Embed Size (px)

Citation preview

ANNUAL REPORT

2015

ENGEN BOTSWANA LIMITED

2

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

CONTENTSENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

CONTENTS

0102

0304

Financial Highlights 01About Engen 02Presence 03

INTRODUCTION

Board of Directors 05Chairman’s Report 07Managing Director’s Report 09Financial Results 11Financial Summury 12

COMMENTARY

Sustainablity Report 15Commercial ReportProperty Report 19Distribution 20Retail Results 21Human Resources 23Corporate Social Responsibility Report 24

SECTORS

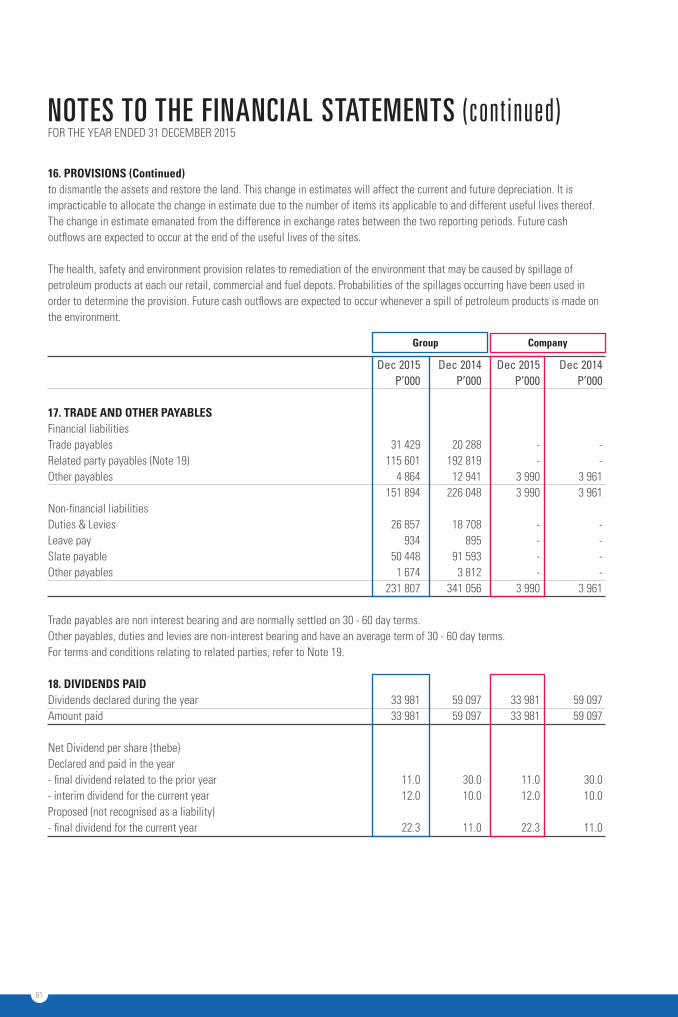

Governance 25Management 27Five Year Reveiw 28

GOVERNANCE

05ANNUALCONSOLIDATED FINANCIALSTATEMENTS

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

3

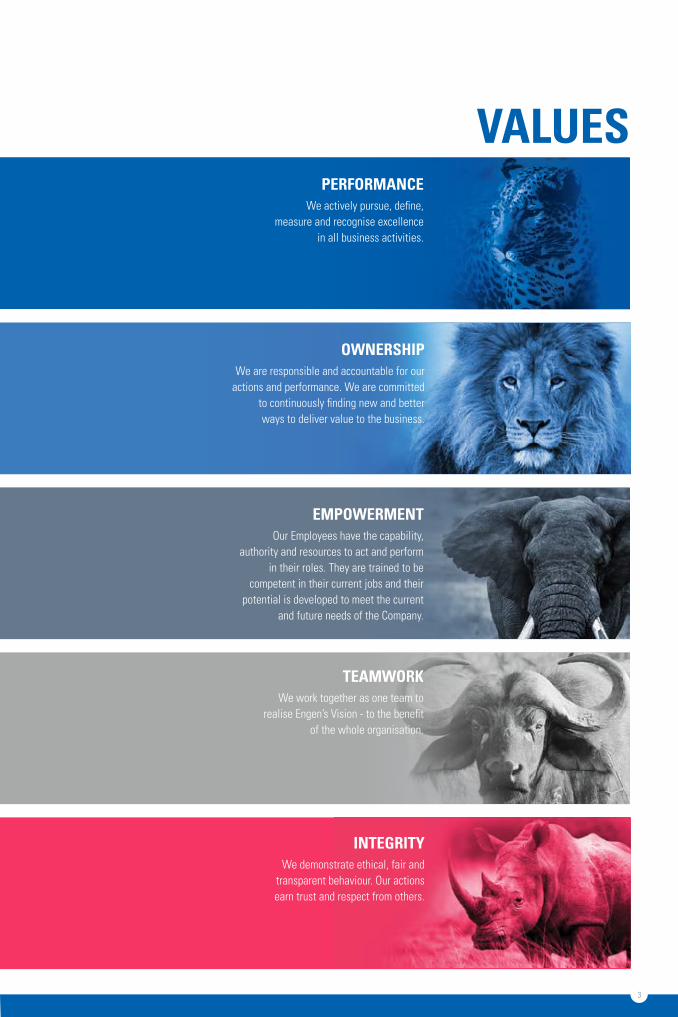

VALUESPERFORMANCE

We actively pursue, define, measure and recognise excellence

in all business activities.

OWNERSHIPWe are responsible and accountable for our

actions and performance. We are committed to continuously finding new and better ways to deliver value to the business.

EMPOWERMENTOur Employees have the capability,

authority and resources to act and perform in their roles. They are trained to be

competent in their current jobs and their potential is developed to meet the current

and future needs of the Company.

TEAMWORKWe work together as one team to

realise Engen’s Vision - to the benefit of the whole organisation.

INTEGRITYWe demonstrate ethical, fair and

transparent behaviour. Our actions earn trust and respect from others.

1

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

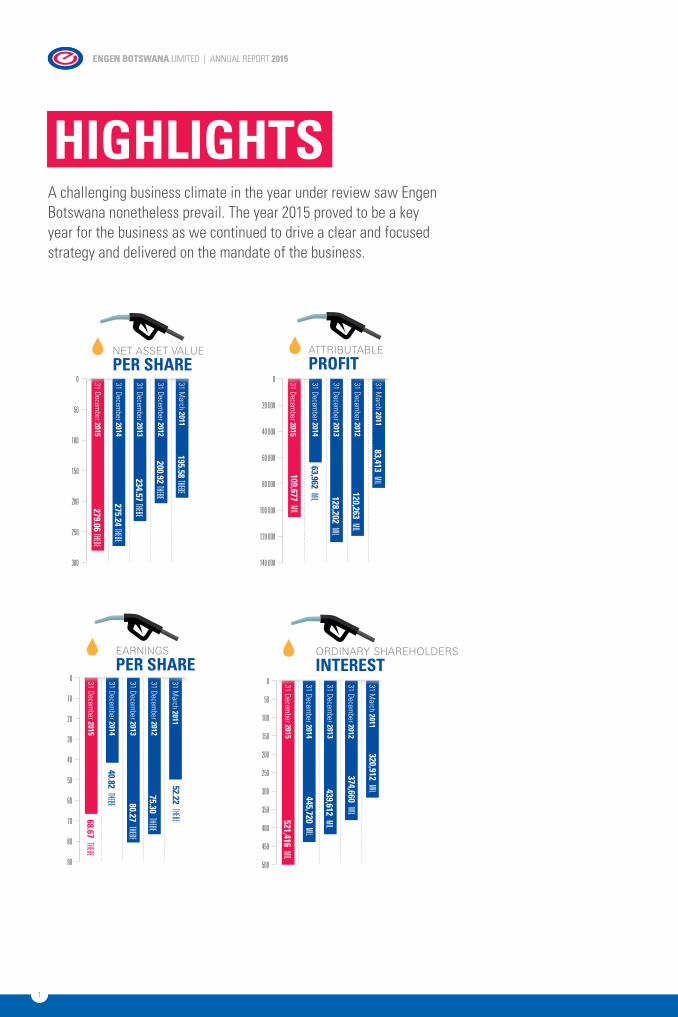

HIGHLIGHTS

Net Asset VAluePER SHARE

AttributAblePROFIT

31 December 2015

31 December 2014

31 December 2013

31 December 2012

31 March 2011

0

20 000

40 000

80 000

140 000

60 000

120 000

100 000

109,677 mil

63,962 mil 128,202 mil

120,263 mil

83,413 mil

31 December 2015

31 December 2014

31 December 2013

31 December 2012

31 March 2011

0

50

100

200

300

150

250

279.06 ThEbE

275.24 ThEbE

234.57 ThEbE

200.92 ThEbE

195.58 ThEbE

500

450

OrdiNAry shArehOldersINTEREST

31 December 2015

31 December 2014

31 December 2013

31 December 2012

31 March 2011

0

50

150

100

350

300

250

200

400

521,416 mil

445,720 mil

439,612 mil

374,660 mil

320,912 mil

eArNiNgsPER SHARE

31 December 2015

31 December 2014

31 December 2013

31 December 2012

31 March 2011

0

20

10

30

50

90

80

40

70

60

68.67 ThEbE

40.82 ThEbE 80.27 ThEbE

75.30 ThEbE

52.22 ThEbE

A challenging business climate in the year under review saw Engen Botswana nonetheless prevail. The year 2015 proved to be a key year for the business as we continued to drive a clear and focused strategy and delivered on the mandate of the business.

2

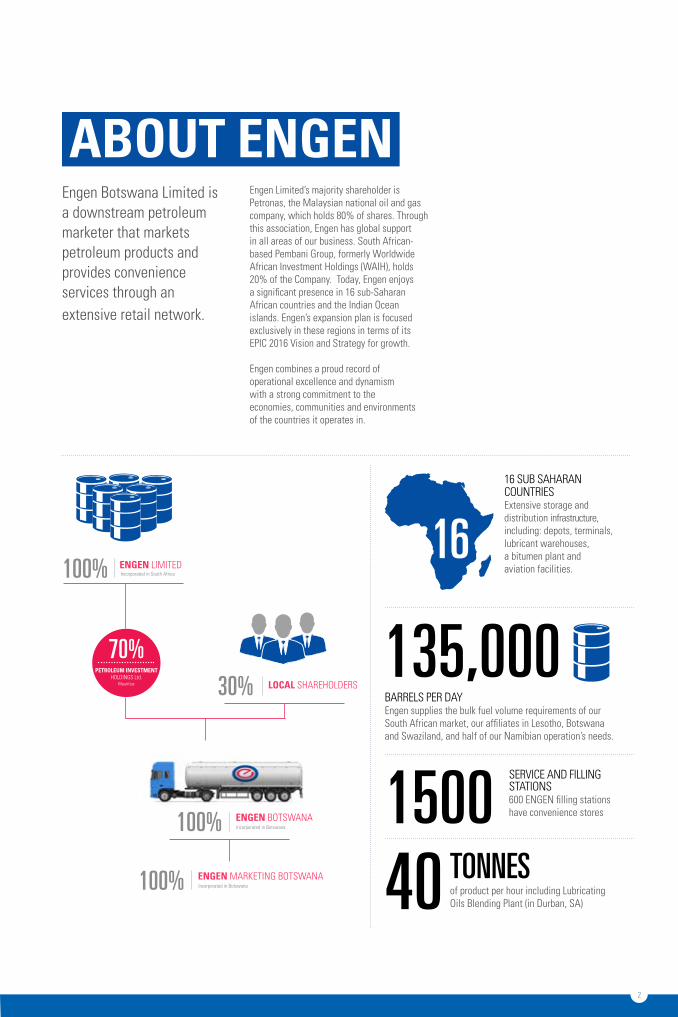

Engen Limited’s majority shareholder is Petronas, the Malaysian national oil and gas company, which holds 80% of shares. Through this association, Engen has global support in all areas of our business. South African-based Pembani Group, formerly Worldwide African Investment Holdings (WAIH), holds 20% of the Company. Today, Engen enjoys a significant presence in 16 sub-Saharan African countries and the Indian Ocean islands. Engen’s expansion plan is focused exclusively in these regions in terms of its EPIC 2016 Vision and Strategy for growth.

Engen combines a proud record of operational excellence and dynamism with a strong commitment to the economies, communities and environments of the countries it operates in.

Engen Botswana Limited is a downstream petroleum marketer that markets petroleum products and provides convenience services through an extensive retail network.

ABOUT ENGEN

100% ENGEN LIMITEDIncorporated in South Africa

70%PETROLEUM INVESTMENT

HOLDINGS Ltd.Mauritius

100% ENGEN BOTSWANAIncorporated in Botswana

30% LOCAL SHAREHOLDERS

100% ENGEN MARKETING BOTSWANAIncorporated in Botswana

1616 SUB SAHARAN COUNTRIESExtensive storage and distribution infrastructure, including: depots, terminals, lubricant warehouses,a bitumen plant and aviation facilities.

135,000BARRELS PER DAYEngen supplies the bulk fuel volume requirements of our South African market, our affiliates in Lesotho, Botswana and Swaziland, and half of our Namibian operation’s needs.

1500SERVICE AND FILLING STATIONS600 ENGEN filling stations have convenience stores

40 TONNESof product per hour including Lubricating Oils Blending Plant (in Durban, SA)

3

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

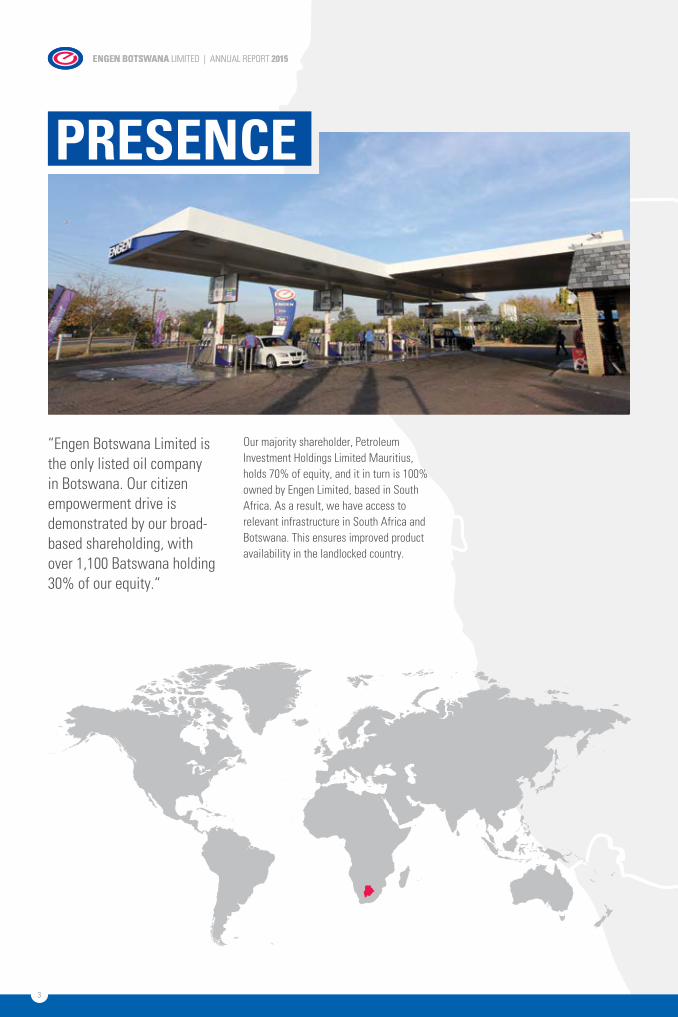

PRESENCE

“Engen Botswana Limited is the only listed oil company in Botswana. Our citizen empowerment drive is demonstrated by our broad-based shareholding, with over 1,100 Batswana holding 30% of our equity.“

Our majority shareholder, Petroleum Investment Holdings Limited Mauritius, holds 70% of equity, and it in turn is 100% owned by Engen Limited, based in South Africa. As a result, we have access to relevant infrastructure in South Africa and Botswana. This ensures improved product availability in the landlocked country.

