Embed Size (px)

DESCRIPTION

Housing experts predict a disaster for buy-to-let landlords as Labour vows to interfere with the market by capping rent rises

Citation preview

06/05/2015 Housing experts predict disaster if Labour caps rent rises | Daily Mail Online

http://www.dailymail.co.uk/money/buytolet/article-3065446/Experts-predict-disaster-country-s-landlords-Labour-vows-interfere-market-capping-rental-rises.html?printingPage=true 1/8

SHARE SELECTION

Click here to print

Wednesday, May 6th 2015 4PM 10°C 7PM 10°C 5Day ForecastHome TopHome Top

Housing experts predict a disaster for buytolet landlords as Labourvows to interfere with the market by capping rent risesBy Jeff Prestridge, Financial Mail on Sunday

Published: 22:04, 2 May 2015 | Updated: 13:45, 3 May 2015

Britain's growing army of buytolet landlords will hold its breath this week – and pray that a Labour Government is not elected.

Many experts believe a Government led by Ed Miliband will wreak havoc on the attractive investment returns that many people now earn from owning abuytolet property – or a portfolio of properties.

Mismanagement of the economy by Miliband and likely Chancellor of the Exchequer Ed Balls, they say, could trigger interest rate rises and a sharphousing market correction, proving disastrous for buytolet investors.

Rewards: Former Bank of England economist Rob Thomas says buytolet returns are'superior' in his report

Also, Labour has confirmed it intends interfering in the private rental market to the detriment of landlords. It has pledged to cap rental increases thatlandlords can impose, introduce longer leases and remove tax reliefs for those who fail to look after their properties.

The changes, Miliband claims, will give millions of ‘forgotten’ renters – prevented from buying through soaring house prices – a fairer deal. But few agree,with some decrying his planned interference in the private landlord market as a ‘stunningly bad idea’ that could backfire spectacularly as buytoletlandlords give up the ghost and the supply of rented property shrinks.

RELATED ARTICLESPrevious1Next

SIMON LAMBERT: Rent controls linked to inflation would have... How landlords can save money next winter spring clean your... Cost of

renting rises across the UK and London tops the... Rents have outpaced inflation since last general election ...

Share this articleShare68 shares

06/05/2015 Housing experts predict disaster if Labour caps rent rises | Daily Mail Online

http://www.dailymail.co.uk/money/buytolet/article-3065446/Experts-predict-disaster-country-s-landlords-Labour-vows-interfere-market-capping-rental-rises.html?printingPage=true 2/8

HOW THIS IS MONEY CAN HELPTen tips for buytolet: the essential advice for property investors

Eric Pentecost, Professor of Economics at Loughborough University, says: ‘Buytolet investors face several potential downsides on the horizon. Theyinclude a future rise in interest rates, a fall in house prices and political interference in the rental sector. A Labour administration would more likely bringthese downsides much closer to home.’

Since the 2008 financial crisis, Britain has been transformed into a nation of amateur landlords. Fuelled by a cocktail of cheap mortgages, moribundsavings rates and a generation of youngsters priced out of the housing market, a buytolet frenzy has gripped the country.

People armed with wads of cash – some released from pensions under new rules introduced last month – and cheap interestonly loans have bought upinvestment property in droves. The Bank of England recently published data confirming that buytolet lending as a share of overall mortgage lending isnow higher than it was before the crisis.

An estimated one million people – amateur landlords, professionals, and so called megalandlords – now run buytolet portfolios. Investors comprisecelebrities, the retired and those simply looking to supplement their salary. It is not difficult to see why buytolet has become the ‘best’ (most sellable)investment story in town – bigger than the technology fuelled investment fund buying spree of the late 1990s – a spree that, rather ominously, endedcalamitously for millions when the tech bubble burst in the spring of 2000.

