Embed Size (px)

Citation preview

ConstructionConstruction Performance Audits: How to AchieveHow to AchieveCompliance and Program Goals Presenters: Curtis Matthews Partner Curtis Matthews, Partner Shirley Komoto, Senior Manager

October 7, 2010

AgendaAgenda

≡ Current Situation ≡ Why Construction Programs Are So Risky≡ Common Construction Program Exposures ≡ Performance Audit Definitions≡ Compliance Performance Audits ≡ Economy, Efficiency and Internal Control Performance Audits ≡ Q&A≡ Q&A

MOSS ADAMS LLP | 2

Th C t Sit ti The Current Situation

MOSS ADAMS LLP | 3

Current Situation with Education FacilitiesCurrent Situation with Education Facilities

≡ Aging facilities and increase in facilities use≡ Demographic population shift to western and/or sun belt states ≡ Significant public interest and internal stakeholder impact

MOSS ADAMS LLP | 4

≡ Significant public interest and internal stakeholder impact

Current Situation with Education Facilities

Current Situation with Education Facilities

≡ Statutory requirements (e.g. CA Proposition 39) ≡ Senate Bill No. 1473 requiring GAGAS compliance≡ Changing curriculum requirements impacting facilities ≡ Fluctuating material and labor costs and exceedingly

MOSS ADAMS LLP | 5

≡ Fluctuating material and labor costs, and exceedingly competitive contractor bids

Current Situation with Education FacilitiesCurrent Situation with Education Facilities

≡ Narrowly defined Bond Compliance requirements ≡ Shortage of available funds (restricted state funding) ≡ Severe consequences for the perception of failure

MOSS ADAMS LLP | 6

Ri k Risk

MOSS ADAMS LLP | 7

Why Construction Programs are So Risky≡ Significant expenditures ≡ High profile projects/programs receive extra scrutiny

Why Construction Programs are So Risky

≡ High profile projects/programs receive extra scrutiny≡ Misunderstanding of compliance requirements ≡ Construction is not your core competency ≡ High reliance on outside architects, engineers and contractors ≡ Problems can lead to huge losses, significant litigation issues ≡ Construction delays could affect readiness for classes≡ Construction delays could affect readiness for classes

MOSS ADAMS LLP | 8

Why Construction Programs are So RiskyWhy Construction Programs are So Risky

MOSS ADAMS LLP | 9

P E

Program Exposures

MOSS ADAMS LLP | 10

Common Construction Program Exposures: Financial and Audit Compliance

≡ Bond monies allocated and used for general fund purposes ≡ Bond fund expenditures used for projects not listed in the Bond ≡ Audit firm not qualified or work does not comply with GAGAS

MOSS ADAMS LLP | 11

Common Construction Program Exposures:

Operations Effectiveness and Efficiency

≡ Excessive requirements and scope creep ≡ Excessive change order costs ≡ Project delays and disruptions ≡ Cost escalation overcharges and costly practices

MOSS ADAMS LLP | 12

≡ Cost escalation, overcharges and costly practices≡ Construction quality issues

Wh t i What is a Performance Audit?

