Embed Size (px)

Citation preview

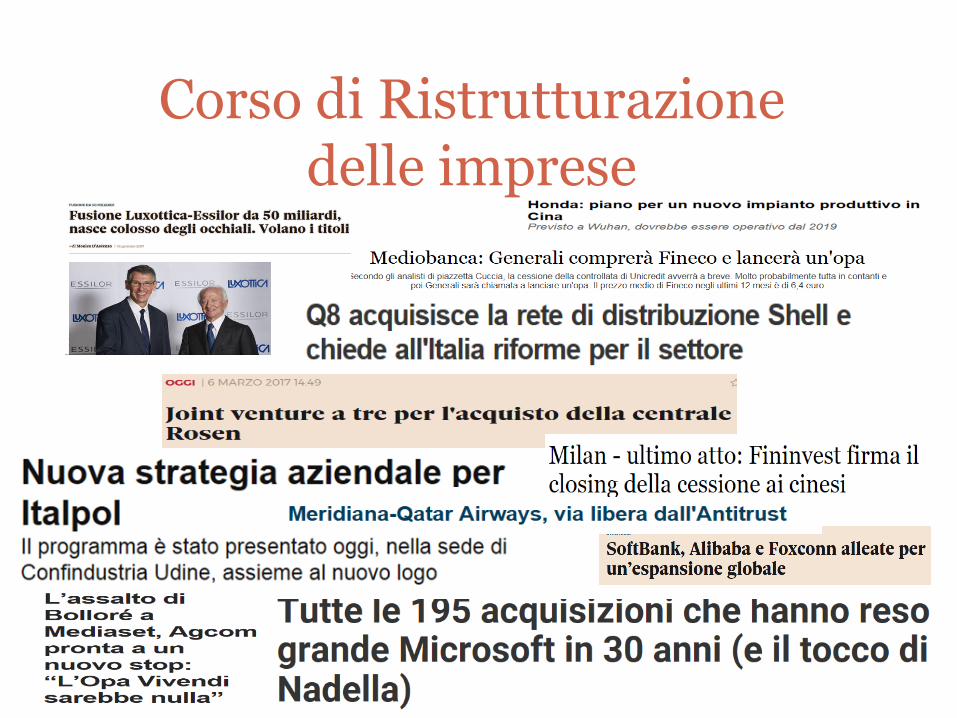

Corso di Ristrutturazione delle imprese

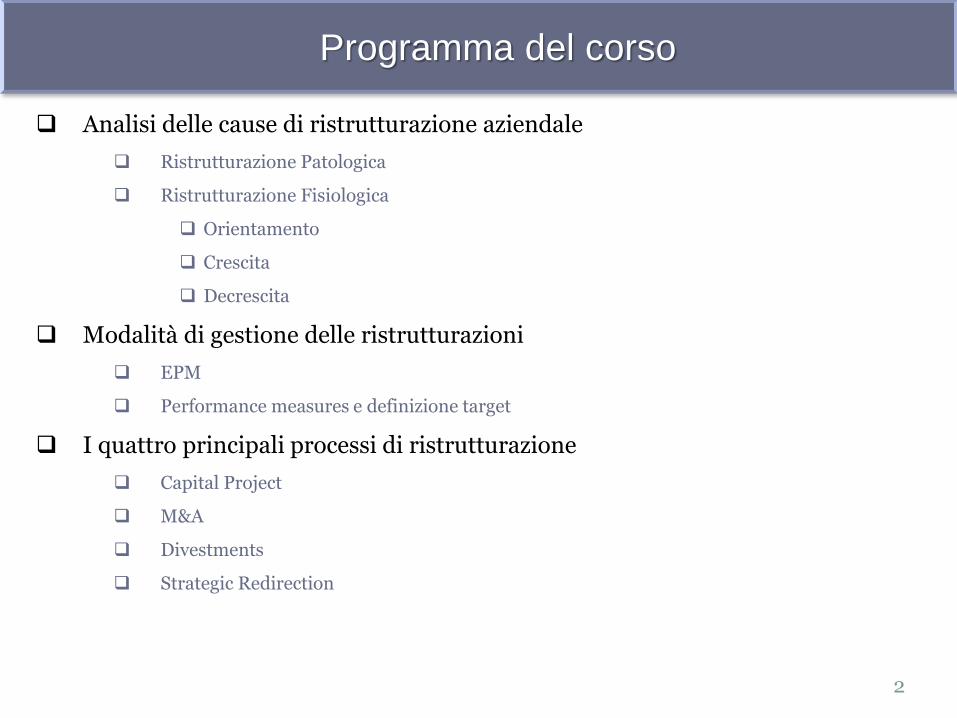

Programma del corso

Analisi delle cause di ristrutturazione aziendale

Ristrutturazione Patologica

Ristrutturazione Fisiologica

Orientamento

Crescita

Decrescita

Modalità di gestione delle ristrutturazioni

EPM

Performance measures e definizione target

I quattro principali processi di ristrutturazione

Capital Project

M&A

Divestments

Strategic Redirection

2

Le ristrutturazione sono eventi straordinari

Le ristrutturazioni sono eventi straordinari con processi e regole proprie

Le ristrutturazioni avvengono spesso in maniera improvvisa e accelerata

Modificano la struttura finanziaria, produttiva, organizzativa o la forma giuridica dell’impresa in maniera pervasiva e permanente

Introduzione

Perché ristrutturarsi…..

Il fine di una ristrutturazione è quello di acquisire conservare, sviluppare un vantaggio competitivo attraverso una maggiore EFFICIENZA

Un’azione è efficiente quando lo sforzo per compierla è minore dei benefici che da questa ne derivano. In Economia aziendale questo significa che il valore economico che si produce è maggiore del dell’investimento intrapreso per ottenerlo.

Questo gap è in genere determinato attraverso l’analisi «Discounted Cash Flows» (DCF)

Introduzione

Tipologie di ristrutturazione aziendale

Sono moltissime le cause che spingono le aziende a ristrutturarsi per ricercare efficienza e valore.

Una prima distinzione vede due macro aree di ricerca dell’efficienza:

Recuperare Efficienza compromessa (Ristrutturazione Patologica)

Perseguire aumento di Efficienza (Ristrutturazione Fisiologica)

Orientamento

Crescita

Decrescita

5

Introduzione

La pianificazione strategica dell’impresa

Gestire un’impresa significa governarla, coordinare ed amministrare i diversi fattori della produzione al fine di conseguire lo sviluppo mediante la creazione di equilibri economici, patrimoniali, finanziari.

6

Per elaborare una strategia, e quindi individuare i fini ed obiettivi dell’impresa, è necessaria un’analisi dei seguenti elementi:

L’ambiente nel quale l’impresa opera

Le risorse disponibili

I vantaggi competitivi

Le sinergie

Le ristrutturazioni legate a un nuovo orientamento

strategico

Il depositario della strategia è in un’ultima analisi l’azionista o il suo rappresentante (CDA, Amministratore Delegato etc,)

La ristrutturazione per un nuovo orientamento strategico può avvenire per diversi motivi:

Modifica della Governance/Nuova proprietà

Nuova strategia che riflette le mutate condizioni del mercato o delle priorità aziendali riviste periodicamente dall’ Alta Direzione

7

Le ristrutturazioni legate a un nuovo orientamento

strategico

Lo sviluppo dimensionale può essere realizzato tramite:

Operazioni di crescita esterna Acquisizione di capacità specifiche o di posizioni nel business

Miglioramento del Portafoglio di Business

Sviluppo interno.

8

Le strategie di crescita di un’azienda

Operazioni di crescita e relative motivazioni

Principali suddivisioni:

Sinergie

Economie dimensionali

Potere di mercato e vantaggio competitivo

Altre motivazioni

9

Due macro-famiglie di motivazioni all’attuazione della crescita:

• Migliorare l’efficienza • Ridurre la conflittualità

Le strategie di crescita di un’azienda

Sinergie

Valutate dal confronto tra catene del valore delle singole unità e quella

risultante dall’unione delle due

Determinanti nella definizione del prezzo di cessione determinato dalla

contrapposizione di interessi tra cedente e acquirente

Diverse tipologie:

Collusive: derivanti da aumento di quota di mercato

Operative: legate all’efficienza produttivo/commerciale

Finanziarie : legate alla diminuzione del rischio e alla maggiore

stabilità dei risultati

Molto difficili da prevedere e realizzare per incompletezza delle

informazioni ex ante e per difficoltà di implementazione 10

Le strategie di crescita di un’azienda

Economie dimensionali

Economie di scala (settore, trade off efficienza/flessibilità)

Economie di scopo (es. produzione congiunta di prodotti o componenti, asset

immateriali condivisibili)

Economie dimensionali e funzioni aziendali (produzione,

approvvigionamento, finanza, distribuzione, R&S, marketing, immagine e

brand extension)

Diseconomie e grande dimensione

Dimensione e redditività (matrice BCG e GE-McKinsey)

11

Le strategie di crescita di un’azienda

Potere di mercato e vantaggio competitivo

Possibilità di mantenere prezzi più elevati di quelli che si formerebbero in regime di piena concorrenza

Il ‘’modello di Porter’’ si propone di individuare le forze (e di studiarne intensità ed importanza) che incidono sulla possibilità di ottenere e mantenere un vantaggio competitivo.

Tali forze agiscono infatti con continuità, e, se non opportunamente monitorate e fronteggiate, portano alla perdita di competitività.

Gli attori di tali forze sono:

Concorrenti diretti

Fornitori

Clienti/Acquirenti

Potenziali entranti

Produttori di beni sostitutivi

12

Le strategie di crescita di un’azienda

Altre motivazioni

Vantaggi fiscali (trasferimento perdite fiscali, fiscalità internazionale)

Riorganizzazione assetti societari (assetto proprietario/imprenditoriale) In relazione ad una maggiore o minore intensità di intervento possiamo individuare quattro categorie principali di operazioni:

Leverage buy out (New Co, target, garanzie, finanziamento, fusione)

Costituzione di gruppi di imprese (gestione della leva azionaria)

13

Le strategie di crescita di un’azienda

ristrutturaz. riconversione trasformaz. turnaround

Alto Basso Intensità intervento

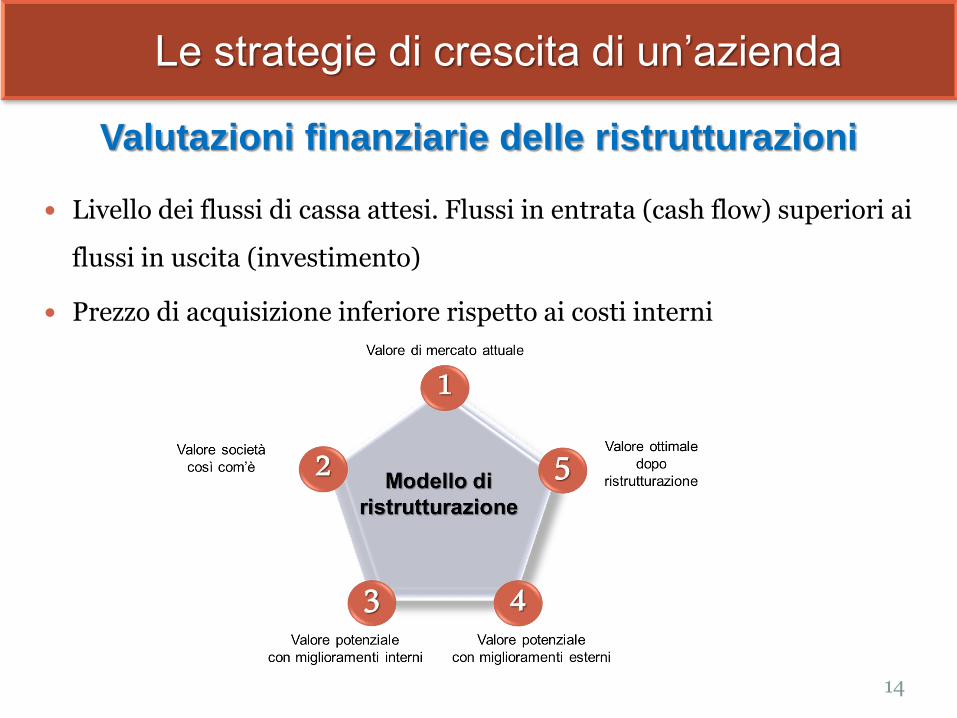

Valutazioni finanziarie delle ristrutturazioni

Livello dei flussi di cassa attesi. Flussi in entrata (cash flow) superiori ai

flussi in uscita (investimento)

Prezzo di acquisizione inferiore rispetto ai costi interni

14

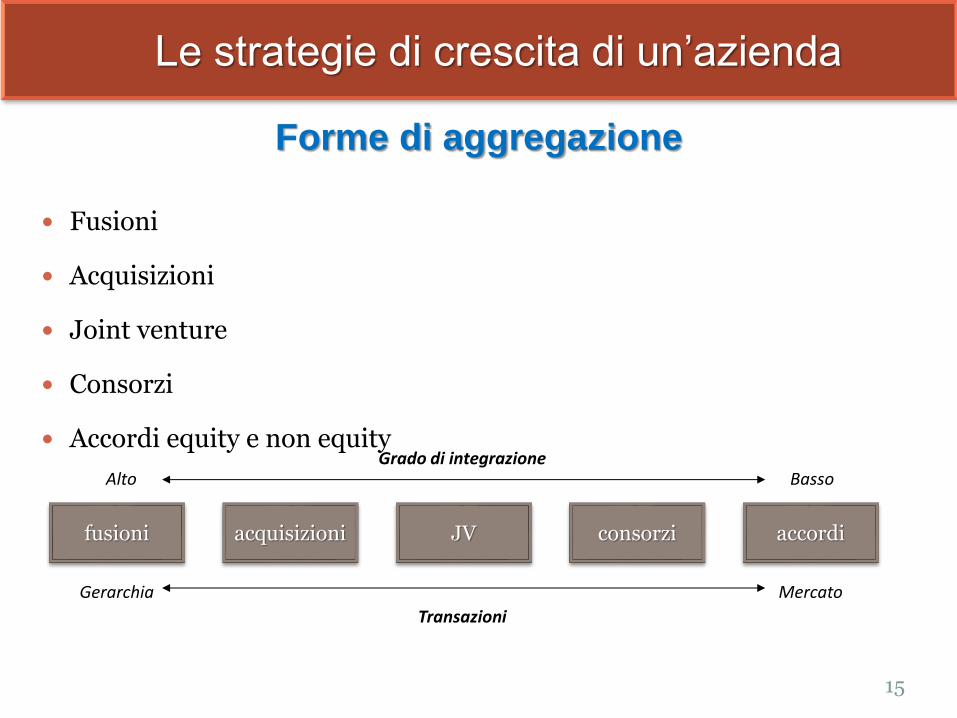

Le strategie di crescita di un’azienda

Forme di aggregazione

Fusioni

Acquisizioni

Joint venture

Consorzi

Accordi equity e non equity

15

Le strategie di crescita di un’azienda

fusioni acquisizioni JV consorzi accordi

Alto Basso Grado di integrazione

Gerarchia Mercato

Transazioni

Le direzioni della Crescita: Integrazione verticale

Le fasi del processo di produzione sono internalizzate

Valutazioni di Make or Buy

Costi di produzione interna

Costi di ricorso al mercato (imperfezione mercato, opportunismo operatori)

Fabbisogno di integrazione:

Alto (processi integrati)

Medio (Business di base comuni)

Basso (operazioni rimangono disgiunte)

Pro: Economie di scala, di informazione, stabilità, potere contrattuale

Cons: Incremento costi fissi, diseconomie , coordinamento competenze

Integrazione e tendenze verso l’esternalizzazione 16

Le strategie di crescita di un’azienda

Le direzioni della crescita: Integrazione orizzontale

Aumento delle quote di mercato, economie dimensionali

Necessità di screening attento

Verifica della compatibilità delle strutture ed affinità dei partner

17

Le strategie di crescita di un’azienda

Le direzioni della crescita :Diversificazione

Si aggiunge una nuova attività a quelle già esistenti

La diversificazione concentrica Migliore utilizzazione delle Risorse (sinergie tecnico produttive)

Economie dimensionali

Raggiungimento di massa critica dimensionale (es.R&S)

La diversificazione conglomerale Miglioramento rendimento finanziario a parità di rischio

Sincronizzazione flussi di cassa

Opportunità di mercato

Fondamentale: Controllo della performance e Formula organizzativa

equilibrata

18

Le strategie di crescita di un’azienda

Ridimensionamento/Disinvestimento

Le scelte di ridimensionamento possono essere legate a:

Revisione endogena della strategia legata a mutate priorità;

Revisione esogena della strategia legata a mutamenti dell’ambiente

competitivo in cui l’impresa opera (mercato in forte contrazione,

aumentata competizione, …)

