes only and is not intended for specific legal, accounting, investment,

income tax or other professional advice. Please note that other plan types, strategies, and features may exist.

Responsibility

10ABA Retirement Funds Program Presentation

Selection of providers

Maintains the participant records; trades the shares when contributions are deposited and when participants reallocate their portfolios; provides the web site and call center for the participants and plan sponsors; and generates and mails the participant statements.

Recordkeeper

Drafts the plan document; performs the compliance testing; and prepares the annual IRS Forms 5500. These tasks are sometimes part of a bundled service provided by a recordkeeper.

Third Party

Administrator

A Bank or Trust Company acts as Custodian; initially accepts the contributions, processes loan-and distribution checks; and prepares tax reporting.Trust Company

Provides advice and guidance on investment selection and allocation to the trustees; may also serve as directed or discretionary trustee; and on rare occasions can take on investment fiduciary role.

Investment

Advisor

Consultant can be used in the request for proposal (“RFP”) process and retained to evaluate the plan’s merits from time to time.Consultants

Provides advice and guidance on investment options to employees participating in the plan; may take on professional asset management role for a fee; may take on fiduciary responsibility for participant in-plan investments.

Advisory Firm

Can advise on plan types, plan features, and plan documents. May also help resolve plan qualification issues or disputes.

ERISA Attorney

While payroll companies offer services unrelated to retirement plans, the link between payroll and participant contributions to qualified plans does require consideration when picking a payroll vendor.

Payroll Company

This example was designed for educational purposes only and is not intended for specific legal, accounting, investment, income tax or other professional advice. Please note that other

plan types, strategies, and features may exist.

