Embed Size (px)

Citation preview

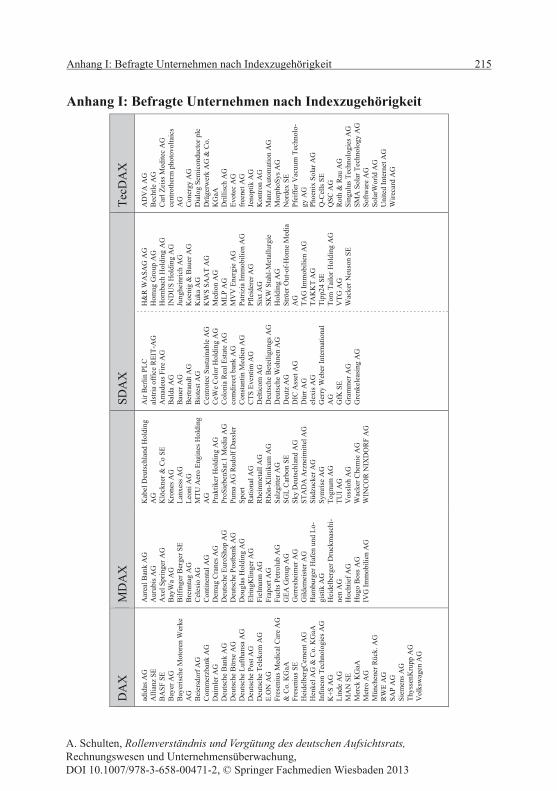

Anhang I: Befragte Unternehmen nach Indexzugehörigkeit 215

Anhang I: Befragte Unternehmen nach Indexzugehörigkeit Te

cDA

X

AD

VA

AG

B

echt

le A

G

Car

l Zei

ss M

edite

c A

G

cent

roth

erm

pho

tovo

ltaic

s A

G

Con

ergy

AG

D

ialo

g Se

mic

ondu

ctor

plc

D

räge

rwer

k A

G &

Co.

K

GaA

D

rillis

ch A

G

Evot

ec A

G

free

net A

G

Jeno

ptik

AG

K

ontro

n A

G

Man

z A

utom

atio

n A

G

Mor

phoS

ys A

G

Nor

dex

SE

Pfei

ffer

Vac

uum

Tec

hnol

o-gy

AG

Ph

oeni

x So

lar A

G

Q-C

ells

SE

QSC

AG

R

oth

& R

au A

G

Sing

ulus

Tec

hnol

ogie

s AG

SM

A S

olar

Tec

hnol

ogy

AG

So

ftwar

e A

G

Sola

rWor

ld A

G

Uni

ted

Inte

rnet

AG

W

ireca

rd A

G

SDA

X

H&

R W

ASA

G A

G

Hom

ag G

roup

AG

H

ornb

ach

Hol

ding

AG

IN

DU

S H

oldi

ng A

G

Jung

hein

rich

AG

K

oeni

g &

Bau

er A

G

Kuk

a A

G

KW

S SA

AT

AG

M

edio

n A

G

MLP

AG

M

VV

Ene

rgie

AG

Pa

trizi

a Im

mob

ilien

AG

Pf

leid

erer

AG

Si

xt A

G

SKW

Sta

hl-M

etal

lurg

ie

Hol

ding

AG

St

röer

Out

-of-

Hom

e M

edia

A

G

TAG

Imm

obili

en A

G

TAK

KT

AG

Ti

pp24

SE

Tom

Tai

lor H

oldi

ng A

G

VTG

AG

W

acke

r Neu

son

SE

Air

Ber

lin P

LC

alst

ria o

ffic

e R

EIT-

AG

A

mad

eus F

ire A

G

Bal

da A

G

Bau

er A

G

Ber

trand

t AG

B

iote

st A

G

Cen

trote

c Su

stai

nabl

e A

G

CeW

e C

olor

Hol

ding

AG

C

olon

ia R

eal E

stat

e A

G

com

dire

ct b

ank

AG

C

onst

antin

Med

ien

AG

C

TS E

vent

im A

G

Del

ticom

AG

D

euts

che

Bet

eilig

ungs

AG

D

euts

che

Woh

nen

AG

D

eutz

AG

D

IC A

sset

AG

D

ürr A

G

elex

is A

G

Ger

ry W

eber

Inte

rnat

iona

l A

G

GfK

SE

Gra

mm

er A

G

Gre

nkel

easi

ng A

G

MD

AX

Kab

el D

euts

chla

nd H

oldi

ng

AG

K

löck

ner &

Co

SE

Kro

nes A

G

Lanx

ess A

G

Leon

i AG

M

TU A

ero

Engi

nes H

oldi

ng

AG

Pr

aktik

er H

oldi

ng A

G

ProS

iebe

nSat

.1 M

edia

AG

Pu

ma

AG

Rud

olf D

assl

er

Spor

t R

atio

nal A

G

Rhe

inm

etal

l AG

R

hön-

Klin

ikum

AG

Sa

lzgi

tter A

G

SGL

Car

bon

SE

Sky

Deu

tsch

land

AG

ST

AD

A A

rzne

imitt

el A

G

Südz

ucke

r AG

Sy

mris

e A

G

Togn

um A

G

TUI A

G

Vos

sloh

AG

W

acke

r Che

mie

AG

W

INC

OR

NIX

DO

RF

AG

Aar

eal B

ank

AG

A

urub

is A

G

Axe

l Spr

inge

r AG

B

ayW

a A

G

Bilf

inge

r Ber

ger S

E B

renn

tag

AG

C

eles

io A

G

Con

tinen

tal A

G

Dem

ag C

rane

s AG

D

euts

che

Euro

Shop

AG

D

euts

che

Post

bank

AG

D

ougl

as H

oldi

ng A

G

Elrin

gKlin

ger A

G

Fiel

man

n A

G

Frap

ort A

G

Fuch

s Pet

rolu

b A

G

GEA

Gro

up A

G

Ger

resh

eim

er A

G

Gild

emei

ster

AG

H

ambu

rger

Haf

en u

nd L

o-gi

stik

AG

H

eide

lber

ger D

ruck

mas

chi-

nen

AG

H

ocht

ief A

G

Hug

o B

oss A

G

IVG

Imm

obili

en A

G

DA

X

adid

as A

G

Alli

anz

SE

BA

SF S

E B

ayer

AG

B

ayer

isch

e M

otor

en W

erke

A

G

Bei

ersd

orf A

G

Com

mer

zban

k A

G

Dai

mle

r AG

D

euts

che

Ban

k A

G

Deu

tsch

e B

örse

AG

D

euts

che

Lufth

ansa

AG

D

euts

che

Post

AG

D

euts

che

Tele

kom

AG

E.

