Embed Size (px)

Citation preview

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 1/73

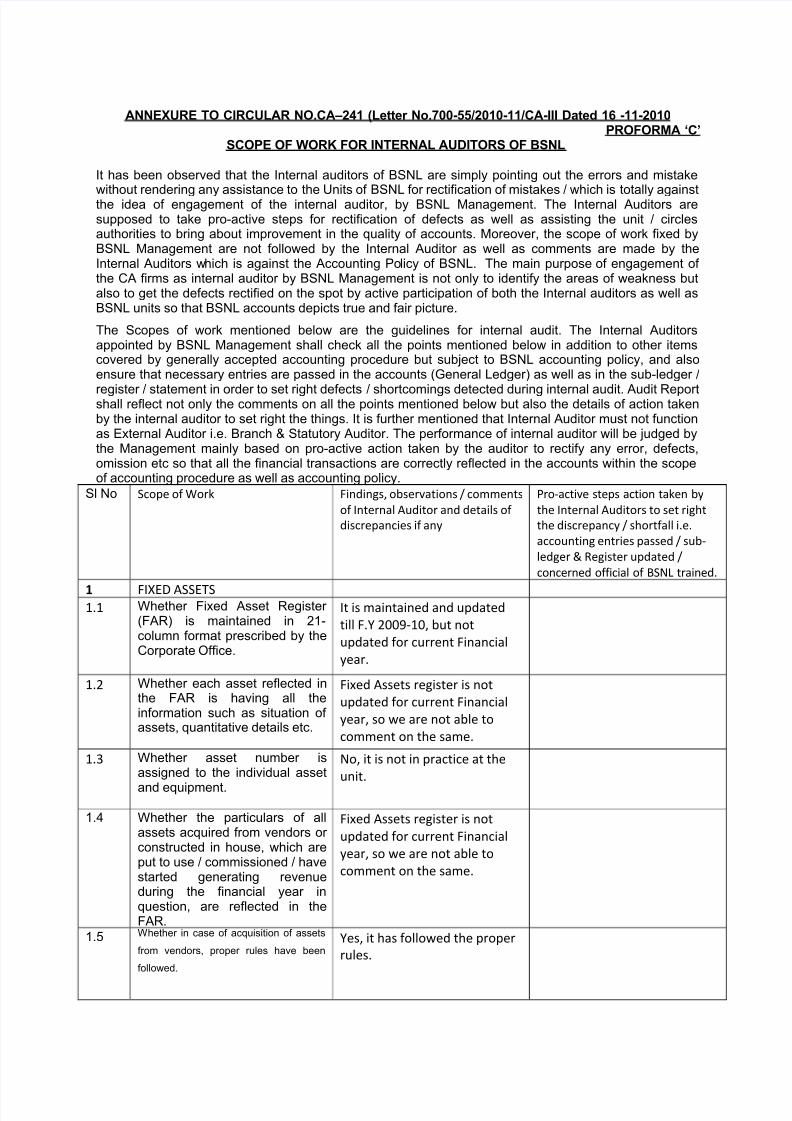

ANNEXURE TO CIRCULAR NO.CA±241 (Letter No.700-55/2010-11/CA-III Dated 16 -11-2010

PROFORMA µC¶SCOPE OF WORK FOR INTERNAL AUDITORS OF BSNL

It has been observed that the Internal auditors of BSNL are simply pointing out the errors and mistakewithout rendering any assistance to the Units of BSNL for rectification of mistakes / which is totally againstthe idea of engagement of the internal auditor, by BSNL Management. The Internal Auditors aresupposed to take pro-active steps for rectification of defects as well as assisting the unit / circlesauthorities to bring about improvement in the quality of accounts. Moreover, the scope of work fixed byBSNL Management are not followed by the Internal Auditor as well as comments are made by theInternal Auditors which is against the Accounting Policy of BSNL. The main purpose of engagement of the CA firms as internal auditor by BSNL Management is not only to identify the areas of weakness butalso to get the defects rectified on the spot by active participation of both the Internal auditors as well asBSNL units so that BSNL accounts depicts true and fair picture.

The Scopes of work mentioned below are the guidelines for internal audit. The Internal Auditorsappointed by BSNL Management shall check all the points mentioned below in addition to other itemscovered by generally accepted accounting procedure but subject to BSNL accounting policy, and alsoensure that necessary entries are passed in the accounts (General Ledger) as well as in the sub-ledger /

register / statement in order to set right defects / shortcomings detected during internal audit. Audit Reportshall reflect not only the comments on all the points mentioned below but also the details of action takenby the internal auditor to set right the things. It is further mentioned that Internal Auditor must not functionas External Auditor i.e. Branch & Statutory Auditor. The performance of internal auditor will be judged bythe Management mainly based on pro-active action taken by the auditor to rectify any error, defects,omission etc so that all the financial transactions are correctly reflected in the accounts within the scopeof accounting procedure as well as accounting policy.

Sl No Scope of Work Findings, observations / comments

of Internal Auditor and details of

discrepancies if any

Pro-active steps action taken by

the Internal Auditors to set right

the discrepancy / shortfall i.e.

accounting entries passed / sub-

ledger & Register updated /

concerned official of BSNL trained.

1 FIXED ASSETS1.1 Whether Fixed Asset Register

(FAR) is maintained in 21-column format prescribed by theCorporate Office.

It is maintained and updated

till F.Y 2009-10, but not

updated for current Financial

year.

1.2 Whether each asset reflected inthe FAR is having all theinformation such as situation of assets, quantitative details etc.

Fixed Assets register is not

updated for current Financial

year, so we are not able to

comment on the same.

1.3 Whether asset number isassigned to the individual asset

and equipment.

No, it is not in practice at the

unit.

1.4 Whether the particulars of allassets acquired from vendors or constructed in house, which areput to use / commissioned / havestarted generating revenueduring the financial year inquestion, are reflected in theFAR.

Fixed Assets register is not

updated for current Financial

year, so we are not able to

comment on the same.

1.5 Whether in case of acquisition of assets

from vendors, proper rules have been

followed.

Yes, it has followed the proper

rules.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 2/73

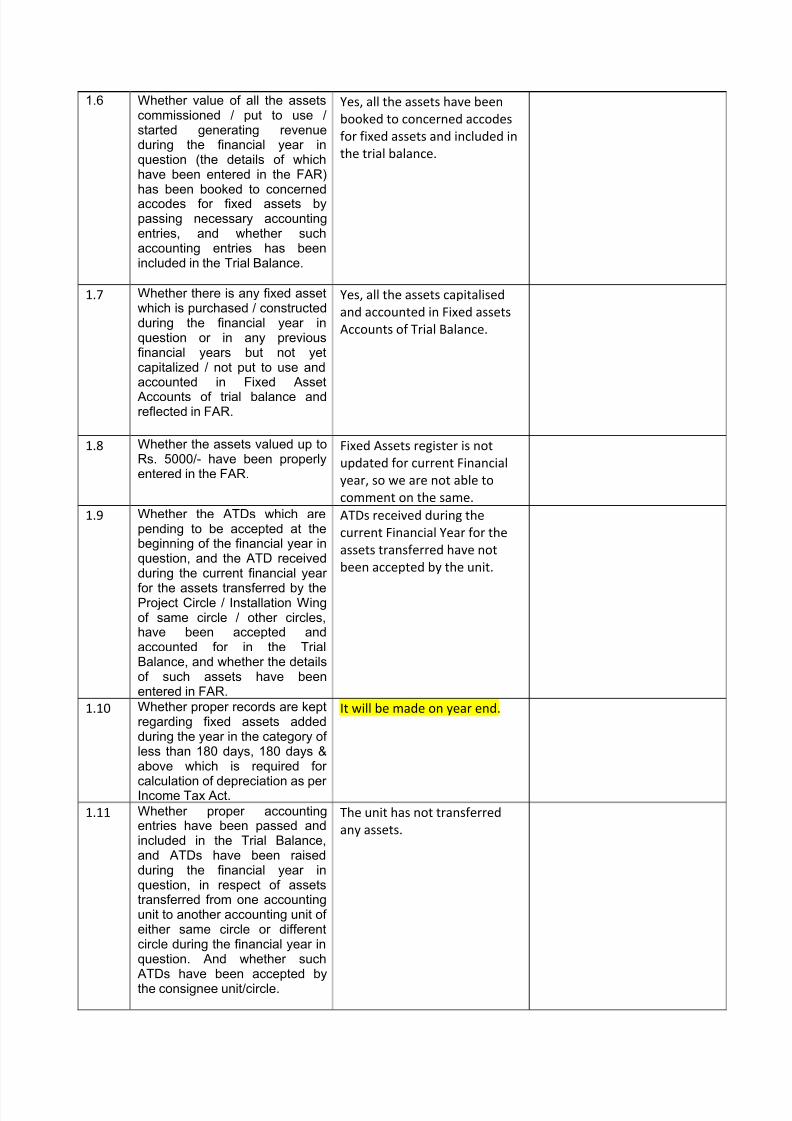

1.6 Whether value of all the assetscommissioned / put to use /started generating revenueduring the financial year inquestion (the details of whichhave been entered in the FAR)has been booked to concernedaccodes for fixed assets bypassing necessary accountingentries, and whether suchaccounting entries has beenincluded in the Trial Balance.

