Embed Size (px)

Citation preview

IFRS and its impact on Financial Reporting for the Life Sciences Sector

January 2007www.pwc.com/uk/lifesciences

Foreword

The transition to International Financial Reporting Standards (‘IFRS’) continues to be a significant issue for the life sciences sector to address.

With a significant number of life sciences companies being quoted on the Alternative Investment Market (“AIM”) the development of IFRS practice is emerging more slowly in this sector than for many others.

We have analysed the annual reports of those companies in the techMARK mediscience index that have reported their first IFRS results. The constituent companies of the index at the time of analysis are included in Appendix A. From this we have assessed the income statement effect for the first full year of adoption. We have summarised the principal adjustments which have arisen and provide some guidance on each of these and the practical hurdles which need to be overcome. We also briefly consider the non-financial impacts that have arisen as well as the take up by companies of any exemptions that were available to them under IFRS 1 ‘First time adoption of International Accounting Standards’. The story is far from over but there are a number of valuable observations which can be made at this stage.

Due to the nature of this sector this analysis provides a powerful insight into the impact of IFRS to date – but as with any form of empirical analysis, there are inherent limitations.

This report does not seek to cover all of the accounting rules, but focuses instead on considering the principal GAAP differences arising to date and offers guidance. Each company will ultimately need to consider its own circumstances and apply the rules accordingly. A complete list of the IFRS, IAS and IFRICs is included in Appendix B.

PricewaterhouseCoopers continues to lead the debate within this sector and is committed to helping companies maximise the benefits of IFRS and improve the quality of their IFRS report.We hope you find this document helpful and look forward to discussing your comments and questions.