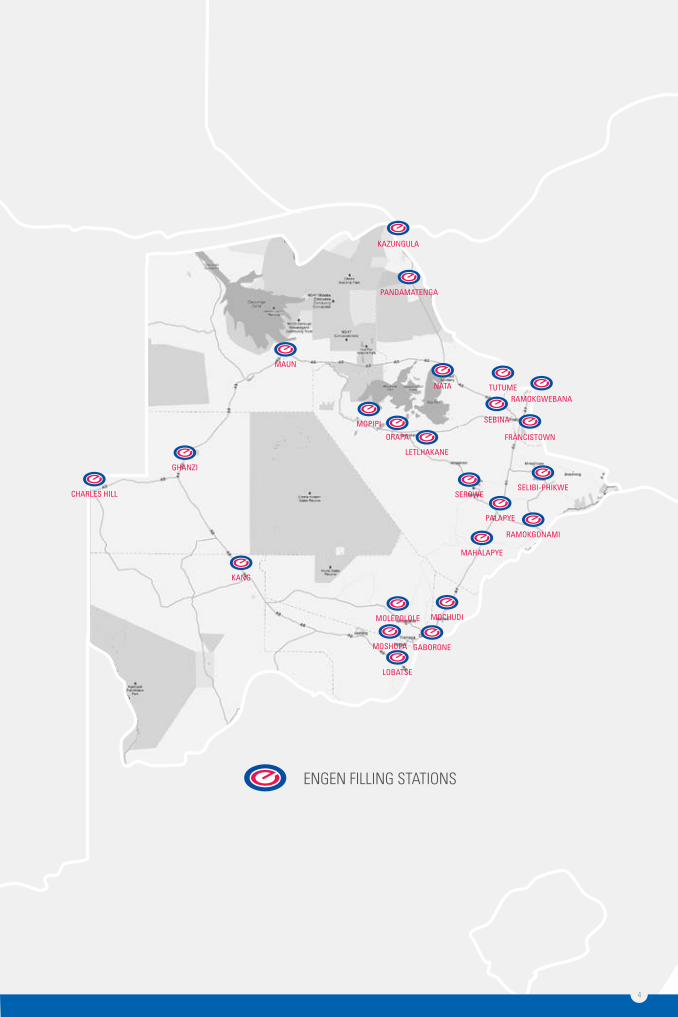

ENGEN FILLING STATIONS

KAZUNGULA

RAMOKGWEBANA

SEBINA

FRANCISTOWN

NATA

MAUN

CHARLES HILL

GHANZI

KANG

MOLEPOLOLE

MAHALAPYE

RAMOKGONAMI

PALAPYE

SELIBI-PHIKWESEROWE

MOPIPI

ORAPA

LETLHAKANE

TUTUME

LOBATSE

MOCHUDI

GABORONE

4

MOSHUPA

PANDAMATENGA

5

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

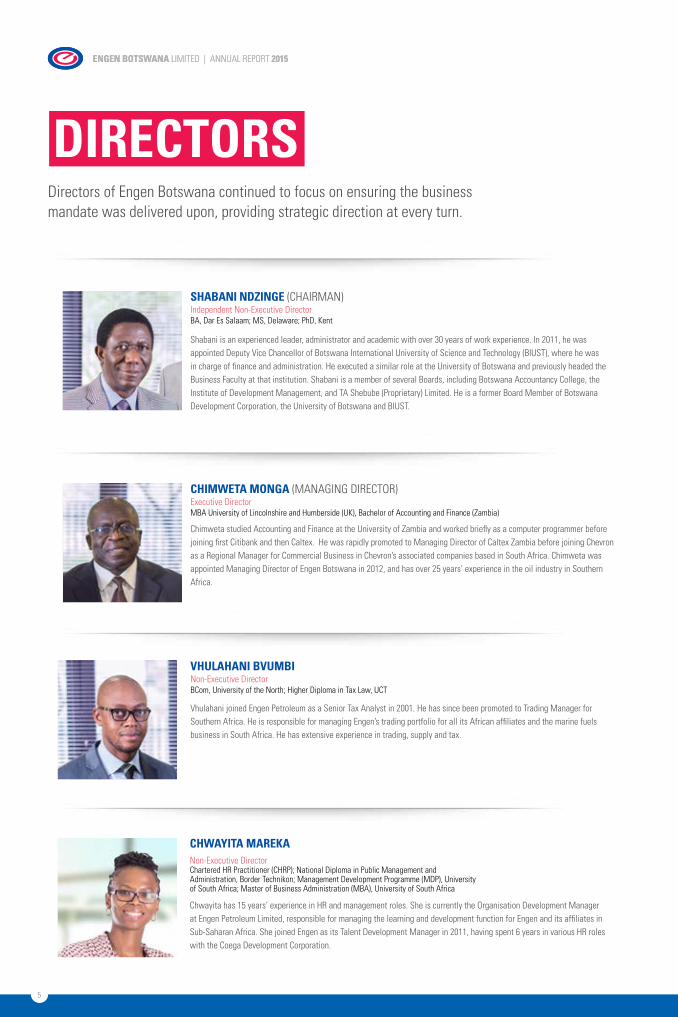

DIRECTORS

Shabani is an experienced leader, administrator and academic with over 30 years of work experience. In 2011, he was appointed Deputy Vice Chancellor of Botswana International University of Science and Technology (BIUST), where he was in charge of finance and administration. He executed a similar role at the University of Botswana and previously headed the Business Faculty at that institution. Shabani is a member of several Boards, including Botswana Accountancy College, the Institute of Development Management, and TA Shebube (Proprietary) Limited. He is a former Board Member of Botswana Development Corporation, the University of Botswana and BIUST.

SHABANI NDZINGE (CHAIRMAN)Independent Non-Executive DirectorBA, Dar Es Salaam; MS, Delaware; PhD, Kent

Chimweta studied Accounting and Finance at the University of Zambia and worked briefly as a computer programmer before joining first Citibank and then Caltex. He was rapidly promoted to Managing Director of Caltex Zambia before joining Chevron as a Regional Manager for Commercial Business in Chevron’s associated companies based in South Africa. Chimweta was appointed Managing Director of Engen Botswana in 2012, and has over 25 years’ experience in the oil industry in Southern Africa.

CHIMWETA MONGA (MANAGING DIRECTOR) Executive DirectorMBA University of Lincolnshire and Humberside (UK), Bachelor of Accounting and Finance (Zambia)

Vhulahani joined Engen Petroleum as a Senior Tax Analyst in 2001. He has since been promoted to Trading Manager for Southern Africa. He is responsible for managing Engen’s trading portfolio for all its African affiliates and the marine fuels business in South Africa. He has extensive experience in trading, supply and tax.

VHULAHANI BVUMBINon-Executive DirectorBCom, University of the North; Higher Diploma in Tax Law, UCT

Chwayita has 15 years’ experience in HR and management roles. She is currently the Organisation Development Manager at Engen Petroleum Limited, responsible for managing the learning and development function for Engen and its affiliates in Sub-Saharan Africa. She joined Engen as its Talent Development Manager in 2011, having spent 6 years in various HR roles with the Coega Development Corporation.

CHWAYITA MAREKANon-Executive DirectorChartered HR Practitioner (CHRP); National Diploma in Public Management and Administration, Border Technikon; Management Development Programme (MDP), University of South Africa; Master of Business Administration (MBA), University of South Africa

Directors of Engen Botswana continued to focus on ensuring the business mandate was delivered upon, providing strategic direction at every turn.

6

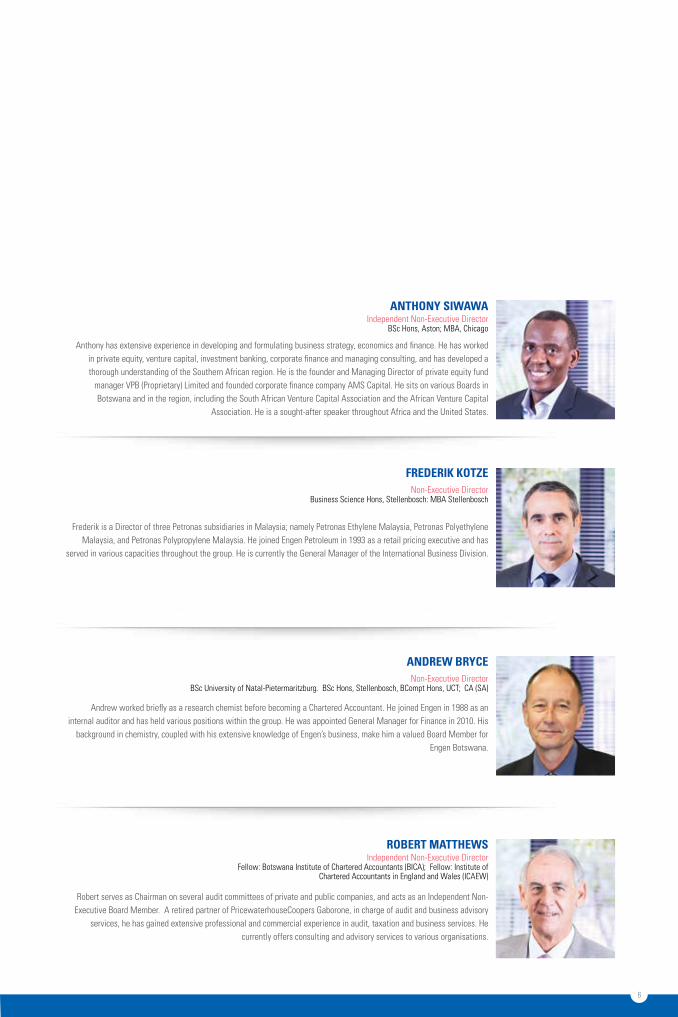

Anthony has extensive experience in developing and formulating business strategy, economics and finance. He has worked in private equity, venture capital, investment banking, corporate finance and managing consulting, and has developed a thorough understanding of the Southern African region. He is the founder and Managing Director of private equity fund

manager VPB (Proprietary) Limited and founded corporate finance company AMS Capital. He sits on various Boards in Botswana and in the region, including the South African Venture Capital Association and the African Venture Capital

Association. He is a sought-after speaker throughout Africa and the United States.

ANTHONY SIWAWAIndependent Non-Executive Director

BSc Hons, Aston; MBA, Chicago

Frederik is a Director of three Petronas subsidiaries in Malaysia; namely Petronas Ethylene Malaysia, Petronas Polyethylene Malaysia, and Petronas Polypropylene Malaysia. He joined Engen Petroleum in 1993 as a retail pricing executive and has

served in various capacities throughout the group. He is currently the General Manager of the International Business Division.

FREDERIK KOTZENon-Executive Director

Business Science Hons, Stellenbosch: MBA Stellenbosch

Andrew worked briefly as a research chemist before becoming a Chartered Accountant. He joined Engen in 1988 as an internal auditor and has held various positions within the group. He was appointed General Manager for Finance in 2010. His

background in chemistry, coupled with his extensive knowledge of Engen’s business, make him a valued Board Member for Engen Botswana.

ANDREW BRYCENon-Executive Director

BSc University of Natal-Pietermaritzburg. BSc Hons, Stellenbosch, BCompt Hons, UCT; CA (SA)

Robert serves as Chairman on several audit committees of private and public companies, and acts as an Independent Non-Executive Board Member. A retired partner of PricewaterhouseCoopers Gaborone, in charge of audit and business advisory

services, he has gained extensive professional and commercial experience in audit, taxation and business services. He currently offers consulting and advisory services to various organisations.

ROBERT MATTHEWSIndependent Non-Executive Director

Fellow: Botswana Institute of Chartered Accountants (BICA); Fellow: Institute of Chartered Accountants in England and Wales (ICAEW)

7

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

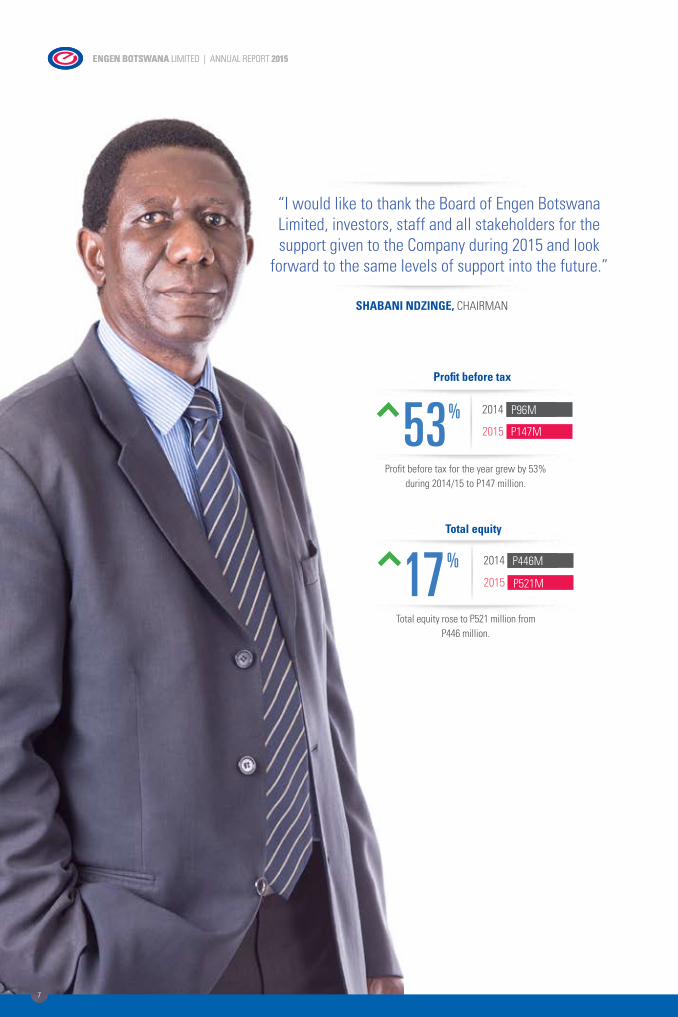

SHABANI NDZINGE, CHAIRMAN

“I would like to thank the Board of Engen Botswana Limited, investors, staff and all stakeholders for the support given to the Company during 2015 and look

forward to the same levels of support into the future.”

53Profit before tax

P96M2014

2015 P147M

Total equity

%

Profit before tax for the year grew by 53% during 2014/15 to P147 million.

Total equity rose to P521 million from P446 million.

17 P446M2014

2015 P521M

%

8

CHAIRMAN’S REPORT

SUppORTING OUR pEOpLEGrOwiNG Our iNduSTryBusiness EnvironmentThe continued slowdown of the global economy, particularly in the second half of 2015, negatively affected the Botswana economy and aggravated the challenges that confronted the country. There was a weakening in the markets for diamonds and other minerals which form a major part of Botswana’s exports. Real GDP growth for the world economy was estimated at around 3.1% in 2015, which was well below the average annual growth rate of 3.7% attained during the past 30 years.