Yes, all the assets have been

booked to concerned accodes

for fixed assets and included in

the trial balance.

1.7 Whether there is any fixed assetwhich is purchased / constructedduring the financial year inquestion or in any previousfinancial years but not yetcapitalized / not put to use andaccounted in Fixed Asset

Accounts of trial balance andreflected in FAR.

Yes, all the assets capitalised

and accounted in Fixed assets

Accounts of Trial Balance.

1.8 Whether the assets valued up toRs. 5000/- have been properlyentered in the FAR.

Fixed Assets register is not

updated for current Financial

year, so we are not able to

comment on the same.

1.9 Whether the ATDs which arepending to be accepted at thebeginning of the financial year inquestion, and the ATD receivedduring the current financial year

for the assets transferred by theProject Circle / Installation Wingof same circle / other circles,have been accepted andaccounted for in the TrialBalance, and whether the detailsof such assets have beenentered in FAR.

ATDs received during the

current Financial Year for the

assets transferred have not

been accepted by the unit.

1.10 Whether proper records are keptregarding fixed assets addedduring the year in the category of less than 180 days, 180 days &above which is required for

calculation of depreciation as per Income Tax Act.

It will be made on year end.

1.11 Whether proper accountingentries have been passed andincluded in the Trial Balance,and ATDs have been raisedduring the financial year inquestion, in respect of assetstransferred from one accountingunit to another accounting unit of either same circle or differentcircle during the financial year inquestion. And whether suchATDs have been accepted bythe consignee unit/circle.

The unit has not transferred

any assets.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 3/73

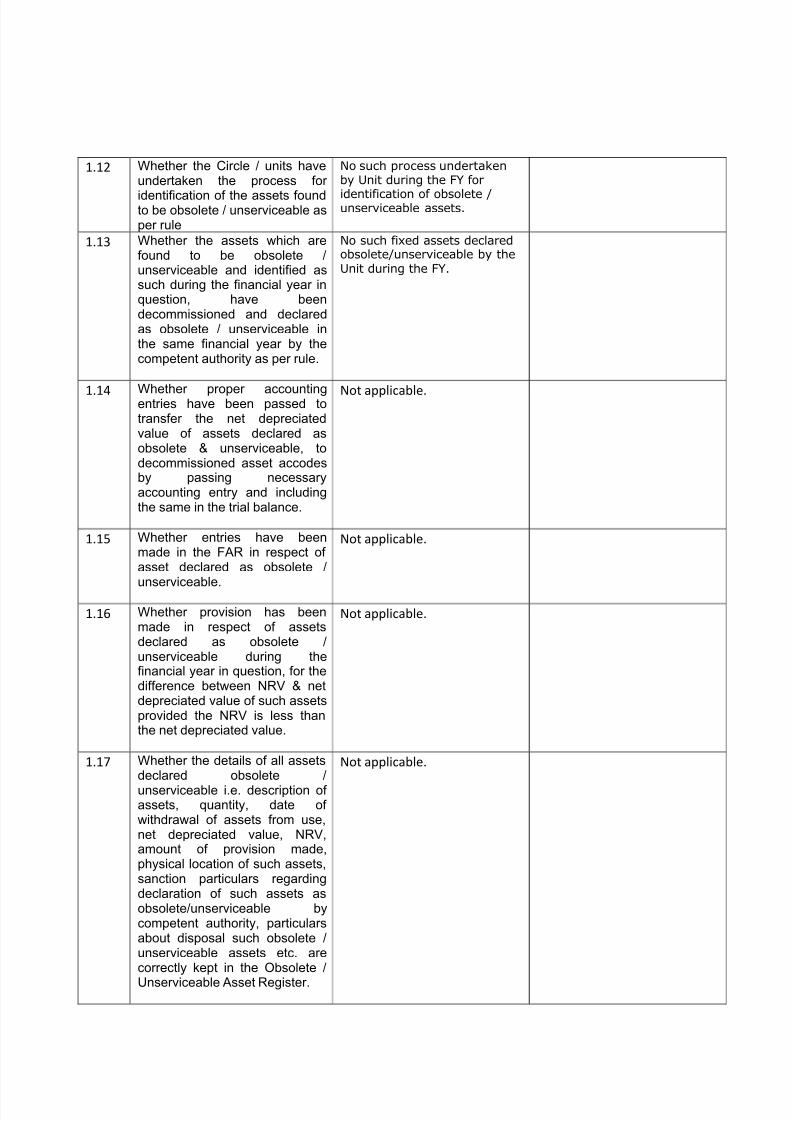

1.12 Whether the Circle / units haveundertaken the process for

identification of the assets foundto be obsolete / unserviceable asper rule

No such process undertakenby Unit during the FY for

identification of obsolete /unserviceable assets.

1.13 Whether the assets which arefound to be obsolete /unserviceable and identified assuch during the financial year inquestion, have beendecommissioned and declaredas obsolete / unserviceable inthe same financial year by thecompetent authority as per rule.

No such fixed assets declaredobsolete/unserviceable by theUnit during the FY.

1.14 Whether proper accountingentries have been passed totransfer the net depreciatedvalue of assets declared asobsolete & unserviceable, todecommissioned asset accodesby passing necessaryaccounting entry and includingthe same in the trial balance.

Not applicable.

1.15 Whether entries have beenmade in the FAR in respect of asset declared as obsolete /unserviceable.

Not applicable.

1.16 Whether provision has beenmade in respect of assetsdeclared as obsolete /unserviceable during thefinancial year in question, for thedifference between NRV & netdepreciated value of such assetsprovided the NRV is less thanthe net depreciated value.

Not applicable.

1.17 Whether the details of all assetsdeclared obsolete /

unserviceable i.e. description of assets, quantity, date of withdrawal of assets from use,net depreciated value, NRV,amount of provision made,physical location of such assets,sanction particulars regardingdeclaration of such assets asobsolete/unserviceable bycompetent authority, particularsabout disposal such obsolete /unserviceable assets etc. arecorrectly kept in the Obsolete /

Unserviceable Asset Register.

Not applicable.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 4/73

1.18 Whether value of obsolete /unserviceable assets reflected inthe accounts (under decommissioned asset accode)are reconciled with the entriesmade in Obsolete /Unserviceable Assets Register and the difference if anybetween the two sets of recordsis settled.

Not applicable.

1.19 Whether obsolete &unserviceable assets lying under decommissioned asset head aredisposed off promptly under proper sanction of the competentauthority.

Not applicable.

1.20 Whether proper accountingentries have been passed for inrespect of obsolete /unserviceable assets disposedoff during the financial year inquestion i.e. provision made if any at the time of declaring suchassets asobsolete/unserviceable havebeen utilized / written back andproper accounting entries havebeen passed to account for salevalue.

Not applicable.

1.21 Whether there are any assets,which have been retired from

service forever, but not removedfrom Fixed Asset Accounts (TB)and FAR, and depreciation iscontinued to be charged on suchassets.

No such case noticed during

the period of audit.

1.22 Whether in case of addition or deletion of assets proper recordsare kept for the purpose of preparation of Fixed AssetSchedule (Proforma IIStatement).

The FAR is not updated for

current Financial year, so we

are not able to comment.

1.23 Whether the value of all the

assets reflected in the FAR isreconciled with the valuereflected in the trial balance andwhether the difference foundduring the financial year hasbeen settled in the samefinancial year .

The FAR is not updated for

current Financial year, so weare not able to comment.

1.24 Whether depreciation has beencharged correctly in respect allassets reflected in the FAR.

It will be charged at year end .

1.25 In case of assets i.e. put to use /

commissioned during thefinancial year in questionwhether depreciation has been

It will be charged at year end .

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 5/73

charged from the date of commission / put to use.

1.26 Whether depreciation has alsobeen charged in respect of assets which have been

decommissioned / dismantledtemporarily for utilization of thesame in some other location or for some other purpose

Not applicable.

1.27 Whether in respect of assetsdeclared as obsolete /unserviceable during the year,depreciation has been chargedin the accounts correctly i.e. upto last date of functioning of suchasset.

Not applicable.

1.28 Whether depreciation has alsobeen charged in respect of stand-by assets.

There is no stand by assets.

1.29 Whether full depreciation hasbeen charged on assets valuedup to Rs. 5000/- in the 1

styear of

installation/commissioning asper instructions issued bycorporate office.