Clive Birch Ian Dixon Stephen Wyborn

2

Contents

Executive summary

Key IFRS issues for the life sciences sector

Share based awards

Research and development expenditure

Goodwill and intangibles

Business combinations

Revenue recognition

Holiday pay and other employee benefits

Financial instruments

Other adjustments

Making it more than just about the numbers

Embedding IFRS

Appendix A

Appendix B

Your IFRS contacts

4

�

Key IFRS issues for the life sciences sector

Executive summary

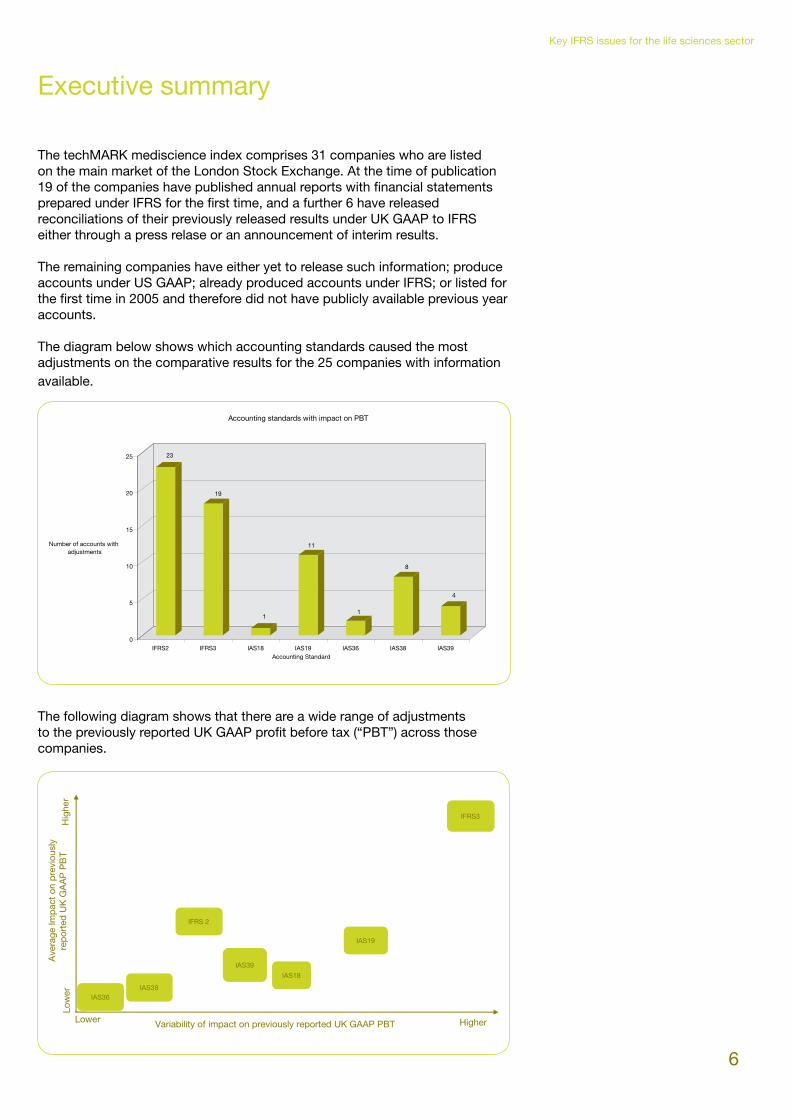

The techMARK mediscience index comprises �1 companies who are listed on the main market of the London Stock Exchange. At the time of publication 19 of the companies have published annual reports with financial statements prepared under IFRS for the first time, and a further 6 have released reconciliations of their previously released results under UK GAAP to IFRS either through a press relase or an announcement of interim results.

The remaining companies have either yet to release such information; produce accounts under US GAAP; already produced accounts under IFRS; or listed for the first time in 200� and therefore did not have publicly available previous year accounts.

The diagram below shows which accounting standards caused the most adjustments on the comparative results for the 2� companies with information available.

The following diagram shows that there are a wide range of adjustments to the previously reported UK GAAP profit before tax (“PBT”) across those companies.

23

19

1

11

1

8

4

0

5

10

15

20

25

Number of accounts with adjustments

IFRS2 IFRS3 IAS18 IAS19 IAS36 IAS38 IAS39Accounting Standard

Accounting standards with impact on PBT

Variability of impact on previously reported UK GAAP PBTLower

Low

er

Higher

Hig

her

IAS19

IAS18

IAS38

IFRS3

Ave

rage

Imp

act

on p

revi

ousl

y re

por

ted

UK

GA

AP

PB

T

IFRS 2

IAS39

IAS36

6

Key IFRS issues for the life sciences sector

Executive summary

The standards having the most impact are discussed later.

Our survey also showed that all apart from one of the companies who had made acquisitions prior to their IFRS transition date took the exemption available under IFRS1 to not restate the acquisition in accordance with IFRS� ‘Business Combinations’. Whilst this may not in itself be surprising it does show that for one reason or another one of the companies opted to restate the acquisition.

All companies took the exemption available to only account for equity settled for share options which were granted after 7 November 2002 and had not vested at the later of 1 January 200� or the transition date.

