Embed Size (px)

Citation preview

CombinedHeatandPowerSystems:IdentifyingEconomicandPolicyBarrierstoGrowth

AdilKalam,AbigailKing,EllenMoret,UpekhaWeerasinghe

AdilKalam,AbigailKing,EllenMoret,UpekhaWeerasinghe

Consultant:MichaelRoytburd

EnergyandEnergyPolicy

FallQuarter2009

2

TableofContents

ExecutiveSummary......................................................................................................3

Introduction.................................................................................................................4

Technology ................................................................................................................10

PolicyEnvironment ....................................................................................................17

EconomicOverview ...................................................................................................22

AnalysisPartOne:StatisticalAnalysisofStatePolicies...............................................26

AnalysisPartTwo:Cost‐BenefitAnalysis ....................................................................31

ConclusionsandRecommendations ...........................................................................41

AppendixA–RegressionData....................................................................................43

AppendixB–STATARegressionResults .....................................................................45

AppendixC‐CostandPerformanceAssumptions .......................................................49

AppendixD‐CapitalCosts ..........................................................................................50

AppendixE‐O&MCosts .............................................................................................52

AppendixF‐BasicCostAnalysis.................................................................................52

AppendixG‐LevelizedCostResults ............................................................................53

References .................................................................................................................55

3

ExecutiveSummaryCombinedHeatandPowersystemscanprovidearangeofbenefitstouserswithregardstoefficiency,reliability,costsandenvironmentalimpact.Furthermore,increasingtheamountofelectricitygeneratedbyCHPsystemsintheUnitedStateshasbeenidentifiedashavingsignificantpotentialforimpressiveeconomicandenvironmentaloutcomesonanationalscale.GiventhebenefitsfromincreasingtheadoptionofCHPtechnologies,thereisvalueinimprovingourunderstandingofhowdesiredincreasesinCHPadoptioncanbebestachieved.Theseobstaclesarecurrentlyunderstoodtostemfromregulatoryaswellaseconomicandtechnologicalbarriers.Inourresearch,weanswerthefollowingquestions:GiventhecurrentpolicyandeconomicenvironmentfacingtheCHPindustry,whatchangesneedtotakeplaceinthisspaceinorderforCHPsystemstobecompetitiveintheenergymarket?WefocusouranalysisprimarilyonCombinedHeatandPowerSystemsthatusenaturalgasturbines.Ouranalysistakesatwo‐prongedapproach.WefirstconductastatisticalanalysisoftheimpactofstatepoliciesonincreasesinelectricitygeneratedfromCHPsystem.Second,weconductaCost‐BenefitanalysistodetermineinwhichcircumstancesfundingincentivesarenecessarytomakeCHPtechnologiescost‐competitive.OurpolicyanalysisshowsthatregulatoryimprovementsdonotexplainthegrowthinadoptionofCHPtechnologiesbutholdthepotentialtoencourageincreasesinelectricitygeneratedfromCHPsysteminsmall‐scaleapplications.OurCost‐BenefitanalysisshowsthatCHPsystemsareonlycostcompetitiveinlarge‐scaleapplicationsandthatfundingincentiveswouldbenecessarytomakeCHPtechnologycost‐competitiveinsmall‐scaleapplications.Fromthesynthesisoftheseanalysesweconcludethatbecauselarge‐scaleapplicationsofnaturalgasturbinesarealreadycost‐competitive,policyinitiativesaimedataCHPmarketdominatedprimarilybylarge‐scale(andthereforealreadycost‐competitive)systemshavenotbeeneffectivelydirected.OurrecommendationisthatforCHPtechnologiesusingnaturalgasturbines,policyfocusesshouldbeonincreasingCHPgrowthinsmall‐scalesystems.Thisresultcanbebestachievedthroughredirectionofstateandfederalincentives,researchanddevelopment,adoptionofsmartgridtechnology,andoutreachandeducation.

4

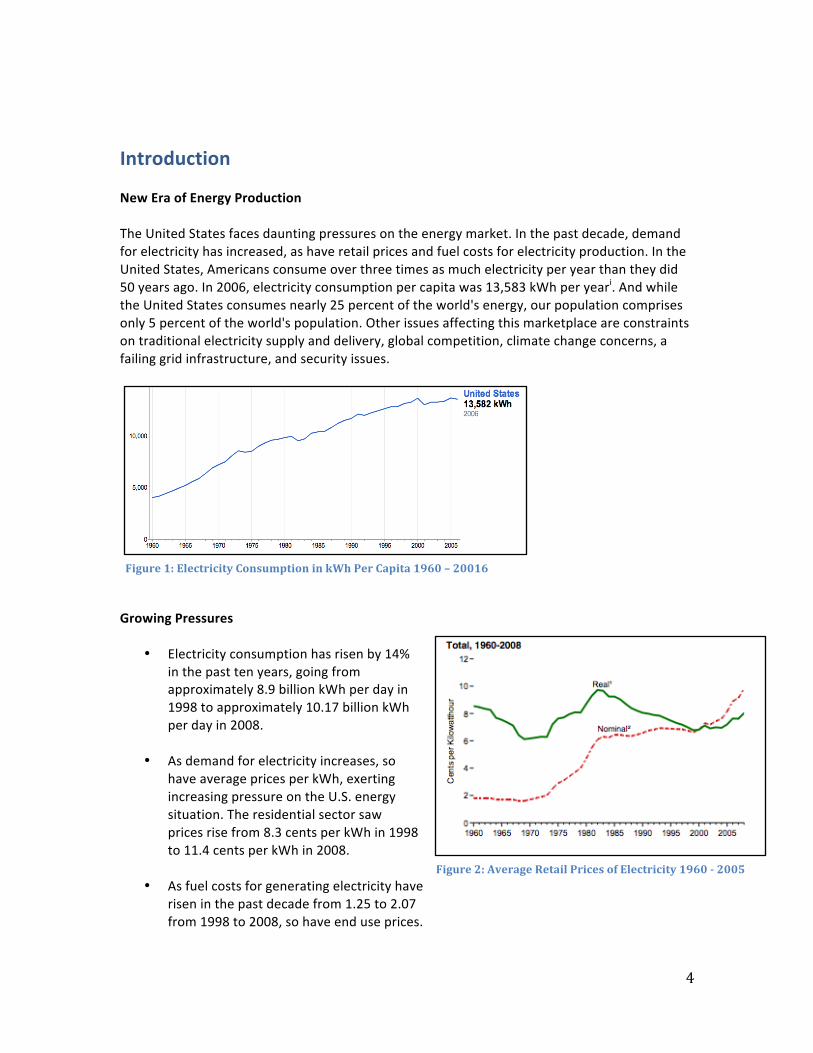

IntroductionNewEraofEnergyProductionTheUnitedStatesfacesdauntingpressuresontheenergymarket.Inthepastdecade,demandforelectricityhasincreased,ashaveretailpricesandfuelcostsforelectricityproduction.IntheUnitedStates,Americansconsumeoverthreetimesasmuchelectricityperyearthantheydid50yearsago.In2006,electricityconsumptionpercapitawas13,583kWhperyeari.AndwhiletheUnitedStatesconsumesnearly25percentoftheworld'senergy,ourpopulationcomprisesonly5percentoftheworld'spopulation.Otherissuesaffectingthismarketplaceareconstraintsontraditionalelectricitysupplyanddelivery,globalcompetition,climatechangeconcerns,afailinggridinfrastructure,andsecurityissues.

GrowingPressures

• Electricityconsumptionhasrisenby14%inthepasttenyears,goingfromapproximately8.9billionkWhperdayin1998toapproximately10.17billionkWhperdayin2008.

• Asdemandforelectricityincreases,sohaveaveragepricesperkWh,exertingincreasingpressureontheU.S.energysituation.Theresidentialsectorsawpricesrisefrom8.3centsperkWhin1998to11.4centsperkWhin2008.

• Asfuelcostsforgeneratingelectricityhaveriseninthepastdecadefrom1.25to2.07from1998to2008,sohaveenduseprices.

Figure1:ElectricityConsumptioninkWhPerCapita1960–20016

Figure2:AverageRetailPricesofElectricity19602005

5

Thepictureisclear;theU.S.needsaffordablesolutionstocombatincreasingcostanddemandpressureinelectricitymarkets.Energyefficiencyisunderstoodtobethecornerstoneofimprovingourfutureenergyportfolio.InstallingenergyefficienttechnologieslikecommercialandindustrialCHParecost‐negative.CombinedHeatandPowertechnologyisoneofthemostappealingenergyefficiencymeasuresavailabletoustoday;itcanloweroverallenergydemand,reducerelianceonfuelforgeneration,increasethecompetitivenessofbusinesses,cutgreen‐housegasemissions,andreducethepressureforelectricitygridinfrastructureimprovements.CombinedHeatandPower,orCHP,isanimmediatelyemployablesolutionthatcanaddressthegrowingconstraintsonAmerica’senergyfuture.TheCHPProcessCombinedheatandpowerdescribesanysystemthatsimultaneouslyorsequentiallygenerateselectricityandrecoversandre‐usesthethermalenergybyproductofthisprocess.CHPsystemshavehugeenergyefficiencyimprovementsbecausetheyproducetwoformsofusefulenergy–heatandelectricity,fromasinglefuelsource.CHPextractsmoreusefulenergyfromonefuelsourcethandothecombinationofprocessesthatoccurattraditionalpowerplantsthatproduceelectricityandseparatefacilitiesthatproduceheat.iiIncomparisonwithastandardpowerplant,whichoperatesatabout45%efficiency,aCHPfacilityoperatesat80%efficiency.CHPfacilitiesextractthisenergythroughtwomaintypesofpowercyclesknownastoppingandbottomingcycles.Thetoppingcycle,alsoknownasacombinedcycle,isthemostwidelyusedandappliedtechnology.Atoppingcyclesystemusesfueltopowertheprimaryprocessofgeneratingelectricalpower.Thentheexcessheatfromthisprocessisharvestedanduseddirectlytoheatairorwater,orasanenergysourceforheat‐drivencoolingsystems.iiiAbottomingcycleusestheprimaryfuelsourcetodriveaheatingmechanism.Theexcessheatfromthisprocessisthenusedtogenerateelectricityforon‐siteuseortosellbacktotheelectricalgrid.AstheU.S.electricitygridbecomesmorefocusedonclean,renewable,efficientenergyandmovesawayfromafocusoncentralizedpowerplants,on‐sitepowergeneration,knownasDistributedGeneration,isgarneringincreasingattention.ManytypesofCHPapplicationsareformsofDistributedGeneration.Typically,smaller‐scaleCHPsystemsproduceaportionoftheelectricityneededbyafacilitysomeorallofthetimeon‐site,withthebalanceofelectricneedssatisfiedbypurchasefromthegrid.CHPasaformofdistributedgenerationincreasesefficiencyintwoimportantways.First,thesystemitselfrecoverswasteheattogeneratemoreKWHperunitoffuel.Second,generatingelectricityon‐sitereducestheamountofenergylostintransmittingelectricity.

Figure1:FuelCostsforElectricityGeneration19962007

6

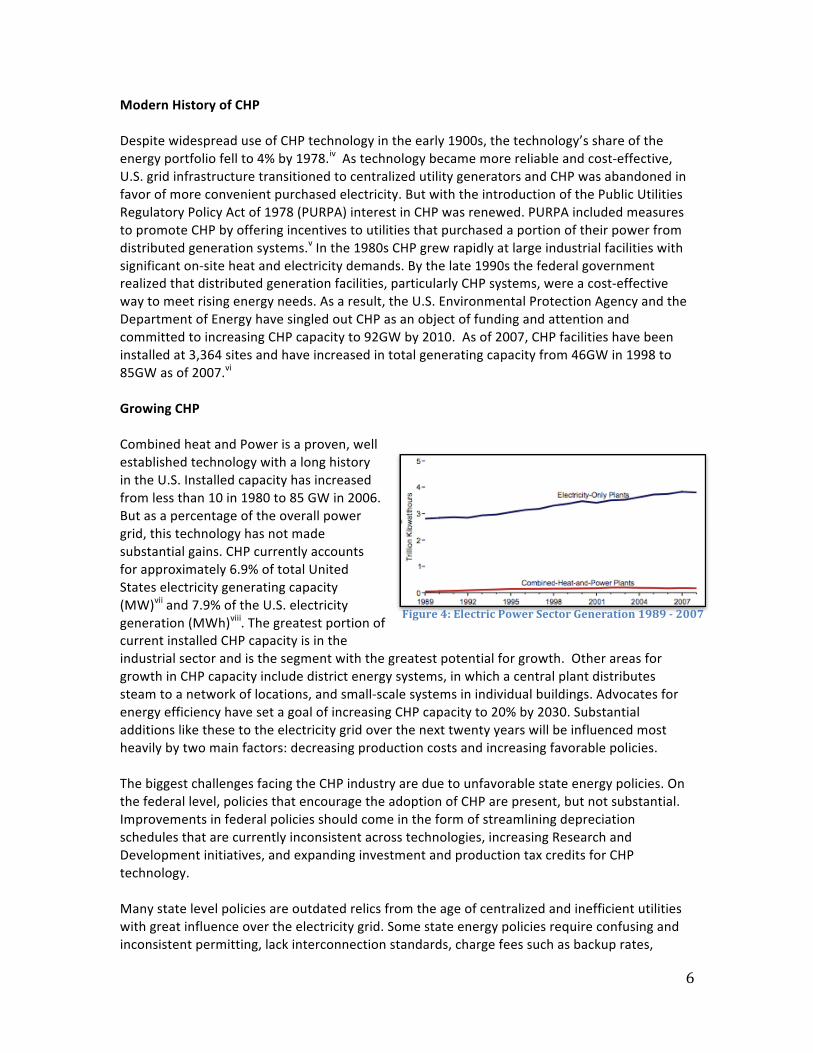

ModernHistoryofCHPDespitewidespreaduseofCHPtechnologyintheearly1900s,thetechnology’sshareoftheenergyportfoliofellto4%by1978.ivAstechnologybecamemorereliableandcost‐effective,U.S.gridinfrastructuretransitionedtocentralizedutilitygeneratorsandCHPwasabandonedinfavorofmoreconvenientpurchasedelectricity.ButwiththeintroductionofthePublicUtilitiesRegulatoryPolicyActof1978(PURPA)interestinCHPwasrenewed.PURPAincludedmeasurestopromoteCHPbyofferingincentivestoutilitiesthatpurchasedaportionoftheirpowerfromdistributedgenerationsystems.vInthe1980sCHPgrewrapidlyatlargeindustrialfacilitieswithsignificanton‐siteheatandelectricitydemands.Bythelate1990sthefederalgovernmentrealizedthatdistributedgenerationfacilities,particularlyCHPsystems,wereacost‐effectivewaytomeetrisingenergyneeds.Asaresult,theU.S.EnvironmentalProtectionAgencyandtheDepartmentofEnergyhavesingledoutCHPasanobjectoffundingandattentionandcommittedtoincreasingCHPcapacityto92GWby2010.Asof2007,CHPfacilitieshavebeeninstalledat3,364sitesandhaveincreasedintotalgeneratingcapacityfrom46GWin1998to85GWasof2007.viGrowingCHPCombinedheatandPowerisaproven,wellestablishedtechnologywithalonghistoryintheU.S.Installedcapacityhasincreasedfromlessthan10in1980to85GWin2006.Butasapercentageoftheoverallpowergrid,thistechnologyhasnotmadesubstantialgains.CHPcurrentlyaccountsforapproximately6.9%oftotalUnitedStateselectricitygeneratingcapacity(MW)viiand7.9%oftheU.S.electricitygeneration(MWh)viii.ThegreatestportionofcurrentinstalledCHPcapacityisintheindustrialsectorandisthesegmentwiththegreatestpotentialforgrowth.OtherareasforgrowthinCHPcapacityincludedistrictenergysystems,inwhichacentralplantdistributessteamtoanetworkoflocations,andsmall‐scalesystemsinindividualbuildings.AdvocatesforenergyefficiencyhavesetagoalofincreasingCHPcapacityto20%by2030.Substantialadditionslikethesetotheelectricitygridoverthenexttwentyyearswillbeinfluencedmostheavilybytwomainfactors:decreasingproductioncostsandincreasingfavorablepolicies.ThebiggestchallengesfacingtheCHPindustryareduetounfavorablestateenergypolicies.Onthefederallevel,policiesthatencouragetheadoptionofCHParepresent,butnotsubstantial.Improvementsinfederalpoliciesshouldcomeintheformofstreamliningdepreciationschedulesthatarecurrentlyinconsistentacrosstechnologies,increasingResearchandDevelopmentinitiatives,andexpandinginvestmentandproductiontaxcreditsforCHPtechnology.Manystatelevelpoliciesareoutdatedrelicsfromtheageofcentralizedandinefficientutilitieswithgreatinfluenceovertheelectricitygrid.Somestateenergypoliciesrequireconfusingandinconsistentpermitting,lackinterconnectionstandards,chargefeessuchasbackuprates,

Figure4:ElectricPowerSectorGeneration19892007

7

standbyratesandexitfees,enforcenon‐outputbasedemissionstandards,coupleutilityrevenueswithelectricitysales,andlackRenewablePortfolioStandardsthatincludeCHP.OursubsequentanalysiswillfocusontheeffectofthesepoliciesonCHPgrowthonastate‐by‐statebasis.CHPAdvantagesCombinedHeatandPowersystemscanprovidearangeofbenefitstouserswithregardstoefficiency,reliability,costsandenvironmentalimpact.ReducedEnergyConsumptionThroughIncreasedEfficiencyix

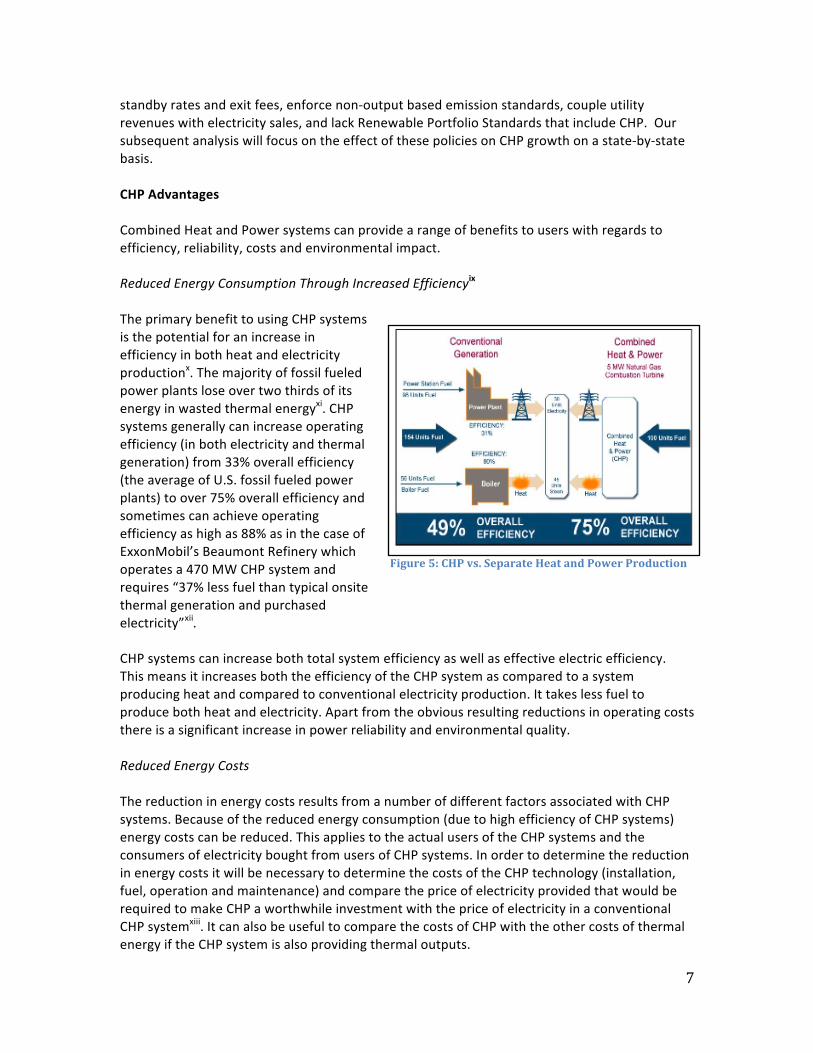

TheprimarybenefittousingCHPsystemsisthepotentialforanincreaseinefficiencyinbothheatandelectricityproductionx.Themajorityoffossilfueledpowerplantsloseovertwothirdsofitsenergyinwastedthermalenergyxi.CHPsystemsgenerallycanincreaseoperatingefficiency(inbothelectricityandthermalgeneration)from33%overallefficiency(theaverageofU.S.fossilfueledpowerplants)toover75%overallefficiencyandsometimescanachieveoperatingefficiencyashighas88%asinthecaseofExxonMobil’sBeaumontRefinerywhichoperatesa470MWCHPsystemandrequires“37%lessfuelthantypicalonsitethermalgenerationandpurchasedelectricity”xii.CHPsystemscanincreasebothtotalsystemefficiencyaswellaseffectiveelectricefficiency.ThismeansitincreasesboththeefficiencyoftheCHPsystemascomparedtoasystemproducingheatandcomparedtoconventionalelectricityproduction.Ittakeslessfueltoproducebothheatandelectricity.Apartfromtheobviousresultingreductionsinoperatingcoststhereisasignificantincreaseinpowerreliabilityandenvironmentalquality.ReducedEnergyCostsThereductioninenergycostsresultsfromanumberofdifferentfactorsassociatedwithCHPsystems.Becauseofthereducedenergyconsumption(duetohighefficiencyofCHPsystems)energycostscanbereduced.ThisappliestotheactualusersoftheCHPsystemsandtheconsumersofelectricityboughtfromusersofCHPsystems.InordertodeterminethereductioninenergycostsitwillbenecessarytodeterminethecostsoftheCHPtechnology(installation,fuel,operationandmaintenance)andcomparethepriceofelectricityprovidedthatwouldberequiredtomakeCHPaworthwhileinvestmentwiththepriceofelectricityinaconventionalCHPsystemxiii.ItcanalsobeusefultocomparethecostsofCHPwiththeothercostsofthermalenergyiftheCHPsystemisalsoprovidingthermaloutputs.

