Embed Size (px)

Citation preview

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 1/96

A

Brief Analysis of

EXPANSION OF DISTRIBUTION CHANNEL

at

AVIVA LIFE INSURANCE

NOIDA

Submitted To

KHANDELWAL COLLEGEOf

Management Science and Technology Bareilly

In Partial Fulfillment Of

MASTER IN BUSINESS ADMINISTRATION

Session : 2006-2008

Submitted to: Submitted by:

Miss.Richa Sharma Rohit Sharma

M.B.A. (3ed Sem.)

- 1 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 2/96

EXPANSION OF DISTRIBUTION CHANNEL

OF AVIVA LIFE INSURANCE

- 2 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 3/96

ACKNOWLEDGMENT

Initially I would like to express thanks to staff & industrial employees

and all to those who are involved in my project work of two months. I have

gained a lot of experience, deep knowledge about the organization. I also

thanks to the top level management to provide me this opportunity to study

the organization atmosphere working culture inside the AVIVA LIFE

INSURANCE.Under whose supervision this study instituted his able

guidance valuable suggestion most generous and constant encouragement

made is possible for me to complete this project work.

I am thankful to the Mr. Syeed Mohd. Saleem(Sales Manager) and

all staff of finance department who helped me to provide the apart-

unity to gain the profit of experience.

I would also like to thank to my Director Dr. Amresh Kumar, myAstt. Director of Management Department Dr. Swatantra Kumar and my

faculty member for giving me proper guideline for making of my project.

I am thankful to all people who helped me in preparation of my

project and also thank the people who took my work and give moral

support, they are respected, all member of AVIVA LIFE INSURANCE.

- 3 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 4/96

ROHIT SHARMA

PREFACE

Expasion Of Distribution Channel is one of the crucial issues of any organization.

Today, wild the cut throat competition is prevailing. In such, we need a better way to

manage our Distribution channel.

It is a matter of great satisfaction and privilege for me to place before esteemedreport of Expansion of Distribution channel.

The opportunity to bring out project report has been well utilized in thoroughly

analyses and interprets beside retaining and strengthening the plus feature of this report

of Expansion of Distribution channel

It is divided in to seven parts, which are as follows:

I am confident that with all study and adaptation of the working capital is

expected to meet the combined requirement of working capital management of ACME

Tele Power. Constructive and helpful suggestions for improvement in the working capital

will be beneficial for the company.

ROHIT SHARMA

- 4 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 5/96

CHAPTER 1

OBJECTIVE

- 5 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 6/96

OBJECTIVE

During my training at AVIVA Life Insurance, the job assigned to

me as a trainee was Expansion of Distribution Channel for the

company i.e. to increase the Advisor sales force for the company.

Following steps had to be taken in order to achieve the desired

end result.

Convincing people on the benefits of becoming an AVIVA

Life Insurance Advisor. This included meeting people, fixing

appointments, making phone calls and collecting

references.

Taking up practical challenges and enhancing my

interpersonal skills.

Learning on how people are categorised by the companies

on the basis of their occupations.

- 6 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 7/96

Understanding the basic target segment for recruiting the

advisors.

The job was very interactive in nature as I had a very broad

category of clients to contact. People from different

backgrounds for e.g. Doctors, Engineers, Tax Consultants,

Charted Accounts were contacted.

- 7 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 8/96

AN INTRODUCTION TO INSURANCE

A system under which the insurer, for a consideration usually

agreed upon in advance, promises to reimburse the insured or to

render services to the insured in the event that certain accidental

occurrences result in losses during a given period. It thus is a

method of coping with risk. Its primary function is to substitute

certainty for uncertainty as regards the economic cost of loss-

producing events.

Insurance relies heavily on the “law of large numbers.” In large

homogeneous populations it is possible to estimate the normal

frequency of common events such as deaths and accidents.

Losses can be predicted with reasonable accuracy, and this

accuracy increases as the size of the group expands. From a

theoretical standpoint, it is possible to eliminate all pure risk if an

infinitely large group is selected.

- 8 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 9/96

From the standpoint of the insurer, an insurable risk must meet

the following requirements:

1. The objects to be insured must be numerous enough and

homogeneous enough to allow a reasonably close

calculation of the probable frequency and severity of losses.

2. The insured objects must not be subject to simultaneous

destruction. For example, if all the buildings insured by one

insurer are in an area subject to flood, and a flood occurs,

the loss to the insurance underwriter may be catastrophic.

3. The possible loss must be accidental in nature, and beyond

the control of the insured. If the insured could cause the

loss, the element of randomness and predictability would be

destroyed.

4. There must be some way to determine whether a loss has

occurred and how great that loss is. This is why insurance

- 9 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 10/96

contracts specify very definitely what events must take

place, what constitutes loss, and how it is to be measured.

From the viewpoint of the insured person, an insurable risk is one

for which the probability of loss is not so high as to require

excessive premiums. What is “excessive” depends on individual

circumstances, including the insured's attitude toward risk. At the

same time, the potential loss must be severe enough to cause

financial hardship if it is not insured against. Insurable risks

include losses to property resulting from fire, explosion,

windstorm, etc.; losses of life or health; and the legal liability

arising out of use of automobiles, occupancy of buildings,

employment, or manufacture. Uninsurable risks include losses

resulting from price changes and competitive conditions in the

market. Political risks such as war or currency debasement are

usually not insurable by private parties but may be insurable by

governmental institutions. Very often contracts can be drawn in

such a way that an “uninsurable risk” can be turned into an

“insurable” one through restrictions on losses, redefinitions of

perils, or other methods.

- 10 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 11/96

Life insurance industry

Life insurance may be defined as a plan under which large groups

of individuals can equalize the burden of loss from death by

distributing funds to the beneficiaries of those who die. From the

individual standpoint life insurance is a means by which an estate

may be created immediately for one's heirs and dependents. It

has achieved its greatest acceptance in Canada, the United

States, Belgium, South Korea, Australia, Ireland, New Zealand,

The Netherlands, and Japan, countries in which the face value of

life insurance policies in force generally exceeds the national

income.

In the United States in 1990 nearly $9.4 trillion of life insurance

was in force. The assets of the more than 2,200 U.S. life

insurance companies totaled nearly $1.4 trillion, making life

insurance one of the largest savings institutions in the United

States. Much the same is true of other wealthy countries, in

which life insurance has become a major channel of saving and

investment, with important consequences for the national

economy.

- 11 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 12/96

Life insurance is relatively little used in poor countries, although

its acceptance has been increasing.

Group life insurance

Under group life insurance an employer signs a master contract

with the insurance company outlining the provisions of the plan.

Each employee receives a certificate that gives evidence of

participation in the plan. The amount of insurance depends on

the employee's salary or job classification; usually the employer

pays a portion of the premium and the employee pays the rest,

but sometimes the employer pays the entire cost of the plan.

A major advantage of group life insurance to an employee is that

usually coverage may be obtained regardless of health. An

employee who leaves the group may, without a medical

examination, convert the group coverage to an individual policy.

The premiums on group life insurance are considerably less than

on comparable individual policies, mainly because the selling and

administrative costs are minimal.

- 12 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 13/96

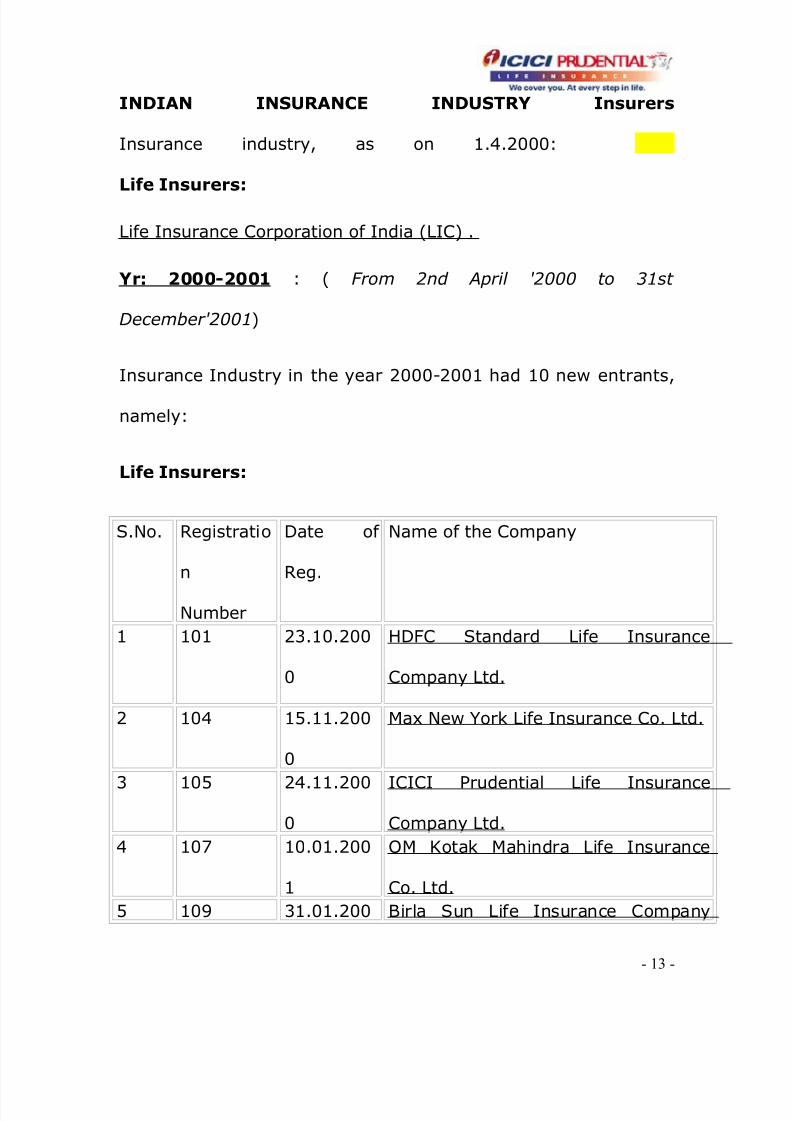

INDIAN INSURANCE INDUSTRY Insurers

Insurance industry, as on 1.4.2000:

Life Insurers:

Life Insurance Corporation of India (LIC) .

Yr: 2000-2001 : ( From 2nd April '2000 to 31st

December'2001)

Insurance Industry in the year 2000-2001 had 10 new entrants,

namely:

Life Insurers:

S.No. Registratio

n

Number

Date of

Reg.

Name of the Company

1 101 23.10.200

0

HDFC Standard Life Insurance

Company Ltd.

2 104 15.11.200

0

Max New York Life Insurance Co. Ltd.

3 105 24.11.200

0

ICICI Prudential Life Insurance

Company Ltd.

4 107 10.01.200

1

OM Kotak Mahindra Life Insurance

Co. Ltd.

