Embed Size (px)

Citation preview

Ministry of Finance

October 29, 2009

Fi sc a l st a b i l i z a t i o n :Th e Ch i l ea n ex per i en c e\

ТӨСВИЙН ТОГТВОРЖИЛТ: ЧИЛИ УЛСЫН ТУРШЛАГА

M o n g o l i a Ec o n o m i c Po l i c yCo n f er en c e 2009

Eric Parrado

International Finance Coordinator

Эрик ПаррадоОлон улсын санхүүгийн зохицуулагч

Ministry of Finance

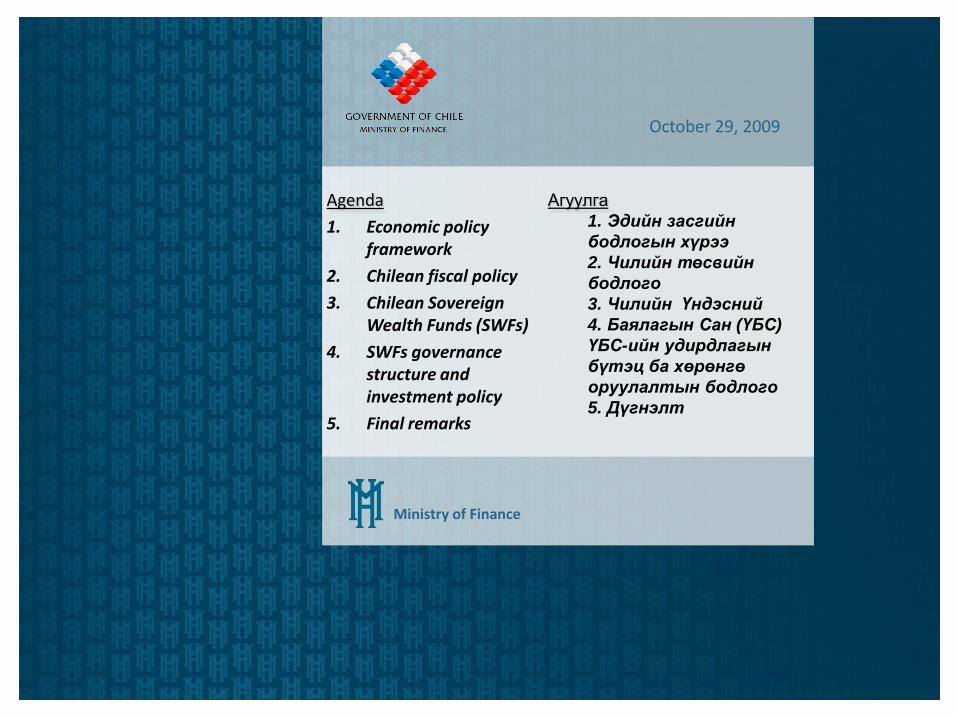

Агуулга1. Эдийн засгийн бодлогын хүрээ 2. Чилийн төсвийн бодлого 3. Чилийн Үндэсний 4. Баялагын Сан (ҮБС)ҮБС-ийн удирдлагын бүтэц ба хөрөнгө оруулалтын бодлого 5. Дүгнэлт

October 29, 2009

Agenda

1. Economic policy framework

2. Chilean fiscal policy

3. Chilean Sovereign Wealth Funds (SWFs)

4. SWFs governance structure and investment policy

5. Final remarks

Ministry of Finance

Ec o n o m i c po l i c y f r a m ew o r k

ЭДИЙН ЗАСГИЙН БОДЛОГЫН ХҮРЭЭ

1

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

Chilean economic policy strength is the result of an institutional design that ensures macroeconomic stability

The ability to reduce the effects of external shocks depends crucially on the implementation of a set of countercyclical policies

Countercyclical Monetary policy

Flexible exchange rateCountercyclical Fiscal policy

Sound financial system

Гадаад шокын нөлөөллийг бууруулах чадавхи нь эдийн засгийн мөчлөгийг дагасан биш бодлогын хэрэгжилтээс үндсэндээ хамаардаг

Мөчлөгийн эсрэг мөнгөний бодлого

Валютын уян хатан ханш

Санхүүгийн сайн тогтолцоо

Мөчлөгийн эсрэг төсвийн бодлого

Чилийн эдийн засгийн бодлогын давуу тал нь макро эдийн засгийн тогтворжилтийг хангаж байдаг институциональ бүтцийн үр дүн юм

Ministry of Finance

Chilean economic policy strength is the result of an institutional design that ensures macroeconomic stability

October 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

The ability to reduce the effects of external shocks depends crucially on the implementation of a set of countercyclical policies

1. The fiscal rule applied since 2001

unlinks the revenues with the

cyclical (temporary!) revenues

fiscal prudence

2. The Central Bank is autonomous

and enjoys high credibility

3. A flexible exchange rate that

absorbs external shocks

4. A strict financial regulation that

allows a sound financial system

Гадаад шокын нөлөөллийг бууруулах чадавхи нь эдийн засгийн мөчлөгийг дагасан биш (мөчлөгийн эсрэг)бодлогын хэрэгжилтээс үндсэндээ хамаардаг

1. 2001 оноос үйлчилж байсан төсвийн дүрэм журам нь мөчлөгийн (түр зуурын) орлоготой уялдаагүй төсвийн болгоомжлол

2. Төв Банк нь хэнд ч захирагддаггүй бөгөөд энэхүү өндөр эрх мэдэлдээ нэн тааламжтай байдаг

3. Гадаад шокыг шингээх чадавхи бүхий уян хатан ханш

4. Санхүүгийн сайн тогтолцоог бүрдүүлэхүйц хатуу чанга санхүүгийн зохицуулалт

Чилийн эдийн засгийн бодлогын давуу тал нь макро эдийн засгийн тогтворжилтийг хангаж байдаг институциональ бүтцийн үр дүн юм