There is no asset, valued up to

Rs 5000/- commissioned /

installed.

1.30 Whether fixed asset have beenphysically verified as per order of Corporate Office.

Fixed assets have not been

physically verified.

1.31 Whether detailed record of

physical verifications has beenprepared in the formatprescribed by Corporate Office.

No any detailed record of

Physical verification has been

made.

1.32 Whether all the assets, whichare physically available as per physical verification, arereflected in the FAR.

Physical verification has not

been carried out.

1.33 Whether there is any differencebetween the assets, which arefound on physical verification,and as reflected in FAR, and if

so whether the difference hasbeen reconciled and rectificationentries have been made in FAR.

Not applicable.

1.34 Whether the value of assetsfound on physical verificationhave been reconciled with thevalue of the asset reflected inthe FAR as well as in the trialbalance and whether differencein value if any has been set rightby passing necessaryaccounting entries.

Not applicable.

1.35 Whether replacement of assetshas been accounted as per

There is no any replacement of

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 6/73

instructions issued by CorporateOffice.

assets.

1.36 Whether intangible assets havebeen properly accounted andamortized as per order of the

Corporate Office.

The unit has no intangible

assets.

1.37 Whether all the lands inpossession of the units / circleshave been analysed andcompletely bifurcated asfreehold and leasehold.

The unit has no land either

freehold or leasehold.

1.38 Whether initial lease value of leasehold land is properlyamortized over the lease period

on straight-line method.

The unit has no land either

freehold or leasehold.

1.39 Whether proper action has beentaken by the Unit / circleauthorities to renew the leaseperiod of the leasehold landwhose lease period has alreadyexpired / to be expired verysoon.

Not applicable.

1.40 Whether any leasehold land inpossession whose lease periodhas been expired, but not yetrenewed.

Not applicable.

1.41 In case of theft of assets / loss of asset due to natural calamity,fire etc whether proper accounting entry has beenpassed to relieve the FixedAsset Account (General Ledger)& FAR and whether provision for the net depreciated value of assets lost has been made

There are no any such cases.

1.42 In case of loss of asset due tonatural calamity whether the net

depreciated value of such assetshas been written off by thecompetent authority andprovision made earlier if any,has been utilized and adjusted inthe accounts.

There is no such case.

1.43 In case of loss of asset due to

theft and other reason whether

action has been taken by the

authority for recovery of asset.

Whether provision has been

made for the net depreciatedvalue of such asset. In case of

There is no such case.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 7/73

non-recovery of such asset or

partial recovery of such assets

whether competent authority

has written off the net

depreciated value of such assets

and provision made earlier has

been utilized / written back.

1.44 Whether obsolete andunserviceable assets asreflected in Register of Obsolete/ Unserviceable assets havebeen verified physically anddifference if any has beenreconciled and settled.

Not applicable.

1.45 In case of misclassification of fixed asset / components i.e.fixed asset / component hasbeen booked to wrong accodes,whether rectification of misclassification has been doneproperly as well as depreciationcharged earlier has beenadjusted correctly.

There is no such case.

1.46 Whether the amount of assets,CWIP, AccumulatedDepreciation, Sundry Debtors,Sundry Creditors etc. relating toMSC based CDMA service

which were earlier reflected inBasic Segment has beentransferred to CMTS Segmentby passing proper accountingentries.

There is no such case.

2. Capital Work In Progress

(including Civil & Electrical works

of capital nature)

2.1 Whether the competent authority

has sanctioned the project and

detailed estimate for the works

under execution.

Not applicable

2.2 Whether any cost overrun inrespect of each work completed/ under execution has occurredand whether such cost overrunhas been sanctioned by thecompetent authority.

Not applicable

2.3 Whether CWIP register / WorksRegister / Sub-ledger has beenmaintained by the units for eachof the works under execution.

It is maintained and updated

till F.Y 2009-10, but not

updated for current Financialyear.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 8/73

2.4 Whether details of each workunder execution have beenreflected in the CWIP Register /Works Register / sub-ledger.

CWIP register is not up to date.

hence, unable to comment.

2.5 Whether CWIP register / WorksRegister / sub-ledger in respectof each work has been updatedwith the transactions occurredduring the financial year inquestion i.e. services availed

from contractor for execution of work, payment is made for suchservices to the contractor,material is purchased andutilized in works

CWIP register is not up to date.

hence, unable to comment.

2.6 Whether Measurement Book hasbeen maintained for recordingthe details of works executed bythe contractor

No

2.7 Whether the project executingauthority have recorded the

details of work executed by thecontractor and services providedby the contractor during theyear, in the Measurement Book.

CWIP register is not up to date.

hence, unable to comment.

2.8 Whether based on entries madein the measurement bookexpenditure / payment has beenapproved and paid to thecontractor. Whether Measurement book has beenupdated in respect of paymentmade to the contractor

Not applicable

2.9 Whether ATDs for material /stores received from StoreDepots of BSNL / other units of BSNL for execution of works,have promptly been acceptedand booked to concernedaccode of CWIP account.Whether necessary entries havebeen made in CWIP Register /Works Register / sub-ledger inrespect of such storesimmediately.

Not applicable

2.10 Whether the stores / equipments CWIP register is not up to date.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 9/73

issued to the Contractor /turnkey project executing vendor for execution of works / turnkeyprojects have been accounted toaccode for ³Material / stores withcontractor´.

hence, unable to comment.

2.11 Whether material / equipmentactually utilized by the contractor / turnkey project executingvendor in the works, have beenbooked to CWIP accode bygiving credit to accode for

³Material / stores withcontractor´.

CWIP register is not up to date.

hence, unable to comment.

2.12 Whether necessary entriesabout utilization of stores by thecontractor / turnkey projectexecuting vendor have beenmade in CWIP Register / WorksRegister / sub-ledger.

CWIP register is not up to date.

hence, unable to comment.

2.13 Whether on completion of worksthe un-utilized / surplus materialshave been taken back to store

Depot and accounted toinventory head by giving credit to³Material / equipment withcontractor´.

CWIP register is not up to date.

hence, unable to comment.

2.14 Whether amount booked toaccode for ³Material / equipmentwith contractor´ have beenreviewed from to time andproper adjustment has beenmade about utilization of thematerial / equipment in theproject and / or return of un-

utilized items to Store Depot.

CWIP register is not up to date.

hence, unable to comment.

2.15 Whether material issued tocontractor / turn-key projectexecuting vendor but remainedun-utilized at the close of thefinancial year, have beenphysically verified and talliedwith value of the materialreflected under accode for ³Material / equipment withcontractor´.

CWIP register is not up to date.

hence, unable to comment.

2.16 Whether overheads have beencharged to capital works as per policy of BSNL i.e. on actual

CWIP register is not up to date.hence, unable to comment.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 10/73

basis i.e. whether salary of staff who have actually been engagedin execution of concernedproject work has been chargedas overhead to the projectestimate / account of the saidwork, and whether administrativeexpenditure, which are directlyattributable and identifiable to aparticular capital work, havebeen charged as overhead tothe project account / estimate of the said work.

2.17 Whether depreciation of testinginstruments, motor vehicle etc.which have been utilized for execution of a project work, hasbeen charged as overhead tocapital account / estimate of thesaid work.

CWIP register is not up to date.

hence, unable to comment.

2.18 Whether necessary accountingentries have been passed andincluded in the trial balance for transferring the overhead fromµRemuneration¶, µAdministrativeExpenditure¶ & µDepreciation¶Schedules by giving debit toCWIP accode of concernedproject work / estimate andcredit to accodes for µDeductExpenditure¶ available inconcerned µRemuneration¶,

µAdministration¶ & µDepreciation¶schedules.

CWIP register is not up to date.

hence, unable to comment.

2.19 Whether expenditure of revenuenature has been charged toProject works / CWIP and if sowhether rectification entries havebeen passed in the trial balanceto withdraw such revenueexpenditure from CWIP as wellas necessary rectification entryhas been made in the CWIPRegister / Works Register / Sub-

ledger

CWIP register is not up to date.

hence, unable to comment.

2.20 Whether liability has beencreated in the accounts for thevalue of services provided by thecontractor for execution of worksduring the financial year inquestions particularly for theservices provided by thecontractor at the fag end of thefinancial year for which either billhas not been received or nopayment has been made within

the close of the financial year.

CWIP register is not up to date.

hence, unable to comment.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 11/73

2.21 In respect of project workcompleted during the financialyear in question whether all theliabilities for executing the saidworks (cost of stores utilized,cost of services of contractor utilized, overhead i.e. salary of staff engaged in execution of work & administrative overheaddirectly attributable to concernedwork, and other liabilities if any)have been taken into account for transferring the total cost of thesaid completed project work tothe consignee circle / consigneeunit of same circle and for capitalization of the saidcompleted projects by theconcerned custodian / owner of the assets.

