Embed Size (px)

Citation preview

Competing For Advantage競爭優勢

Part I – Strategic Thinking

Chapter 1 – What is Strategic Management?

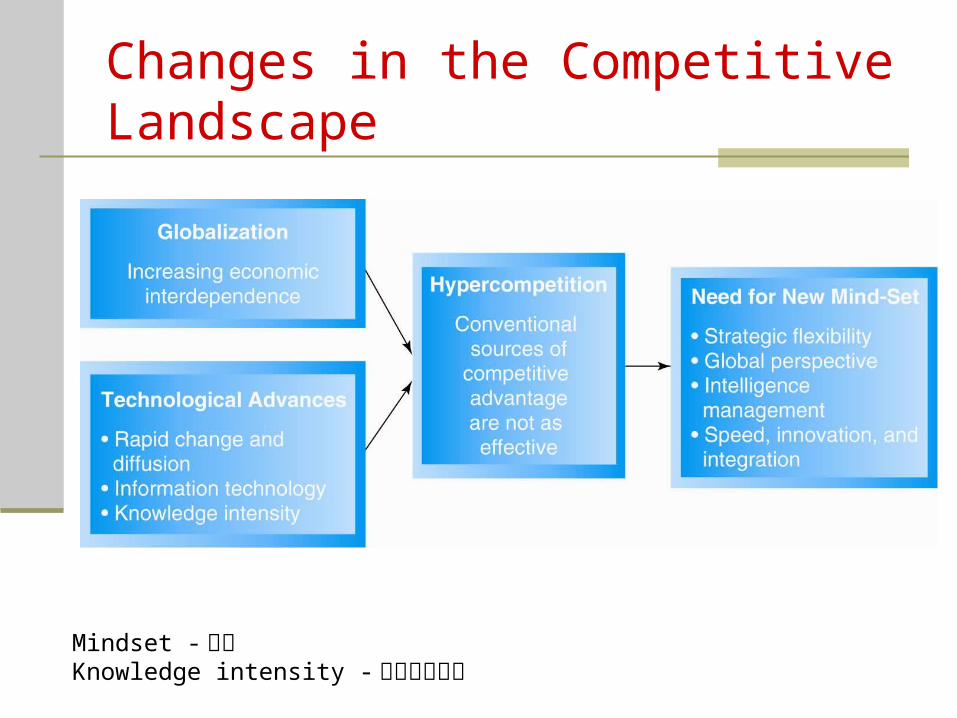

Globalization of Markets and Industries

Key Terms Globalization – increased economic

interdependence增加了經濟上的相互依賴among countries as reflected in the flow of goods and services, financial capital金融資本 , and knowledge across country borders跨國界 (jiè)

Hypercompetition超級競爭– extremely intense rivalry among competing firms, characterized by escalating and increasingly aggressive competitive moves不斷升級和越來越競爭的招式

Technological Advances

Key Terms Strategic Flexibility戰略靈活性– set of

capabilities used to respond設置功能,用於回答 to various demands and opportunities existing in a dynamic and uncertain competitive environment

Increasing rate of technological change and diffusion擴散 , and increasing speed at which technologies become available可得到and are used

Dramatic information technology changes of recent years, and different ways that information is being used (e.g., email)

