Embed Size (px)

Citation preview

Corporate social responsibilitydisclosure and its relation on

institutional ownershipEvidence from public listed companies

in Malaysia

Mustaruddin SalehDepartment of Management, Faculty of Economics, Tanjungpura University,

Pontianak, Indonesia, and

Norhayah Zulkifli and Rusnah MuhamadFaculty of Business and Accountancy, University of Malaya,

Kuala Lumpur, Malaysia

Abstract

Purpose – The aim of this paper is to explore corporate social responsibility (CSR) disclosure and itsrelation to institutional ownership (IO) of Malaysian public listed companies (PLCs).

Design/methodology/approach – Testing of hypotheses have been conducted by applyingmultivariate regression techniques utilizing longitudinal data analysis of companies’ annual reports.Two well-established models, the fixed effects model and random effects model are conducted inthis paper.

Findings – Results which confirmed earlier estimations indicated that there are positive andsignificant relationships between CSR disclosure (CSRD) and IO. This result suggests that MalaysianPLCs are able to attract and maintain their institutional investors while they engage in social activities.

Practical implications – Companies should be encouraged to be involved in CSR activities as one oftheir strategies in attracting investment as well as to improve their reputation and image.

Originality/value – Most studies on CSRD in Malaysia pertain to the analysis of such reporting andmotivations of managers towards CSRD. This paper conducts a comprehensive empirical research onthe relationship between CSRD and IO in Malaysian PLCs.

Keywords Corporate social responsibility, Disclosure, Public ownership, Malaysia, Stock exchanges

Paper type Research paper

IntroductionThe current globalization trend and growing demand from stakeholders towardcompanies to adopt corporate social responsibility (CSR) practices encourages theinvolvement of companies in CSR practices (Chapple andMoon, 2005). CSR has emergedas an important subject in company’s activities (Vilanova et al., 2009). CSR is a generalstatement indicating a company’s obligation to utilize its economic resources in itsbusiness activities to provide and contribute to its internal and external stakeholders(Kok et al., 2001).

The growth in shares held by institutional investors has increased considerably.For instance, institutional investors control close to 60 percent of outstanding sharesof common stock in the USA (Hayashi, 2003). In the Malaysian capital market, there are

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/0268-6902.htm

Corporate socialresponsibility

disclosure

591

Received 17 November 2009Revised 22 January 2010

Accepted 8 February 2010

Managerial Auditing JournalVol. 25 No. 6, 2010

pp. 591-613q Emerald Group Publishing Limited

0268-6902DOI 10.1108/02686901011054881

three major categories of institutional investors, namely, pension funds, mutual fundsand life insurance companies, which managed assets totalling around US$114 billionor 96.4 percent of gross domestic product at the end of 2004 (Ghosh, 2006). Currently,a total of 51.03 percent of shares in the top ten highest market capitalizations ofcompanies listed on Bursa Malaysia are held by institutional investors.

Institutional investors in Malaysia are dominated by several large institutions, suchas the Employees Provident Fund (EPF), Lembaga Tabung Haji (formerly known asPilgrimage Management and Fund Board), and Permodalan Nasional Berhad(Malaysia’s biggest fund management agency), and have significant influence incorporate governance. Because of themagnitude of the assets controlled by institutionalinvestors, it is a challenge for public listed companies (PLCs) to attract these investorswho are interested in looking for new investment opportunities in Malaysian PLCs thathave good CSR practices. For example, EPF, being the largest institutional investor inMalaysia, has invested in about 19.7 percent of the total assets (US$70 billion) of theequity market (Ghosh, 2006). In order to find out whether CSR practices can be used toattract institutional investors in Malaysian PLCs, an empirical assessment of therelationship between CSR and institutional ownership (IO) is crucial.

In the academic literature, it is found that although the number of studies on CSR ishigh, an empirical examination on the relationship between CSR and IO in theMalaysiancontext is limited. The lack of empirical studies on this issue could be one of the factorsexplaining why Malaysian PLCs are less concerned or involved in promoting their CSRactivities to various stakeholder groups (Bursa Malaysia, 2007; Williams and Pei, 1999).Hence, by using CSR disclosure (CSRD) as a proxy for themeasurement of CSR activitieswhich are published in the companies’ annual reports, the study provides a contributionto examinewhether there is any relationship between CSRD and IO forMalaysian PLCs.

Literature reviewCSR practices in MalaysiaThe involvement of the government and the Security Commission to promote CSRbenefits will slowly increase the commitment to CSR in Malaysian companies. Somecompanies are actively involved in CSR practices, especially in community involvement.Prathaban (2005) recorded that 65 companies registered on Bursa Malaysia contributedRM82.1 million to various charitable community programs. The telecommunicationsector contributed RM19.6 million (23.87 percent of total donation), which was thehighest amount. The banking and financial services sector was second highest withRM17.1 million (20.83 percent of total donation) followed by construction and propertyrelated companies, which donated RM10.9million (13.27 percent of total donations). Thefourth highest were government-linked companies that gave a total of RM9.6 million(11.69 percent of total donations).

The prior studies conducted by Gardiner et al. (2003) and Seifert et al. (2003) statedthat the size of a business is an important variable in CSR, and acts as a barometer as towhy a company engages in CSR activities. Gardiner et al. (2003) conclude that CSR willonly appear noticeably different if the CSR concept is fully integrated with the principlesand practices of a company and when its progress is monitored regularly. However, thepercentage of CSR contributions for Malaysian companies is only 0.31 percent of theirincome. This is still low when compared to certain European Union countries, whichcontribute at least 1 percent of the profit to the community (Prathaban, 2005).

MAJ25,6

592

Zulkifli andAmran (2006) observed that CSR activity trends inMalaysian companiesare usually carried out in fields similar to their business activities. For example, MaxisCorporation promotes social development involving advances in informationtechnology, bringing about direct advantages to communities. Maxis focuses oneducation, adolescents and information and communication technology under theMaxisBridging Communities (MBC) program. TheMBC core is the Cyber-kid Camps, which isa smart partnership program between Maxis and the government. The TelekomMalaysia group is another large donor that is serious about its social responsibility.It helps provide the digital bridge between rural communities and urban areas, andmoves the nation into the digital era, thereby helping place Malaysia on the world map.

PuncakNiaga is the biggest water treatment company inMalaysia and it has workedhard to introduce and promote public awareness regarding the conservation andprotection of the environment. The Puncak Niaga educational program teaches theyounger generation about protecting and conserving the environment. The Public Bankstrongly believes thatmeeting its CSRwill increase its reputation andbranding, and thatthis is important for the industry services. It also reduces the investment risk andimproves the long term sustainability of the Public Bank Group. In carrying out its CSR,the group focuses on healthcare, education, professional development, charity andconservation of the environment.

The trend of the Malaysian companies shows that they are increasingly becominginvolved in CSR activities from different levels of CSR activities among companies(Zulkifli and Amran, 2006). Ethnicity and religion are influencing factors for CSRactivities in Malaysian companies. Further, Zulkifli and Amran concluded that CSRactivities in Malaysia are seasonal. For instance, many companies spread theirmagnanimity by distributing contributions to the old and poor communities as well asorphans duringAidilfitri,Deepavali, and Chinese NewYear celebrations. Tay Kay Luan,who is the director of ACCA, Association of Southeast Asian Nations, and Australia,states thatmost local companies have anarrowview of the definition of CSR (Tam, 2007).From the viewpoint of the Malaysian companies and leaders of the government, CSR isrestricted to doing of good for the society through contributions, philanthropy, and thedevelopment of sports, or participation in good deeds. Therefore, CSR activities tend tofocus more on programs that have a direct impact on the company’s performance.

The CSR 2007 Status Report revealed poor CSR involvement by PLCs in Malaysia.In general, the survey showed a lack of knowledge and awareness of CSR byMalaysianPLCs. This indicates the need to seriously improve efforts in CSRD and achieve a fullerunderstanding of the concept of CSR. It shows that the majority of companies fell farbehind global best CSR practices and there is a need to improve the level of disclosureand CSR practices.

CSRD research in MalaysiaIn this study, CSRD is defined as the CSR activities communicated to stakeholders via acompany’s annual reports (MohdGhazali, 2007;NikAhmad et al., 2003; CheZuriana et al.,2003; Robert, 1992; Kin, 1990). Hence, CSRD is considered to represent all of CSRactivities which companies disclose in their annual reports.

Earlier studies in this field can be categorized in two different forms. Several studiesconsidered the extent of CSRD (e.g. Abdul Hamid, 2004; Thompson and Zakaria, 2004;NikAhmad et al., 2003; Che Zuriana et al., 2003; Kin, 1990), while other studies examined

Corporate socialresponsibility

disclosure

593

and recognized the driving factors behind the disclosure of CSR activities (Amran andDevi, 2007; Rashid and Ibrahim, 2002; Teoh and Thong, 1984).

For example, Kin (1990) used the Annual Report of 100 registered Malaysiancompanies, and classified five themes. They reported that only 66 companies disclosedinformation on products and services, 31 on employee relations, 22 companies oncommunity involvement and only one on the environment. Since then, there has been noother CSRD research published in Malaysia until 2002, when a research was publishedby Che Zuriana et al. (2003). They used 100 Malaysian PLCs for the period of 1995-1999.They noticed that less than 30 percent of the companies disclosed informationconcerning CSR. Their study also showed that most disclosure concerned humanresources information. Several companies disclosed in both narrative and quantitativepatterns.