19

Le ristrutturazioni legate a

Ridimensionamento/Disinvestimento

Introduzione ed applicabilità del

“Enhanced Project Management (EPM)”

20

Enhanced Project Management (EPM)

EPM è un processo di semplice utilizzo, basato sull’esperienza e la pratica;

Obiettivo generale: fornire un processo strutturato atto a gestire progetti diversificati e potenzialmente di ampia dimensione;

Gli elementi chiave per progetti di investimento includono:

o Sistema per fasi che copre tutti i processi vitali, incentrato sul carico front-end o “Assurance reviews” per sfruttare il knowhow aziendale o Sviluppo di pacchetti di supporto per fornire la migliore informazione a chi deve

prendere le decisioni o Concludere i progetti con delle review interne per facilitare le lesson learned o Sistema di misurazione della performance aziendale o Costante gestione del rischio e degli interessi di tutte le parti interessate

Processi specifici per progetti di capitale, fusioni & acquisizioni, disinvestimenti

e reindirizzamenti strategici

22

Valutaz.

offerte

Fasi EPM per le seguenti categorie di progetto: • Progetti di Capitale

• M&A • Disinvestimenti • Reindirizzamento Strategico

Fattibilità Definizione Implementazione

Operatività Screening Fattibilità FEED EPC Start

-up

Decisione per

disinvestire

Strategia per

disinvestire

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

4

Integrazione Origine e

screening Business plan Esecuzione

Chiusura,

approvazioni

Deal

close

Progetti di

capitale

M&A

Disinvesti

menti

Generazione idee

e screening

1

2

3

Gate

1

Gate

2 Gate

3

Gate

1

Gate

3

Gate

2

Gate

1

Gate

2

Gate

4

Gate

3

Diagnostica Progettazione Implementazione Strategic

redirection 4 Gate

1

Gate

2

23

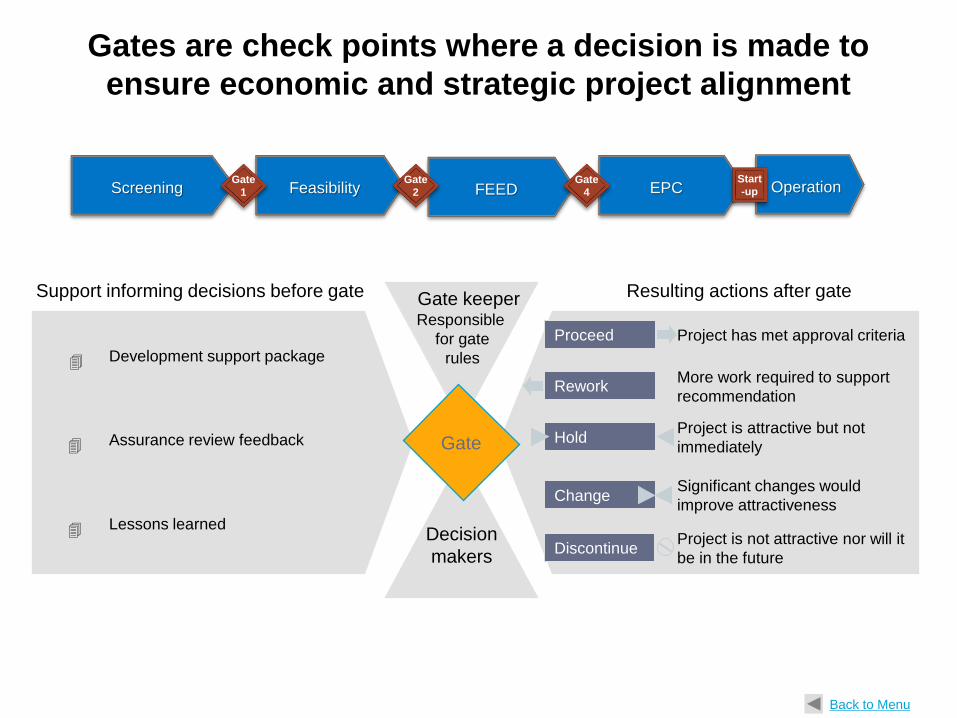

Gates are check points where a decision is made to

ensure economic and strategic project alignment

Project has met approval criteria

More work required to support

recommendation

Project is attractive but not

immediately

Significant changes would

improve attractiveness

Project is not attractive nor will it

be in the future

Proceed

Rework

Hold

Change

Discontinue

Gate keeper Responsible

for gate

rules

Gate

Development support package

Assurance review feedback

Lessons learned

Support informing decisions before gate Resulting actions after gate

Decision

makers

Overview

Back to Menu

Operation Screening Feasibility FEED EPC Start

-up Gate

1

Gate

2

Gate

4

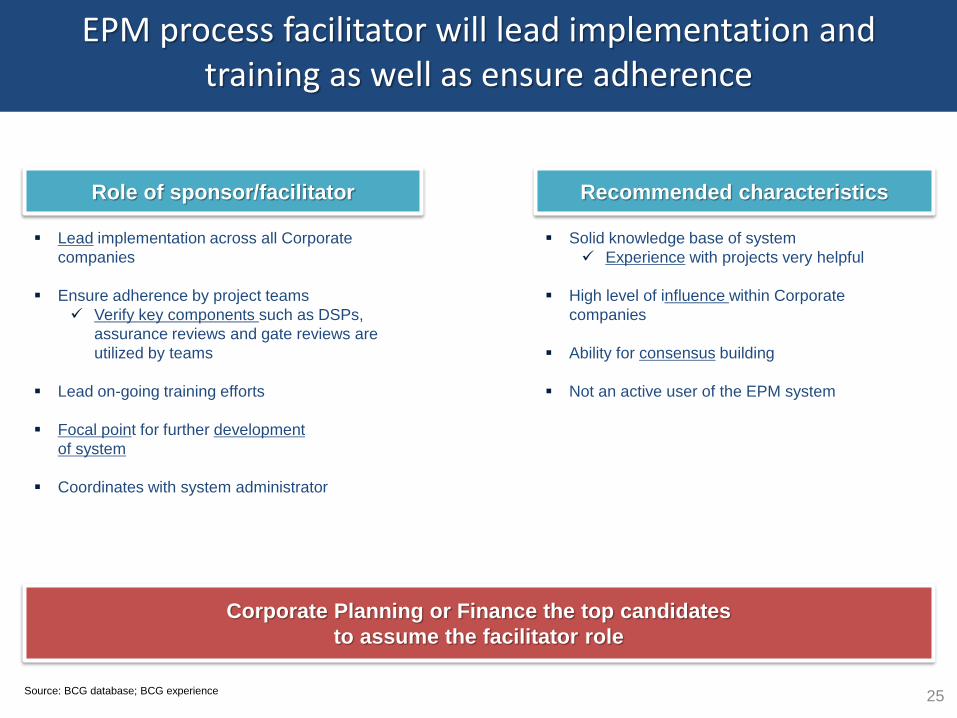

Solid knowledge base of system

Experience with projects very helpful

High level of influence within Corporate

companies

Ability for consensus building

Not an active user of the EPM system

Lead implementation across all Corporate

companies

Ensure adherence by project teams

Verify key components such as DSPs,

assurance reviews and gate reviews are

utilized by teams

Lead on-going training efforts

Focal point for further development

of system

Coordinates with system administrator

EPM process facilitator will lead implementation and training as well as ensure adherence

Role of sponsor/facilitator Recommended characteristics

Corporate Planning or Finance the top candidates

to assume the facilitator role

Source: BCG database; BCG experience 25

Disseminating company

wide knowledge

through lessons learned

to

Project personnel

Corporate staff

JV staff and

partners

Administrator regulates

access to knowledge

sharing database

Transforming raw

knowledge into a form

that can be easily shared

via lessons learned

Storing/maintaining

lessons learned in central

database

Administrator must

maintain structure/

organization of lessons

learned in system

By phase

Lessons learned are critical part of knowledge management process Knowledge management process

Codification Application

Feedback

Acquisition of

knowledge Dissemination

Translating learnings to

current context or

project

•Continual improvement

of the system

Identifying lessons

learned on current and

past projects by all levels

of staff

Within Corporate

Within Affiliates

From JVs, partners

or external

benchmarks

Administrator provides

quality check and control

for lessons learned/

documents in knowledge

sharing system

26

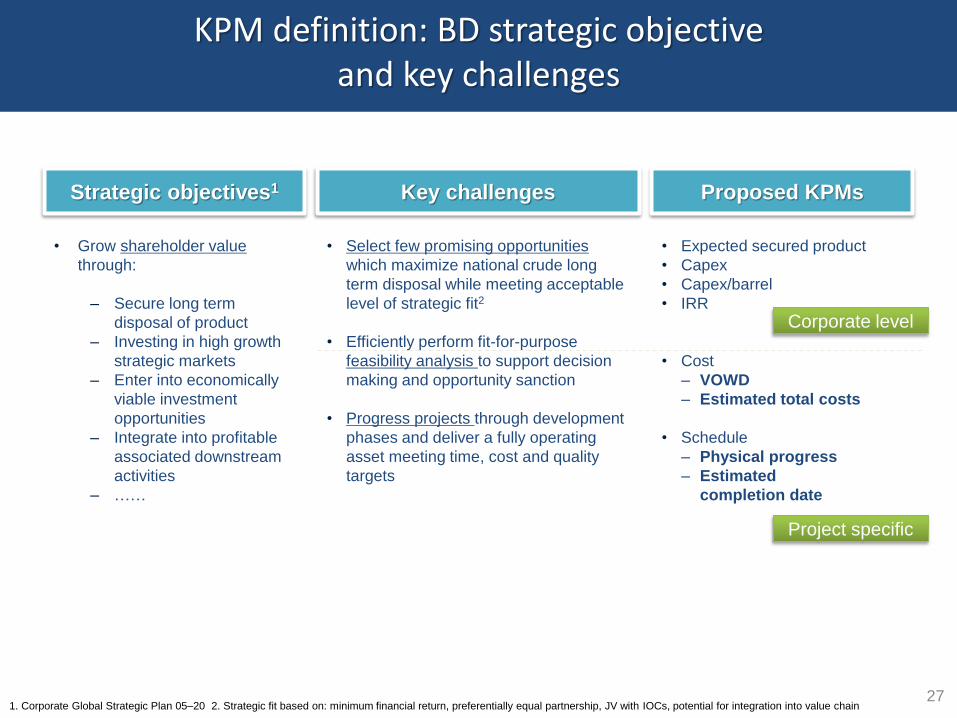

• Expected secured product

• Capex

• Capex/barrel

• IRR

• Cost

– VOWD

– Estimated total costs

• Schedule

– Physical progress

– Estimated

completion date

• Grow shareholder value

through:

– Secure long term

disposal of product

– Investing in high growth

strategic markets

– Enter into economically

viable investment

opportunities

– Integrate into profitable

associated downstream

activities

– ……

KPM definition: BD strategic objective and key challenges

Strategic objectives1 Key challenges

• Select few promising opportunities

which maximize national crude long

term disposal while meeting acceptable

level of strategic fit2

• Efficiently perform fit-for-purpose

feasibility analysis to support decision

making and opportunity sanction

• Progress projects through development

phases and deliver a fully operating

asset meeting time, cost and quality

targets

Proposed KPMs

1. Corporate Global Strategic Plan 05–20 2. Strategic fit based on: minimum financial return, preferentially equal partnership, JV with IOCs, potential for integration into value chain

Project specific

Corporate level

27

Capital projects

Operation

Capital Projects overview

Screening Feasibility FEED EPC

Projects

• Strategic fit

• Basis of

design, FEED

• Engineering

procurement

construction

Phase a

ctivity

Decis

ion

• Allocate

resources for

feasibility

• Approve

project;

• fund next

phase

• Final Investment

Decision (FID);

fund project

• Internal

check after

BOD

Start

-up Gate

1

Gate

2

Gate

3

Rework, Change,

Hold, Discontinue Proceed Rework, Change,

Hold, Discontinue Proceed

Rework, Change,

Hold, Discontinue Proceed

Appro

val

• Project originator/sponsor leads • Project team leads

• Project team assembled

• Operations

Role

Hand

over

JV

1

• MOU signed • Major commercial

/Technical items finalized • JV agreements

finalized

Start

-up

• Corporate

1st level • Corporate 1st level

• Corporate 2nd level

• Economic and

technical evaluation

• On-going

operations

Opportunities

• Corporate

1st level

• Corporate 1st level

• Corporate 2nd level

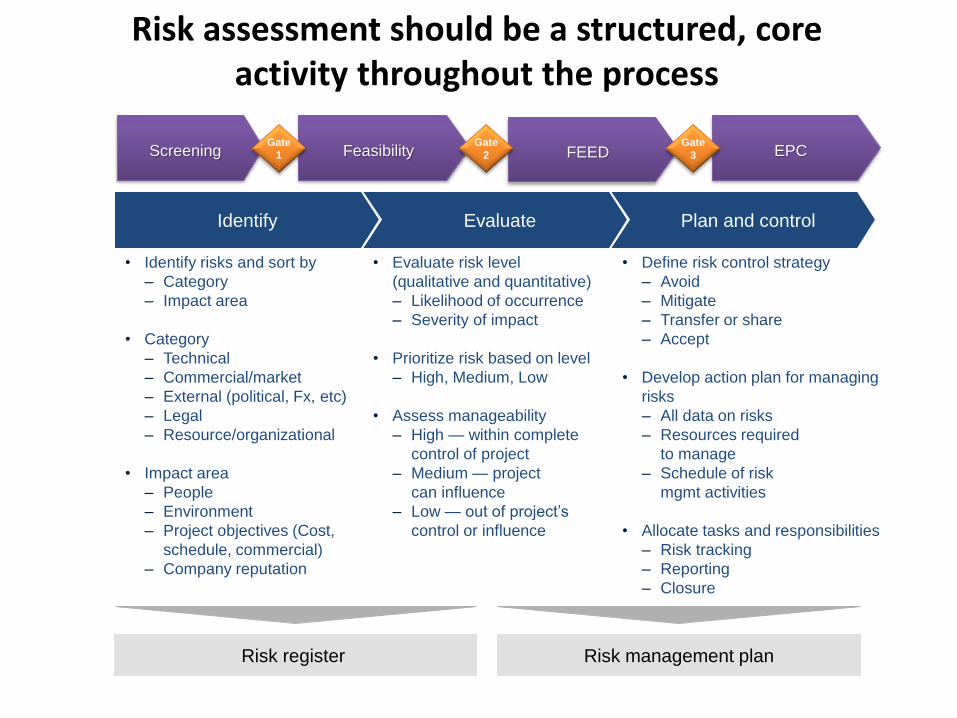

• Identify risks and sort by

– Category

– Impact area

• Category

– Technical

– Commercial/market

– External (political, Fx, etc)

– Legal

– Resource/organizational

• Impact area

– People

– Environment

– Project objectives (Cost,

schedule, commercial)

– Company reputation

• Evaluate risk level

(qualitative and quantitative)

– Likelihood of occurrence

– Severity of impact

• Prioritize risk based on level

– High, Medium, Low

• Assess manageability

– High — within complete

control of project

– Medium — project

can influence

– Low — out of project’s

control or influence

• Define risk control strategy

– Avoid

– Mitigate

– Transfer or share

– Accept

• Develop action plan for managing

risks

– All data on risks

– Resources required

to manage

– Schedule of risk

mgmt activities

• Allocate tasks and responsibilities

– Risk tracking

– Reporting

– Closure

Risk assessment should be a structured, core activity throughout the process

Identify Evaluate Plan and control

Risk register Risk management plan

Screening Feasibility FEED EPC Gate

1

Gate

2

Gate

3

Risk assessment

Screening phase

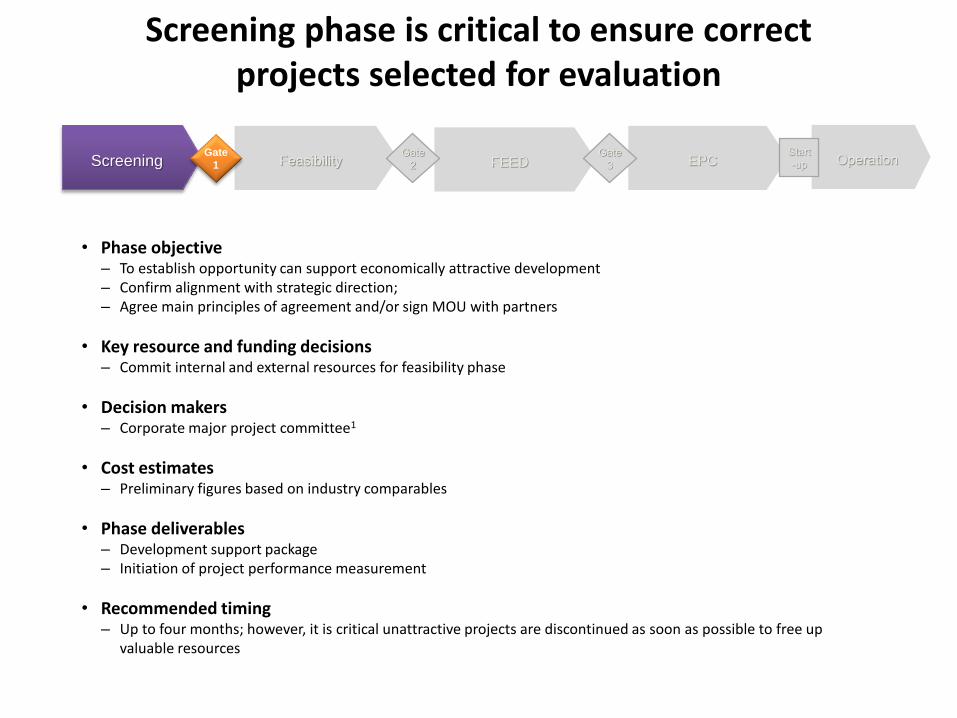

Screening phase is critical to ensure correct projects selected for evaluation

• Phase objective – To establish opportunity can support economically attractive development – Confirm alignment with strategic direction; – Agree main principles of agreement and/or sign MOU with partners

