Embed Size (px)

DESCRIPTION

Â

Citation preview

Working for

the best

Geschäftsbericht 2014

Geschäftsbericht 2014

Geschäftsbericht 2014 | Seite 3

Inhalt

MEGATECH Jahresrückblick Seite 6 Highlights 2014 Seite 8 Vorstand und Aufsichtsrat Seite 14

Interview mit dem Vorstand der MEGATECH Seite 16 Die wichtigsten MEGATECH Produkte im Überblick Seite 26

Die weltweiten Standorte der MEGATECH Group Seite 28 Die Selfie-Welt von MEGATECH Seite 30 Joint Management Meeting Seite 32 Megahoney Seite 36 Bericht des Aufsichtsrats Seite 37 Consolidated Financial Statements as of 31/12/2014 Seite 39

Management Report Seite 113 Auditor‘s Report Seite 125

Impressum Seite 126

Geschäftsbericht 2014 | Seite 4

MegAteCh industries hlinsko fertigt für die dritte genera-tion des Audi tt Coupé die heckklappenverkleidung, den rahmen der heckscheibe und die Ladekante.

Geschäftsbericht 2014 | Seite 4

Geschäftsbericht 2014 | Seite 5Geschäftsbericht 2014 | Seite 5

Geschäftsbericht 2014 | Seite 6

Dass wir diesen rückblick mit einem superlativ be-ginnen, geschieht aus respekt und Dankbarkeit

gegenüber allen, die den Weg gemeinsam mit uns gehen, die Verantwortung gemeinsam mit uns schul-tern, die entscheidungen gemeinsam mit uns tra-gen und die Leistung ge-meinsam mit uns erbrin-gen. gemeinsam gehört uns daher auch der erfolg und der stolz auf den fol-genden superlativ: 2014

war das erfolgreichste Jahr in der geschichte der MegAteCh industries Ag.

Was uns im abgelaufenen geschäftsjahr erfreute und ermutigte:

Die Auftragslage auf dem europäischen Markt

Unsere europäischen Werke arbeiteten nahe ihrer Vollauslastung und erzielten dank vieler gelungener operativer Verbesserungen einen gewinn nach steuern.

für drei Modelle von Audi – dem A3 Cabrio, dem tt und dem tt Cabrio – hatten wir 2014 Produktionsanläufe. für diese Modelle produ-zieren wir u. a. die heckklappenverkleidungen,

heckscheibenrahmen, Ladekanten und koffer-raumverkleidungen.

Mit opel, Porsche, bentley und Volkswagen nutzfahrzeuge konnten vier bedeutende neu-kunden dazugewonnen werden.

Das tech Center wächst unter neuer Leitung stetig weiter und ist dabei dank der anhaltend guten Auftragslage voll ausgelastet.

im Jahresdurchschnitt hatten 1.400 Mitarbeiter einen sicheren und zukunftsträchtigen Arbeits-platz innerhalb der verschiedenen einheiten der MegAteCh gruppe.

erfolgreiche strukturelle Verbesserungen

Das forschungs- und entwicklungsteam unse-res tech Centers ist ins Automotive intelligence Center in boroa bei bilbao übersiedelt und kann hier endlich unter einem Dach entwickeln, die Projektabwicklung steuern und die notwendi-gen Prototypen fertigen.

Das baulich veraltete Werk Liberec wurde ge-schlossen und die Produktion, soweit wir sie weiterführen, in die Werke hlinsko und Jablo-nec verlagert.

im september wurde die neue Produktionshalle 100 in hlinsko mit einem tag der offenen tür eröffnet. Mehr als 1.000 besucher strömten an diesem tag ins Werk.

Wir bliCkEn MiT FrEuDE AuF DAS AbGElAuFEnE GESCHäFTS-

jAHr 2014 zurüCk.

2014 war das erfolgreichste Geschäftsjahr in der Geschichte der

MEGATECH industries AG seit 2009.

Es ist uns gelungen,mit Opel, Porsche,

Bentley und Volkswagen nutzfahrzeuge vier

bedeutende neukunden zu gewinnen.

Geschäftsbericht 2014 | Seite 7

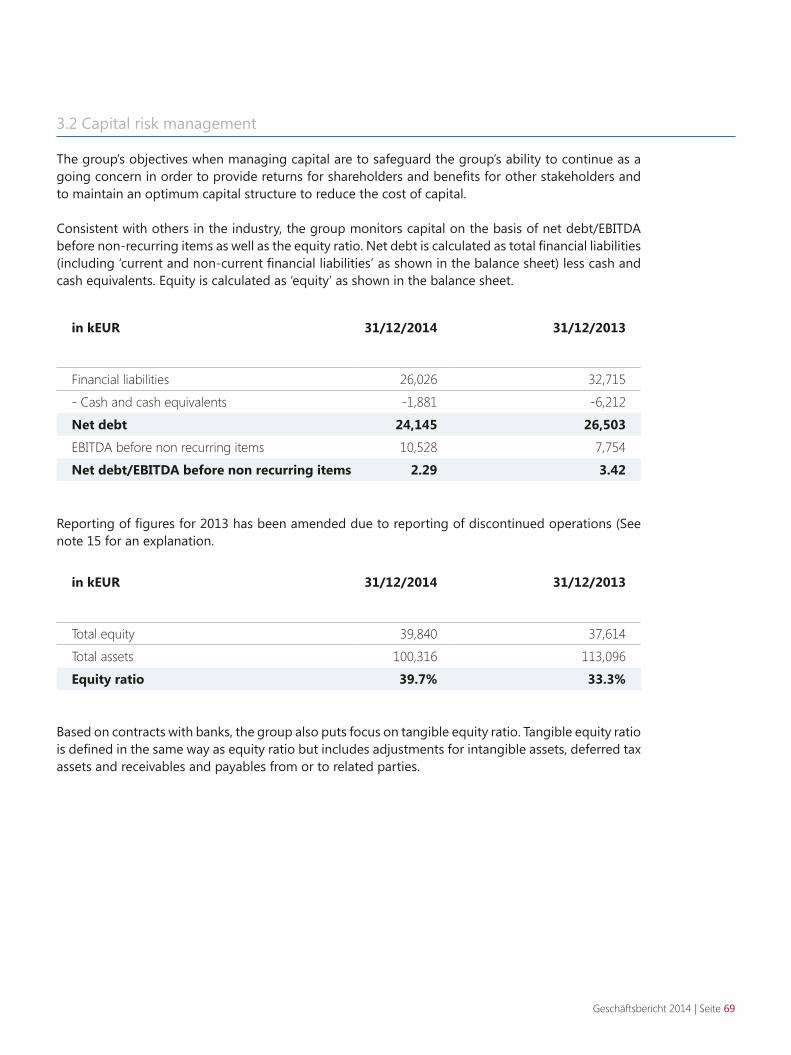

Die solide finanzierungsbasis

WirhabenmitČeskáspořitelnaeinenneuenFi-nanzierungspartner unserer tschechischen Wer-ke gewonnen und dadurch die finanzierung der laufenden und zukünftigen Projekte auf eine langfristig solide basis gestellt.

Auch in spanien hat sich die finanzierung von Werkzeugen und Projektabwicklung erfreulich entwickelt.

Der positive trend spiegelt sich auch in der 2014 erfolgten Aktualisierung unseres Corporate Design und unseres Webauftrittes mit optimierter verbes-serter homepage.

Der Aufsichtsrat der gesellschaft hat im november 2014 gerhard Pesout zum dritten Mitglied des Vor-stands bestellt. er gehört bereits seit september 2013 in seiner funktion als Country Manager unse-rer tschechischen Werke dem führungsteam an. Darüber hinaus wurde die systematische Verstär-kung unseres Managements in allen einheiten und Ländern weiter fortgesetzt.

im bewusstsein, dass solche stolzen erfolgsmel-dungen erstens Momentaufnahmen sind und zweitens eigentlich schon die Vergangenheit abbil-den, wenden wir uns der gegenwart und Zukunft zu – und damit beträchtlichen herausforderungen:

so erfreulich das geschäftsjahr 2015 für unsere europäischen Werke und das tech Center begon-nen hat: Unser standort brasilien bleibt leider ein sorgenkind. Die schwierige wirtschaftliche Lage unddierückläufigeAutomobilproduktioninBrasi-lien haben unsere bemühungen der vergangenen Jahre zunichte gemacht und dazu geführt, dass 2014 wieder ein Verlust verzeichnet werden musste.

obwohl brasilien ein für MegAteCh langfristig strategisch wichtiger Markt ist, müssen wir uns an-gesichts des derzeitigen schwierigen Marktumfel-des und der angespannten Wirtschaftslage vorbe-halten, sämtliche optionen zu überprüfen.

Davon unbeeinträchtigt bleiben unsere interna-tionalen expansionszie-le: Wir wollen unser Unternehmen durch or-ganisches Wachstum und Akquisitionen wei-ter ausbauen und bemü-hen uns deshalb ver-stärkt um internationale kooperationen, um auch in Ländern, auf Märkten und mit Produkten tätig werden zu können, in denen wir heute noch nicht vertreten sind.

Auch für 2015 haben wir uns ehrgeizige Ziele ge-steckt. große Anstrengungen werden notwendig sein, um sie zu erreichen, aber die erfolge des ab-gelaufenen geschäftsjahres machen diesbezüglich Mut. Wir danken allen kolleginnen, die durch ihre persönliche Leistung dazu beigetragen haben, von herzen.

Maximilian gesslerMitglied des Vorstandes

Große Anstrengungenwerden notwendig sein,um unsere ehrgeizigen ziele zu erreichen, aber die Erfolge des abgelaufenen Geschäft-jahres machen Mut.

MAXiMiliAn GESSlErMitglied des Vorstandes

der MegAteCh industries Ag

Geschäftsbericht 2014 | Seite 8

MegAteCh industries Ag

Das abgelaufene Jahr 2014 war das erfolgreichste in der geschichte der MegAteCh industries Ag. Alle Werke – mit Ausnahme des Werks in brasilien – schlossen mit einem gewinn nach steuern ab.

Die 2013 aufgebauten und initiierten Controlling- & reportingprozesse inklusive der implementierung einer eigenen konsolidierungs- und Planungs-soft-ware für alle standorte konnten 2014 abgeschlossen werden. somit sind sämtliche unserer standorte in den bereichen Controlling & reporting auf kapital-marktfähigem niveau.

insbesondere aus finanzierungssicht war 2014 ein besonders erfreuliches Jahr. Mittels einer erfolgrei-chen Umschuldung des kredit-Portfolios in tsche-chienistdieRefinanzierunggelungen.

im bereich des recruitings wurden unsere Manage-ment teams in allen Ländern und einheiten ver-stärkt. Mit gerhard Pesout wurde im november 2014 ein drittes Mitglied in den Vorstand bestellt. Zuvor war herr Pesout als Country Manager in tschechien für MegAteCh tätig.

