Embed Size (px)

Citation preview

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 1/13

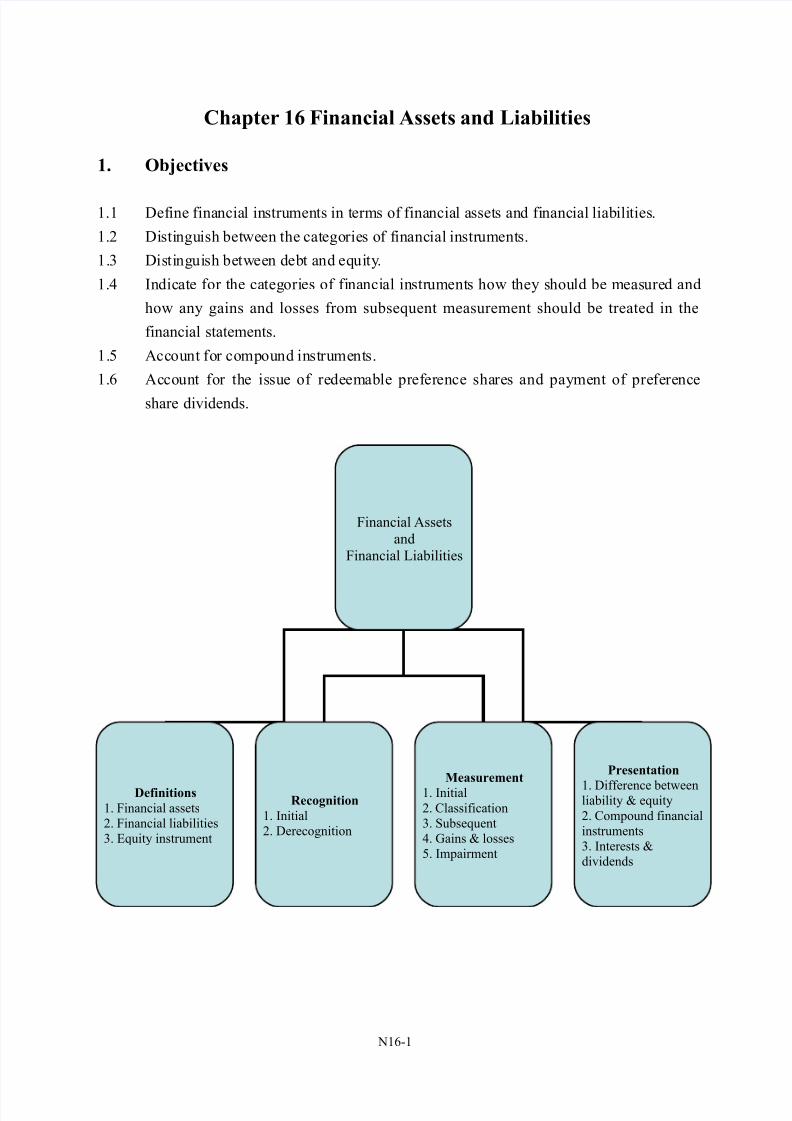

Chapter 16 Financial Assets and Liabilities

1. Objectives

1.1 Define financial instruments in terms of financial assets and financial liabilities.

1.2 Distinguish between the categories of financial instruments.

1.3 Distinguish between debt and equity.

1.4 Indicate for the categories of financial instruments how they should be measured and

how any gains and losses from subsequent measurement should be treated in the

financial statements.

1.5 Account for compound instruments.

1. Account for the issue of redeemable preference shares and payment of preference

share di!idends.