Figure5:CHPvs.SeparateHeatandPowerProduction

8

Asidefromthedirectbenefitsfromreducedenergycosts,CHPsystemsalsoprovidethebenefitsofoffsetcapitalcostsandimprovedreliability.Conventionalpowerandthermalenergysystemsrequireboilers,chillersandothermajorheatingorcoolingequipmenttobereplacedorupdated,andifCHPsystemsareinstalledinplaceofthenowunnecessaryboilersandchillers,thecapitalcostsofinstallationareoffset.Furthermore,asaresultofthereliabilitybenefitsdescribedinthenextsection,therearealsoeconomicbenefitsfromimprovedreliabilityforCHPusersbecauseCHPsystemsoffertheabilitytouseCHPasbackuppowerandallowuserstosupplytheirownpowerwhenpricesofelectricityareveryhighxiv.BecauseCHPsystemsareoftenlocatedonsite,theyallowuserstoavoidtransmissionsanddistributionlossesusuallyassociatedwithconventionaloff‐siteenergygeneration.

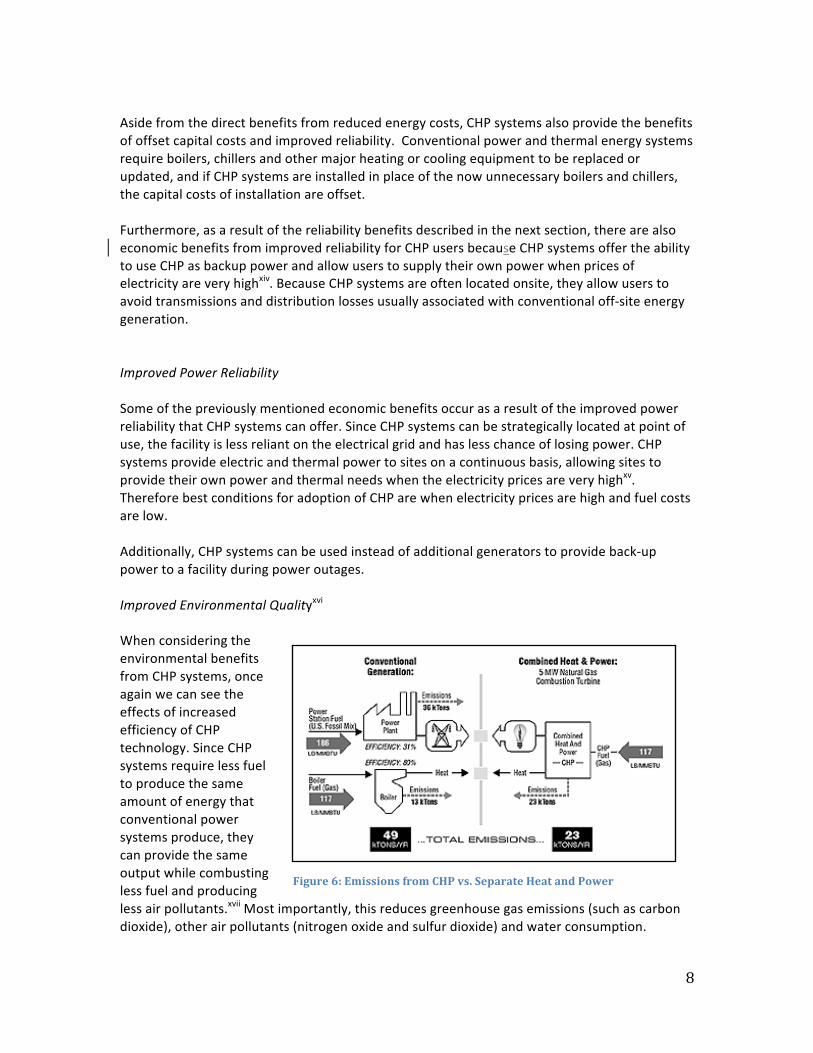

ImprovedPowerReliabilitySomeofthepreviouslymentionedeconomicbenefitsoccurasaresultoftheimprovedpowerreliabilitythatCHPsystemscanoffer.SinceCHPsystemscanbestrategicallylocatedatpointofuse,thefacilityislessreliantontheelectricalgridandhaslesschanceoflosingpower.CHPsystemsprovideelectricandthermalpowertositesonacontinuousbasis,allowingsitestoprovidetheirownpowerandthermalneedswhentheelectricitypricesareveryhighxv.ThereforebestconditionsforadoptionofCHParewhenelectricitypricesarehighandfuelcostsarelow.Additionally,CHPsystemscanbeusedinsteadofadditionalgeneratorstoprovideback‐uppowertoafacilityduringpoweroutages.ImprovedEnvironmentalQualityxviWhenconsideringtheenvironmentalbenefitsfromCHPsystems,onceagainwecanseetheeffectsofincreasedefficiencyofCHPtechnology.SinceCHPsystemsrequirelessfueltoproducethesameamountofenergythatconventionalpowersystemsproduce,theycanprovidethesameoutputwhilecombustinglessfuelandproducinglessairpollutants.xviiMostimportantly,thisreducesgreenhousegasemissions(suchascarbondioxide),otherairpollutants(nitrogenoxideandsulfurdioxide)andwaterconsumption.

Figure6:EmissionsfromCHPvs.SeparateHeatandPower

9

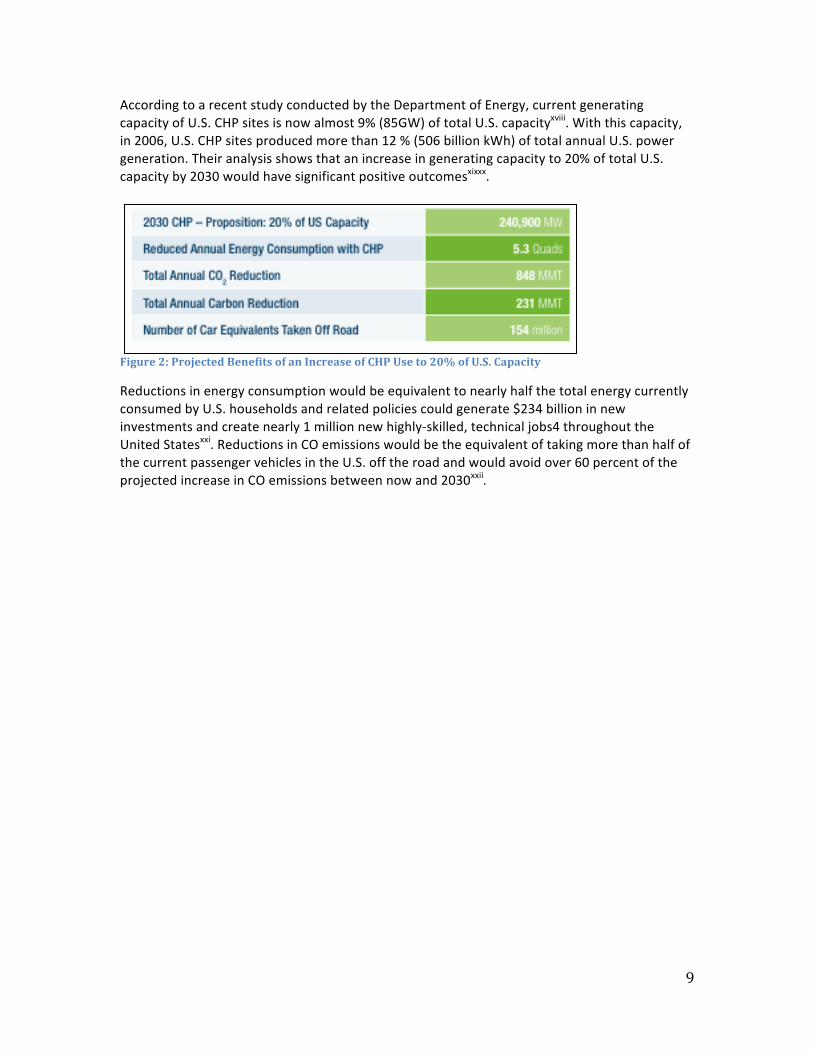

AccordingtoarecentstudyconductedbytheDepartmentofEnergy,currentgeneratingcapacityofU.S.CHPsitesisnowalmost9%(85GW)oftotalU.S.capacityxviii.Withthiscapacity,in2006,U.S.CHPsitesproducedmorethan12%(506billionkWh)oftotalannualU.S.powergeneration.Theiranalysisshowsthatanincreaseingeneratingcapacityto20%oftotalU.S.capacityby2030wouldhavesignificantpositiveoutcomesxixxx.

Figure2:ProjectedBenefitsofanIncreaseofCHPUseto20%ofU.S.Capacity

ReductionsinenergyconsumptionwouldbeequivalenttonearlyhalfthetotalenergycurrentlyconsumedbyU.S.householdsandrelatedpoliciescouldgenerate$234billioninnewinvestmentsandcreatenearly1millionnewhighly‐skilled,technicaljobs4throughouttheUnitedStatesxxi.ReductionsinCOemissionswouldbetheequivalentoftakingmorethanhalfofthecurrentpassengervehiclesintheU.S.offtheroadandwouldavoidover60percentoftheprojectedincreaseinCOemissionsbetweennowand2030xxii.

10

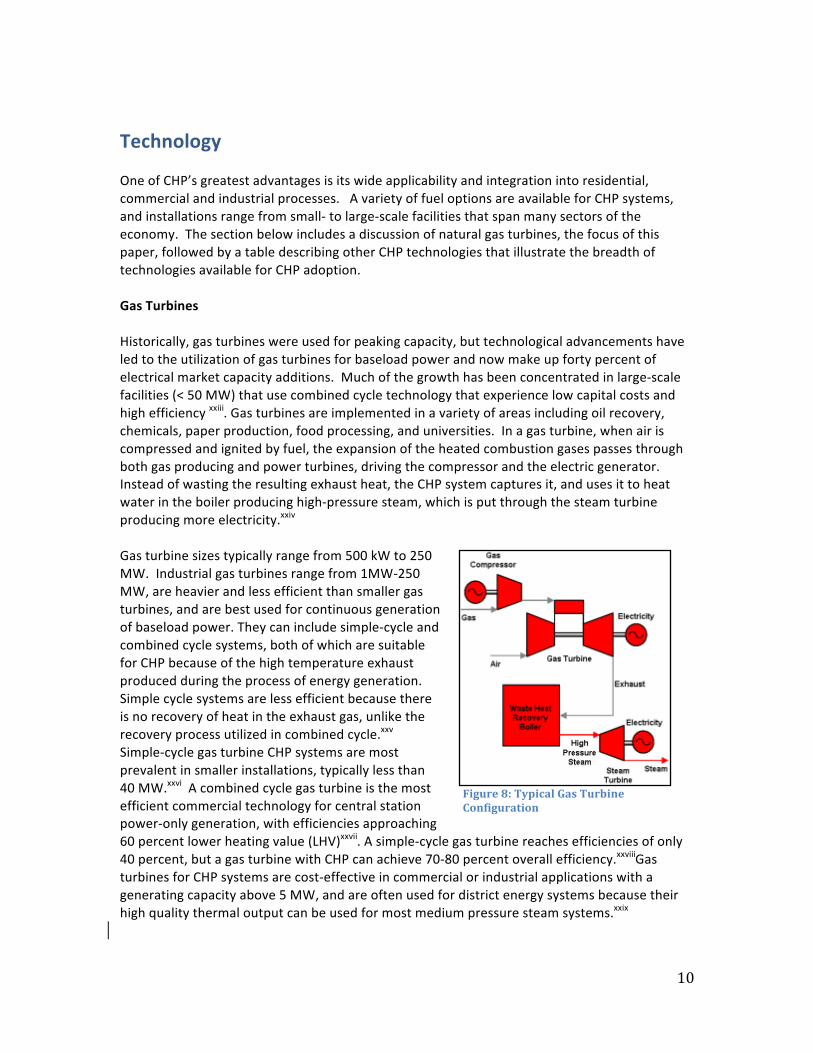

TechnologyOneofCHP’sgreatestadvantagesisitswideapplicabilityandintegrationintoresidential,commercialandindustrialprocesses.AvarietyoffueloptionsareavailableforCHPsystems,andinstallationsrangefromsmall‐tolarge‐scalefacilitiesthatspanmanysectorsoftheeconomy.Thesectionbelowincludesadiscussionofnaturalgasturbines,thefocusofthispaper,followedbyatabledescribingotherCHPtechnologiesthatillustratethebreadthoftechnologiesavailableforCHPadoption.GasTurbinesHistorically,gasturbineswereusedforpeakingcapacity,buttechnologicaladvancementshaveledtotheutilizationofgasturbinesforbaseloadpowerandnowmakeupfortypercentofelectricalmarketcapacityadditions.Muchofthegrowthhasbeenconcentratedinlarge‐scalefacilities(<50MW)thatusecombinedcycletechnologythatexperiencelowcapitalcostsandhighefficiencyxxiii.Gasturbinesareimplementedinavarietyofareasincludingoilrecovery,chemicals,paperproduction,foodprocessing,anduniversities.Inagasturbine,whenairiscompressedandignitedbyfuel,theexpansionoftheheatedcombustiongasespassesthroughbothgasproducingandpowerturbines,drivingthecompressorandtheelectricgenerator.Insteadofwastingtheresultingexhaustheat,theCHPsystemcapturesit,andusesittoheatwaterintheboilerproducinghigh‐pressuresteam,whichisputthroughthesteamturbineproducingmoreelectricity.xxivGasturbinesizestypicallyrangefrom500kWto250MW.Industrialgasturbinesrangefrom1MW‐250MW,areheavierandlessefficientthansmallergasturbines,andarebestusedforcontinuousgenerationofbaseloadpower.Theycanincludesimple‐cycleandcombinedcyclesystems,bothofwhicharesuitableforCHPbecauseofthehightemperatureexhaustproducedduringtheprocessofenergygeneration.Simplecyclesystemsarelessefficientbecausethereisnorecoveryofheatintheexhaustgas,unliketherecoveryprocessutilizedincombinedcycle.xxvSimple‐cyclegasturbineCHPsystemsaremostprevalentinsmallerinstallations,typicallylessthan40MW.xxviAcombinedcyclegasturbineisthemostefficientcommercialtechnologyforcentralstationpower‐onlygeneration,withefficienciesapproaching60percentlowerheatingvalue(LHV)xxvii.Asimple‐cyclegasturbinereachesefficienciesofonly40percent,butagasturbinewithCHPcanachieve70‐80percentoverallefficiency.xxviiiGasturbinesforCHPsystemsarecost‐effectiveincommercialorindustrialapplicationswithageneratingcapacityabove5MW,andareoftenusedfordistrictenergysystemsbecausetheirhighqualitythermaloutputcanbeusedformostmediumpressuresteamsystems.xxix

Figure8:TypicalGasTurbineConfiguration

11

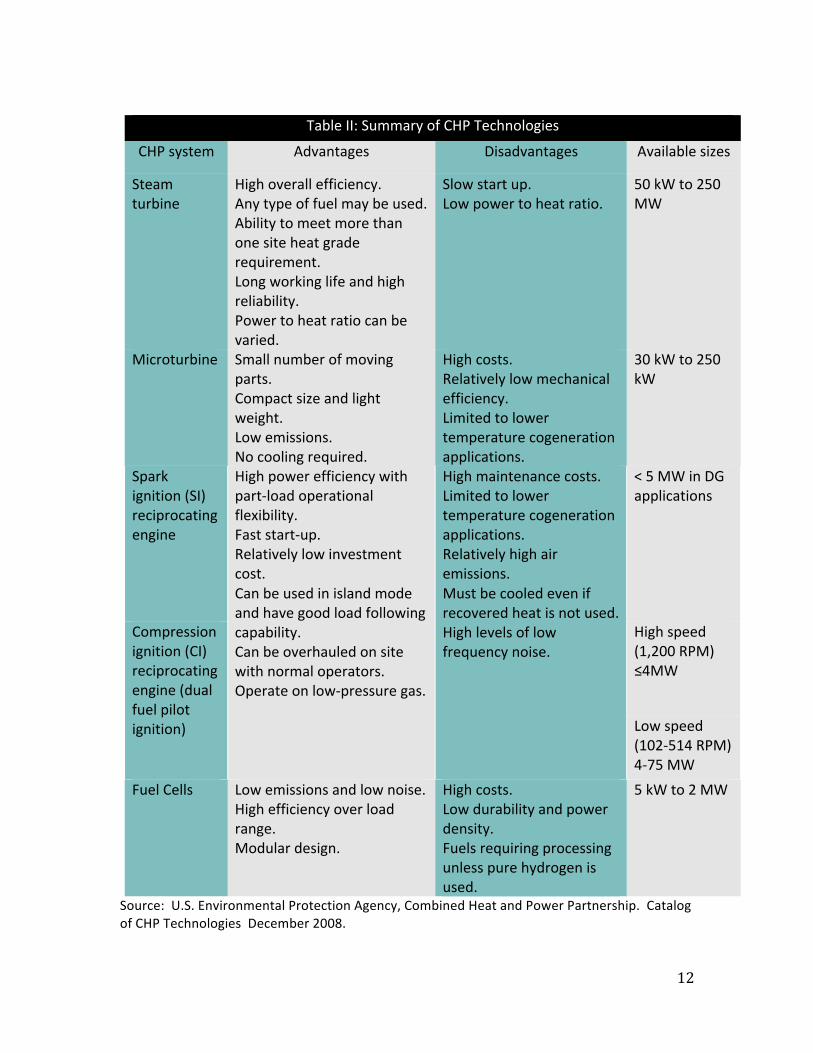

OtherCHPTechnologiesAlthoughthefocusofthispaperdoesnotincludethetechnologytypesbelow,itisimportanttohaveabroadoverviewoftechnologiesapplicabletoCHPdevelopment.SteamturbinesarewidelyusedinCHPsystemsbecausemostoftheelectricitycurrentlyproducedintheUnitedStatescomesfromsteamturbines.BecausethecostperkilowattofasteamturbineCHPsystemishighduetoitslowpowertoheatratio,itismostcommonlyusedinmedium‐to‐largescaleindustrialfacilities.BenefitstoCHPsteamturbinesincludeincreasedboilerefficienciesrangingfrom70to85percent,andtheavailabilityofawiderangeoffuels(naturalgas,coal,oils,municipalsolidwastes,sludges).Microturbines,orsmallgasturbines,aremorecomplexthansimple‐cyclegasturbinesandarebestusedfordistributedgenerationbecauseoftheflexibilityingridconnectionmethods.ReciprocatingenginesarebestusedinCHPsystemsforcommercialandinstitutionalbuildingsthatusespaceheatingandhavehotwaterrequirements.Fuelcellscurrentlyexperiencehighcosts,butmaybecomemorecost‐effectiveinthefutureasthetechnologymatures.

12

TableII:SummaryofCHPTechnologies

CHPsystem Advantages Disadvantages Availablesizes

Steamturbine

Highoverallefficiency.Anytypeoffuelmaybeused.Abilitytomeetmorethanonesiteheatgraderequirement.Longworkinglifeandhighreliability.Powertoheatratiocanbevaried.

Slowstartup.Lowpowertoheatratio.

50kWto250MW

Microturbine Smallnumberofmovingparts.Compactsizeandlightweight.Lowemissions.Nocoolingrequired.

Highcosts.Relativelylowmechanicalefficiency.Limitedtolowertemperaturecogenerationapplications.

30kWto250kW

Sparkignition(SI)reciprocatingengine

<5MWinDGapplications

Highspeed(1,200RPM)≤4MW

Compressionignition(CI)reciprocatingengine(dualfuelpilotignition)

Highpowerefficiencywithpart‐loadoperationalflexibility.Faststart‐up.Relativelylowinvestmentcost.Canbeusedinislandmodeandhavegoodloadfollowingcapability.Canbeoverhauledonsitewithnormaloperators.Operateonlow‐pressuregas.

Highmaintenancecosts.Limitedtolowertemperaturecogenerationapplications.Relativelyhighairemissions.Mustbecooledevenifrecoveredheatisnotused.Highlevelsoflowfrequencynoise.

Lowspeed(102‐514RPM)4‐75MW

FuelCells Lowemissionsandlownoise.Highefficiencyoverloadrange.Modulardesign.

Highcosts.Lowdurabilityandpowerdensity.Fuelsrequiringprocessingunlesspurehydrogenisused.

5kWto2MW

Source:U.S.EnvironmentalProtectionAgency,CombinedHeatandPowerPartnership.CatalogofCHPTechnologiesDecember2008.

13

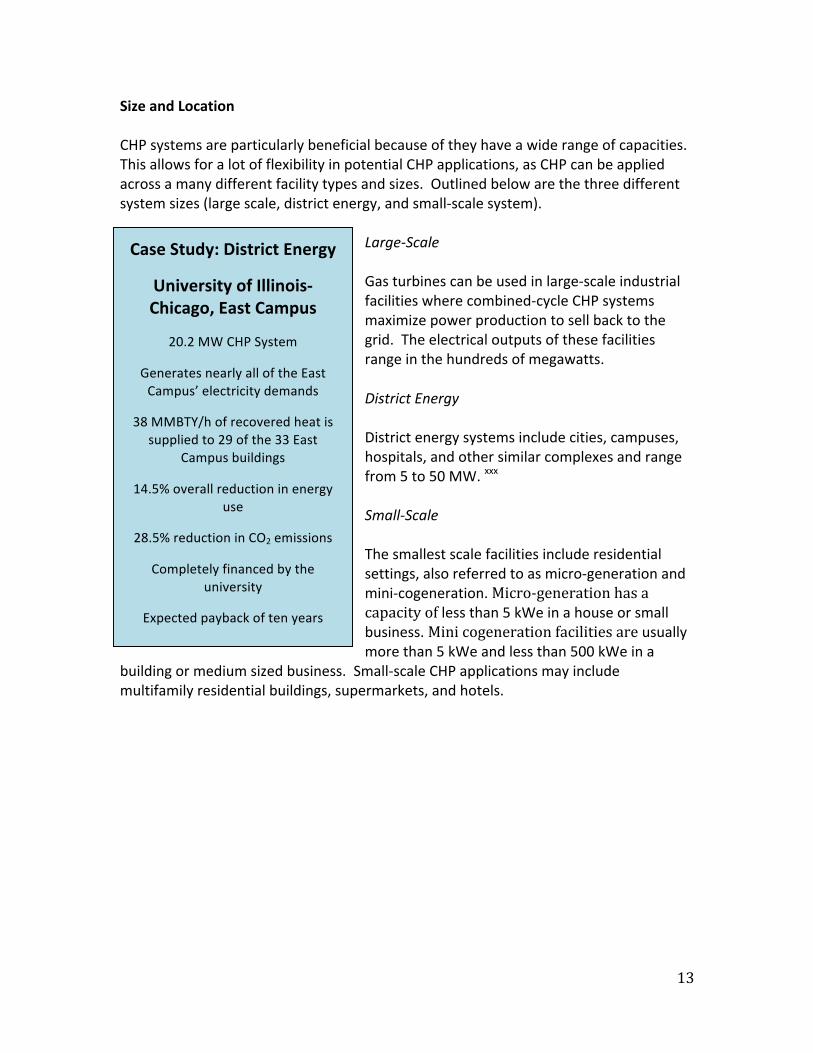

SizeandLocationCHPsystemsareparticularlybeneficialbecauseoftheyhaveawiderangeofcapacities.ThisallowsforalotofflexibilityinpotentialCHPapplications,asCHPcanbeappliedacrossamanydifferentfacilitytypesandsizes.Outlinedbelowarethethreedifferentsystemsizes(largescale,districtenergy,andsmall‐scalesystem).