• Key resource and funding decisions – Commit internal and external resources for feasibility phase

• Decision makers – Corporate major project committee1

• Cost estimates – Preliminary figures based on industry comparables

• Phase deliverables – Development support package – Initiation of project performance measurement

• Recommended timing – Up to four months; however, it is critical unattractive projects are discontinued as soon as possible to free up

valuable resources

Overview

Operation Screening Feasibility FEED EPC Start

-up Gate

1

Gate

2

Gate

3

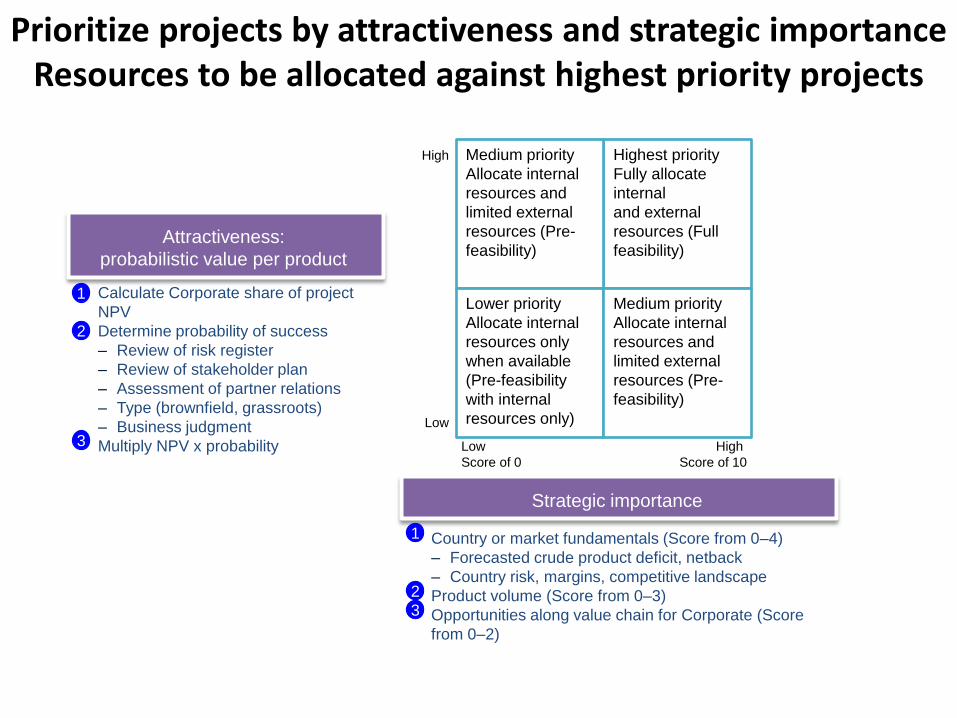

• Country or market fundamentals (Score from 0–4)

– Forecasted crude product deficit, netback

– Country risk, margins, competitive landscape

• Product volume (Score from 0–3)

• Opportunities along value chain for Corporate (Score

from 0–2)

• Calculate Corporate share of project

NPV

• Determine probability of success

– Review of risk register

– Review of stakeholder plan

– Assessment of partner relations

– Type (brownfield, grassroots)

– Business judgment

• Multiply NPV x probability

Prioritize projects by attractiveness and strategic importance Resources to be allocated against highest priority projects

Attractiveness:

probabilistic value per product

Strategic importance

Low

Score of 0

High

Score of 10

Low

High Highest priority

Fully allocate

internal

and external

resources (Full

feasibility)

Medium priority

Allocate internal

resources and

limited external

resources (Pre-

feasibility)

Lower priority

Allocate internal

resources only

when available

(Pre-feasibility

with internal

resources only)

Medium priority

Allocate internal

resources and

limited external

resources (Pre-

feasibility)

1

2

3

1

2

3

Prioritization process is a key management decision tool Priorities likely to change as projects are further developed

Low High Strategic importance

Low

High

Attractiveness

probabilistic value

of product

($)

Total Corporate NPV

represented

as size of bubble

Project C

Project B

Project A

$200MM

Project D

Project E

Project prioritization helps allocate resources to the most

valuable projects

Feasibility phase

36

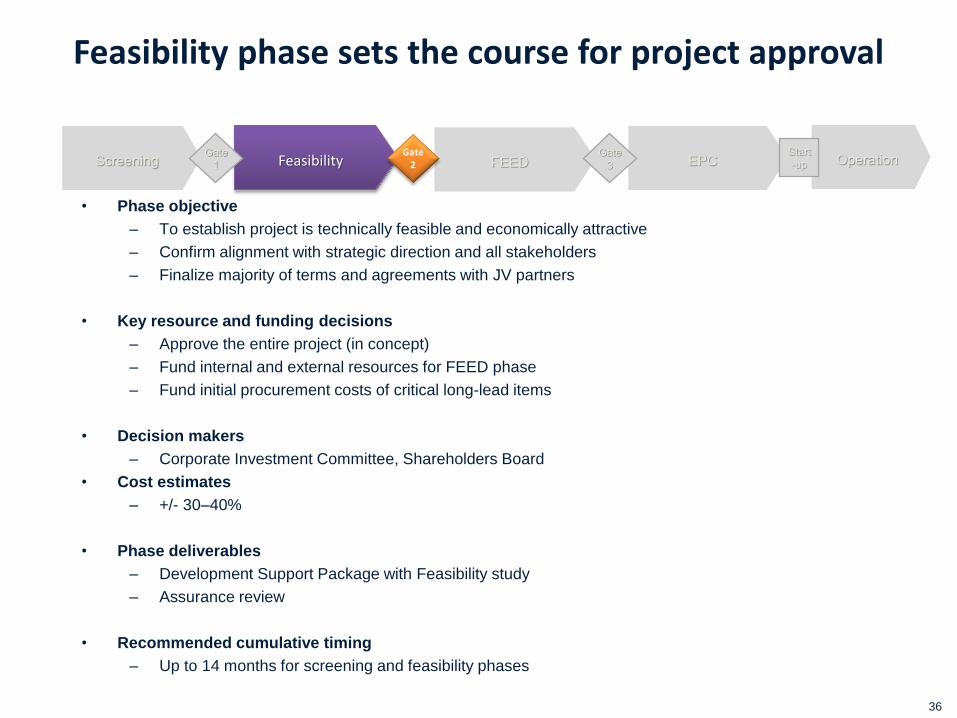

Feasibility phase sets the course for project approval

• Phase objective

– To establish project is technically feasible and economically attractive

– Confirm alignment with strategic direction and all stakeholders

– Finalize majority of terms and agreements with JV partners

• Key resource and funding decisions

– Approve the entire project (in concept)

– Fund internal and external resources for FEED phase

– Fund initial procurement costs of critical long-lead items

• Decision makers

– Corporate Investment Committee, Shareholders Board

• Cost estimates

– +/- 30–40%

• Phase deliverables

– Development Support Package with Feasibility study

– Assurance review

• Recommended cumulative timing

– Up to 14 months for screening and feasibility phases

Overview

Operation Screening Feasibility FEED EPC Start

-up Gate

1

Gate 2

Gate

3

FEED Phase

38

FEED phase utilizes one mandatory and one optional gate while stressing Front-End loading

Overview

FEED mid-phase gate (Optional1) FEED end of phase gate

Phase

objective

• To define the technical and commercial aspects of the

project in enough detail to start FEED phase

(eg, completion of basis of design)

• Alignment with strategic direction and all stakeholders

• To define the technical and commercial aspects of the

project in enough detail to start EPC phase

• Alignment with strategic direction and all stakeholders

1. Under defined guidelines

Key

decisions

• Proceed with FEED • Finalize all terms and agreements with JV partners

Decision

makers

• Corporate major project committee, Shareholders Board • Final Investment Decision (FID)

• Fund internal and external resources for the project

• Overruns during as per Corporate policy

Cost

estimates

• +/- 25% • Corpoarte major project committee, Shareholders Board,

Corporate 2nd level,

• +/-10%

Phase

deliverables

• Development Support Packages with preliminary project

execution plan

• Assurance reviews

• Development Support Packages with project execution

plan

• Assurance reviews

Timing • Up to 32 months for screening, feasibility, and

FEED phases

• Up to 32 months for screening, feasibility, and

FEED phases

Operation Screening Feasibility FEED EPC Start

-up

Gate

1

Gate

2

Gate 3

39

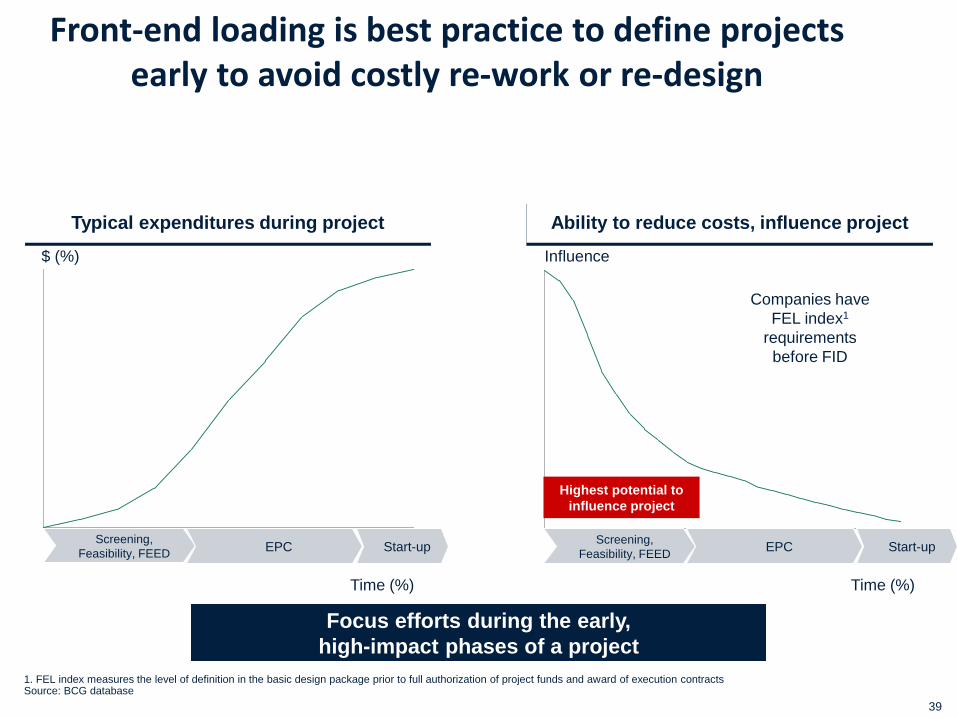

Front-end loading is best practice to define projects early to avoid costly re-work or re-design

$ (%)

Time (%)

Influence

Time (%)

Typical expenditures during project Ability to reduce costs, influence project

Highest potential to

influence project

Screening,

Feasibility, FEED EPC Start-up

Screening,

Feasibility, FEED EPC Start-up

Companies have

FEL index1

requirements

before FID

Overview

Focus efforts during the early,

high-impact phases of a project

1. FEL index measures the level of definition in the basic design package prior to full authorization of project funds and award of execution contracts Source: BCG database

EPC phase

41

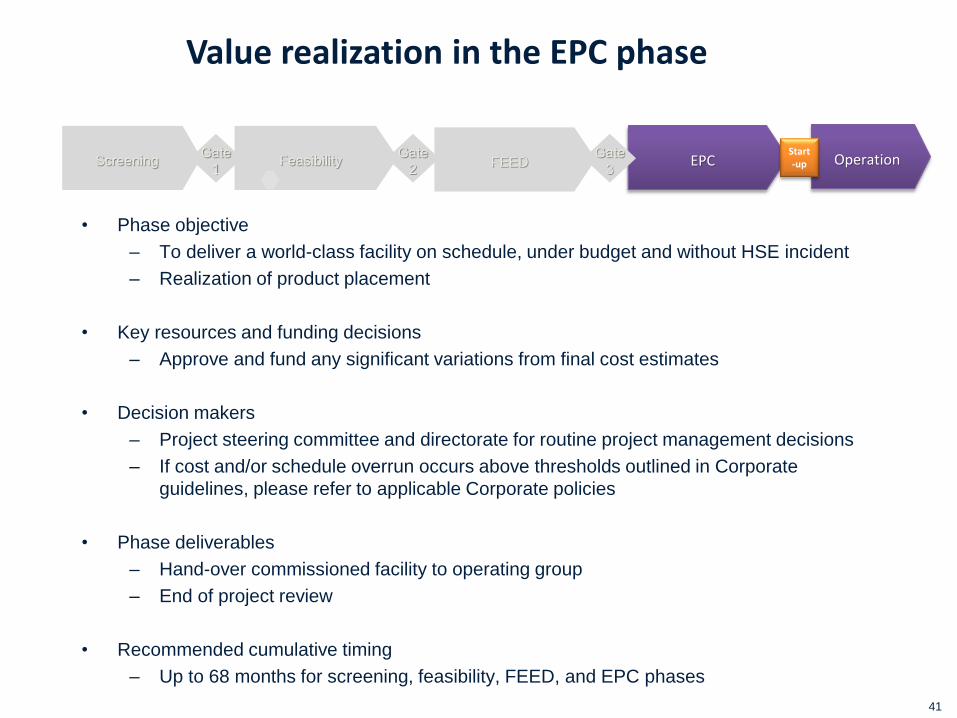

Value realization in the EPC phase

• Phase objective

– To deliver a world-class facility on schedule, under budget and without HSE incident

– Realization of product placement

• Key resources and funding decisions

– Approve and fund any significant variations from final cost estimates

• Decision makers

– Project steering committee and directorate for routine project management decisions

– If cost and/or schedule overrun occurs above thresholds outlined in Corporate

guidelines, please refer to applicable Corporate policies

• Phase deliverables

– Hand-over commissioned facility to operating group

– End of project review

• Recommended cumulative timing

– Up to 68 months for screening, feasibility, FEED, and EPC phases

Overview

Operation Screening Feasibility FEED EPC Start -up

Gate

1

Gate

2

Gate

3

42

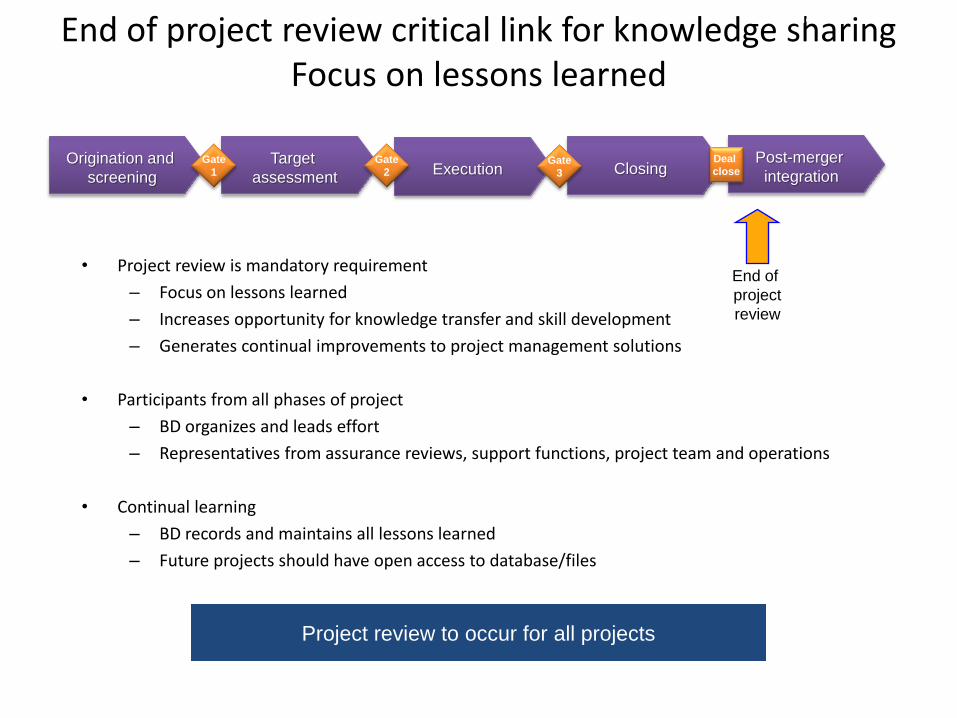

• Project review is mandatory requirement

– Focus on lessons learned

– Increases opportunity for knowledge transfer and

skill development

– Generates continual improvements to project

management solutions

• Participants from all phases of project

– BD organizes and leads effort

– Representatives from assurance reviews, support

functions, project team, and operations

• Continual learning

– BD records and maintains all lessons learned

– Future projects should have open access to

database/files

End of project review critical link for knowledge sharing Focus on lessons learned