2014 wurde das MegAWAtt system weiter ausge-baut, ein Programm, bei dem alle Mitarbeiter dazu eingeladen werden, innovative ideen einzureichen. Die besten Vorschläge werden in regelmäßigen intervallen direkt in den Werken ausgewählt, umge-setzt und mit Preisen ausgezeichnet.

Zur Verbesserung unserer internen kommunikation haben wir den firmennewsletter „Megazin insider“

gestartet und ausgebaut. Der newsletter erscheint einmal im Monat und berichtet über Wissenswertes aus den Werken weltweit. für die externe kommuni-kation wurde erstmals ein geschäftsbericht publi-ziert und die Webpage neu gestaltet.

MegAteCh tech Center & sales (spanien)

Das tech Center wurde Anfang des Jahres nach bo-roa bei bilbao in das AiC-Automotive intelligence Center – einem forschungs- und entwicklungszent-rum für firmen des Automobilsektors – ausgelagert. Dadurch war es uns möglich, die forschung, Pla-nung, Projektabwicklung und Prototypenfertigung an einem standort konzentriert zusammenzufassen. Durch die gute Auftragslage war das tech Center voll ausgelastet und konnte zusätzliche Mitarbeiter aufnehmen.

DiE HiGHliGHTS 2014 Ein ereignisreiches Geschäftsjahr als starkes

Fundament für die kommenden jahre.

AiC – Automotive intelligence Center

Geschäftsbericht 2014 | Seite 9

MegAteCh industries Czech republic

im ersten halbjahr 2014 wurde das Werk in Liberec geschlossen und die Produktion, soweit sie weiter-geführt wird, in die Werke hlinsko und Jablonec ver-lagert. für die belegschaft des Werks MegAteCh industries Liberec wurde ein outplacement Pro-gramm entwickelt, um sie bei der suche nach einer neuen Arbeitsstelle zu unterstützen. einige Mit-arbeiter konnten in anderen standorten der MegA-teCh industries weiterbeschäftigt werden.

Das Werk in hlinsko verzeichnete zahlreiche Auf-tragseingänge von Peugeot, Volkswagen, Audi, seat, Škoda, den neukunden Porsche und Volkswagen nutzfahrzeuge sowie von Automotive Lighting und Mahle behr.

nach mehreren Jahren der Verluste verzeichneten beide Werke 2014 einen gewinn, und das Werk hlinsko konnte in diesem Jahr erstmals seine Mit-arbeiterzahl erhöhen.

im september 2014 lud MegAteCh industries in hlinsko zum tag der offenen tür mit mehr als 1.000 besuchern – in einer stadt mit 10.000 einwohnern. im Zuge dessen wurde die renovierte Produktions-halle „Hall 100“ durchdie Bürgermeisterin offizielleröffnet. Das Werk wurde sponsor der eishockey-mannschaft hC hlinsko und des kulturzentrums der stadt.

MegAteCh industries Jablonec

OffizielleEröffnungvon„Hall100“beim tag der offenen tür für besucher

Geschäftsbericht 2014 | Seite 10

MegAteCh industries Peninsula iberica (spanien/Portugal)

in unseren Werken in spanien und Portugal wurden zahlreiche Verbesserungen des Produktionsablaufes vorgenommen, um sowohl die Qualität als auch die Produktivität zu steigern und gleichzeitig den La-gerbestand zu reduzieren. hervorzuheben sind die erfreulichen gewinne unserer Werke in orense (spa-nien) und Marinha grande (Portugal).

Die Werke der iberischen halbinsel erhielten Aufträ-ge von Peugeot für die entwicklung und herstellung eines innovativen, multifunktionellen ViP tisches – einer Mittelkonsole für fahrzeuge mit gehobener Ausstattung. erfreulich ist weiters die erweiterung der kunden um zwei namhafte Autohersteller mit bentley und opel, für die bedeutende Umfänge für den fahrzeuginnenraum hergestellt werden.

neben der optimierung der Arbeitsabläufe wurde auch in die Verbesserung der Ausstattung investiert.

MegAteCh industries brazil

trotz der äußerst schwierigen gesamtwirtschaftli-chen situation in brasilien konnte MegAteCh in-dustries brazil Auftragseingänge von renault und Volkswagen sowie samvardhana Motherson Pegu-form (sMP) verzeichnen.

Produktionsbereich brasilien

Produktionshalle MegAteCh industries orense (spanien)

Produktionshalle MegAteCh industries Marinha grande (Portugal)

Geschäftsbericht 2014 | Seite 11

Die geschulte Mitarbeiterin an unserem Standort in Portugal garantiert verlässliche Qualität.

Aus unserem Werk MegAteCh industries hlinsko kommen ebenfalls Verkleidungs-teile des kofferraums für die soeben neu gestartete Produktion des Audi tt Cabrio.

Geschäftsbericht 2014 | Seite 12

Geschäftsbericht 2014 | Seite 13

Geschäftsbericht 2014 | Seite 14

Dr. GEorG FlAnDorFEr wurde am 14. november 2011 als Vorsitzender in den Aufsichtsrat der MEGATECH Industries AG gewählt. Er ist ehemaliges Mitglied des Vorstands der Volkswagen AG.

AuFSiCHTSrAT

MAG. ulrikE GESSlEr-WolFinGEr ist notarin in Wien. Sie ist seit 26. november 2009 Mitglied des Aufsichtsrats der MEGATECH industries AG.

MAG. HErbErT HouF wurde am 24. Februar 2012 in den Aufsichtsrat der MEGATECH Industries AG gewählt und ist dessen stellvertretender Vorsitzender und Mitglied des Prüfungsausschusses. Hauptberuflich ist Mag. Houf als Wirtschaftsprüfer und Steuerberater in Wien tätig.

MATTHiAS übEl, bA, MbA wurde mit 4. April 2013 in den Aufsichtsrat der MEGATECH industries AG gewählt. Er gehört ebenfalls dem Prüfungsausschuss an. Er ist Mitglied des Vorstands der Endurance Capital AG in München.

Die funktionsperiode aller Aufsichtsratmitglieder endet mit dem Ablauf jener hauptversammlung, die über das ergebnis des Jahresabschlusses 2014 entscheidet.

Geschäftsbericht 2014 | Seite 15

VorSTAnD

Dr. MAXiMiliAn GESSlEr ist seit 26. november 2009 Mitglied des Vorstands und zeichnet sich verantwortlich für die bereiche Strategie, Vertrieb, Entwicklung, Personal, kommunikation und business Development.

DkFM. rAinEr DiECk ist seit 1. April 2013 Mitglied des Vorstands und zuständig für die bereiche Finanzen, Controlling, iT, Einkauf sowie M&A.

DiPl. inG. GErHArD PESouT verantwortet als Mitglied des Vorstands seit 10. november 2014 die bereiche Produktion, Qualität, logistik und MEGATECH Excellence System.

Geschäftsbericht 2014 | Seite 16

MAXiMiliAn GESSlErseit Juli 2008 Ceo der

MegAteCh gruppe

er ist seit 1986 in der in-

dustrie tätig – seit 1989 als

Unternehmer in der Metall-

und kunststoffbranche.

rAinEr DiECkseit April 2013 Cfo der

MegAteCh industries Ag

Davor war rainer Dieck

sechs Jahre lang in leitender

Position bei kPMg Advisory

Ag, Wien tätig.

Der studierte Diplom-kauf-

mann ist seit 1993 in ver-

schiedenen funktionen als

berater und Manager tätig.

Geschäftsbericht 2014 | Seite 16

Geschäftsbericht 2014 | Seite 17

MEGATECH IST in AllEn bErEiCHEn

ATTrAkTiVEr GEWorDEnMaximilian GESSlEr,

rainer DiECk und Gerhard PESouT im großen Vorstands-interview

GEHARD PESouTseit Juni 2014 Coo der

MegAteCh industries Ag

er ist seit 1978 in leitenden

Positionen in der Auto-

mobilbranche tätig und

war zuletzt Werkleiter

von faurecia in Peine,

Deutschland.

Geschäftsbericht 2014 | Seite 17

Geschäftsbericht 2014 | Seite 18

Der Vorstand der MegAteCh industries Ag, Maximilian gessler (group Ceo), rainer Dieck (group Cfo) und gerhard Pesout (group Coo) im gespräch über das vergangene geschäftsjahr, aktuelle Pläne und künftige herausforderungen.

ein kurzer rückblick auf das geschäftsjahr 2014 ...

MAXiMiliAn GESSlEr: 2014 war erfreulicher-weise ein sehr erfolgreiches geschäftsjahr, in dem es uns gelungen ist, einen großteil unse-rer Vorhaben umzusetzen. Wir haben mit einer

einzigen Ausnahme an al-len standorten gewinne erzielt, waren aber auch auf nicht operativen ge-bieten erfolgreich: bei der Akquisition neuer Aufträge, Refinanzierungen oder derVerbesserung aller Prozesse.

rAinEr DiECk: insbesonde-re auch aus finanzierungs-sicht war es ein erfreuliches Jahr, da uns die erfolgrei-che Umschuldung eines 25 Mio. eUr kredit-Portfolios in tschechien gelungen ist.

DurchdieseRefinanzierung sowiedie guteGe-schäftsentwicklung im letzten Jahr haben sich die Voraussetzungen für eine stabile finanzierungs-truktur in der gesamten gruppe deutlich verbes-sert. Die banken sehen MegAteCh mittlerweile wieder als verlässlichen Partner an. Leider verlief die entwicklung unseres standortes in brasilien kritisch. Dort ist es ab februar 2014 zu einem dramatischen Markteinbruch gekommen, der in dieser form von niemandem vorhergesehen wer-den konnte.

GErHArD PESouT: obwohl ich erst seit kurzem bei MegAteCh bin, waren 2014 im Vergleich zu 2013 die optimierung der organisation in tsche-chien mit entsprechend besseren ergebnissen und die Vorbereitung auf die nunmehr angelau-fenen und anstehenden neuen Aufträge positi-ve highlights für mich. Wir haben durch unsere bessere Leistung an Attraktivität für kunden und nicht zuletzt auch für banken gewonnen.

Worin erkennt ein Unternehmen seine eigene Attraktivität?