Ministry of Finance

Ch i l ea n Fi sc a l Po l i c y

ЧИЛИЙН ТӨСВИЙН БОДЛОГО

2

Ministry of Finance

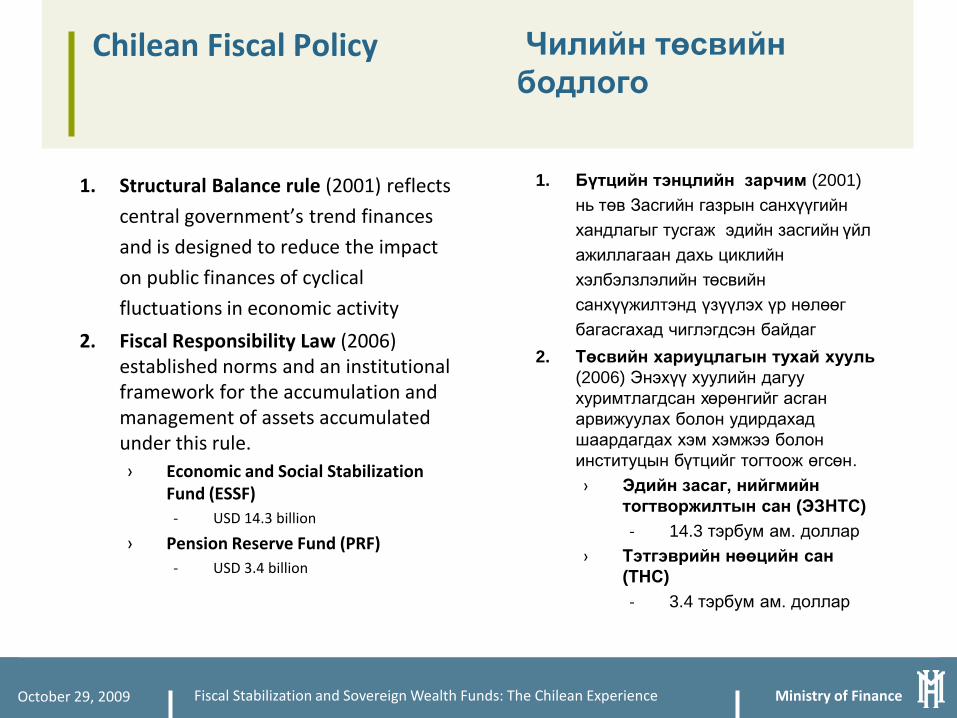

Chilean Fiscal Policy

October 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

1. Structural Balance rule (2001) reflects

central government’s trend finances

and is designed to reduce the impact

on public finances of cyclical

fluctuations in economic activity

2. Fiscal Responsibility Law (2006) established norms and an institutional framework for the accumulation and management of assets accumulated under this rule.› Economic and Social Stabilization

Fund (ESSF)‐ USD 14.3 billion

› Pension Reserve Fund (PRF)‐ USD 3.4 billion

1. Бүтцийн тэнцлийн зарчим (2001) нь төв Засгийн газрын санхүүгийн хандлагыг тусгаж эдийн засгийн үйл ажиллагаан дахь циклийн хэлбэлзлэлийн төсвийн санхүүжилтэнд үзүүлэх үр нөлөөг багасгахад чиглэгдсэн байдаг

2. Төсвийн хариуцлагын тухай хууль(2006) Энэхүү хуулийн дагуу хуримтлагдсан хөрөнгийг асган арвижуулах болон удирдахад шаардагдах хэм хэмжээ болон институцын бүтцийг тогтоож өгсөн.› Эдийн засаг, нийгмийн

тогтворжилтын сан (ЭЗНТС)‐ 14.3 тэрбум ам. доллар

› Тэтгэврийн нөөцийн сан(ТНС)‐ 3.4 тэрбум ам. доллар

Чилийн төсвийн бодлого

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

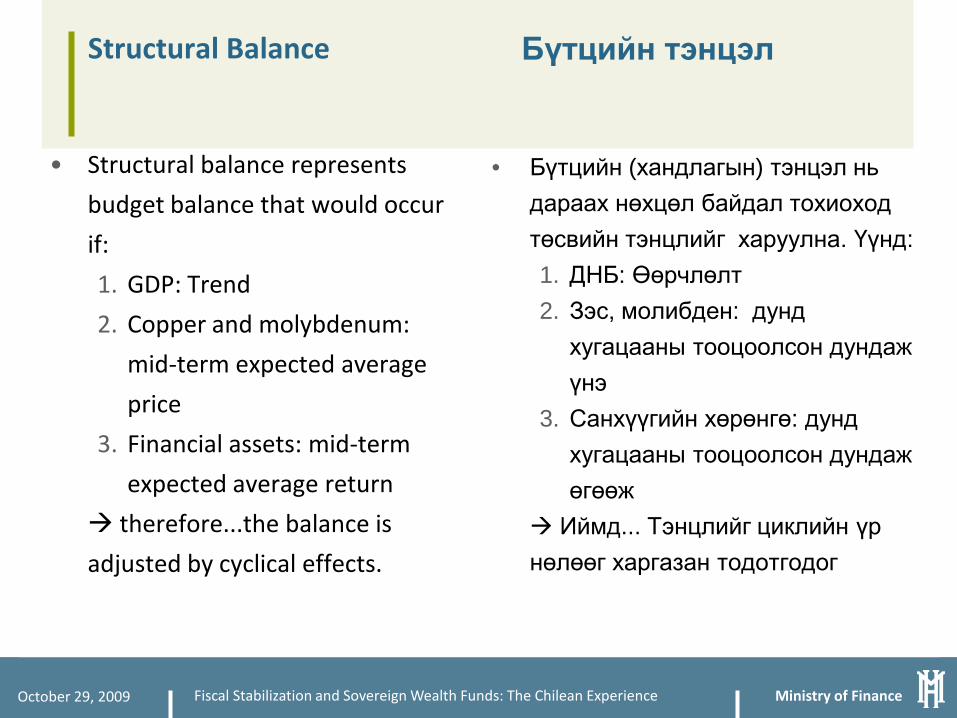

Structural Balance

• Structural balance represents

budget balance that would occur

if:

1. GDP: Trend

2. Copper and molybdenum:

mid‐term expected average

price

3. Financial assets: mid‐term

expected average return

therefore...the balance is

adjusted by cyclical effects.

• Бүтцийн (хандлагын) тэнцэл нь дараах нөхцөл байдал тохиоход төсвийн тэнцлийг харуулна. Үүнд: 1. ДНБ: Өөрчлөлт2. Зэс, молибден: дунд

хугацааны тооцоолсон дундаж үнэ

3. Санхүүгийн хөрөнгө: дунд хугацааны тооцоолсон дундаж өгөөж

Иймд... Тэнцлийг циклийн үр нөлөөг харгазан тодотгодог

Бүтцийн тэнцэл

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

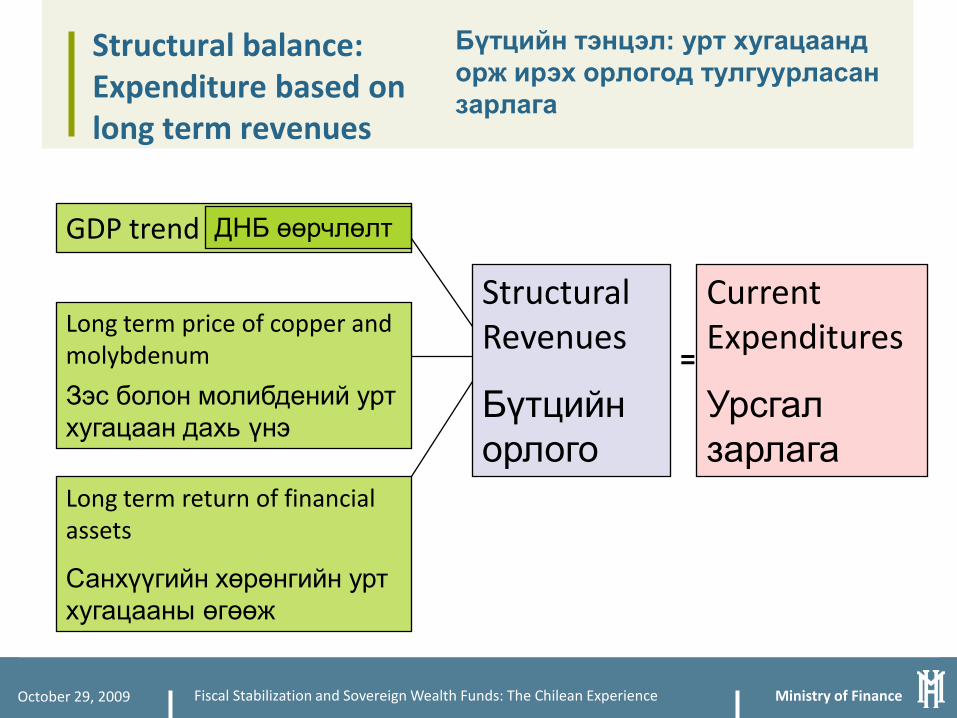

Structural balance: Expenditure based onlong term revenues

GDP trend

Long term price of copper and molybdenum

Зэс болон молибдений урт хугацаан дахь үнэ

Long term return of financialassets

Санхүүгийн хөрөнгийн урт хугацааны өгөөж

StructuralRevenues

Бүтцийн орлого

CurrentExpenditures

Урсгал зарлага

=

ДНБ өөрчлөлт

Бүтцийн тэнцэл: урт хугацаанд орж ирэх орлогод тулгуурласан зарлага

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

Structural balance: Expenditure based on long term revenues implies a countercyclical action