CWIP register is not up to date.

hence, unable to comment.

2.22 Whether payment made tocontractor for execution of project has been debited toaccode for µliability¶ / µprovision¶where the amount of liabilitywhich was created earlier for thesaid work either on actual basisor on estimated basis, isreflected.

CWIP register is not up to date.

hence, unable to comment.

2.23 Whether reconciliation of entriesmade in the CWIP Register /

Works Register / sub-ledger inrespect of expenditure incurredon capital work has been carriedout with the entries made in theCWIP Account of General ledger and whether the difference foundif any between two sets of figures has been settled bypassing necessary entries either in the accounts or in the CWIPRegister / Works Register / sub-ledger during the same financialyear

CWIP register is not up to date.

hence, unable to comment.

2.24 Whether Telecom Project Circles/ Civil & Electrical wing /installation wing of territorialtelecom circles have transferredthe capital cost of all the workscompleted during the financialyear in question to theconsignee i.e. Maintenancecircles / other Circles / units of same circle, through ATD alongwith all related documentsimmediately after the work hasbeen completed / commissioned.

CWIP register is not up to date.

hence, unable to comment.

2.25 Whether Telecom Project Circle CWIP register is not up to date.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 12/73

/ Civil & Electrical Wings /Installation wing of territorialtelecom circles have takenproper steps to get all the ATDs(raised by it) accepted by theconsignee circles i.e.Maintenance Circles / Other circles / units of same circlewithin the financial year inquestion in which the ATDs havebeen raised.

hence, unable to comment.

2.26 Whether there are instances of handing over all thecompleted works and raising

of huge number of ATDs onlyat the close of the f inancialyear by Project Cir cles andother installation wing including Civil & Electr icalwings. In such cases whataction taken by the Inter nalAuditor .

CWIP register is not up to date.

hence, unable to comment.

2.27 Whether there are project workswhich have been completedduring the financial year inquestion by the Telecom ProjectCircles / Installation wing of Territorial Telecom Circles / Civil& Electrical Wings, as well asput to use / started generatingrevenue, but could not becapitalized due to non-issue of completion report / managementcertificate regarding completionby the Project executingauthority; or completed projectworks have not been handedover to the concerned circles /units; and value of such

completed works has not beentransferred to consignee circles /units by Telecom Project Circles/ installation wing / Civil &ElectricalWings through ATD.

No

2.28 Whether consignee circles /units have accepted thecompleted works received fromTelecom Project Circles /Installation wing of TerritorialTelecom Circles / Civil &Electrical Wing during thefinancial year in question,

capitalized the same in the samefinancial year, entered the

Works has not been completed

during the year.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 13/73

particulars of such assets inFAR, and accounted the cost of the asset in asset accode of general ledger on acceptance of the ATD in the same financialyear.

2.29W

hether consignee circles havereceived the completed worksbut could not accept, capitalizeand account for the cost of completed projects due to non-receipt of completion report /management certificate, other relevant details, or due to receiptof partial information / data etcfrom the Project Executingauthority.

Works has not been completedduring the year

2.30 Whether project sanctioning andproject executing authority havereviewed all the pending CWIPparticularly the old outstandingprojects, whether age-wiseanalysis of all pending projectworks has been done by theproject sanctioning and projectexecuting authority, whether project sanctioning & projectexecuting authority have takenappropriate steps for completionof old project work particularlythe projects which are pendingfor more than one year, whether

the project sanctioning andproject executing authority havereviewed the pending projectworks from the angle of costoverrun and time overrun andwhether appropriate action hasbeen taken by the projectsanctioning and projectexecuting authorityManagement to complete eachproject within the time framefixed for completion and withinthe sanctioned cost.

CWIP register is not up to date.

hence, unable to comment.

2.31 Whether Project ExecutingAuthority has completed theCWIP during the financial year inquestion for which provision wasmade in previous financialyear(s) based on the Branch andStatutory Auditor¶s observations(being an old project) andwhether the provision created inprevious financial year(s) for such old projects has beenwritten back due to completion of such project works in the currentfinancial year.

CWIP register is not up to date.

hence, unable to comment.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 14/73

2.32 Whether any project works hasbeen abandoned during thefinancial year in question by thecompetent authority.

CWIP register is not up to date.

hence, unable to comment.

2.33 Whether appropriate accounting

entries have been passed andincorporated in the CWIPaccount of General Ledger andprovision has been made for theestimated loss in respect of project work, which has beenabandoned under the sanction of the competent authority.

CWIP register is not up to date.

hence, unable to comment.

2.34 Whether entries have beenmade in the CWIP Register /sub-ledger in respect of projectsabandoned during the financialyear in question.

CWIP register is not up to date.

hence, unable to comment.

2.35 Whether serviceable stores /equipments recovered from suchabandoned projects have beentransferred to Store Depots /other works and necessaryaccounting entries have beenpassed

CWIP register is not up to date.

hence, unable to comment.

2.36 Whether damaged /unserviceable stores /equipments recovered fromabandoned projects have been

disposed off and necessaryaccounting entries have beenpassed for the sale value etc.

Not applicable

2.37 Whether necessary write off sanction for the actual loss(worked out after taking intoaccount the amount to berealized on disposal of equipments / stores, value of serviceable items / storesreturned to the Store Deport /other works) has been issued by

the competent authority inrespect of project worksabandoned by the competentauthority. In case provisionexists for such abandoned CWIPwhether it has been utilized andexcess provision has beenwritten back.

CWIP register is not up to date.

hence, unable to comment

2.38 Whether physical verification of CWIP has been carried out bythe authorities of Circle / unit asper instructions of the Corporate

Office.

Physical verification has not

been carried out during the

year.

2.39 Whether details of physicalverification of CWIP are

Not applicable.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 15/73

recorded in the formatprescribed by Corporate Office

2.40 Whether reconciliation of CWIPfound on physical verification,has been made with the

particulars of concerned CW

IPas available in the CWIPRegister / Works Register / sub-ledger and the difference if anyhas been settled by passingnecessary entries in the CWIPRegister / Works Register / Sub-ledger.

Not applicable.

2.41 Whether value of CWIPphysically available has been

reconciled with the valuereflected in CWIP account of General ledger and difference if any has been settled by passingnecessary accounting entries.

Not applicable.

2.42 Whether stores found surplus atworksite in respect of completedworks have been sent back tostores depots or transferred toother works (where required)and necessary accountingentries have been made by thedebiting the Inventory Account(in case stores sent to storedepot) / debiting the worksaccount (in case storestransferred to other work) bygiving credit to CWIP accode for concerned Project work.

Not applicable.

2.43 Whether surplus stores lyingwith contractor in respect of completed works have beentaken back from the contractor and transferred to stores depotsor to other works (where

required) and necessaryaccounting entries have beenmade by the debiting theInventory Account (in casestores sent to store depot) /debiting the works account (incase stores transferred to other work) by giving credit to accodefor µmaterial issued to contractor where value was earlier bookedat the time issue of such storesto contractor.

Not applicable.

2.44 Whether diversion of inventory /equipment from one project work

Not applicable.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 16/73

to another project work has beenproperly accounted.

3. Inventory

3.1 Whether Wholesale Depot,Circle Telecom Store Depots

and Store Dumps havemaintained the bin cards andPriced Store Ledger.

It is not practice to maintain

Bin cards and Price Store

Ledger in the store.But,

quantitywise Stock Register is

maintained.

3.2 Whether all the stores / materialreceived from Vendor / supplier during the financial year inquestion or in any of the

previous financial years, havebeen recorded in the Bin Card,Priced Store Ledger (quantityand other details) immediatelyon their receipt and acceptanceby the consignee. (Stores /material received must not bedirectly charged to CWIP but tobe routed through InventoryAccount).

The same is recorded in Stock

register immediately on their

receipt.

3.3 Whether full liability for storesreceived in good condition fromsupplier/vendor as per terms and

conditions of purchase order during the financial year inquestion, has been created,whether accounting entries for such liability has been passedand included in the InventoryAccount of General Ledger,whether necessary entry for thevalue of such stores has beenmade in the Priced Store Ledger immediately on acceptance of the material by the consignee incase the accounting unit of theconsignee is the paying authorityof the stores received. Andwhether payment made tovendor / supplier subsequentlyagainst such stores has beendebited to accode where theamount of liability / provision hasbeen credited at the timecreating the liability (on actualbasis) / provision (on estimationbasis).

Yes, Necessary entry is made.

3.4 In case the paying authority for the stores received, is a different

accounting unit whether thevalue of the stores has been

No Such Case.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 17/73

accounted in the Inventoryaccount of general ledger immediately on receipt of ATD or from the information / data of ATDs uploaded by the payingauthority in IBTMS Package andwhether necessary entry aboutvalue of such stores has beenposted in the Priced StoresLedger immediately.

