Embed Size (px)

Citation preview

Debt Instruments and Markets Professor Carpenter

Convexity 1

Convexity

ConceptsandBuzzwords• DollarConvexity• Convexity

• Curvature• Taylorseries• Barbell,Bullet

Readings• Veronesi,Chapter4• Tuckman,Chapters5and6

Debt Instruments and Markets Professor Carpenter

Convexity 2

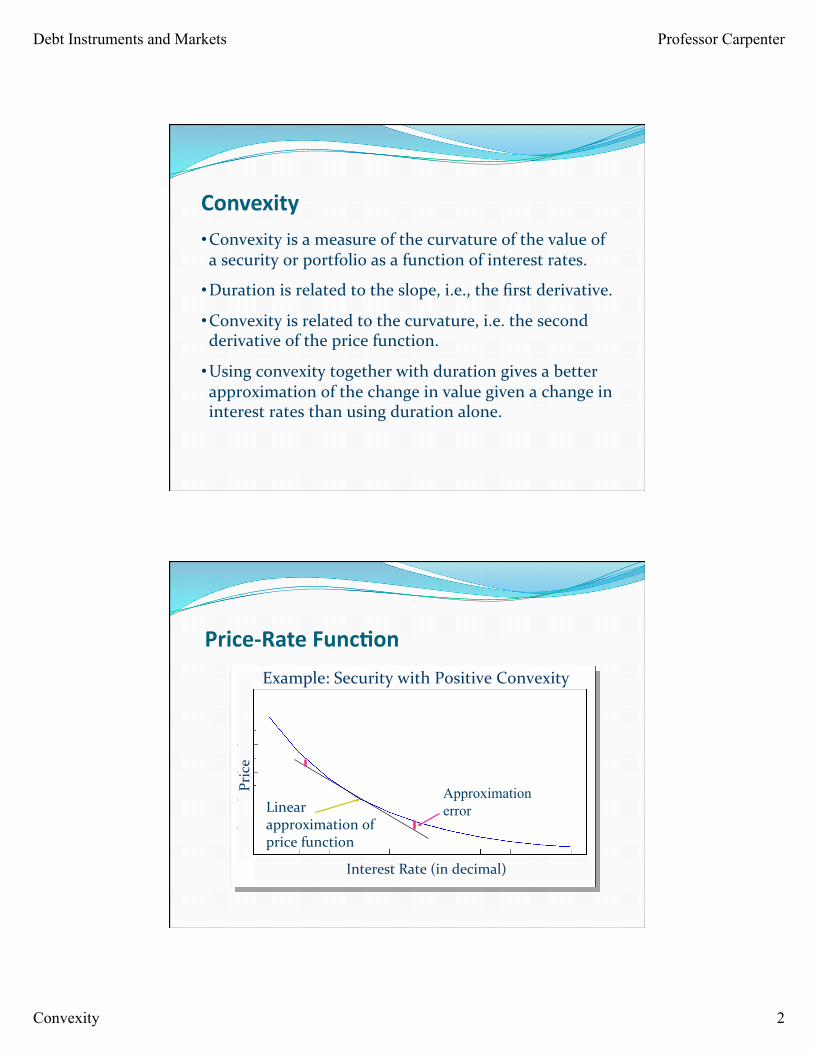

Convexity• Convexityisameasureofthecurvatureofthevalueofasecurityorportfolioasafunctionofinterestrates.

• Durationisrelatedtotheslope,i.e.,thefirstderivative.

• Convexityisrelatedtothecurvature,i.e.thesecondderivativeofthepricefunction.

• Usingconvexitytogetherwithdurationgivesabetterapproximationofthechangeinvaluegivenachangeininterestratesthanusingdurationalone.

Price

InterestRate(indecimal)

Example:SecuritywithPositiveConvexity

Price‐RateFunc:on

Linearapproximationofpricefunction

Approximation error

Debt Instruments and Markets Professor Carpenter

Convexity 3

Correc:ngtheDura:onError

• Theprice‐ratefunctionisnonlinear.

• Durationanddollardurationusealinearapproximationtothepriceratefunctiontomeasurethechangeinpricegivenachangeinrates.

• Theerrorintheapproximationcanbesubstantiallyreducedbymakingaconvexitycorrection.

TaylorSeries• TheTaylorTheoremfromcalculussaysthatthevalueofafunctioncanbeapproximatednearagivenpointusingits“Taylorseries”aroundthatpoint.

• Usingonlythefirsttwoderivatives,theTaylorseriesapproximationis:

€

f (x) ≈ f (x0) + f '(x0) × (x − x0) +12f ' '(x0) × (x − x0)2

Or, f (x) − f (x0) ≈ f '(x0) × (x − x0) +12f ' '(x0) × (x − x0)2

Debt Instruments and Markets Professor Carpenter

Convexity 4

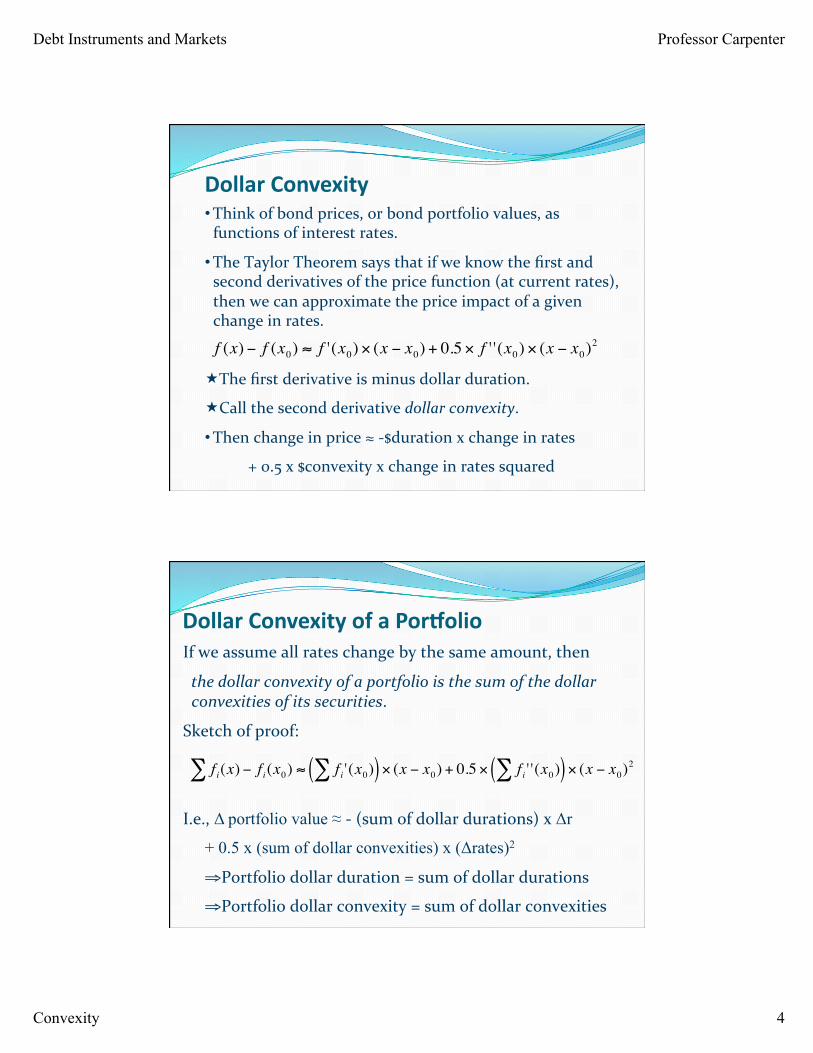

DollarConvexity• Thinkofbondprices,orbondportfoliovalues,asfunctionsofinterestrates.

• TheTaylorTheoremsaysthatifweknowthefirstandsecondderivativesofthepricefunction(atcurrentrates),thenwecanapproximatethepriceimpactofagivenchangeinrates.

Thefirstderivativeisminusdollarduration.

Callthesecondderivativedollarconvexity.• Thenchangeinprice≈‐$durationxchangeinrates +0.5x$convexityxchangeinratessquared

€

f (x) − f (x0) ≈ f '(x0) × (x − x0) + 0.5 × f ' '(x0) × (x − x0)2

DollarConvexityofaPorBolioIfweassumeallrateschangebythesameamount,then

thedollarconvexityofaportfolioisthesumofthedollarconvexitiesofitssecurities.

Sketchofproof:

I.e.,Δ portfolio value ≈ ‐(sumofdollardurations)xΔr

+ 0.5 x (sum of dollar convexities) x (Δrates)2

⇒ Portfoliodollarduration=sumofdollardurations

⇒ Portfoliodollarconvexity=sumofdollarconvexities

€

f i(x) − f i(x0)∑ ≈ f i '(x0)∑( ) × (x − x0) + 0.5 × f i ' '(x0)∑( ) × (x − x0)2

Debt Instruments and Markets Professor Carpenter

Convexity 5

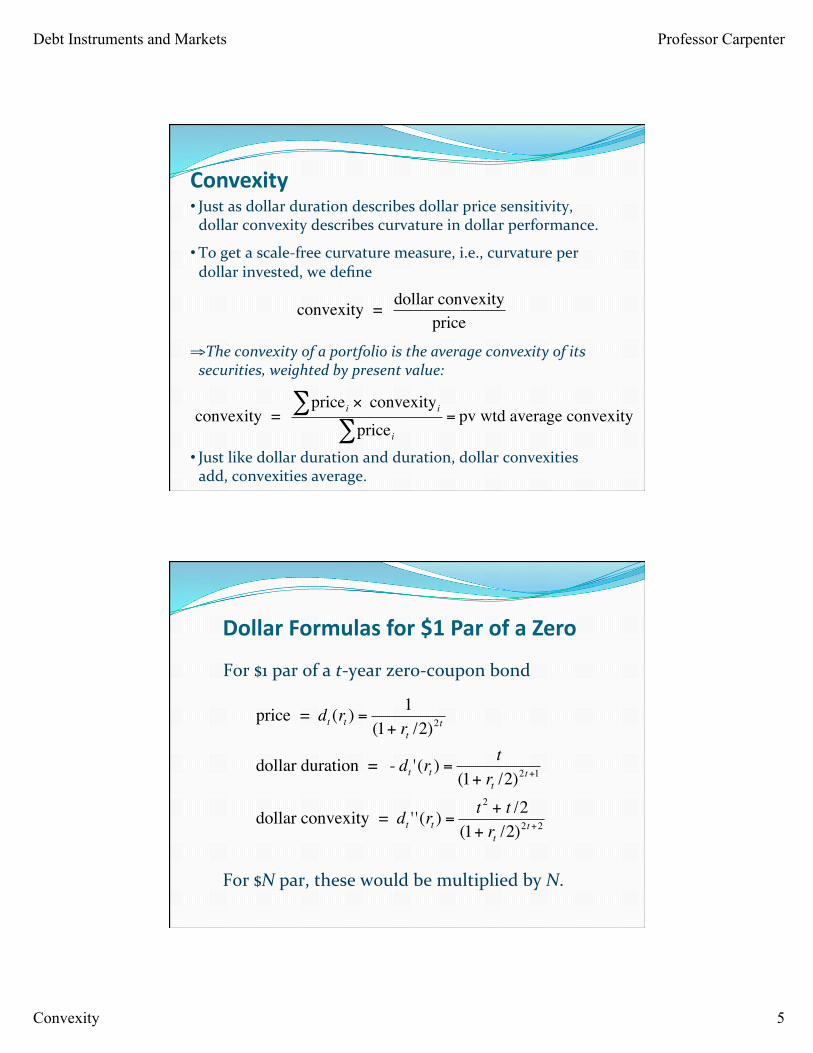

Convexity• Justasdollardurationdescribesdollarpricesensitivity,dollarconvexitydescribescurvatureindollarperformance.

• Togetascale‐freecurvaturemeasure,i.e.,curvatureperdollarinvested,wedefine

⇒ Theconvexityofaportfolioistheaverageconvexityofitssecurities,weightedbypresentvalue:

• Justlikedollardurationandduration,dollarconvexitiesadd,convexitiesaverage.

€

convexity = dollar convexityprice

€

convexity = pricei∑ × convexityi

pricei∑= pv wtd average convexity

DollarFormulasfor$1ParofaZero

For$1parofat‐yearzero‐couponbond

€

price = dt (rt ) =1

(1+ rt /2)2t

dollar duration = - dt '(rt ) =t

(1+ rt /2)2t+1

dollar convexity = dt ' '(rt ) =t 2 + t /2

(1+ rt /2)2t+2

For$Npar,thesewouldbemultipliedbyN.

Debt Instruments and Markets Professor Carpenter

Convexity 6

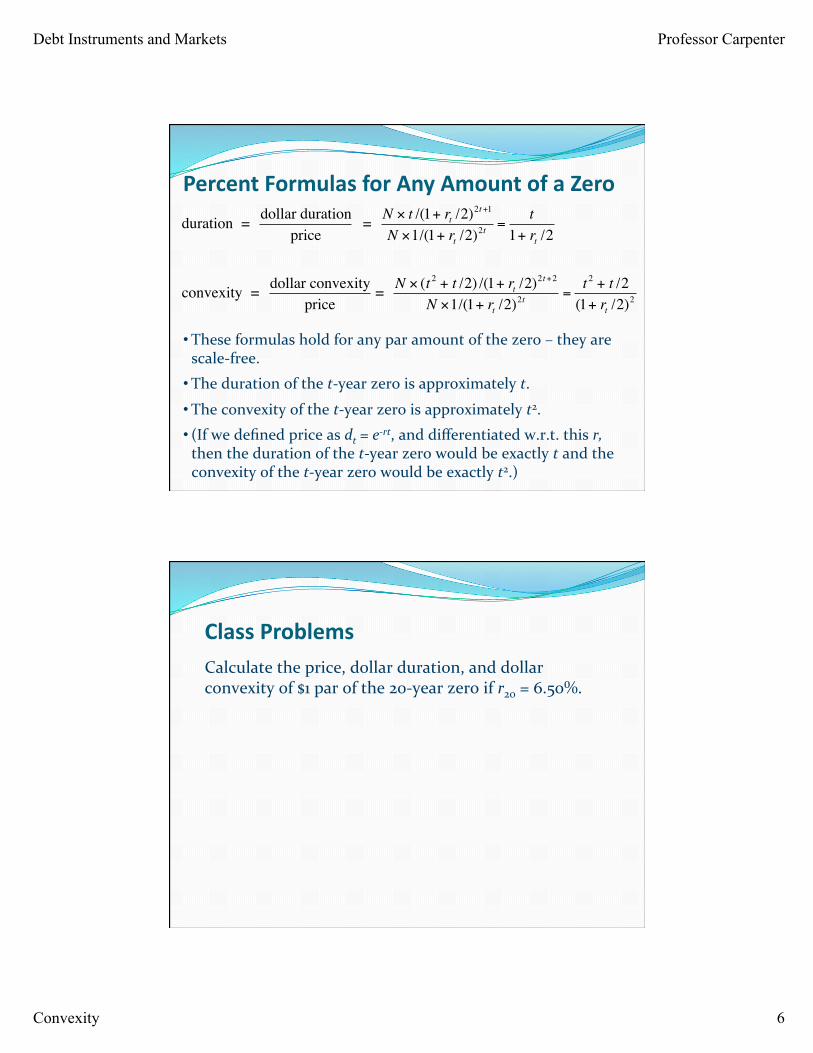

PercentFormulasforAnyAmountofaZero

€

duration = dollar durationprice

= N × t /(1+ rt /2)2t+1

N ×1/(1+ rt /2)2t =t

1+ rt /2

convexity = dollar convexityprice

= N × (t 2 + t /2) /(1+ rt /2)2t+2

N ×1/(1+ rt /2)2t =t 2 + t /2

(1+ rt /2)2

• Theseformulasholdforanyparamountofthezero–theyarescale‐free.

• Thedurationofthet‐yearzeroisapproximatelyt.

• Theconvexityofthet‐yearzeroisapproximatelyt2.

• (Ifwedefinedpriceasdt=e‐rt,anddifferentiatedw.r.t.thisr,thenthedurationofthet‐yearzerowouldbeexactlytandtheconvexityofthet‐yearzerowouldbeexactlyt2.)

