Embed Size (px)

Citation preview

Final Results

for the year ended 30 June 2015.

Disclaimer

This presentation, which has been prepared by Regenersis PLC (“the Company”), includes statements that are, or may be

deemed to be, “forward-looking statements”. These forward-looking statements can be identified by the use of forward-

looking terminology, including the terms “believes”, “estimates”, “plans”, “projects”, “anticipates”, “expects”, “foresees”,

“intends”, “may”, “will” or “should” or, in each case, their negative or other variations or comparable terminology. These

forward-looking statements include matters that are not historical facts and include statements regarding the Company’s

intentions, beliefs or current expectations. By their nature, forward-looking statements involve risk and uncertainty because

they relate to future events and circumstances. A number of factors could cause actual results and developments to differ

materially from those expressed or implied by the forward looking statements. Any forward-looking statements in this

presentation reflect the Company’s view with respect to future events and other risks, uncertainties and assumptions

relating to the Company’s operations, results of operations, growth strategy and liquidity. The Company undertakes no

obligation publicly to release the results of any revisions or up-dates to any forward-looking statements in this presentation

that may occur due to change in its expectations or to reflect events or circumstances after the date of this presentation.

This presentation comprises information which is already in the public domain. No reliance may be placed for any

purposes whatsoever on the information contained in this document or on its completeness. None of the Company, its

advisers, or any other party is under any duty to update or inform you of any changes to the information contained in this

presentation.

2

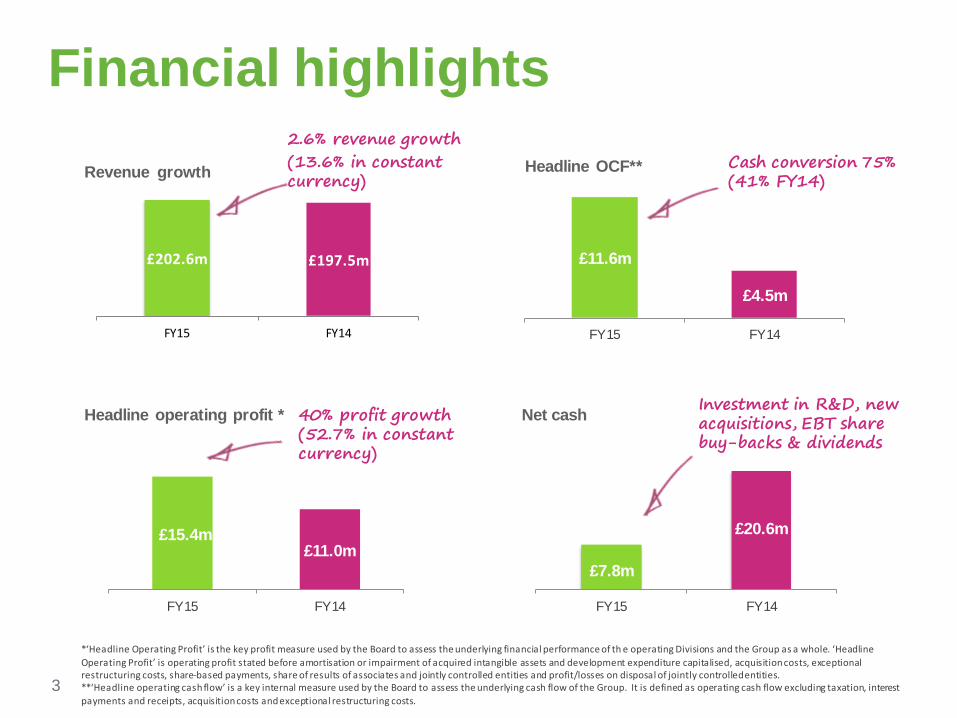

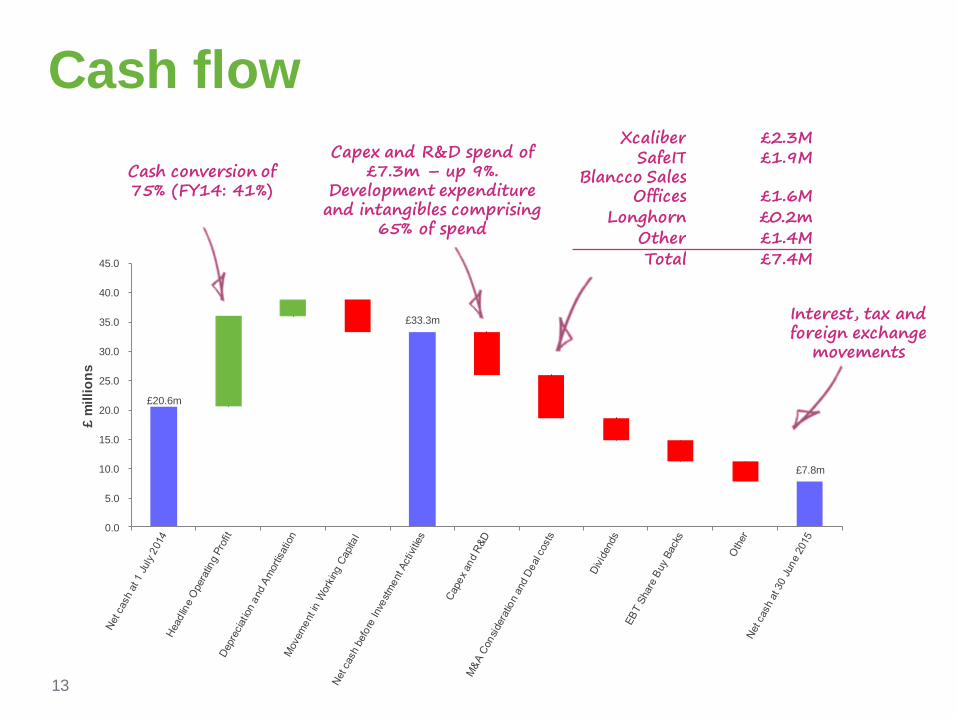

£7.8m

£20.6m

FY15 FY14

£202.6m £197.5m

FY15 FY14

Financial highlights2.6% revenue growth(13.6% in constant currency)Revenue growth