Overview of project review

Other gate requirement

Operation Screening Feasibility FEED EPC Start -up

Gate

1

Gate

2

Gate

3

End of

project

review

Project review to occur for all projects, even those

that do not proceed to Operational phase

Mergers & Acquisitions (M&A)

M&A overview M&A process usually completed in condensed timeframe with high level of confidentiality

M&A — overview

Ph

ase

activity

• Post

merger

integration

• Deal closing/signing

• Regulatory

approvals

• Due diligence,

final valuation

• Negotiations

• Structure

transaction

• Documentation

• Economic and

technical

evaluation

• Strategic due

diligence

• Strategic fit

• Generate ideas

• Review inbound

opportunities

• CA signed • Initial bid/non-

binding term-sheet • Bid

Ap

pro

va

l

• Corp. 1st

level • Corp. 1st level

• Shareholder

Board

• Corp. 2nd level

• Corp. 1st level

• Shareholder

Board

Decis

ion

• Asset strategic;

explore options

• Approve

merger/

acquisition

• Approve final

price and

structure – as

required

Post Merger

Integration Origination and

Screening

Target

Assessment Execution Closing

Deal

close

Gate

1

Gate

2

Gate

3

Deals Opportunities

1. As required 2. Corporate Investment Committee: Corporate president, applicable VPs and 2 Shareholders Board board members

Interaction of traditional external advisors varies by phase

Strategy consultants Strategy consultants

Investment bankers

Legal counsel

Auditors

KPI deal team

Tra

ditio

nal co

nstitu

encie

s

an

d r

ole

s

M&A — Org and skills

Post Merger

Integration Origination and

Screening

Target

Assessment Execution Closing

Deal

close

Gate

1

Gate

2

Gate

3

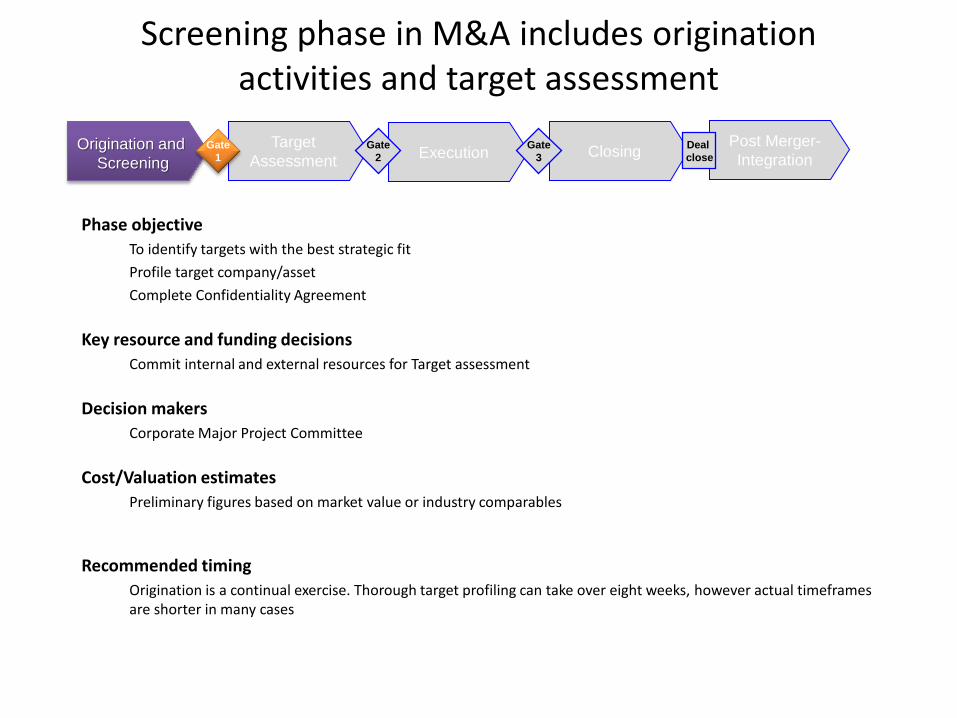

Screening phase in M&A includes origination activities and target assessment

Phase objective

To identify targets with the best strategic fit

Profile target company/asset

Complete Confidentiality Agreement

Key resource and funding decisions

Commit internal and external resources for Target assessment

Decision makers

Corporate Major Project Committee

Cost/Valuation estimates

Preliminary figures based on market value or industry comparables

Recommended timing

Origination is a continual exercise. Thorough target profiling can take over eight weeks, however actual timeframes are shorter in many cases

M&A — overview

Post Merger-

Integration Origination and

Screening

Target

Assessment Execution Closing

Deal

close

Gate

1

Gate

2

Gate

3

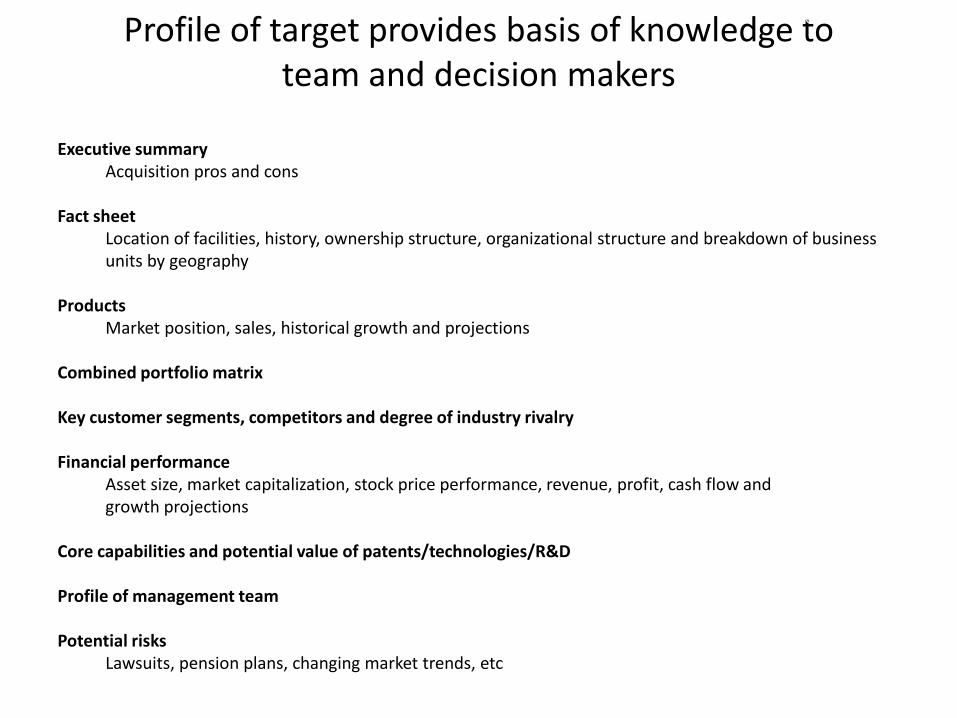

Profile of target provides basis of knowledge to team and decision makers

Executive summary Acquisition pros and cons

Fact sheet

Location of facilities, history, ownership structure, organizational structure and breakdown of business units by geography

Products

Market position, sales, historical growth and projections Combined portfolio matrix Key customer segments, competitors and degree of industry rivalry Financial performance

Asset size, market capitalization, stock price performance, revenue, profit, cash flow and growth projections

Core capabilities and potential value of patents/technologies/R&D Profile of management team Potential risks

Lawsuits, pension plans, changing market trends, etc

M&A — overview

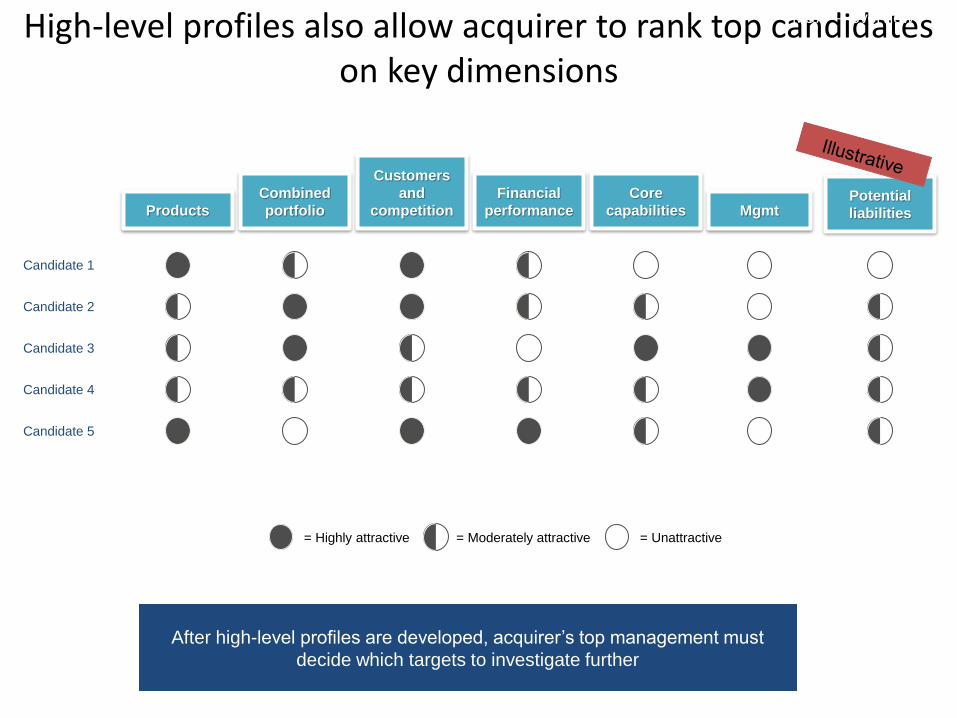

High-level profiles also allow acquirer to rank top candidates on key dimensions

= Unattractive = Highly attractive

After high-level profiles are developed, acquirer’s top management must

decide which targets to investigate further

Candidate 1

Candidate 2

Candidate 3

Candidate 4

Candidate 5

Mgmt

Financial

performance Products

Combined

portfolio

Customers

and

competition

Core

capabilities Potential

liabilities

= Moderately attractive

M&A — overview

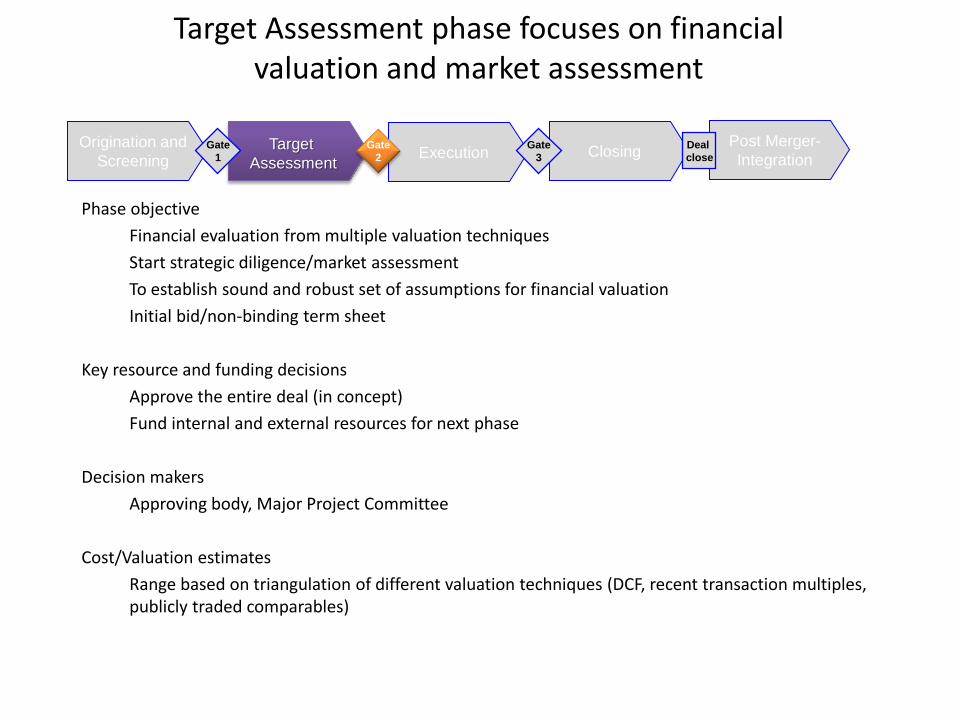

Target Assessment phase focuses on financial valuation and market assessment

Phase objective

Financial evaluation from multiple valuation techniques

Start strategic diligence/market assessment

To establish sound and robust set of assumptions for financial valuation

Initial bid/non-binding term sheet

Key resource and funding decisions

Approve the entire deal (in concept)

Fund internal and external resources for next phase

Decision makers

Approving body, Major Project Committee

Cost/Valuation estimates

Range based on triangulation of different valuation techniques (DCF, recent transaction multiples, publicly traded comparables)

M&A — overview

Post Merger-

Integration Origination and

Screening Target

Assessment Execution Closing

Deal

close

Gate

1

Gate

2

Gate

3

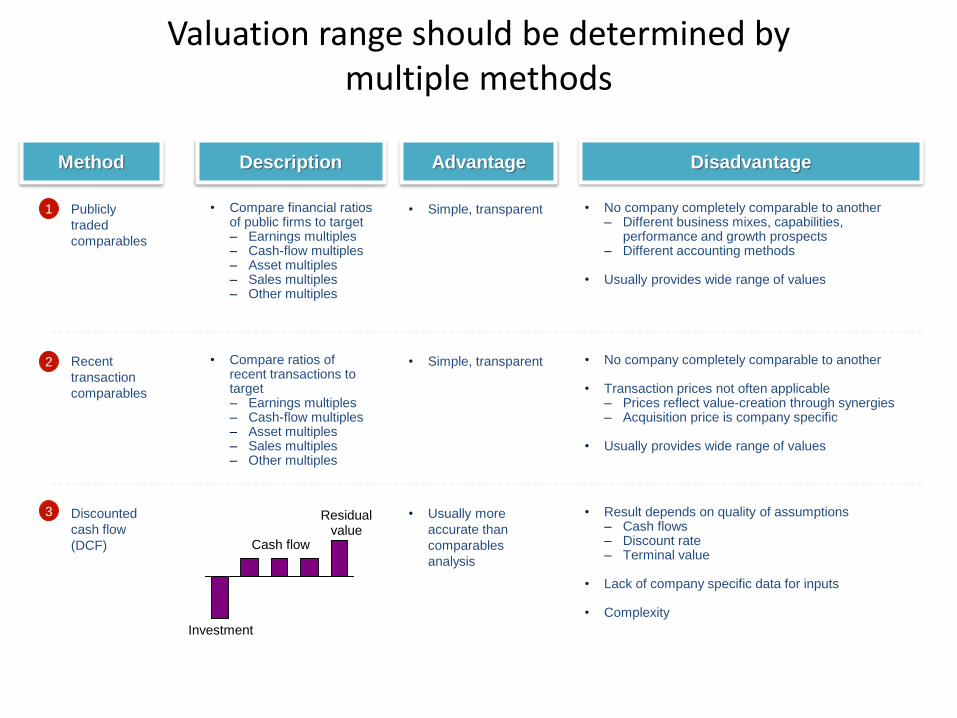

• Result depends on quality of assumptions – Cash flows – Discount rate – Terminal value

• Lack of company specific data for inputs

• Complexity

• No company completely comparable to another

• Transaction prices not often applicable – Prices reflect value-creation through synergies – Acquisition price is company specific