Long term price of copper

Price of copper

Savings

Use of savings

Long term price of copper defines fiscal returns and consequently this will be the ceiling amount for fiscal expenditures

Example: All fiscal revenues come from copper

Хадгаламж

Бүтцийн тэнцэл: урт хугацааны орлогод суурилсан зарлага нь эдийн засгийн мөчлөгийн хувирлыг дагаагүй үйл явцыг илэрхийлдэг

Жишээ: Бүх орлого зэсийн борлуулалтаас орж ирсэн

Зэсийн үнэ

Зэсийн урт хугацаан дахь үнэ

Хадгаламжаа ашиглах

Зэсийн урт хугацаан дахь үнэ нь төсвийн өгөөжийгхаруулах бөгөөд энэ нь эцсийн дүндээ төсвийн зарлагын дээд хязгаарын дүнг харуулах болно

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

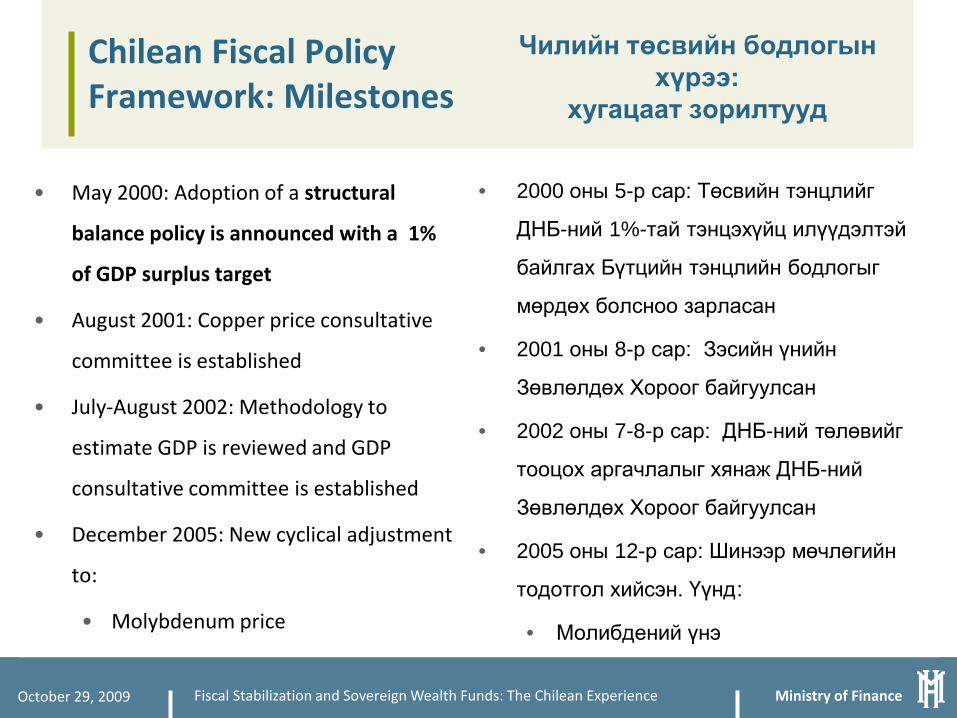

Chilean Fiscal Policy Framework: Milestones

• May 2000: Adoption of a structural

balance policy is announced with a 1%

of GDP surplus target

• August 2001: Copper price consultative

committee is established

• July‐August 2002: Methodology to

estimate GDP is reviewed and GDP

consultative committee is established

• December 2005: New cyclical adjustment

to:

• Molybdenum price

• 2000 оны 5-р сар: Төсвийн тэнцлийг

ДНБ-ний 1%-тай тэнцэхүйц илүүдэлтэй

байлгах Бүтцийн тэнцлийн бодлогыг

мөрдөх болсноо зарласан

• 2001 оны 8-р сар: Зэсийн үнийн

Зөвлөлдөх Хороог байгуулсан

• 2002 оны 7-8-р сар: ДНБ-ний төлөвийг

тооцох аргачлалыг хянаж ДНБ-ний

Зөвлөлдөх Хороог байгуулсан

• 2005 оны 12-р сар: Шинээр мөчлөгийн

тодотгол хийсэн. Үүнд:

• Молибдений үнэ

Чилийн төсвийн бодлогын хүрээ:

хугацаат зорилтууд

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

Chilean Fiscal Policy Framework: Milestones

• May 2007: The structural balance

policy is announced with a 0.5% of

GDP surplus for 2008

• October 2008: New cyclical

adjustment regarding financial

income from financial assets is

incorporated.

• January 2009: A extraordinary fiscal

stimulus plan reduced target to 0%

of GDP (for 2009)

Чилийн төсвийн бодлогын хүрээ:

хугацаат зорилтууд

• 2007 оны 5-р сар: 2008 онд Төсвийн

тэнцлийг ДНБ-ний 0.5%-тай тэнцэхүйц

илүүдэлтэй байх зорилтыг зарласан

• 2008 оны 10-р сар: Санхүүгийн хөрөнгөөс

олсон санхүүгийн орлоготой холбогдуулж

циклийн шинэ тодотгол хийж тусгасан.

• 2009 оны 1-р сар: Төсвийн дэмжлэгийн

онцгой төлөвлөгөөний дагуу зорилтоо

бууруулж 2009 оны Төсвийн тэнцлийг

ДНБ-ний 0 %-тай тэнцүү байхаар

тогтоосон

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

Structural Balance

• The expenditures are determined

according to structural revenues (no

current revenues)

• The rule implies:

1. Savings during windfalls

2. Finance deficits when slowdowns in

economic activity, and/or copper

and molybdenum prices and

investment returns are under mid‐

term trend

• However, structural balance may be

larger or smaller than actual balance

(depending on negative or positive

economic cycles)

Бүтцийн тэнцэл

• Бүтцийн орлогын дагуу зарлагыг

тодорхойлсон (урсгал орлого байхгүй)

• Үйлчилж буй дүрэм:

1. Гэнэтийн ашгийн үед хадгаламж хийх

2. Эдийн засгийн үйл ажиллагаа

саарсан, эсвэл зэс болон

молибдений үнэ буурсан болон

хөрөнгө оруулалтын өгөөж дунд

хугацааны таамагдаж байснаас доош

орсон үед дэх санхүүгийн алдагдал

• Гэхдээ, бүтцийн тэнцэл нь бодит тэнцлээс

нилээд их эсвэл бага байж болох юм

(эдийн засгийн эерэг эсвэл сөрөг

мөчлөгөөс хамаарч)

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

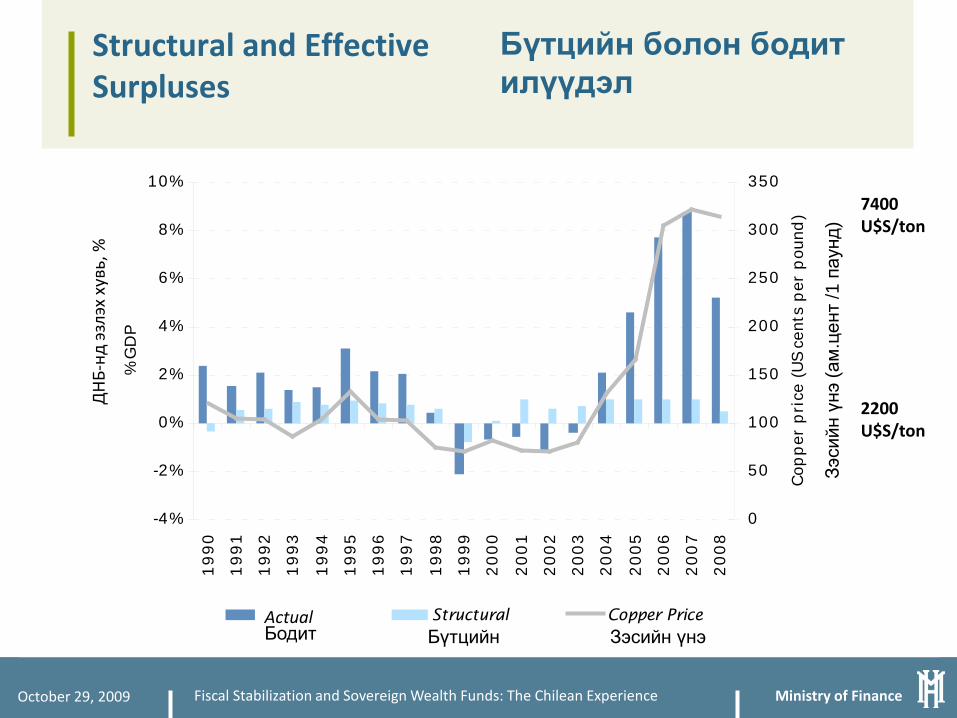

Structural and Effective Surpluses

-4%

-2%

0%

2%

4%

6%

8%

10%19

9019

9119

9219

93

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

% G

DP

0

50

100

150

200

250

300

350

Copp

er p

rice

(US

cent

s pe

r po

und)

Effective Structural Copper PriceActual

2200 U$S/ton

7400 U$S/ton

Бүтцийн болон бодит илүүдэл

Бодит Бүтцийн Зэсийн үнэ

Зэси

йн ү

нэ (а

м.ц

ент

/1 п

аунд

)

ДН

Б‐нд

эзл

эх х

увь,

%

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

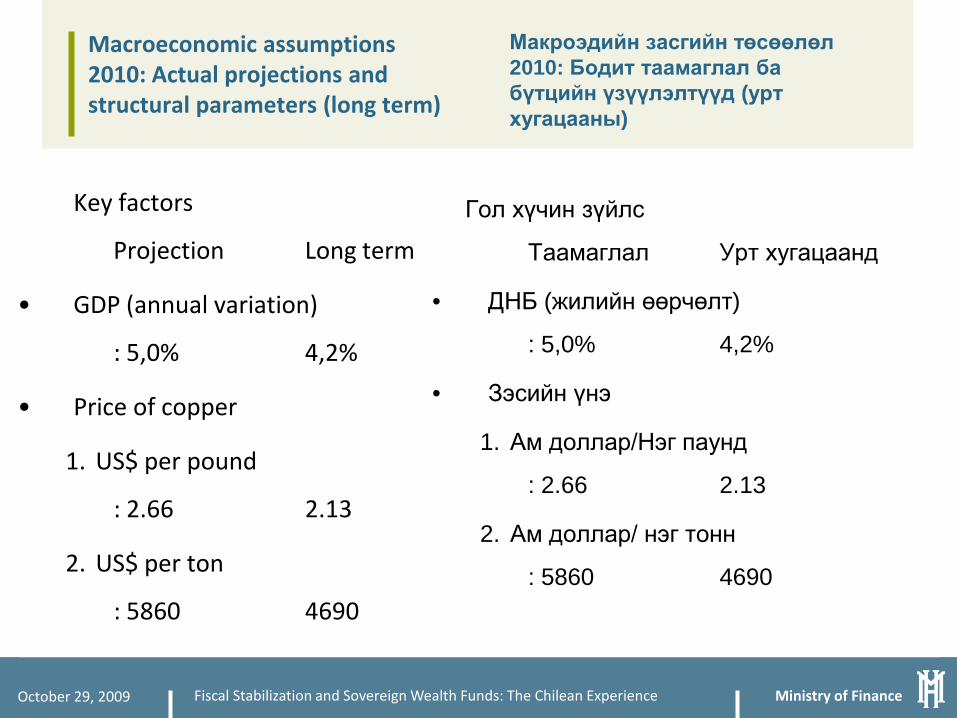

Macroeconomic assumptions 2010: Actual projections and structural parameters (long term)

Key factors

Projection Long term

• GDP (annual variation)

: 5,0% 4,2%

• Price of copper

1. US$ per pound

: 2.66 2.13

2. US$ per ton

: 5860 4690

Макроэдийн засгийн төсөөлөл2010: Бодит таамаглал ба бүтцийн үзүүлэлтүүд (урт хугацааны)

Гол хүчин зүйлс

Таамаглал Урт хугацаанд

• ДНБ (жилийн өөрчөлт)