5 109 31.01.200 Birla Sun Life Insurance Company

- 13 -

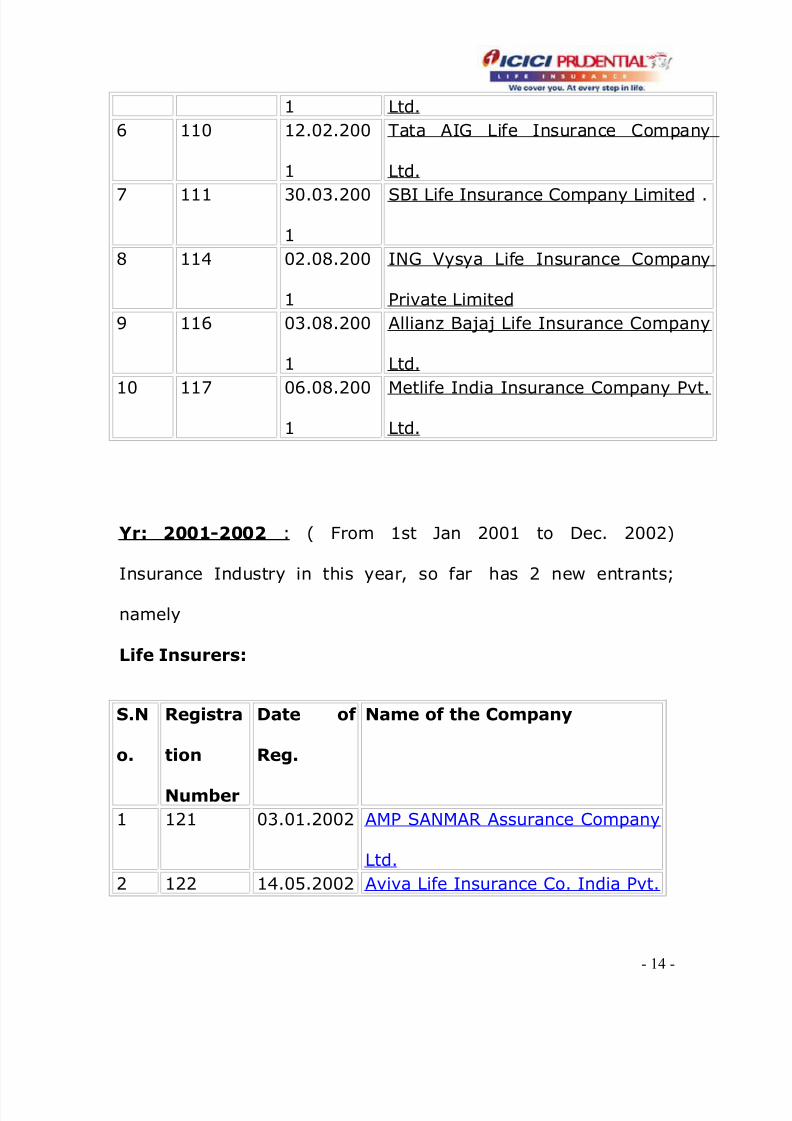

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 14/96

1 Ltd.

6 110 12.02.200

1

Tata AIG Life Insurance Company

Ltd.

7 111 30.03.200

1

SBI Life Insurance Company Limited .

8 114 02.08.200

1

ING Vysya Life Insurance Company

Private Limited

9 116 03.08.200

1

Allianz Bajaj Life Insurance Company

Ltd.

10 117 06.08.200

1

Metlife India Insurance Company Pvt.

Ltd.

Yr: 2001-2002 : ( From 1st Jan 2001 to Dec. 2002)

Insurance Industry in this year, so far has 2 new entrants;

namely

Life Insurers:

S.N

o.

Registra

tion

Number

Date of

Reg.

Name of the Company

1 121 03.01.2002 AMP SANMAR Assurance Company

Ltd.

2 122 14.05.2002 Aviva Life Insurance Co. India Pvt.

- 14 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 15/96

Ltd.

- 15 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 16/96

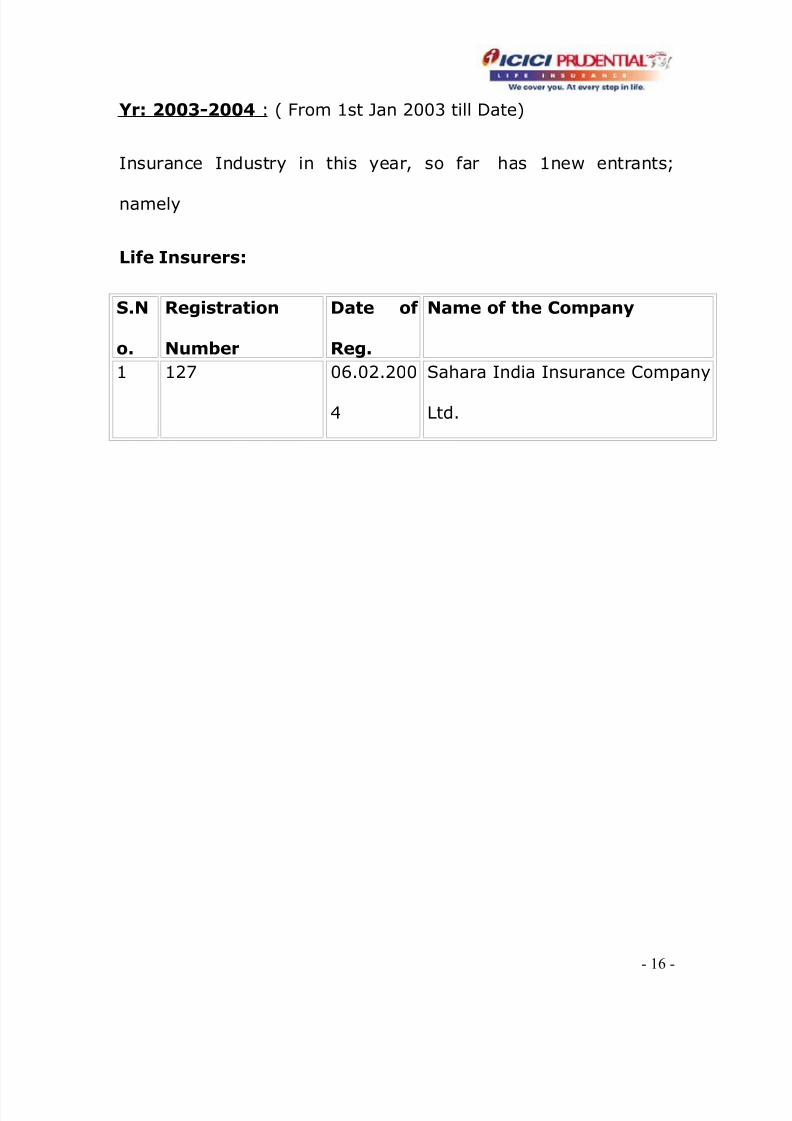

Yr: 2003-2004 : ( From 1st Jan 2003 till Date)

Insurance Industry in this year, so far has 1new entrants;

namely

Life Insurers:

S.N

o.

Registration

Number

Date of

Reg.

Name of the Company

1 127 06.02.200

4

Sahara India Insurance Company

Ltd.

- 16 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 17/96

INSURANCE SECTOR IN INDIA

The insurance sector in India has come a full circle from being an

open competitive market to nationalisation and back to a

liberalised market again. Tracing the developments in the Indian

insurance sector reveals the 360-degree turn witnessed over a

period of almost two centuries.

A brief history of the Insurance sector

The business of life insurance in India in its existing form started

in India in the year 1818 with the establishment of the Oriental

Life Insurance Company in Calcutta.

Some of the important milestones in the life insurance business

in India are:

• 1912: The Indian Life Assurance Companies Act enacted as

the first statute to regulate the life insurance business.

• 1928: The Indian Insurance Companies Act enacted to

enable the government to collect statistical information

about both life and non-life insurance businesses.

- 17 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 18/96

• 1938: Earlier legislation consolidated and amended to by

the Insurance Act with the objective of protecting the

interests of the insuring public.

• 1956: 245 Indian and foreign insurers and provident

societies taken over by the central government and

nationalised. LIC formed by an Act of Parliament, viz. LIC

Act, 1956, with a capital contribution of Rs. 5 crore from

the Government of India.

The General insurance business in India, on the other hand, can

trace its roots to the Triton Insurance Company Ltd., the first

general insurance company established in the year 1850 in

Calcutta by the British.

Some of the important milestones in the general insurance

business in India are:

• 1907: The Indian Mercantile Insurance Ltd. set up, the first

company to transact all classes of general insurance

business.

- 18 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 19/96

• 1957: General Insurance Council, a wing of the Insurance

Association of India, frames a code of conduct for ensuring

fair conduct and sound business practices.

• 1968: The Insurance Act amended to regulate investments

and set minimum solvency margins and the Tariff Advisory

Committee set up.

• 1972: The General Insurance Business (Nationalisation)

Act, 1972 nationalised the general insurance business in

India with effect from 1st January 1973.

• 107 insurers amalgamated and grouped into four

companies viz. the National Insurance Company Ltd., the

New India Assurance Company Ltd., the Oriental Insurance

Company Ltd. and the United India Insurance Company Ltd.

GIC incorporated as a company.

.

LIFE INSURANCE SECTOR IN INDIA

Many may not be aware that the life insurance industry of India

is as old as it is in any other part of the world. The first Indian

life insurance company was the Oriental Life Insurance Company,

- 19 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 20/96

which was started in India in 1818 at Kolkata1. A number of

players (over 250 in life and about 100 in non-life) mainly with

regional focus flourished all across the country. However, the

Government of India, concerned by the unethical standards

adopted by some players against the consumers, nationalised the

industry in two phases in 1956 (life) and in 1972 (non-life). The

insurance business of the country was then brought under two

public sector companies, Life Insurance Corporation of India

(LIC) and General Insurance Corporation of India (GIC).

In line with the economic reforms that were ushered in India in

early nineties, the Government set up a Committee on Reforms

(popularly called the Malhotra Committee) in April 1993 to

suggest reforms in the insurance sector. The Committee

recommended throwing open the sector to private players to

usher in competition and bring more choice to the consumer. The

objective was to improve the penetration of insurance as a

percentage of GDP, which remains low in India even compared to

some developing countries in Asia.

Reforms were initiated with the passage of Insurance Regulatory

and Development Authority (IRDA) Bill in 1999. IRDA was set up

as an independent regulatory authority, which has put in place

- 20 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 21/96

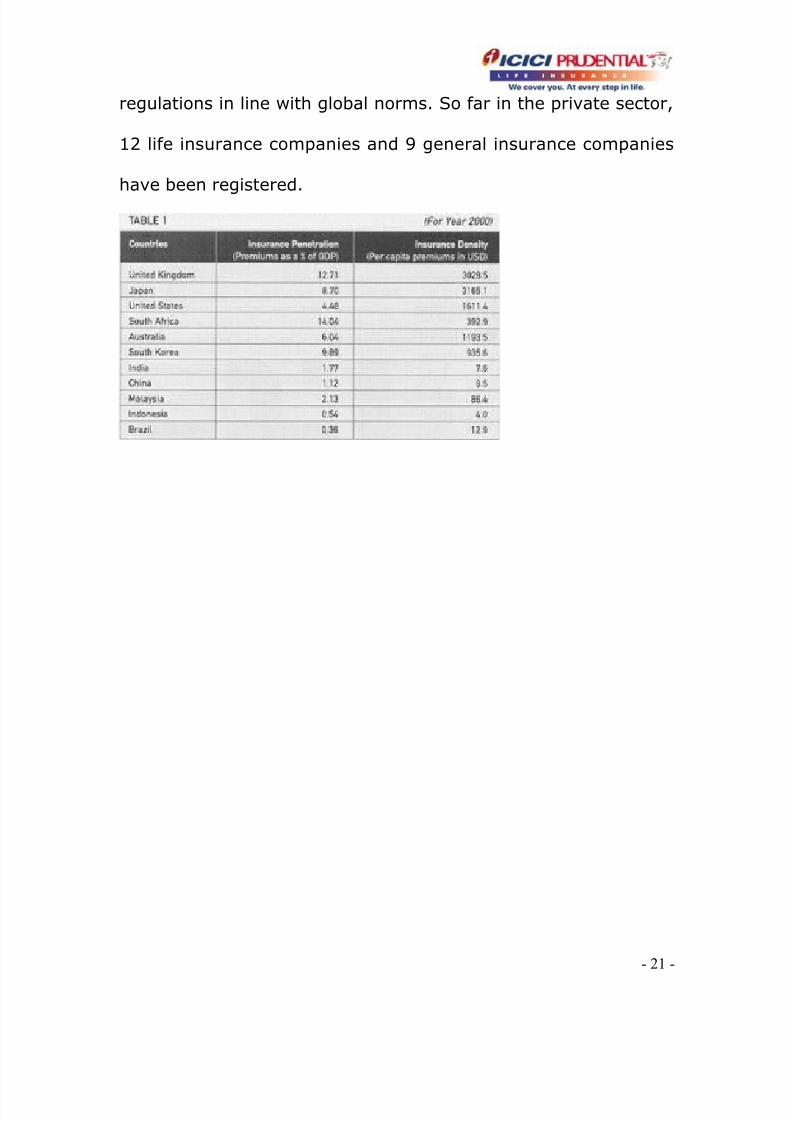

regulations in line with global norms. So far in the private sector,

12 life insurance companies and 9 general insurance companies

have been registered.