MOSS ADAMS LLP | 13

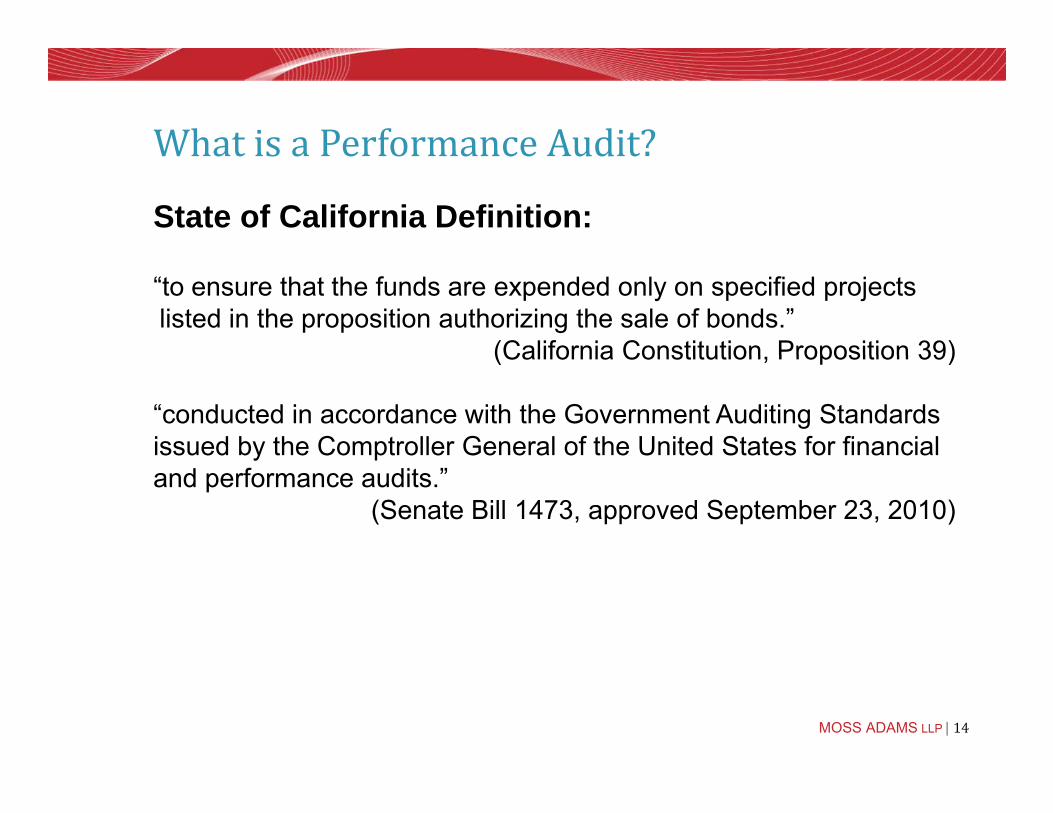

What is a Performance Audit?What is a Performance Audit?

State of California Definition: “to ensure that the funds are expended only on specified projects listed in the proposition authorizing the sale of bonds.”

(California Constitution Proposition 39)(California Constitution, Proposition 39) “conducted in accordance with the Government Auditing Standards issued by the Comptroller General of the United States for financial y pand performance audits.”

(Senate Bill 1473, approved September 23, 2010)

MOSS ADAMS LLP | 14

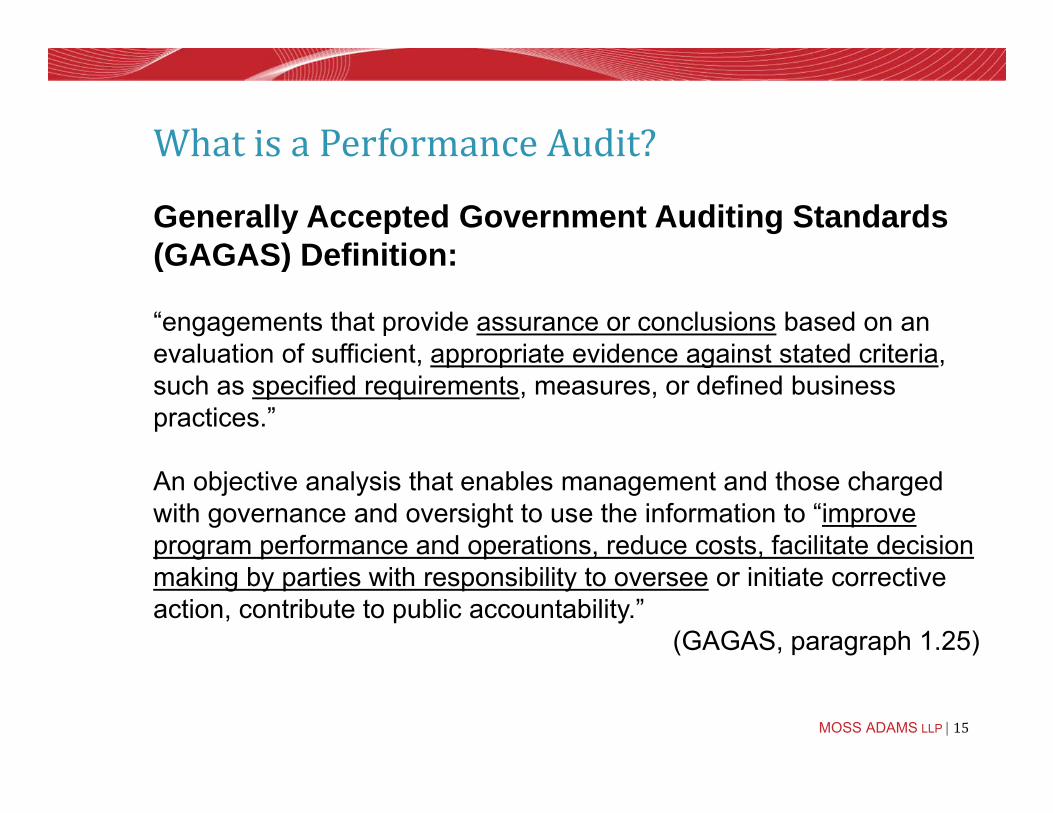

What is a Performance Audit?

