Embed Size (px)

Citation preview

2 | P a g e

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

NCL Industries Ltd

II nn

ii ttii aa

ttii nn

gg CC

oovv

eerraa

ggee

–– 11

55 SS

eepp

ttee

mmbb

eerr 22

0011

55

4

Recommendation BUY Cementing the Turnaround

NCL Industries Limited is a south based small cement company. The company operates through four related business divisions such as cement, cement boards, ready-mix-concrete and energy (hydro power) division. Its brand “Nagarjuna” enjoys a brand loyalty and a premium position in the region. NCL operates two cement plants, one at Telangana and another at Andhra Pradesh State with combine capacity of 1.95MT with cement contribution of 82% in the total sales. The company also has two hydro power plants situated in state of Andhra Pradesh and Karnataka with 7.5 MW and 8.25MW, respectively.

Investment Rationale:

The Southern market will drive slow and steady growth with prices holding at high levels The southern markets, specifically in Telangana and Andhra Pradesh have seen a strong pricing discipline in last the 6-9 months. Stable prices in the southern markets and cost control have contributed to a better performance of NCL and helped it to turn the corner. Southern region, which had witnessed the highest capacity addition of around 125 MT in the last five years, will see a considerable slowdown in fresh capacity addition by only 6 MTPA to 7 MTPA in the next two years.

Better utilization and realization through its product mix NCL has been in the cement market for nearly three decades and had established one of the largest networks of 1500 dealers to penetrate the southern region under the brand image of “Nagarjuna”. NCL is one of the few cement manufactures approved by Indian railway to produce and supply cement for railway sleepers. The company has added advantage of being one of the plants located just 40kms away to the proposed capital of Andhra Pradesh (Amaravati) and this will act as demand driver for the company. All in all, we feel NCL’s volume growth can be higher than the regional growth in demand for cement segment. This will help the company to improve utilization of plant and result in higher profitability.

Valuation

At the current market price (CMP) of Rs 92, the stock is trading at 3.8x its FY16E EV/EBITDA. We value NCL’s business at 5x FY16E EV/EBITDA and have arrived at a price target of Rs 131, implying an upside potential of 43% in a year. NCL looks like an attractive investment opportunity among small-cap stocks. We Initiate coverage on NCL Industries ltd with BUY Rating

CMP Rs 92

Target Price Rs 131

Sector Cement

Stock Details

BSE Code 502168

NSE Code NCLIND

Bloomberg Code NCLI IN

Market Cap (Rs cr) 338

Free Float (%) 49.6

52- wk HI/Lo (Rs) 113/30

Avg. volume BSE (Quarterly) 86,090

Face Value (Rs) 10

Dividend (FY 15) 0%

Shares o/s (Cr) 3.67

Relative Performance 1Mth 3Mth 1Yr

NCL -9.3% 57.7% 176.2%

Sensex -7.9% -2.7% -4.5%

Shareholding Pattern (%) 30th

June’15

Promoters Holding 50.4

Institutional (Incl. FII) 0.1

Corporate Bodies 7.3

Public & others 42.2

Varsha Bang 39268173 Research Analyst [email protected]

Year

Net Sales (Rs cr)

Growth (%)

EBITDA (Rs cr)

Margin (%)

Adj PAT (Rs cr)

Margin (%)

EPS (Rs) PE (x) $EV/ton EV/EBITDA

FY14 408.7 (3.0%) 28.0 6.9% (40.8) (10.0%) (11.7) (7.8) 41.5 19.0

FY15 533.9 30.6% 70.2 13.1% 8.9 1.7% 2.6 35.9 38.3 7.0

FY16E 628.9 17.8% 123.7 19.7% 52.7 8.4% 14.4 6.4 36.9 3.8

FY17E 716.4 13.9% 147.4 20.6% 74.7 10.4% 20.3 4.5 32.1 2.8

3 | P a g e

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

NCL Industries Ltd

II nn

ii ttii aa

ttii nn

gg CC

oovv

eerraa

ggee

–– 11

55 SS

eepp

ttee

mmbb

eerr 22

0011

55

Company Snapshot

Established in 1983 by first generation entrepreneur Late Mr. K Ramachandra Raju, NCL

Industries Ltd (NCL) is a Hyderabad-based company with business interests in cement,

particle board, ready mix concrete and hydro power. Currently, the business is being

looked after by MR. K. Ravi, MD of the company.