"1#1

$inancial Assetsand

$inancial %iabilities

Definitions

1. $inancial assets2. $inancial liabilities3. &quity instrument

Recognition

1. Initial2. Derecognition

Measureent

1. Initial2. 'lassification3. (ubsequent4. )ains * losses5. Impairment

!resentation

1. Difference betweenliability * equity2. 'ompound financialinstruments3. Interests *di!idends

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 2/13

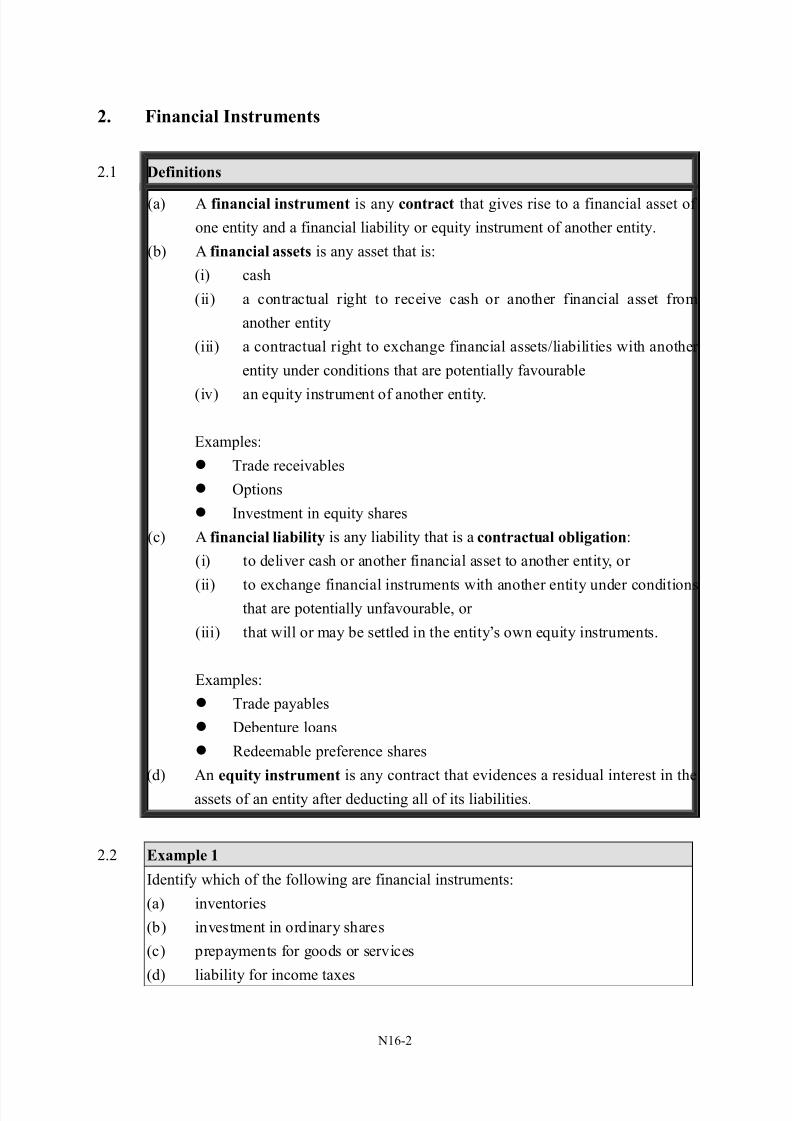

". Financial #nstruents

2.1 Definitions

+a, A financial instruent is any contract that gi!es rise to a financial asset of

one entity and a financial liability or equity instrument of another entity.

+b, A financial assets is any asset that is-

+i, cash

+ii, a contractual right to recei!e cash or another financial asset from

another entity

+iii, a contractual right to echange financial assets/liabilities with another

entity under conditions that are potentially fa!ourable

+i!, an equity instrument of another entity.

&les-

0rade recei!ables

ptions

In!estment in equity shares

+c, A financial liabilit$ is any liability that is a contractual obligation-

+i, to deli!er cash or another financial asset to another entity or

+ii, to echange financial instruments with another entity under conditionsthat are potentially unfa!ourable or

+iii, that will or may be settled in the entitys own equity instruments.

&les-

0rade payables

Debenture loans

edeemable preference shares

+d, An e%uit$ instruent is any contract that e!idences a residual interest in the

assets of an entity after deducting all of its liabilities.

2.2 &'aple 1

Identify which of the following are financial instruments-

+a, in!entories

+b, in!estment in ordinary shares

+c, prepayments for goods or ser!ices

+d, liability for income taes

"1#2

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 3/13

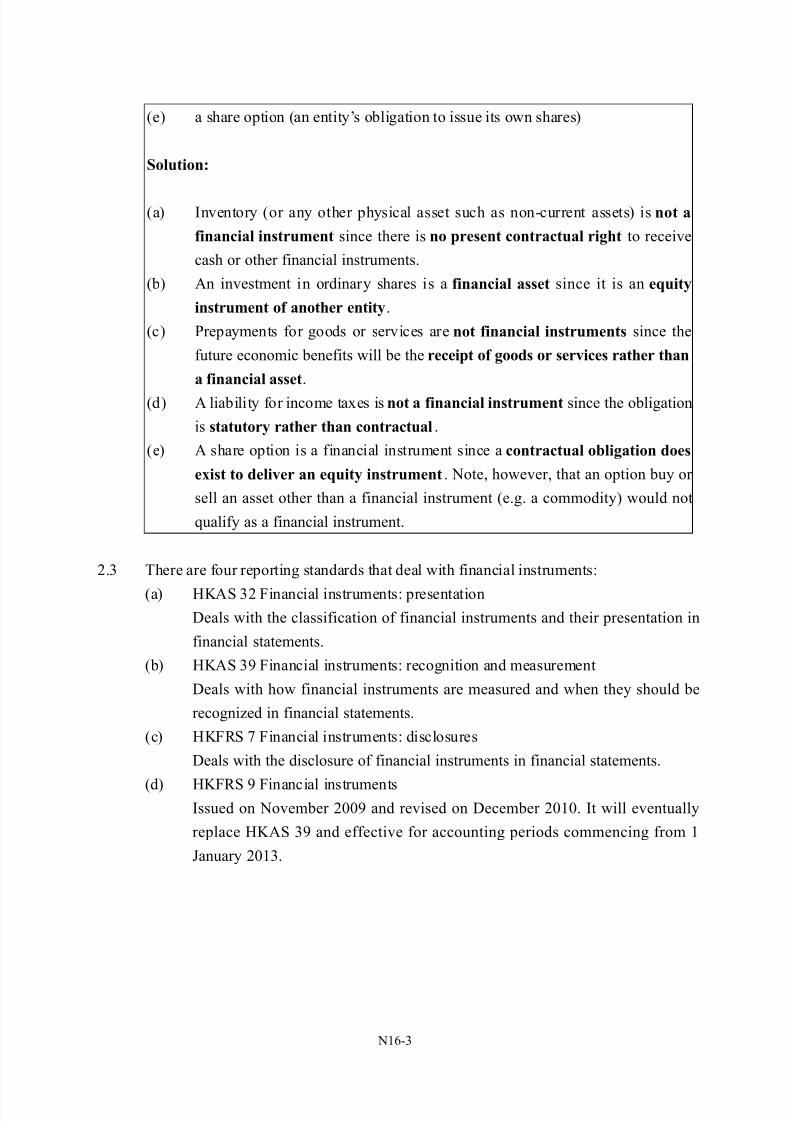

+e, a share option +an entitys obligation to issue its own shares,

(olution)

+a, In!entory +or any other physical asset such as non#current assets, is not a

financial instruent since there is no present contractual right to recei!e

cash or other financial instruments.