Generally Accepted Government Auditing Standards (GAGAS) Definition:

What is a Performance Audit?

(GAGAS) Definition: “engagements that provide assurance or conclusions based on an evaluation of sufficient appropriate evidence against stated criteriaevaluation of sufficient, appropriate evidence against stated criteria, such as specified requirements, measures, or defined business practices.” An objective analysis that enables management and those charged with governance and oversight to use the information to “improve program performance and operations, reduce costs, facilitate decision making by parties with responsibility to oversee or initiate corrective action, contribute to public accountability.”

(GAGAS, paragraph 1.25)

MOSS ADAMS LLP | 15

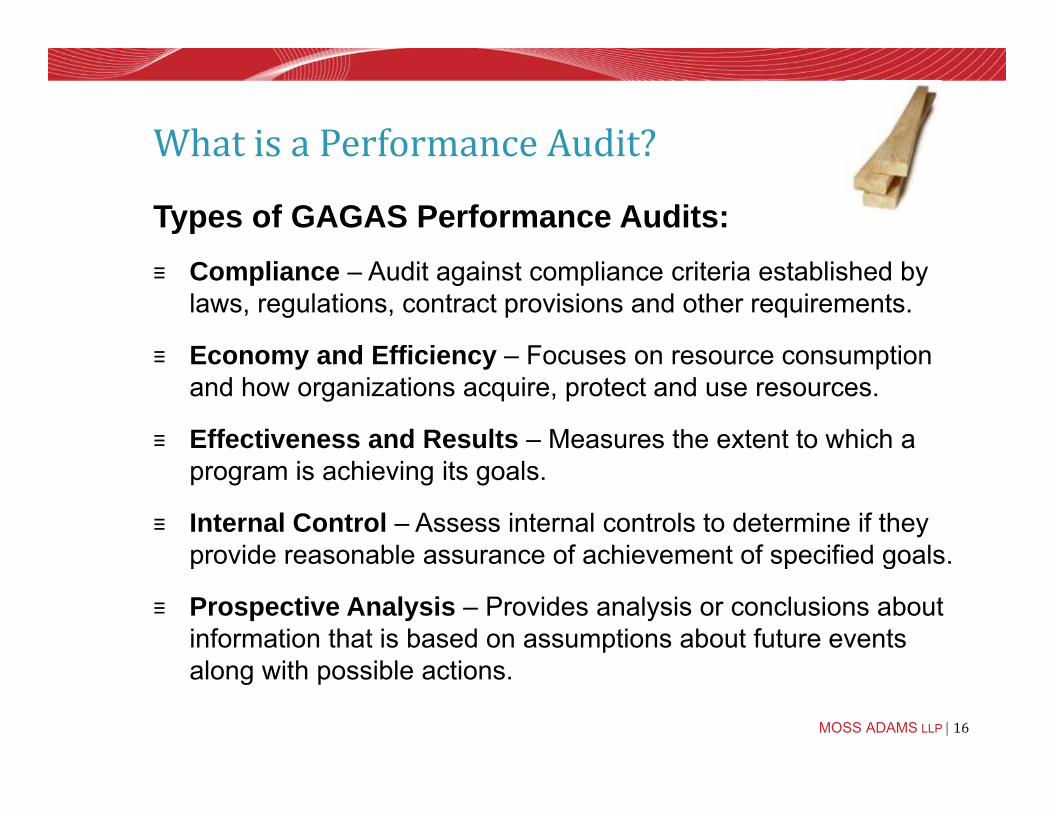

What is a Performance Audit?

Types of GAGAS Performance Audits:

What is a Performance Audit?

≡ Compliance – Audit against compliance criteria established by laws, regulations, contract provisions and other requirements.

≡ Economy and Efficiency Focuses on resource consumption≡ Economy and Efficiency – Focuses on resource consumption and how organizations acquire, protect and use resources.

≡ Effectiveness and Results – Measures the extent to which a program is achieving its goals.

≡ Internal Control – Assess internal controls to determine if they provide reasonable assurance of achievement of specified goalsprovide reasonable assurance of achievement of specified goals.

≡ Prospective Analysis – Provides analysis or conclusions about information that is based on assumptions about future events l ith ibl ti

MOSS ADAMS LLP | 16

along with possible actions.

What is a Performance Audit?