GESSlEr: Anhand der bewerbungen – daran, dass wir für interessante Leute attraktiv werden. Wir haben im vergangenen Jahr deutlich gemerkt, dass wir auch von Menschen, die bei etablierten

Der Auftragseingang 2014 hat ausschließlich

neue Automodellebetroffen, was uns beim

Anlaufen der Produktion 2015 und 2016 entspre-

chend stark steigende umsätze einbringen wird.

A-klasse-Unternehmen tätig sind oder waren, als interessanter Arbeitgeber wahrgenommen wer-den. so ist auch gerhard Pesout zu uns gestoßen, der seine karriere nach jahrelanger tätigkeit bei ford, Volvo, bosch und zuletzt bei faurecia nun bei uns fortsetzt.

Worin lag 2014 das hauptaugenmerk bei den investitionen?

GESSlEr: Der Auftragseingang 2014 hat aus-schließlich neue Automodelle betroffen, was uns beim Anlaufen der Produktion 2015 und 2016 entsprechend stark steigende Umsät-ze einbringen wird. in der entwicklungs- und Vorbereitungsphase bedingen solche neuauf-träge ein entsprechendes investitionsvolumen, etwa in entwicklung, Werkzeuge, Maschinen oder gebäude, wie es im vergangenen Jahr am standort hlinsko geschehen ist.

DiECk: ein schwerpunkt aus meiner sicht war, dass wir wieder verstärkt aus dem eigenen Cashflow investieren konnten. Die hierzu not-wendigeInnenfinanzierungskrafthabenwirunsdurch gute operative ergebnisse in den einzel-nen Werken erarbeitet. neben investitionen in Maschinen und gebäude konnten wir im letz-ten Jahr auch in den it-bereichen unserer tsche-chischen und spanischen Werke weitreichende

Verbesserungen durchführen. in diese richtung wird auch 2015 weitergearbeitet. Aus heutiger sicht können wir fest-stellen, dass alle notwen-digen investitionen für 2015 bereits weitgehend mit entsprechenden fi-nanzierungszusagen ab-gesichert sind.

PESouT: ich bin mit er-fahrung im bereich Lean Management zu MegA-teCh gekommen und sehe die investitionen von 2014 als Meilenstein in der Umsetzung der Prinzipien des Lean Managements. operational excellence an allen standorten ist unser gesetz-tes Ziel.

für welche 2014 auf dem Markt erschienen Modelle wird von MegAteCh zugeliefert?

GESSlEr: Audi tt Coupé und tt Cabrio waren wohl die aufsehenerregendsten Modelle 2014, und die Produktion für den ebenfalls von uns belieferten Audi Q7 wird demnächst starten. Darüber hinaus produzieren wir am standort hlinkso auch für tier 2 Lieferanten.

Audi TT Coupé und TT Cabrio waren wohl die aufsehenerregendstenModelle 2014 und dieProduktion für den eben-falls von uns beliefertenAudi Q7 wirddemnächst starten.

Geschäftsbericht 2014 | Seite 19

Geschäftsbericht 2014 | Seite 20

hat das 2013 neu aufgesetzte Controlling im vergangenen Jahr bereits vollständig gegriffen oder ist dieser Prozess noch in entwicklung?

DiECk: Die 2013 aufgebauten und initiierten Prozesse inklusive der implementierung einer konsolidierungs- und Planungs-software für alle standorte sind praktisch abgeschlossen. Wir haben somit, bezogen auf die reporting-Quali-tät, das erreicht, was ich gerne „Capital Market

standard“ nenne. für eine mittelständische Unterneh-mensgruppe ist das unge-wöhnlich. Wir können heute bereits auf Werks-, Länder- oder gruppenebene monat-liche gewinn- und Verlust-rechnungen, bilanzen und Cash flows zeigen. regional gibt es noch Verbesserungs-bedarf, insbesondere in Accounting-Prozessen. Zu-sätzliche schwerpunkte wer-

den heuer auf it-security und risk Management liegen.

Welche neuen entwicklungen oder Anwendungen wurden 2014 produktseitig umgesetzt?

PESouT: Vor allem Verbesserungen im Leichtbau sind ein ständiges thema und oft mit längerer Vorlaufzeit zu behandeln, weil die erkenntnis-se aus großserienversuchen umgesetzt werden müssen. Die neue europäische gesetzgebung zwingt die Automobilhersteller derzeit zu mas-siven gewichtseinsparungen. MegAteCh ist heute in der Lage, im kunststoffspritzverfahren Produkte mit hohen dekorativen Anforderungen im sichtbereich anzubieten, wobei gewichtsein-sparungen bis zu 30 Prozent möglich sind. Mit diesem Prozess ermöglichen wir ein bedeuten-des Potential für die Produktion. Und auch für die kommenden Jahre arbeiten wir aktiv an wei-teren neuentwicklungen.

hat es im vergangenen Jahr Veränderungen bei den Unternehmensanteilen gegeben?

GESSlEr: ich habe 2014 zwei meiner drei ehema-ligen Partner ausgekauft und deren Anteile er-

Wir haben somit,bezogen auf die

reporting-Qualität, das erreicht, was ich

gerne „Capital Market Standard“ nenne.

Geschäftsbericht 2014 | Seite 21

worben. ich gehe davon aus, dass ich die übrigen Anteile im laufenden Jahr erwerben kann – ein wichtiger Punkt für die langfristige Planung und stabilität im Unternehmen.

Wirken sich schwankungen im neuwagen-geschäft in europa auf die Auftragslage aus?

DiECk: Unser geschäft ist nicht an öffentlich wahrgenommenen Wirtschaftszyklen im Auto-mobilbereich festzumachen. Wenn der Auto-markt sich weltweit um einige Prozentsätze auf oder ab verändert, wirken sich diese schwankun-gen nicht automatisch in gleichem Umfang auf unser geschäft aus. es hängt alles davon ab, für welche Modelle wir von welchen Werken aus be-liefern. hierbei gibt es sozusagen für jedes Werk einen eigenen konjunkturzyklus, der nicht zwin-gend den globalen entwicklungen folgt.

GESSlEr: trotz der Wirtschaftskrise der letzten drei Jahre in spanien und Portugal ist es uns dort vom Volumen her dank unserer Zulieferaufträ-

ge für den Volkswagen golf, den Polo, den seat Leon sehr gut ergangen. Die PsA-gruppe hatte zuletzt nicht immer nur er-freuliche schlagzeilen. für uns verläuft die Zusammen-arbeit durch die fertigung von teilen für den Citroën Picasso aber durchaus posi-tiv. Auch Modelle wie Citro-ën C-elysée, Peugeot 301 und Citroën Cactus sorgen für durchwegs erfreuliche Volumina.

Demnach wurden die erwartungen hinsicht-lich des Anlaufens von neuen Aufträgen erfüllt?

GESSlEr: Die im Vorjahr in Verhandlung stehen-den Aufträge wurden akquiriert, wir stehen jetzt in der Produktentwicklung. Die Produktions-starts erfolgen zwischen 2015 bis Anfang 2017.

Trotz der Wirtschaftskrise in Spanien und Portugalist es uns dort dank unserer Zulieferaufträgefür den Volkswagen Golf VII, den Polo V oder den Seat leon sehr gut ergangen.

Geschäftsbericht 2014 | Seite 22

ein vorsichtiger Ausblick auf neugeschäfte, für die 2015 ein Abschluss zu erwarten ist?

GESSlEr: im deutschen Premiumsegment wol-len wir uns stärker aufstellen und arbeiten auch in diese richtung. Wir sprechen hier derzeit al-lerdings von strategischer Planung, da es Pro-duktionen betrifft, die ab 2018/2019 anlaufen können. Die Zusammenarbeit mit bMW/Mini ist zukunftsträchtig, die beziehungen zum Volkswa-gen konzern und Peugeot sind weiter ausbau-fähig, ebenso wie jene zu unseren strategisch wichtigen systemlieferanten.

DiECk: Zudem geht der trend dahin, dass unse-reKundenhäufigergrößereAuftragspakete fürfahrzeuggruppen auf derselben Plattform oder für mehrere verschiedene fahrzeuge vergeben. Das bedeutet höhere Volumina, aber auch eine größere herausforderung bei der kapazitätspla-nung und finanzierung.

PESouT: An dieser stelle ist zu erwähnen, dass wir mit schneider electric auch einen nicht-Automo-tive kunden haben, für den wir u.a. elektrische spulen fertigen – eine jahrelange und stabile geschäftsbeziehung, die ebenfalls Ausbaumög-

lichkeiten bietet. Der Vorteil ist, dass diese Pro-dukte im Vergleich zu Automotive-Produkten sehr langlebige Produktionszeiten haben, da an einem schaltschrank nur selten Änderungen vor-genommen werden.

ist das Zuliefern an einen der big Player mit hohem Marktanteil für die neukunden- akquise hinderlich oder eine empfehlung?

GESSlEr: Das ist eine empfehlung, weil die außer-ordentlichen Qualitätsansprüche eines großkun-den in der branche gut bekannt sind. Wer diese dauerhaft und in großen stückzahlen erfüllen kann, außerdem ein Produktportfolio vom nutz-fahrzeugbiszurLuxusklasseaufweist,empfiehltsich damit automatisch auch für jeden kunden. Da wir es schaffen, seit dem golf iV durchge-hend die Qualitäts- und Logistik-herausforde-rungen für mehr als 600.000 fahrzeuge pro Jahr zu schaffen, trauen uns auch andere kunden sehr viel zu.

PESouT: bevorzugter Zulieferer für einen groß-konzern zu sein, ist sicherlich eine referenz, das macht sich gut im CV eines Zulieferers. Auch das ist wieder ein Attraktivitäts-Plus.

Geschäftsbericht 2014 | Seite 23

Wie ist nunmehr die finanzierung bei der MegAteCh-holding und den tochtergesell-schaften geregelt?

GESSlEr: großvolumige finanzierungen im be-reich der holding anzusiedeln und damit aus den lokalen gesellschaften rauszuholen, ist ein Projekt, das wir im vergangen Jahr gestartet ha-ben.

DiECk: Diesen Weg wollen wir auch weiter ver-folgen. Voraussetzung dafür ist jedoch ein ka-pitalmarktfähiges rating auf konzernebene. Da sind wir auf einem guten Weg. Wir lassen uns aber auch alle anderen optionen offen – unter bestimmten Voraussetzungen kann es auch vor-teilhafter sein, finanzierungen lokal aufzustellen. insgesamt streben wir die höchstmögliche fle-xibilität bei geringstmöglichen finanzierungs-kosten an, und zwar sowohl bezogen auf die fi-nanzierungsstruktur insgesamt als auch in jedem einzelnen finanzierungsvertrag. große finanzie-rungsvolumina werden aber wohl künftig eher auf holding-ebene zu platzieren sein.

eine Vision für MegAteCh bis 2025 ...