Technological Trends

Changes in the Competitive Landscape

Mindset -思維Knowledge intensity -知識密集累積

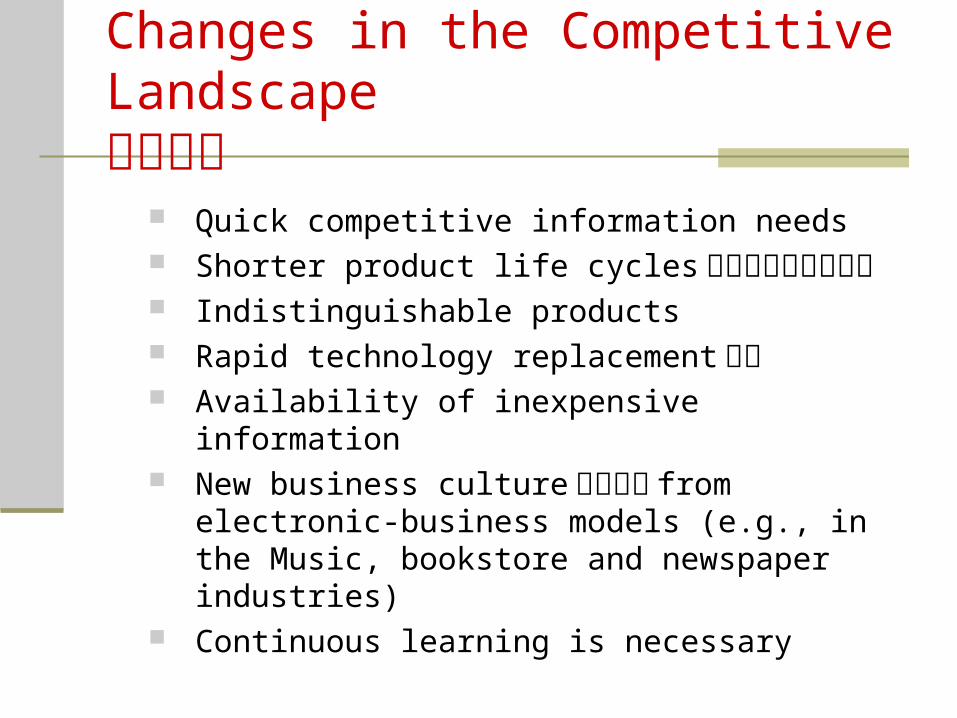

Changes in the Competitive Landscape競爭格局

Quick competitive information needs Shorter product life cycles更短的產品生命週期

Indistinguishable products Rapid technology replacement取代 Availability of inexpensive information New business culture企業文化 from

electronic-business models (e.g., in the Music, bookstore and newspaper industries)

Continuous learning is necessary

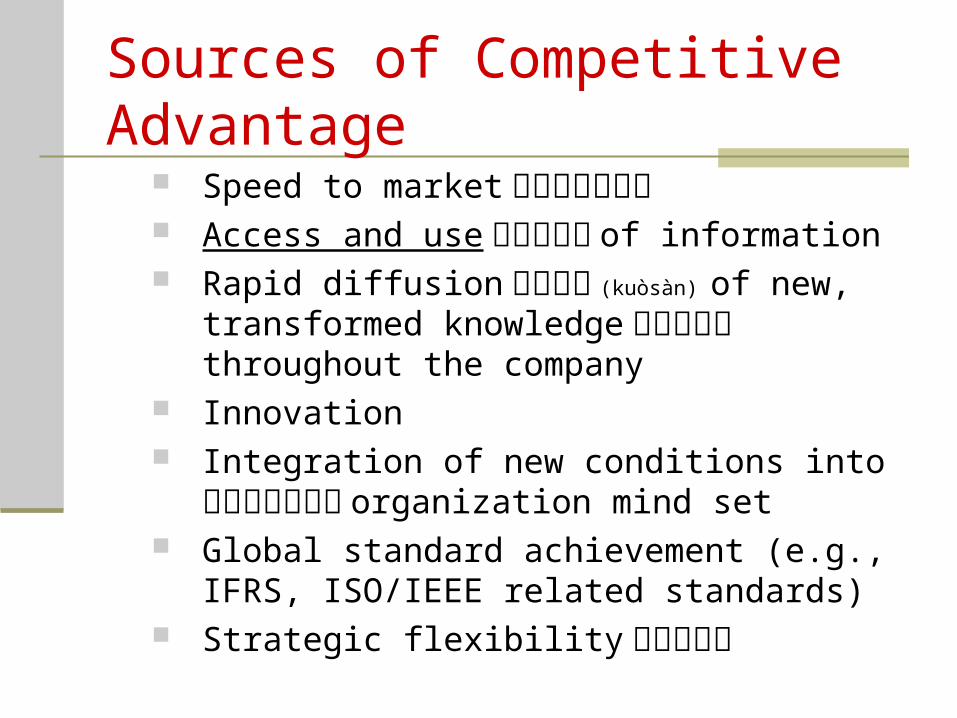

Sources of Competitive Advantage

Speed to market進入市場的速度 Access and use獲取和使用 of information Rapid diffusion快速擴散 (kuòsàn) of new,

transformed knowledge轉變的知識throughout the company

Innovation Integration of new conditions into新的條件整合在 organization mind set

Global standard achievement (e.g., IFRS, ISO/IEEE related standards)