- 21 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 22/96

CHAPTER 2

COMPANY PROFILE

- 22 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 23/96

ABOUT THE COMPANY

AVIVA Life Insurance Company is a joint venture between AVIVA

& DABAR. AVIVA was amongst the first private sector insurance

companies to begin operations in December 2002 after receiving

approval from Insurance IRDA.

AVIVA equity base stands at Rs. 9.25 billion with DABAR and

AVIVA holding 74% and 26% stake respectively. In the last

financial year the company garnered Rs 1584 crore of new

business premiums for a total sum assured of Rs 13,780 crore

and wrote nearly 615,000 policies. The company has a network

of about 56,000 advisors; as well as 7 banc assurance and 150

corporate agent tie-ups. For the past four years, AVIVA has

retained its position as the No. 1 private life insurer in the

country, with a wide range of flexible products that meet the

needs of the Indian customer at every step in life.

- 23 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 24/96

AVIVA LIFE

Established in London in 1848, AVIVA, through its businesses in

the UK and Europe, the US and Asia, provides retail financial

services products and services to more than 16 million

customers, policyholder and unit holders worldwide. As of June

30, 2004, the company had over US$300 billion in funds under

management. AVIVA has brought to market an integrated range

of financial services products that now includes life assurance,

pensions, mutual funds, banking, investment management and

general insurance. In Asia, AVIVA is the leading European life

insurance company with a vast network of 24 life and mutual

fund operations in twelve countries - China, Hong Kong, India,

Indonesia, Japan, Korea, Malaysia, the Philippines, Singapore,

Taiwan, Thailand and Vietnam.

- 24 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 25/96

HISTORY OF THE COMPANY

AVIVA Life Insurance Company Limited is a 74:26 joint venture

between AVIVA & DABAR . The company brings together the local

market expertise and financial strength of DABAR and AVIVA

international life insurance experience. The company was granted

a Certificate of Registration by the IRDA on November 24,

2002and eighteen days later, issued its first policy on December

12.

From its early days, AVIVA seemed to have the wherewithal for a

large-scale business. By March 31, 2003, a little over a year

since its launch, the company had issued 100,000 polices

translating into a premium income of approximately Rs. 1,200

million on a sum assured of over Rs. 23 billion.

When the company began its operations, the need was to build a

brand that was relatable to, symbolised trust and was easily

recognised and understood. It launched a corporate campaign

using the theme of ‘Sindoor’ to epitomise protection, trust,

togetherness and all that is Indian; endearing itself to the

- 25 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 26/96

masses. The success of the campaign, ‘the calling card of the

company’, saw the brand awareness scores almost at par with its

40 year old competitor. The theme of protection was also

extended to subsequent product and category specific campaigns

– from child plans to retirement solutions – which highlight how

the company will be with its customers at every step of life.

From day one, the company has unflinchingly focussed on being

a mass-market player, developing products, creating a

distribution network and deploying resources that would further

its goal. Apart from ramping up and thoroughly training its

advisors, the company has twelve ‘Banc assurance’ partners –

the largest in the country. It swiftly revised and added to its

initial range of products, pioneering market-linked products and

pension plans, to offer customers the most flexible life insurance

policies in the country.

In February 2004, AVIVA increased its capital base by Rs. 500

million, its ninth capital hike, bringing the total paid-up equity

capital to Rs. 6,750 million. With the authorized capital of the

company standing at Rs. 12 billion, AVIVA continues to have the

- 26 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 27/96

highest capital base amongst all life insurers in the country. The

challenge AVIVA now faces is to retain its top-notch position and

continue to deliver the finest life insurance and pension solutions

to its ever-growing customer base

- 27 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 28/96

COMPANY’S VISION

“To make AVIVA the dominant Life and Pensions player built on

trust by world-class people and service.”

This company hopes to achieve by:

Understanding the needs of customers and offering them

superior products and service

Leveraging technology to service customers quickly,

efficiently and conveniently

Developing and implementing superior risk management

and investment strategies to offer sustainable and stable

returns to our policyholders

Providing an enabling environment to foster growth and

learning for our employees

And above all, building transparency in all our dealings.

- 28 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 29/96

The success of the company will be founded in its unflinching

commitment to 5 core values -- Integrity, Customer First,

Boundaryless, Ownership and Passion. Each of the values

describe what the company stands for, the qualities of its people

and the way they work.

- 29 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 30/96

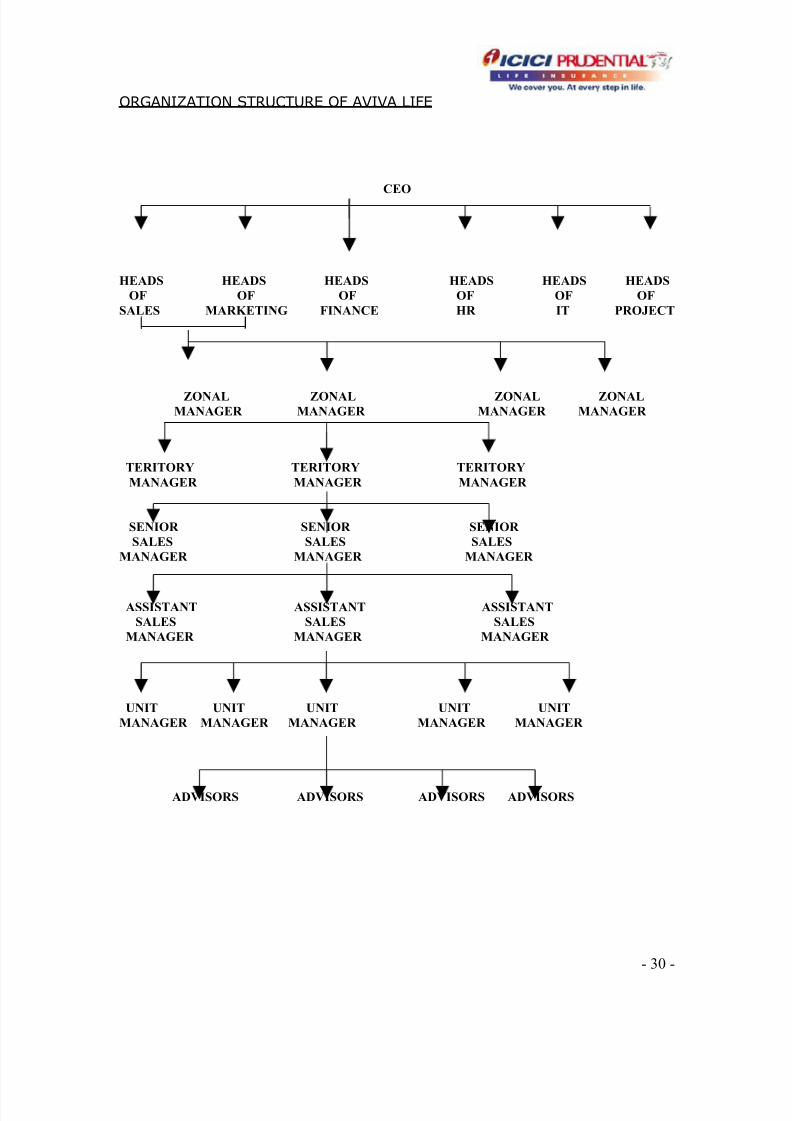

ORGANIZATION STRUCTURE OF AVIVA LIFE

CEO

HEADS HEADS HEADS HEADS HEADS HEADS

OF OF OF OF OF OF

SALES MARKETING FINANCE HR IT PROJECT

ZONAL ZONAL ZONAL ZONALMANAGER MANAGER MANAGER MANAGER

TERITORY TERITORY TERITORY

MANAGER MANAGER MANAGER

SENIOR SENIOR SENIOR

SALES SALES SALES

MANAGER MANAGER MANAGER

ASSISTANT ASSISTANT ASSISTANT

SALES SALES SALES

MANAGER MANAGER MANAGER

UNIT UNIT UNIT UNIT UNIT

MANAGER MANAGER MANAGER MANAGER MANAGER

ADVISORS ADVISORS ADVISORS ADVISORS

- 30 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 31/96

COMPANY’S ACHIEVEMENTS

Beginning operations in December 2004, AVIVA’S success has

been meteoric, becoming the number one private life insurer

within months of launch. Today, it has one of the largest

distribution networks amongst private life insurers in India,

with branches in 54 cities. The total number of policies issued

stands at more than 780,000 with a total sum assured in

excess of Rs. 160 billion.

AVIVA closed the financial year ended March 31, 2004 with a

total received premium income of Rs. 9.9 billion, up 135%

from last years total premium income of Rs. 4.20 billion. New

business premium income shows a 106% growth at Rs. 7.5

billion, driven mainly by the company’s range of unique unit-

linked policies and pension plans. The company’s retail market

share amongst private companies stood at 36%, making it a

clear leader in the segment.

To add to its achievements, in the year 2004/05 it was

adjudged Most Trusted Private Life Insurer (Economic Times

‘Most Trusted Brand Survey’ by ACNielsen ORG-MARG). It was

also conferred the ‘Outlook Money – Best Life Insurer’ award

- 31 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 32/96

for the second year running. The company is also proud to

have won Silver at EFFIES 2004 for its ‘Retire from work, not

life’ campaign. Notably, AVIVA was also short-listed to the

final round for its ‘Sindoor’ campaign in EFFIES 2004.

AVIVA’S success is rooted in its philosophy to always offer the

customer a choice. This has been the driving force behind its

multi-channel distribution strategy, which includes advisors,

banks, direct marketing and corporate agents. In fact, AVIVA

was the first life insurer to invest in multiple channels and

offer the customer choice and access; thus reducing

dependency on any one channel.

AVIVA also made great strides in the retirement solutions and

pensions market. The company's penetration of the retirement

market was driven by the focussed approach towards creating

awareness through a sustained campaign: ‘Retire from work,

not life’. Within six months, the campaign rewarded AVIVA

with an increased share of 23% of the total pensions market

and 78% amongst private players.

- 32 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 33/96

MARKET

For over 50 years, life insurance in India was defined and driven

by only one company – the Life Insurance Corporation of India

(LIC). With the Insurance Regulatory and Development Authority

(IRDA) Bill 1999 paving the way for entry of private companies

into both life and general sectors there was bound to be new-

found excitement – and new success stories. Today, just three

years since their entry, their cumulative share has crossed 13%

(Source: IRDA), far exceeding expectations.