Headline operating profit *

Headline OCF** Cash conversion 75% (41% FY14)

Net cash

*‘Headline Operating Profit’ is the key profit measure used by the Board to assess the underlying financial performance of th e operating Divisions and the Group as a whole. ‘Headline

Operating Profit’ is operating profit stated before amortisation or impairment of acquired intangible assets and development expenditure capitalised, acquisition costs, exceptional restructuring costs, share-based payments, share of results of associates and jointly controlled entities and profit/losses on disposal of jointly controlled entities.**‘Headline operating cash flow’ is a key internal measure used by the Board to assess the underlying cash flow of the Group. It is defined as operating cash flow excluding taxation, interest

payments and receipts, acquisition costs and exceptional restructuring costs.

40% profit growth (52.7% in constant currency)

Investment in R&D, new acquisitions, EBT share buy-backs & dividends

£11.0m£15.4m

FY14FY15

£4.5m

£11.6m

FY14FY15

3

Overview

Solid results across divisions on a constant currency basis

Blancco significantly stronger – revenue, profit, technology, leadership team

Exploring strategic alternatives for the Aftermarket Services business (i.e. non-software)

Increased focus on Digital Security Software

Strengthened Board

4

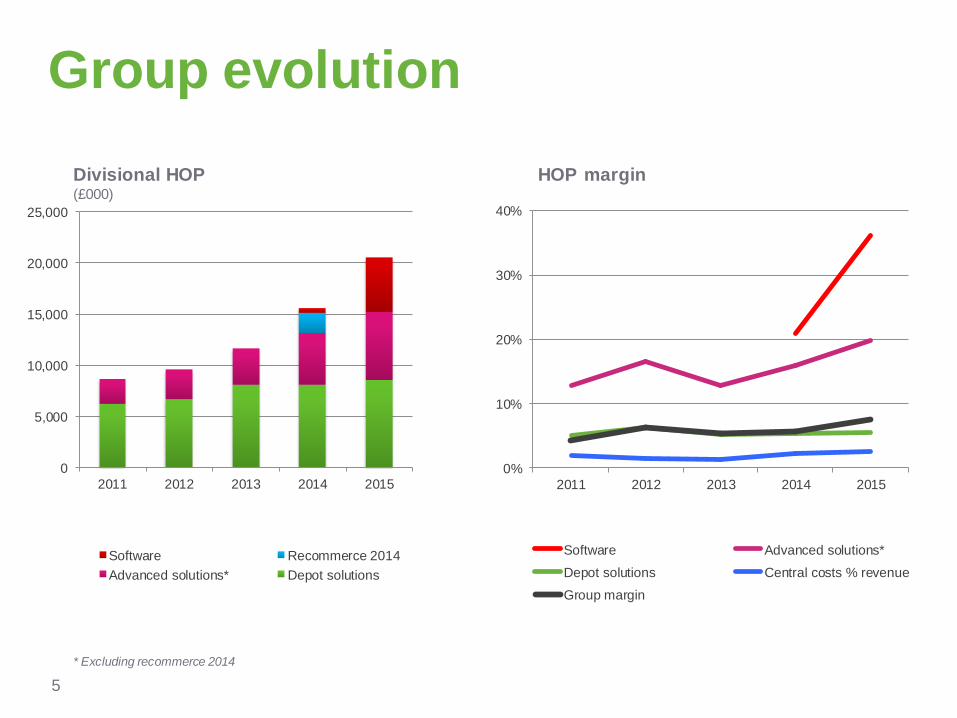

Group evolution

0

5,000

10,000

15,000

20,000

25,000

2011 2012 2013 2014 2015

Software Recommerce 2014

Advanced solutions* Depot solutions

0%

10%

20%

30%

40%

2011 2012 2013 2014 2015

Software Advanced solutions*

Depot solutions Central costs % revenue

Group margin

* Excluding recommerce 2014

Divisional HOP(£000)

