Embed Size (px)

Citation preview

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 1/117

Salaar - Finance

Investment Analysis & Portfolio Theory

MBA-IISpring Semester 2011

Lahore School of Economics

Salaar Farooq ² Assistant Professor

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 2/117

Salaar - Finance

Chapter 17

Fixed Income Securities:

Bonds

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 3/117

Salaar - Finance

Chapter 17

Bond Yields & Prices

Objectives

Bonds & Valuation

Interest rates

Bond Yields

Bond Prices

Bond Price Changes Duration, Modified Duration & Convexity

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 4/117

Salaar - Finance

Bonds

What is a Bond?

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 5/117

Salaar - Finance

BondsWhat is a Bond

Debt instrument to raise money (Loan)

Issued by Corporations & Govts

Interest Only LoanHas a standard Face Value of $1000 (Corp)

Coupons are paid semi-annually

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 6/117

Salaar - Finance

Fixed-Income Securities

BONDS

Capital Markets:

Where debt & equity capital is raised. Market f or long-term securities (stocks &bonds)

Fixed-Income Securities:Securities with specified payment dates and amounts, primarily Bonds

Bonds:

Future stream of cash flows are known at issue.

Principal is paid at maturity.IF, bond is sold bef ore maturity, price will reflectcurrent interest rates.

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 7/117

Salaar - Finance

Fixed-Income Securities

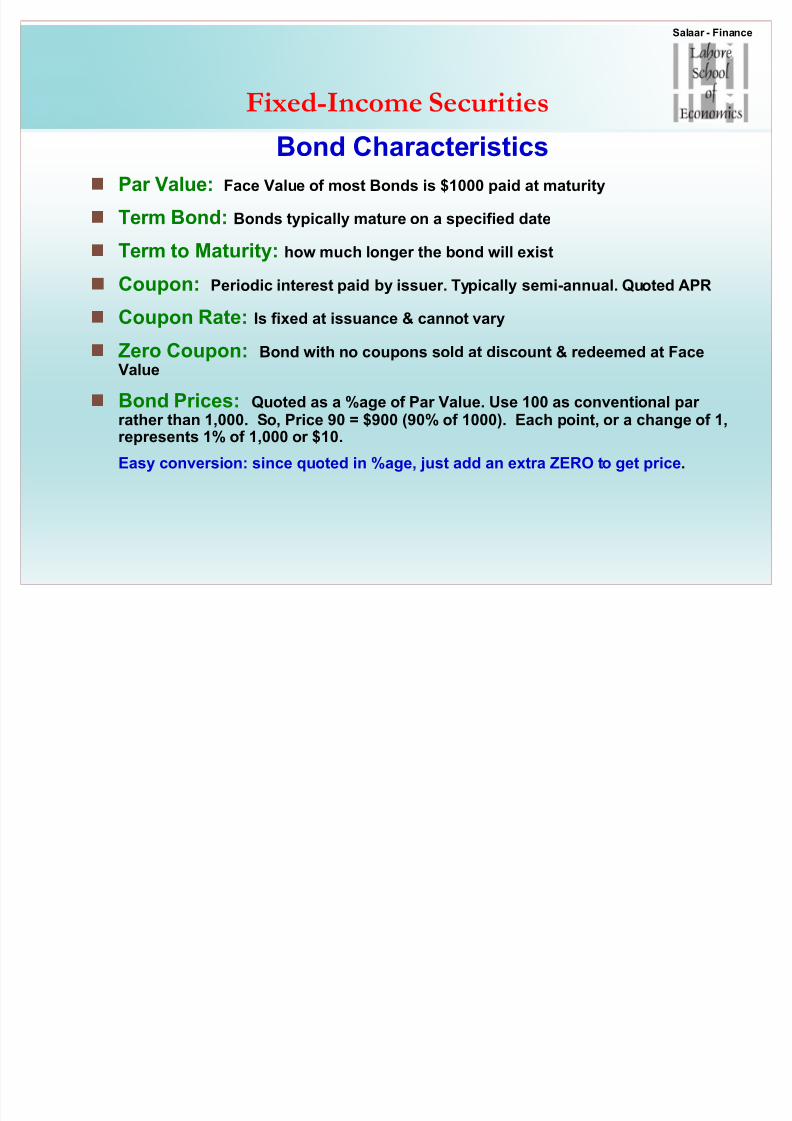

Bond Characteristics

Par Value:

Term Bond:

Term to Maturity:

Coupon:

Coupon Rate:

Zer o Coupon:

Bond Prices: add zer o

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 8/117

Salaar - Finance

Fixed-Income Securities

Bond Characteristics Par Value: Face Value of most Bonds is $1000 paid at maturity

Term Bond: Bonds typically mature on a specified date

Term to Maturity: how much longer the bond will exist

Coupon: Periodic interest paid by issuer. Typically semi-annual. Quoted APR

Coupon Rate: Is fixed at issuance & cannot vary

Zer o Coupon: Bond with no coupons sold at discount & redeemed at FaceValue

Bond Prices: Quoted as a %age of Par Value. Use 100 as conventional par

rather than 1,000. So, Price 90 = $900 (90% of 1000). Each point, or a change of 1,represents 1% of 1,000 or $10.

Easy conversion: since quoted in %age, just add an extra ZERO to get price.

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 9/117

Salaar - Finance

Fixed-Income Securities

More «Bond Characteristics

Indenture:

Registered Form:

Bearer Form:

Security:

Debenture:

Sinking Fund:

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 10/117

Salaar - Finance

Fixed-Income Securities

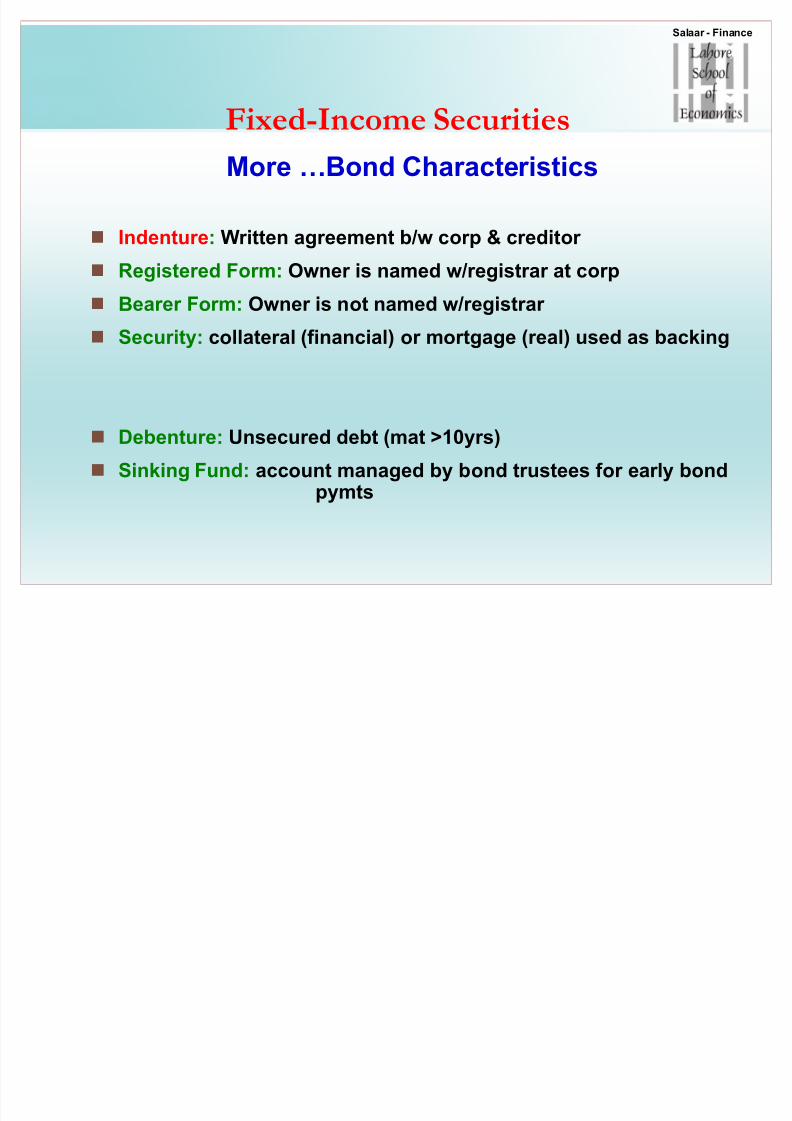

More «Bond Characteristics

Indenture:Written agreement b/w corp & creditor

Registered Form: Owner is named w/registrar at corp

Bearer Form: Owner is not named w/registrar

Security: collateral (financial) or mortgage (real) used as backing

Debenture: Unsecured debt (mat >10yrs)

Sinking Fund: account managed by bond trustees f or early bondpymts

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 11/117

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 12/117

Salaar - Finance

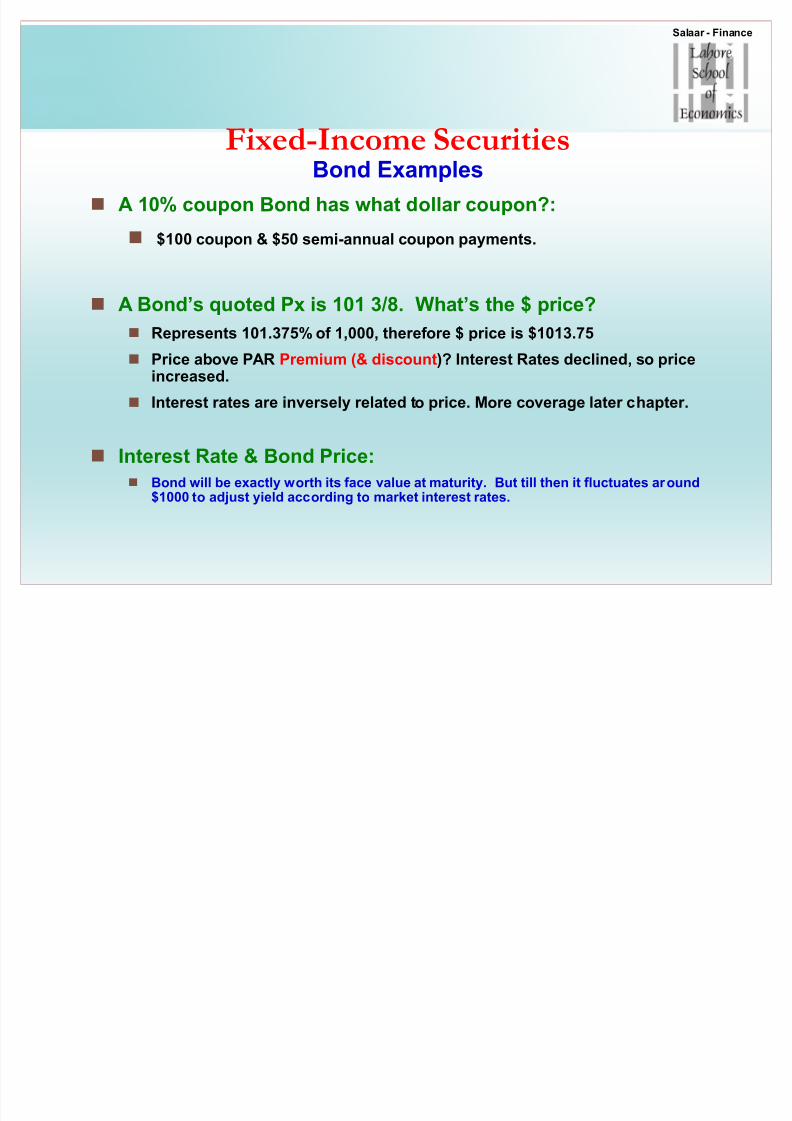

Fixed-Income SecuritiesBond Examples

A 10% coupon Bond has what dollar coupon?:

$100 coupon & $50 semi-annual coupon payments.

A Bond¶s quoted Px is 101 3/8. What¶s the $ price?

Represents 101.375% of 1,000, theref ore $ price is $1013.75

Price above PAR Premium (& discount)? Interest Rates declined, so priceincreased.

Interest rates are inversely related to price. More coverage later chapter.

Interest Rate & Bond Price:

Bond will be exactly worth its face value at maturity. But till then it fluctuates ar ound$1000 to adjust yield according to market interest rates.

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 13/117

Salaar - Finance

Fixed-Income Securities

Bond Characteristics

Call Pr ovision:

When is it attractive to the issuer?

Call Premium

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 14/117

Salaar - Finance

Fixed-Income Securities

Bond Characteristics

Call Pr ovision:

Gives the issuer the right to call in a security & retire it by paying off theobligation.

When is it attractive to the issuer? When interest rates dr op in the markets enough to save the issuer money.

additional cost f or the issuer called CALL PREMIUM

Issuer will CALL & then issue new ones at lower cost.

Most Corp Bonds are callable

Call Premium

Often equals one years interest (if called within a year), then decreases

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 15/117

Salaar - Finance

Fixed-Income Securities

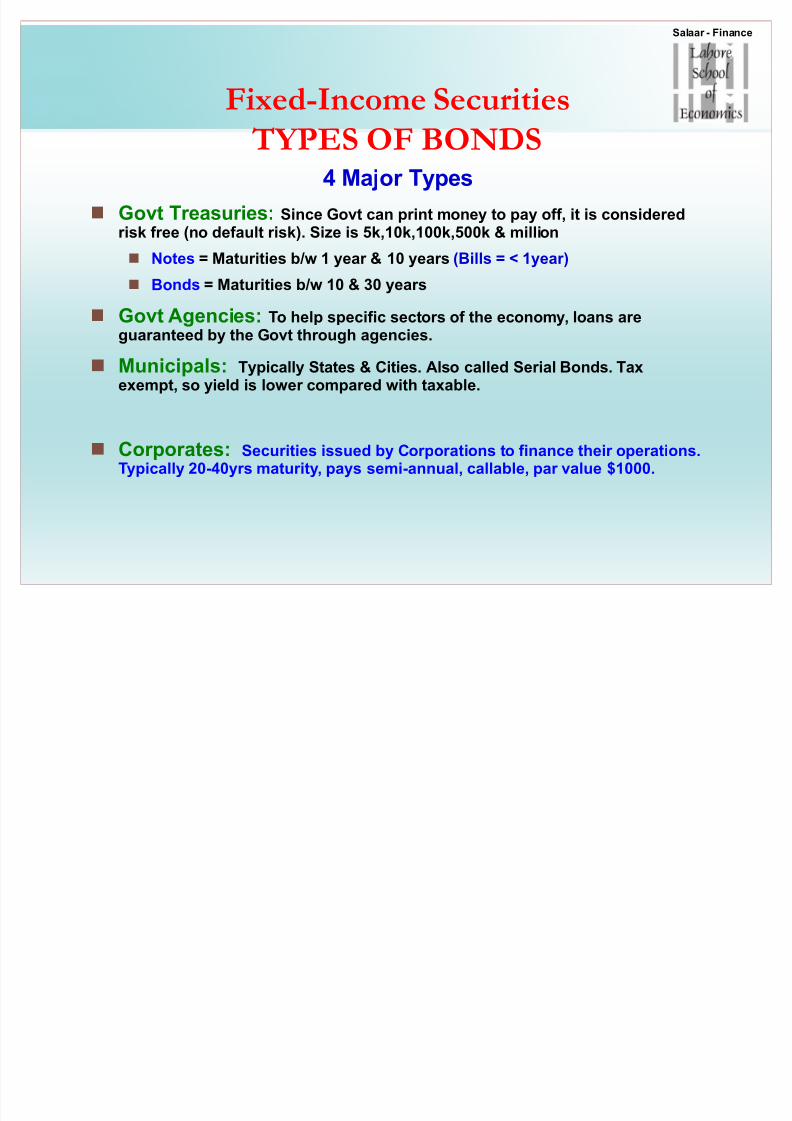

TYPES OF BONDS4 Major Types

Govt Treasuries: Since Govt can print money to pay off, it is consideredrisk free (no default risk). Size is 5k,10k,100k,500k & million

Notes = Maturities b/w 1 year & 10 years (Bills = < 1year)

Bonds = Maturities b/w 10 & 30 years

Govt Agencies: To help specific sectors of the economy, loans areguaranteed by the Govt thr ough agencies.

Municipals: Typically States & Cities. Also called Serial Bonds. Taxexempt, so yield is lower compared with taxable.

Corporates: Securities issued by Corporations to finance their operations.Typically 20-40yrs maturity, pays semi-annual, callable, par value $1000.

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 16/117

Salaar - Finance

Fixed-Income Securities

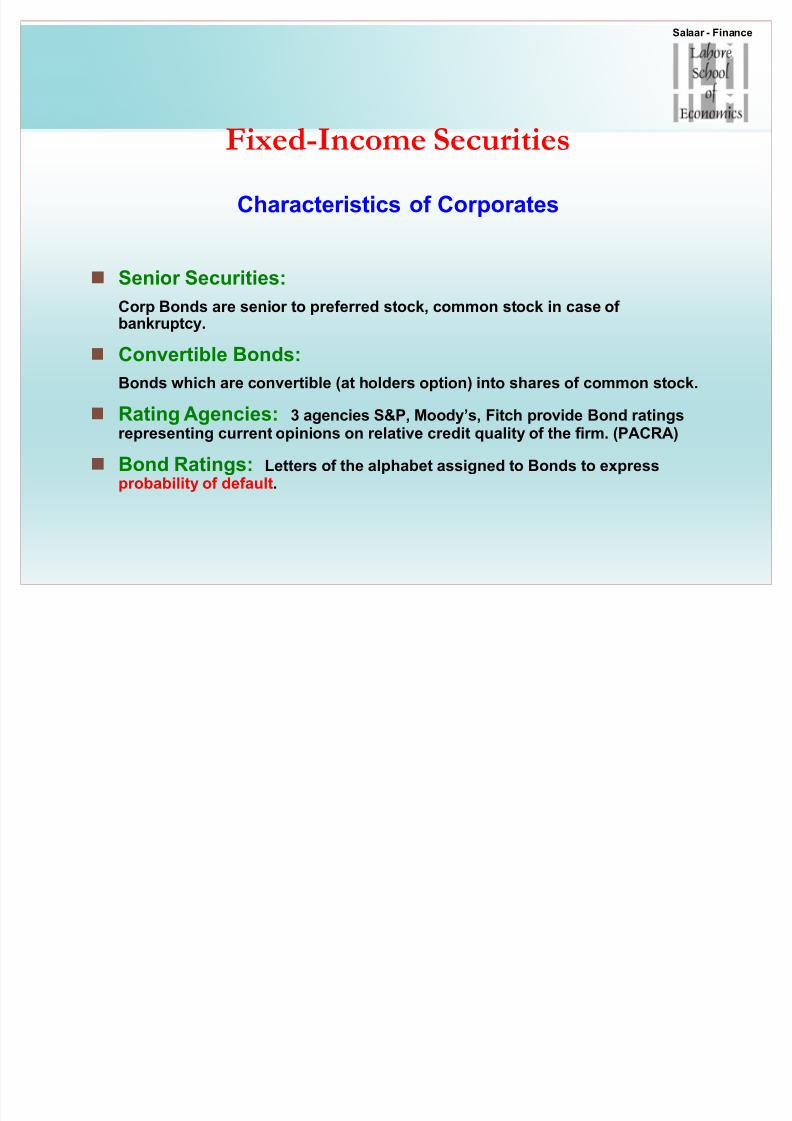

Characteristics of Corporates

Senior Securities:

Convertible Bonds:

Rating Agencies:

Bond Ratings:

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 17/117

Salaar - Finance

Fixed-Income Securities

Characteristics of Corporates

Senior Securities:Corp Bonds are senior to preferred stock, common stock in case of bankruptcy.