NCL operates two cement plants one each at Telangana and Andhra Pradesh State with a

combined capacity of 1.95MT and contributes around 82% of total sales. The cement

sold under the brand name ‘Nagarjuna’ established a premium brand image in the

coastal districts of Andhra Pradesh. The brand “Nagarjuna” enjoys a brand loyalty and a

premium position in the region.

The NCL Business Divisions

Business Divisions Capacity Location Cement 1.975 MTPA Nalgonda and Kondappalli Boards 60000 TPA Nalgonda and Paonta Sahib Ready mix Concrete NA Autonagar and Medak Hydro Plant 15.75 MW Srisailam dam and Tungabhadra dam

Source: Company, NB Research

The company started as a single product company with mere capacity of 0.07MTPA,

which gradually increased to 1.95 MTPA of cement. However, to diversify, NCL entered

into the manufacture of high quality, affordable building materials.

With cement boards and ready mix concrete, the company forward integrated into value

added products. NCL has two small hydro power plants of 7.5MW and 8.25MW situated

in state of Andhra Pradesh and Karnataka, respectively.

After experiencing a particularly turbulent phase of almost three years from early 2012

till mid 2015 due to a host of external issues like political headwinds in Andhra Pradesh

State and pricing pressure on the south region, the company started to fructify slowly.

The company’s balance sheet faced huge stress during the distressed phase and had to

resort to CDR.

4 | P a g e

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

NCL Industries Ltd

II nn

ii ttii aa

ttii nn

gg CC

oovv

eerraa

ggee

–– 11

55 SS

eepp

ttee

mmbb

eerr 22

0011

55

Investment Rationale:

The Southern market will drive slow and steady growth with prices holding at high

levels

Due to the cyclical nature of the cement industry, the cement prices have shown large

fluctuations in the last couple of years, which has given enough of ache to the existing

players in the southern region.

The southern markets has witnessed a serious downturn in cement prices during FY12-

15 , due to overcapacity, weakness in demand, slow growth in economy, slowdown in

the construction activity etc, which has impacting the demand for cement in southern

markets. Apart from this due to higher supply of cement the price remain under pressure

during the period. However, the above trend is changing as the cement prices have

raised sharply in the southern region in the last 6-9 months.

Stable Pricing continues……….. The southern markets, specifically in Telangana and Andhra Pradesh have seen a strong

pricing discipline in last the 6-9 months. Stable prices in the southern markets and cost

control have contributed to a better performance of NCL and helped it to turn the

corner.

Exhibit 2: Cement Prices In The Southern Region

Source: Company, NB Research

The cement industry in the southern India is stable and steadily growing due to demand,

supply and price stability. Southern region, which had witnessed the highest capacity

addition of around 125 MT in the last five years, will see a considerable slowdown in

fresh capacity addition by only 6 MTPA to 7 MTPA in the next two years.

5 | P a g e

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

NCL Industries Ltd

II nn

ii ttii aa

ttii nn

gg CC

oovv

eerraa

ggee

–– 11

55 SS

eepp

ttee

mmbb

eerr 22

0011

55

This is expected to improve cement capacity utilization in this region to 61% to 63% over

the time frame of two years. The incremental demand and slowing new capacity

additions have reduced the volatility in cement prices in southern markets.

For, NCL industries, Q1FY16 were the second consecutive quarter of strong cement

realization resulting in improvement in profitability. We expect the momentum to

continue for the company on account of sustained volume growth, production discipline,

and strong pricing.

Better utilization and realization for NCL

NCL has been a unique company among smaller cement plants. Right from its inception,

the company was focused on establishing a premium image for its brand ‘Nagarjuna’

cement. With an installed cement capacity of 1.95 MTPA, the company sells its cement

under the brand name of ‘Nagarjuna’ which has an established presence in coastal

Andhra Pradesh and Telengana.

Strategically located in the sound markets

NCL has been in the cement market for nearly three decades and has established the

network of 1,500 dealers to penetrate the southern region mainly Telangana and Andhra

Pradesh under brand name ‘Nagarjuna’. Strong focus on developing the retail market will

enable NCL to sustain volume growth with better realization as compared to other

players in the southern region.

The company is one of the few cement manufacturers approved by the Indian Railways

to manufacture and supply special grade cement, as it requires enhanced quality and

performance characteristics for the production of railway sleepers.