HOP margin

5

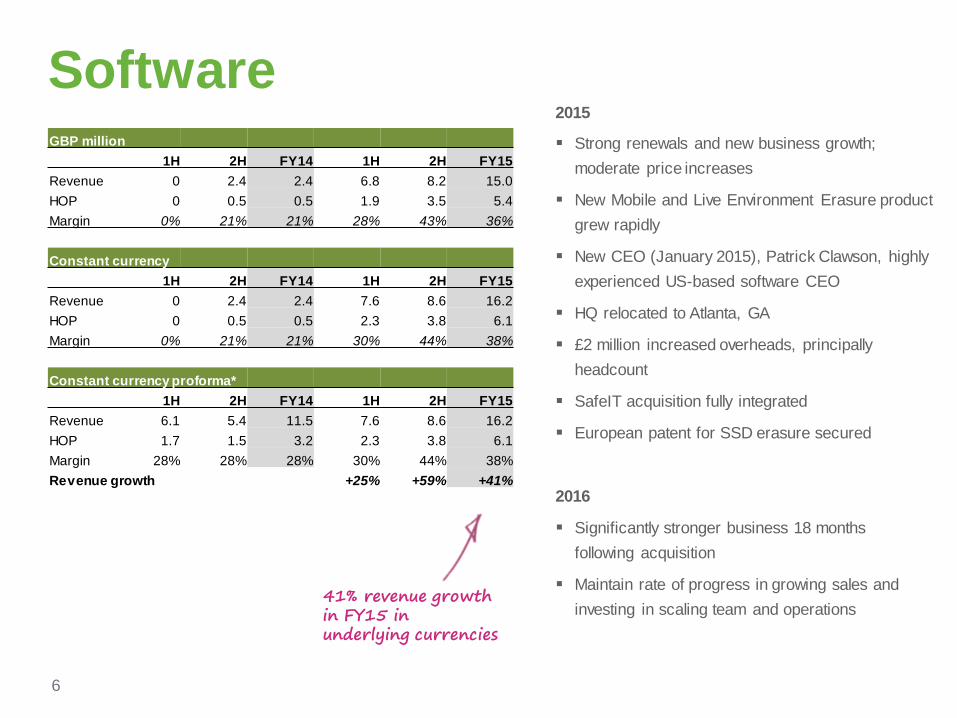

GBP million

1H 2H FY14 1H 2H FY15

Revenue 0 2.4 2.4 6.8 8.2 15.0

HOP 0 0.5 0.5 1.9 3.5 5.4

Margin 0% 21% 21% 28% 43% 36%

Constant currency

1H 2H FY14 1H 2H FY15

Revenue 0 2.4 2.4 7.6 8.6 16.2

HOP 0 0.5 0.5 2.3 3.8 6.1

Margin 0% 21% 21% 30% 44% 38%

Constant currency proforma*

1H 2H FY14 1H 2H FY15

Revenue 6.1 5.4 11.5 7.6 8.6 16.2

HOP 1.7 1.5 3.2 2.3 3.8 6.1

Margin 28% 28% 28% 30% 44% 38%

Revenue growth +25% +59% +41%

2015

Strong renewals and new business growth;

moderate price increases

New Mobile and Live Environment Erasure product

grew rapidly

New CEO (January 2015), Patrick Clawson, highly

experienced US-based software CEO

HQ relocated to Atlanta, GA

£2 million increased overheads, principally

headcount

SafeIT acquisition fully integrated

European patent for SSD erasure secured

2016

Significantly stronger business 18 months

following acquisition

Maintain rate of progress in growing sales and

investing in scaling team and operations

Software

41% revenue growth in FY15 in underlying currencies

6

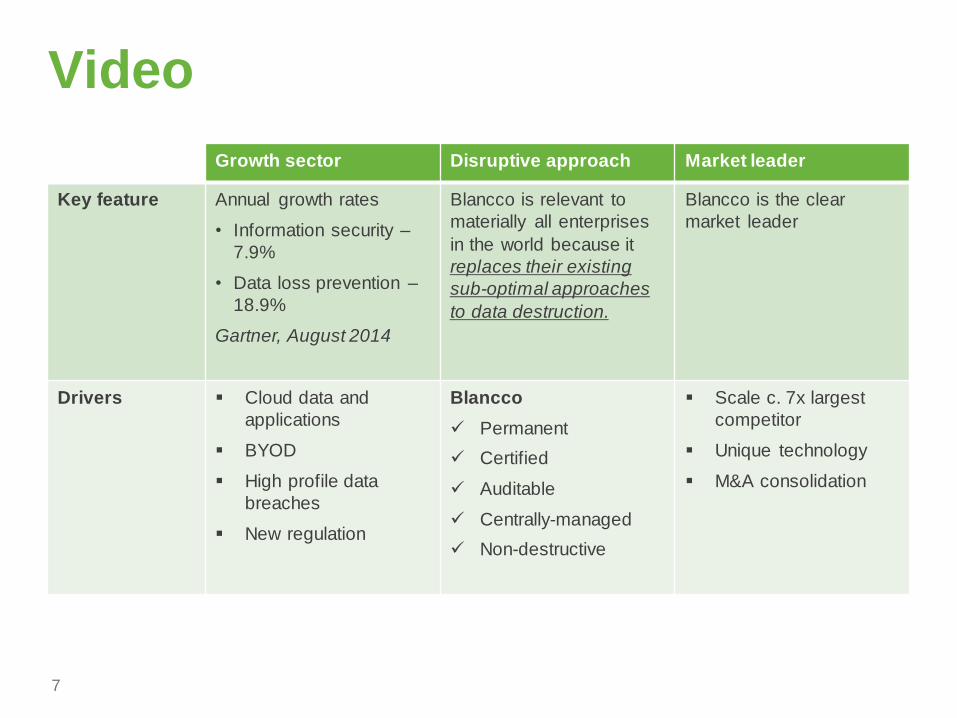

Video

7

Growth sector Disruptive approach Market leader

Key feature Annual growth rates

• Information security –

7.9%

• Data loss prevention –

18.9%

Gartner, August 2014

Blancco is relevant to

materially all enterprises

in the world because it

replaces their existing

sub-optimal approaches

to data destruction.

