Embed Size (px)

Citation preview

Alternative Energy Sector 2014 Outlook

Yin Lei

December 2013

文件名称 日期

Chapter 1 Solar sector review and outlook 5

Chapter 2 Wind sector review and outlook 14

Chapter 3 Valuation and stock picks 20

2

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

3

Wind power upstream industries: earnings recovery and valuation expansion

Wind power downstream industries: grid curtailment further improves; wait for

incentive policies

Solar upstream industries: recovering total demand; stable price; cost and new

techniques

Solar downstream industries: golden period for solar farm development; new business

model

Investment suggestions: we prefer solar downstream and wind power upstream

industries

Stock picks: Goldwind (2208 HK), Goldpoly (686 HK) and Guodian T&E (1296 HK)

Key points

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

4

Company Code Mkt cap Price EPS PE PB ROE %

Rating 2012 2013E 2014E 2012 2013E 2014E 2012 2013E 2014E 2012 2013E 2014E

Goldwind 2208

HK 28288 7.58 0.06 0.15 0.32 126.33 50.87 23.69 1.58 1.55 1.46 1.25 3.05 6.18 Buy

CHS 658 HK 5478 3.89 0.19 0.09 0.30 16.81 35.50 10.53 0.56 0.58 0.56 4.14 3.54 5.43 NR

Longyuan 916 HK 79965 9.97 0.38 0.38 0.49 20.65 20.71 15.98 2.02 1.90 1.73 9.94 9.56 11.15 Neutral

Datang 1798

HK 10983 1.53 0.02 0.05 0.08 102.00 28.87 18.21 1.26 1.23 1.16 1.24 4.27 6.36 Neutral

Huaneng 958 HK 27199 3.38 0.07 0.14 0.18 36.68 18.61 13.83 1.80 1.63 1.47 5.09 9.16 11.08 NR

GCL-Poly 3800

HK 39325 2.54 -0.07 -0.06 0.09 N/A N/A 29.20 1.98 2.53 2.34 -3.77 -5.74 6.72 Buy

Comtec 712 HK 2077 1.61 0.05 0.04 0.10 25.54 29.19 12.14 0.88 0.94 0.87 -3.61 3.53 7.23 Buy

Singyes 750 HK 5964 8.85 0.59 0.79 0.94 11.46 8.58 7.21 2.27 1.85 1.48 21.32 22.93 22.69 Buy

Hdfx 816 HK 20276 2.68 0.17 0.20 0.23 12.44 10.61 8.93 1.49 1.30 1.14 13.42 13.28 13.94 Buy

Jingneng 579 HK 23189 3.65 0.14 0.20 0.29 20.10 13.93 9.57 N/A 1.68 1.46 N/A 12.67 16.19 Buy

Figure: Company earnings forecast

Source: Bloomberg, CMS(HK) Notes: closing prices as of Nov. 29

文件名称 日期 Chapter 1

Solar sector review and outlook

5

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

Solar sector review and outlook

6

Solar industry research framework - factor analysis

Solar sector 2013 review

Solar sector 2014 outlook

1

2

3

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

7

Solar value chain: poly-silicon/mono-crystal silicon-wafer-cell-module-EPC-operation

Poly-silicon: price; cost; poly-silicon import; anti-dumping; GCL(3800.HK), DQ(DQ US EQUITY),

TBEA(600089.CH)

Mono wafer: high conversion efficiency; the US, Japan and China; Comtec(712.HK), Longi(601012.CH),

Zhonghuan(002129.CH)

Cell & module: gross margin; debt ratio; price & cost; overseas demand; US listed companies

EPC/Operating: EPC ASP; EPC gross margin; IRR; Goldpoly(686.HK), Zhongli(002309.CH), Huabei

Expressway(000916.CH), GCL(3800.HK), Guodian T&E(1296.HK), Singyes(750.HK)