Thompson and Zakaria (2004) used content analysis of CSRD of theMalaysian PLCs.They found that 81.3 percent of the 257 Malaysian PLCs made social disclosure. Theyalso found that most companies made disclosures on human resources (40 percent),product and consumer (24 percent), community involvement (22 percent), and theenvironment (16 percent). Abdul Hamid (2004) investigated CSRD practices in thebanking and finance sector forMalaysian PLCs. He used content analysis to explore fourthemes of social disclosure and concluded that product theme attracted the highestdisclosure. The second highest disclosure related to human resources, followed bycommunity and the environment.

The above studies indicate that the CSRD expansion inMalaysia has a clear future asthe number of companies involved in CSRD is growing. Prior studies on CSRDdevelopment in Malaysia indicate that the condition of CSR practices and disclosure arein the emerging stage. Amran (2006) found that Malaysian companies are involved inCSRD because of pressure from the government. The influence on foreign businesspartners was also seen as a contributory factor for engaging in CSRD. Although, somepressure exists, the involvement of CSR forMalaysian PLCs has still not been translatedinto a higher level of social practice and disclosure (Williams and Pei, 1999). Thus, it isnecessary to find what other factors cause the low level of CSR practice and disclosure.A few possible reasons why CSRD inMalaysia is still in its growth stage are consideredbyTeoh andThong (1984), namely, the lack of legislation on CSRD and the perception ofcompanies that they will not receive any benefit from the investor or the community.

As an observation, past CSRD studies in Malaysia were limited to exploring thecontent of CSR activities in companies’ annual reports and revealing the motivation ofmanagers who were engaged in them. Although stakeholder pressure companies to bemore actively involved in CSR activity, the additional number of companies involved inCSRD still does not provide satisfaction to the stakeholders (Williams and Pei, 1999).Earlier studies found that CSRD activities form only a part of the regular report andconsist largely of self praise (Nik Ahmad et al., 2003). However, studies concerning theresponse from the institutional investor when companies engage in CSR are limited.

Empirical studies of the relationship between CSR and IOThere are numerous studies on the relationship between corporate social performance[1]and IO in developed markets (Mahoney and Roberts, 2007; Cox et al., 2004; Johnsonand Greening, 1999; Graves and Waddock, 1994). Previous studies found the existenceof a positive and neutral relationship between CSR and IO. Teoh and Shiu (1990) observe

MAJ25,6

594

the IO attitude towards CSR and the relevant information. They reveal that IO does notusually change decisions concerning investment based on a companies’ disclosurestatement about CSR activities in their conventional financial information, such asannual reports. But, IO accepts CSR information in their account, if it is tuned to specificissues, namely product development and fair business practices.

Graves and Waddock (1994) used a single value of Kinder, Domini and Lydenberg(KDL) index for the measurement of eight characteristics of CSR, developed by KDL &Co., Inc., to explore the relationship between CSR and IO. The results show that there is apositive significant relationship between CSR and numbers of IO, concluding thatinvolvement in CSR activities do not give a negative response to institutional investors.Cox et al. (2004) investigated the pattern of institutional share holding in the UK and itsrelationship with socially responsible behaviour of companies. They found that socialperformance positively related with the long-run institutional investment. Theirconclusion states that institutional investors will choose to place their investments incompanies that have good social achievement and avoid investing in companies thathave poor social performance.

Mahoney and Roberts (2007) examines the impact of CSR on financial performanceand institutional investors, using four years panel data for a sample of Canadiancompanies. These companies exhibit no significant impact of companies’ compositesocial measures on the number of institutions investing in a companies’ stock. However,they found a significant impact of companies’ social ratings regarding theirinternational activities and product quality towards the number of IO.

The discussion of the theoretical and empirical analysis of the relationship betweenCSR and IO in the preceding section proves that the theoretical and empirical relationbetween CSR and IO exists. It can be concluded that most studies in developed marketshave a positive significant relationship between CSR and IO. Hence, this study aims tocontribute to literature in examining the relationship between CSR and IO forMalaysianPLCs from the emerging market setting. IO as dependent variable is presented bynumber and percentage of shares owned by institutional investors, whilst CSRD asindependent variable represents CSR activities of PLCs in Malaysia.

Research methodologySample size and dataThe initial sample in this study consists of the 200 largest companies, which are takenout of 499 companies listed on the main board of Bursa Malaysia during the period2000-2005. The selection is based on their highest market capitalization ranking. Thetime span is selected for two reasons: first, this period is the recovery period from thefinancial crisis that hit the Asian countries particularly the Malaysian capital market(Ariff and AbuBakar, 1999). Hence, post-financial crisis companies can focus on theirinvolvement in CSR activities because they have more resources to contribute theircommunities and other stakeholder. During this period, companies also started toaddress demand of stakeholders which concern with CSR activities (Nik Ahmad andAbdul Rahim, 2003). Second, this period indicates that the awareness level of managerstowards CSRhas just appeared (AbdulHamid, 2004) and therefore, it is asserted that thisis the period of companies’ involvements in CSRD (Thompson and Zakaria, 2004; Rashidand Ibrahim, 2002).

Corporate socialresponsibility

disclosure

595

The companies’ annual reports are chosen in this study as the main data due to thefollowing justifications. First, the annual report is the most important source ofcorporate reporting ( Jenkins and Yakovlena, 2005; Al-Tuwaijri et al., 2004). Second, inMalaysia, annual reports of listed companies are the most accessible source ofinformation, either in hard copy or electronic publications (Sumiani et al., 2007;Christopher et al., 1997; Wiseman, 1982).

Measurement of variablesThis section is a discussion about the measurement of variables. It is divided into twomain variables, namely, dependent variables, which are represented by number andpercentage shares held by institutional investors, and independent variables, which arerepresented by CSRD and dimensions of CSRD and also the set of control variables. Thisstudy utilizes a one-year lag for overall independent variables (for example, year 2001data for dependent variables and year 2000 data for independent variables). Using timelag is in accordance with previous studies (Mahoney and Roberts, 2007) which explorethe relationship between CSR and IO in the future when a company is involved in CSRactivities.

Dependent variables. The primary focus in this study includes the behaviour ofinvestors as represented by IO with respect to CSR activities. In this study, theinvolvement of the Malaysian PLCs towards CSR activities is represented by CSRD.Therefore, IO is represented by the number and percentage shares held by institutionalinvestors and they are used as the dependent variable to examine the relationshipbetween CSRD and IO. Some institutional investors which actively invest in the capitalmarket include public and union pension funds, mutual fund, investment bankers,insurance companies, and employee provident fund.

Independent variables. There are two types of independent variable in this study:the main independent variables and control variables. The main independent variableis CSRD which represent CSR activities and they are divided into four categories ordimensions, namely, employee relations, community involvement, product, andenvironment. Some prior researchers employedmore than four dimensions of CSRD, butas far as the involvement anddisclosure of CSR activities inMalaysia, CSRD is still in theform of general statements and most companies disclose the four categories.

Measurement of CSRD variable. There are two techniques that can be used tomeasure the level of CSRD in the annual reports (Al-Tuwaijri et al., 2004). The firstmeasurement is on the level of the quantity of disclosing such as the number of pages(Gray et al., 1995; Guthrie and Parker, 1990), number of sentences (Hackston and Milne,1996), and number of words (Zeghal and Ahmed, 1990). All these methods have theirlimitations. According to Al-Tuwaijri et al. (2004), the page may possibly include apicture that does not have information on the CSR activities, whereas sentences andwords may possibly ignore a graph or necessary table. The second measurement usesa disclosure scoringmeasurement that comes from content analysis. Thismethod is alsocalled quantitative disclosing (Al-Tuwaijri et al., 2004). This study utilizes both thenumber of sentences of quantity of CSRD and quantitative disclosing. Quantitativedisclosing is assigned to different disclosing items that are based on the perceivedimportance of each item of CSRD dimension, namely, employee relations, communityinvolvement, product, and environment to various users’ group.

MAJ25,6

596

In the Malaysian context, Haniffa and Cooke (2005) and Thompson and Zakaria(2004) in their studies used five categories of content analysis but with different themes.AbdulHamid (2004) used four categories andNikAhmad et al. (2003) identified six typesof CSRD. The number of companies that have reported on the energy theme is very rareand less than 1% (Thompson and Zakaria, 2004; Nik Ahmad et al., 2003). Thus, in thisstudy, energy is combined with the environment theme. Therefore, four categories ofCSRD, namely, employee relations, community involvement, product dimension, andenvironmental dimension are identified in this study. These categories are consistentwith the recent studies (Branco and Rodrigues, 2008; and Abdul Hamid, 2004).

In this study, the value of each item disclosed is measured quantitatively in thatweights are assigned to different disclosing items based on the perceived importance ofevery item to a variety of user groups (Al-Tuwaijri et al., 2004; Hughes et al., 2001). Thereason for the utilization of this technique is because throughout this procedure theresearcher has to re-evaluate the quality of disclosing based on the three criteria ofquantitative disclosing. The disclosing value of each item is assigned into three qualityof classifications of quantitative disclosing:

(1) quantitative disclosure (the greatest weight has an assigned value of 3);

(2) the next highest weight, qualitative specific disclosure (non-quantitativedisclosing but with specific information has an assigned value of 2); and

(3) the lowest weight, qualitative disclosure (the general quantitative disclosinghas an assigned value of 1).

Companies that do not disclose any kind of information for the given categorizes obtain ascore of 0 for the particular dimension.