Blancco is the clear

market leader

Drivers Cloud data and

applications

BYOD

High profile data

breaches

New regulation

Blancco

Permanent

Certified

Auditable

Centrally-managed

Non-destructive

Scale c. 7x largest

competitor

Unique technology

M&A consolidation

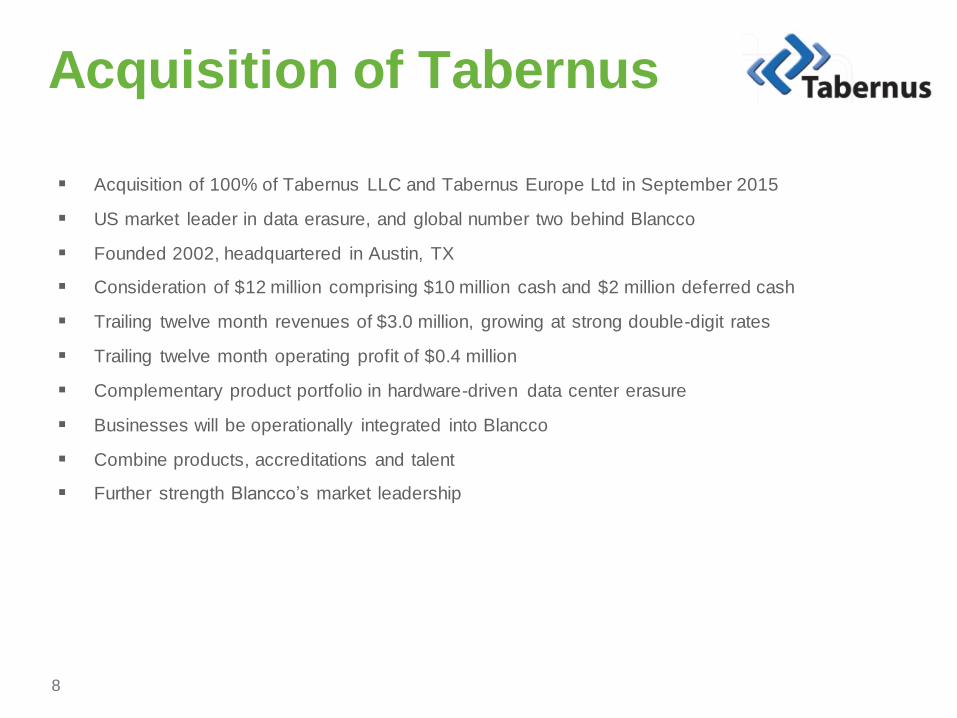

Acquisition of Tabernus

Acquisition of 100% of Tabernus LLC and Tabernus Europe Ltd in September 2015

US market leader in data erasure, and global number two behind Blancco

Founded 2002, headquartered in Austin, TX

Consideration of $12 million comprising $10 million cash and $2 million deferred cash

Trailing twelve month revenues of $3.0 million, growing at strong double-digit rates

Trailing twelve month operating profit of $0.4 million

Complementary product portfolio in hardware-driven data center erasure

Businesses will be operationally integrated into Blancco

Combine products, accreditations and talent

Further strength Blancco’s market leadership

8

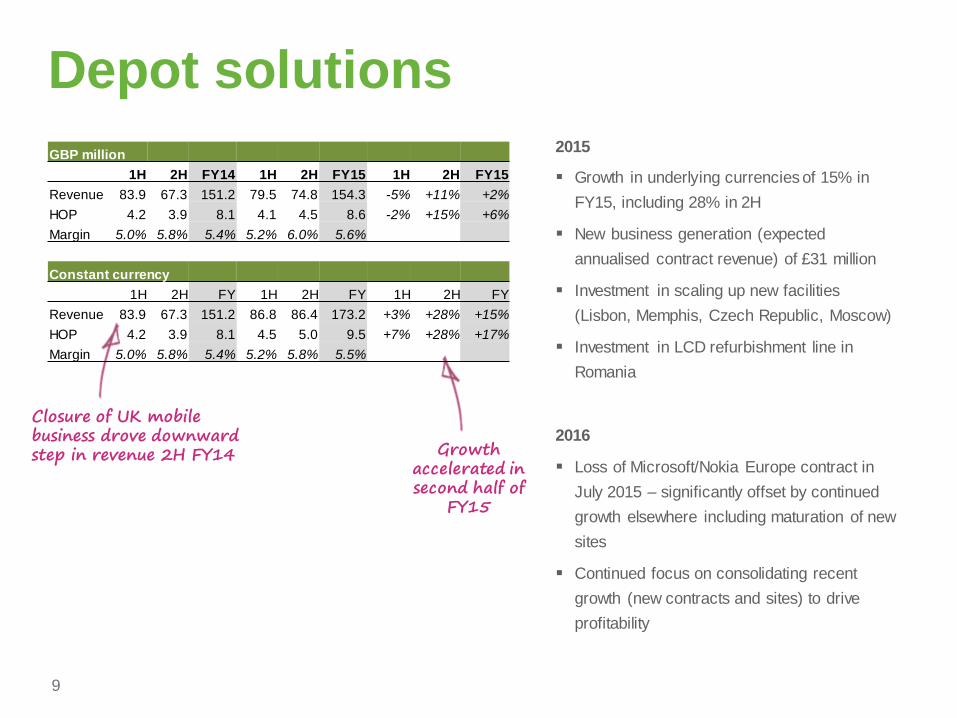

Depot solutions

2015

Growth in underlying currencies of 15% in

FY15, including 28% in 2H

New business generation (expected

annualised contract revenue) of £31 million

Investment in scaling up new facilities

(Lisbon, Memphis, Czech Republic, Moscow)