ON

AG

Fr

esen

ius M

edic

al C

are

AG

&

Co.

KG

aA

Fres

eniu

s SE

Hei

delb

ergC

emen

t AG

H

enke

l AG

& C

o. K

GaA

In

fineo

n Te

chno

logi

es A

G

K+S

AG

Li

nde

AG

M

AN

SE

Mer

ck K

GaA

M

etro

AG

M

ünch

ener

Rüc

k. A

G

RW

E A

G

SAP

AG

Si

emen

s AG

Th

ysse

nKru

pp A

G

Vol

ksw

agen

AG

A. Schulten, Rollenverständnis und Vergütung des deutschen Aufsichtsrats,Rechnungswesen und Unternehmensüberwachung,DOI 10.1007/978-3-658-00471-2, © Springer Fachmedien Wiesbaden 2013

216 Anhang I: Befragte Unternehmen nach Indexzugehörigkeit

Prim

e

TA T

rium

ph A

dler

AG

te

chno

trans

AG

te

lega

te A

G

Tele

s AG

Info

rmat

ions

tech

-no

logi

en

Tom

orro

w F

ocus

AG

Tr

avel

24.c

om A

G

Tria

IT-s

olut

ions

AG

U

MS

Uni

ted

Med

ical

Sys

-te

ms I

nter

natio

nal A

G

Uni

ted

Labe

ls A

G

USU

Sof

twar

e A

G

VB

H H

oldi

ng A

G

Ver

bio

Ver

eini

gte

Bio

Ener

-gi

e A

G

Ver

sate

l AG

V

iller

oy &

Boc

h A

G

VIT

A 3

4 In

tern

atio

nal A

G

Vtio

n W

irele

ss T

echn

olog

y A

G

Was

hTec

AG

W

esta

g +

Get

alit

AG

W

ilex

AG

X

ING

AG

Y

OC

AG

Za

pf C

reat

ion

AG

Zh

ongD

e W

aste

Te

chno

lo-

gy A

G

R. S

tahl

AG

R

ealte

ch A

G

REp

ower

Sys

tem

s AG

R

ücke

r AG

Sa

rtoriu

s AG

Sc

haltb

au H

oldi

ng A

G

schl

ott g

rupp

e A

G

secu

net S

ecur

ity N

etw

orks

A

G

Sedo

Hol

ding

AG

SF

C E

nerg

y A

G

Silic

on S

enso

r Int

erna

tiona

l A

G

Sinn

erSc

hrad

er A

G

SMT

Scha

rf A

G

Softi

ng A

G

Sola

r-Fa

brik

AG

So

lon

SE

Stra

tec

Bio

med

ical

Sys

tem

s A

G

sunw

ays A

G

Surte

co S

E Sü

ss M

icro

Tec

AG

Sy

gnis

Pha

rma

AG

Sy

naxo

n A

G

sysk

opla

n A

G

syst

aic

AG

Sy

zygy

AG

Mag

ix A

G

Mar

seill

e-K

linik

en A

G

Mas

terf

lex

AG

M

BB

Indu

strie

s AG

M

ediC

lin A

G

Med

iGen

e A

G

MeV

is M

edic

al S

olut

ions

A

G

Mob

otix

AG

M

olog

en A

G

MPC

Mün

chm

eyer

Pet

erse

n C

apita

l AG

M

ühlb

auer

Hol

ding

AG

&

Co.

KG

aA

Nem

etsc

hek

AG

N

exus

AG

no

vem

ber A

G

OH

B T

echn

olog

y A

G

OV

B H

oldi

ng A

G

P&I P

erso

nal &

Info

rmat

ik

AG

Pa

ion

AG

pa

rago

n A

G

Petro

tec

AG

PN

E W

ind

AG

Po

lis Im

mob

ilien

AG

Pr

ocon

Mul

tiMed

ia A

G

Prog

ress

-Wer

k A

G

PSI A

G

Puls

ion

Med

ical

Sys

tem

s A

G

PVA

TeP

la A

G

IBS

AG

exc

elle

nce

colla

bo-

ratio

n m

anuf

actu

ring

IFM

Imm

obili

en A

G

init

inno

vatio

n in

traf

fic

syst

ems A

G

Inte

gral

is A

G

Inte

rhyp

AG

In

ters

hop

Com

mun

icat

ions

A

G

InTi

Ca

Syst

ems A

G

InV

isio

n So

ftwar

e A

G

Isra

Vis

ion

AG

ite

llige

nce

AG

IV

U T

raff

ic T

echn

olog

ies

AG

Ja

xx A

G

Jette

r AG

Jo

you

AG

K

löck

ner-

Wer

ke A

G

Kro

mi L

ogis

tik A

G

Leifh

eit A

G

Lloy

d Fo

nds A

G

Loew

e A

G

LPK

F La

ser &

Ele

ctro

nics

A

G

Ludw

ig B

eck

am R

atha

us-

eck-

Text

ilhau

s Fel

dmei

er

AG

D.L

ogis

tics A

G

DA

B b

ank

AG

D

ata

Mod

ul A

G

Deu

tsch

e En

terta

inm

ent A

G

DF

Deu

tsch

e Fo

rfai

t AG

Dr.

Hön

le A

G

Dyc

kerh

off A

G

Ecke

rt &

Zie

gler

Stra

hlen

- un

d M

ediz

inte

chni

k A

G

Einh

ell G

erm

any

AG

El

mos

Sem

icon

duct

or A

G

Envi

Tec

Bio

gas A

G

Epig

enom

ics A

G

Essa

nelle

Hai

r Gro

up A

G

Esta

vis A

G

euro

mic

ron

AG

Fa

ir V

alue

REI

T-A

G

Forte

c El

ektro

nik

AG

Fr

anco

typ-

Post

alia

Hol

ding

A

G

Funk

wer

k A

G

Gen

eral

i Deu

tsch

land

Hol

-di

ng A

G

Ger

athe

rm M

edic

al A

G

GFT

Tec

hnol

ogie

s AG

G

K S

oftw

are

AG

G

raph

it K

ropf

müh

l AG

G

WB

Imm

obili

en A

G

Ham

born

er R

EIT

AG

H

awes

ko H

oldi

ng A

G

HC

I Cap

ital A

G

Hei

ler S

oftw

are

AG

H

elia

d Eq

uity

Par

tner

s G

mbH

& C

o. K

GaA

H

öft &

Wes

sel A

G

Hyp

opor

t AG

1180

00 A

G

3U H

oldi

ng A

G

4SC

AG

A

.S. C

réat

ion

Tape

ten

AG

aa

p Im

plan

tate

AG

ad

pep

per m

edia

Inte

rnat

io-

nal N

.V.