The impact of the slow global growth resulted in reduced demand for commodities, such as oil and other minerals, thereby affecting the revenues generated by many emerging markets including Botswana.

The Botswana economy grew by only 1% in 2015 which underscores the challenges that faced the economy. Pressure on the mining, water and electricity sectors contributed to the slow domestic growth rate, which also

translated into low levels of petroleum products consumption growth. The drop in inflation from 3.8% in January to 3.1% in December 2015, was mainly driven by the reduction in fuel prices. The Government continued to maintain a stable macro- economic environment, which resulted in a relatively stable local currency and a real effective exchange rate that enabled the country to remain competitive in international markets.In the last quarter of 2015, the Government adopted the Economic Stimulus Package (ESP), a strategy designed to stimulate economic growth, promote economic diversification, and create jobs. It is expected that the ESP will support domestic economic activity in the short term while providing a foundation for a sustainable growth through infrastructural development in the long term.

Industry DevelopmentsThe State Oil Company, which was launched in 2014, started the construction of additional fuel storage facilities. This development will increase in-country fuel reserves and reduce the risk of fuel stock-outs in the event of temporary disruptions in supply from the traditional sources. This will also enable indigenous Batswana to participate in the petroleum industry. We would like to commend Government for its foresight in this regard.

During the course of 2015, a number of indigenous petroleum companies

were registered and started to operate either as importers, wholesales or retailers of petroleum products. This was very encouraging as it will provide healthy competition in this sector which had previously been dominated by international oil companies.

The Government-controlled margins continued to be very tight for most of the year under review and were not adjusted in line with inflation, rising operating expenses and high capital investment needs. This resulted in significant pressure on the profitability of the Company. In this regard, I would like to commend management for delivering outstanding results in the face of these challenges.

OutlookWe remain confident that the Botswana economy will continue to be resilient. Economic growth is expected to be around 4.2% in 2016 with expected further growth of 4.3% in 2017. We therefore continue to be positive about the growth prospects of our business in the country.

In conclusion, I would like to thank the Board of Engen Botswana Limited, investors, staff and all stakeholders for the support given to the Company during 2015 and look forward to the same levels of support into the future.

DR. S. NDZINGE, CHAIRMAN

9

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

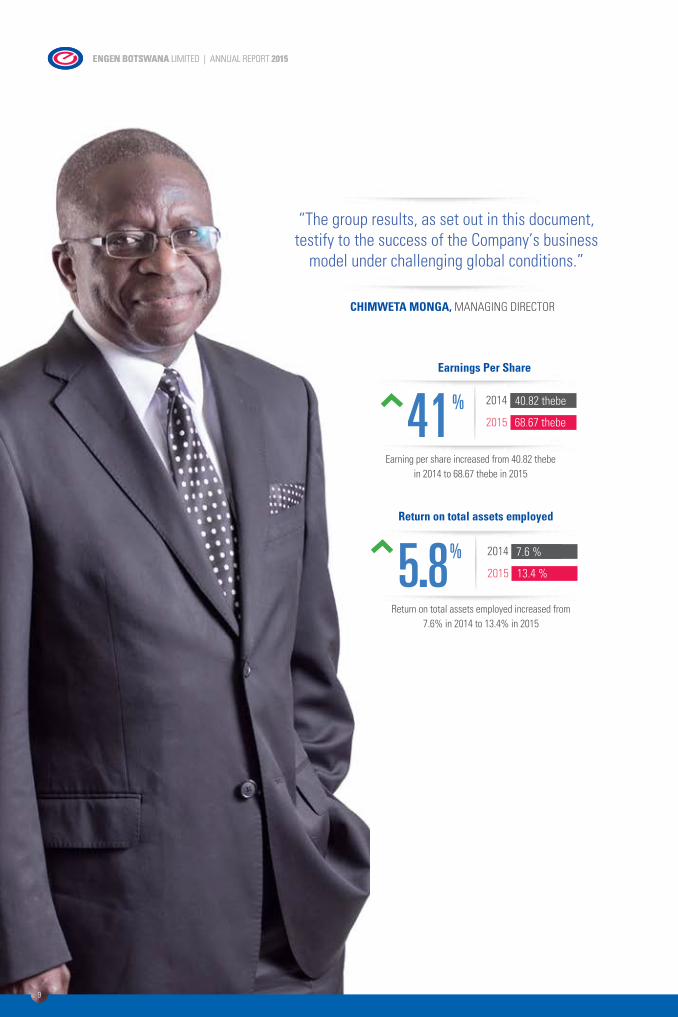

CHIMWETA MONGA, MANAGING DIRECTOR

“The group results, as set out in this document, testify to the success of the Company’s business

model under challenging global conditions.”

41Earnings Per Share

40.82 thebe2014

2015 68.67 thebe

Return on total assets employed

%

Earning per share increased from 40.82 thebe in 2014 to 68.67 thebe in 2015

Return on total assets employed increased from 7.6% in 2014 to 13.4% in 2015

5.8 7.6 %2014

2015 13.4 %

%

10

STIMULATING GROwThChampiONiNG SuSTaiNabiliTyThe 2015 financial year was a good year for Engen Botswana as we produced a robust financial performance despite the difficult economic conditions in which we operated. While the Botswana economy experienced growth of only around 1%, our sales volumes were up by around 5% and our profitability by some 68% over the previous reporting period. Our operating expenses were well managed, coming in below budget.

The group results, as set out in this document, testify to the success of the company’s business model under challenging global conditions. The group results are underpinned by a strong focus on our key values of Integrity, Performance, Team work, Empowerment and Ownership.

Macro-Economic OverviewThe continued slowdown in the global economy in 2015, and the declining demand for commodities such as diamonds, nickel and copper, intensified the economic challenges faced by Botswana. Two copper mines closed during the year, one of which, as a major commercial customer of Engen Botswana, had a direct, significant impact on our financial results. There were also issues around the electricity supply, particularly in the early part of the year. We are grateful to government that they have been able to address this issue.

Also contributing to our economic challenges was the ongoing drought which affected agricultural production. As this sector is a major consumer of petroleum products, this also had an impact on the performance of the company.

Estimated GDP growth for the country for the year under review was only 1% compared to 3.4% in 2014. This led to Government adopting an Economic Stimulus Package (ESP) in the last quarter of 2015 in order to boost economic growth, promote economic diversification, and create jobs. The results of the ESP are likely to be felt in 2016 with anticipated GDP growth of about 4.2%.

Meanwhile, headline inflation fell from 3.8% in December 2014 to 3.1% a year later. The bank rate reduced from 6.5% in January 2015 to 6.0% in August 2015.

MD’S REPORT

11

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

Industry DevelopmentsThis industry is experiencing high – and accelerating – levels of competition. As at the end of June 2015, in excess of 80 indigenous petroleum companies had been registered by Government agencies. Government is being encouraged by the oil industry to properly licence these entities so that their activities are adequately regulated and they fall within the slate and tax net. We are also advocating that all petroleum companies be subjected to the same technical quality standards for equipment and storage. International companies like ours maintain the highest international standards and best practices designed to protect workers within the industry, consumers of petroleum products and the environment from hazards such as undetected leaks.

While there was some decline in international crude oil prices, the decline was not as severe as it was in 2014 which resulted in substantial inventory revaluation losses at the time. The industry continued to individually lobby Government to improve allowed margins in order to ensure the continued financial viability of the oil marketing companies operating in Botswana.

OperationsOur Retail division experienced growth in all its activities. We brought two new service stations on stream. This includes Mmamashia, which is already one of the biggest contributors to our sales volumes, and a smaller operation at Moshupa. Several new service stations are scheduled to come on stream during the course of 2016. We also improved our alternative profit opportunities such as our Quickshops and Corner Bakeries.I am particularly proud of the high levels of service we continued to offer at our service stations where we were rated among the top three in Engen’s international business division. This means that we are meeting the expectations of motorists and building goodwill around our brand.

Our Commercial division had a difficult year in that its customers, particularly in the mining, construction and agricultural sectors, were all adversely affected by the global and local economic conditions. The closure of two copper mines was the most dramatic manifestation of this. However, we also noticed a significant reduction in purchases of petroleum products from across the board, a clear indication of a general scaling back of economic activity.

We made a concerted effort to find alternative customers for our products, and strengthened our distribution channel to assist in this regard. The strategy paid dividends and the efforts of these distributors somewhat helped to offset the loss of our traditional mining customers. Our distribution partners also played a significant role in growing our sales of lubricants.

Supplies into the country were relatively stable during the year, thanks largely to our decision to bring product in from diverse locations within South Africa. We also piloted the importation of product from Beira, Mozambique, as a backup to potential future disruptions of supply in South Africa. This was successful and we are now considering increasing the volume of product imported from Mozambique. While these can be accommodated on an ad hoc basis, we will have to iron out issues around the pricing structures with Government before we can utilise the Mozambique route on a more regular basis.

We have engaged our HR partners to try and see how we can improve our retention and motivation of staff and I am confident that we will make progress in this regard in the year ahead.

12

Looking aheadWe anticipate an improved economic environment for Botswana in 2016. We are confident that the planned growth of our retail network will enable us to conduct a sustainable business going forward. We will continue to realign our strategy to take advantage of opportunities in the retail sector. The uneven playing field in the largely unregulated commercial sector makes it increasingly difficult for international players to remain viable in this space. Nevertheless, while we continue to focus on retail expansion and innovation, we will also seek out commercial customer value adding solutions. Standardisation of our operations in line with international best practices, and prudent management of operating expenses, will remain the cornerstones of our business in Botswana as we strive to maintain our position as one of the leading petroleum companies in the country.

We recognise the commitment of our investors to the Company, and therefore one of our key objectives is to ensure that the Company delivers long term, sustainable and robust performance and value to our shareholders through leverage on technology, people, know-how and strong partnerships.I would like to take this opportunity to thank our valued customers, suppliers, shareholders and all other stakeholders for their on-going support which contributed towards the success of Engen Botswana. My thanks also go to the management and staff for their tremendous effort during the year to ensure that we maintained our position as one of the leading petroleum

companies in Botswana.

“I would like to take this opportunity to thank our valued customers, suppliers, shareholders and all other stakeholders for their on-going support which contributed towards the success of Engen Botswana. My thanks also go to the management and staff for their tremendous effort during the year to ensure that we maintained our position as one of the leading petroleum companies in Botswana.”

ThANkS.

MR. C. MONGA, MANAGING DIRECTOR

13

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

FINANCIAL RESULTS

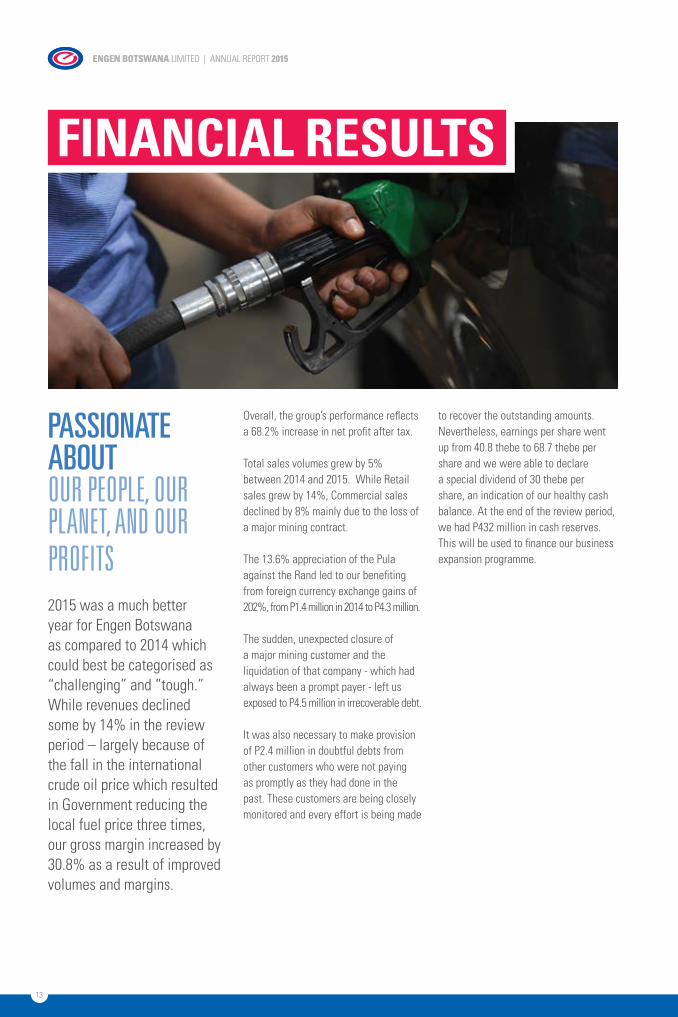

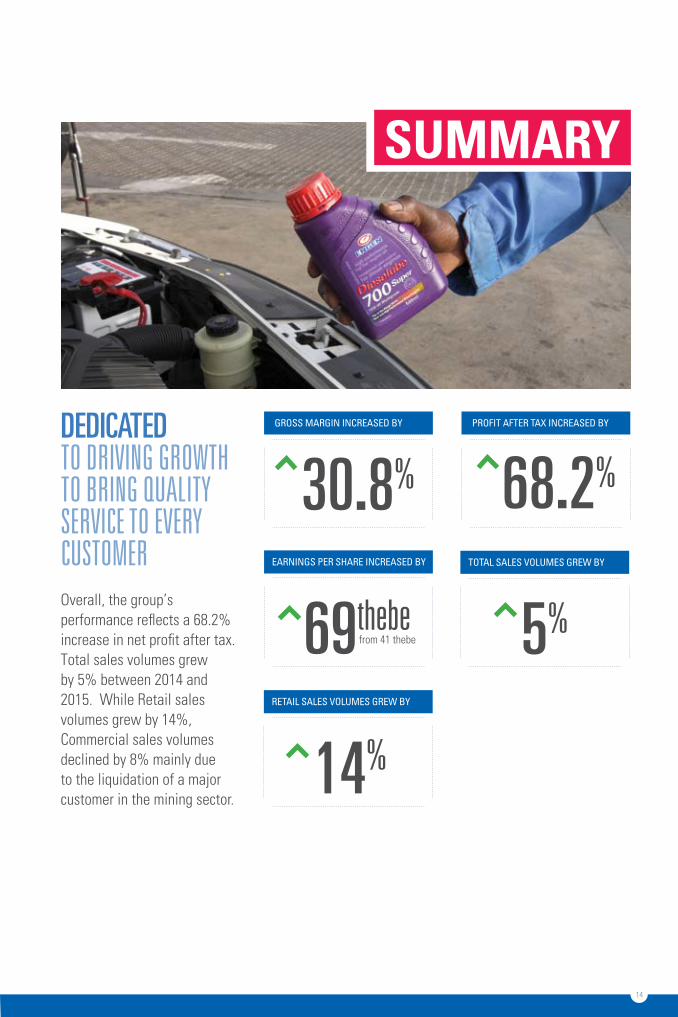

pASSIONATE AbOUTOur pEOplE, Our plaNET, aNd Our prOfiTS2015 was a much better year for Engen Botswana as compared to 2014 which could best be categorised as “challenging” and “tough.” While revenues declined some by 14% in the review period – largely because of the fall in the international crude oil price which resulted in Government reducing the local fuel price three times, our gross margin increased by 30.8% as a result of improved volumes and margins.

