Embed Size (px)

Citation preview

ÅF – leading the way in technical consulting.Our work focuses on energy and the environment,

investments in infrastructure and projects for industry.Our base is in Europe, but our business and clients

extend right across the globe.What makes us unique is our co-workers and the tech-

nical consulting industry’s greatest bank of experience.It’s all summed up in our corporate motto:

“ÅF – innovation by experience.”

Tel +46 10 505 00 00www.afconsult.com

ÅFANNUALREPORT2010

ANNUAL REPORT 2010

THISISÅF

OPERATIONS

ANNUA

LREPORT

CORPO

RATE

GOVERNANCE

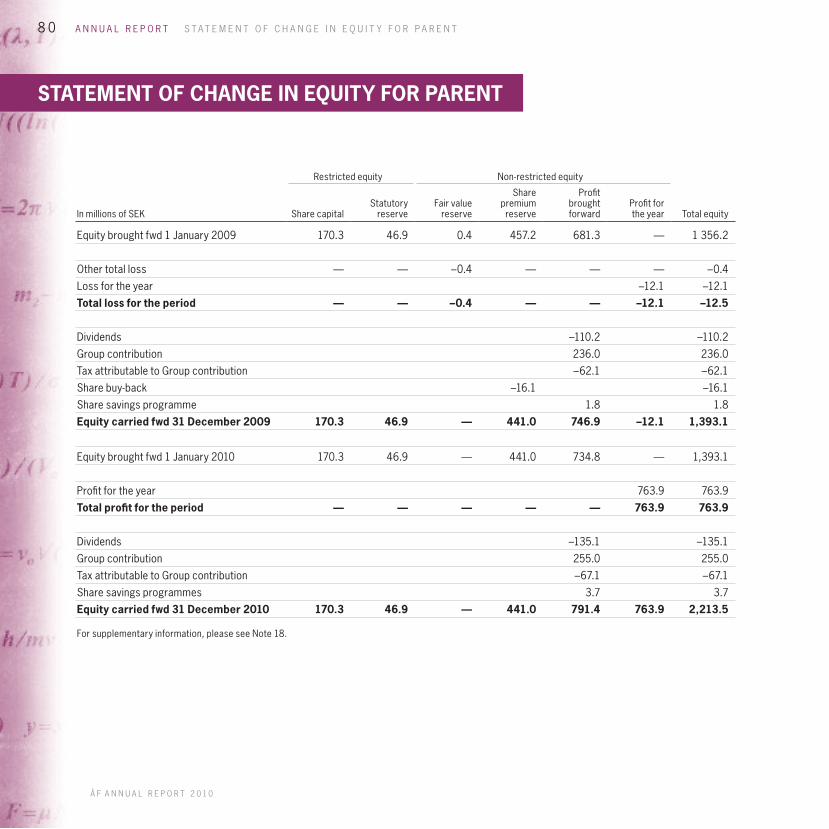

66 Administration report70 Consolidated income statement71 Statement of consolidated comprehensive income72 Consolidated balance sheet74 Statement of change in equity for Group75 Statement of cash flows for Group76 Parent income statement77 Statement of comprehensive income for Parent78 Parent balance sheet80 Statement of change in equity for Parent81 Statement of cash flows for Parent83 Notes121 Audit report

22 Energy28 Industry34 Infrastructure40 Technology46 ÅF shares50 Sustainability is profitability51 Sustainability report58 Risk management and sensitivity analysis63 Definitions64 Five-year financial summary, SEK65 Five-year financial summary, EUR

1 The year at a glance2 This is ÅF4 A message from the President6 Mission, vision, strategies and objectives9 Olympic Green Advisor11 Market trends and business review14 Human resources

ÅF is continuously developing its consulting businessand its capacity to carry out its assignments in thebest possible way. The ambition is clear: to safe-guard successful, long-term sustainable develop-ment for ÅF’s clients and for ÅF itself.

page 8

Striving for profitability and wanting to make theworld a better place aren’t mutually exclusive.Quite the opposite, in fact. A sustainable companyis a long-term venture, which lays the foundationsfor good profitability over time.

page 50

In 2010 ÅF made a number of acquisitions in Europein line with its strategy of becoming number one ortwo in the markets where the company is active.

page 67

The board works to continuously improve the effec-tiveness of its routines and working methods in orderto be able to devote as much time as possible toimportant strategic discussions.

page 122

122 Corporate governance at ÅF123 Corporate governance report128 Board of directors130 Senior management132 Annual general meeting

133 ÅF offices

The English version of the Annual Report of ÅF AB is a translation of the Swedish original. The Swedish text is the binding version and shall prevail in the event of any discrepancies.Å F A N N U A L R E P O R T 2 0 1 0

1 3 3Å F O F F I C E S

Group Head OfficeÅF ABVisitor’s address: Frösundaleden 2, SolnaPost address: SE-169 99 Stockholm, SwedenTel +46 10 505 00 00

Fax – Senior Management: +46 8 653 56 13Fax – Reception: +46 10 505 00 10For further information about addresses,please see www.afconsult.com

SwedenAlingsåsArbogaBorlängeBoråsEnköpingEskilstunaFalunGällivareGävleGothenburgHalmstadHelsingborgHässleholmJönköpingKalmarKarlskogaKarlskronaKarlstadKirunaKristianstadLinköpingLuleåMalmöMora

NorrköpingNynäshamnOskarshamnPiteåSkaraSkellefteåSkövdeSollefteåStenungsundStockholmSundsvallSöderhamnSödertäljeTavelsjöTrollhättanUddevallaUmeåUppsalaVarbergVästeråsVäxjöÅmålÖrebroÖrnsköldsvikÖstersund

Czech RepublicBrnoMêlnikPardubicePlzenPrag

DenmarkCopenhagenHerlevRandersKalundborg

EstoniaNarvaTallinnViljandiVöru

FinlandTampereVantaa

GermanyHamburg

IndiaNew Delhi

IndonesiaJakarta

ItalyRome

KazakhstanAstana

LithuaniaKaunasVilnius

NigeriaGarki Abuja

NorwayBodöLilleströmOsloSandefjordMoss

RussiaMoscowSt PetersburgYekaterinburg

ScotlandEdinburgh

South AfricaDurban

SpainMadridSan Sebastian

SwitzerlandBaden

ThailandBangkok

TurkeyAnkara

TurkmenistanAschabad

UkraineKremenchuk

VietnamHanoi

A110418-02Produced by Solberg in collaboration with the ÅF Group’s CorporateInformation and Corporate Finance Departments. Printed by Elanders.Photos: Peter Bartholdsson and others. Translation: AB Språkman.

A brief historical summaryOn 23 February 1895 Södra Sveriges Ångpanneförening was created when anumber of steam generator owners in the south of Sweden joined forces withthe aim of preventing accidents and making more efficient use of steam power.

In the 115 years that have elapsed since then, ÅF has played a key role in theindustrial developments that have revolutionised society.

The company has guided its clients through four major technology changes –steam, electricity, nuclear power and computerisation – and remained at the fore-front of technology both in the industrial era and in today’s information society.

AB Ångpanneföreningen was first listed on the Stockholm Stock Exchangein January 1986. On 5 May 2008 AB Ångpanneföreningen changed its name toÅF AB, and today it is one of Europe’s largest technical consulting companies.

ÅF OFFICES

1

Å F A N N U A L R E P O R T 2 0 10

T H I S I S Å F T H E Y E A R A T A G L A N C E

201020072006 2008 2009

5,000

4,000

3,000

2,000

1,000

0

Group operating income,excl. capital gain (in millions of SEK)MSEK

500

400

300

200

100

0

12.5

10

7.5

5

2.5

0

MSEK %

Group operating profit andoperating margin, excl. capital gain

201020072006 2008 2009

0

1

2

3

4

Dividend per share 1)

1) A 2:1 share split was implemented on 2 June 2010. Comparative figures adjusted.2) Proposed dividend.

SEK

2010 2)20072006 2008 2009

Financial summary 2010 2009

Operating income, MSEK 4,795.9 4,692.0Operating income excl. capital gain, MSEK 4,338.0 4,684.2Operating profit, MSEK 805.8 388.3Operating profit excl. capital gain, MSEK 317.0 380.5Operating margin, percent 16.8 8.3Operating margin excl. capital gain, percent 7.3 8.1Capacity utilisation, percent 71.9 71.3Profit after net financial items, MSEK 798.1 377.0Profit margin, percent 16.6 8.0Employees (FTEs) 3,966 4,182Equity per share, SEK 69.47 53.68Equity/assets ratio, percent 59.8 51.0Return on equity, percent 32.5 15.8Return on equity excl. capital gain, percent 12.5 15.4Earnings per share before dilution, SEK 21.02 7.93Dividend per share, SEK 1) 4.00 2) 4.001) A 2:1 share split was implemented on 2 June 2010. Comparative figures adjusted.2) Proposed dividend.