+b, An in!estment in ordinary shares is a financial asset since it is an e%uit$

instruent of another entit$.

+c, repayments for goods or ser!ices are not financial instruents since the

future economic benefits will be the receipt of goods or services rather than

a financial asset.

+d, A liability for income taes is not a financial instruent since the obligation

is statutor$ rather than contractual.

+e, A share option is a financial instrument since a contractual obligation does

e'ist to deliver an e%uit$ instruent. "ote howe!er that an option buy or

sell an asset other than a financial instrument +e.g. a commodity, would not

qualify as a financial instrument.

2.3 0here are four reporting standards that deal with financial instruments-

+a, 67A( 32 $inancial instruments- presentation

Deals with the classification of financial instruments and their presentation in

financial statements.

+b, 67A( 38 $inancial instruments- recognition and measurement

Deals with how financial instruments are measured and when they should be

recogni9ed in financial statements.

+c, 67$( : $inancial instruments- disclosures

Deals with the disclosure of financial instruments in financial statements.

+d, 67$( 8 $inancial instrumentsIssued on "o!ember 2;;8 and re!ised on December 2;1;. It will e!entually

replace 67A( 38 and effecti!e for accounting periods commencing from 1

<anuary 2;13.

"1#3

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 4/13

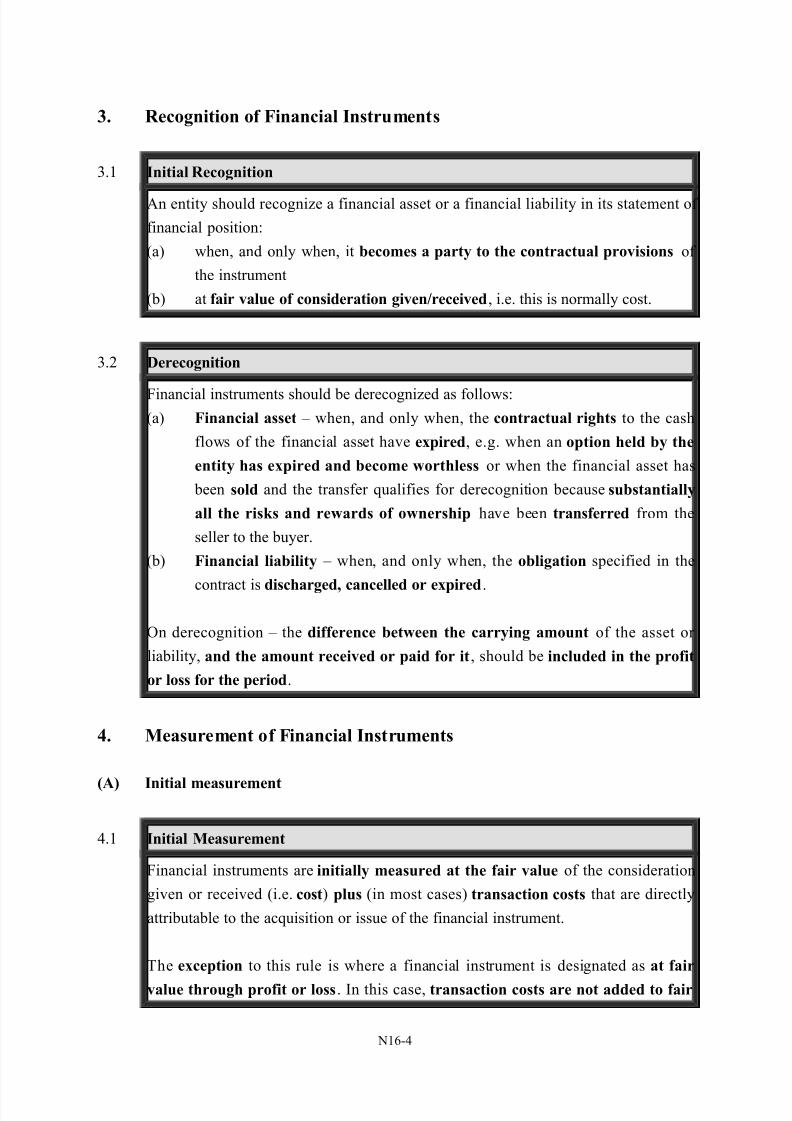

*. Recognition of Financial #nstruents

3.1 #nitial Recognition

An entity should recogni9e a financial asset or a financial liability in its statement of

financial position-

+a, when and only when it becoes a part$ to the contractual provisions of

the instrument

+b, at fair value of consideration given+received i.e. this is normally cost.

3.2 Derecognition

$inancial instruments should be derecogni9ed as follows-

+a, Financial asset = when and only when the contractual rights to the cash

flows of the financial asset ha!e e'pired e.g. when an option held b$ the

entit$ has e'pired and becoe ,orthless or when the financial asset has

been sold and the transfer qualifies for derecognition because substantiall$

all the ris-s and re,ards of o,nership ha!e been transferred from the

seller to the buyer.

+b, Financial liabilit$ = when and only when the obligation specified in the

contract is discharged cancelled or e'pired.

n derecognition = the difference bet,een the carr$ing aount of the asset or

liability and the aount received or paid for it should be included in the profit

or loss for the period.

/. Measureent of Financial #nstruents

0A #nitial easureent

4.1 #nitial Measureent

$inancial instruments are initiall$ easured at the fair value of the consideration

gi!en or recei!ed +i.e. cost, plus +in most cases, transaction costs that are directly

attributable to the acquisition or issue of the financial instrument.