Large‐ScaleGasturbinescanbeusedinlarge‐scaleindustrialfacilitieswherecombined‐cycleCHPsystemsmaximizepowerproductiontosellbacktothegrid.Theelectricaloutputsofthesefacilitiesrangeinthehundredsofmegawatts.DistrictEnergyDistrictenergysystemsincludecities,campuses,hospitals,andothersimilarcomplexesandrangefrom5to50MW.xxxSmall‐ScaleThesmallestscalefacilitiesincluderesidentialsettings,alsoreferredtoasmicro‐generationandmini‐cogeneration.Micro‐generationhasacapacityoflessthan5kWeinahouseorsmallbusiness.Minicogenerationfacilitiesareusuallymorethan5kWeandlessthan500kWeina

buildingormediumsizedbusiness.Small‐scaleCHPapplicationsmayincludemultifamilyresidentialbuildings,supermarkets,andhotels.

CaseStudy:DistrictEnergy

UniversityofIllinois‐Chicago,EastCampus

20.2MWCHPSystem

GeneratesnearlyalloftheEastCampus’electricitydemands

38MMBTY/hofrecoveredheatissuppliedto29ofthe33East

Campusbuildings

14.5%overallreductioninenergyuse

28.5%reductioninCO2emissions

Completelyfinancedbytheuniversity

Expectedpaybackoftenyears

14

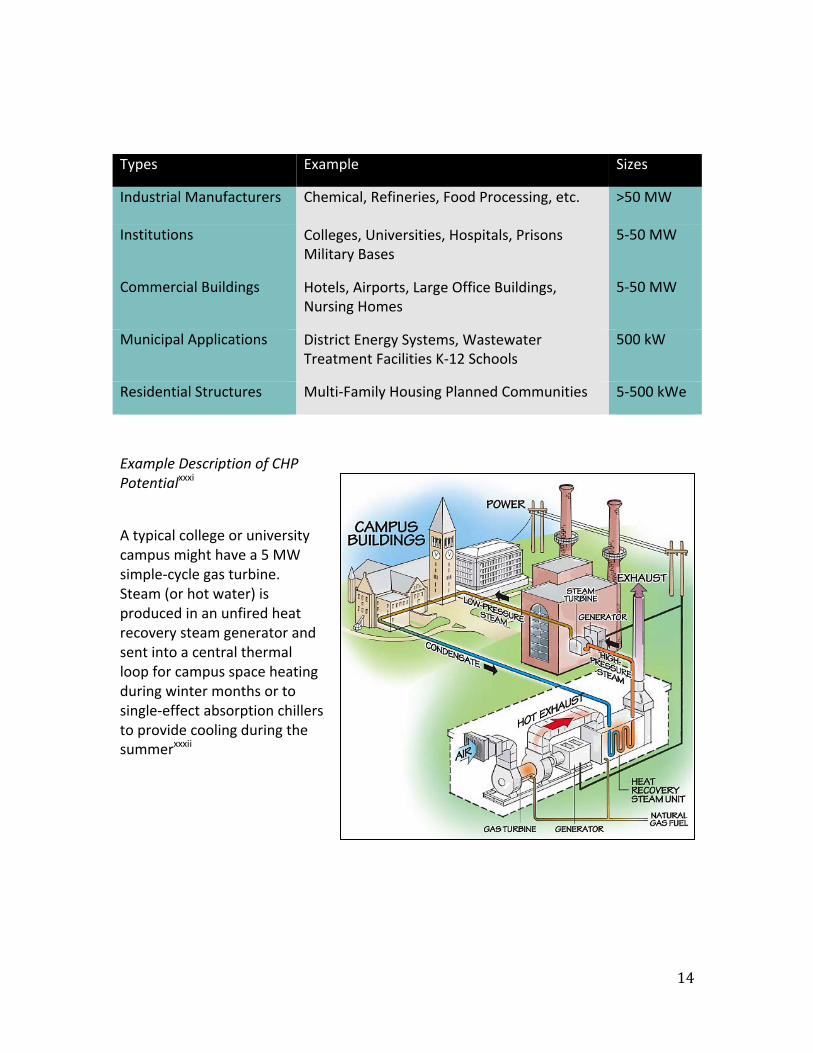

Types Example Sizes

IndustrialManufacturers Chemical,Refineries,FoodProcessing,etc. >50MW

Institutions Colleges,Universities,Hospitals,PrisonsMilitaryBases

5‐50MW

CommercialBuildings Hotels,Airports,LargeOfficeBuildings,NursingHomes

5‐50MW

MunicipalApplications DistrictEnergySystems,WastewaterTreatmentFacilitiesK‐12Schools

500kW

ResidentialStructures Multi‐FamilyHousingPlannedCommunities 5‐500kWe

ExampleDescriptionofCHPPotentialxxxi

Atypicalcollegeoruniversitycampusmighthavea5MWsimple‐cyclegasturbine.Steam(orhotwater)isproducedinanunfiredheatrecoverysteamgeneratorandsentintoacentralthermalloopforcampusspaceheatingduringwintermonthsortosingle‐effectabsorptionchillerstoprovidecoolingduringthesummerxxxii

15

FuturetechnologicaldevelopmentsxxxiiiBytheearly1980s,gasturbineshaddevelopedenoughtechnologicallyintermsoftheirefficiencyandreliabilitytobecomeusedinmanydifferentapplications.Withefficiencyratingsexceeding70%,muchofthedevelopmentofCHPhasbeenconcentratedonusingnaturalgasafueltopowertheseturbines.However,withpushesintherenewableenergyspaceandtheemphasisonefficiencybeingextended,therehavebeendevelopmentsinotherareas,namelymicroturbinesandfuelcells.MuchofthisisdrivenbytheneedtoprovidesmallerCHPunitsthatcanbeplacedinbuildingsorhomesaswellbytheneedformoreenvironmentallyfriendlytechnologies.MicroturbinesxxxivMicroturbines,whicharesmallelectricitygeneratorsthatburngaseousandliquidfuelstocreatehigh‐speedrotationthatturnsanelectricalgenerator,beganfield‐testingin1997.Thesemicroturbinescanbeusedinpower‐onlygenerationorincombinedheatandpowersystems,justaslargergasturbinesareused.WithinCHPapplications,thewasteheatfromamicroturbineisusedtoproducehotwater,toeitherheatbuildings,driveabsorptioncooling,andtosupplyotherthermalenergyneeds.Amajoradvantageofmicroturbinesistheirabilitytooperateonavarietyofdifferentinputfuels–naturalgas,sourgases(highsulfur,lowBtucontent),andliquidfuelssuchasgasoline,kerosene,anddieselfuel/distillateheatingoil.Thisallowsforthepotentialhedgingofenergyinputcosts,asthepriceofnaturalgascanfluctuate,whichisillustratedinalatersection.FuelCellsxxxvFuelcelltechnologyisanothermajorareaofdevelopmentandhasthepotentialtoallowasmallsizedcelltopoweranentirehome.Theadvantageliesinthatfuelcellsproduceelectricitythroughachemicalreactionratherthanbyburningfuel,resultinginmuchloweremissionsthanitscompetitortechnologies.Thechemicalreactiondoes,however,producecarbondioxide,whichispollutant,butdoessoinmuchlowerquantities.Furthermore,thehigherefficiencyoffuelcellsallowsforlowerfuelusage,reducednoisepollution,andthelackofacentralizedsystem/generationplants.Asitstandsnow,fuelcellCHPsystemsareveryexpensiveandfocusedonthepremiumpowermarketwithaneedfortheadvancedbenefitsthatfuelcellsprovide.Finally,theNationalElectricCode(NEC)andtheNationalFireProtectionAssociation(NFPA)codeswillapplytofuelcellsusedinresidentialapplications;however,regulationsconcerningtheconnectionoffuelcellswiththehomeelectricalsystemarestillbeingdeveloped.SolarCHPxxxviAnothertechnologythatisindevelopmentpresentsaveryuniquedynamicwith

16

combinedheatandpowersystems.Thepotentialforphotovoltaicandsolarthermaltechnologieshasbeenpresentedthroughdecadesofresearch;however,thesetechnologiesareamongthemostexpensivesourcesofrenewablepower.WiththedevelopmentofconcentratingsolarPV‐thermalhybridtechnologies,otherwisereferredtoasSolarCHP,couldpotentiallyreducethecostofsolarpowerbymakinguseoftheelectricalandthermalenergycapturedbyacollectorwhilereducingthematerialscostthroughconcentration.Thesystemmakesuseofthermalenergytooffsetconventionalfuelconsumption.TherearealreadypatentedsolarCHPsystemsinthedevelopmentphase,lookingforopportunitiestocommercialize.ThepotentialforsolarCHPisemerging,andwhileitdoesnothavethecloutofmicroturbinesandfuelcells,itdoeshavetheinvestmentandresearchfuelingitsadvancement.

17

PolicyEnvironment

Introduction

ThepolicyenvironmentinwhichtheCHPindustryoperatesismulti‐faceted;energypolicyisuniqueandcomplicatedbynatureoftheelectricitygridinfrastructure.TheFederalEnergyRegulatoryCommissionhasauthorityoverinter‐,butnotintra‐stateelectricitysales,whichmeansthatstateelectricitypolicyhasanenormouseffectonCHPoutcomes.CurrentpolicieseffectingCHPcanbebroadlysplitintotwocategories.FinancialpoliciessuchastaxcreditstoencourageprivateinvestmentinCHPandgovernmentfundingofResearchandDevelopmentprojectsexistonboththestateandfederallevel,butaremoreinfluentialonafederalscale.RegulatorypoliciesandinstitutionalsystemsdemonstratehugevariabilityacrossstatesandarepurportedtobeoneofthemostimportantfactorsintheadoptionofCHP.Ouranalysissectionwillfurtherexplorethisnotioninhopesofidentifyingthemostimportantobstaclesfacingtheindustry.FundingandFinancialIncentives–FederalLevelAllfederallevelpolicyimpactingtheCHPmarketplacecomesintheformofincentives.Whilesomenon‐fiscalfederalpoliciesdoimpactCHPindirectlythroughelectricitygridregulationsthroughFERCandotherinterstatecommerceissues,thepoliciesthataremostinfluentialtoCHPdevelopmentaretheresultofdirectfundingandincentives.TheFederalInvestmentTaxCreditandProductionCredit,FederalTaxDepreciationSchedules,ResearchandDevelopmentfunding,andotherinitiativesliketheCHPPartnershipcomprisethenationalpolicyspacefacingCombinedHeatandPowersystems.NaturalGasTurbineCHPsystemsareabletotakeadvantageofmostnationalfundingresources,detailedhere.FederalCHPInvestmentTaxCreditTheEnergyImprovementandExtensionActof2008createdatenpercentinvestmenttaxcredit(ITC)forthecostsofthefirst15MWofCHPproperties.Toqualifyforthetaxcredit,theCHPsystemmustproduceatleast20percentofitsusefulenergyaselectricityandtwentypercentintheformofusefulthermalenergy.TheITCisonlyextendedtosystemssmallerthan50MWandtonaturalgasturbinesystems(orothernon‐biomassfueledsystems)thatachieveatleastsixtypercentefficiency.TheITCmaybeusedtooffsetthealternativeminimumtax,andtheCHPsystemmustbeoperationalintheyearinwhichthecreditisfirsttaken.TheAmericanRecoverandReinvestmentActof2009extendedthescopeoftheFederalCHPInvestmentTaxCreditbyextendingtheoptionofagrantofequalvalueinlieuofataxliabilityreduction.QualifiedEnergyConservationBonds(QECB)The2007EnergyIndependenceandSecurityActcreatedafundingmechanismsimilartoCleanRenewableEnergyBonds,andsimilartootherProductionTaxCredits,whichawardsbondsintheformoftaxcreditsinsteadofpayingoutinterest.Thesystemoperatesbyauthorizingstate

18

andlocalgovernmentstoissueQECBsandfundsupto$800millionthroughtheIRS.The2009stimulusincreasedthebondingauthorityby$2.4billion.FederalBonusDepreciationSchedulesBusinessesmayrecoverinvestmentsincertainpropertythroughdepreciationdeductions.Thispolicyestablishesasetofclasslivesforvarioustypesofproperty,rangingfromthreeto50years,overwhichthepropertymaybedepreciated.ThebonusdepreciationscheduleallowsbusinessestotakehalfofthedepreciationvalueofCHPpropertyoffoftheirtaxliabilityforthefirstyear,andtheremaininghalfoverthecourseofthenextfouryears.

FederalResearchandDevelopmentGrantsTwoprogramscurrentlyexistonthefederalleveltodirectlystimulateinnovationintheCHPsector.TheDepartmentofEnergyClimateChangeTechnologyProgramprovides$3milliontoencourageresearch,development,demonstrationanddeploymentoftechnologytoreducegreenhousegasemissions.TheDOE’sInventionsandInnovationsProgramoffersfinancialandtechnicalsupportthroughcompetitivegrantsforresearchanddevelopmentofinnovative,energy‐savinginventions.OtherGrants,RebatesandLoansTheFederalGovernmentprovidesfundsforavarietyofcompetitivegrantandloanprogramsforrenewableenergyandenergyefficiencyprograms,forwhichCHPsystemsmaybeeligible.Theseinclude:

• TheRuralEnergyforAmericaProgram,forwhichagriculturalproducersareeligibletoreceivegrantsfor25%ofcostsorloansfor75%ofcosts.

• TheAdvancedPowerSystemsTechProgram,partofthe2005EnergyPolicyAct,offersarebateof1.8centsperkWhofelectricitygenerationuptothefirst10millionkWhperyear.

• EnergyEfficiencyandConservationBlockGrantprovides$3.2billioninformulaandcompetitivegrantstolocalandstategovernmentsforenergyefficiencyimprovementsinordertoreduceenergyuseandfossilfuelemissions.

• DOEEnergyEfficiency/RenewableEnergyLoanGuaranteesunderthe2005EnergyPolicyActoffers$10billionforenergyefficiency,renewableenergyandadvancedtransmissionanddistributionprojectsforupto100%oftheamountofaloanthatfundsupto80%oftotalprojectcosts.

• EnergyEfficientCommercialBuildingsTaxDeduction• EnergyOpportunitiesProgram:Rebate• StateEnergyProgram:Providesgrantstostates• DOEGrantProgram:DeploymentofCHPSystems,DistrictEnergySystems,Waste

EnergyRecoverySystems,andEfficientIndustrialEquipment• CombinedHeatandPowerSystemsTechnologyDevelopmentDemonstration• WasteEnergyRecoveryRegistryandGrantProgram

19

StateFinancialIncentivesHundredsofstateprogramsexistintheformofgrants,rebates,loans,loanguarantees,andtaxincentives.CHPPartnership(EPA)In2001,theDepartmentofEnergy(DOE)andU.S.EnvironmentalProtectionAgency(EPA)havecollaboratedtoestablishtheCHPPartnership,avoluntaryprogramaimedatencouragingCHPgrowthintheUnitedStates.Thepartnershipfostersrelationshipsbetweeninterestedstakeholdersincludingindustry,state,andlocalgovernments,andpromotesenergyefficientCHPtechnologiesxxxvii.RegionalApplicationCentershavebeenestablishedthroughthePartnershipthattargetCHPdevelopmentbyregion,providinganalysisandinformationforthoseinterestedinCHPsystems.ThisPartnershipprovideseducationandoutreachactivitiestohelppromotegrowthintheCHPsector.

RegulatoryandInstitutionalBarriersFinancialincentivesareoneaspectofthepolicyarenaaffectingCHPdevelopment.OtherlimitstoCHPadoptionresultfromregulatoryandinstitutionalbarrierslocatedmostlyatthestate‐levelofgovernment.xxxviiiTheseregulationscanencourageorinhibitadoptionofCHPfacilities.BecauseCHPandotherformsofdistributedgenerationoperateunderabroadframeworkofenergyproduction,distributionandregulation,changesinthisframeworkcaninfluencetheextenttowhichCHPisdeveloped.xxxixDescribedbelowisacomprehensivelistofregulatorybarriers,andsuggestionsastohowstateregulationsmightbestreamlinedtoappropriatelyincentivizeCHPapplication.InterconnectionstandardsInterconnectionistheabilityofanonutilitygeneratortooperatewhileconnectedtotheelectrictransmission/distributionsystem.MostCHPfacilitiesmustinterconnecttotheelectricgridforbackuppower,incasethefacilitycannotgenerateenoughelectricityonitsown,orintheeventthatitexperiencesanoutage;aswellastosellbackanyexcesspoweritproduces.WhileCHPsystemsmayimprovethereliabilityofthegridbyreducinggridcongestion,manystatesdonotfacilitateconnectiontothegrid.Thereisagenerallackofuniformityinprocessesandfees,andtheenforcementofcurrentstandardsmakesitdifficultformanufacturerstodesignand/orproducemodularpackagesthatmaybesoldinlargequantities.xlThisreducestheincentiveforCHPimplementation,particularlyforsmall‐scalesystemsthatmustpredictthecostsandrequirementsforaccesstothegrid.Thereisalsoaproblemwithjurisdiction,whichissplitbetweentheFederalEnergyRegulatoryCommission(FERC)andthestates’utilityregulatorybody.Currently,eachutilityandserviceterritoryestablishesitsowninterconnectionrules.Modelsandprocedureshavebeendevelopedbyfederalagencies,butnonearemandatoryorenforceable.TheInstituteofElectricalandElectronicEngineers(IEEE)developedIEEE1547StandardforDistributedResourcesInterconnectedwithElectricPowerSystems,whichoutlinesproceduresandrequirementsforthetesting,operation,safetyandmaintenanceoftheinterconnectionofdistributedresources.TheEnergyPolicyActof2005requiredstate

20

commissionstoconsiderthestandardsproposedbyIEEEbutdidnotmandateadoptionofthestandards.xli

Fifteenstateshaveadoptedinterconnectionstandardsthatarefavorabletodistributedgeneration.Thestandardsestablishclearguidelinesthatstreamlinetheprocess,aswellasprovidetechnicalrequirementsthatreduceinterconnectionandcostuncertainty.xlii

UtilityRateStructures/DecouplingManyutilityratestructuresprovideutilitieswithadisincentivetopromoteenergyefficiency,includingCHPsystems.BylinkingutilityrevenueswithnumberofkWhsold,utilitiesbenefitfrommaximumelectricaloutputxliii.Itinhibitscompaniesfromsupportingmoreefficientenergyresources.Decouplingprogramstodisassociaterevenuesfromsalesforceutilitiestoappropriatelyvalueefficiencyandsavedcosts,makingCHPimplementationeasier.Thisbetteralignsutilities’profitmotiveswiththegoalofprovidingpowerattheleastcosttoconsumers.xlivOtherexamplesofmisalignedrateincentivesincludehighstandbychargesforCHPsystems,makingCHPratestoocostlytocompetewithbaseloadpower;penaltiesforusingelectricityfromthegridduringunplannedoutages;lowerratesforcompaniesconsideringCHP,makingCHPlessattractive;andcostlyexitfees.AlloftheseadditionalcostscanmakeCHPinstallationsprohibitivelyexpensiveforsmallerinstallations,andperhapsforlargerfacilitiesaswell.xlvCurrently,eightstateshaveadoptedstandardsthatvaluethetruecostsandbenefitsofdistributedgeneration,includingCHP.RenewablePortfolioStandardsRenewablePortfolioStandards(RPS)arestate‐adoptedpoliciesthatrequireutilityproviderstogenerateapercentageoftheirenergygenerationfromrenewableenergysourcesbyaparticulardate.RenewablePortfolioStandardsareestablishedtopromotethegrowthofrenewableenergyaspartofastate’soverallenergyportfolio.Currently,24stateshaveRPSinplace,althoughtherequirementsandgoalsdifferbystate.FourteenstateshaveRPSsthatincludeCHPasaneligibletechnology.xlviAdoptingRPSstandardsthatincludeCHPwouldencourageutilitiestomaketheprocessofCHPimplementationeasierforfacilitiesofallsizesbecausegrowthintheCHPsectorwouldbeessentiallymandatedbythestate.Output‐BasedRegulationsandPermittingPolicies

Output‐basedemissionsregulations,asairpollutioncontrolmechanisms,limitemissionsbasedonemissionsoutput,ratherthaninput.Traditionally,stateshaveplacedenvironmentalregulationsontheinputofemissionsxlvii,thefuelthatgoesintoapowerplantorenergy‐usingfacility.BecauseCHPsystemsmayusemoreinputfuelthanconventionalsystems,inputregulationsdiscourageCHPimplementation.Output‐basedregulations,however,encouragetheadoptionofCHPbecauseittakesintoaccountenergyefficiency.CHPsystemsuselessfuelperunitofoutputthanaconventionalsystem,andtheenergysavingswouldbeincorporatedintooutput‐basedregulations.xlviiiTheenergysavingsgainedfromaCHPsystemisshowninFigure5.Currently,twelvestateshaveadoptedoutput‐basedregulationsstandardsthatreflectefficiencyimprovementsaspollutionprevention.

21

AnexampleofafederalenvironmentalpermittingbarrieristheCleanAirAct’sNewSourceReview(NSR),whichrequireslargepoint‐sourcepolluterstoinstallpollutioncontrolcomponents.ThesecomponentscansometimesinterferewithCHPadoption,furtherreducingincentivestoinstallCHP.xlix

ElectricityRestructuring

Electricityrestructuringreferstothederegulationoftheelectricitymarket,orthemovementfromthetraditionallyregulatedmonopolysystemtowardscompetitivemarkets.DeregulationchangesthelandscapeunderwhichCHPsystems(andthepowerindustryasawhole)operate.Beginningintheearly1990s,federalinitiatives,includingPURPAandtheEnergyPolicyActof1992beganencouragingcompetitionintheelectricitymarket.lStateregulatorsbeganinvestigatingrestructuringaroundthatsametime,andtherearecurrentlyfourteenstatesthathaverestructuredtheelectricindustrytomakeutilitiesmorecompetitive.Eightstateshavesuspendedrestructuringactivities.liAlthoughsomebasicfeaturesofrestructuringpoliciesareconsistentacrossstates,detailsofthelegislationvarygreatly.CompetitionintheelectricitymarketwillprovideopportunityforCHPadoption,althoughvariationsbetweenstatesmaketheeffectdifficulttopredict.