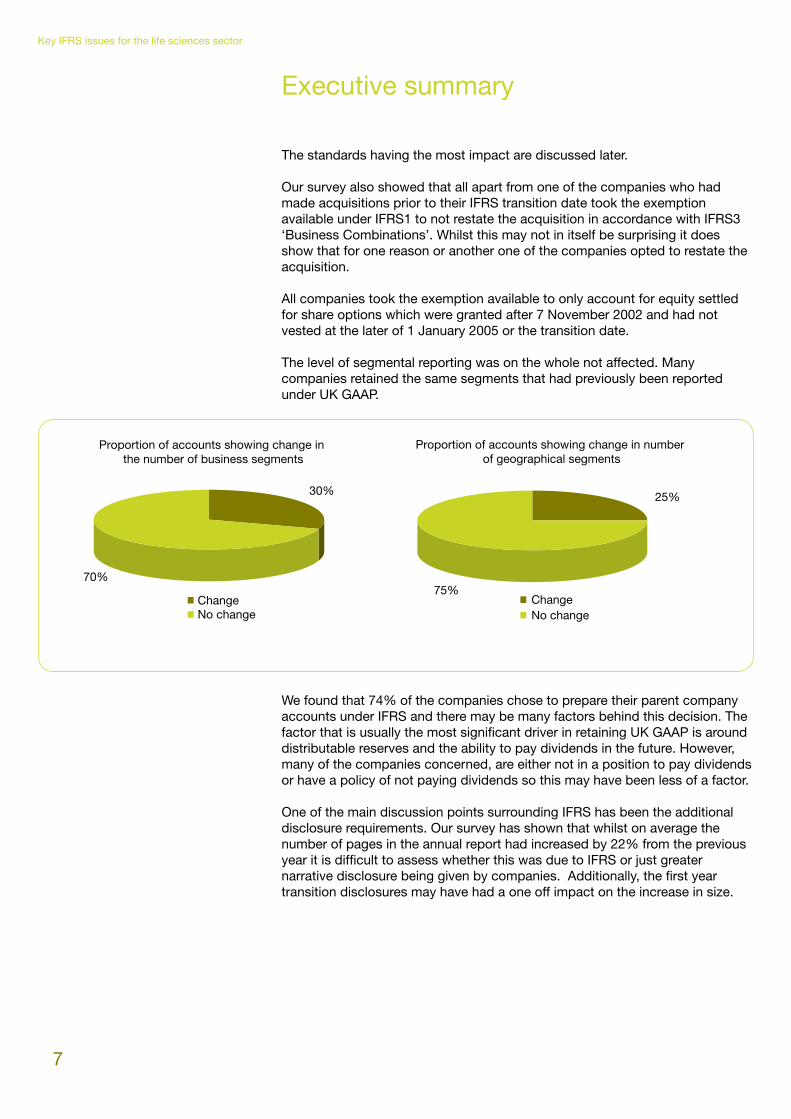

The level of segmental reporting was on the whole not affected. Many companies retained the same segments that had previously been reported under UK GAAP.

We found that 74% of the companies chose to prepare their parent company accounts under IFRS and there may be many factors behind this decision. The factor that is usually the most significant driver in retaining UK GAAP is around distributable reserves and the ability to pay dividends in the future. However, many of the companies concerned, are either not in a position to pay dividends or have a policy of not paying dividends so this may have been less of a factor.

One of the main discussion points surrounding IFRS has been the additional disclosure requirements. Our survey has shown that whilst on average the number of pages in the annual report had increased by 22% from the previous year it is difficult to assess whether this was due to IFRS or just greater narrative disclosure being given by companies. Additionally, the first year transition disclosures may have had a one off impact on the increase in size.

Proportion of accounts showing change in the number of business segments

30%

70%

ChangeNo change

Proportion of accounts showing change in number of geographical segments

25%

75%ChangeNo change

7

Key IFRS issues for the life sciences sector

Share Based Awards

Accounting Issue

The use of share-based awards as employee incentives are common place across most industries, but especially the life sciences sector. Under previous UK GAAP the accounting principles focused on the intrinsic value (difference between market value of shares at date of grant and exercise price of option) as a basis to charge the profit and loss account (with SAYE schemes exempt). Under the requirements of IFRS 2 ‘Share based payment’ the fair value needs to be determined by the use of a valuation model and the resultant profit and loss account charge recognised over the vesting period.

With UK GAAP adopting FRS20 for unlisted companies with financial periods beginning on or after 1 January 2006 this GAAP difference is set to disappear, and therefore for those companies who will report their first IFRS results in 2007 there will be no impact. There will remain a difference in how to account for any employer’s NIC payable, with it being accounted for as a cash settled award under IFRS but using the intrinsic method required by UITF2� ‘National Insurance on Share Option Gains’ under UK GAAP.

Market Analysis

Of the 2� companies who have quantified the effect, 2� incurred a charge in respect of share-based awards. The average charge represented 6% of the previously reported UK GAAP profit/loss before tax of those companies, with the largest charge representing 27% of the previously reported UK GAAP pre-tax result.

All of the companies have taken the exemption available under IFRS1 to not account for those options issued prior to 7 November 2002 or those options that were granted after 7 November 2002 but which had vested prior to the later of 1 January 200� and the date of transition to IFRS.

