Embed Size (px)

DESCRIPTION

CIMA GBC Report - Case Crackers

Citation preview

1

Team Name

CASE CRACKERS

Report Title

CeeCee in the next 5 years

University

Nanyang Technological University

Team members

Chen Xinyi

Lee Wai Hon Gabriel

Liu Xinyi

Yeo Shi Yuan

2

TABLE OF CONTENTS

Page

1. Executive Summary ………………………………………..3

2. Introduction ……………………………………………….. 4

3. Strategic Analysis…………………………………………..5

3.1 Company Analysis

3.2 Industry Analysis

3.3 SWOT analysis

4. Financial Analysis…………………………………………..8

4.1 Financial Ratios

5. Issues Analysis and Recommendations………………..10

5.1 Prioritization of Issues

5.2 Core Competencies Issues

5.2.1 Distributor‟s Strike

5.2.2 Failure of the New Online IT System

5.3 Diversification and Marketing Plans

5.3.1 Celebrity Marketing

5.3.2 Expansion into Jewellery Range

5.4 Child labour accusations

6. Achievability of the five-year plan………………………..22

7. Summary of Issues and Recommendations …………... 23

8. Appendices…………………………………………………24

3

This report aims to prioritise, analyse and evaluate the current issues plaguing

CeeCee. The report begins with a strategic and financial analysis of CeeCee and

the industry. The 4 main issues CeeCee face have been categorized into 2 broad

categories, namely issues that threaten core competencies and plans relating to

expansion and marketing. The issues that threaten core competencies are more

pressing issues that CeeCee should address, given the highly tangible impact

and risks present which will threaten business profitability.

For the first issue regarding the distributor‟s strike, the team recommends that in

the short run, CeeCee should engage an alternative distributor and re-evaluate

their distribution model in the long run. The second issue - failure of the online IT

sales system, can be dealt with by employing an external agency to recover the

debts and improving the controls inherent in the system.

With regards to diversification and marketing plans, CeeCee should implement

the celebrity marketing proposal as the expenses are not substantial in relation to

their sales. However, Kool may not be the best spokesperson for CeeCee. Next,

CeeCee should reject into the second proposal of expansion into the jewellery

range as the proposal is not operationally feasible despite the positive net

present value and the small capital outlay required. The final issue is the ethical

implications from child labour accusations. A moral analysis utilizing the beliefs of

the 6 major ethical systems demonstrated that CeeCee should abide by the law

and discontinue the use of child labour.

Finally, the achievability of the five-year plan is evaluated. After taking into

account the issues plaguing CeeCee, the ending cash balance is positive. Thus,

the five-year plan is feasible. The excess cash balances that CeeCee has can be

further utilized for expansion or other proposals.

1.0 EXECUTIVE SUMMARY

4

CeeCee, founded in 1989, is a high street fashion retailer specializing in trendy

and affordable female fashion. By adopting a just-in-time system for fast

turnarounds with short production runs and limited inventory, CeeCee positions

itself as a trendy and exclusive fashion retailer. Though it only has a market

share of about 15%, it has the highest gross margin at 60.1% compared to its

main competitors.

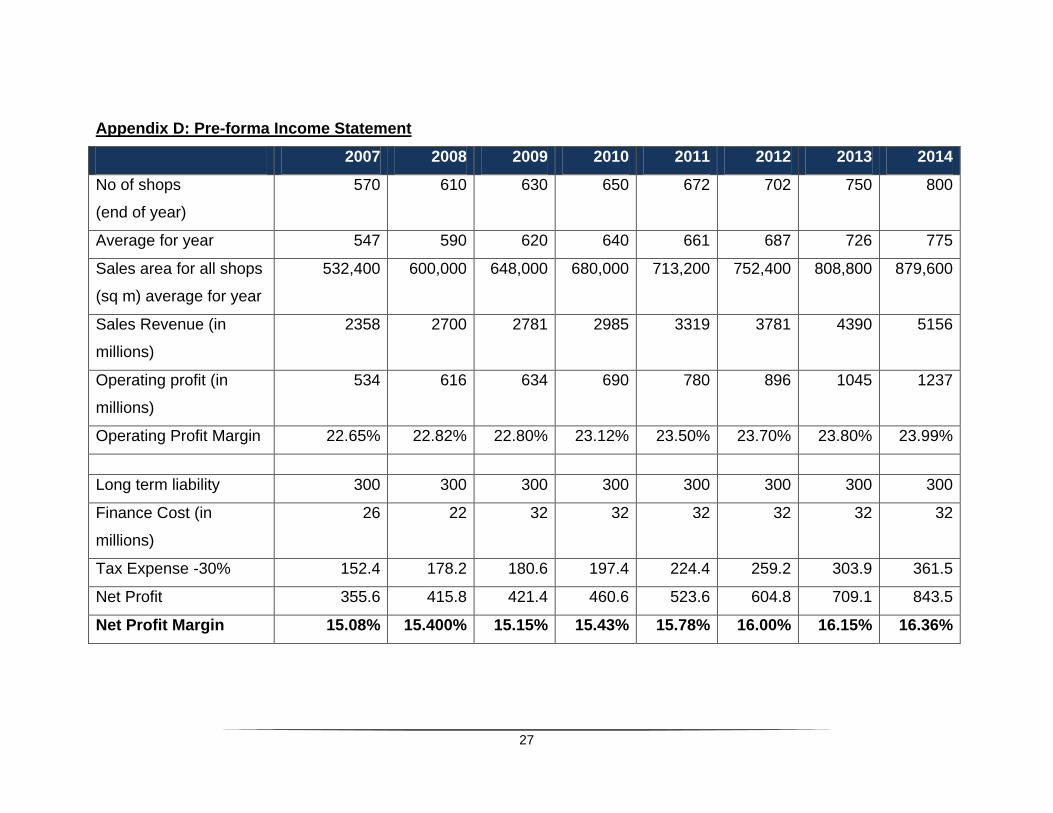

CeeCee has devised a five year plan that will aim to achieve the following

milestones by 2014:

- Number of shops – Increase by 30% to 800 in 2014

- Sales revenue – Increase by 85% to €5156m in 2014

- Operating Profit – Increase by 95% to €1237m in 2014

2.0 INTRODUCTION

5

3.1 Company Analysis

CeeCee has adopted the „fast fashion model‟ to differentiate itself from other

high-street retailers, departmental stores and value retailers and has built a

strong customer base. This model was possible as CeeCee possess core

competencies in the form of short product life cycles and fast creation of new

designs. The model also relies on having a sophisticated IT system and also

remaining in close contact with suppliers.

3.2 Industry Analysis

CeeCee competes in the fashion industry, or more specifically, the high street

fashion retail market.

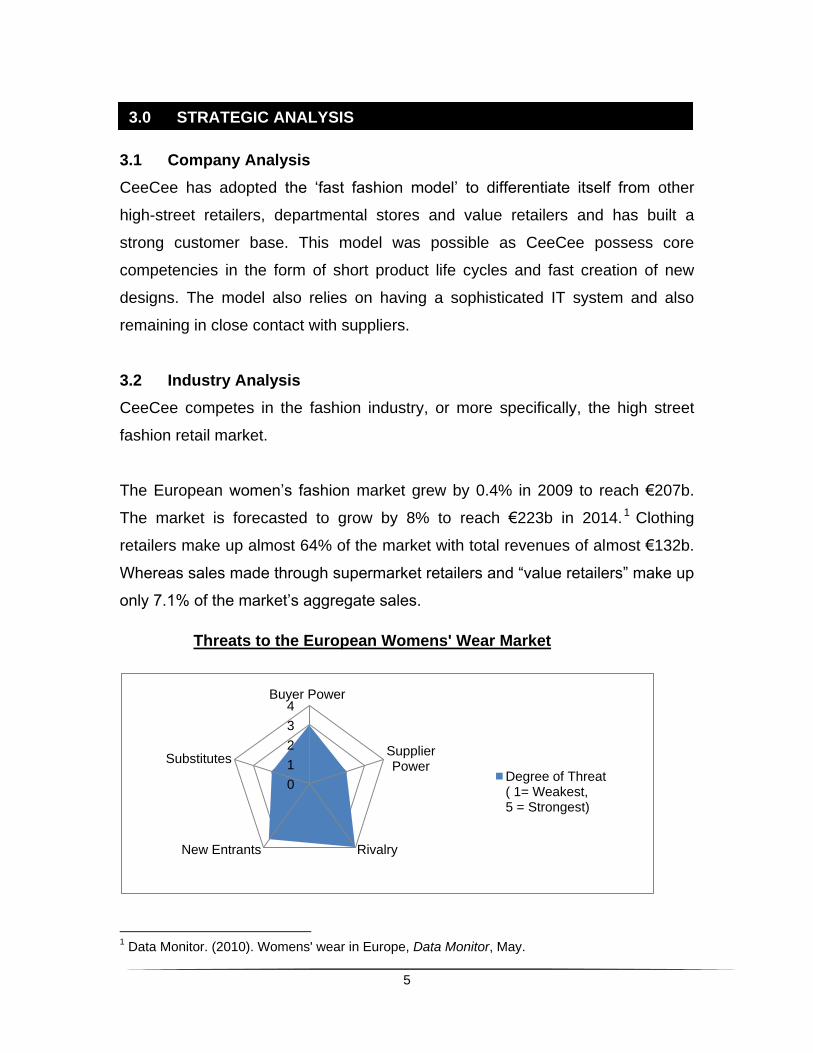

The European women‟s fashion market grew by 0.4% in 2009 to reach €207b.

The market is forecasted to grow by 8% to reach €223b in 2014.1 Clothing

retailers make up almost 64% of the market with total revenues of almost €132b.

Whereas sales made through supermarket retailers and “value retailers” make up

only 7.1% of the market‟s aggregate sales.

1 Data Monitor. (2010). Womens' wear in Europe, Data Monitor, May.

0

1

2

3

4Buyer Power

Supplier Power

RivalryNew Entrants

Substitutes

Degree of Threat ( 1= Weakest, 5 = Strongest)

Threats to the European Womens' Wear Market

3.0 STRATEGIC ANALYSIS

6

Although the European women‟s fashion market is large, it is rather fragmented.