Fundamentals

Policy: newly added installation plan; FIT policy change

Earnings: earnings turning point of the whole industry has appeared

Demand: domestic market emerges; weakened EU market; strong demand from the US & Japan

Generation cost: grid parity in the near future; new techniques and high conversion efficiency

Stock price factors

Policy change, price, new orders, earnings trend, event driven

Unique opinions

Industry recovery, not short term rebound; closer to the grid parity

Steady industry recovery; overcapacity may not be a great concern

Solar industry research framework - factor analysis

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

8

2013 in review

Solar trade war between China & the EU

Better than expected EU anti-dumping case

Price guarantee agreement: a minimum import price for Chinese solar panels of €0.56 per Watt has been

set with no more than 7GW of product entering the EU market from China annually

The anti-subsidy investigation would continue

Finally, import price of Chinese solar panels has actually increased around 20%; Chinese panel makers only

lose 30% of the original market share in the EU

Disappointing poly-silicon anti-dumping in China

In July, China’s Ministry of Commerce(MOFCOM) imposed anti-dumping import tariff of to 53.7%-57% on

solar-grade poly-silicon from the US and of 2.4%-48.7% from South Korea but did not impose anti-dumping

tariff on solar-grade poly-silicon from the EU temporarily.

In September, China’s Ministry of Commerce imposed preliminary anti-subsidy duties on some solar-grade

poly-silicon imports from the U.S. Beginning on September 20, importers of poly-silicon from Hemlock

Semiconductor Corp and AE Poly-silicon Corp will have to pay the duties.

The poly imports to China in 2013Q3 was 19,723 MT, representing a 10.03% increase from 17,925MT in Q2.

The unit price was slightly higher but is likely to stay below the manufacturing cost of foreign producers. The

poly imports from US and South Korea in September were mainly in the form of processing trade and

imports through tax-free zones, leading to lower-than-expected ASP increase of poly-silicon.

China's Ministry of Commerce announced on October 31, 2013 that it will extend its anti-dumping and anti-

subsidy investigations of solar-grade poly-silicon imports from the EU for another six months.

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

9

2013 in Review

Figure: Monthly poly import in China

Disappointing poly-silicon anti-dumping in China

Since August, poly-silicon import has remained high and import price has remained

low

Stock price of GCL-Poly fluctuated with the price of poly-silicon

Figure: GCL stock price & poly price

Source: Company data, Wind Source: PVinsights

18.5

17.7

19.4

18.0 18.2

18.8

20.0

18.8

19.6

18.3

16.5

17.0

17.5

18.0

18.5

19.0

19.5

20.0

20.5

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2013/0

1

2013/0

2

2013/0

3

2013/0

4

2013/0

5

2013/0

6

2013/0

7

2013/0

8

2013/0

9

2013/1

0

Poly import(MT) ASP($/w)

10.0 11.0 12.0 13.0 14.0 15.0 16.0 17.0 18.0 19.0 20.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

20

13-0

1-0

2

20

13-0

1-2

3

20

13-0

2-1

3

20

13-0

3-0

6

20

13-0

3-2

7

20

13-0

4-1

7

20

13-0

5-0

8

20

13-0

5-2

9

20

13-0

6-1

9

20

13-0

7-1

0

20

13-0

7-3

1

20

13-0

8-2

1

20

13-0

9-1

1

20

13-1

0-0

2

20

13-1

0-2

3

20

13-1

1-1

3

GCL-Poly stock price(HK$) Poly price(US$/w)

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

10

2013 in Review

Solar policy review and outlook

Existing policy March 1st: State Grid-Comments on grid connection of distributive generation

May: Ministry of Finance-Notice of auditing of Golden Sun subsidy

June 16th: NEA-Drafts on demonstration area of solar distributive generation

July 15th: the State Council-Opinions on promoting healthy development of solar industry