Complexities arising out of application of IFRS

Many companies have used the Black-Scholes model for determining fair values. In the Black-Scholes model the most significant variables which will drive the fair value are: • Volatility: Companies look to history to determine which volatility to use, but most companies have

found the historical volatility may appear to be inconsistent with the requirements of the standard - to form a view on the future expected volatility over the life of the award. Companies will need to consider historical volatility over different time periods, look to market volatility and consider the one-off items in their history or future which may need to be discounted or included. This will require a significant amount of judgement.

• Expected life of awards: In long established companies, history can be the best indicator for the expected life of awards, as the use of share options and the time taken to exercise is well established. However for life sciences companies, the history is likely to include under-water options, a high turnover of staff and other circumstances whereby there is insufficient history to establish a discernable pattern. Other than history, the following factors could also be taken into account:

• The length of vesting period. • Price of underlying shares, as experience may indicate that employees exercise once the share price

has reached a specified level above the exercise price. • How long shares are held, senior employees hold onto than more junior employees. • More volatile shares with exercise periods to lock in will require judgement.

Final Thoughts

Companies will need to:

• Make sure that they have the right model considering the type of performance conditions that the options have.

• Remember that whilst models are relatively simple to obtain it is the assumptions input into the model which are challenging companies.

• Consider the continued appropriateness of the use of incentive schemes. There are many companies who have already begun to reduce their use of share options due to the resultant earnings volatility.

• Remember that they are required to recognise (or at least disclose) a deferred tax asset where there is a deductible temporary difference equal to the intrinsic value of share options at the date of transition to IFRS. This applies to all options regardless of whether they were prior to 7 November 2002. Whilst many companies have focused on the profit and loss account, the next hurdle is to provide all of the extensive disclosures required for the annual report and accounts.

8

Key IFRS issues for the life sciences sector

Research and development expenditure

Accounting Issue

Under IFRS development costs must be capitalised when the future technical feasibility and economic benefit of the asset can be demonstrated.

Market Analysis

None of the companies analysed had capitalised any internal research and development costs. This is in line with the norm seen in larger pharmaceutical companies which do not capitalise costs until such time as regulatory approval has been obtained.

As far as external research and development costs are concerned there has been capitalisation to reflect that patents etc have been purchased which are deemed to have a value to the business going forward.

Complexities arising out of application of IFRS

Under UK GAAP companies were given a choice with respect to development expenditure which, together with the widespread application of the prudence concept, resulted in all expenditure being routinely expensed. Under IFRS all of the following must be demonstrated prior to capitalisation:

• Technical feasibility• Clear intention to complete and use/sell it• Ability to use/sell it• Ability to generate probable future economic benefits• Availability of adequate resources to complete development• Ability to reliably measure the expenditure attributable to the asset

In practice, most internal costs should continue to be expensed as until regulatory approval is obtained it would be difficult for any company to demonstrate that there was an ability to generate probable future economic benefits.

Final Thoughts

The life sciences sector is not the only sector wrestling with how to apply the rules in a practical way but it does benefit from having an external party that determines when products can be sold.

Goodwill and intangibles

Accounting Issue

Under IFRS � and IAS �6 ‘Impairment of Assets’ goodwill is no longer amortised through the profit and loss account but will be subject to an annual impairment test. In addition to the intangibles recognised as part of acquisitions many companies have separately disclosed acquired software as intangibles.

Market Analysis

All companies with goodwill made adjustments for non-amortisation of goodwill and some of the benefits to the reported results have been significant, ranging from a few percent to three times the previously reported UK GAAP profit/loss results. This clearly highlights how consolidation remains a critical business issue and together with the new accounting of business combinations will change the accounting landscape for acquisitions and post acquisition results.

Complexities arising out of application of IFRS

With goodwill now subject to an annual impairment test, it will be necessary for companies to determine cash generating units to which the goodwill is related and perform the impairment review at that level.

Final Thoughts

Companies with goodwill need to:

• Determine the cash generating units to which the goodwill relates • Establish a methodology for carrying out the reviews, which is agreed with their auditors • Ensure the appropriate valuation techniques are used, which will include establishing the correct

discount value, having the right cash flows and having the correct terminal value.