06/05/2015 Housing experts predict disaster if Labour caps rent rises | Daily Mail Online

http://www.dailymail.co.uk/money/buytolet/article-3065446/Experts-predict-disaster-country-s-landlords-Labour-vows-interfere-market-capping-rental-rises.html?printingPage=true 3/8

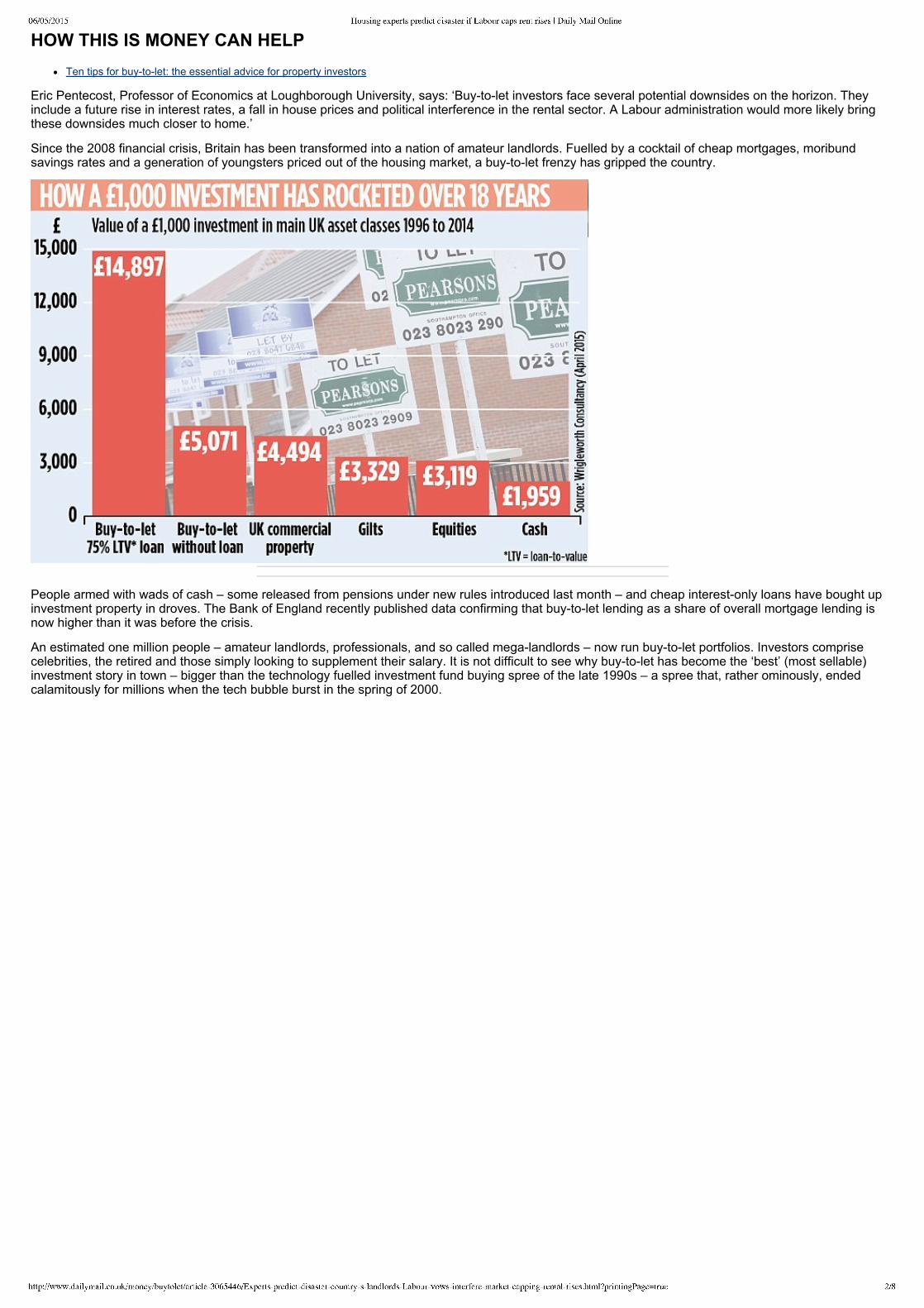

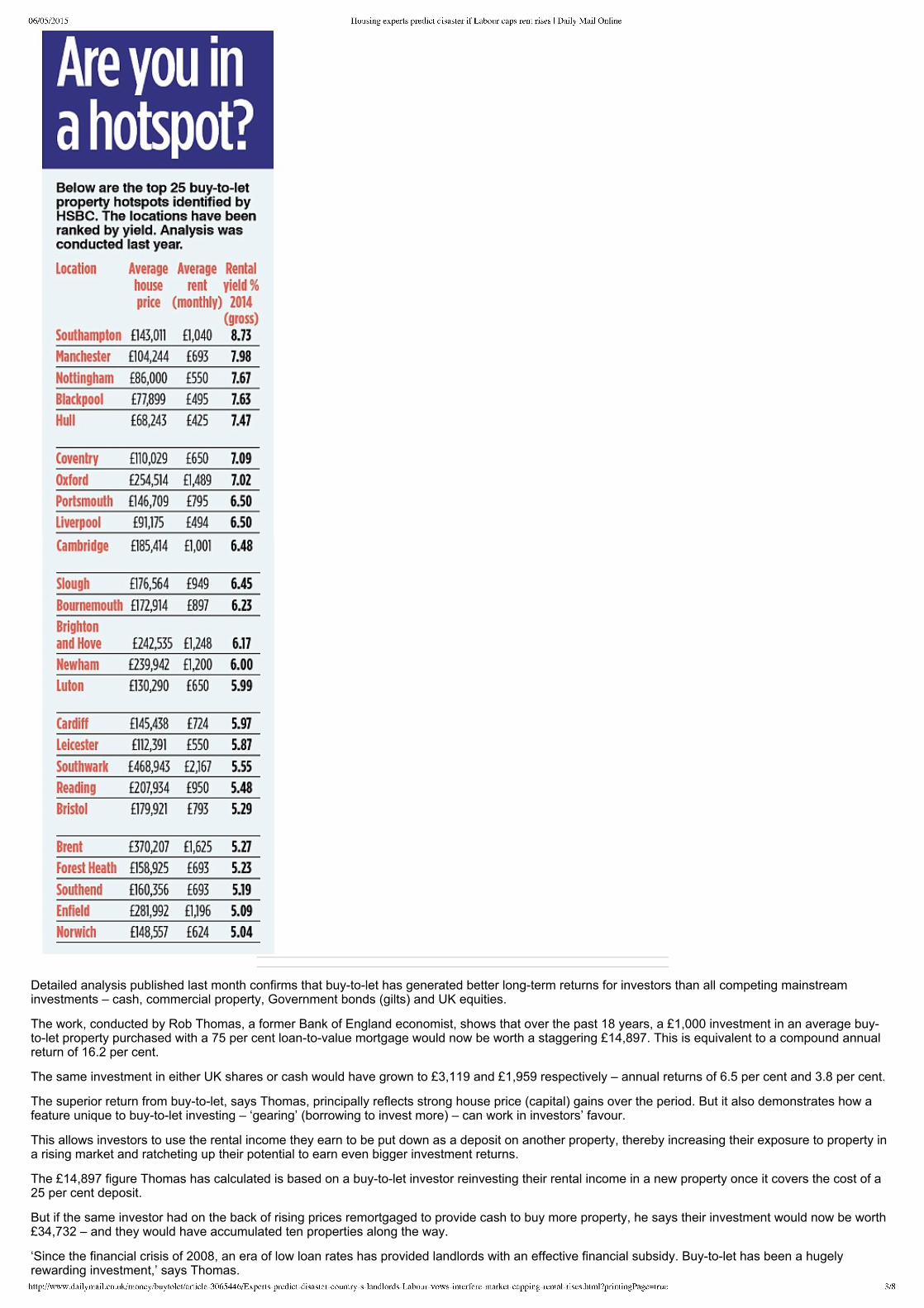

Detailed analysis published last month confirms that buytolet has generated better longterm returns for investors than all competing mainstreaminvestments – cash, commercial property, Government bonds (gilts) and UK equities.