This, combined with the slow growth in 2009, has resulted in strong rivalry

among firms and lowered CeeCee‟s revenue growth to 3%

Buyer’s power – Moderate: Despite fairly low switching costs among retailers,

buying decisions are easily influenced by factors such as social status, branding

and advertising. Hence, this indicates a need to create strong brand awareness

and run intensive advertising campaigns to erode the bargaining power of buyers

and maintain market share.

New entrants and rivalry – Strong: The threat of new entrants is high because

of the lack of barriers of entry. Given that the market is growing, new entrants are

expected to enter and compete on similar products. As existing players are also

increasingly aggressive in their product offering and branding, the rivalry in the

industry is definitely strong.

3.3 SWOT Analysis

SWOT Analysis

Strengths

- Fast turnarounds of fashion designs

- Close contact with manufacturers

- Sophisticated IT systems

- Short product life cycle

- Prime location of shops

- Visually appealing store and

window layouts

- Brand loyalty

- Good Management staff

Weaknesses

- Heavily focused on ladies fashion

- Does not engage in aggressive

marketing and advertising

- Short term financials

- Large number of suppliers

- Moderately high amount of unsold

goods

7

Opportunities

- High gross margins for accessories

- Fast growing markets in Eastern

Europe and Asia

- Online shopping market

Threats

- Increased competition from „value

retailers‟

- Price sensitive customers

As CeeCee has numerous strength and opportunities especially in the area of

accessories, a diversification strategy which entails offering new and different

products could be employed.

However, CeeCee also needs to carefully balance the potential threats to its

current business. Since the women‟s fashion business constitutes the majority of

its revenue, it should build up its strength to reduce its vulnerability to external

threats. It should seek to enhance brand consciousness and loyalty in order to

retain market share as it faces stiff competition.

Therefore, CeeCee‟s priorities would be to be first focus on strengthening its

current women‟s fashion business, and at the same time, explore ways to

diversify its product offerings.

8

4.1 Financial ratios

Profitability and Operating Margin

Ratios 2008 2007

Operating Return of Assets (ROA) 36.9% 38.7%

Financial Leverage Gain 4.4% 6.1%

Return of Equity 41.3% 44.8%

NOPAT Margin 15.4% 15.1%

CeeCee‟s ROA ratio indicates that it has high profitability in its operations. Its

high ROE ratios are mainly contributed by its profitable operations rather than

from the financial leverage gain. This high profitability is likely due to their low

manufacturing cost established through strong manufacturing networks and

distribution channels. The NOPAT margin of about 15% reflects that CeeCee has

performed well in terms of its operations.

Investment Management

Ratios 2008 2007

Operating working capital -€323m -€317m

Operating working capital turnover -8.36 -7.44

CeeCee‟s operating working capital is negative, highlighting a large amount of

current liabilities (exclude current debt) compared to current assets. Even when

cash holdings are included, CeeCee still falls short of fulfilling their short term

obligations. Hence, there is high likelihood that CeeCee will face cash flow

problems.

4.0 FINANCIAL ANALYSIS

9

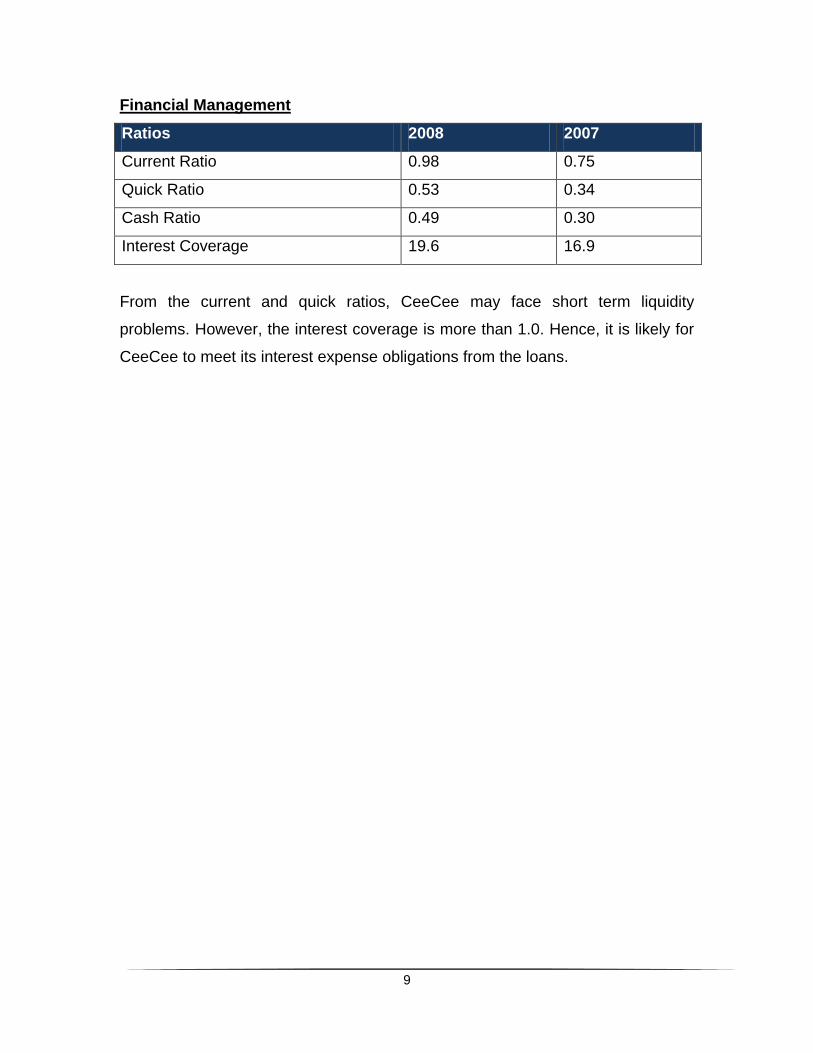

Financial Management

Ratios 2008 2007

Current Ratio 0.98 0.75

Quick Ratio 0.53 0.34

Cash Ratio 0.49 0.30

Interest Coverage 19.6 16.9

From the current and quick ratios, CeeCee may face short term liquidity

problems. However, the interest coverage is more than 1.0. Hence, it is likely for

CeeCee to meet its interest expense obligations from the loans.

10

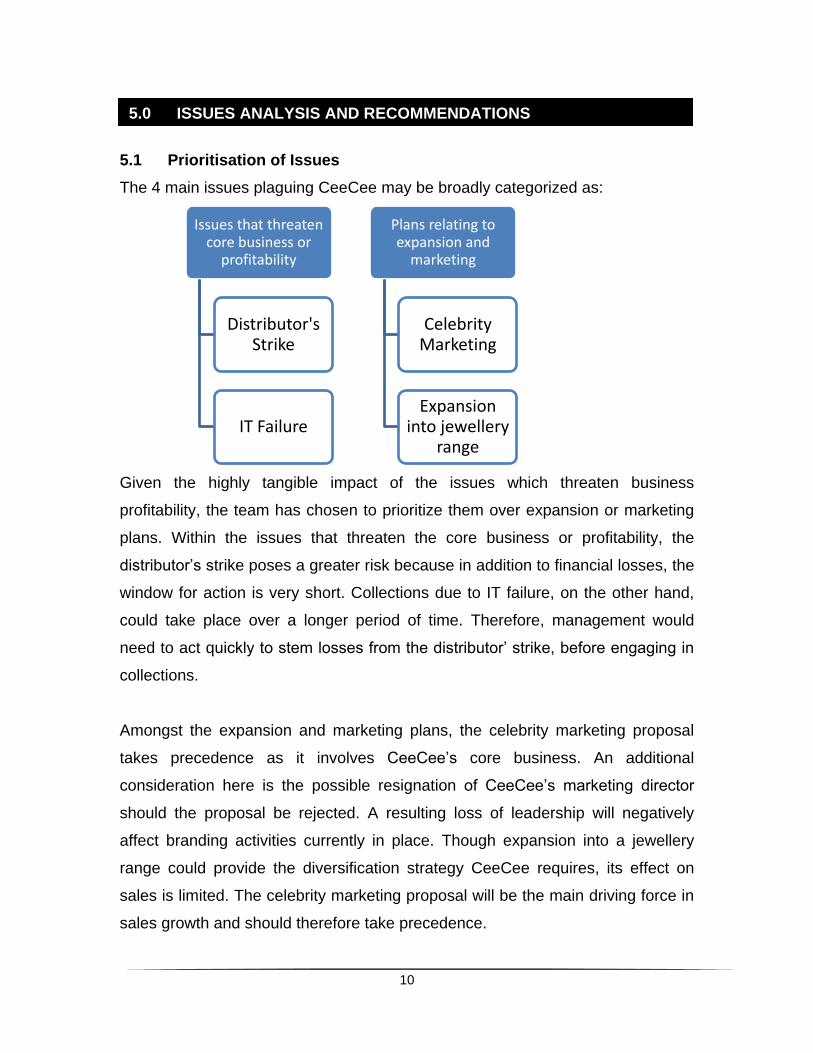

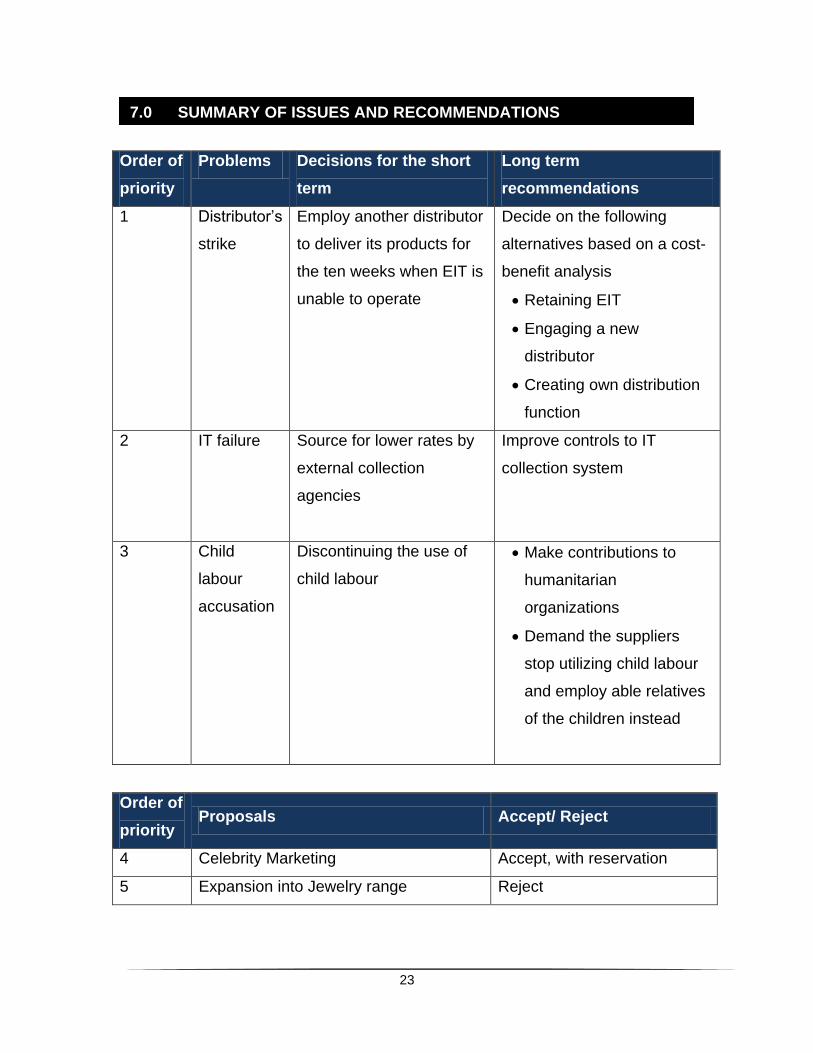

5.1 Prioritisation of Issues

The 4 main issues plaguing CeeCee may be broadly categorized as:

Given the highly tangible impact of the issues which threaten business

profitability, the team has chosen to prioritize them over expansion or marketing

plans. Within the issues that threaten the core business or profitability, the

distributor‟s strike poses a greater risk because in addition to financial losses, the

window for action is very short. Collections due to IT failure, on the other hand,

could take place over a longer period of time. Therefore, management would

need to act quickly to stem losses from the distributor‟ strike, before engaging in

collections.

Amongst the expansion and marketing plans, the celebrity marketing proposal

takes precedence as it involves CeeCee‟s core business. An additional

consideration here is the possible resignation of CeeCee‟s marketing director

should the proposal be rejected. A resulting loss of leadership will negatively

affect branding activities currently in place. Though expansion into a jewellery

range could provide the diversification strategy CeeCee requires, its effect on

sales is limited. The celebrity marketing proposal will be the main driving force in

sales growth and should therefore take precedence.

Issues that threaten core business or

profitability

Distributor's Strike

IT Failure

Plans relating to expansion and

marketing

Celebrity Marketing

Expansion into jewellery

range

5.0 ISSUES ANALYSIS AND RECOMMENDATIONS

11

5.2 Core Competencies Issues

5.2.1 Distributor’s strike

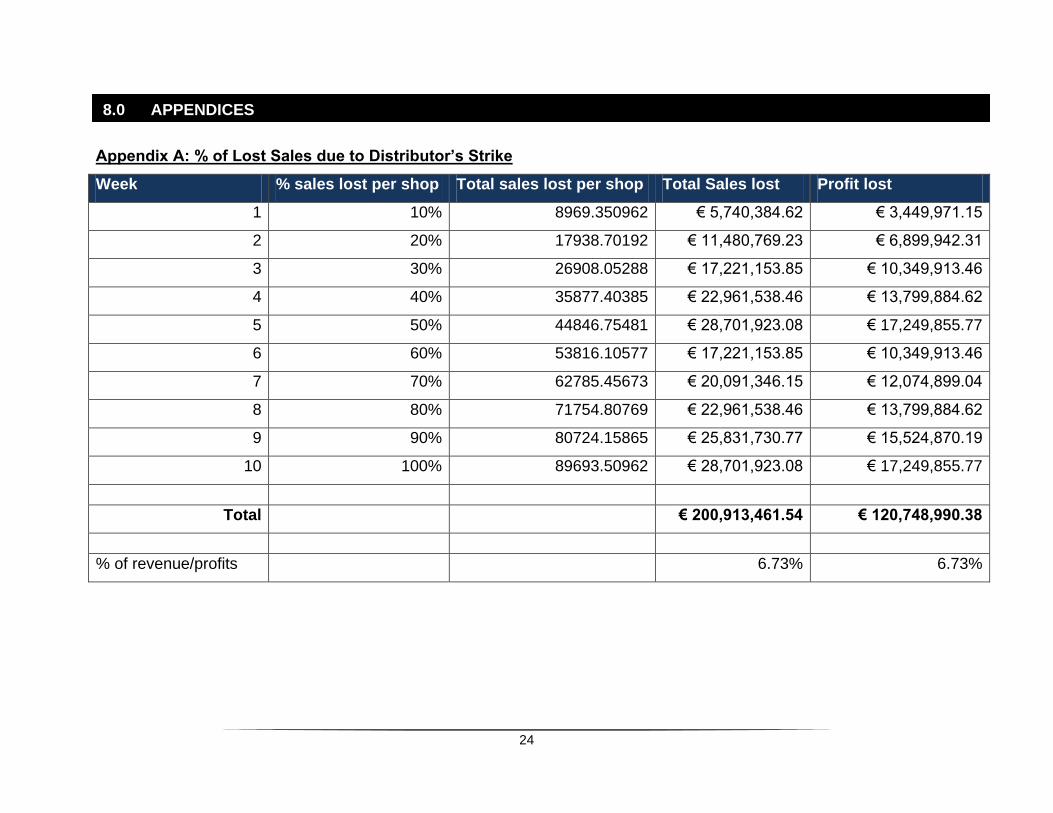

Financial impact

Due to the union-led strike in EIT, severe disruptions of deliveries to stores are

expected. Sales revenue and profits for 2010 is expected to be reduced by 6.73%

as a result of the lost sales from lack of deliveries to CeeCee shops2.

Strategic impact

The distributor‟s strike will affect CeeCee‟s fast fashion concept, which relies on

the fast creation and supply to shops. This highlights the dependence of CeeCee

on a single distributor which may expose CeeCee‟s business model to

uncontrollable risks. Furthermore, the fact that EIT is a unionized business in the

European sphere, which has pro-labour laws, also raises concerns about future

disruptions to deliveries.

Reputational impact

The lack of new goods delivered to CeeCee stores may affect its reputation as

one of the fastest retailer of trendy styles. Customers may be disappointed when

expectations of new styles appearing in CeeCee stores are not fulfilled. This may

lead to a reduction in customer base as customers turn to other fashion stores for

trendy designs.

Assessment of Potential solutions

Engaging an alternative Distributor temporarily

CeeCee should source for and engage an alternative distributor immediately to

deliver product from the large distribution centre in Northern Europe to the

various shops. A short term contract for the deliveries can be signed for the

duration of the ten weeks in which the strike occurs to prevent further disruption

of deliveries.

2 Refer to Appendix A

12

The company should be prepared for higher costs of distribution due to the

immediate need of a new distributor and be prepared for slower delivery time as

the new distributor may not be as familiar with CeeCee‟s model.

Re-evaluate distribution model and change to a new distributor

CeeCee can also re-evaluate its distribution model and consider changing to one

or more new distributors permanently. CeeCee can try to reduce its dependency

of its distribution on EIT by sourcing for other more reliable distributors in the

region. This will reduce the risk of disruption to deliveries due to the disruption of

operations of any one distributor.

CeeCee should be prepared to take some time in sourcing for new distributors

and do a cost-benefit analysis.

Develop In-house distribution capabilities

Another option for CeeCee is to build its own distribution capabilities instead of

outsourcing. This can reduce CeeCee‟s dependency and increase efficiency.

However, this may be time consuming and requires expertise that CeeCee does

not currently have. High startup costs may be required (to acquire delivery trucks)

and develop its distribution and logistics IT system.

Recommendations

Short-term

To solve the immediate problem, CeeCee should engage a reliable alternative

distributor for the ten weeks. The Head of Logistics, Jim Bold, should be

responsible for sourcing for a temporary distributor immediately, together with the

Finance director. A suitable distributor with the relevant experience and capacity

and the most reasonable quotation should be identified and contracted within the

first week of the strike.

13

Long-term

During the ten weeks, a thorough evaluation of EIT should be done to determine

if CeeCee should continue its partnership with EIT, select new distributors or to

build in-house distribution capabilities. A special task team should be set up to

evaluate this issue with the Head of logistics, Jim Bold, and the Finance director,

Diane Innes, to lead the team. A cost-benefit analysis of using new distributors or

creating its own distribution function should also be done to aid the decision. If a

decision to use a new distributor is made, the team should be tasked with

sourcing for new distributors and negotiating the new contracts.

5.2.2 Failure of the new online IT sales system

Financial Impact

As the issue had gone on for 3 months before detection by the external audit

team, the total estimated loss in revenue stands at €6,000,0003 before taking into

account the amounts that CeeCee may be able to recover.

Strategic Impact

As CeeCee seeks to tap on growing market opportunity and trend towards online

retail, it is crucial for it to have an efficient online sales system that provides

customers with a smooth-sailing shopping experience. Failure to collect

customers‟ payments may deter CeeCee from moving towards online retail. This

may cause CeeCee to lose out on opportunities of direct Internet selling as more

customers prefer shopping in the comfort of their homes, as with the case in

Levis Strauss when they discontinued their online sales in 1999, with one of its

reasons being the complications arising from payment processes.