Convertible Bonds:

Bonds which are convertible (at holders option) into shares of common stock.

Rating Agencies: 3 agencies S&P, Moody¶s, Fitch pr ovide Bond ratingsrepresenting current opinions on relative credit quality of the firm. (PACRA)

Bond Ratings: Letters of the alphabet assigned to Bonds to expresspr obability of default.

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 18/117

Salaar - Finance

Fixed-Income Securities

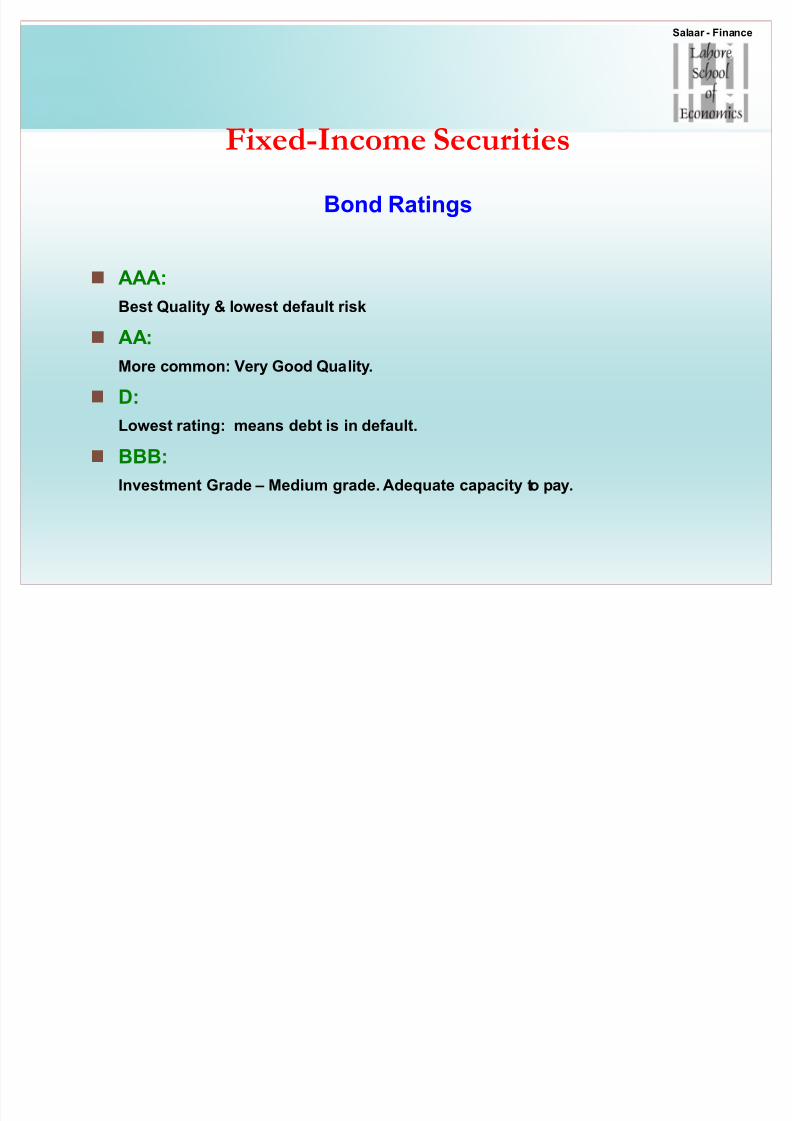

Bond Ratings

AAA:Best Quality & lowest default risk

AA:

More common: Very Good Quality.

D:

Lowest rating: means debt is in default.

BBB:

Investment Grade ± Medium grade. Adequate capacity to pay.

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 19/117

Salaar - Finance

Bond Prices

Valuation Principle

Bond Valuation

R1

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 20/117

Salaar - Finance

Bond Prices

Valuation Principle

Price of a security is based on estimated values based on

expectations. This is also called the Intrinsic Value.

It is the PV of all EXPECTED Cash Flows fr om thatasset

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 21/117

Salaar - Finance

Bond Prices

Cash Flows fr om a security can be in any f orm:

Example??

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 22/117

Salaar - Finance

Bond Prices

Cash Flows fr om a security can be in any f orm:

Dividends

Interest Payments

Coupons

Redemption value

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 23/117

Salaar - Finance

Bond Prices

Since C/F¶s are in future, they must be

Discounted

And converted to PV.

Sum of all the PV¶s of C/f¶s = Estimated Intrinsic Value

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 24/117

Salaar - Finance

Bond Prices

Formula f or any asset:

Value = E ??

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 25/117

Salaar - Finance

Bond Prices

Formula f or any asset:

Value = E C/F¶s / (1+i)^n

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 26/117

Salaar - Finance

Bond Valuation

Bond has TWO types of Cash Flows:?

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 27/117

Salaar - Finance

Bond Valuation

Bond has TWO types of Cash Flows:

1. Coupons

2. Face Value

Both of these are known in advance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 28/117

Salaar - Finance

Bond Prices

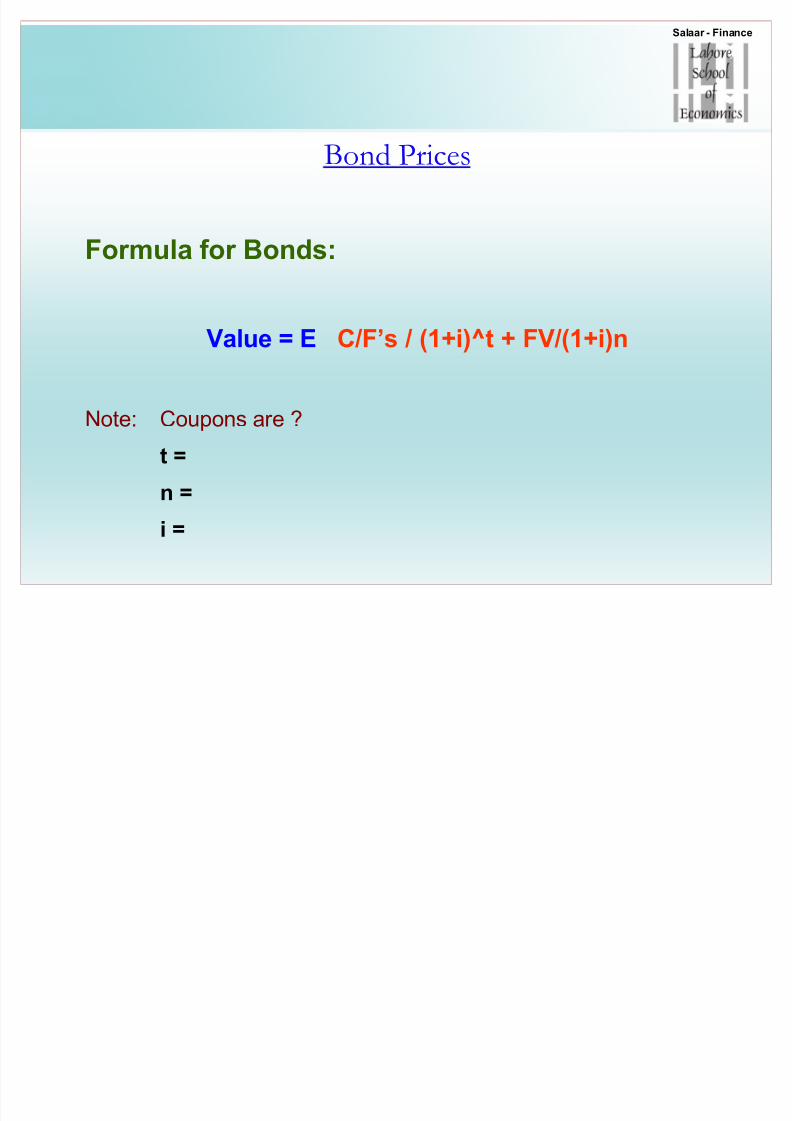

Formula f or Bonds:

Value = E C/F¶s / (1+i)^t + FV/(1+i)n

Note: Coupons are ?

t =

n =

i =

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 29/117

Salaar - Finance

Bond Prices

Formula f or Bonds:

Value = E C/F¶s / (1+i)^t + FV/(1+i)n

Note: Coupons are semi-annual

t = period on semi-annual basis

n = periods also semi-annual

i = semi-annual rate

John Burr Williams published this eq. in 1938

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 30/117

Salaar - Finance

Bond Prices

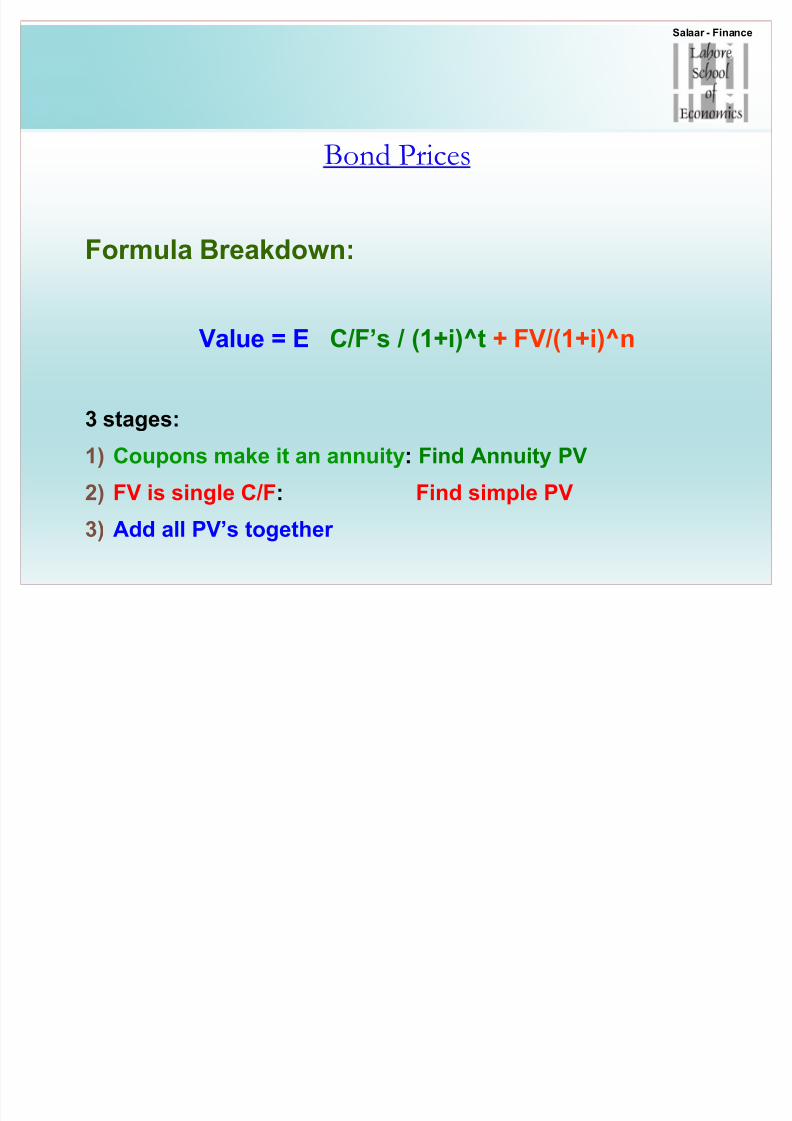

Formula Breakdown:

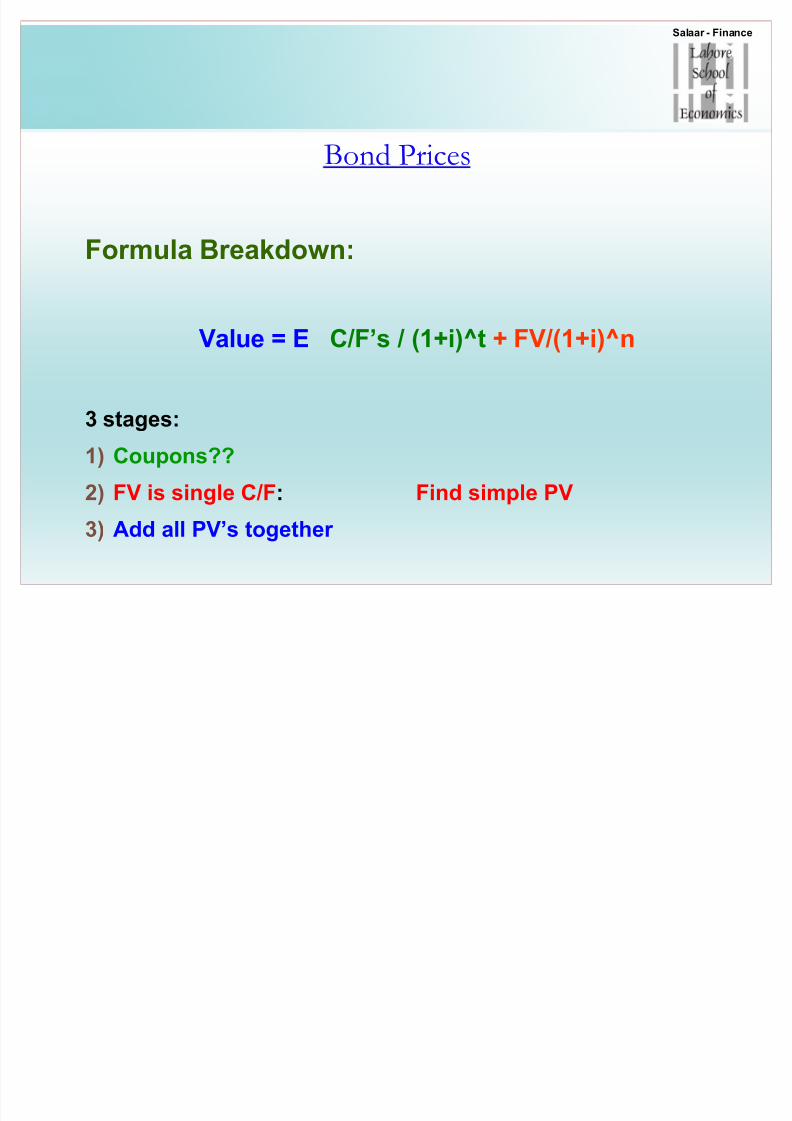

Value = E C/F¶s / (1+i)^t + FV/(1+i)^n

3 stages:

1) Coupons??

2) FV is single C/F: Find simple PV

3) Add all PV¶s together

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 31/117

Salaar - Finance

Bond Prices

Formula Breakdown:

Value = E C/F¶s / (1+i)^t + FV/(1+i)^n

3 stages:

1) Coupons make it an annuity: Find Annuity PV

2) FV is single C/F: Find simple PV

3) Add all PV¶s together

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 32/117

Salaar - Finance

M55

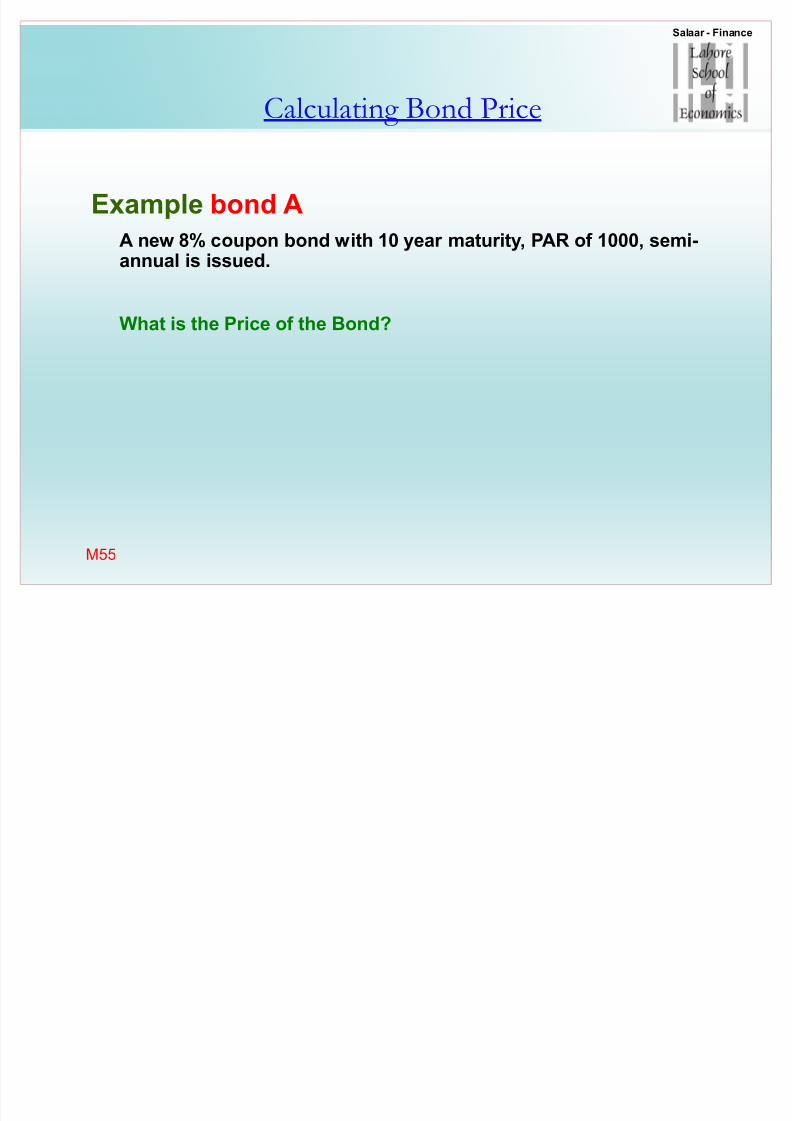

Calculating Bond Price

Example bond AA new 8% coupon bond with 10 year maturity, PAR of 1000, semi-annual is issued.