Total scores value of CSRD is summed from all sub-scores value of dimensions ofCSRD comprises total scores values of employee relation dimension, communityinvolvement dimension, product dimension and environment dimension. Hence, CSRDas independent variable is utilized as proxy to measure CSR activities which aredisclosed in companies’ annual reports. Themethod to scoring is additive of unweightedindexes that is calculated to the sum of the final CSRD score[2]:

CSRDj ¼

Pnjt¼1Xij

nj

where:

CSRDj ¼ CSR disclosure score for jth company.

nj ¼ Total number of items estimated for jth company.

Xij ¼ 3 if ith item is quantitative disclosed, 2 if ith item is non-quantitative butspecific information disclosed, 1 if ith item is common qualitativedisclosed, and 0 if ith item does not disclosed any information.

The modelsTwo well-established models, the fixed effects model and random effects model areconducted in this study. The difference between the fixed and random effects modelsis based on whether the unobserved individual effects that are correlated with the

Corporate socialresponsibility

disclosure

597

regressors, which is the case for the fixed effects, or not in the models, as in the caseof the random effects model. (Greene, 2008; Wagner, 2005) In the fixed effects model, theintercept in the regressionmodel is allowed to differ among individuals in recognition ofthe fact that each individual or cross section unit may have some special characteristicsof its own. In conclusion, the fixed effectsmodel is represented by the following equation:

git ¼ xi;t21bþ vi þ mit ð1Þ

where y is the dependent variable (in this study, it refers to institutional ownershipmeasurements, namely, number of share held by institutional investors (NUMBIO) andpercentage of share held by institutional investors (PERCIO); x represents one-year lagin the independent variables (in this study, it refers to the variables CSRD, dimensions ofCSRD, namely, Employee Relation Disclosure (EMPD), Community InvolvementDisclosure (COMD), Product Disclosure (PROD), Environment Disclosure (ENVD), andall the control variables including Firms’ systematic risk (BETA), leverage (LEV),LogSize (LSIZE), LogSales (LSALES), asset turnover (ATR), and earnings per share(EPS). b is the coefficient of the independent variables; m represents the error term; v isthe unobserved firm effect; i indicates a firm number; and t represents time.

To choosewhich of the twomodels that fixed or random effectsmodel ismore precise,the Hausman test is employed. This test evaluates the significance level betweenestimators, in case, fixed effect or random effect models. The error term (mit) for therandom effects model using equation (1) can be defined as:

mit ¼ ei þ vit ð2Þ

In equation (2), ei is the cross-section error component and nit, combines the cross-sectionand time series error component.

Hypothesis development of CSR on IOThis study attempts to discover evidence of CSR activities which are represented byCSRD in Malaysian PLCs. It can be explained by utilizing the stakeholder theory,because this theory is useful to explain voluntary CSR for two reasons. First, itdistinguishes between the social and stakeholder issues. Clarkson (1995) argued thatmanagers deal with their company stakeholders and not with the public. Second, thestakeholder theory is considered to bemore appropriate to develop a testable hypothesis.

In the context of this study, the stakeholders demand that CSR be a stakeholder issueas in the Malaysian context, CSR is still unregulated (Elijido-Ten, 2004). Hence, thestakeholder theory offers a practical framework to assess CSR by using informationfrom CSRD (Snider et al., 2003).

Malaysian managers of companies have the moral support to engage in CSR anddisclose information about their CSR activities for important interest groups. Recently,external primary stakeholders, such as the government and capital market authorities,have also exerted force, through acts and regulations, for companies to be involved onCSR activities. For example, Bursa Malaysia released a CSR framework for PLCs, andthe 2006 Budget speech of PrimeMinister of Malaysia required all PLCs to disclose theirCSR activities (Bursa Malaysia, 2007). Thus, the stakeholder theory can be used toclarify the CSR practices in Malaysian PLCs (Nik Ahmad et al., 2003). So, it isimportant to know the impact of information concerning CSR on the level of IO as

MAJ25,6

598

empirical evidence, because from the stakeholder theory position, investors could viewcompanies with high social responsibility as being a superior match with theirenvironment, and for this reason the investment risk is lower in the long term(Simerly, 1995).

Empirical studies show a positive and significant relationship between socialperformance and shares held by institutional investors (Graves and Waddock, 1994).Cox et al. (2004) find that CSR is positively related to long-term institutional investment.Findings of a recent study by Mahoney and Roberts (2007) also report a significantrelationship between companies’s CSR and the number of institutions investing in itsshares.

In the case of Malaysia, it is found that companies’ annual reports disclose more CSRwhen shares are owned by government agencies (Mohd Ghazali, 2007). At the sametime, debt monitoring and foreign ownership have a significant impact on corporateperformance (Che Haat et al., 2008). Based on empirical results, it is revealed thatCSRD information has caused market reactions (Epstein and Freedman, 1994). Mostprior studies found that investors require CSRD as information for their investmentdecisions (Mahoney and Roberts, 2007; Epstein and Freedman, 1994). Hence, CSRD isas a proxy to measurement of CSR for the Malaysian PLCs, this leads to the followinghypothesis:

H1. There is a positive relationship between CSRD and IO.

Several institutional investors confirm that they select a company to invest in thatwhichis consistent with their personal values (Sauer, 1997). As socially responsible investorsbecome aware of the companies’ non-responsiveness to social concerns, they can placepressure on those companies to change. Taub (2001) found that more than 76 percent of89 participants in his survey find that institutional investors place more pressure oncompanies to improve business governance.

Good corporate citizenship may create strong loyalty of employee to a company, and,as a result, a responsible company may improvement in employee relations, as well aspresenting an optimum position to attract and maintain good employees. McGuire et al.(1988) revealed that employee loyalty is advantageous for a company as it improvesproductivity, innovation, lowers production cost, thereby increasing profitability.

The empirical research by Cox et al. (2004) found a positive and significant impact ofemployee relations on long-term institutional investors, whereas Mahoney andRoberts (2007) reveal a negative partially significant effect on employee relations and thenumber of IO. Hence, this leads to the hypothesis which is developed as follows:

H2. There is a positive relationship between employee relations dimension and IO.

Kanter (1999) noticed that a vital type of benefit that companies can obtain fromcommunity involvement programmes is that society can be utilized as a learninglaboratory for its innovations. Besides, being attentive to financial performance, productquality, and the environment, institutional investors may also be pondering oncompany’s contributions to local communities and their relationships with women,minorities, and employees (Schwab and Thomas, 1998).

A recent empirical study byMahoney and Roberts (2007) reveal that there is positivebut not significant impact of community involvement on the percentage of sharesownership of institutional investors. However, a study by Cox et al. (2004) found

Corporate socialresponsibility

disclosure

599

a positive partially significant relationship between community involvement activitiesand long-term investors. This leads to the following hypothesis:

H3. There is a positive relationship between community involvement dimensionand IO.

Companies have the incentive and tools to determine the information that prospectivecustomers for their products may find useful. Benston (1997) observes that if investorscannot easily consider the products, it is worth less to them. Consequently, the productshave to sell at a lower price to compete with alternative investments that are moreefficient. On the other hand, investors will not pay compensation for excessiveinformation costs provided by companies.

Empirical testing by Mahoney and Roberts (2007) and Teoh and Shiu (1990) revealthat the product dimension of CSR relates to shares owned by IO. Their conclusionproposes that institutional investors pay special attention to how companies arrangethis CSR dimension. Hence, the following hypothesis is formulated:

H4. There is a positive relationship between product dimension and IO.

According to Turban and Greening (1997), institutional investors notice the long-termbenefits from a socially responsible company through maintaining the quality ofproducts, more attention to the environment, community, and their employees. Spicer(1978) argues that institutional investors assume that low level of social responsible ofcompany and poor in environment performance indicate that investment risk in suchcompanies are high.

The empirical testing byCox et al. (2004) found that the environmental dimension andlong-term investors is positive and significantly related, whereas contrary results byMahoney and Roberts (2007) report a negative significant impact of the environmentaldimension on the number of institutional owners, as well as the percentage ofinstitutional ownership. This leads to the following hypothesis:

H5. There is a positive relationship between environment dimension and IO.

FindingsThis research uses longitudinal disclosure over a seven year period. As a result, duringthis period it is revealed that the participation of companies’ involvement in CSRactivities is increasing both in terms of the amount of disclosure as well as the number ofparticipating companies. However, the growing level of involvement and disclosure ofCSR activities is still limitedwith general information and qualitative statements. Hence,this result suggests that the situation of CSRD inMalaysia is at an emerging periodwithrespect to disclosure of CSR activities.

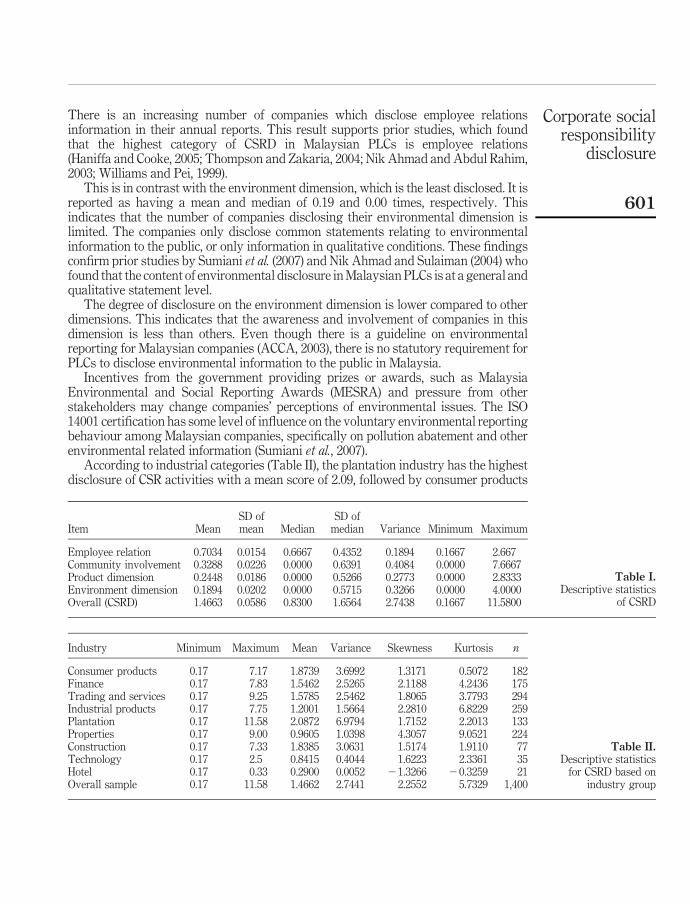

Descriptive statistics of CSRDThis section presents the descriptive statistics employing mean values of each CSRDdimension. The mean value is the most commonly used to measure central tendency.Results for mean values of each CSRD dimension are presented in Table I. Findingsreveal that employee relations are the highest disclosed dimension with a mean value of0.70, median value of 0.67 and standard deviation of 0.43. This indicates that PLCs inMalaysia is more concerned with human resources as compared to other dimensions.