GESSlEr: Wir haben eine reihe von praktischen Aufgaben. Die konsolidierung der niederlas-sung in brasilien wird nur hand in hand mit einer erholung der gesamten brasilianischen Volkswirtschaft gelingen. immerhin handelt es sich um einen heimmarkt von mehr als 200 Millionen Menschen und einem entsprechenden bedarf an fahrzeugen, das Potenzial ist also da. Weiters das Aufschließen der spa-nischen und tschechischen betriebe zu unseren excel-lence-standards. Und unser Team mit hochqualifiziertenMitarbeitern, die von renom-mierten firmen kommen, zu verstärken. Die geschäftsan-bahnung mit weiteren glo-balen herstellern sehen wir ebenfalls als spannende herausforderung. bei der erweiterung der geschäftsfelder soll trotz-dem die balance zwischen Auftragskonzentrie-rung und einem zu großen split gehalten werden – mit diesen Aufgaben sind wir für die Zukunft bis 2025 gut beschäftigt und zugleich gerüstet.

Da wir es schaffen, seit dem Golf iV durchge-hend die Qualitäts- undlogistik-Herausforderun-gen für mehr als 600.000Fahrzeuge pro jahr zuschaffen, trauen unsauch andere kunden sehr viel zu.

in unserem Werk MegAteCh industries hlinkso produzieren wir für das Audi A3 Cabrio die rückwandseitenverkleidung, die sich aus zwei teilen zusammensetzt.

Geschäftsbericht 2014 | Seite 24

Geschäftsbericht 2014 | Seite 25

Geschäftsbericht 2014 | Seite 26

Innenausstattung

A-Säulenverkleidung rechte Seite | SEAT | Leon III 5T | SE 370

A-Säulenverkleidung linke Seite | SKODA | Rapid | SK 251

C-Säulenverkleidung linke Seite | SKODA | Rapid | SK 251

B-Säulenverkleidung linke Seite | SEAT | Leon III 5T | SE 370

A-Säulenverkleidung rechte Seite | VW | Golf VII + Golf Variant | VW 370 + VW 372

A-Säulenverkleidung linke Seite | VW |

Golf VII + Golf Variant | VW 370 + VW 372

C-Säulenverkleidung „Sonnenrollo“ weiß rechte Seite | VW | CC | VW 469

B-Säulenverkleidung weiß rechte Seite | VW | CC | VW 469

C-Säulenverkleidung „Sonnenrollo“ weiß linke Seite | VW | CC | VW 469

B-Säulenverkleidung rechte Seite | VW | Polo V | VW 250 |

B-Säulenverkleidung schwarz rechte Seite | VW | CC | VW 469

C-Säulenverkleidung schwarz linke Seite | VW | CC | VW 469

C-Säulenverkleidung rechte Seite | VW | Polo V | VW 250

A-Säulenverkleidung weiß rechte Seite | VW | CC | VW 469

A-Säulenverkleidung weiß linke Seite | VW | CC | VW 469

Radzierkappen | SKODA | Octavia 3 | SK 371

Einstiegsleiste | VW | Golf VII + Golf Variant | VW 370 + VW 372

B-Säulenverkleidung rechte Seite | VW | Golf VII + Golf Variant | VW 370 + VW 372

VW | CC | VW 469

B-Säulenverkleidung rechte Seite |

linke Seite | VW | CC | VW 469

C-Säulenverkleidung rechte Seite |

C-Säulenverkleidung C-Säulenverkleidung

A-Säulenverkleidung linke Seite | VW | Polo V | VW 250

A-Säulenverkleidung

VW | Polo V | VW 250

Technische Teile

Sitzteile

Module und Konsolen

Radzierkappen |

Außenkomponenten

SKODA | Octavia 3 |

KofferraumkomponentenKofferraumkomponenten

Untere Sitzverkleidung | CITROËN | C4 Picasso | B78

Sitzschublade | CITROËN |

C4 Picasso | B78

2K Wasserkasten | CITROËN | Elysée | M3 | PEUGEOT | 301 | M4

3K Luftführung | CITROËN | C4 Picasso | B78

B-Säulenverkleidung linke Seite | SKODA | Rapid | SK 251

B-Säulenverkleidung weiß linke Seite | VW | CC | VW 469

C-Säulenverkleidung schwarz rechte Seite | VW | CC | VW 469

B-Säulenverkleidung linke Seite | VW | Polo V | VW 250

CD-Säulenverkleidung linke Seite | SKODA | Rapid Spaceback | SK 253

A-Säulenverkleidung schwarz rechte Seite | VW | CC | VW 469

A-Säulenverkleidung schwarz linke Seite |VW | CC | VW 469

B-Säulenverkleidung schwarz linke Seite | VW | CC | VW 469

A-Säulenverkleidung rechte Seite | VW | Polo V | VW 250

C-Säulenverkleidung linke Seite | VW | Polo V | VW 250

CD-Säulenverkleidung rechte Seite | SEAT | Leon III 5T | SE 370

Dachkonsole | CITROËN |Citroën Berlingo | B9

B Säulenverkleidung außen | SEAT | Leon III 5T | SE 370

Mittelkonsole | CITROËN | Citroën Berlingo | B9

Mittelkonsole | CITROËN | Citroën Berlingo | B9

3K Luftführung | CITROËN | C4 Picasso | B78

DIE PRODUKTE DERMEGATECHAuf einen Blick: Unsere wichtigsten Produkte – gegliedert nach Produktkategorien mit allen Informationen zu Fahr-zeugmarken, Modellen und Modellcodes.

Kofferraumseitenverkleidung | SEAT | Leon III ST | SE 373

e-Box | MERCEDES | Vito | NCV2

Radhausverkleidung | CITROËN | C4 Picasso | B78

2K Wasserkasten | SEAT | Leon III 5T/ST | SE 370 + SE 373

Heckklappenverkleidung oberer Rahmen | Heckklappenverkleidung unterer Rahmen | AUDI | Q3 | AU 316

Ladekante | AUDI | Q3 | AU 316

Radzierkappen | VW | Passat | VW 461

Radzierkappen | SKODA | Superb B5 |

SK 451

CITROËN | C4 Picasso | B78

Elektrische Spule | Schneider Electric

Außenkomponenten

2K Wasserkasten | 2K Wasserkasten | CITROËN | Elysée | M3 | PEUGEOT | 301 | M4

KofferraumkomponentenKofferraumkomponenten

Radhausverkleidung | CITROËN | C4 Picasso | B78C4 Picasso | B78

Geschäftsbericht 2014 | Seite 27

Innenausstattung

A-Säulenverkleidung rechte Seite | SEAT | Leon III 5T | SE 370

A-Säulenverkleidung linke Seite | SKODA | Rapid | SK 251

C-Säulenverkleidung linke Seite | SKODA | Rapid | SK 251

B-Säulenverkleidung linke Seite | SEAT | Leon III 5T | SE 370

A-Säulenverkleidung rechte Seite | VW | Golf VII + Golf Variant | VW 370 + VW 372

A-Säulenverkleidung linke Seite | VW |

Golf VII + Golf Variant | VW 370 + VW 372

C-Säulenverkleidung „Sonnenrollo“ weiß rechte Seite | VW | CC | VW 469

B-Säulenverkleidung weiß rechte Seite | VW | CC | VW 469

C-Säulenverkleidung „Sonnenrollo“ weiß linke Seite | VW | CC | VW 469

B-Säulenverkleidung rechte Seite | VW | Polo V | VW 250 |

B-Säulenverkleidung schwarz rechte Seite | VW | CC | VW 469

C-Säulenverkleidung schwarz linke Seite | VW | CC | VW 469

C-Säulenverkleidung rechte Seite | VW | Polo V | VW 250

A-Säulenverkleidung weiß rechte Seite | VW | CC | VW 469

A-Säulenverkleidung weiß linke Seite | VW | CC | VW 469

Radzierkappen | SKODA | Octavia 3 | SK 371

Einstiegsleiste | VW | Golf VII + Golf Variant | VW 370 + VW 372

B-Säulenverkleidung rechte Seite | VW | Golf VII + Golf Variant | VW 370 + VW 372

VW | CC | VW 469

B-Säulenverkleidung rechte Seite |

linke Seite | VW | CC | VW 469

C-Säulenverkleidung rechte Seite |

C-Säulenverkleidung C-Säulenverkleidung

A-Säulenverkleidung linke Seite | VW | Polo V | VW 250

A-Säulenverkleidung

VW | Polo V | VW 250

Technische Teile

Sitzteile

Module und Konsolen

Radzierkappen |

Außenkomponenten

SKODA | Octavia 3 |

KofferraumkomponentenKofferraumkomponenten

Untere Sitzverkleidung | CITROËN | C4 Picasso | B78

Sitzschublade | CITROËN |

C4 Picasso | B78

2K Wasserkasten | CITROËN | Elysée | M3 | PEUGEOT | 301 | M4

3K Luftführung | CITROËN | C4 Picasso | B78

B-Säulenverkleidung linke Seite | SKODA | Rapid | SK 251

B-Säulenverkleidung weiß linke Seite | VW | CC | VW 469

C-Säulenverkleidung schwarz rechte Seite | VW | CC | VW 469

B-Säulenverkleidung linke Seite | VW | Polo V | VW 250

CD-Säulenverkleidung linke Seite | SKODA | Rapid Spaceback | SK 253

A-Säulenverkleidung schwarz rechte Seite | VW | CC | VW 469

A-Säulenverkleidung schwarz linke Seite |VW | CC | VW 469

B-Säulenverkleidung schwarz linke Seite | VW | CC | VW 469

A-Säulenverkleidung rechte Seite | VW | Polo V | VW 250

C-Säulenverkleidung linke Seite | VW | Polo V | VW 250

CD-Säulenverkleidung rechte Seite | SEAT | Leon III 5T | SE 370

Dachkonsole | CITROËN |Citroën Berlingo | B9

B Säulenverkleidung außen | SEAT | Leon III 5T | SE 370

Mittelkonsole | CITROËN | Citroën Berlingo | B9

Mittelkonsole | CITROËN | Citroën Berlingo | B9

3K Luftführung | CITROËN | C4 Picasso | B78

DIE PRODUKTE DERMEGATECHAuf einen Blick: Unsere wichtigsten Produkte – gegliedert nach Produktkategorien mit allen Informationen zu Fahr-zeugmarken, Modellen und Modellcodes.