Age

nnix

AG

A

hler

s AG

A

IRE

Gm

bH &

Co.

KG

aA

Aix

tron

AG

al

eo so

lar A

G

All

for O

ne M

idm

arke

t AG

A

lpha

form

AG

A

ltana

AG

A

naly

tik Je

na A

G

Arq

ues I

ndus

tries

AG

ar

tnet

AG

A

sian

Bam

boo

AG

A

toss

Sof

twar

e A

G

Aug

usta

Tec

hnol

ogie

AG

B

asle

r AG

B

eate

Uhs

e A

G

Bet

a Sy

stem

s Sof

twar

e A

G

biol

itec

AG

bm

p A

G

Brü

der M

anne

sman

n A

G

burg

bad

AG

C

anco

m IT

Sys

tem

e A

G

Cen

it A

G

Cen

troso

lar G

roup

AG

C

eoTr

onic

s AG

C

olex

on E

nerg

y A

G

Com

arch

Sof

twar

e un

d B

e-ra

tung

AG

C

ompu

GR

OU

P M

edic

al A

G

CO

R&

FJA

AG

C

ropE

nerg

ies A

G

Cur

anum

AG

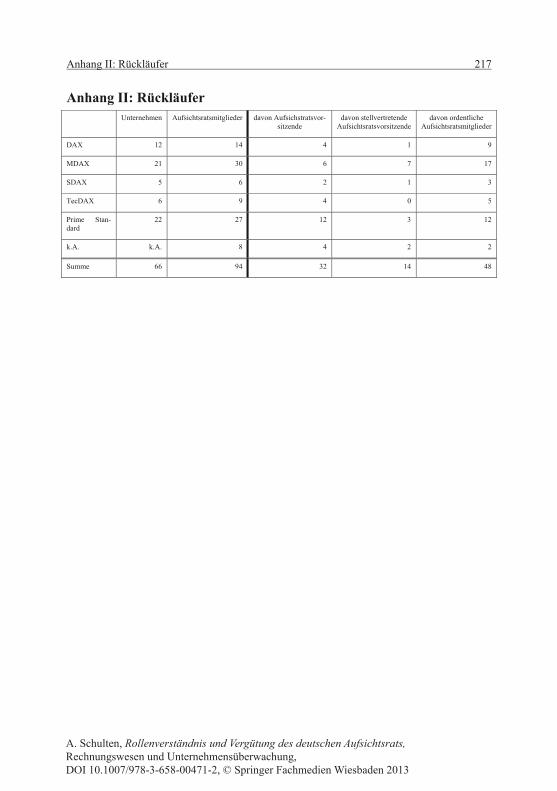

Anhang II: Rückläufer 217

Anhang II: Rückläufer Unternehmen Aufsichtsratsmitglieder davon Aufsichstratsvor-

sitzende davon stellvertretende

Aufsichtsratsvorsitzende davon ordentliche

Aufsichtsratsmitglieder

DAX 12 14 4 1 9

MDAX 21 30 6 7 17

SDAX 5 6 2 1 3

TecDAX 6 9 4 0 5

Prime Stan-dard

22 27 12 3 12

k.A. k.A. 8 4 2 2

Summe 66 94 32 14 48

A. Schulten, Rollenverständnis und Vergütung des deutschen Aufsichtsrats,Rechnungswesen und Unternehmensüberwachung,DOI 10.1007/978-3-658-00471-2, © Springer Fachmedien Wiesbaden 2013

218 Anhang III: Anschreiben des Fragebogens

Anhang III: Anschreiben des Fragebogens

A. Schulten, Rollenverständnis und Vergütung des deutschen Aufsichtsrats,Rechnungswesen und Unternehmensüberwachung,DOI 10.1007/978-3-658-00471-2, © Springer Fachmedien Wiesbaden 2013

Anhang IV: Fragebogen 219

Anhang IV: Fragebogen

A. Schulten, Rollenverständnis und Vergütung des deutschen Aufsichtsrats,Rechnungswesen und Unternehmensüberwachung,DOI 10.1007/978-3-658-00471-2, © Springer Fachmedien Wiesbaden 2013

220 Anhang IV: Fragebogen

Anhang IV: Fragebogen 221

222 Anhang IV: Fragebogen

Anhang IV: Fragebogen 223

224 Anhang IV: Fragebogen

Anhang IV: Fragebogen 225

226 Anhang IV: Fragebogen

Anhang IV: Fragebogen 227

228 Anhang V: Bildungsgrad der Aufsichtsräte in Abhängigkeit der Unternehmensbranche

Anhang V: Bildungsgrad der Aufsichtsräte in Abhängigkeit der Unternehmensbranche

Abschluss Total

BWL Ingenieur Jura Natur- wissenschaft Sonstige

Branche Automobil/Transport 4 3 4 0 0 11

Banken/Finanzdiestleister 2 0 1 1 0 4

Chremie/Pharma 3 0 0 3 2 8

Bau 1 0 1 0 0 2

Versicherungen 0 0 1 0 0 1

Maschinenbau/Industrie 11 8 4 2 2 27

Konsumgüter 2 0 0 0 4 6

Informationstechnologie 7 4 0 0 0 11

Versorger/Telekommunikation 0 1 2 0 1 4

Sonstige 1 0 1 0 0 2

Total 31 16 14 6 9 76

A. Schulten, Rollenverständnis und Vergütung des deutschen Aufsichtsrats,Rechnungswesen und Unternehmensüberwachung,DOI 10.1007/978-3-658-00471-2, © Springer Fachmedien Wiesbaden 2013

Literaturverzeichnis 229

Literaturverzeichnis

Adams, R. B., Ferreira, D. (2008): Do directors perform for pay? Journal of Account-ing and Economics, 46, S. 154-171.