July 18th: NDRC-Interim measures of management of solar generation

July 24th: Ministry of Finance-New FIT policy of solar distributive generation

August 9th: NEA-Notice about demonstration area construction of solar distributive

generation

August 26th: NDRC-Notice about using price tools to promote healthy development of the

solar industry

August 30th: NDRC-Notice about adjustment of electricity price surcharge of renewable

energy

September: NEA-Interim measures of solar project management

September: The Ministry of Industry and Information Technology-Standards of solar

manufacturing industry

September: NEA&NDB-Opinions on supportive financial services of solar distributive

generation

November: NEA-Interim measures of solar distributive generation

December: NEA-Interim measures of operation and supervision of solar generation

Upcoming policies Renewable Portfolio Standard (under review)

The Ministry of Industry and Information Technology-Guidance on M&A of the solar

industry(under review)

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

11

2013 in Review

Figure: Quarterly gross margin of US listed solar

stocks

In 1H2013 earnings turning point of the industry was confirmed

In Q3, profit margins continued to improve.

Main reasons: increased cell & module prices; some companies extend the business

to downstream solar farms.

Figure: Quarterly net profit margin of US listed

solar stocks

-200%

-150%

-100%

-50%

0%

50%

100%

3Q

2010

4Q

2010

1Q

2011

2Q

2011

3Q

2011

4Q

2011

1Q

2012

2Q

2012

3Q

2012

4Q

2012

1Q

2013

2Q

2013

3Q

2013

Trina Yingli LDK JA SolarHanwha Canadian Solar ReneSola JinkoCSUN DQ

-1400%

-1200%

-1000%

-800%

-600%

-400%

-200%

0%

200%

3Q

2010

4Q

2010

1Q

2011

2Q

2011

3Q

2011

4Q

2011

1Q

2012

2Q

2012

3Q

2012

4Q

2012

1Q

2013

2Q

2013

3Q

2013

Trina Yingli LDK JA SolarHanwha Canadian Solar ReneSola JinkoCSUN DQ

Source: Bloomberg Source: Bloomberg

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

12

Solar Industry 2014 Outlook

Macro View

Government continues to strongly support the whole industry

Market performances may differentiate after announcement of the annual results

Marginal utility of incentive policies for stock prices may decrease

Meso View

Distributive generation vs concentrated generation: Distributive generation is the future trend. In the short

term, however, concentrated projects have higher IRRs.

EPC only vs new business model: Gross margin of solar EPC has downside risks. Solar projects with

favorable grid connection are scarce resources. Financing may be a problem for private companies.

Opportunities for solar manufacturing: new techniques to improve the conversion efficiency and decrease

the cost; extension to solar farm business; M&A

Micro View

Goldpoly(686.HK): Brand new business model may be recognized by the market.

Guodian T&E(1296.HK): provides solar EPC for Goldpoly

GCL-Poly(3800.HK): captive power plant in Q1, FBR techniques in Q4, and solar farm business

Comtec(712.HK): The market may expect a turning point of profit margins; enlarged customer base

Singyes Solar(750.HK): EPC gross margin and new EPC orders

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

13

Solar Industry 2014 Outlook

Figure: 2013-2014 Global Solar Installation Forecast

According to IHS’s report, global new installation may reach 40-45GW in 2014 with an

increase of 15% YoY.

According to NEA’s guidance, China will increase 8 GW solar distributive generation

and 4GW concentrated projects.

According to Opinions on promoting healthy development of the solar industry issued

by the State Council, at least 10 GW solar projects will be installed each year between

2013 and 2015.