Strategic flexibility戰略靈活性

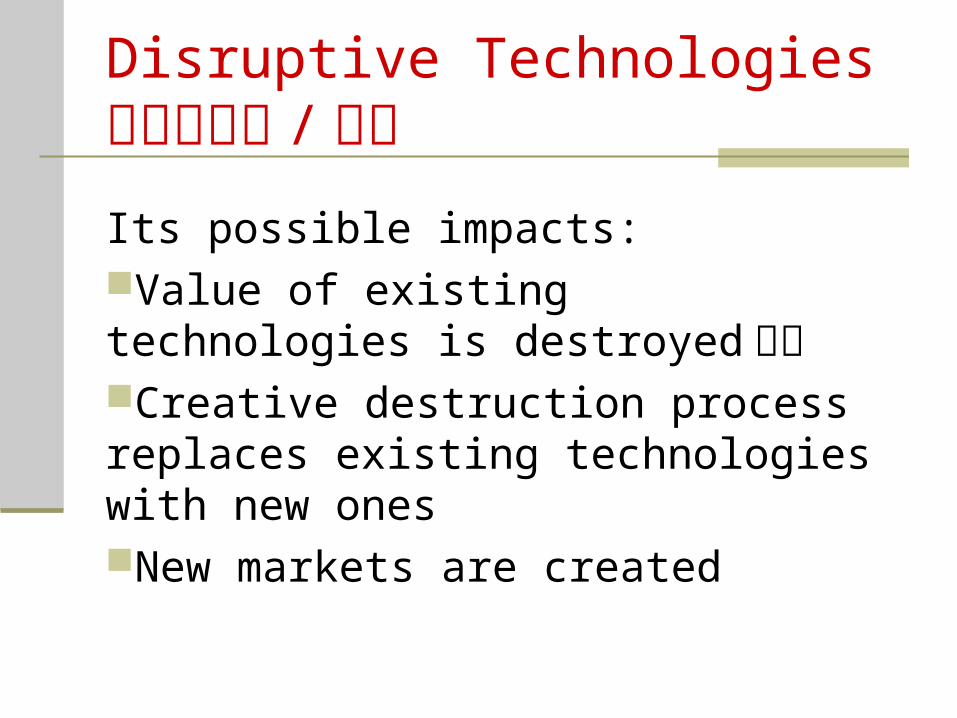

Disruptive Technologies破壞性技術 /科技Its possible impacts:Value of existing technologies is destroyed破壞Creative destruction process replaces existing technologies with new onesNew markets are created

Early Influences on the Strategy Concept

Key Terms Agency Theory委託代理理論 – the idea that

agency problems exist when managers take actions that are in their own best interests rather than those of shareholders股東

Transactions Costs Economics交易成本經濟學 – examination of the efficiency of economic activity活動的經濟效率 that instructs firms to buy required resources through a market transaction, unless certain conditions exist that efficiently allow firms to create them internally

Foundational Concepts

The use of Agency Theory to focus on shareholder returns as a primary criterion for firm success股東收益作為首要標準公司成功

The use of Transactions Costs Economics to determine whether a business should produce or acquire生產或獲得 the resources needed

Modern Strategic Management現代戰略管理 Key Terms

Deterministic確定性 Perspective – the argument that a firm should adapt to its environment, establishing "fit“ (environmental situation determines the most effective strategies for achieving success)企業應該適應環境建立“適合”

Enactment法規– the principle that recognizes the potential承認潛在的 of influencing the environment through human action (environmental forces do not entirely determine strategic moves to create a competitive advantage)

Three Perspectives on Value Creation價值創造

Industrial/Organization (I/O) Economic Model工業 /組織(經濟模型

Resource-Based View資源基礎觀 Stakeholder Approach利益相關者方法

The Industrial/Organization (I/O) Model of Above-Average Returns高於平均水平的收益

Basic Premise (starting assumption)基本前提 of the I/O Model – to explain the dominant influence of the external environment外部環境的影響 on a firm's strategic actions and performance戰略行動和業績