Kofferraumseitenverkleidung | SEAT | Leon III ST | SE 373

e-Box | MERCEDES | Vito | NCV2

Radhausverkleidung | CITROËN | C4 Picasso | B78

2K Wasserkasten | SEAT | Leon III 5T/ST | SE 370 + SE 373

Heckklappenverkleidung oberer Rahmen | Heckklappenverkleidung unterer Rahmen | AUDI | Q3 | AU 316

Ladekante | AUDI | Q3 | AU 316

Radzierkappen | VW | Passat | VW 461

Radzierkappen | SKODA | Superb B5 |

SK 451

CITROËN | C4 Picasso | B78

Elektrische Spule | Schneider Electric

Außenkomponenten

2K Wasserkasten | 2K Wasserkasten | CITROËN | Elysée | M3 | PEUGEOT | 301 | M4

KofferraumkomponentenKofferraumkomponenten

Radhausverkleidung | CITROËN | C4 Picasso | B78C4 Picasso | B78

Geschäftsbericht 2014 | Seite 28

4. MEGATECH Industries Amurrio, S.L.

Spanien

Das Werk im baskenland be-schäftigt rund 240 Mitarbei-ter. Es verfügt über ein sehr breites Produktspektrum und stellt diverse Teile für zahlrei-che namhafte kunden in der Automobilbranche her.

2. MEGATECH Industries Hlinsko s.r.o.

Tschechien

In der tschechischen Stadt Hlinsko sind rund 440 Mit-arbeiter im stark expandie-renden, neu ausgebauten Werk der MEGATECH Gruppe beschäftigt. neben sichtba-ren Fahrzeuginnenteilen als auch technischen Teilen für klima- und lüftungsanlagen werden Scheinwerferreflek-toren und elektrotechnische komponenten hergestellt.

5. MEGATECH Industries Orense, S.L.

Spanien

in der galizischen Stadt arbei-ten rund 130 Mitarbeiter im modernsten Werk der Grup-pe, das als Vorbild für alle Werke der MEGATECH Grup-pe gilt. Hier werden die meis-ten neuen Prozesse erprobt. Das Werk spezialisiert sich auf die Erzeugung anspruchsvol-ler, sichtbarer Innenteile und technischer Teile.

3. MEGATECH Industries Jablonec s.r.o.

Tschechien

in der Glas- und Schmuck-produktionsstadt im norden Tschechiens sind rund 270 Mitarbeiter angestellt. Das Werk wurde 2010–2012 auf den neusten industriellen Standard gebracht und pro-duziert seither ausschließlich für OEMs sichtbare Fahr-zeuginnenteile und radzier-blenden. Die Geschichte des Werks reicht bis ins 19. jahr-hundert zurück.

6. MEGATECH Brasil Componentes Automotivos Ltda., Brasilien

Seit 1979 ist MEGATECH in brasilien präsent. Das Werk in Curitiba beschäftigt rund 120 Mitarbeiter und verfügt über eine breite Produktpalette. in einem zusätzlichen Vertriebs-büro in Sao Paulo betreuen Mitarbeiter die kunden direkt vor ort.

1. MEGATECH Industries AG

Österreich

im vierten Wiener Gemein-debezirk laufen die Fäden der MEGATECH-Welt zusammen. neben dem CEo und CFo arbeiten neun weitere Mit-arbeiter in der Firmenzent-rale, die für die strategische Planung, den Vertrieb und das konzerncontrolling ver-antwortlich sind.

6

2

7

5 84

3 2

111

10

DiE WElT VonMEGATECHDie weltweiten Standorte der MEGATECH Group im überblick: alle Werke, alle Tech Center, alle Verkaufsbüros in Europa und übersee.

10. MEGATECH Industries Deutschland

GmbH Deutschland

Die acht Mitarbeiter in Deutschland sind für die Projektabwicklung und den Vertrieb für alle deutschen kunden zuständig. ihr Aufga-benbereich umfasst ebenso die technische Betreuung der Werke der kunden MEGA-TECHs. Technisches Verständ-nis und kundennähe sind selbstverständlich.

12. MEGATECH Industries India Private

Ltd., Indien

um auch auf dem boomen-den asiatischen Märkten prä-sent zu sein, hat MEGATECH seit 2012 eine repräsentanz in der indischen Metropole Pune, dem Zentrum der in-dischen Automobilindustrie, eingerichtet.

7. MEGATECH Industries Marinha Grande, Lda. Portugal

In Marinha Grande, einer der wichtigsten Werkzeugform-bauregionen Europas, befin-det sich die jüngste Fabrik der MEGATECH Gruppe. Das stark expandierende Werk mit rund 50 Mitarbeitern musste nach der Akquisition 2011 zuerst auf den automotiven Stan-dard gebracht werden und konzentriert sich nun aus-schließlich auf das Automobil-geschäft.

8. MEGATECH Industries Technical Center, A.I.E., Spanien

Das Tech Center der MEGA-TECH Gruppe befindet sich in der nähe von bilbao. Die rund 70 Mitarbeiter entwickeln Produkte und Werkzeuge im kundenauftrag. Darüber hin-aus beschäftigen sie sich mit Grundlagenforschung und neuen Materialien.

9. SC MEGATECH Engineering Center S.R.L

Rumänien

Die CAD-Entwicklung der Produkte für die gesamte MEGATECH Gruppe erfolgt in der rumänischen Haupt-stadt bukarest. Die zehn Mitarbeiter arbeiten wei-ters mit allen im Entwick-lungsprozess notwendigen Simulationsprogrammen.

12

9

Geschäftsbericht 2014 | Seite 29

11. MEGATECH Sales Office

Frankreich

Drei Mitarbeiter kümmern sich um die Projektabwick-lung und den Vertrieb für die französischen kunden der MEGATECH Gruppe.

DiE SElFiE-WElT VonMEGATECHMehr als 1.350 Mitarbeiter in den niederlassungen in Österreich, Deutschland, Spanien, Portugal, Rumänien, Tschechien und Brasilien bilden das Rückgrat unseres unternehmens. Hier ein paar Fotogrüße von unseren Standorten.

Geschäftsbericht 2014 | Seite 30

1

3

4

5

2

Geschäftsbericht 2014 | Seite 31

1, 2, 3, 7, 8, 10: Mitarbeiter der MEGATECH Industries Orense (Spanien)

4, 5: Mitarbeiter der MEGATECH Industries Amurrio (Spanien)

6: Mitarbeiter der MEGATECH Industries Hlinsko (Tschechien)

9, 11: Mitarbeiter der MEGATECH Industries Marinha Grande (Portugal)

6

7

8

11

10

9

Geschäftsbericht 2014 | Seite 32

in dreitätigen Workshops und Diskussionsrunden werden erfahrungen und neue ideen ausgetauscht, aktuelle themen behandelt sowie implementie-rungspläne für weitere strategische Projekte ent-wickelt.DieJointManagementMeetingsfindeninder nähe eines unserer Produktionsstandorte oder büros statt, um es allen teilnehmern zu ermögli-chen, die Projektumsetzungen in den Werken re-gelmäßig vor ort mitverfolgen zu können.

Das erste Joint Management Meeting 2014 fand im Mai in Marinha grande in Portugal statt und stand unter dem Motto „Lean Development“, wo-bei die verstärkten synergien zwischen dem tech Center und den Werken diskutiert wurden. Wäh-rend einer Werksführung in MegAteCh industries Marinha grande wurden die umfangreichen Mo-dernisierungsarbeiten in der Produktion präsen-tiert. im rahmen des treffens wurde dem Werk hlinsko die Auszeichnung „best factory 2013“ so-wie dem Werk in brasiien der Preis „best improve-ment 2013“ verliehen.

im november 2014 lud das technische büro in ru-mänien nach bukarest zum zweiten Joint Manage-ment Meeting des Jahres. bei diesem treffen lag der schwerpunkt auf dem thema kostenoptimie-rung. im Zuge dessen wurde bei einem eigenen Workshop zum thema „smart optimization“ die optimale nutzung der Mitarbeiter-ressourcen er-örtert. Die teilnehmer des JMM erarbeiteten in fünf gruppen optimierungspläne in unterschied-lichen bereichen – wie einkauf und Vertragsma-nagement, der optimalen Verwendung von geld-mitteln oder risikomanagement.

joinT MAnAGEMEnT

MEETinGEin Fixpunkt der MEGATECH-Gruppe sind die zweimal jährlich

stattfindenden joint Management Meetings (jMM), bei denen der Vorstand, die landesmanager sowie

Werks- und Abteilungsleiter aller Standorte zusammentreffen.

Geschäftsbericht 2014 | Seite 33

Werksbesuch des joint Management Meeting Teams in MEGATECH Industries Marinha Grande (Portugal)

Das joint Management Meeting Team zu Gast beim SC MEGATECH Engineering Center in Bukarest

Workshop zum Thema “Smart optimization” während des Joint Management Meetings in Rumänien

Geschäftsbericht 2014 | Seite 34

Im Mittelpunkt unserer Produktionsstätten

stehen immer unsere Mitarbeiter und ihre besonderen Fähigkeiten.

Geschäftsbericht 2014 | Seite 35

Geschäftsbericht 2014 | Seite 36

MEGAHonEynatural best quality

product fromour plant in hlinsko

CORPORATESoCiAl rESPonSibiliTy:

MEGAHonEy

Im Herbst 2011 wurden auf dem Gelände

des Werks Hlinsko fünf bienenvölker angesiedelt,

die von einem erfahrenen Imker betreut werden.

Der gewonnene Honig – unser Megahoney –

ist ein beliebtes Geschenk für kunden und besucher.

Das Jahr 2014 war somit für das Werk nicht nur in der Produktion

der kunststoffteile äußerst erfolgreich, sondern auch in der Honigernte

mit 350 Gläsern feinstem blüten- und Waldhonig.

Geschäftsbericht 2014 | Seite 37

Der Vorstand der Megatech industries Ag hat die Mitglieder des Aufsichtsrats regelmäßig, zeitnah und umfassend sowohl schriftlich als auch münd-lich über die Lage, den geschäftsverlauf und die finanzsituation des Unternehmens sowie der toch-tergesellschaften im konzern informiert.

im geschäftsjahr 2014 wurden sechs Aufsichtsrats-sitzungen abgehalten, an denen in drei sitzungen alle Mitglieder des Aufsichtsrats teilgenommen hatten. Am 29.04.2014 konnte fernando del Val nicht an der Aufsichtsratssitzung teilnehmen. Am 25.07.2014 sowie am 29.08.2014 konnte Matthias Übel nicht an den Aufsichtsratssitzungen teilneh-men und wurde jeweils durch Vollmacht von Ulrike Gessler-Wolfingervertreten.

in diesen Aufsichtsratssitzungen, aber auch darü-ber hinaus, wird eine offene kommunikation zwi-schen dem Vorstand und dem Aufsichtsrat geführt.