The work, conducted by Rob Thomas, a former Bank of England economist, shows that over the past 18 years, a £1,000 investment in an average buytolet property purchased with a 75 per cent loantovalue mortgage would now be worth a staggering £14,897. This is equivalent to a compound annualreturn of 16.2 per cent.

The same investment in either UK shares or cash would have grown to £3,119 and £1,959 respectively – annual returns of 6.5 per cent and 3.8 per cent.

The superior return from buytolet, says Thomas, principally reflects strong house price (capital) gains over the period. But it also demonstrates how afeature unique to buytolet investing – ‘gearing’ (borrowing to invest more) – can work in investors’ favour.

This allows investors to use the rental income they earn to be put down as a deposit on another property, thereby increasing their exposure to property ina rising market and ratcheting up their potential to earn even bigger investment returns.

The £14,897 figure Thomas has calculated is based on a buytolet investor reinvesting their rental income in a new property once it covers the cost of a25 per cent deposit.

But if the same investor had on the back of rising prices remortgaged to provide cash to buy more property, he says their investment would now be worth£34,732 – and they would have accumulated ten properties along the way.

‘Since the financial crisis of 2008, an era of low loan rates has provided landlords with an effective financial subsidy. Buytolet has been a hugelyrewarding investment,’ says Thomas.

06/05/2015 Housing experts predict disaster if Labour caps rent rises | Daily Mail Online

http://www.dailymail.co.uk/money/buytolet/article-3065446/Experts-predict-disaster-country-s-landlords-Labour-vows-interfere-market-capping-rental-rises.html?printingPage=true 4/8

Other positives have driven forward the buytolet market. Demand for rented accommodation has remained firm. Analysis by upmarket estate agentKnight Frank indicates that four million households – 17 per cent of all households – now live in privately rented accommodation. By the end of next year,this will have grown to five million.

Strong demand means many landlords have been able to consistently push up rents, make a healthy income profit on their properties and nudge them inthe direction of further investment property purchases.