0he e'ception to this rule is where a financial instrument is designated as at fair

value through profit or loss. In this case transaction costs are not added to fair

"1#4

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 5/13

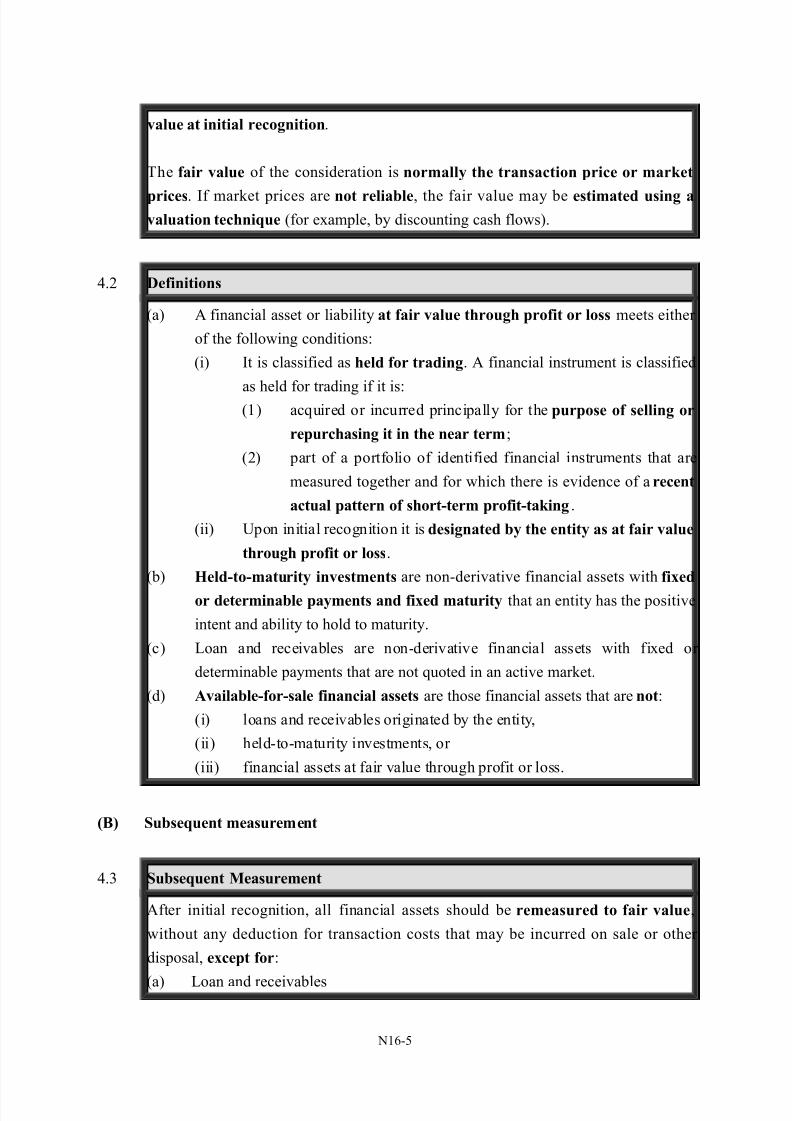

value at initial recognition.

0he fair value of the consideration is norall$ the transaction price or ar-et

prices. If mar>et prices are not reliable the fair !alue may be estiated using avaluation techni%ue +for eample by discounting cash flows,.

4.2 Definitions

+a, A financial asset or liability at fair value through profit or loss meets either

of the following conditions-

+i, It is classified as held for trading. A financial instrument is classified

as held for trading if it is-+1, acquired or incurred principally for the purpose of selling or

repurchasing it in the near ter?

+2, part of a portfolio of identified financial instruments that are

measured together and for which there is e!idence of a recent

actual pattern of short2ter profit2ta-ing.

+ii, @pon initial recognition it is designated b$ the entit$ as at fair value

through profit or loss.

+b, 3eld2to2aturit$ investents are non#deri!ati!e financial assets with fi'ed

or deterinable pa$ents and fi'ed aturit$ that an entity has the positi!e

intent and ability to hold to maturity.

+c, %oan and recei!ables are non#deri!ati!e financial assets with fied or

determinable payments that are not quoted in an acti!e mar>et.

+d, Available2for2sale financial assets are those financial assets that are not-

+i, loans and recei!ables originated by the entity

+ii, held#to#maturity in!estments or

+iii, financial assets at fair !alue through profit or loss.

04 (ubse%uent easureent

4.3 (ubse%uent Measureent

After initial recognition all financial assets should be reeasured to fair value

without any deduction for transaction costs that may be incurred on sale or other

disposal e'cept for-

+a, %oan and recei!ables

"1#5

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 6/13

+b, 6eld to maturity in!estments

+c, In!estments in equity instruments that do not ha!e a quoted mar>et price in an

acti!e mar>et and whose fair !alue cannot be reliably measured.

Loans and receivables and held to aturit$ investents should be easured at

aortised cost using the effective interest ethod.

4.4 &'aple " 5 Aortised cost

n 1 <anuary 2;11 A' 'o purchases a debt instrument for its fair !alue of B1;;;.

0he debt instrument is due to mature on 31 December 2;15. 0he instrument has a

principal amount of B125; and the instrument carries fied interest at 4.:2C that is

paid annually. 0he effecti!e rate of interest is 1;C.

6ow should A' 'o account for the debt instrument o!er its fi!e year term

(olution)

A' 'o will recei!e interest of B58 +125; E 4.:2C, each year and B125; when the

instrument matures.