: 5,0% 4,2%

• Зэсийн үнэ

1. Ам доллар/Нэг паунд

: 2.66 2.13

2. Ам доллар/ нэг тонн

: 5860 4690

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

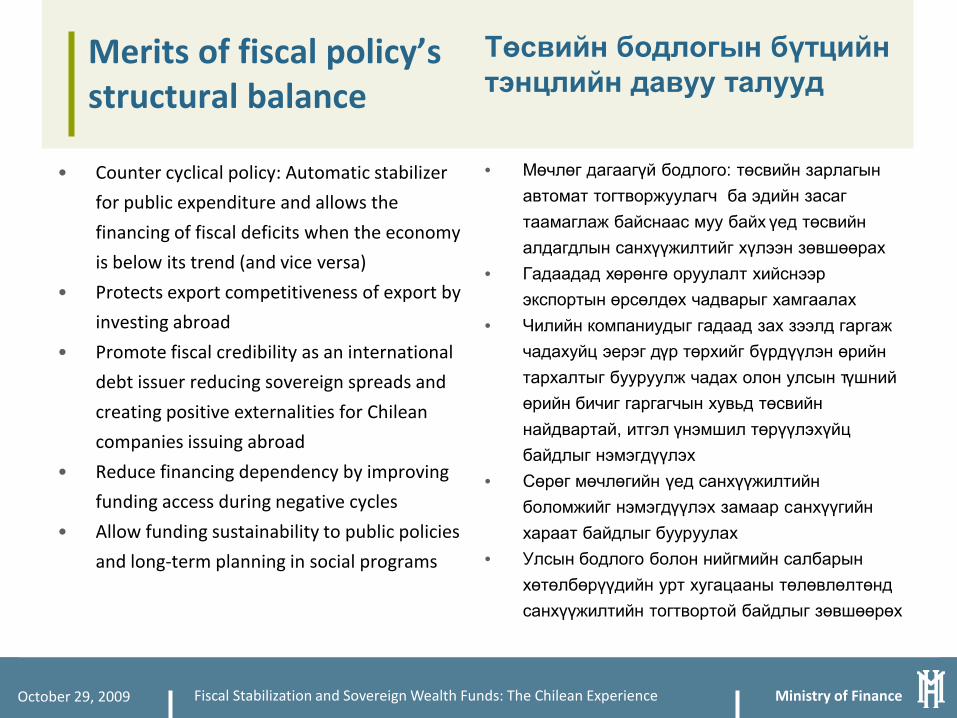

Merits of fiscal policy’s structural balance

• Counter cyclical policy: Automatic stabilizer

for public expenditure and allows the

financing of fiscal deficits when the economy

is below its trend (and vice versa)

• Protects export competitiveness of export by

investing abroad

• Promote fiscal credibility as an international

debt issuer reducing sovereign spreads and

creating positive externalities for Chilean

companies issuing abroad

• Reduce financing dependency by improving

funding access during negative cycles

• Allow funding sustainability to public policies

and long‐term planning in social programs

Төсвийн бодлогын бүтцийн тэнцлийн давуу талууд

• Мөчлөг дагаагүй бодлого: төсвийн зарлагын автомат тогтворжуулагч ба эдийн засагтаамаглаж байснаас муу байх үед төсвийн алдагдлын санхүүжилтийг хүлээн зөвшөөрах

• Гадаадад хөрөнгө оруулалт хийснээр экспортын өрсөлдөх чадварыг хамгаалах

• Чилийн компаниудыг гадаад зах зээлд гаргаж чадахуйц эерэг дүр төрхийг бүрдүүлэн өрийн тархалтыг бууруулж чадах олон улсын түшний өрийн бичиг гаргагчын хувьд төсвийн найдвартай, итгэл үнэмшил төрүүлэхүйц байдлыг нэмэгдүүлэх

• Сөрөг мөчлөгийн үед санхүүжилтийн боломжийг нэмэгдүүлэх замаар санхүүгийн хараат байдлыг бууруулах

• Улсын бодлого болон нийгмийн салбарын хөтөлбөрүүдийн урт хугацааны төлөвлөлтөндсанхүүжилтийн тогтвортой байдлыг зөвшөөрөх

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

Volatility measured as coefficient of variation

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1980-1986 1987-2000 2001-2006-

1

2

3

4

5

6

7

8

9Govt. investment growth volatilityGovt. spending growth volatilityOutput gap volatility

Source: Ministry of Finance

Merits of fiscal policy’s structural balance: reduction of macroeconomic volatility

Төсвийн бодлогын бүтцийн тэнцлийн давуу талууд: макроэдийн засгийн хэлбэлзэлийн багасалт

Хэлбэлзэл нь хэлбэлзлийн кофицентээр илэрхийлэгдсэн болно

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

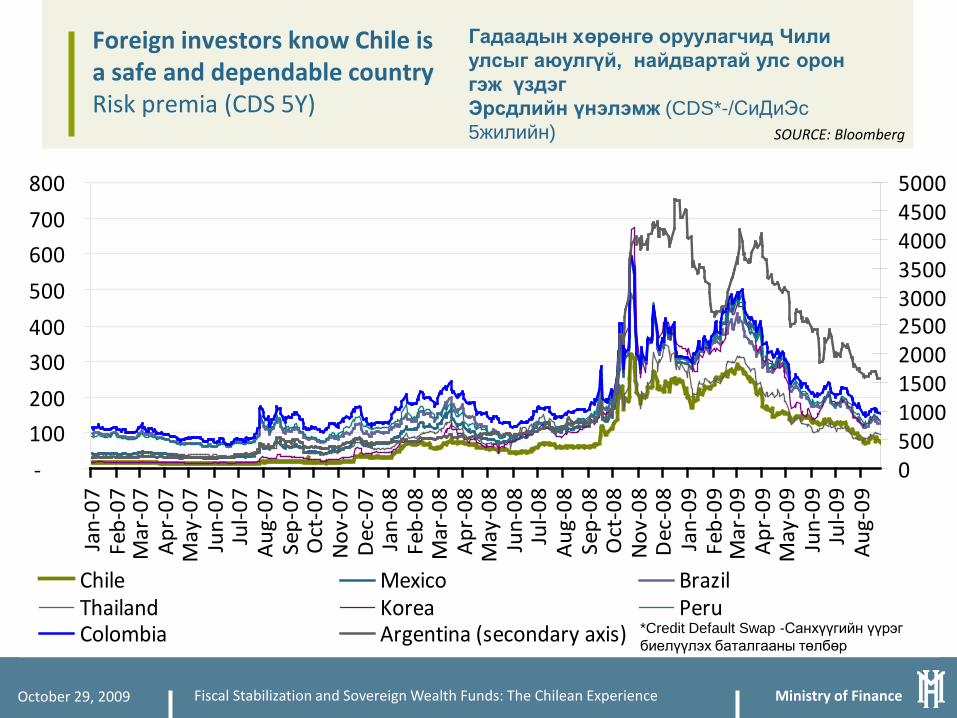

Foreign investors know Chile is a safe and dependable countryRisk premia (CDS 5Y)

SOURCE: Bloomberg

‐

100

200

300

400

500

600

700

800

Jan‐

07Fe

b‐07

Mar

‐07

Apr

‐07

May

‐07

Jun‐

07Ju

l‐07

Aug

‐07

Sep‐

07O

ct‐0

7N

ov‐0

7D

ec‐0

7Ja

n‐08

Feb‐

08M

ar‐0

8A

pr‐0

8M

ay‐0

8Ju

n‐08

Jul‐0

8A

ug‐0

8Se

p‐08

Oct

‐08

Nov

‐08

Dec

‐08

Jan‐

09Fe

b‐09

Mar

‐09

Apr

‐09

May

‐09

Jun‐

09Ju

l‐09

Aug

‐09

0500100015002000250030003500400045005000

Chile Mexico BrazilThailand Korea PeruColombia Argentina (secondary axis)

Гадаадын хөрөнгө оруулагчид Чили улсыг аюулгүй, найдвартай улс орон гэж үздэгЭрсдлийн үнэлэмж (CDS*-/СиДиЭс5жилийн)

*Credit Default Swap -Санхүүгийн үүрэг биелүүлэх баталгааны төлбөр

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

Chile is one of largest recipient of FDIForeign investment inflows (2008, % of GDP)

Чили улс нь Гадаадын хөрөнгө оруулалтыг хамгийн их хэмжээгээр хүлээж авдаг улс орнуудын нэг юм