Investment in LCD refurbishment line in

Romania

2016

Loss of Microsoft/Nokia Europe contract in

July 2015 – significantly offset by continued

growth elsewhere including maturation of new

sites

Continued focus on consolidating recent

growth (new contracts and sites) to drive

profitability

Closure of UK mobile business drove downward step in revenue 2H FY14 Growth

accelerated in second half of

FY15

GBP million

1H 2H FY14 1H 2H FY15 1H 2H FY15

Revenue 83.9 67.3 151.2 79.5 74.8 154.3 -5% +11% +2%

HOP 4.2 3.9 8.1 4.1 4.5 8.6 -2% +15% +6%

Margin 5.0% 5.8% 5.4% 5.2% 6.0% 5.6%

Constant currency

1H 2H FY 1H 2H FY 1H 2H FY

Revenue 83.9 67.3 151.2 86.8 86.4 173.2 +3% +28% +15%

HOP 4.2 3.9 8.1 4.5 5.0 9.5 +7% +28% +17%

Margin 5.0% 5.8% 5.4% 5.2% 5.8% 5.5%

9

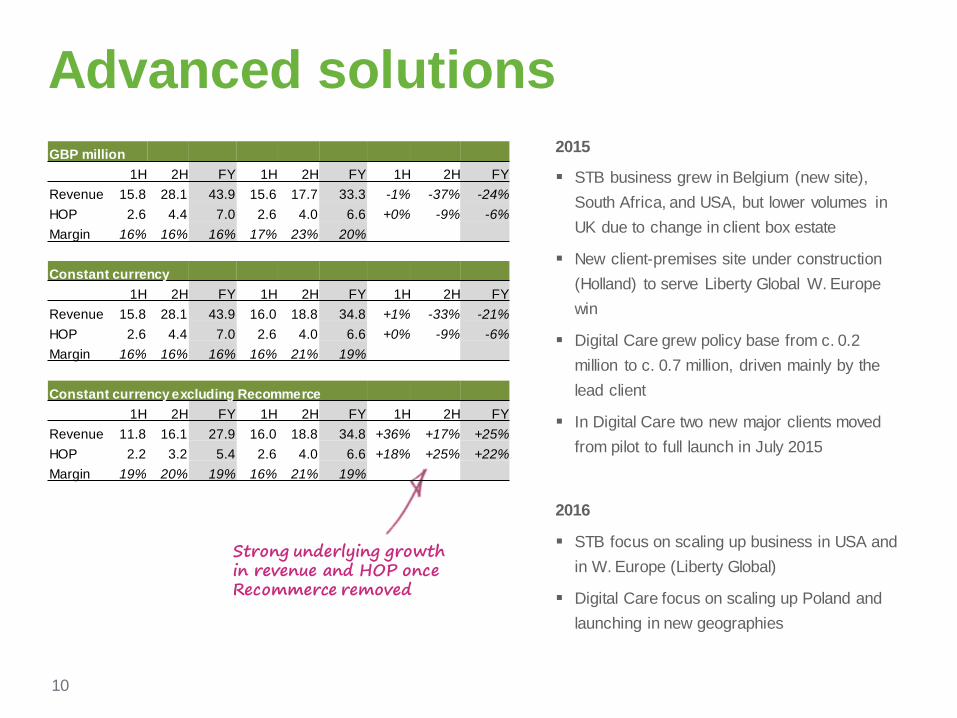

Advanced solutions

Strong underlying growth in revenue and HOP once Recommerce removed

2015

STB business grew in Belgium (new site),

South Africa, and USA, but lower volumes in

UK due to change in client box estate

New client-premises site under construction

(Holland) to serve Liberty Global W. Europe

win

Digital Care grew policy base from c. 0.2

million to c. 0.7 million, driven mainly by the

lead client

In Digital Care two new major clients moved

from pilot to full launch in July 2015

2016

STB focus on scaling up business in USA and

in W. Europe (Liberty Global)

Digital Care focus on scaling up Poland and

launching in new geographies

GBP million

1H 2H FY 1H 2H FY 1H 2H FY

Revenue 15.8 28.1 43.9 15.6 17.7 33.3 -1% -37% -24%

HOP 2.6 4.4 7.0 2.6 4.0 6.6 +0% -9% -6%

Margin 16% 16% 16% 17% 23% 20%

Constant currency

1H 2H FY 1H 2H FY 1H 2H FY

Revenue 15.8 28.1 43.9 16.0 18.8 34.8 +1% -33% -21%

HOP 2.6 4.4 7.0 2.6 4.0 6.6 +0% -9% -6%

Margin 16% 16% 16% 16% 21% 19%

Constant currency excluding Recommerce

1H 2H FY 1H 2H FY 1H 2H FY

Revenue 11.8 16.1 27.9 16.0 18.8 34.8 +36% +17% +25%

HOP 2.2 3.2 5.4 2.6 4.0 6.6 +18% +25% +22%

Margin 19% 20% 19% 16% 21% 19%

10

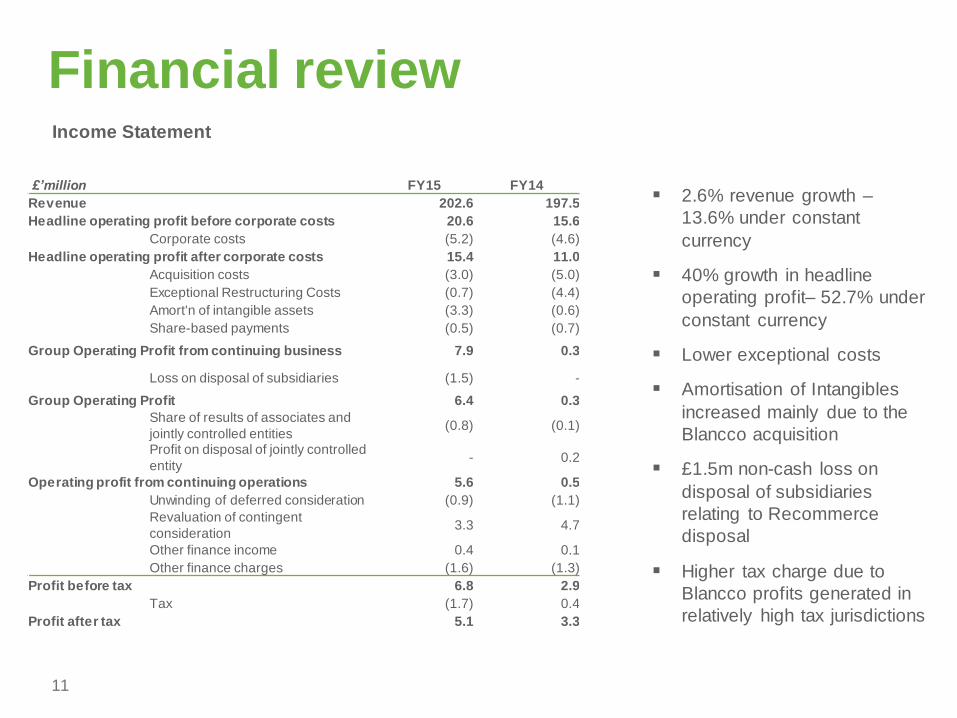

Financial reviewIncome Statement

2.6% revenue growth –

13.6% under constant

currency

40% growth in headline

operating profit– 52.7% under

constant currency

Lower exceptional costs

Amortisation of Intangibles

increased mainly due to the

Blancco acquisition

£1.5m non-cash loss on

disposal of subsidiaries

relating to Recommerce

disposal

Higher tax charge due to

Blancco profits generated in

relatively high tax jurisdictions

11

£’million FY15 FY14

Revenue 202.6 197.5

Headline operating profit before corporate costs 20.6 15.6

Corporate costs (5.2) (4.6)