Adams, R. B., Hermalin, B. E., Weisbach, M. S. (2010): The Role of Boards of Direc-tors in Corporate Governance: A Conceptual Framework and Survey. Journal of Economic Literature, 48 (1), S. 58–107.

Addison, J. T., Schnabel, C., Wagner, J. (2004): The Course of Research into the Eco-nomic Consequences of German Works Councils. British Journal of Industrial Re-lations, 42 (2), S. 255–281.

Adjaoud, F., Zeghal, D., Andaleeb, S. (2007): The Effect of Board’s Quality on Per-formance: a study of Canadian firms. Corporate Governance, 15 (4), S. 623-635.

Agarwal, R., Elston, J. A. (2001): Bank–firm relationships, financing and firm perfor-mance in Germany. Economics Letters, 72, S. 225–232.

Agrawal, A., Knoeber, C. R. (2001): Do some outside directors play a political role? Journal of Law and Economics, 44, S. 179-198.

Agarwal, A., Knoeber, C. R. (1996): Firm Performance and Mechanisms to Control Agency Problems between Managers and Shareholders. Journal of Financial and Quantitative Analysis, 31 (3), S. 377-397.

Aguilera, R. V., Cuervo-Cazurra, A. (2009): Codes of Good Governance. Corporate Governance: An International Review, 17 (3), S. 376-387.

Andreas, J. M., Rapp, M. S., Wolff, M. (2010): Determinants of Director Compensation in Two-Tier-Systems: Evidence from German Panel Data. CEFS Working Paper, SSRN: http://ssrn.com/abstract=1486325.

Arnegger, M. (2010): Aufsichtsräte deutscher Unternehmen: Mandatsträger, Vergü-tungsdeterminanten, Gremienzusammensetzung, Dissertation Universität Mann-heim.

Arnegger, M., Hofmann, C., Pull, K., Vetter, K. (2010): Unterschiede in der fachlichen und demographischen Zusammensetzung deutscher Aufsichtsräte: Eine empirische Bestandsaufnahme für HDAX- und SDAX-Unternehmen. Die Betriebswirtschaft, 70. (3), S. 239-257.

A. Schulten, Rollenverständnis und Vergütung des deutschen Aufsichtsrats,Rechnungswesen und Unternehmensüberwachung,DOI 10.1007/978-3-658-00471-2, © Springer Fachmedien Wiesbaden 2013

230 Literaturverzeichnis

Bagozzi, R., Philips, L. (1982): Representing and Testing Organizational Theories: A Holistic Construal. Administrative Science Quarterly, 27, S. 459-489.

Balsmeier, B., Buchwald, A. (2011): Motive der Ausübung externer Kontrollmandate durch Vorstandsvorsitzende in deutschen Großunternehmen. Die Betriebswirt-schaft, 71 (2), S. 101-119.

Bamberg, G., Baur, F., Krapp, M. (2011): Statistik. 16., überarbeitete Auflage, Olden-bourg: München.

Barney, J. B. (2011): Gaining and sustaining competitive advantage. 4th international edition, Upper Saddle River: New Jersey.

Barnhart, S. W., Marr, M. W., Rosenstein, S. (1994): Firm and Board Composition: Some New Evidence. Managerial and Decision Economics, 15 (4), S. 329-340.

Baums, T. (1995): Der Aufsichtsrat – Aufgaben und Reformfragen. Zeitschrift für Wirtschaftsrecht, 16, S. 11-18.

Baums, T., Frick, B. (1999): Co-Determination in Germany: The Impact of Court De-cisions on the Market Value of Fims. Economic Analysis, 1, S. 144-161.

Baysinger, B., Butler, H. (1985): Corporate Governance and the Board of Directors: Performance Effects of Changes in Board Composition. Journal of Law, Econom-ics and Organization, 1, S. 101-124.

Bebchuk, L., Cohen, A., Ferrell, A. (2009): What matters in corporate governance? Review of Financial Studies, 22 (2), S. 783-827.

Beckmann, S. (2009): Die Informationsversorgung von Mitgliedern des Aufsichtsrats börsennotierter Aktiengesellschaften: Theoretische Grundlagen und empirische Er-kenntnisse, Gabler: Wiesbaden.

Benninghaus, H. (2005): Einführung in die sozialwissenschaftliche Datenanalyse. 7., unwesentlich veränderte Auflage, Oldenbourg: München, Wien.

Berle, A., Means, G. (1932): The Modern Corporation and Private Property. Mcmillan: New York.

Bhagat, S., Black, B. (2002): The Non-Correlation Between Board Independence and Long-Term Firm Performance. The Journal of Corporation Law, 27 (2), S. 231-273.

Literaturverzeichnis 231

Bhagat, S., Black, B. (1999): The Uncertain Relationship Between Board Composition and Firm Performance. Business Lawyer, 54, S. 921-963.

Bischof, J. (2006): Zweckmäßigkeit erfolgsunabhängiger Aufsichtsratsvergütung. Be-triebs-Berater, 61 (48), S. 2627-2633.

Bleicher, K. (1987): Der Aufsichtsrat im Wandel: eine repräsentative Studie über die Aufsichtsräte in bundesdeutschen Aktiengesellschaften. Bertelsmann Stiftung: Gü-tersloh.

Bleicher, K., Leber, D., Paul, H. (1989): Unternehmungsverfassung und Spitzenorga-nisation: Führung und Überwachung von Aktiengesellschaften im internationalen Vergleich. Wiesbaden: Gabler.

Böcking, H.-J., Dutzi, A., Fey, G., Leven, F.-J. (2005): Wertorientierte Überwachung durch den Aufsichtsrat: Ausgewählte Ergebnisse einer Umfrage. In: Rosen, R. v. (Hrsg.): Studien des deutschen Aktieninstituts, Heft 32, Frankfurt am Main.

Booth, J. R., Deli, D. N. (1999): On executives of financial institutions as outside di-rectors. Journal of Corporate Finance, 5, S. 227–250.

Booth, J. R., Deli, D. N. (1996): Factors affecting the number of outside directorships held by CEOs. Journal of Financial Economics, 40, S. 81-104.

Bortz, J., Döring, N. (2006). Forschungsmethoden und Evaluation für Human- und Sozialwissenschaftler. 4., überarbeitete Auflage, Springer: Heidelberg.