A' 'o must allocate the discount of B25; and the interest recei!able o!er the fi!e

year term at a constant rate on the carrying amount of the debt. 0o do this it must

apply the effecti!e interest rate of 1;C. 0he following table shows the allocation

o!er the years-

Fear Amortised

cost at

beginning of

year

Income

statement-

interest income

for year +G1;C,

Interest recei!ed

during year

+cash inflow,

Amortised

cost at end of

year

B B B B

2;11 1;;; 1;; +58, 1;41

2;12 1;41 1;4 +58, 1;H

2;13 1;H 1;8 +58, 113

2;14 113 113 +58, 118;

2;15 118; 118 +125; 58, #

&ach year the carrying amount of the financial asset is increased by the interest

"1#

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 7/13

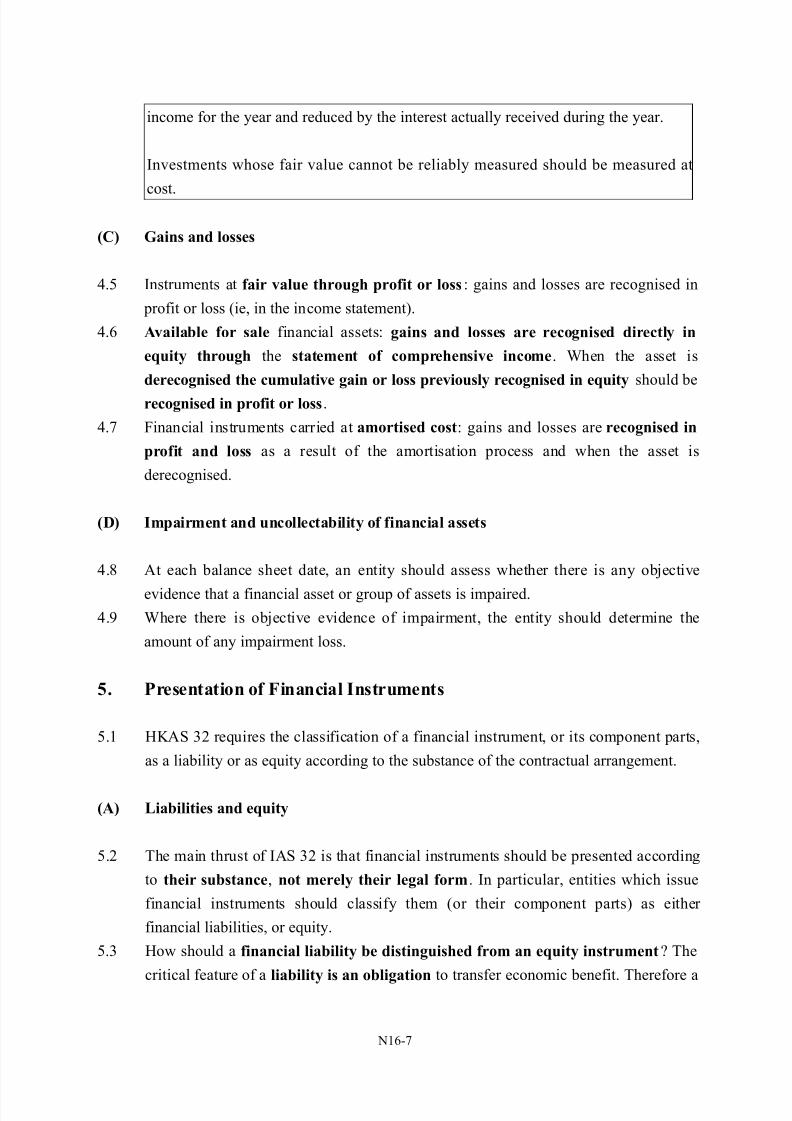

income for the year and reduced by the interest actually recei!ed during the year.

In!estments whose fair !alue cannot be reliably measured should be measured at

cost.

0C ains and losses

4.5 Instruments at fair value through profit or loss- gains and losses are recognised in

profit or loss +ie in the income statement,.

4. Available for sale financial assets- gains and losses are recognised directl$ in

e%uit$ through the stateent of coprehensive incoe. Jhen the asset is

derecognised the cuulative gain or loss previousl$ recognised in e%uit$ should be

recognised in profit or loss.

4.: $inancial instruments carried at aortised cost- gains and losses are recognised in

profit and loss as a result of the amortisation process and when the asset is

derecognised.

0D #pairent and uncollectabilit$ of financial assets

4.H At each balance sheet date an entity should assess whether there is any obKecti!e

e!idence that a financial asset or group of assets is impaired.

4.8 Jhere there is obKecti!e e!idence of impairment the entity should determine the

amount of any impairment loss.

7. !resentation of Financial #nstruents

5.1 67A( 32 requires the classification of a financial instrument or its component parts

as a liability or as equity according to the substance of the contractual arrangement.

0A Liabilities and e%uit$

5.2 0he main thrust of IA( 32 is that financial instruments should be presented according

to their substance not erel$ their legal for. In particular entities which issue

financial instruments should classify them +or their component parts, as either

financial liabilities or equity.

5.3 6ow should a financial liabilit$ be distinguished fro an e%uit$ instruent 0he

critical feature of a liabilit$ is an obligation to transfer economic benefit. 0herefore a

"1#:

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 8/13

financial instrument is a financial liability if there is a contractual obligation on the

issuer either to deli!er cash or another financial asset to the holder or to echange

another financial instrument with the holder under potentially unfa!ourable conditions

to the issuer.

5.4 Jhere the abo!e critical feature is not met then the financial instrument is an e%uit$

instruent. 67A( 32 eplains that although the holder of an equity instrument may

be entitled to a pro rata share of any distributions out of equity the issuer does not

have a contractual obligation to a-e such a distribution.