Assessment of Potential solutions

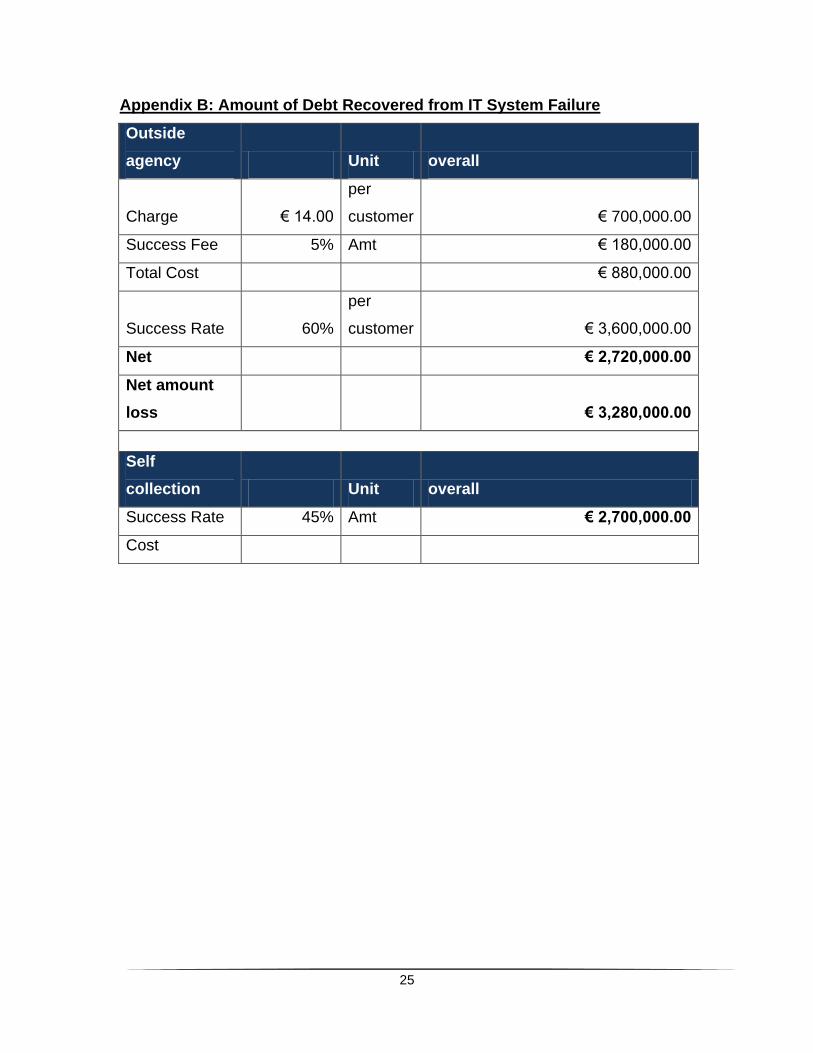

Collection of amounts by external collection agency

One of the potential solutions is to employ a collection agency to recover the debt

amounts at a charge of €14 per customer and a success fee of 5% of the 3 Refer to Appendix B

14

amounts recovered. CeeCee anticipates that a higher percentage of the money,

60%, will be recovered by using an external collection agency.

By looking at the financial figures, it seems that CeeCee should employ an

external agency to recover the amounts, given that the net amount collected after

deducting charges is €20,000 higher than via the finance department.

However, considering a broader view, factors like reputation might be important

to CeeCee as it seeks to establish its brand name. The external agency will be

establishing relationships with CeeCee‟s customers and it could be potentially

harmful if they sour that relationship by not dealing with invoices in a courteous,

diplomatic and professional manner which protects customer private information.

Therefore, it is important that CeeCee selects a reputable collection agency

should it decide to outsource the collection.

Collection of amounts by CeeCee’s finance department

An alternative solution is for CeeCee‟s finance department to collect the money

itself. However, the department reckons that only 45% of the money will be

recovered by its already overstretched staff. We recommend CeeCee‟s

management to not take this figure at face value and investigate whether it is

indeed the case that the department is overstretched given the large gulf (25%

lesser compared to external vendor) between the success rates.

Nevertheless, based on the facts of the case, using an external agency would be

the superior solution.

Recommendations

Short-term

In the short run, CeeCee would want to recover as much money as possible. The

finance department should be responsible for sourcing for a reputable collection

agency that charges lower collection fees than costs incurred if CeeCee collect

15

the amounts itself. This ensures cost efficiency and allows CeeCee to

concentrate her resources on her other proposals.

Long-term

The more pertinent issue in the long run is the implementation of controls to

prevent future system lapses. CeeCee and ProveIT should conduct a meeting to

review its payment and processing controls. The IT director, Roberta Downs,

should review the contract and establish a Service Level Agreement with ProveIT,

with specific terms to ensure CeeCee will not succumb to such errors again.

CeeCee should include the amount of compensation it will receive from ProveIT

should there be any amounts uncollected. Downs can also implement more

robust error handling and reporting systems. As Downs only intends to stay in

CeeCee for no longer than five years, the IT team should be involved in the

contract discussion and control processes should be documented thoroughly to

prevent any loss of information should Downs eventually leave CeeCee.

5.3 Diversification and Marketing Plans

5.3.1 Celebrity Marketing

Background

Juliette Lespere (Sales and Marketing Director) is considering using celebrity

marketing. She has strong belief celebrity endorsements will create a more

visible CeeCee brand. She proposes that CeeCee engages with Kool, a popular

European singer of rock music.

Factors Proposal Intends to Achieve

Increased visibility of CeeCee’s brand

With links to an iconic artist, more people will be convinced that CeeCee is

indeed a brand that celebrities endorse and purchase. Given that clothing is

easily influenced by factors such as social status, branding and advertising, this

will convince more people that CeeCee is an iconic high street brand.

16

Meet sales forecast

In order to meet the sales forecast for next five years, intensive marketing and

advertising will be required. By 2014, CeeCee expects sales growth to increase

by 85% to €5,156m. Such targets can partly be achieved by the use of more

visible marketing.

Endorsement of Juliette’s work

Compared to many high street retailers which have a marketing budget of about

3-4% of sales revenue, CeeCee‟s budget was only 0.5%. Juliette may feel rather

disgruntled that she does not have a large enough budget to spend on marketing

programs. Thus, Juliette may use this proposal to test whether she has the

support of Carla Celli.

Factors affecting the proposal

Dilution of CeeCee’s brand

CeeCee has long been considered a brand offering trendy and affordable

clothing. As it is the first time that CeeCee is engaging in celebrity marketing, it

has to be careful that the marketing message is well positioned. There will be a

message incongruence given that Kool‟s “rock star” image does not fit well with

CeeCee‟s young, female consumers. Therefore it is proposed that CeeCee

instead engage trendy female celebrities such as Kiera Knightley and Emma

Watson.

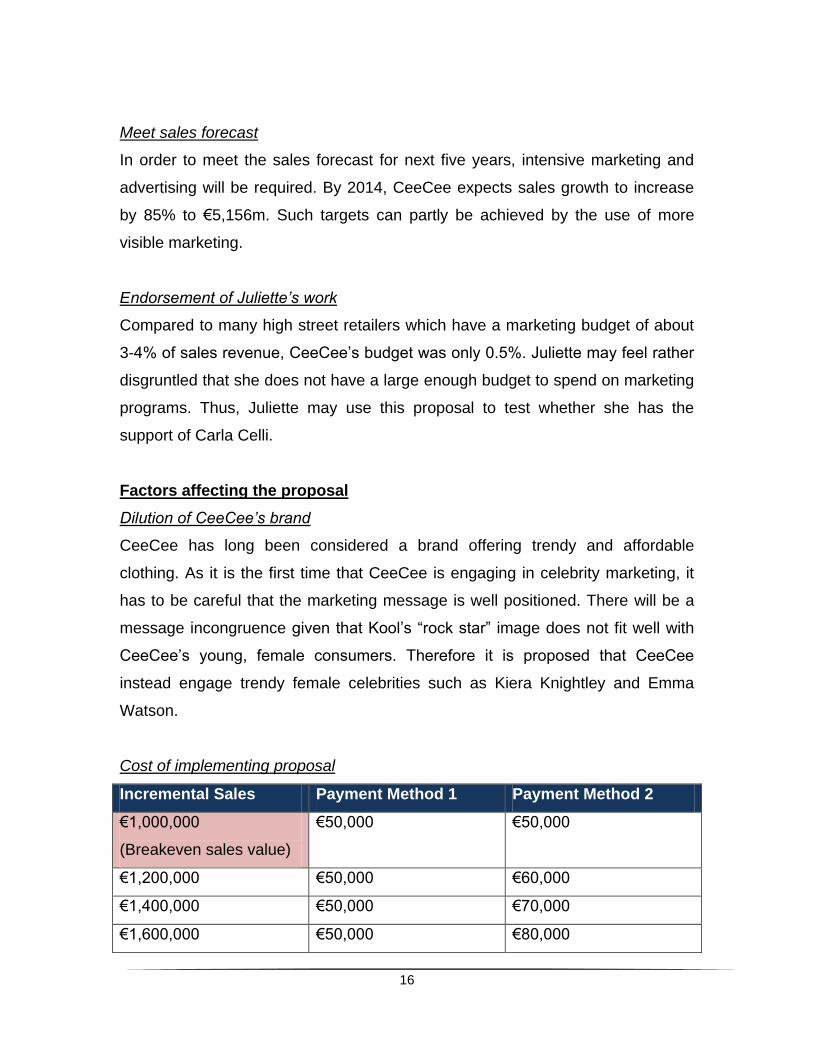

Cost of implementing proposal

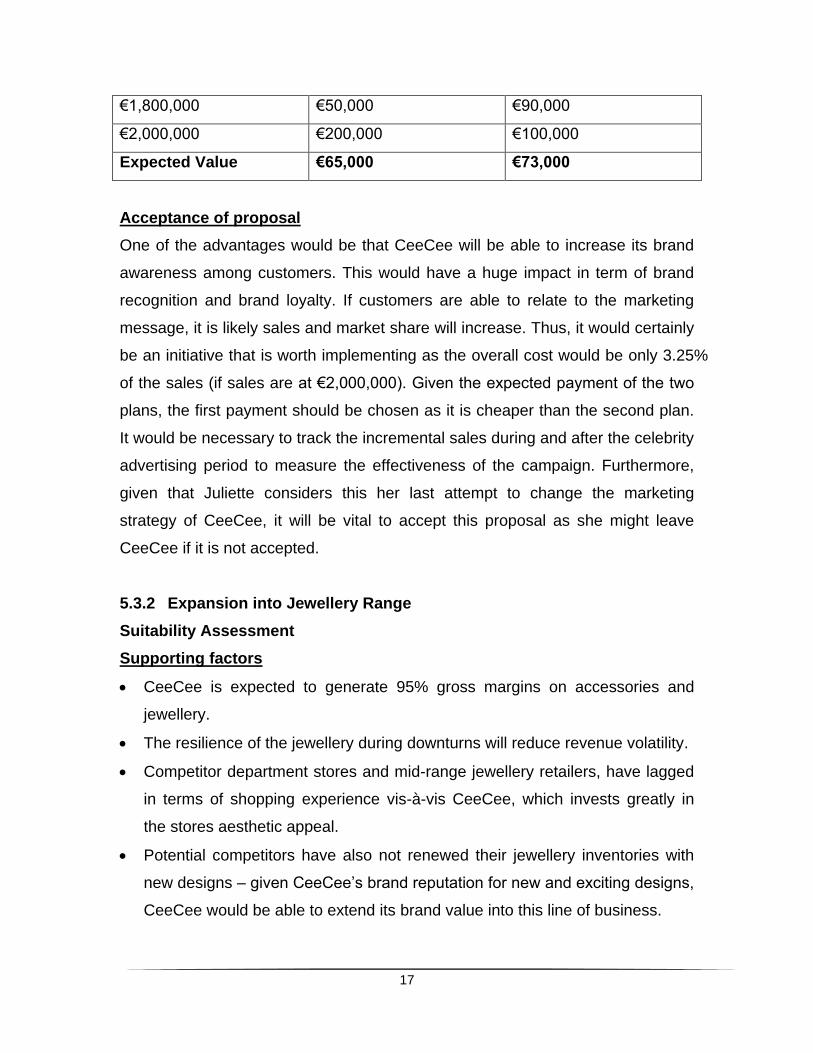

Incremental Sales Payment Method 1 Payment Method 2

€1,000,000

(Breakeven sales value)