THE YEAR AT A GLANCE

4,338Operating income excludingcapital gain totalled SEK

million (2009: SEK 4,684 million)

717Profit after tax amounted to SEK

million (2009: SEK 275 million)

317Operating profit excludingcapital gain totalled SEK

million (2009: SEK 380 million)

21.02Earnings per share before dilution: SEK

(2009: SEK 7.93)

2 T H I S I S Å F Å F A T A G L A N C E

THIS IS ÅF

Division ÅF offices

Infrastructure

The Infrastructure Division holds a leading position in the field of consultingservices for infrastructure development in Scandinavia.

Industry

The Industry Division is a leader in consulting services in the fields of processtechnology, energy efficiency, environmental engineering, industrial IT, automation,electrical power systems and mechanical engineering.

Energy

The Energy Division offers technical and financial consulting services forthe energy sector and is a world leader in the field of nuclear power.

Technology

The Technology Division offers solutions and consulting services in fieldsthat include telecommunications, defence and development.

Å F A N N U A L R E P O R T 2 0 10

3T H I S I S Å F Å F A T A G L A N C E

Clients Operating income Operating profit Employees (FTEs)Operating profit

per FTE

• Road and rail

• Property sector

MSEK 1,233

29 % 20 % 28 %

MSEK 69.0 1,065

SEK 65,000

• All sectors of industry:in Scandinavia, also energyand nuclear power

MSEK 1,340

31 % 35 % 32 %

MSEK 119.9 1,200

SEK 100,000

3 3

MSEK 1,012 MSEK 83.1 906

SEK 92,000

23 % 25 % 24 %2 2 2• Power industry andenergy companies

• Government bodies

• Financial institutions

• All industries and sectors

MSEK 719

17 % 20 % 16 %

MSEK 69.1 616

SEK 112,000

Å F A N N U A L R E P O R T 2 0 10

Total, all divisions MSEK 4,304 MSEK 341.1 3,787 SEK 90,000

Other/Eliminations*) MSEK 492 MSEK 464.7 179 —

Total including eliminations MSEK 4,796 MSEK 805.8 3,966 SEK 203,000

Divisional contributions to Group totals for 2010 are shown as a percentage.*) Includes the Inspection Division, which was sold in Q1 2010.

4

Å F A N N U A L R E P O R T 2 0 10

T H I S I S Å F T H E P R E S I D E N T ’ S C O M M E N T S

CEO Jonas Wiström explains how ÅF sharpenedits focus in 2010 and what is top of the agendaover the next few years. The key themes areprofitability, growth and sustainability.

So, Jonas Wiström, how would you summarise 2010?“For ÅF, 2010 was a year of strategic realignment. The decision tosell our Inspection Division, ÅF Kontroll, proved a good move for usand the division’s 500 co-workers, but more important still, it under-lined our strategy to become number one or two in our fields ofexpertise in our chosen markets. The inspection market is domi-nated by a handful of big global players, so the opportunities for usto expand our operations in this segment were limited. Moreover,ÅF’s growth, particularly in nuclear power, was making it increas-ingly problematical to combine the dual roles of project implementa-tion and independent inspection under one and the same corporatebanner. The decision also meant we had to sell our share in ÅF-TÜVNord, but the income from these divestments helped to fund anumber of strategic acquisitions during the year in our focus areasof industry, energy and infrastructure. The acquisitions of Energo,Gatubolaget i Göteborg, Platom and VPC Mining in Sweden, Meacontin the Czech Republic and Mercados in Spain added the strengthsof more than 550 highly qualified new co-workers to our core com-petences. This represents a significant reinforcement of our marketposition and leaves us very well placed to grow further and to cap-

ture new market share at the start of what we hope is an upturn inthe economy.”

What has been happening in the various divisions?“As far as market developments in general are concerned, therecovery in 2010 turned out to be slower than we had initially antici-pated. We didn’t witness any real increase in client activity until theautumn. The Energy Division won several important assignments in2010, but was also affected by clients deferring their investmentplans and by structural shifts in the market. The Industry Divisionreported a continuous improvement in the level of profitability, andearnings were good towards the end of the year. Growth was goodin the Infrastructure Division, especially in infrastructure planning,where the division demonstrated its strengths by securing somemajor assignments in connection with the Stockholm Bypass Project.However, profitability in the division was undermined by the costs ofmajor restructuring work in Norway. The Technology Division devel-oped in a highly positive direction, reporting good capacity utilisation,healthy profitability and good growth. Overall, ÅF increased its marketshares over the course of the year.”

ÅF is committed to doubling its consulting workforceand increasing turnover significantly over the next fiveyears. How do you aim to go about achieving that?“We will achieve our vision through what, in the longer term, will bea more or less evenly balanced mix of organic and acquired growth.As our strategy is to be a market leader in our chosen areas of exper-tise, most of the initial growth will be in countries and fields where wehave already made a name for ourselves. It’s clear to me that ourrecent successes have been built on a strong, well-known brand andthe ability to consistently exceed our clients’ expectations.”

A more focused ÅF – ready toserve a stronger market

“Our first-class offers in global growthareas will produce good results.”

A MESSAGE FROM THE PRESIDENT

5

Å F A N N U A L R E P O R T 2 0 10

T H I S I S Å F T H E P R E S I D E N T ’ S C O M M E N T S

How do you make sure that rapid growth doesn’tundermine profitability?“Personally, I can’t see why growth and profitability should not becompatible. On the contrary, the lines of business that have beenmost profitable at ÅF are those that have grown most rapidly.Growth creates an entrepreneurial spirit and fosters a corporateculture whose hallmarks are creativity, a willingness to listen andthe ability to deliver. Our clients benefit from this in the form of in-telligent solutions that, in turn, increase demand for our services.”

“Olympic Green Advisor” is a new concept.What does it actually mean?“As Olympic Green Advisor, ÅF acts as a consultant to the nationalOlympic Committees in Finland, Norway, Sweden and Switzerlandon issues relating to sustainability. In Sweden, for example, we havebegun the process of educating leaders and athletes on sustainabilityissues. We have already carried out a sustainability study for theSwedish Olympic Committee and, in the longer term, we hope to beable to play our part in helping to make the Olympic Games greener.Our aim is to make a difference and to influence general opinion bynudging it in the right direction. The broader but related concept of‘ÅF Green Advisor’ places us in a unique position to market anumber of strong offers across our client base.”

Tell us about ÅF’s work with sustainability.“The world needs new technology, creativity and strong politicalaction to meet the challenges facing humanity. We must embrace thetechnological solutions that lead to a better, more prosperous andmore environmentally sustainable world. And it will be engineerswho lead us along this path.For ÅF, sustainability is the basis for long-term profitability. Eco-

nomic, environmental and social sustainability are the cornerstoneson which we need to build in order to be able to continue to deliverthe best solutions to clients who want their business operations tobe sustainable, successful and profitable.For the first time ÅF is reporting its sustainability performance

over the past year with reference to the guidelines of the GlobalReporting Initiative (GRI). In the autumn ÅF also launched its owntough targets for the company’s internal sustainability work: theseinclude halving climate impact by 2015 (calculated per individual,with 2009 as the baseline year) and aiming to ensure that ÅF alwaysoffers clients an alternative ‘green’ solution to every challenge we

are asked to solve. In 2010 we also launched a web-based sustain-ability training programme for all ÅF employees.”

Where does the focus lie in 2011?“After the slowdown in business that followed the financial crisis, it’snow time for us to start to grow again. We did capture new sharesof the market during the economic downturn, but our sights are nowfirmly set on growth in absolute terms, where the most importantthing is to grow organically. We have first-class offers in globalgrowth areas and these will produce results.”

What is the best thing about ÅF?“The accumulated knowledge and experience of our 4,500 or soco-workers. It’s truly fantastic. And I would argue, too, that our abilityto make systematic use of the knowledge we gain is quite unique.It means our clients always have fast-track access to tried-and-tested methods and techniques.”

And finally…?“The sale of ÅF-Kontroll was an important milestone in our corporateevolutionary process. It has sharpened the focus within ÅF and givenus the financial resources to grow in our core activities. Today wehave an organisation that is fully focused on and geared to meetingour commercial targets. I believe the market will improve in 2011,and the ÅF brand is now stronger than ever. Add that to ÅF’s evergreater appeal as an employer (ÅF was recently voted one ofEurope’s top 50 employers in a major survey of engineering stu-dents), and I’m convinced that the outlook for the future is good.Finally I would like to say thank you to all the co-workers who have

contributed to ÅF’s suc-cess. I look forward tocontinuing to work withyou all in building thecorporate values thatare so important to ourclients, shareholdersand other stakeholders.”