9

Key IFRS issues for the life sciences sector

Business combinations

Accounting Issue

The standard on business combinations, IFRS �, was issued on �1 March 2004. It provides new recognition criteria for acquired intangible assets, with the result that many intangible assets which would previously have been subsumed within goodwill will now have to be separately identified, valued and capitalised on the balance sheet.

An intangible asset is identifiable when it either arises from contractual or other legal rights or is separable i.e. capable of being separated or divided from the entity and sold, transferred, licensed, rented or exchanged, either individually or together with a related contract, asset or liability. The most common ones for life sciences companies are likely to include:

• In-process research and development costs as long as it is probable that future benefits will accrue from them

• Customer contracts and related relationships • Non-contractual customer relationships • Production processes or know-how • Trademarks • Non-compete agreements • Patents • Unpatented technology • Licensing or royalty agreements

The main type of ‘asset’ of an acquired company that does not meet the criteria to be capitalised as an intangible is its workforce.

Market Analysis

Only one of the companies have re-opened acquisitions prior to the date of transition leading to intangibles being separately recognised with resulting goodwill being lower than previously stated under UK GAAP.

Complexities arising out of application of IFRS

The acquisition process has become more complex. There is a need for greater evaluation of the target business so that intangible assets can be fair valued at the time of acquisition, which is likely to require a costly external valuation exercise. There will be greater scrutiny to ensure intangibles have been properly identified and then to establish what the remaining goodwill represents.

There may be more volatility as a result of impairments due to the more frequent and rigorous impairment testing of goodwill and other acquired intangibles.

Final Thoughts

With the requirement to value intangible assets acquired we may see the structure of deals changing with the purchaser forming such valuations in advance of completing the deal, which may then affect the purchase price as management/investors may question what the resultant goodwill really represents or whether the deal is overpriced.

It is not uncommon for even small deals to require a valuation exercise to identify and value intangibles. The expertise to carry out this exercise is rarely found in-house.

As well as affecting the structure, price and accounting for potential deals, the recognition of intangible assets and their subsequent amortisation will also have an impact on key performance indicators, stock options and management targets.

It is likely that a deferred tax liability, associated with the acquired intangibles, will need to be provided for.

Any tax losses not recognised as deferred tax assets at the time of an acquisition due to the uncertainty over their recoverability will need to be offset against goodwill in future years if the losses are subsequently utilised.

10

Key IFRS issues for the life sciences sector

Revenue recognition

Accounting Issue

IAS 18 ‘Revenue recognition’ requires companies to recognise revenue when there is a gross inflow of economic benefits during its ordinary course of business.

Market Analysis

From the 2� companies in our study only one of them identified any revenue recognition GAAP differences.The difference arising related to deferring revenue from up front licence receipts which had, under UK GAAP, been recognised immediately in full as there had been no material future obligations to fulfill and the receipt was deemed to be in relation to past service.

Complexities arising out of application of IFRS

Most commentators would argue that with the introduction of FRS �, Application Note G ‘Revenue recognition’ in the UK, there cannot be many instances where revenue recognition for life sciences companies would be different under IFRS, and this would seem to agree with the results of this survey.

However, companies undertake business in many different ways and there is no substitute for reviewing your own revenue recognition model. In addition, both IAS 18 and Application Note G are not prescriptive rules and therefore the practical application requires judgement which itself could give rise to a GAAP difference.

Final thoughts

This area remains complex and the requirement to apply principles could give rise to different practices within the industry and despite some views to the contrary could give rise to GAAP differences between IFRS and US GAAP. US GAAP has a rules based approach and in some instances has stricter interpretations of principles such as fair value.

PricewaterhouseCoopers delivers specific revenue recognition training to help companies work through the principles and highlight potential GAAP differences.

Holiday pay and other employee benefits

Accounting Issue

Holiday pay and other short-term compensated absences are dealt with by IAS 19, ‘Employee benefits’ together with accounting for defined benefit pension schemes. Where holiday benefit is accumulating (ie. holiday benefit is earned over time and capable of being carried forward) a reporting entity should provide for the expected cost of the accumulated benefit. The fact that employees may lose the benefit if they leave the company does not remove the need for a provision, although it may influence the measurement of the provision (i.e. if you can estimate how many leave due to regular turnover of staff).