NetMetering

Netmeteringallowsutilitycustomerstooffsetallorpartoftheirelectricityneedsbyproducingtheirownelectricity,andsellingexcesspowerbackataone‐to‐onecreditperkWh.liiNetmeteringencouragesinvestmentinrenewableenergyandenergyefficiencytechnologies,andmayimprovetransmissiongridreliabilityifconsumersareproducingelectricityduringpeakperiods.liiiInconjunctionwithinterconnectionstandards,netmeteringisthoughttohelpencourageCHPexpansionbyloweringcoststoentertheelectricitymarket.AsofAugust2009,forty‐twostateshaveadoptednetmeteringpolicies.Ofthose,fifteenstatesallowCHPasaneligibletechnologyfornetmetering.liv

22

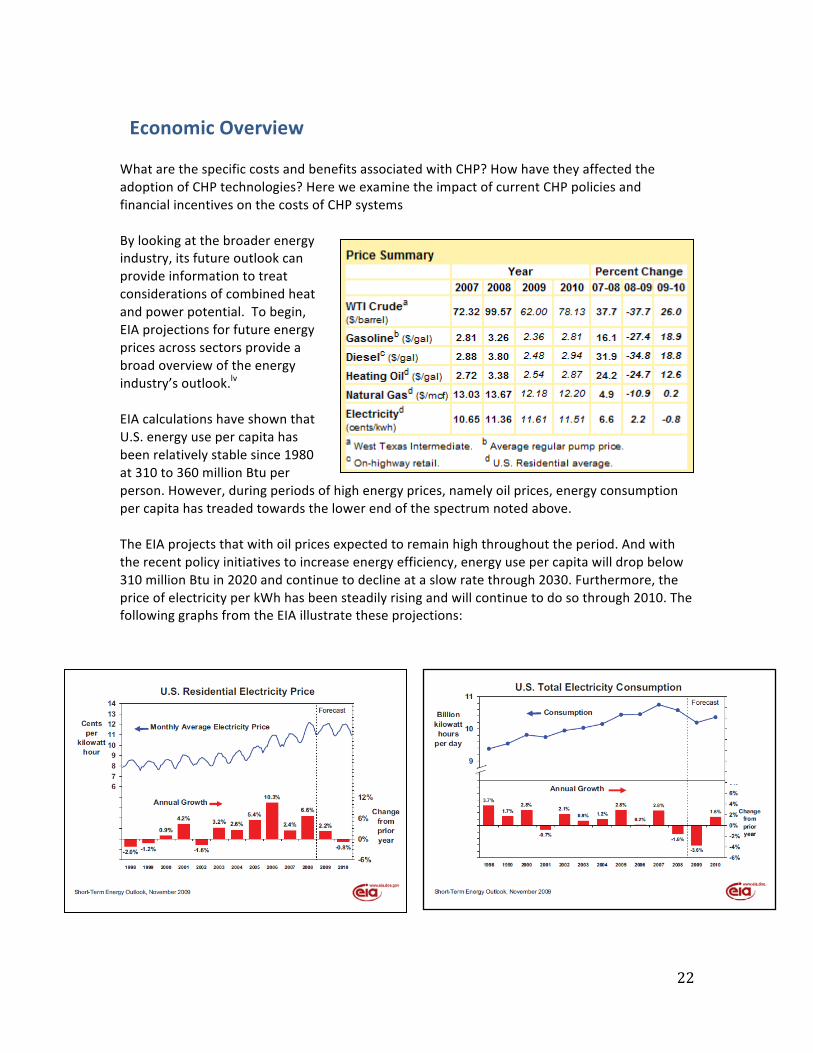

EconomicOverviewWhatarethespecificcostsandbenefitsassociatedwithCHP?HowhavetheyaffectedtheadoptionofCHPtechnologies?HereweexaminetheimpactofcurrentCHPpoliciesandfinancialincentivesonthecostsofCHPsystemsBylookingatthebroaderenergyindustry,itsfutureoutlookcanprovideinformationtotreatconsiderationsofcombinedheatandpowerpotential.Tobegin,EIAprojectionsforfutureenergypricesacrosssectorsprovideabroadoverviewoftheenergyindustry’soutlook.lvEIAcalculationshaveshownthatU.S.energyusepercapitahasbeenrelativelystablesince1980at310to360millionBtuperperson.However,duringperiodsofhighenergyprices,namelyoilprices,energyconsumptionpercapitahastreadedtowardsthelowerendofthespectrumnotedabove.TheEIAprojectsthatwithoilpricesexpectedtoremainhighthroughouttheperiod.Andwiththerecentpolicyinitiativestoincreaseenergyefficiency,energyusepercapitawilldropbelow310millionBtuin2020andcontinuetodeclineataslowratethrough2030.Furthermore,thepriceofelectricityperkWhhasbeensteadilyrisingandwillcontinuetodosothrough2010.ThefollowinggraphsfromtheEIAillustratetheseprojections:

23

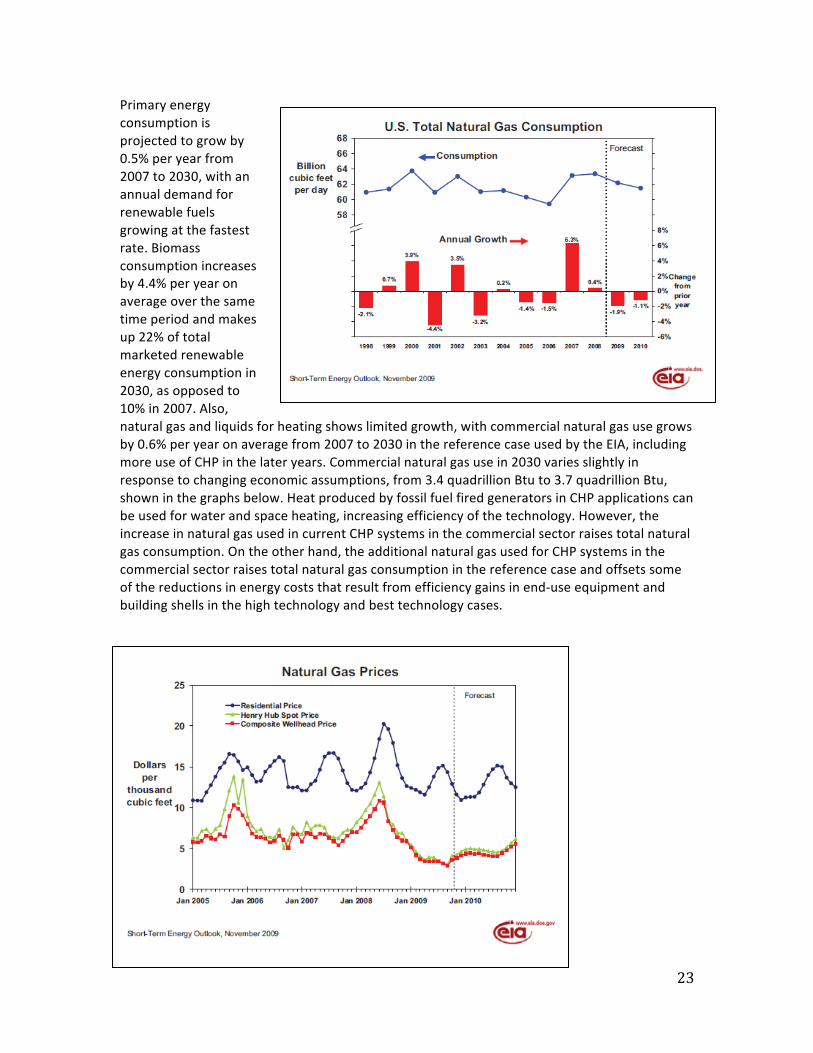

Primaryenergyconsumptionisprojectedtogrowby0.5%peryearfrom2007to2030,withanannualdemandforrenewablefuelsgrowingatthefastestrate.Biomassconsumptionincreasesby4.4%peryearonaverageoverthesametimeperiodandmakesup22%oftotalmarketedrenewableenergyconsumptionin2030,asopposedto10%in2007.Also,naturalgasandliquidsforheatingshowslimitedgrowth,withcommercialnaturalgasusegrowsby0.6%peryearonaveragefrom2007to2030inthereferencecaseusedbytheEIA,includingmoreuseofCHPinthelateryears.Commercialnaturalgasusein2030variesslightlyinresponsetochangingeconomicassumptions,from3.4quadrillionBtuto3.7quadrillionBtu,showninthegraphsbelow.HeatproducedbyfossilfuelfiredgeneratorsinCHPapplicationscanbeusedforwaterandspaceheating,increasingefficiencyofthetechnology.However,theincreaseinnaturalgasusedincurrentCHPsystemsinthecommercialsectorraisestotalnaturalgasconsumption.Ontheotherhand,theadditionalnaturalgasusedforCHPsystemsinthecommercialsectorraisestotalnaturalgasconsumptioninthereferencecaseandoffsetssomeofthereductionsinenergycoststhatresultfromefficiencygainsinend‐useequipmentandbuildingshellsinthehightechnologyandbesttechnologycases.

24

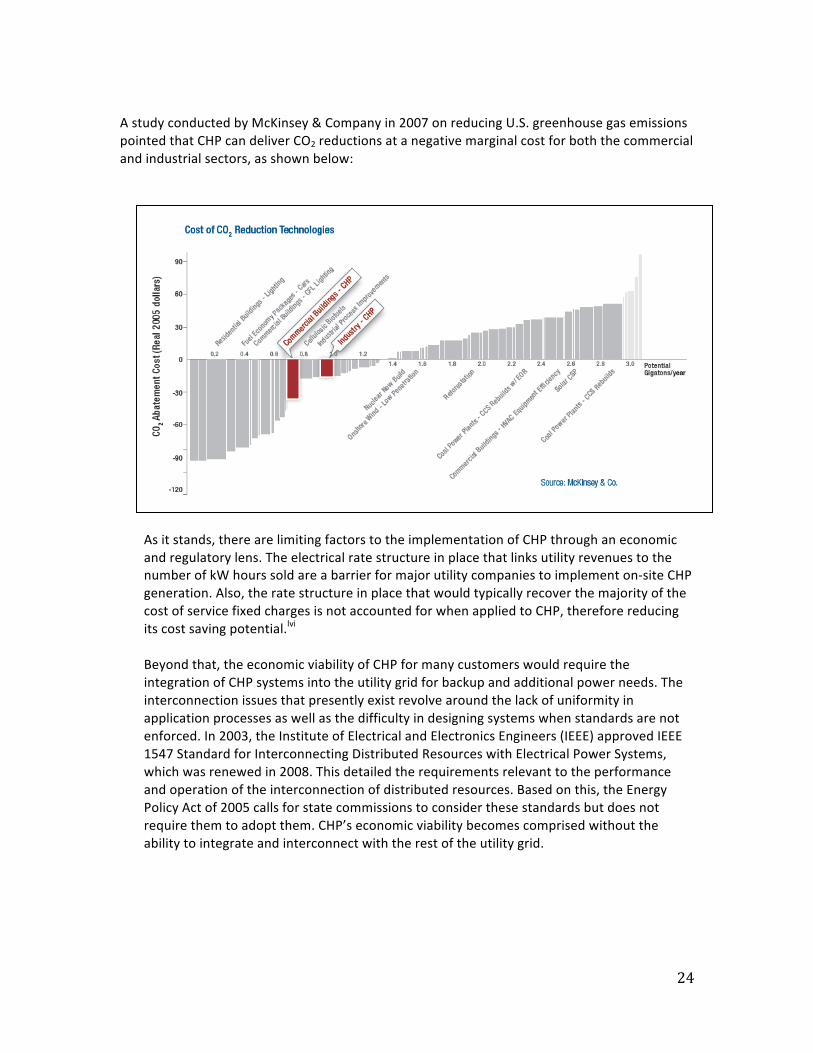

AstudyconductedbyMcKinsey&Companyin2007onreducingU.S.greenhousegasemissionspointedthatCHPcandeliverCO2reductionsatanegativemarginalcostforboththecommercialandindustrialsectors,asshownbelow:

Asitstands,therearelimitingfactorstotheimplementationofCHPthroughaneconomicandregulatorylens.TheelectricalratestructureinplacethatlinksutilityrevenuestothenumberofkWhourssoldareabarrierformajorutilitycompaniestoimplementon‐siteCHPgeneration.Also,theratestructureinplacethatwouldtypicallyrecoverthemajorityofthecostofservicefixedchargesisnotaccountedforwhenappliedtoCHP,thereforereducingitscostsavingpotential.lviBeyondthat,theeconomicviabilityofCHPformanycustomerswouldrequiretheintegrationofCHPsystemsintotheutilitygridforbackupandadditionalpowerneeds.Theinterconnectionissuesthatpresentlyexistrevolvearoundthelackofuniformityinapplicationprocessesaswellasthedifficultyindesigningsystemswhenstandardsarenotenforced.In2003,theInstituteofElectricalandElectronicsEngineers(IEEE)approvedIEEE1547StandardforInterconnectingDistributedResourceswithElectricalPowerSystems,whichwasrenewedin2008.Thisdetailedtherequirementsrelevanttotheperformanceandoperationoftheinterconnectionofdistributedresources.Basedonthis,theEnergyPolicyActof2005callsforstatecommissionstoconsiderthesestandardsbutdoesnotrequirethemtoadoptthem.CHP’seconomicviabilitybecomescomprisedwithouttheabilitytointegrateandinterconnectwiththerestoftheutilitygrid.

25

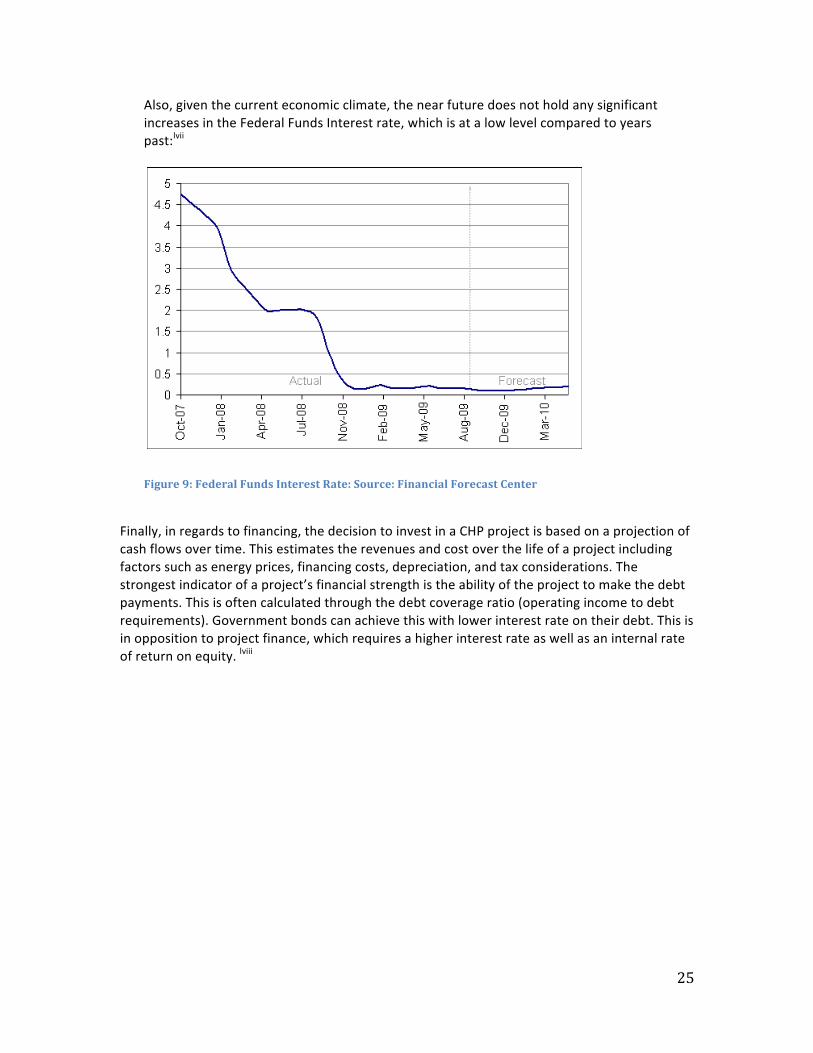

Also,giventhecurrenteconomicclimate,thenearfuturedoesnotholdanysignificantincreasesintheFederalFundsInterestrate,whichisatalowlevelcomparedtoyearspast:lvii

Figure9:FederalFundsInterestRate:Source:FinancialForecastCenter

Finally,inregardstofinancing,thedecisiontoinvestinaCHPprojectisbasedonaprojectionofcashflowsovertime.Thisestimatestherevenuesandcostoverthelifeofaprojectincludingfactorssuchasenergyprices,financingcosts,depreciation,andtaxconsiderations.Thestrongestindicatorofaproject’sfinancialstrengthistheabilityoftheprojecttomakethedebtpayments.Thisisoftencalculatedthroughthedebtcoverageratio(operatingincometodebtrequirements).Governmentbondscanachievethiswithlowerinterestrateontheirdebt.Thisisinoppositiontoprojectfinance,whichrequiresahigherinterestrateaswellasaninternalrateofreturnonequity.lviii

26

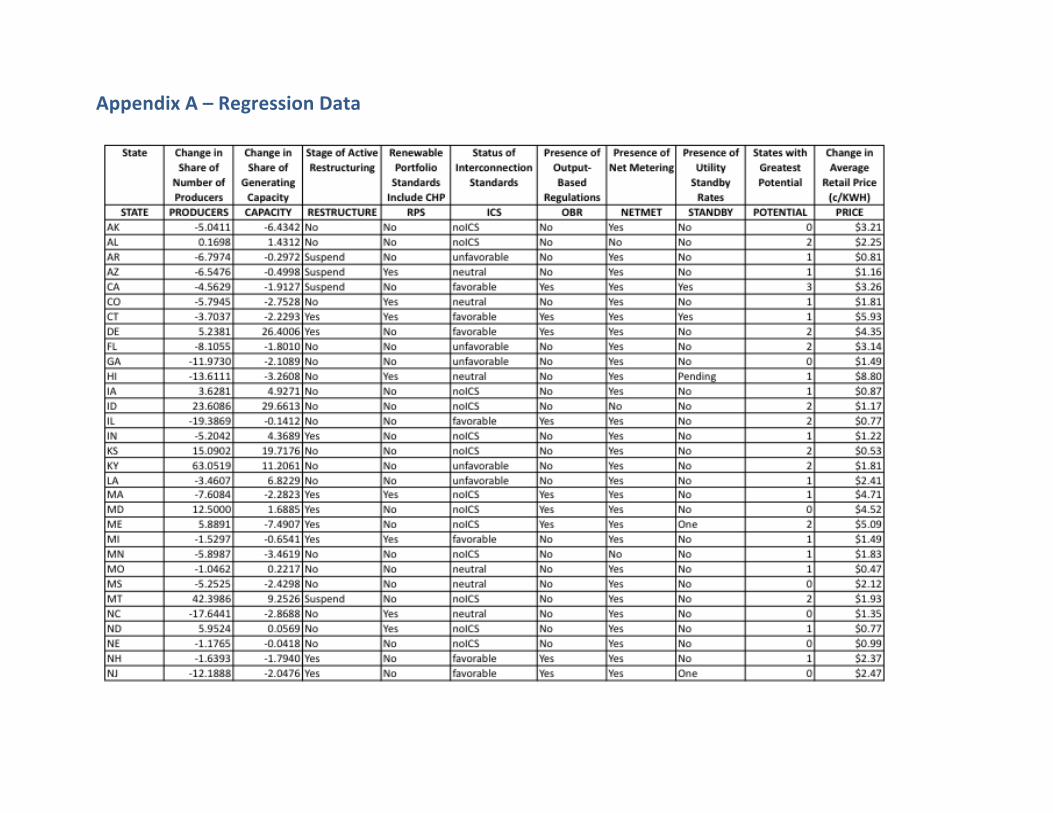

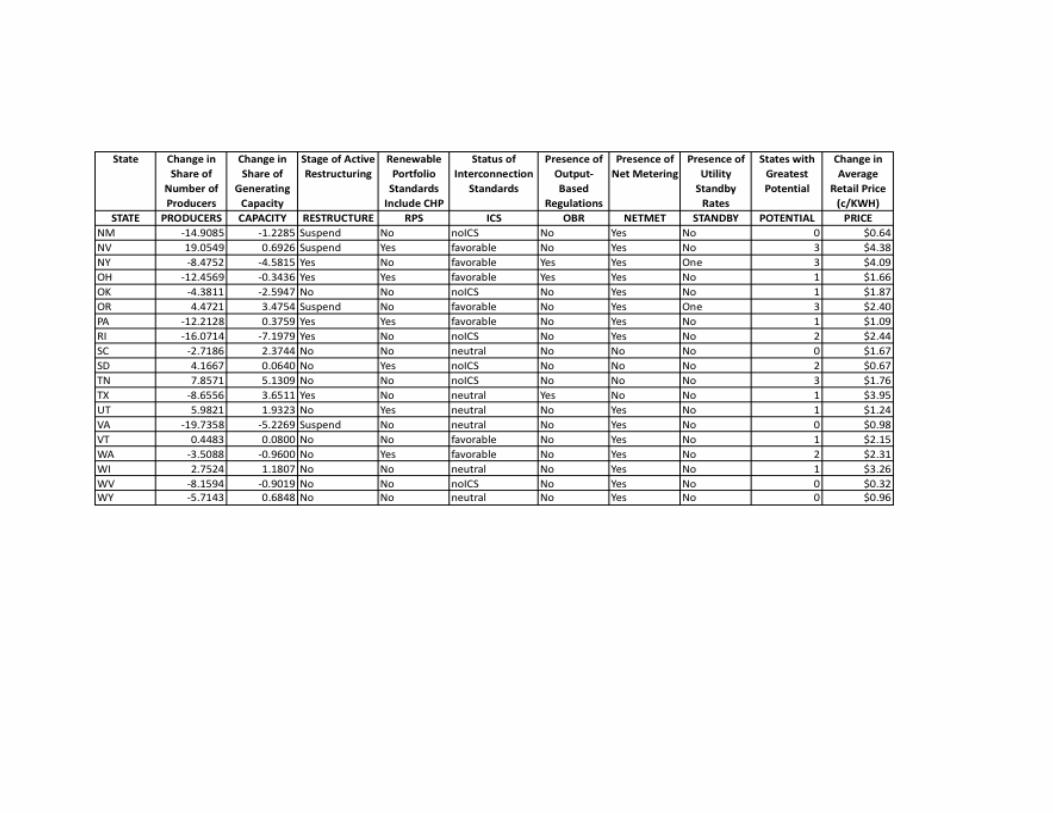

AnalysisPartOne:StatisticalAnalysisofStatePoliciesIntroductionStrongsupportersofCHPgrowthexistacrossthenationinalllevelsofgovernment,privatesectorandnon‐profitgroups.Inthe1990stheU.S.EPAandDOEtookonthegrowthoftheCHPsectorasagoalatbothagencies,whichresultedinthecreationoftheEPACHPPartnership,eightRegionalCHPApplicationCenters,theDOECHPApplicationsProgramandincreasedresearchatDOENationalLaboratories.TradeorganizationsintheprivatesectorliketheUnitedStatesCleanHeatandPowerAssociation,interestgroupsliketheNortheastCombinedHeatandPowerInitiative,andadvocacyorganizationsliketheAmericanCouncilforanEnergyEfficientEconomyandtheRegulatoryAssistanceProjectallvaryintheirapproachestoadvocatingforCHPadoption,buttheyallsharethegoalofremovingbarrierstoCHPdevelopment.AcrossthespectrumofthesegroupsandtheassociatedliteratureistheassertionthatunfavorableregulationsatthestatelevelarethemostnumerousandinfluentialbarriersfacingtheadvancementofCHPsystems.Despitethebreadthofmaterialregardingtheremovalofinconsistenciesinstandards,fees,permittingproceduresandotherstateregulationsdetailedabove,thereisalackofstatisticalanalysisofthedirecteffectofpoliciesonthegrowthoftheCHPindustry.Here,weattempttoaddtothecurrentknowledgeofthemostimportantchallengesfacingtheCombinedHeatandPowerIndustry.CanincreasesanddecreasesintheamountofelectricitygeneratedfromCHPsystemsonastate‐by‐statebasisfrom1997to2007beexplainedbytheintroductionoreliminationoffavorablepolicieswithinthattimeperiod?MethodologyWeperformedalogisticregressiontoassessthesignificanceofsevencategoricalvariablesandonecontinuousvariableagainstthedependentvariableofthechangeintheshareofCHPgeneratingcapacity.ResultswereevaluatedwithT‐tests,usingP‐ValuesandAdjustedR‐Squaredstatistics.ThesourcesforthedatasetincludetheDOE’sEnergyInformationAdministration(EIA),EPA,OakRidgeNationalLaboratory(ORNL)andtheDatabaseofStateIncentivesforRenewables&Efficiency(DSIRE),whichisfundedbytheDOE’sOfficeofEnergyEfficiencyandRenewableEnergy(EERE)andoperatedbytheNationalRenewableEnergyLaboratory(NREL).DependentVariableTheDependentVariablewascreatedwithstatisticsfromtheEnergyInformationAdministration’sreport,ElectricPowerAnnual2007–StateDataTables.lixThestatisticshowingtheNameplateCapacityofallsectorsofelectricityproducerswascomparedtotheNameplateCapacityfromonlytheCHPsector.WenormalizedtheCHPcapacityinMWbythetotalcapacity