Since last two years, railway had been holding back orders for new sleepers. But in the

current year railways has started the process of tendering orders for new sleepers. The

company is expecting good demand from this segment, which will help it to increase

utilization more than its peers in the region.

The company also has forward integration in the form of ready mix concrete and building

materials such as laminated cement bonded particles, which helps NCL industries in

better capacity utilization.

The political turmoil in Andhra Pradesh has led to a sharp fall in infrastructure

development in this region. However, signs of growth are slowly re-emerging following

the bifurcation of the state and political stability, which is expected to revive economic

activity in the region with a pick-up in demand for infrastructure from both the states.

6 | P a g e

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

NCL Industries Ltd

II nn

ii ttii aa

ttii nn

gg CC

oovv

eerraa

ggee

–– 11

55 SS

eepp

ttee

mmbb

eerr 22

0011

55

NCL has the added advantage of being one of the plants close to the proposed capital of

Andhra Pradesh (Amaravati). The new capital will require a lot of infrastructure

development, which can create additional demand for cement.

One of NCL’s plants is located just 40 km away from the proposed capital and will act as

demand driver for the company. All in all, we feel NCL’s volume growth can be higher

than the regional growth in demand for cement. This will help the company to improve

utilization of plant and result in higher profitability.

Steady Performance of Cement board division

NCL has a unique feature of being the producer of cement particle boards having a

manufacturing plant in State of Telangana and Himachal Pradesh with install capacity of

60000 TPA. The plant was set up in a technical collaboration of Bioson Werke of

Germany, the world leaders in particle board technology. To provide value addition, the

company has developed a unique lamination process to laminate cement boards.

Cement boards division is performing well and running at full capacity. The division was

consistently making profit, even in the difficult time of company, which help it to realize

higher value.

Cement board Division FY12 FY13 FY14 FY15

Install Capacity (TTPA) 60.0 60.0 60.0 60.0

Sales (TTPA) 51.0 51.2 52.6 57.0

Capacity Utilization (%) 85.0% 85.3% 87.6% 95.0%

Growth (%) 4.2% 0.3% 2.8% 8.4%

Sales (Rs in Cr) 67.4 77.3 78.9 93.9

Growth (%) 9.7% 14.7% 2.0% 19.0%

EBIT 9.8 11.7 12.4 15.3 EBIT Margin (%) 14.6% 15.2% 15.8% 16.3%

Source: NB Research

7 | P a g e

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

NCL Industries Ltd

II nn

ii ttii aa

ttii nn

gg CC

oovv

eerraa

ggee

–– 11

55 SS

eepp

ttee

mmbb

eerr 22

0011

55

Q1FY16 Quarterly Result Review NCL Industries Ltd delivered strong performance in Q1FY16, net sales grew by 67.6% YoY

to Rs. 157.4 crs due to higher realization that were up by 22.8% to Rs. 6646 YoY (-1.1%

QoQ). Total Sales volume has increased by 50% YoY (down 7.7% QoQ) to 0.3MT. The

company realization for cement and cement board has improved, due to stable pricing

disciple seen in the southern markets during the quarter.

For, NCL industries, Q1FY16 were the second consecutive quarter of strong cement

realization resulting in improvement in profitability. We expect the momentum to

continue for the company on account of sustained volume growth, production discipline,

and strong pricing.

Quarterly Result (Rs in cr)

