Embed Size (px)

Citation preview

Customer Experience Management Transformation 5th November 2014

[European Utility Week – Disclosure] Additional disclosure with written approval from HCL only

2

Introductions / Contact

Kris Hillstrand SVP – Technology and Operations [email protected] 617.818.0392 (m/txt)

3

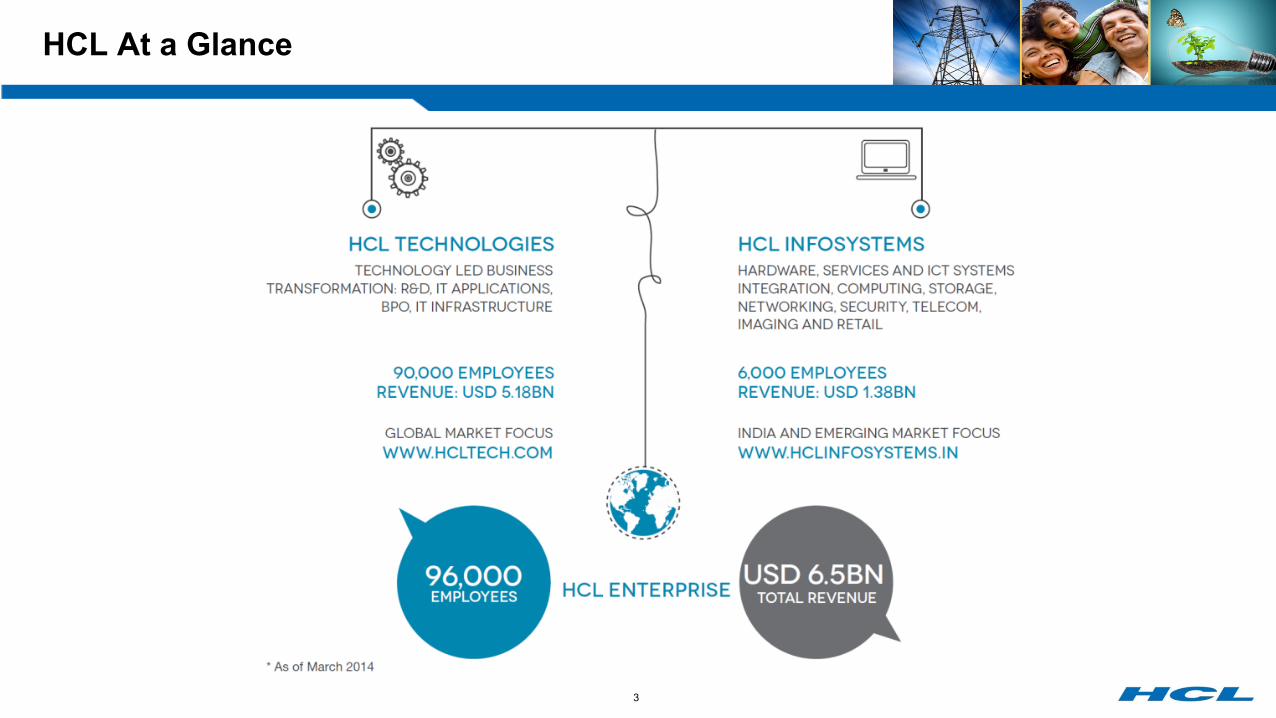

HCL At a Glance

4

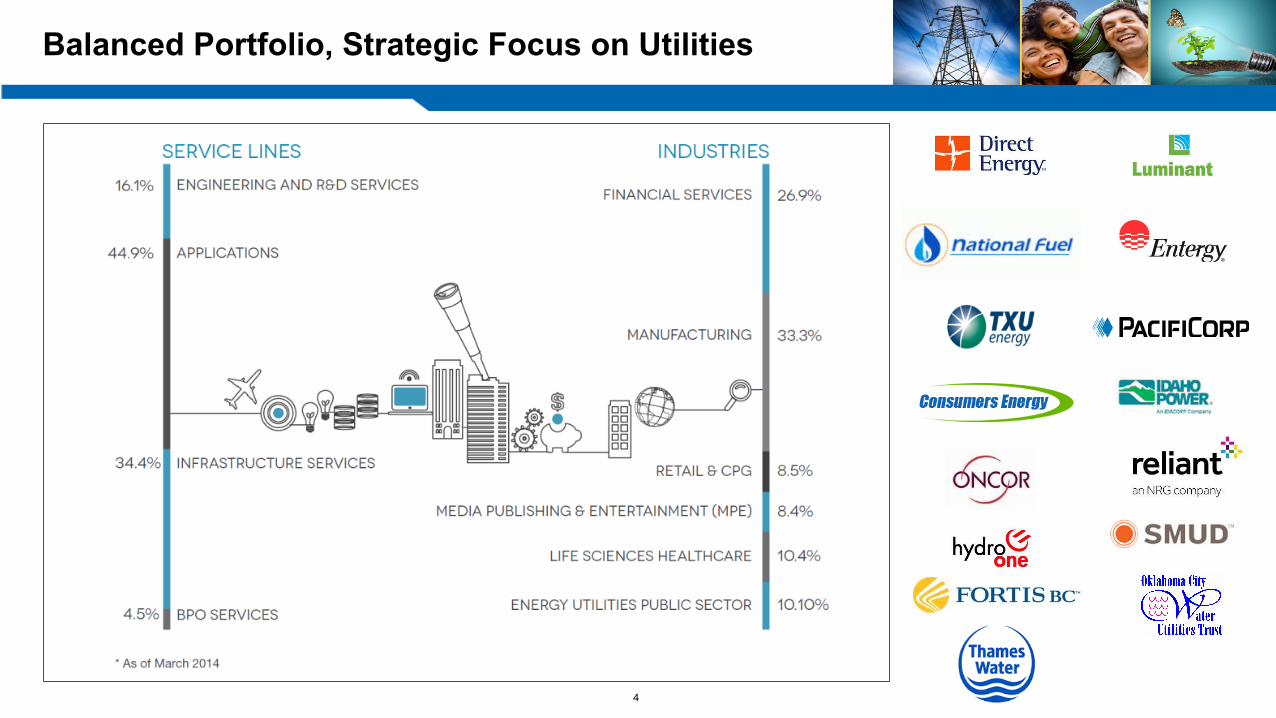

Balanced Portfolio, Strategic Focus on Utilities

5

Agenda

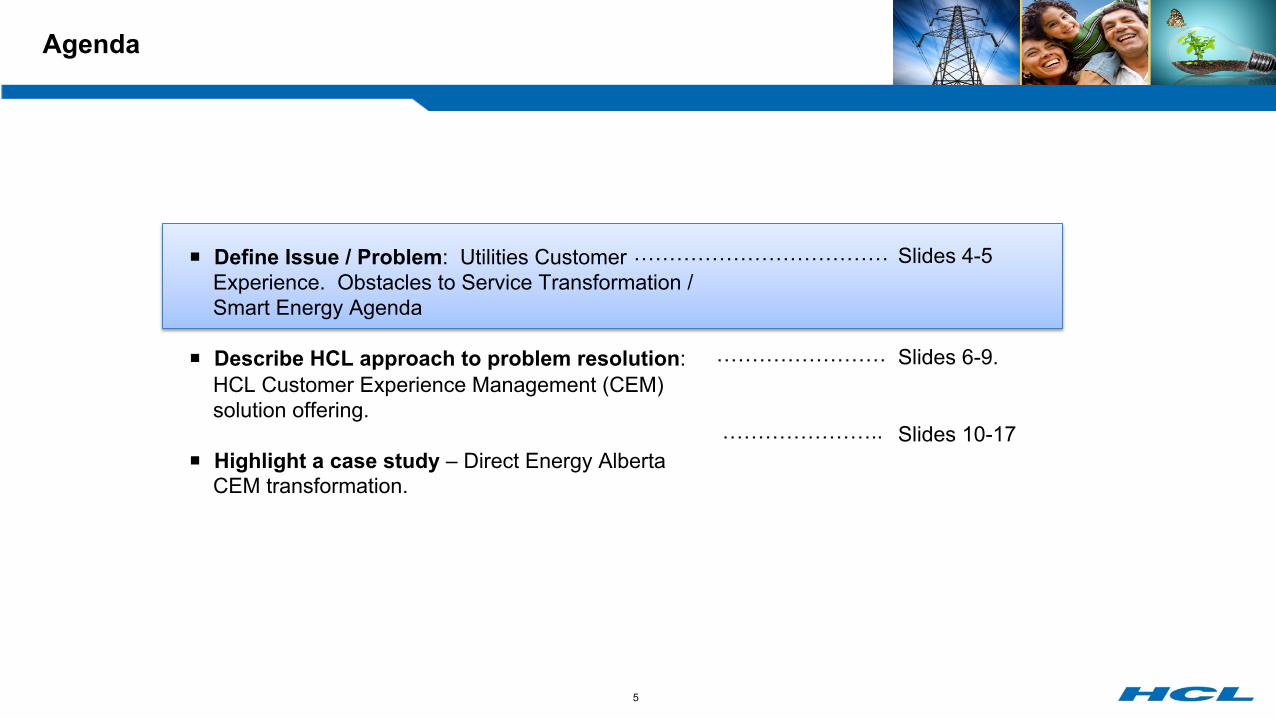

¡ Define Issue / Problem: Utilities Customer Experience. Obstacles to Service Transformation / Smart Energy Agenda

¡ Describe HCL approach to problem resolution: HCL Customer Experience Management (CEM) solution offering.

¡ Highlight a case study – Direct Energy Alberta CEM transformation.

Slides 4-5

Slides 6-9.

Slides 10-17

……………………………… ……………………

…………………..

6

Customer’s experience expectations have been established by innovators outside of the Utilities Industry

¡ Table stakes: Customers engage in the energy category infrequently – when they do, they expect service excellence.

¡ Channels: Interaction expectations are rapidly evolving. Increasingly, consumers expect to interact on their terms, on their time, and on their favored platform.

¡ Engagement: Customer satisfaction is enabled through, customer awareness and anticipation. Trust is enabled though operational transparency and education.

¡ Simplicity: Best in class customer experience is uncomplicated. Human factors engineering and industrial design matter. Customers expect an elegant interaction masking the complexity of the markets and technologies that serve them.

¡ Brand Consistency: It helps to stand for something and to reinforce what you stand for in every interaction.