Figure: 2013-2015 China Solar Installation Forecast

Source: CMS(HK) estimates

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2008 2009 2010 2011 2012 2013E 2014E 2015E

New installation(GW) Distributive generation(GW)

文件名称 日期 Chapter 2

Wind sector review and outlook

14

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

Wind sector review and outlook

15

Wind sector research framework- factor analysis

Wind sector 2013 review

Wind sector 2014 outlook

1

2

3

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

16

Wind sector value chain: components - wind turbine - wind farm operation

Components: gearbox, electronic control system, generator, blade, tower and etc

Wind turbine: direct drive and double fed; Goldwind(2208.HK)

Wind farm operation: power generation groups such as Longyuan(under Guodian Group)

Fundamental factors

Components & Wind turbine: gross margin, price, demand

Wind operating: utilization hour, grid curtailment, wind turbine price, debt ratio and policy

Stock price factors

Policy expectation, new capacity, grid curtailment, industry consolidation

Unique views

Optimistic views on earnings recovery and valuation expansion

Optimistic views on grid curtailment

Incentive policies deserve attention

Wind sector research framework - factor analysis

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

17

2013 in review

Figure: Quarterly open tender of wind turbine/GW

Wind turbine tender totaled12.8GW in the first three quarters of 2013 and is expected to reach

15GW in 2013 (+80% YoY). NEA has approved 90GW projects so far (60% of which have not

started bidding or are not under construction)

Wind turbine bidding prices remain stable and industry leaders enjoy price premium. Wind turbine

gross margins improve significantly. In the short term, however, increasing transport cost as more

projects are located in southern provinces may deserve attention.

Figure: Wind turbine price trend and Goldwind’s profit

margins

Source: Company data, CMS(HK) estimates

8.4

3.9

3.0

5.5

2.2 2.2

1.4

2.5

3.8

5.0

4.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Source: Company data, CMS(HK)

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

3,400

3,500

3,600

3,700

3,800

3,900

4,000

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

Wind turbine price(yuan/kw)

Gross margins of Goldwind

Net profit margins of Goldwind

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

18

2013 in Review

Figure: Wind turbine market share in 1H2013

Wind turbine market share: In 1H, market concentration ratio increased (88% for top

10 players). Market shares of Goldwind and Mingyang increased, while market shares

of Sinovel and Dongfang Electric decreased.

Accelerated UHV line construction: Two lines are finished in 2013 (one is Hami to

Zhengzhou South with 6GW transmission capacity, which has not started bidding).

Three lines are expected to be finished in 2014. Planned transmission capacity may

reach 137GW as of the end of 2015.

Figure: Key planned transmission lines

Source: Company data Source: Company data, CMS(HK)

Goldwind, 23.30%

United Power, 14.60%

Mingyang, 10.20%

XEMC, 9.30%

Shanghai Electric, 8.50%

Sinovel, 7.10%

Haizhuang, 5.70%

Envision, 4.50%

Gamesa, 2.50%

Dongfang Electric, 2.40%

Others, 11.90%

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

19

Wind industry 2014 outlook

Macro view

Government supports the development of renewable energy

Meso view

Industry recovering trend. We prefer wind turbine & components stocks.

Incentive policies: Opinions on promoting healthy development of the wind power industry, Renewable

Portfolio Standard

Micro view

Goldwind(2208.HK): industry recovery, earnings recovery, more concentrated market

Figure: 2013-2015 new installation forecast Figure: New capacity plans for leading wind operators

Source: CWEA, CMS(HK) Source: Company data, CMS(HK) estimates

0

500

1000

1500

2000

2500

Longyuan Huaneng Renewables

Datang Renewable

Power

2011 2012 2013E 2014E

3.3 6.2

13.8

18.9 17.6

13.0 15.0

18.0 20.0

0

20

40

60

80

100

120

140

0

5

10

15

20

25

New installation/GW Accumulated installation/GW

文件名称 日期 Chapter 3

Valuation and stock picks

20

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

Valuation and stock picks

21

Indices and sector performance

Sector valuation

Stock picks

1

2

3

Valuation and ratings of HK listed stocks 4

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

HK solar stocks lag behind HK wind stocks

22

Figure: Wind Renewable Energy Index Figure: S&P Global Clean Energy Index

Source: Wind, CMS(HK) Source: Bloomberg, CMS(HK)