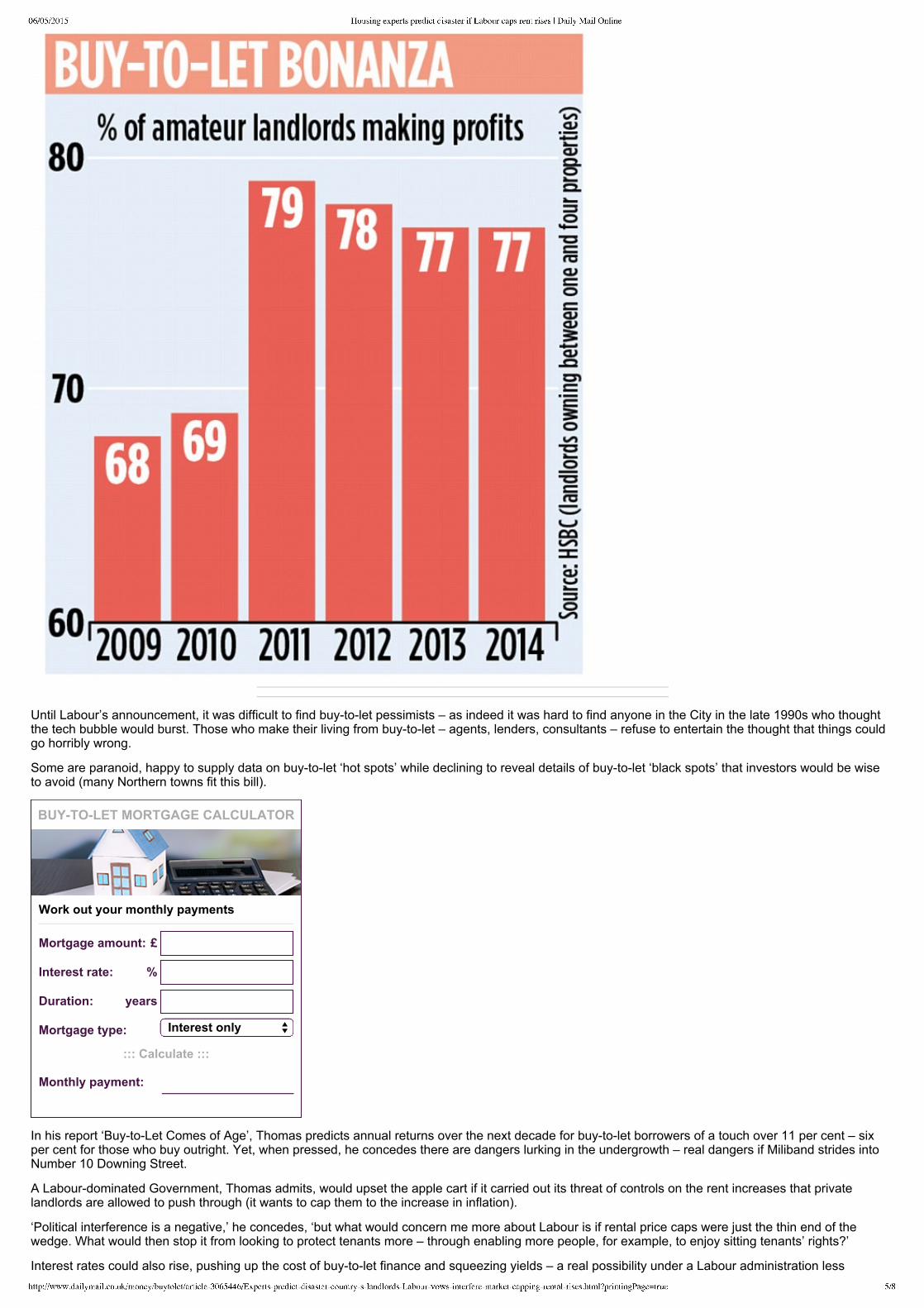

Latest research from bank HSBC (done prior to Labour’s announcement on rental controls) suggests that many amateur landlords – those with portfoliosof between one and four properties – remain in good spirits.

Its survey of more than 1,000 landlords indicates that average rental yields – rental income minus mortgage and maintenance costs expressed as apercentage of a portfolio’s value – remain robust at 5.7 per cent despite sustained house price inflation. With more than three in four landlords making anincome profit last year from their portfolios, it says 23 per cent of landlords are looking to buy more properties in the coming 12 months.

Tracie Pearce, head of mortgages at the bank, says: ‘Confidence among small portfolio landlords is at its highest level for five years. It’s attributable to anumber of positive trends – robust rental yields and continued strong demand across the UK for quality accommodation.’

The market is also awash with cheap buytolet finance, a function of low interest rates and the fact that banks and building societies are not required bythe City regulator to put borrowers through the same onerous affordability tests that now apply to homebuyers under so called Mortgage Market Reviewrules introduced a year ago.

THE MARKET KNOWN FOR ITS UPS AND DOWNS

Martin Skinner and his partner Magdalena Stepnowska

Although economist Rob Thomas says buytolet investors have enjoyed 18 years of outstanding investment returns, not everyone has been a winner.

Martin Skinner, from Chelsea in West London, has endured a rollercoaster buytolet ride which resulted in him going bankrupt after the 2008 financialcrisis.

In the early 2000s, he got so caught up in buytolet that he became a fulltime landlord with properties situated primarily in Docklands, East London,offering tenants a room and shared facilities.

He then set up a business called Nice Group to manage a portfolio of buytolet properties. Nice went into administration when his backers pulled the plugin early 2009 in the teeth of the financial crisis.

Despite this, Martin, 36, has not lost faith in buytolet. In fact, he has managed to buy back some of his original portfolio by striking a deal with the trusteeoverseeing his bankruptcy. He has also set up a company called Inspired Asset Management that converts old office buildings in London suburbs andturns them into affordable apartments for firsttime buyers.

Engaged to Magdalena Stepnowska, 37, who works in his business, he says: ‘I would encourage most people to do buytolet, but there are potentialtrapdoors. You’ve got to choose carefully and stay close to your investment. Buy in areas that are being gentrified and with good amenities.’