Stockholm, Sweden –March 2011

Jonas WiströmPresident and CEO

6 T H I S I S Å F M I S S I O N , V I S I O N , S T R A T E G I E S A N D O B J E C T I V E S

MISSION, VISION, STRATEGIES AND OBJECTIVES

MissionÅF’s joint pool of expertise and experiencecreates solutions that are profitable, safeand sustainable.

ÅF contributes to the sustainable development of indus-try and society as a whole. More than 100 years’ experi-ence in the business has taught us to raise our sights.

Our collective experience places ÅF firmly in the frontrank of technological progress. Even so, the solution ÅFdelivers is not necessarily the most technically sophisti-cated – but it’s always the best! ÅF never experimentswith its clients or their businesses, especially when theirinterests are best served by tried and tested technology.

Our total independence from suppliers and other part-ners is every client’s guarantee of an optimum solution.

That’s why ÅF creates solutions that are profitable, safeand sustainable for its clients.

ÅF’s core values:• Great people

• Teamwork

• Indisputable independence

Our mottoInnovation by experience.

VisionThe best partner for the best clients• ÅF meets every technical challenge.

• ÅF’s business model outperforms all competitors.

• ÅF sales will total 1 billion euros by 2015.

ÅF meets every technical challengeÅF has access to more than 100 million hours of engi-neering experience – know-how and solutions that aredocumented in “ONE”, our unique knowledge databasethat is available to every ÅF employee. This means that:

• every ÅF employee can make use of the full,combined strength of ÅF.

• ÅF is ready to tackle every technical challenge,now and in the future.

ÅF’s business model outperforms allcompetitorsÅF does not charge for its time, but for the value it cre-ates. That increases the productivity in our projects andreduces costs for the clients. Partnership plays a cen-tral role in our assignments, because it is as a partnerthat ÅF can deliver real value – the right quality at thelowest overall cost.

Å F A N N U A L R E P O R T 2 0 10

7

Å F A N N U A L R E P O R T 2 0 10

T H I S I S Å F M I S S I O N , V I S I O N , S T R A T E G I E S A N D O B J E C T I V E S

Our outstanding co-workers are one step ahead interms of technical expertise, business acumen and totalindependence.For our clients and competitors it is clear that here at

ÅF we demand more of ourselves. We have the will to win.

ÅF sales will total 1 billion euros by 2015ÅF will become Europe’s leading technical consultant.For us, that means becoming the most profitable com-pany among our biggest competitors in the business.Our rate of growth will be high. We will grow both

organically and through corporate acquisitions, but wewill also be careful to ensure that the companies weacquire make a positive contribution to our profitabilityand to the ÅF culture.

StrategiesOperations will be decentralised• under one and the same brand• with common processes and systems• with shared values and a common corporate culture in orderto concert efforts and fully exploit the potential of all theexperience that is represented within the ÅF Group.

ONE ÅF is a huge, shared bank of knowledge available to all ÅFco-workers that enables ÅF to improve profitability for its clientsby proposing safe, sustainable solutions to a wide variety ofchallenges.

ONE ÅF is a common workplace where co-workers are encour-aged to pursue their career within ÅF, for example in a differentcountry or with new, technical challenges.

ONE ÅF is a joint sales organisation through which clients areoffered the entire range of ÅF’s services.

ONE ÅF is the firm base for the corporate culture and sharedvalues of ÅF.

Acquisitions strategyÅF’s acquisitions policy is based on the above. Every effort will bemade to develop the business when the right opportunities arise,but expansion will not take place at the expense of profitability.

8

Å F A N N U A L R E P O R T 2 0 10

T H I S I S Å F M I S S I O N , V I S I O N , S T R A T E G I E S A N D O B J E C T I V E S

Business support and shared processesÅF is continuously developing its consulting business and itscapacity to carry out its assignments in the best possible way.The ambition is clear: to safeguard successful, long-term sus-tainable development for ÅF’s clients and for ÅF itself.One example of this is ONE, ÅF’s recently developed IT plat-

form. At the same time as it acts as a driving force for collabo-ration within ÅF and with clients and subcontracted suppliers,ONE also guarantees a modern approach to working with pro-cesses, projects and knowledge retrieval at ÅF, freeing up timefor development and innovation in client assignments.ONE is a web-based tool, mostly in English, that is accessible

to employees throughout the ÅF Group.ONE also serves as ÅF’s business support system, a central

operational control system that makes ÅF’s business operationsconsiderably more cost-effective while assuring quality and con-sistency in the company’s approach.The system includes tools for shared processes, project docu-

mentation and a searchable database of engineering and busi-ness experience that pinpoints any similarities between the manyassignments undertaken by ÅF. When a client commissions ÅF toperform an assignment, the chances are great that ÅF has alreadysuccessfully completed a similar assignment elsewhere.ONE enables ÅF management to control and support opera-

tions and meet the criteria for certification for environmentaland quality management in accordance with ISO 14001:2004and ISO 9001: 2008.

Long-term objectivesFinancial objectivesÅF shall be the most profitable company among its closest com-parable competitors in the industry and achieve an operatingmargin (EBIT) of at least 10 percent over a business cycle.

ÅF shall have net debt over a period of time, but net indebted-ness shall not exceed 40 percent of equity.

Growth objectiveSales of 1 billion euros by 2015.

Human resources objectivesBetter balance in the gender ratio. An initial target is for at least 25percent of the company’s consultants and managers to be women.Staff turnover, based on resignations, to be 7–13 percent.All employees to take part in a personal development inter-

view each year.

Sustainability objectivesIn 2010 ÅF adopted a plan for the company’s sustainability workfor the period up to 2015 and embraced three overarching sus-tainability objectives:

By the year 2015 ÅF aims to:• have halved its direct climate impact (baseline year 2009,calculated per individual).

• include a proposal in every offer or tender that ÅF submits,to enhance the sustainability aspect of the project.

• be perceived as the technical consulting firm that, from asustainability perspective, best solves the technical chal-lenges that its clients are faced with.

In 2010 ÅF began the work of producing a sustainability frame-work for the entire ÅF Group that comprises a sustainabilitypolicy, including revised tools for managing risks. The plan isto launch this sustainability framework in spring 2011.For further details of ÅF’s work with sustainability issues and

the company’s GRI report, please refer to pages 51–56.

9T H I S I S Å F O LY M P I C G R E E N A D V I S O R

OLYMPIC GREEN ADVISOR

ÅF has embarked on an important jointventure with the Olympic Committees inFinland, Norway, Sweden and Switzerland,assuming the role of Olympic partner andGreen Advisor to all four of these nationalorganisations.

ÅF provides consulting and advisory services on green issuesand takes an active role in developing Olympic sporting activi-ties from a sustainability perspective. Sustainability is an issuethat is rapidly growing in importance in the Olympic movement,

particularly when it comes to choosing host cities for futureOlympic events. The focus is on policies, strategies and actionprogrammes, and on the education of staff, coaches and theathletes themselves.ÅF is also a sponsor for the national Olympic Committees in

Finland, Norway, Sweden and Switzerland. A sponsorship agree-ment has been signed for the period 2010–2014 that will coverthree Olympic Games.The Olympic rings and the exclusive title of Green Advisor

have been integrated into ÅF’s external communications. TheOlympic rings and the Olympic Association are the world’sstrongest and most fiercely protected non-commercial brand.

World-class managerial conferenceAmong those gathered for the annual ÅFManagers’ Conference were three of theworld’s top names in ice hockey and athletics– Peter Forsberg, Sanna Kallur and AndreasThorkildsen. All three took the stage to explainthe importance of focus, mental training, andthe drive and desire to be best in the worldat what you do.

Å F A N N U A L R E P O R T 2 0 10

1 0

Å F A N N U A L R E P O R T 2 0 10

Martin Jonsson works inStockholm as a section manager for RockEngineering & Measurement Technologyin the Infrastructure Division. He likes tospend his spare time with friends, andenjoys cooking, running in the Swedishmountains and long walks in the woods.

“I want a stimulating environment with peoplewho set me the kind of challenges that help meto grow as a person. I love solving problems.The best thing about ÅF is the positive atmos-phere – and the challenges! Nothing is impossibleand we set ambitious targets. It’s an approachthat runs through the entire organisation.”

1 1

Å F A N N U A L R E P O R T 2 0 10

T H I S I S Å F M A R K E T T R E N D S A N D B U S I N E S S R E V I E W

ÅF’s services in briefÅF is a leader in technical consulting. Our work focuses onenergy and the environment, infrastructure and projects forindustry.Our base is in Europe, but our business and clients extend

right across the globe. What makes us unique is our co-workersand the technical consulting industry’s greatest bank of collec-tive experience. It’s all summed up in our corporate motto:“ÅF – innovation by experience.”