Responsibility

6

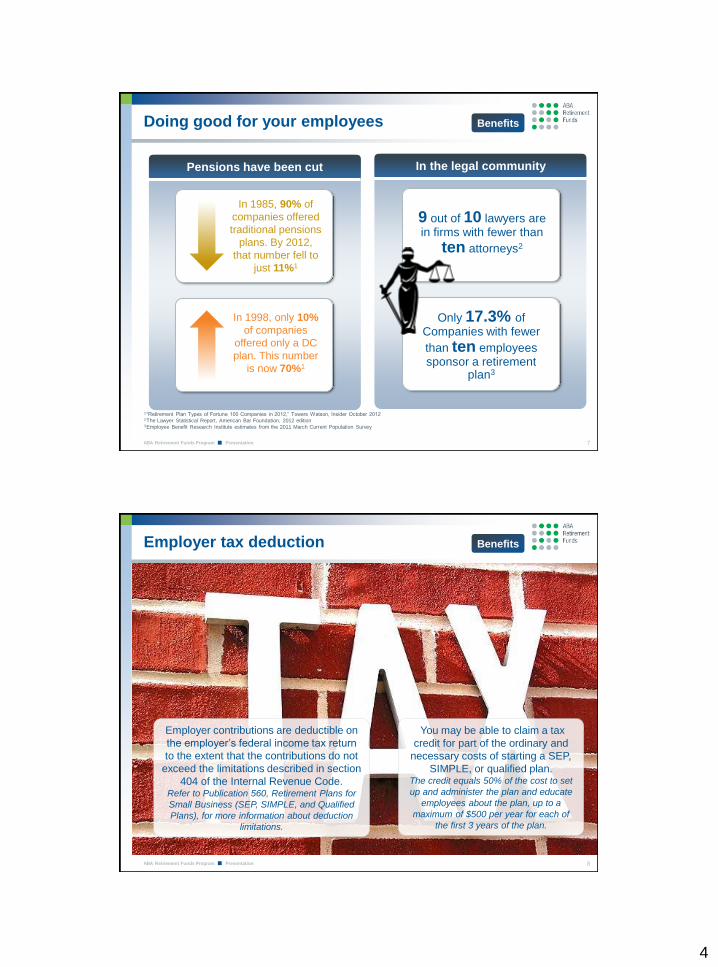

11ABA Retirement Funds Program Presentation

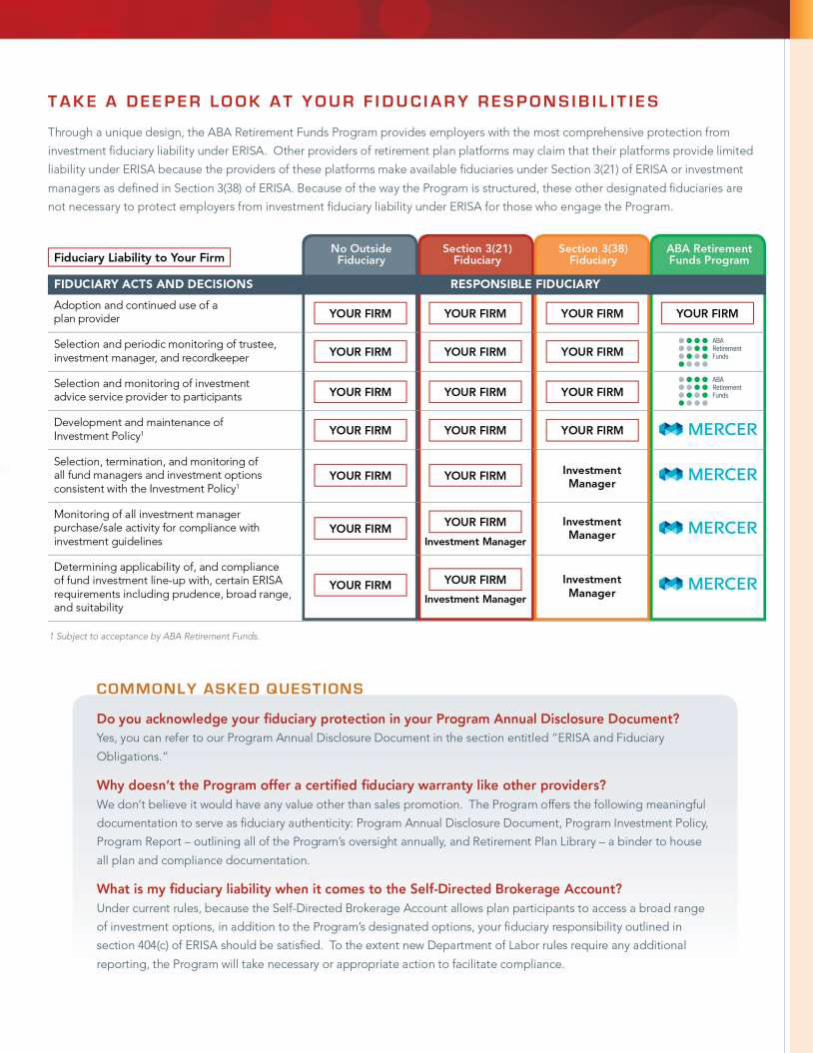

TYPICAL PLAN

TRUSTEE

No Outside

FiduciaryFiduciary Liability to Your Firm

Adoption and continued use of a Plan Provider

Selection and periodic monitoring of trustee,

investment manager, and recordkeeper

Selection and monitoring of investment advice

service provider to participants

Development and maintenance of Investment

Policy1

Selection, termination, and monitoring of all fund

managers, and investment options consistent

with the Investment Policy1

Monitoring of all investment advisor

purchase/sale activity for compliance with

investment guidelines

Determining applicability and compliance of

fund investment line-up for certain ERISA

requirements

1Subject to acceptance by ABA Retirement Funds

DIRECTED

TRUSTEE

Section 3(21)

Fiduciary

Section 3(38)

Fiduciary

Investment

Manager

Investment

Manager

Investment

Manager

DISCRETIONARY

TRUSTEE

ABA Retirement

Funds Program

The bottom line about your fiduciary responsibility

Your Firm /

Investment

Manager

Your Firm /

Investment

Manager

RESPONSIBLE FIDUCIARYFIDUCIARY ACTS AND DECISIONS

Your Firm Your Firm Your Firm Your Firm

Your Firm Your Firm Your Firm

Your Firm Your Firm Your Firm

Your Firm Your Firm Your Firm

Your Firm Your Firm

Your Firm

Your Firm

Responsibility

TIPAsk yourself: How much fiduciary responsibility do I really want?