Felix Ghauri, 41, from central London, has had an altogether better experience with buytolet. He has been involved in the sector since 2006 and gave uphis job as a management consultant to become a professional landlord.

Felix, who has five buytolets – four in London and one in Cheltenham – says: ‘There is a lot of work involved. If you borrow to buy, you are taking ondebt so you need to manage your investment carefully. That means minimising surprises. Map out scenarios so that if anything happens – for example, aproblem with a tenant or repairs that need to be done – you are prepared.’

In addition, borrowers are able to access interestonly loans – mortgages no longer available to nearly all homebuyers who are required to take outrepayment loans that involve higher monthly costs.

Although most buytolet lenders insist on a 25 per cent deposit, some are happy to lend to people as old as 70 and provide finance for 35 years.

‘Buytolet investors have a significant affordability advantage over wannabe owneroccupiers,’ says Matthew Pointon, property economist at thinktankCapital Economics. ‘Until such time that buytolet lending becomes subject to the same draconian regulations that govern firsttime buyers and homemovers, the share of lending going to investors will continue to rise. Buytolet investors have an edge.’

06/05/2015 Housing experts predict disaster if Labour caps rent rises | Daily Mail Online

http://www.dailymail.co.uk/money/buytolet/article-3065446/Experts-predict-disaster-country-s-landlords-Labour-vows-interfere-market-capping-rental-rises.html?printingPage=true 5/8

£Mortgage amount:

%Interest rate:

yearsDuration:

Mortgage type: Interest only

Monthly payment:

Until Labour’s announcement, it was difficult to find buytolet pessimists – as indeed it was hard to find anyone in the City in the late 1990s who thoughtthe tech bubble would burst. Those who make their living from buytolet – agents, lenders, consultants – refuse to entertain the thought that things couldgo horribly wrong.

Some are paranoid, happy to supply data on buytolet ‘hot spots’ while declining to reveal details of buytolet ‘black spots’ that investors would be wiseto avoid (many Northern towns fit this bill).

BUYTOLET MORTGAGE CALCULATOR

Work out your monthly payments

::: Calculate :::

In his report ‘BuytoLet Comes of Age’, Thomas predicts annual returns over the next decade for buytolet borrowers of a touch over 11 per cent – sixper cent for those who buy outright. Yet, when pressed, he concedes there are dangers lurking in the undergrowth – real dangers if Miliband strides intoNumber 10 Downing Street.

A Labourdominated Government, Thomas admits, would upset the apple cart if it carried out its threat of controls on the rent increases that privatelandlords are allowed to push through (it wants to cap them to the increase in inflation).

‘Political interference is a negative,’ he concedes, ‘but what would concern me more about Labour is if rental price caps were just the thin end of thewedge. What would then stop it from looking to protect tenants more – through enabling more people, for example, to enjoy sitting tenants’ rights?’

Interest rates could also rise, pushing up the cost of buytolet finance and squeezing yields – a real possibility under a Labour administration less

06/05/2015 Housing experts predict disaster if Labour caps rent rises | Daily Mail Online

http://www.dailymail.co.uk/money/buytolet/article-3065446/Experts-predict-disaster-country-s-landlords-Labour-vows-interfere-market-capping-rental-rises.html?printingPage=true 6/8

committed in practice to keeping spending down and deficits under control than in preElection talk.Higher interest rates would also cause financial havocfor buytolet investors leveraged up to the hilt.

Again, Thomas accepts higher interest rates are a potential blip on the horizon – especially in light of the fact that the minutes published from the latestBank of England rate setting meeting indicate rate rises may come sooner than the market expects.

‘It’s the 64,000 dollar question as to whether interest rates will remain so low,’ he says, ‘but there are no strong indications that they are about to rise eventhough we are seven years out of the financial crisis. There is more disinflation in the world’s financial system and the only tools available to counter thisare low interest rates and more quantitative easing – printing of money. The cost of money is being pushed down and that is terrible for savers, great forborrowers.’