7

Smart Utility / Smart Home – Customer Experience Aspirations

Ambition

¡ Establish customer relevance of smart meter and other near real time data.

¡ Establish role of trusted energy advisor to customers.

¡ Position goods and services beyond the meter:

§ Innovative demand response / direct load control

§ Core Positioning amongst the “internet of things”. Smart Home Services Aggregation / Smart Energy Consumption Management

§ Energy related intelligent asset sales, financing, operations (from thermostats to rooftop solar).

Current Limitations to that ambition

¡ Engagement – Driving a rich “conversation” with consumers. Anticipating needs and providing proactive service based upon behavior, interaction, market trends and the needs of “like” customers. (think Amazon, Netflix, Harrah’s).

¡ Channel Shift – Increase customer self service via Web, Mobility, Social Media, Text, IVR, others. (think USAA, Apple)

¡ Transparency – Provide situational awareness in an age of of increasingly transparent logistics (think UPS, FedEx, Uber).

8

Agenda

¡ Define Issue / Problem: Utilities Customer Experience. Obstacles to Transformation.

¡ Describe HCL approach to problem resolution: HCL Customer Experience Management (CEM) solution offering.

¡ Highlight a case study – Direct Energy Alberta CEM transformation.

Slides 4-5

Slides 6-9.

Slides 10-17

……………………………… ……………………

…………………..

9

The Utility CEM Business Case Challenge

Customer Experience Management Transformation – is difficult to “green light”. More difficult to execute.

¡ CIS replacements are complex, costly and disruptive - impacting hundreds of core business processes, thousands of users and millions of customers. And CIS alone falls well short of the state of the market.