Q1FY16 Q4FY15 QoQ Q1FY15 YOY

Net Sales 157.8 177.8 -11.3% 95.7 64.8%

Operating Expenses 118.2 143.6 -17.7% 99.7 18.6%

EBITDA 39.6 34.2 15.6% (3.9) -1106.8%

EBITDA Margin 25.1 19.2

Depreciation 6.1 3.1 100.1% 7.4 -17.4%

EBIT 33.4 31.2 7.3% (11.4) -394.0%

Interest 7.5 11.6 -35.6% 7.8 -4.0%

Other Income 0.0 0.9 -96.9% 0.0 -33.5%

Exceptional Income 0.0 2.1 -100.0% 0.0 0.0%

PBT 26.0 22.4 15.7% (19.1) -235.6%

Tax 5.6 3.1 79.4% 0.1 5515.8%

Tax Rate 21.6 13.9

Reported PAT 20.3 19.3 5.3% (19.2) -205.7%

PAT Margin 12.9 10.9

No of Equity Shares 3.7 3.5 3.5

EPS 5.5 5.5 0.2% (5.5) -200.6%

CEPS 7.2 6.4 12.5% (3.4) -313.5%

8 | P a g e

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

NCL Industries Ltd

II nn

ii ttii aa

ttii nn

gg CC

oovv

eerraa

ggee

–– 11

55 SS

eepp

ttee

mmbb

eerr 22

0011

55

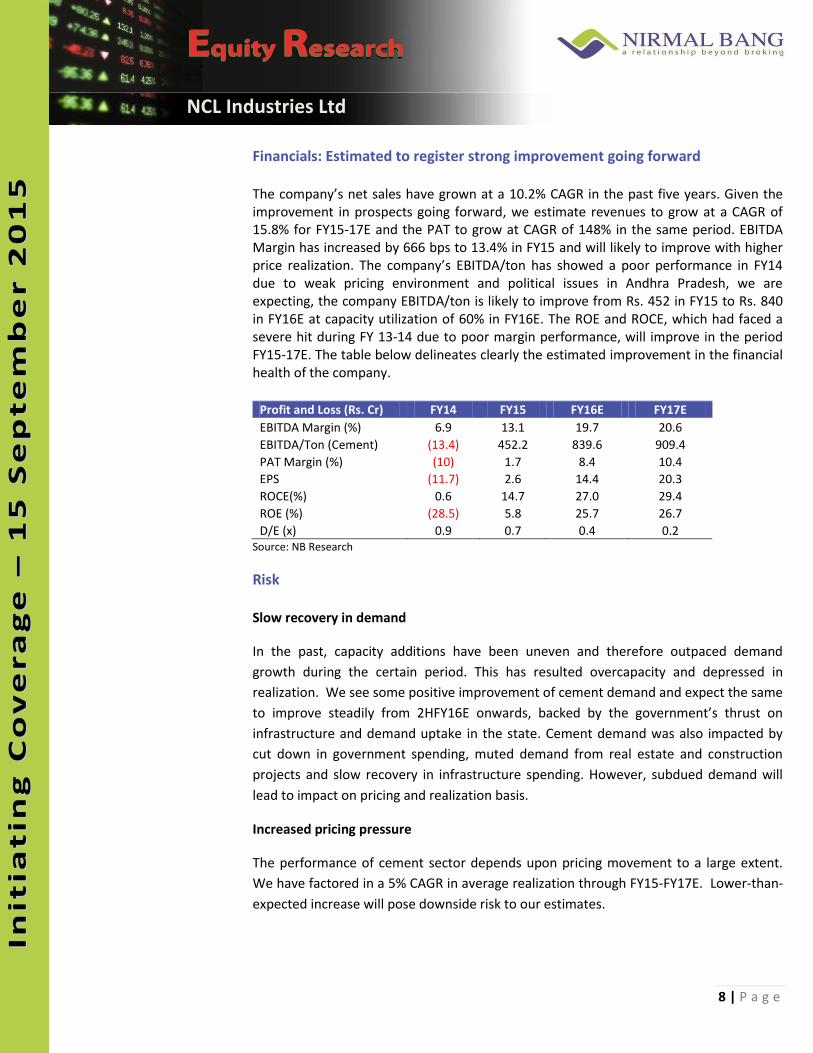

Financials: Estimated to register strong improvement going forward The company’s net sales have grown at a 10.2% CAGR in the past five years. Given the improvement in prospects going forward, we estimate revenues to grow at a CAGR of 15.8% for FY15-17E and the PAT to grow at CAGR of 148% in the same period. EBITDA Margin has increased by 666 bps to 13.4% in FY15 and will likely to improve with higher price realization. The company’s EBITDA/ton has showed a poor performance in FY14 due to weak pricing environment and political issues in Andhra Pradesh, we are expecting, the company EBITDA/ton is likely to improve from Rs. 452 in FY15 to Rs. 840 in FY16E at capacity utilization of 60% in FY16E. The ROE and ROCE, which had faced a severe hit during FY 13-14 due to poor margin performance, will improve in the period FY15-17E. The table below delineates clearly the estimated improvement in the financial health of the company.