Overall, the group’s performance reflects a 68.2% increase in net profit after tax.

Total sales volumes grew by 5% between 2014 and 2015. While Retail sales grew by 14%, Commercial sales declined by 8% mainly due to the loss of a major mining contract.

The 13.6% appreciation of the Pula against the Rand led to our benefiting from foreign currency exchange gains of 202%, from P1.4 million in 2014 to P4.3 million.

The sudden, unexpected closure of a major mining customer and the liquidation of that company - which had always been a prompt payer - left us exposed to P4.5 million in irrecoverable debt.

It was also necessary to make provision of P2.4 million in doubtful debts from other customers who were not paying as promptly as they had done in the past. These customers are being closely monitored and every effort is being made

to recover the outstanding amounts.Nevertheless, earnings per share went up from 40.8 thebe to 68.7 thebe per share and we were able to declare a special dividend of 30 thebe per share, an indication of our healthy cash balance. At the end of the review period, we had P432 million in cash reserves. This will be used to finance our business expansion programme.

14

30.8%

GROSS MARGIN INCREASED BY

69thebe

EARNINGS PER SHARE INCREASED BY

from 41 thebe

PROFIT AFTER TAx INCREASED BY

5%

TOTAL SALES vOLUMES GREW BY

14%

RETAIL SALES vOLUMES GREW BY

DEDICATEDTO driviNG GrOwTh TO briNG qualiTy SErviCE TO EvEry CuSTOmErOverall, the group’s performance reflects a 68.2% increase in net profit after tax. Total sales volumes grew by 5% between 2014 and 2015. While Retail sales volumes grew by 14%, Commercial sales volumes declined by 8% mainly due to the liquidation of a major customer in the mining sector.

SUMMARY

68.2%

15

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

SUSTAINABILITY

MINDFUL OFhEalTh, SafETy, ENvirONmENT, aNd qualiTyHealth, safety and environmental matters continue to hold a central position within Engen Botswana as components of the three main pillars of sustainability: people, planet and profit.

Everything we do, indeed every project we undertake, is referenced against the impact this will have on our people – our employees, our customers and the communities in which we operate; our planet – the environment in which we work and for which we have an inalienable obligation to promote and protect; and our profits – recognising that a sustainable business is not possible without being in harmony with the other two pillars of sustainability.

We strive to ingrain our international parent company’s Health, Safety, Environment and Quality (HSEQ) protocols into our daily activities despite the fact that the financial implications of some of these requirements can be substantial. We recognise that maintaining the very highest health, safety and environment protection standards in the world is non-negotiable for any organisation that regards itself as a good corporate citizen.

The introduction of our LOPC (Loss of Primary Containment) programme in 2014 yielded excellent results in 2015,

with not a single major spill reported. A single accidental contamination incident occurred at one of our service stations, but this was quickly rectified before any significant damage occurred.

Environmental Health and SafetyRecognising that we work in a high-risk industry as far as the health and safety of our employees, suppliers and customers is concerned, we make considerable strides in implementing all the elements of the Mandatory Control Framework (MFC) management system. We employed external consultants to conduct a health risk assessment which was designed to determine the concentration of airborne contaminant concentrations within our operational sites including our depot, warehouse, office and retail sites.

Consultants were also charged with identifying any other potential health hazards in respect of the Occupational Health and Safety Act, as well as developing a comprehensive legal register and protocols for all our operational sites.

16

In addition, all employees who are exposed to airborne contamination underwent two routine health checks during the review period, neither of which produced anything untoward. Similar health checks will be extended to other staff members during the current financial year.

On the safety front, we conducted a Crisis Management exercise at the Dumela depot in Francistown during the year. This simulation exercise also included participants from Botswana Oil, Vivo Energy, Puma, transporters, MedRescue and the Botswana Police. It was designed to test our response to an emergency situation and evaluate how effective our emergency response plan is.

The outcome of this exercise was satisfactory. Training of our people in fire fighting, first aid and other emergency procedures will be ongoing.

The winner of the Mochudi Farmers’ Dream draw receiving the tractor keys.

The winner of the Francistown draw posing with his family.

17

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

COMMERCIAL

CLEAR FOCUSuNparallElEd dEdiCaTiON2015 was an exceptionally difficult year for the Commerical division and the fall in global demand for commodities had a devastating effect on the mining industry. This saw many mines being forced to cut production and one of our largest customers going into liquidation in February 2015.

The construction industry was also under pressure, with Government postponing several major infrastructure developments due to the depressed economy. This resulted in lower demand for both fuels and lubricants.

Despite this, there were also several positive developments which augur well for the future of the division.

Foremost among these was the introduction of two fuel distributors as an additional marketing channel. Both distributors purchased significant quantities of diesel and this, coupled with organic growth and other new business, went some way to ameliorate the loss of the major mining customer, which had previously accounted for a significant percentage of diesel sales.

The loss of this account, however, and the difficulties experienced by our other mining customers, had a ripple effect on lubricants, which experienced a 17% reduction in sales volume compared to the previous review period. This result was mitigated by concerted efforts of our lubricants distributor whose purchases increased by some 42% over the previous year. Joint sales promotions with the distributor also helped to cushion the losses resulting from the closure of the large mining customer.

Another positive development in the review period was the 9% growth in petrol sales year-on-year. This can be attributed largely to organic growth in sales to some commercial customers.

18

Kerosene sales were satisfactory during the review period while sales of LPG rose by some 30% year-on-year. This excellent result could have been even better had we not experienced stock shortages in March, July and August as a result of unplanned refinery shutdowns.

Looking ahead, we will continue to aggresively market our products in the commercial sector, with a particular focus on lubricants. We will continue to seek innovative ways of growing both sales and profits. We are also positioning ourselves to benefit from the announcement by Government regarding the P88 billion Economic Stimulus Package (ESP) which will focus on construction, agricultural production and manufacturing – these are all areas in which we are active.

19

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

PROPERTY

SENSITIVE TOwARDSThE ClimaTE wE wOrk iNDuring the year under review, we were able to stream two of our planned developments, one of which, Mmamashia, rapidly rose to become a star performer in our portfolio following its opening in early 2015. The Mmamashia Quickshop and Corner Bakery also did exceptionally well.

A second new service station in Moshupa had a more difficult passage because of a delay in opening the rest of the adjacent shopping centre.

Several of our sites were revamped during the review period:

• Kazungula – upgraded forecourt and new Corner Bakery installed (complete)

• Mopipi – oxygenation of storage tanks (complete)

• Tlokweng – feeder canopies installed (complete)

• Lobatse – feeder canopies installed (complete)

We also took over the Pandamatenga service station early in 2015, but plans to rebrand it as an Engen site were delayed pending the approval of an Environmental Impact Assessment.

Looking ahead, we have several new projects scheduled for completion in 2016. This will include revamping several of our long-term lease sites as well as the opening or acquisition of new service stations.

Our shopping centres in Maun and Palapye both performed extremely well, maintaining 100 percent occupancy throughout the review period.

20

DISTRIBUTION

ExpERTS IN OUR FIELDwiTh a STrONG NETwOrk TO kEEp ThiNGS mOviNG2015 was characterised by fairly stable supplies of bulk product, with product being procured from a wider range of sources both in South Africa – Tarlton and Langlaagte as well as Durban; and from Beira in Mozambique.

These were supplemented by supplies from Botswana Oil when necessary, such as during the Botswana Unified Revenue Services (BURS) strike. This strike negatively affected our road fleet turnaround between Botswana and South

Africa, although rail was not affected.

Most importantly, we were able to continue to supply our Commercial and

Retail customers without interruption.

Our excellent relationship with our transporter continued throughout the year. The number of vehicles was reduced during April to align with business plans, but the transporter increased the number of vehicles in the operation during December to cater for increased demand. Despite the large number of trucks on the road at any one time, there were no serious incidents reported.

There were also very minimal operational losses at our depots and what little there was remained within tolerance.

21

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

STRATEGIC FOCUSON GrOwTh aNd pErfOrmaNCE imprOvEmENT2015 was a very good year for the Retail division, both on our forecourts and in our convenience stores. We experienced year-on-year fuel volume growth of 13.9% and outperformed our target buy 6.2% in the face of increasingly robust competition. Our Quickshops’ turnover rose by 9% and Corner Bakery grew by an impressive 29%.

This excellent performance can be attributed to several factors:

1. PromotionsWe ran several promotions throughout the year including dealer incentives and our flagship Farmers’ Dream Win-a-Tractor promotion. There were also continuous promotions at our convenience stores. All promotions produced good results in terms of volumes sold. They also served to build our brand amongst consumers

2. Credit ManagementWe continued to pursue a prudent credit management strategy that encourages and rewards dealers for timely payment. Synchronisation between our credit management and distribution systems ensured the availability of our products on our forecourts at all times.

3. Product availabilityThe automatic replenishment of stock based on analysis of the daily sales at each petrol station ensured sites never ran dry. This proved particularly beneficial at times of extremely high demand such as December ,when we outperformed our target by a wide margin.

4. Service excellenceOur SMILE programme, which defines how our customers must be served, continued to differentiate Engen from our competitors. Every site was visited by a mystery shopper each month; reports on the service provided were analysed and remedial action such as additional training, was taken where necessary. Social media was also monitored for positive and negative feedback and attendants were rewarded and incentivised for providing good service. During the review period, we maintained our position as one of the top three of all Engen’s international operations in terms of service, with an overall service rating of 72%.

5. Clean FuelsThe introduction of cleaner fuels undoubtedly helped to increase sales. There was a marked increase in the number of new passenger motor vehicles with diesel engines which require cleaner fuels.

RETAIL RESULTS

22

Our fast food partnerships with Wimpy and Barcelos also performed well in the review period. A highlight of 2015 was the launch of our mobile App. Once consumers downloaded the App to their smartphone, they were informed about all the promotions taking place at Engen service stations, as well as at our Quickshops and Corner Bakeries. It also informed drivers of the distance and location of the next or closest Engen filling station, enabling them to plan their journeys with confidence. In the first few months following its launch in mid-2015, the App was downloaded more than 300 times – an outstanding performance for what was, essentially, a pilot phase of the project.

During the 2016 year, additional functionality will be added to the App including an ability to track one’s fuel consumption. This is likely to drive greater utilisation of the App.

Looking ahead, there are several exciting developments planned for all aspects of the Retail business in 2016, from expanding our Corner Bakery offering to potentially introducing a payment card for use at all our sites.

Several new filling stations are also planned to come on stream in the ensuing financial year. The locations of these have been carefully chosen as we remain acutely aware that filling stations are proliferating across the country. The challenge for Engen, therefore, will be to ensure we take proactive steps to remain ahead of the competition.

23

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

HUMAN RESOURCES

GROwING OUR pEOpLESTrENGThENiNGOur TEamEvery business requires skilled, motivated and well trained people if it is to fulfil its mandate to all its stakeholders. However, in an environment in which competition for skills is fierce, recruiting and retaining the right calibre of employee remains a perpetual challenge.

At the end of the review period, our staff complement stood at 42 permanent employees and a further six on fixed-term contracts.

The challenges we face in retaining and recruiting appropriately skilled personnel are addressed through an integrated Talent Management Programme which incorporates the provision of training and development opportunities. During the review period, virtually every employee underwent at least one training programme, either to ensure their skills remain current within their respective areas of operation, or to prepare them for growth and promotion opportunities within the organisation. New recruits received training on operational and system requirements, improving their productivity and quality of output as quickly as possible.

During the review period, one manager completed the Executive Development Programme at the University of Cape Town Graduate School of Business, while two new members of the management

committee completed a contracting workshop. The latter had previously been completed by other members of the committee.

Despite the fact that our salary structure is largely determined by our international parent company, we strive to ensure that our remuneration is market related while simultaneously offering value-adding employee benefits. Our participation in the Mercer annual salary survey ensured we remained abreast of remuneration trends in Botswana.

Our ongoing focus on wellness – physical, mental and financial – was appreciated by employees. Corporate wellness sessions focusing on education as well as screening for chronic health conditions were held quarterly at all sites during the review period. This was supplemented by a comprehensive Wellness Day that enabled employees to engage with a host of wellness providers offering services in everything from personal hygiene and weight control to substance abuse, oral health and family health.

24

DRIVING IMpACTiN Our COmmuNiTiESThere is no question that the future of any country, and the sustainability of its economy, is largely dependent on the quality of education available to its children.

Engen Botswana is therefore honoured to have been able to make a contribution to this through our three-year collaboration with the Ministry of Education & Skills Development and the Sebilo Book Services. The programme we were fortunate to be a part of saw the provision of library facilities to disadvantaged schools.

During the review period, we “adopted” the Kgomodiatshaba Primary School in the remote Kgatleng District. We assisted with the conversion of two offices, previously used by the villagers as reading rooms, into a fully equipped library facility. This entailed painting the walls, tiling the floor, and providing both shelving and an effective air conditioning unit.

The library was then equipped with computers loaded with educational software, and educational books. We further worked to develop an inviting children’s corner kitted out with comfortable cushions, child-sized tables and chairs, books, and learning and playing materials. The aim was to create a warm, encouraging environment in which children could truly benefit from the joy of learning and reading. These efforts are just one testament to our unwavering dedication towards championing sustainable community development across Botswana.

COrpOrAte sOCiAl

RESPONSIBILITY

25

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

GOVERNANCE

The Directors believe that effective corporate governance is an essential requirement for the successful realisation of Engen Botswana’s business objectives. The Board is committed to the principles of openness, integrity and high ethical standing in the fulfilment of Engen Botswana’s corporate responsibilities.

The Group is committed to the highest standards of corporate governance and is working towards full implementation of the King III Code of Corporate Governance. We have been able to implement some of the recommendations already as we comply with all international accounting regulations and the Engen Group standardises best practices in corporate governance while being sensitive to country context.

Engen also has its own code of ethics which substantially complies with the recommendations contained in the King III Report and continues to review areas requiring further attention.

The following information is provided to give our stakeholders a better appreciation of Engen Botswana’s current procedures to ensure a high standard of corporate governance.