3.5 In case of stores / materialreceived during the financial

year in question or any of theprevious financial years fromother units of BSNL whether entries about quantity and other information of the stores havebeen made in the Bin card &Priced Stores Ledger immediately on receipt of Stores.Whether value of such storeshas been accounted in theinventory account of generalledger immediately on receipt of ATD or from the information of

ATDs uploaded by theaccounting unit of consignor (BSNL unit) in IBTMS Packageand whether necessary entryabout value of such stores hasbeen made in priced storesledger immediately.

No Such Case.

3.6 Whether valuation of inventoryhas been made taking intoaccount all cost including cost of stores paid to the supplier /vendor, transportation cost ±primary distribution cost andexcluding the CENVAT portionfor excise duty & CVD. Whether the amount of inward freight,taxes and duties (not eligible for CENVAT), octroi etc in questionhave been merged with thevalue of inventory and notbooked separately to accodeswhich had been allotted earlier but deleted latter on. Whether store-keeping charges have notbeen taken for valuation of inventory.

Not applicable

3.7 Whether weighted average rateof each item of store has been

Weighted average rate is notcalculated.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 18/73

calculated at the time receipt of new consignment. Whether weighted average rate has beenentered in the Priced StoreLedger.

3.8W

hether stores have beenissued on the basis of approved(by the competent authority)indent placed by the consignee /indenter.

Yes, Stores are issued on theapproval of DGM.

3.9 Whether particulars of stores

issued during the financial year in question have been noted inthe Bin Card, Priced StoresLedger immediately on issue of the stores to theconsignee/works.

Such particulars are maintained

in Stock Register.

3.10 In respect of stores issued fromthe Store Depot / units of BSNLto works during the financial year in question whether ATDs for thevalue of stores worked out atweighted average rate prevailing

at the time of issue, have beensent along with all document of issue to the accounting units of consignee immediately thestores are issued, whether corresponding entries for suchissue have been made in thePriced Stores Ledger, whether accounting entries have beenmade in inventory account of General Ledger and whether particulars of ATDs have beennoted in IBTMS package so thatconsignee can account for thesame.

Not applicable

3.11 Whether entries in Bin Cardabout receipt and issue of storeshave been reconciled with theentries available in the Pricedstores ledger and difference if any, has been settled promptly.

Bin Cards and Price Store

Ledger are not maintained.

3.12 Whether the value of the storesreflected in the Priced StoreLedger has been reconciled withthe value reflected in the

Inventory account of GeneralLedger and difference if any has

Not applicable

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 19/73

been settled immediately withinthe financial year in question.

3.13 Whether proper stock register has been maintained for thestores lying at work sites and

with the contractor.

Not applicable

3.14 Whether physical verification of inventory has been carried out atthe close of the financial year covering all items of inventory.

Physical Verification of

Inventory has not been carried

out in current financial year.

3.15 Whether proper documents of physical verification of storeshave been prepared in theformat prescribed by CorporateOffice (Circular No. 132 dt.17.04.2008 & Circular No. CA-240 dt. 15.11.2010)

Not applicable

3.16 Whether the quantity of storesfound on physical verificationhas been reconciled with thosereflected in the Bin card & PricedStore Ledger and whether the

difference if any has been sortedout / settled immediately bymaking necessary entries.

Not applicable

3.17 Whether value of stores foundon physical verification has beenreconciled with the value of stores reflected in Inventoryaccount of General Ledger andPriced Stores Ledger andwhether difference if any hasbeen settled within the financialyear by passing necessary

accounting entries.

Not applicable

3.18 In case of stores found shortduring physical verification ascompared with the quantityreflected in the Bin card / pricedstores ledger and such shortage/ difference could not be settledwithin the financial year inquestion, whether provision hasbeen made for the value of theshortage and necessaryaccounting entry regarding suchprovision has been incorporatedin the accounts i.e. in thegeneral ledger.

Not applicable

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 20/73

3.19 In case of stores found shortduring physical verificationconducted in previous financialyear(s) and such shortage couldnot be settled in previous

financial year(s), whether suchshortage has been totally settledduring the current financial year and whether the provision if anymade in previous financialyear(s) for such shortage, hasbeen fully adjusted in the currentyear¶s account by passingnecessary accounting entry.

Not applicable

3.20 Whether physical verification hasbeen carried out as per order of Corporate Office in respect of inventory lying unutilised with thecontractor and lying un-utilizedat work site at the close of thefinancial year and whether difference if any, has beensettled immediately.

Not applicable

3.21 In case of loss of stores due tonatural calamity, fire etc whether proper accounting entry has

been passed to relieve theInventory Account of GeneralLedger, whether entries hasbeen made in Bin Card andPriced Stores Ledger for suchstores, whether provision for thevalue of such stores has beenmade, whether the value of suchstore has been written off by thecompetent authority and whether provision for such stores madeearlier, has been adjusted bypassing necessary accountingentry in the general ledger.

No Such Case

3.22 In case of loss of inventory dueto theft and other reasonwhether proper accounting entryhas been passed to relieve theInventory Account of GeneralLedger, whether entries hasbeen made in Bin Card andPriced Stores Ledger for suchstores, whether provision for thevalue of such stores has beenmade, whether the value of suchstore has been written off by the

competent authority due to non-recovery / partial recovery of

No Such Case

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 21/73

such stores and whether provision for such stores madeearlier has been utilized /adjusted by passing necessaryaccounting entries.

3.23 Whether inventory has been

totally verified by the StoresScrapping Committee to identifythe obsolete / unserviceable /non-moving inventory and slowmoving.

Such identification has not

been made.

3.24 Whether report of the Storescrapping committee and thedetails of stores identified asobsolete and unserviceable hasbeen submitted to the competentauthority for declaring suchstores as obsolete /unserviceable.

Not applicable.

3.25 Whether NRV has beenascertained for the storesidentified as obsolete /

unserviceable

Not applicable.

3.26 Whether proper provision hasbeen made for the differencebetween the NRV and bookvalue of stores declared asobsolete / unserviceableprovided the NRV is less thanbook value of the stores.

Not applicable.

3.27 Whether the stores declared asunserviceable / obsolete by thecompetent authority have been

accounted to accode for µunserviceable/obsolete stores¶by crediting to inventory account.

Not applicable.

3.28 Whether the details of allinventory declared obsolete /unserviceable i.e. description of stores, quantity, book value,NRV, amount of provision made,physical location of suchinventory, sanction particularsregarding declaring such storesas obsolete/unserviceable by

competent authority, particularsabout disposal of such obsolete /unserviceable stores etc. have

Obsolete / Unserviceable StoreRegister is not maintainedseperately.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 22/73

been kept in the µObsolete /Unserviceable Store Register¶.

3.29 Whether obsolete /unserviceable stores reflected inthe accounts have been

reconciled with the entries madein µObsolete / UnserviceableStore Register¶ and thedifference if any between the twosets of records has been settled.

Not applicable.

3.30 Whether obsolete &unserviceable stores lying under obsolete/unserviceable inventoryaccode has been disposed off promptly under proper sanctionof the competent authority,whether provision made if any atthe time of declaring the storesas obsolete/unserviceable hasbeen utilized / written back,whether proper accountingentries has been made toaccount for sale value, andwhether loss occurred ondisposal of such obsolete /unserviceable stores has beenwritten off by the Competentauthority.

Not applicable

3.31 Whether appropriate action hasbeen taken by the Circle Heads /

Planning Section to utilize theslow moving and non-movingitems of inventory either in worksof the Circle or works of other circle

No such action has been

undertaken.

3.32 Whether stores lying unutilisedwith contractor at the close of the financial year has beentaken to inventory account bypassing accounting entries andat the beginning of the nextfinancial year such entry hasbeen reversed.

Yes

3.33 Whether storage arrangementfor keeping inventory isadequate, proper and safe.

Yes

3.34 A status report regardingcomputerization of inventoryrecords must be given in theInternal Audit report

3.35 Whether the quantity of inventory which have beenprocured during the currentfinancial year are actually

required i.e. whether decision for procurement of quantity of storesin question during the current

Not applicable.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 23/73

financial year has been takenbased on the total quantity of stores required for execution of already sanctioned projects; andtaking into account the quantityof such stores which are alreadylying in stock of the Circle andquantity of such stores which areon the pipeline at the time of deciding procurement of suchfresh quantity in question duringthe current financial year, andwhether the conditionsmentioned above have beenconsidered before takingdecision of procuring thequantity of stores in question.

3.36 Whether obsolete andunserviceable inventory asreflected in Register of Obsolete/ Unserviceable inventory havebeen verified physically anddifference if any has beenreconciled and settled.

Not applicable.

3.37 Whether proper accounting of tradable equipments has beendone as per instructions issuedby CA Section through Circular No. CA-218, CA-218A, & CA-218B

No Such case.