¡ Operational benefits, technology and implementation costs are uncertain. Departmental distrust inhibits accountability and drives to incremental, tactical and often disjointed solutions.

¡ Transformation benefits are often discounted by uncertainty and diffuse stakeholder accountability.

.

In response HCL CEM offers:

¡ Reference Architecture across all aspects of Customer Experience.

¡ Multi Channel customer interaction with industrialized performance measurement. Social Media, Web, Mobile, Agent assisted, IVR, virtual agent and chat with conversation portability across platforms.

¡ Differentiated customer experience (interaction, correspondence selling) enabled by real time analytics / in memory computing.

¡ Transformation Project, Technology and Business Operations Cost and Benefit Certainty.

¡ Business Process Operations – tailored to balance your control, cost and risk objectives.

¡ Financial and Solution constructs designed to optimise Opex, CapEx, Cash flow, Recovery or other objectives.

10

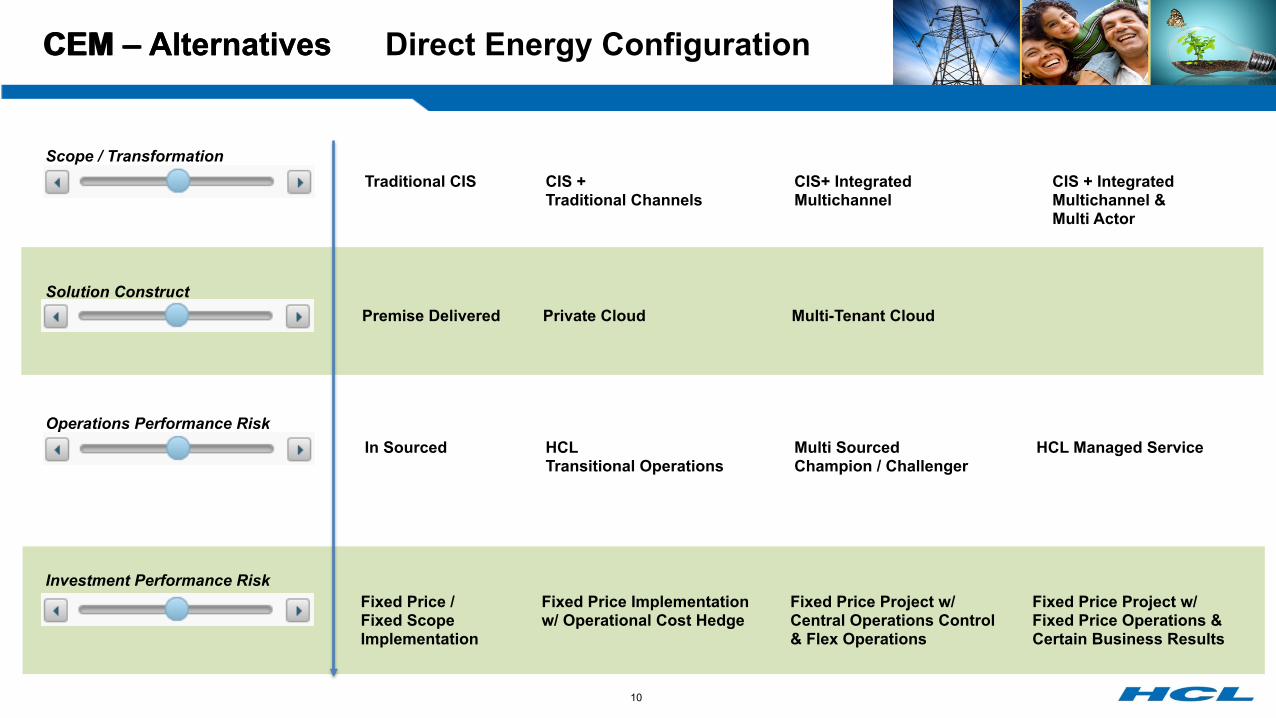

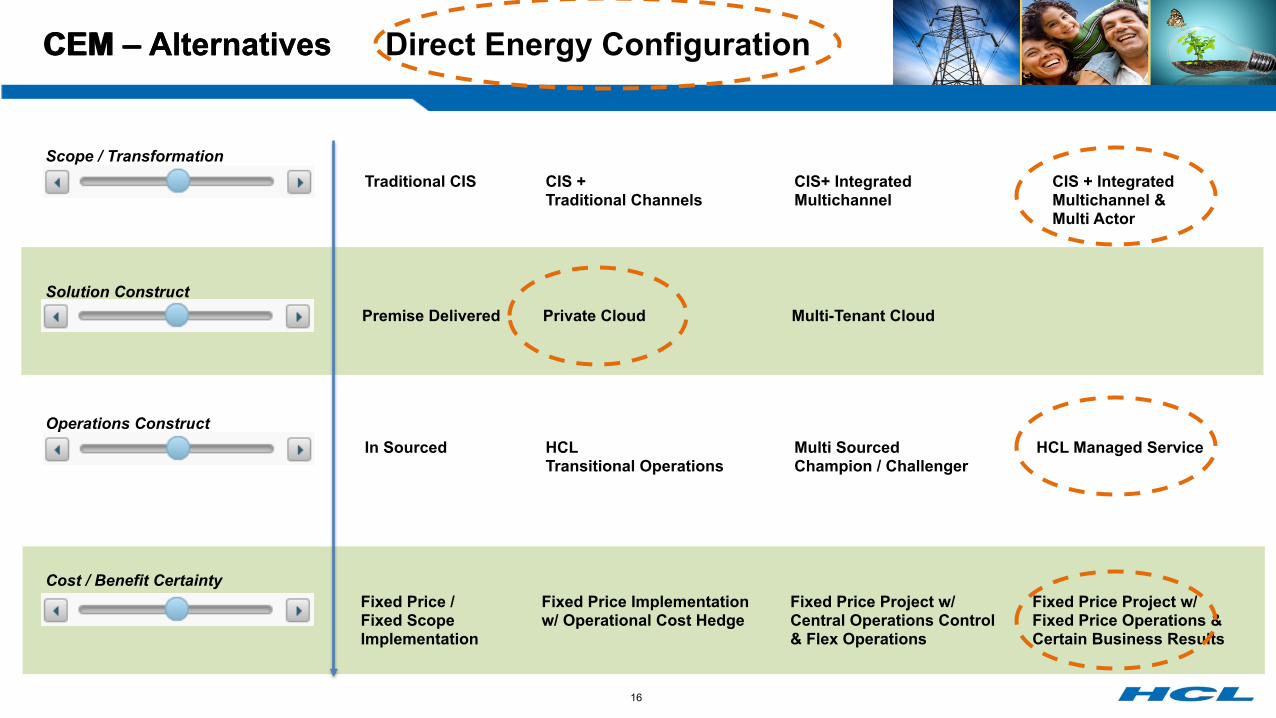

CEM – Alternatives

Solution Construct Premise Delivered Private Cloud Multi-Tenant Cloud

Operations Performance Risk In Sourced Multi Sourced

Champion / Challenger HCL Managed Service HCL

Transitional Operations

Scope / Transformation Traditional CIS CIS +

Traditional Channels CIS+ Integrated Multichannel

CIS + Integrated Multichannel & Multi Actor

Investment Performance Risk Fixed Price / Fixed Scope Implementation

Fixed Price Implementation w/ Operational Cost Hedge

Fixed Price Project w/ Central Operations Control & Flex Operations

Fixed Price Project w/ Fixed Price Operations & Certain Business Results

CEM – Alternatives Direct Energy Configuration

11

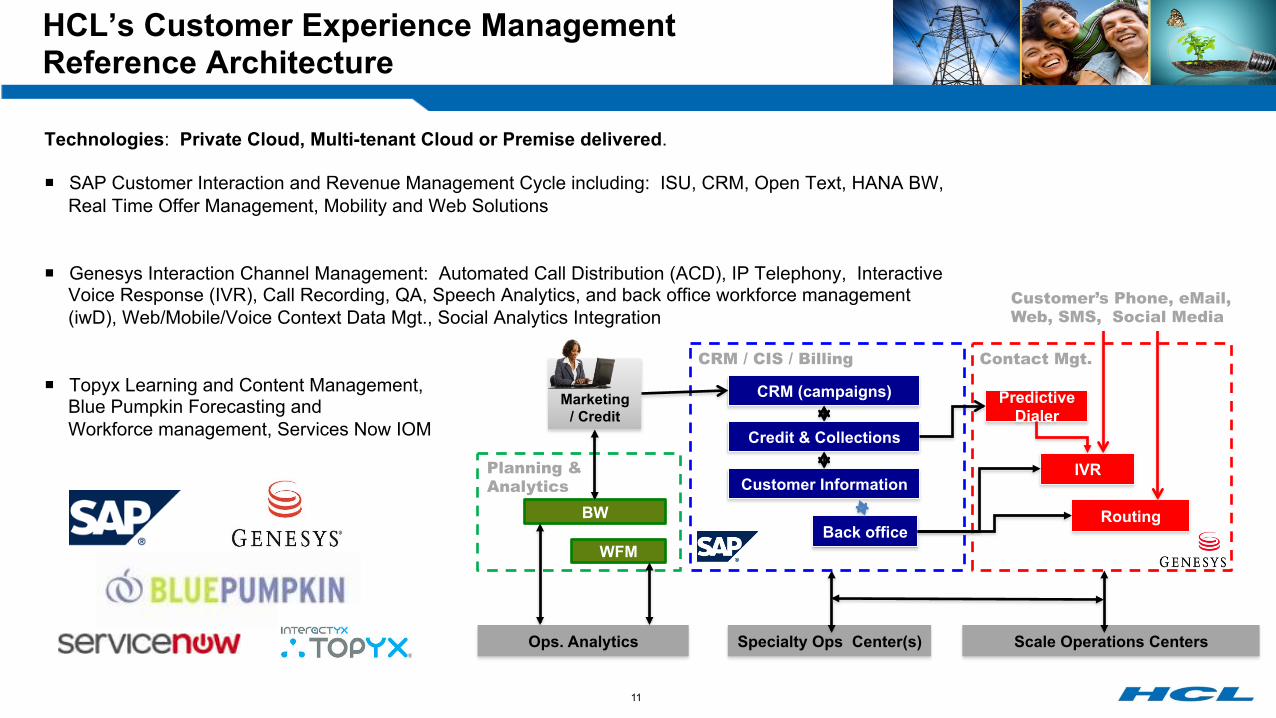

HCL’s Customer Experience Management Reference Architecture

IVR

Scale Operations Centers

Predictive Dialer

Routing

Specialty Ops Center(s)

CRM (campaigns)

Customer Information

Credit & Collections

Back office

CRM / CIS / Billing Contact Mgt.