What is the Price of the Bond?

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 33/117

Salaar - Finance

Calculating Bond Price

Example bond AA new 8% coupon bond with 10 year maturity, PAR of 1000, semi-annual is issued.

What is the Price of the Bond? Ordinary annuity of 40

APV = 40 x ((1- 1/1.04^20) / .04

= 40 *( 1-0.4563)/ .04 = 40*13.59

= 543.61 (coupons PV)

FV PV = (1000) / (1.04)^20 = 1000*.45638 = 456.38

Bond PV = 543.61 + 456.38 = 1000 (same as Face value)

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 34/117

Salaar - Finance

Calculating Bond Price

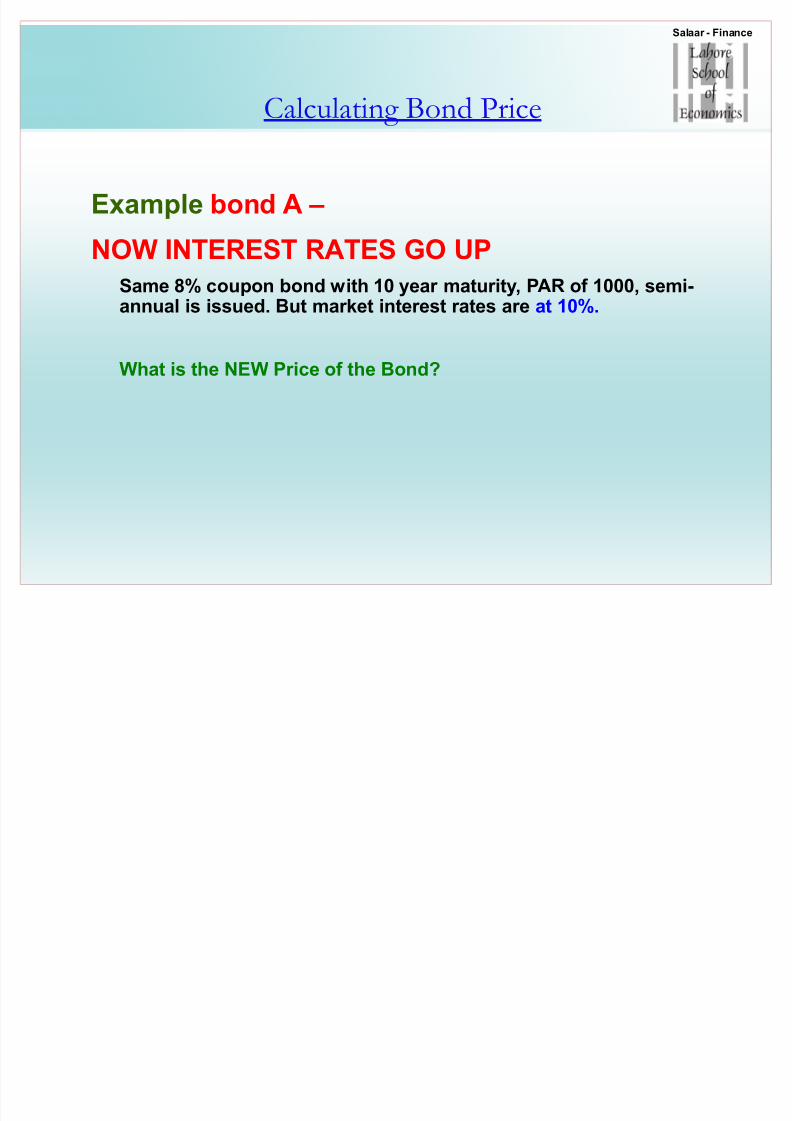

Example bond A ±

NOW INTEREST RATES GO UP

Same 8% coupon bond with 10 year maturity, PAR of 1000, semi-annual is issued. But market interest rates are at 10%.

What is the NEW Price of the Bond?

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 35/117

Salaar - Finance

Calculating Bond Price

Example bond A ± NOW INTEREST RATES GO UPSame 8% coupon bond with 10 year maturity, PAR of 1000, semi-annual isissued. But market interest rates are at 10%.

What is the NEW Price of the Bond? Ordinary annuity of 40

APV = 40 x ((1- 1/1.05^20) / .05

= 40 *( 1-0.3768)/ .05 = 40*12.46

= 498.48 (coupons PV)FV PV = (1000) / (1.05)^20 = 1000*.3768 = 376.89

Bond PV = 498.48 + 376.89 = 875.36 (Now at discount since i is up)

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 36/117

Salaar - Finance

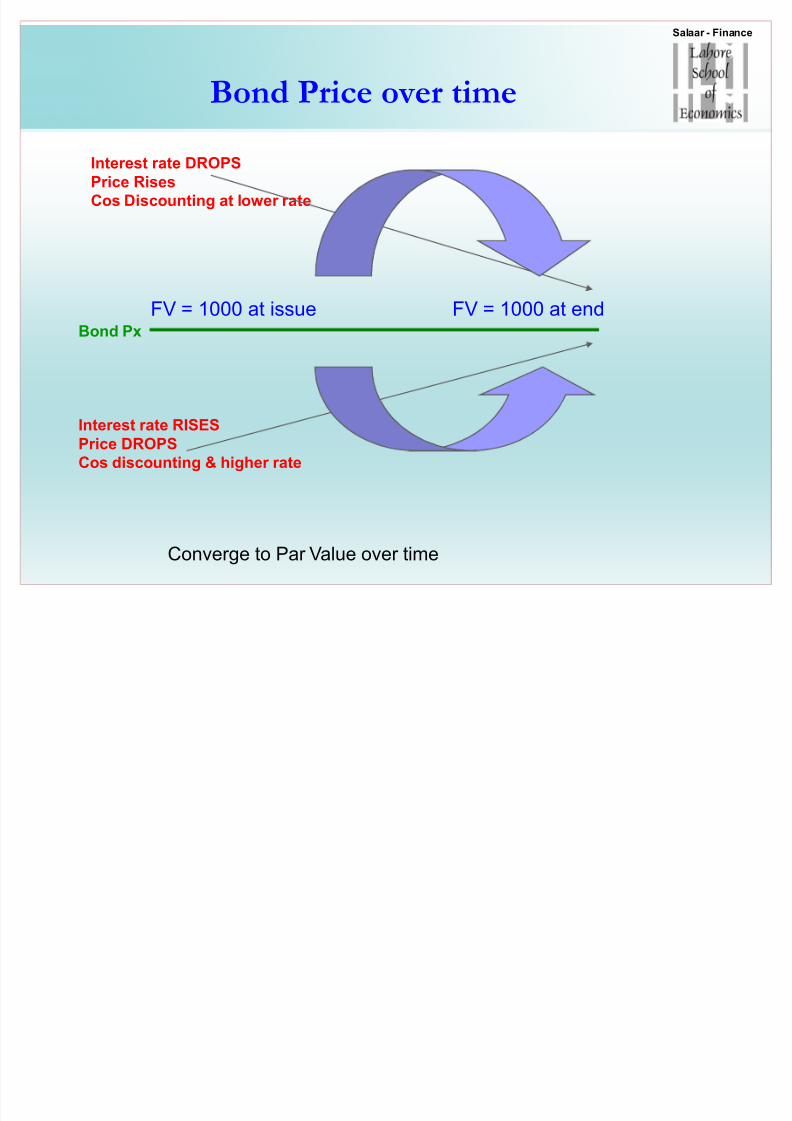

Bond Price over time

FV = 1000 at issue FV = 1000 at end

Interest rate DROPSPrice RisesCos Discounting at lower rate

Interest rate RISESPrice DROPSCos discounting & higher rate

Bond Px

Converge to Par Value over time

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 37/117

Salaar - Finance

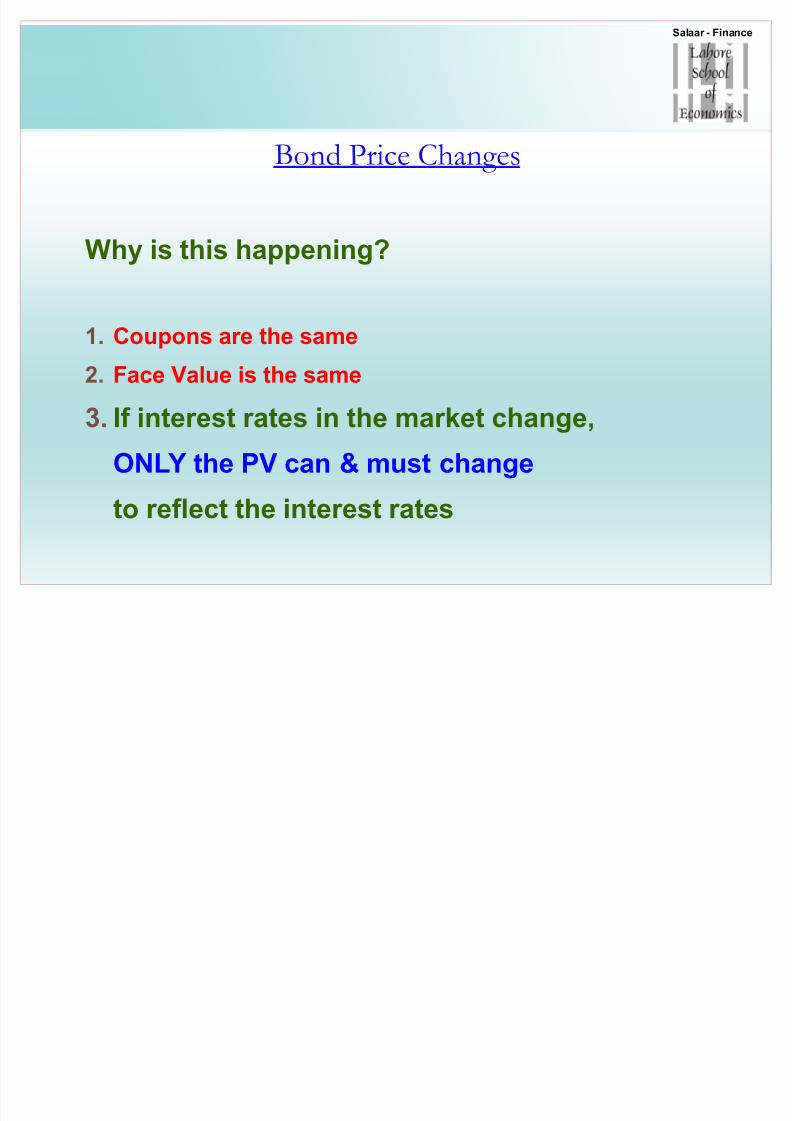

Bond Price Changes

Why is this happening?

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 38/117

Salaar - Finance

Bond Price Changes

Why is this happening?

1. Coupons are the same

2. Face Value is the same

3. If interest rates in the market change,ONLY the PV can & must change

to reflect the interest rates

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 39/117

Salaar - Finance

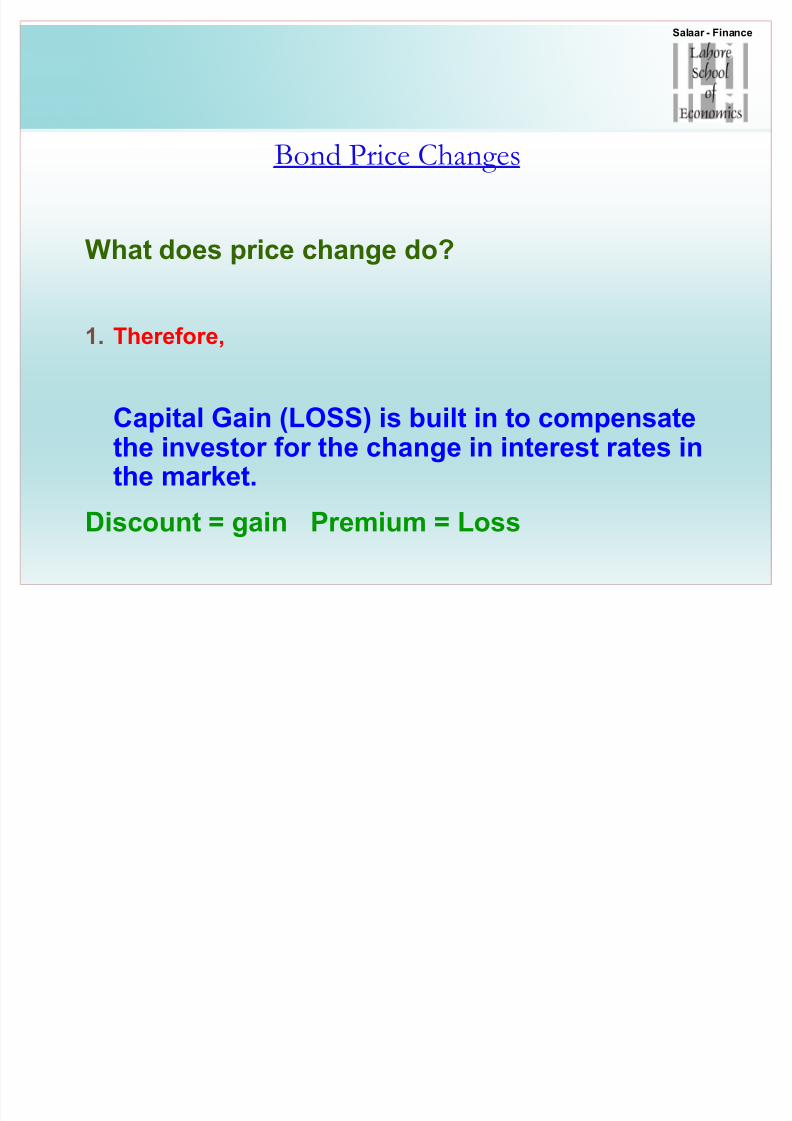

Bond Price Changes

What does price change do?

1. Theref ore,

Capital Gain (LOSS) is built in to compensatethe investor f or the change in interest rates inthe market.

Discount = gain Premium = Loss

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 40/117

S l Fi

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 41/117

Salaar - Finance

Calculating Bond Price

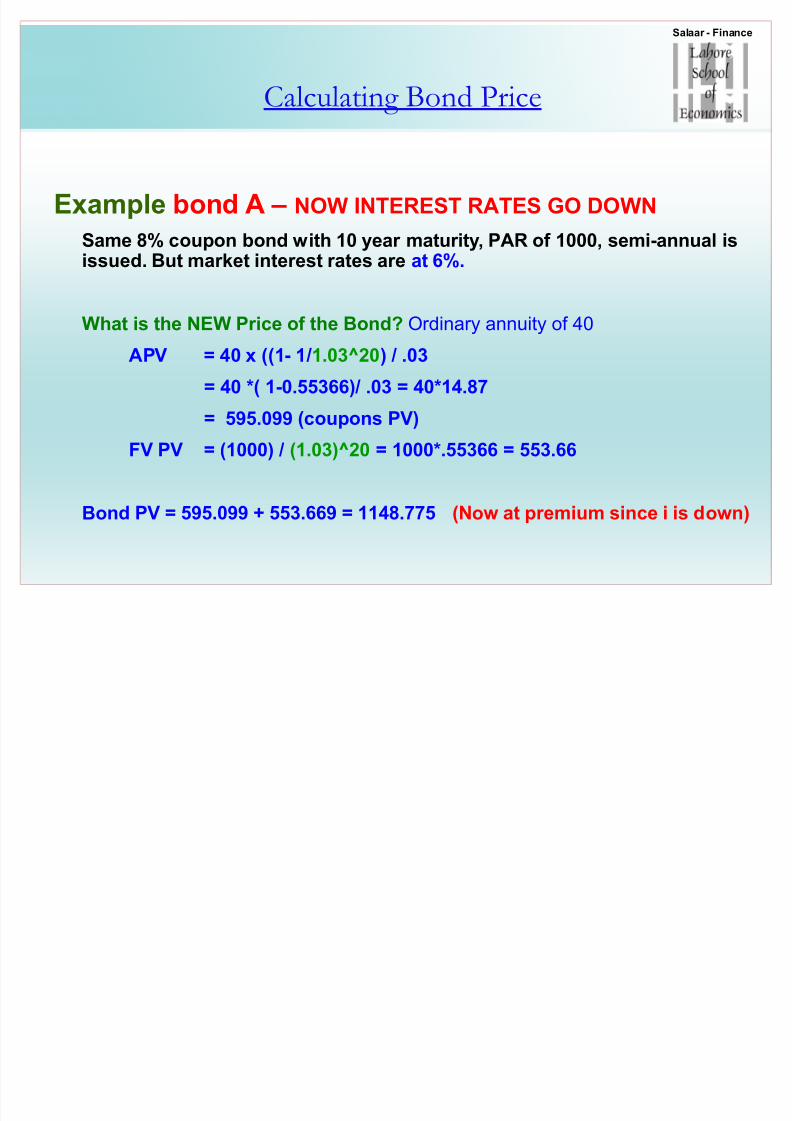

Example bond A ± NOW INTEREST RATES GO DOWN

Same 8% coupon bond with 10 year maturity, PAR of 1000, semi-annual isissued. But market interest rates are at 6%.

What is the NEW Price of the Bond? Ordinary annuity of 40

APV = 40 x ((1- 1/1.03^20) / .03

= 40 *( 1-0.55366)/ .03 = 40*14.87

= 595.099 (coupons PV)FV PV = (1000) / (1.03)^20 = 1000*.55366 = 553.66

Bond PV = 595.099 + 553.669 = 1148.775 (Now at premium since i is down)

S l Fi

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 42/117

Salaar - Finance

R elationship Bond Px & Interest R ates

Bond Px is«?