The Industrial/Organization (I/O) Model of Above-Average Returns

Underlying Assumptions That the external environment imposes

pressures and constraints強加壓力和限制 that determine the strategies判斷策略 resulting in above-average returns

That most firms competing within a particular industry行業 or industry segment control similar strategically relevant resources控制類似的戰略相關資源 and pursue追求 similar strategies in light of those resources

The Industrial/Organization (I/O) Model of Above-Average Returns

Underlying Assumptions (cont.) That resources for implementing strategies

are highly mobile流動性很大 across firms, and that due to this mobility any resource differences between firms will be short lived短暫的

That organizational decision makers are rational and committed理性並致力於 to acting in the firm's best interests最佳利益 , as shown by their profit-maximizing behaviors追求利潤最大化的行為

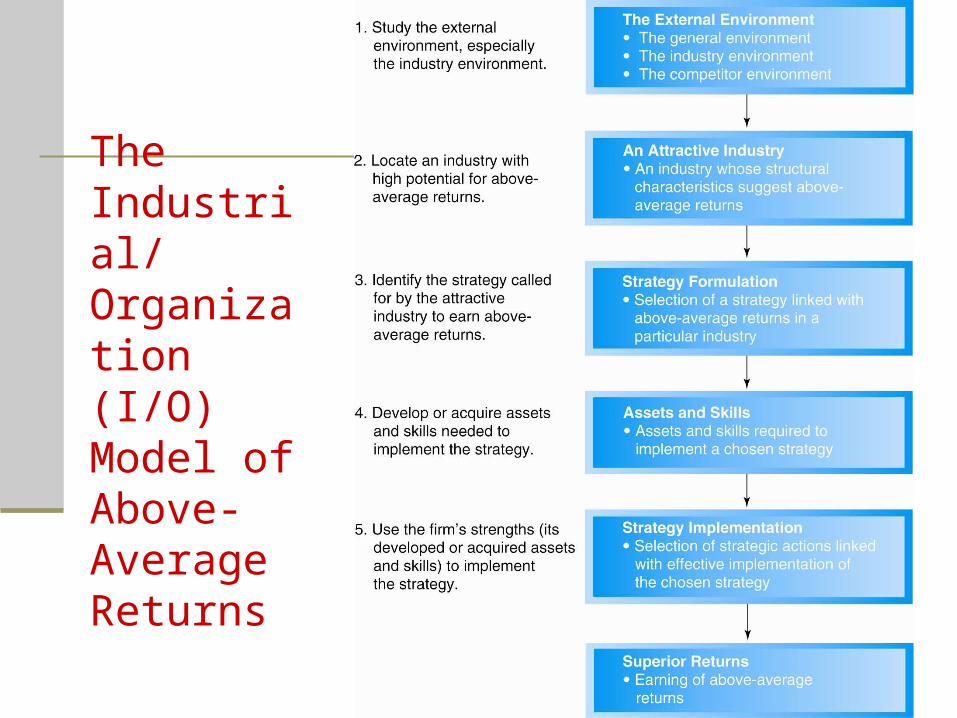

The Industrial/ Organization (I/O) Model of Above-Average Returns

The Industrial/Organization (I/O) Model of Above-Average Returns

Limitations限制 Only two strategies are suggested:

Cost Leadership低成本領先 Differentiation差異化

Internal resources and capabilities內部資源和能力 are not considered

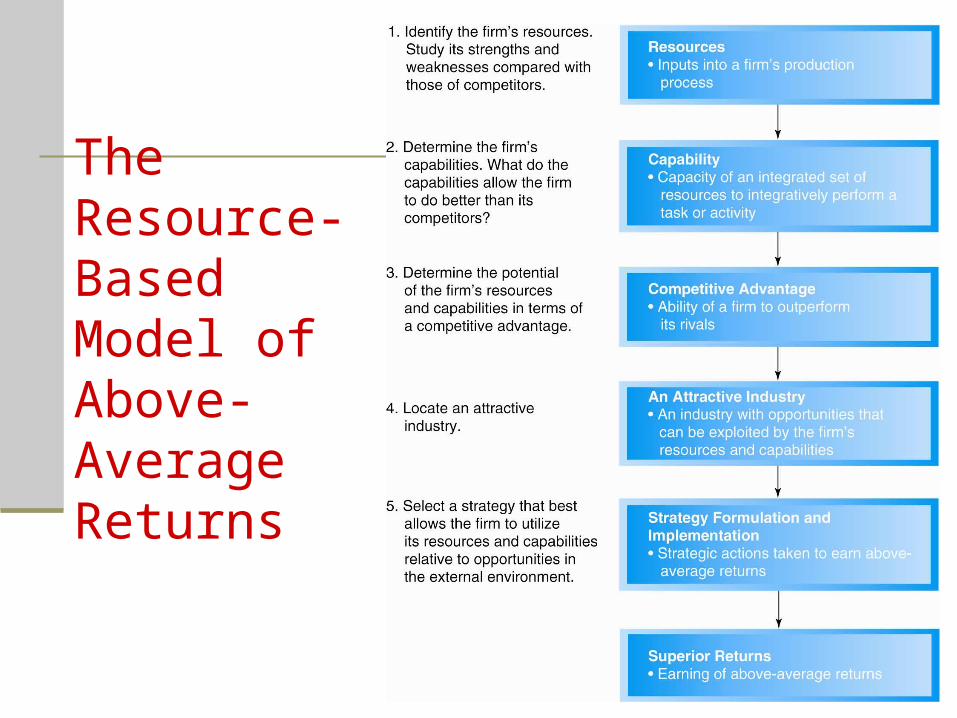

The Resource-Based Model資源基礎模型 of Above-Average Returns Key Terms

Distinctive Competencies特有的競爭優勢– attributes that allow a firm to pursue a certain strategy more efficiently than other firms

Resources – inputs into a firm's production process, such as capital equipment資本設備 , employee skills員工技能 , patents專利 , high-quality managers, financial condition, etc.

Capability能力– capacity for a set of resources to perform a task or activity in an integrative manner一體化的模式

The Resource-Based Model of Above-Average Returns Key Terms (cont.)

Core Competencies核心競爭力– a firm’s resources and capabilities that serve as sources of competitive advantage over its rivals

Competitive Advantage – the successful formulation and execution of strategies成功的制定和執行戰略 that are different from and produce more value than the strategies of competitors

Sustainable可持續 Competitive Advantage (referred to as "Competitive Advantage" in text) – competitive advantage that is possible only after competitors' efforts to duplicate the value-creating strategy複製該價值創造戰略 have ceased or failed

The Resource-Based Model資源基礎模型 of Above-Average Returns

Basic Premise (starting assumption)基本前提 of the Resource-Based Model proposes that

a firm's unique resources and capabilities should define its strategic actions定義其戰略行動 and be used effectively to exploit opportunities in the external environment to ensure successful performance

The Resource-Based Model of Above-Average Returns

Three Categories of Resources Physical物質 Human人力 Organizational capital組織資本

The Resource-Based Model of Above-Average Returns

Types of resources that become a competitive advantage must have the characteristics of