Profit and Loss (Rs. Cr) FY14 FY15 FY16E FY17E

EBITDA Margin (%) 6.9 13.1 19.7 20.6

EBITDA/Ton (Cement) (13.4) 452.2 839.6 909.4

PAT Margin (%) (10) 1.7 8.4 10.4

EPS (11.7) 2.6 14.4 20.3

ROCE(%) 0.6 14.7 27.0 29.4

ROE (%) (28.5) 5.8 25.7 26.7

D/E (x) 0.9 0.7 0.4 0.2 Source: NB Research

Risk Slow recovery in demand

In the past, capacity additions have been uneven and therefore outpaced demand

growth during the certain period. This has resulted overcapacity and depressed in

realization. We see some positive improvement of cement demand and expect the same

to improve steadily from 2HFY16E onwards, backed by the government’s thrust on

infrastructure and demand uptake in the state. Cement demand was also impacted by

cut down in government spending, muted demand from real estate and construction

projects and slow recovery in infrastructure spending. However, subdued demand will

lead to impact on pricing and realization basis.

Increased pricing pressure

The performance of cement sector depends upon pricing movement to a large extent.

We have factored in a 5% CAGR in average realization through FY15-FY17E. Lower-than-

expected increase will pose downside risk to our estimates.

9 | P a g e

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

NCL Industries Ltd

II nn

ii ttii aa

ttii nn

gg CC

oovv

eerraa

ggee

–– 11

55 SS

eepp

ttee

mmbb

eerr 22

0011

55

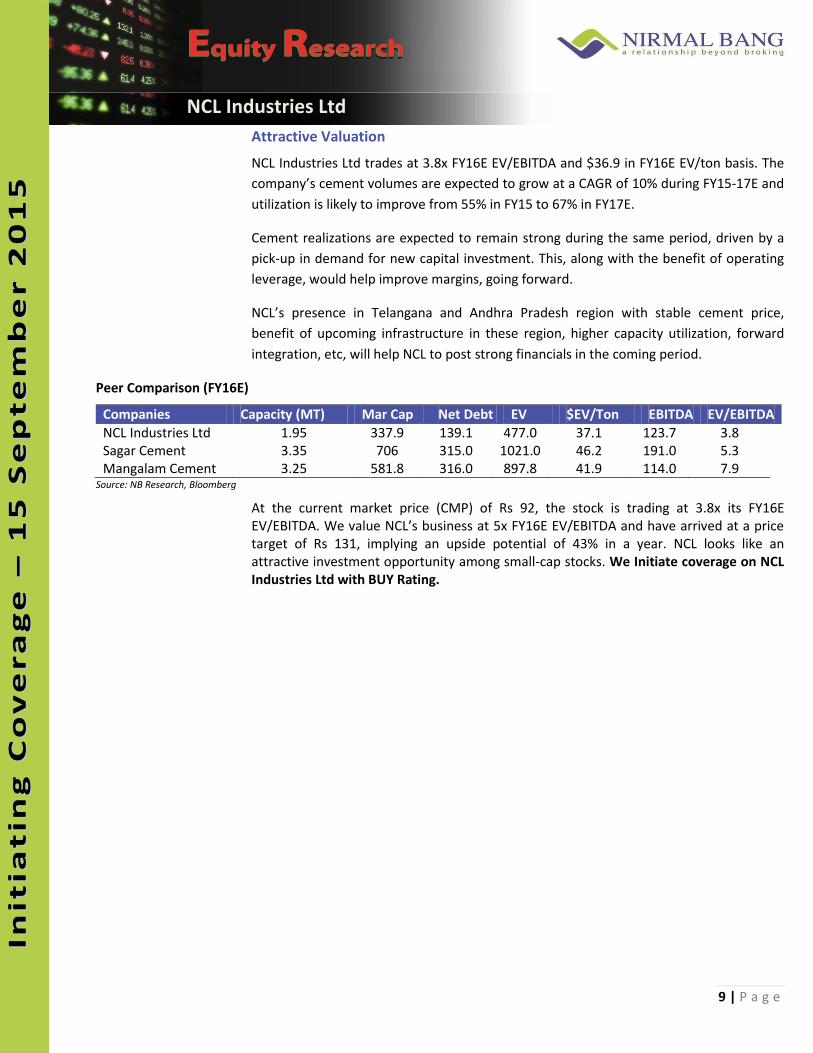

Attractive Valuation

NCL Industries Ltd trades at 3.8x FY16E EV/EBITDA and $36.9 in FY16E EV/ton basis. The

company’s cement volumes are expected to grow at a CAGR of 10% during FY15-17E and

utilization is likely to improve from 55% in FY15 to 67% in FY17E.