ÅF is made up of four specialist divisionsThe Energy Division focuses on technical and financial consult-ing for the energy sector, from advice on business models toimplementing investments in power plants and the many relatedenvironmental issues.The Industry Division is Northern Europe’s leading industrial

consultant offering services in process technology, automation,industrial IT, electrical power systems and mechanical engineer-ing. In Scandinavia, the division is also responsible for ÅF’soffers to the energy market.

The Infrastructure Division is a leader in the consulting industryfor infrastructure development in Scandinavia and has clients inindustry, the public sector and the property sector.The Technology Division works mostly with assignments in

Sweden, where it is a leading name in product development anddefence technology. The division also enjoys a strong position inthe market for telecommunications and IT consulting services.

ClientsEach year ÅF performs more than 30,000 assignments for some10,000 clients. Assignments vary in length from just a few hoursto hundreds of thousands.ÅF’s ten largest clients in 2010 together accounted for

approximately 23 percent of total invoiced sales. They wereEricsson, the Swedish Defence Materiel Administration (FMV),Ringhals nuclear power plant, the Swedish National Rail Adminis-tration (Banverket), the Stockholm municipal water utility Stock-holm Vatten, ATEL, Gusinoozersk CHP, the Danish Road Directo-rate (Vejdirektoratet), Stockholm’s regional transport authority(SL), and Siemens.

MARKET TRENDS AND BUSINESS REVIEW

Client base – sales by sector 2010

Public sector Private sector

29 % 71 %

ÅF’s operations arebecoming increasinglyinternational. It hasoffices in more than 20countries, but conductsbusiness activities andattracts clients through-out the world.

Geographical spread of ÅF businessNumber of employees per country, December 2010

Sweden

Finland

Norway

Denmark

Switzerland

Czech Republic

Russia

Rest of world

1 2

Å F A N N U A L R E P O R T 2 0 10

T H I S I S Å F M A R K E T T R E N D S A N D B U S I N E S S R E V I E W

MarketIn 2010 the market for ÅF’s services began to stabilise after thefinancial crisis. However, while demand in the energy and infra-structure sectors remains high, elsewhere the recovery hasbeen relatively slow as companies continue to be cautiousabout major new investments in industrial production capacity.In the energy sector the recovery was worldwide, enabling

companies to restart many projects that they had previouslysuspended.In the Nordic region, demand from process industries and the

energy and nuclear power sectors was generally good during2010, particularly towards the end of the year, and most espe-cially in Sweden. Demand from industry was chiefly driven bythe need for efficiency improvements in manufacturing plants,environmental engineering projects, the development of alterna-tive fuels and conversion to efficient energy management.The market for consulting services to the pulp and paper

industry remained weak in Europe in 2010, although the situa-tion was better in South America, Asia and Africa. ÅF has rela-tively large business interests in Chile, so it was encouraging tonote signs of a recovery in that market after the major earth-quake there at the start of the year.Demand was good throughout 2010 for services to the prop-

erty, construction and industrial plant sectors. The propertysector in particular really took off during the autumn. Publiclyfinanced projects proceeded according to plan, with new busi-ness picking up again after a slight slowdown in the wake of thefinancial crisis.Demand from the defence sector remained steady in 2010,

while the market in telecoms and the automotive industryimproved as the year progressed, particularly from the secondquarter onwards.

Outlook – Nordic countriesIt appears that growth in the Nordic energy market will continueto be driven mainly by investments in nuclear power in Finland,preparations for the expansion of nuclear power facilities inSweden, and renewable energy sources in the other Nordiccountries. Alongside major new investments that have alreadybeen approved, there is a constant need for a large number ofefficiency improvement projects, upgrades, capacity increasesand environmental improvements in existing plants, in both thepower industry and elsewhere.Nordic industry will continue to need to significantly improve

the efficiency of its production facilities and to make energy-sav-ing investments. The outlook in the mining, petrochemical,energy, food and pharmaceutical industries is particularly good.The engineering sector, including the automotive industry, isrecovering after several difficult years, but growth is comingfrom a low level.The energy sector is undergoing a period of major adjustment

to new types of energy, the need for greater efficiency and in-creased competition. These factors are likely to drive demandfor technical consulting services for many years to come.The forest industry is restructuring, with several companies

expanding their operations from solely pulp and paper process-ing to include biofuels and electricity.Nordic industry leads the way when it comes to incorporating

sustainability into business operations. This gives it a competi-tive edge internationally and generates considerable demand fortechnical consulting services.In purely geographical terms, the Öresund region is likely to

undergo considerable growth, thanks in part to the very largeESS project, an inter-disciplinary research facility for materialsstudies. There is also good potential for growth in the north,where the mining sector is a key driver of business.

1 3T H I S I S Å F M A R K E T T R E N D S A N D B U S I N E S S R E V I E W

There are many similarities between Sweden, Norway andDenmark when it comes to the market for services that supportpublic-sector investment in roads and railways. These threecountries have strong government finances and their infrastruc-tures are becoming increasingly integrated with each other atthe same time as investments are being made at a similar rateand to a similar extent. The prospects appear to be very rosyfor all three countries.In the construction and property sectors, demand for energy

efficiency initiatives is expected to remain high across the region.The automotive industry seems to have bottomed out and is

expected to show stable growth, albeit from what are histori-cally very low levels.

Outlook – other marketsDemand in the energy sector in Western and Central Europecontinues to be driven primarily by the expansion of new nuclearpower and biofuel facilities. Older coal-fired power stationsurgently need to improve their efficiency and environmental per-formance. In Eastern Europe and Southeast Asia, the marketslook capable of recovering slightly after the significant downturntriggered by the financial crisis.Asia is a strong engine that affects growth in many other mar-

kets, which suggests that demand for energy and raw materials

should continue to be good. Europe also requires vast amountsof energy, which, for ÅF, translates into continued demand forservices in both power generation and distribution. Strong glo-bal demand for raw materials means that future growth in themining sector is also likely to be considerable.Demand from projects to improve environmental performance

and increase energy efficiency in industry is likely to continue tobe healthy, in line with developments in recent years.Growth in the pulp and paper sector is expected to come

from Asia, South America and Africa. Europe is tending to investmore in recycled paper processing and general efficiency gainsthan in new production plant.

Increased internationalisationIn recent years ÅF has expanded through acquisitions andorganic growth, becoming increasingly international. Parallelwith this development, a great deal of effort has been made tostandardise the structure of our competence developmentwork, internal databases, intranet, and brand identity, and toestablish an understanding within the organisation of our sharedcorporate values and aims. Each part of ÅF enjoys considerableautonomy, and this helps secure strong local roots while thecompany’s global structure contributes strength and stability.

In 2010, for the fourth consecutive year, ÅF was involved in “The Swedish Innovation Award”, together with the Swedishbusiness magazine Veckans Affärer and VINNOVA, the Swedish Governmental Agency for Innovation Systems, andAlmega, the employer and trade organisation for the Swedish service sector. The SEK 100,000 prize for 2010 wentto Daniel Ek, the founder of Spotify, for “achieving the impossible by persuading people to pay for music-streamingservices”. The music industry is relieved: in two years Spotify has grown from nothing to a company with 10 millionusers worldwide, and two million in Sweden alone.The first in a new category of Student Innovation Awards, also worth SEK 100,000, went to Solarcool, the brain-

child of Mikael Andersson and Robert Lyngman, two students at Sweden’s KTH Royal Institute of Technology. Combiningthe sun as a source of energy with revolutionary nanotechnology, the duo have developed a low-cost refrigerator thatruns entirely on solar power.The Swedish Innovation Awards are funded with support from ÅForsk, Ångpanneföreningen’s Foundation for

Research & Development.

Innovation means daring to challenge old ideasInnovation means daring to challenge old ideas

Å F A N N U A L R E P O R T 2 0 10

1 4 T H I S I S Å F H U M A N R E S O U R C E S

HUMAN RESOURCES

ÅF has a strong corporate culture and abrand that is becoming increasingly wellknown. These are essential attributes for anycompany that aims to be an industry leaderin Europe and needs to be able to recruitand retain co-workers of outstanding calibre.ÅF has many years’ experience of solvingtechnical challenges, and both the technicaland commercial aspects of its consultants’work are continuously being developed.Every ÅF co-worker has an important partto play in consistently conveying the rightimage of the company to clients and otherstakeholders.

Corporate culture and core valuesThe company’s culture, values and working methods are describedin the ÅF Blue Book (2.0), which is aimed at all co-workers andserves as a tool for pooling the company’s strengths as “One ÅF”.The ÅF core values – great people, teamwork and indisputable

independence – are the bedrock of the day-to-day work of ÅFco-workers and their attitudes to clients and colleagues. ÅFemployees exceed their clients’ expectations in terms of thesolutions they offer and their combination of technical expertiseand business-mindedness. But ÅF employees are also goodcommunicators, good team players and good listeners. Theyare positive in their outlook, deliver on their promises and showrespect in their dealings with clients.