Headline operating profit after corporate costs 15.4 11.0

Acquisition costs (3.0) (5.0)

Exceptional Restructuring Costs (0.7) (4.4)

Amort'n of intangible assets (3.3) (0.6)

Share-based payments (0.5) (0.7)

Group Operating Profit from continuing business 7.9 0.3

Loss on disposal of subsidiaries (1.5) -

Group Operating Profit 6.4 0.3

Share of results of associates and

jointly controlled entities(0.8) (0.1)

Profit on disposal of jointly controlled

entity- 0.2

Operating profit from continuing operations 5.6 0.5

Unwinding of deferred consideration (0.9) (1.1)

Revaluation of contingent

consideration3.3 4.7

Other finance income 0.4 0.1

Other finance charges (1.6) (1.3)

Profit before tax 6.8 2.9

Tax (1.7) 0.4

Profit after tax 5.1 3.3

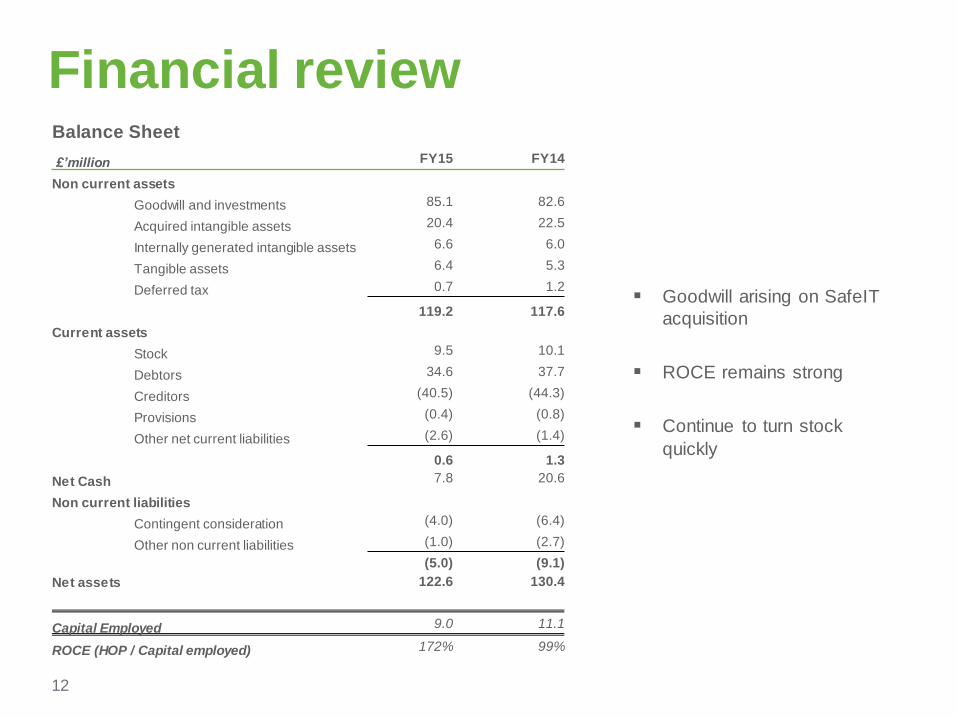

Financial review

Goodwill arising on SafeIT

acquisition

ROCE remains strong

Continue to turn stock

quickly

£’million FY15 FY14

Non current assets

Goodwill and investments 85.1 82.6

Acquired intangible assets 20.4 22.5

Internally generated intangible assets 6.6 6.0

Tangible assets 6.4 5.3

Deferred tax 0.7 1.2

119.2 117.6

Current assets

Stock 9.5 10.1

Debtors 34.6 37.7

Creditors (40.5) (44.3)

Provisions (0.4) (0.8)

Other net current liabilities (2.6) (1.4)

0.6 1.3

Net Cash 7.8 20.6

Non current liabilities

Contingent consideration (4.0) (6.4)

Other non current liabilities (1.0) (2.7)

(5.0) (9.1)

Net assets 122.6 130.4

Capital Employed 9.0 11.1

ROCE (HOP / Capital employed) 172% 99%

12

Balance Sheet

£20.6m

£33.3m

£7.8m

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

£ m

illi

on

s

Capex and R&D spend of £7.3m – up 9%.

Development expenditure and intangibles comprising

65% of spend

Xcaliber £2.3MSafeIT £1.9M

Blancco Sales Offices £1.6M

Longhorn £0.2mOther £1.4MTotal £7.4M

Interest, tax and foreign exchange

movements

Cash conversion of 75% (FY14: 41%)