Der Aufsichtsrat war damit stets in der Lage, die geschäftsgebarung des Unternehmens fundiert zu überprüfen und den Vorstand bei grundsätzlichen entscheidungen zu unterstützen.

Der Aufsichtsrat hat die ihm nach gesetz, satzung und geschäftsordnung obliegenden Aufgaben unter beachtung der einschlägigen bestimmungen wahrgenommen. sofern erforderlich, hat der Auf-sichtsrat beschlüsse im schriftlichen Verfahren ge-fasst.

PwC Wirtschaftsprüfungs gmbh hat eine Prüfung des unternehmensrechtlichen Jahresabschlusses zum 31. Dezember 2014 nach den geltenden ge-setzlichen bestimmungen der §§ 268 ff. Ugb sowie eine freiwillige Prüfung des ifrs konzernabschlus-ses zum 31. Dezember 2014 nach den international standards on Auditing (isA) vorgenommen.

Die Prüfung hat nach ihrem abschließenden ergeb-nis keinen Anlass zu beanstandungen ergeben.

Der Abschlussprüfer hat daher bestätigt, dass der Jahresabschluss der Megatech lndustries Ag samt Lagebericht des Vorstandes sowie der konzernab-schluss samt konzernlageberichts des Vorstands des Megatech lndustries konzerns nach ifrs den gesetzlichen bestimmungen entsprechen.

sie vermitteln unter der beachtung ordnungsge-mäßer buchführung ein möglichst getreues bild der Vermögens-, finanz- und ertragslage der ge-sellschaft und ihrer tochtergesellschaften.

Der Aufsichtsrat erklärt sich mit dem Lagebericht des Vorstandes einverstanden und billigt den Jah-resabschluss 2014 der Megatech industries Ag. Der Jahresabschluss 2014 ist somit festgestellt.

Der Aufsichtsrat schließt sich der empfehlung des Vorstands an, das ergebnis des geschäftsjahres 2014 auf neue rechnung vorzutragen.

Weiters schlägt der Aufsichtsrat vor, PwC Öster-reich gmbh Wirtschaftsprüfungsie für einegesell-schaft in der ordentlichen hauptversammlung für das geschäftsjahr 2015 als Abschlussprüfer der Megatech industries Ag zu bestellen.

Die Mitglieder des Aufsichtsrats sprechen dem Vorstand sowie allen Mitarbeiterinnen und Mit-arbeitern im konzern Anerkennung und Dank für die hohen Leistungen und ihr großes engagement im geschäftsjahr 2015 aus.

Wien, am 20.04.2015

Dr. georg flandorfer

Bericht des Aufsichtsrats derMEGATECH Industries AGfür das Geschäftsjahr 2014

Geschäftsbericht 2014 | Seite 38

Working for

the best

Working for

the best

Consolidated Financial Statements as of 31/12/2014

Geschäftsbericht 2014 | Seite 40

I. Consolidated income statement

in kEUR Note 2014 2013

Revenue 5 124,451 131,516

Changes in inventories of finished goods and work in progress -457 -45

Capitalisation of development costs 17 3,215 2,723

Raw materials and consumables used 6 -83,198 -91,948

Employee benefit expenses 7 -26,004 -26,923

Other income 8 2,051 2,385

other expenses 22 -11,204 -9,835

EBITDA before non-recurring items 10,528 7,754

non-recurring items 10 -753 -949

EBITDA after non-recurring items 9,775 6,805

Depreciation and amortisation 11 -5,223 -5,896

Operating result (EBIT) 4,552 909

Interest income 12 328 304

Interest costs 12 -1,975 -2,002

other financial result 13 2,036 -928

Financial result 389 -2,626

Result before tax 4,941 -1,717

income tax expense 14 -507 177

Result after tax continued operations 4,434 -1,540

Discontinued operations 15 -2,413 -378

Result for the year 2,021 -1,918

in kEUR 2014 2013

Result attributable to:

Owner of the parent 2,021 -1,927

non-controlling interests 0 9

Result for the year 2,021 -1,918

Reportingoffiguresfor2013hasbeenamendedduetoreportingofdiscontinuedoperations(see note 15 for an explanation).

Geschäftsbericht 2014 | Seite 41

II. Consolidated statement of comprehensive income

in kEUR 2014 2013

Result for the year 2,021 -1,918

Other comprehensive income for the year:

Items that will not be reclassified to profit or loss

remeasurements of employment benefit obligations 4 4

4 9

Items that may be subsequently reclassified toprofit or loss

Currency translation differences -8 -120

-8 -120

Comprehensive income for the year continuedoperations -4 -111

Comprehensive income for the year discontinuedoperations 209 -196

Other comprehensive income for the year, net of tax 205 -307

Total comprehensive income for the year 2,226 -2,225

in kEUR 2014 2013

Total comprehensive income attributable to:

Owner of the parent 2,226 -2,234

non-controlling interests 0 9Total comprehensive income for the year 2,226 -2,225

items in the statement above are disclosed net of tax. the income tax relating to each component of other comprehensive income is disclosed in note 14.1.

Reportingoffiguresfor2013hasbeenamendedduetoreportingofdiscontinuedoperations(see note 15 for an explanation).

Geschäftsbericht 2014 | Seite 42

in kEUR Note 2014 2013

AssetsNon-current assets

Property, plant and equipment 16 41,276 43,550

Intangible assets 17 18,174 12,586

Deferred tax assets 14 707 775

Available-for-sale financial assets 60 60

Derivative financial instruments 19 0 1

non-current other receivables 22 11,955 12,860

72,172 69,832

Current assets

Inventories 20 10,757 11,368

Trade receivables 21 10,723 20,638

Other receivables 22 4,783 4,923

Cash and cash equivalents 23 1,881 6,335

28,144 43,264

Total assets 100,316 113,096

Total equity and liabilities 100.316 113.096

III. Consolidated balance sheet

Geschäftsbericht 2014 | Seite 43

in kEUR Note 2013 2012

Equity and liabilities

Equity

Registered capital 24 7,050 7,050

Other reserves 24 34,900 41,948

Currency translation differences 641 440

Retained earnings -2,751 -11,824

39,840 37,614

Non-current liabilities

non-current financial liabilities 25 13,683 4,449

Government grants 28 1,317 1,355

non-current employee benefits 29 392 434

non-current other provisions 30 744 1,246

other non-current liabilities 27 1,544 0

Deferred tax liabilities 14 2,960 4,036

20,640 11,520

Current liabilities

Current financial liabilities 25 12,343 28,577

Trade payables 26 20,888 26,390

Other payables 27 5,947 8,755

Government grants 28 22 24

Current provisions 30 636 216

39,836 63,962

Total liabilities 60,476 75,482

Total equity and liabilities 100,316 113,096

in previous year 2013, „trade and other receivables” and “trade and other payables” were shown in oneline.Forabetterunderstandingofthefigures2014,asplitwasdoneinbothareas.

Geschäftsbericht 2014 | Seite 44

IV. Consolidated statement of changes in equity

in kEUR

Regi

ster

ed

capi

tal

Oth

er

rese

rves

Curr

ency

tr

ansl

atio

n di

ffer

ence

s

Reta

ined

ea

rnin

gs

Non

- co

ntro

lling

in

tere

sts

Tota

l eq

uity

31 December 2012 7,050 41,761 756 -9,901 -39 39,627

Result for the year 0 0 0 -1,927 9 -1,918

Remeasurements of employment benefit obligations 0 0 0 9 0 9

Currency translation differences 0 0 -316 0 0 -316

Total comprehensive income 0 0 -316 -1,918 9 -2,225

Transactions with owners

Shareholders' contribution 0 187 0 0 75 262

Transactions with non-controlling interests 0 0 0 -5 -45 -50

Total transactions with owners 0 187 0 -5 30 212

31 December 2013 7,050 41,948 440 -11,824 0 37,614

Result for the year 0 0 0 2,021 0 2,021

remeasurements of employment benefit obligations 0 0 0 4 0 4

Currency translation differences 0 0 201 0 0 201

Total comprehensive income 0 0 201 2,025 0 2,226

Reclassifications 0 -7,048 0 7,048 0 0

31 December 2014 7,050 34,900 641 -2,751 0 39,840

Geschäftsbericht 2014 | Seite 45

V. Consolidated statement of cash flows

in kEUR 2014 2013

EBIT 4,552 909

Depreciation and amortisation 5,223 5,896

Change in inventory -3 4,286

Change in trade receivables 8,593 978

Change in trade payables -4,259 1,359

Change in other current assets/liabilities -1,047 -1,927

Change in working capital 3,284 4,696

Change in provisions -388 -123

Government grants -40 -54

Gain (-) / loss (+) from disposal of assets 38 -211

Interest received 22 45

Interest paid -283 -643

Taxes paid -1,139 -343

Cash flow from operating activities continued operations 11,269 10,172

Cash flow from operation activities discontinued operations -712 391

Total cash flow from operating activities 10,557 10,563

Investments in property, plant and equipment -2,435 -2,274

Investments in intangible assets -4,365 -2,972

Transactions with non-controlling interests 0 -50

Proceeds from disposal of fixed assets 93 3,275

Cash flow from investing activities continued operations -6,707 -2,021

Cash flow from investing activities discontinued operations -954 -121

Total cash flow from investing activities -7,661 -2,142

Free Cash flow 2,896 8,421

Geschäftsbericht 2014 | Seite 46

Reportingoffiguresfor2013hasbeenamendedduetoreportingofdiscontinuedoperations(seenote 15 for an explanation).

in kEUR 2014 2013

Repayment of bank loans -22,812 -1,113

Proceeds from new loans 25,992 1,008

Proceeds from other financing 21 0

Changes in bank overdrafts and recourse factoring -9,384 -2,469

Finance lease -307 -369

interest paid for long-term financing -1,386 -1,100

Transactions with non-controlling interest 0 75

Currency differences -83 200

Cash flow from financing activities continued operations -7,959 -3,768

Cashflowfromfinancingactivitiesdiscontinuedoperations 760 -345

Total cash flow from financing activities -7,199 -4,113

Total cash flow -4,303 4,308

Cash and cash equivalents at beginning of the year 6,335 2,257

Currency differences -28 -230

Total cash flow -4,303 4,308

Disposed cash and cash equivalents -123 0

Cash and cash equivalents at end of the year 1,881 6,335

Cash and free overdrafts 2,381 7,676

Geschäftsbericht 2014 | Seite 47

VI. Notes to the consolidated financial statements

1 general information

Megatech industries Ag (‘the company’) is located in taubstummengasse 13/9, 1040 Vienna, Austria, and is registered under the commercial registry number fn 337381z at the Vienna Commercial Court. the company is owned to the extent of 99.3% by Megatech industries s.L. located in Amurrio, spain. Ultimate parent is eib beteiligungsgesellschaft mbh, located in taubstummengasse 13/12, 1040 Vienna, Austria, registered at the Vienna Commercial Court under the commercial registry number fn 135029y. Ultimate controlling party is Mr. Maximilian gessler. eib beteiligungsgesellschaft mbh preparestheconsolidatedfinancialstatementsforthelargestandsmallestgroupofcompanies.ThisgroupreportisdisclosedattheViennaCommercialCourt.Infirstquarter2015theultimateparentchanged to Megatech industries Aktiengesellschaft, Vaduz, Liechtenstein.