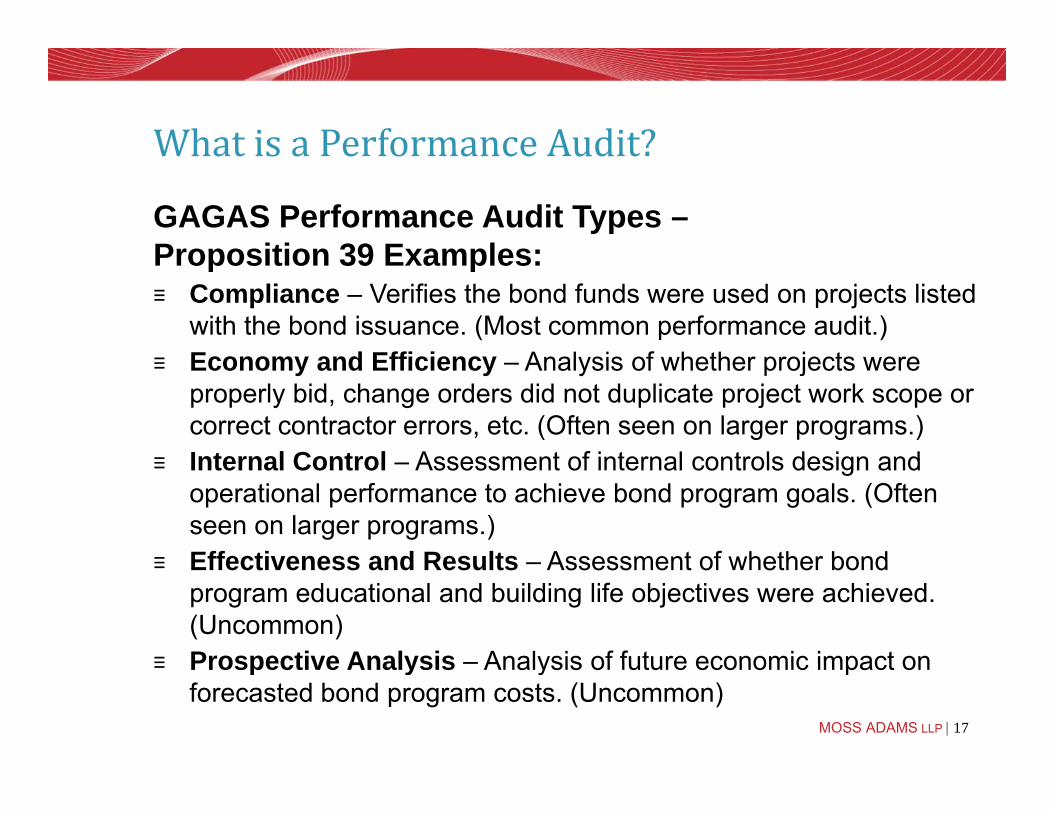

GAGAS Performance Audit Types – Proposition 39 Examples:

What is a Performance Audit?

Proposition 39 Examples:≡ Compliance – Verifies the bond funds were used on projects listed

with the bond issuance. (Most common performance audit.) E d Effi i A l i f h th j t≡ Economy and Efficiency – Analysis of whether projects were properly bid, change orders did not duplicate project work scope or correct contractor errors, etc. (Often seen on larger programs.)

≡ Internal Control Assessment of internal controls design and≡ Internal Control – Assessment of internal controls design and operational performance to achieve bond program goals. (Often seen on larger programs.)

≡ Effectiveness and Results Assessment of whether bond≡ Effectiveness and Results – Assessment of whether bond program educational and building life objectives were achieved. (Uncommon)

≡ Prospective Analysis – Analysis of future economic impact on

MOSS ADAMS LLP | 17

≡ Prospective Analysis – Analysis of future economic impact on forecasted bond program costs. (Uncommon)