Valuable有價值的 Rare難得的 Costly to imitate難以模仿 Nonsubstitutable不可替 (tì)代

The Resource-Based Model of Above-Average Returns

Two types of core competencies核心能力

Managerial competencies管理能力

Product-related competencies產品相關能力

The Resource-Based Model of Above-Average Returns

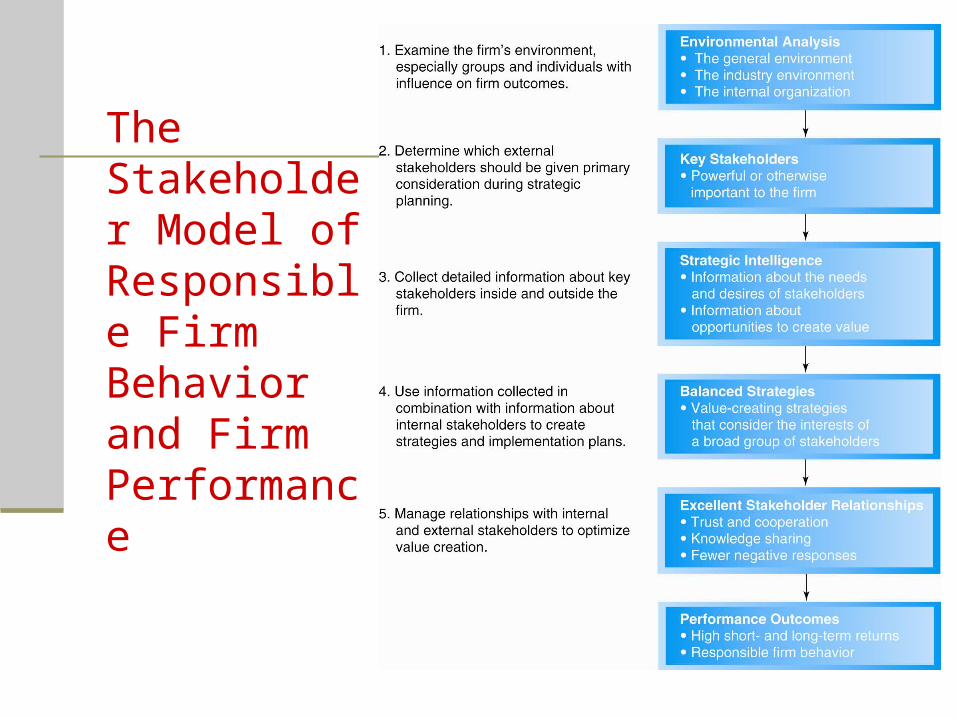

The Stakeholder Model of Responsible Firm Behavior and Firm Performance

Key Terms Stakeholders – individuals and groups that

can affect (and are affected by) the strategic outcomes a firm achieves, and that have enforceable claims on a firm's performance

Strategic Intelligence – information that firms collect from their network of stakeholders and use to deal with diverse and cognitively complex competitive situations

The Stakeholder Model of Responsible Firm Behavior and Firm Performance

Basic Premise of the Stakeholder Model – to propose that a firm can effectively manage stakeholder relationships to create a competitive advantage and outperform its competitors