Planning & Analytics

BW

WFM

Marketing / Credit

Ops. Analytics

Customer’s Phone, eMail, Web, SMS, Social Media

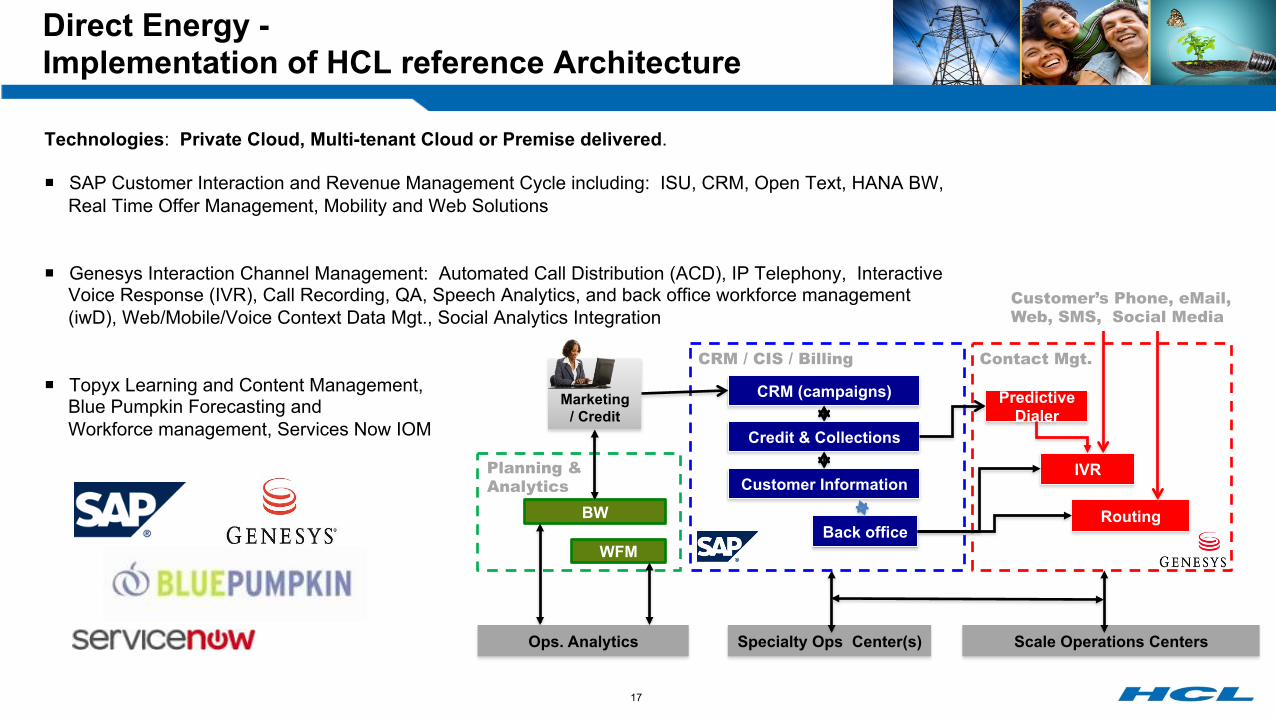

Technologies: Private Cloud, Multi-tenant Cloud or Premise delivered.

¡ SAP Customer Interaction and Revenue Management Cycle including: ISU, CRM, Open Text, HANA BW, Real Time Offer Management, Mobility and Web Solutions

¡ Genesys Interaction Channel Management: Automated Call Distribution (ACD), IP Telephony, Interactive Voice Response (IVR), Call Recording, QA, Speech Analytics, and back office workforce management (iwD), Web/Mobile/Voice Context Data Mgt., Social Analytics Integration

¡ Topyx Learning and Content Management, Blue Pumpkin Forecasting and Workforce management, Services Now IOM

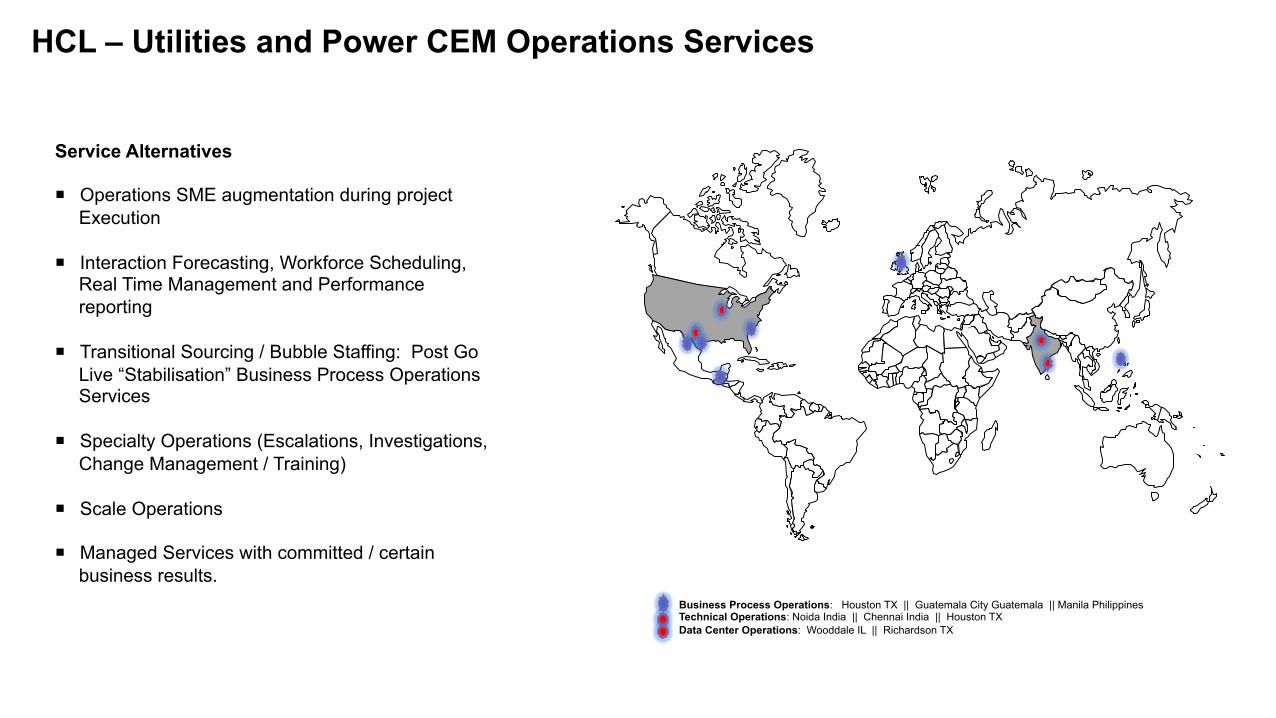

HCL – Utilities and Power CEM Operations Services

1 1

1

1 1

1

1

• Business Process Operations: Houston TX || Guatemala City Guatemala || Manila Philippines • Technical Operations: Noida India || Chennai India || Houston TX • Data Center Operations: Wooddale IL || Richardson TX

1

1 1

Service Alternatives

¡ Operations SME augmentation during project Execution

¡ Interaction Forecasting, Workforce Scheduling, Real Time Management and Performance reporting

¡ Transitional Sourcing / Bubble Staffing: Post Go Live “Stabilisation” Business Process Operations Services

¡ Specialty Operations (Escalations, Investigations, Change Management / Training)

¡ Scale Operations

¡ Managed Services with committed / certain business results.