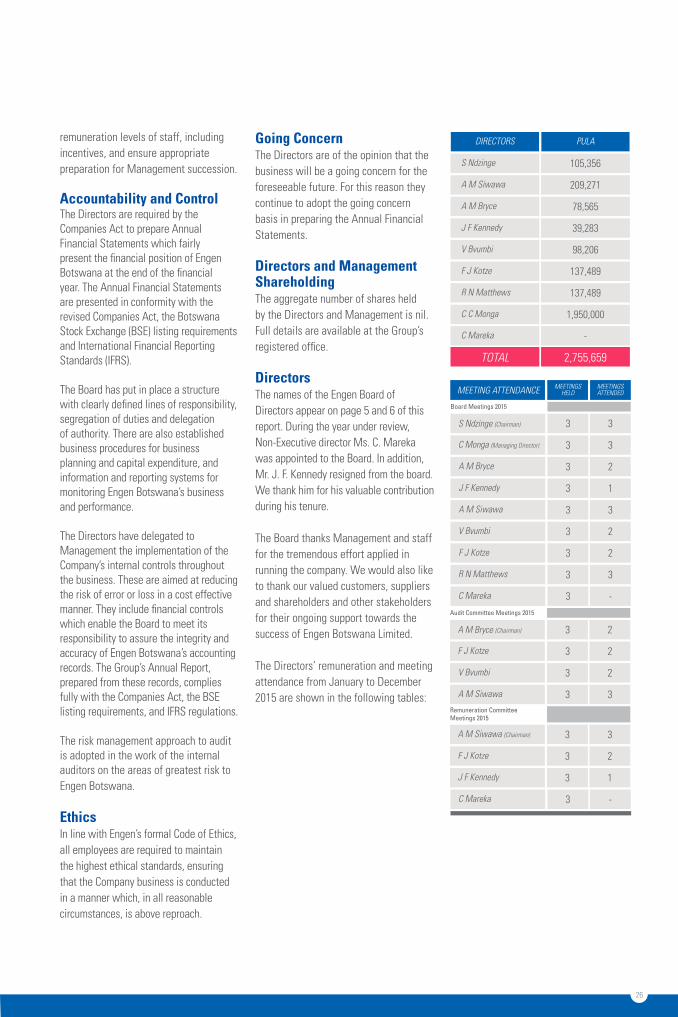

Board and Committee StructureThe Engen Botswana Board is comprised of seven Non-Executive and one Executive Director and meets at least three times a year. Dr. Shabani Ndzinge is the Chairman of the Board. All Non-Executive Directors have a wide range of skills and significant commercial and other experience, enabling them to bring independent judgment to Board deliberations and decisions. The Directors have access to the advice and services of the Company Secretary and are entitled at the Company’s expense to seek independent professional advice regarding the business.

The Management Committee is chaired by Chimweta Monga, the Managing

Director, and includes all of the Group’s divisional managers. The Management Committee meets at least eleven times a year and deals with all operational, business and strategic development issues of the Group not specifically reserved for the Board.

The Audit Committee is comprised of four Non-Executive Directors, chaired by Andrew Bryce, and meets at least twice a year. The Audit Committee is regulated by specific terms of reference, which include the reviewing of the effectiveness of the Company’s internal controls, the monitoring and approval of accounting policies, corporate governance matters, and financial reporting. The Audit Committee receives reports from the Company’s internal and external auditors who attend its meetings and who have unrestricted access to the Chairman and Audit Committee members. This ensures their independence is in no way impaired.The Remuneration Committee comprises of three Non-Executive directors and is chaired by Anthony Siwawa. It meets at least twice a year. Its mandate is to regulate policy, approve senior management appointments and compensation, determine the

26

remuneration levels of staff, including incentives, and ensure appropriate preparation for Management succession.

Accountability and ControlThe Directors are required by the Companies Act to prepare Annual Financial Statements which fairly present the financial position of Engen Botswana at the end of the financial year. The Annual Financial Statements are presented in conformity with the revised Companies Act, the Botswana Stock Exchange (BSE) listing requirements and International Financial Reporting Standards (IFRS).

The Board has put in place a structure with clearly defined lines of responsibility, segregation of duties and delegation of authority. There are also established business procedures for business planning and capital expenditure, and information and reporting systems for monitoring Engen Botswana’s business and performance.

The Directors have delegated to Management the implementation of the Company’s internal controls throughout the business. These are aimed at reducing the risk of error or loss in a cost effective manner. They include financial controls which enable the Board to meet its responsibility to assure the integrity and accuracy of Engen Botswana’s accounting records. The Group’s Annual Report, prepared from these records, complies fully with the Companies Act, the BSE listing requirements, and IFRS regulations.

The risk management approach to audit is adopted in the work of the internal auditors on the areas of greatest risk to Engen Botswana.

EthicsIn line with Engen’s formal Code of Ethics, all employees are required to maintain the highest ethical standards, ensuring that the Company business is conducted in a manner which, in all reasonable circumstances, is above reproach.

Going ConcernThe Directors are of the opinion that the business will be a going concern for the foreseeable future. For this reason they continue to adopt the going concern basis in preparing the Annual Financial Statements.

Directors and Management ShareholdingThe aggregate number of shares held by the Directors and Management is nil. Full details are available at the Group’s registered office.

DirectorsThe names of the Engen Board of Directors appear on page 5 and 6 of this report. During the year under review, Non-Executive director Ms. C. Mareka was appointed to the Board. In addition, Mr. J. F. Kennedy resigned from the board. We thank him for his valuable contribution during his tenure.

The Board thanks Management and staff for the tremendous effort applied in running the company. We would also like to thank our valued customers, suppliers and shareholders and other stakeholders for their ongoing support towards the success of Engen Botswana Limited.

The Directors’ remuneration and meeting attendance from January to December 2015 are shown in the following tables:

MEETING ATTENDANCE MEETINGS MEETINGSHELD ATTENDED

S Ndzinge (Chairman)

Board Meetings 2015

3

3

3

3

3

2

3

1

C Monga (Managing Director)

A M Bryce

J F Kennedy

A M Bryce (Chairman)

A M Siwawa (Chairman)

Audit Committee Meetings 2015

Remuneration CommitteeMeetings 2015

3

3

3

3

3

3

3

3

3

3

2

3

2

1

2

2

3

2

2

3

F J Kotze

F J Kotze

V Bvumbi

J F Kennedy

A M Siwawa

V Bvumbi

F J Kotze

R N Matthews

3 3A M Siwawa

DIRECTORS

S Ndzinge

A M Siwawa

A M Bryce

J F Kennedy

V Bvumbi

F J Kotze

R N Matthews

PULA

105,356

209,271

78,565

39,283

98,206

137,489

137,489

TOTAL 2,755,659

C C Monga 1,950,000

C Mareka -

3 -C Mareka

3 -C Mareka

27

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

ThE hUb OF bOTSwANA’S TOp miNdS pOSiTiONEd fOr SuCCESSAt Engen, we pride ourselves in bringing Botswana’s captains of industry, who hold the wisdom, credentials and passion to lead our people to drive both results and innovation. With backgrounds derived from a variety of different corporate cultures and experiences, our strong leaders and champions of the Engen Botswana brand are committed towards ensuring that each and every customer experience transcends the level of excellence even they may expect.

MANAGEMENT

THUSO PULEDistribution Manager

PAUL SHABANEHealth, Safety, Environment and Quality (HSEQ) Manager

BRIAN SAMEKEFinance Manager

FRANCINAH TSWAIHuman Capital Manager

CHIMWETA MONGAManaging Director

SANDY MFOSICommercial Manager

BOBBY TLHABIWERetail Manager

ISHMAEL MBULAWAProperty Manager

28

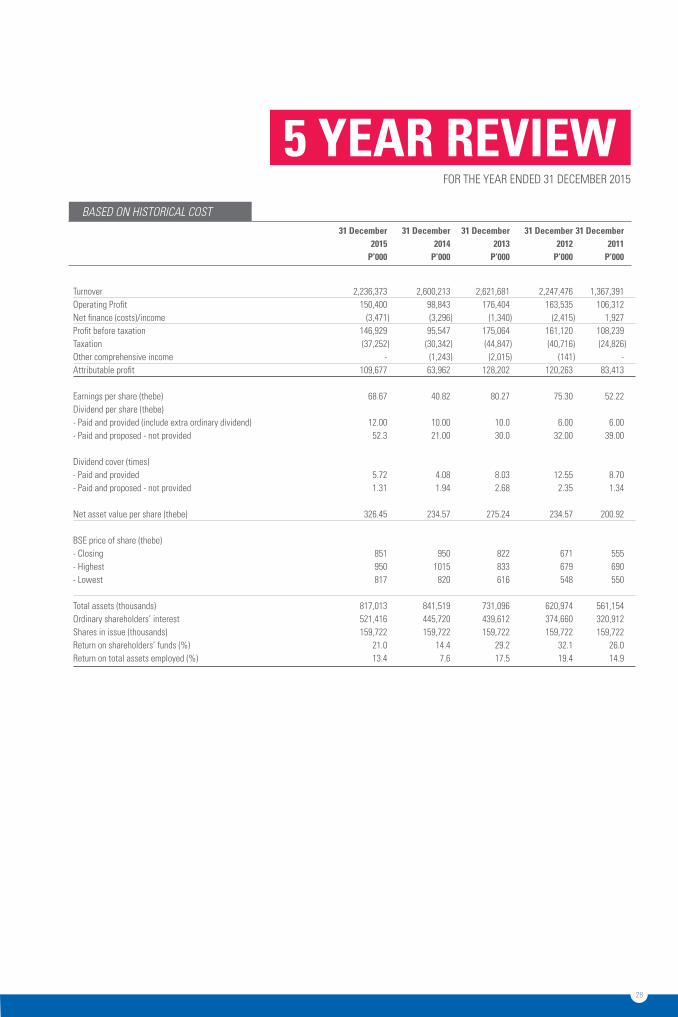

5 YEAR REVIEWBASED ON HISTORICAL COST

Turnover 2,236,373 2,600,213 2,621,681 2,247,476 1,367,391 Operating Profit 150,400 98,843 176,404 163,535 106,312 Net finance (costs)/income (3,471 ) (3,296 ) (1,340 ) (2,415 ) 1,927 Profit before taxation 146,929 95,547 175,064 161,120 108,239 Taxation (37,252 ) (30,342 ) (44,847 ) (40,716 ) (24,826 )Other comprehensive income - (1,243 ) (2,015 ) (141 ) - Attributable profit 109,677 63,962 128,202 120,263 83,413 Earnings per share (thebe) 68.67 40.82 80.27 75.30 52.22 Dividend per share (thebe) - Paid and provided (include extra ordinary dividend) 12.00 10.00 10.0 6.00 6.00 - Paid and proposed - not provided 52.3 21.00 30.0 32.00 39.00 Dividend cover (times) - Paid and provided 5.72 4.08 8.03 12.55 8.70 - Paid and proposed - not provided 1.31 1.94 2.68 2.35 1.34 Net asset value per share (thebe) 326.45 234.57 275.24 234.57 200.92 BSE price of share (thebe) - Closing 851 950 822 671 555- Highest 950 1015 833 679 690- Lowest 817 820 616 548 550 Total assets (thousands) 817,013 841,519 731,096 620,974 561,154 Ordinary shareholders’ interest 521,416 445,720 439,612 374,660 320,912 Shares in issue (thousands) 159,722 159,722 159,722 159,722 159,722 Return on shareholders’ funds (%) 21.0 14.4 29.2 32.1 26.0 Return on total assets employed (%) 13.4 7.6 17.5 19.4 14.9

31 December 31 December 31 December 31 December 31 December 2015 2014 2013 2012 2011 P’000 P’000 P’000 P’000 P’000

FOR THE YEAR ENDED 31 DECEMBER 2015

29

ENGEN BOTSWANA LIMITED | ANNUAL REPORT 2015

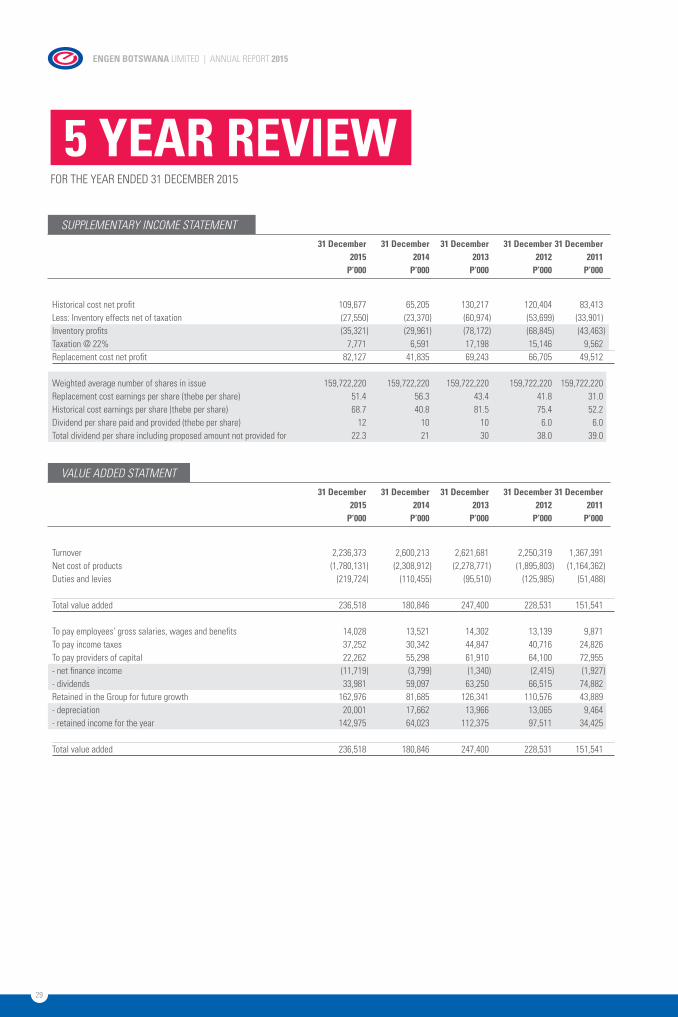

SUPPLEMENTARY INCOME STATEMENT

Historical cost net profit 109,677 65,205 130,217 120,404 83,413 Less: Inventory effects net of taxation (27,550 ) (23,370 ) (60,974 ) (53,699 ) (33,901) Inventory profits (35,321 ) (29,961 ) (78,172 ) (68,845 ) (43,463 )Taxation @ 22% 7,771 6,591 17,198 15,146 9,562 Replacement cost net profit 82,127 41,835 69,243 66,705 49,512 Weighted average number of shares in issue 159,722,220 159,722,220 159,722,220 159,722,220 159,722,220 Replacement cost earnings per share (thebe per share) 51.4 56.3 43.4 41.8 31.0 Historical cost earnings per share (thebe per share) 68.7 40.8 81.5 75.4 52.2 Dividend per share paid and provided (thebe per share) 12 10 10 6.0 6.0 Total dividend per share including proposed amount not provided for 22.3 21 30 38.0 39.0

31 December 31 December 31 December 31 December 31 December 2015 2014 2013 2012 2011 P’000 P’000 P’000 P’000 P’000

5 YEAR REVIEWFOR THE YEAR ENDED 31 DECEMBER 2015

VALUE ADDED STATMENT

Turnover 2,236,373 2,600,213 2,621,681 2,250,319 1,367,391 Net cost of products (1,780,131 ) (2,308,912 ) (2,278,771 ) (1,895,803 ) (1,164,362 )Duties and levies (219,724 ) (110,455 ) (95,510 ) (125,985 ) (51,488 ) Total value added 236,518 180,846 247,400 228,531 151,541 To pay employees’ gross salaries, wages and benefits 14,028 13,521 14,302 13,139 9,871 To pay income taxes 37,252 30,342 44,847 40,716 24,826 To pay providers of capital 22,262 55,298 61,910 64,100 72,955 - net finance income (11,719 ) (3,799 ) (1,340 ) (2,415 ) (1,927 )- dividends 33,981 59,097 63,250 66,515 74,882 Retained in the Group for future growth 162,976 81,685 126,341 110,576 43,889 - depreciation 20,001 17,662 13,966 13,065 9,464 - retained income for the year 142,975 64,023 112,375 97,511 34,425 Total value added 236,518 180,846 247,400 228,531 151,541

31 December 31 December 31 December 31 December 31 December 2015 2014 2013 2012 2011 P’000 P’000 P’000 P’000 P’000

30

FINANCIALSANNUAL CONSOLIDATED FINANCIAL STATEMENTS

Directors’ Report

Statement of Profit or Loss and other Comprehensive Income

Statement of Financial Position

Statement of Cash Flows

Statement of Changes in Equity

Notes to the Financial Statements

Report of the Independent Auditors

33

34

35

36

37

39

75

31

Directors: S Ndzinge (Chairman) C C Monga (Managing Director) A M Siwawa A M Bryce F J Kotze V Bvumbi J F Kennedy (Resigned 29 May 2015) R N Matthews C Mareka (Appointed 15 November 2015)

PrinciPal activities: Petrochemical investments and property operations

Parent comPany: Petroleum Investment Holdings Limited Mauritius

Ultimate Parent comPany: Petronas

transfer secretary: PricewaterhouseCoopers FairgroundsOfficePark Plot 50371 P O Box 1453, Gaborone

comPany nUmber 1966/335

registereD office: Plot 54026 Western Bypass P O Box 867 Gaborone aUDitor: Ernst & Young, Botswana

GENERAL INFORMATIONFOR THE YEAR ENDED 31 DECEMBER 2015

32

bankers: First National Bank of Botswana Limited Barclays Bank of Botswana Limited Standard Chartered Bank Botswana Limited Stanbic Bank Botswana Limited coUntry of incorPorationanD Domicile: Botswana

cUrrency: Botswana Pula

aPProval of annUalconsoliDateD financial statements Theannualconsolidatedfinancialstatements for the year ended 31 December 2015 were authorised for issue in accordance with a resolution of the directors and are signed on their behalf by:

Director 17 March 2016

Director

33

financial resUltsRevenue decreased by 14% mainly due to three downward price adjustments during the year. Total sales volumes grew by 5% between 2014 and 2015. While retail sales grew by 14%, commercial sales declined by 8% mainly due to the liquidation of a customer which had a major fuel supply contract.