Market Analysis

Out of the 2� companies reporting to date 6 recognised a holiday pay accrual. The adjustments were largely insignificant, with the largest adjustment from IAS19 arising, perhaps unsurprisingly, as a result of defined benefit pension arrangements.

Complexities arising out of application of IFRS

In most territories holiday pay has historically been accrued consistent with local practice.

Whilst it is widely considered that accounting for holiday pay should not be a difference between UK GAAP and IFRS, in previous years the practice for UK companies has been to not record such an accrual not least because most companies have a ‘use it or lose it’ policy in respect of each financial year.

Final Thoughts

UK practice had been not to recognise holiday pay accruals but under IFRS companies have an explicit requirement to establish an accrual and they will need to keep accurate holiday records in order to establish the accrual at each reporting period.

The use of defined pension schemes within the life sciences industry is not common and therefore the impact of IAS19 on accounting for pensions has not had a widespread impact.

11

Key IFRS issues for the life sciences sector

Financial instruments

Accounting Issue

IAS�9, ‘Financial Instruments: Recognition and Measurement’ requires that any derivative financial instrument taken out for the purposes of hedging a transaction be fair valued, unless the instrument meets the criteria for hedge accounting, with the gain/loss being recorded through the income statement. Under UK GAAP if companies did not apply hedge accounting the derivative could be held at cost.

Market Analysis

The onerous requirements of IAS�9 to have documentation in place and to test for hedge effectiveness in order to enable hedge accounting appears to have resulted in companies not adopting hedge accounting, and instead recording the fair value of the instrument in the income statement. Two companies were impacted in this way.

Two other companies were impacted as receivables held in the balance sheet have to be held at the amortised cost which was not the case under UK GAAP.

Complexities arising out of application of IFRS

In order to qualify for hedge accounting companies are having to put in place documentation at the start of the hedge and perform effectiveness testing at each reporting date. This is an onerous and complex process which is designed to represent a significant hurdle.

Final Thoughts

Whilst companies will continue to take out hedges for commercial reasons the accounting will not necessarily match the commercial benefit.

Companies will need to remember that despite not hedge accounting they will still be hedged.

12

Key IFRS issues for the life sciences sector

Other adjustments

As well as those set out in the preceding pages the other key adjustments that companies have reported include:

Defined benefit schemes

For December year end companies the accounting for defined benefit schemes under IFRS differs to the policy that would have been followed under UK GAAP. IAS19 requires assets/liabilities to be recognised on the balance sheet in a similar way to FRS17 with charges through the profit and loss account based on finance cost as well as service cost. But there are still a few key differences between the two standards.

Deferred taxation

Many of the IFRS adjustments have deferred tax consequences and some companies have recognised the deferred tax assets arising out of the share based charges being expensed. Lease accounting

No company identified any differences between the classification of operating and finance leases, but in future companies will still need to go through the process of identification and determination to reach that conclusion. One company identified that there was a difference in relation to accounting for lease incentives – under UK GAAP the incentive was amortised to the first break period in the lease whereas under IFRS it is required to be amortised over the full length of the lease.

Consolidation of subsidiaries

Under IAS27 companies are required to consolidate all subsidiaries which are controlled by the company. Control is defined as the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. Therefore consolidation is required if there is the power to control, even if actual control is not exercised. Under UK GAAP companies did not need to consolidate if they could demonstrate that they did not exercise control.

Accounting for associates

Under IAS28 groups are required to equity account for all investments where the group has a significant influence, defined as being the power to participate in the financial and operating policy decisions of the investee. A holding of 20% is presumed to provide such influence; holding less than 20% is presumed to not give such influence unless it can be demonstrated otherwise. UK GAAP required that the investor had both a participating interest and exercised significant influence.

1�

Making it more than just about the numbers – embedding IFRS

Having completed the transition, it is now time to have IFRS underpin the numbers and the business as a whole. If IFRS is not embedded into your organisation, management could find it difficult to meet the expectations of both their internal and external stakeholders.