Clearly insurance is on a growth path. The percentage of

premium income to GDP which was just 2.3% in 2000/01 rose to

3.3% in 2002/03; and life insurance has emerged as the

dominant contributor to this growth.

The industry presented a huge opportunity. Life insurance

penetration, for instance, was at an abysmal 22% of the

insurable population. However, private players have had to rise

to many challenges. They were faced with attitudinal barriers

- 33 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 34/96

towards the category and the perception that insurance was only

a tax-saving tool. Insurance per se had lost it basic rationale:

protection. It wasn’t surprising then that its potential lay frozen

and unexploited. The challenge for private insurance players was

to change the established category driver and get customers to

evaluate life insurance as an investment-cum-protection tool.

- 34 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 35/96

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 36/96

CHAPTER 3

COMPETITION

- 36 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 37/96

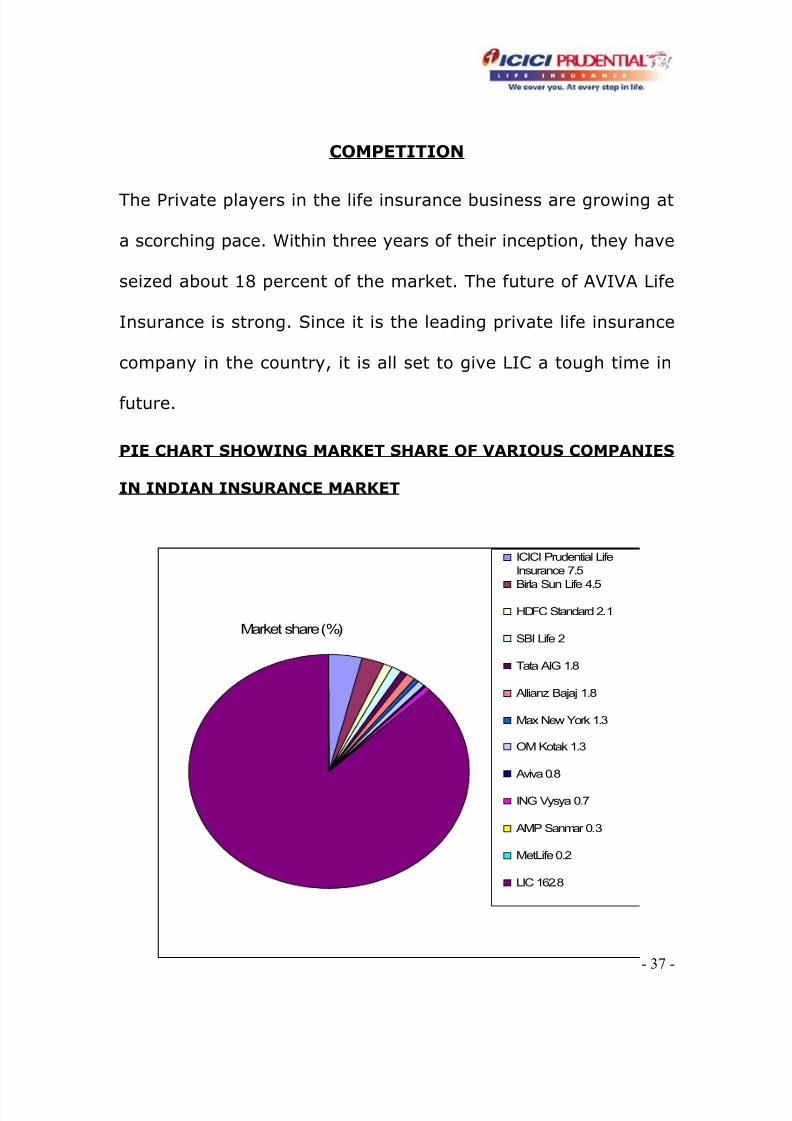

COMPETITION

The Private players in the life insurance business are growing at

a scorching pace. Within three years of their inception, they have

seized about 18 percent of the market. The future of AVIVA Life

Insurance is strong. Since it is the leading private life insurance

company in the country, it is all set to give LIC a tough time in

future.

PIE CHART SHOWING MARKET SHARE OF VARIOUS COMPANIES

IN INDIAN INSURANCE MARKET

- 37 -

Market share (%)

ICICI Prudential Life

Insurance 7.5

Birla Sun Life 4.5

HDFC Standard 2.1

SBI Life 2

Tata AIG 1.8

Allianz Bajaj 1.8

Max New York 1.3

OM Kotak 1.3

Aviva 0.8

ING Vysya 0.7

AMP Sanmar 0.3

MetLife 0.2

LIC 162.8

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 38/96

CHAPTER 4

JOB DESCRIPTION

- 38 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 39/96

DETAILED JOB PROFILE

During my specified training at AVIVA Life Insurance, our job

profile was “Agency Recruitment”. Agency Recruitment means

the recruitment of Advisors/Agents for the channel development

which is done by identifying people from qualified background

with good communication and selling skills to bring good

business for the company.

In the training period, I made telephone calls for the company,

providing information to the people on the benefits of becoming a

financial advisor for AVIVA LIFE. This was followed by filling up of

Advisor’s Recruitment Form by the people who were interested in

this proposal.

- 39 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 40/96

Advantages of becoming a financial advisor with AVIVA life

insurance:

Be your own Boss.

Work from home or Office.

No prior selling skills required.

World-class training enhances personal skills.

No start up capital required.

Work with a flexible working environment.

Unlimited earning potential.

- 40 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 41/96

AGENT/ADVISOR

An agent is one who acts on behalf of others. An “Agent” is a

person employed to do any act for another or represent another

in dealing with a third person. In the insurance industry, the term

‘agent’ is applied to a person engaged by the insurer to procure

new business.

Independent Financial Advisors (IFAs) are very common in

overseas makets, but are new in India. IFAs are qualified

professionals who can provide invaluable help to the customer in

identifying the product that suits his personal requirements. IFAs

aid the clients/customers in selection of insurance products. They

charge for their services, in contrast to the company paying

commissions.

- 41 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 42/96

ROLE OF ADVISOR

To identify prospective customers by providing them the

complete information about the products offered,

Providing tailor-made solutions to cater their individual

needs,

Conduct regular reviews to keep customers on track,

Achieve targets and also providing them better services

which is most important in life insurance because unlike

other savings or investment plans, life insurance is a long

term commitment.

- 42 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 43/96

ADVISOR BENEFITS

A premium product portfolio that caters to wide range of financial

needs,

Excellent backend support,

Attractive payments and benefits,

Round the clock customer service,

Extensive training for that edge over their competition.

ADVISOR REWARDS AND RECOGNITIONS

AVIVA’S advisors are constantly recognized and rewarded for

their performance. Numerous contests all year round promote

healthy competition amongst advisors and recognition for their

efforts. Depending on the level of business the advisor achieves

in a year, he or she can become a member of various clubs such

as the President’s club, Gold Star International and the AVIVA

- 43 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 44/96

Star India club. Each of these clubs have specific performance

criteria for qualification and members of these clubs are entitled

to attend seminars held at exotic international and domestic

locations each year. Advisors can also qualify for the renowned

MDRT (Million Dollar Round Table), an exclusive international

insurance advisors club.

WHAT DO ADVISOR POSSESS?

Confidence

Self motivation

Persuasion

Urge to be financially independent

Relationship Skills

Recognition programs

Foreign trips and Seminars.

Club Memberships

- President’s Club

- 44 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 45/96

- Achiever’s Club

- AVIVA Star Club

- MDRT Membership

SUPPORT AND TRAINING

At AVIVA Life Insurance company Limited, training is an intrinsic

element of the company’s support system for the new advisors.

Some of the training initiatives are:

FOUNDATION PROGRAM

Independent of their work experience, the foundation program

will perfect the advisors knowledge about the insurance industry;

equip them with excellent selling skills along with the

comprehensive knowledge about the products.

INSTANT RECOGNITION

Advisors achievements in the first three months of business will

be well acknowledge with the company’s SPRINT and RACE

- 45 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 46/96

awards. These are the trophies accompanied by the certificate

and point rewards given to the advisor for getting off to a flying

start.

BUSINESS DEVELOPMENT CLINIC

After one month of field experience, this program

Will give them the practical insights on objections handling and

generate ideas to get new customers and big premium policies.

ADVANCE TRAINING PROGRAMS

Once the person is accustomed to the insurance industry, the

company will continuously upgrade their capability and

knowledge through sophisticated training programs on financial

products and markets. These advance selling skills seminars will

assist them in planning for high net worth and building their

business through relationship management.

AVIVA LIFE understands the importance of training in a dynamic

business environment. Their advisors go through both generic

and specific, professional programs that help them remain well

informed and knowledgeable about the company’s products in

- 46 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 47/96

the market. There is a further focus on soft skills such as

communication, managing long-term relationships and selling

skills, which are very relevant in a service-driven industry like life

insurance.

State of the art infrastructure training facilities coupled with an

excellent faculty, guarantee an exceptional learning environment.

For advisors who might be occupied with their daily

business/professional routines, AVIVA also offers convenient

training options such as online and self-learning are also provided

by the organization.

A 17-day training schedule covers the mandatory IRDA training

requirements and AVIVA product-training module. Revision

session ensure that the candidates thoroughly understand the

course contents and are well prepared for the licensing

examination. Theoretical training is interspersed with practical

appointment settings with potential customers, giving advisors a

feel of how their business will work from the very first day. All

through, the Unit Manager and the management provide

- 47 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 48/96

continuous support to the advisors in achieving independence

towards garnering business.

PROCEDURE OF RECRUITING AN ADVISOR

Following are some of the steps of recruiting an Advisor for the

Company:

Identification of the target market.

Selection of potential individuals from the target market.

Calling them and providing them the necessary information

regarding this business opportunity.

Fixing up meetings of the interested individuals with the

Unit Manager or meeting them personally.

- 48 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 49/96

Providing them complete information regarding the

business opportunity and the benefits that they will receive.

Further, if they like the proposal, and agree to become the

advisor, they are required to fill up the forms.

FORMS INCLUDES

Insurance Advisor Application Form,

Agreement for Appointment of Insurance Advisor,

Application for Pre-Recruitment Test for Agents.

DOCUMENTS REQUIRED

Some of the documents required at the time of submitting the

forms are:

12th pass certificate/Graduation certificate.

- 49 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 50/96

Address proof

Age proof document

Seven photographs

A demand draft of Rs 1000/- cash.

SELECTION PROCEDURE

The enrolled individuals’ undergoes100 hours of intensive

training given by the company followed by an examination by

IRDA (Insurance Regulatory Development Authority). On

successful completion of the examination, he becomes the

Advisor for that company and has to bring business for them.

The selection of the Advisors is done on the basis of a “Q SCORE

CARD” issued by the company. In order to obtain the Q SCORE

CARD the candidate must meet atleast three of the following

criteria:

At least 25 years of age.

- 50 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 51/96

Married

Minimum Total family income of Rs 2

lakhs per annum.

Must be a resident of Delhi for at least

5 years.

A Graduate.

AREA ASSIGNED

For identifying an insurance agent for the company, our first

target market was our natural market. This natural market

consists of persons to whom we know and to whom we recognize

like friends, relatives, and the reference collected from them. For

this the company has a special format of Recruitment Profiling

which included various categories like:

Doctors

- 51 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 52/96

Housewives

Businessman

Brokers

Lawyers

Retired persons

Teachers

GIC Agents

Chattered Accountants

Each of these has to be approached in a different way and all of

these have to be identified within NCR. A person who is not the

resident of Delhi cannot be an advisor for the company in Delhi.