Bratton, W. W., Wachter, M. (2009): The Case Against Shareholder Empowerment. Law & Economics Research Paper Series, Georgetown Law School, No. 1480290, S. 1-59.

Bremert, M., Schulten, A. (2012): The relation between supervisory board characteris-tics and firm perfomance. Working Paper Universität Mannheim.

Bresser, R. K., Thiele, R. V. (2008): Ehemalige Vorstandsvorsitzende als Aufsichts-ratschefs: Evidenz zu ihrer Effektivität im Falle des erzwungenen Führungswech-sels. Zeitschrift für Betriebswirtschaft, 28 (2), S. 175-203.

Brick, I. E., Palmon, O., Wald, J. K. (2006): CEO compensation, director compensa-tion, and firm performance: Evidence of cronyism? Journal of Corporate Finance, 12, S. 403-423.

232 Literaturverzeichnis

Brickley, J. A., Coles, J. L., Jarrell, G. (1997): Leadership structure: Seperating the CEO and Chariman of the Board. Journal of Corporate Finance, 3, S. 189-220.

Brown, L. D., Caylor, M. L. (2009): Corporate governance and firm operating perfor-mance. Review of Quantitative Finance & Accounting, 32 (2), S. 129-144.

Brown, L. D., Caylor, M. L. (2004): Corporate governance and firm performance. Working Paper, Dezember 2004.

Büschemann, K-H., Theile, C. (2011): Erntezeit: Aufsichtsräte haben ihre Einkommen in 2010 deutlich erhöht. Jetzt beginnt eine neue Diskussion über die Gehälter. Süd-deutsche Zeitung v. 25.03.2011, S. 24.

Byrd, J., Parrino, R., Pritsch, G. (1998): Stockholder-Manager Conflicts and Firm Value. Financial Analyst Journal, 54 (3), S. 14-30.

Cable, J. (1985): Capital market information and industrial performance: the role of west German banks. Economic Journal, 95 (377), S. 118-132.

Charkham, J. P. (2008): Keeping Better Company: Corporate Governance Ten Years On. Oxford University Press: Oxford et al.

Collins, D. W., Gong, G., Li, H. (2009): Corporate Governance and Backdating of Ex-ecutive Stock Options. Contemporary Accounting Research, 26, (2), S. 403-445.

Conyon, M. J., Muldoon, M. R. (2006): The Small World of Corporate Boards. Journal of Business Finance & Accounting, 33, S. 1321–1343.

Conyon, M. J., Peck, S. I. (1998): Board size and corporate performance: evidence from European countries. The European Journal of Finance, 4, S. 291-304.

Cordeiro, J., Veliyath, R., Eramus, E. J. (2000): An Empirical Investigation of the De-terminants of Outside Director Compensation. Corporate Governance, 8 (3), S. 268-279.

Debus, M. (2010): Evaluation des Aufsichtsrats: Theoretische Grundlagen und empiri-sche Befunde. Gabler: Wiesbaden.

Deloitte Consulting (Hrsg.) (2004): Entwicklung der Aufsichtsratspraxis in Deutsch-land, Studie, Düsseldorf.

Denis, D. K. (2001): Twenty-five years of corporate governance research … and counting. Review of Financial Economics, 10, S. 191-212.

Literaturverzeichnis 233

Deutsch, Y. (2005): The Impact of Board Composition on Firms’ Critical Decisions: A Meta-Analytic Review. Journal of Management, 31 (3), S. 424-444.

Deutsche Bundesbank: Kapitalmarktstatistik. Abrufbar unter: URL: http://www.bundesbank. de/statistik/statistik.php

Deutscher Corporate Governance Kodex (2010): URL: http://www.corporate-governance-code.de/ger/kodex/1.html.

Dey, A., Engel, E., Liu, X. (2011): CEO and board chair roles: To split or not to split? Journal of Corporate Finance, 17, S. 1595-1618.

Dittmann, I., Maug, E., Schneider, C. (2010): Bankers on the Boards of German Firms: What they do, what they are worth, and why they are (still) there. Review of Finance, 14, S. 35-71.

Dittmann, I., Maug, E., Schneider, C. (2008): How Preussag Became TUI: A Clinical Study of Institutional Blockholders and Restructuring in Europe. Financial Ma-nagement, 37 (3), S. 571-598.

Drobetz, W., Schillhofen, A., Zimmermann, H. (2004): Ein Corporate Governance Ra-ting für deutsche Publikumsgesellschaften. Zeitschrift für Betriebswirtschaftslehre, 74, S. 5-25.

Dutzi, A. (2005): Der Aufsichtsrat als Instrument der Corporate Governance. Deut-scher Universitäts-Verlag: Wiesbaden.

Ebert, M. (2010): Der Konzernabschluss als Element der Corporate Governance. Dis-sertation Universität Mannheim 2009, Gabler: Wiesbaden.

Eisenberg, T., Sundgren, S., Wells, M. (1998): Larger Board Size and Decreasing Firm Value in Small Firms. Journal of Financial Economics, 48, S. 35-54.

Elston, J. A., Goldberg, L. G. (2003): Executive compensation an agency costs in Germany. Journal of Banking & Finance, 27 (7), S. 1391-1410.

Entorf, H., Gattung, F., Möbert, J., Pahlke, I. (2008): Aufsichtsratsverflechtungen und ihr Einfluss auf die Vorstandsbezüge von DAX-Unternehmen. ZEW Discussion Paper Nr. 08-036.

Fairchild, L., Li, J. (2005): Director Quality and Firm Performance. The Financial Re-view, 40, S. 257-279.

234 Literaturverzeichnis

Fallgatter, M. J. (2003): Variable Vergütung von Mitgliedern des Aufsichtsrates: Re-sultiert eine verbesserte Unternehmensüberwachung? Die Betriebswirtschaft, 63 (6), S. 703-713.

Fama, E. F. (1980): Agency problems and the theory of the firm. Journal of Political Economy, 88 (2). S. 288-307.

Fama, E., Jensen, M. (1983): Separation of Ownership and Control. Journal of Law and Economics, 26, S. 301-325.

Farell, K. A., Friesen, G. C., Hersch, P. L. (2008): How do firms adjust director com-pensation? Journal of Corporate Finance, 14, S. 153-162.