ClassProblemsCalculatetheprice,dollarduration,anddollarconvexityof$1parofthe20‐yearzeroifr20=6.50%.

Debt Instruments and Markets Professor Carpenter

Convexity 7

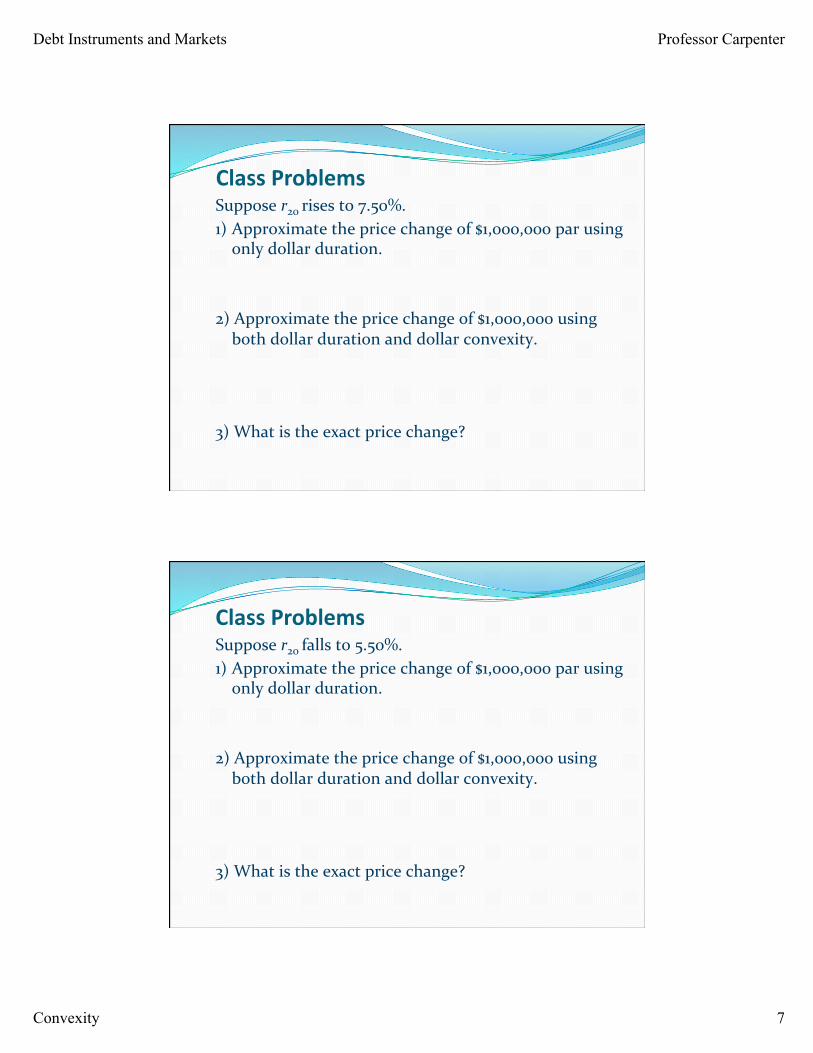

ClassProblemsSupposer20risesto7.50%.1) Approximatethepricechangeof$1,000,000parusingonlydollarduration.

2)Approximatethepricechangeof$1,000,000usingbothdollardurationanddollarconvexity.

3)Whatistheexactpricechange?

ClassProblemsSupposer20fallsto5.50%.1) Approximatethepricechangeof$1,000,000parusingonlydollarduration.

2)Approximatethepricechangeof$1,000,000usingbothdollardurationanddollarconvexity.

3)Whatistheexactpricechange?