- 52 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 53/96

However, a person who is the advisor of the company can bring

business from anywhere in the country.

- 53 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 54/96

TARGET ASSIGNED

The target given to us during our summer training was to recruit

minimum three advisors for the company with good qualification

and background.

DAY TO DAY ON JOB EXPERIENCE

Experience comes through learning. Our two months training was

a good learning experience for me. During this period, I came

across a lot of people, and was exposed to various different

aspects of the corporate environment.

During my training process, I met people having different views,

attitude and perception towards Life Insurance sector.

Usually people have a perception that becoming a life insurance

advisor is a hectic job as it is a long and boring process. Most of

the people were not even ready to listen, as they were not

interested to step into this industry.

- 54 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 55/96

I even came across such people, who were interested towards

this business opportunity, but they were very busy with their

work as they were full-time professionals. So, it was a difficult

and challenging task but I enjoyed my experience.

The kind of support my organization gave me was what I was

looking forward for during my training. Our Unit Manager was

supportive and the whole staff members in the organization were

very cooperative with us. The existing advisors of the company

also helped me in the recruitment process and taught me a lot

regarding their profession and about this industry.

All in all, it was a wonderful experience working with this

organization, which has enabled me to improve my marketing

skills, and also taught me how to deal with different situations in

the corporate environment.

- 55 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 56/96

CHAPTER 5

LIMITATIONS

- 56 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 57/96

LIMITATIONS

Nothing can be achieved without difficulties and the same

happened with me. During my summer training, I came across

some difficulties but that did not stop me to achieve my target.

Some of those difficulties were:

FROM THE ORGANIZATION POINT OF VIEW

Not enough training was provided to us; as a result, it was

difficult for us to provide people with the complete

information regarding what are the benefits that they will

get from this profession.

No database was provided which restricted our target

market to our natural market only.

- 57 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 58/96

No identity card was issued at all, as a result there was no

proof that we are the representatives of the company, this

was a major problem while interacting with the

professionals like Charted Accountants, Lawyers and

Doctors.

FROM THE CUSTOMERS POINT OF VIEW

Since LIC is the leading life insurance company in the

country, it was difficult to convince people to become an

AVIVA life insurance advisor.

Money was the major problem for the people. Majority of

the people were not ready to pay Rs. 1000 as the advisor’s

examination fee.

Immediate feedback was not received from the individuals;

as a result a lot of time was wasted into it.

- 58 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 59/96

CHAPTER 6

RECOMMENDATIONS

- 59 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 60/96

RECOMMENDATIONS

The company should open up more fields for the summer

trainees in their organization apart from Agency recruitment

for their channel development.

Provide the trainees with the sufficient formal training, so

that they can carry out their task with ease.

Provide motivational schemes to the trainees, so that they

can work with confidence and zeal.

Provide some sort of database to the trainees.

- 60 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 61/96

CHAPTER 7

CONCLUSION

- 61 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 62/96

CONCLUSION

India is one of the best markets to be in. Over 75 per cent of its

vast population is without insurance; as a result of this,

insurance advisors have a very huge opportunity of capturing it.

With more than one million policyholders, AVIVA is all set to

increase their market share. The profile of the insurance advisor

too will undergo a transformation, by providing them endless

growth opportunities.

The size of the market has grown and the size of the insurable

population in India is indeed vast and the existing player has

managed to cover about one-fourth of it. The opportunities

before the players are therefore a plenty in terms of target

audience. Life insurance has today become a mainstay of any

market economy since it offers plenty of scope for garnering

large sums of money for long periods of time. A well-regulated

life insurance industry which moves with the times by offering its

customers tailor-made products to satisfy their financial needs is,

therefore, essential if we desire to progress towards a worry-free

future.

- 62 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 63/96

According to me, this is an era of mergers and acquisitions. With

such a large population and the untapped market area of this

population, Insurance happens to be a very big opportunity in

India. The insurance sector in India has come to a position of

very high potential and competitiveness in the market and those

companies that are able to best utilize their data and provide

their customer with the most personalized options will have the

distinct competitive advantage. In the current scenario, life is full

of uncertainties and life insurance is the only way that enables us

to look towards a secure and worry free future. With strong

brand and world-class sales force, it offers the advisors an

opportunity to boost up their career, achieve goals and make

tremendous progress.

- 63 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 64/96

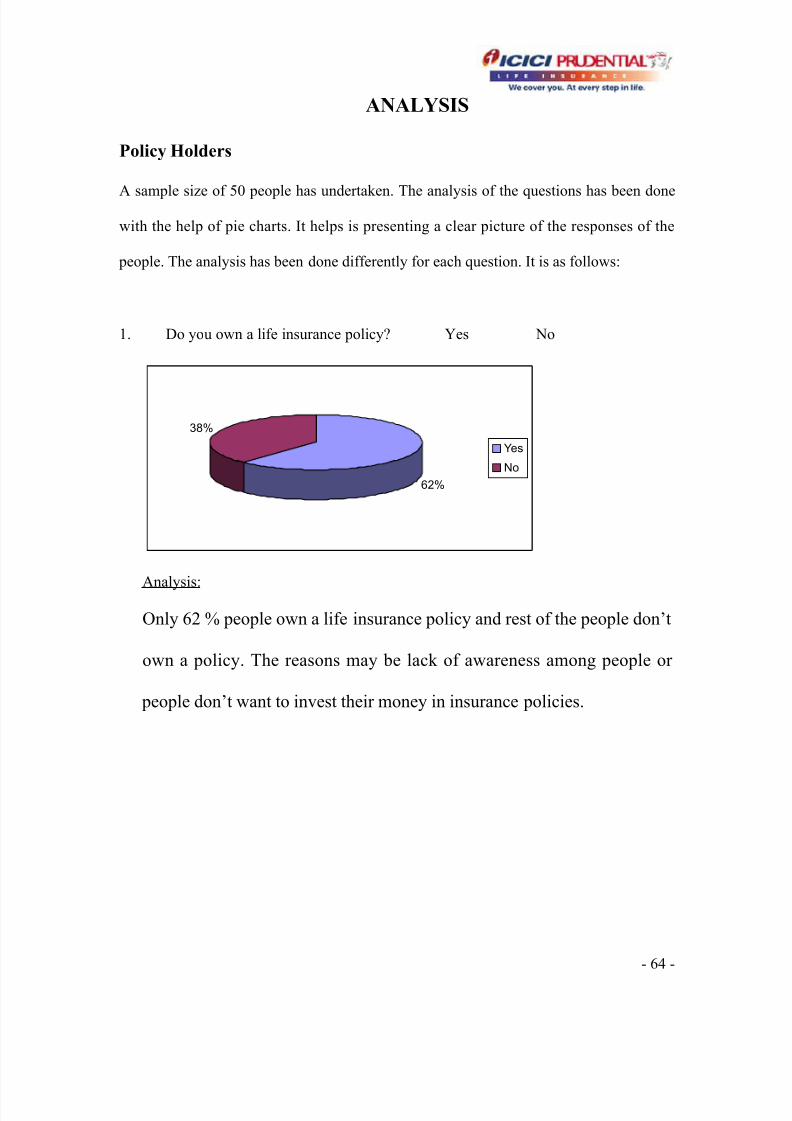

ANALYSIS

Policy Holders

A sample size of 50 people has undertaken. The analysis of the questions has been done

with the help of pie charts. It helps is presenting a clear picture of the responses of the

people. The analysis has been done differently for each question. It is as follows:

1. Do you own a life insurance policy? Yes No

62%

38%

Yes

No

Analysis:

Only 62 % people own a life insurance policy and rest of the people don’t

own a policy. The reasons may be lack of awareness among people or

people don’t want to invest their money in insurance policies.

- 64 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 65/96

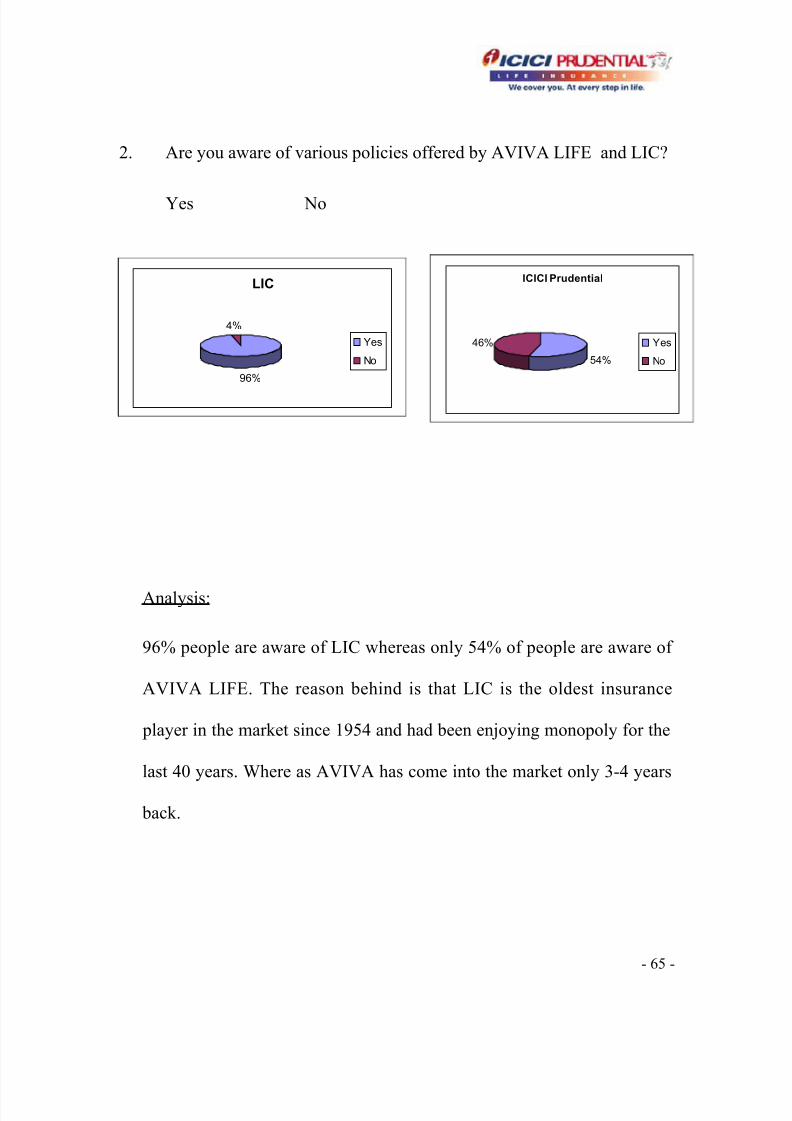

2. Are you aware of various policies offered by AVIVA LIFE and LIC?

Yes No

Analysis:

96% people are aware of LIC whereas only 54% of people are aware of

AVIVA LIFE. The reason behind is that LIC is the oldest insurance

player in the market since 1954 and had been enjoying monopoly for the

last 40 years. Where as AVIVA has come into the market only 3-4 years

back.

- 65 -

ICICI Prudential

54%

46% Yes

No

LIC

96%

4%

Yes

No

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 66/96

3. Do you want any addition in your current policy? Yes No

If yes, specify

Analysis:

As it is human nature that nobody can be satisfied with their existing

holdings. All the policyholders want some change in their existing

policies. All the policyholders of LIC i.e., 25 want some flexibility in

their policies whereas AVIVA i.e., 6 want lower premium to be charged.