MAJ25,6

600

There is an increasing number of companies which disclose employee relationsinformation in their annual reports. This result supports prior studies, which foundthat the highest category of CSRD in Malaysian PLCs is employee relations(Haniffa and Cooke, 2005; Thompson and Zakaria, 2004; Nik Ahmad and Abdul Rahim,2003; Williams and Pei, 1999).

This is in contrast with the environment dimension, which is the least disclosed. It isreported as having a mean and median of 0.19 and 0.00 times, respectively. Thisindicates that the number of companies disclosing their environmental dimension islimited. The companies only disclose common statements relating to environmentalinformation to the public, or only information in qualitative conditions. These findingsconfirm prior studies by Sumiani et al. (2007) and Nik Ahmad and Sulaiman (2004) whofound that the content of environmental disclosure inMalaysian PLCs is at a general andqualitative statement level.

The degree of disclosure on the environment dimension is lower compared to otherdimensions. This indicates that the awareness and involvement of companies in thisdimension is less than others. Even though there is a guideline on environmentalreporting for Malaysian companies (ACCA, 2003), there is no statutory requirement forPLCs to disclose environmental information to the public in Malaysia.

Incentives from the government providing prizes or awards, such as MalaysiaEnvironmental and Social Reporting Awards (MESRA) and pressure from otherstakeholders may change companies’ perceptions of environmental issues. The ISO14001 certification has some level of influence on the voluntary environmental reportingbehaviour among Malaysian companies, specifically on pollution abatement and otherenvironmental related information (Sumiani et al., 2007).

According to industrial categories (Table II), the plantation industry has the highestdisclosure of CSR activities with a mean score of 2.09, followed by consumer products

Item MeanSD ofmean Median

SD ofmedian Variance Minimum Maximum

Employee relation 0.7034 0.0154 0.6667 0.4352 0.1894 0.1667 2.667Community involvement 0.3288 0.0226 0.0000 0.6391 0.4084 0.0000 7.6667Product dimension 0.2448 0.0186 0.0000 0.5266 0.2773 0.0000 2.8333Environment dimension 0.1894 0.0202 0.0000 0.5715 0.3266 0.0000 4.0000Overall (CSRD) 1.4663 0.0586 0.8300 1.6564 2.7438 0.1667 11.5800

Table I.Descriptive statistics

of CSRD

Industry Minimum Maximum Mean Variance Skewness Kurtosis n

Consumer products 0.17 7.17 1.8739 3.6992 1.3171 0.5072 182Finance 0.17 7.83 1.5462 2.5265 2.1188 4.2436 175Trading and services 0.17 9.25 1.5785 2.5462 1.8065 3.7793 294Industrial products 0.17 7.75 1.2001 1.5664 2.2810 6.8229 259Plantation 0.17 11.58 2.0872 6.9794 1.7152 2.2013 133Properties 0.17 9.00 0.9605 1.0398 4.3057 9.0521 224Construction 0.17 7.33 1.8385 3.0631 1.5174 1.9110 77Technology 0.17 2.5 0.8415 0.4044 1.6223 2.3361 35Hotel 0.17 0.33 0.2900 0.0052 21.3266 20.3259 21Overall sample 0.17 11.58 1.4662 2.7441 2.2552 5.7329 1,400

Table II.Descriptive statisticsfor CSRD based on

industry group

Corporate socialresponsibility

disclosure

601

at 1.87, construction at 1.84, trading and services at 1.58, finance at 1.54, industrialproducts at 1.20, property at 0.96, technology at 0.84, and hotel at 0.29. There aredifferences in the disclosure level for each CSRD dimension between the differentindustries. For example, the plantation and construction industries which have asignificant impact on nature and the environment, disclose more environmentalinformation than other industries.

The tobacco and alcoholic drink industries are associated with highly discerniblesocial problems such as health and crime. These industries must be concerned withdisclosing product and community involvement related activities. By acknowledgingthe stature of their name among the community, individual companiesmake the creationand maintenance of good relationships with local society very important. Hence, somecompanies in this industry such as British American Tobacco (Malaysia) Berhad,Carlsberg Brewery Malaysia Berhad, and Guinness Anchor Berhad are activelyinvolved in disclosing their CSR activities. Furthermore, in anticipation of pressure fromvarious stakeholders such as non-governmental organizations, consumers andgovernmental bodies, these companies also show that they make an importantcontribution to the public and the nation.

Apart from addressing various pressures to observe socially responsible practices,other reasons companies disclose their CSR activities in the companies’ annual reportingmay result from a decoupling strategy for Malaysian companies to follow their businessassociates from overseas, who are already applying CSRD (Thompson and Zakaria,2004). The majority of industries in Malaysia export extensively to developed markets,with the USA as one of the main importers. Although the awareness level of CSR byMalaysian companies is far behind their business partners in these markets, copyingand following their business partners in applying CSR activities has the potential toenhance demand for products from Malaysian companies in the USA and otherdeveloped markets.

Certain Malaysian companies attempt to be superior corporate citizens to obtaincertain contracts from the government (Amran and Devi, 2007). Another reason whyMalaysian companies should be concerned with better CSR practices is to attract moreforeign funds as cost of capital in foreign markets is cheaper than the local market. If acompany has superior CSR practices, it is easier to attract foreign institutional investorssuch as pension funds and SRI, thereby helping companies develop their business fasterand profitably. CSR provides a good differentiation for the company’s image; making iteasier to recruit and retain key employees who play essential roles in sustainingbusiness success (Investor Digests, 2003). Therefore, PLCs in Malaysia need to integrateCSR activities with the company’s business operations. In this regard, the company’sinvolvement in CSR activities is an effort to build business relationships withstakeholders in order to remain sustainable in the long term of providing optimalservices to its stakeholders (Amran et al., 2007).

Based on these facts it can be concluded that the level of CSRD for PLCs inMalaysia isstill limited to general statements. Nevertheless, the number of companies involved inCSRD is growing (Mohd Ghazali, 2007). There is a need to find different ways to supportcompanies in not only awareness level enhancement, but also on how to become activelyinvolved in CSR activities and disclosure. The trends in developed markets suchas North America and Europe show a widespread of empirical testing of CSR

MAJ25,6

602

on institutional ownerships. Hence, the following section discusses the empirical testresults between CSRD and IO in a Malaysian context.

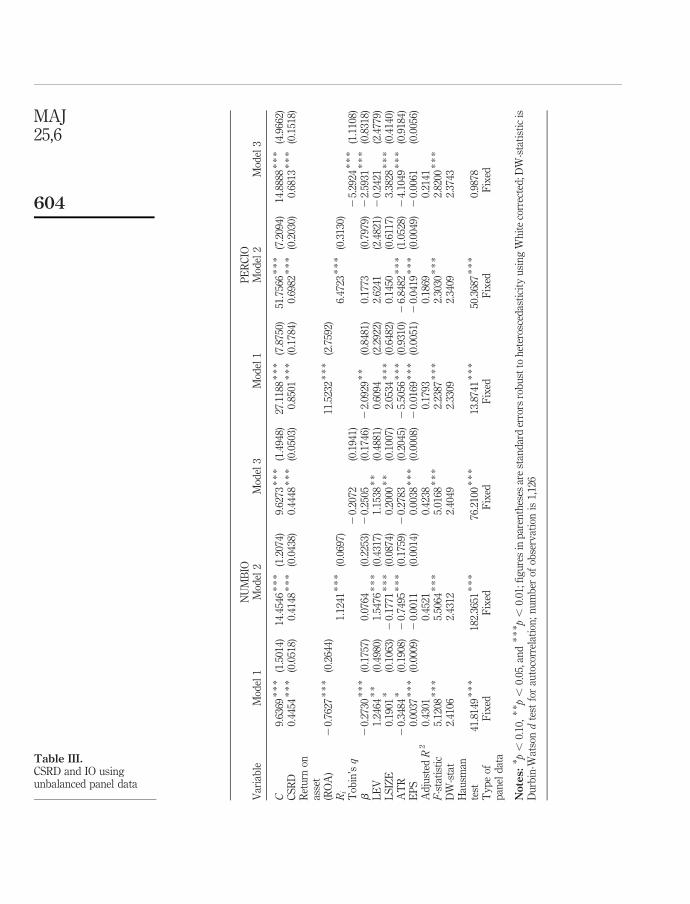

The relationship between CSRD and IOTable III shows the hypothesis testing results between CSRD and IO. There is positiveand significantly related between CSRD and IO. This result supports previous studiesby Mahoney and Roberts (2007), Cox et al. (2004), Johnson and Greening (1999), andGraves and Waddock (1994) which reported a significant positive relationship betweensocial performance and institutional investors. This indicates that institutionalinvestors are interested in how managers handle the social issues of their company.Moreover, these results are also consistent with previous findings (Mahoney andRoberts, 2007; Coffey and Fryxell, 1991; Teoh and Shiu, 1990) which stated institutionalinvestors make CSR a source of important information when considering the decision toretain or release their shares in a given company.