27

inordertoshowthevariableasachangeinpercentageoftotalstateelectricityproduction.Weperformedthesamestepsforthedatafrom1997andmeasuredthechangeinthepercentageoftotalstatecapacitycontributedbyCHPsystemsovertheten‐yearperiodofthestudy.IndependentVariablesInterconnectionStandards(ICS)In2008,theEPAevaluatedinterconnectionstandardstodeterminewhichstateshadinterconnectionstandards,andspecifically,whetherornotthosestandardsfavoreddistributedgeneration.Theirassessmentwasbasedonthefollowingcriteria:standardinterconnectionforms,simplifiedprocedureforsmallersystems(>10kW),timelineforapplicationapproval,systemsizelimits,insurancerequirements,andtechnicalrequirements.ThecategoriesusedintheanalysisforthispaperaretakendirectlyfromtheEPA’sassessment.Thevaluesattachedwitheachcategoryandtheirmeaningsinclude:

0.Unfavorable:Policyinplace,buthasunfavorableattributessuchashighfeesandinsurancerequirements,ormayonlyallowsmallsystemstointerconnect.1.NoICS:Nopolicyinplace.2.Neutral:Policyinplace,butitdoesn’tfavorDGspecifically.3.Favorable:Welldefinedpolicywithatleastonebeneficialattribute

RenewablePortfolioStandards(RPS)DatacamefromtheEPA,whohaslistedthestatesthathaverenewableportfoliostandardsandplace,andspecifically,whichstatesincludeCHPorwasteheatrecoverysystemsaseligibletechnologies.lxForthepurposesofthispaper,stateswereidentifiedaseitherhavinganRPSthatincludesCHPornot:

0.No1.Yes

OutputBasedRegulations(OBR)DatacamefromtheEPA,wholiststhestatesthatcurrentlyhaveoutputregulations.lxiForthispaper’sanalysis,thevariableidentifieswhetherornotastatehasadoptedregulations:

0.No1.Yes

ElectricityRestructuring(Restructure)DatacamefromtheEIA,whohasidentifiedwhichstateshaveundergoneelectricityrestructuringandhasincludedalistofeachstate’sprocess,outliningtheprogressstateshavemadetodate.ThecategoriesusedintheanalysisforthispaperaretakendirectlyfromtheEIA’slistings.lxiiThecategoryandvaluesattachedwitheachinclude:

0.No1.Suspended2.Yes

NetMetering(NetMet)DatacamefromDSIREandliststhestatesthatincludeCHPasaneligibletechnologyfornetmetering:lxiii

0.No1.Yes

28

UtilityStandbyRates(Standby)In2008,theEPAassessedutilitystandbyratestoidentifywhichstateshaveratesthatvaluethecostsandbenefitsofdistributedgeneration.Tomeasurethis,theEPAreviewedthestandbyrateslistedinutilities'rateschedules,calledandquestionedutilitieswithnostandbyratelistedintheirratescheduleastohowtheychargecustomerswithon‐sitegeneration,andcalculatedhypotheticalelectricbillsacrosseachutility.lxivTheEPAevaluated91utilities,thetoptwoineachstate.ThecategoriesusedintheanalysisforthispaperaretakendirectlyfromtheEPA’sassessment.Thevaluesattachedwitheachcategoryandtheirmeaningsinclude:

0.No:Twoutilitiesthatonlyhaveconflictingratesornegativerates1.Pending:Statesareconsideringeffectivepolicies2.One:Effectivepolicyforonlyoneutility3.Yes:Effectivepolicyinplacefortoptwoutilities

PotentialORNLhasdevelopedalistofstateswiththegreatesttechnicalpotentialforCHPadoption.ThecategoriesusedintheanalysisforthispaperaretakendirectlyfromORNL’sassessment.Thevaluesattachedwitheachcategoryandtheirmeaningsinclude:

0.Potentialislessthan1,000MW1.Potentialbetween1,000‐3,000MW2.Potentialbetween3,000‐8,000MW3.Potentialisgreaterthan8,000MW

RetailPriceofElectricity(Price)WecreatedthecontinuousvariableofthechangeintheretailpriceofelectricityoverthetimehorizonofthestudyfromtheEnergyInformationAdministration’sreport,ElectricPowerMonthly‐2009.Thedataispresentedasthechangeintheaverageretailprice,incentsperkWh,ofelectricitytoultimatecustomersofallend‐usesectorsfrom1997to2007.

29

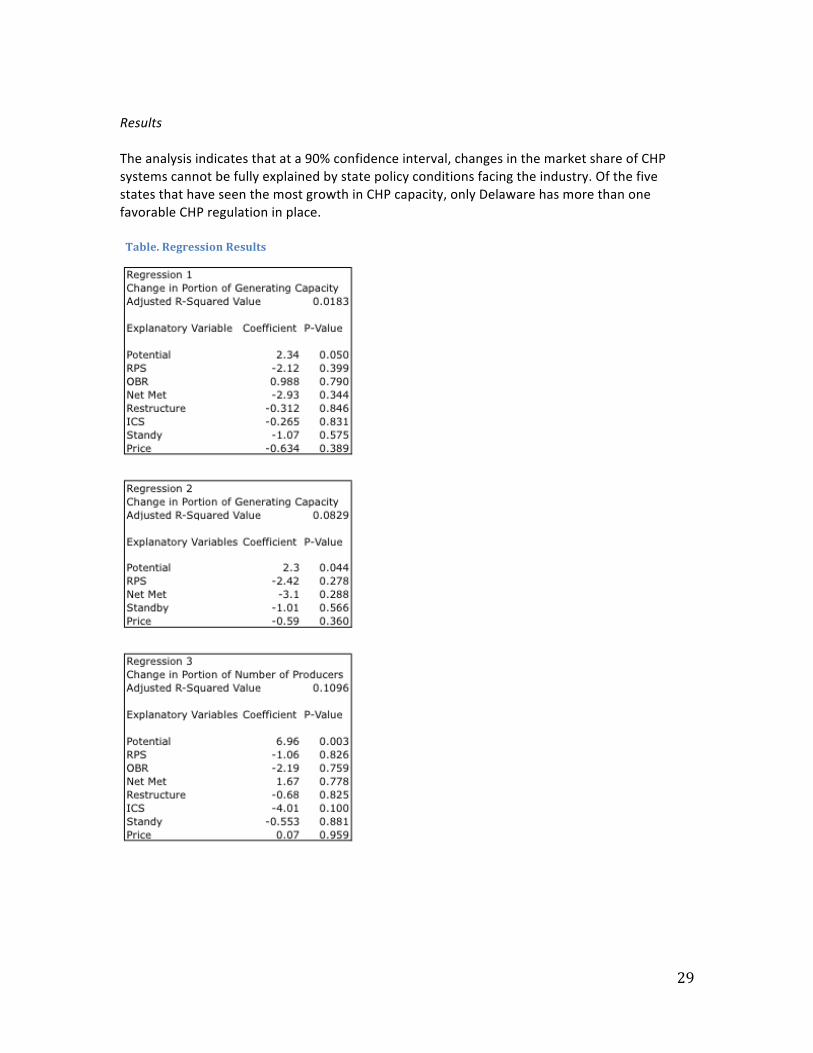

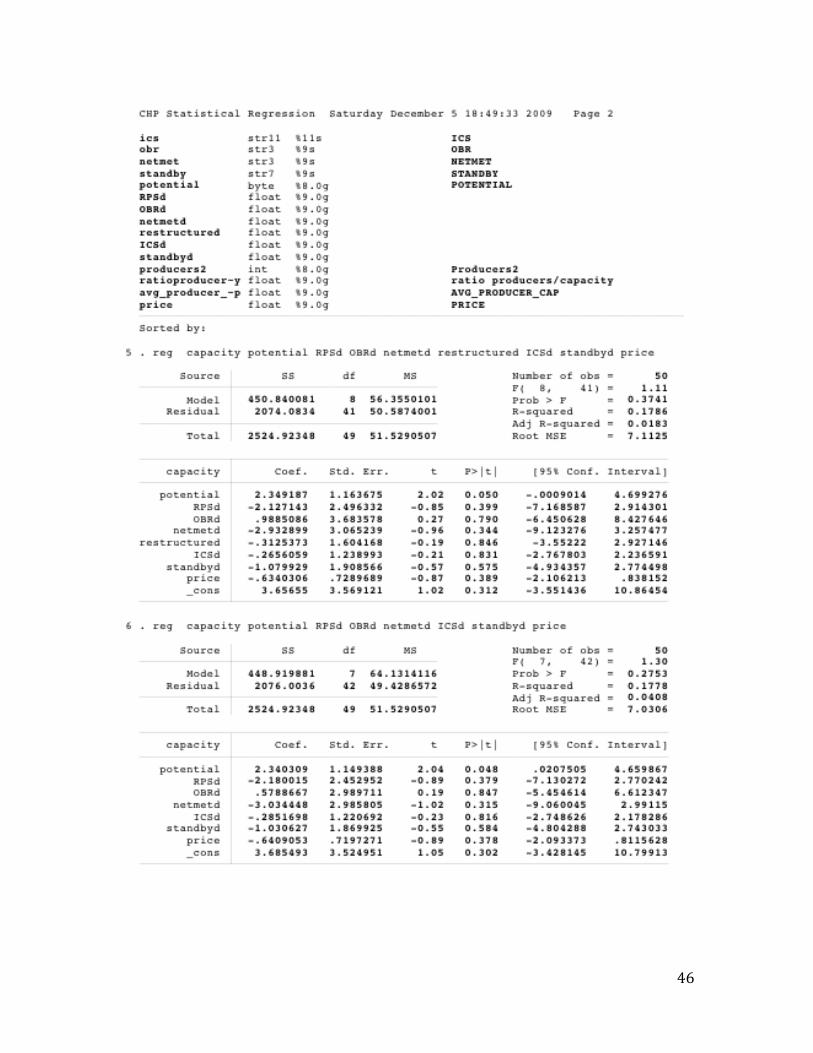

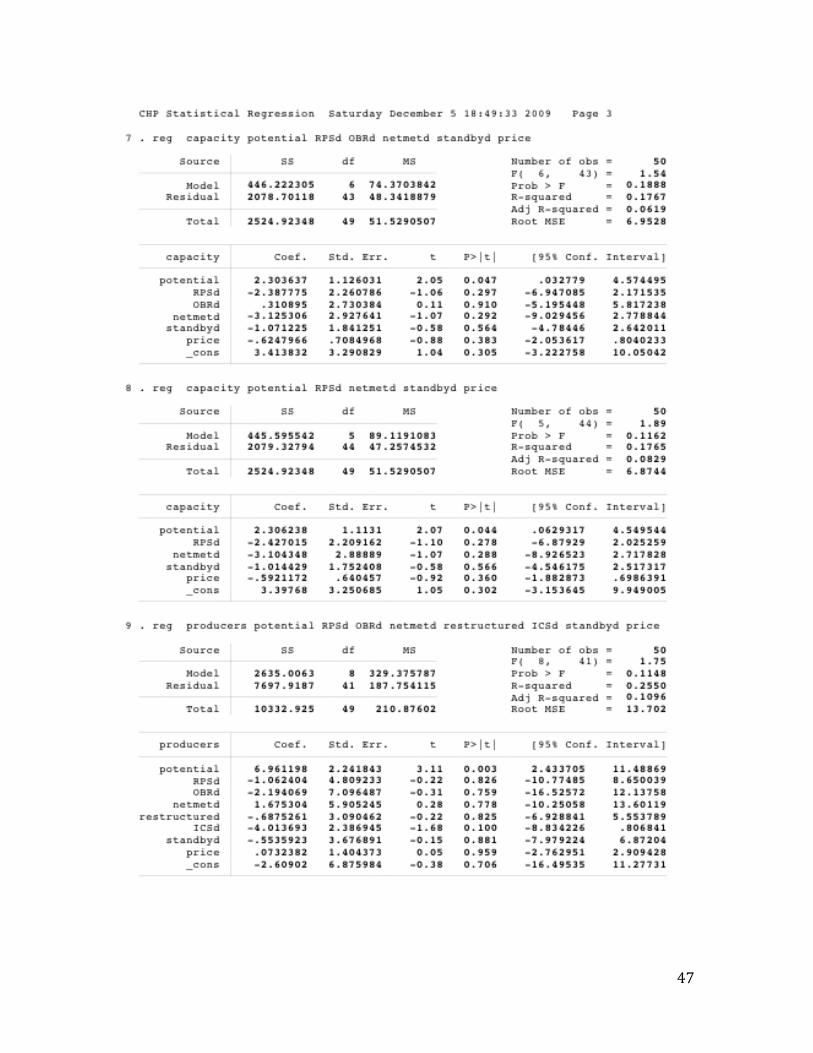

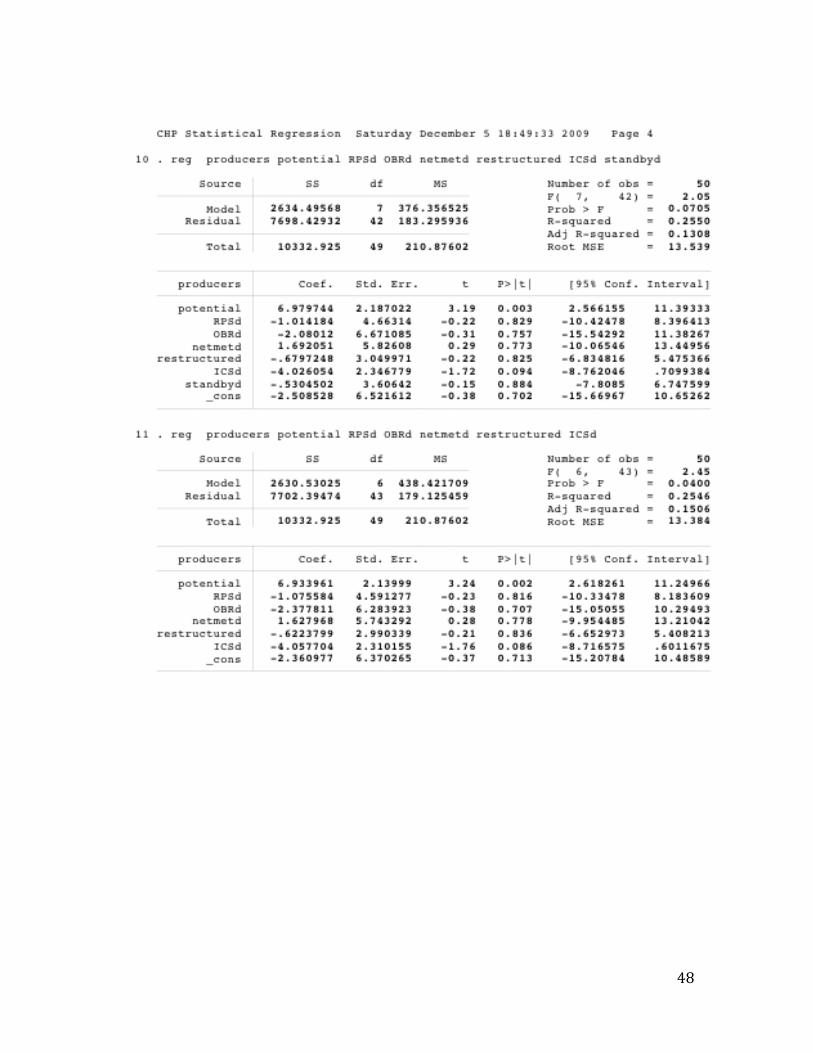

Results Theanalysisindicatesthatata90%confidenceinterval,changesinthemarketshareofCHPsystemscannotbefullyexplainedbystatepolicyconditionsfacingtheindustry.OfthefivestatesthathaveseenthemostgrowthinCHPcapacity,onlyDelawarehasmorethanonefavorableCHPregulationinplace.Table.RegressionResults

30

ImplicationsTheresultsimplythatthereareother,possiblymoresignificantfactorsthatexplaintheshareofelectricitygenerationfromCHPsystemsandtheshareofelectricityproducersoverthepasttenyears.Theanalysisdoesnotquantifyfinancialincentives,andtheymayplayamoresignificantrolethanpolicies.AstheCost‐BenefitAnalysis(Analysis2)shows,CHPisalreadycompetitiveinlarge‐scalesystems,meaningthatthegrowthwouldnotbeduetofavorablepolicies,butratherthecost‐effectivenessofCHPsystems.Thisargumentisstrengthenedbythefactthatduringtheyearscoveredinthisanalysis,muchofthegrowthwasconcentratedinlarge‐scalefacilities.AlthoughtheresultsindicatethatstateregulatoryandinstitutionalpoliciesdonotaffectCHPcapacitygrowth,itdoesnotnecessarilysuggestthatthepoliciesarecompletelyineffective.TheanalysiscoveredCHPgrowthduringtheyears1997‐2007,whichwereprobablyaresultofPURPAandmuchofthegrowthoccurredinlarge‐scalefacilities.ThetrendinCHPandelectricitygenerationingeneralismovingtowardsdistributedgeneration,asopposedtothetraditionalbaseloadpowerconfigurationthatexiststoday.StateregulationsthatfavorCHPwouldmakesmallerinstallationsmorecosteffective,andmayhaveamoresignificanteffectonCHPgrowthinthefuture.OpportunitiesForFurtherAnalysisAstatisticalanalysisoftherelationshipsbetweenfavorableCHPpoliciesandgrowthratesofthesectorcouldbeimprovedandexpandedbycreatingalargerdatabaseofpoliciesthatcouldshowdynamicpolicyvariables.Forthepurposesofourstudy,thesevariablesarestaticindicatorsthatoccurredduringthetimeperiodofthestudy.Ifchangesinpolicywereincludedfrombeforethetimehorizon,orwereexaminedonayearlybasis,wemightseemorenuancedresults.AnotheropportunityforfurtheranalysisistoexaminethepotentialtimelagbetweenCHP‐relatedpolicyimplementationandCHPnameplatecapacitychanges.Thescopeofthisstudydidnotincludefinancialincentivesofferedbystates;amoresophisticatedmodelthatincludedtheseindicatorscouldshedfurtherlightontherelationshipsinquestion.

31

AnalysisPartTwo:Cost‐BenefitAnalysisIntroduction

Inthisanalysiswecontinuetotryandidentify,throughacostbenefitanalysis,thefundingopportunitieswithhighestpotentialtoincreaseoptimaladoptionofCHPtechnologies.Aswehavealreadyindicated,thereisarangeoffederalandstateincentivesaimed,throughvariousmeasures,atencouragingtheadoptionofCHPtechnology.

Inordertodeterminetheeffectivenessofsomeoftheseincentives,ourpreviousanalysisfocusedondeterminingtheimpactofnon‐fundingrelatedstateincentivesonincreasesinCHPapplicationsNevertheless,asthepreviousanalysishasshown,regulatoryincentiveshavenotincreasedtheadoptionofCHPtechnologiesinapplicationsthroughouttheUnitedStates.

GiventhatpreviousanalysistodeterminewhetherthereisasignificanteffectofincentivesonincreasingCHPadoption,thisanalysisattemptstodeterminewhetherthereisasignificantneedforincentivesinordertoallowCHPtechnologiestobeadoptedinacompetitivemarket.Inotherwords,thisstudyattemptstodiscoverwhetherCHPtechnologiescanbecost‐competitivewithoutfundingincentives.

Analysis

ThepurposeofthisanalysisistodeterminewhetherCHPtechnologyneedsfundingincentivesinordertobecostcompetitive.Inordertoconductthisanalysis,wewillcomparethecostofinstallingandusingCHPtechnologywithoutanyfundingincentivesoroffsetcapitalcostsandthendetermineifthiscostislowerthanthecosttosimplypurchasetheelectricityfromthegrid.DomainThedomainofouranalysiswillbeU.S.naturalgasfiredelectricpowerplantsthatadoptcombinedcyclegasturbineCHPtechnology.TheDepartmentofEnergyestimatesthat900outofthenext1000U.S.powerplantswillusenaturalgas.Furthermore,sinceasignificantportionofCHPtechnologiesareimplementedinnaturalgaspowerplants,itismeaningfultoconductananalysisfocusedonCHPtechnologiesinnaturalgaspoweredsystemslxv.