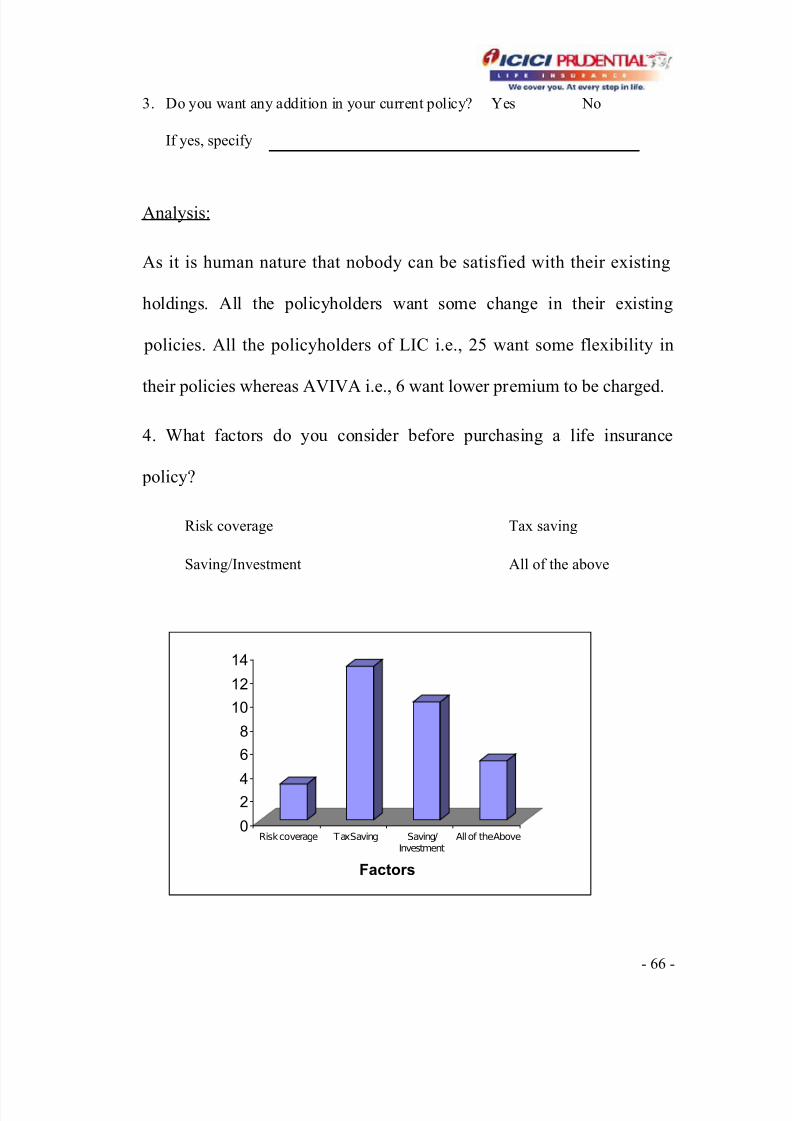

4. What factors do you consider before purchasing a life insurance

policy?

Risk coverage Tax saving

Saving/Investment All of the above

0

2

4

6

8

10

12

14

Risk coverage Tax Saving Saving/Investment

All of the Above

Factors

- 66 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 67/96

Analysis:

13 out of 31 people want life insurance as a tax saving option rather than a risk

coverage instrument. Whereas 10 people consider life insurance policy as an investment

option and only 5 people want all the features in their policies. Only 3 people are

considering risk factor as the major reason for taking a life insurance policy, which is not

an acceptable norm.

5. Do you want to comment on the products & services offered by AVIVA & LIC?

Analysis:

Most of the people whereof the view that both the companies should

come up with new products and improve their marketing strategy for

opening up the insurance sector.

6. Do you think that services have improved after allowing private players in

insurance sector? Yes No

- 67 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 68/96

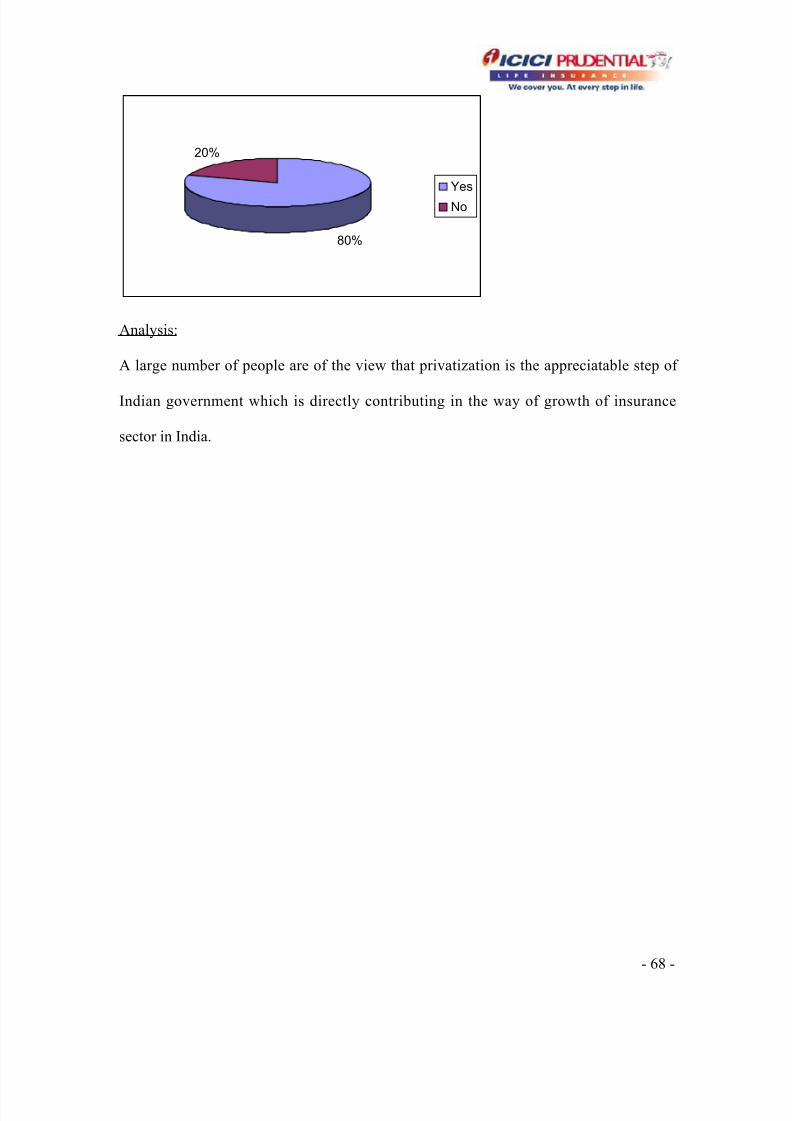

80%

20%

Yes

No

Analysis:

A large number of people are of the view that privatization is the appreciatable step of

Indian government which is directly contributing in the way of growth of insurance

sector in India.

- 68 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 69/96

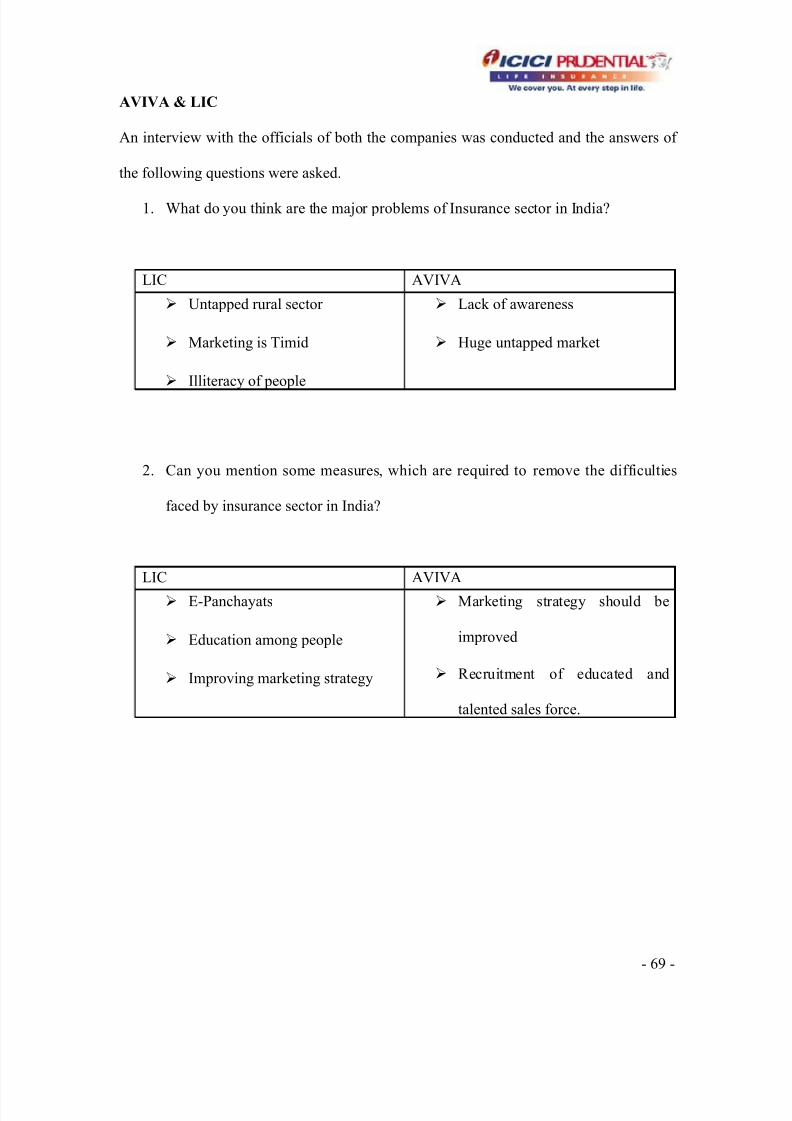

AVIVA & LIC

An interview with the officials of both the companies was conducted and the answers of

the following questions were asked.

1. What do you think are the major problems of Insurance sector in India?

LIC AVIVA

Untapped rural sector

Marketing is Timid

Illiteracy of people

Lack of awareness

Huge untapped market

2. Can you mention some measures, which are required to remove the difficulties

faced by insurance sector in India?

LIC AVIVA

E-Panchayats

Education among people

Improving marketing strategy

Marketing strategy should be

improved

Recruitment of educated and

talented sales force.