€50,000 €50,000

€1,200,000 €50,000 €60,000

€1,400,000 €50,000 €70,000

€1,600,000 €50,000 €80,000

17

€1,800,000 €50,000 €90,000

€2,000,000 €200,000 €100,000

Expected Value €65,000 €73,000

Acceptance of proposal

One of the advantages would be that CeeCee will be able to increase its brand

awareness among customers. This would have a huge impact in term of brand

recognition and brand loyalty. If customers are able to relate to the marketing

message, it is likely sales and market share will increase. Thus, it would certainly

be an initiative that is worth implementing as the overall cost would be only 3.25%

of the sales (if sales are at €2,000,000). Given the expected payment of the two

plans, the first payment should be chosen as it is cheaper than the second plan.

It would be necessary to track the incremental sales during and after the celebrity

advertising period to measure the effectiveness of the campaign. Furthermore,

given that Juliette considers this her last attempt to change the marketing

strategy of CeeCee, it will be vital to accept this proposal as she might leave

CeeCee if it is not accepted.

5.3.2 Expansion into Jewellery Range

Suitability Assessment

Supporting factors

CeeCee is expected to generate 95% gross margins on accessories and

jewellery.

The resilience of the jewellery during downturns will reduce revenue volatility.

Competitor department stores and mid-range jewellery retailers, have lagged

in terms of shopping experience vis-à-vis CeeCee, which invests greatly in

the stores aesthetic appeal.

Potential competitors have also not renewed their jewellery inventories with

new designs – given CeeCee‟s brand reputation for new and exciting designs,

CeeCee would be able to extend its brand value into this line of business.

18

Within consumer discretionary goods, exclusivity is an important buying

consideration – CeeCee‟s tradition of only producing limited numbers of a

certain design will allow the firm to provide higher markups for its jewellery

pieces.

Carla Celli and Juliette Lespere are both keen on expanding the jewellery line.

Should the proposal for celebrity marketing not be implemented, Carla may

suggest for Juliette to focus instead on launching this business line in order to

retain her interest in working for the firm.

Risks/Costs Factors

One risk is that precious metal prices are expected to increase due to excess

liquidity in a low interest rate environment. This would increase costs of

manufacturing beyond budgeted. In addition, reduction in discretionary spending

amongst consumers as Europe emerges from the global financial crisis may

negatively affect projected revenues.

Acceptability Assessment

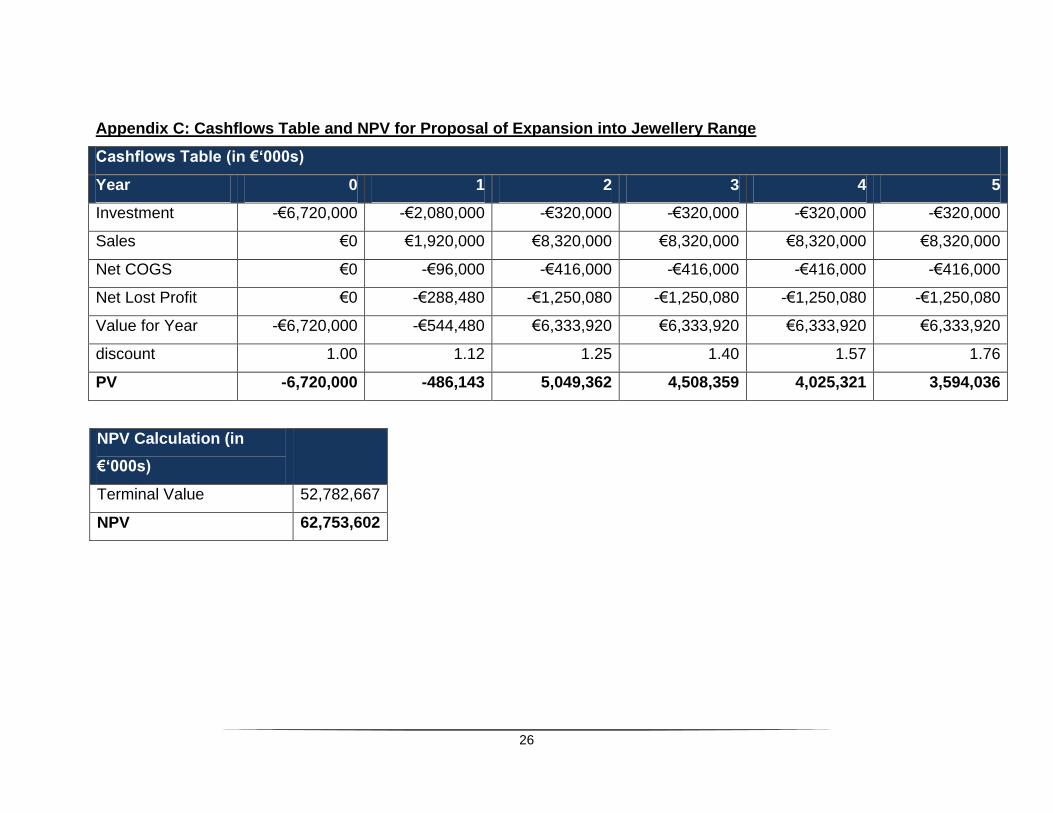

To assess the returns project, we utilize the NPV method by projecting cash flow

for the project lifespan.

Given that NPV, €62,753,6024 > 0, it may be concluded that the project is worth

undertaking. Shareholder risk is minimized as project is expected to start

internally financing itself in the T+1 years.

Feasibility Assessment

Given CeeCee‟s large cash reserves, it is expected that the jewellery expansion

project will be financed from cash holdings. As it stands, the capital outlay

required is 0.6% of cash reserves, which will not significantly impact CeeCee‟s

short term liquidity.

4 Refer to Appendix C

19

However, it is recognized that the proposal is operationally difficult to implement

and risky:

1. Disruption of CeeCee‟s business due to renovation

2. Insufficient transferrable competences to ensure business survival –

particularly in the areas of design, logistics and branding.

Recommendation

Based on the above assessments, this proposal should be rejected. This is due

to the poor business viability that a jewellery line has for CeCee.

However, should CeeCee choose to pursue this business, we believe the best

method would be to acquire a jewellery chain, financed from CeeCee‟s large

cash reserves, to acquire required competences.

5.4 Child labour accusations

Background

CeeCee‟s Asian suppliers have been using child labour to manufacture garments

for CeeCee. The agent believes that the issue is commonly reported that

newspapers have grown bored and CeeCee would not be able to do much.

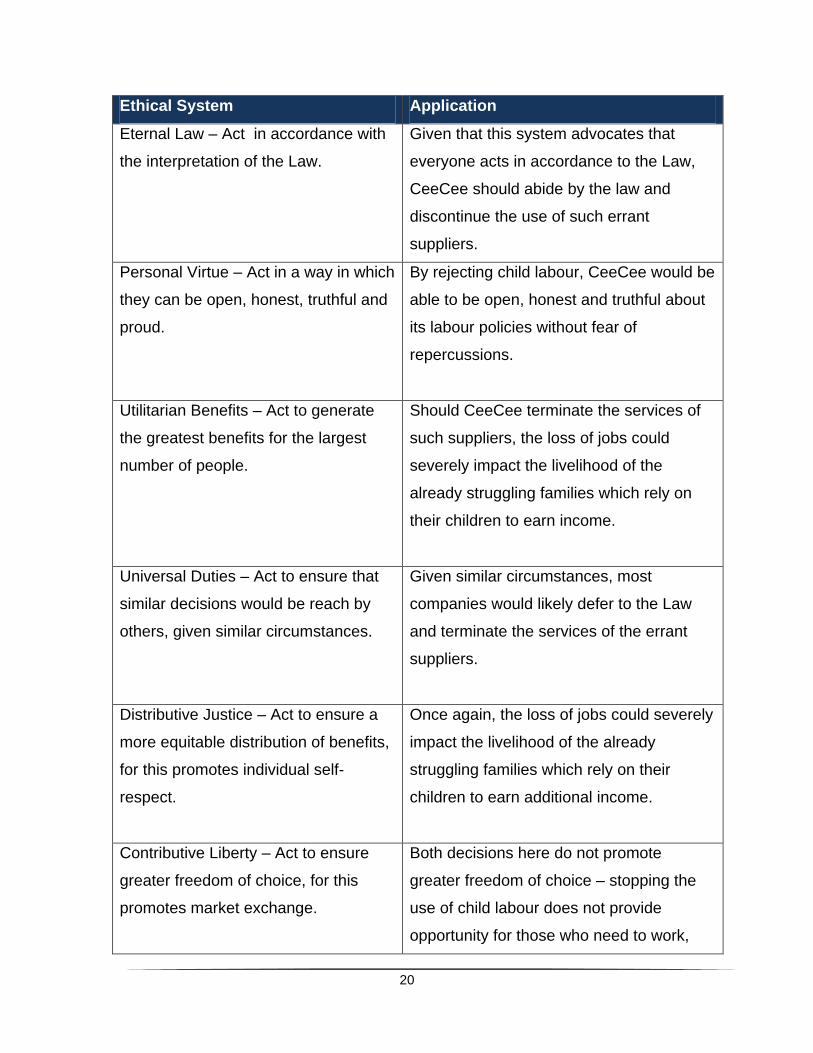

Dilemma

CeeCee faces an ethical tradeoff between severing the contract with Asian

suppliers using child labour – potentially costing the children‟s families who face

financial difficulties, or violating child labour laws – which represent the moral

consensus of society at large. To perform this moral analysis, the beliefs of the 6

major ethical systems is utilized.