ЭХ СУРВАЛЖ: ОУВС

SOURCE: IMF

Hun

gary

Chi

le

Col

ombi

a

Tha

iland

Chi

na

Peru

Pola

nd

Bra

zil

Mex

ico

Irel

and

Rus

sia

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35% •Гадаадын хөрөнгө оруулалтын орох урсгал (2008, ДНБ-нд эзлэх хувь, %)

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

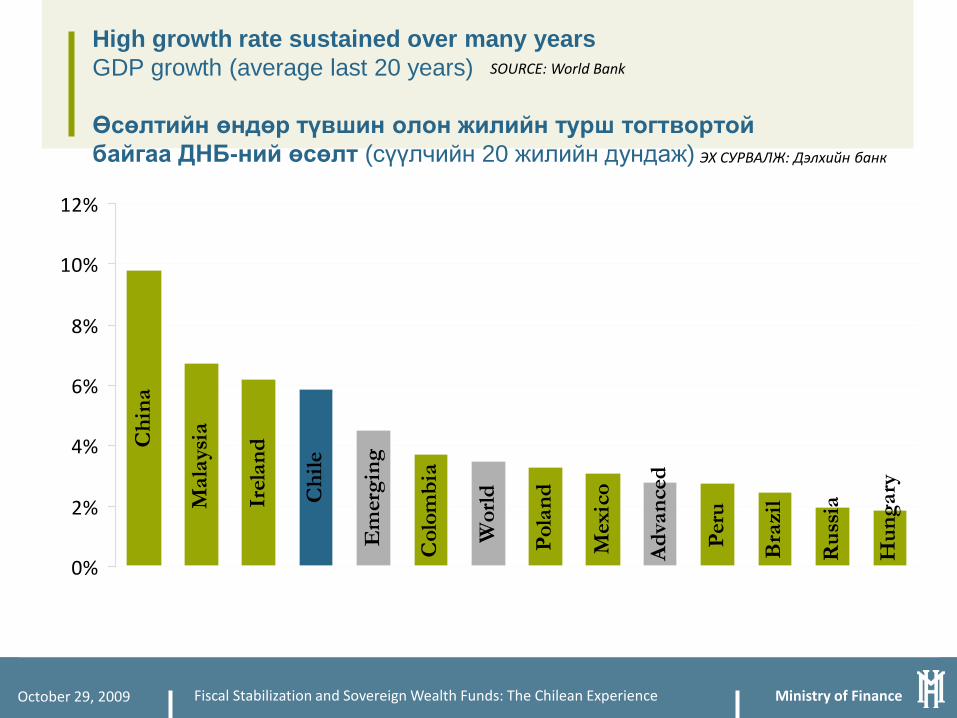

High growth rate sustained over many yearsGDP growth (average last 20 years)

Өсөлтийн өндөр түвшин олон жилийн турш тогтвортой байгаа ДНБ-ний өсөлт (сүүлчийн 20 жилийн дундаж)

SOURCE: World Bank

Chi

na

Mal

aysi

a

Irel

and

Chi

le

Em

ergi

ng

Col

ombi

a

Wor

ld

Pola

nd

Mex

ico

Adv

ance

d

Peru

Bra

zil

Rus

sia

Hun

gary

0%

2%

4%

6%

8%

10%

12%

ЭХ СУРВАЛЖ: Дэлхийн банк

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

Fiscal Policy Төсвийн бодлого Public debt Засгийн газрын өр(as percentage of GDP) (ДНБ‐нд эзлэх хувь, %)

SOURCE: Budget Office

-20%

-10%

0%

10%

20%

30%

40%

50%

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Gross Government Debt Net Government Debt

The Chilean Government has become a net creditor. During good times we saved and prepared for the lean times.

Чилийн Засгийн газар нь зээлдүүлэгч болсон. Бид сайн цагт хуримталж хэцүү цаг үеийн бэлтгэлийг хангасан

Засгийн газрын нийт өр Засгийн газрын цэвэр өр

ЭХ СУРВАЛЖ: Төсвийн газар

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

A flexible exchange rate policy and the responsible management of fiscal resources ensure competitiveness.

Exchange rate Мөнгөний ханш Multilateral real exchange rate Олон талт бодит ханшны түвшин

SOURCE: Central Bank of Chile

75

80

85

90

95

100

105

110

115

120

Jan‐

90

Oct

‐90

Jul‐9

1

Apr

‐92

Jan‐

93

Oct

‐93

Jul‐9

4

Apr

‐95

Jan‐

96

Oct

‐96

Jul‐9

7

Apr

‐98

Jan‐

99

Oct

‐99

Jul‐0

0

Apr

‐01

Jan‐

02

Oct

‐02

Jul‐0

3

Apr

‐04

Jan‐

05

Oct

‐05

Jul‐0

6

Apr

‐07

Jan‐

08

Oct

‐08

Multilateral Real Exchange Rate Average Jun1999‐Jun2009

Ханшны уян хатан бодлого болон төсвийн хөрөнгийн хариуцлагатай удирдлага нь өрсөлдөх чадварыг хангана.

Олон талт бодит ханшны түвшин1999 оны 6-р сараас 2009 оны6-р сар хүртэлх дундаж

ЭХ СУРВАЛЖ: Чилийн төв банк

Ministry of Finance

Chilean Sovereign Wealth Funds

ЧИЛИЙН ҮНДЭСНИЙ БАЯЛГИЙН САН3

Ministry of Finance

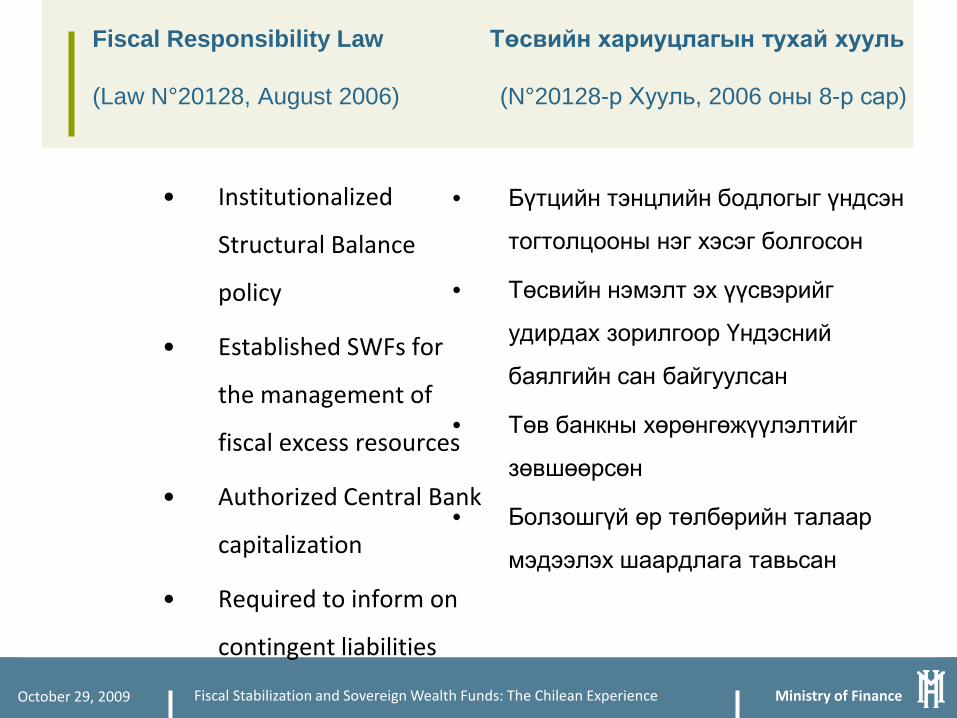

Fiscal Responsibility Law Төсвийн хариуцлагын тухай хууль

(Law N°20128, August 2006) (N°20128-р Хууль, 2006 оны 8-р сар)