• Usually provides wide range of values

• No company completely comparable to another – Different business mixes, capabilities,

performance and growth prospects – Different accounting methods

• Usually provides wide range of values

• Compare ratios of recent transactions to target – Earnings multiples – Cash-flow multiples – Asset multiples – Sales multiples – Other multiples

• Compare financial ratios of public firms to target – Earnings multiples – Cash-flow multiples – Asset multiples – Sales multiples – Other multiples

Method Description Advantage Disadvantage

Valuation range should be determined by multiple methods

• Publicly

traded

comparables

• Simple, transparent

Cash flow

Investment

Residual value

• Recent

transaction

comparables

• Simple, transparent

• Discounted

cash flow

(DCF)

• Usually more

accurate than

comparables

analysis

1

2

3

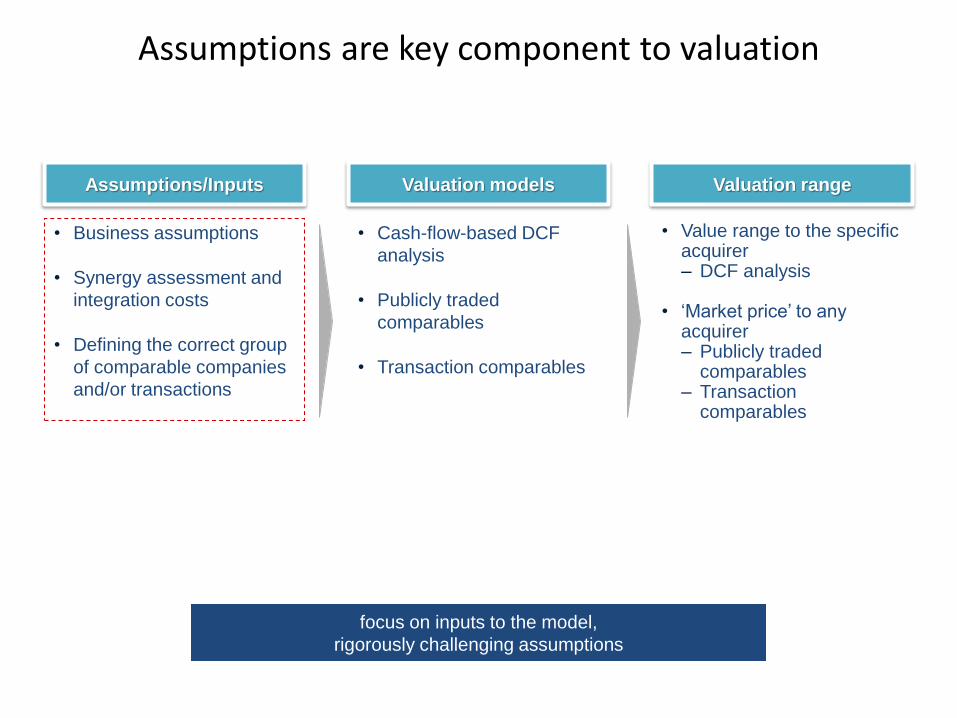

M&A — overview

• Value range to the specific acquirer – DCF analysis

• ‘Market price’ to any acquirer – Publicly traded

comparables – Transaction

comparables

Assumptions/Inputs

• Business assumptions

• Synergy assessment and

integration costs

• Defining the correct group

of comparable companies

and/or transactions

Valuation models

• Cash-flow-based DCF

analysis

• Publicly traded

comparables

• Transaction comparables

Valuation range

Assumptions are key component to valuation

focus on inputs to the model,

rigorously challenging assumptions

M&A — overview

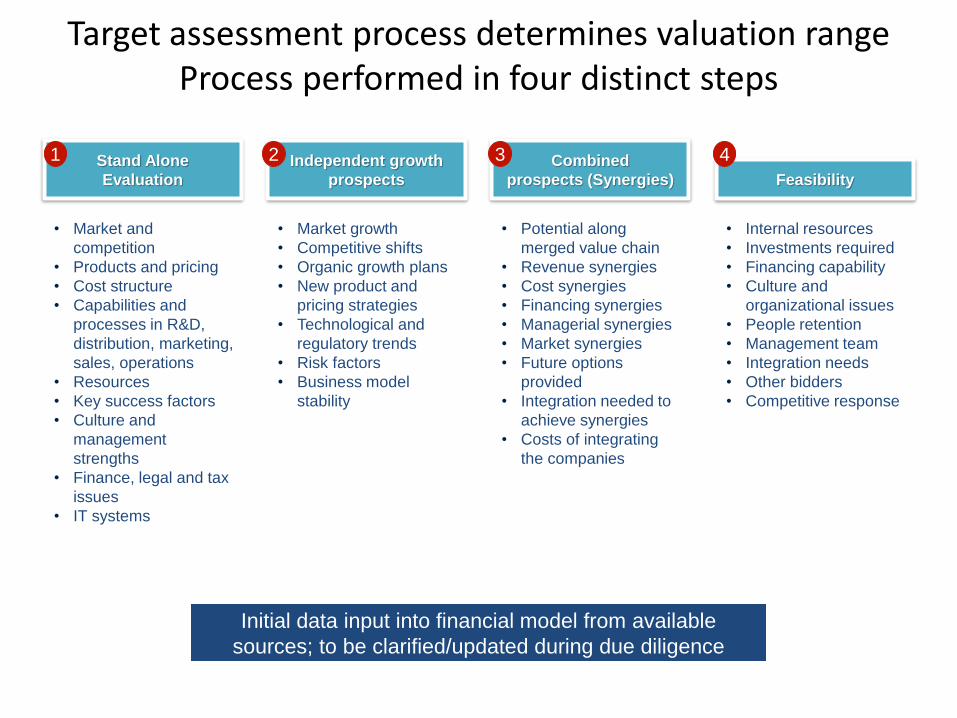

Target assessment process determines valuation range Process performed in four distinct steps

Stand Alone

Evaluation

• Market and

competition

• Products and pricing

• Cost structure

• Capabilities and

processes in R&D,

distribution, marketing,

sales, operations

• Resources

• Key success factors

• Culture and

management

strengths

• Finance, legal and tax

issues

• IT systems

Independent growth

prospects

• Market growth

• Competitive shifts

• Organic growth plans

• New product and

pricing strategies

• Technological and

regulatory trends

• Risk factors

• Business model

stability

Combined

prospects (Synergies)

• Potential along

merged value chain

• Revenue synergies

• Cost synergies

• Financing synergies

• Managerial synergies

• Market synergies

• Future options

provided

• Integration needed to

achieve synergies

• Costs of integrating

the companies

Feasibility

• Internal resources

• Investments required

• Financing capability

• Culture and

organizational issues

• People retention

• Management team

• Integration needs

• Other bidders

• Competitive response

1 2 3 4

Initial data input into financial model from available

sources; to be clarified/updated during due diligence

M&A — overview

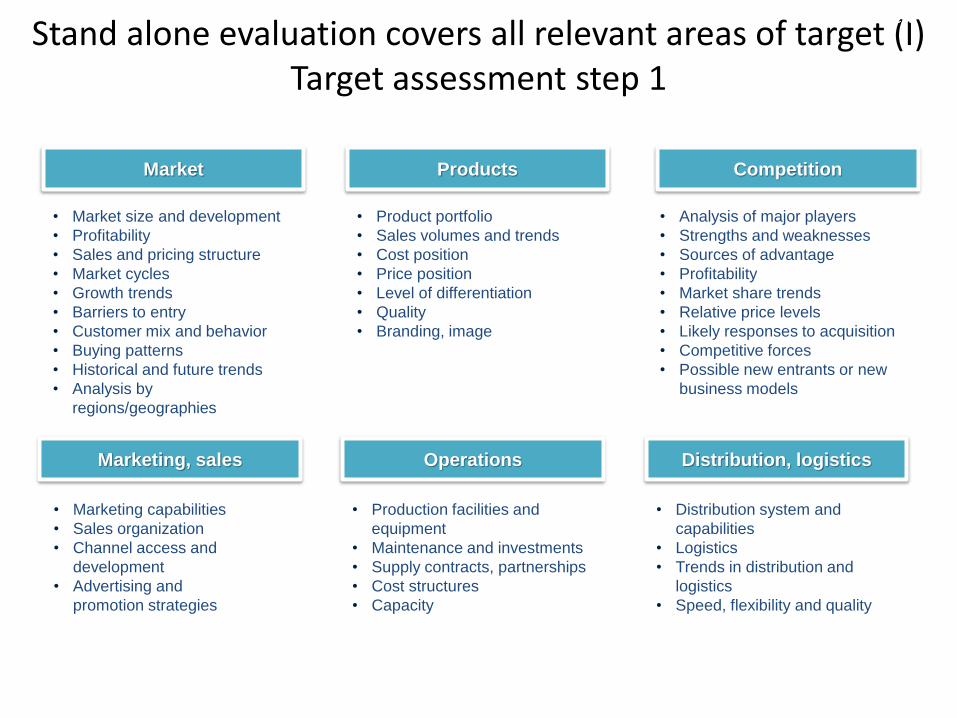

Stand alone evaluation covers all relevant areas of target (I) Target assessment step 1

Market

• Market size and development

• Profitability

• Sales and pricing structure

• Market cycles

• Growth trends

• Barriers to entry

• Customer mix and behavior

• Buying patterns

• Historical and future trends

• Analysis by

regions/geographies

Products

• Product portfolio

• Sales volumes and trends

• Cost position

• Price position

• Level of differentiation

• Quality

• Branding, image

Marketing, sales

• Marketing capabilities

• Sales organization

• Channel access and

development

• Advertising and

promotion strategies

Competition

• Analysis of major players

• Strengths and weaknesses

• Sources of advantage

• Profitability

• Market share trends

• Relative price levels

• Likely responses to acquisition

• Competitive forces

• Possible new entrants or new

business models

Operations

• Production facilities and

equipment

• Maintenance and investments

• Supply contracts, partnerships

• Cost structures

• Capacity

Distribution, logistics

• Distribution system and

capabilities

• Logistics

• Trends in distribution and

logistics

• Speed, flexibility and quality

M&A — overview

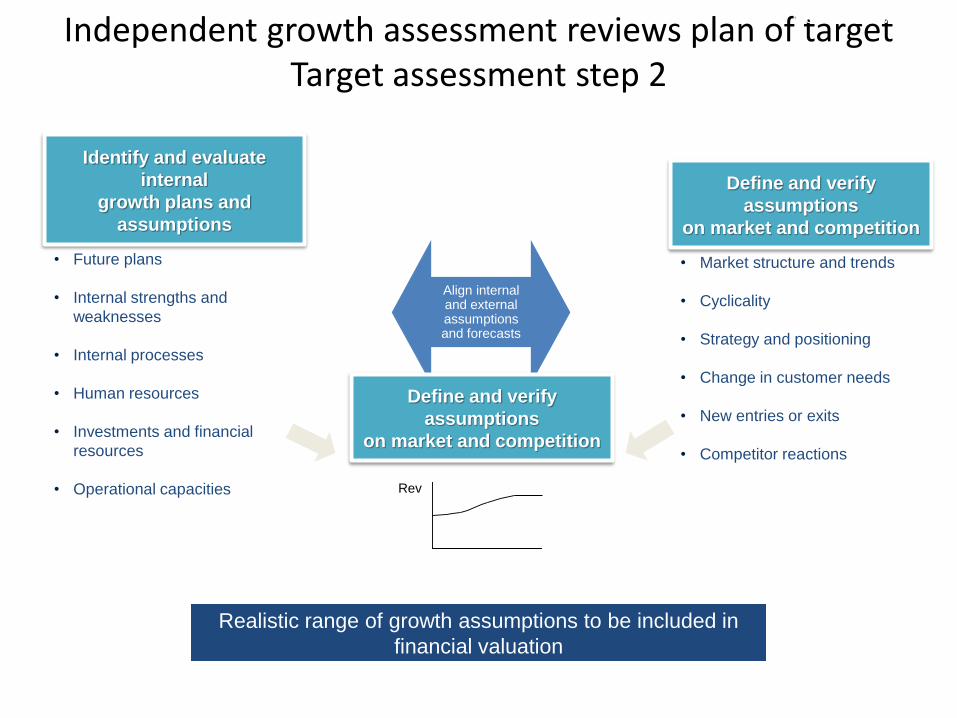

Align internal and external assumptions and forecasts

Independent growth assessment reviews plan of target Target assessment step 2

Identify and evaluate

internal

growth plans and

assumptions

• Future plans

• Internal strengths and

weaknesses

• Internal processes

• Human resources

• Investments and financial

resources

• Operational capacities

Define and verify

assumptions

on market and competition

• Market structure and trends

• Cyclicality

• Strategy and positioning

• Change in customer needs

• New entries or exits

• Competitor reactions

Define and verify

assumptions

on market and competition

Rev

Realistic range of growth assumptions to be included in

financial valuation

M&A — overview

Value creation depends on

ability to realize synergies

Combined prospects values potential synergies Target assessment step 3

Operating synergies

• Potential synergies exist in all

steps of the value chain from

R&D to after-market service

Financial synergies

• Acquisitions may provide tax

shields, improved credit rating,

access to capital, etc

Managerial synergies

• Acquisitions can improve

management practices

• Can provide additional talented

managers

Market-evaluation

reassessment

• Market may view the acquirer

as a survivor in a consolidating

industry

Realistic expectations of synergies should be included in

financial valuation

M&A — Overview

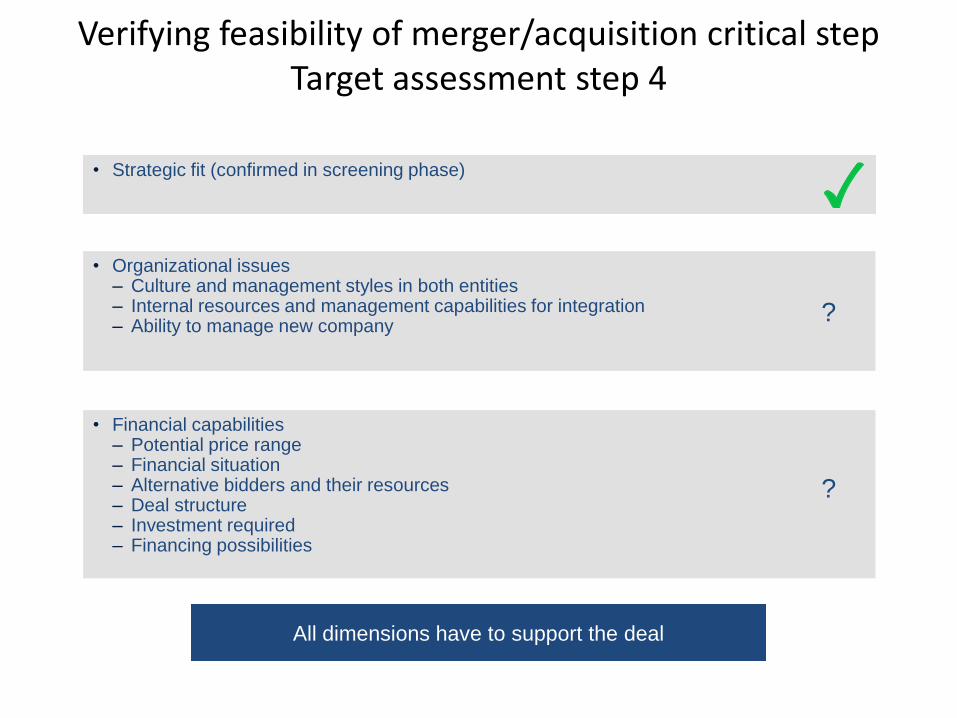

Source: BCG experience; adaptation of Chakravarty in Business Today, March 1998

• Financial capabilities – Potential price range – Financial situation – Alternative bidders and their resources – Deal structure – Investment required – Financing possibilities

• Organizational issues – Culture and management styles in both entities – Internal resources and management capabilities for integration – Ability to manage new company

• Strategic fit (confirmed in screening phase)

?

?