20

Ethical System Application

Eternal Law – Act in accordance with

the interpretation of the Law.

Given that this system advocates that

everyone acts in accordance to the Law,

CeeCee should abide by the law and

discontinue the use of such errant

suppliers.

Personal Virtue – Act in a way in which

they can be open, honest, truthful and

proud.

By rejecting child labour, CeeCee would be

able to be open, honest and truthful about

its labour policies without fear of

repercussions.

Utilitarian Benefits – Act to generate

the greatest benefits for the largest

number of people.

Should CeeCee terminate the services of

such suppliers, the loss of jobs could

severely impact the livelihood of the

already struggling families which rely on

their children to earn income.

Universal Duties – Act to ensure that

similar decisions would be reach by

others, given similar circumstances.

Given similar circumstances, most

companies would likely defer to the Law

and terminate the services of the errant

suppliers.

Distributive Justice – Act to ensure a

more equitable distribution of benefits,

for this promotes individual self-

respect.

Once again, the loss of jobs could severely

impact the livelihood of the already

struggling families which rely on their

children to earn additional income.

Contributive Liberty – Act to ensure

greater freedom of choice, for this

promotes market exchange.

Both decisions here do not promote

greater freedom of choice – stopping the

use of child labour does not provide

opportunity for those who need to work,

21

while continuing the use does not allow

children to choose their working conditions.

Recommendations

Based on the above moral analysis, CeeCee shoud abide by the law and

discontinue the use of child labour. To mitigate the ramifications of this decision,

CeeCee can choose to:

Make contributions to humanitarian organizations specializing in helping

children born into poverty

Demand the suppliers stop utilizing child labour and employ able relatives

of the children instead

22

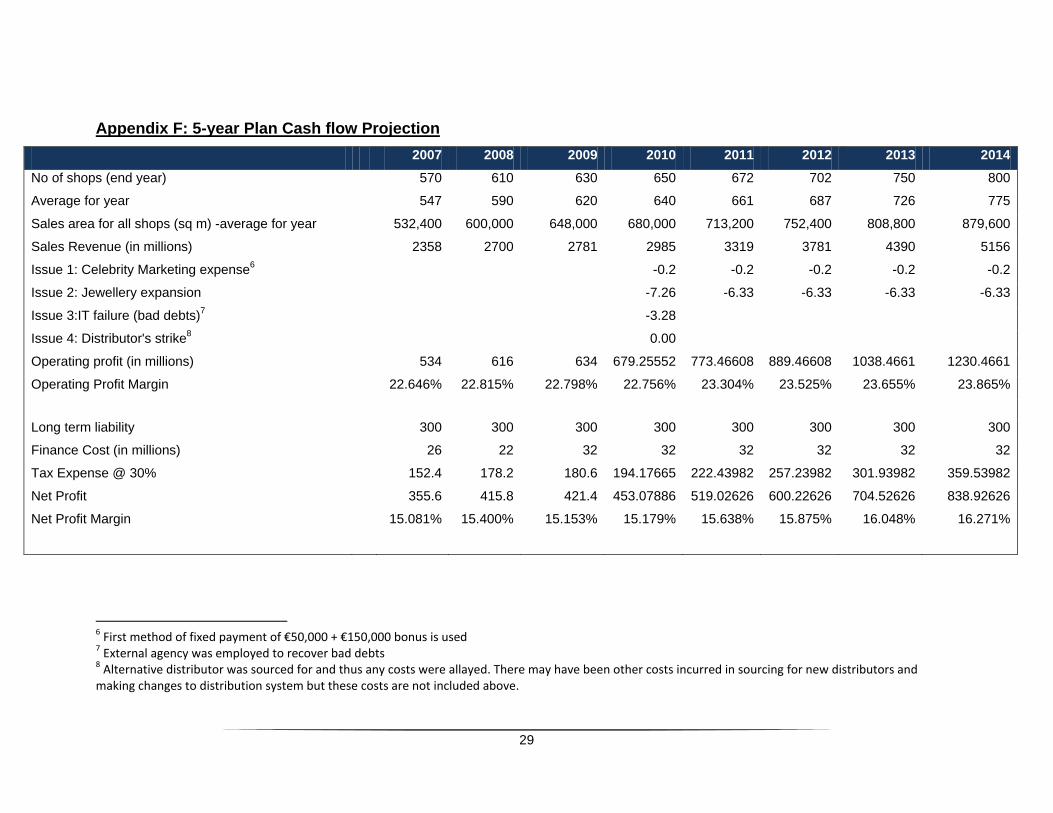

Based on the cash flow position derived from the forecasted figures for 2011 to

2014, the five year plan is financially feasible. CeeCee ends on a net positive

cash flow position at the end of each year and the cash flows increase as

forecasted profits increase. The cash flow position is net positive even when

basic costs for the short term recommendations of the five issues are included5.

The year on year growth rates forecasted increases from 7.34% to 17.45% for

revenues and 7.14% to 18.49% for operating profits, with operating margin

remaining relatively constant. This gradual increase in revenue and profit growth

is consistent with past trends. Sales revenue grew 14.5% in year 2008 and

decreased drastically to 3% in 2009 due to the financial crisis. We expect the

economy to gradually recover till it exceeds its previous levels in the next five

years as we proceed with the marketing plans for CeeCee.

Nevertheless, CeeCee should be prepared for unforeseen events which may

depress its earnings and affect its cash flow positions. With its low current ratios,

CeeCee would be more vulnerable to cash flow fluctuations. CeeCee should

maintain a monthly cash flow forecast to ensure that its cash positions remain

viable in each individual month and be prepared for any contingencies.

5 Refer to Appendix F

6.0 ACHIEVABILITY OF THE FIVE-YEAR PLAN

23

Order of

priority

Problems Decisions for the short

term

Long term

recommendations

1 Distributor‟s

strike

Employ another distributor

to deliver its products for

the ten weeks when EIT is

unable to operate

Decide on the following

alternatives based on a cost-

benefit analysis

Retaining EIT

Engaging a new

distributor

Creating own distribution

function

2 IT failure Source for lower rates by

external collection

agencies

Improve controls to IT

collection system

3 Child

labour

accusation

Discontinuing the use of

child labour

Make contributions to

humanitarian

organizations

Demand the suppliers

stop utilizing child labour

and employ able relatives

of the children instead

Order of

priority Proposals Accept/ Reject

4 Celebrity Marketing Accept, with reservation

5 Expansion into Jewelry range Reject

7.0 SUMMARY OF ISSUES AND RECOMMENDATIONS

24

Appendix A: % of Lost Sales due to Distributor’s Strike

Week % sales lost per shop Total sales lost per shop Total Sales lost Profit lost

1 10% 8969.350962 € 5,740,384.62 € 3,449,971.15

2 20% 17938.70192 € 11,480,769.23 € 6,899,942.31

3 30% 26908.05288 € 17,221,153.85 € 10,349,913.46

4 40% 35877.40385 € 22,961,538.46 € 13,799,884.62

5 50% 44846.75481 € 28,701,923.08 € 17,249,855.77

6 60% 53816.10577 € 17,221,153.85 € 10,349,913.46

7 70% 62785.45673 € 20,091,346.15 € 12,074,899.04

8 80% 71754.80769 € 22,961,538.46 € 13,799,884.62

9 90% 80724.15865 € 25,831,730.77 € 15,524,870.19

10 100% 89693.50962 € 28,701,923.08 € 17,249,855.77

Total

€ 200,913,461.54 € 120,748,990.38

% of revenue/profits

6.73% 6.73%

8.0 APPENDICES

25

Appendix B: Amount of Debt Recovered from IT System Failure

Outside

agency Unit overall

Charge € 14.00

per

customer € 700,000.00

Success Fee 5% Amt € 180,000.00

Total Cost

€ 880,000.00

Success Rate 60%

per

customer € 3,600,000.00

Net

€ 2,720,000.00

Net amount

loss

€ 3,280,000.00

Self

collection Unit overall

Success Rate 45% Amt € 2,700,000.00

Cost

26

Appendix C: Cashflows Table and NPV for Proposal of Expansion into Jewellery Range

Cashflows Table (in €‘000s)

Year 0 1 2 3 4 5

Investment -€6,720,000 -€2,080,000 -€320,000 -€320,000 -€320,000 -€320,000

Sales €0 €1,920,000 €8,320,000 €8,320,000 €8,320,000 €8,320,000

Net COGS €0 -€96,000 -€416,000 -€416,000 -€416,000 -€416,000

Net Lost Profit €0 -€288,480 -€1,250,080 -€1,250,080 -€1,250,080 -€1,250,080

Value for Year -€6,720,000 -€544,480 €6,333,920 €6,333,920 €6,333,920 €6,333,920

discount 1.00 1.12 1.25 1.40 1.57 1.76

PV -6,720,000 -486,143 5,049,362 4,508,359 4,025,321 3,594,036

NPV Calculation (in

€‘000s)

Terminal Value 52,782,667

NPV 62,753,602

27

Appendix D: Pre-forma Income Statement

2007 2008 2009 2010 2011 2012 2013 2014

No of shops

(end of year)

570 610 630 650 672 702 750 800

Average for year 547 590 620 640 661 687 726 775

Sales area for all shops

(sq m) average for year

532,400 600,000 648,000 680,000 713,200 752,400 808,800 879,600

Sales Revenue (in

millions)

2358 2700 2781 2985 3319 3781 4390 5156

Operating profit (in

millions)

534 616 634 690 780 896 1045 1237

Operating Profit Margin 22.65% 22.82% 22.80% 23.12% 23.50% 23.70% 23.80% 23.99%

Long term liability 300 300 300 300 300 300 300 300

Finance Cost (in

millions)