A workplace where you can feel at homeÅF wants employees to take pride in their work and the company,to feel confidence in their managers and to enjoy working along-side their colleagues. To meet the demands made on a modernemployer, ÅF adopts a highly focused, long-term approach to HRissues at all levels within the company and conducts regular co-worker surveys to assess the prevailing mood within the Group.

An increasingly attractiveemployer throughout Europe

• ÅF is an international workplace with offices in more than20 countries.

• ÅF currently employs a total of some 4,500 co-workers.

• In 2010 ÅF co-workers performed projects in more than70 countries.

Å F A N N U A L R E P O R T 2 0 10

1 5

Universum’s Career Barometer 2010 Ranking

IKEA 1

Google 2

ÅF 3

ABB 4

Volvo Group 5

Ericsson 6

T H I S I S Å F H U M A N R E S O U R C E S

To make clear its position on a number of employment-relatedissues, ÅF has formulated guidelines in key areas such as humanresources, pay, equal opportunities and the working environment.HR activities differ from country to country, but the aim remains

the same: to foster a sense of togetherness and create a pleasantatmosphere at work.ÅF works hard to create a good gender balance, an ambition

that is reflected in the company’s recruitment activities. Thefirst step towards a better gender balance is to raise the propor-tion of female consultants and managers to 25 percent by 2015.Whenever a managerial post becomes vacant, at least onewoman must be short-listed. By the end of 2010, the proportionof female consultants was 19 percent (2009: 17 percent). Theproportion of female senior consultants was 17 (15) percent,while female employees made up 23 (21) percent of the totalworkforce. Three of the eight ÅF directors elected by the AnnualGeneral Meeting are women: this corresponds to a 38 percentrepresentation on the board.

ÅF Recruiter – fast-tracking candidateswith the right profileÅF has a web-based recruitment tool that enables external andinternal candidates to register their interest in a searchable

database used by ÅF managers when recruiting new membersto their team. The system handles the entire chain of adminis-trative recruitment procedures, from job advert to contract ofemployment. Simple interfaces mean that the tool can be usedboth via the ÅF website and by external recruitment agencies.

Many development opportunitiesÅF has set itself the target of having approximately 10,000employees by 2015. But such growth means being able to offeran attractive working environment with good opportunities fordevelopment. Working as an ÅF consultant offers enormousopportunities to develop, for example, in different professionalroles, through different levels of expertise, in a wide range oflocations and through international assignments.ÅF has identified three distinct career paths within the com-

pany – as project manager, specialist/expert and manager –each offering a variety of roles, levels and development stages.Whichever path you choose, there are plenty of opportunities todevelop within your role or to switch between roles, for exam-ple, from project leader to specialist and back again. Careerpaths provide support for setting individual targets and actionplans, often as part of the annual personal development inter-views between managers and their co-workers.

ÅF, Sweden’s favourite technical consultant is more popular than ever in Europe

Å F A N N U A L R E P O R T 2 0 10

In the 2010 Career Barometer survey of professional engineers, ÅF wasranked as Sweden’s third most popular employer overall and the numberone choice among technical consulting companies. In the European sur-vey of students at Europe’s top universities, ÅF came 48th in the overallemployer rankings.The Career Barometer is an annual attitude survey conducted by

Universum Communications. All respondents are “young professionals”no more than 40 years old, with an engineering degree from a universityor college plus two to eight years of working experience in their special-ist area. More than 3,000 engineers took part in the Swedish survey,while the European survey canvassed 6,000 technology students.

1 6

Å F A N N U A L R E P O R T 2 0 10

T H I S I S Å F H U M A N R E S O U R C E S

ÅF AcademyThe ÅF Academy is ÅF’s own training organisation, providingsupport for the ÅF career paths and the development of the con-sultant’s role. This includes comprehensive foundation coursesfor new consultants as well as specialised advanced coursesand training tailored to individual requirements. Lecturers andfacilitators come both from within ÅF and from external serviceproviders. The 2010 programme included courses in salestraining, commercial skills and service, all firmly founded onthe ÅF approach to sound entrepreneurial skills.

CertificationAt the ÅF Academy, ÅF project managers undergo training toobtain certification in accordance with the European accredita-tion standard, IPMA. At the time of writing, ÅF has 232 certifiedproject managers at four different levels of certification: A, B, Cand D. For project managers involved in international projects,the certification process is conducted in English.

Education and training in nuclear powerThe ÅF Nuclear Academy is a competence development initia-tive designed to prepare consultants to meet the increasinglystringent requirements of the nuclear power industry and itsregulatory bodies. Courses lead to certification at four levels,and 16 individuals received certification in 2010. The initiativehas stimulated considerable interest in the industry and givesindividual employees outstanding opportunities for professionaldevelopment. Courses are also open to clients and other industrystakeholders.

Variable salaries and Group bonusThe four ÅF divisions have adopted different systems for variableremuneration packages, either based on the results of the divisionas a whole or on individual performance.To underline the relationship between the efforts made by

each individual co-worker and the profitability of the ÅF Group inthe short term and the long term, a bonus model has been intro-duced. Under the current system, part of all profit generated atGroup level is shared out in the form of a bonus payment that isthe same for all co-workers in the company.

Other benefitsAlongside exciting opportunities for professional development,other benefits open to ÅF employees, such as occupationalpensions, favourable insurance deals, company cars, etc., varyfrom country to country depending on local practice and nationaltax regimes.All ÅF Group employees are entitled to rent one of the cottages

or apartments that are owned, managed or leased by the ÅFStaff Foundation.

Sickness absenceSickness absence among ÅF employees was 2.1 percent in2010 (2009: 2.2 percent).

Å F A N N U A L R E P O R T 2 0 10

Elena Kozhevnikova, BusinessDevelopment manager,ÅF in St Petersburg, Russia:“It’s exciting to be part of the era of knowledge capital. My mainresponsibility is developing the organisation in terms of professionaland social skills, knowledge accumulation and integration betweenour various units. The ÅF Group is a fantastic example of rapid yetbalanced growth. If we want to stay on top, however, it’s crucial thatwe continue to make use of the experience and expertise we have indifferent sectors and geographical areas. We need to make the bestpossible use of our synergies.”

Liisa Mäki, HR manager,

ÅF in Vantaa, Finland:“One key aspect of our work is to support managers so that we cancreate the best possible management culture and safeguard ourgood reputation as an employer. This will enable us to recruit thebest co-workers from among both experienced engineers and youngpeople who are just embarking on a career. We also invest a lot ofeffort in motivational issues, to achieve a whole that is greater thanthe sum of its parts.”

Liselotte Trösch, HR manager,ÅF-Colenco in Baden,

Switzerland:“Our biggest challenges are to recruit highly educated and experi-enced engineers who speak several languages, and to sort out thecomplexities of international social insurance, labour law and taxissues for our employees working abroad.”

Charlotte Witt, ÅF’s Directorfor Human Resources,

Stockholm, Sweden:“Our greatest challenge is to focus on efficient processes andintelligent ways of working. We need to be service-oriented,knowledgeable and able to work closely with the client. Successfulgrowth will require recruiting more co-workers and making sure thatwe have managers who set clear targets and aims together withtheir teams. And this, of course, will bring in even more interestingand stimulating projects.”

Growing our most important asset

1 7T H I S I S Å F H U M A N R E S O U R C E S

Å F A N N U A L R E P O R T 2 0 10

Dieter Müller, PhD, manager of the Hydro-power unit at ÅF-Colenco in Switzerland

What has the leadership programmegiven you?“I’ve gained new insights into interesting subjectsthat support the long-term strategy for our busi-ness. I liked all the great communication and lead-ership ideas, which are useful in my day-to-daywork. But I also appreciated the chance to networkand find out more about ÅF’s business.”

What would be a typical day at work?“My working day generally starts with checking mye-mail. If I’m in the office I’ll have internal meetingswith our project managers on decisions relating tocurrent projects or I’ll discuss various proposals,agreements or recruitment matters with othermembers of the management group. Then thereare meetings with, or phone calls to, clients andpartners. During breaks I schedule in brief conver-sations with my staff about their various chal-lenges. Early mornings or late afternoons aregenerally spent preparing for meetings or readingthrough documents.”

Maria Åkesson, section manager atTelecom East, Technology Division

What has the leadership programmegiven you?“It’s bolstered my business expertise. It’s alsodeveloped my leadership skills and given me lotsof good communication skills. What’s more, I’vebuilt up a fantastic network within ÅF.”