According to the above result, there is a good opportunity to attract institutionalinvestors to invest in PLCs in Malaysia, as institutional investors will select shares ofcompanies that have a higher social achievement. The additional investment criteriathat institutional investors consider, besides being concerned with the financialperformance of their investment as normal investors, also assumes that investments arean expansion of their values and social beliefs in their business environment(Webley et al., 2001; Lewis and Mackenzie, 2000). Thus, if companies want to attractthese investors, managers have considered declaring their CSR activities in annualreports as an effective means of communicating with institutional investors.

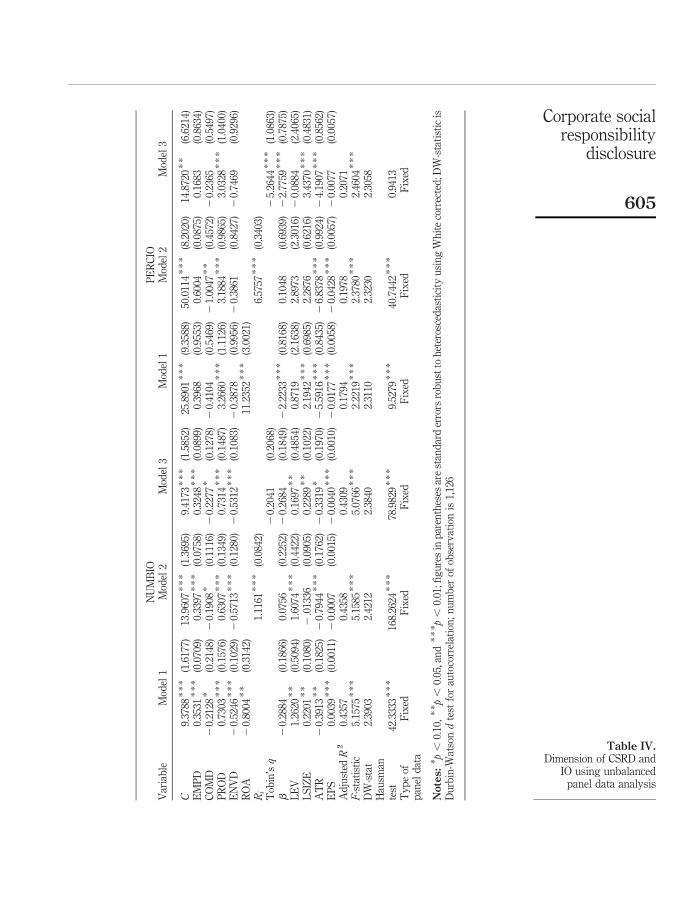

The relationship between dimensions of CSRD and IOTable IV reports results of the relationship between the CSRD dimensions and IO.Overall four dimensions are significantly related to IO. There are two dimensionsnamely employee relation and product, which are positive and significantly related toIO;whereas the other twodimensions namely community involvement and environmentare negative and significantly related to IO. These findings reveal that there are twovariables namely employee relations and product that supportH2 andH4. These resultsare also consistent with the latest study by Cox et al. (2004), which reported thatemployee relations is positive and significantly related to IO and Mahoney and Roberts(2007) who found that there is a positive and significant relationship between productdimension and IO.

These results provide evidence consistent with the conjecture that institutionalinvestors pay attention to the way Malaysian companies manage social issues. Theseresults are also consistent with prior studies (Mahoney and Roberts, 2007; Cox et al.,2004; Graves and Waddock, 1994; Coffey and Fryxell, 1991; Teoh and Shiu, 1990) thatsuggest institutional investors take CSR information into account in decidingwhether tohold their shares in a given company. Hence, managers can conclude that improvingsocially responsible practices will not depress institutional shared ownerships (Gravesand Waddock, 1994). These results indicate that Malaysian institutional investors arenormally concerned with the impact of company decisions. These issues which relate toCSR activitieswill bemore effective if communicated directly to the stakeholders. Hence,managers have to be proactive in accommodating the requirements of institutional

Corporate socialresponsibility

disclosure

603

NUMBIO

PERCIO

Variable

Model1

Model2

Model3

Model1

Model2

Model3

C9.6369

***

(1.5014)

14.4546***

(1.2074)

9.6273

***

(1.4948)

27.1188***

(7.8750)

51.7566***

(7.2094)

14.8888***

(4.9662)

CSRD

0.4454

***

(0.0518)

0.4148

***

(0.0438)

0.4448

***

(0.0503)

0.8501

***

(0.1784)

0.6982

***

(0.2030)

0.6813

***

(0.1518)

Return

onasset

(ROA)

20.7627

***

(0.2644)

11.5232***

(2.7592)

Ri

1.1241

***

(0.0697)

6.4723

***

(0.3130)

Tobin’sq

20.2072

(0.1941)

25.2924

***

(1.1108)

b20.2730

***

(0.1757)

0.0764

(0.2253)

20.2505

(0.1746)

22.0929

**

(0.8481)

0.1773

(0.7979)

22.5931

***

(0.8318)

LEV

1.2464

**

(0.4980)

1.5476

***

(0.4317)

1.1538

**

(0.4881)

0.6094

(2.2922)

2.6241

(2.4821)

20.2421

(2.4779)

LSIZE

0.1901

*(0.1063)

20.1771

***

(0.0874)

0.2000

**

(0.1007)

2.0534

***

(0.6482)

0.1450

(0.6117)

3.3828

***

(0.4140)

ATR

20.3484

*(0.1908)

20.7495

***

(0.1759)

20.2783

(0.2045)

25.5056

***

(0.9310)

26.8482

***

(1.0528)

24.1049

***

(0.9184)

EPS

0.0037

***

(0.0009)

20.0011

(0.0014)

0.0038

***

(0.0008)

20.0169

***

(0.0051)

20.0419

***

(0.0049)

20.0061

(0.0056)

Adjusted

R2

0.4301

0.4521

0.4238

0.1793

0.1869

0.2141

F-statistic

5.1208

***

5.5064

***

5.0168

***

2.2387

***

2.3030

***

2.8200

***

DW-stat

2.4106

2.4312

2.4049

2.3309

2.3409

2.3743

Hausm

antest

41.8149***

182.3651

***

76.2100***

13.8741***

50.3687***

0.9878

Typeof

paneldata

Fixed

Fixed

Fixed

Fixed

Fixed

Fixed

Notes:* p

,0.10,** p

,0.05,and

*** p

,0.01;fi

guresin

parentheses

arestandarderrors

robustto

heteroscedasticity

usingWhitecorrected;D

W-statisticis

Durbin-W

atsondtest

forautocorrelation;number

ofobservationis1,126

Table III.CSRD and IO usingunbalanced panel data

MAJ25,6

604

NUMBIO

PERCIO

Variable

Model1

Model2

Model3

Model1

Model2

Model3

C9.3788

***

(1.6177)

13.9607***

(1.3695)

9.4173

***

(1.5852)

25.8901***

(9.3588)

50.0114***

(8.2020)

14.8720**

(6.6214)

EMPD

0.3531

***

(0.0709)

0.3397

***

(0.0758)

0.3248

***

(0.0899)

0.3968

(0.9553)

0.6004

(0.0875)

0.1683

(0.8634)

COMD

20.2128

*(0.2148)

20.1908

*(0.1116)

20.2277

*(0.1278)

20.4104

(0.5469)

21.0047

**

(0.4572)

20.2365

(0.5497)

PROD

0.7303

***

(0.1576)

0.6307

***

(0.1349)

0.7314

***

(0.1487)

3.2660

***

(1.1126)

3.1884

***

(0.9865)

3.0328

***

(1.0400)

ENVD

20.5246

***

(0.1029)

20.5713

***

(0.1280)

20.5312

***

(0.1083)

20.3878

(0.9956)

20.3861

(0.8427)

20.7469

(0.9296)

ROA

20.8004

**

(0.3142)

11.2352***

(3.0021)

Ri

1.1161

***

(0.0842)

6.5757

***

(0.3403)

Tobin’sq

20.2041

(0.2068)

25.2644

***

(1.0863)

b20.2884

(0.1866)

0.0756

(0.2252)

20.2684

(0.1849)

22.2233

***

(0.8168)

0.1048

(0.6939)

22.7759

***

(0.7875)

LEV

1.2620

**

(0.5094)

1.6074

***

(0.4422)

0.1697

**

(0.4854)

0.8719

(2.1638)

2.8973

(2.3016)

20.0884

(2.4065)

LSIZE

0.2201

**

(0.1080)

2.01336

(0.0905)

0.2289

**

(0.1022)

2.1942

***

(0.6985)

2.2876

(0.6216)

3.4370

***

(0.4831)

ATR

20.3913

**

(0.1825)

20.7944

***

(0.1762)

20.3319

*(0.1970)

25.5916

***

(0.8435)

26.8378

***

(0.9924)

24.1907

***

(0.8562)

EPS

0.0039

***

(0.0011)

20.0007

(0.0015)

20.0040

***

(0.0010)

20.0177

***

(0.0058)

20.0428

***

(0.0057)

20.0077

(0.0057)

Adjusted

R2

0.4357

0.4358

0.4309

0.1794

0.1978

0.2071

F-statistic

5.1575

***

5.1585

***

5.0766

***

2.2219

***

2.3780

***

2.4604

***

DW-stat

2.3903

2.4212

2.3840

2.3110

2.3230

2.3058

Hausm

antest

42.3333***

168.2624

***

78.9829***

9.5279

***

40.7442***

0.9413

Typeof

paneldata

Fixed

Fixed

Fixed

Fixed

Fixed

Fixed

Notes:* p

,0.10,** p

,0.05,and

*** p

,0.01;fi

guresin

parentheses

arestandarderrors

robustto

heteroscedasticity

usingWhitecorrected;D

W-statisticis

Durbin-W

atsondtest

forautocorrelation;number

ofobservationis1,126

Table IV.Dimension of CSRD and

IO using unbalancedpanel data analysis

Corporate socialresponsibility

disclosure

605

investors as shareholders of the company, especially in providing information about thecompany’s involvement in CSR activities.