1 1

1

13

Agenda

¡ Define Issue / Problem: Utilities Customer Experience. Obstacles to Transformation.

¡ Describe HCL approach to problem resolution: HCL Customer Experience Management (CEM) solution offering.

¡ Highlight a case study – Direct Energy Alberta CEM transformation.

Slides 4-5

Slides 6-9.

Slides 10-17

……………………………… ……………………

…………………..

14

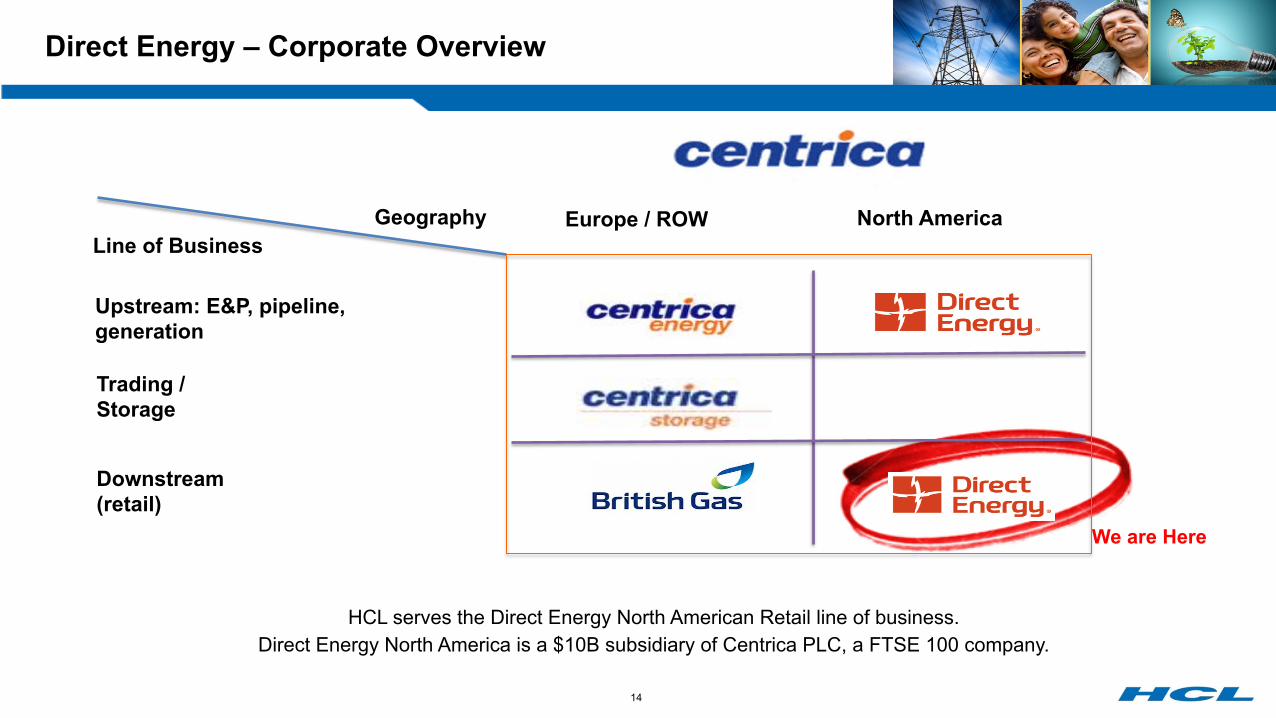

Direct Energy – Corporate Overview

North America Europe / ROW

Upstream: E&P, pipeline, generation

Trading / Storage

Downstream (retail)

We are Here

HCL serves the Direct Energy North American Retail line of business. Direct Energy North America is a $10B subsidiary of Centrica PLC, a FTSE 100 company.