12ABA Retirement Funds Program Presentation

Administration and maintenanceEligibility and data changes

Responsibility

Employer determines eligibility

1

Employee elects to

participate in plan

2

Employee completes

enrollment process

3

Employer verifies

enrollment (optional)

4

Recordkeeper processes

enrollment and beneficiary

5

Recordkeeper establishes

account access and password

6

Recordkeeper sends

enrollment notice(s)

7

Follow plan document eligibility rules

TIP

Make sure you have enough enrollment kits on hand

Some law firms appreciate the opportunity to verify enrollments in the plan

TIP

Make sure you are meeting your participant communication responsibilities

7

13ABA Retirement Funds Program Presentation

Responsibility

Some plan types allow participants to make their own contributions to their accounts,

while other plan types only allow the employer — the firm — to contribute.

To make it easier to understand and track the

contribution limits imposed by the IRS, it may be

helpful to think of the limits in terms of layers.

For example:

TIP

For the plan types that allow employer contributions, the formula the plan uses to allocate employer contributions to its participants is described in its plan documents.

Layer 1 — the limit imposed on

the employer.

For profit sharing plans, the total

employer contributions cannot

exceed 25% of aggregate

eligible compensation of all

eligible employees (401(k)

elective salary deferral

contributions are not included in

employer contributions for this

limit).

Layer 2 — the limit imposed on

the participant (known as the

"annual additions limit").

For all contributions to all

employer plans in which the

individual participates,

contributions cannot exceed the

lesser of 100% of the participant’s

eligible compensation and a

prescribed indexed dollar

amount. For 2016, prescribed

indexed dollar amount is

$53,000.

Layer 3 — the dollar limit for

elective contributions (including

pre-tax elective contributions and

Roth 401(k) contributions).

This dollar limit is indexed each

year. The limit is $18,000 for

2016. The catch-up contribution

limit for 2016 for a participant

who attains age 50 before year-

end is $6,000.

TIP

Timely Deposit RulesRemember, participant contributions must be forwarded to your recordkeeper as soon as they can be segregated from the employer's assets.

Administration and maintenanceContributions

Responsibility

14ABA Retirement Funds Program Presentation

Responsibility

Typically, your participants have several options to make investment

election changes and transfers

TIPDoes your provider offer service level guarantees?

Things to keep in mind:

1 Make sure your participants are familiar with any trading or transfer restrictions

within your plan’s fund lineup

2 If your plan includes a self-directed brokerage window, investment election

changes and restrictions may be different from those of funds in the plan

3 Beware of cut off times for processing of investment election changes as this is

often a source of complaint by participants

4 Find out if your current provider offers automatic investment reallocation to keep

participant accounts on track

Administration and maintenanceInvestment election changes and transfers

Responsibility

8

15ABA Retirement Funds Program Presentation

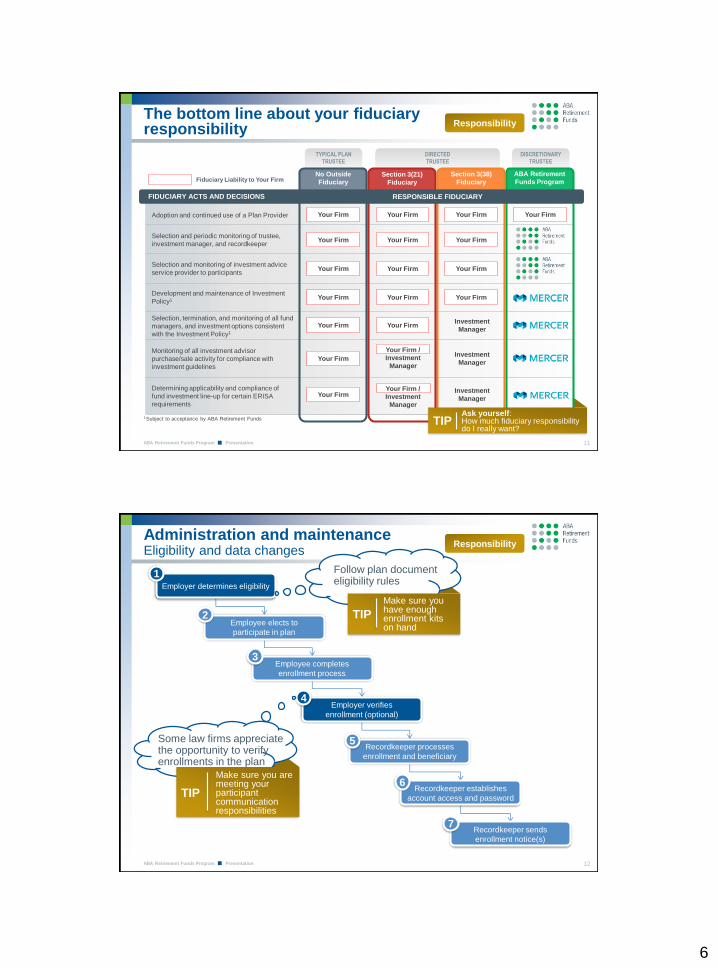

Responsibility

There are a few different ways participants typically access funds

from their plan accounts

1 2 3 4 5

Distribution resulting from termination occurs when a participant quits, retires,

or is fired.

When a participant dies, you are responsible for checking the

participant’s records to determine the named beneficiary and the

type of death benefit, if any, the beneficiary should receive.

Typically for the employee who has met the age- or service-based criteria for

withdrawal and is still employed.

Only specific financial conditions qualify for hardship withdrawals.

Assuming loans are

allowed under your plan,

a participant may request

a loan from the vested

portion of his or her

account.

TIP

When a participant leaves your firm, an account distribution is not

required. In fact, a participant with a vested account balance of more

than $5,000 can maintain the account with your firm’s plan (subject to

required minimum distributions at age 70½).

Administration and maintenanceAccessing funds

Responsibility

16ABA Retirement Funds Program Presentation

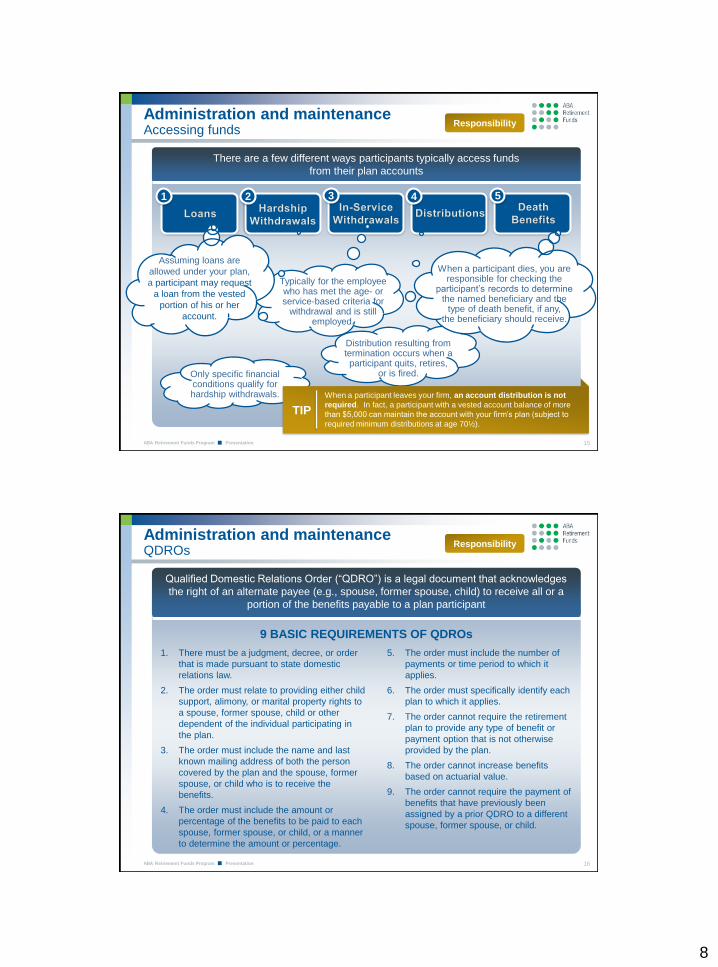

Qualified Domestic Relations Order (“QDRO”) is a legal document that acknowledges

the right of an alternate payee (e.g., spouse, former spouse, child) to receive all or a

portion of the benefits payable to a plan participant

Responsibility

1. There must be a judgment, decree, or order

that is made pursuant to state domestic

relations law.