4 Bank & cash transaction

4.1 Whether cashbook andbankbook are properlymaintained and updated on dailybasis with all transactions takenplace during the day.

Yes, Cash book and Bank book

are properly maintained and

updated on daily basis.

4.2 Whether cash collected during aday has been remitted to bankon the same day and there is nodelay in the remittance

Yes, it is remitted to bank on

the same day.

4.3 Whether amount collected onthe last working day of thefinancial year has been remittedto bank on the same last day of the financial year.

Yes, it is remitted to bank on

the same day.

4.4 Whether bank has credited thecash remitted by the unit incollection bank account of theunit on the date of remittance, if not what action the unit has

taken to get the credit.

Yes, the bank has credited the

cash remitted by the unit in

collection bank account of the

unit on the same day.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 24/73

4.5 Whether the unit has reconciledthe amount transferred by theBank from the Escrow Account.

The unit has not any Escrow

account.

4.6 Whether cheques has beenremitted to bank on the date of

their receipt and there is nodelay in remittance

Yes, cheques have been

remitted to bank on the date of

their receipt.

4.7 Whether cheques / DD receivedon the last day of the financialyear have been remitted to bankon the same last day of thefinancial year.

Yes, it has been remitted to

bank on the same last day of

the financial year.

4.8 Whether all the cheques / DDsreceived on the closing day of the financial year but could notbe remitted to bank on the sameday due to circumstance beyondcontrol, have been treated aspart of cash balance anddisclosure in this regard hasbeen given in the annualaccounts.

Yes, it has been treated as part

of cash balance.

4.9 Whether all the cases of cheques deposited but notcredited by bank (as reflected inthe Bank reconciliationstatement), have been analysedage-wise, and whether matter has been properly pursued withthe bank authorities for earlycredit to BSNL account.

Yes, it has been analysed andmatter has been properly

pursued with the bank

authorities.

4.10 Whether in respect of dishonored / stale cheques theinstruments have been timely

forwarded by the banks alongwith consolidated list, whether the accounting unit has reversedthe amount of such dishonoredcheques in the Bank Book andbilling system and whether appropriate action has beentaken by TRA Branch and other concerned branch of unit for realization of such amount fromdebtors.

Yes, the instruments have been

timely forwarded by the banks

along with consolidated list.

4.11 Whether there are instances thatcash / cheques / DDs have been

remitted / deposited to / withbank but not accounted for by

There is no such case.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 25/73

the Accounting unit in theaccounts.

4.12 Whether the banks havetransferred the money from theCollection Account of Units to

Circle IFA and in turn from IFA toCorporate Office without anyfloat. In case of delay intransferring the money by bankwhether accounting unit and IFAhave recovered interest for thedelay as per terms andconditions of agreement enteredwith the banks.

Yes, the banks have transferred

the money from the CollectionAccount of Units to Circle IFA

without any float.

4.13 Whether TT sent by the units toIFA collection account havebeen credited by bank to IFA¶scollection account correctly andpromptly and there is nodifference between the amountaccounted by the remitting unitto concerned originating accodefor bank transfer & IFA toconcerned responding accodefor bank transfer.

Yes.

4.14 Whether all the cases of TT sentby the Units to Circle IFA and byCircle IFA to Corporate Office,but not credited to IFA collectionaccount / Corporate officeaccount or wrongly credited or

credited short, have beenanalyzed age-wise and whether the Unit and Circle office havevigorously pursued the case withthe bank authorities to get thecredit and to settle all suchcases.

Yes.

4.15 Whether all the accounting unitshaving bank account havecarried out bank reconciliation inrespect of each and every bankaccounts of units and

reconciliation has been done inrespect of all transactionsoccurred up to the close of thefinancial year, whether bankreconciliation statements haveproperly been prepared showingall the pending items and sent tothe banking cell at circleheadquarters.

Yes, the unit has carried out

bank reconciliation in respect of

each and every bank accounts of

units and reconciliation has been

done in respect of all transactions

occurred .

4.16 Whether details of each andevery item pending in the Bankreconciliation statement are

available in the unit, whether Unit has reviewed thoroughly allsuch pending items pending in

Yes, the details of each and

every item pending in the BRS

are available in the unit and the

unit has reviewed thoroughlyall such pending items .

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 26/73

the Bank ReconciliationStatement of each bank account,whether segregation of varioustypes of items have been done,whether the unit has made age-wise analysis of the pendingitems in the range of > 6 monthsbut < 1 year, >1 year but < 2years, > 2 years.

4.17 Whether the unit and SSA havetaken appropriate action to settlethe wrong / excess / short / debitand credit afforded by bankswhich are reflected in Bankreconciliation statement and howmany old wrong / excess / shortdebit and credit items (bothquantity and value involved)which were pending at the

beginning of the financial year inquestion, have been settled bythe Unit / SSA during the currentfinancial year.

Yes, the unit has taken

appropriate action to settle the

wrong / excess / short /debit

and credit afforded by Banks

which are reflected in BRS and

annexure 1 is attached for

details.

4.18 Whether SSA / accounting unithave taken proper action to clear the unlinked debit and creditreflected in the BankReconciliation Statement andhow many old un-reconciledunlinked debit and credit items(both quantity and value

involved) have been settled /cleared by the SSA / unit duringthe current financial year.

No Such Case

4.19 Whether the amount recoverablefrom bank which will be reflectedunder accode 1130816 has beentallied with the details of individual amount recoverablefrom bank kept in subsidiaryrecords, whether appropriateaction has been taken to settlethe cases, how many caseshave been settled during the

current financial year (amountinvolved) and what are thependency.

Not applicable.

4.20 Whether proper accountingentries have been passed inrespect of cheques issued butnot presented to bank by partyand has become time barred,whether full details of all the timebarred cheques have been keptin the register of Time-barredcheques, whether details of allthe time barred cheque as

available in the register of timebarked cheques have beenreconciled with the amount

Yes, proper accounting entries

have been passed in respect of

cheques issued but not presented

to bank by party and has become

time barred and full details are

available and it has been

reconciled.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 27/73

reflected in the accode for µTimebarred cheque and whether anypayment made subsequentlyagainst such time barredcheques, has been routedthrough the Register of timebarred cheque and debited toaccode for µtime barred cheque¶where the amount was creditedearlier when the cheque becametime barred, and necessary entryabout such payment has beenmade in the Register of timebarred cheque against thecorresponding entry..

4.21 Whether there is any un-identified difference / un-reconciled balance / un-confirmed balance in thecashbook and bankbook andwhether the same has beensettled promptly by the units.

There is no such case.

4.22 Whether sweeping facility hasbeen availed by the units in

respect of operation bankaccount and whether interestafforded / to be afforded by bankin such cases has beenaccounted by the units onaccrual basis.

Yes, the unit has availed

sweeping facility.

4.23 Whether interest afforded by thebank on account of sweepingfacility or delay in remitting themoney of collection bankaccount to IFA and IFA toCorporate Office is correct. If not

correct whether appropriateaction has been for recovery of the same from the bank.

Yes, the interest afforded by the

bank on account of sweepingfacility or delay in remitting themoney of collection bankaccount to IFA is correct.

4.24 Whether charges debited bybank to operation / collectionbank account are as per agreement with the bank, if notwhether all such cases has beenvigorously pursued by units andsettled by the bank authorities.

Yes, the charges debited by

bank to operation / collectionbank account are as per agreement with the bank.

4.25 Whether higher officers haveverified the cash and imprestbalance during the currentfinancial year.

Yes, higher officers have verified

the cash balance.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 28/73

4.26 Whether the units havemaintained authorized cash andbank balance and there is noholding of abnormal cash andbank balance in the operationaccount.

Yes, higher officers have verified

the cash balance.

4.27 Whether bank contra & cashcontra has been tallied and nodifference is left at the end of each month and also at theclose of the financial year.

Yes.

4.28 Whether insurance policy hasbeen taken in respect of cash inchest and cash in transit.

No, there is no insurance policy

has been taken in respect of

cash in chest and cash in

transit.

4.29 Carry out surprise check of cashat least twice once before 31

st

December and another before31

stMar ch and ensure that

certificate of cash in hand andcash on bank are correct.

Surprise check has been carried

out as on 28/12/2010.

4.30 Whether payment through cashhas been made as per rule andacknowledgement of receipt of cash by the receiver has beenobtained by the cashier.

Yes, it has been made as per

rule and acknowledgement of

receipt has been taken.

4.31 Whether revenue stamp hasbeen affixed as per applicablerules.

It is not in practice at the unit.

4.32 Whether the accounting unit hasobtained the confirmation of balance in the bank account atthe close of the financial year and the same has been talliedwith balance as per bankbookmaintained by the unit.