M&A — overview

All dimensions have to support the deal

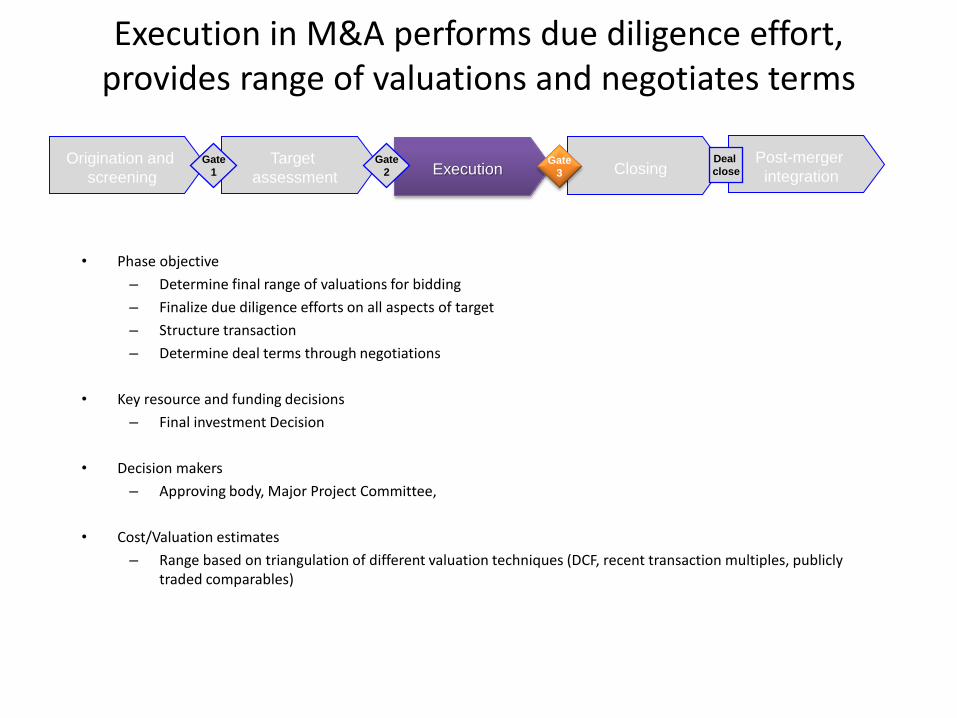

Verifying feasibility of merger/acquisition critical step Target assessment step 4

• Phase objective

– Determine final range of valuations for bidding

– Finalize due diligence efforts on all aspects of target

– Structure transaction

– Determine deal terms through negotiations

• Key resource and funding decisions

– Final investment Decision

• Decision makers

– Approving body, Major Project Committee,

• Cost/Valuation estimates

– Range based on triangulation of different valuation techniques (DCF, recent transaction multiples, publicly traded comparables)

Execution in M&A performs due diligence effort, provides range of valuations and negotiates terms

M&A — overview

Post-merger

integration Origination and

screening

Target

assessment Execution Closing

Deal

close Gate

1

Gate

2 Gate

3

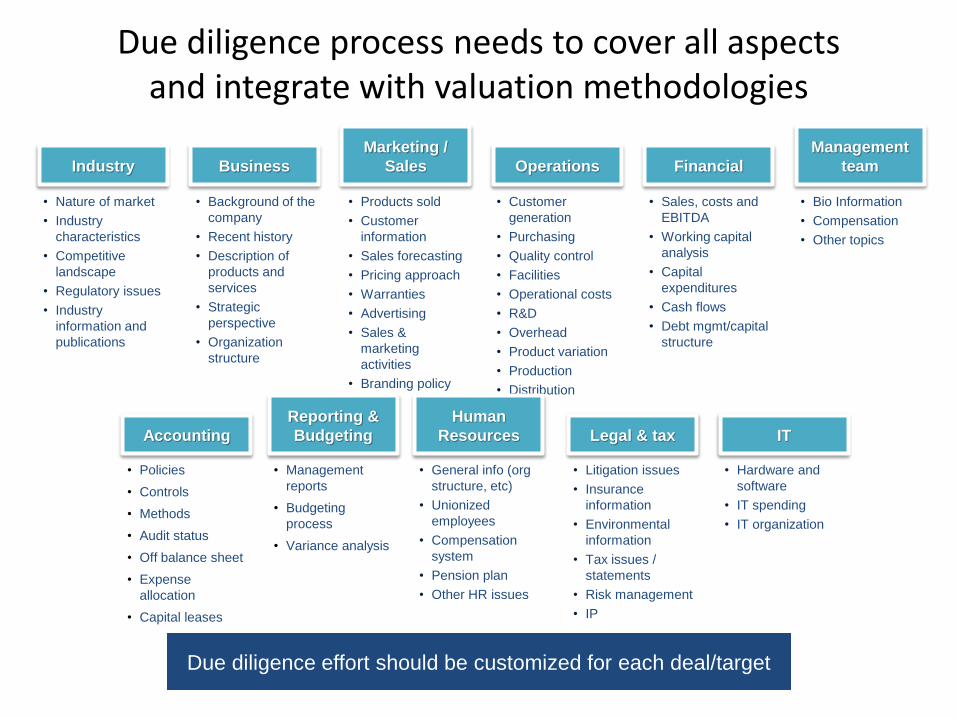

Due diligence process needs to cover all aspects and integrate with valuation methodologies

• Nature of market

• Industry

characteristics

• Competitive

landscape

• Regulatory issues

• Industry

information and

publications

• Background of the

company

• Recent history

• Description of

products and

services

• Strategic

perspective

• Organization

structure

• Products sold

• Customer

information

• Sales forecasting

• Pricing approach

• Warranties

• Advertising

• Sales &

marketing

activities

• Branding policy

• Customer

generation

• Purchasing

• Quality control

• Facilities

• Operational costs

• R&D

• Overhead

• Product variation

• Production

• Distribution

• Sales, costs and

EBITDA

• Working capital

analysis

• Capital

expenditures

• Cash flows

• Debt mgmt/capital

structure

• Bio Information

• Compensation

• Other topics

• Policies

• Controls

• Methods

• Audit status

• Off balance sheet

• Expense

allocation

• Capital leases

• Management

reports

• Budgeting

process

• Variance analysis

• General info (org

structure, etc)

• Unionized

employees

• Compensation

system

• Pension plan

• Other HR issues

• Litigation issues

• Insurance

information

• Environmental

information

• Tax issues /

statements

• Risk management

• IP

• Hardware and

software

• IT spending

• IT organization

Industry Business

Marketing /

Sales Operations Financial

Management

team

Accounting

Reporting &

Budgeting

Human

Resources Legal & tax IT

Due diligence effort should be customized for each deal/target

M&A — overview

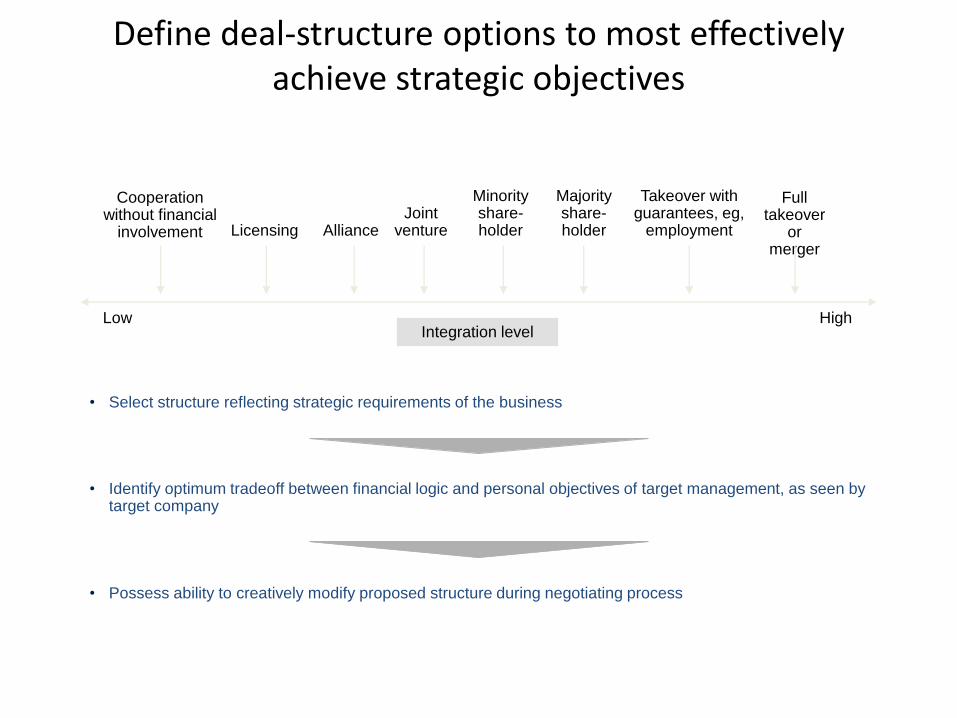

Minority share-holder

• Select structure reflecting strategic requirements of the business

High

Full takeover

or merger

Takeover with guarantees, eg,

employment

Majority share-holder

Joint venture Licensing

Cooperation without financial

involvement

Integration level Low

Alliance

Define deal-structure options to most effectively achieve strategic objectives

• Identify optimum tradeoff between financial logic and personal objectives of target management, as seen by target company

• Possess ability to creatively modify proposed structure during negotiating process

M&A — overview

Negotiation preparation key to successful transaction

• Price matters

– For the acquirer, value can be destroyed despite sound business logic

– For the seller, returns must be maximized for its owners

• Deal structure can affect the economics

– For the acquirer, there is a need for new information, reassessment, renegotiation

– For the seller, post-sale risk can be minimized by the terms of the deal

• Better information is acquired about the target and buyer

– Negotiations should be viewed as a learning process — one can always walk away

• New management organization starts to form and the organizational tone is set

– For the acquirer, the key is to get and keep the right people post-merger

– Need to set a good tone for post-merger success

Objective is to create the optimal agreement with

common goals and aligned incentives

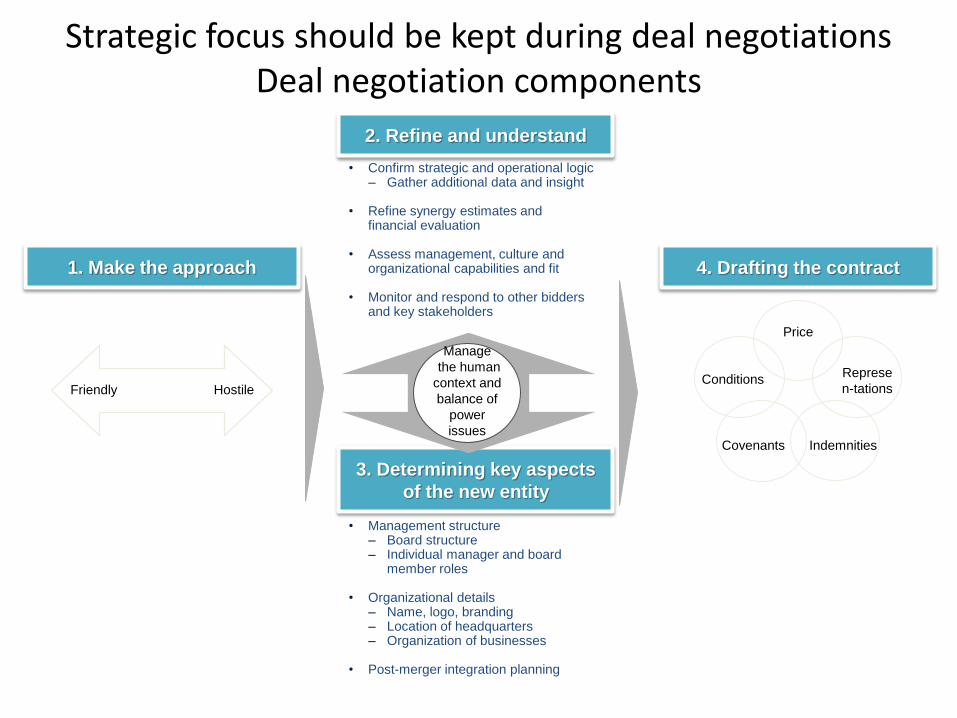

M&A — overview

• Management structure – Board structure – Individual manager and board

member roles

• Organizational details – Name, logo, branding – Location of headquarters – Organization of businesses

• Post-merger integration planning

• Confirm strategic and operational logic – Gather additional data and insight

• Refine synergy estimates and financial evaluation

• Assess management, culture and organizational capabilities and fit

• Monitor and respond to other bidders and key stakeholders

3. Determining key aspects

of the new entity

4. Drafting the contract

Represe

n-tations

Indemnities

Conditions

Covenants

Price

Friendly Hostile

1. Make the approach

2. Refine and understand

Manage

the human

context and

balance of

power

issues

Strategic focus should be kept during deal negotiations Deal negotiation components

M&A — overview

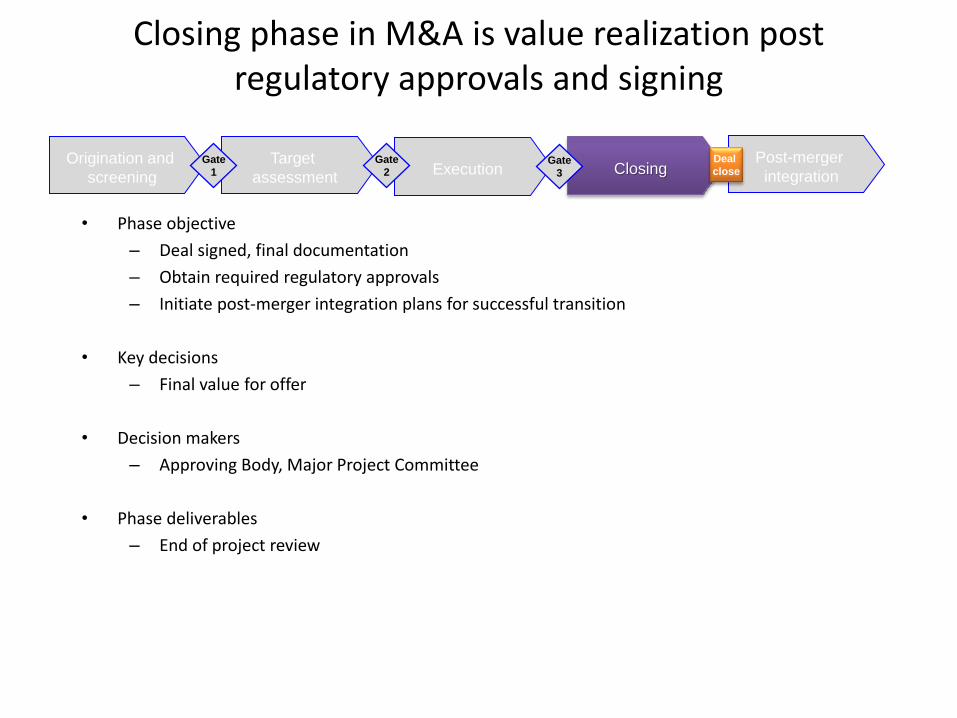

Closing phase in M&A is value realization post regulatory approvals and signing

• Phase objective

– Deal signed, final documentation

– Obtain required regulatory approvals

– Initiate post-merger integration plans for successful transition

• Key decisions

– Final value for offer

• Decision makers

– Approving Body, Major Project Committee

• Phase deliverables

– End of project review

M&A — overview

Post-merger

integration Origination and

screening

Target

assessment Execution Closing

Deal

close Gate

1

Gate

2 Gate

3

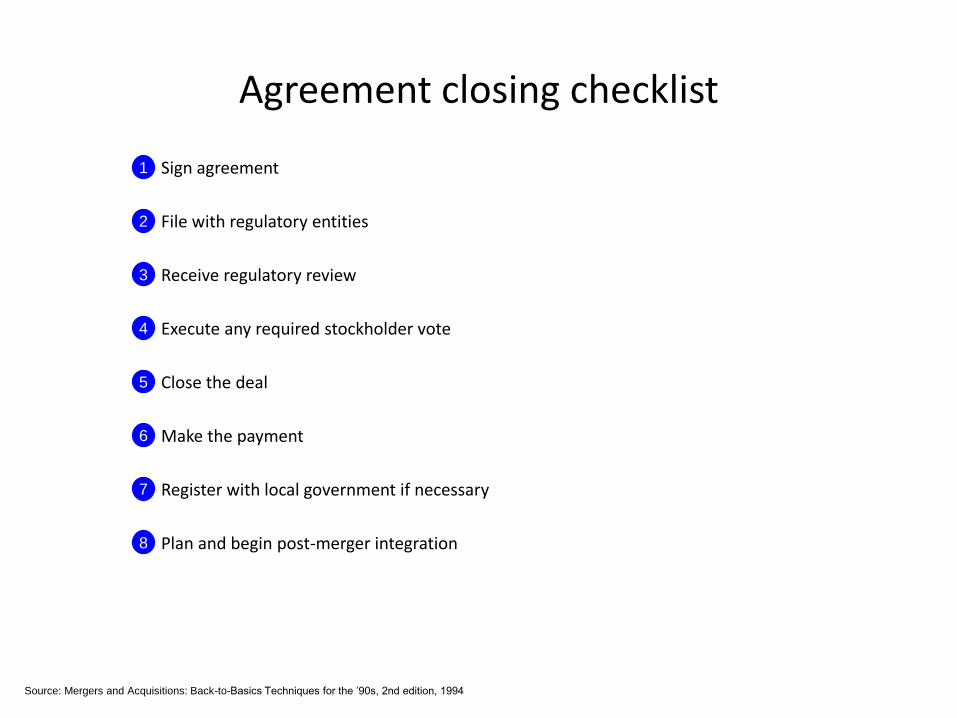

Agreement closing checklist

• Sign agreement

• File with regulatory entities

• Receive regulatory review

• Execute any required stockholder vote

• Close the deal

• Make the payment

• Register with local government if necessary

• Plan and begin post-merger integration

Source: Mergers and Acquisitions: Back-to-Basics Techniques for the ’90s, 2nd edition, 1994