26 22 32 32 32 32 32 32

Tax Expense -30% 152.4 178.2 180.6 197.4 224.4 259.2 303.9 361.5

Net Profit 355.6 415.8 421.4 460.6 523.6 604.8 709.1 843.5

Net Profit Margin 15.08% 15.400% 15.15% 15.43% 15.78% 16.00% 16.15% 16.36%

28

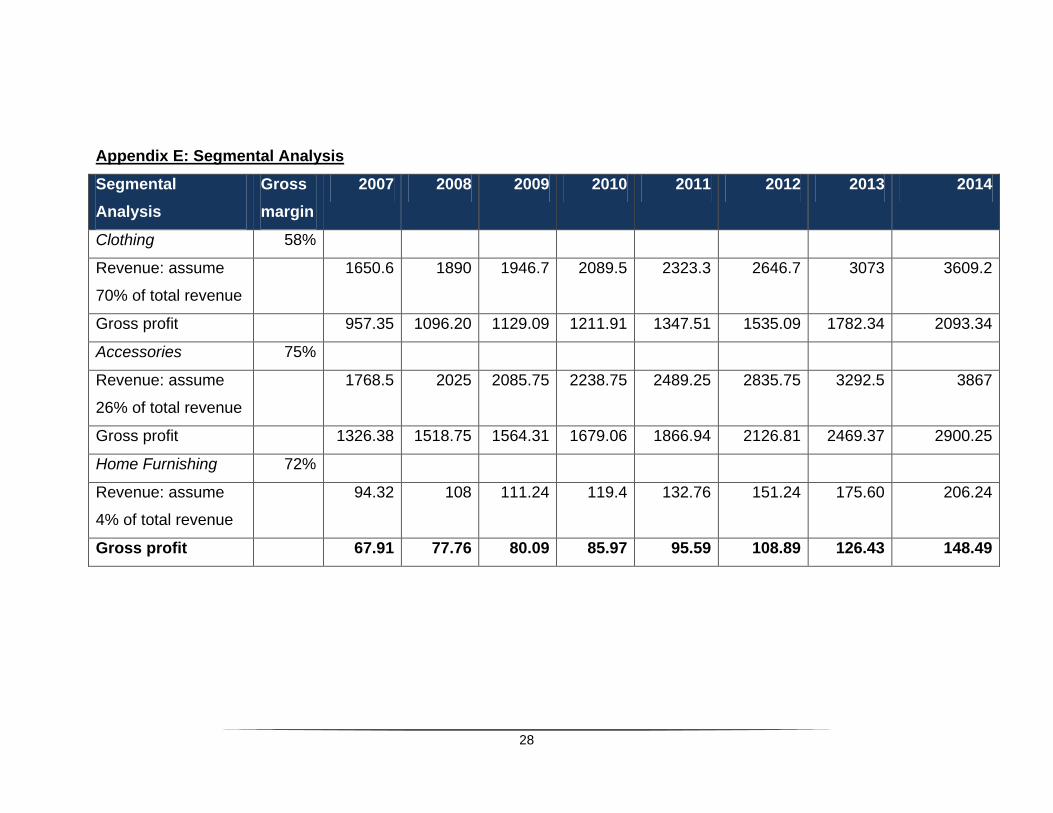

Appendix E: Segmental Analysis

Segmental

Analysis

Gross

margin

2007 2008 2009 2010 2011 2012 2013 2014

Clothing 58%

Revenue: assume

70% of total revenue

1650.6 1890 1946.7 2089.5 2323.3 2646.7 3073 3609.2

Gross profit 957.35 1096.20 1129.09 1211.91 1347.51 1535.09 1782.34 2093.34

Accessories 75%

Revenue: assume

26% of total revenue

1768.5 2025 2085.75 2238.75 2489.25 2835.75 3292.5 3867

Gross profit 1326.38 1518.75 1564.31 1679.06 1866.94 2126.81 2469.37 2900.25

Home Furnishing 72%

Revenue: assume

4% of total revenue

94.32 108 111.24 119.4 132.76 151.24 175.60 206.24

Gross profit 67.91 77.76 80.09 85.97 95.59 108.89 126.43 148.49

29

Appendix F: 5-year Plan Cash flow Projection

2007 2008 2009 2010 2011 2012 2013 2014

No of shops (end year)

570 610 630 650 672 702 750 800

Average for year

547 590 620 640 661 687 726 775

Sales area for all shops (sq m) -average for year

532,400 600,000 648,000 680,000 713,200 752,400 808,800 879,600

Sales Revenue (in millions)

2358 2700 2781 2985 3319 3781 4390 5156

Issue 1: Celebrity Marketing expense6

-0.2 -0.2 -0.2 -0.2 -0.2

Issue 2: Jewellery expansion

-7.26 -6.33 -6.33 -6.33 -6.33

Issue 3:IT failure (bad debts)7

-3.28

Issue 4: Distributor's strike8

0.00

Operating profit (in millions)

534 616 634 679.25552 773.46608 889.46608 1038.4661 1230.4661

Operating Profit Margin

22.646% 22.815% 22.798% 22.756% 23.304% 23.525% 23.655% 23.865%

Long term liability

300 300 300 300 300 300 300 300

Finance Cost (in millions)

26 22 32 32 32 32 32 32

Tax Expense @ 30%

152.4 178.2 180.6 194.17665 222.43982 257.23982 301.93982 359.53982

Net Profit

355.6 415.8 421.4 453.07886 519.02626 600.22626 704.52626 838.92626

Net Profit Margin

15.081% 15.400% 15.153% 15.179% 15.638% 15.875% 16.048% 16.271%

6 First method of fixed payment of €50,000 + €150,000 bonus is used 7 External agency was employed to recover bad debts 8 Alternative distributor was sourced for and thus any costs were allayed. There may have been other costs incurred in sourcing for new distributors and making changes to distribution system but these costs are not included above.

30

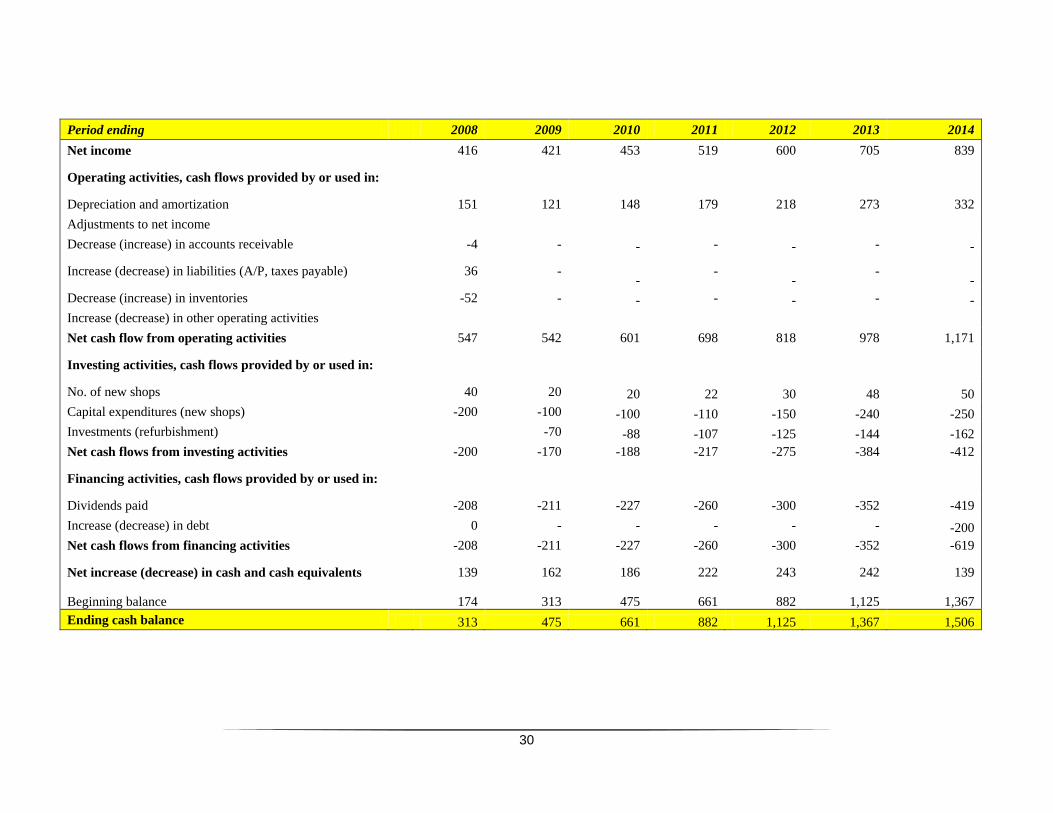

Period ending 2008 2009 2010 2011 2012 2013 2014

Net income

416 421 453 519 600 705 839

Operating activities, cash flows provided by or used in:

Depreciation and amortization

151 121 148 179 218 273 332

Adjustments to net income

Decrease (increase) in accounts receivable

-4 - - - - - -

Increase (decrease) in liabilities (A/P, taxes payable)

36 - -

- -

- -

Decrease (increase) in inventories

-52 - - - - - -

Increase (decrease) in other operating activities

Net cash flow from operating activities

547 542 601 698 818 978 1,171

Investing activities, cash flows provided by or used in:

No. of new shops

40 20 20 22 30 48 50

Capital expenditures (new shops)

-200 -100 -100 -110 -150 -240 -250

Investments (refurbishment)

-70 -88 -107 -125 -144 -162

Net cash flows from investing activities

-200 -170 -188 -217 -275 -384 -412

Financing activities, cash flows provided by or used in:

Dividends paid

-208 -211 -227 -260 -300 -352 -419

Increase (decrease) in debt

0 - - - - - -200

Net cash flows from financing activities

-208 -211 -227 -260 -300 -352 -619

Net increase (decrease) in cash and cash equivalents

139 162 186 222 243 242 139

Beginning balance 174 313 475 661 882 1,125 1,367

Ending cash balance 313 475 661 882 1,125 1,367 1,506

31

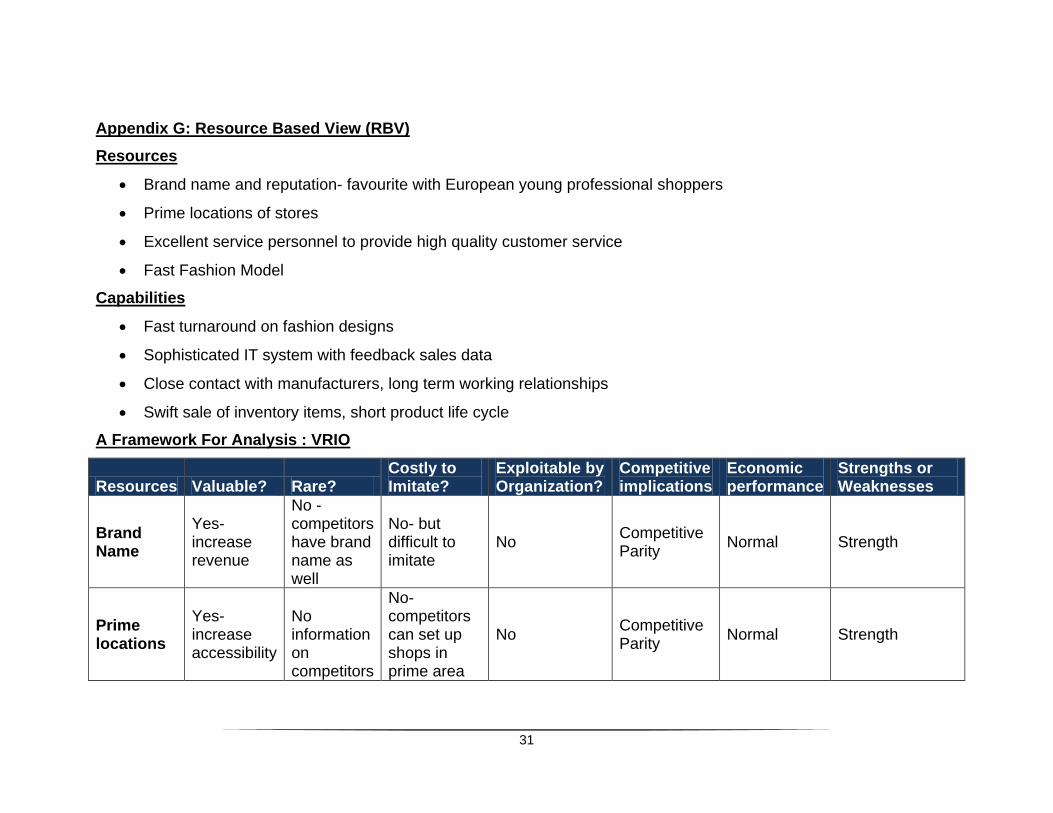

Appendix G: Resource Based View (RBV)

Resources

Brand name and reputation- favourite with European young professional shoppers

Prime locations of stores

Excellent service personnel to provide high quality customer service

Fast Fashion Model

Capabilities

Fast turnaround on fashion designs

Sophisticated IT system with feedback sales data

Close contact with manufacturers, long term working relationships

Swift sale of inventory items, short product life cycle

A Framework For Analysis : VRIO

Resources Valuable? Rare? Costly to Imitate?

Exploitable by Organization?

Competitive implications

Economic performance

Strengths or Weaknesses

Brand Name

Yes- increase revenue

No -competitors have brand name as well

No- but difficult to imitate

No Competitive Parity

Normal Strength

Prime locations

Yes- increase accessibility

No information on competitors

No- competitors can set up shops in prime area

No Competitive Parity

Normal Strength

32

to form valid conclusion

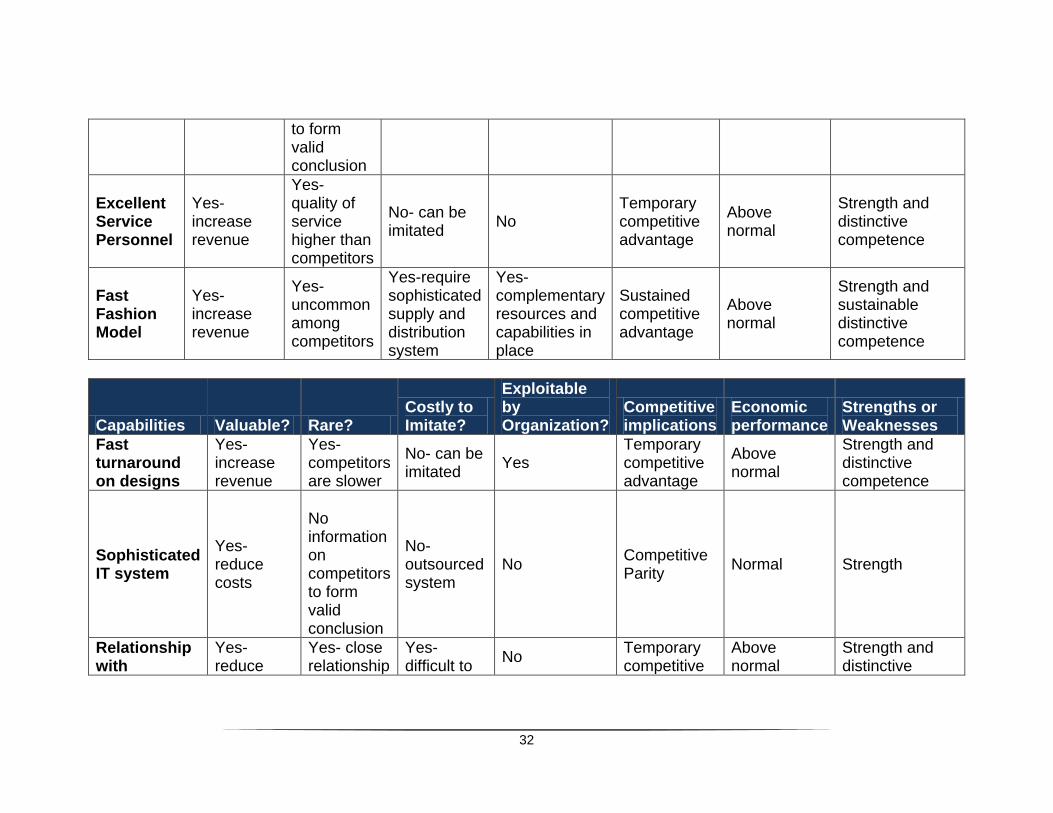

Excellent Service Personnel

Yes- increase revenue

Yes- quality of service higher than competitors

No- can be imitated

No Temporary competitive advantage

Above normal

Strength and distinctive competence

Fast Fashion Model

Yes- increase revenue

Yes-uncommon among competitors

Yes-require sophisticated supply and distribution system

Yes- complementary resources and capabilities in place

Sustained competitive advantage

Above normal

Strength and sustainable distinctive competence

Capabilities Valuable? Rare? Costly to Imitate?

Exploitable by Organization?

Competitive implications

Economic performance

Strengths or Weaknesses

Fast turnaround on designs

Yes- increase revenue

Yes- competitors are slower

No- can be imitated

Yes Temporary competitive advantage

Above normal

Strength and distinctive competence

Sophisticated IT system

Yes- reduce costs

No information on competitors to form valid conclusion

No- outsourced system

No Competitive Parity

Normal Strength

Relationship with

Yes- reduce

Yes- close relationship

Yes- difficult to

No Temporary competitive

Above normal

Strength and distinctive

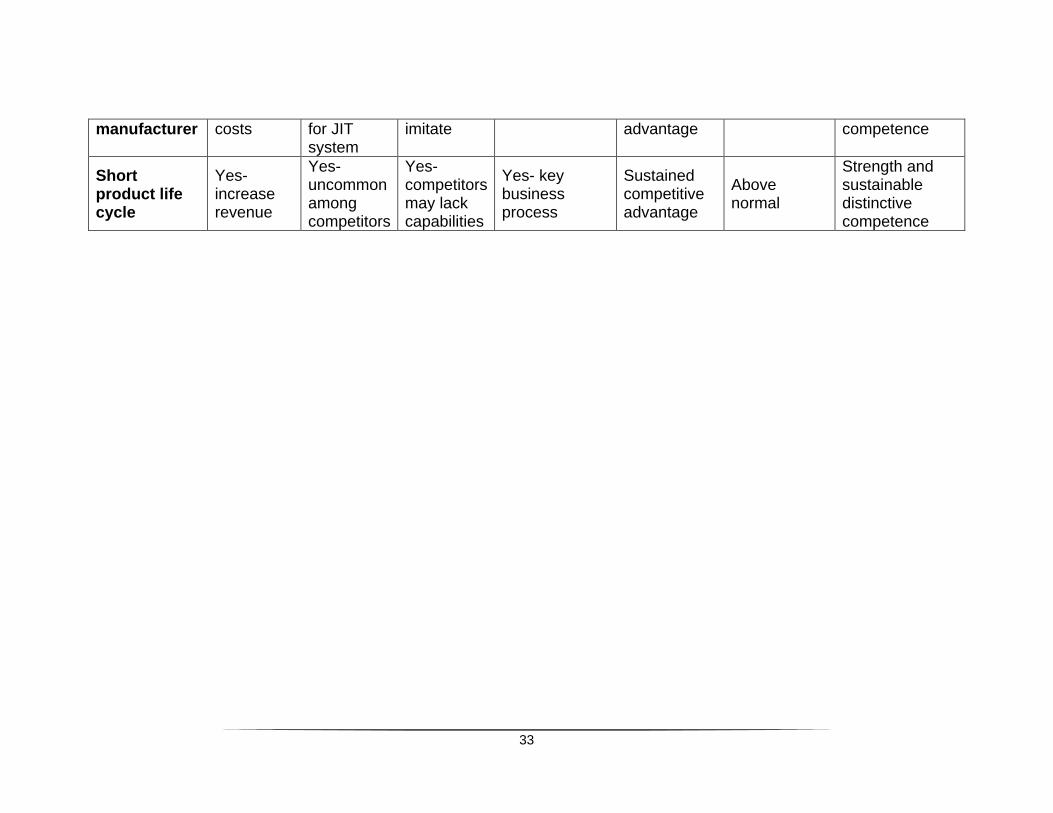

33

manufacturer costs for JIT system

imitate advantage competence

Short product life cycle

Yes- increase revenue

Yes-uncommon among competitors

Yes-competitors may lack capabilities

Yes- key business process

Sustained competitive advantage

Above normal

Strength and sustainable distinctive competence

34