- 69 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 70/96

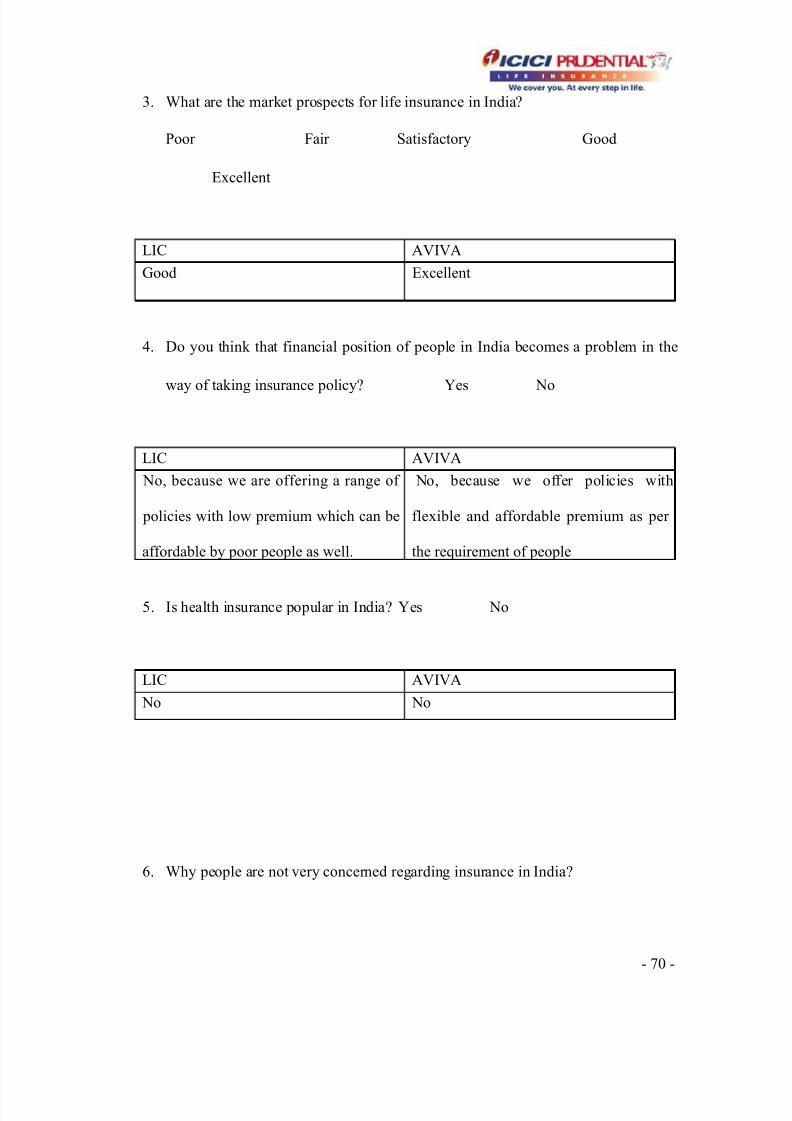

3. What are the market prospects for life insurance in India?

Poor Fair Satisfactory Good

Excellent

LIC AVIVA

Good Excellent

4. Do you think that financial position of people in India becomes a problem in the

way of taking insurance policy? Yes

No

LIC AVIVA

No, because we are offering a range of

policies with low premium which can be

affordable by poor people as well.

No, because we offer policies with

flexible and affordable premium as per

the requirement of people

5. Is health insurance popular in India? Yes No

LIC AVIVA

No No

6. Why people are not very concerned regarding insurance in India?

- 70 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 71/96

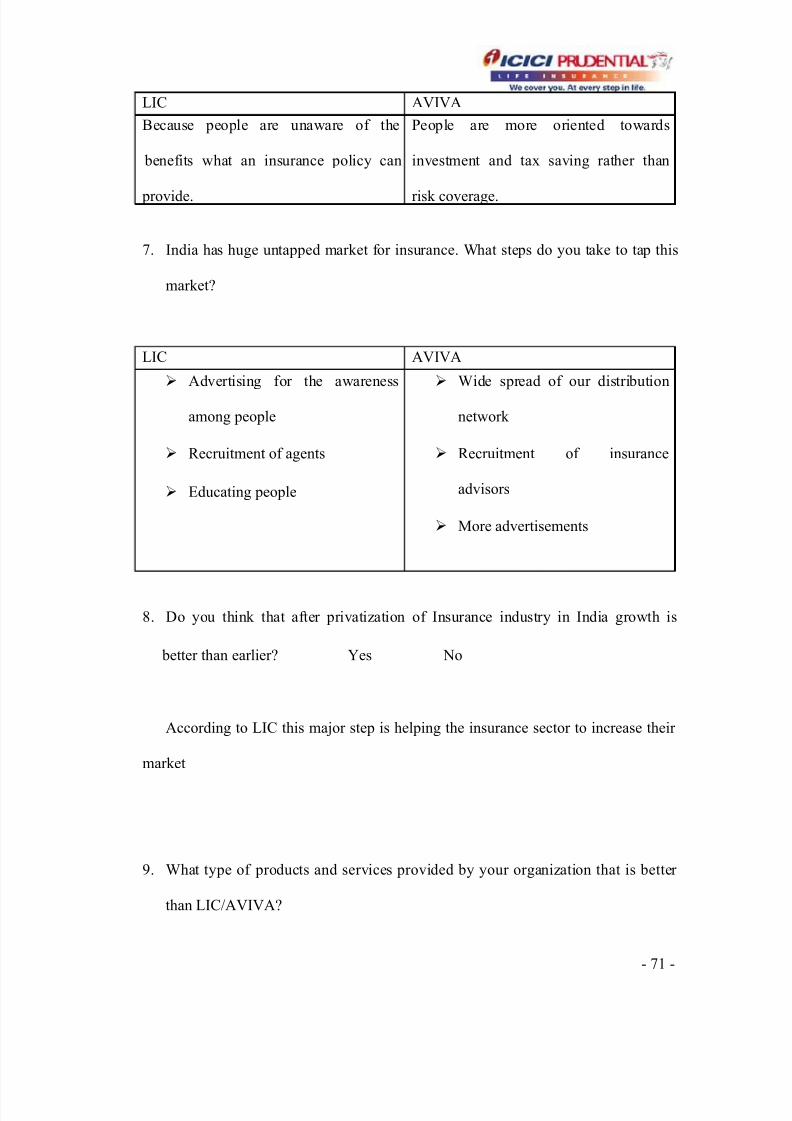

LIC AVIVA

Because people are unaware of the

benefits what an insurance policy can

provide.

People are more oriented towards

investment and tax saving rather than

risk coverage.

7. India has huge untapped market for insurance. What steps do you take to tap this

market?

LIC AVIVA

Advertising for the awareness

among people

Recruitment of agents

Educating people

Wide spread of our distribution

network

Recruitment of insurance

advisors

More advertisements

8. Do you think that after privatization of Insurance industry in India growth is

better than earlier? Yes No

According to LIC this major step is helping the insurance sector to increase their

market

9. What type of products and services provided by your organization that is better

than LIC/AVIVA?

- 71 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 72/96

LIC AVIVA

Premiums are lower

More awareness of our policies

as Compare to other players

Huge distribution network

Pension plans are better

Market returns are better as

compare to LIC and others

Online services, quick settlement

of claims, flexibility

AVIVA LIFE POLICYHOLDERS

A sample size of 50 people has undertaken. The analysis of the questions has been

done and following advantages of AVIVA’S products came into picture under the

following categories:

• UNIT-LINKED PLANS

• PENSION PLANS

• CHILD PLANS

UNIT LINKED PLANS

AVIVA

VS

- 72 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 73/96

TATA AIG INVEST ASSURE, LIC BIMA PLUS,MAX NEW YORK LIFE

MAKER ,BIRLA SUNLIFE CLASSIC LIFE

LifeTime does not have any entry age restrictions based on the term chosen.

LifeTime gives you the option to choose your own term based on your requirements.

LifeTime also gives you the flexibility to choose your premium paying term and still

continue the policy as long as you wish to. LifeTime gives you the flexibility to

completely withdraw the units from the 3rd year onwards, in case of any eventuality.

In case of any unforseen eventuality, LifeTime gives you the option to reduce the

premium amount without any change in the policy benefits. Plus, in case of an

increase in the premium paying capacity of the individual, Lifetime gives you the

flexibility to increase the premiums. Customisation of the funds is possible even in

case of LifeTime, by using the premium allocation benefit wherein the premium can

be invested in each fund based on your requirement. With increasing responsibilities,

your need for protection will also increase. LifeTime gives you the added flexibility

to increase / decrease your protection cover to suit your lifestage requirements. To

- 73 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 74/96

reward the customers for the persistency in premium payment, LifeTime offers

bonus units at regular intervals based on the premium amount paid. LifeTime does

not have any restriction on the number of top-ups in a particular year. Also the

minimum top-up allowed in LifeTime is much lower and so are the charges. LifeTime

offers partial withdrawals from the 1st year itself in case one needs to withdraw funds

due to any eventuality. LifeTime does not levy a charge on the premium holiday

facility. This is purely available as an additional benefit. LifeTime levies the charges

based on the premium invested and not on the term chosen or the age of the

individual.

PENSION PLANS

AVIVA

VS

- 74 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 75/96

LIC JEEVAN NIDHI,BIRLA FLEXI SECURELIFE RETIREMENT,HDFC

LINKED PENSION,TATA AIG NIRVANA PLUS

LifeTime Pension II allows you to accmulate till you reach the ripe old age of 75

years giving you the option to maximise your retirement kitty even if you have begun

late. In addition to giving the option of choosing a Sum Assured, LifeTime Pension

also offers a Zero Life Cover option, thereby serving as a pure accumulation vehicle

for your retirement. Lifetime Pension II gives you the flexibility to increase the

savings for your retirement in case of an increase in savings potential. On the

contrary, it also allows you to decrease your contribution levels in case of any

emergencies. LTP II allows you to choose a fund or a combination of funds as per

your risk profile and investment priorities. It also allows you to switch between funds

at any time. This helps the client to maximise his returns as per his risk appetite.

Jeevan Nidhi does not give such choices. Lifetime Pension II maximises the value for

the client in case he wishes to use some other vehicle for accumulation of his

- 75 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 76/96

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 77/96

CHILD PLANS

AVIVA

VS

LIC JEEVAN ANURAG CHILD PLAN, HDFC CHILD PLAN,BIRLA

SUNLIFE CHILD PLAN

SmartKid gives you the flexibility to choose any one of the structures based on

your needs, whether you require the money at periodic milestones or in the last few

years of the policy. All the future premiums are not waived in case of Jeevan Anurag.

In this case even in the case of the parent's death, the premiums will have to be paid

to continue the policy…which is an extra burden on the family. Option to avail of an

Income Benefit Rider - which will take care of your child's upbringing and all - round

development, if you are not around. Higher Surrender value offered in case of

SmartKid. Gives you the flexibility to choose any one of the structures based on your

needs, whether you require the money at periodic milestones or in the last few years

of the policy. All this in the same plan

- 77 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 78/96

SUMMARY

After analyzing the whole survey I come to know that market prospects of insurance is at

a growing pace. Privatization is playing an important role in the way of growth of

insurance sector in India. Most of the people are aware of the brand LIC as compare to

AVIVA, the reason being that LIC is enjoying monopoly for the last 40 years and ICICI

Prudential is the new player in the market and trying to give a stiff competition to LIC.

People expect some flexibility from LIC and lower premium from AVIVA. In India

policies are sold for tax saving purposes rather than risk coverage instrument.

As per experts views insurance sector is facing a number of problems like lack of brand

image, awareness of insurance needs, timid marketing, and illiteracy etc. Some measures

were suggested by the experts like improved marketing strategies, huge distribution

network, penetrating the rural sector etc. All the players for a better market prospect

should follow these measures.

- 78 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 79/96

CONCLUSION

For the last few years I have seen the development in the

insurance sector after privatization. This step of government

of India has resulted in form of competition in the market &

prospects to cover up the huge untapped market. Before

privatization LIC had 100 % market share but after

privatization it has come down to 90 % and 10 % for private

players. Insurance sector is developing at a faster pace as

compare to earlier one but still it has more scope to grow at

the fastest pace it ever grows. Private players are giving a

stiff competition to LIC. Though LIC offers a wide range of

products as compare to other private players like AVIVA ,

but still they are performing better with features like online

services, transparency, flexibility, quick settlement of claims

etc. AVIVA has become the # 1private player in the market

due to its performance as I can measure by its 3 % holding

of market share out of 10 % holding of all the private players

in the market.