October 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

• Institutionalized

Structural Balance

policy

• Established SWFs for

the management of

fiscal excess resources

• Authorized Central Bank

capitalization

• Required to inform on

contingent liabilities

• Бүтцийн тэнцлийн бодлогыг үндсэн

тогтолцооны нэг хэсэг болгосон

• Төсвийн нэмэлт эх үүсвэрийг

удирдах зорилгоор Үндэсний

баялгийн сан байгуулсан

• Төв банкны хөрөнгөжүүлэлтийг

зөвшөөрсөн

• Болзошгүй өр төлбөрийн талаар

мэдээлэх шаардлага тавьсан

Ministry of Finance

Extraordinary fiscal revenues are saved

Төсвийн хэвийн бус нэмэлт орлогыг хуримтлуулсан

October 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

Economic and Social

Stabilization Fund (ESSF)Fiscal Surplus – PRF and CBC

Capitalization Central Bank (CBC)

0.5% GDP in 5 years (optional)

Pension Reserve Fund (PRF)

• 0.2% GDP (min)

• 0.5% GDP (max)

Capitalization Central Bank (CBC)0.5% GDP in 5 years (optional)

Fiscal Surplus

Тэтгэврийн Нөөцийн Сан (ТНС)•ДНБ-ний 0.2% (мin) • ДНБ-ний 0.5% (мах)

Төв Банкны Хөрөнгөжүүлэлт (ТБХ)5 жилд ДНБ-ний 0.5% хүргэх(заавал биш)

Эдийн засгийн болон нийгмийн тогтворжилтын Сан (ЭЗНТС)Төсвийн тэнцлийн ашиг – ТНС болон ТБХС

Төсвийн тэнцлийн илүүдэл

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

0

0.5

1

1.5

2

2.5

3

3.5

-0.4 -0.1 0.2 0.5 0.8 1.1 1.4 1.7 2 2.3 2.6 2.9

Effective fiscal balance

Cont

ribu

tion

s

ESSF Capitalization BCCh PRF

(% of GDP)

Fiscal Saving Rule

Төсвийн Хуримтлалын Зарчим

......

... (ДНБ‐нд эзлэх хувь, %)

Ору

улса

н ху

вь х

эмж

ээ

ЭЗНТС Чилийн Төв Банкны хөрөнгөжүүлэлт

ТНС

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

ESSF EvolutionЭдийн засгийн болон нийгмийн тогтворжилтын Сан (ЭЗНТС)-гийн хөгжил

14,9

16

15,2

23

17,1

92

17,2

51

17,1

32

18,7

70

19,7

71

19,4

60

19,2

68

18,7

91

19,1

64

20,2

11

19,5

41

19,3

34

19,6

18

17,9

80

17,5

07

15,7

67

15,0

15

14,3

43

1,75

0

2,70

0

4,37

7

5,25

7

6,09

7

200

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

22,500Ja

n‐08

Feb‐

08

Mar

‐08

Apr

‐08

May

‐08

Jun‐

08

Jul‐0

8

Aug

‐08

Sep‐

08

Oct

‐08

Nov

‐08

Dec

‐08

Jan‐

09

Feb‐

09

Mar

‐09

Apr

‐09

May

‐09

Jun‐

09

Jul‐0

9

Aug

‐09

USD

Mill

ion

Fund Balance Cumulative withdrawals

Сая

ам

. дол

лар

Сангийн үлдэгдэл

Зарцуулсан хөрөнгө, өссөн дүнгээр

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

PRF Evolution

Тэтгэврийн Нөөцийн Сан (ТНС)-гийн хөгжил1,

506

1,53

7

1,57

4

1,54

3

2,43

4

2,45

2

2,45

2

2,41

4

2,39

0

2,33

1

2,37

6

2,50

7

2,42

3

2,39

8

2,45

8

2,44

8

2,51

5

3,34

0

3,36

7

3,40

7

0

500

1,000

1,500

2,000

2,500

3,000

3,500Ja

n‐08

Feb‐

08

Mar

‐08

Apr

‐08

May

‐08

Jun‐

08

Jul‐

08

Aug

‐08

Sep‐

08

Oct

‐08

Nov

‐08

Dec

‐08

Jan‐

09

Feb‐

09

Mar

‐09

Apr

‐09

May

‐09

Jun‐

09

Jul‐

09

Aug

‐09

USD

Mill

ion

Fund Balance

Сая

ам

. дол

лар

Сангийн үлдэгдэл

Ministry of Finance

General Objectives Ерөнхий зорилго

October 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

1. To reduce volatility of

fiscal expenditure

(especially social) and

its dependency on

cyclical swings in

economic activity, the

price of copper and

other variables that

determine effective

fiscal income.

2. To promote export

sector competitiveness.

1. Төсвийн зарцуулалтын, ялангуяа нийгмийн зардлын хэлбэлзлэлийг багасгах, төсвийн бодит орлогыг тодорхойлдог эдийн засгийн үйл ажиллагааны циклийн огцом өөрчлөлт, зэсийн үнэ болон хувьсах бусад хүчин зүйлээс түүний хамаарлыг бууруулах

2. Экспортын салбаруудын өрсөлдөх чадварыг нэмэгдүүлэх

Ministry of Finance

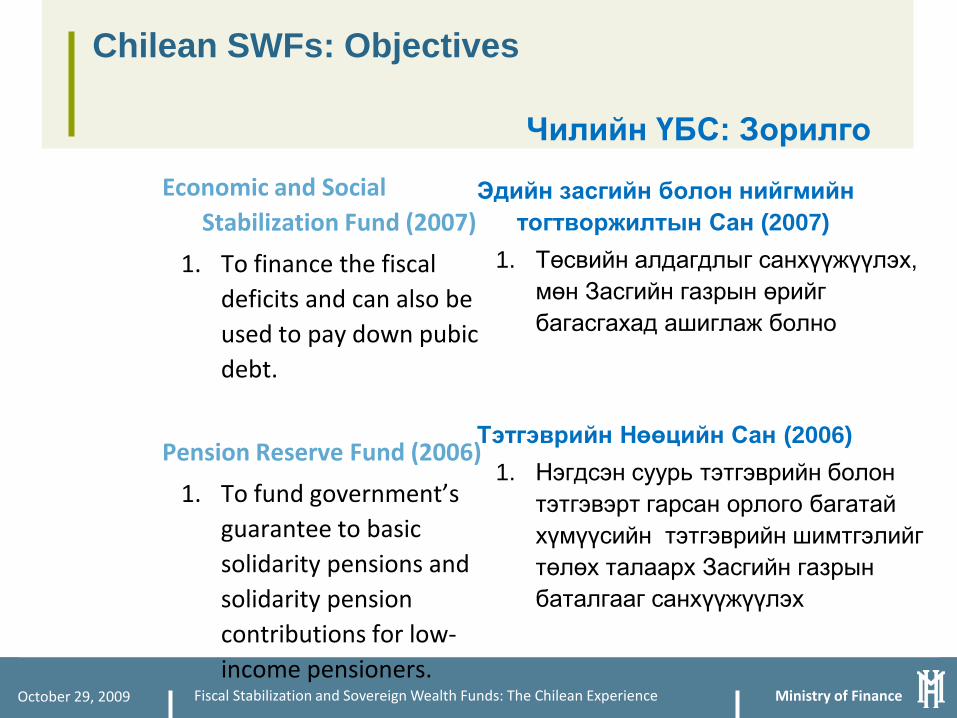

Chilean SWFs: Objectives

Чилийн ҮБС: Зорилго

October 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

Economic and Social Stabilization Fund (2007)

1. To finance the fiscal deficits and can also be used to pay down pubic debt.

Pension Reserve Fund (2006)

1. To fund government’s guarantee to basic solidarity pensions and solidarity pension contributions for low‐income pensioners.