32

UsingLevelizedCostsSinceoneofthemajorcostsisanup‐frontfixedcapitalcost(thisincludesinstallationcosts),theinitialcosttoCHPusersinthefirstyearwouldbedisproportionallylargerthaninanyoftheensuingyearssoitwouldnotbemeaningfultocomparethecoststotheusersofCHPtechnologyeachyearwithelectricitypricesineachyear.Foramoremeaningfulanalysis,wecalculatethelevelizedcostsofgeneratingelectricitywhenusingCHPtechnology.LevelizedcostsindicatethepresentvalueofthetotalcostofconstructingandoperatingCHPtechnologyinanaturalgasplantoverthetechnology’seconomiclife,whenconvertedtoaverageannualpaymentslxvi.Inotherwords,ittakesthemainfixedcosts(theinitialcapitalcosts,operationsandmaintenanceandfuelcosts)andassumesthatthelump‐sumcostscanbespreadoutovertimeandshowswhattheequivalentyearlypaymentforthecostofinstallingaCHPplantwouldbe.AlthoughCHPsystemsproduceacombinationofheatandelectricity,inthisanalysiswewillassumethatenergyisconvertedtoelectricity.ThereforeweareassumingthatiftheuserdidnotuseCHPtoproducetheheatandelectricitytheywouldhavetopurchasetheequivalentamountofelectricityfromthegrid.

TheCalculation

Averagelifetimelevelizedelectricitygenerationcost(EGC)lxvii=Σ[(Ct+O&Mt+Ft‐It)(1+r)^‐t]/Σ[Et(1+r)^‐t]WherethevariablesrelevanttocalculatingtheaveragelevelizedcostofCHPare:Ct=CapitalexpendituresintheyeartO&Mt=OperationsandmaintenanceexpendituresintheyeartFt=FuelExpenditureintheyeartIt=FundingIncentivesintheyeartEt=Electricitygenerationintheyeartr=Discountratet=year

Theresultinganalysiswilltaketwomainsteps:1)FirstwewillcalculatethelevelizedcoststogenerateelectricitywhenusingCHPtechnologywithoutanyfundingincentivesoroffsetcapitalcosts 2)Thenthelevelizedcostcanbecomparedtothecostofelectricityifpurchaseddirectlyfromthegrideachyear.Ifthiscostislowerthanthepriceofpurchasingelectricitydirectlyfromthegrid,thenwecanassumethatCHPtechnologyiscost‐competitiveincombinedcyclesteamturbineapplicationsinU.S.naturalgasplants.

33

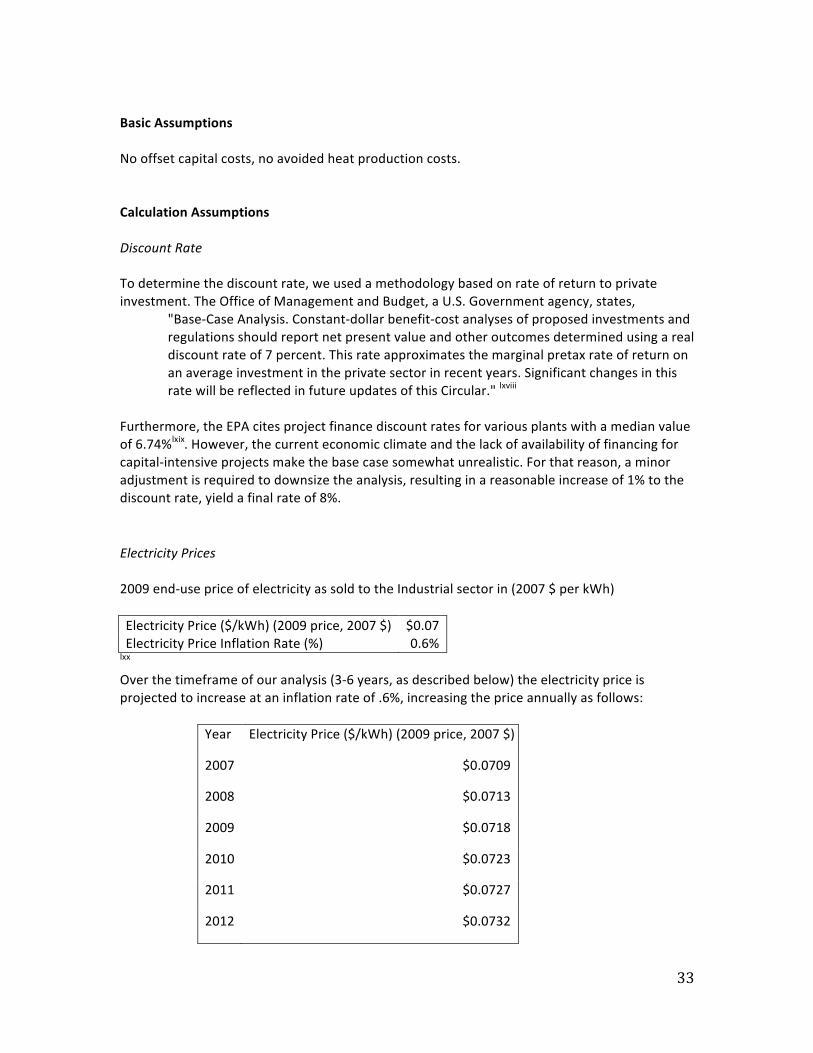

BasicAssumptionsNooffsetcapitalcosts,noavoidedheatproductioncosts.CalculationAssumptions DiscountRateTodeterminethediscountrate,weusedamethodologybasedonrateofreturntoprivateinvestment.TheOfficeofManagementandBudget,aU.S.Governmentagency,states,

"Base‐CaseAnalysis.Constant‐dollarbenefit‐costanalysesofproposedinvestmentsandregulationsshouldreportnetpresentvalueandotheroutcomesdeterminedusingarealdiscountrateof7percent.Thisrateapproximatesthemarginalpretaxrateofreturnonanaverageinvestmentintheprivatesectorinrecentyears.SignificantchangesinthisratewillbereflectedinfutureupdatesofthisCircular."lxviii

Furthermore,theEPAcitesprojectfinancediscountratesforvariousplantswithamedianvalueof6.74%lxix.However,thecurrenteconomicclimateandthelackofavailabilityoffinancingforcapital‐intensiveprojectsmakethebasecasesomewhatunrealistic.Forthatreason,aminoradjustmentisrequiredtodownsizetheanalysis,resultinginareasonableincreaseof1%tothediscountrate,yieldafinalrateof8%.ElectricityPrices2009end‐usepriceofelectricityassoldtotheIndustrialsectorin(2007$perkWh)ElectricityPrice($/kWh)(2009price,2007$) $0.07ElectricityPriceInflationRate(%) 0.6%

lxxOverthetimeframeofouranalysis(3‐6years,asdescribedbelow)theelectricitypriceisprojectedtoincreaseataninflationrateof.6%,increasingthepriceannuallyasfollows:

Year ElectricityPrice($/kWh)(2009price,2007$)$)

2007 $0.0709

2008 $0.0713

2009 $0.0718

2010 $0.0723

2011 $0.0727

2012 $0.0732

34

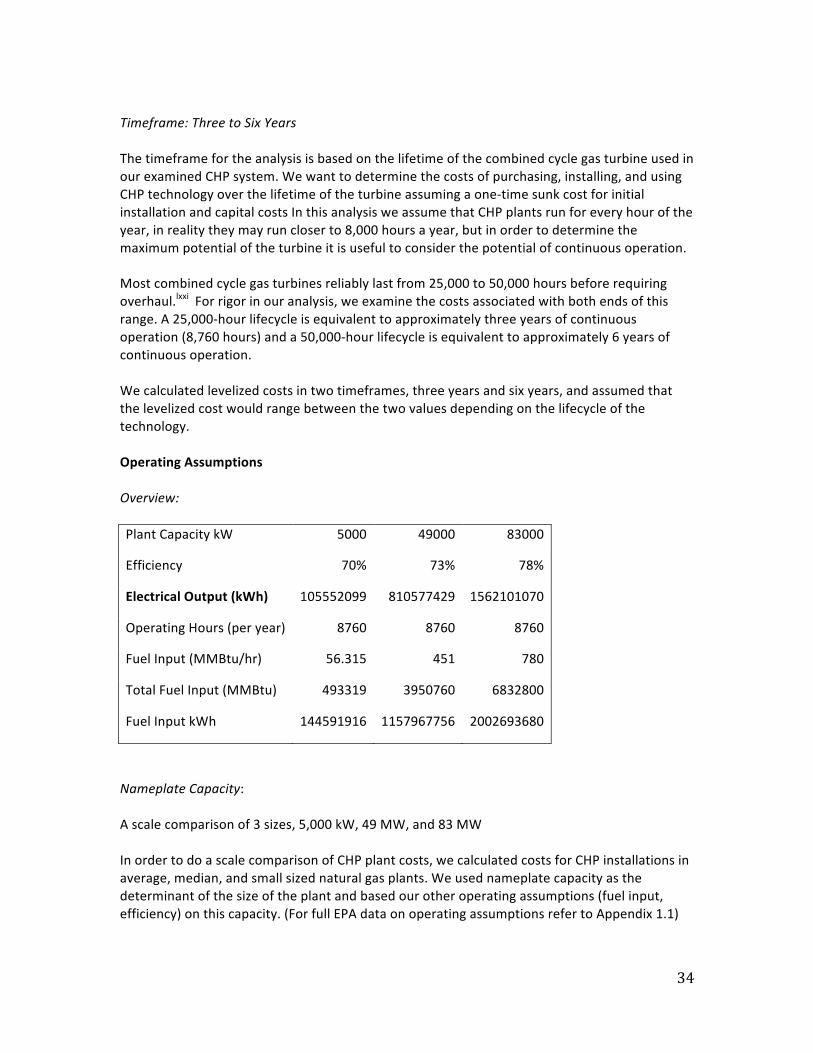

Timeframe:ThreetoSixYearsThetimeframefortheanalysisisbasedonthelifetimeofthecombinedcyclegasturbineusedinourexaminedCHPsystem.Wewanttodeterminethecostsofpurchasing,installing,andusingCHPtechnologyoverthelifetimeoftheturbineassumingaone‐timesunkcostforinitialinstallationandcapitalcostsInthisanalysisweassumethatCHPplantsrunforeveryhouroftheyear,inrealitytheymayruncloserto8,000hoursayear,butinordertodeterminethemaximumpotentialoftheturbineitisusefultoconsiderthepotentialofcontinuousoperation.Mostcombinedcyclegasturbinesreliablylastfrom25,000to50,000hoursbeforerequiringoverhaul.lxxiForrigorinouranalysis,weexaminethecostsassociatedwithbothendsofthisrange.A25,000‐hourlifecycleisequivalenttoapproximatelythreeyearsofcontinuousoperation(8,760hours)anda50,000‐hourlifecycleisequivalenttoapproximately6yearsofcontinuousoperation.Wecalculatedlevelizedcostsintwotimeframes,threeyearsandsixyears,andassumedthatthelevelizedcostwouldrangebetweenthetwovaluesdependingonthelifecycleofthetechnology.OperatingAssumptionsOverview:PlantCapacitykW 5000 49000 83000

Efficiency 70% 73% 78%

ElectricalOutput(kWh) 105552099 810577429 1562101070

OperatingHours(peryear) 8760 8760 8760

FuelInput(MMBtu/hr) 56.315 451 780

TotalFuelInput(MMBtu) 493319 3950760 6832800

FuelInputkWh 144591916 1157967756 2002693680

NameplateCapacity:Ascalecomparisonof3sizes,5,000kW,49MW,and83MWInordertodoascalecomparisonofCHPplantcosts,wecalculatedcostsforCHPinstallationsinaverage,median,andsmallsizednaturalgasplants.Weusednameplatecapacityasthedeterminantofthesizeoftheplantandbasedourotheroperatingassumptions(fuelinput,efficiency)onthiscapacity.(ForfullEPAdataonoperatingassumptionsrefertoAppendix1.1)

35

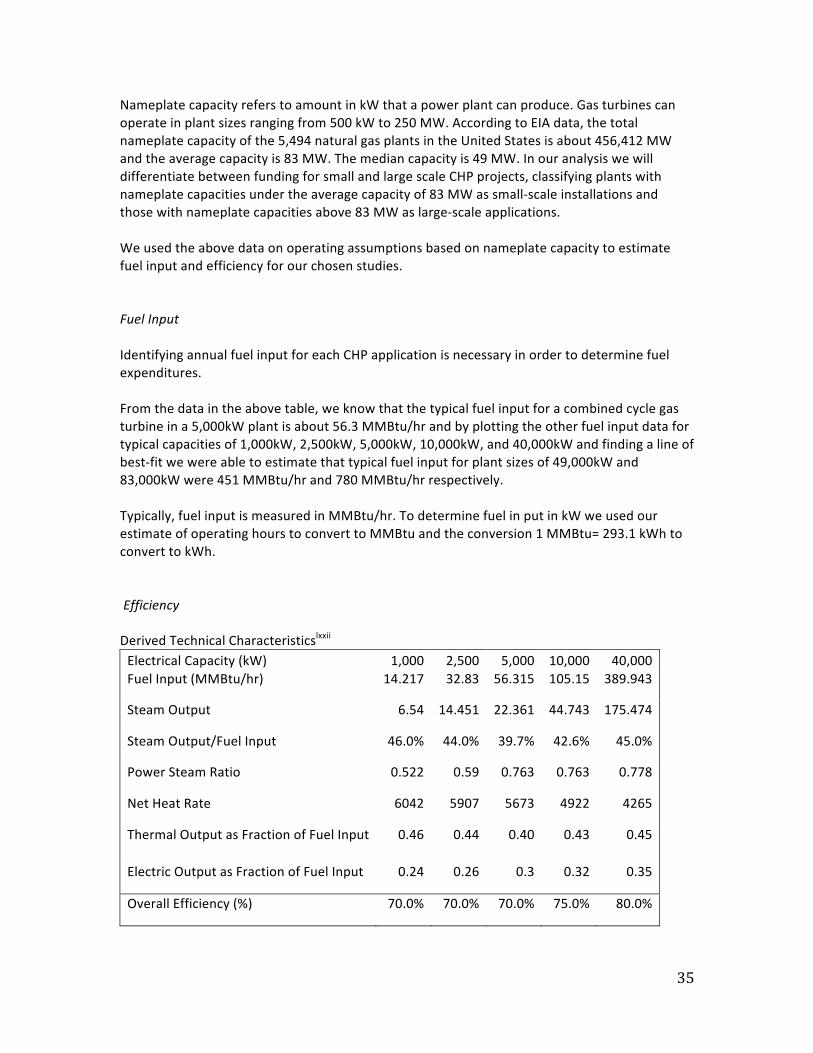

NameplatecapacityreferstoamountinkWthatapowerplantcanproduce.Gasturbinescanoperateinplantsizesrangingfrom500kWto250MW.AccordingtoEIAdata,thetotalnameplatecapacityofthe5,494naturalgasplantsintheUnitedStatesisabout456,412MWandtheaveragecapacityis83MW.Themediancapacityis49MW.InouranalysiswewilldifferentiatebetweenfundingforsmallandlargescaleCHPprojects,classifyingplantswithnameplatecapacitiesundertheaveragecapacityof83MWassmall‐scaleinstallationsandthosewithnameplatecapacitiesabove83MWaslarge‐scaleapplications.Weusedtheabovedataonoperatingassumptionsbasedonnameplatecapacitytoestimatefuelinputandefficiencyforourchosenstudies.FuelInputIdentifyingannualfuelinputforeachCHPapplicationisnecessaryinordertodeterminefuelexpenditures.Fromthedataintheabovetable,weknowthatthetypicalfuelinputforacombinedcyclegasturbineina5,000kWplantisabout56.3MMBtu/hrandbyplottingtheotherfuelinputdatafortypicalcapacitiesof1,000kW,2,500kW,5,000kW,10,000kW,and40,000kWandfindingalineofbest‐fitwewereabletoestimatethattypicalfuelinputforplantsizesof49,000kWand83,000kWwere451MMBtu/hrand780MMBtu/hrrespectively.Typically,fuelinputismeasuredinMMBtu/hr.TodeterminefuelinputinkWweusedourestimateofoperatinghourstoconverttoMMBtuandtheconversion1MMBtu=293.1kWhtoconverttokWh.EfficiencyDerivedTechnicalCharacteristicslxxiiElectricalCapacity(kW) 1,000 2,500 5,000 10,000 40,000FuelInput(MMBtu/hr) 14.217 32.83 56.315 105.15 389.943

SteamOutput 6.54 14.451 22.361 44.743 175.474

SteamOutput/FuelInput 46.0% 44.0% 39.7% 42.6% 45.0%

PowerSteamRatio 0.522 0.59 0.763 0.763 0.778

NetHeatRate 6042 5907 5673 4922 4265

ThermalOutputasFractionofFuelInput 0.46 0.44 0.40 0.43 0.45

ElectricOutputasFractionofFuelInput 0.24 0.26 0.3 0.32 0.35

OverallEfficiency(%) 70.0% 70.0% 70.0% 75.0% 80.0%

36

CHPplantefficiencyisdeterminedasthecombinethermalandelectricoutputasafractionoffuelinput.Thermaloutputisdeterminedbythesteamoutputoverfuelinputandelectricoutputisdeterminebyusingthepowertosteamratioandthesteamoutputoverfuelinputtocalculateelectricoutputasafractionoffuelcost.

Giventhesecalculationsandthedataavailablefortypicalplantsizes(refertoabovetable)weusedthesamemethodaswhenweestimatedfuelinputforlargerplantsizestoestimatea73%and78%efficiencyforplantcapacitiesof49MWand83MWrespectively.

37

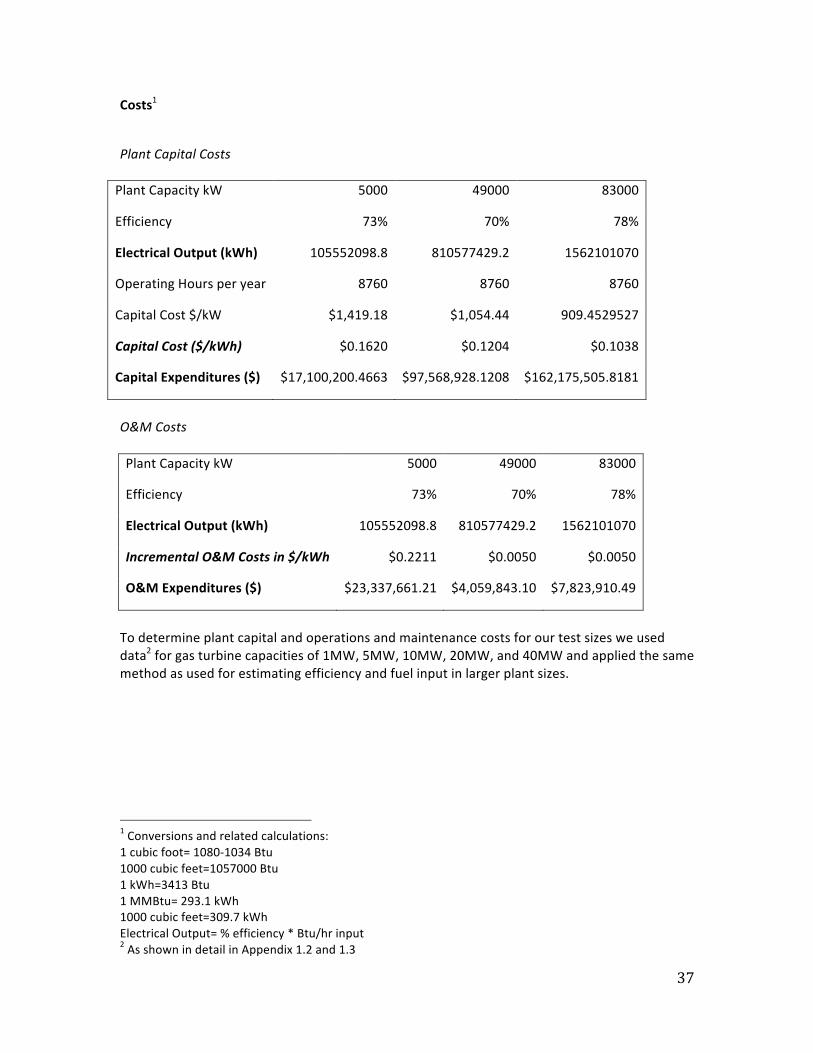

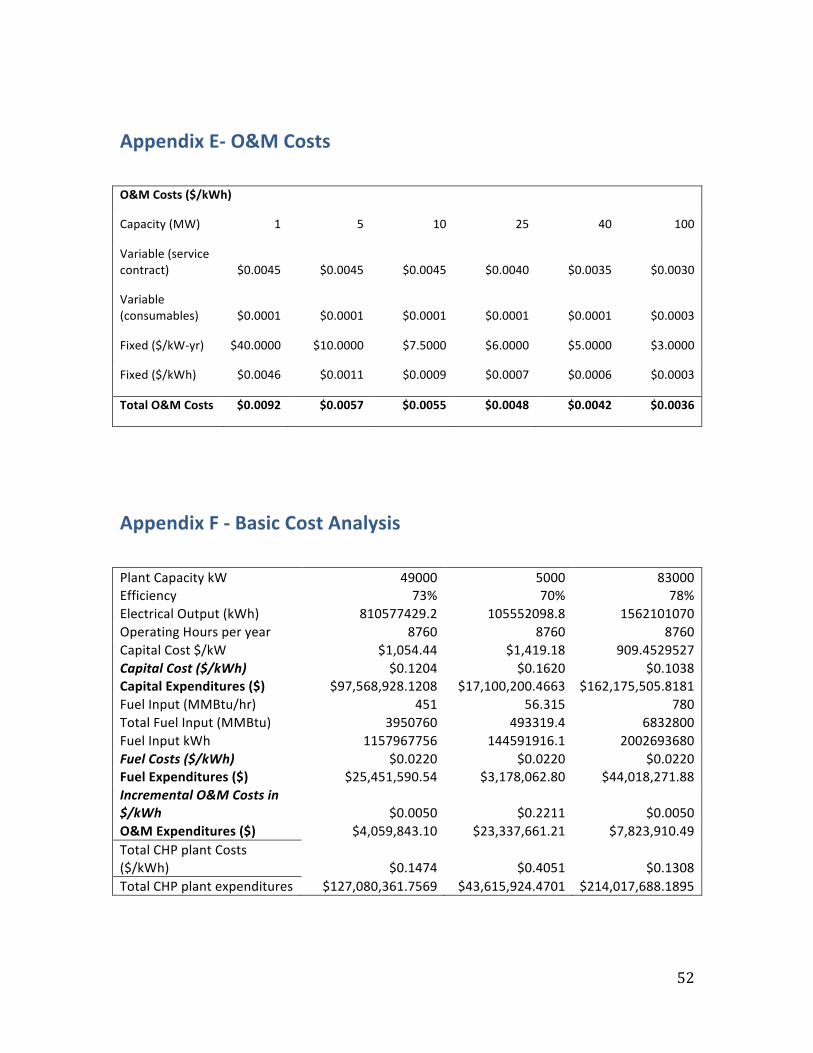

Costs1

PlantCapitalCostsPlantCapacitykW 5000 49000 83000

Efficiency 73% 70% 78%

ElectricalOutput(kWh) 105552098.8 810577429.2 1562101070

OperatingHoursperyear 8760 8760 8760

CapitalCost$/kW $1,419.18 $1,054.44 909.4529527

CapitalCost($/kWh) $0.1620 $0.1204 $0.1038

CapitalExpenditures($) $17,100,200.4663 $97,568,928.1208 $162,175,505.8181

O&MCostsPlantCapacitykW 5000 49000 83000

Efficiency 73% 70% 78%

ElectricalOutput(kWh) 105552098.8 810577429.2 1562101070

IncrementalO&MCostsin$/kWh $0.2211 $0.0050 $0.0050

O&MExpenditures($) $23,337,661.21 $4,059,843.10 $7,823,910.49

Todetermineplantcapitalandoperationsandmaintenancecostsforourtestsizesweuseddata2forgasturbinecapacitiesof1MW,5MW,10MW,20MW,and40MWandappliedthesamemethodasusedforestimatingefficiencyandfuelinputinlargerplantsizes.