Cash flow

13

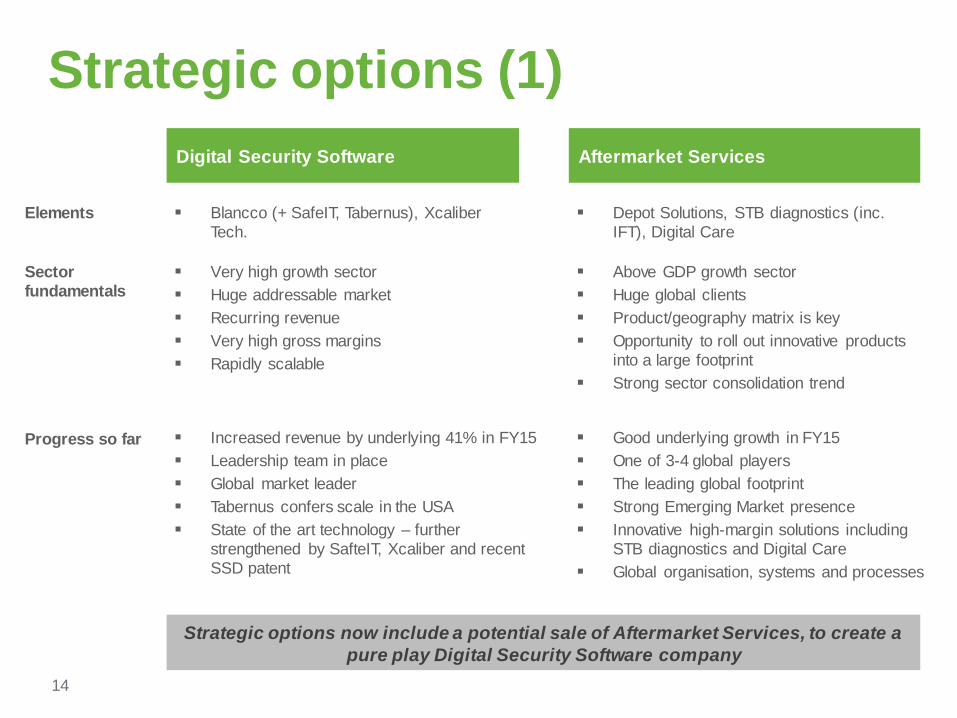

Strategic options (1)

Very high growth sector

Huge addressable market

Recurring revenue

Very high gross margins

Rapidly scalable

Above GDP growth sector

Huge global clients

Product/geography matrix is key

Opportunity to roll out innovative products

into a large footprint

Strong sector consolidation trend

Digital Security Software Aftermarket Services

14

Blancco (+ SafeIT, Tabernus), Xcaliber

Tech.

Depot Solutions, STB diagnostics (inc.

IFT), Digital Care

Increased revenue by underlying 41% in FY15

Leadership team in place

Global market leader

Tabernus confers scale in the USA

State of the art technology – further

strengthened by SafteIT, Xcaliber and recent

SSD patent

Sector

fundamentals

Elements

Progress so far Good underlying growth in FY15

One of 3-4 global players

The leading global footprint

Strong Emerging Market presence

Innovative high-margin solutions including

STB diagnostics and Digital Care

Global organisation, systems and processes

Strategic options now include a potential sale of Aftermarket Services, to create a

pure play Digital Security Software company

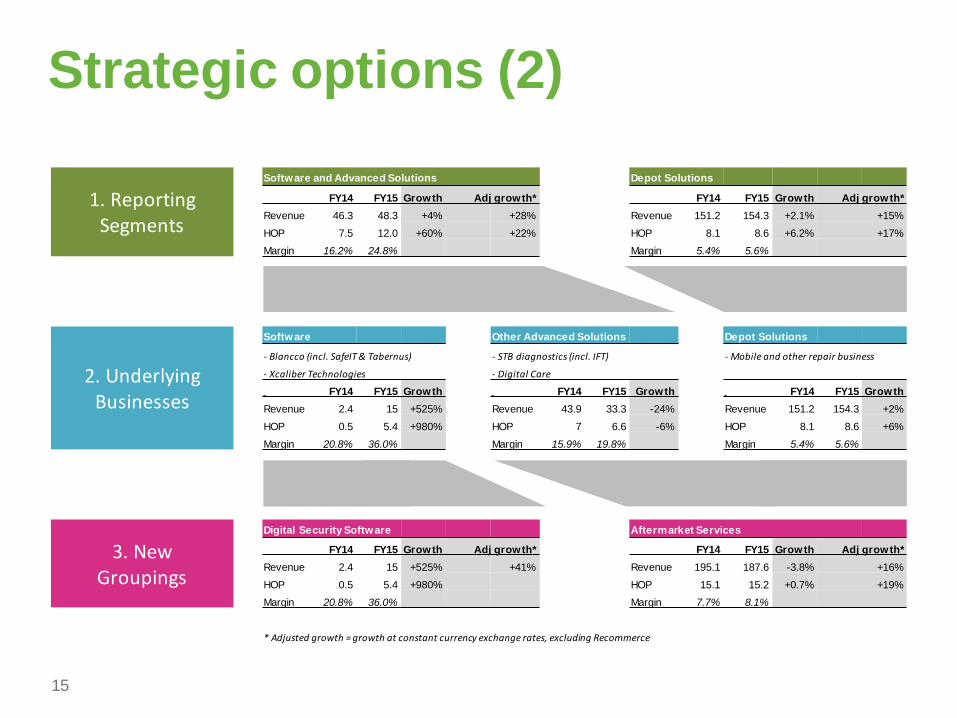

Strategic options (2)

1. Reporting Segments

Software and Advanced Solutions Depot Solutions

FY14 FY15 Growth Adj growth* FY14 FY15 Growth Adj growth*

Revenue 46.3 48.3 +4% +28% Revenue 151.2 154.3 +2.1% +15%

HOP 7.5 12.0 +60% +22% HOP 8.1 8.6 +6.2% +17%

Margin 16.2% 24.8% Margin 5.4% 5.6%

2. Underlying Businesses

Software Other Advanced Solutions Depot Solutions

- Blancco (incl. SafeIT & Tabernus) - STB diagnostics (incl. IFT) - Mobile and other repair business

- Xcaliber Technologies - Digital Care

FY14 FY15 Growth FY14 FY15 Growth FY14 FY15 Growth

Revenue 2.4 15 +525% Revenue 43.9 33.3 -24% Revenue 151.2 154.3 +2%

HOP 0.5 5.4 +980% HOP 7 6.6 -6% HOP 8.1 8.6 +6%

Margin 20.8% 36.0% Margin 15.9% 19.8% Margin 5.4% 5.6%

3. New Groupings

Digital Security Software Aftermarket Services

FY14 FY15 Growth Adj growth* FY14 FY15 Growth Adj growth*

Revenue 2.4 15 +525% +41% Revenue 195.1 187.6 -3.8% +16%

HOP 0.5 5.4 +980% HOP 15.1 15.2 +0.7% +19%

Margin 20.8% 36.0% Margin 7.7% 8.1%

* Adjusted growth = growth at constant currency exchange rates, excluding Recommerce