Эдийн засгийн болон нийгмийн тогтворжилтын Сан (2007)

1. Төсвийн алдагдлыг санхүүжүүлэх, мөн Засгийн газрын өрийг багасгахад ашиглаж болно

Тэтгэврийн Нөөцийн Сан (2006)1. Нэгдсэн суурь тэтгэврийн болон

тэтгэвэрт гарсан орлого багатай хүмүүсийн тэтгэврийн шимтгэлийг төлөх талаарх Засгийн газрын баталгааг санхүүжүүлэх

Ministry of Finance

SWFs Governance Structure and investment policy

ҮБС-ИЙН ЗАСАГЛАЛЫН БҮТЭЦ БА ХӨРӨНГӨ ОРУУЛАЛТЫН БОДЛОГО

4

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

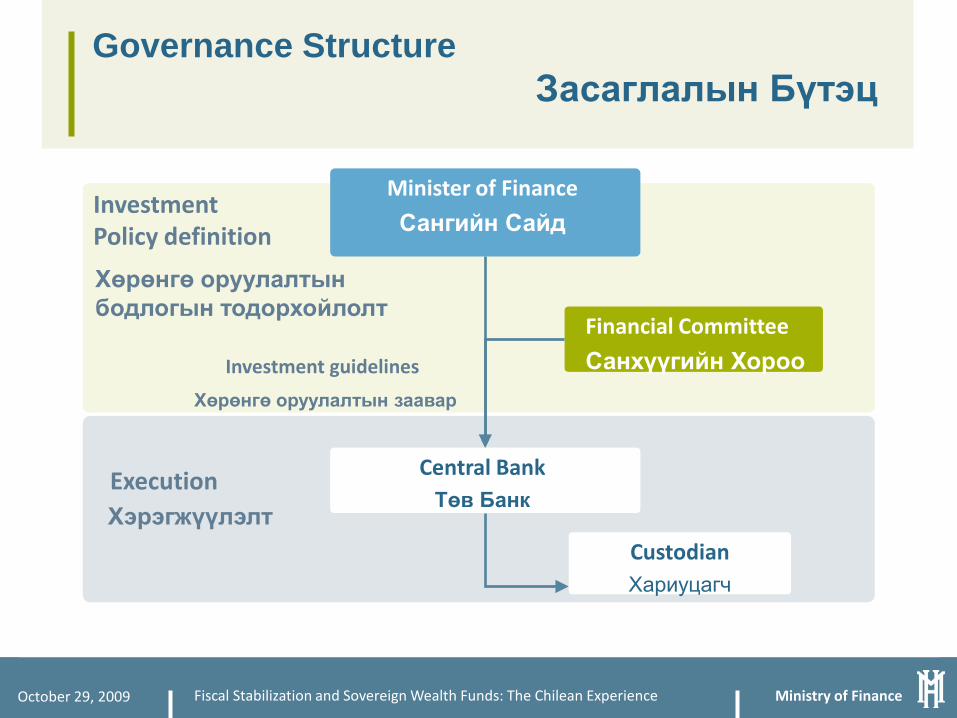

Governance StructureЗасаглалын Бүтэц

Minister of Finance

Сангийн Сайд

Financial Committee

Санхүүгийн Хороо

Central BankТөв Банк

Investment Policy definition

Execution

CustodianХариуцагч

Investment guidelines

Хөрөнгө оруулалтын заавар

Хэрэгжүүлэлт

Хөрөнгө оруулалтын бодлогын тодорхойлолт

Ministry of FinanceOctober 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

Current Asset Allocation: All investments are abroad and in lower risk instruments

Эргэлтийн Хөрөнгийн Хуваарилалт: Бүх хөрөнгө оруулалт гадаадад хийгдсэн ба маш бага эрсдэлтэй хэрэгсэлүүд

29.4%

4.0%

30.1%

3.7%

66.6%

ESSF 66.1%

PRF

Sovereign BondsMoney MarkeyInflation‐indexed bonds

Засгийн газрын бонд

Мөнгөний зах зээлИнфляцтай

индексжүүлсэн бонд

Ministry of Finance

Final remarks

ДҮГНЭЛТ5

Ministry of Finance

In sum Дүгнэлт

October 29, 2009 Fiscal Stabilization and Sovereign Wealth Funds: The Chilean Experience

• Fiscal stability and a clear legal framework pays off

• Our savings belong to all Chileans. They constitute a national good since they provide confidence to our economy by stabilizing social expenditure and maintaining public investment in the future.

• The assets accumulated in the ESSF have enabled us to finance countercyclical fiscal stimulus measures to boost activity and employment during 2009.

• Төсвийн тогтвортой байдал болон маш тодорхой хууль эрх зүйн хүрээ нь үр дүнд хүргэсэн

• Манай улсын ҮБС-ийн хөрөнгө нь Чилийн бүх ард түмний өмч. Энэхүү хөрөнгө нь нийгмийн зардлыг тогтворжуулан ирэйдүйн хөрөнгө оруулалтыг хангаж манай эдийн засагт итгэх итгэлийг бататгаж байгаагаараа үндэсний бүтээгдэхүүн юм

• Эдийн засаг, нийгмийн тогтворжилтын Санд хуримтлагдсан хөрөнгө нь 2009 онд үйл ажиллагаа, ажил эрхлэлтийг нэмэгдүүлэхэд чиглэгдсэн эдийн засгийн сөрөг мөчлөгийн үе дэх төсвийн дэмжлэгийг санхүүжүүлэх боломж олгосон

Ministry of Finance October 29, 2009

Fiscal stabilization: Төсвийн тогтворжилт:

The Chilean experience Чили улсын туршлага

Eric Parrado Эрик Паррадо

International Finance CoordinatorОлон улсын санхүүгийн зохицуулагч

![Fabrikasi Dan Karakterisasi Pandu Gelombang Planar … · implantation, dan ion exchange (pertukaran ion)[4]. Dalam teknik pertukaran ion, ion dari substrat dipertukarkan dengan ion](https://img.pdfslide.tips/doc/110x75/5b3f54c07f8b9a2f138bf310/fabrikasi-dan-karakterisasi-pandu-gelombang-planar-implantation-dan-ion-exchange.jpg)