Fauver, L., Fuerst, M. E. (2006): Does good corporate governance include employee representation? Evidence from German corporate boards. Journal of Financial Eco-nomics, 82, S. 673–710.

Ferris, S., Jagannathan, M., Pritchard, A. (2003): Too Busy to Mind the Business? Monitoring by Directors with Multiple Board Appointments. The Journal of Fi-nance, 58 (3), S. 1087-1111.

Fich, E. M. (2005): Are Some Outside Directors Better than Others? Evidence from Director Appointments by Fortune 1000 Firms. Journal of Business, 78 (5), S. 1943-1971.

Fich, E. M., Shivdasani, A. (2006): Are Busy Boards Effective Monitors? The Journal of Finance, 61 (2), S. 689-724.

Fich, E. M., Slezak, S. L. (2008): Can corporate governance save distressed firms from bankrupcy? An empirical analysis. Reviev of Quantitative Finance and Account-ing, 30, S. 225-251.

Fich, E. M., White, L. J. (2005): Why do CEOs reciprocally sit on each other’s boards? Journal of Corporate Finance, 11, S. 175– 195.

Freeman, R. B., Lazear, E. P. (1995): An Economic Analysis of Works Councils. In: Rogers, J., Steeck, W. (Hrsg.): Works Councils: Consultation, Representation, and Cooperation in Industrial Relations, University of Chicago Press: Chicago, S. 27-50.

Gerum, E. (2007): Das deutsche Corporate Governance System: Eine empirische Un-tersuchung. Schäffer-Poeschel: Stuttgart.

Literaturverzeichnis 235

Gerum, E. (1991): Aufsichtsratstypen – Ein Beitrag zur Theorie der Organisation der Unternehmensführung. Die Betriebswirtschaft, 51, S. 719-731.

Gillian, S. L. (2006): Recent Developments in Corporate Governance: An Overview. Journal of Corporate Finance, 12 (3), S. 381-402.

Gorton, G., Schmid, F. A. (2000): Universal banking and the performance of German firms. Journal of Financial Economics, 58, S. 29-80.

Grant, R. M. (2011): Contemporary strategy analysis : text and cases. 7th edition, Wiley: Chichester.

Grathwohl, J., Feicha, D. (2012): The impact of task separation on manager compen-sation: Empirical evidence from Germany. Working Paper, Universität Mannheim.

Hambrick, D. C., v. Werder, A., Zajac, E. J. (2008): New Directions in Corporate Governance Research. Organization Science, 19 (3), S. 381-385.

Harris, I. C., Shimizu, K. (2004): Too Busy To Serve? An Examination of the Influ-ence of Overboarded Directors. Journal of Management Studies, 41 (5), S. 775-798.

Hartmann, K. (2003): Die Aufsichtsratsvergütung als Erfolgsfaktor im deutschen Cor-porate-Governance-System. Peter Lang: Frankfurt am Main et al.

Helbig, C. (2003): Aufsichtsratsvergütung bei deutschen börsennotierten Unterneh-men. In: Rosen, R. v. (Hrsg.): Studien des deutschen Aktieninstituts, Heft 20, Frankfurt am Main.

Helbig, C., Kramarsch, M. H., Leven, F.-J., Ziegler, S. U. (2003): Empfehlungen zur Aufsichtsratsvergütung - ein Modell. In: Rosen, R. v. (Hrsg.): Studien des deut-schen Aktieninstituts, Heft 23, Frankfurt am Main.

Helm, R. (2003): Vergütungsstrukturen des Aufsichtsrats mittelständischer, nicht bör-sennotierter Aktiengesellschaften. Der Betrieb, 56 (51/52), S. 2718-2723.

Hermalin, B. E., Weisbach, M. S. (2003): Boards of Directors as an Endogenously De-termined Institution: A Survey of the Economic Literature. Economic Policy Re-view, 9 (1), S. 7-26.

Hermalin, B. E., Weisbach, M. S. (1998): Endogeneously Chosen Boards of Directors and Their Monitoring of the CEO. The American Economic Review, 88 (1), S. 96-118.

236 Literaturverzeichnis

Hermalin, B. E., Weisbach, M. S. (1991): The Effects of Board Composition and Di-rect Incentives on Firm Performance. Financial Management, 20, 101-112.

Holmström, B. (1979): Moral Hazard and Observability. Bell Journal of Economics, 10, S. 74-91.

Homburg, C. (2012): Marketingmanagement: Strategie – Instrumente – Umsetzung - Unternehmensführung. 4., überarbeitete und erweiterte Auflage, Gabler: Wiesba-den.

Homburg, C., Giering, A. (1996): Konzeptualisierung und Operationalisierung kom-plexer Konstrukte: Ein Leitfaden für die Marketingforschung, Marketing – Zeit-schrift für Forschung und Praxis, 18 (1), S. 5-24.

Homburg, C., Krohmer, H. (2009): Marketingmanagement. 3., überarbeitete und er-weiterte Auflage, Gabler: Wiesbaden.

Homburg, C., Pflesser, C., Klarmann, M. (2008): Strukturgleichungsmodelle mit la-tenten Variablen: Kausalanalyse. In: Herrmann, A., Homburg, C., Klarmann, M. (Hrsg.): Handbuch Marktforschung – Methoden, Anwendungen, Praxisbeispiele, 3., vollständig überarbeitete und erweiterte Auflage, Gabler: Wiesbaden, S. 547-578.

Jacob, J., Jorgensen, B. N. (2007): Earnings management and accounting income ag-gregation. Journal of Accounting and Economics, 43 (2-3), S. 369-390.

Jensen, M. C. (1993): The Modern Industrial Revolution, Exit, and the Failure of In-ternal control Systems. The Journal of Finance, 48 (3), S. 831-880.

Jensen, M. C., Meckling, W. (1976): Theory of the Firm: Managerial Behaviour, Agency Costs and Ownership Structure. Journal of Financial Economics, 3, S. 305-360.

Johnson, J. L., Daily, C. M., Ellstrand, A. E. (1996): Boards of Directors: A Review and Research Agenda. Journal of Management, 22 (3), S. 409-438.

Kaplan, S., Reishus, D.(1990): Outside directorships and corporate performance. Jour-nal of Financial Economics, 27, S. 389–410.

Kendall, M. (1962): Rank Correlation Methods. Third edition, Hafner: New York.