Cement realizations are expected to remain strong during the same period, driven by a

pick-up in demand for new capital investment. This, along with the benefit of operating

leverage, would help improve margins, going forward.

NCL’s presence in Telangana and Andhra Pradesh region with stable cement price,

benefit of upcoming infrastructure in these region, higher capacity utilization, forward

integration, etc, will help NCL to post strong financials in the coming period.

Peer Comparison (FY16E)

Companies Capacity (MT) Mar Cap Net Debt EV $EV/Ton EBITDA EV/EBITDA

NCL Industries Ltd 1.95 337.9 139.1 477.0 37.1 123.7 3.8 Sagar Cement 3.35 706 315.0 1021.0 46.2 191.0 5.3 Mangalam Cement 3.25 581.8 316.0 897.8 41.9 114.0 7.9

Source: NB Research, Bloomberg

At the current market price (CMP) of Rs 92, the stock is trading at 3.8x its FY16E EV/EBITDA. We value NCL’s business at 5x FY16E EV/EBITDA and have arrived at a price target of Rs 131, implying an upside potential of 43% in a year. NCL looks like an attractive investment opportunity among small-cap stocks. We Initiate coverage on NCL Industries Ltd with BUY Rating.

10 | P a g e

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

NCL Industries Ltd

II nn

ii ttii aa

ttii nn

gg CC

oovv

eerraa

ggee

–– 11

55 SS

eepp

ttee

mmbb

eerr 22

0011

55

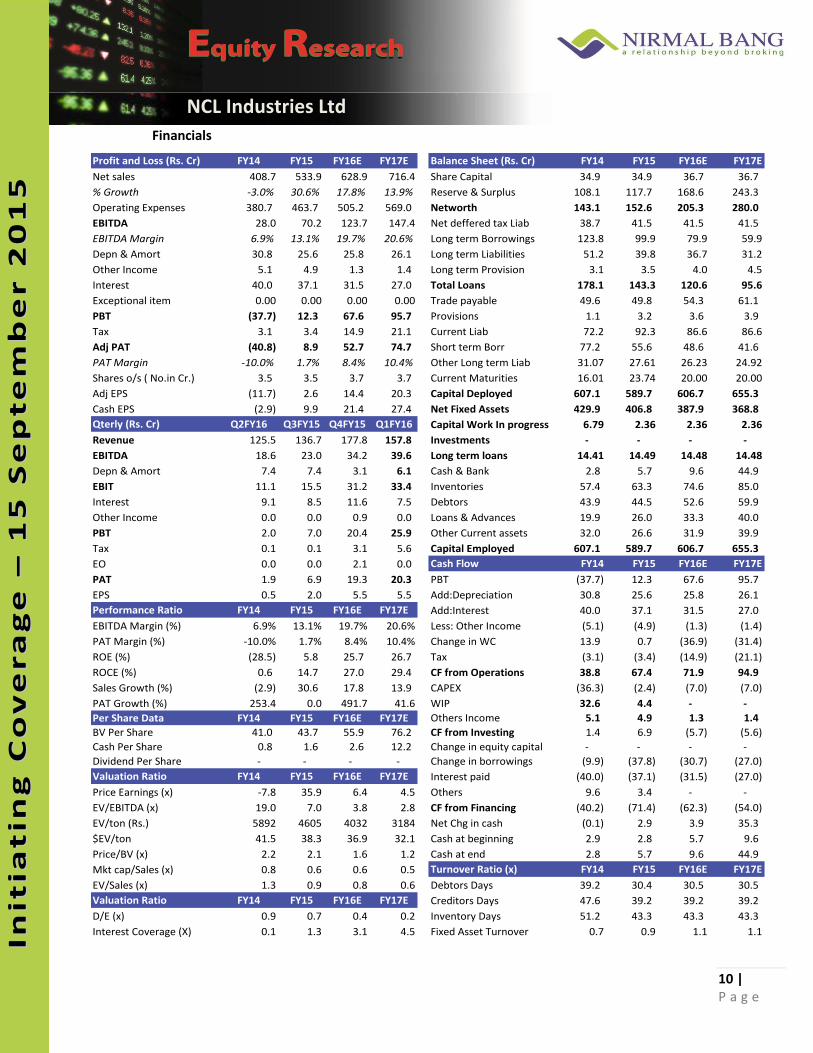

Financials

Profit and Loss (Rs. Cr) FY14 FY15 FY16E FY17E Balance Sheet (Rs. Cr) FY14 FY15 FY16E FY17E