In contrast, results on the community involvement and environmental dimensions donot support H3 and H5. Results of both dimensions are significant negatively relatedto institutional investors. A negative link exists between the community involvementand environmental dimensions with IO. A high investment in both dimensions indicateinstitutional investors assuming additional costs; particularly from the short-teminstitutional investors perspective such as unit and investment trusts, which makedecisions based on risk and return in short-term period orientation. The extra spendingmay come from charitable activities such as conducting extensive donations, promotingcommunity development plans and establishing environmental protection activities.

The existence of negative relations for both the community involvement andenvironmental dimensions to IO has some arguments, including that the institutionalinvestors assumed that investing in both dimensions require significant financing. Theextra expenditure may come from activities such as doing extensive charitabledonations, promoting community development plans and establishing environmentalprotection activities. In particular, the environmental dimension is also assumed to havehigher expenditure. In order to fulfil implementation of environmental managementprogrammes, some companies set aside investment in their capital expenditure, such asresearch and development and building alternative plans, or enhancing their productionprocessing to minimize adverse impact on the environment. These investmentsinfluence a company’s cash flow during the financial reporting. However, theseexpenditures might find the companies at an economic disadvantage compared withother companies that are less socially responsible (Balabanis et al., 1998).

Other arguments include that institutional investors in Malaysia are less concernedwith both dimensions (community involvement and environment), possibly because nobenefits can be taken directly into their portfolio investments. Itmay be that institutionalinvestors in Malaysia are heavily profit oriented, and particularly short-terminstitutional investors who just focus on making profits in shorter time periods.Results of the relationship between CSR dimensions and IO reveal that institutionalinvestors pay attention to how companies manage certain dimensions in a Malaysiancontext, and that the only focus is on employee relations and product dimensions. Thisindicates that institutional investors are not totally opposed to company involvement insocial activities (Teoh and Shiu, 1990). However, companies can improve theiradvantages in social performance through proactive promotion and recruiting ofmanagers who are concerned with environmental orientation (Simerly, 1995).

Discussion and conclusionThe first objective of this study is to establish the CSRD status of Malaysian PLCs.The longitudinal data analysis for the period of 2000-2005 reveals that the involvementand disclosures of CSR activities are improving gradually. The highest disclosuretheme is employee relations, followed by community involvement, product, and finallythe environment dimension. Most PLCs in Malaysia disclose their CSR activities ingeneral statement terms where information content is limited. However, the number ofcompanies that participated during the seven-year period of analysis did not improvesignificantly in accordance with stakeholders’ expectations (Bursa Malaysia, 2007).

MAJ25,6

606

The second objective of this study is to examine whether there are any relationshipsbetweenCSRDand its dimensions and IO.The information of companies’ involvement inCSR activities is represented byCSRD in annual reports. The findings of the longitudinaldata analysis show that CSRD is positive and significantly related to IO. This resultreveals that institutional investors that select portfolio investments tend to considerthe social performance of companies. This finding is consistent with the findings of priorstudies that indicate investors consider social disclosure in their investment decision(Milne and Chan, 1999). Their choices avoid or exclude those companies with poor socialperformance. Numerous investors believe that the more the companies are sociallyresponsible, the safer their investment (Mahoney and Roberts, 2007).

The results of this study however show that among the CSR dimensions, institutionalinvestors are less concerned with companies engaging in community contributionpractices and those related to the environmental exposure in which the companyoperates. The lack of concern could be due to the assumption that neither activity hasdirect impact on the investment portfolios of these institutional investors. Nevertheless,institutional investors are not totally opposed to companies that are involved in socialactivities (Milne and Chan, 1999; Teoh and Shiu, 1990). Hence, companies can improvetheir advantage in social performance through proactive promotion and the recruitmentof managers who are concerned with environmental protection (Simerly, 1995).However, institutional investors respond positively to the employee relations andproduct dimensions. This indicates that institutional investors appreciate fair managerswho assist in attracting and maintaining the best workforce, and are concerned withproduct quality and safety.

This study is the possibility for institutional investors to design their investmentcriteria. For example, an investor can plan long-term benefits by placing and holdingshares over a longer period of time in companies that are involved in socially responsibleactivities. Numerous companies feel pleased to enhance their CSR activities as part of aneffort to build public trust. Good CSR practices of the Malaysian PLCs will increase theconfidential of the institutional investors. This is because institutional investors arerisk-averse in their investment decision. This suggests that institutional investors mayfeel more secure if they retain their portfolio investments in the companies that areactively engaged in CSR practices.

The findings suggest that policy-makers especially the Security Commission shouldconsider the need to establish CSRD requirements that are beneficial to the stakeholders.The Security Commission may consider providing criteria to measure socialperformance as well as establishing a social performance ranking for PLCs inMalaysia. This ranking could be used as a benchmark target for PLCs in Malaysia andsimultaneously provide a general standard to evaluate other companies engaging inCSR activities. The introduction of such criteria might not only be of assistance tocompanymanagerswhofind it difficult tomeasure the success of their ownCSRpolicies,it can also be used to attract investors especially ethical investments that have grownrapidly in recent times. Future empirical studies concerning the relationship betweenCSRD and IO are expected to increase rapidly if a general evaluation standard for CSRactivities by PLCs in Malaysia is made available.

Finally, a general confirmation can be made that this study has proven a positiveand significant relationship between CSRD and IO. This confirms that increasedactive involvement and promotion of CSR activities brings together the interests

Corporate socialresponsibility

disclosure

607

of stakeholders, therefore having a positive on IO. Disclosure of CSR activities canalso be used as leverage to attract institutional investors to actively invest in MalaysianPLCs that have solid platforms for socially responsible practices.

Certain limitations of the study and recommendations on how to overcome themare explored in this section. First, the study utilizes the content analysis methodwhich according to prior studies is subject to human error as the study uses judgment toexplore what represents CSRD (Abdul Hamid, 2004; Thompson and Zakaria, 2004;Mathews, 1997; Hackston andMilne, 1996). The study solely focuses on the disclosure ofcompanies’ annual reports, even though it is known that companies utilize other masscommunicationmechanisms. Hence, future researchmay have to consider disclosures ofCSR activities exposed by other media such as companies’ stand-alone reporting,in-house magazines, newspapers, and web sites.

The diversification of IO in future studies can be considered. There are two categoriesof institutional investors, namely short- and long-term ones. Both have a differentorientation towards companies’ involvement in CSR activities (Cox et al., 2004). Thesedifferent categories of institutional investors are likely to demonstrate differentinvestment behaviours and pursue varied objectives that are subject to variousconditions and constraints. Hence, it may help companies attract appropriateinstitutional investors with their respective orientation of investment.

Notes

1. Most prior studies have examined the relationship between CSP and IO (Mahoney andRoberts, 2007; Cox et al., 2004; Johnson and Greening, 1999; Simerly, 1995; and Graves andWaddock, 1994). The concept of CSP evolved from the concepts of CSR and corporate socialresponsiveness, which responded to questions concerning companies’ social responsibilitiesand how these should be enacted (Neville et al., 2006). However, “CSR” and “CSP” are oftenemployed interchangeably (Barnett, 2007). For consistency, in this study, the term utilized isCSR.

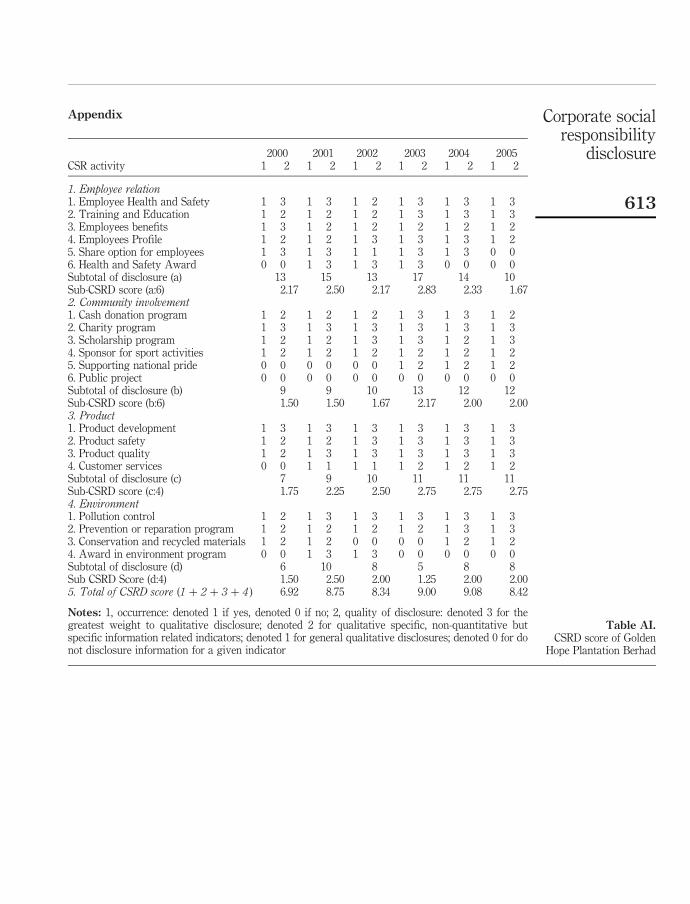

2. For instance, result of CSRD score of the company is presented in the Appendix Table AI.

References

Abdul Hamid, F.Z. (2004), “Corporate social disclosure by banks and finance companies:Malaysian evidence”, Corporate Ownership and Control, Vol. 1 No. 4, pp. 118-29.