Debt Instruments and Markets Professor Carpenter

Convexity 8

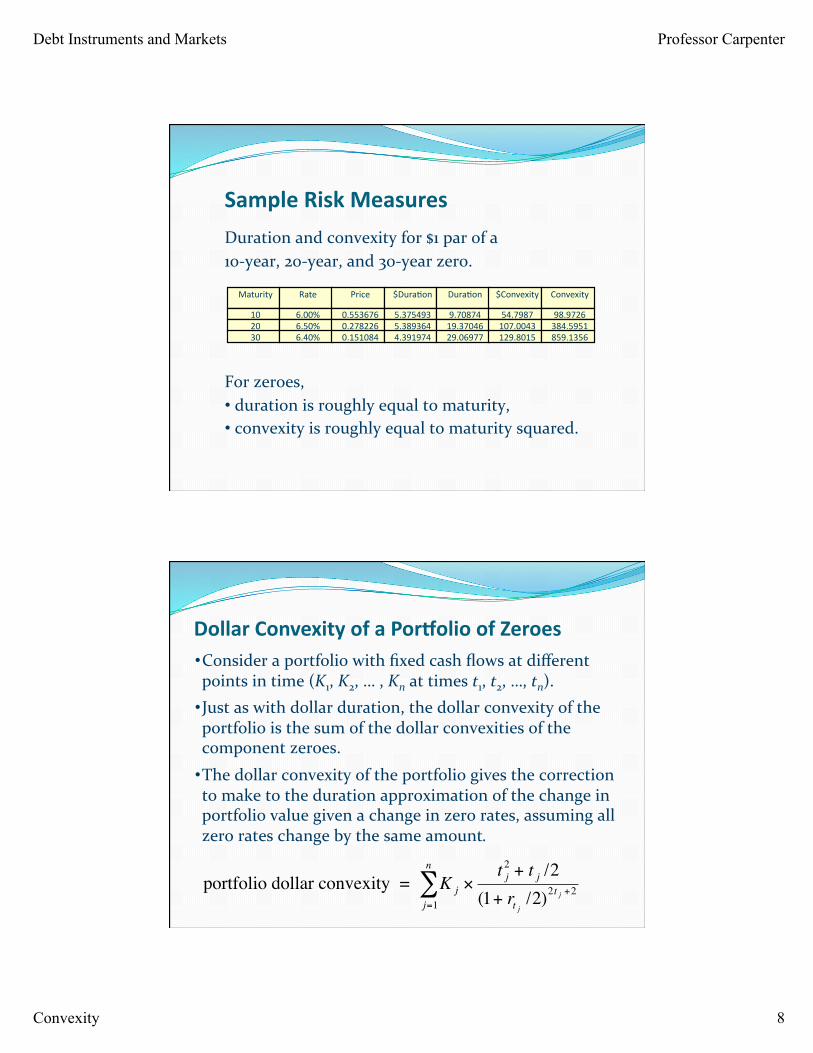

SampleRiskMeasures

Maturity Rate Price $Dura/on Dura/on $Convexity Convexity

10 6.00% 0.553676 5.375493 9.70874 54.7987 98.972620 6.50% 0.278226 5.389364 19.37046 107.0043 384.595130 6.40% 0.151084 4.391974 29.06977 129.8015 859.1356

Durationandconvexityfor$1parofa10‐year,20‐year,and30‐yearzero.

Forzeroes,• durationisroughlyequaltomaturity,• convexityisroughlyequaltomaturitysquared.

DollarConvexityofaPorBolioofZeroes• Consideraportfoliowithfixedcashflowsatdifferentpointsintime(K1,K2,…,Knattimest1,t2,…,tn).• Justaswithdollarduration,thedollarconvexityoftheportfolioisthesumofthedollarconvexitiesofthecomponentzeroes.

• Thedollarconvexityoftheportfoliogivesthecorrectiontomaketothedurationapproximationofthechangeinportfoliovaluegivenachangeinzerorates,assumingallzerorateschangebythesameamount.

€

portfolio dollar convexity = K jj=1

n

∑ ×t j

2 + t j /2(1+ rt j /2)2t j +2

Debt Instruments and Markets Professor Carpenter

Convexity 9

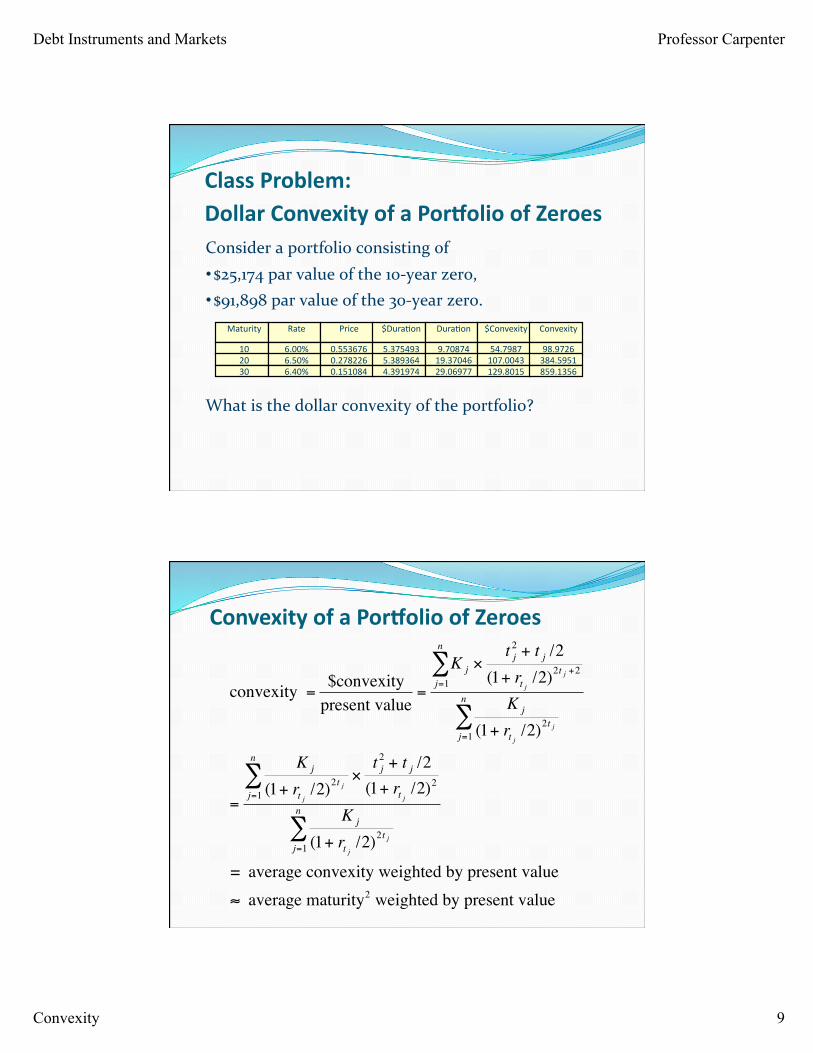

ClassProblem:DollarConvexityofaPorBolioofZeroesConsideraportfolioconsistingof• $25,174parvalueofthe10‐yearzero,• $91,898parvalueofthe30‐yearzero.

Whatisthedollarconvexityoftheportfolio?