Net sales 408.7 533.9 628.9 716.4 Share Capital 34.9 34.9 36.7 36.7

% Growth -3.0% 30.6% 17.8% 13.9% Reserve & Surplus 108.1 117.7 168.6 243.3

Operating Expenses 380.7 463.7 505.2 569.0 Networth 143.1 152.6 205.3 280.0

EBITDA 28.0 70.2 123.7 147.4 Net deffered tax Liab 38.7 41.5 41.5 41.5

EBITDA Margin 6.9% 13.1% 19.7% 20.6% Long term Borrowings 123.8 99.9 79.9 59.9

Depn & Amort 30.8 25.6 25.8 26.1 Long term Liabilities 51.2 39.8 36.7 31.2

Other Income 5.1 4.9 1.3 1.4 Long term Provision 3.1 3.5 4.0 4.5

Interest 40.0 37.1 31.5 27.0 Total Loans 178.1 143.3 120.6 95.6

Exceptional item 0.00 0.00 0.00 0.00 Trade payable 49.6 49.8 54.3 61.1

PBT (37.7) 12.3 67.6 95.7 Provisions 1.1 3.2 3.6 3.9

Tax 3.1 3.4 14.9 21.1 Current Liab 72.2 92.3 86.6 86.6

Adj PAT (40.8) 8.9 52.7 74.7 Short term Borr 77.2 55.6 48.6 41.6

PAT Margin -10.0% 1.7% 8.4% 10.4% Other Long term Liab 31.07 27.61 26.23 24.92

Shares o/s ( No.in Cr.) 3.5 3.5 3.7 3.7 Current Maturities 16.01 23.74 20.00 20.00

Adj EPS (11.7) 2.6 14.4 20.3 Capital Deployed 607.1 589.7 606.7 655.3

Cash EPS (2.9) 9.9 21.4 27.4 Net Fixed Assets 429.9 406.8 387.9 368.8

Qterly (Rs. Cr) Q2FY16 Q3FY15 Q4FY15 Q1FY16 Capital Work In progress 6.79 2.36 2.36 2.36

Revenue 125.5 136.7 177.8 157.8 Investments - - - -

EBITDA 18.6 23.0 34.2 39.6 Long term loans 14.41 14.49 14.48 14.48

Depn & Amort 7.4 7.4 3.1 6.1 Cash & Bank 2.8 5.7 9.6 44.9

EBIT 11.1 15.5 31.2 33.4 Inventories 57.4 63.3 74.6 85.0

Interest 9.1 8.5 11.6 7.5 Debtors 43.9 44.5 52.6 59.9

Other Income 0.0 0.0 0.9 0.0 Loans & Advances 19.9 26.0 33.3 40.0

PBT 2.0 7.0 20.4 25.9 Other Current assets 32.0 26.6 31.9 39.9

Tax 0.1 0.1 3.1 5.6 Capital Employed 607.1 589.7 606.7 655.3

EO 0.0 0.0 2.1 0.0 Cash Flow FY14 FY15 FY16E FY17E

PAT 1.9 6.9 19.3 20.3 PBT (37.7) 12.3 67.6 95.7

EPS 0.5 2.0 5.5 5.5 Add:Depreciation 30.8 25.6 25.8 26.1

Performance Ratio FY14 FY15 FY16E FY17E Add:Interest 40.0 37.1 31.5 27.0

EBITDA Margin (%) 6.9% 13.1% 19.7% 20.6% Less: Other Income (5.1) (4.9) (1.3) (1.4)

PAT Margin (%) -10.0% 1.7% 8.4% 10.4% Change in WC 13.9 0.7 (36.9) (31.4)

ROE (%) (28.5) 5.8 25.7 26.7 Tax (3.1) (3.4) (14.9) (21.1)

ROCE (%) 0.6 14.7 27.0 29.4 CF from Operations 38.8 67.4 71.9 94.9

Sales Growth (%) (2.9) 30.6 17.8 13.9 CAPEX (36.3) (2.4) (7.0) (7.0)