Geography Line of Business

15

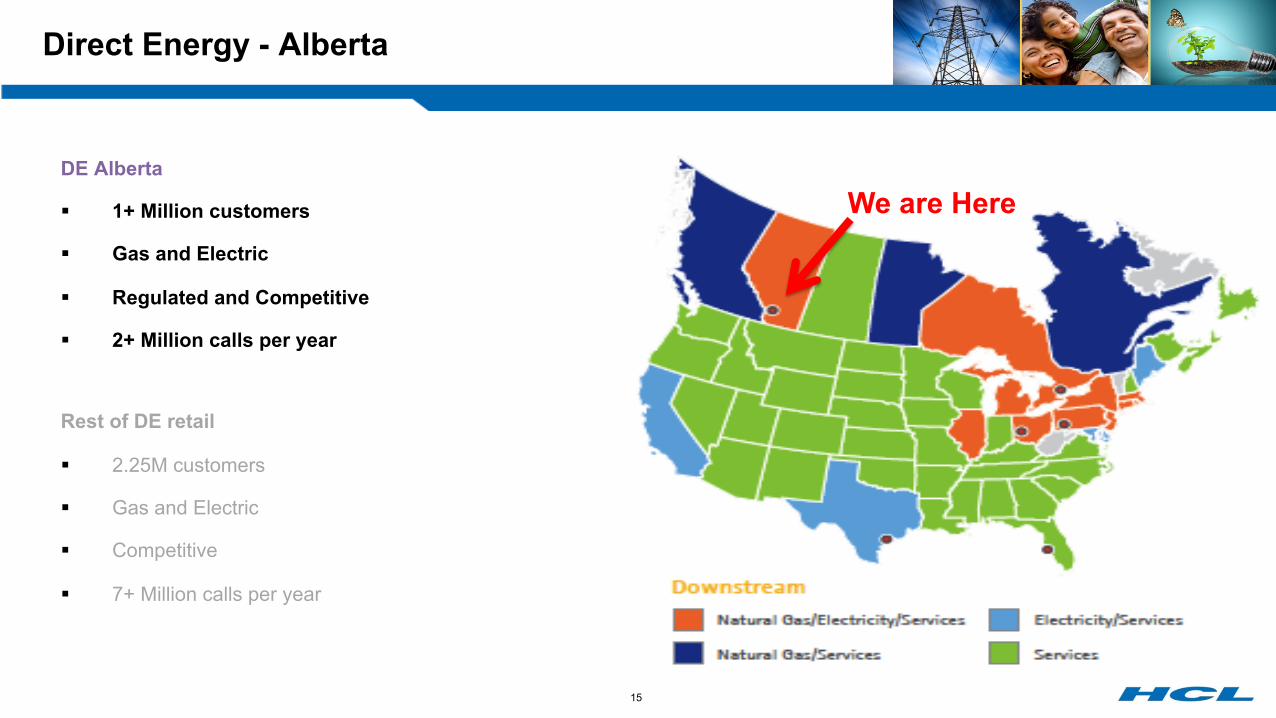

Direct Energy - Alberta

DE Alberta

§ 1+ Million customers

§ Gas and Electric

§ Regulated and Competitive

§ 2+ Million calls per year

Rest of DE retail

§ 2.25M customers

§ Gas and Electric

§ Competitive

§ 7+ Million calls per year

We are Here

16

CEM – Alternatives

Solution Construct Premise Delivered Private Cloud Multi-Tenant Cloud

Operations Construct In Sourced Multi Sourced

Champion / Challenger HCL Managed Service HCL

Transitional Operations

Scope / Transformation Traditional CIS CIS +

Traditional Channels CIS+ Integrated Multichannel

CIS + Integrated Multichannel & Multi Actor

Cost / Benefit Certainty Fixed Price / Fixed Scope Implementation

Fixed Price Implementation w/ Operational Cost Hedge

Fixed Price Project w/ Central Operations Control & Flex Operations

Fixed Price Project w/ Fixed Price Operations & Certain Business Results

CEM – Alternatives Direct Energy Configuration

17

Direct Energy - Implementation of HCL reference Architecture

IVR

Scale Operations Centers

Predictive Dialer

Routing

Specialty Ops Center(s)

CRM (campaigns)

Customer Information

Credit & Collections

Back office

CRM / CIS / Billing Contact Mgt.

Planning & Analytics

BW

WFM

Marketing / Credit

Ops. Analytics

Customer’s Phone, eMail, Web, SMS, Social Media

Technologies: Private Cloud, Multi-tenant Cloud or Premise delivered.

¡ SAP Customer Interaction and Revenue Management Cycle including: ISU, CRM, Open Text, HANA BW, Real Time Offer Management, Mobility and Web Solutions

¡ Genesys Interaction Channel Management: Automated Call Distribution (ACD), IP Telephony, Interactive Voice Response (IVR), Call Recording, QA, Speech Analytics, and back office workforce management (iwD), Web/Mobile/Voice Context Data Mgt., Social Analytics Integration

¡ Topyx Learning and Content Management, Blue Pumpkin Forecasting and Workforce management, Services Now IOM

18

Engagement Scope – Direct Energy Business Process Operations

Front Office Services - inbound and outbound call handling including:

• Service,

• Sales,

• Billing,

• Credit

Back Office Services including:

• escalations,

• correspondence,

• billing exception management,

• cash processing,

• credit data management

• offline interactions – eMail, SMS, and chat (future)

500 (peak), 300 (steady state) FTEs

Service delivery locations in Manila, Guatemala City, Noida

• Symmetric Scale Operations in Manila and Guatemala City

• Command Center / Escalations in Houston,

• Shared Service workforce forecasting / scheduling in Noida

19

Selected KPIs / Commercial Performance Measures

Technical Performance Business Performance

• Go Live Date

• Severity 1 errors ahead of Go Live date

• Percentage of Business Requirements

met ahead of go live date

• System Availability

• Incident response times

• Incident resolution times

• Self Service Adoption Rates

• Billing Accuracy

• Billing Timeliness

• Average Speed of Answer

• Average Handle Times

• First Call Resolution Rates

• Customer Satisfaction

• Compliance with Law and Regulation

Given HCL’s construction, technical and business operations responsibilities, commercial incentives and penalties are aligned to both inputs (technical performance) and outcomes

(business performance).

20

Committed Benefits

Certain business outcomes –

¡ Charging Mechanism: Cost per Customer invoiced monthly

¡ Call option – right to insource / resource at any time at known cost

¡ Operational and Technical Transparency

¡ Post Go Live Operations Performance Certainty – HCL absorbs all “change” human performance effectiveness risk

Operations outcomes

¡ Eight figure operations cost reductions

¡ >20% increase in customer self service

¡ Committed levels of Customer Satisfaction, Agent Efficiency, First Call Resolution, Billing accuracy and timeliness, Collections list penetration

¡ Cross Channel interaction awareness, consistency, visibility, Cross Sales / Up Sales.

¡ Differentiated service levels and interaction paths

Technical outcomes –

¡ Fixed price for certain outcomes.

¡ Full asset and Intellectual property transfer at conclusion of services term

¡ Operational platform including:

§ SAP ISU CCS, HANA, Mobility, and Web Self Service, Real Time Offer Management (next phase)

§ Genesys, ACD, IVR, VOIP, SoftPhone, Speach Analytics, MultiChannel Integration

§ Services Now – IT Service Management Platform

§ Topyx - Learning management and Content management solution.