Foreign exchange gains increased from P 1.4 million at the end of 2014 to P 4.3 million at the end of 2015. This was due to the depreciation of the South African Rand to other trading currencies.

The group exercised good margin management and cost control throughout the year.

Overall the group’s performance reflects a 68.2% increase in net profit after tax.

conclUsionThe Directors would like to thank our valued customers, suppliers, shareholders and all other stakeholders for their ongoing support towards the performance of Engen Botswana Limited.

DIRECTORS’ REPORTFOR THE YEAR ENDED 31 DECEMBER 2015

34

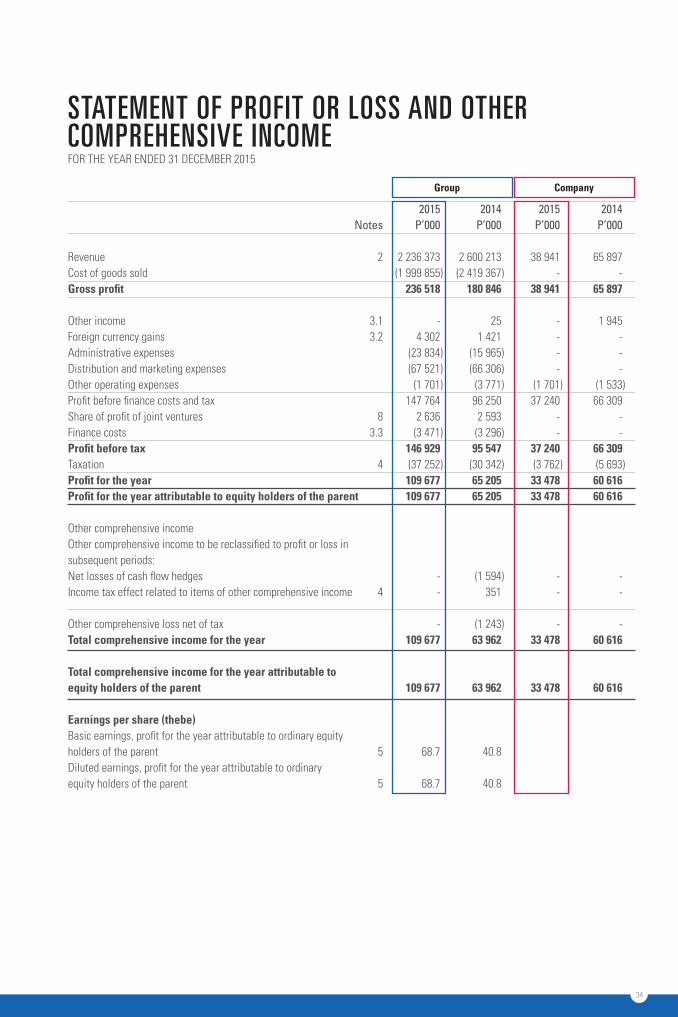

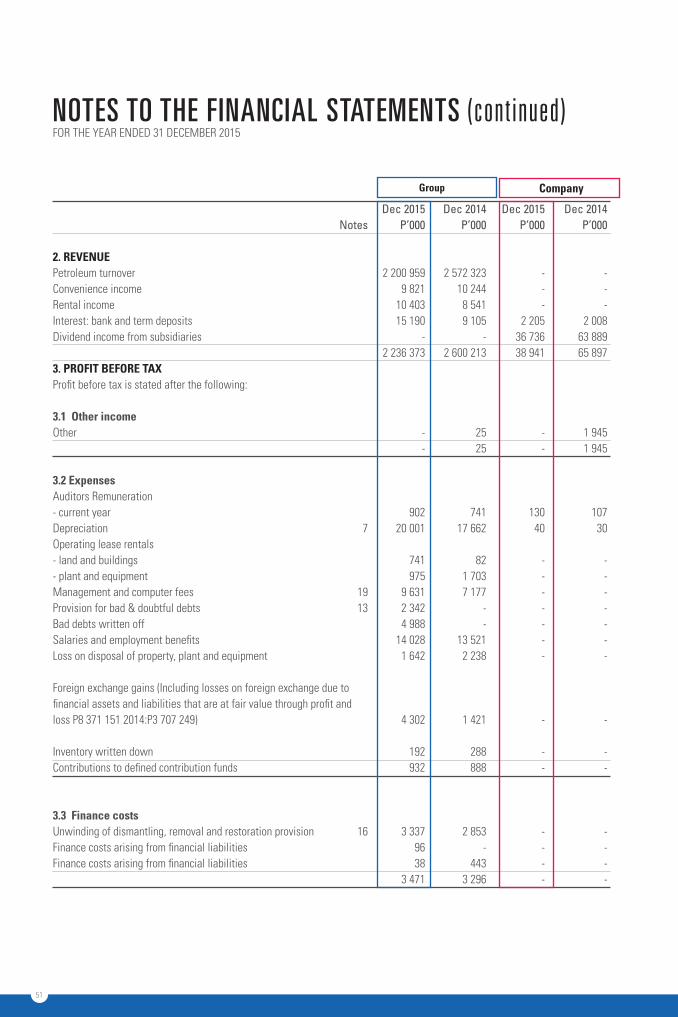

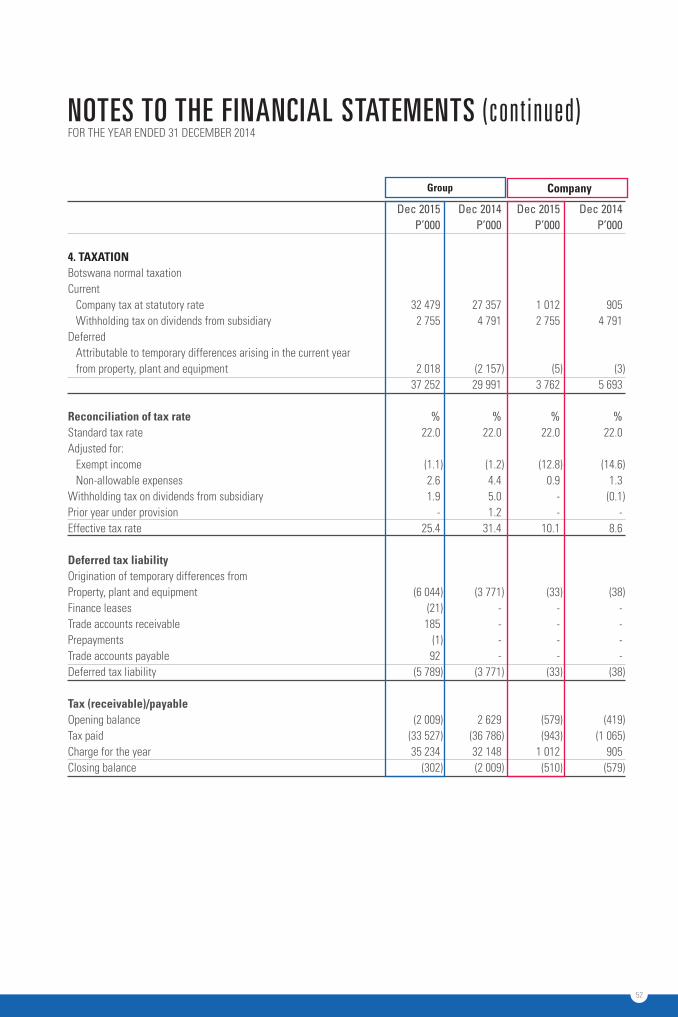

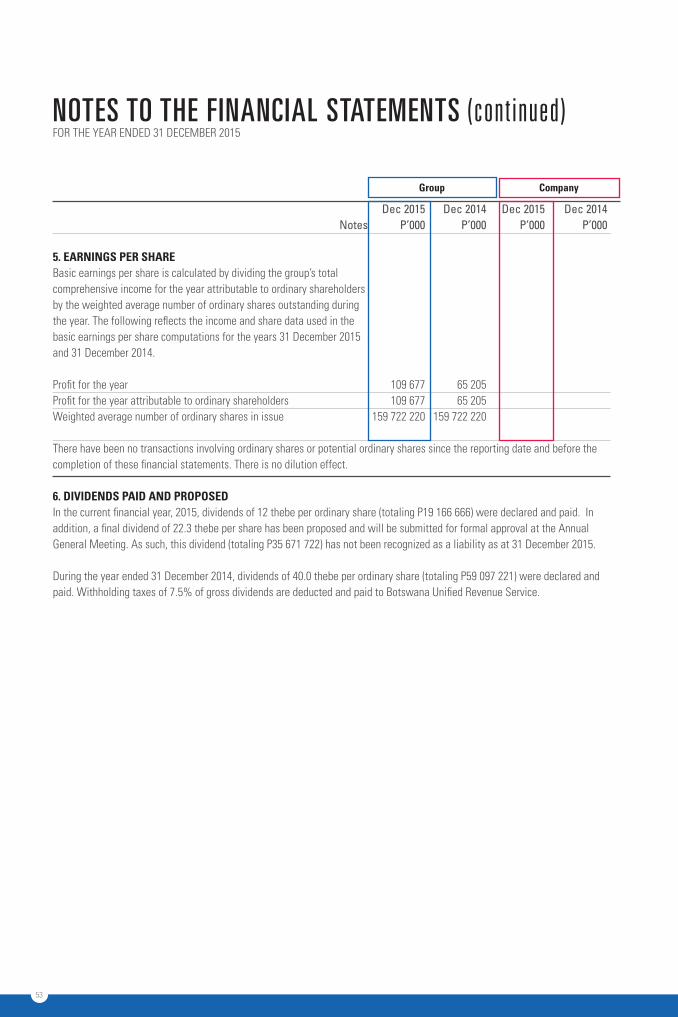

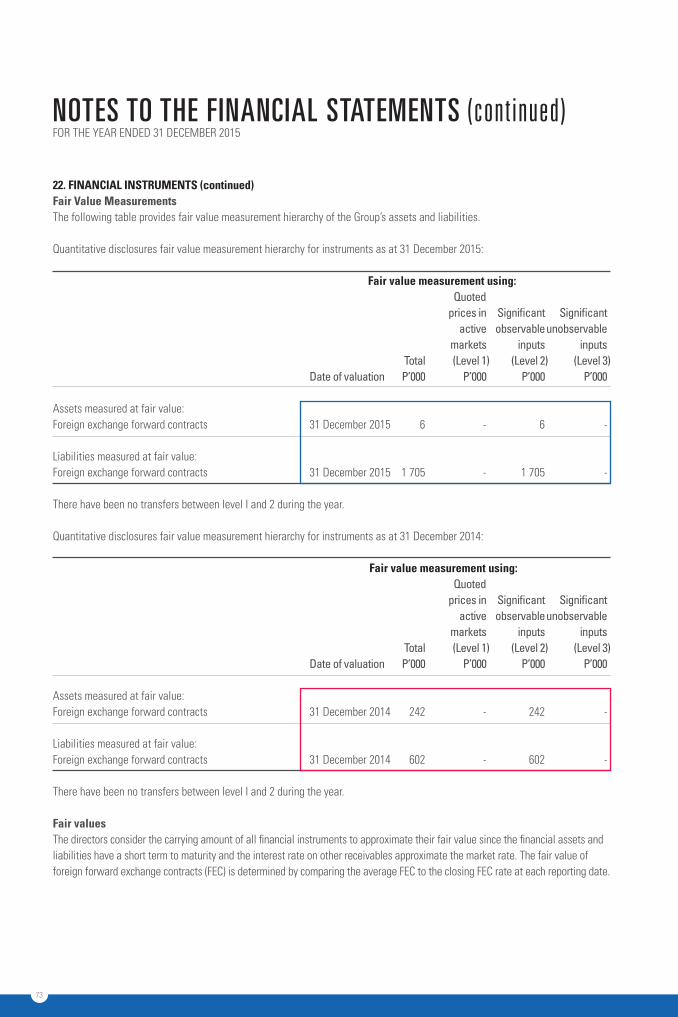

2015 2014 2015 2014 Notes P’000 P’000 P’000 P’000 Revenue 2 2 236 373 2 600 213 38 941 65 897Cost of goods sold (1 999 855 ) (2 419 367 ) - -gross profit 236 518 180 846 38 941 65 897 Other income 3.1 - 25 - 1 945Foreign currency gains 3.2 4 302 1 421 - -Administrative expenses (23 834 ) (15 965 ) - -Distribution and marketing expenses (67 521 ) (66 306 ) - -Other operating expenses (1 701 ) (3 771 ) (1 701 ) (1 533 )Profit before finance costs and tax 147 764 96 250 37 240 66 309Share of profit of joint ventures 8 2 636 2 593 - -Finance costs 3.3 (3 471 ) (3 296 ) - -Profit before tax 146 929 95 547 37 240 66 309Taxation 4 (37 252 ) (30 342 ) (3 762 ) (5 693 )Profit for the year 109 677 65 205 33 478 60 616Profit for the year attributable to equity holders of the parent 109 677 65 205 33 478 60 616 Other comprehensive income Other comprehensive income to be reclassified to profit or loss insubsequent periods: Net losses of cash flow hedges - (1 594 ) - -Income tax effect related to items of other comprehensive income 4 - 351 - -

Other comprehensive loss net of tax - (1 243 ) - -total comprehensive income for the year 109 677 63 962 33 478 60 616

total comprehensive income for the year attributable toequity holders of the parent 109 677 63 962 33 478 60 616

earnings per share (thebe) Basic earnings, profit for the year attributable to ordinary equityholders of the parent 5 68.7 40.8 Diluted earnings, profit for the year attributable to ordinaryequity holders of the parent 5 68.7 40.8