5.5 Lany entities issue preference shares which must be redeeed b$ the issuer for a

fi'ed 0or deterinable aount at a fi'ed 0or deterinable future date.

Alternati!ely the holder may ha!e the right to require the issuer to redeem the shares

at or after a certain date for a fied amount. In such cases the issuer has an obligation.

0herefore the instrument is a financial liabilit$ and should be classified as such.

5. 0he distinction between redeeable and non2redeeable preference shares is

important. Lost preference shares are redeeable and are therefore classified as a

financial liabilit$.

04 Copound financial instruents

5.: (ome financial instruments contain both a liabilit$ and an e%uit$ eleent. In such

cases 67A( 32 requires the component parts of the instrument to be classified

separatel$ according to the substance of the contractual arrangement and the

definitions of a financial liability and an equity instrument.

5.H ne of the most common types of compound instrument is convertible debt. 0his

creates a primary financial liability of the issuer and grants an option to the holder of

the instrument to con!ert it into an equity instrument +usually ordinary shares, of the

issuer. 0his is the economic equi!alent of the issue of con!entional debt plus a warrant

to acquire shares in the future.

5.8 0he two elements must be separately recogni9ed in the statement of financial position-+a, the liability element

+b, the equity element.

5.1; 0o account for a con!ertible debt +loan,-

+a, Calculate fair value of liabilit$ component first

+i, based on present value of future cash flo,s assuming non#

con!ersion

+ii, appl$ discount rate e%uivalent to interest on siilar non2

convertible debt instruent.

+b, &%uit$ 8 reainder

"1#H

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 9/13

5.11 &'aple * 5 Copound instruentsA' 'o issues a con!ertible loan that attracts interest of 2C. 0he mar>et rate is HC

being the interest rate for an equi!alent debt without the con!ersion option. 0he loan

of B5 million is repayable in full after three years or con!ertible to equity. Discount

factors are as follows-

Fear Discount factor at HC

1 ;.82

2 ;.H5:

3 ;.:84

Re%uired)

(plit the loan between debt and equity at inception and calculate the finance charge

for each year until con!ersion/redemption.

(olution)

At inception-

Fear 'ash flow +B;;;, D$ G HC M +B;;;,

1 1;; ;.823 82

2 1;; ;.H5: H

3 51;; ;.:84 4;48

Debt 422:

&quity +bal., ::3

'ash inflow 5;;;

9ear Opening Finance 0:; !aid Closing

B;;; B;;; B;;; B;;;

1 422: 33H +1;;, 445

2 445 35: +1;;, 4:22

3 4:22 3:H +1;;, 5;;;

"1#8

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 10/13

0C #nterest and dividends

5.12 As well as loo>ing at presentation in the statement of financial position 67A( 32

considers how financial instruments affect the income statement or statement of

comprehensi!e income +and mo!ements in equity,. 0he treatment !aries according to

whether interest di!idends losses or gains relate to a financial liability or an equity

instrument.

+a, &%uit$ dividends declared are reported directly in e%uit$.

+b, Dividends on redeeable preference shares classified as a liabilit$ are an

e'pense in the income statement.

5.13 &'aple / 5 Redeeable preference shares

n 1 April 2;1; a company issued 4;;;; B1 redeemable preference shares with a

coupon rate of HC at par. 0hey are redeemable at a large premium which gi!es them

an effecti!e finance cost of 12C per annum.

6ow would these redeemable preference shares appear in the financial statements for

the years ending 31 Larch 2;11 and 2;12

(olution)

Annual payment N B4;;;; HC N B32;;

9ear Opening Finance 01"; !aid < :; Closing

B B B B

2;11 4;;;; 4H;; +32;;, 41;;

2;12 41;; 4882 +32;;, 43382

9ear ended *1 March "=11#ncoe stateent 0e'tract

= $inance cost B4H;;

(tateent of financial position 0e'tract

"on#current liabilities

= edeemable preference shares B41;;

9ear ended *1 March "=1"

"1#1;