Figure: Stock performance of solar sector Figure: Stock performance of the wind sector

Source: Bloomberg, CMS(HK) Source: Bloomberg, CMS(HK)

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

350%

S&P Global Clean Energy Index

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Wind Renewable Energy Index

-100%

-50%

0%

50%

100%

150%

2010-01-01 2011-01-01 2012-01-01 2013-01-01

HK solar sector HSI Index

-40%

-20%

0%

20%

40%

60%

80%

100%

HSI Index HK Wind Sector

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

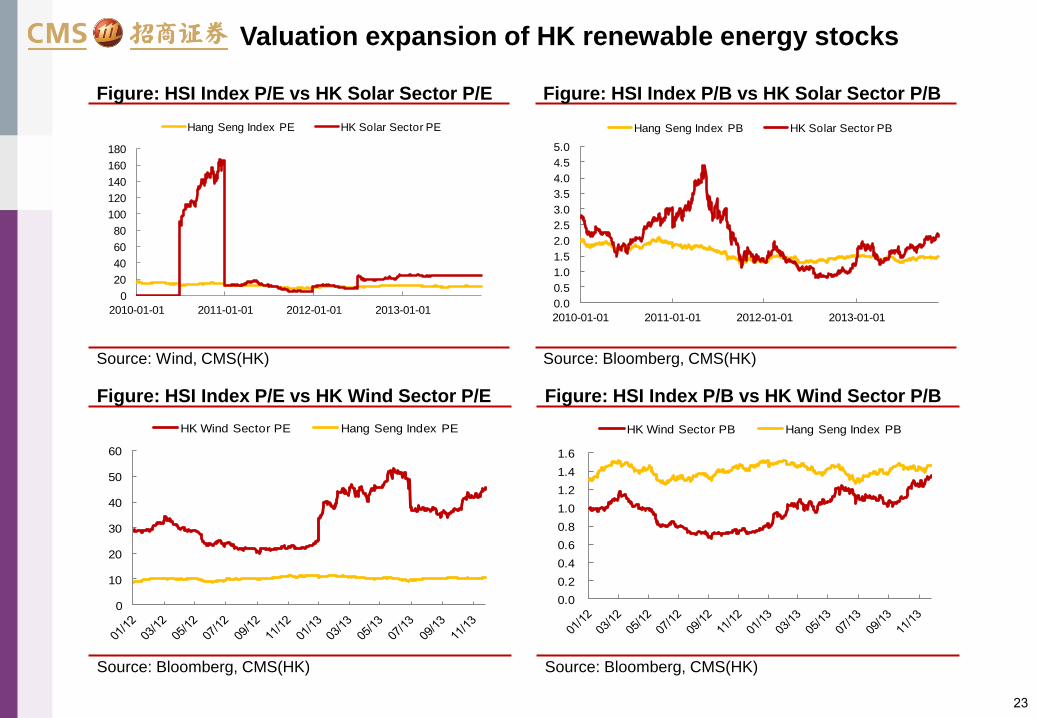

Valuation expansion of HK renewable energy stocks

23

Figure: HSI Index P/E vs HK Solar Sector P/E Figure: HSI Index P/B vs HK Solar Sector P/B

Source: Wind, CMS(HK) Source: Bloomberg, CMS(HK)

Figure: HSI Index P/E vs HK Wind Sector P/E Figure: HSI Index P/B vs HK Wind Sector P/B

Source: Bloomberg, CMS(HK) Source: Bloomberg, CMS(HK)

0

20

40

60

80

100

120

140

160

180

2010-01-01 2011-01-01 2012-01-01 2013-01-01

Hang Seng Index PE HK Solar Sector PE

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2010-01-01 2011-01-01 2012-01-01 2013-01-01

Hang Seng Index PB HK Solar Sector PB

0

10

20

30

40

50

60

HK Wind Sector PE Hang Seng Index PE

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

HK Wind Sector PB Hang Seng Index PB

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

Our sock picks

24

Goldwind (2208.HK, HK$7.58, Buy, TP HK$10.04): Strong leading position

Industry recovery: New installation may resume positive growth in 2013

Strong leading position: In 1H2013, domestic market share of Goldwind reached of 23%.