Kieser, A., Walgenbach, P. (2010): Organisation. 6., überarbeitete Auflage, Schäffer-Poeschel: Stuttgart.

Literaturverzeichnis 237

Klein, A. (1998): Firm Performance and Board Committee Structure. Journal of Law & Economics, 41 (1), S. 275-303.

Knoll, L., Knoesel, J., Probst, U. (1997): Aufsichtsratsvergütung in Deutschland: Em-pirische Befunde. Zeitschrift für betriebswirtschaftliche Forschung, 49 (3), S. 236-253.

Köhler, A. G. (2005): Audit Committees in Germany – Theoretical Reasoning and Empirical Evidence. Schmalenbach Business Review, 57, S. 229-252.

Kommission Mitbestimmung (2006) Kommission zur Modernisierung der deutschen Unternehmensmitbestimmung: Bericht der wissenschaftlichen Mitglieder der Kommission mit Stellungnahmen der Vertreter der Unternehmen und der Vertreter der Arbeitnehmer, Berlin.

Kose, J., Senbet, L. (1998): Corporate Governance and Board Effectiveness. Journal of Banking and Finance, 22 (4), S. 371-403.

KPMG (2002): Corporate Governance in Europe: KPMG Survey 2001/02.

Kromrey, H. (2009): Empirische Sozialforschung: Modelle und Methoden der standar-disierten Datenerhebung und Datenauswertung. Lucius & Lucius: Stuttgart.

Laksmana, I. (2008): Corporate Board Governance and Voluntary Disclosure of Exec-utive Compensation Practices. Contemporary Accounting Research, 25 (4), S. 1147-1182.

Larcker, D. F., Rusticus, T. O. (2007): Endogeneity and Empirical Accounting Re-search. European Accounting Review, 16 (1), S. 207-215.

Lee, K. W., Lev, B., Yeo, G. H. H. (2008): Executive pay dispersion, corporate govern-ance, and firm performance. Review of Quantitative Finance and Accounting, 30, S. 315-338.

Lee, Y. S., Rosenstein, S., Wyatt, J. G. (1999): The value of financial outside directors on corporate boards. International Review of Economics and Finance, 8, S. 421–431.

Lehn, K. M., Patro, S., Zhao, M. (2009): Determinants of the Size and Composition of US Corporate Boards: 1935-2000. Financial Management, 3, S. 747-780.

238 Literaturverzeichnis

Lentfer, T. (2005): Einflüsse der internationalen Corporate Governance-Diskussion auf die Überwachung der Geschäftsführung – Eine kritische Analyse des deutschen Aufsichtsratssystems. Deutscher Universitäts-Verlag: Wiesbaden.

Lin, S., Pope, P. F., Young, S. (2003): Stock Market Reaction to the Appointment of Outside Directors. Journal of Business Finance & Accounting, 30, S. 351-382.

Lipton, M., Lorsch, J. W. (1992): A Modest Proposal for Improved Corporate Govern-ance. The Business Lawyer, 48, S. 59-77.

Mallin, C. A. (2010): Coporate Governance. Third edition, Oxford: New York.

Mayer, C. (1988): New Issues in Corporate Finance. European Economic Review, 32, S. 1167-1189.

Mehran, H. (1995): Executive compensation structure, ownership, and firm perfor-mance. Journal of Financial Economics, 38 (2), S. 163-184.

Minnick, K., Zhao, M. (2009): Backdating and Director Incentives: Money or Reputa-tion? The Journal of Financial Research, 32 (4), S. 449-477.

Nagy, R. (2002): Corporate Governance in der Unternehmenspraxis: Akteure, Instru-mente und Organisation des Aufsichtsrates, Deutscher Universitätsverlag: Wiesba-den.

Nicholson, G. J., Kiel, G. C. (2007): Can Directors Impact Performance? A case-based test of three theories of corporate governance. Corporate Governance, 15 (4), S. 585-608.

Niebel, T. (2010): Der Dienstleistungssektor in Deutschland – Abgrenzung und empi-rische Evidenz. ZEW Dokumentation Nr. 10-01.

Ning, Y., Davidson, W. N., Wang, J. (2010): Does Optimal Corporate Board Size Ex-ist? An Empirical Analysis. Journal of Applied Finance, 20 (2), S. 57-69.

OECD-Grundsätze der Corporate Governance (2004): URL: http://www.oecd.org/document/ 49/0,3746,en_2649_34813_31530865_1_1_1_1,00.html

Oser, P., Orth, C., Wader, D.(2004): Beachtung der Empfehlungen des Deutschen Corporate Governance Kodex: Erste Ergebnisse einer empirischen Folgeuntersu-chung der Entsprechenserklärungen börsennotierter Unternehmen. Betriebs Bera-ter, 59 (21), S. 1121-1126.

Literaturverzeichnis 239

Oser, P., Orth, C., Wader, D.(2003): Die Umsetzung des Deutschen Corporate Gover-nance Kodex in der Praxis - Empirische Untersuchung zur Entsprechenserklärung börsennotierter Unternehmen. Der Betrieb, 56 (25), S. 1337-1341.

o.V. (2010): Studien zur Aufsichtsratsvergütung. Der Aufsichtsrat, 7, S. 180.

Perry, T., Peyer, U. (2005): Board seat accumulation by executives: A shareholder’s perspective. The Journal of Finance, 60, S. 2083–2123.

Pfannschmidt, A. (1995): Mehrfachmandate in deutschen Unternehmen: Ökonomi-scher Erklärungsansatz. Zeitschrift für Betriebswirtschaft, 65, S. 177-203.

Potthoff, E., Trescher, K., Theisen, M. R. (2003): Das Aufsichtsratsmitglied, Ein Handbuch der Aufgaben, Rechte und Pflichen. 6., neu bearbeitete Auflage, Schäf-fer-Poeschel: Stuttgart.

Probst, A., Theisen, M. (2011): Aufsichtsratsinteraktion und Aufsichtsratsfinanzierung: Ergebnisse der 8. Panel-Befragung. Der Aufsichtsrat, 8, S. 70-72.

Raible, K.-F., Schmidt, W. (2009): Vergütungssysteme für Management und Auf-sichtsrat. In: Wagenhofer, A. (Hrsg.): Controlling und Corporate Governance-Anforderungen - Verbindungen, Maßnahmen, Umsetzung. Schmidt: Berlin, S. 59-85.