Provided Miliband does not march into power on Friday, there seems little to suggest that a nation of amateur landlords is about to implode. But all betsare off if Red Ed fools the nation.

HOW TO BE A PROPERTY MAGNATE

1. If you are borrowing, expect to have to put down a 25 per cent deposit. Smaller deposits will result in higher mortgage rates.

2. Some lenders will not entertain you unless you have earned income (minimum £25,000). How much is lent will hinge on the level of rental income youcan command from the property. Lenders look for the rent to cover the mortgage interest by 125 per cent – with the rate used in this calculation beingeither five or six per cent. So a £150,000 buytolet mortgage would require monthly rent of at least £781.

3. Big buytolet lenders include BM Solutions (part of Lloyds Banking Group), Coventry Building Society and The Mortgage Works (part of NationwideBuilding Society). Mortgage fees are commonplace. Most loans must be arranged through a broker.

4. Buytolet is hard work and time consuming – ‘aggro’ according to Eric Pentecost, Professor of Economics at Loughborough University. You must factorinto your financial calculations the possibility of rental voids, late payments and repair costs. Getting someone to manage your property can reduce stressbut will eat into your investment returns. If you are going to selfmanage, it is better to buy close to home and in an area you know well and are upbeatabout (in terms of tenant demand). Greater regulation is creeping into the sector – on energy maintenance for example – so be prepared to spend timeand money ensuring your property complies.

5. Tax is an issue. Income from buytolet is taxable but mortgage and running costs can be offset against this. Capital gains from buytolet sales aretaxable.

6. Don't just depend upon buytolet, says Pentecost. ‘Investment in buytolet should really only be done as part of a diversified portfolio of assets.’

Comments (326)

Share what you think

NewestOldestBest ratedWorst rated

View all

Click to rate

Ant, braintree, United Kingdom, 23 minutes ago

I bet maggie thatcher never thought selling the council houses would lead to a btl brigade renting private properties funded by housing benefit !

ReplyNew Comment 01

Click to rate

willow123, godstone, United Kingdom, 5 hours ago

As an experienced BTL landlady there is no such thing as a free lunch and those on fantasy island hoping for a property crash or price correction remember you stillneed a deposit and you will still need to pay for it. Living in any city is expensive and out of reach of the majority and you either move to a cheaper are or rent aproperty outside the capital and use this to rent where you want! its not difficult to work out!

ReplyNew Comment 14

Click to rate

pgc, sittingbourne, 5 hours ago

It Puzzles me so many people here think that all landlords are wealthy millionaires making vast sums of money, here is a buy to let example of a property rented out, 3bed Victorian house rented to a family with three children, rent £625pcm. agent fees £52.pcm, mortgage £380 pcm, leaving £193pcm out of this sum comes landlordbuilding ins, gas certificate, any repairs and maintainance, this would come to approx. £100pcm, leaving a profit of £21.46p per week. for this you have theresponsibilities to the tenants involved by being a landlord, and the responsibility of paying the mortgage in any void periods should they occur, this is a very realbreakdown, I own this property and am not anywhere near a millionaire, and have happy tenants that want to stay long term, Anyone thinking landlords have it easyreally should give it a go.

ReplyNew Comment 06

Click to rate

James, London, United Kingdom, 9 hours ago

Most of the BTL is overseas investors, some using local family or companies to funnel their investment. I would guess that many of our MPs will be BTL, especially ifthey lose their seats and hang onto their second homes paid for by the taxpayers. These homes, in the London area will have gone up millions in price and they willeither pocket the profits or hang onto these 'free' houses and sell their other property or rent them out. How will the HMRC handle these gifts. Will they now be taxedas unearned income, will the MPs be required to pay capital gains? It is all a big scam.

ReplyNew Comment 45

Click to rate

hondonroy, alicante, Spain, 11 hours ago

I for one have given notice to my tenants to leave and decided to get out of the rental market. Once Governments start interfering in things they NO NOTHINGABOUT, just to get VOTES, its time to go back to a quiet life.

ReplyNew Comment 19