1Conversionsandrelatedcalculations:1cubicfoot=1080‐1034Btu1000cubicfeet=1057000Btu1kWh=3413Btu1MMBtu=293.1kWh1000cubicfeet=309.7kWhElectricalOutput=%efficiency*Btu/hrinput2AsshownindetailinAppendix1.2and1.3

38

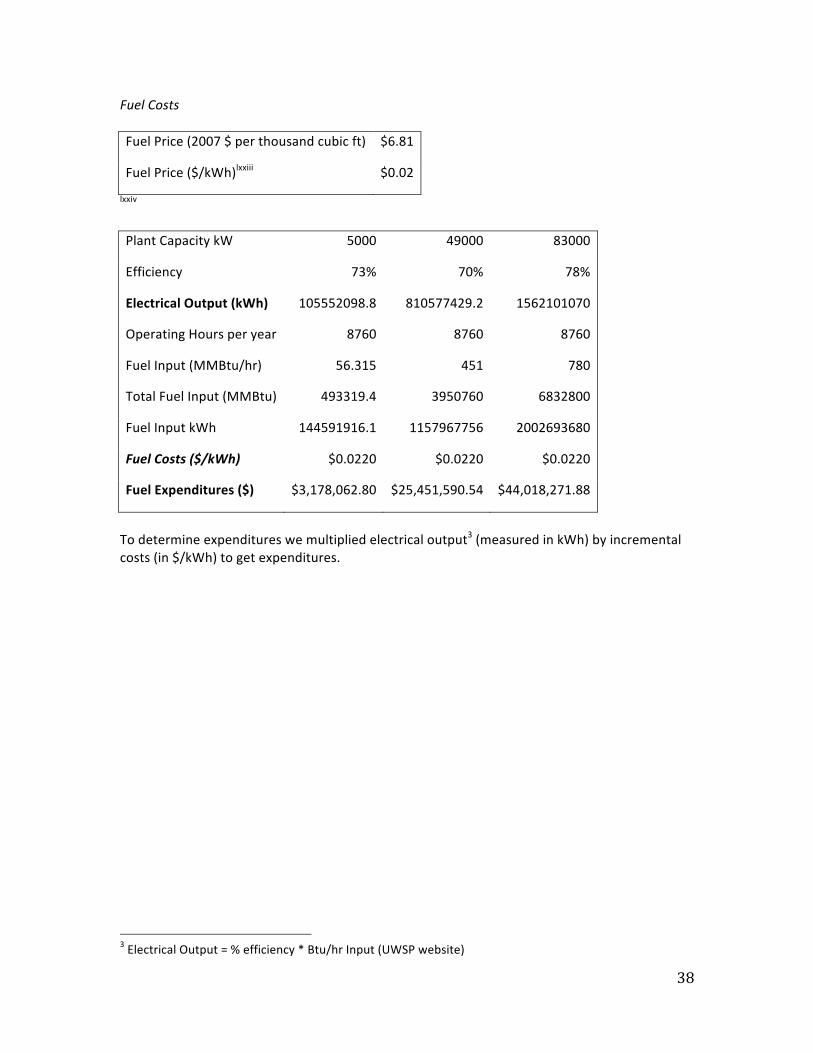

FuelCostsFuelPrice(2007$perthousandcubicft) $6.81

FuelPrice($/kWh)lxxiii $0.02

lxxivPlantCapacitykW 5000 49000 83000

Efficiency 73% 70% 78%

ElectricalOutput(kWh) 105552098.8 810577429.2 1562101070

OperatingHoursperyear 8760 8760 8760

FuelInput(MMBtu/hr) 56.315 451 780

TotalFuelInput(MMBtu) 493319.4 3950760 6832800

FuelInputkWh 144591916.1 1157967756 2002693680

FuelCosts($/kWh) $0.0220 $0.0220 $0.0220

FuelExpenditures($) $3,178,062.80 $25,451,590.54 $44,018,271.88

Todetermineexpenditureswemultipliedelectricaloutput3(measuredinkWh)byincrementalcosts(in$/kWh)togetexpenditures.

3ElectricalOutput=%efficiency*Btu/hrInput(UWSPwebsite)

39

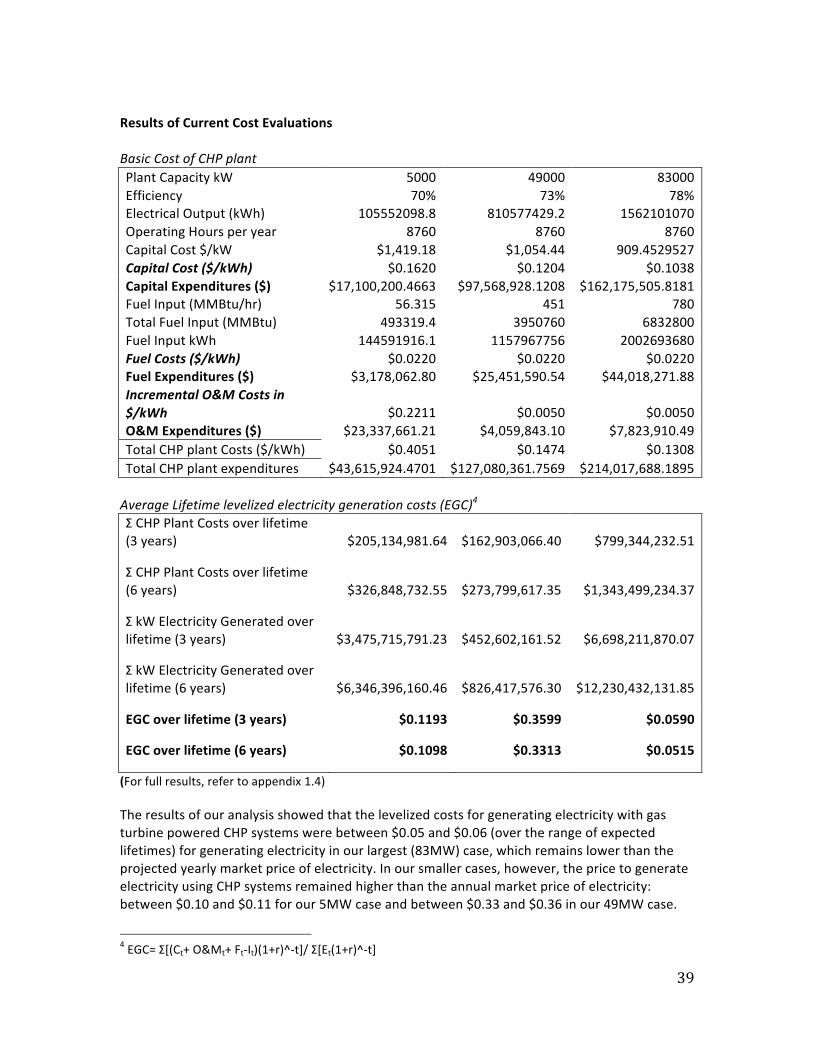

ResultsofCurrentCostEvaluationsBasicCostofCHPplantPlantCapacitykW 5000 49000 83000Efficiency 70% 73% 78%ElectricalOutput(kWh) 105552098.8 810577429.2 1562101070OperatingHoursperyear 8760 8760 8760CapitalCost$/kW $1,419.18 $1,054.44 909.4529527CapitalCost($/kWh) $0.1620 $0.1204 $0.1038CapitalExpenditures($) $17,100,200.4663 $97,568,928.1208 $162,175,505.8181FuelInput(MMBtu/hr) 56.315 451 780TotalFuelInput(MMBtu) 493319.4 3950760 6832800FuelInputkWh 144591916.1 1157967756 2002693680FuelCosts($/kWh) $0.0220 $0.0220 $0.0220FuelExpenditures($) $3,178,062.80 $25,451,590.54 $44,018,271.88IncrementalO&MCostsin$/kWh $0.2211 $0.0050 $0.0050O&MExpenditures($) $23,337,661.21 $4,059,843.10 $7,823,910.49TotalCHPplantCosts($/kWh) $0.4051 $0.1474 $0.1308TotalCHPplantexpenditures $43,615,924.4701 $127,080,361.7569 $214,017,688.1895AverageLifetimelevelizedelectricitygenerationcosts(EGC)4ΣCHPPlantCostsoverlifetime(3years) $205,134,981.64 $162,903,066.40 $799,344,232.51

ΣCHPPlantCostsoverlifetime(6years) $326,848,732.55 $273,799,617.35 $1,343,499,234.37

ΣkWElectricityGeneratedoverlifetime(3years) $3,475,715,791.23 $452,602,161.52 $6,698,211,870.07

ΣkWElectricityGeneratedoverlifetime(6years) $6,346,396,160.46 $826,417,576.30 $12,230,432,131.85

EGCoverlifetime(3years) $0.1193 $0.3599 $0.0590

EGCoverlifetime(6years) $0.1098 $0.3313 $0.0515

(Forfullresults,refertoappendix1.4)TheresultsofouranalysisshowedthatthelevelizedcostsforgeneratingelectricitywithgasturbinepoweredCHPsystemswerebetween$0.05and$0.06(overtherangeofexpectedlifetimes)forgeneratingelectricityinourlargest(83MW)case,whichremainslowerthantheprojectedyearlymarketpriceofelectricity.Inoursmallercases,however,thepricetogenerateelectricityusingCHPsystemsremainedhigherthantheannualmarketpriceofelectricity:between$0.10and$0.11forour5MWcaseandbetween$0.33and$0.36inour49MWcase.

4EGC=Σ[(Ct+O&Mt+Ft‐It)(1+r)^‐t]/Σ[Et(1+r)^‐t]

40

ImplicationsWecanthereforeconcludethatingasturbineapplicationsCHPtechnologyiscost‐competitivewithoutfundingincentivesinapplicationswheregenerationcapacityifaverageorhigherthanaverage(>83MW).Inapplicationswheregeneratingcapacityisbelowaverage,CHPtechnologywouldneedfundingincentivestobecosteffective.Therefore,incasesofaverageorlargercaseapplicationsofgasturbineCHPtechnology,thetechnologyandmarkethaveprogressedtowhichthereisnolongeraneedforfundingincentives.Thismayhelptoexplainourperviousfindings(inourpolicyanalysis)thatregulatoryimprovementsdonotexplainthegrowthinadoptionofCHPtechnologiesbecausecurrentregulationsarefocusedprimarilyonlargescaleapplicationswherethereisnolongerneedforfundinginordertomakeusingCHPcost‐competitive.Large‐scaleapplicationsarecost‐competitiveontheirown,sofundingincentivesdisproportionatelyskewthemarkettowardslarge‐scaleapplications,whilesmallscaleCHPapplicationsshowgreatpotentialforgrowth(asshowninAnalysisOne)butrequirefundingtobecost‐competitive.Furthermore,unnecessaryfundingmayreducetheincentivetofurtherdevelopefficiencyoflarge‐scaleapplications.OpportunitiesforFurtherAnalysisThehigherlevelizedcostforthesmallerapplicationsismostlikelyduetotwomainfactors:1)thehigherincrementalcost(S/kWh)ofcapitalandinstallationforsmallercasesand2)therelativelyfastoverhaulofgasturbines.OurresultsindicateaspaceforpromisingresultsinCHPapplicationswithlowercapitalcostsandturbineswithlongerlifecycle.Alonglifecycleallowscoststobelevelizedoveramuchlongertimeperiodbecausethecapitalcostsonlyhavetobeincurredonceperlifetime.Aquickextensionoftheiterationsusedtocalculateourlevelizedcostsinthecastofgasturbinesshowsthatanincreaseinlifecyclelowersthecostofgeneratingelectricitybelowthemarketpriceofelectricity.LengtheningthelifecycleofgasturbinesthereforeholdsthepotentialtodramaticallyreducethecosttogenerateelectricityandmakeCHPcostcompetitiveeveninsmallerapplications.Researchanddevelopmentholdstheprimarypotentialtoprovideopportunitiestolengthengasturbinelifecyclesandreducetheincrementalcapitalcosts.InaccomplishingthesegoalsthiswillallowthetechnologyandmarkettomergeandincreasetherangeofpotentialCHPapplicationsinbothlargeandsmall‐scalesites.Finally,thoughoutsidethescopeofouranalysis,steamturbinesofferthebenefitsofamuch‐increasedlifecycleofupto50yearswithsimilarcapital,fuelandO&Mcoststothoseofgasturbines.Inthiswaysteamturbinesalreadyholdthepotentialforcost‐competitiveness,especiallyinsmall‐scaleapplications.

41

ConclusionsandRecommendationsConclusions

Ourcost‐benefitanalysisshowsthatlarge‐scalenaturalgasturbineCHPsystemsarecost‐competitivewithoutfinancialincentives.Thisresultisconsistentwithourpolicyanalysisthatsuggestsfactor(s)otherthanstateregulationsexplainthegrowthinCHPcapacity.BecauseCHPgrowthduringthetenyearstudyperiodwasconcentratedinlarge‐scaleindustrialfacilities,theincreaseincapacitywaslikelyduetothecosteffectivenessofinstallingCHPsystems,ratherthantheadoptionofpoliciesthatfavorCHP.

Theanalysisindicatesthatsmall‐scalenaturalgasturbineCHPsystemsarenotcosteffectivewithoutfinancialincentives.AdoptingtheregulationsexaminedinthispaperwoulddecreasethecostofCHPsystemsbyremovingbarriersthataretoocostlyforsmall‐scalesystems,suggestingthatstatepoliciesmayplayamoreimportantroleinthefutureastheCHPindustrytrendstowardssmallerinstallations.

Recommendations

Theobjectoffutureeffortsofstatepolicy‐makerstoencouragethegrowthofNaturalGaspoweredCHPsystemsshouldbesmall‐scalesitesthataretypicallydistributedgenerationfacilities.Ourcost‐benefitanalysisdemonstratesthatlarge‐scaleapplicationsofnaturalgasturbinesarecost‐competitivewithoutfederalorstatefinancialincentives.OurstatisticalanalysisofstatepoliciesconcludesthatpolicyinitiativesaimedatthegeneralCHPmarketplacearenoteffectiveatfosteringgrowthofsmall‐scalenaturalgassystemsthatarestillfacingcostandregulatorydisadvantages.

Goingforward,themajorityofgrowthinthemarketshareofCHP‐generatedelectricitywillcomefromdistributedgenerationfacilitiesproducinglessthan5MW.Themosteffectiveapproachforgrowingthissectorisforpolicy‐makersandprivate‐sectorplayerstofocusonremovingthebarriersuniquelyfacingsmallsystems.Werecommendfourapproachesthatinclude:redirectingstateandfederalincentives,investinginresearchanddevelopment,directingregulationsandpoliciesthatwillquickentheadoptionofSmartGridtechnology,andfocusingonoutreachandeducation.

DirectionofStateandFederalIncentives

Asshowninthesynthesisofouranalyses,weknowthatbecauselarge‐scaleapplicationsofnaturalgasturbinesarealreadycost‐competitive,policyinitiativesaimedataCHPmarketdominatedprimarilybylarge‐scale(andthusalreadycost‐competitive)systemshavenotbeeneffectivelydirected.Therefore,federalandstateincentivesshouldbedirectedtowardsensuringthatsmall‐scaleCHPapplicationsarecostcompetitive.Inthisre‐direction,uniformityofpoliciesisimportant;interstatecoordinationandcooperationtodevelopuniformpoliciescouldbeimportantforfurthergrowthandwillmakeiteasierforfirmstoprojectfuturecostsandbenefits.

42

ResearchandDevelopment

TechnologyimprovementsarethemostimportantdriverforincreasingsmallscaleCHPgrowth.AsshowninourCostBenefitAnalysis,increasingthelifecycleofturbinesanddecreasingtheincrementalcapitalcostswilldecreasethelevelizedcoststogenerateelectricityusingCHP.

ThereforeresearchanddevelopmentofCHPtechnologyholdsthepotentialtomakeCHPtechnologycost‐competitiveinallsizeapplications.Suchdevelopmentswouldallowconvergenceoftechnologyandthemarketandmakefundingincentivesunnecessary.Furthermore,inacompetitivemarkettherewillbemoreofanincentivetoincreaseefficiencyandfurtherimprovetheeffectivenessofCHPtechnology.

SmartGrid

ImprovementsinU.S.electricityinfrastructurearecrucialtosignificantlyimprovingtheefficiencyofthemarket.Currentlyregulatingtheenergygridpresentsalargesetofuniquechallengesincoordinatingbetweencustomers,utilities,stategovernments,andFERC.Acommonthreadinthesechallengesisthelackofabilityforalltheessentialplayerstocommunicateaboutelectricitysupply,demand,andprices.Stateandfederallevelinvestmentinresearch,developmentand,mostimportantly,deploymentofaSmartGridwouldallowcustomersaccesstoreal‐timepricinginformationofelectricity.Thiswouldallowsavingsinenergyefficiencytobemoreeasilypricedthroughinthemarketplace,sincecustomerswouldpaymoreforelectricitythatcostsmoretoproduce.

SmallnaturalgasturbineCHPsystemsfacechallengesinconnectingtotheelectricitygridbecauseoftheonerousandinconsistentstateregulationswehavedetailedinthispaper.Onesignificantadvantagetoasmartgridisthatgridoperatorsareabletohandlemanymoreinputsofelectricity.Thiswouldsignificantlydecreasethebarriersthatsmalldistributedgenerationfacilitiesfacebyeliminatingthebuilt‐innaturalmonopolythatcurrentlyfacilitatesthedominanceoflargecentralizedpowerplants.

SmartGridtechnologywillcontributetoavastlyimprovedenergymarket.Amarketthatvaluesefficiency,facilitatesinformationsharing,andeliminatesbarrierstoentrywillplaceanappropriatevalueonCombinedHeatandPowersystems.

OutreachandEducation

Finally,oneoftheremainingbarrierstoadoptionofsmall‐scaleCHPuseisthatmanyusersinthesmall‐scalespace(hospitals,schools,etc.)areunawareofthepotentialbenefitsofusingCHPtechnologiesintheirfacilities.Thereforeeducationandoutreach,byincreasingawarenessofthepotentialofCHP,wouldgogreatlengthstoensuringthatviableCHPapplicationsarenotoverlooked.