What would be a typical day at work?“My working days tend to start early. That way, Ican make sure I have a quiet period before every-thing really gets going. I generally spend this timeon admin, such as e-mail and other odds and ends.During the day I’ll be involved in a variety of things,ranging from meetings with clients, lunchtimemeetings with consultants who are working in thefield, job interviews and project follow-ups. I gohome in the afternoon with my head held high,really proud of my consulting team and the workwe do for our clients.”

T H I S I S Å F H U M A N R E S O U R C E S

ÅF’s Business Executive Leadership Programme is a joint venture with IFL Executive Educationthat is aimed at selected managers within the ÅF Group. Training is spread over a 12-monthperiod during which participants acquire a deeper understanding of ÅF as a company. Amongthe topics covered are strategic planning, international leadership and communication skills.January 2011 marked the end of the first programme, in which Maria Åkesson and DieterMüller were two of the 18 participants.

Growth needs good leaders

1 8

1 9

2008 2009 2010

0

1,000

2,000

3,000

4,000

Number of employees (all forms of employment)

Men Women

2008 2009 2010

0

6

12

18

24

Staff turnover (resignations) %

30 – 39– 29 40 – 49 50 – 59 60 –Age group

Staff turnover based on resignations.Total 2010: 8.9 percent (2009: 6.3 percent).

Age distributionPercentage

Age group, years 2008 2009 2010

–29 14 14 1430–39 30 29 3040–49 27 27 2750–59 19 19 1960– 10 11 11Average age 43.1 43.4 43.3

Length of employmentPercentage

Years of employment 2008 2009 2010

–2 34 26 223–5 21 27 336–10 19 19 1811–20 16 17 1621– 10 11 11Average length of employment 7.8 7.9 7.9

Education, %2008 2009 2010

Postgrad. licentiate or Ph.D studies 3.2 3.6 3.2University degree 43.8 46.6 53.2Other post-secondary education 13.4 13.7 15.0Secondary 39.6 36.1 28,6

Å F A N N U A L R E P O R T 2 0 10

T H I S I S Å F H U M A N R E S O U R C E S

2 0

Å F A N N U A L R E P O R T 2 0 10

M E D A R B E TA R E Å F 2 010

Armada

• Sweden’s largest careers fair fortechnology students.

• Organised by the student union atthe Royal Institute of Technology inStockholm.

• In November 2010 some 8,000 visitorscame into contact with around 150companies over two days.

• Various peripheral events over a two-weekperiod include the Enova and ArmadaChallenge problem-solving competitions.

T H I S I S Å F H U M A N R E S O U R C E S

10:00 Armada opens. ÅF welcomesstudents with an informal chat, fresh fruit anda great cup of coffee. The day combines lotsof information with opportunities for makingcontacts and networking.

ÅF is working actively on employer branding to presentitself as a good employer for potential employees andstrengthen its image in general. In 2010 ÅF was the mainsponsor together with Ericsson of the Armada CareerDays event at Sweden’s Royal Institute of Technology.Armada is Sweden’s largest careers fair for engineeringstudents. Here’s how we got on!

Calling all students!

11:37 Jenny Voss, an electri-cal engineer who works in technicalsales at ÅF’s Nynäshamn office, meetsSawayos Jaynutapong who is studyingfor a master’s degree in sustainabletechnology. She advises him on wherehis skills could take him.

2 1

Å F A N N U A L R E P O R T 2 0 10

T H I S I S Å F H U M A N R E S O U R C ES

12:18 “If you don’t knowwhere you’re going, then you’ll never getthere.” The excitement is palpable whenan ÅF project management veteran talksabout what it takes to be a successfulproject manager. ÅF’s lunchtime presen-tation is packed with over 200 studentswho are totally tuned into this taste ofreality.

14:22 “I think ÅF has made a majorimpression on the students who’ve comealong to these career days,” says Moa Moss-berg (right), student union project managerfor Armada. Although it is a hectic day, shemanages to exchange a few words with ZahraParsa. Zahra, a civil engineering graduatespecialising in geotechnical engineering, isa business developer at ÅF in Borlänge.

ÅF employer branding activities

• A number of external activities are car-ried out every year at universities, bothIRL (“in real life”) and via social media.

• This work strengthens ÅF’s profile not onlyamong potential employees, but alsoamong future clients and competitors.

• Students come away with good contactsfor degree project placements andcareers enquiries in their specialist field.ÅF attaches considerable importance tomeeting students’ needs and puttingthem in touch with the right personquickly.

• 2010 marked the start of the “Sustain-ability Case Tour”, an opportunity for stu-dents from Chalmers University of Tech-nology in Gothenburg, the Royal Instituteof Technology in Stockholm and the tech-nical universities in Linköping and Lundto test their problem-solving skills ininfrastructure planning and sustainability.

• ÅF took part in the new “Career Days”event in Stockholm’s Globen Arena inorder to meet more practising engineers.

22:07 “Armada 2010,what a fair! Every company wants tobe there. Apply to us, apply to us.Come and share your genius!” At theclosing banquet, Sofia von Celsing,who is responsible for employerbranding at ÅF, thanked the projectgroup – in verse! – for all its hardwork.

2 2 O P E R AT I O N S E N E R G Y D I V I S I O N

ENERGY

Key figures 2010 2009

Operating income (in millions of SEK) 1,012.1 1,192.2

Operating profit (in millions of SEK) 83.1 126.5

Operating margin, % 8.2 10.6

Contribution to Group income % 23 27

Number of employees (FTEs) 906 841

Operating profit per FTE (in thousands of SEK) 92 150

The historical figures above have been adjusted, proforma, to take account ofthe corporate restructurings implemented on 1 January and 1 October 2010.

Contribution toGroup sales

23%

The Energy Division offers technical consult-ing services for the energy sector. It hasoperations in large parts of the world and isa market leader in the Nordic region, Switzer-land and the Baltic countries. In 2010 ENRmagazine (Engineering News Record) rankedÅF as the world’s sixth-largest internationalenergy consultant.

The offer – consulting for the entire investment cycleThe Energy Division offers technical and financial consultingservices for the energy sector, with the emphasis on power gen-eration and district heating. Services include everything fromadvice on energy markets and their regulations to the imple-mentation of investments in power plant new-builds.Already a market leader in Finland, Switzerland and the Baltic

countries, the division is also enjoying rapid growth in Russiaand Central Europe. 2010 brought the acquisition of the Czechconsulting company Meacont, strengthening the division’s mar-ket position in the Czech Republic and Slovakia. At the end ofthe year the division acquired Mercados Energy Markets Interna-

A catalyst for ÅF’sinternational growth

Å F A N N U A L R E P O R T 2 0 10

Å F A N N U A L R E P O R T 2 0 10

Energy Division – facts at a glance

• Consulting services for all types of energy.

• Global operations.

• 1,100 co-workers in the Czech Republic, Estonia, Finland, India, Lithuania,Nigeria, Russia, Spain, Switzerland, Thailand and Vietnam.

• Contribution to total Group sales: 23 percent.

• All assignments are conducted outside Sweden. (Please see Industry Divisionfor energy assignments in Scandinavia.)

Meet Eero AurannePresident, Energy Division

What are you happiest about in 2010?“We made two strategic acquisitions: CzechMeacont Praha in May and Spanish MercadosEMI in December. The former will strengthenour business both internationally and innuclear power, while Mercados will bringa new strategic dimension to the division’srange through its strong presence in theinternational energy markets.”

What’s top of your agenda for 2011?“To consolidate our rapid acquired growthand integrate the new operations so that wecan offer a cohesive international ÅF range.”

What’s the best thing about ÅF?“ÅF has expanded its international operationsconsiderably over the last five years. At thesame time we have consistently deliveredsound financial results and are now theworld’s sixth-largest international consultantin power and energy.”

tional, a Spanish-based consulting company. Energy has also establisheda firm foothold in the growth regions of India and Southeast Asia.The division’s specialist expertise, breadth of experience and ability to

take projects from the drawing board to implementation are some of thekey factors behind its success.The Energy Division offers a broad spectrum of services that includes

aspects of technology, financing, management and energy consulting.While assignments are frequently connected to major investment projects,the division also takes on projects to increase the efficiency and capacityof existing plants and offers strategic advice at managerial level on energymarkets and power deals. It also carries out environmental and safetyinvestigations.Most of Energy’s turnover is derived from services relating to invest-

ments in power plants. Consultants offer support throughout the life cycleof a project: analyses and feasibility studies in the initial stages, pre-engi-neering and engineering once the investment decision has been made,and project management during the implementation phase. This includesservices such as project steering, the basic design of process solutions,procurement negotiations, manufacturing, design and installation inspec-

2 3

2 4

Å F A N N U A L R E P O R T 2 0 10

O P E R AT I O N S E N E R G Y D I V I S I O N

ENERGY

tions, and functionality testing. Once the plant is fully opera-tional the division can also assist with a range of other services,from troubleshooting to maintenance planning.