P iti 39 Proposition 39 Compliance

Performance Audits

Performance Audits

MOSS ADAMS LLP | 18

FocusFocus

Compliant use of funds

MOSS ADAMS LLP | 19

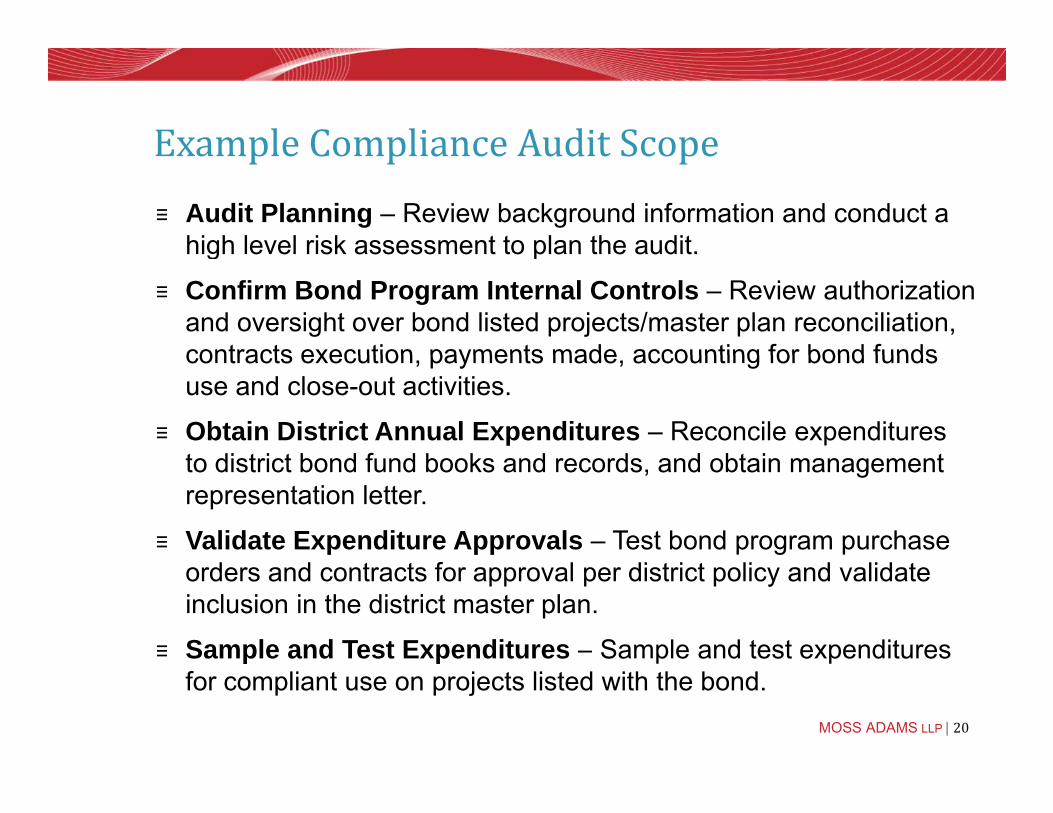

Example Compliance Audit Scope≡ Audit Planning – Review background information and conduct a

high level risk assessment to plan the audit.

Example Compliance Audit Scope

high level risk assessment to plan the audit.

≡ Confirm Bond Program Internal Controls – Review authorization and oversight over bond listed projects/master plan reconciliation, contracts execution payments made accounting for bond fundscontracts execution, payments made, accounting for bond funds use and close-out activities.

≡ Obtain District Annual Expenditures – Reconcile expenditures t di t i t b d f d b k d d d bt i tto district bond fund books and records, and obtain management representation letter.

≡ Validate Expenditure Approvals – Test bond program purchase orders and contracts for approval per district policy and validate inclusion in the district master plan.

≡ Sample and Test Expenditures – Sample and test expenditures

MOSS ADAMS LLP | 20

p p p pfor compliant use on projects listed with the bond.