2. The order must relate to providing either child

support, alimony, or marital property rights to

a spouse, former spouse, child or other

dependent of the individual participating in

the plan.

3. The order must include the name and last

known mailing address of both the person

covered by the plan and the spouse, former

spouse, or child who is to receive the

benefits.

4. The order must include the amount or

percentage of the benefits to be paid to each

spouse, former spouse, or child, or a manner

to determine the amount or percentage.

5. The order must include the number of

payments or time period to which it

applies.

6. The order must specifically identify each

plan to which it applies.

7. The order cannot require the retirement

plan to provide any type of benefit or

payment option that is not otherwise

provided by the plan.

8. The order cannot increase benefits

based on actuarial value.

9. The order cannot require the payment of

benefits that have previously been

assigned by a prior QDRO to a different

spouse, former spouse, or child.

9 BASIC REQUIREMENTS OF QDROs

Administration and maintenanceQDROs

Responsibility

9

17ABA Retirement Funds Program Presentation

Reporting requirements

Form 5500 is the annual

return for your retirement

plan that must be filed. It is

required to ensure employee

benefit plans are operated

and managed correctly.

3

Responsibility

As Plan Administrator, you will need to determine the requirements that apply to your

plan based on the number of participants in your plan and your plan type

Participant communication

requirements

1

The Department of Labor

(“DOL”) mandates that

certain communications to

plan participants be

conducted, and may

include:

1. Enrollment kit for

eligible employees

2. Summary plan

description

3. Summary of material

modifications

4. Summary annual report

5. Participant disclosure

Plan testing requirements

2

Testing is done each year to

monitor whether the plan is

in compliance with certain

IRS and DOL requirements,

and includes:

1. Annual additions

2. Top-heavy

3. ADP and ACP

nondiscrimination

testing

4. 410(b)

Coverage

testing

ResponsibilityAdministration and maintenanceCompliance and communications

18ABA Retirement Funds Program Presentation

Responsibility

Although employers establish retirement plans with every intention of having a long-term

retirement vehicle, there are occasions when the decision is made to terminate it

When Must You Terminate the Plan?

Some, but not all, examples of occasions when the plan must be terminated

are as follows:

• Firm has dissolved and is no longer doing business,

• Sole proprietor has passed away and a successor employer will not be

continuing the plan, or

• Sole proprietor has retired and a successor employer will not be

continuing the plan.

TIP

A partial termination of the plan may be triggered if a significant portion of the firm’s

employees have severed employment due to firm-initiated employee dismissal such as a

layoff. The IRS presumes that a partial termination has occurred if the plan's turnover rate

is at least 20% of the active employees. When a partial termination of the plan occurs,

affected participants (e.g., those who are no longer participants due to the event) must

become 100% vested. There is no requirement that the plan must be terminated or that

other participants be vested or receive distributions.

ResponsibilityAdministration and maintenancePlan termination

10

19ABA Retirement Funds Program Presentation

Responsibility

http://www.dol.gov/ebsa/

publications/401kplans.