Clients – large-scale projects and partnershipsEnergy’s clients are private and publicly owned energy compa-nies, energy-intensive industries, public institutions and financialinstitutions. These clients’ investments are usually large-scaleand extend over many years. As such, client relationships arelong-term and often characterised by a sense of partnership.Thanks to the fact that the division has established a presencein many different locations, geographical proximity to clients isgood.• The division currently has several hundred clients.• A large proportion of clients come back with repeat business.• The ten largest clients account for 39 percent of the division’ssales.

• Clients include Alpiq (Switzerland and Central Europe), Fortum(Nordic countries and Russia), Energo Service and Remener-gomontazh (Russia), CEZ (the Czech Republic and EasternEurope) and many national power companies such as EestiEnergia, Latvenergo, Lietuvos Elektrine and ElectrobrasNuclear Brazil.

Market and trends – healthy order books and marketrecoveryThe division began 2010 with major projects on its books, whichensured a satisfactory level of capacity utilisation. However,economic uncertainty meant that the markets in Russia, the Bal-tic countries, Finland and Southeast Asia suffered a downturnafter the orders had been secured, which resulted in reducedinvestments in energy and tougher price competition. Nonethe-less, 2010 brought clear signs of recovery to the investmentmarkets, and many projects that had been put on hold resumed.Despite the global recovery in the power sector, the downturn

in other process industries led to excess capacity and pressureon prices for some engineering services in Finland and the Bal-tic countries. Furthermore, the sharp drop in the value of theeuro relative to the Swiss franc caused problems for the Swissoperation.Despite these short-term difficulties, the world still has a fun-

damental need for more energy, primarily electricity. Consump-tion is increasing in many countries, driving a relentless questfor additional capacity that must be met by both conventionaland renewable forms of energy. Furthermore, existing plantneeds to be made more efficient in order to increase capacityand improve environmental performance. Sustainability issuesrelating to energy consumption have become a natural part ofcompanies’ business opportunities in more and more markets.The division expects the energy sector to remain a growth

area with considerable potential.

2 5

Å F A N N U A L R E P O R T 2 0 10

Important events in 2010

Major expansion inthe Czech RepublicIn May ÅF acquired Meacont, a Czech tech-nical consulting company headquartered inPrague. While the company’s market focusis the Czech Republic and Slovakia, it alsocarries out projects internationally.Meacont has worked for many years withÅF on various international projects. Theacquisition will strengthen ÅF’s position asa leading consulting company in the energysector, especially nuclear power.

Significant energyproject in LatviaIn the spring the Latvian state energycompany Latvenergo appointed ÅF astechnical consultant for the constructionof a new gas-fired power station in Riga,scheduled to start operations in the sum-mer of 2013. ÅF is responsible for projectmanagement, design review, commission-ing services and quality control.

Important energyprojects in northernFinland and LithuaniaAt the beginning of the year Energy won amajor energy contract in Finland for designand project management services for thenew Uleåborg Energi power station in thenorth of the country. It is what is known asa “waste-to-energy” unit, where electricityis generated from incinerating householdand industrial waste.

In Lithuania ÅF won a similar project forFortum for technical consulting servicesand project management for the construc-tion of a new power station in Klaipeda.

Both of these waste-incineration facilitiesare the first of their kind in their region.

Expansion in SpainDecember saw ÅF’s acquisition of theinternational energy and managementconsultancy Mercados Energy MarketsInternational. Headquartered in Madrid,Spain, the company also has offices inRussia, the UK, Turkey, India and Italy.Mercados EMI has established an inter-national reputation as a technical consul-tant with extensive experience in the areasof energy studies, policy design, paymentmodels and energy reforms for govern-ment agencies and energy companies inmore than 40 countries.

New power stationsin EstoniaIn November the Energy Division signed anagreement with the Estonian state powercompany Eesti Energia AS on technical con-sulting services for the construction of a newsteam turbine plant in Narva. The project willdraw on the expertise and resources of ÅF’soffices in Finland, Sweden, Estonia and theCzech Republic.

In December Eesti Energia went on toappoint ÅF as lead technical consultant onthe construction of a new waste-to-energypower station in Maardu, Estonia.

International hydro-power projectsDuring the year ÅF signed contracts towork on several international hydropowerprojects in countries that included Indiaand Switzerland.

O P E R AT I O N S E N E R G Y D I V I S I O N

A V S N I T T Å F 2 0102 6

Å F A N N U A L R E P O R T 2 0 10

ENERGY

Å F A N N U A L R E P O R T 2 0 10

Transforming the Alpsinto storage batteries

2 7

The Nant de Drance pumped-storage facilitywas conceived to exploit the enormous hydro-electric potential of the Swiss Alps. The plantis jointly owned by two listed energy utilitiesand a railway operator. ÅF-Colenco’s engi-neers were assigned responsibility for allphases of the project, from design engineer-ing and issues relating to permits to commis-sioning. The new underground facility makesuse of a difference in height of more than 350metres between two reservoirs connected viaa system of subterranean channels, and willhave a capacity of 900 megawatts. Betweenthe reservoirs a huge gallery is being exca-vated to house a power station with six 150-megawatt pump-turbines. When demand forelectricity is low, the turbines will pump thewater from the lower to the upper reservoirin a process similar to that of charging abattery. When demand increases, the waterthat has previously been pumped up can beused to produce electricity. In all, some 14kilometres of tunnels and chambers need tobe excavated in the mountainside to provideaccess and house the logistics.

“We chose an external specialist with the compe-tence to design, plan and assist in all aspects ofthe project development and implementation.ÅF-Colenco was one of the forerunners throughoutthe selection process because of the company’sprevious experience from similar major projects.ÅF-Colenco works across a wide spectrum of engi-neering activities, offering specialist expertise indisciplines such as civil engineering, deep mining,electromechanics, electrical engineering, automa-tion and construction technologies. The companyhas a proven track record of its ability to deliverand to act promptly if delays occur. Everyone knowswhat they have to do and how to do it, and a strongteam spirit has always been one of the distinguish-ing characteristics of the company.”

Eric Wuilloud, CEO Nant de Drance Ltd.,Martigny, Switzerland.

SwitzerlandPhoto: Jean-Luc Lugon

2 8

Å F A N N U A L R E P O R T 2 0 10

O P E R AT I O N S I N D U S T R Y D I V I S I O N

INDUSTRY

31%

Boosting client profitabilitythroughout the business cycle

The Industry Division is the leading technicalconsultant for industries in the Nordic regionand enjoys a unique standing in industrialautomation. This is a field in which consultingservices are in demand throughout the busi-ness cycle, as automation provides excellentopportunities for clients to improve profitabil-ity and reduce their environmental impact.Geographical proximity to clients, a thoroughunderstanding of the sectors in which they

work and experience gained from previousprojects pave the way for long-term clientrelationships.

The offer: from pre-study to commissioning– and more full-service projectsThe Industry Division is the largest independent consultant in itsfield in the Nordic region, with responsibility for energy andnuclear power assignments in Scandinavia, where it cooperatesclosely with the Energy Division. In all other sectors of industrythe division operates worldwide.

Å F A N N U A L R E P O R T 2 0 10

Contribution toGroup sales

Key figures 2010 2009

Operating income (in millions of SEK) 1,340.0 1,386.8

Operating profit (in millions of SEK) 119.9 129.9

Operating margin, % 9.0 9.4

Contribution to Group income % 31 32

Number of employees (FTEs) 1,200 1,222

Operating profit per FTE (in thousands of SEK) 100 106

The historical figures above have been adjusted, proforma, to take account ofthe corporate restructurings implemented on 1 January and 1 October 2010.

Å F A N N U A L R E P O R T 2 0 10

Industry Division – facts at a glance

• Responsible for energy and nuclear power assignments in Scandinavia and otherindustrial contracts worldwide.

• Offers engineering consulting services in all fields and in all sectors of industry.

• 1,300 co-workers in some 50 offices in Sweden, Norway, Denmark, Germany,Spain, Estonia and South Africa.

• Contribution to total Group sales: 31 percent.

• Approximately 20 percent of assignments are conducted outside Sweden.

Meet Per MagnussonPresident, Industry Division

What were you happiest about in 2010?“I’m proud of the fact that – despite toughtimes for industry and growth that had stag-nated in absolute terms – we succeeded inwinning new assignments and developingour existing business. This meant that weincreased our market share from nine per-cent to eleven percent.”

What’s top of your agenda for 2011?“Strong growth! I’m convinced there’s a verygreat need for our services. I’m counting onthe lion’s share of growth in 2011 being organic.We will be placing great emphasis on this inall areas of the division throughout the year.”