S l Fi

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 43/117

Salaar - Finance

R elationship Bond Px & Interest R ates

Bond Px is«

INVERSELY Related TO Interest Rates

Salaar Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 44/117

Salaar - Finance

Measuring Bond Yields

There are 4 measures

Current Yield

Yield to Maturity

Yield to Call

Realized Compound Yield

Salaar Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 45/117

Salaar - Finance

Measuring Bond Yields

There are 4 measures

Current Yield (CY)

A Bond¶s annual coupon divided by current market price.

Yield to Maturity (YTM)

Pr omised Compound rate of return at the current market price till mat.

Yield to Call (YC)Pr omised return on a Bond fr om present till date it is likely to be called

Realized Compound Yield (RCY) Yield earned based on actual reinvestment rates-Historical

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 46/117

Salaar - Finance

Measuring Bond Yields

Current Yield (CY)

A Bond¶s annual coupon divided by current market price.

Ratio of coupon interest to current Mkt px.

e.g.A 3 year 10% coupon Bond with interest payments occurring exactly 6mths fr om now & so on. Current price of the Bond is $1052.42

What¶s the current yield?

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 47/117

Salaar - Finance

Measuring Bond Yields

A 3 year 10% coupon Bond with interest payments occurring exactly 6mths fr om now & so on. Current price of the Bond is $1052.42

What¶s the current yield?

C/Px = 100 / 1052.10 = 9.5%

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 48/117

Salaar Finance

Measuring Bond Yields

Yield to Maturity (YTM) ± semiannual rate

Pr omised Compound rate of return at the current market price till mat.

The rate most often quoted

Return based on fixed assumptions«???

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 49/117

Salaar Finance

Measuring Bond Yields

Yield to Maturity (YTM) ± semiannual rate

Pr omised Compound rate of return at the current market price till mat.

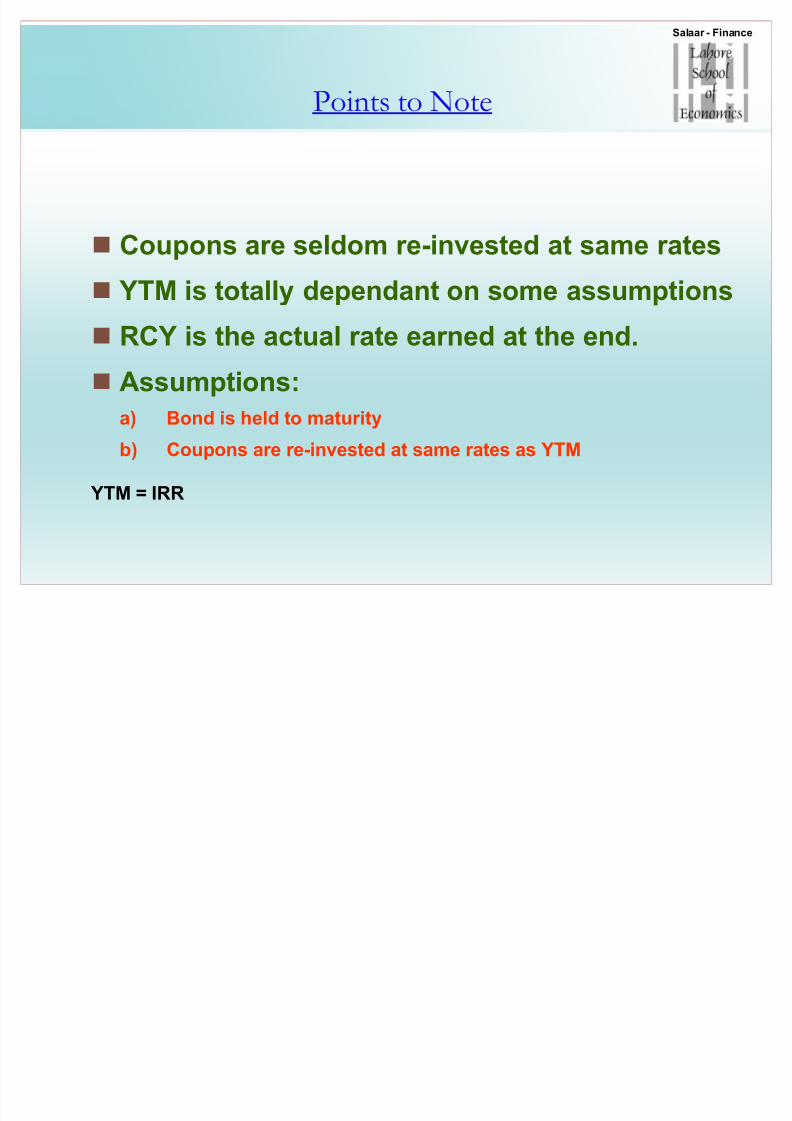

The rate most often quotedReturn based on fixed assumptions

1) The Bond is held to Maturity

2) Coupons are re-invested at the YTM

Means: Compounded return giving PV of Bond as its current price

Same as IRR f or the Bond

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 50/117

Salaar Finance

Measuring Bond Yields

Yield to Maturity (YTM)

Pr omised Compound rate of return at the current market price till mat.

Small letters = semi-annual

Capital letters = annual

PV = E c/(1+ytm)^t + FV/ (1+ytm)^n

FV = 1000

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 51/117

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 52/117

YTM

Example on zer o-coupon

A zer o coupon bond has 12 yrs to maturity & is selling f or $300.

Calculate the ytm & BEY?

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 53/117

YTM

Example on zer o-couponA zer o coupon bond has 12 yrs to maturity & is selling f or $300.

Calculate the ytm & BEY.

PV = FV / (1+ytm)^n

300 = 1000 / (1+ytm)^24

1+ytm^24 = 1000/300

1+ ytm = 3.33^(1/24)

ytm = 3.33^.04166 = 1.0514 ± 1 = 5.14% ytm

5.14x2 = 10.28 BEY

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 54/117

YTM

Example on regular coupon bondA 10% coupon bond has 3 yrs to maturity & is selling f or 1052.42

Calculate the ytm & BEY.

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 55/117

YTM

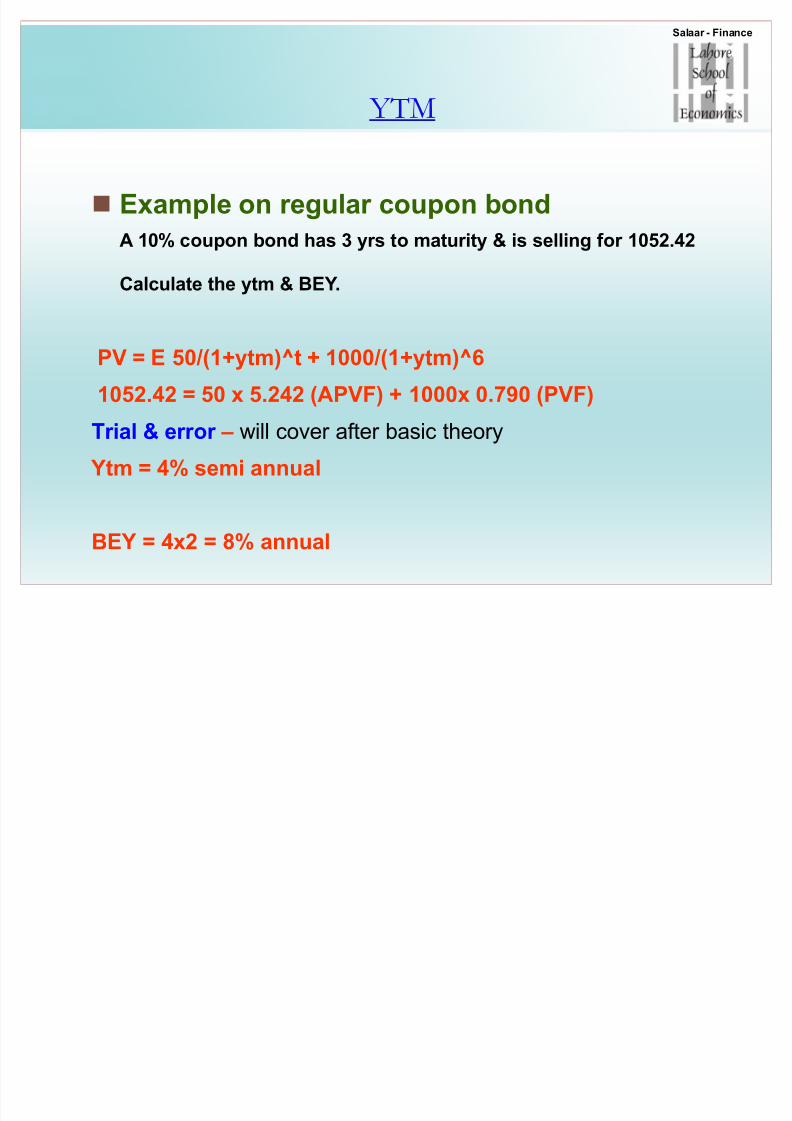

Example on regular coupon bondA 10% coupon bond has 3 yrs to maturity & is selling f or 1052.42

Calculate the ytm & BEY.

PV = E 50/(1+ytm)^t + 1000/(1+ytm)^6

1052.42 = 50 x 5.242 (APVF) + 1000x 0.790 (PVF)

Trial & err or ± will cover after basic theory

Ytm = 4% semi annual

BEY = 4x2 = 8% annual

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 56/117

Measuring Bond Yields

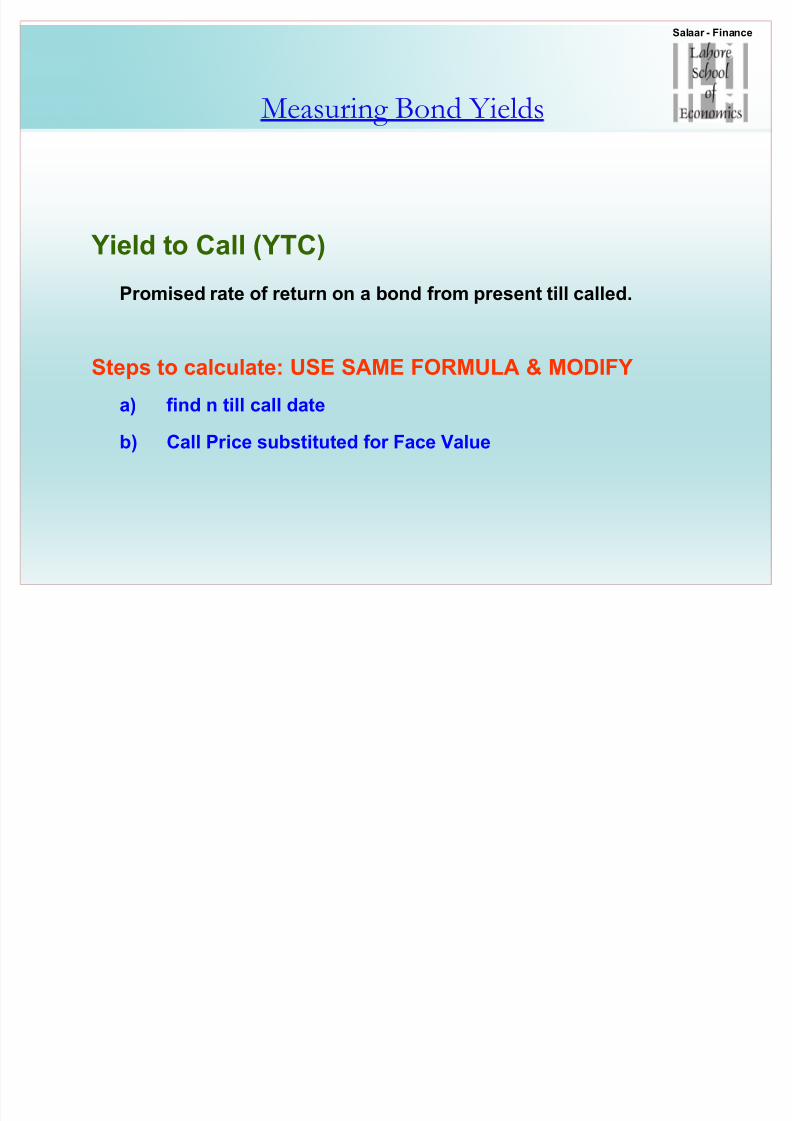

Yield to Call (YTC)

Pr omised rate of return on a bond fr om present till called.

Steps to calculate: USE SAME FORMULA & MODIFY

a) find n till call date

b) Call Price substituted f or Face Value

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 57/117

Measuring Bond Yields

Realized Compound Yield (RCY)-historical

Yield earned based on actual re-investment rates (IRR)

Semi-annual realized compound yield is:

RCY = ( total wealth=FV / Pur. Px=PV ) ^ 1/n - 1

NOTE: comes from the FV=PV(1+i)^n, reshuffling for i

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 58/117

R C Y (realized c yield)

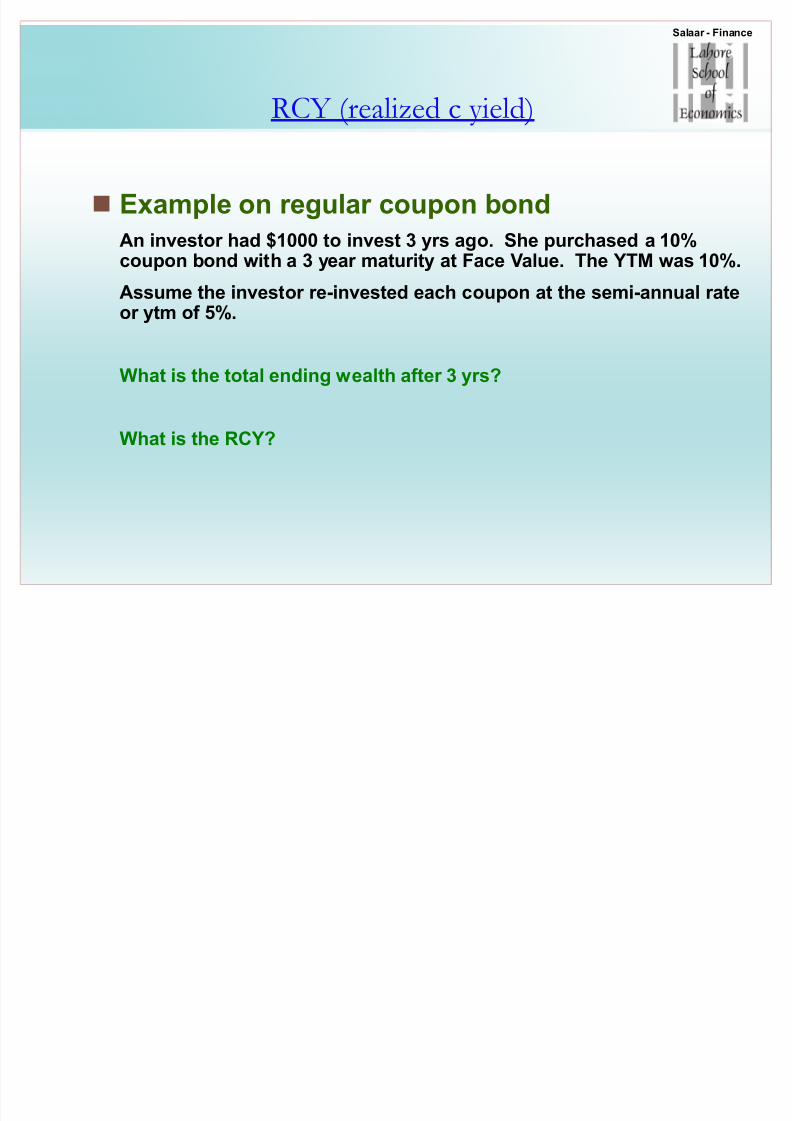

Example on regular coupon bondAn investor had $1000 to invest 3 yrs ago. She purchased a 10%coupon bond with a 3 year maturity at Face Value. The YTM was 10%.

Assume the investor re-invested each coupon at the semi-annual rateor ytm of 5%.

What is the total ending wealth after 3 yrs?

What is the RCY?

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 59/117

R C Y

Example on regular coupon bondAn investor had $1000 to invest 3 yrs ago. She purchased a 10%coupon bond with a 3 year maturity at Face Value. The YTM was 10%.

Assume the investor re-invested each coupon at the semi-annual rateor ytm of 5%.

What is the total ending wealth after 3 yrs?

(1+.05)^6= 1.340095 * 1000 = 1340.09 (includes the initial outlay)

thus, earnings were 340.09

What is the RCY?

(1340.10 / 1000 )̂ 1/6 ± 1 = 1.05 ± 1 = .05 RCY x2 = 10% BEY

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 60/117

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 61/117

R e-investment R isk

assumption

Part of interest rate risk resulting fr om

uncertainty abo

ut the rate at which futureinterest coupons can be re-invested

Assumption is unlikely in real life«why?

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 62/117

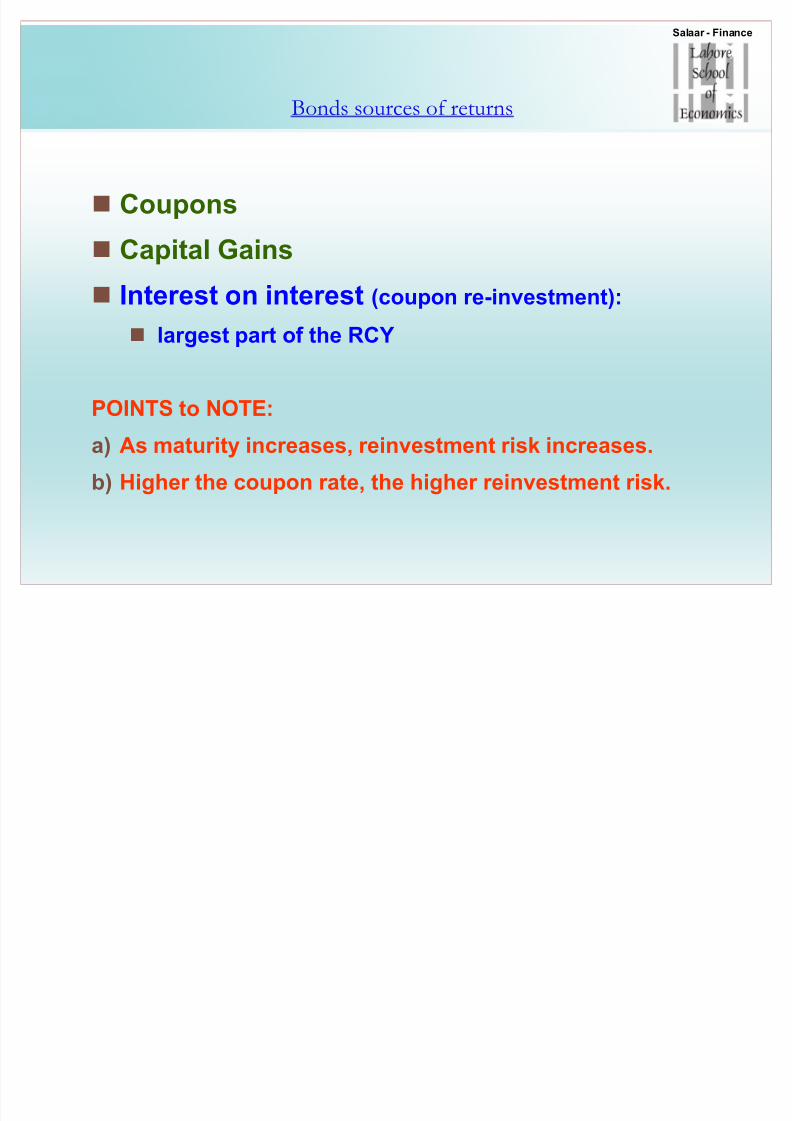

Bonds sources of returns

Coupons

Capital Gains

Interest on interest (coupon re-investment):

largest part of the RCY

POINTS to NOTE:

a) As maturity increases, reinvestment risk increases.

b) Higher the coupon rate, the higher reinvestment risk.