However, still now there is a huge untapped market for insurance in India. In a survey it

was found that still there is 250million strong middle class population of India, which is

- 79 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 80/96

still untapped. On the other hand rural areas and small towns offer a huge potential to the

Insurance companies. This potential was largely untapped due to inadequate distribution

It shows that there is a great scope of insurance business in India. In India health

insurance is also not so popular. The reason behind is that people are not aware of their

insurance needs. In India insurance is sold only as a tax saving and investment option

rather than a risk-cover instrument. In my survey I found a number of reasons for the

inadequate performance of insurance sector in India. Reasons like brand image, lack of

awareness for insurance needs, lack of educated & talented sales force with insurance

companies, Lack of penetration due to inadequate marketing/delivery system are main

problems. Therefore, steps should be taken by AVIVA to overcome these hassles and

try to become a leader in the insurance sector.

- 80 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 81/96

RECOMMENDATIONS

Opening up the sector certainly means more awareness

amongst customers and higher expectations, which can

be satisfied by brand awareness i.e brand image has to

be created, new products, better packaging and

improved customer service. Potential buyers for most of

this Insurance lie in the middle class. AVIVA will have to

explore new distribution and marketing channels to

reach the customers. They should follow proper

advertising strategies as they just started by endorsing

SachinTendulkar .

The vast potential of the 250million strong middle class population of India, can

be unleashed by repositioning Life Insurance as a risk cover instrument.

The key to tap the rural market can be through Co-operative societies, Village

Panchayats and Post Offices. Where the Co-operative societies and village

Panchayats can act as ‘Corporate Agents’ to create the brand image of AVIVA in

the rural market.

ANNEXURE

- 81 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 82/96

Questionnaire 1

(AVIVA)

1 What do you think are the major problems of Insurance sector in India?

2 Can you mention some measures, which are required to remove the difficulties

faced by insurance sector in India?

3 What are the market prospects for life insurance in India?

Poor _ Fair _ Satisfactory _ Good _ Excellent _

4 Do you think that financial position of people in India becomes a problem in the

way of taking insurance policy?

Yes _ No _

5 Is health insurance popular in India?

Yes _ No _

6 Why people are not very concerned regarding insurance in India?

7 India has huge untapped market for insurance. What steps do you take to tap this

market?

8 What type of products and services provided by your organization that is better

than LIC?

Questionnaire 2

(LIC)

- 82 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 83/96

1 What do you think are the major problems of Insurance sector in India?

2 Can you mention some measures, which are required to remove the

difficulties faced by insurance sector in India?

3 Do you think that after privatization of Insurance industry in India growth

is better than earlier?

Yes _ No _

4 What are the market prospects for life insurance in India?

Poor _ Fair _ Satisfactory _ Good _

Excellent _

5 Do you think that financial position of people in India becomes a problem in

the way of taking insurance policy?

Yes _ No _

6 Is health insurance popular in India?

Yes _ No _

7 Why people are not very concerned regarding insurance in India?

8 India has huge untapped market for insurance. What steps do you take to

tap this market?

9 What type of products and services provided by your organization that is

better than AVIVA LIFE?

Questionnaire 3

(Policy Holders)

- 83 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 84/96

1 Do you own a life insurance policy?

` Yes _ No _

2 Are you aware of various policies offered by AVIVA and LIC?

Yes _ No _

3 Do you want any addition current policy?

Yes _ No _

If yes, specify

4 What factors do you consider before purchasing a life insurance policy?

_ Risk coverage _ Tax saving

_ Saving/Investment _ All of the above

5 Do you want to comment on the products & services offered by AVIVA & LIC?

6 Do you think that services have improved after allowing private players in

insurance sector?

Yes _ No _

Questionnaire 4

(AVIVA Policy Holders)

1 Do you own a life insurance policy?

` Yes _ No _

- 84 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 85/96

2 Are you aware of various policies offered by AVIVA and LIC?

Yes _ No _

3 Do you want any addition in your current policy?

Yes _ No _

If yes, specify

4 What factors do you consider before purchasing a life insurance policy?

_ Risk coverage _ Tax saving

_ Saving/Investment _ All of the above

5. Which plan you are right now under and why did you bought that?

6. Please comment on the advantages you think AVIVA products have over the other

companies’ products?

7. Do you think that services of AVIVA is much better than others?

Yes _ No _

- 85 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 86/96

BIBLIOGRAPHY

1. Insurance Management – Anand Ganguly (New Age

International)

2. Insurance & Risk Management – Dr. P. K. Gupta (HPH)

3. Insurance in India – P. S. Palande, Shah & M. L. Lunawat

(Response books)

4. Principles and Practice of Insurance – Dr. P. Periswamy

(HPH)

Brochures / Information Booklets

• AVIVA LIFE

• L.I.C. Annual Report

• Product List L.I.C.

Report/Acts

• Malhotra Committee Report on Reforms in the Insurance Sector, 1993.

• The Insurance Regulatory and Development Authority Bill, 1999.

Newspapers / Magazines

• Insurance Post

• The Economic Times

- 86 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 87/96

• The Insurance Times

PROBLEMS AND OBJECTIVES

THE PROBLEM

There are too many companies/players in the market

who are offering a number of policies to the customers. As a

result individual is confused about the brand and the policy

he/she should take and from which insurer for fulfillment of

his/her life needs.

Objectives of the Project

Primary objectives-

• Study will be conducted on Brand Image of AVIVA Life Insurance.

• An attempt will also be made to study the viewpoint of policyholders and further

to suggest the modalities to improve the efficiency of AVIVA LIFE

Secondary objectives-

To find out the advantages of the policies offered by AVIVA over various

companies.

- 87 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 88/96

An attempt will also be made to study the differentiating strategies adopted by

AVIVA to win the customers.

Research Methodology

Data is collected from both primary & secondary sources. As a primary source a

survey of policyholders & company officials has been conducted.

Articles, , newspapers, magazines, referral books and Internet services have been

used as secondary source of data.

Different tools like ratio analysis, correlation and regression have

been used to analyse the collected data.

- 88 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 89/96

SWOT ANALYSIS OF AVIVA

LIFE INSURANCE COMPANY

S TRENGTHS

• Efficiently trained sales force and advisors.

• There is improvement in response and turnaround times in specific areas such as

delivery of first policy receipt, policy document, premium notice, final maturity

payment, settlement of claims etc.

• Competitive activity, evolution of the distribution channels

WEAKNESSES

More or less all players (including the market leader LIC) have

aggressively recruited and trained advisors, appointed agents, launched

new products, improved customer service standards and

revamped/expanded their distribution networks. If at all there was any

major difference between players it was only in time lag in launching of

services.

• Consumer awareness, though increasing, is still low and

the different types of policies available and the specific

- 89 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 90/96

benefits of each often confuse them; thus it’s the job of

insurance companies to educate them about these.

O PPORTUNITIES

There are 17 insurance companies in the market today. More

companies like Reliance and Sahara will soon enter the fray. According

to a UN survey, only 4 to 6 per cent of India's population is insured. Of

this, 22 per cent are under-insured. So the market presents

opportunities for the enterprising

Only 22 per cent of the insurable population possesses life insurance.

What’s more, in a country of over one billion people, life insurance

premia forms only 1.8 per cent of the GDP, indicating the extent of

underinsurance

AVIVA Life Insurance Company has entered into a strategic tie-up with

the Federal Bank for the distribution of life insurance products. AVIVA

- 90 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 91/96

financial service consultants (FSC's) could now approach Federal Bank

customers, based on referrals from the Bank. This alliance expands

AVIVA reach to around 2 lakh customers across 30 bank branches in

Kerala and 30 in other cities including a large number of NRI

customers.

AVIVA Life Insurance Company has recruited talent at a lateral level from various

industries, such as FMCG, banking, telecom, etc, for its middle and senior management

teams. Says Shubhro Mitra, Chief, Human Resources, AVIVA Life, "The candidates

must have the requisite qualifications in their functions and relevant experience, however

not necessarily in the field of insurance. In fact, only two people amongst the senior

management team has any experience in insurance — the head of sales and the chief

actuary. Most importantly, the individuals must have a winning attitude, energy,

willingness to learn and be able to bring fresh ideas and perspectives to the business."

AVIVA Life Insurance has flagged off operations in Chennai,

the fourth office of the company. It has accepted five

proposals sponsored by Madras Cements Ltd and Lucas TVS

favouring underprivileged children. 'Salaam zindagi', a social

- 91 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 92/96

sector policy will cover larger groups amongst the

economically weaker sections of society.

The company targets to cross the one lakh policy mark by

the end of the next fiscal and has already sold 1,500 policies

till date. It hopes to break even in four to six years and for

now has no plans to introduce any new products. AVIVA has

very quickly gone on to become India’s largest private life

insurance company. Again the success lay in aggressive

marketing, smart advertising, omnipresence and quick

expansion.

A large part of the success of the new entrants ran be attributed to the government-

appointed Insurance Regulatory and Development Agency (IRDA), which developed the

regulatory framework. The regulations governingthe life and non-life insurers are

pragmatic and forward-looking, ensuring the customer is protected and creating an

environment for thriving private sector participation and a level playing field.

Bancassurance and corporate agents are the two emerging channels that give companies

an opportunity to reach out to a much larger number of individuals who might be

interested in insurance. Moreover, people inherently trust their local bank with which

they have transacted for many years, so an insurance product through that channel is also

regarded with less suspicion. These channels have only just emerged, but are already

- 92 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 93/96

making their mark. With time and the appropriate regulations, the contribution of such

channels is bound to drive penet.'at;on.of the category

Multiple touchpoints have emerged -- contact centres, email, facsimile, websites, and of

course snail-mail - which enable the customer to get in touch with insurance companies

quickly, easily and directly.

With the transformation in the industry comes a huge opportunity to tap hitherto largely

ignored segments. One of the most promising areas for life insurers is retirement

solutions. Consider this: Only 89% of the working population in our country has a form

of social security for old age. People in the unorganized sector, selfemployed persons and

those engaged in agriculture, have no form of guaranteed post-retirement income. Add to

this the fact that life expectancy is expected to rise from 77 years to 85 years in the next

decade. And that persons aged 60 and above are expected to form 8.6% of the total

population by the year 2016. It becomes obvious that the task of retirement planning and

pensions is immense and require a comprehensive, long-ranging regulations.

Penetration of life insurance is beginning to cut across socio-economic classes and attract

people who have never purchased insurance before. With this heightened awareness and

consumer education comes a willingness to view life insurance as an integral part of the

financial portfolio, marking a significant change from the earlier attitude, where

insurance was purchased as a tax-saving

- 93 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 94/96

THREATS

With multiple branches across the country a need was

identified by the head office to service their internal

employees in the same way as they would service an

external customer. The user base was growing with people

being added every day.

The Problem:

• AVIVA wanted to service its employees across different functions in the same

way as they would service an external customer while t.

• Data flow throughout the organization was via emails – thus all data was stored in

silos – an individual’s mailbox. There was no visibility or count of the issues

being faced in the organization.

• Data was hence not centrally available to gather information and convert the same

into knowledge base.

• Employees often spent considerable time in finding out from whom to seek

information. This in turn had an overall enterprise efficiency impact.

• With multiple branches all across the country, the need existed to be able to

centrally provide a pool of experts as it was not possible to have experts for every

function at every branch level.

- 94 -

8/6/2019 AVIVA SHARMA ROHIT

http://slidepdf.com/reader/full/aviva-sharma-rohit 95/96

• This in turn would mean that a user would have to know the expert, location of

the expert and his availability and correspond with him over email or long

distance phone calls. This was not feasible, as it was not possible to educate all

the users of the different experts and with possible transfer of experts the problem

was greater than it seemed.

The Challenge:

• Need of a solution that would be...

o Easy to Use – without any training, as it was not possible to train an

employee force of 1500+ spread across 40+ locations.