What’s the best thing about ÅF?“The people who work here! They’re outstand-ing. There’s a unique mix of experience andpioneering spirit at ÅF that I’ve never encoun-tered anywhere else. When we work together,we’re more than a match for every challenge.That creates the basis for close relations withour clients – a kind of partnership, with vestedinterests in one another’s development andsuccesses.”

The Industry Division provides experienced process engineers withskills in most sectors, multidisciplinary project leaders for major projects,technical specialists and a broad spectrum of engineering expertise, totake care of every link in the chain, from feasibility studies to the finishedplant. The division’s main focus areas are process technology, designand analysis calculations, control technology, industrial IT, automation,electrical power systems, mechanical engineering, piping design andinspections.Services are aimed at companies with industrial production facilities.

Consultants can work as an integral part of the client’s own organisation;alternatively, the division can assume total overall responsibility for thedelivery of a specific function or even an entire project. Most contractsinvolve modernising existing facilities or making them more efficient, butthe division is, of course, also involved in building new industrial plants.The division’s long experience and cutting-edge know-how are provinga valuable combination as various aspects of sustainability becomeincreasingly important for clients in industry.

2 9

3 0

Å F A N N U A L R E P O R T 2 0 10

O P E R AT I O N S I N D U S T R Y D I V I S I O N

INDUSTRY

Typical assignments include technology and financial impactassessments to produce the documentation on which clientsbase decisions on future investments, control technology for pro-duction lines, the integration of production systems and businessmanagement systems, and design engineering projects for bio-fuel furnaces or nuclear power plants.

Clients – a broad cross-section, low sensitivity to theeconomic cycleThe Industry Division offers services to all sectors of industrybut enjoys a particularly strong standing in energy, nuclearpower, mining, food technology, pharmaceuticals, pulp andpaper, and other process industries. Not only does this diverseclient base across a range of industries leave the division rela-tively unscathed by ups and downs in the business cycle, thedivision’s offer also remains attractive whatever the health ofthe economy: industry has a constant need for improvements inproductivity, environmental adaptations and measures to saveenergy and improve safety.The division works in geographical proximity to its clients and

collaborates closely with them. The strategy is for around 80 per-cent of the division’s business to be generated by local clients,while the remaining 20 percent derives from joint projects withother units within the division or with other ÅF divisions. This cre-ates flexibility within the organisation and the ability to accommo-date clients’ expansion ambitions. Consequently, relationshipswith clients are increasingly assuming the character of partner-ships, where the division shoulders a great deal of responsibilityfor the delivery of the projects as a whole.

• The division has approximately 3,400 active clients.• The ten largest clients account for 30 percent of the division’searnings.

• The largest single client accounts for 8 percent of earnings.• Major clients include ABB, Fortum, Korsnäs, LKAB, Novo Nor-disk A/S, Rexcell Tissue, Siemens, SSAB, the municipal waterutility Stockholm Vatten, Sweden’s nuclear power plants atForsmark and Ringhals, and Westinghouse.

Market and trends – efficiency improvements andredeployment of resourcesThe Industry Division is a market leader in the Nordic regionwith a market share of eleven percent.The division’s strengths in automation proved invaluable during

the economic downturn: with the main emphasis of most newassignments on making existing operations more efficient, Indus-try won new shares of a market that, as a whole, had more orless stagnated.After a sluggish start to the year, by September there were at

last clear signs of a recovery in the business cycle. While this wasevident in all sectors, demand remained strongest for efficiencyimprovements in production plants, environmental projects, thedevelopment of alternative fuels and energy-efficiency conver-sions. In geographical terms, operations are strongest in the min-ing industry in the north of Sweden and in the energy and pharma-ceutical industries in the south of Sweden.

3 1

Important events in 2010

Continued investmentin focus area ofnuclear powerDuring the autumn ÅF acquired the tech-nical consulting company Platom AB. Theacquisition will strengthen the IndustryDivision’s offer in the field of nuclearpower with high-quality process andanalysis services.

Major investmentin miningThe summer saw the acquisition of the tech-nical consulting company VPC Mining fromVattenfall. The company provides high-qualityengineering services for the mining industryand will enable ÅF to consolidate its positionas one of pre-eminent technical consultingcompanies in the north of Sweden. The miningsector grew strongly during the year, and ÅFcoordinates and develops projects through itsMining Competence Centre. ÅF is involved in anumber of projects, including a major prospect-ing project in Pajala for Northland Resources.

Important project inenergy/pulp and paperIn April ÅF was appointed lead technicalconsultant for the investment in a newblock heat power plant on the Korsnäsindustrial site in Gävle, Sweden, adjacentto the Korsnäs pulp and paper mill. Theclient is Bomhus Energi AB, which is jointlyowned by forestry group Korsnäs and muni-cipal power company Gävle Energi. This ÅFassignment is a multidisciplinary EPCMproject that covers all areas of technologyrelating to the investment, including projectmanagement and administration. Readmore overleaf.

Strategic investmentin hydropower andelectricity networksThe end of the year brought the acquisitionof Energo, which has operations in Stock-holm, Malmö and Helsingborg. This willstrengthen Industry’s position in hydro-power, dam safety, windpower, electricalnetworks and power supply. The Infrastruc-ture Division and Technology Division alsostand to benefit from Energo’s specialistexpertise.

Stronger position inSwedish energyAt the end of the year ÅF signed a four-yearcontract as an ‘A’ supplier to Vattenfall. Indoing so, ÅF strengthened its position as astrategic partner in nuclear power, hydro-power and windpower. The agreement re-lates to the provision of technical consult-ing services in all disciplines. ÅF intendsto step up its recruitment of personnelwith experience in the energy sector asa consequence of the agreement.

O P E R AT I O N S I N D U S T R Y D I V I S I O N

A V S N I T T Å F 2 0103 2

Å F A N N U A L R E P O R T 2 0 10

INDUSTRY

Å F A N N U A L R E P O R T 2 0 10

3 3

Gävle, SwedenPhoto: Andreas Björklund

Municipality andindustry join forceson district heatingBomhus Energi is a new energy company thatis jointly owned by forestry company KorsnäsAB and municipal power company GävleEnergi. The two teamed up to build a jointpower plant when Korsnäs wanted to makeits energy process more efficient and GävleEnergi needed to guarantee a good price forits district heating. ÅF was assigned to runthe project, which involves overall projectmanagement, project planning, financialfollow-ups, HSE work and quality follow-ups,and process, pipe, low-voltage and instru-ment project engineering.

“Korsnäs has been working with consultants fromÅF for many years on both environmental and pulpand paper projects that have required expertise inprocess engineering and energy. In our opinion,ÅF has highly skilled employees. They are easy towork with and can make a quick start on projectsas they know our industry so well. We’ve alwaysbeen pleased with the work they’ve done for us,which is why we’ve gone back to them time andagain. ÅF won the important job of lead consultantfor the construction of the new power plant prima-rily because of the company’s track record in theindustry and its undisputed ability to deliver.”

Mats Törnkvist,Technical Director, Korsnäs AB

3 4

Å F A N N U A L R E P O R T 2 0 10

O P E R AT I O N S I N F R A S T R U C T U R E D I V I S I O N

29%

INFRASTRUCTURE

Market leader with sustainablesolutions for tomorrow’s world

The Infrastructure Division leads the Scandi-navian market for technical solutions forinfrastructure projects. The division’sstrengths include a strong sales organisa-tion, sound commercial skills and a portfolioof services with a firm focus on sustainabil-ity. The division is continuously enhancing itsmarket potential by developing innovativesolutions that boost client profitability andsupport clients’ target fulfilment aspirations.

The offer – sustainability integral to all servicesThe Infrastructure Division comprises five business areas: Instal-lations, Environment, Rail, Roads and Sound & Vibrations.Installations is the largest of the division’s business areas and

Sweden’s number one technical consultant for qualified servicesrelated to the construction and modernisation of commercial,industrial and public-sector premises. Many of its assignmentsrevolve around improving functionality, reducing operating costsand enhancing environmental performance.Rail offers everything from surveys and investigations to

more technically oriented installations assignments where thefocus is on track-laying, electrical and signalling systems, and

Å F A N N U A L R E P O R T 2 0 10

Contribution toGroup sales

Key figures 2010 2009

Operating income (in millions of SEK) 1,233.1 1,167.6

Operating profit (in millions of SEK) 69.0 101.9

Operating margin, % 5.6 8.7

Contribution to Group income % 29 27

Number of employees (FTEs) 1,065 994

Operating profit per FTE (in thousands of SEK) 65 103

The historical figures above have been adjusted, proforma, to take account ofthe corporate restructurings implemented on 1 January and 1 October 2010.

Å F A N N U A L R E P O R T 2 0 10

Infrastructure Division – facts at a glance

• Clients in the property market, construction and industrial plant, and the publicsector.