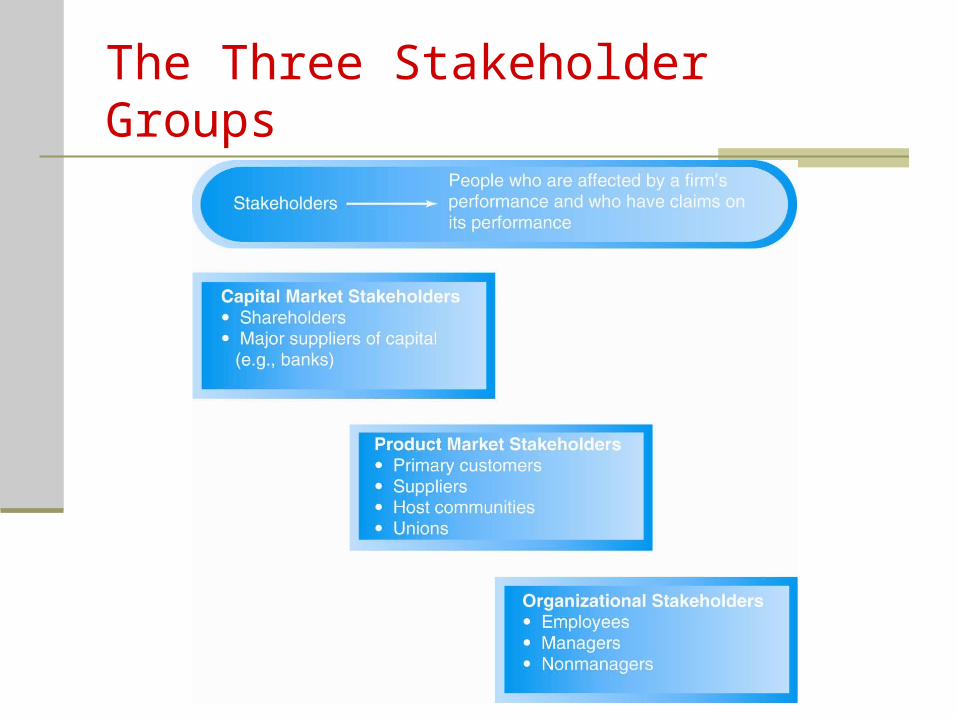

The Three Stakeholder Groups

Secondary Stakeholders

Government entities and administrators

Activists and advocacy groups Religious organizations Other nongovernmental

organizations

The Stakeholder Model of Responsible Firm Behavior and Firm Performance

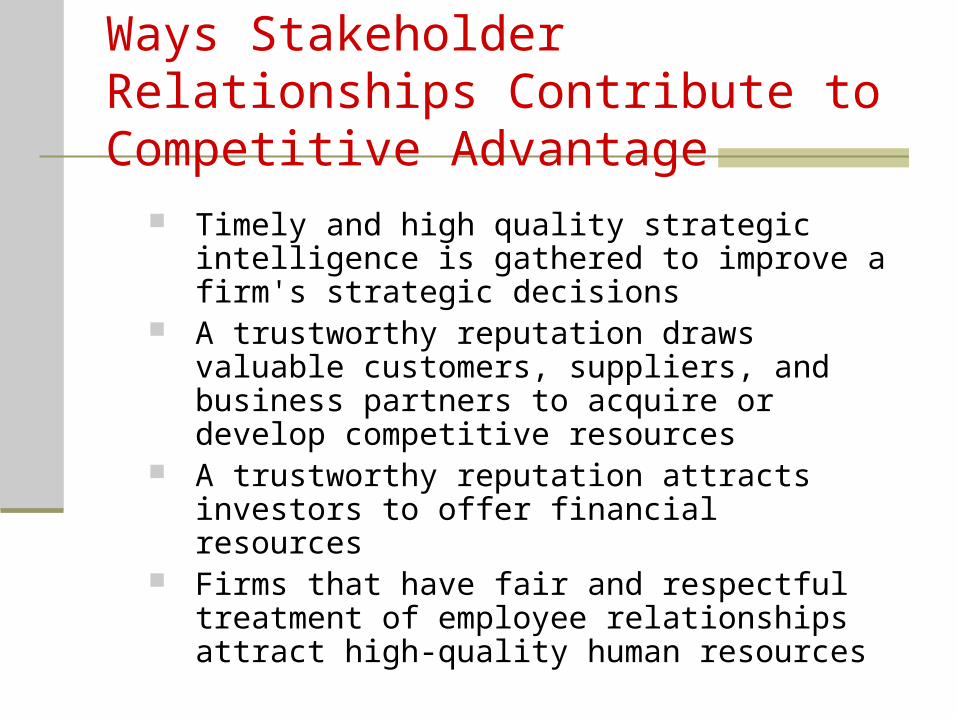

Ways Stakeholder Relationships Contribute to Competitive Advantage

Timely and high quality strategic intelligence is gathered to improve a firm's strategic decisions

A trustworthy reputation draws valuable customers, suppliers, and business partners to acquire or develop competitive resources

A trustworthy reputation attracts investors to offer financial resources

Firms that have fair and respectful treatment of employee relationships attract high-quality human resources