ACCA (2003), Environmental Reporting Guidelines for Malaysian Companies, CertifiedAccountants Educational Trust, London.

Al-Tuwaijri, S.A., Christensen, T.E. and Hughes, K.E. II (2004), “The relations amongenvironmental disclosure, environmental performance, and economic performance:a simultaneous equations approach”, Accounting, Organizations and Society, Vol. 29,pp. 447-71.

Amran, A. (2006), “Corporate social reporting in Malaysia: an intuitional perspective”,unpublished PhD thesis, University of Malaya, Kuala Lumpur.

Amran, A. and Devi, S.S. (2007), “Corporate social reporting in Malaysia: an institutionalperspective”, World Review of Entrepreneurship, Management and SustainableDevelopment (WREMSD), Vol. 3 No. 1, pp. 20-36.

Amran, A., Ling, L.L. and Sofri, Y. (2007), “A study of corporate philanthropic traits amongmajor Malaysian corporations”, Social Responsibility Journal, Vol. 3 No. 4, pp. 21-30.

MAJ25,6

608

Ariff, M. and AbuBakar, S.Y. (1999), “The Malaysian financial crisis: economic impactand recovery prospects”, The Developing Economies, Vol. 37 No. 4, pp. 417-38.

Balabanis, G., Philip, H.G. and Lyall, J. (1998), “Corporate social responsibility and economicperformance in the top British companies: are they linked?”, European Business Review,Vol. 98 No. 1, pp. 25-44.

Barnett, M.L. (2007), “Stakeholder influence capacity and the variability of financial returns tocorporate social responsibility”,Academy ofManagement Review, Vol. 32No. 3, pp. 794-816.

Benston, J. (1997), “Voluntary vs mandated disclosure (an evaluation of the basis for therecommendations of the working group on improved product and adviser disclosure)”,Report prepared for the New Zealand Business Roundtable, Wellington, pp. 1-20,available at: http://repositories.cdlib.org/cgi/viewcontent.cgi?article

Branco, M.C. and Rodrigues, L.L. (2008), “Factors influencing social responsibility disclosure byPortuguese companies”, Journal of Business Ethics, Vol. 83, pp. 685-701.

Bursa Malaysia (2007), “Corporate social responsibility in Malaysian PLCs, an executivesummary”, available at: http://klse.com.my/website/bm/about us/the organization/csr/downloaded/csr_booklet.pdf/ (accessed July 12, 2008).

Chapple, W. and Moon, J. (2005), “Corporate social responsibility (CSR) in Asia: a seven-countrystudy of CSR web site reporting”, Business & Society, Vol. 44 No. 4, pp. 415-41.

Che Haat, M.H., Abdul Rahman, R. and Mahenthiran, S. (2008), “Corporate governance,transparency and performance of Malaysian companies”, Managerial Auditing Journal,Vol. 23 No. 8, pp. 744-78.

Che Zuriana, M.J., Kasumalinda, A. and Rapiah, M. (2003), “Corporate social responsibilitydisclosure in the annual reports of Malaysian companies: a longitudinal study”, Social& Environmental Accounting Journal, Vol. 22 No. 2, pp. 5-9.

Christopher, T., Hutomo, Y.B.S. and Monroe, G. (1997), “Voluntary environmental disclosure byAustralian listed mineral mining companies: an application of stakeholder theory”,The International Journal of Accounting & Business Society, Vol. 5 No. 1, pp. 42-65.

Clarkson, M.B.E. (1995), “A stakeholder framework for analyzing and evaluating corporate socialperformance: an empirical investigation”, Journal of Consumer Marketing, Vol. 14 No. 6,pp. 421-32.

Coffey, B.S. and Fryxell, G.E. (1991), “Institutional ownership of stock and dimensions ofcorporate social performance: an empirical examination”, Journal of Business ethics, Vol. 10No. 6, pp. 437-44.

Cox, P., Brammer, S. and Millington, A. (2004), “An empirical examination of institutionalinvestor preferences for corporate social performance”, Journal of Business Ethics, Vol. 52No. 1, pp. 27-42.

Elijido-Ten, E. (2004), “Determinants of environmental disclosures in a developing country:an application of the stakeholder theory”, 4th Asian Pacific Interdisciplinary Research inAccounting Conference Proceedings, APIRA, Singapore.

Epstein, M.J. and Freedman, M. (1994), “Social disclosure and the individual investor”,Accounting, Auditing & Accountability Journal, Vol. 7 No. 4, pp. 94-109.

Gardiner, L., Rubbens, C. and Bonfiglioni, E. (2003), “Big business, big responsibilities”,Corporate Governance, Vol. 3 No. 3, pp. 67-77.

Ghosh, S.R. (2006), East Asian Finance: The Road to Robust Markets, World Bank, Washington,DC, available at: http://web.worldbank.org/WBSITE/EXTERNAL/COUNTRIES/EASTASIAPACIFICEXT/EXTEAPREGTOPFINFINSECDEV/0,contentMDK:20968028,pagePK:34004173,piPK:34003707,theSitePK:589810,00.html

Corporate socialresponsibility

disclosure

609

Graves, S.B. and Waddock, S.A. (1994), “Institutional owner and corporate social performance”,The Academy of Management Journal, Vol. 37 No. 4, pp. 1034-46.

Gray, R., Kouhy, R. and Lavers, S. (1995), “Corporate social and environmental reporting: a reviewof the literature and a longitudinal study of UK disclosure”, Accounting, Auditing &Accountability Journal, Vol. 8 No. 2, pp. 47-77.

Greene, W.H. (2008), Econometric Analysis, 6th ed., Pearson Education, Upper Saddle River, NJ.

Guthrie, J. and Parker, L.D. (1990), “Corporate social disclosure practice: a comparativeinternational analysis”, Advance in Public Interest Accounting, Vol. 3, pp. 159-75.

Hackston, D. and Milne, D.M. (1996), “Some determinant of social and environmental disclosuresin the New Zealand companies”, Accounting, Auditing & Accountability Journal, Vol. 9No. 1, pp. 77-108.

Haniffa, R.M. and Cooke, T.E. (2005), “The impact of culture and governance on corporate socialreporting”, Journal of Accounting & Public Policy, pp. 1-40.

Hayashi, A.M. (2003), “Effect of institutional ownership”, MITSLOAN Management Review,Vol. 45 No. 1, pp. 6-7.

Hughes, S.B., Anderson, A. and Golden, S. (2001), “Corporate environmental disclosures: are theyuseful in determining environmental performance?”, Journal of Accounting and PublicPolicy, Vol. 20, pp. 217-40.

Investor Digests (2003), “Why corporate social responsibility matters”, Investor Digests, availableon: Database: Business Source Premier (accessed on May 16, 2005) .

Jenkins, H. and Yakovlena, N. (2005), “Corporate social responsibility in the mining industry:exploring trends in social and environmental disclosure”, Journal of Cleaner Production,Vol. 14 Nos 3/4, pp. 1-14.

Johnson, R.A. and Greening, D.W. (1999), “The effects of corporate governance and institutionalownership types on corporate social performance”, Academy of Management Journal,Vol. 42 No. 5, pp. 564-76.

Kanter, R. (1999), “Change is everyone’s job: managing the extended enterprise in a globallyconnected world”, Organizational Dynamics, Vol. 28, pp. 6-24.

Kin, H.S. (1990), “Corporate social responsibility disclosures in Malaysia”, Akauantan Nasional,Vol. 1, pp. 4-9.

Kok, P., Weile, T.V.D., McKenna, R. and Brown, A. (2001), “A corporate social responsibilityaudit within a quality management framework”, Journal of Business Ethics, Vol. 31 No. 4,pp. 285-97.

Lewis, A. and Mackenzie, C. (2000), “Support for investor activism among UK ethical investors”,Journal of Business Ethics, Vol. 24 No. 3, pp. 215-22.

McGuire, J., Sundgren, A. and Schneeweis, T. (1988), “Corporate social responsibility and firmfinancial performance”, Academy of Management Journal, Vol. 31 No. 4, pp. 854-72.

Mahoney, L. and Roberts, R.W. (2007), “Corporate social performance, and financial performanceand institutional ownership in Canadian firms”, Accounting Forum, Vol. 31, pp. 233-53.

Mathews, M.R. (1997), “Twenty five years of social and environment accounting research: is thereany silver jubilee to celebrate?”, Accounting, Auditing & Accountability Journal, Vol. 10No. 4, pp. 481-531.

Milne, M.J. and Chan, C.C.C. (1999), “Narrative corporate social disclosures: how muchof a difference do they make to investment decision-making?”, British Accounting Review,Vol. 31, pp. 439-57.