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 63/117

Bonds sources of returns

For a zer o-coupon bond«.

What is the RCY equal to?

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 64/117

Bonds sources of returns

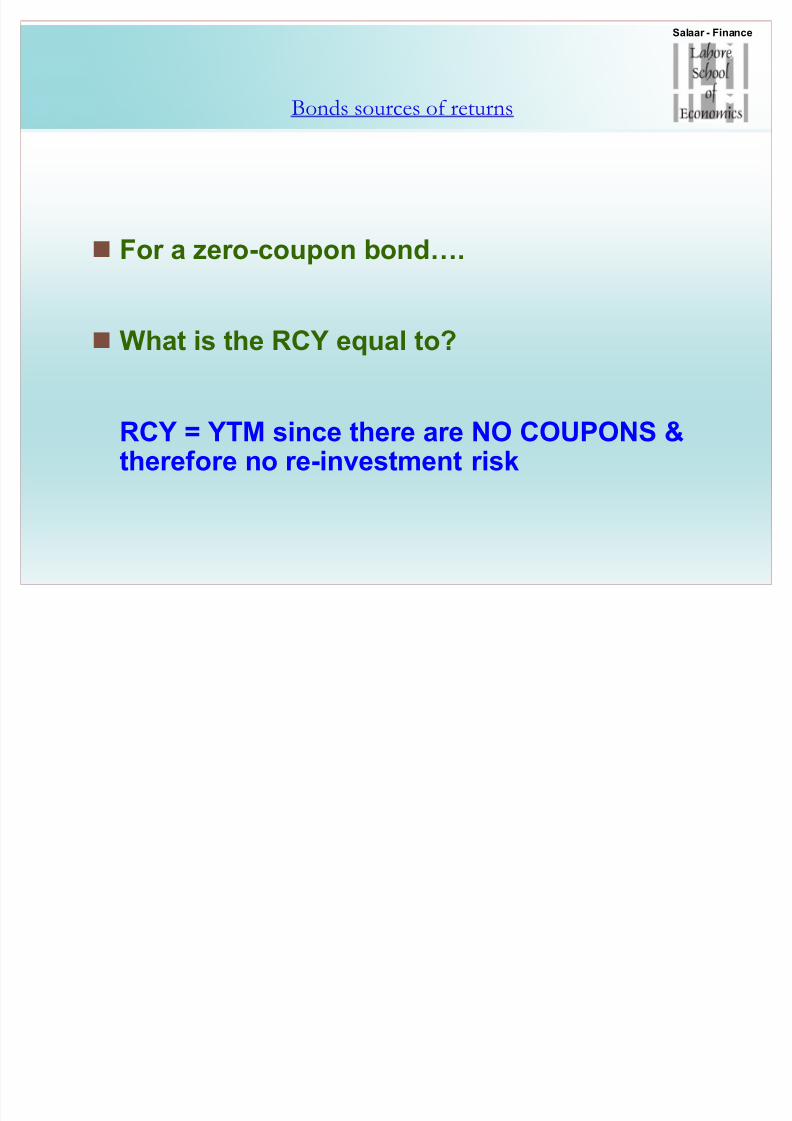

For a zer o-coupon bond«.

What is the RCY equal to?

RCY = YTM since there are NO COUPONS &theref ore no re-investment risk

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 65/117

Illustration of re-investment portion

Example on regular coupon bondA 10% coupon bond with 20yr maturity purchased at PAR ($1000). If all coupons are re-invested at 5% on semi-annual basis, (ytm=5%),

then«.

What is the total dollar return at end 20yrs?

What is the break down of returns? FV+Coupons+interest on interest

M20

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 66/117

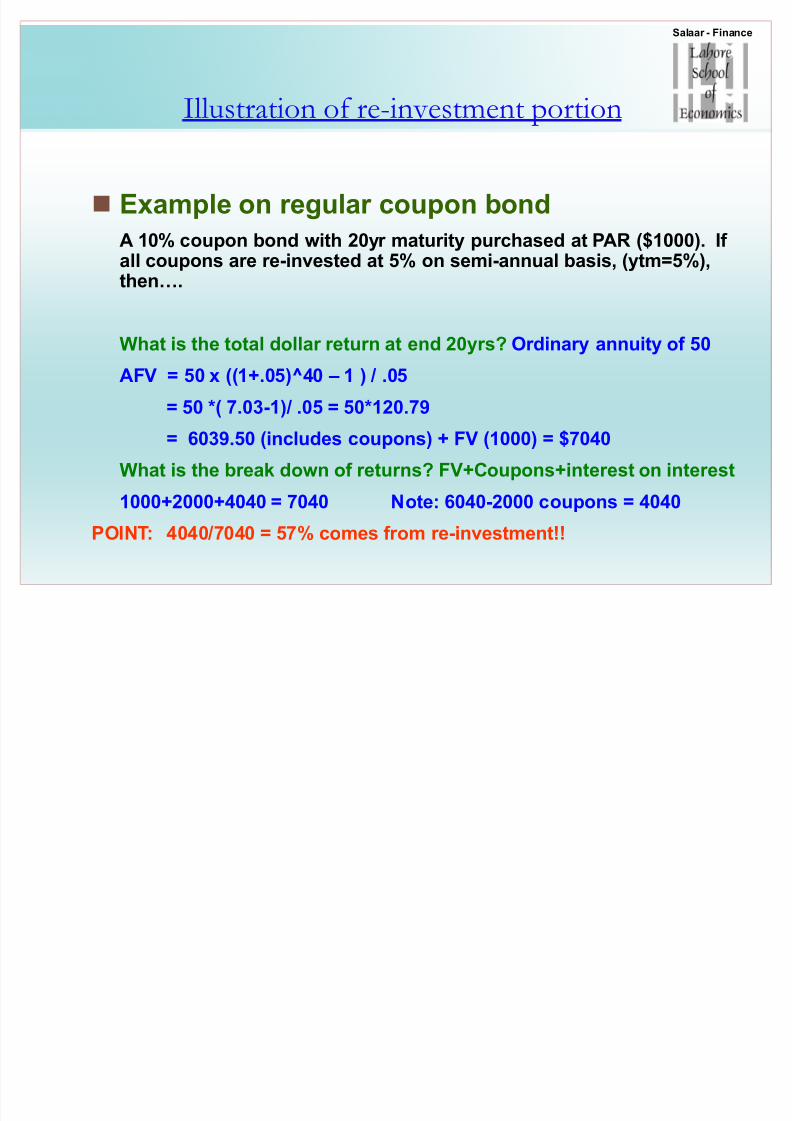

Illustration of re-investment portion

Example on regular coupon bondA 10% coupon bond with 20yr maturity purchased at PAR ($1000). If all coupons are re-invested at 5% on semi-annual basis, (ytm=5%),

then«.

What is the total dollar return at end 20yrs? Ordinary annuity of 50

AFV = 50 x ((1+.05)^40 ± 1 ) / .05

= 50 *( 7.03-1)/ .05 = 50*120.79

= 6039.50 (includes coupons) + FV (1000) = $7040

What is the break down of returns? FV+Coupons+interest on interest

1000+2000+4040 = 7040 Note: 6040-2000 coupons = 4040

POINT: 4040/7040 = 57% comes fr om re-investment!!

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 67/117

W hat is one advantage of

Zer o-coupon bond«.in terms of risk?

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 68/117

W hat is one advantage of

Zer o-coupon bond«.in terms of risk?

NO Re-investment risk, since no coupons

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 69/117

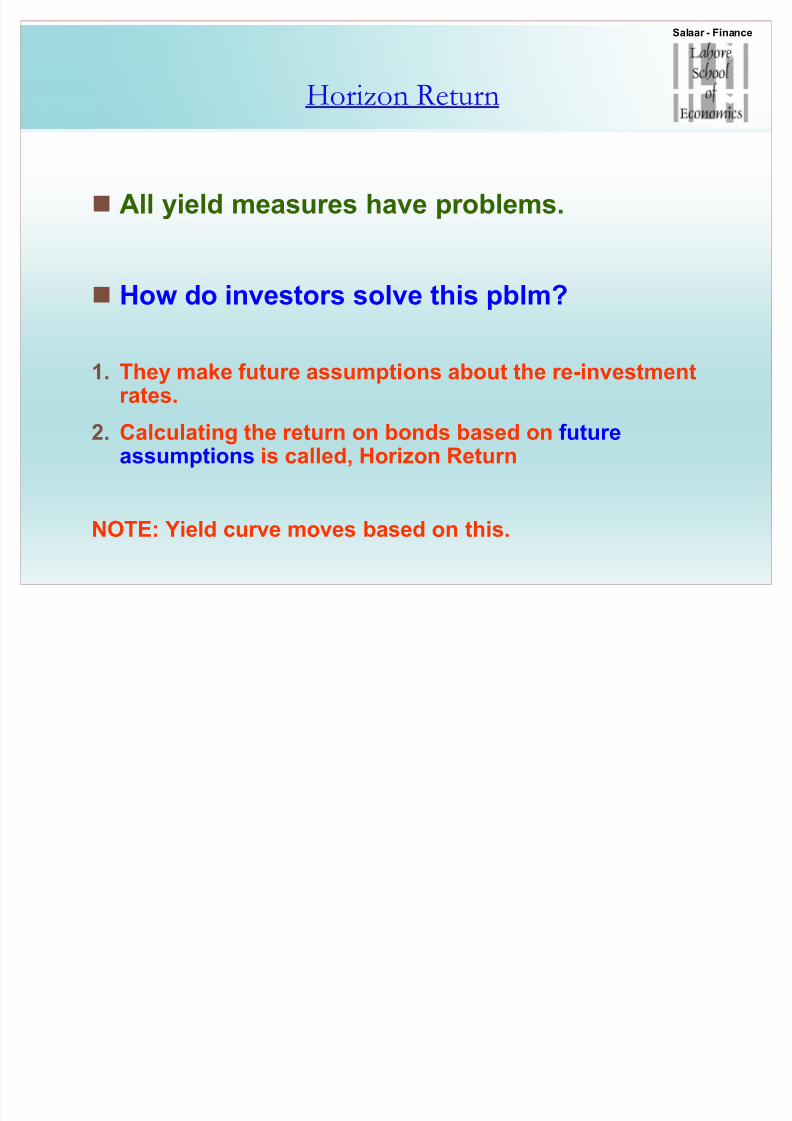

Horizon R eturn

All yield measures have pr oblems.

How do investors solve this pblm?

1. They make future assumptions about the re-investmentrates.

2. Calculating the return on bonds based on futureassumptions is called, Horizon Return

NOTE: Yield curve moves based on this.

Salaar Salaar --FinanceFinance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 70/117

PART II

BONDS & INTEREST RATES

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 71/117

Bonds

What is a Bond?

Skip

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 72/117

BondsWhat is a Bond

Debt instrument to raise money (Loan)

Issued by Corporations & Govts

Interest Only Loan

Has a standard Face Value of $1000 (Corp)

Coupons are paid semi-annually

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 73/117

Bond Yields

2 Components of Interest rates

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 74/117

Bond Yields

Components of Interest rates

Real Risk Free rate:

opportunity cost of f oregoing consumption (given no inflation)

Nominal Interest Rates:

Real rate PLUS inflation adjustment

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 75/117

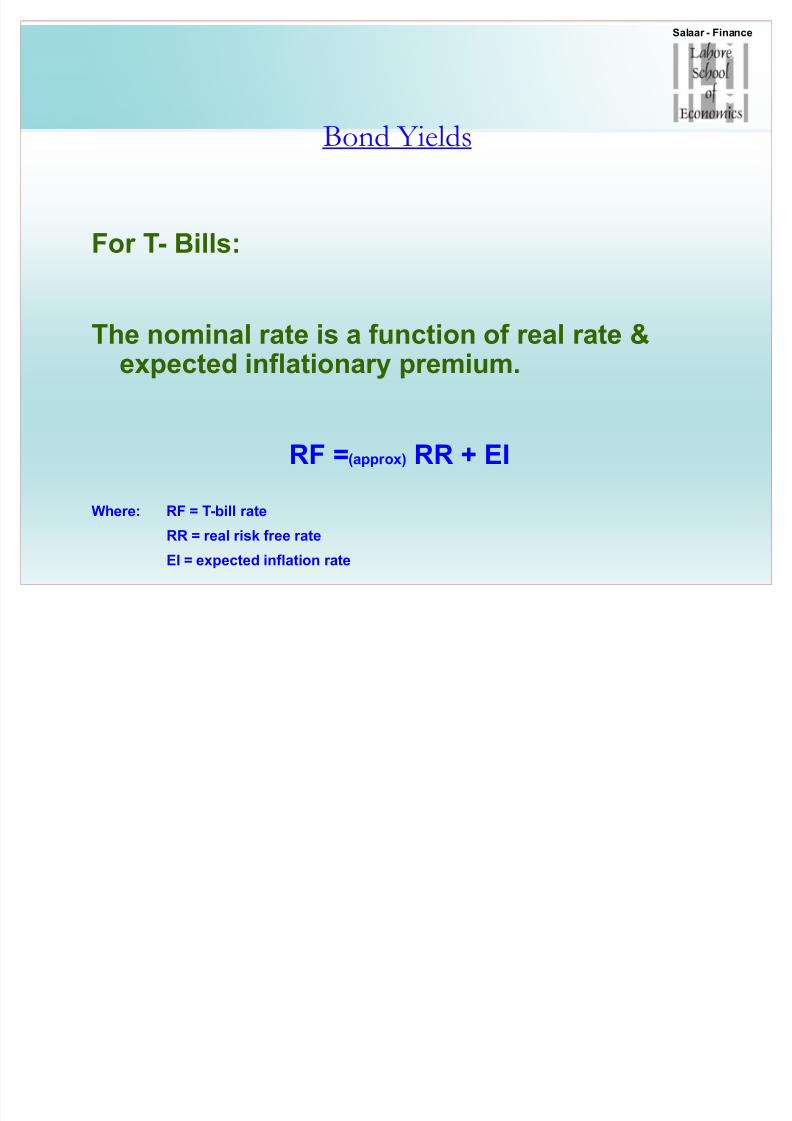

Bond Yields

For T- Bills:

The nominal rate is a function of real rate &expected inflationary premium.

RF =(appr ox) RR + EI

Where: RF = T-bill rate

RR = real risk free rate

EI = expected inflation rate

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 76/117

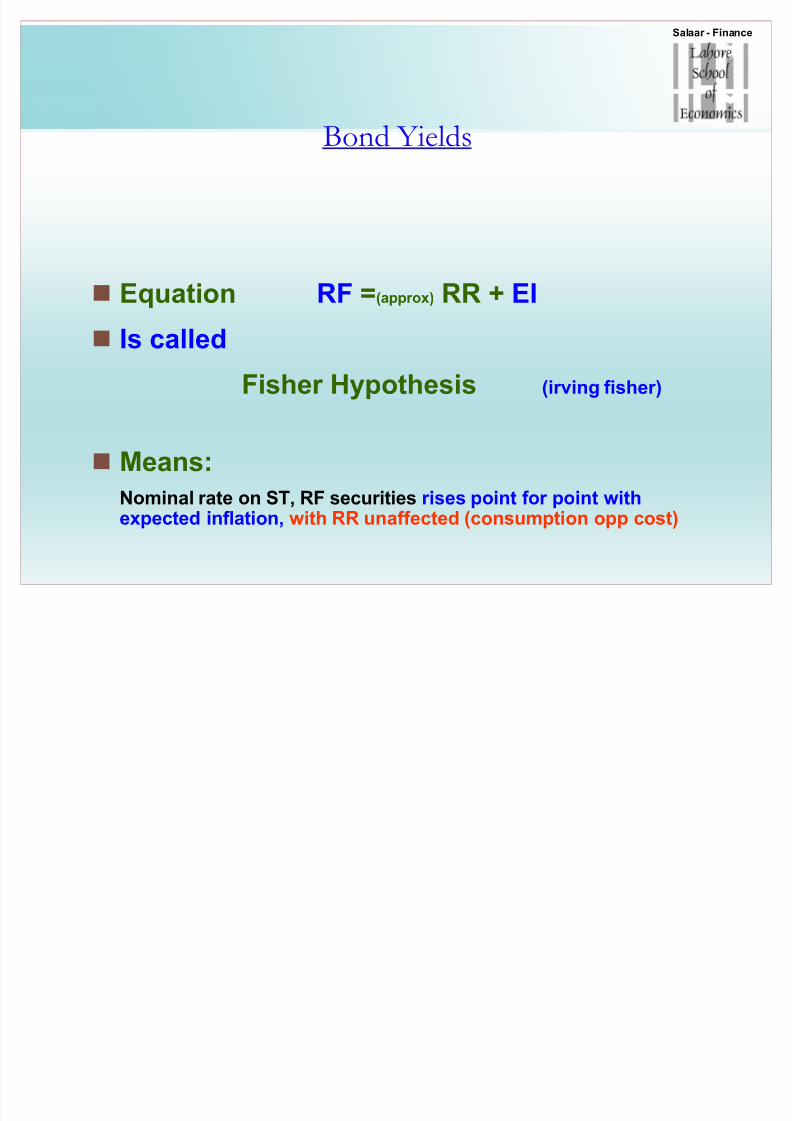

Bond Yields

Equation RF =(appr ox) RR + EI

Is called

Fisher Hypothesis (irving fisher)

Means:Nominal rate on ST, RF securities rises point f or point withexpected inflation, with RR unaffected (consumption opp cost)

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 77/117

Fish

er Effect

The nominal rate R is a function of real rate r

& expected inflatio

nary premium h.