Improving condition for grid curtailment: Accelerated UHV line construction; increased new

capacity plans for wind farm operators

Robust price: Recovering gross margin. Goldwind still enjoys around 7% price premium.

Figure: 2013-2015 revenue forecast and YoY growth Figure: 2013-2015 net profit forecast and YoY growth

Source: Company data, CMS(HK) Source: Company data, CMS(HK)

12810 11273

12865

16142

19042

-27%

-12%

14%

25%

18%

-30%

-20%

-10%

0%

10%

20%

30%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2011

2012

2013

E

2014

E

2015

E

Revenue yoy%

mil RMB

607

153

415

858

1210

-74% -75%

171%

107%

41%

-100%

-50%

0%

50%

100%

150%

200%

0

200

400

600

800

1000

1200

1400

2011

2012

2013

E

2014

E

2015

E

Net profit yoy%

mil RMB

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

Our stock picks

25

Goldpoly (686.HK, HK$1.75, Not Rated): innovative business model

Strong shareholder background: China Merchants New Energy Group is the single largest shareholder of the

company. China Merchants New Energy Group, a subsidiary of China Merchants Group, is engaged in investment,

development and operation of solar power plants. Goldpoly has been granted exclusive rights of developing solar

resources of China Merchants Group.

Abundant strategic co-operation resources: Goldpoly has established ‘PGO’ with peers. In this organization,

GD solar, GCL, Singyes Solar, etc. take charge of development and construction of solar farms, CDB and China

Merchants Group provide financial support, and Goldpoly takes charge of investment, acquisition and operation of

solar farms.

Special capacity expansion model: Goldpoly only acquires grid-connected solar power plants. Required IRRs

(unleveraged) of target projects are around 9%. Project sellers must guarantee the solar power generating capacity

(within a period of 8 to 10 years).

Figure:2009-2012 revenue and YoY growth Figure: 2009-2012 net profit and YoY growth

Source: Company data, CMS(HK) Source: Company data, CMS(HK)

98

250

843

225

154%

238%

-73%-100%

-50%

0%

50%

100%

150%

200%

250%

300%

0

100

200

300

400

500

600

700

800

900

2009

1010

2011

2012

Revenue yoy%

mil RMB

-24 -15

-1149

-815

0%

20%

40%

60%

80%

100%

120%

-1400

-1200

-1000

-800

-600

-400

-200

0

2009

1010

2011

2012

Net profit yoy%

mil RMB

文件名称 日期

R: 235 G: 213 B: 235

R: 200 G: 140 B: 200

R: 154 G: 170 B: 182

R: 130 G: 62 B: 130

R: 191 G: 191 B: 191

R: 127 G: 127 B: 127

R: 234 G: 236 B: 235

Our stock picks

26

Guodian T&E (1296.HK, HK$2.05, Not Rated): solar and wind turbine businesses deserve attention Bright prospect of solar EPC business: GD Solar under the company is the largest company providing solar

EPC services in China. 600MW is the breakeven point for the company’s solar business due to the heavy

investment in previous years. 500MW EPC means significant loss reduction in the second half of the year.

Recovering wind turbine business: The subsidiary Guodian United Power is the second largest wind turbine

manufacturer in China, next only to Xinjiang Goldwind. The environment for wind turbine is favorable in China, with

considerable demand, rising price and low costs. The trend of growing share of high-power generating units will

help to improve gross margin. Demand for Guodian United Power Technology’s products mainly comes from

Longyuan Power, the largest wind power operator in China. Despite slow recognition of sales, we believe the

company will enjoy evident improvement in wind turbine sales between 2014 and 2015.