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOMEFOR THE YEAR ENDED 31 DECEMBER 2015

group company

35

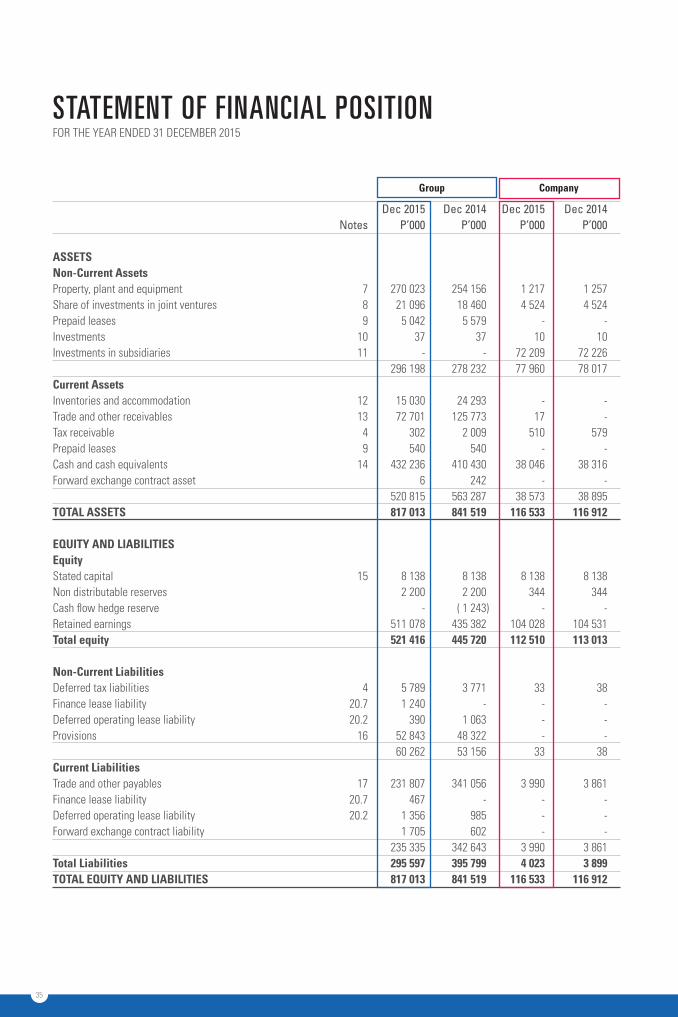

Dec 2015 Dec 2014 Dec 2015 Dec 2014 Notes P’000 P’000 P’000 P’000 assets non-current assets Property, plant and equipment 7 270 023 254 156 1 217 1 257Share of investments in joint ventures 8 21 096 18 460 4 524 4 524Prepaid leases 9 5 042 5 579 - -Investments 10 37 37 10 10Investments in subsidiaries 11 - - 72 209 72 226 296 198 278 232 77 960 78 017current assets Inventories and accommodation 12 15 030 24 293 - -Trade and other receivables 13 72 701 125 773 17 -Tax receivable 4 302 2 009 510 579Prepaid leases 9 540 540 - -Cash and cash equivalents 14 432 236 410 430 38 046 38 316Forward exchange contract asset 6 242 - - 520 815 563 287 38 573 38 895total assets 817 013 841 519 116 533 116 912 eQUity anD liabilities equity Stated capital 15 8 138 8 138 8 138 8 138Non distributable reserves 2 200 2 200 344 344Cash flow hedge reserve - ( 1 243 ) - -Retained earnings 511 078 435 382 104 028 104 531total equity 521 416 445 720 112 510 113 013 non-current liabilities Deferred tax liabilities 4 5 789 3 771 33 38Finance lease liability 20.7 1 240 - - -Deferred operating lease liability 20.2 390 1 063 - -Provisions 16 52 843 48 322 - - 60 262 53 156 33 38current liabilities Trade and other payables 17 231 807 341 056 3 990 3 861Finance lease liability 20.7 467 - - -Deferred operating lease liability 20.2 1 356 985 - -Forward exchange contract liability 1 705 602 - - 235 335 342 643 3 990 3 861total liabilities 295 597 395 799 4 023 3 899total eQUity anD liabilities 817 013 841 519 116 533 116 912

STATEMENT OF FINANCIAL POSITIONFOR THE YEAR ENDED 31 DECEMBER 2015

group company

36

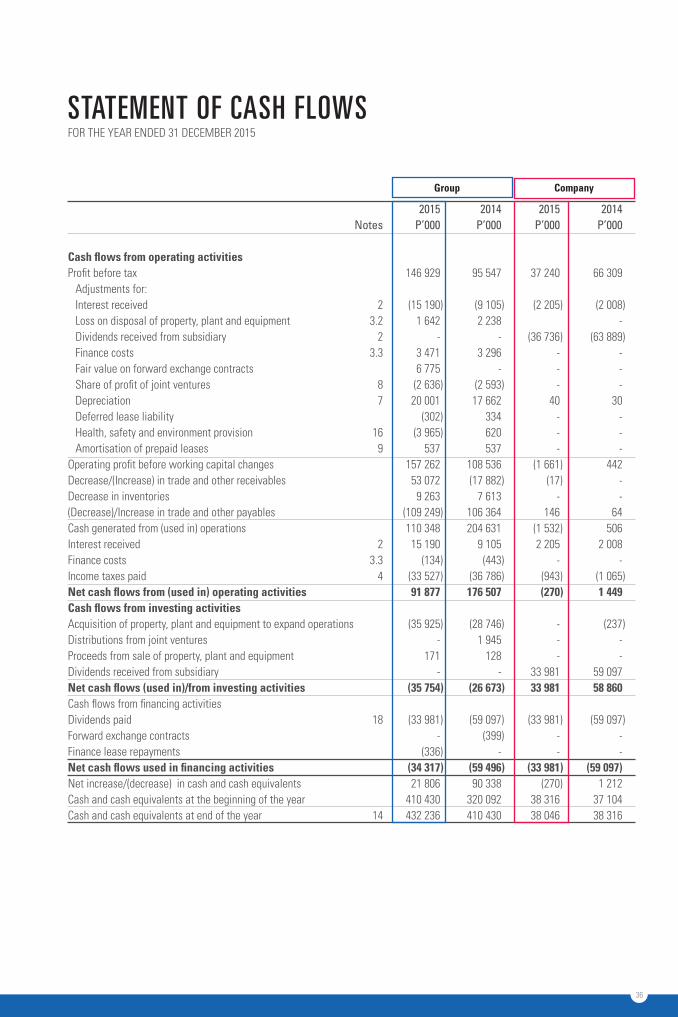

2015 2014 2015 2014 Notes P’000 P’000 P’000 P’000 cash flows from operating activities Profit before tax 146 929 95 547 37 240 66 309

Adjustments for: Interest received 2 (15 190 ) (9 105 ) (2 205 ) (2 008 )Loss on disposal of property, plant and equipment 3.2 1 642 2 238 -Dividends received from subsidiary 2 - - (36 736 ) (63 889 ) Finance costs 3.3 3 471 3 296 - -Fair value on forward exchange contracts 6 775 - - -Share of profit of joint ventures 8 (2 636 ) (2 593 ) - - Depreciation 7 20 001 17 662 40 30 Deferred lease liability (302 ) 334 - -Health, safety and environment provision 16 (3 965 ) 620 - - Amortisation of prepaid leases 9 537 537 - -

Operating profit before working capital changes 157 262 108 536 (1 661 ) 442Decrease/(Increase) in trade and other receivables 53 072 (17 882 ) (17 ) -Decrease in inventories 9 263 7 613 - - (Decrease)/Increase in trade and other payables (109 249 ) 106 364 146 64Cash generated from (used in) operations 110 348 204 631 (1 532 ) 506Interest received 2 15 190 9 105 2 205 2 008Finance costs 3.3 (134 ) (443 ) - -Income taxes paid 4 (33 527 ) (36 786 ) (943 ) (1 065 ) net cash flows from (used in) operating activities 91 877 176 507 (270 ) 1 449cash flows from investing activities Acquisition of property, plant and equipment to expand operations (35 925 ) (28 746 ) - (237 )Distributions from joint ventures - 1 945 - -Proceeds from sale of property, plant and equipment 171 128 - -Dividends received from subsidiary - - 33 981 59 097net cash flows (used in)/from investing activities (35 754 ) (26 673 ) 33 981 58 860Cash flows from financing activities Dividends paid 18 (33 981 ) (59 097 ) (33 981 ) (59 097 )Forward exchange contracts - (399 ) - -Finance lease repayments (336 ) - - -net cash flows used in financing activities (34 317 ) (59 496 ) (33 981 ) (59 097) Net increase/(decrease) in cash and cash equivalents 21 806 90 338 (270 ) 1 212Cash and cash equivalents at the beginning of the year 410 430 320 092 38 316 37 104Cash and cash equivalents at end of the year 14 432 236 410 430 38 046 38 316

STATEMENT OF CASH FLOWSFOR THE YEAR ENDED 31 DECEMBER 2015

group company

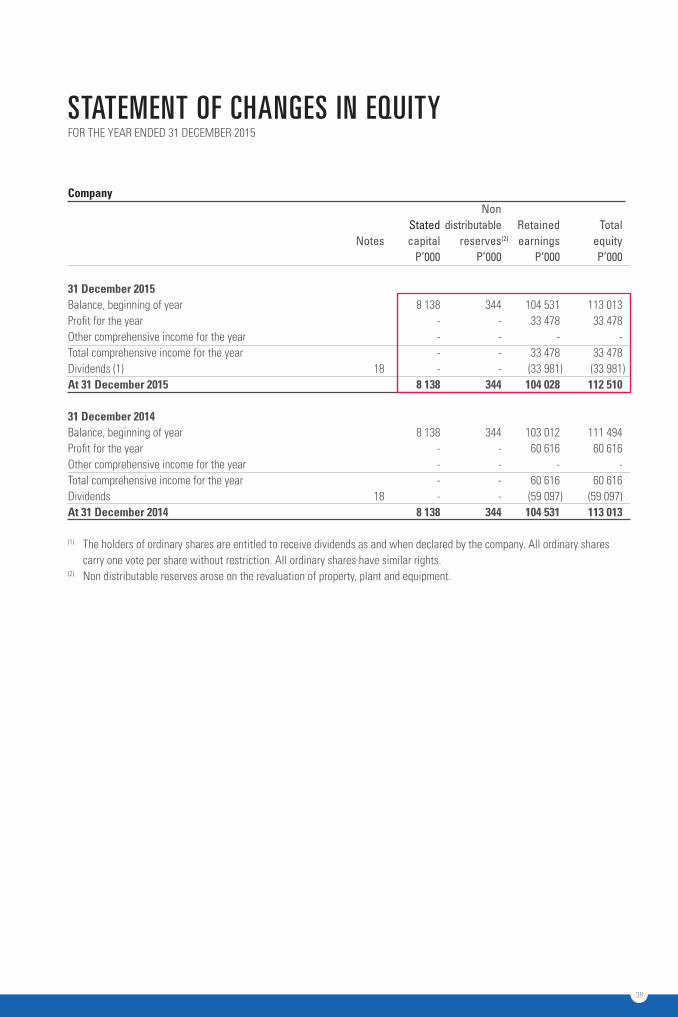

37

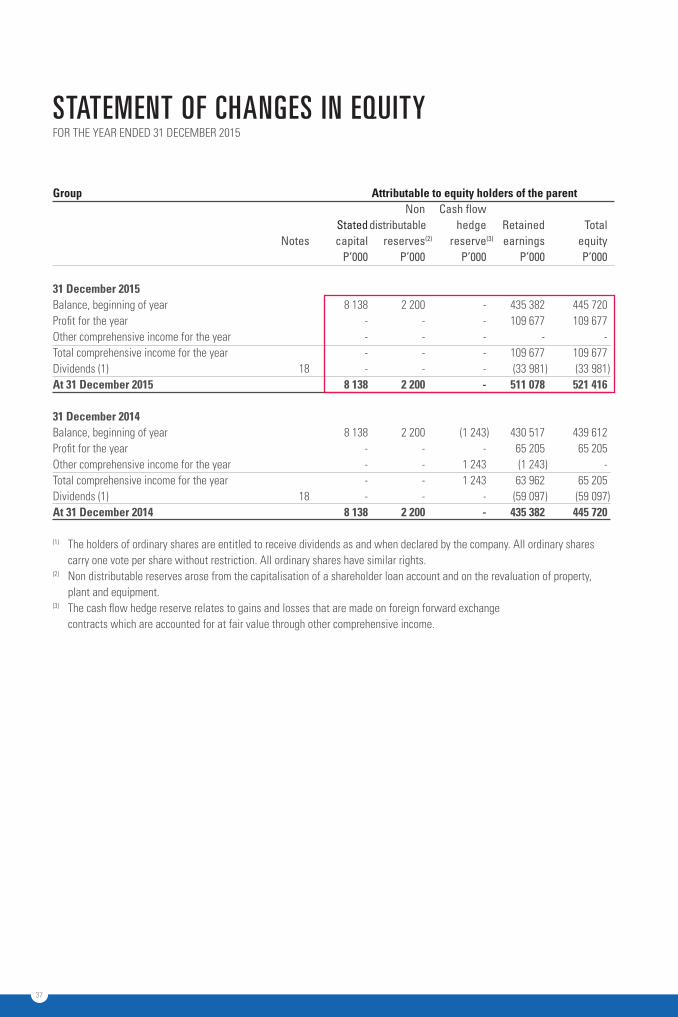

group attributable to equity holders of the parent Non Cash flow Stated distributable hedge Retained Total Notes capital reserves (2) reserve (3) earnings equity P’000 P’000 P’000 P’000 P’000 31 December 2015 Balance, beginning of year 8 138 2 200 - 435 382 445 720Profit for the year - - - 109 677 109 677Other comprehensive income for the year - - - - -Total comprehensive income for the year - - - 109 677 109 677Dividends (1) 18 - - - (33 981 ) (33 981 )at 31 December 2015 8 138 2 200 - 511 078 521 416 31 December 2014 Balance, beginning of year 8 138 2 200 (1 243 ) 430 517 439 612Profit for the year - - - 65 205 65 205Other comprehensive income for the year - - 1 243 (1 243 ) -Total comprehensive income for the year - - 1 243 63 962 65 205Dividends (1) 18 - - - (59 097 ) (59 097 )at 31 December 2014 8 138 2 200 - 435 382 445 720

(1) The holders of ordinary shares are entitled to receive dividends as and when declared by the company. All ordinary shares carry one vote per share without restriction. All ordinary shares have similar rights.

(2) Non distributable reserves arose from the capitalisation of a shareholder loan account and on the revaluation of property, plant and equipment.

(3) The cash flow hedge reserve relates to gains and losses that are made on foreign forward exchange contracts which are accounted for at fair value through other comprehensive income.

STATEMENT OF CHANGES IN EQUITYFOR THE YEAR ENDED 31 DECEMBER 2015

38

company Non Stated distributable Retained Total Notes capital reserves (2) earnings equity P’000 P’000 P’000 P’000 31 December 2015 Balance, beginning of year 8 138 344 104 531 113 013Profit for the year - - 33 478 33 478Other comprehensive income for the year - - - -Total comprehensive income for the year - - 33 478 33 478Dividends (1) 18 - - (33 981 ) (33 981 )at 31 December 2015 8 138 344 104 028 112 510 31 December 2014 Balance, beginning of year 8 138 344 103 012 111 494Profit for the year - - 60 616 60 616Other comprehensive income for the year - - - -Total comprehensive income for the year - - 60 616 60 616Dividends 18 - - (59 097 ) (59 097)at 31 December 2014 8 138 344 104 531 113 013

(1) The holders of ordinary shares are entitled to receive dividends as and when declared by the company. All ordinary shares carry one vote per share without restriction. All ordinary shares have similar rights.