Equation is«?

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 78/117

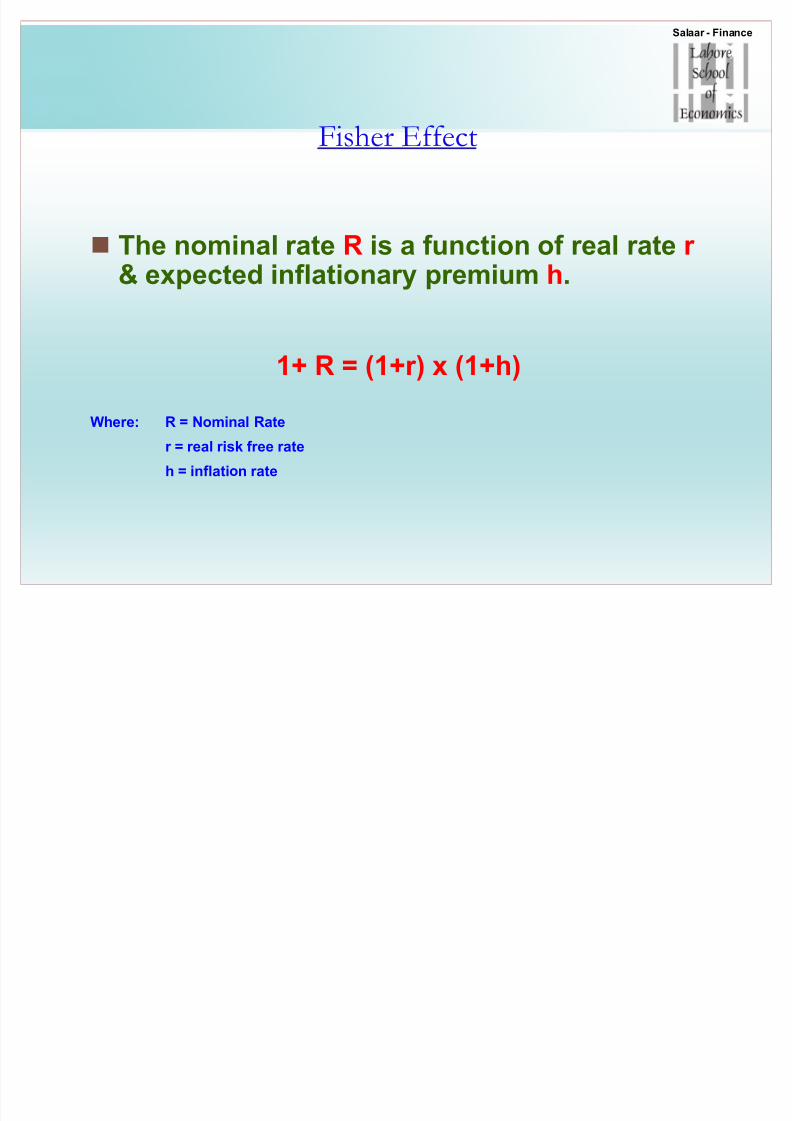

Fish

er Effect

The nominal rate R is a function of real rate r

& expected inflatio

nary premium h.

1+ R = (1+r) x (1+h)

Where: R = N

ominal Rate

r = real risk free rate

h = inflation rate

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 79/117

M

EASUR

INGR

ETUR

NSFormula ± Real Returns

Real Return (inflation adjusted)

TRia (r) = ( (1+ R (nominal) ) / (1+h) ) ± 1

TRia = total return inflation adjusted

h = inflation rate

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 80/117

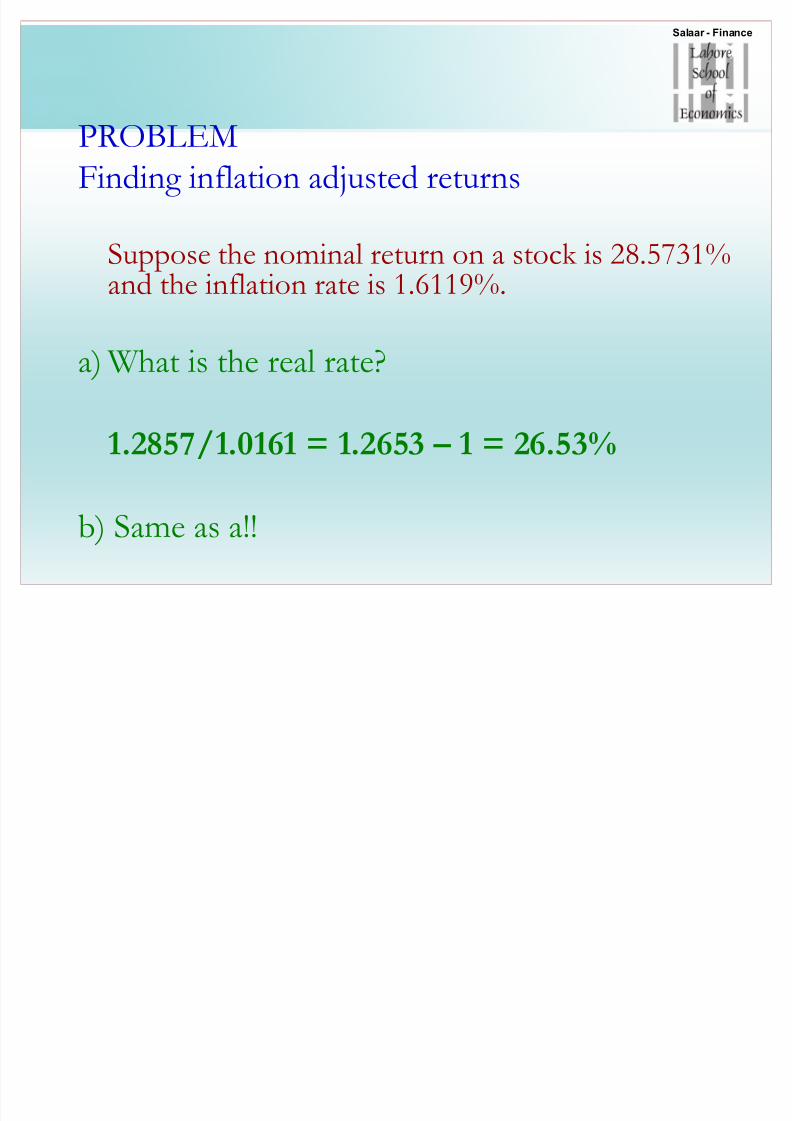

PROBLEM Finding inflation adjusted returns

Suppose the nominal return on a stock is 28.5731%and the inflation rate is 1.6119%.

a) W h

at is th

e real rate?b) W hat is the inflation adjusted return?

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 81/117

PROBL

EM

Finding inflation adjusted returns

Suppose the nominal return on a stock is 28.5731%

and the inflation rate is 1.6119%.

a) W hat is the real rate?

1.2857/1.0161 = 1.2653 ² 1 = 26.53%

b) Same as a!!

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 82/117

PO

INT TO

NO

TE

Most financial rates are quoted in NOMINAL.

We will use the symbol R f or this nominal rate

START

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 83/117

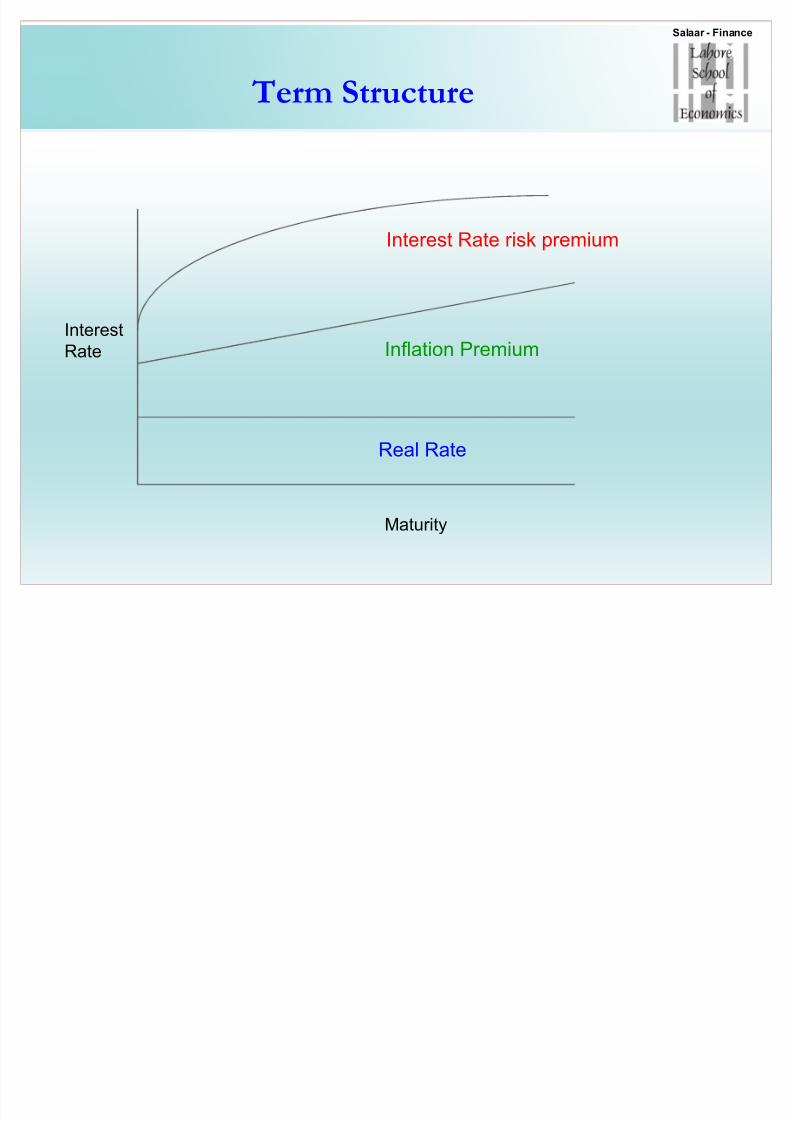

D

eterminants of B

ond Yields

Term Structure of Interest Rates

1) Real Rate (opportunity cost)

2) Expected Inflation (investors require higher nominal rates)

3) Interest Rate risk premium (coupon bonds) ± yield curve

Definition of TSIR

Nominal rate on default-free, pure discount bonds of all maturities

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 84/117

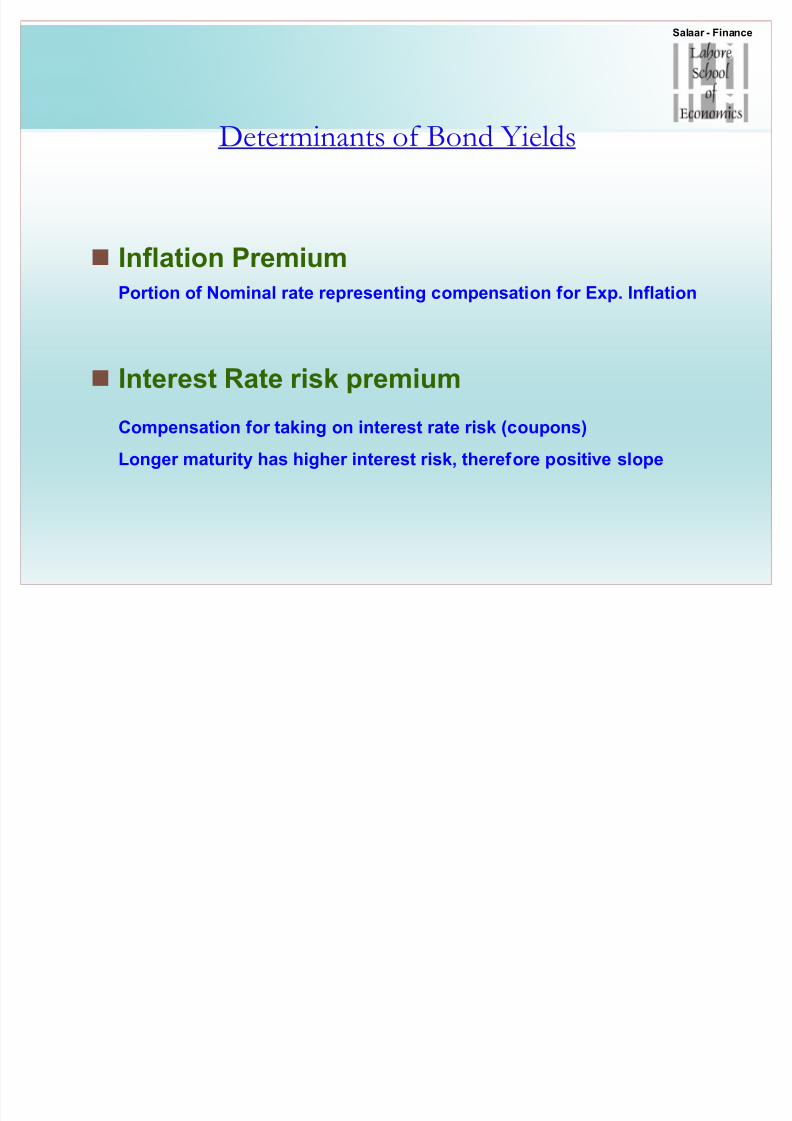

D

eterminants of B

ond Yields

Inflation Premium

Portion of Nominal rate representing compensation f or Exp. Inflation

Interest Rate risk premium

Compensation f or taking on interest rate risk (coupons)

Longer maturity has higher interest risk, theref ore positive slope

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 85/117

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 86/117

M5

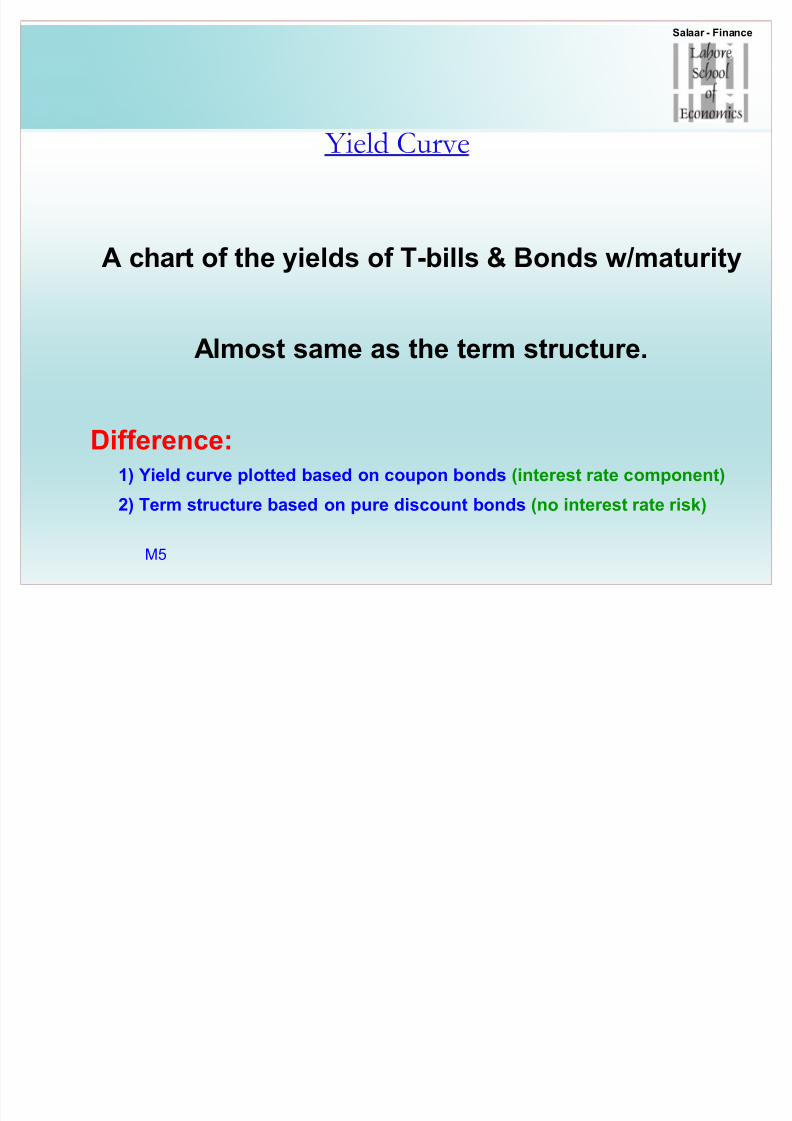

Yield Curve

A chart of the yields of T-bills & Bonds w/maturity

Almost same as the term structure.