AppendixA–RegressionData

AppendixB–STATARegressionResults

46

47

48

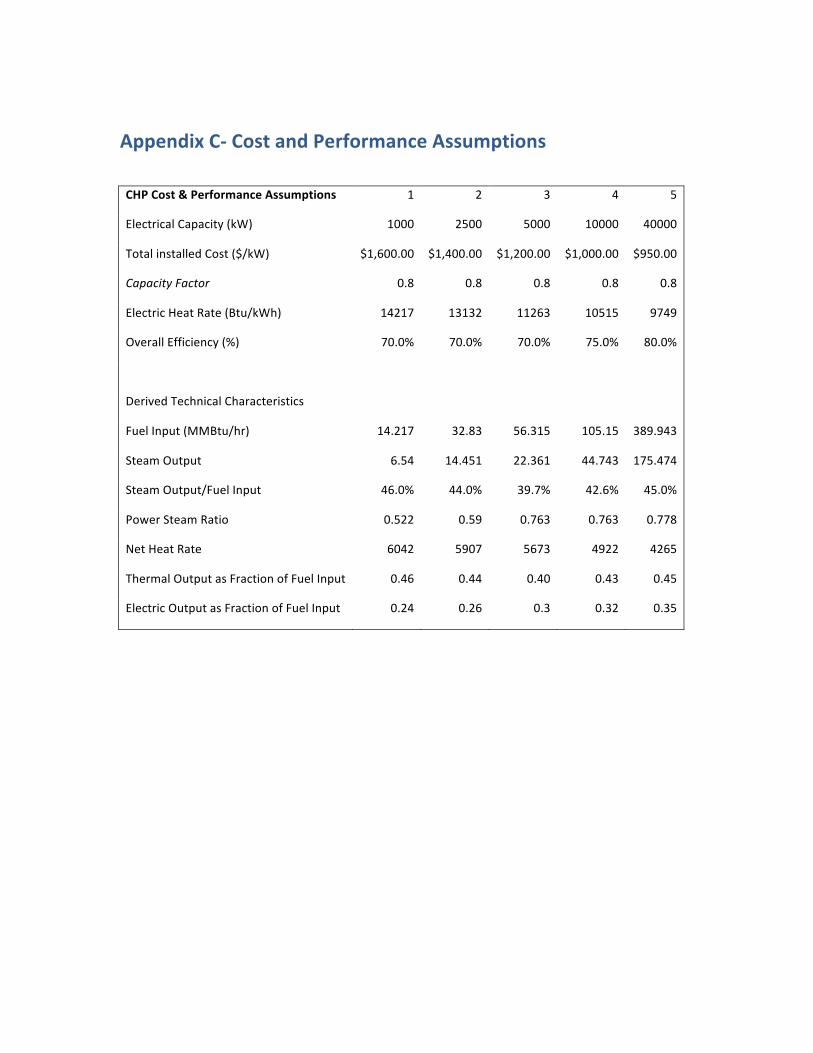

AppendixC‐CostandPerformanceAssumptions

CHPCost&PerformanceAssumptions 1 2 3 4 5

ElectricalCapacity(kW) 1000 2500 5000 10000 40000

TotalinstalledCost($/kW) $1,600.00 $1,400.00 $1,200.00 $1,000.00 $950.00

CapacityFactor 0.8 0.8 0.8 0.8 0.8

ElectricHeatRate(Btu/kWh) 14217 13132 11263 10515 9749

OverallEfficiency(%) 70.0% 70.0% 70.0% 75.0% 80.0%

DerivedTechnicalCharacteristics

FuelInput(MMBtu/hr) 14.217 32.83 56.315 105.15 389.943

SteamOutput 6.54 14.451 22.361 44.743 175.474

SteamOutput/FuelInput 46.0% 44.0% 39.7% 42.6% 45.0%

PowerSteamRatio 0.522 0.59 0.763 0.763 0.778

NetHeatRate 6042 5907 5673 4922 4265

ThermalOutputasFractionofFuelInput 0.46 0.44 0.40 0.43 0.45

ElectricOutputasFractionofFuelInput 0.24 0.26 0.3 0.32 0.35

50

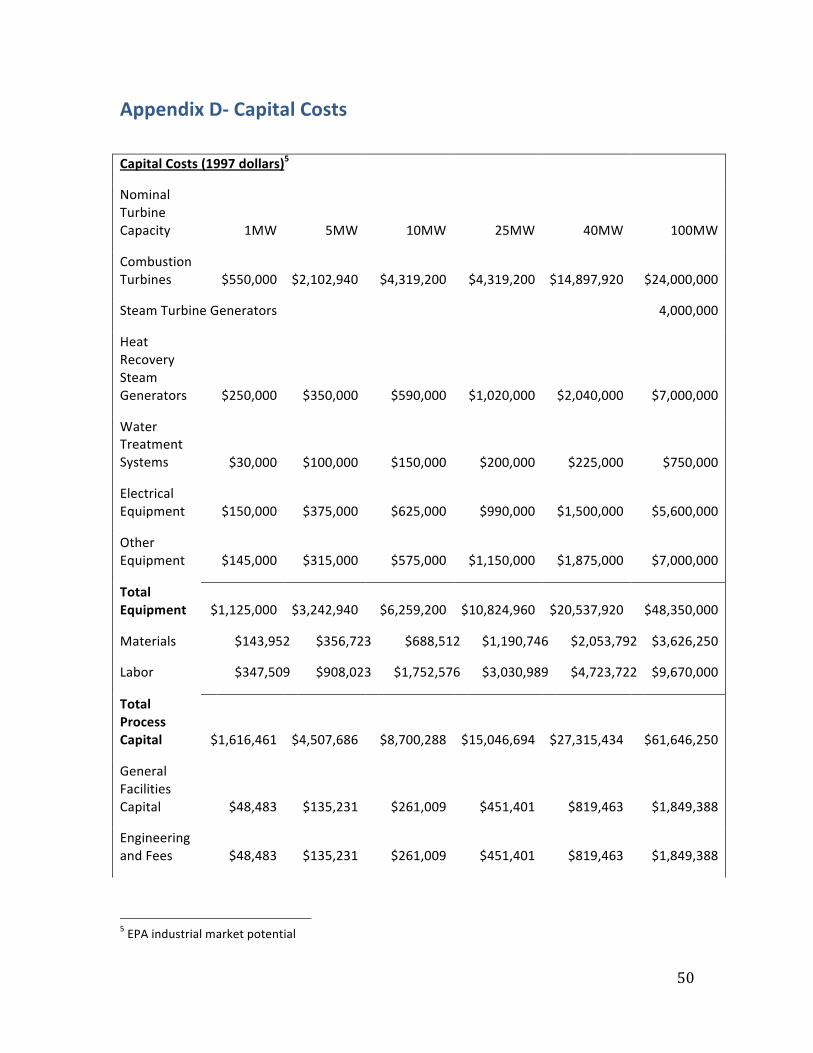

AppendixD‐CapitalCosts

CapitalCosts(1997dollars)5

NominalTurbineCapacity 1MW 5MW 10MW 25MW 40MW 100MW

CombustionTurbines $550,000 $2,102,940 $4,319,200 $4,319,200 $14,897,920 $24,000,000

SteamTurbineGenerators 4,000,000

HeatRecoverySteamGenerators $250,000 $350,000 $590,000 $1,020,000 $2,040,000 $7,000,000

WaterTreatmentSystems $30,000 $100,000 $150,000 $200,000 $225,000 $750,000

ElectricalEquipment $150,000 $375,000 $625,000 $990,000 $1,500,000 $5,600,000

OtherEquipment $145,000 $315,000 $575,000 $1,150,000 $1,875,000 $7,000,000

TotalEquipment $1,125,000 $3,242,940 $6,259,200 $10,824,960 $20,537,920 $48,350,000

Materials $143,952 $356,723 $688,512 $1,190,746 $2,053,792 $3,626,250

Labor $347,509 $908,023 $1,752,576 $3,030,989 $4,723,722 $9,670,000

TotalProcessCapital $1,616,461 $4,507,686 $8,700,288 $15,046,694 $27,315,434 $61,646,250

GeneralFacilitiesCapital $48,483 $135,231 $261,009 $451,401 $819,463 $1,849,388

EngineeringandFees $48,483 $135,231 $261,009 $451,401 $819,463 $1,849,388

5EPAindustrialmarketpotential

51

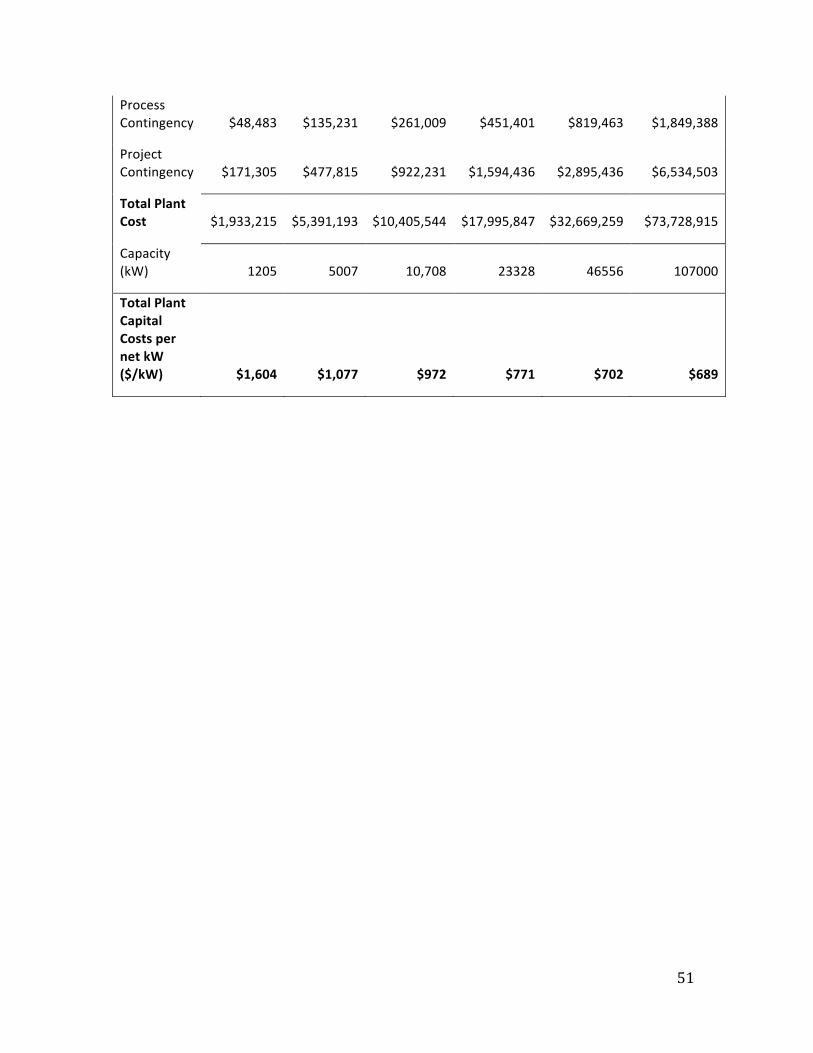

ProcessContingency $48,483 $135,231 $261,009 $451,401 $819,463 $1,849,388

ProjectContingency $171,305 $477,815 $922,231 $1,594,436 $2,895,436 $6,534,503

TotalPlantCost $1,933,215 $5,391,193 $10,405,544 $17,995,847 $32,669,259 $73,728,915

Capacity(kW) 1205 5007 10,708 23328 46556 107000

TotalPlantCapitalCostspernetkW($/kW) $1,604 $1,077 $972 $771 $702 $689

52

AppendixE‐O&MCosts

O&MCosts($/kWh)

Capacity(MW) 1 5 10 25 40 100

Variable(servicecontract) $0.0045 $0.0045 $0.0045 $0.0040 $0.0035 $0.0030

Variable(consumables) $0.0001 $0.0001 $0.0001 $0.0001 $0.0001 $0.0003

Fixed($/kW‐yr) $40.0000 $10.0000 $7.5000 $6.0000 $5.0000 $3.0000

Fixed($/kWh) $0.0046 $0.0011 $0.0009 $0.0007 $0.0006 $0.0003

TotalO&MCosts $0.0092 $0.0057 $0.0055 $0.0048 $0.0042 $0.0036

AppendixF‐BasicCostAnalysis

PlantCapacitykW 49000 5000 83000Efficiency 73% 70% 78%ElectricalOutput(kWh) 810577429.2 105552098.8 1562101070OperatingHoursperyear 8760 8760 8760CapitalCost$/kW $1,054.44 $1,419.18 909.4529527CapitalCost($/kWh) $0.1204 $0.1620 $0.1038CapitalExpenditures($) $97,568,928.1208 $17,100,200.4663 $162,175,505.8181FuelInput(MMBtu/hr) 451 56.315 780TotalFuelInput(MMBtu) 3950760 493319.4 6832800FuelInputkWh 1157967756 144591916.1 2002693680FuelCosts($/kWh) $0.0220 $0.0220 $0.0220FuelExpenditures($) $25,451,590.54 $3,178,062.80 $44,018,271.88IncrementalO&MCostsin$/kWh $0.0050 $0.2211 $0.0050O&MExpenditures($) $4,059,843.10 $23,337,661.21 $7,823,910.49TotalCHPplantCosts($/kWh) $0.1474 $0.4051 $0.1308TotalCHPplantexpenditures $127,080,361.7569 $43,615,924.4701 $214,017,688.1895

53

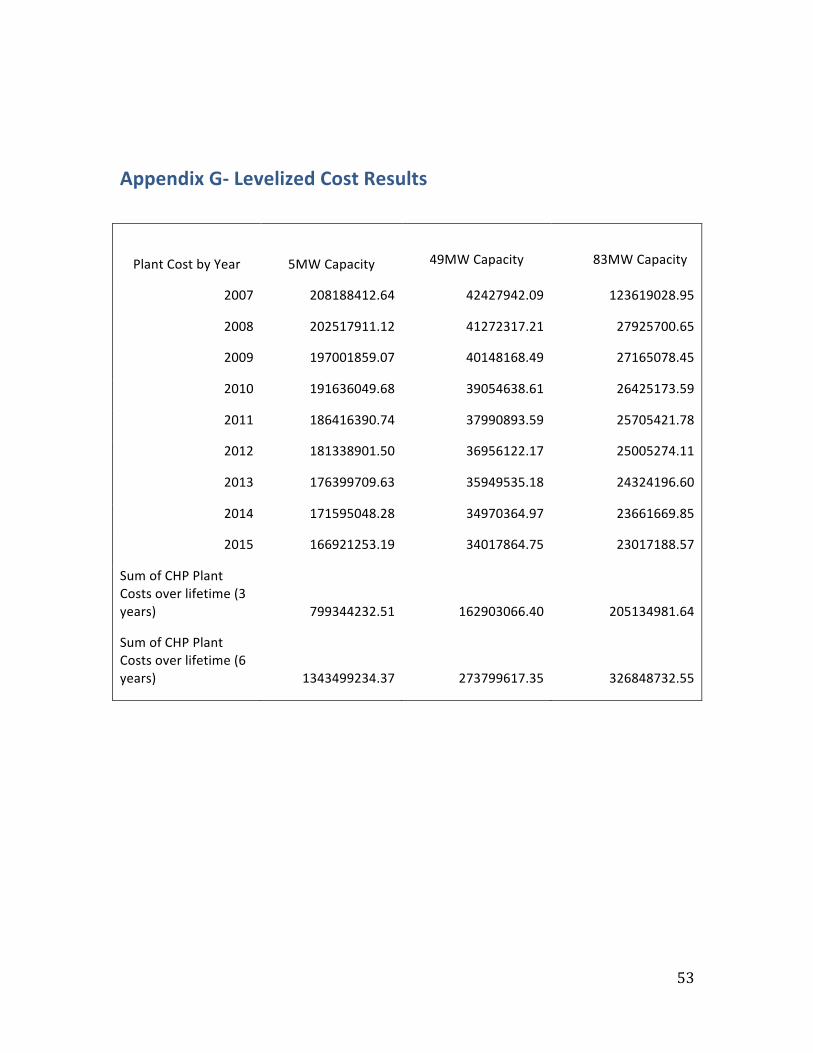

AppendixG‐LevelizedCostResults

PlantCostbyYear

5MWCapacity 49MWCapacity

83MWCapacity

2007 208188412.64 42427942.09 123619028.95

2008 202517911.12 41272317.21 27925700.65

2009 197001859.07 40148168.49 27165078.45

2010 191636049.68 39054638.61 26425173.59

2011 186416390.74 37990893.59 25705421.78

2012 181338901.50 36956122.17 25005274.11

2013 176399709.63 35949535.18 24324196.60

2014 171595048.28 34970364.97 23661669.85

2015 166921253.19 34017864.75 23017188.57

SumofCHPPlantCostsoverlifetime(3years) 799344232.51 162903066.40 205134981.64

SumofCHPPlantCostsoverlifetime(6years) 1343499234.37 273799617.35 326848732.55

54

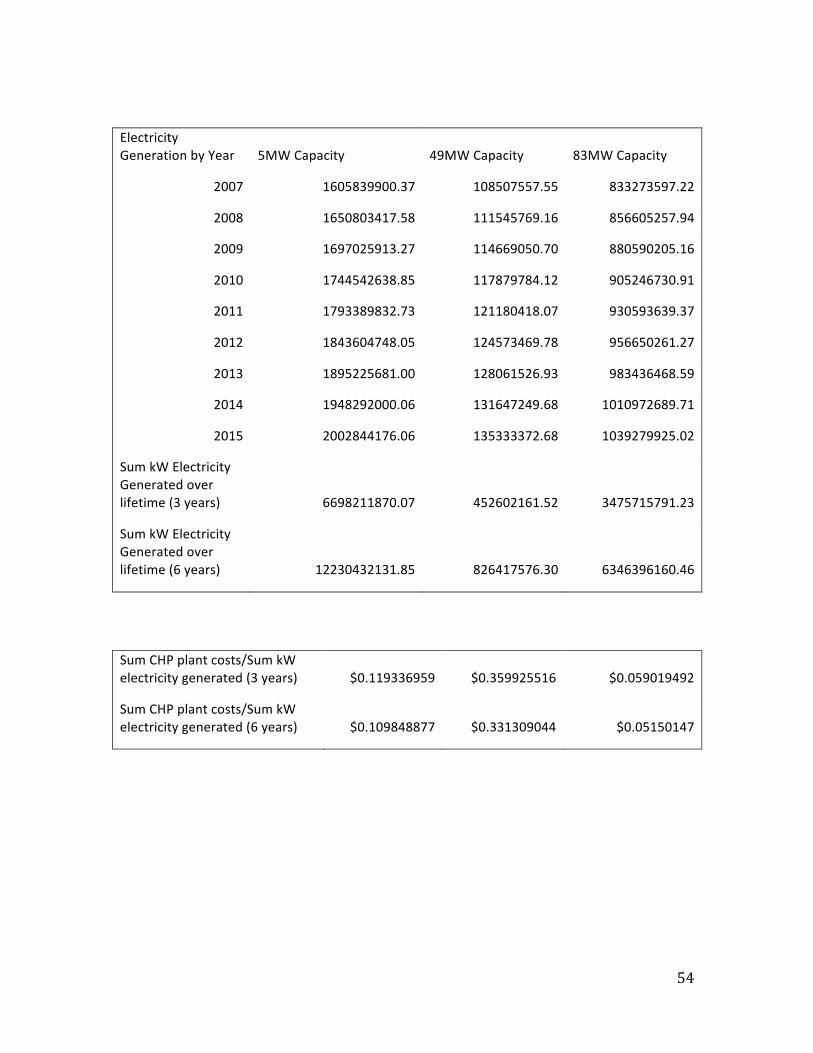

ElectricityGenerationbyYear 5MWCapacity 49MWCapacity 83MWCapacity

2007 1605839900.37 108507557.55 833273597.22

2008 1650803417.58 111545769.16 856605257.94

2009 1697025913.27 114669050.70 880590205.16

2010 1744542638.85 117879784.12 905246730.91

2011 1793389832.73 121180418.07 930593639.37

2012 1843604748.05 124573469.78 956650261.27

2013 1895225681.00 128061526.93 983436468.59

2014 1948292000.06 131647249.68 1010972689.71

2015 2002844176.06 135333372.68 1039279925.02

SumkWElectricityGeneratedoverlifetime(3years) 6698211870.07 452602161.52 3475715791.23

SumkWElectricityGeneratedoverlifetime(6years) 12230432131.85 826417576.30 6346396160.46

SumCHPplantcosts/SumkWelectricitygenerated(3years) $0.119336959 $0.359925516 $0.059019492

SumCHPplantcosts/SumkWelectricitygenerated(6years) $0.109848877 $0.331309044 $0.05150147

55

ReferencesiDevelopmentIndicator–WorldBank.Retrieved12/07/2009fromhttp://datafinder.worldbank.org/about‐world‐development‐indicators?cid=GPD_WDIiiAGuidetoCombinedHeatandPowerSystemsforBoilerOwnersandOperators.–OakRidgeNationalLaboratory2004.Retrieved12/07.2009fromwww1.eere.energy.gov/industry/bestpractices/pdfs/guide_chp_boiler.pdfiiiAGuidetoCombinedHeatandPowerSystemsforBoilerOwnersandOperators.–OakRidgeNationalLaboratory2004.Retrieved12/07.2009fromwww1.eere.energy.gov/industry/bestpractices/pdfs/guide_chp_boiler.pdfivCombinedHeatandPower:CapturingWastedEnergy.R.NealElliottandSpurr,Mark.1999.AmericanCouncilforanEnergyEfficientEconomy.vCombinedHeatandPower:CapturingWastedEnergy.R.NealElliottandSpurr,Mark.1999.AmericanCouncilforanEnergyEfficientEconomy.viTheStateofTheCHPIndustry.UnitedStatesCleanHeatandPowerAssociation.JessicaBridges.2008.Availableat:http://www.epa.gov/chp/documents/meeting_52508_bridges.pdf.(Accessed12/06/2009)viiElectricpowerannual‐existingcapacitybyproducertypeRetrieved12/7/2009,2009,fromhttp://www.eia.doe.gov/cneaf/electricity/epa/epat2p3.htmlviiiElectricpowerannual‐existingcapacitybyproducertypeRetrieved12/7/2009,2009,fromhttp://www.eia.doe.gov/cneaf/electricity/epa/epat1p2.htmlix“EfficiencyBenefits|CombinedHeatandPowerPartnershipHome|U.S.EPA,”http://www.epa.gov/chp/basic/efficiency.html.x“Efficiency|U.S.EPA”xii“Efficiency|U.S.EPA”xiii“EconomicBenefits|CombinedHeatandPowerPartnership|U.S.EPA,”http://www.epa.gov/chp/basic/economics.html.xiv“EconomicBenefits|U.S.EPA”xvReliabilityBenefits|CombinedHeatandPowerPartnership|U.S.EPA,”http://www.epa.gov/chp/basic/reliability.html

56

xvi“EnvironmentalBenefits|CombinedHeatandPowerPartnership|U.S.EPA,”http://www.epa.gov/chp/basic/environmental.html.xvii“EnvironmentalBenefits|U.S.EPA”

xviiiDepartmentofenergy‐naturalgasRetrieved12/7/2009,2009,fromhttp://www.energy.gov/energysources/naturalgas.htm

xixAnnaShipleyetal.,CombinedHeatandPower:EffectiveEnergySolutionsforaSustainableFuture,EnergyEfficiencyandRenewableEnergy(OakRidge,Tennessee:OakRidgeNationalLaboratory,December1,2008).xxShipleyetal.,8xxiShipleyetal.,8xxiiShipleyetal,8xxiiiUnitedStatesDepartmentofEnergy,OfficeofEnergyEfficiencyandRenewableEnergy.ReviewofCombinedHeatandPowerTechnologies.October2009.Availableat:http://www.eere.energy.gov/de/pdfs/chp_review.pdf.AccessedDecember4,2009.

xxivE.ONUK‐combinedheatandpowerRetrieved12/7/2009,2009,fromhttp://www.eon‐uk.com/generation/chp.aspx

xxvUnitedStatesDepartmentofEnergy,OfficeofEnergyEfficiencyandRenewableEnergy.ReviewofCombinedHeatandPowerTechnologies.October2009.Availableat:http://www.eere.energy.gov/de/pdfs/chp_review.pdf.AccessedDecember4,2009.xxviU.S.EnvironmentalProtectionAgency,CombinedHeatandPowerPartnership.CatalogofCHPTechnologies.December2008.

xxviiE.ONUK‐combinedheatandpowerRetrieved12/7/2009,2009,fromhttp://www.eon‐uk.com/generation/chp.aspx

xxviiiU.S.EnvironmentalProtectionAgency,CombinedHeatandPowerPartnership.CatalogofCHPTechnologies.December2008.xxixUnitedStatesDepartmentofEnergy,OfficeofEnergyEfficiencyandRenewableEnergy.ReviewofCombinedHeatandPowerTechnologies.October2009.Availableat:http://www.eere.energy.gov/de/pdfs/chp_review.pdf.AccessedDecember4,2009.xxxMidwestCHPApplicationCenter.ProjectProfile:UniversityofIllinoisChicago(EastCampus).http://www.chpcentermw.org/15‐00_profiles.html#colleges