M&A — checklist

1

2

3

4

5

6

7

8

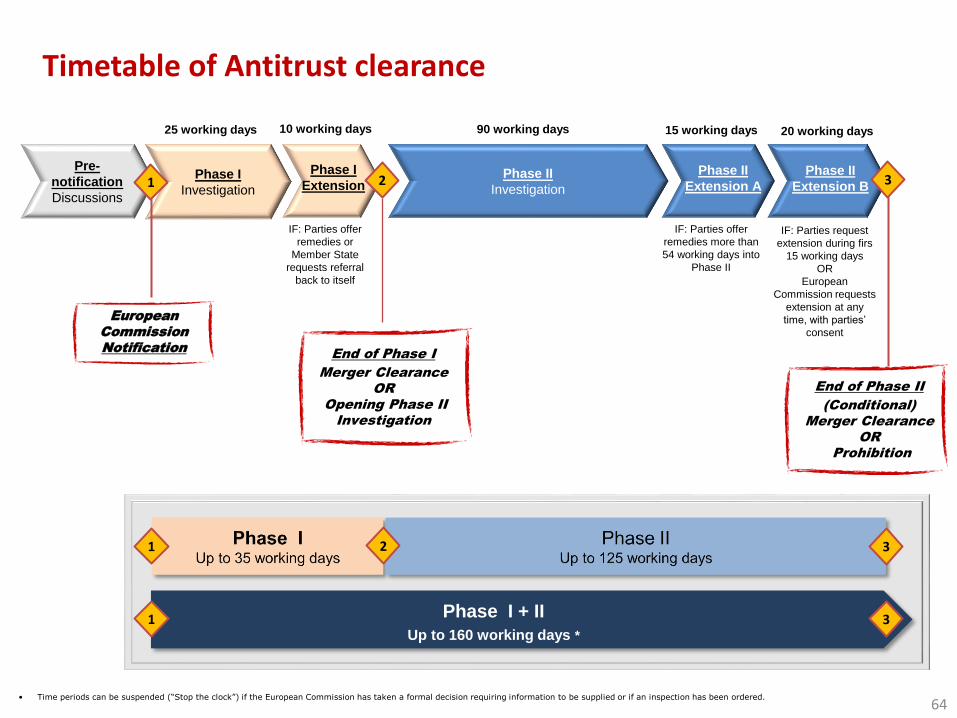

Pre-

notification

Discussions

European

Commission

Notification

Phase II

Investigation

64

25 working days

Timetable of Antitrust clearance

IF: Parties offer

remedies or

Member State

requests referral

back to itself

10 working days

End of Phase I

Merger Clearance

OR

Opening Phase II

Investigation

90 working days 15 working days

Phase I

Investigation 2

Phase I

Extension Phase II

Extension A

IF: Parties offer

remedies more than

54 working days into

Phase II

Phase II

Extension B

20 working days

IF: Parties request

extension during firs

15 working days

OR

European

Commission requests

extension at any

time, with parties’

consent

End of Phase II

(Conditional)

Merger Clearance

OR

Prohibition

3

Phase I + II

Up to 160 working days *

1

• Time periods can be suspended (“Stop the clock”) if the European Commission has taken a formal decision requiring information to be supplied or if an inspection has been ordered.

1 2 3

1 3

• Project review is mandatory requirement

– Focus on lessons learned

– Increases opportunity for knowledge transfer and skill development

– Generates continual improvements to project management solutions

• Participants from all phases of project

– BD organizes and leads effort

– Representatives from assurance reviews, support functions, project team and operations

• Continual learning

– BD records and maintains all lessons learned

– Future projects should have open access to database/files

End of project review critical link for knowledge sharing Focus on lessons learned

End of

project

review

M&A — overview

Post-merger

integration Origination and

screening

Target

assessment Execution Closing

Deal

close Gate

1

Gate

2 Gate

3

Project review to occur for all projects

Divestments

Divestment process overview

• Due diligence and Q&A

• Teaser and

information

memo

• Deal

closing,

signing

• Regulatory

approvals

• Strategic fit

and rationale

• Valuation and

impact

• Timing

• Best owners /

transaction

models

• Mgmt

presentation

• Site visits,

expert

meetings

• Negotiations

Ph

ase a

cti

vit

y

Decis

ion

A

pp

rov

al • Corporate

• Corporate 1st lvl

• Shareholder board

• Corporate 2nd lvl

• Asset not

strategic;

explore options

• Approve

divestment

• Approve final

divestment

price

Divestment — overview

• Evaluate

initial bids

• Qualify short-

list of bidders

• CA signed

and non-

binding offers

rec’d

• Bids

rec’d

• Data

room

Divestment process

'Unlocking the value'

Divestment preparation

'Creating the case'

Marketing

and bid

evaluation

Divestment

decision

Divestment

strategy

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

1

Gate

4

Gate

3

Gate

2

• Corporate 1st lvl

• Shareholder board

• Corporate 2nd lvl

• Corporate 1st lvl

• Shareholder board

• Corporate 2nd lvl

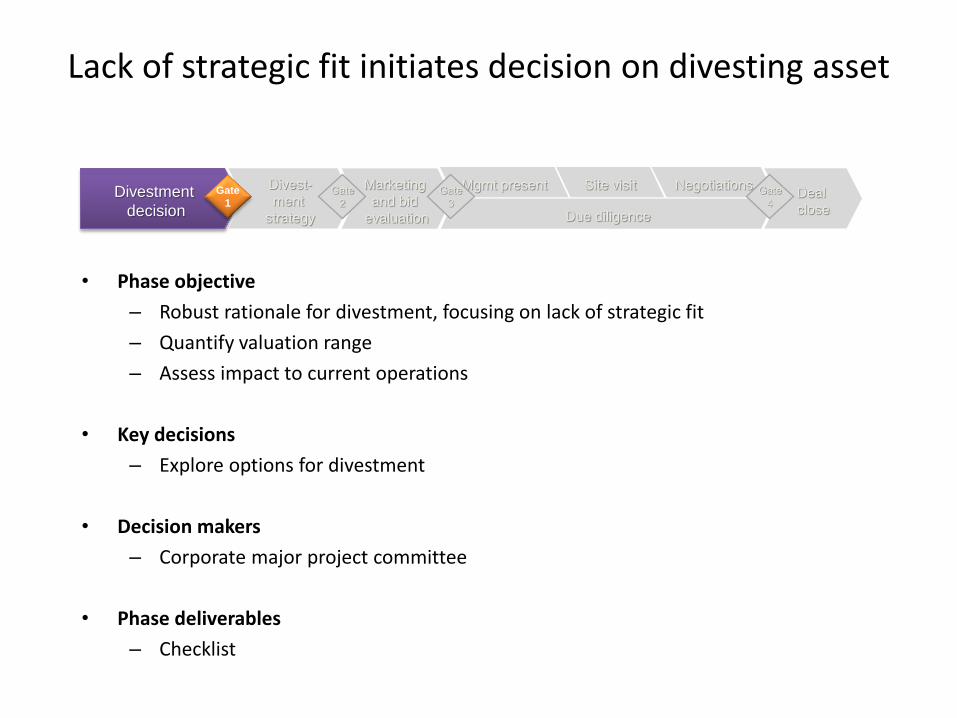

• Phase objective

– Robust rationale for divestment, focusing on lack of strategic fit

– Quantify valuation range

– Assess impact to current operations

• Key decisions

– Explore options for divestment

• Decision makers

– Corporate major project committee

• Phase deliverables

– Checklist

Lack of strategic fit initiates decision on divesting asset

Marketing

and bid

evaluation

Divestment

decision

Divest-

ment

strategy

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

1

Gate

4

Gate

3

Gate

2

Divestment — overview

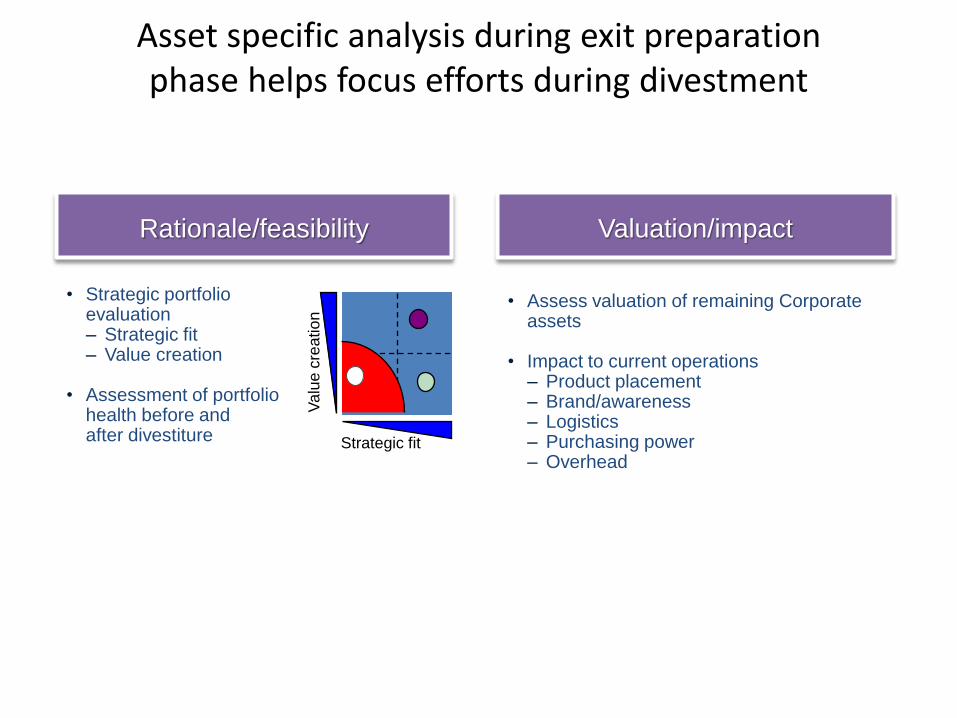

• Assess valuation of remaining Corporate assets

• Impact to current operations – Product placement – Brand/awareness – Logistics – Purchasing power – Overhead

• Strategic portfolio evaluation – Strategic fit – Value creation

• Assessment of portfolio health before and after divestiture

Asset specific analysis during exit preparation phase helps focus efforts during divestment

Rationale/feasibility Valuation/impact

Va

lue

cre

atio

n

Strategic fit

Divestment — overview

• Phase objective

– Robust rationale for divestment, focusing on lack of strategic fit

– Determine best timing for divestment

– Short-list potential buyers; estimate values potential buyers willing to pay

• Key decisions

– Approve divestment

• Decision makers

– Corporate Major Project Committee, Shareholders, Corporate 2nd level

• Phase deliverables

– Checklist

Divestment strategy formulates best timing and potential buyers

Divestment — overview

Marketing

and bid

evaluation

Divestment

decision

Divest-

ment

strategy

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

1

Gate

4

Gate

3

Gate

2

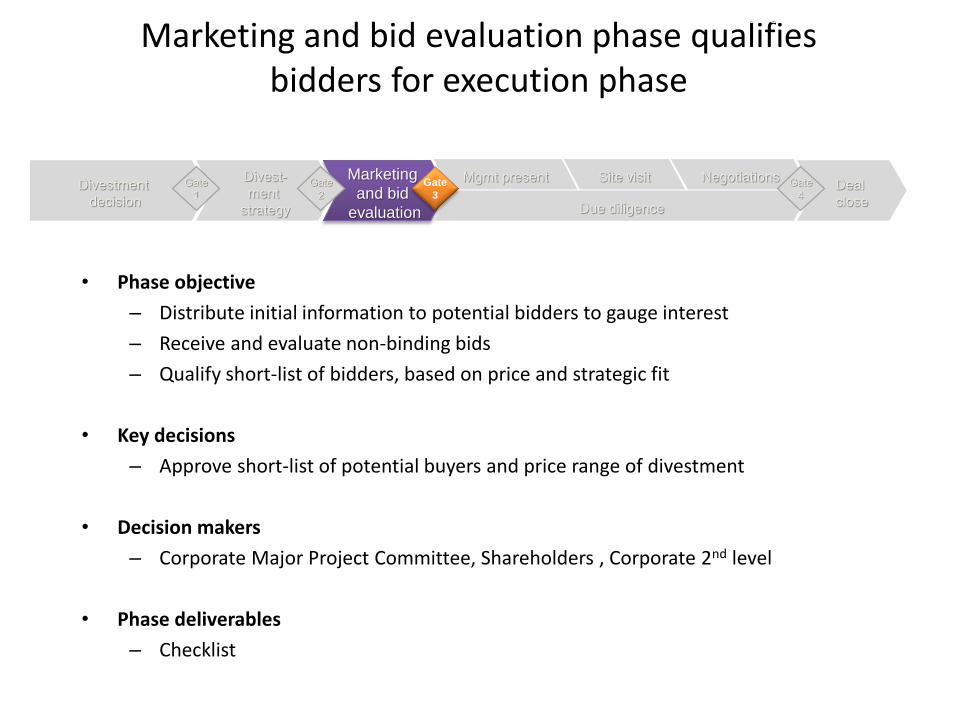

• Phase objective

– Distribute initial information to potential bidders to gauge interest

– Receive and evaluate non-binding bids

– Qualify short-list of bidders, based on price and strategic fit

• Key decisions

– Approve short-list of potential buyers and price range of divestment

• Decision makers

– Corporate Major Project Committee, Shareholders , Corporate 2nd level

• Phase deliverables

– Checklist

Marketing and bid evaluation phase qualifies bidders for execution phase

Divestment — overview

Marketing

and bid

evaluation

Divestment

decision

Divest-

ment

strategy

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

4

Gate

3

Gate

2

Gate

1

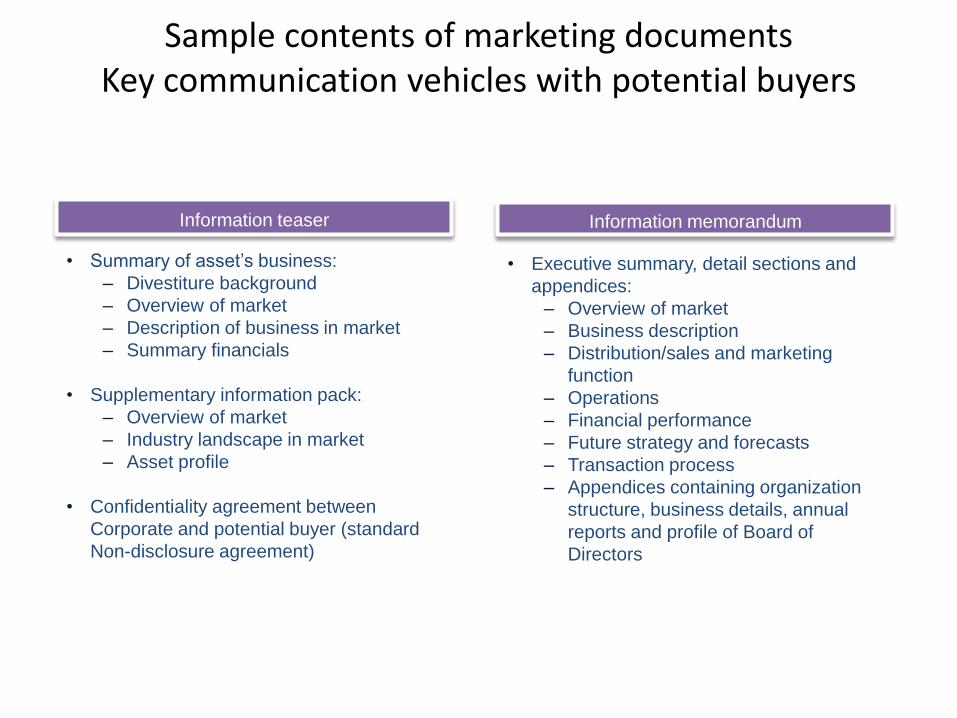

• Confidentiality and indemnity agreements between

– Client and potential buyers

– External advisors and potential buyers

• Describes the 'opportunity' (does not include reserved information)

– Business summary

– Divestiture background

– Key financials

Investor marketing material must clearly articulate strategic rationale for investment case

Information teaser

Information

Memorandum (IM)