21

Background slides

22

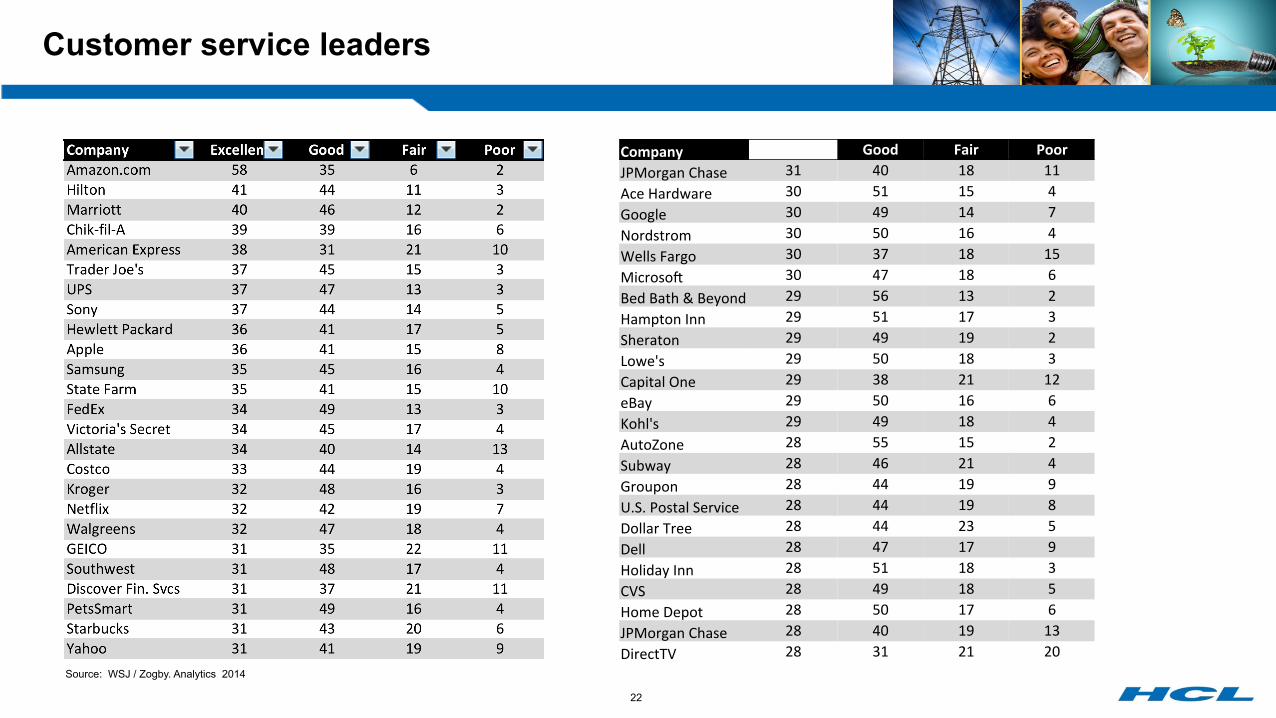

Customer service leaders

Company Excellent Good Fair Poor JPMorgan Chase 31 40 18 11 Ace Hardware 30 51 15 4 Google 30 49 14 7 Nordstrom 30 50 16 4 Wells Fargo 30 37 18 15 MicrosoD 30 47 18 6 Bed Bath & Beyond 29 56 13 2 Hampton Inn 29 51 17 3 Sheraton 29 49 19 2 Lowe's 29 50 18 3 Capital One 29 38 21 12 eBay 29 50 16 6 Kohl's 29 49 18 4 AutoZone 28 55 15 2 Subway 28 46 21 4 Groupon 28 44 19 9 U.S. Postal Service 28 44 19 8 Dollar Tree 28 44 23 5 Dell 28 47 17 9 Holiday Inn 28 51 18 3 CVS 28 49 18 5 Home Depot 28 50 17 6 JPMorgan Chase 28 40 19 13 DirectTV 28 31 21 20

Source: WSJ / Zogby. Analytics 2014

23

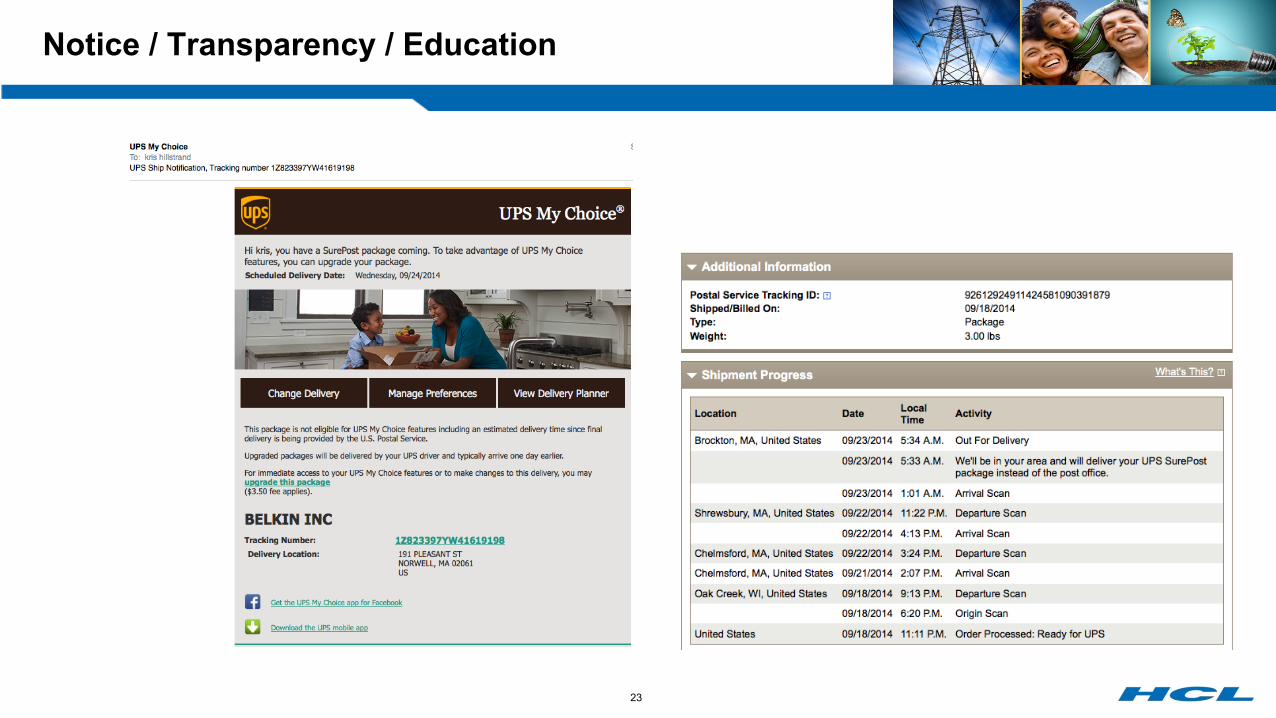

Notice / Transparency / Education