Rechner, P. L., Dalton, D. R. (1991): CEO Duality and Organizational Performance: A Longitudinal Analysis. Strategic Management Journal, 12 (2), S. 155-160.

Roe, M. J. (1990): Political and legal restraints on ownership and control of public companies. Journal of Financial Economics, 27 (1), S. 7-41.

Rosenstein, S., Wyatt, J. G. (1994): Shareholder Wealth Effects When an Officer of One Corporation Joins the Board of Directors of Another. Managerial and Decision Economics, 15 (4), S. 317-327.

Rosenstein, S., Wyatt, J. G. (1990): Outside directors, board independence, and share-holder wealth. Journal of Financial Economics, 26, S. 175-191.

Ruhwedel, P., Epstein, R. (2003): Eine empirische Analyse der Strukturen und Prozes-se in den Aufsichtsräten deutscher Aktiengesellschaften. Betriebs Berater, 58. (4), S. 161-166.

Schleifer, A., Vishny, R. W. (1997): A Survey of Corporate Governance. The Journal of Finance, 52 (2), S. 737-783.

240 Literaturverzeichnis

Schmid, F. A. (1997): Vorstandsbezüge, Aufsichtsratsvergütung, und Aktionärsstruk-tur. Zeitschrift für Betriebswirtschaft, 67 (1), S. 67-83.

Schmidt, R. H. (2007): Stakeholderorientierung, Systemhaftigkeit und Stabilität der Corporate Governance in Deutschland. In: Jürgens, U. (Hrsg.): Perspektiven der Corporate Governance: Bestimmungsfaktoren unternehmerischer Entscheidungs-prozesse und Mitwirkung der Arbeitnehmer. Nomos: Baden-Baden, S. 31-54.

Schöndube-Pirchegger, B., Schöndube, J. R. (2010): On the Appropriateness of Per-formance-Based Compensation for Supervisory Board Members – An Agency Theoretic Approach. European Accounting Review, 19 (4), S. 817-835.

Shivdasani, A., Yermack, D. (2004). CEO Involvement in the Selection of New Board Members: An Empirical Analysis. The Journal of Finance, 54 (5), S. 1829-1853.

Smith, A. (1937): The Wealth of Nations. Cannan Edition, Modern Library, New York.

Srinivasan, S. (2005): Consequences of Financial Reporting Failure for Outside Direc-tors: Evidence from Accounting Restatements and Audit Committee Members. Journal of Accounting Research, 42 (2), S. 291-334.

Szymanski, D. M., Bharadwaj, S. G., Varadarajan, P. R. (1993): An Analysis of the Market Share-Profitability Relationship. Journal of Marketing, 57, S. 1-18.

Theisen, M. (2004): Zwölf Hürden für eine „gute Unternehmensüberwachung“ in Deutschland. Betriebswirtschaftliche Forschung und Praxis, 56, S. 480-492.

Tirole, J. (2001): Corporate Governance. Econometrica, 69 (1), S. 1-35.

Tirole, J. (1986): Hierarchies and Bureaucracies: On the Role of Collusion in Organi-zations. Journal of Law, Economics and Organization, 2, S. 181-214.

Toutenburg, H., Heumann, C. (2008): Deskriptive Statistik : eine Einführung in Me-thoden und Anwendungen mit R und SPSS. 6., aktualisierte und erweiterte Aufla-ge, Springer: Heidelberg, Berlin.

Vafeas, N. (2000). The Determinants of Compensation Committee Membership. Cor-porate Finance, 8 (4), S. 356-366.

Vafeas, N. (1999): Board meeting frequency and Firm performance. Journal of Finan-cial Economics, 53, S. 113-142.

v. Werder, A., Böhme, J. (2011): Corporate Governance Report 2011. Der Betrieb, 64 (23) S. 1285-1290 (Teil 1) und (24), S. 1345-1353 (Teil 2).

Literaturverzeichnis 241

v. Werder, A., Talaulicar, T. (2010): Kodex Report 2010: Die Akzeptanz der Empfeh-lungen und Anregungen des Deutschen Corporate Governance Kodex. Der Betrieb, 63, S. 853-861.

v. Werder, A., Talaulicar, T. (2009): Kodex Report 2009: Die Akzeptanz der Empfeh-lungen und Anregungen des Deutschen Corporate Governance Kodex. Der Betrieb, 62, S. 689-696.

Wadewitz, S. (2012): Wiedervorlage Aufsichtsratsvergütung. Börsen-Zeitung v. 16.02.2012, S. 8.

Wagenhofer, A., Ewert, R. (2007): Externe Unternehmensrechnung. 2., überarbeitete und erweiterte Auflage, Springer: Berlin et al.

Wagner, J. (2009): One-third Codetermination at Company Supervisory Boards and Firm Performance in German Manufacturing Industries: First Direct Evidence from a New Type of Enterprise Data. IZA Discussion Paper No. 4352, August 2009, S. 1-23.

Witt, P. (2004): Vergütung von Führungskräften. In: Schreyögg, G., v. Werder, A. (Hrsg.): Handwörterbuch Unternehmensführung und Organisation, 4. Auflage, Schäffer-Poeschel: Stuttgart, Spalte 1573-1581.

Witt, P. (2003): Corporate Governance-Systeme im Wettbewerb. Deutscher Universi-tätsverlag: Wiesbaden.

Wolf, J. (2011): Organisation, Management, Unternehmensführung : Theorien, Praxis-beispiele und Kritik. Gabler: Wiesbaden.

Yermack, D. (2004): Remuneration, Retention, and Reputation - Incentives for Outside Directors. The Journal of Finance, 59 (5), S. 2281-2308.

Yermack, D. (1996): Higher market valuation of companies with a small board of di-rectors. Journal of Financial Economics, 40, S. 185-211.

Zahra, S., Pearce, J. (1989): Boards of Directors and Corporate Financial Perfor-mance: A Review and Integrative Model. Journal of Management, 15 (2), S. 291-344.

Zein, N. (2009): Die Qualität der Unternehmensüberwachung durch Abschlussprüfer und Aufsichtsrat. Dissertation Universität Mannheim.

242 Literaturverzeichnis

Ziegler, S., Kramarsch, M. (2003): Zeitgemäße Aufsichtsratsvergütung und Corporate Governance. Personal, 55, S. 20-23.