Environmental protection and energy saving business: Pay attention to potential earnings drivers including green power station EPC, water treatment, and the denitration concession business.

Figure: 2008-2012 revenue and YoY growth Figure: 2008-2012 net profit and YoY growth

Source: Company data, CMS(HK) Source: Company data, CMS(HK)

3969 5355

11009

18759

21853

35%

106%

70%

16%

0%

20%

40%

60%

80%

100%

120%

0

5000

10000

15000

20000

25000

2008

2009

2010

2011

2012

Revenue yoy%

mil RMB

91 96

350

841

693

5%

267%

140%

-18%

-50%

0%

50%

100%

150%

200%

250%

300%

0

100

200

300

400

500

600

700

800

900

2008

2009

2010

2011

2012

Net profit yoy%

mil RMB

文件名称 日期

DISCLAIMER

This document is prepared by China Merchants Securities (HK) Co., Limited (“CMS HK”). CMS HK is a licensed corporation to carry on Type 1 (dealing in securities), Type 2 (dealing in futures),

Type 4 (advising on securities), Type 6 (advising on corporate finance) and Type 9 (asset management) regulated activities under the Securities and Futures Ordinance (Chapter 571). This

document is for information purpose only. Neither the information nor opinion expressed shall be construed, expressly or impliedly, as an advice, offer or solicitation of an offer, invitation,

advertisement, inducement, recommendation or representation of any kind or form whatsoever to buy or sell any security, financial instrument or any investment or other specific product.

The securities, instruments or strategies discussed in this document may not be suitable for all investors, and certain investors may not be eligible to participate in some or all of them.

Certain services and products are subject to legal restrictions and cannot be offered worldwide on an unrestricted basis and/or may not be eligible for sale to all investors.

The information and opinions, and associated estimates and forecasts, contained herein have been obtained from or are based on sources believed to be reliable. CMS HK, its holding or

affiliated companies, or any of its or their directors, officers or employees (“CMS Group”) do not represent or warrant, expressly or impliedly, that it is accurate, correct or complete and it

should not be relied upon. CMS Group will not accept any responsibility or liability whatsoever for any use of or reliance upon this document or any of the content thereof. The contents and

information in this document are only current as of the date of their publication and will be subject to change without prior notice. Past performance is not indicative of future performance.

Estimates of future performance are based on assumptions that may not be realized. The analysis contained herein is based on numerous assumptions. Different assumptions could result in

materially different results. Opinions expressed herein may differ or be contrary to those expressed by other business divisions or other members of CMS Group as a result of using different

assumptions and/or criteria.

This document has been prepared without regard to the individual financial circumstances and investment objectives of the persons who receive it. Use of any information herein shall be at

the sole discretion and risk of the user. Investors are advised to independently evaluate particular investments and strategies, take financial and/or tax advice as to the implications (including

tax) of investing in any of the securities or products mentioned in this document, and make their own investment decisions without relying on this publication.

CMS Group may have a long or short position, make markets, act as principal or agent, or engage in transactions in securities of companies referred to in this document and may also perform

or seek to perform investment banking services or provide advisory or other services for those companies. This document is for the use of intended recipients only and this document may not

be reproduced, distributed or published in whole or in part for any purpose without the prior consent of CMS Group. CMS Group will not be liable for any claims or lawsuits from any third

parties arising from the use or distribution of this document. This document is for distribution only under such circumstances as may be permitted by applicable law. This document is not

directed at you if CMS Group is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available to you. In particular, this document is only made available to

certain US persons to whom CMS Group is permitted to make available according to US securities laws, but cannot otherwise be made available, distributed or transmitted, whether directly or

indirectly, into the US or to any US person. This document also cannot be distributed or transmitted, whether directly or indirectly, into Japan and Canada and not to the general public in the

People’s Republic of China (for the purpose of this document, excluding Hong Kong, Macau and Taiwan).

27

文件名称 日期

Thank you!

28