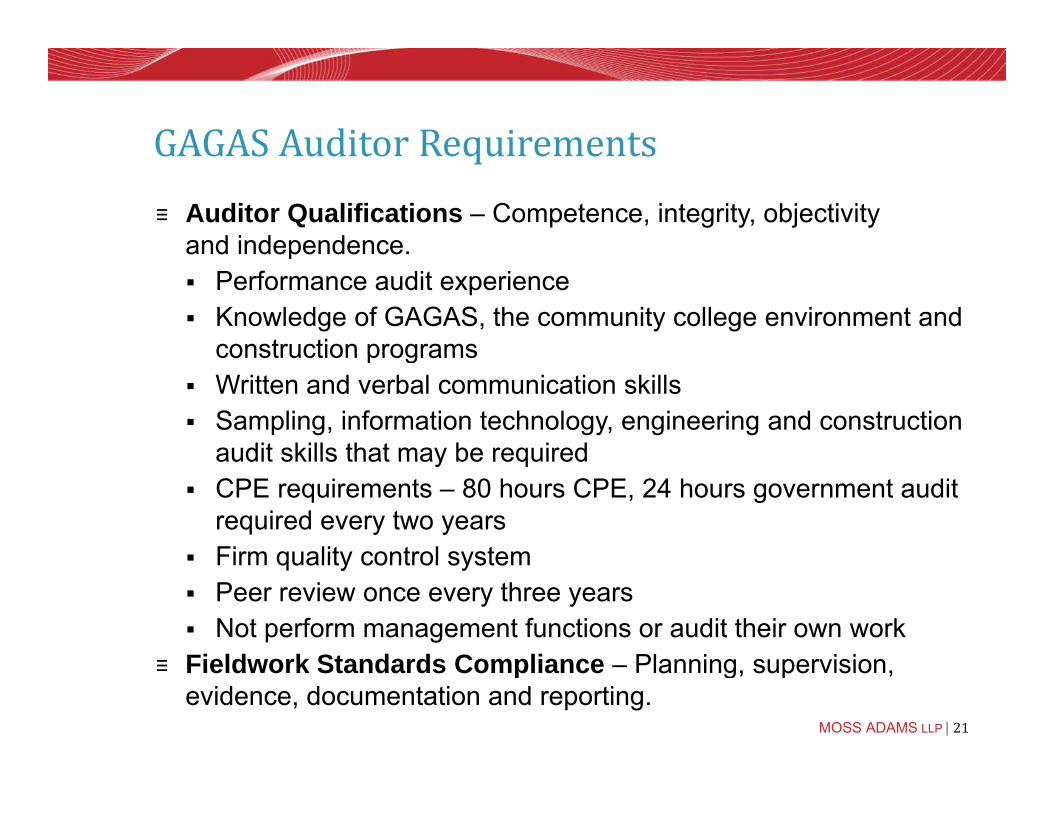

GAGAS Auditor Requirements≡ Auditor Qualifications – Competence, integrity, objectivity

and independence.

GAGAS Auditor Requirements

and independence. Performance audit experience Knowledge of GAGAS, the community college environment and

construction programsconstruction programs Written and verbal communication skills Sampling, information technology, engineering and construction

audit skills that may be requiredaudit skills that may be required CPE requirements – 80 hours CPE, 24 hours government audit

required every two years Firm quality control system Firm quality control system Peer review once every three years Not perform management functions or audit their own work

≡ Fieldwork Standards Compliance Planning supervision

MOSS ADAMS LLP | 21

≡ Fieldwork Standards Compliance – Planning, supervision, evidence, documentation and reporting.

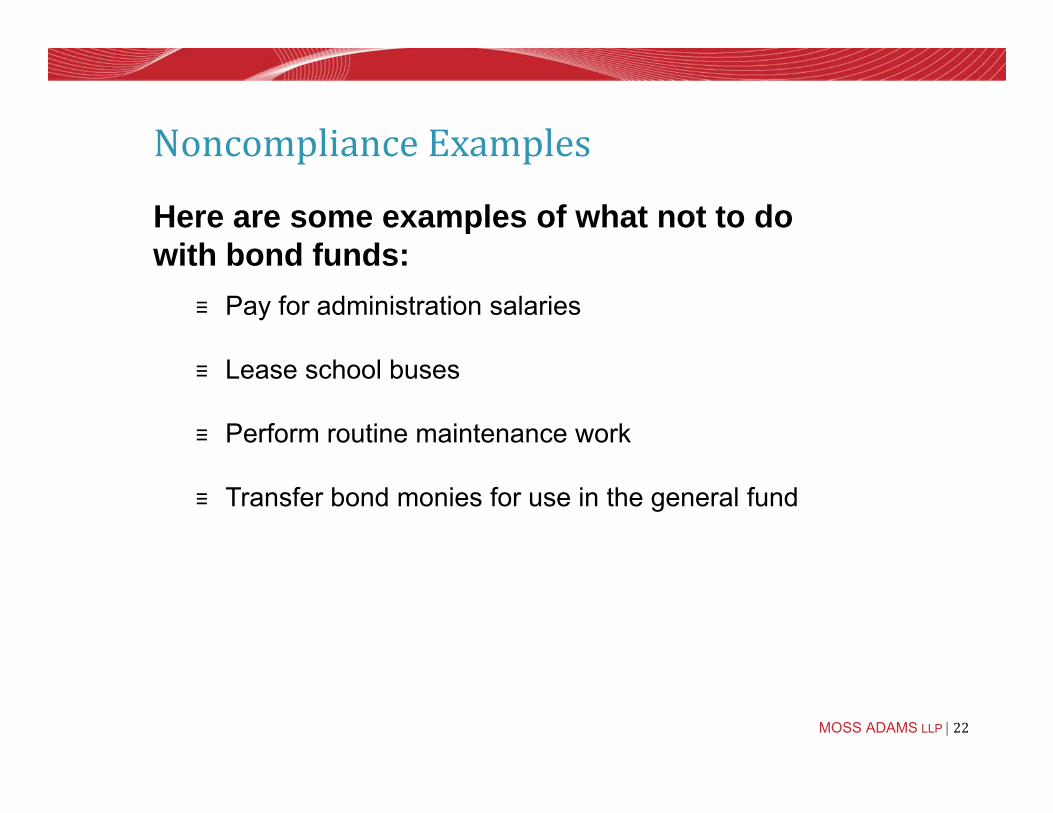

Noncompliance Examples

Here are some examples of what not to do with bond funds:

Noncompliance Examples

with bond funds:≡ Pay for administration salaries

≡ Lease school buses

≡ Perform routine maintenance work

≡ Transfer bond monies for use in the general fund

MOSS ADAMS LLP | 22

P iti 39 Proposition 39 Economy, Efficiency and

Internal Control

Internal Control Performance Audits

MOSS ADAMS LLP | 23

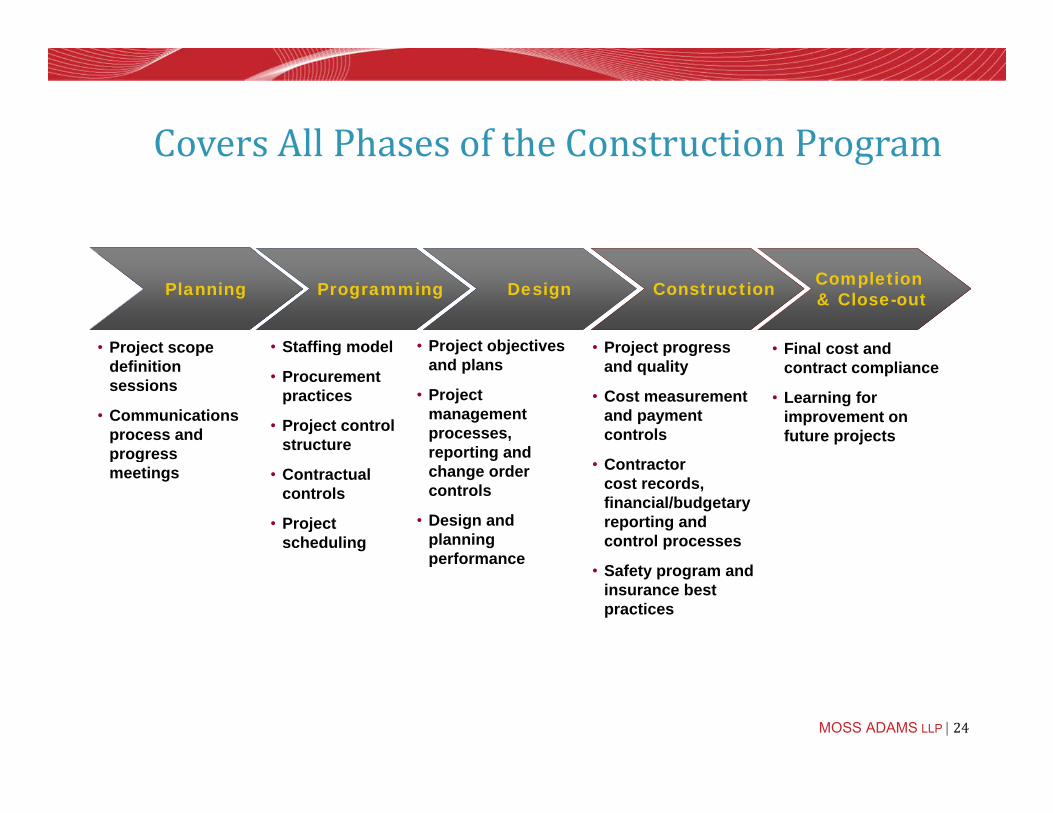

Covers All Phases of the Construction ProgramCovers All Phases of the Construction Program

• Project scope • Project objectives • Final cost and • Staffing model

Completion & Close-out Planning Programming Design Construction

• Project progress j pdefinition sessions

• Communications process and progress

and plans

• Project management processes, reporting and

contract compliance

• Learning for improvement on future projects

• Procurement practices

• Project control structure

j p gand quality

• Cost measurement and payment controls

progress meetings

p gchange order controls

• Design and planning performance

• Contractual controls

• Project scheduling

• Contractor cost records, financial/budgetary reporting and control processes

performance• Safety program and

insurance best practices

MOSS ADAMS LLP | 24

Provides:

Provides:

More complete and balanced performance audit reporting p p p g

to address stakeholder perceptions Efficiencies to better achieve program goals Adaptation of good practices from other programs

MOSS ADAMS LLP | 25

Adaptation of good practices from other programs

Focus AreasFocus Areas

Ch d d Change order and closeout controls to prevent litigation prevent litigation

MOSS ADAMS LLP | 26

Focus Areas (cont )Focus Areas (cont.)

Stakeholder communication and

it bl equitable use of funds

MOSS ADAMS LLP | 27

Focus Areas (cont )Focus Areas (cont.)

Staffing needed Staffing needed to deliver projects

on time and within budget

MOSS ADAMS LLP | 28

Focus Areas (cont )Focus Areas (cont.)

Consistent li i f application of

construction program policies program policies and procedures

MOSS ADAMS LLP | 29

Focus Areas (cont )Focus Areas (cont.)

Construction productivity and

efficiency management

MOSS ADAMS LLP | 30

Focus Areas (cont )Focus Areas (cont.)