Megatech industries Ag (‘the company’) and its subsidiaries (together, ‘the group’) develop, manufacture, assemble and supply interior and exterior plastic components for the global automotive industry. Production sites are located in spain, Portugal and the Czech republic, complemented by a sales company in germany. the group owns two tech Centers, one in spain and one in romania, for the design and development of products.

Geschäftsbericht 2014 | Seite 48

Consolidated companies are as follows:

*) Megatech brasil Componentes Automotive Ltda, brazil was sold as at 31 December 2014. the result is reported as result from discontinued operations (see note 15).

The consolidated financial statements as at 31December 2014were prepared by themanagingdirectors and released for issue on the date when this report was signed. The entity financialstatementsoftheparentcompany,whichhavebeenincludedintheconsolidatedfinancialstatementsafter transition to the applicable accounting standards, will be presented to the supervisory board for review and approval.

TheconsolidatedfinancialstatementswerepreparedinEUR.Unlessstatedotherwiseallamountsareshowninthousandsofeuro(kEUR).Allfigurespresentedarerounded,sominordiscrepanciesmayarise in the addition of these amounts.

Company Place of business

Country Share in capital

Acitivites

Megatech Industries AG Vienna Austria Holding

Megatech industries Amurrio. S.l. Amurrio Spain 100.0% Production

Megatech industries orense S.l. Orense Spain 100.0% Production

Megatech Perfect Plastics Marinha Grande ltda.

Marinha Grande Portugal 100.0% Production

Megatech industries Hlinsko s.r.o. Hlinsko Czech Republic 100.0% Production

Megatech industries jablonec s.r.o. Jablonec Czech Republic 100.0% Production

SC Megatech Engineering Center S.r.l. Bucharest Romania 100.0% Engineering

Megatech Industries Intellectual Property S.l.u Amurrio Spain 100.0% Engineering

Megatech industries Technical Center A.i.E. Amurrio Spain 100.0% Engineering

Megatech Brasil Componentes Automotivos ltda. *) Curritiba brazil 100.0% Production

Megatech Industries Deutschland GmbH Wolfsburg Germany 100.0% Sales

Megatech Automotive GmbH Vienna Austria 100.0% Dormant

Megatech industries india Pl Pune India 100.0% Dormant

Geschäftsbericht 2014 | Seite 49

2Summaryofsignificantaccountingpolicies

Theprincipalaccountingpoliciesappliedinthepreparationoftheseconsolidatedfinancialstatementsare set out below. these policies have been consistently applied to all the years presented, unless stated otherwise.

2.1 basis of preparation

The consolidated financial statements of the group have been prepared in accordance withinternational financial reporting standards and ifriC interpretations as adopted by the eU. the consolidated financial statements have been prepared under the historical cost convention, asmodifiedbytherevaluationofavailable-for-salefinancialassets,andfinancialassetsandfinancialliabilities(includingderivativeinstruments)atfairvaluethroughprofitorloss.

Thepreparationoffinancialstatements inconformitywith IFRSrequirestheuseofcertaincriticalaccounting estimates. it also requires management to exercise its judgement in the process of applying the group’s accounting policies. the areas involving a higher degree of judgement or complexity, or areaswhereassumptionsandestimatesaresignificanttotheconsolidatedfinancialstatementsaredisclosed in note 4.

2.2.1 Changes in accounting policy and disclosures

2.1.1.1 new standards, amendments and interpretations adopted by the group

IFRS10,‘Consolidatedfinancialstatements’,buildsonexistingprinciplesbyidentifyingtheconceptof control as the determining factor in whether an entity should be included in the consolidated financialstatementsoftheparentcompany.Thestandardprovidesadditionalguidancetoassistinthedeterminationofcontrolwherethisisdifficulttoassess.IFRS10doesnothaveamaterialimpactonthegroupsconsolidatedfinancialstatements.

ifrs 11, ‘Joint arrangements’, focuses on the rights and obligations of the parties to the arrangement rather than its legal form. there are two types of joint arrangements: joint operations and joint ventures. Joint operations arise where the investors have rights to the assets and obligations for the liabilities of an arrangement. A joint operator accounts for its share of the assets, liabilities, revenue and expenses. Joint ventures arise where the investors have rights to the net assets of the arrangement; joint ventures are accounted for under the equity method. Proportional consolidation of joint arrangements is no longer permitted. ifrs 11 does not have a material impact on the group’s consolidatedfinancialstatements.

ifrs 12, ‘Disclosures of interests in other entities’, includes the disclosure requirements for all forms of interests in other entities, including joint arrangements, associates, structured entities and other off-balancesheetvehicles.IFRS12doesnothaveamaterialimpactonthegroup’sconsolidatedfinancialstatements.

Geschäftsbericht 2014 | Seite 50

2.1.1.2 new standards and interpretations not yet adopted

A number of new standards and amendments to standards and interpretations are effective for annual periods beginning after 1 January 2015, and have not been applied in preparing these consolidated financial statements. None of these is expected to have a significant effect on the consolidatedfinancialstatementsofthegroup,exceptthefollowingsetoutbelow:

IFRS9,‘Financialinstruments’,addressestheclassification,measurementandrecognitionoffinancialassetsandfinancialliabilities.ThecompleteversionofIFRS9wasissuedinJuly2014.ItreplacestheguidanceinIAS39thatrelatestotheclassificationandmeasurementoffinancialinstruments.IFRS9retainsbutsimplifiesthemixedmeasurementmodelandestablishesthreeprimarymeasurementcategories forfinancialassets:amortisedcost, fairvaluethroughOCIandfairvaluethroughP&L.Thebasis of classificationdependson the entity’s businessmodel and the contractual cash flowcharacteristicsofthefinancialasset.Investmentsinequityinstrumentsarerequiredtobemeasuredatfairvaluethroughprofitorlosswiththeirrevocableoptionatinceptiontopresentchangesinfairvalue in oCi not recycling. there is now a new expected credit losses model that replaces the incurred lossimpairmentmodelusedinIAS39.Forfinancialliabilitiestherewerenochangestoclassificationand measurement except for the recognition of changes in own credit risk in other comprehensive income,forliabilitiesdesignatedatfairvaluethroughprofitorloss.IFRS9relaxestherequirementsfor hedge effectiveness by replacing the bright line hedge effectiveness tests. it requires an economic relationship between the hedged item and hedging instrument and for the ‘hedged ratio’ to be the same as the one management actually use for risk management purposes. Contemporaneous documentation is still required but is different to that currently prepared under iAs 39. the standard is effective for accounting periods beginning on or after 1 January 2018. early adoption is permitted. the group is yet to assess ifrs 9’s full impact.

ifrs 15, ‘revenue from contracts with customers’, deals with revenue recognition and establishes principlesforreportingusefulinformationtousersoffinancialstatementsaboutthenature,amount,timinganduncertaintyofrevenueandcashflowsarisingfromanentity’scontractswithcustomers.revenue is recognised when a customer obtains control of a good or service and thus has the ability todirect theuseandobtain thebenefits fromthegoodorservice.Thestandardreplaces IAS18‘revenue’ and iAs 11, ‘Construction contracts’, and related interpretations. the standard is effective for annual periods beginning on or after 1 January 2017, and earlier application is permitted. the group is assessing the impact of ifrs 15.

there are no other ifrss or ifriC interpretations that are not yet effective that would be expected to have a material impact on the group.

Geschäftsbericht 2014 | Seite 51

2.2 Consolidation

subsidiaries are all entities (including structured entities) over which the group has control. the group controls an entity when the group is exposed to, or has rights to, variable returns from its involvement with the entity. subsidiaries are fully consolidated from the date on which control is transferred to the group. they are deconsolidated from the date that control ceases. As of 31 December 2014 and 31 December 2013 the group has 100% of shares and voting rights of all subsidiaries included in the scope of consolidation.

the group uses the acquisition method to account for business combinations. the consideration transferred for the acquisition of a subsidiary is the fair value of the assets transferred, the liabilities incurred to the former owners of the acquiree and the equity interests issued by the group. the consideration transferred includes the fair value of any asset or liability resulting from a contingent considerationarrangement.Acquisition-relatedcostsareexpensedas incurred. Identifiableassetsacquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair value at the acquisition date. the group recognises any non-controlling interest in the acquiree on an acquisition-by-acquisition basis, either at fair value or at the non-controlling interest’sproportionateshareoftherecognisedamountsoftheacquiree’sidentifiablenetassets.

the excess of the consideration transferred, the amount of any non-controlling interest in the acquiree and the acquisition-date fair value of any previous equity interest in the acquiree over the fair value of thegroup’sshareoftheidentifiablenetassetsacquiredisrecordedasgoodwill.Ifthisislessthanthefair value of the net assets of the subsidiary acquired in the case of a bargain purchase, the difference is recognised in the income statement.

transactions with non-controlling interests that do not result in loss of control are accounted for as equity transactions – that is, as transactions with the owners in their capacity as owners. the difference between the fair value of any consideration paid and the relevant share acquired of the carrying value of net assets of the subsidiary is recorded in equity. gains or losses on disposals to non-controlling interests are also recorded in equity.