Maturity Rate Price $Dura/on Dura/on $Convexity Convexity

10 6.00% 0.553676 5.375493 9.70874 54.7987 98.972620 6.50% 0.278226 5.389364 19.37046 107.0043 384.595130 6.40% 0.151084 4.391974 29.06977 129.8015 859.1356

ConvexityofaPorBolioofZeroes

€

convexity =$convexity

present value=

K jj=1

n

∑ ×t j

2 + t j /2(1+ rt j /2)2t j +2

K j

(1+ rt j /2)2t jj=1

n

∑

=

K j

(1+ rt j /2)2t j×t j

2 + t j /2(1+ rt j /2)2

j=1

n

∑

K j

(1+ rt j /2)2t jj=1

n

∑

= average convexity weighted by present value≈ average maturity2 weighted by present value

Debt Instruments and Markets Professor Carpenter

Convexity 10

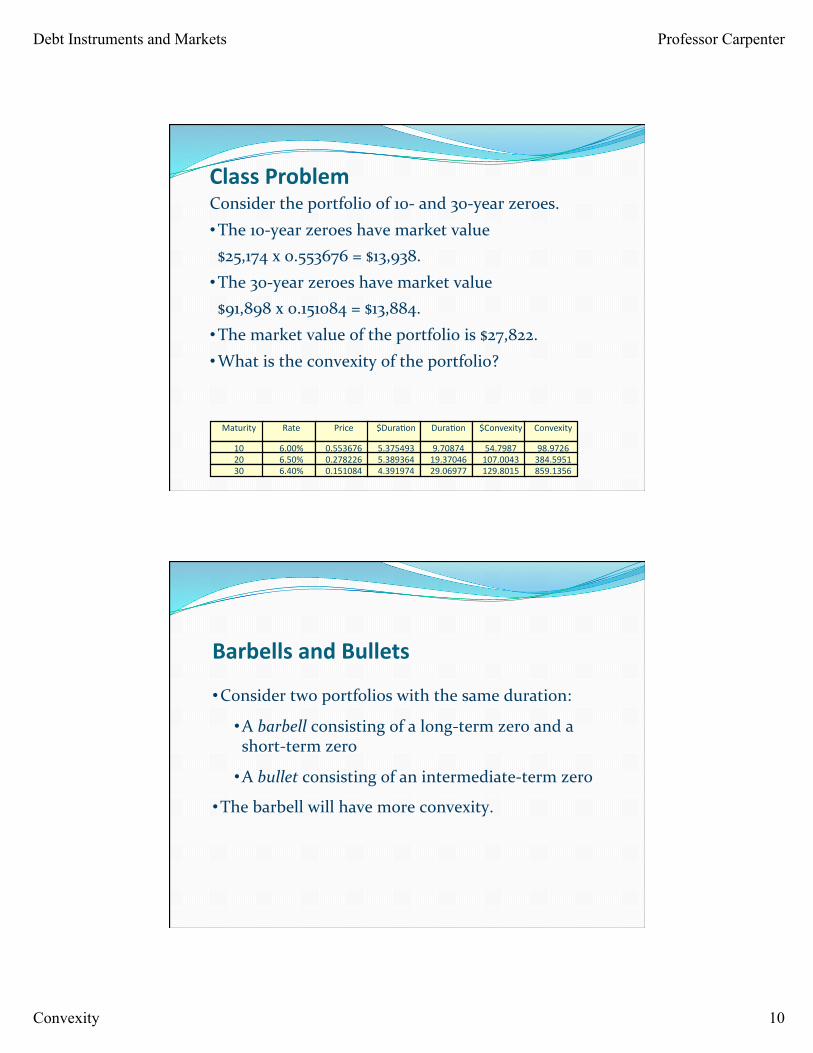

ClassProblemConsidertheportfolioof10‐and30‐yearzeroes.• The10‐yearzeroeshavemarketvalue$25,174x0.553676=$13,938.• The30‐yearzeroeshavemarketvalue$91,898x0.151084=$13,884.• Themarketvalueoftheportfoliois$27,822.• Whatistheconvexityoftheportfolio?

Maturity Rate Price $Dura/on Dura/on $Convexity Convexity

10 6.00% 0.553676 5.375493 9.70874 54.7987 98.972620 6.50% 0.278226 5.389364 19.37046 107.0043 384.595130 6.40% 0.151084 4.391974 29.06977 129.8015 859.1356

BarbellsandBullets

• Considertwoportfolioswiththesameduration:

• Abarbellconsistingofalong‐termzeroandashort‐termzero

• Abulletconsistingofanintermediate‐termzero

• Thebarbellwillhavemoreconvexity.