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 11/13

#ncoe stateent 0e'tract

= $inance cost B4882

(tateent of financial position 0e'tract "on#current liabilities

= edeemable preference shares B43382

&'aination (t$le >uestions

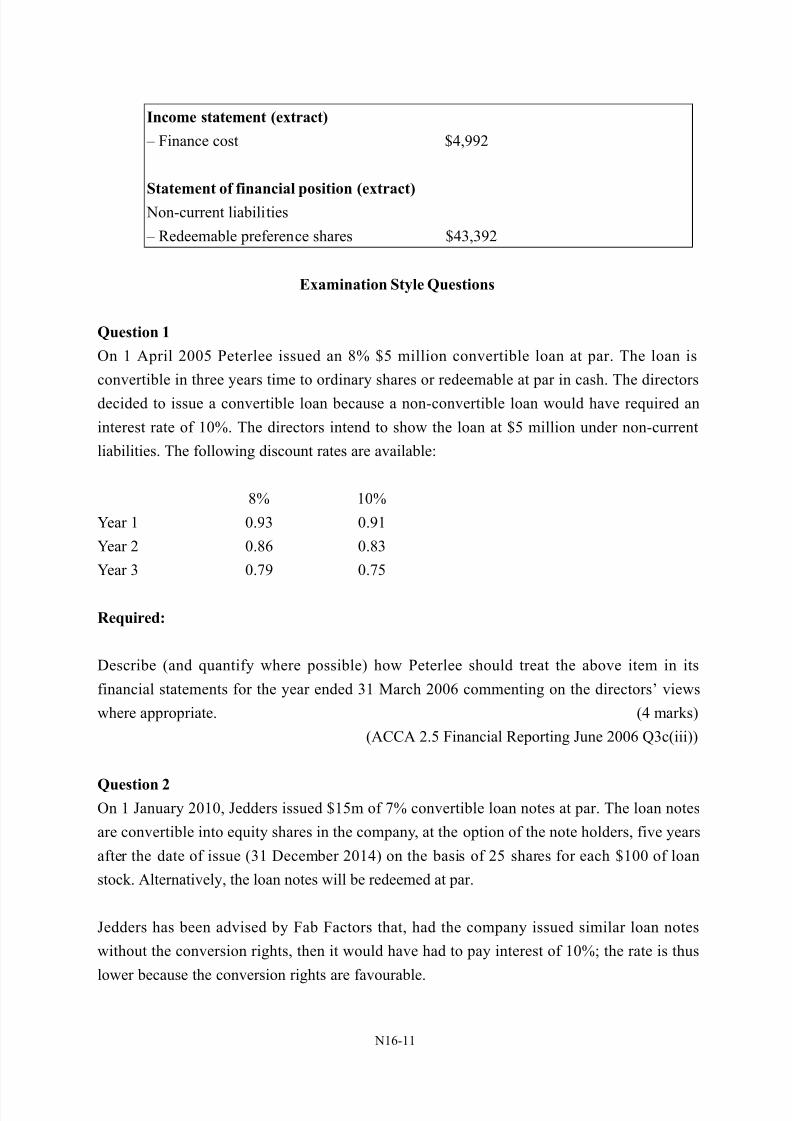

>uestion 1

n 1 April 2;;5 eterlee issued an HC B5 million con!ertible loan at par. 0he loan is

con!ertible in three years time to ordinary shares or redeemable at par in cash. 0he directors

decided to issue a con!ertible loan because a non#con!ertible loan would ha!e required an

interest rate of 1;C. 0he directors intend to show the loan at B5 million under non#current

liabilities. 0he following discount rates are a!ailable-

HC 1;C

Fear 1 ;.83 ;.81

Fear 2 ;.H ;.H3

Fear 3 ;.:8 ;.:5

Re%uired)

Describe +and quantify where possible, how eterlee should treat the abo!e item in its

financial statements for the year ended 31 Larch 2;; commenting on the directors !iews

where appropriate. +4 mar>s,

+A''A 2.5 $inancial eporting <une 2;; O3c+iii,,

>uestion "n 1 <anuary 2;1; <edders issued B15m of :C con!ertible loan notes at par. 0he loan notes

are con!ertible into equity shares in the company at the option of the note holders fi!e years

after the date of issue +31 December 2;14, on the basis of 25 shares for each B1;; of loan

stoc>. Alternati!ely the loan notes will be redeemed at par.

<edders has been ad!ised by $ab $actors that had the company issued similar loan notes

without the con!ersion rights then it would ha!e had to pay interest of 1;C? the rate is thus

lower because the con!ersion rights are fa!ourable.

"1#11

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 12/13

$ab $actors also suggest that as some of the loan note holders will choose to con!ert the loan

notes are in substance equity and should be treated as such on <eddersP statement of financial

position. 0hus as well as a reduced finance cost being achie!ed to boost profitability <eddersP

gearing has been impro!ed compared to a straight issue of debt.

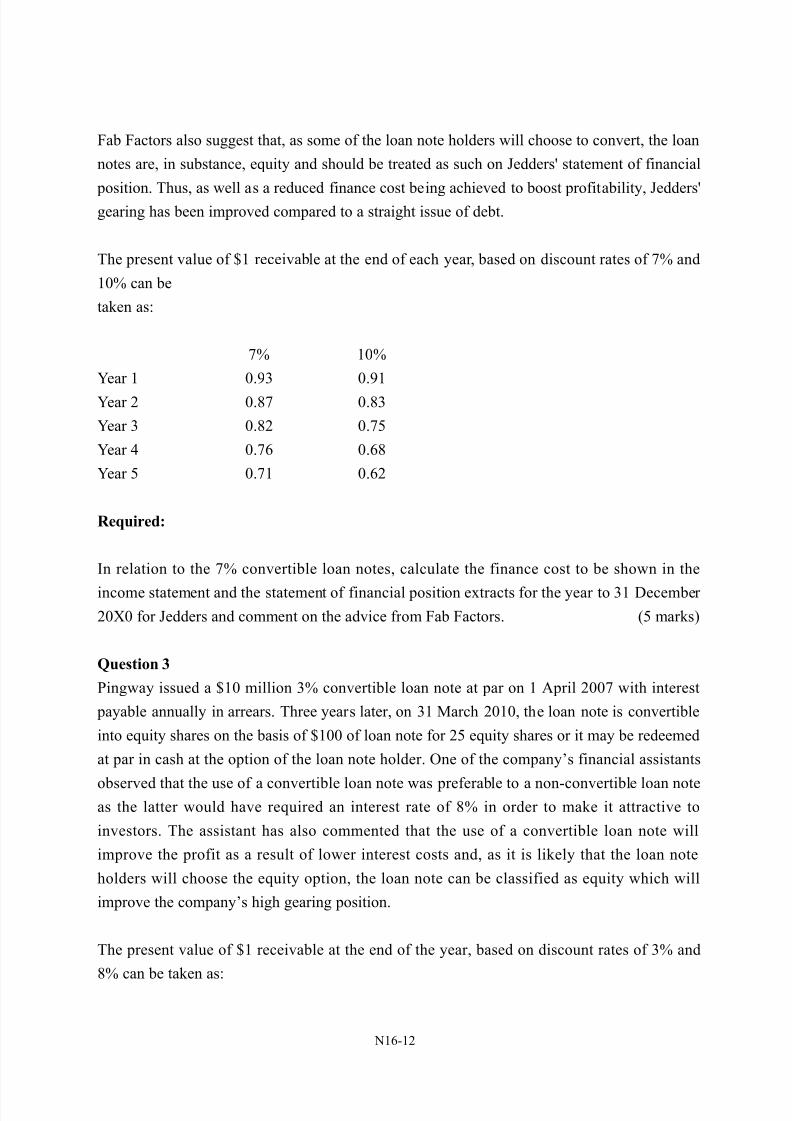

0he present !alue of B1 recei!able at the end of each year based on discount rates of :C and