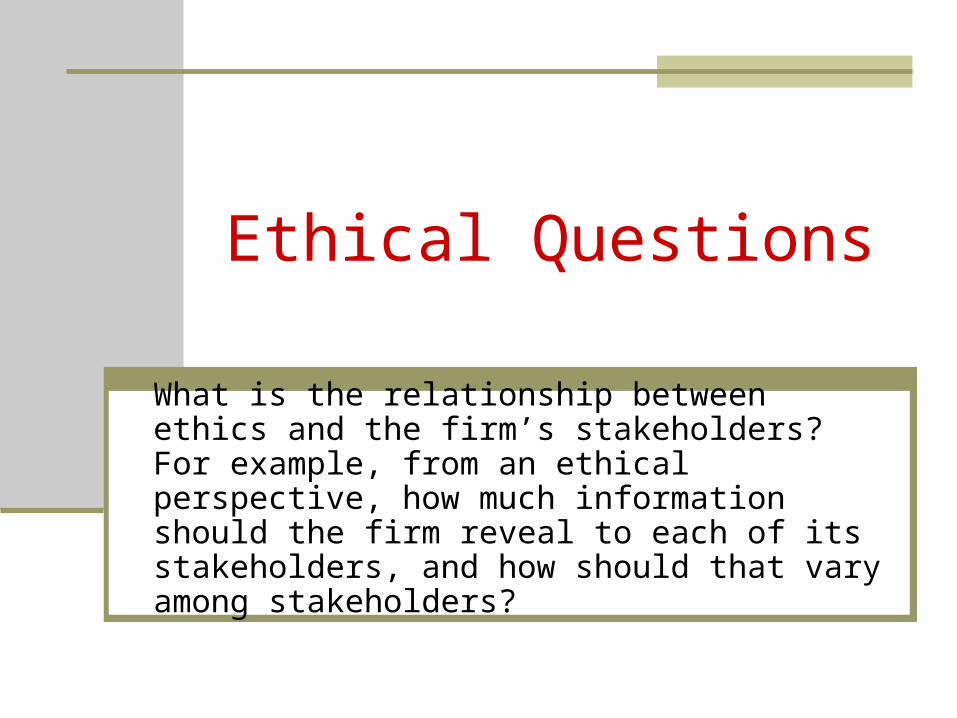

Ethical Questions

What is the relationship between ethics and the firm’s stakeholders? For example, from an ethical perspective, how much information should the firm reveal to each of its stakeholders, and how should that vary among stakeholders?

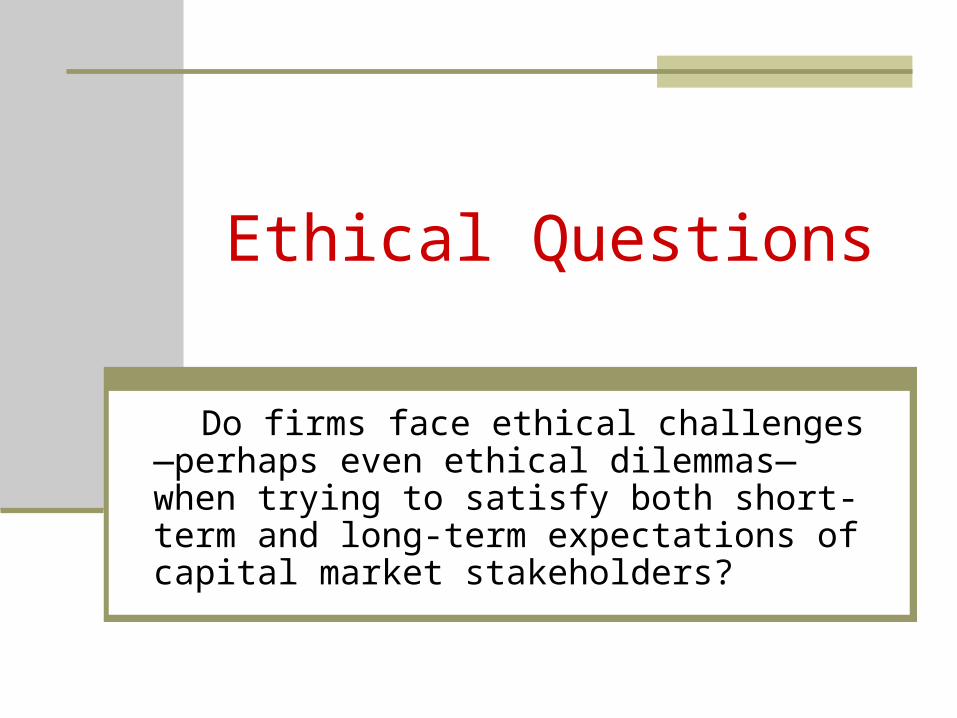

Ethical Questions

Do firms face ethical challenges—perhaps even ethical dilemmas—when trying to satisfy both short-term and long-term expectations of capital market stakeholders?

Ethical Questions

What types of ethical issues and challenges do firms encounter when competing internationally?

Ethical Questions

What ethical responsibilities does the firm have when it earns above-average returns? Who should make decisions regarding these issues, and why?

Ethical Questions

How should ethical considerations be included in analyses of the firm’s external environment and internal organization?

Ethical Questions

What should top-level managers do to ensure that a firm’s strategic management process leads to outcomes that are consistent with the firm’s values?

![Competing Values Scan at [CLIENT]](https://img.pdfslide.tips/doc/110x75/568bda5e1a28ab2034aa885b/competing-values-scan-at-client.jpg)