Completeness and integrity of

t ti construction program reporting

MOSS ADAMS LLP | 31

Focus Areas (cont )Focus Areas (cont.)

P j t t Project management information systems use and data integrity use and data integrity

MOSS ADAMS LLP | 32

Focus Areas (cont )Focus Areas (cont.)

Construction contract controls contract controls

MOSS ADAMS LLP | 33

Focus Areas (cont )Focus Areas (cont.)

Contractor billing compliance controls

MOSS ADAMS LLP | 34

Focus Areas (cont )Focus Areas (cont.)

Contractor solvency monitoring monitoring

MOSS ADAMS LLP | 35

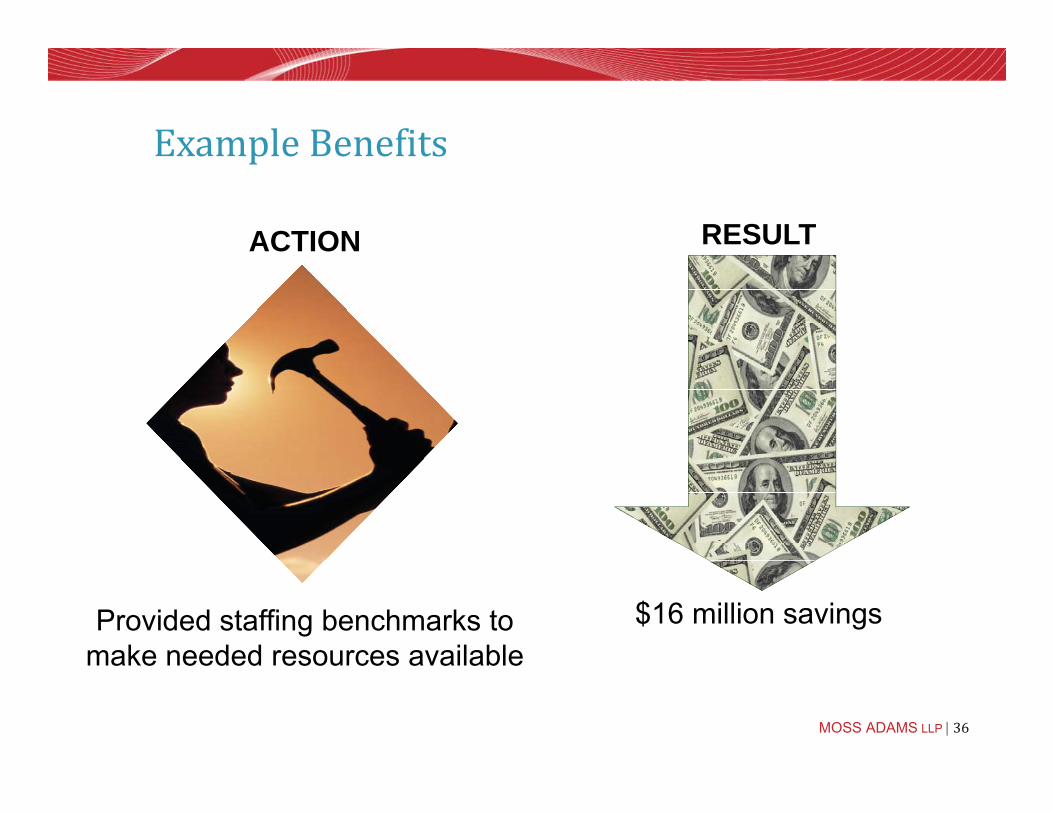

Example Benefits

ACTION RESULT

Example Benefits

Provided staffing benchmarks to

make needed resources available$16 million savings

MOSS ADAMS LLP | 36

make needed resources available

Example Benefits (cont )

ACTION RESULT

Example Benefits (cont.)

Identified excessive

change order charges$4.5 million savings

MOSS ADAMS LLP | 37

change order charges

Example Benefits (cont )

ACTION RESULT

Example Benefits (cont.)

Identified duplicated

change order work scope$4 million savings

MOSS ADAMS LLP | 38

change order work scope

Other Benefits of a Performance Audit

≡ Provides best practice

Other Benefits of a Performance Audit

pconstruction program master planning controls

≡ Implements best practice≡ Implements best practice policies and procedures for successful programs B tt t k h ld≡ Better stakeholder understanding of program good practices and exposure areas

MOSS ADAMS LLP | 39

Q&A Q&A

MOSS ADAMS LLP | 40

Moss Adams Contacts

C ti M tth

Moss Adams Contacts

Curtis Matthews (503) 704‐6943

Shirley Komoto (562) 618‐7993

h l k [email protected]

MOSS ADAMS LLP | 41