Non-disclosure

agreements

Divestment — overview

• Comprehensive document providing

– Overview of market

– Detailed business description, detailed financials including forecasts

– Future outlook and business strategy

– Transaction process

• Only numbered hard copies of Information Memorandum to be released

for confidentiality purposes

• Executive summary, detail sections and

appendices:

– Overview of market

– Business description

– Distribution/sales and marketing

function

– Operations

– Financial performance

– Future strategy and forecasts

– Transaction process

– Appendices containing organization

structure, business details, annual

reports and profile of Board of

Directors

• Summary of asset’s business:

– Divestiture background

– Overview of market

– Description of business in market

– Summary financials

• Supplementary information pack:

– Overview of market

– Industry landscape in market

– Asset profile

• Confidentiality agreement between

Corporate and potential buyer (standard

Non-disclosure agreement)

Sample contents of marketing documents Key communication vehicles with potential buyers

Divestment — overview

Information teaser Information memorandum

Divestment execution

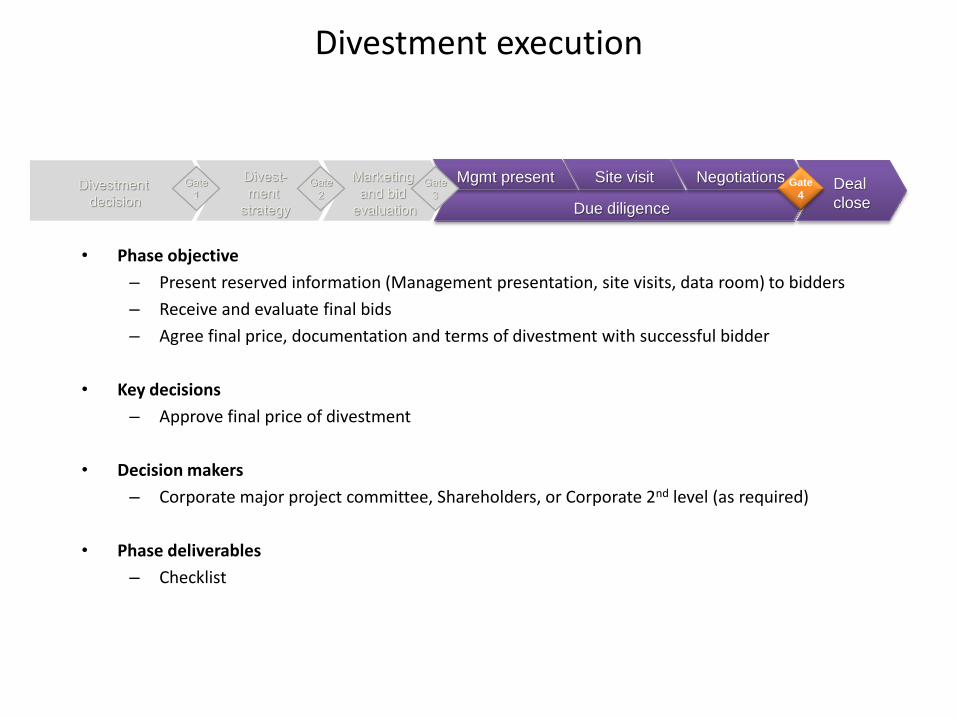

• Phase objective

– Present reserved information (Management presentation, site visits, data room) to bidders

– Receive and evaluate final bids

– Agree final price, documentation and terms of divestment with successful bidder

• Key decisions

– Approve final price of divestment

• Decision makers

– Corporate major project committee, Shareholders, or Corporate 2nd level (as required)

• Phase deliverables

– Checklist

Divestment — overview

Marketing

and bid

evaluation

Divestment

decision

Divest-

ment

strategy

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

4

Gate

3

Gate

2

Gate

1

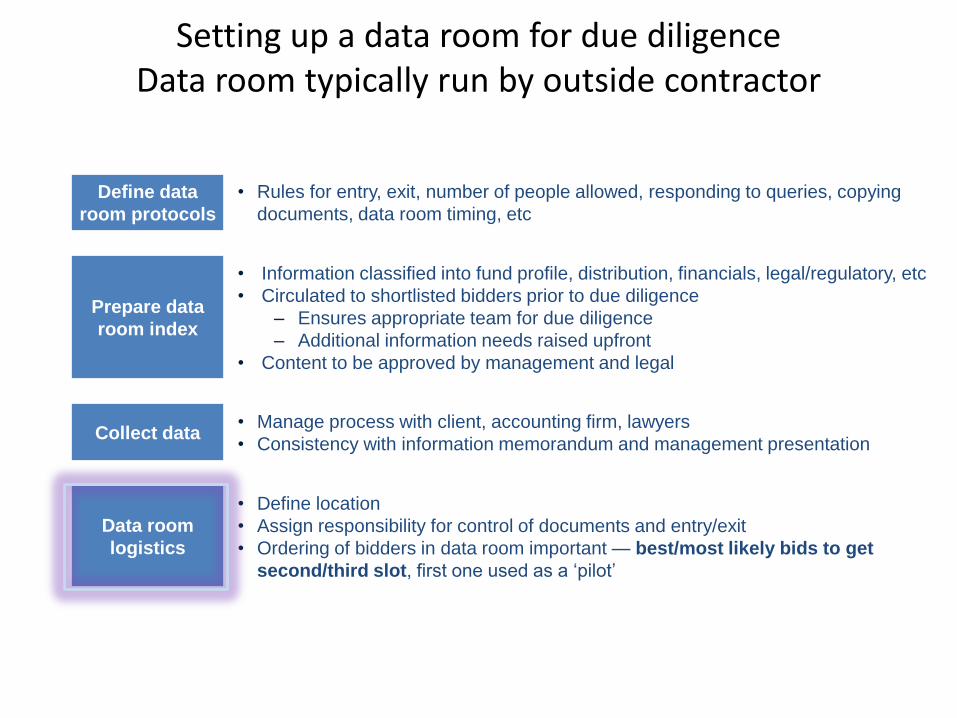

• Information classified into fund profile, distribution, financials, legal/regulatory, etc

• Circulated to shortlisted bidders prior to due diligence

– Ensures appropriate team for due diligence

– Additional information needs raised upfront

• Content to be approved by management and legal

Setting up a data room for due diligence Data room typically run by outside contractor

Define data

room protocols

• Rules for entry, exit, number of people allowed, responding to queries, copying

documents, data room timing, etc

Prepare data

room index

Collect data • Manage process with client, accounting firm, lawyers

• Consistency with information memorandum and management presentation

Data room

logistics

• Define location

• Assign responsibility for control of documents and entry/exit

• Ordering of bidders in data room important — best/most likely bids to get

second/third slot, first one used as a ‘pilot’

Strategic Redirection

76

Marketing

and bid

evaluation

Feasibility Definition Implementation

Operation Screening Feasibility FEED EPC Start

-up

Divestment

decision

Divestment

strategy

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

4

Post- merger

integration

Origination and

screening Business plan Execution

Closing, reg

approvals

Deal

close

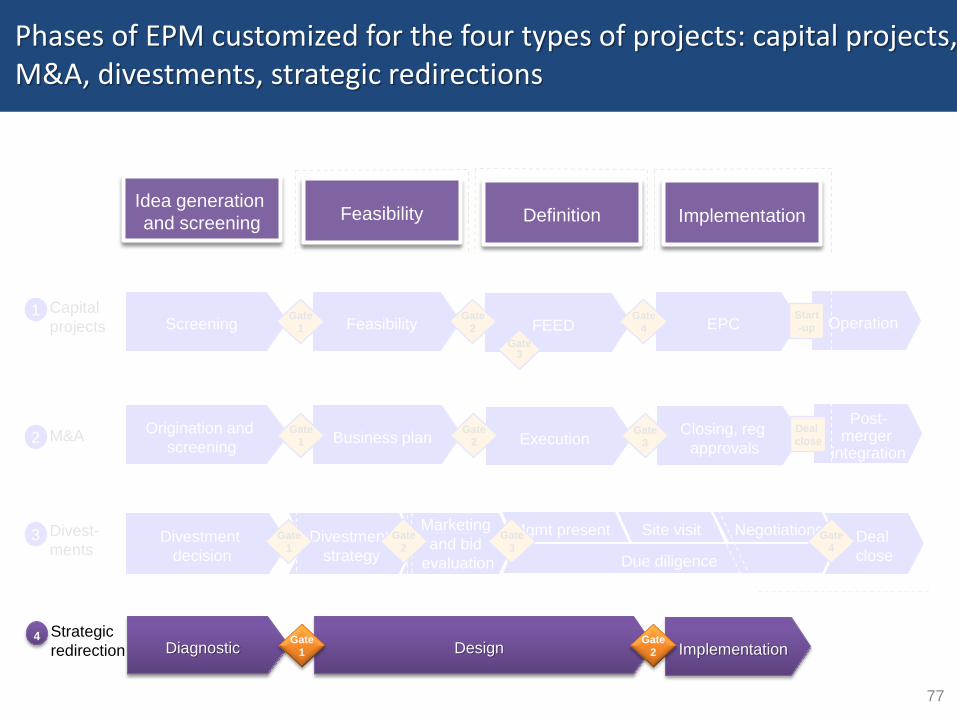

Capital

projects

M&A

Divest-

ments

Idea generation

and screening

1

2

3

Gate

1

Gate

2 Gate

3

Gate

1

Gate

3

Gate

2

Gate

1

Gate

2

Gate

4

Gate 3

Diagnostic Design Implementation Strategic

redirection 4 Gate

1

Gate

2

77

Phases of EPM customized for the four types of projects: capital projects, M&A, divestments, strategic redirections

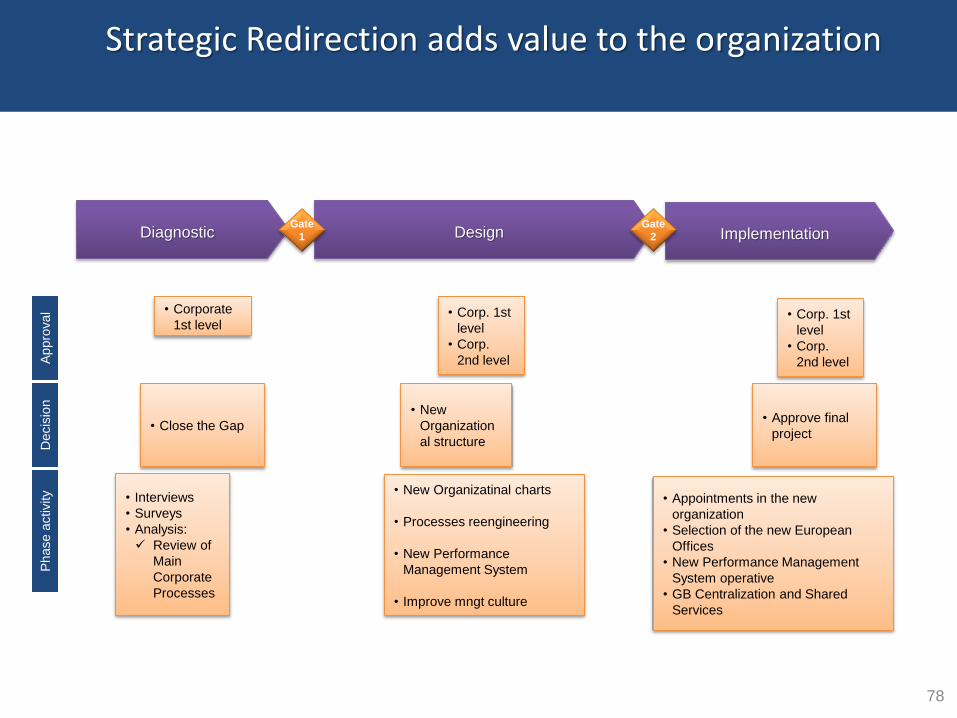

Strategic Redirection adds value to the organization

• Interviews

• Surveys

• Analysis:

Review of

Main

Corporate

Processes

• New Organizatinal charts

• Processes reengineering

• New Performance

Management System

• Improve mngt culture

Phase a

ctivity

Decis

ion

A

ppro

val • Corporate

1st level • Corp. 1st

level

• Corp.

2nd level

• Close the Gap • Approve final

project

• New

Organization

al structure

Diagnostic Design Implementation Gate

1

Gate

2

• Corp. 1st

level

• Corp.

2nd level

• Appointments in the new

organization

• Selection of the new European

Offices

• New Performance Management

System operative

• GB Centralization and Shared

Services

78

Wo

rkin

g D

raft - L

ast M

od

ified

31

/12

/20

10

08

:20

:35

P

rinte

d

|

Corporate Restructuring: 3 Step approach

79

Diagnostic Implementation

Interviews:

- 40 in the OUs

- 20 in Corporate

Surveys: - 185 Respondents

Analysis: - Review of Main Corporate

Processes

Design

New organizational

Chart

Critical Processes

re-engineered

New Performance

Management System

Appointments in the new

organization

Selection of the new CC

Offices

New Process Manuals

issued

New Performance

Management System

operative

Wo

rkin

g D

raft - L

ast M

od

ified

31

/12

/20

10

08

:20

:35

P

rinte

d

| 80

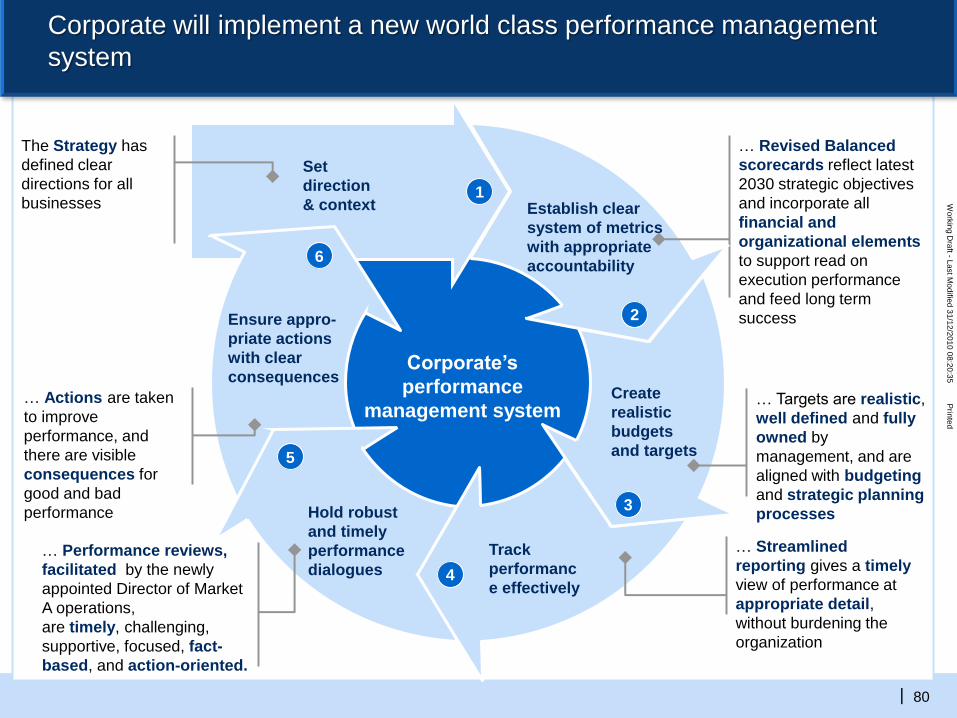

The Strategy has

defined clear

directions for all

businesses

… Performance reviews,

facilitated by the newly

appointed Director of Market

A operations,

are timely, challenging,

supportive, focused, fact-

based, and action-oriented.

… Actions are taken

to improve

performance, and

there are visible

consequences for

good and bad

performance

… Revised Balanced

scorecards reflect latest

2030 strategic objectives

and incorporate all

financial and

organizational elements

to support read on

execution performance

and feed long term

success

Corporate’s

performance

management system

Set

direction

& context 1

Establish clear

system of metrics

with appropriate

accountability

Create

realistic

budgets

and targets

Track

performanc

e effectively

2

3

4

5

6

Ensure appro-

priate actions

with clear

consequences

Hold robust

and timely

performance

dialogues

… Targets are realistic,

well defined and fully

owned by

management, and are

aligned with budgeting

and strategic planning

processes

… Streamlined

reporting gives a timely

view of performance at

appropriate detail,

without burdening the

organization

Corporate will implement a new world class performance management

system

![INCREMENTO DELL’EFFICIENZA DI CONVERSIONE … · quota minima di trasformazione del potere calorifico dei rifiuti in energia utile […] ”. ... è stato effettuato un calcolo](https://img.pdfslide.tips/doc/110x75/5c6aa28709d3f20f298cdf78/incremento-dellefficienza-di-conversione-quota-minima-di-trasformazione-del.jpg)