15

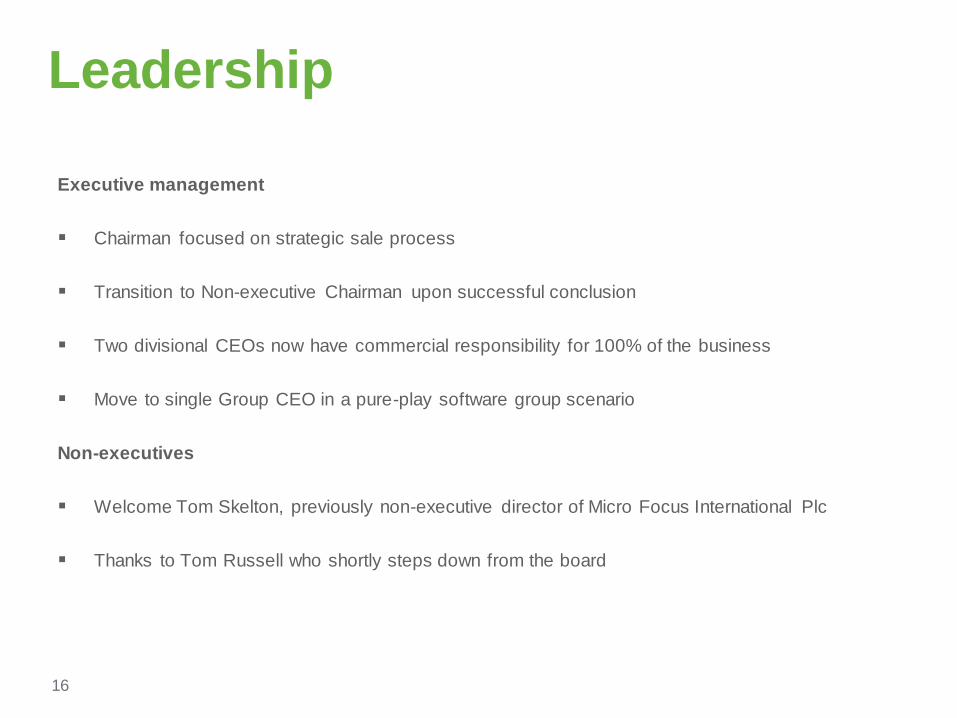

Leadership

Executive management

Chairman focused on strategic sale process

Transition to Non-executive Chairman upon successful conclusion

Two divisional CEOs now have commercial responsibility for 100% of the business

Move to single Group CEO in a pure-play software group scenario

Non-executives

Welcome Tom Skelton, previously non-executive director of Micro Focus International Plc

Thanks to Tom Russell who shortly steps down from the board

16

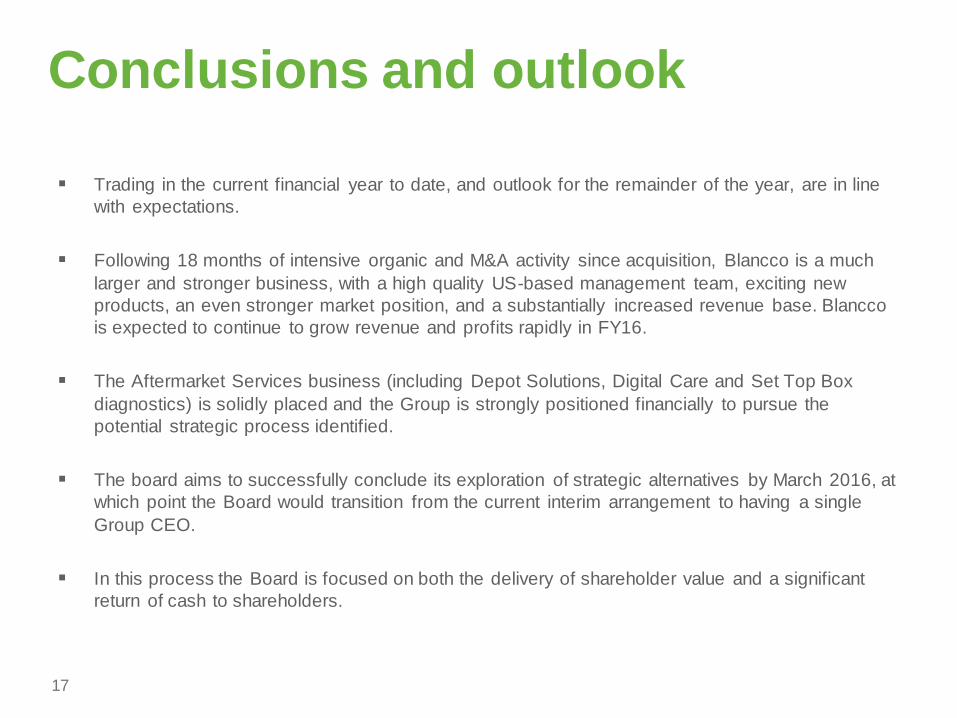

Conclusions and outlook

Trading in the current financial year to date, and outlook for the remainder of the year, are in line

with expectations.

Following 18 months of intensive organic and M&A activity since acquisition, Blancco is a much

larger and stronger business, with a high quality US-based management team, exciting new

products, an even stronger market position, and a substantially increased revenue base. Blancco

is expected to continue to grow revenue and profits rapidly in FY16.

The Aftermarket Services business (including Depot Solutions, Digital Care and Set Top Box

diagnostics) is solidly placed and the Group is strongly positioned financially to pursue the

potential strategic process identified.

The board aims to successfully conclude its exploration of strategic alternatives by March 2016, at

which point the Board would transition from the current interim arrangement to having a single

Group CEO.

In this process the Board is focused on both the delivery of shareholder value and a significant

return of cash to shareholders.

17