MAJ25,6

610

Mohd Ghazali, N.A. (2007), “Ownership structure and corporate social responsibility disclosure:some Malaysian evidence”, Corporate Governance Journal, Vol. 7 No. 3, pp. 251-66.

Neville, B.A., Bell, S.J. and Meng̈c, B. (2006), “Corporate reputation, stakeholders and the socialperformance-financial performance relationship”, European Journal of Marketing, Vol. 39Nos 9/10, pp. 1184-98.

Nik Ahmad, N.N. and Sulaiman, M. (2004), “Environmental disclosure in Malaysian annualreports: a legitimacy theory perspective”, International Journal of Commerce& Management, Vol. 14 No. 1, pp. 44-58.

Nik Ahmad, N.N., Sulaiman, M. and Siswantoro, D. (2003), “Corporate social responsibilitydisclosure in Malaysia: an analysis of annual reports of KLSE listed companies”, IIUMJournal of Economics and Management, Vol. 11 No. 1, pp. 1-37.

Nik Ahmad, N.Z. and Abdul Rahim, N.L.A. (2003), “Awareness of the concepts of corporate socialresponsibility among Malaysian managers in selected public listed companies”,paper presented at the 7th International Conference on Global Business and EconomicDevelopment, Plaza Athanee Hotel, Bangkok, January 8-11.

Prathaban, V. (2005), “Big earners, small givers?”, Malaysian Business, September 16.

Rashid, Z.A. and Ibrahim, S. (2002), “Executive and management attitudes towards corporatesocial responsibility in Malaysia”, Corporate Governance, Vol. 2 No. 4, pp. 10-16.

Robert, R.W. (1992), “Determinants of corporate social responsibility disclosure: an application ofstakeholder theory”, Accounting, Organisations and Society, Vol. 17 No. 6, pp. 595-612.

Sauer, D.A. (1997), “The impact of social-responsibility screens on investment performance:evidence from Domini 400 social index and Domini equity mutual fund”, Review ofFinancial Economics, Vol. 6 No. 1, pp. 137-49.

Schwab, K.J. and Thomas, R.S. (1998), “Realigning corporate governance: shareholder activismby labour unions”, Michigan Law Review, Vol. 96, pp. 1018-94.

Seifert, B., Morris, S.A. and Bartkus, B.R. (2003), “Comparing big givers and small givers:financial correlates of corporate philanthropy”, Journal of Business Ethics, Vol. 45,pp. 195-211.

Simerly, R.L. (1995), “Institutional ownership, corporate social performance, and firms financialperformance”, Psychological Reports, Vol. 77, pp. 515-25.

Snider, J., Hill, P.R. and Martin, D. (2003), “Corporate social responsibility in the 21st century:a view from the World’s most successful firms”, Journal of Business Ethics, Vol. 48,pp. 175-87.

Spicer, B.H. (1978), “Investors, corporate social performance and information disclosure:an empirical study”, The Accounting Review, Vol. 53, pp. 94-111.

Sumiani, Y., Haslinda, Y. and Lehman, G. (2007), “Environmental reporting in a developingcountry: a case study on status and implementation in Malaysia”, Journal of CleanerProduction, Vol. 15, pp. 895-901.

Tam, S. (2007), “The next wave of CSR”, The Star Online, available at: http://biz.thestar.com.my/news/story.asp?file¼/2007/9/3/business/18731567&sec¼business

Taub, S. (2001), “In 2002, disclosure in, employee ownership out: survey says institutionalinvestors likely to demand better governance, less dilution”, Investor Relations,December 1-2, available at: http://cfo.com/article.cfm/3002734/c_2984303?f¼bc

Teoh, H.Y. and Shiu, G.Y. (1990), “Attitudes towards corporate social responsibility andperceived importance of social responsibility information characteristics in a decisioncontext”, Journal of Business Ethics, Vol. 9 No. 1, pp. 71-7.

Corporate socialresponsibility

disclosure

611

Teoh, H.Y. and Thong, G. (1984), “Another look at corporate social responsibility and reporting:an empirical study in a developing country”, Accounting, Organizations and Society, Vol. 9No. 2, pp. 189-206.

Thompson, P. and Zakaria, Z. (2004), “Corporate social responsibility reporting in Malaysia:progress and prospects”, Journal of Corporate Citizenship, Vol. 13 No. 1, pp. 125-36.

Turban, D.B. and Greening, D.W. (1997), “Corporate social performance and organizationalattractiveness to prospective employees”, Academy of Management Journal, Vol. 40 No. 3,pp. 658-72.

Vilanova, M., Lozano, J.M. and Arenas, D. (2009), “Exploring the nature of the relationshipbetween CSR and competitiveness”, Journal of Business Ethics, Vol. 87, pp. 57-69.

Wagner, M. (2005), “How to reconcile environmental and economic performance to improvecorporate sustainability: corporate environmental strategies in the European paperindustry”, Journal of Environmental Management, Vol. 79, pp. 105-18.

Webley, P., Lewis, A. and Mackenzie, C. (2001), “Commitment among ethical investors:an experimental approach”, Journal of Economic Psychology, Vol. 22, pp. 27-42.

Williams, S.M. and Pei, C.H.W. (1999), “Corporate social disclosures by listed companies on theirweb sites: an international comparison”, The International Journal of Accounting, Vol. 34No. 3, pp. 389-419.

Wiseman, J. (1982), “An evaluation of environmental disclosures made in corporate annualreports”, Accounting, Organizations and Society, Vol. 7 No. 1, pp. 53-63.

Zeghal, D. and Ahmed, S.A. (1990), “Comparison of social responsibility information disclosuremedia used by Canadian firms”, Accounting, Auditing & Accountability Journal, Vol. 3No. 1, pp. 38-53.

Zulkifli, N. and Amran, A. (2006), “Realising corporate social responsibility in Malaysia: viewfrom the accounting profession”, Journal of Corporate Citizenship, Vol. 24 No. 4, pp. 101-14.

Further reading

Andrew, B.H., Gul, F.A., Guthrie, J.E. and Teoh, H.Y. (1989), “A note on corporate socialdisclosure practices: the case of Malaysia and Singapore”, British Accounting Review,Vol. 21 No. 4, pp. 371-6.

Freeman, R.E. (1994), “The politics of stakeholder theory: some future directions”, BusinessEthics Quarterly, Vol. 4 No. 4, pp. 409-29.

Renneboog, L., Horst, J.T. and Zhang, C. (2008), “Socially responsible investments: institutionalaspects, performance, and investor behavior”, Journal of Banking & Finance, Vol. 32 No. 9,pp. 1723-42.

Corresponding authorMustaruddin Saleh can be contacted at: [email protected]

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints

MAJ25,6

612

Appendix

2000 2001 2002 2003 2004 2005CSR activity 1 2 1 2 1 2 1 2 1 2 1 2

1. Employee relation1. Employee Health and Safety 1 3 1 3 1 2 1 3 1 3 1 32. Training and Education 1 2 1 2 1 2 1 3 1 3 1 33. Employees benefits 1 3 1 2 1 2 1 2 1 2 1 24. Employees Profile 1 2 1 2 1 3 1 3 1 3 1 25. Share option for employees 1 3 1 3 1 1 1 3 1 3 0 06. Health and Safety Award 0 0 1 3 1 3 1 3 0 0 0 0Subtotal of disclosure (a) 13 15 13 17 14 10Sub-CSRD score (a:6) 2.17 2.50 2.17 2.83 2.33 1.672. Community involvement1. Cash donation program 1 2 1 2 1 2 1 3 1 3 1 22. Charity program 1 3 1 3 1 3 1 3 1 3 1 33. Scholarship program 1 2 1 2 1 3 1 3 1 2 1 34. Sponsor for sport activities 1 2 1 2 1 2 1 2 1 2 1 25. Supporting national pride 0 0 0 0 0 0 1 2 1 2 1 26. Public project 0 0 0 0 0 0 0 0 0 0 0 0Subtotal of disclosure (b) 9 9 10 13 12 12Sub-CSRD score (b:6) 1.50 1.50 1.67 2.17 2.00 2.003. Product1. Product development 1 3 1 3 1 3 1 3 1 3 1 32. Product safety 1 2 1 2 1 3 1 3 1 3 1 33. Product quality 1 2 1 3 1 3 1 3 1 3 1 34. Customer services 0 0 1 1 1 1 1 2 1 2 1 2Subtotal of disclosure (c) 7 9 10 11 11 11Sub-CSRD score (c:4) 1.75 2.25 2.50 2.75 2.75 2.754. Environment1. Pollution control 1 2 1 3 1 3 1 3 1 3 1 32. Prevention or reparation program 1 2 1 2 1 2 1 2 1 3 1 33. Conservation and recycled materials 1 2 1 2 0 0 0 0 1 2 1 24. Award in environment program 0 0 1 3 1 3 0 0 0 0 0 0Subtotal of disclosure (d) 6 10 8 5 8 8Sub CSRD Score (d:4) 1.50 2.50 2.00 1.25 2.00 2.005. Total of CSRD score (1 þ 2 þ 3 þ 4 ) 6.92 8.75 8.34 9.00 9.08 8.42

Notes: 1, occurrence: denoted 1 if yes, denoted 0 if no; 2, quality of disclosure: denoted 3 for thegreatest weight to qualitative disclosure; denoted 2 for qualitative specific, non-quantitative butspecific information related indicators; denoted 1 for general qualitative disclosures; denoted 0 for donot disclosure information for a given indicator

Table AI.CSRD score of Golden

Hope Plantation Berhad

Corporate socialresponsibility

disclosure

613