Difference:1) Yield curve plotted based on coupon bonds (interest rate component)

2) Term structure based on pure discount bonds (no interest rate risk)

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 87/117

Corp Bonds have additional

Premiums

Default risk premium

Compensation f or possibility of default

Taxability PremiumCompensation f or unfavorable tax implications

Liquidity PremiumCompensation f or lack of liquidity (ability to sell)

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 88/117

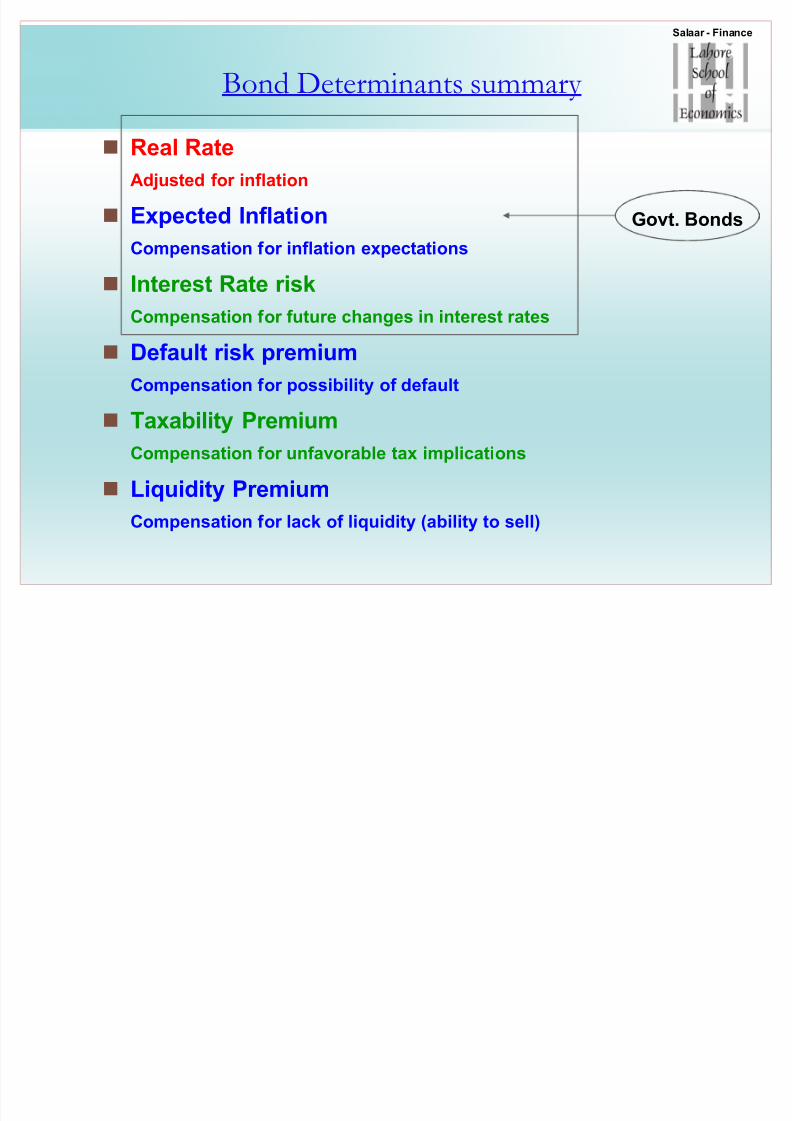

Bond Determinants summary

Real RateAdjusted f or inflation

Expected Inflation

Compensation f or inflation expectations

Interest Rate riskCompensation f or future changes in interest rates

Default risk premium

Compensation f or possibility of default

Taxability PremiumCompensation f or unfavorable tax implications

Liquidity Premium

Compensation f or lack of liquidity (ability to sell)

Govt. Bonds

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 89/117

W hat affects Bond Prices

Effects of Maturity? +ve

Effects of coupon size? -ve

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 90/117

W hat affects Bond Prices

Effects of Maturity?

For a given change in rates, price of longer term

bonds will change more than shorter term bonds

Effects of coupon size?

Bond Px fluctuations (volatility) are inversely related to coupon rates.

The larger the coupon, f or same maturity, the lower the volatility

m40 Bond Px sensitivity ( 100bp chg on 10% & 100% coupons effect on %px chg!)

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 91/117

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 92/117

F

orB

onds

Longer the maturity, higher the IR risk

WHY?

Cos Longer term has a greater discounting effect(compounding curve) on the Face Value receivedat maturity!

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 93/117

For Bonds

Maturity exposure

Longer the maturity, higher the IR risk

Theref ore

Since the Principal is at end, Bond¶s Px ismore sensitive to time (maturity)

PV on 30yrs is more sensitive to PV on 1 year!! (f or Face Value)

NOTE: But it increases (term risk) at a decreasing rate

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 94/117

For Bonds

The other factor

Coupon Rate risk

?

WHY?

M20

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 95/117

For Bonds

The other factor

Coupon Rate risk

Lower Coupons have higher risk.

WHY?

M20

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 96/117

For Bonds

The other factor

Coupon Rate risk

Lower Coupons have higher risk.

Lower coupons make Bond Px more dependant on FV!

(Risk = % changes in Bond px f or given chg in interest rates)

WHY?

Since C/F¶s are paid towards the back end of time line &

relative to Face value are smaller in size! (affected moreby discounting)

NOTE: compare PV of zer o-coupon vs regular

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 97/117

Measuring Bond Yields

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 98/117

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 99/117

Measuring Volatility:

Duration

Duration

A measure of a bond¶s lifetime which accounts f or the

entire pattern of cash flows.Measures the weighted average maturity of C/F¶s on a PVbasis.

To solve which pr oblem?

Changes in interest rates result in different % changes inBond Px¶s. Duration combines the coupon & maturity

(size & timing) of C/F effects into one yardstick.

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 100/117

Measuring Volatility:

Duration Example

Duration of 4.054 (on 5 yr bond) means:

The TVM weighted average number of years

needed to

reco

ver the co

sto

f thisBo

nd is 4.054.

Although the bond has 5 yrs to maturity, interest paymentsare received in the first 4 yrs

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 101/117

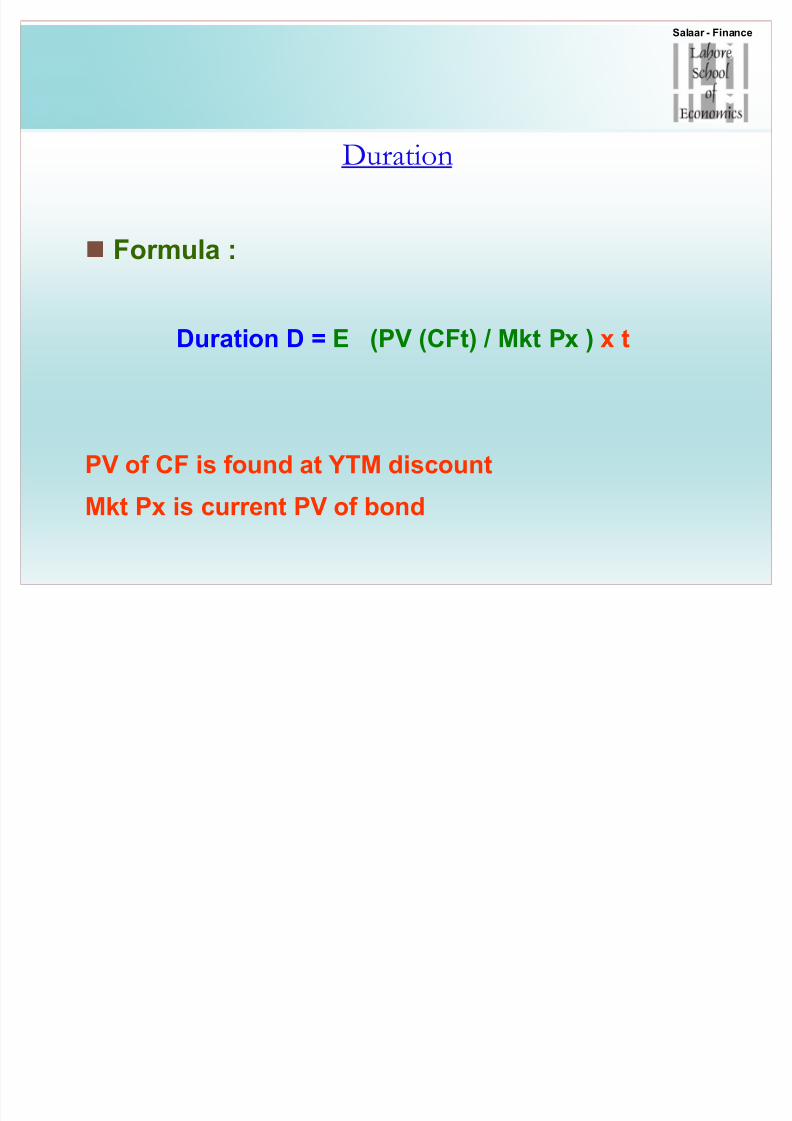

Calculating Duration

Duration (stated in yrs)

Co

nvert TIME to

a weighted time perio

d.

Concept

All time periods are weighted & summed. The result is

duration.

PV of each cash flow as a %age of the current price serves asthe weights, which are then applied to time periods. SUM of these equals 1.0

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 102/117

Salaar - Finance

Exercise

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 103/117

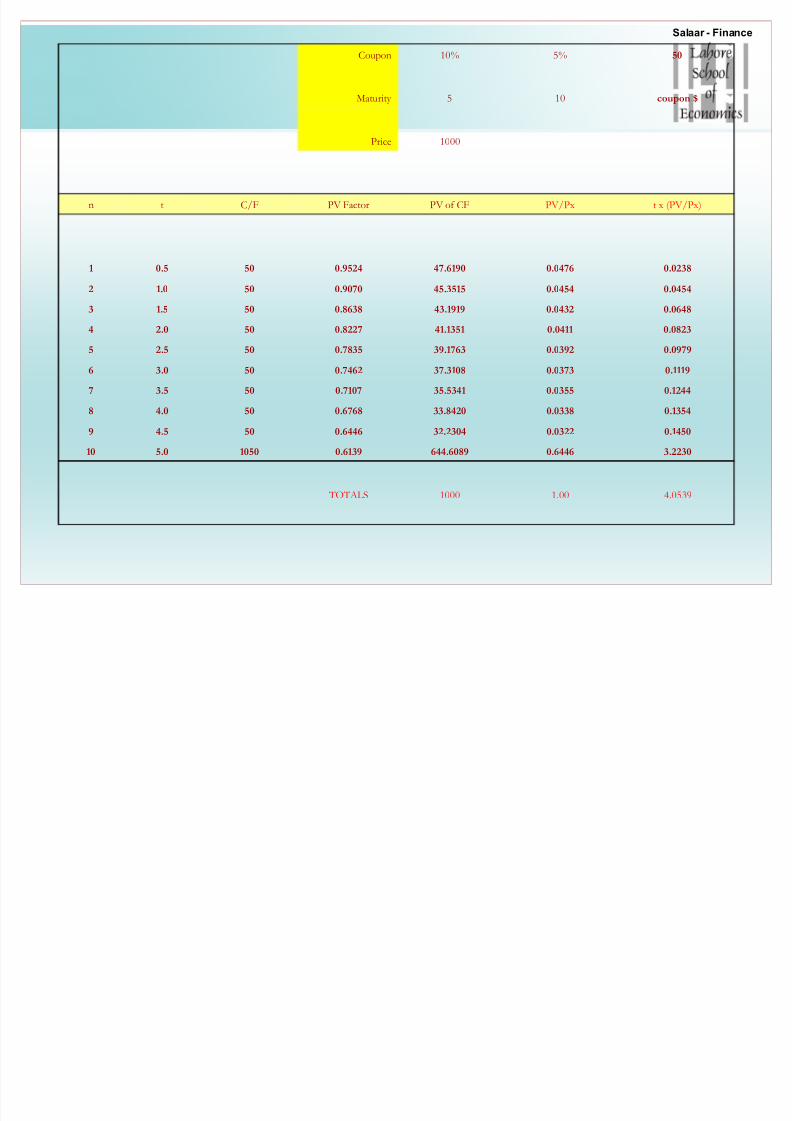

Coupon 10% 5% 50

Maturity 5 10 coupon $

Price 1000

n t C/F PV Factor PV of CF PV /Px t x (PV /Px)

1 0.5 50 0.9524 47.6190 0.0476 0.0238

2 1.0 50 0.9070 45.3515 0.0454 0.0454

3 1.5 50 0.8638 43.1919 0.0432 0.0648

4 2.0 50 0.8227 41.1351 0.0411 0.0823

5 2.5 50 0.7835 39.1763 0.0392 0.0979

6 3.0 50 0.7462 37.3108 0.0373 0.1119

7 3.5 50 0.7107 35.5341 0.0355 0.1244

8 4.0 50 0.6768 33.8420 0.0338 0.1354

9 4.5 50 0.6446 32.2304 0.0322 0.1450

10 5.0 1050 0.6139 644.6089 0.6446 3.2230

TO TALS 1000 1.00 4.0539

Salaar - Finance

Coupon 10% 5% 50

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 104/117

Maturity 5 10 coupon $

Price 1000

n t C/F PV Factor PV of CF PV /Px t x (PV /Px)

1 0.5 50 0.9524 47.6190 0.0476 0.0238

2 1.0 50 0.9070 45.3515 0.0454 0.04543 1.5 50 0.8638 43.1919 0.0432 0.0648

4 2.0 50 0.8227 41.1351 0.0411 0.0823

5 2.5 50 0.7835 39.1763 0.0392 0.0979

6 3.0 50 0.7462 37.3108 0.0373 0.1119

7 3.5 50 0.7107 35.5341 0.0355 0.1244

8 4.0 50 0.6768 33.8420 0.0338 0.1354

9 4.5 50 0.6446 32.2304 0.0322 0.1450

10 5.0 1050 0.6139 644.6089 0.6446 3.2230

TO TALS 1000 1.00 4.0539

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 105/117

Duration

Shorter Formula :

Duration D = (1+ytm)/ytm . ( 1- (1/ytm^n))

Use semi-annual rateDouble the n

Divide answer by 2 to convert to annual basisM10

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 106/117

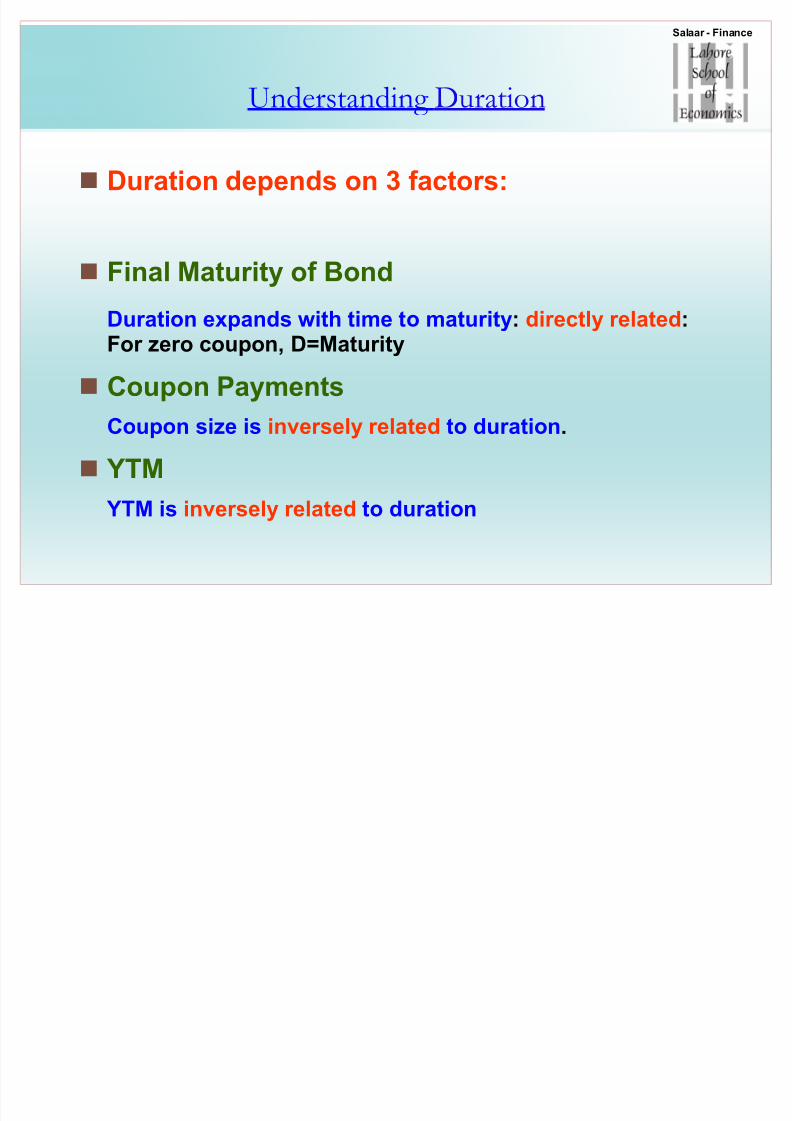

Understanding Duration

Duration depends on 3 factors:

Final Maturity of Bond

Duration expands with time to maturity: directly related:For zer o coupon, D=Maturity

Coupon Payments

Coupon size is inversely related to duration.

YTM

YTM is inversely related to duration

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 107/117

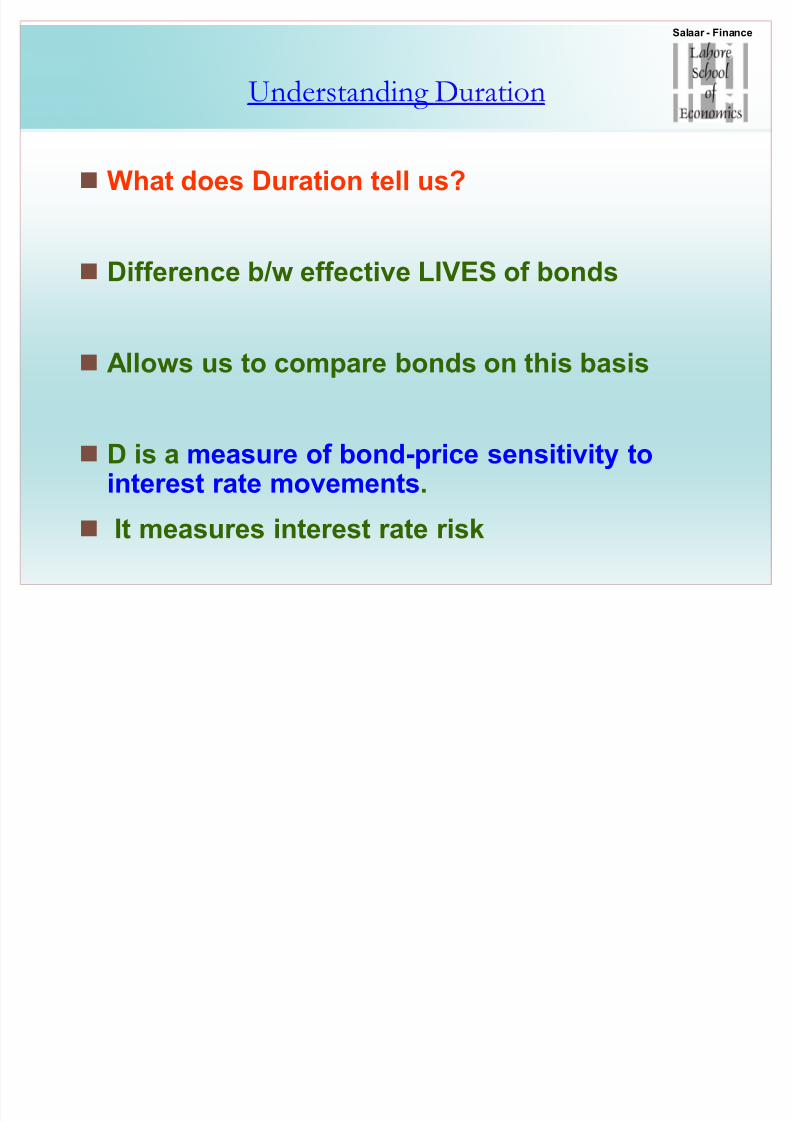

Understanding Duration

What does Duration tell us?