Yes

4.33 Whether booking made to inter bank transfer accode i.e.19801xx (originating), 19802xx(responding),49801xx(originating) and49802xx (responding) i.e.originating and responding for transfer of fund from Circle IFAto SSA / Accounting of Circleand vice versa have been totallyreconciled and whether thebalance under originatingaccode has been totally tallied

with balance under corresponding respondingaccode.

Yes, The same has been tallied.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 29/73

4.34 Whether amount booked to inter-current bank transfer originatingaccode 19701xx and 49701xx bythe Circle IFA for transfer of fundof IFA¶s collection bank account

to Corporate Office as well asthe amount booked toresponding accode 19702xx &49702xx to acknowledge theamount received from CorporateOffice has been tallied with thebooking made by CorporateOffice to accode 19702xx &49702xx

Yes, The same has been tallied.

4.35 Internal Auditor should reviewthe control procedure availablefor cash, cheque managementand suggest better system andmake detailed mention aboutthis in their report.

Yes, cash & cheque

management is adequate and

proper at the unit.

4.36 In case of fake notes received,whether provision has beenmade for the amount of fakenotes and whether appropriateaction has been taken to recover the amount from the officials /external entity and in case of non-recovery whether the losshas been written off as per sanction of the competentauthority.

The unit has not received any

fake notes.

4.37 Whether proper accounting hasbeen made in respect of depositmade as per order of the Courtand in respect of amountwithdrawn by statutory authorityfrom BSNL Bank Account.

Yes, proper accounting has

been made in respect of

deposit made as per order of

the court.

5 Sundry Debtors

5.1 Whether there is difference ason 1

stApril of the current

financial year between the total

amounts of all type of debtors asreflected in sub-ledger of debtorsand debtors as reflected inaccodes of debtors under General Ledger. If so thequantum of difference shall bementioned.

There is no any difference.

5.2 Whether difference as on 1st

April of current financial year,between all types of debtorsincluding debtors for leased andVPN circuits as reflected in the

sub-ledger and the total amountof debtors as per General

Not applicable.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 30/73

Ledger has been thoroughlyanalysed and reconciled. Thedetails of such difference of debtors settled / cleared duringthe current financial year shallbe furnished.

5.3 Whether the debtor s bookedin the general ledger from 1

st

Apr il of current f inancial year to 31

stMar ch has been totally

reconciled with sub-ledger of debtor s and no differenceexist in respect of suchdebtor s at the close of thecurrent f inancial year. If thereis any difference the sameshall be reported.

Yes.

5.4 Whether ageing analysis of sundry debtor pending at theclose of current financial year inthe range of < 6 months, >6months but <1 year, > 1 year but< 2 years and >2 years has beencorrectly worked out.

Ageing analysis of sundry

debtor will be done at the close

of financial year.

5.5 Whether appropriate action hasbeen taken to collect the

outstanding bills particularly theold outstanding from the debtorsand out of such efforts howmuch recovery against theoutstanding bills has been madeduring the financial year?

Such effort has not been taken.

5.6 How much recovery of oldoutstanding has been madeduring the financial year through projects / schemes launched as per recommendation of M/s BCGand against such collection how much cost has been incurred in the form of incentives, TA & DA etc apartfrom the salary of staff andwhether such scheme andproject are cost effective.

Not applicable.

5.7 Out of the old outstandingcleared during the financial year how much old outstanding have been cleared throughactual collection of cash andhow much by cancellation &wr ite off . The break up in this

regard shall be indicated in thereport.

There is no such case.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 31/73

5.8 Whether all the paymentreceived against the billedamount, which remainedunadjusted due to variousreasons, have been thoroughly

reviewed, linked to concerneddebtors and adjusted. Thedetails of such adjustment shallbe mentioned in the report

There is no such case.

5.9 Whether the bills, which havebeen cancelled during thecurrent financial year, are proper as per rules and whether suchcancellations have been adjusted against revenue andnot against provision for doubtful debt.

There is no such case.

5.10 Whether debts, which have beenwritten off during the financialyear, are proper as per rules andsupported by sanction given bythe competent authority as per financial powers.

There is no such case.

5.11 Whether the debts, which havebeen written off during the year,

have been charged to P&L A/cand not to provision for doubtfuldebt as per the instructionsgiven in Circular 118 dt.06.02.2008.

There is no such case.

5.12 Whether provision for doubtfuldebt at the close of the financialyear is done as per policy of BSNL and according to Circular 118 dt. 06.02.2008 & 137 dt.15.05.2008.

Provision for doubtful debt is to

be made at the close of the

financial year.

6 Loans & Advances given to

employees (including unabsorbed

employees who are either working

in BSNL or presently working in

DOT, DOP, MTNL)

6.1 Whether proper Register of loans

and advance / Recovery Register

has been maintained by the units to

record all types of interest bearing

& non-interest bearing loans and

advances (including pay advance,

TA Advance, medical advance,

excess payment etc) given by BSNL

to its employees and unabsorbed

employees who are presently either

Yes, it has maintained proper

Register.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 32/73

working in BSNL or in DOT / DOP /

MTNL

6.2 Whether proper entries have been

made in the Register at the time of

disbursing such loans and advances

(including other advance, excess

payment etc) to such employees.

Yes, it is updated at the time of

disbursement of loan and

advances.

6.3 Whether recovery of principal

amount of loans and advances and

other advances, excess payment etc

wherever applicable, has been

made on regular basis as per rule

and noted in the Register.

Yes, it is updated at the time of

recovery of loan and advances.

6.4 Whether the details of balance of

each type of loans and advances

pending to be recovered as

reflected in the Register of

employees loans & advance have

been reconciled with those

reflected in the General and no

difference exists between two sets

of figures.

Yes.

6.5 Whether the difference between

the amount of loans and advances

as reflected in the Register of loans

and advances and the amount of

loans and advances as per General

Ledger which was pointed out by

the Branch Auditors and C&AG in

previous financial years, have been

fully settled during the current

financial year.

There is no such case.

6.6 Whether interest on loans and

advances wherever applicable has

been correctly calculated, interest

has been recovered and noted in

the Recovery Register.

Yes, interest on loans and

advances have been correctly

calculated, interest has been

recovered.

6.7 Whether loans and advances given

by DOT to absorbed employees and

employees on deputation in BSNL

has not been booked as current

assets of BSNL. (Only the recovery

of such loan and advances will be

remitted to CCAs of DOT)

Yes, it has not been booked as

current assets and recovery of

such loan will be remitted to

CCAs.

7 Various type of deposits made by

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 33/73

BSNL units with different

authorities / local bodies / others

and advances given to vendors /

contractors / Govt. companies &

organization etc.

7.1 Whether proper sub-ledger /

Register has been maintained for

various types security deposits /

other deposits such as deposit with

Electricity Board / local authorities

made by BSNL units

Yes, it has maintained.

7.2 Whether proper sub-ledger /

Register has been maintained for

advances given to supplier /

contractors / Govt. companies &

organization etc.

Yes, it has maintained.

7.3 Whether proper entries have been

made in the sub-ledger / Register

for security deposits and Register of

advances at the time of givingSecurity deposit / other deposits

and advances.

Yes.

7.4 Whether recovery of amount of

advances given to vendor / supplier

/ contractor / Govt. companies &

organization and interest thereon

has been made as per terms and

conditions of giving advance and

such recovery has been noted in

the concerned Register

Yes.

7.5 Whether the balance of security

deposits / other deposits and

advances as reflected in the

concerned Register / sub-ledger has

been reconciled with entries made

in the general ledger and no

difference exists between two sets

of figures.

Yes, it has been reconciled.

7.6 Whether the difference between

the amount of security deposits /There is no such difference.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 34/73

other deposits and advances as

reflected in the Register of Security

Deposits / other deposits and

Register of advances and the

amount of security deposits /

deposits and advances as reflected

in the General Ledger, which waspointed out by the Branch Auditors

and C&AG in previous financial

years, have been fully settled

during the current financial year.

8 EMD, SD given by BSNL Units and Bank guarantee given byBSNL Units to other s

8.1 Whether proper sub-ledger /Register has been maintainedfor keeping details of EMD & SDgiven by BSNL Units.

Yes, it has been maintained.

8.2 Whether refund of EMD & SDhas promptly been obtained onfulfilment of all the terms andconditions related to it and samehas been noted in the EMD/SD

Register.

Yes, the EMD/SD register has

been maintained and refund is

noted properly in the same.

8.3 Whether the details of EMD &SD as reflected in the EMD &SD register / sub-ledger havebeen totally reconciled with thebooked figure of EMD / SDreflected in the General Ledger and difference if any, betweentwo sets of figure has beensettled.

Yes, it has been reconciled.

8.4 Whether Register for Bank

Guarantees given by BSNL Unithas been maintained and detailsof all such bank guaranteeshave been kept in the saidRegister.

No such case noticed during

the year.