html

ResponsibilityAdministration and maintenanceForms, tools and resources

20ABA Retirement Funds Program Presentation

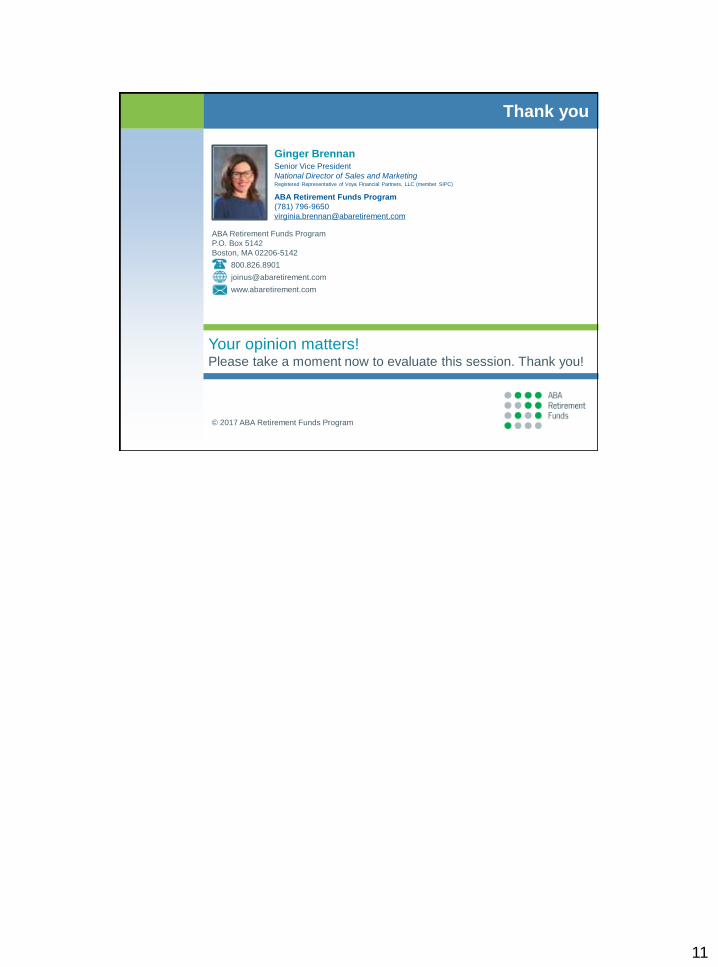

Mercer Trust Company and its

affiliates globally, have 40+ years of

investment experience, advising on

over $9 trillion1

Has provided consulting services to

8 of the 10 largest US pension funds1

Oversight Responsibility

Board of Directors comprised of no fewer than

10 attorneys

Board of Directors supported by:

• Full-time Staff; Executive Director,

Program Operations Director

• Outside experts including independent

counsel & consultants

ABA Retirement Funds

All data as of December 31, 2015 or otherwise noted.1 Assets under advisement includes aggregated data for Mercer Trust Company and its affiliated companies globally

(“Mercer”). Data is derived from a variety of sources, including, but not limited to, third-party custodians or investment

managers, regulatory filings, and client self-reported data. Mercer has not independently verified the data. Where

available, data is provided as of December 31, 2015 (“Reporting Date”). If data was not available as of the Reporting Date,

information from a date closest in time to the Reporting Date, which may be of a more recent date than the Reporting

Date, was included. Data includes assets of clients that have engaged Mercer to provide project-based services within the

12-month period ending on the Reporting Date, and assets of clients that subscribe to Mercer’s Manager Research

database.

2 As published by Pensions and Investments Special Report of top DC Recordkeepers as of April 4, 2016 (based on

September 2015 data).3 TD Ameritrade was evaluated against 15 others in the 2016 Barron’s Online Broker Review, March 19, 2016. The firm was

ranked 1st in the categories “Best for Long-Term Investing” and “Best for Novices.” TD Ameritrade was also awarded the

highest star ratings (4.5) in “Best for Options Traders” (shared with 2 others) and (4) in “Best for In-Person Service”

(shared with 4 others). Also received 4 stars in “Best for Frequent Traders”. Star ratings are out of a possible 5. Barron’s is

a trademark of Dow Jones. L.P. All rights reserved.

ABA Retirement Funds

Program sponsor; not-for-profit corporation

More than 3,800 law firm retirement plans

Over $5 billion in assets

More than 50 years of service to the legal

community

Investment Fiduciary,Trustee, and Custodian

A leading provider of financial

products and services in the U.S.

One of the largest Defined

Contribution Recordkeepers with

46,698 plans2

Recordkeeping, Client Service and Sales

Offers over 13,000 domestic and

international mutual funds

Ranked #1 for Long-Term Investing

and #1 for Novices in Barron’s 2016

Online Broker Review3

Self-Directed Brokerage Service

ABA Retirement Funds Program structure

11

www.abaretirement.comwww.abaretirement.com

Ginger BrennanSenior Vice President

National Director of Sales and MarketingRegistered Representative of Voya Financial Partners, LLC (member SIPC)

ABA Retirement Funds Program

(781) 796-9650

Thank you

Your opinion matters!Please take a moment now to evaluate this session. Thank you!

ABA Retirement Funds Program

P.O. Box 5142

Boston, MA 02206-5142

800.826.8901

www.abaretirement.com

© 2017 ABA Retirement Funds Program

Your opinion matters!

Please take a moment

now to evaluate this

session.