(2) Non distributable reserves arose on the revaluation of property, plant and equipment.

STATEMENT OF CHANGES IN EQUITYFOR THE YEAR ENDED 31 DECEMBER 2015

39

basis of preparation The financial statements are presented in Botswana Pula. The functional currency is also the Botswana Pula. The amounts in the financial statements have been rounded to the nearest thousand. The financial statements have been prepared on a historical cost basis except as modified by the revaluation of certain financial instruments to fair as indicated in the notes below.

statement of complianceThe financial statements have been prepared in compliance with the International Financial Reporting Standards issued by the International Accounting Standards Board (“IASB”), Interpretations issued by the International Financial Reporting Interpretations Committee of the IASB and the requirements of the Companies Act of Botswana (Companies Act, 2003).

basis of consolidationThe consolidated financial statements comprise the financial statements of the Group and its subsidiaries as at 31 December 2015. Control is achieved when the Group is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee. Specifically, the Group controls an investee if and only if the Group has:• Power over the investee (i.e.

existing rights that give it the current ability to direct the relevant activities of the investee)

• Exposure, or rights, to variable returns from its involvement with the investee, and

• The ability to use its power over the investee to affect its returns

When the Group has less than a majority of the voting or similar rights of an investee, the Group considers allrelevant facts and circumstances in assessing whether it has power over an investee, including:• The contractual arrangement

with the other vote holders of the investee

• Rights arising from other contractual arrangements

• The Group’s voting rights and potential voting rights

The Group re-assesses whether or not it controls an investee if facts and circumstances indicate that there arechanges to one or more of the three elements of control. Consolidation of a subsidiary begins when the Groupobtains control over the subsidiary and ceases when the Group loses control of the subsidiary. Assets, liabilities, income and expenses of a subsidiary acquired or disposed of during the year are included in the statement of profit or loss and other comprehensive income from the date the Group gains control until the date the Group ceases to control the subsidiary.

Profit or loss and each component of other comprehensive income (OCI) are attributed to the equity holders of the parent of the Group and to the non-controlling interests, even if this results in the non-controlling interests having a deficit balance. When necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies into line with the Group’s accounting policies. All intra-group assets and liabilities, equity, income, expenses and cash flows relating to transactions between members of the Group are eliminated in full on consolidation.

A change in the ownership interest of a subsidiary, without a loss of control, is accounted for as an equity transaction. If the Group loses control over a subsidiary, it:• Derecognises the assets (including

goodwill) and liabilities of the subsidiary

• Derecognises the carrying amount of any non-controlling interests

• Derecognises the cumulative translation differences recorded in equity

• Recognises the fair value of the consideration received

• Recognises the fair value of any investment retained

• Recognises any surplus or deficit in profit or loss

• Reclassifies the parent’s share of components previously recognised in OCI to profit or loss or retained earnings, as appropriate, as would be required if the Group had directly disposed of the related assets or liabilities.

foreign currency translationfunctional currencyTransactions in foreign currency are initially recorded in the functional currency at a rate of exchange ruling on transaction date. Monetary assets and liabilities designated in foreign currencies are subsequently translated at rates of exchange ruling at the reporting date. Non monetary assets and liabilities that are measured in terms of historical cost in a foreign currency are translated at the exchange rate at the date of the initial transaction.

Foreign exchange translation gains or losses arising on the settlement of monetary items or on translating monetary items at rates different from those used when translating at initial recognition during the period or in

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2015

1. sUmmary of significant accoUnting Policies

40

NOTES TO THE FINANCIAL STATEMENTS (continued)FOR THE YEAR ENDED 31 DECEMBER 2015

previous financial statements are taken to the statement of profit or loss and other comprehensive income in the year they arise.

investments in subsidiariesInvestments in subsidiaries are measured at cost in the separate financial statements of the Company.

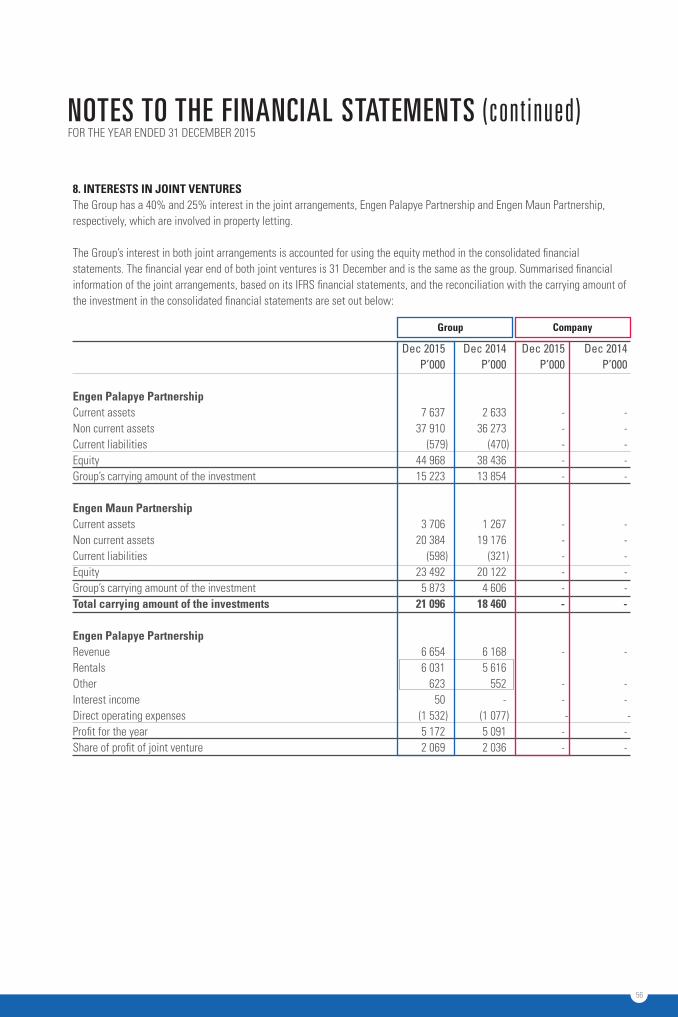

investments in joint venturesA joint venture is a type of joint arrangement whereby the parties that have joint control of the arrangement have rights to the net assets of the joint venture. Joint control is the contractually agreed sharing of control of an arrangement, which exists only when decisions about the relevant activities require unanimous consent of the parties sharing control. The considerations made in determining joint control are similar to those necessary to determine control over subsidiaries.

The Group’s investments in joint ventures are accounted for using the equity method.

Under the equity method, the investment in a joint venture is initially recognised at cost. The carrying amount of the investment is adjusted to recognise changes in the Group’s share of net assets of the joint venture since the acquisition date. Goodwill relating to the joint venture is included in the carrying amount of the investment and is neither amortised nor individually tested for impairment. The statement of profit or loss reflects the Group’s share of the results of operations of the joint venture. Any change in Other Comprehensive Income (OCI) of those investees is presented as part of the Group’s OCI. In addition, when there has been a change recognised directly in the equity of the joint venture, the Group recognises its share of any changes, when applicable,

in the statement of changes in equity. Unrealised gains and losses resulting from transactions between the Group and the joint venture are eliminated to the extent of the interest in the joint venture.

The aggregate of the Group’s share of profit or loss of a joint venture is shown on the face of the statement of profit or loss and other comprehensive income outside operating profit and represents profit or loss after tax and non-controlling interests in the subsidiaries of the joint venture.

The financial statements of the joint venture are prepared for the same reporting period as the Group. When necessary, adjustments are made to bring the accounting policies in line with those of the Group.

After application of the equity method, the Group determines whether it is necessary to recognise an impairment loss on its investment in its joint venture. At each reporting date, the Group determines whether there is objective evidence that the investment in the joint venture is impaired. If there is such evidence, the Group calculates the amount of impairment as the difference between the recoverable amount of the joint venture and its carrying value, then recognises the loss as ‘Share of loss of a joint venture’ in the statement of profit or loss and other comprehensive income.Upon loss of the joint control over the joint venture, the Group measures and recognises any retained investment at its fair value. Any difference between the carrying amount of the joint venture upon loss of joint control and the fair value of the retained investment and proceeds from disposal is recognised in the statement of profit or loss and other comprehensive income. Joint ventures are carried at cost in the separate financial statements of the company

leasesThe determination of whether an arrangement is, or contains, a lease is based on the substance of the arrangement at inception date: whether fulfilment of the arrangement is dependent on the use of a specific asset or assets or the arrangement conveys a right to use the asset.

finance leasesFinance leases, which transfer to the Group substantially all the risks and benefits incidental to ownership of the leased item, are capitalised at the inception of the lease at the fair value of the leased property or, if lower, at the present value of the minimum lease payments. Lease payments are apportioned between the finance charges and reduction of the lease liability so as to achieve a constant periodic rate of interest on the remaining balance of the liability. Finance charges are reflected in profit or loss.

Capitalised leased assets are depreciated over the shorter of the estimated useful life of the asset and the lease term, if there is no reasonable certainty that the Group will obtain ownership by the end of the lease term. If reasonable certainty exists that ownership will be obtained by the group by the end of the lease term, the leased asset is depreciated over its useful life.

operating leasesLeases where the Group does not transfer or where there is no transfer to it of substantially all the risks and benefits of ownership of the asset are classified as operating leases. Initial direct costs incurred in negotiating an operating lease are added to the carrying amount of the leased asset and recognised over the lease term on the same bases as rental income. Rental

1. sUmmary of significant accoUnting Policies (continued)

41

income or expenses related to minimum lease payments are recognised on a straight line basis over the lease term. Contingent rents are recognised as revenue in the year in which they are incurred.

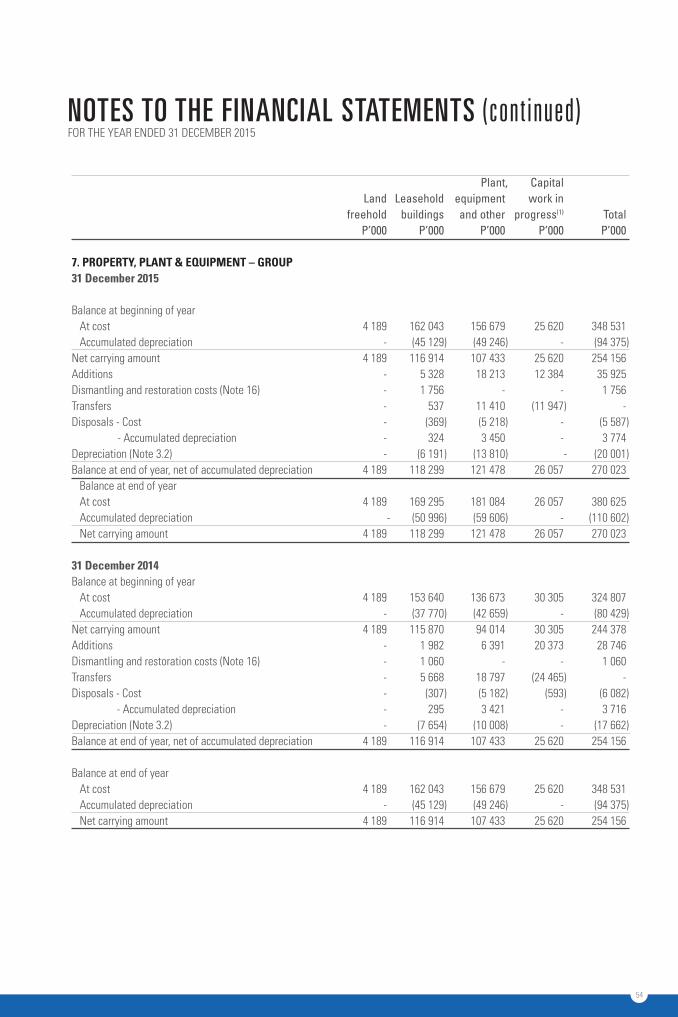

Property, plant and equipment Property, plant and equipment are stated at historical cost excluding the costs of day to day servicing that are expensed, less accumulated depreciation and any impairment in value. Cost includes the cost of replacing part of such plant and equipment when that cost is incurred if the recognition criteria are met.Costs also include the estimated costs of dismantling and removing the assets where the obligation has been incurred when the asset was acquired or as a consequence of using the asset.Subsequent costs are included in the asset’s carrying amount or recognised as a component, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the Group and the cost of the item can be measured reliably. All other repairs and maintenance expenditures are charged to the statement of comprehensive income during the financial period in which they are incurred.

Depreciation commences when the assets are available for their intended use. Property, plant and equipment are depreciated on a straight-line basis over the expected useful lives of the various classes of assets, after taking into account residual values. Each part of an item of property, plant and equipment with a cost that is significant in relation to the total cost of the item is depreciated separately.

Depreciation of an asset ceases at the earlier of the date that the asset is

classified as held for sale or is included in a disposal group that is classified as held for sale or the date that the asset is derecognised.

The residual value of an asset may increase to an amount equal to or greater than the asset’s carrying amount. If it does, the asset’s depreciation charge is zero until its residual value subsequently decreases to an amount below the asset’s carrying amount.

Useful lives of the property, plant and equipment, the depreciation method, depreciation rates, and residual values are reviewed on an annual basis. Estimated useful lives of the assets are as follows:

Leasehold buildings shorter of period of lease or 50 yearsPlant, equipment, and other 4 – 30 years

Land is not depreciated as it is deemed to have an indefinite life. No depreciation is provided on capital work-in-progress. The carrying amounts of assets are reviewed at each reporting date to assess if there are any indications of impairment. If any such indication exists and where assets are recorded in excess of their recoverable amounts, assets or cash generating units are written down to their recoverable amounts. A cash generating unit is considered only when the recoverable amount for the individual asset cannot be determined.

An item of property, plant and equipment is derecognized upon disposal or when no future economic benefits are expected from its use or disposal. Any gain or loss on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in the statement of profit or loss and other

comprehensive income in the year the asset is derecognized.

Improvements to assets held under operating leases are capitalized and depreciated over the remaining lease term.

Capital work in progress comprises costs incurred in constructing property, plant and equipment that are directly attributable to the construction of the asset. Assets remain in capital work in progress until they are available for use. At that time they are transferred to the appropriate class of property, plant and equipment additions. impairment of non-financial assets The Group assesses, at each reporting date, whether there is an indication that an asset may be impaired. If any indication exists, or when annual impairment testing for an asset is required, the Group estimates the asset’srecoverable amount. An asset’s recoverable amount is the higher of an asset’s or cash-generating unit’s (CGU)fair value less costs of disposal and its value in use. Recoverable amount is determined for an individual asset,unless the asset does not generate cash inflows that are largely independent of those from other assets orgroups of assets. When the carrying amount of an asset or CGU exceeds its recoverable amount, the asset isconsidered impaired and is written down to its recoverable amount.

In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. In determining fair value less costs of disposal, recent market

FOR THE YEAR ENDED 31 DECEMBER 2015NOTES TO THE FINANCIAL STATEMENTS (continued)

1. sUmmary of significant accoUnting Policies (continued)

42

NOTES TO THE FINANCIAL STATEMENTS (continued)FOR THE YEAR ENDED 31 DECEMBER 2015