Debt Instruments and Markets Professor Carpenter

Convexity 11

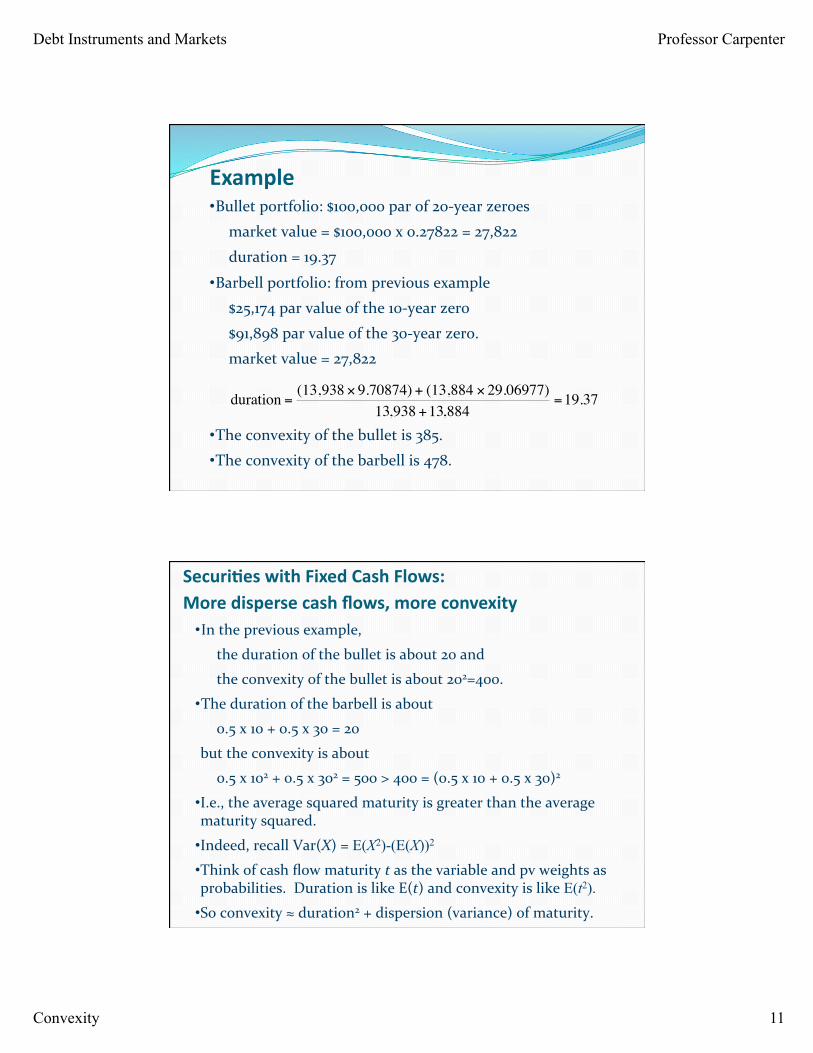

• Bulletportfolio:$100,000parof20‐yearzeroesmarketvalue=$100,000x0.27822=27,822

duration=19.37

• Barbellportfolio:frompreviousexample

$25,174parvalueofthe10‐yearzero

$91,898parvalueofthe30‐yearzero.

marketvalue=27,822

• Theconvexityofthebulletis385.• Theconvexityofthebarbellis478.

€

duration =(13,938 × 9.70874) + (13,884 × 29.06977)

13,938 +13,884=19.37

Example

• Inthepreviousexample,

thedurationofthebulletisabout20and

theconvexityofthebulletisabout202=400.

• Thedurationofthebarbellisabout0.5x10+0.5x30=20

buttheconvexityisabout

0.5x102+0.5x302=500>400=(0.5x10+0.5x30)2

• I.e.,theaveragesquaredmaturityisgreaterthantheaveragematuritysquared.

• Indeed,recallVar(X)=E(X2)-(E(X))2

• Thinkofcashflowmaturitytasthevariableandpvweightsasprobabilities.DurationislikeE(t)andconvexityislikeE(t2). • Soconvexity≈duration2+dispersion(variance)ofmaturity.