When the group ceases to have control any retained interest in the entity is remeasured to its fair valueatthedatewhencontrol is lost,withthechangeincarryingamountrecognisedinprofitorloss. the fair value is the initial carrying amount for the purposes of subsequently accounting for the retainedinterestasanassociate,jointventureorfinancialasset.Inaddition,anyamountspreviouslyrecognised in other comprehensive income in respect of that entity are accounted for as if the group had directly disposed of the related assets or liabilities. this may mean that amounts previously recognisedinothercomprehensiveincomearereclassifiedtoprofitorloss.

inter-company transactions, balances and unrealised gains on transactions between group companies are eliminated. Unrealised losses are also eliminated. Accounting policies of subsidiaries have been changed where necessary to ensure consistency with the policies adopted by the group.

Geschäftsbericht 2014 | Seite 52

Globale innovationen: Das Tech Center ist 2014

in das AiC-Automotive Intelligence Center bei Bilbao

übersiedelt.

Geschäftsbericht 2014 | Seite 53

Geschäftsbericht 2014 | Seite 54

2.3 foreign currency translation

2.3.1 Functional and presentation currency

Items included in thefinancial statementsofeachof thegroup’sentitiesaremeasuredusing thecurrency of the primary economic environment in which the entity operates (‘the functional currency’). Theconsolidatedfinancialstatementsarepresentedinthousandsofeuro(kEUR),whichisthegroup’spresentation currency.

2.3.2 Transactions and balances

foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions or valuation where items are remeasured. foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in theincomestatement,exceptwhendeferredinothercomprehensiveincomeasqualifyingcashflowhedges and qualifying net investment hedges.

foreign exchange gains and losses that relate to borrowings and cash and cash equivalents are presentedintheincomestatementunder‘otherfinancialresults’.Allotherforeignexchangegainsand losses are presented in the income statement under ‘other income’ / ‘other expenses’.

Changes in the fair value of monetary securities denominated in foreign currency classified asavailable-for-sale are determined on the basis of translation differences resulting from changes in the amortised cost of the security and other changes in the carrying amount of the security. translation differencesrelatingtochangesinamortisedcostarerecognisedinprofitorloss,andotherchangesin carrying amount are recognised in other comprehensive income.

Translationdifferences innon-monetaryfinancialassetsandliabilitiessuchasequitiesheldatfairvalue throughprofitor lossare recognised inprofitor lossaspartof the fair valuegainor loss.Translationdifferencesinnon-monetaryfinancialassetssuchasequitiesclassifiedasavailable-for-sale are included in other comprehensive income.

2.3.3 Group companies

Theresultsandfinancialpositionofallthegroupentities(noneofwhichhasthecurrencyofahyper-inflationaryeconomy)thathaveafunctionalcurrencydifferentfromthepresentationcurrencyaretranslated into the presentation currency as follows:

assets and liabilities for each balance sheet presented are translated at the closing rate at the date of that balance sheet;

income and expenses for each income statement are translated at average exchange rates (unless this average is not a reasonable approximation of the cumulative effect of the rates prevailing on the transaction dates, in which case income and expenses are translated at the rate on the dates of the transactions); and

all resulting exchange differences are recognised in other comprehensive income.

Geschäftsbericht 2014 | Seite 55

on consolidation, exchange differences arising from the translation of the net investment in foreign operations, and of borrowings and other currency instruments designated as hedges of such investments, are posted to other comprehensive income. When a foreign operation is partially disposed of or sold, exchange rate differences that were recorded in equity are recognised in the income statement as part of the gain or loss on sale.

goodwill and fair value adjustments arising from the acquisition of a foreign entity are treated as assets and liabilities of the foreign entity and translated at the closing rate.

2.4 Property, plant and equipment

Landandbuildingscomprisemainlyfactoriesandoffices.Property,plantandequipmentisstatedathistorical cost less depreciation. historical cost includes expenditure that is directly attributable to the acquisition of these items.

subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate,onlywhenitisprobablethatfutureeconomicbenefitsassociatedwiththeitemwillflowto the group and the cost of the item can be measured reliably. the carrying amount of a replaced part is derecognised. All other repairs and maintenance are charged to the income statement during thefinancialperiodinwhichtheyareincurred.

borrowing costs are only capitalised when they are directly attributable to the acquisition or production of a qualifying asset as part of the asset, all other borrowing costs are recognised as an expense in the period in which they occur.

Land is not depreciated. Depreciation on other assets is calculated using the straight-line method to allocate their cost to their residual value over their estimated useful lives, as follows:

buildings 25-33 yearsMachinery 5-15 yearsforklifts 5 yearsVehicles 3-5 yearsFurniture,fittingsandequipment 3-10years

the residual values and useful lives of assets are reviewed, and adjusted if appropriate, at the end of each reporting period. An asset’s carrying amount is written down immediately to its recoverable amount if the carrying amount is greater than the estimated recoverable amount. gains and losses on disposals are determined by comparing the proceeds with the carrying amount and are recognised under ‘other income’ or ‘other expenses’ in the income statement.

Geschäftsbericht 2014 | Seite 56

2.5 intangible assets

2.5.1 Trademarks

Acquired trademark rights are capitalised on the basis of the costs incurred to acquire and bring to use those rights. these costs are amortised over their estimated useful lives of ten years.

2.5.2 Research and development cost

no intangible asset is recognised in the research phase. the expenditure is recognised as an expense when it is incurred. An intangible asset arising from development is only recognised if the company can demonstrate all of the following: the technical feasibility of completing the intangible asset so that it will be available for use or

sale; its intention to complete the intangible asset and use or sell it; its ability to use or sell the intangible asset; howtheintangibleassetwillgenerateprobablefutureeconomicbenefits; theavailabilityofadequatetechnical,financialandotherresourcestocompletethedevelopment

and to use or sell the intangible asset; the ability to reliably measure the expenditure attributable to the intangible asset during its

development.

Directly attributable costs that are capitalised as part of the projects include employee costs, material costs, external costs and an appropriate portion of relevant overheads.

Development costs recognised are amortised on a straight-line basis over the project period related to the development costs, usually not exceeding six years.

2.5.3 Software licences

Acquired computer software licences are capitalised on the basis of the costs incurred to acquire and bring to use the specific software. these costs are amortised over their estimated useful lives of three to five years.

2.5.4 Contractual customer relationships

Contractual customer relationships acquired in a business combination are recognised at fair value attheacquisitiondate.Thecontractualcustomerrelationshaveafiniteusefullifeof15yearsandare carried at cost less accumulated amortisation. Amortisation is calculated using the straight-line method over the expected life of the customer relationship.

2.5.5 Patents

self-developed patents whose fair value can be measured reliably are capitalised based either on an expert valuation or on the expected turnover which will be generated with the patent. Amortisation is calculated using the straight-line method to allocate the cost of patents over their estimated useful life. the useful life is based on the project time period for which the patents were developed usually not exceeding six years.

Geschäftsbericht 2014 | Seite 57

2.6Impairmentofnon-financialassets

Assetsthathaveanindefiniteusefullife–forexample,goodwillorintangibleassetsnotreadyforuse – are not subject to amortisation and are tested annually for impairment. Assets that are subject to amortisation are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. the recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. for the purpose of assessing impairment,assetsaregroupedatthelowestlevelsforwhichthereareseparatelyidentifiablecashflows(cash-generatingunits).Non-financialassetsotherthangoodwillthatsufferedanimpairmentare reviewed for possible reversal of the impairment at each reporting date.

2.7 financial assets

2.7.1 Classification

Thegroupclassifiesitsfinancialassetsinthefollowingcategories:atfairvaluethroughprofitorloss,loansandreceivables,andavailableforsale.Theclassificationdependsonthepurposeforwhichthefinancialassetswereacquired.Managementdetermines theclassificationof itsfinancialassetsatinitial recognition.

Financialassetsatfairvaluethroughprofitorloss

Financialassetsatfairvaluethroughprofitor lossarefinancialassetsheldfortrading.Afinancialassetisclassifiedinthiscategoryifacquiredprincipallyforthepurposeofsellingintheshortterm.Derivatives are also categorised as held for trading unless they are designated as hedges. Assets in thiscategoryareclassifiedascurrentassetsifexpectedtobesettledwithin12months;otherwise,theyareclassifiedasnon-current.

Loans and receivables

Loansandreceivablesarenon-derivativefinancialassetswithfixedordeterminablepaymentsthatare not quoted in an active market. they are included in current assets, except for maturities greater than12monthsafter theendof the reportingperiod.Theseareclassifiedasnon-currentassets.the group’s loans and receivables comprise ‘trade receivables’, ‘other receivables’ and ‘cash and cash equivalents’ in the balance sheet.

Available-for-salefinancialassets

Available-for-salefinancialassetsarenon-derivativesthatareeitherdesignatedinthiscategoryornot classified in any of the other categories. They are included in non-current assets unless theinvestment matures or management intends to dispose of it within 12 months after the end of the reporting period.

Geschäftsbericht 2014 | Seite 58

2.7.2 Recognition and measurement

Regular purchases and sales of financial assets are recognised on the trade date – the date onwhich the group commits to purchase or sell the asset. investments are initially recognised at fair valueplus transactioncosts forallfinancialassetsnotcarriedat fair value throughprofitor loss.Financialassetsarederecognisedwhentherightstoreceivecashflowsfromtheinvestmentshaveexpired or have been transferred and the group has substantially transferred all risks and rewards of ownership.Available-for-salefinancialassetsandfinancialassetsatfairvaluethroughprofitorlossare subsequently carried at fair value. Loans and receivables are subsequently carried at amortised costusingtheeffectiveinterestmethod.Financialassetscarriedatfairvaluethroughprofitorlossareinitially recognised at fair value, any transaction costs are expensed in the income statement.

When securities classified as available-for-sale are sold or impaired, the accumulated fair valueadjustments recognised in equity are included in the income statement as ‘gains and losses from investment securities’. interest on available-for-sale securities calculated using the effective interest method is recognised in the income statement as part of other income. Dividends on available-for-saleequityinstrumentsarerecognisedintheincomestatementaspartoffinancialresultwhenthegroup’s right to receive payments is established. Changes in fair value are recognised as gains and losses in comprehensive income.

2.7.3 Offsetting financial instruments

financial assets and liabilities are offset and the net amount reported in the balance sheet when there is a legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis or realise the asset and settle the liability simultaneously. the legally enforceable right must not be contingent on future events and must be enforceable in the normal course of business and in the event of default, insolvency or bankruptcy of the company or the counterparty.

the group did not offset any amounts in 2014 and 2013 except one transaction with related parties (see note 35.1 for details).

2.8Impairmentoffinancialassets

2.8.1 Assets carried at amortised cost