1;C can be

ta>en as-

:C 1;C

Fear 1 ;.83 ;.81

Fear 2 ;.H: ;.H3

Fear 3 ;.H2 ;.:5

Fear 4 ;.: ;.H

Fear 5 ;.:1 ;.2

Re%uired)

In relation to the :C con!ertible loan notes calculate the finance cost to be shown in the

income statement and the statement of financial position etracts for the year to 31 December

2;Q; for <edders and comment on the ad!ice from $ab $actors. +5 mar>s,

>uestion *

ingway issued a B1; million 3C con!ertible loan note at par on 1 April 2;;: with interest

payable annually in arrears. 0hree years later on 31 Larch 2;1; the loan note is con!ertible

into equity shares on the basis of B1;; of loan note for 25 equity shares or it may be redeemed

at par in cash at the option of the loan note holder. ne of the companys financial assistants

obser!ed that the use of a con!ertible loan note was preferable to a non#con!ertible loan noteas the latter would ha!e required an interest rate of HC in order to ma>e it attracti!e to

in!estors. 0he assistant has also commented that the use of a con!ertible loan note will

impro!e the profit as a result of lower interest costs and as it is li>ely that the loan note

holders will choose the equity option the loan note can be classified as equity which will

impro!e the companys high gearing position.

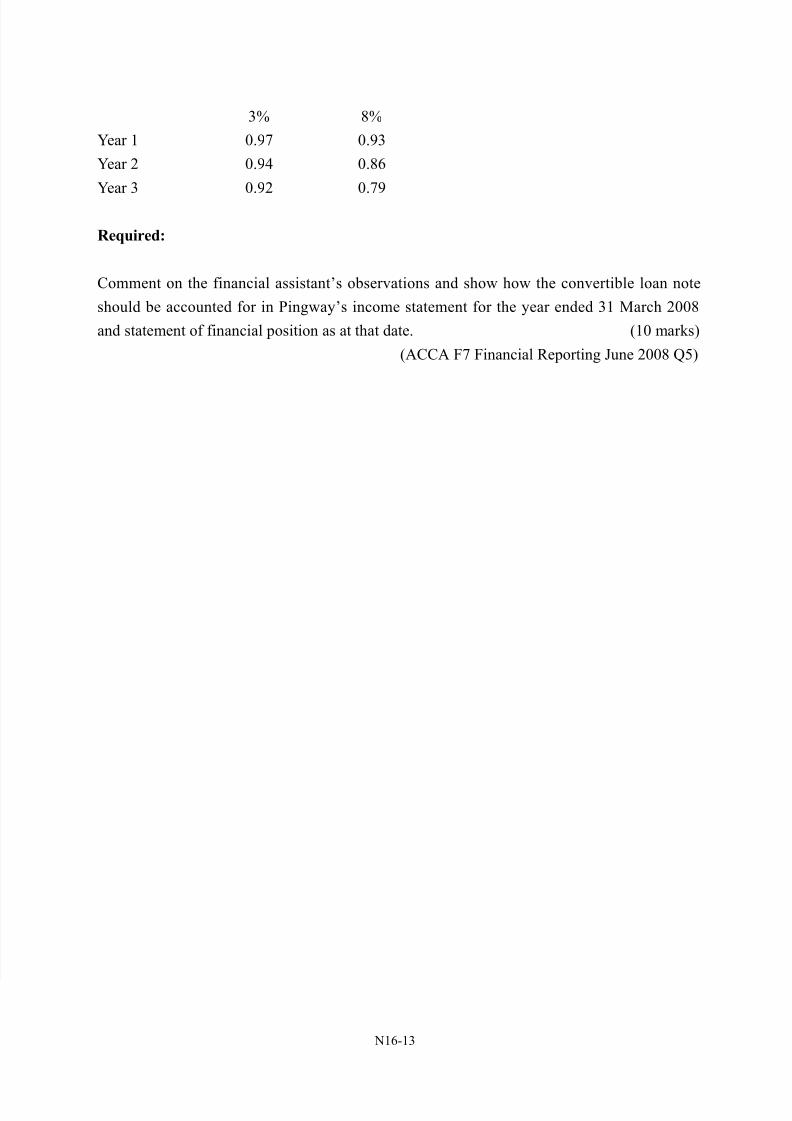

0he present !alue of B1 recei!able at the end of the year based on discount rates of 3C and

HC can be ta>en as-

"1#12

8/13/2019 Ch16-FinAssetLiab

http://slidepdf.com/reader/full/ch16-finassetliab 13/13

3C HC

Fear 1 ;.8: ;.83

Fear 2 ;.84 ;.H

Fear 3 ;.82 ;.:8

Re%uired)

'omment on the financial assistants obser!ations and show how the con!ertible loan note

should be accounted for in ingways income statement for the year ended 31 Larch 2;;H

and statement of financial position as at that date. +1; mar>s,

+A''A $: $inancial eporting <une 2;;H O5,

"1#13