Securi:eswithFixedCashFlows:Moredispersecashflows,moreconvexity

Debt Instruments and Markets Professor Carpenter

Convexity 12

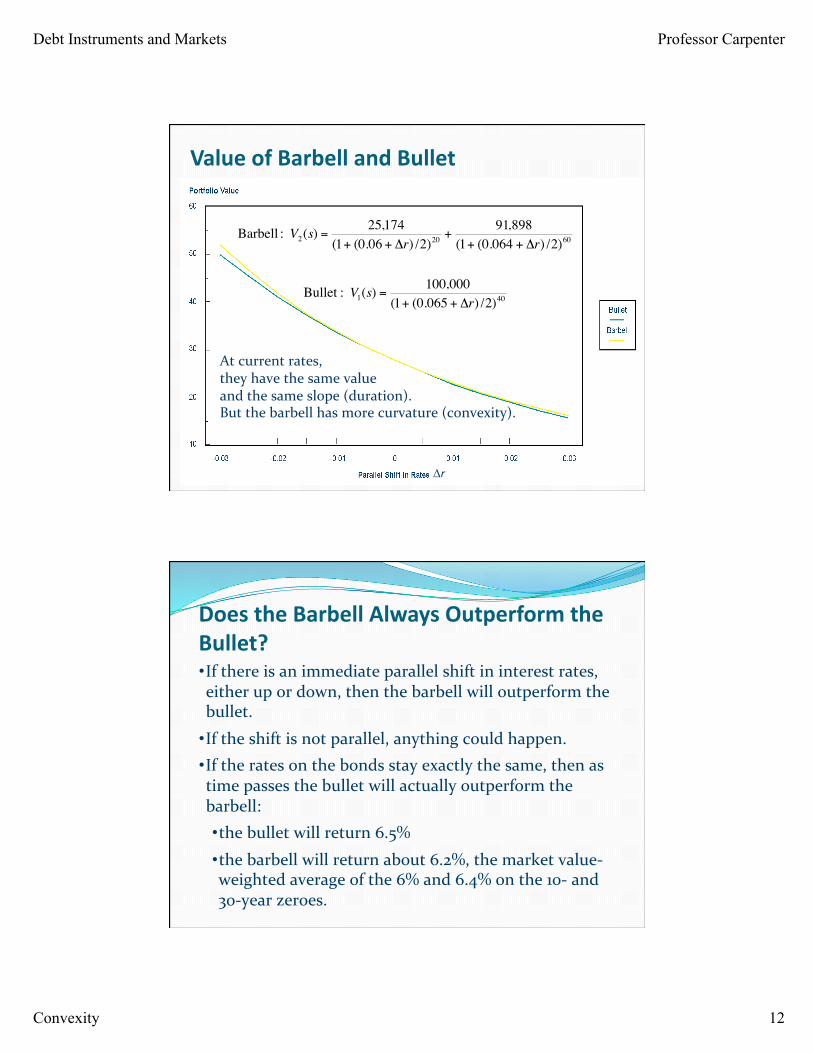

ValueofBarbellandBullet

€

Barbell : V2(s) =25,174

(1+ (0.06 + Δr) /2)20 +91,898

(1+ (0.064 + Δr) /2)60

Bullet : V1(s) =100,000

(1+ (0.065 + Δr) /2)40

Atcurrentrates,theyhavethesamevalueandthesameslope(duration).Butthebarbellhasmorecurvature(convexity).

Δr

DoestheBarbellAlwaysOutperformtheBullet?• Ifthereisanimmediateparallelshiftininterestrates,eitherupordown,thenthebarbellwilloutperformthebullet.

• Iftheshiftisnotparallel,anythingcouldhappen.• Iftheratesonthebondsstayexactlythesame,thenastimepassesthebulletwillactuallyoutperformthebarbell:• thebulletwillreturn6.5%

• thebarbellwillreturnabout6.2%,themarketvalue‐weightedaverageofthe6%and6.4%onthe10‐and30‐yearzeroes.

Debt Instruments and Markets Professor Carpenter

Convexity 13

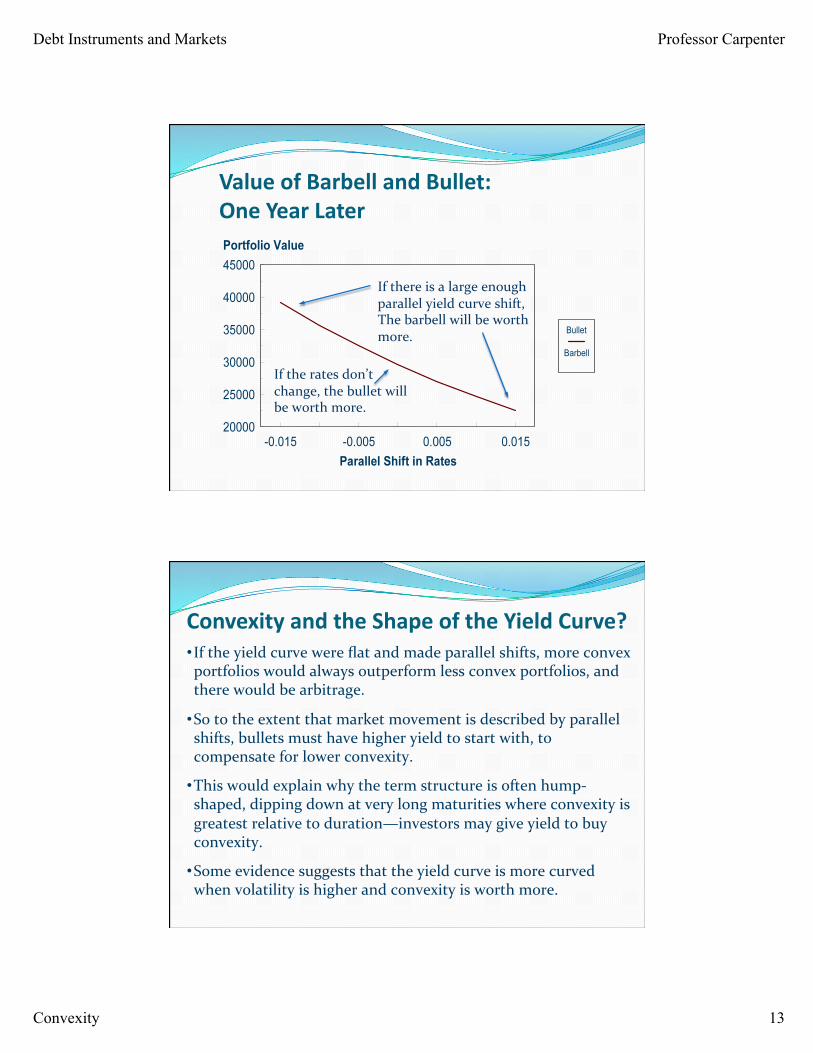

ValueofBarbellandBullet:OneYearLater

Iftheratesdon’tchange,thebulletwillbeworthmore.

Ifthereisalargeenoughparallelyieldcurveshift,Thebarbellwillbeworthmore.

ConvexityandtheShapeoftheYieldCurve?• Iftheyieldcurvewereflatandmadeparallelshifts,moreconvexportfolioswouldalwaysoutperformlessconvexportfolios,andtherewouldbearbitrage.

• Sototheextentthatmarketmovementisdescribedbyparallelshifts,bulletsmusthavehigheryieldtostartwith,tocompensateforlowerconvexity.

• Thiswouldexplainwhythetermstructureisoftenhump‐shaped,dippingdownatverylongmaturitieswhereconvexityisgreatestrelativetoduration—investorsmaygiveyieldtobuyconvexity.

• Someevidencesuggeststhattheyieldcurveismorecurvedwhenvolatilityishigherandconvexityisworthmore.