8.5 Whether BSNL units have got the

bank guarantees released promptly

on fulfillment of terms and

conditions.

No such case noticed during

the year.

9 Temporary advance & Imprest

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 35/73

9.1 Each and every expendituremade from temporary advanceand the Inter nal Auditor mustscrutinize imprest frompropr ietary angle.

Yes, the expenditure made

from temporary advance has

been scrutinized.

9.2 The genuineness of at least25% of voucher s of temporaryadvance and imprest for itemsprocured / services availed mustbe checked by the Inter nalAuditor. The findings of suchchecking should be reported inthe Internal Audit Report.

The vouchers of temporaryadvance have been vouched

and it is found to be correct.

9.3 Whether there are incidence of taking temporary advanceinvolving huge amountfrequently / within shortinterval by selective group of off icer s and whether there is justif ication for suchtemporary advance in view of the fact that repair &maintenance of most of assets are done through annualmaintenance contract andmost of other works of recurr ing nature are carr iedout through contractor selected through establishedprocedures. The InternalAuditor to the Circle IFA mustreport any abnormality in this

respect. The f indings shouldbe given in the inter nal auditreport.

There is no such case.

9.4 Whether there are instances of granting temporary advancewithout adjusting the previous one. If so, what action has beentaken by the IFA / Head of theUnit to prevent such type of irregularities must be indicatedby the Internal Auditor in theAudit Report.

There is no such case.

9.5 Whether there are instances of non-submission of bills againsttemporary advance within thescheduled time frame for adjustment of temporaryadvances. In case of delaywhether interest has been recovered for the delay as per order from the concer nedoff icer who has defaulted, andcredited to BSNL Account.The Internal Auditors in the Audit

Report shall indicate theremedial action taken by theManagement in this regard.

Yes, interest has been

recovered for the delay.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 36/73

9.6 The Internal Auditor in the Audit

Report shall indicate what action

has been taken by the Head of Unit

and IFA of the Circle to control the

expenditure from TemporaryAdvance and Imprest.

The head of the unit has

implemented a system to not

sanction any further temporary

advance until the first one is

settled (i.e. bill & invoicesubmitted and balance is

settled)

10 Amount recoverable from DOT,

DOP, MTNL

10.1 Whether Control Registers /Sub-ledgers have beenmaintained for various type of amount recoverable from DOTsuch as GPF advance/finalwithdrawal given by BSNL to its

absorbed staff, salary of BSNLstaff working in DOT, leavesalary paid to BSNL employeesworking in DOT on deputation.

Yes, Control Registers have

been maintained for varioustype of amount recoverablefrom DOT such as GPFadvance.

10.2 Whether proper entries havebeen made in the Register /Sub-ledger at the time of

disbursement of such amount toconcerned staffs, which arerecoverable from DOT.

Yes, proper entries have been

made in the Sub-ledger at thetime of disbursement of such

amount to concerned staffs,which are recoverable fromDOT.

10.3 Whether Register / Sub-ledger ismaintained for amountrecoverable from DOP such asrent of BSNL buildings occupiedby DOP, house keeping chargesof such buildings, servicesprovided by BSNL to DOP etc.

Not applicable.

10.4 Whether claim bills supported by

detailed schedules for each typeof claim have been preferred toDOT & DOP promptly, noted inthe Register, and activepersuasion has been made for recovery of such claimparticularly the old claim bills.

Not applicable.

10.5 Whether payment received fromDOT & DOP has been noted inregister.

Not applicable.

10.6 Whether balances which are

pending to be recovered fromDOT & DOP as reflected in theRegister / Sub-ledger have been

Not applicable.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 37/73

reconciled with the balances asreflected in the General Ledger and difference if any has beensettled.

10.7 Whether details of amount

recoverable from DOT onvarious account have beenuploaded in Web based systemand the same has been talliedwith booked figure reflected inGeneral ledger.

Not applicable.

10.8 Whether claim bills supported bydetailed schedules for recoveryof principal amount of loans andadvances (including payadvance, medical advance, TAadvance) which have been givenby BSNL to unabsorbedemployees who are presentlyworking in DOT, DOP & MTNL,have been preferred to DOT,DOP & MTNL

No such case noticed during

the year.

10.9 Whether claim bill for recovery of interest on loan & advances(wherever applicable) given by

BSNL to unabsorbed employeeswho are presently working inDOT, DOP & MTNL, have beenpreferred to DOT, DOP & MTNL

Not applicable.

10.10 Whether the Unit has activelypursued and taken proper stepsfor recovery of principal amountof such loan and advances andinterest thereon (wherever applicable) from DOT, DOP &MTNL and whether the details of principal and interest amountrecovered from DOT, DOP &

MTNL have been noted in theRegister of loans & advances asmentioned Sl. 6.1 above.

Not applicable.

11 Various deposits taken from the

subscribers / other operators

11.1 Whether there is any bookingunder the accode for ³Beforeconnection deposit´. If so,whether all the details of all suchdeposits are available in³Register of Before connection

deposit´.

Not applicable at the unit.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 38/73

11.2 Whether refund / adjustment of µBefore Connection Deposit¶ hasbeen routed through the sub-ledger / register of Beforeconnection Deposit and suchrefund / adjustment has beencorrectly noted in the Register of Before Connection Deposit.

Not applicable at the unit.

11.3 Whether before connectiondeposit reflected in Register of µBefore Connection Deposit¶ hasbeen reconciled with the waitinglist and the difference if any hasbeen settled.

Not applicable at the unit.

11.4 Whether the total balance of µBefore Connection Deposits¶ asreflected in the Register / Sub-ledger are tallied with thosereflected in General Ledger anddifference if any has beensettled.

Not applicable at the unit.

11.5Whether details of all After connection Deposits have

properly been maintained inµRegister of after connectionDeposit¶.

Not applicable at the unit.

11.6 Whether refund / adjustment of µAfter Connection Deposit¶ hasbeen routed through theRegister of After ConnectionDeposit and such refund andadjustment have been correctlynoted in the Register of After Connection Deposit.

Not applicable at the unit.

11.7W

hether the balance of µAfter Connection Deposit¶ as reflectedin the Register of After Connection Deposit¶ have beenreconciled with the booked figurein General Ledger and differenceif any between two sets of figurehas been fully settled. Whether the details of after connectiondeposits have been reconciledwith the working connection andthere is no difference.

Not applicable at the unit.

11.8 Check whether proper details of

all other deposits (other thanbefore connection and after

Yes, it has been maintained.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 39/73

connection deposit) taken fromsubscribers / other operators /service providers have beenmaintained in the Sub-ledger /Register of other deposits.

11.9W

hether refund / adjustment of other deposits has been routedthrough the Register / Sub-ledger of other deposit and suchrefund and adjustment havebeen correctly noted in theRegister of other Deposit.

Yes.

11.10 Whether the balance of all suchother deposits as reflected inRegister of other deposits arereconciled with those reflected inthe General Ledger anddifference if any has been fullyadjusted.

Yes, it has been reconciled.

11.11 Whether liability for interest onsubscribers deposit wherever applicable, has been createdand accounted.

No interest has been charged

on other deposits.

12 EMD, SD, Bank Guarantee

taken by BSNL from other s

12.1 Whether details of EMD & SDtaken by BSNL Units have beenproperly kept in sub-ledger /Register of EMD / SD.

Yes, it is maintained by the

unit.

12.2 Whether EMD & SD arerefunded promptly on fulfilmentof all the terms and conditionsrelated to it and same is noted inthe EMD/SD Register.

Yes.

12.3W

hether refund / adjustment of EMD & SD has been routedthrough the sub-ledger / register of EMD & SD and such refund /adjustment has been correctlynoted in the Register of EMD &SD.

Yes.

12.4 Whether the total balance of EMD & SD as reflected in theEMD & SD register/sub-ledger have been reconciled with thebooked figure of EMD / SDreflected in the General Ledger and difference if any, has beensettled.

Yes, it has been reconciled.

8/7/2019 CGMT PATNA IA SEPT 2010

http://slidepdf.com/reader/full/cgmt-patna-ia-sept-2010 40/73

12.5 Whether register has beenmaintained for bank guaranteetaken by BSNL Units from others

Yes, It is maintained by Unit.

12.6 Whether details of bankguarantee taken by BSNL units

have been kept in the Register.

Yes, It is maintained by Unit.

12.7 Whether bank guarantee takenby BSNL units has beenreleased promptly on fulfilmentof terms and conditions.

Yes, It is found in order.

12.8 Whether the Units has got thebank guarantee renewedwherever required as per termsand conditions, on expiry of validity period of the bankguarantee in question.

Yes.

12.9 Whether the Unit has encashedthe bank guarantee promptly asper terms and conditions relatedto such bank guarantees.

No such case noticed during

the year.

13 Sundry creditor s & provisions

13.1 Whether Sub-ledger / Register