PAT Growth (%) 253.4 0.0 491.7 41.6 WIP 32.6 4.4 - -

Per Share Data FY14 FY15 FY16E FY17E Others Income 5.1 4.9 1.3 1.4

BV Per Share 41.0 43.7 55.9 76.2 CF from Investing 1.4 6.9 (5.7) (5.6)

Cash Per Share 0.8 1.6 2.6 12.2 Change in equity capital - - - -

Dividend Per Share - - - - Change in borrowings (9.9) (37.8) (30.7) (27.0)

Valuation Ratio FY14 FY15 FY16E FY17E Interest paid (40.0) (37.1) (31.5) (27.0)

Price Earnings (x) -7.8 35.9 6.4 4.5 Others 9.6 3.4 - -

EV/EBITDA (x) 19.0 7.0 3.8 2.8 CF from Financing (40.2) (71.4) (62.3) (54.0)

EV/ton (Rs.) 5892 4605 4032 3184 Net Chg in cash (0.1) 2.9 3.9 35.3

$EV/ton 41.5 38.3 36.9 32.1 Cash at beginning 2.9 2.8 5.7 9.6

Price/BV (x) 2.2 2.1 1.6 1.2 Cash at end 2.8 5.7 9.6 44.9

Mkt cap/Sales (x) 0.8 0.6 0.6 0.5 Turnover Ratio (x) FY14 FY15 FY16E FY17E

EV/Sales (x) 1.3 0.9 0.8 0.6 Debtors Days 39.2 30.4 30.5 30.5

Valuation Ratio FY14 FY15 FY16E FY17E Creditors Days 47.6 39.2 39.2 39.2

D/E (x) 0.9 0.7 0.4 0.2 Inventory Days 51.2 43.3 43.3 43.3

Interest Coverage (X) 0.1 1.3 3.1 4.5 Fixed Asset Turnover 0.7 0.9 1.1 1.1

11 | P a g e

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

NCL Industries Ltd

II nn

ii ttii aa

ttii nn

gg CC

oovv

eerraa

ggee

–– 11

55 SS

eepp

ttee

mmbb

eerr 22

0011

55

Disclaimer:

Nirmal Bang Securities Private Limited (hereinafter referred to as “NBSPL”) is a registered Member of National Stock Exchange of India

Limited, Bombay Stock Exchange Limited and MCX stock Exchange Limited. NBSPL is in the process of making an application with SEBI for

registering as a Research Entity in terms of SEBI (Research Analyst) Regulations, 2014.

NBSPL or its associates including its relatives/analyst hold beneficial ownership of more than 1% in the company covered by Analyst.

NBSPL or its associates/analyst has not received any compensation from the company covered by Analyst during the past twelve months.

NBSPL /analyst has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making

activity of the company covered by Analyst.

The views expressed are based solely on information available publicly and believed to be true. Investors are advised to independently evaluate

the market conditions/risks involved before making any investment decision.

This document, at best, represents Analyst opinion and is meant for general information only. NBSPL, its directors, officers or employees shall

not in any way be responsible for the contents stated herein. NBSPL expressly disclaims any and all liabilities that may arise from information,

errors or omissions in this connection. This document is not to be considered as an offer to sell or a solicitation to buy any securities.

Nirmal Bang Research (Division of Nirmal Bang Securities Pvt. Ltd.)

B-2, 301/302, Marathon Innova, Opp. Peninsula Corporate Park

Off. Ganpatrao Kadam Marg Lower Parel (W), Mumbai-400013 Board No. : 91 22 3926 8000/8001

Fax. : 022 3926 8010

![· QSa RS W\RcQW` ZO `\W\S`OZWhOQW]\ \]`[OZ RSZ VcSa] g RS ^`SdS\W` SZ `O_cWbWa[]% =Og dO`WOa QZOaSa RS JWbO[W\O 9% ^S`] RS W[^]`](https://img.pdfslide.tips/doc/110x75/5b8094f87f8b9ae6088dcb75/-qsa-rs-wrcqw-zo-wsozwhoqw-oz-rsz-vcsa-g-rs-sdsw-sz-ocwbwa.jpg)

![( f ¡ [ $* Èj€¦ · ]l [ 6¢ " ¢! / g f Ú 8 Ð ! !k !g [1920 - Rs. 1 1940 -Rs. 10](https://img.pdfslide.tips/doc/110x75/5f506d44cc9b672d07606ed5/-f-j-l-6-g-f-8-k-g-1920-rs-1-1940-rs.jpg)