Difference b/w effective LIVES of bonds

Allows us to compare bonds on this basis

D is a measure of bond-price sensitivity to interest rate movements.

It measures interest rate risk

Salaar - Finance

d d

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 108/117

Understanding Duration

Example

Given a 10% coupon bond, ytm of 10%..

If maturity is 5yrs, D = 4.054 (effective life!)

If maturity is 10yrs, D = 6.76

If maturity is 20yrs, D = 9.36

If maturity is 50yrs, D = 10.91 yrs

Reason is, C/F¶s in distant future result in smaller PV¶s

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 109/117

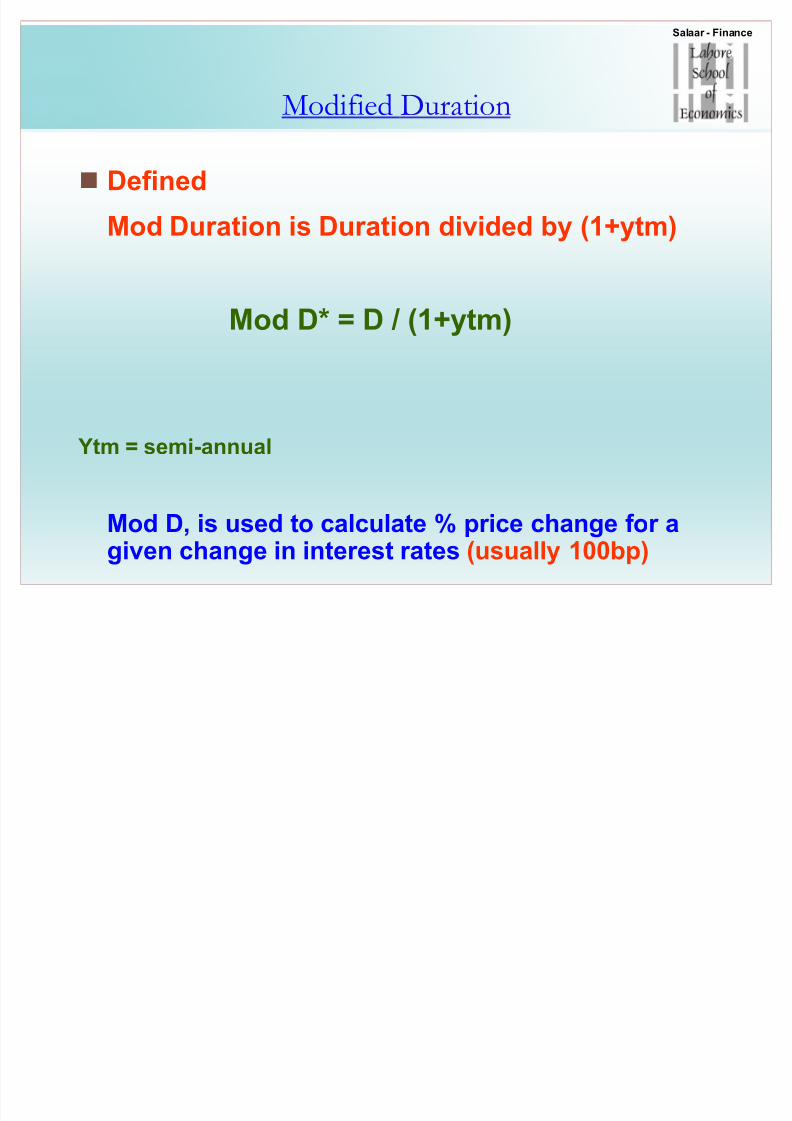

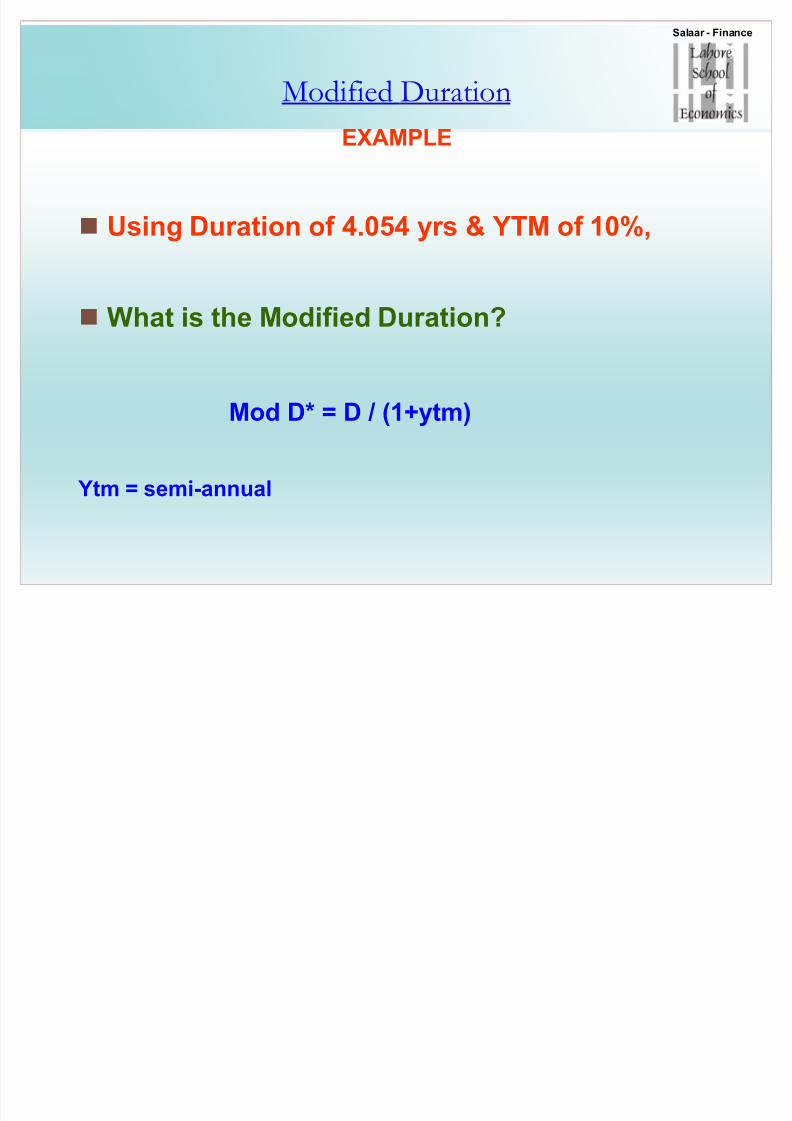

Modified Duration

Defined

Mod Duration is Duration divided by (1+ytm)

Mod D* = D / (1+ytm)

Ytm = semi-annual

Mod D, is used to calculate % price change f or agiven change in interest rates (usually 100bp)

Salaar - Finance

M difi d D i

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 110/117

Modified Duration

EXAMPLE

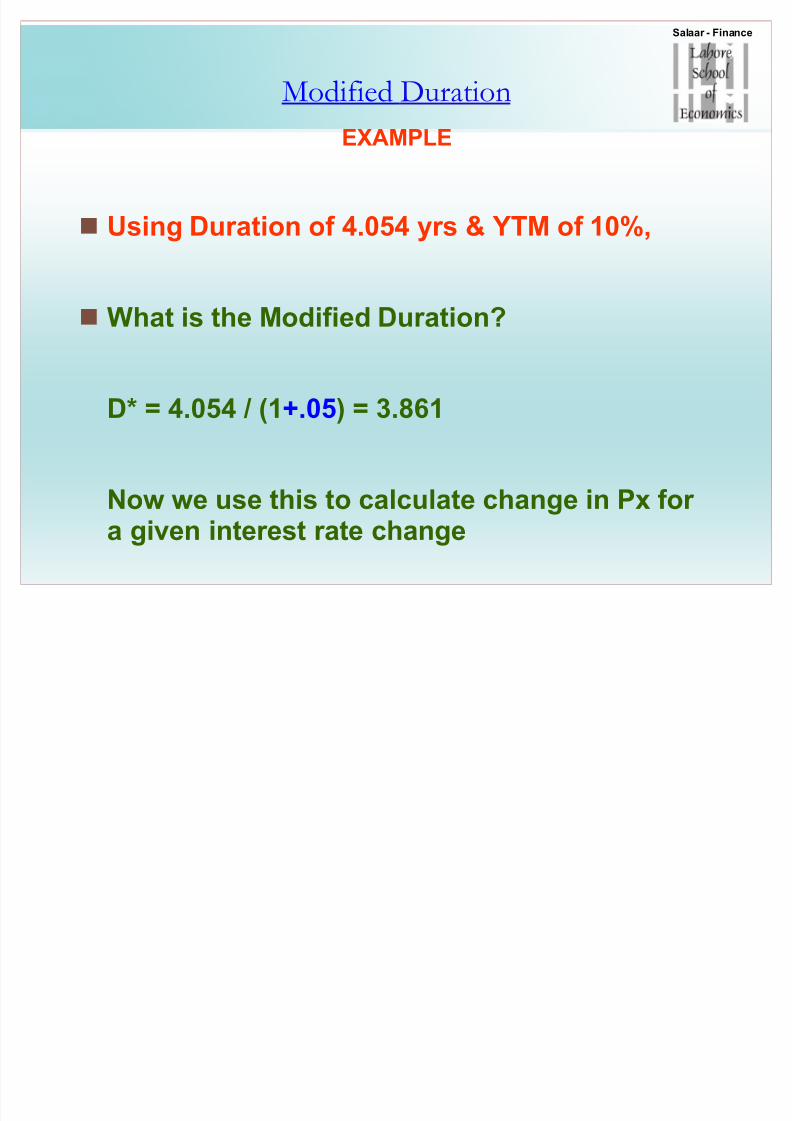

Using Duration of 4.054 yrs & YTM of 10%,

What is the Modified Duration?

Mod D* = D / (1+ytm)

Ytm = semi-annual

Salaar - Finance

M difi d D i

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 111/117

Modified Duration

EXAMPLE

Using Duration of 4.054 yrs & YTM of 10%,

What is the Modified Duration?

D* = 4.054 / (1+.05) = 3.861

Now we use this to calculate change in Px f or a given interest rate change

Salaar - Finance

M difi d D i

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 112/117

Modified Duration

EXAMPLE

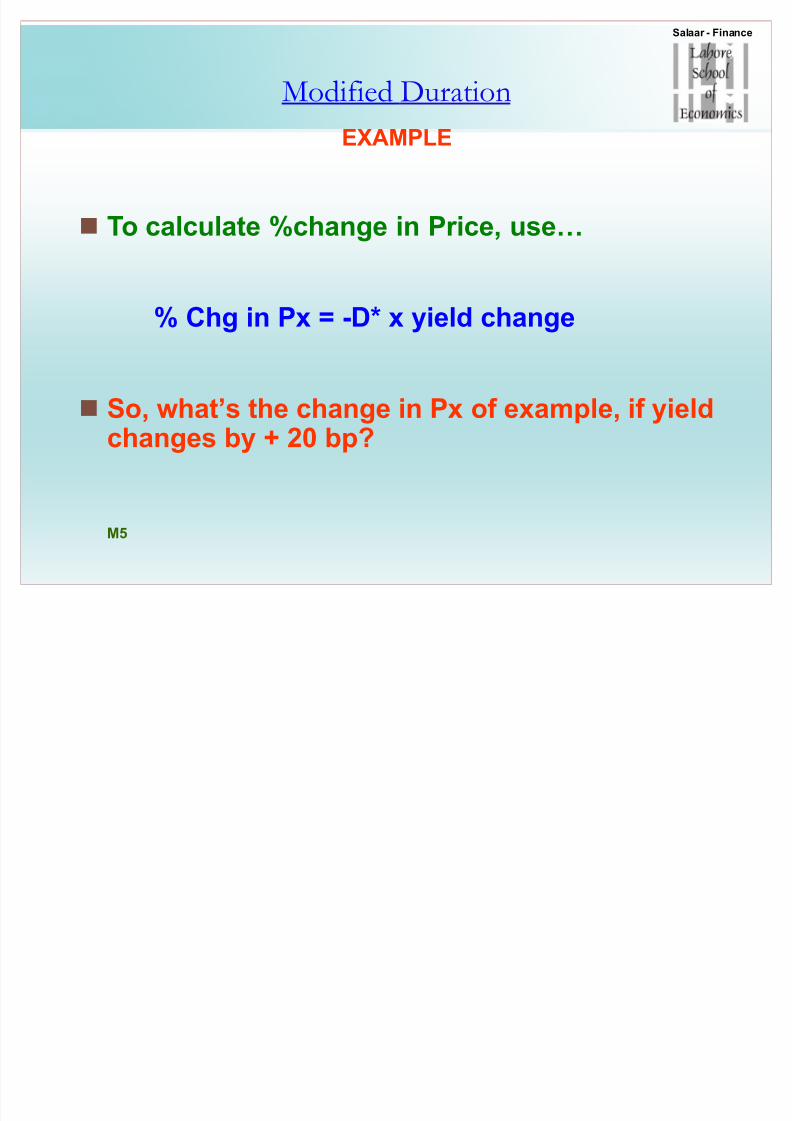

To calculate %change in Price, use«

% Chg in Px = -D* x yield change

So, what¶s the change in Px of example, if yield

changes by + 20 bp?

M5

Salaar - Finance

M difi d D i

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 113/117

Modified Duration

EXAMPLE

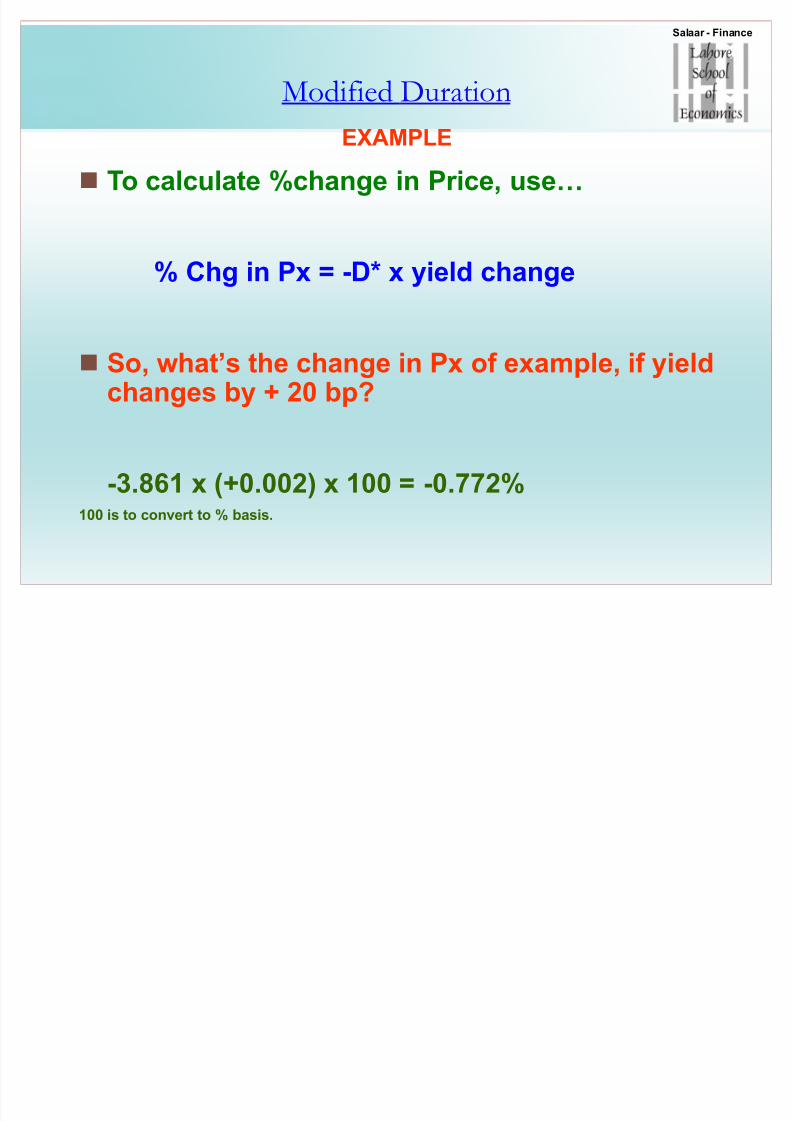

To calculate %change in Price, use«

% Chg in Px = -D* x yield change

So, what¶s the change in Px of example, if yieldchanges by + 20 bp?

-3.861 x (+0.002) x 100 = -0.772%100 is to convert to % basis.

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 114/117

Salaar - Finance

C it

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 115/117

Convexity

rice ro i a ion in ra ion

¡

¢

£

¤

¥ ¦

¥ ¥

¥ §

¥ ̈

¥ ©

¥

¦ ¦ ¦ § ¦ ¦ © ¦ ¦ ¡ ¦ ¦ £ ¦ ¥ ¦ ¥ § ¦ ¥ © ¦ ¥ ¡ ¦ ¥ £ ¦ §

ie l

r i c e

PRICE EST. PRICE

Salaar - Finance

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 116/117

Finance Environment?

OVERVIEW

COVER HERE & Ref Charts

GDP (Equation, components, growth bands, & targets)

Inflation (result of growth)

Interest Rates (tool of central banks, fed funds & principle)

Yield Curve (fisher equation, expected inflation back end)

MARKET DASH BOARD!

Salaar - Finance

Chapter 17

8/7/2019 Ch17Bonds MBA2

http://slidepdf.com/reader/full/ch17bonds-mba2 117/117

p

Bond Yields & Prices

What we have learnt

Bonds & Valuation

Interest rates

Bond Yields

Bond Prices

Bond Price Changes

Duration, Modified Duration & Convexity