Most companies have taken a tactical approach to IFRS, often driven by necessity, due to timing and resource constraints. Some companies have delegated the preparation of external reporting to external contractors or consultants, therefore IFRS reports are produced outside the company’s normal reporting systems and there is limited knowledge transfer to other staff.

The goal of embedding IFRS is to make compliance with the new reporting standards ‘business as usual’. Management needs to establish disciplines and procedures that can be repeated, period after period, in an efficient and robust manner, without reliance on resources, processes and systems that do not exist on an every day basis - effectively having to be ‘switched on’ for external financial reporting. Manual intervention and spreadsheets are part of the immediate solution for some, which can increase the risk of error, be inefficient and make effective control more difficult.

The technical skill required by the finance team has been hugely underestimated. Companies need to consider how to keep their organisation up to date on the new standards or incur additional costs from external advisers.

Many commentators and regulators have begun to question the presentation of information by companies who have sought to adjust items to take account of some of the impact of IFRS. The rationale is that the adjusted measures are a more representative measure of the underlying performance of the company. If it becomes recommended, or even required, practice to report only IFRS GAAP numbers, it will be just another reason to ensure IFRS is embedded within the organisation.

Embedding IFRS will need management to consider:

• Processes • Data systems and technology • Controls • People capability • Organisational structure • Planning strategies and reporting.

14

Key IFRS issues for the life sciences sector

Appendix A

The constituent companies of the London Stock Exchange techMARK mediscience index at 9 October 2006 were:

Acambis plcAlizyme plc Antisoma plc Ardana plc Ark Therapeutics plc Asterand plc Axis-Shield plc Biocompatibles International plc Biotrace International plc BTG plc Celsis International plc Corin Group plc Ferraris Group plc Genemedix plcGyrus Group plcHuntleigh Technology plcInion OyInnovata plc Isotron plcOptos plcOxford BioMedica plc Phytopharm plc ProStraken Group plc Protherics plc PuriCore plcRenovo Group plcSkyePharma plc Theratase plc Vernalis Group plcWhatman Group plc XTL Biopharmaceuticals Ltd

1�

Key IFRS issues for the life sciences sector

Appendix B

Standards and interpretations

IFRS 1 First-time Adoption of International Financial Reporting Standards

IFRS 2 Share-based Payment

IFRS � Business Combinations

IFRS 4 Insurance Contracts

IFRS � Non-current Assets Held for sale and Discontinued Operations

IFRS 6 Exploration for and Evaluation of Mineral Resources

IFRS 7 Financial Instruments: Disclosures

IAS 1 Presentation of Financial Statements

IAS 2 Inventories

IAS 7 Cash Flow Statements

IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors

IAS 10 Events After the Balance Sheet Date

IAS 11 Construction Contracts

IAS 12 Income Taxes

IAS 14 Segment Reporting

IAS 16 Property, Plant and Equipment

IAS 17 Leases

IAS 18 Revenue

IAS 19 Employee Benefits

IAS 20 Accounting for Government Grants and Disclosure of Government Assistance

IAS 21 The Effects of Changes in Foreign Exchange Rates

IAS 2� Borrowing Costs

IAS 24 Related Party Disclosures

IAS 26 Accounting and Reporting by Retirement Benefit Plans

IAS 27 Consolidated and Separate Financial Statements

IAS 28 Investments in Associates

IAS 29 Financial Reporting in Hyperinflationary Economies

IAS �0 Disclosures in the Financial Statements of Banks and Similar Financial Institutions

IAS �1 Interests in Joint Ventures

IAS �2 Financial Instruments: Disclosure and Presentation

IAS �� Earnings Per Share

IAS �4 Interim Financial Reporting

IAS �6 Impairment of Assets

IAS �7 Provisions, Contingent Liabilities and Contingent Assets

IAS �8 Intangible Assets

IAS �9 Financial Instruments: Recognition and Measurement

IAS 40 Investment Property

IAS 41 Agriculture

IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities

IFRIC 2 Members’ Shares in Co-operative Entities and Similar Instruments

IFRIC � Emission Rights

IFRIC 4 Determining whether an Arrangement contains a Lease

IFRIC � Rights to Interests arising from Decommissioning, Restoration and Environmental Rehabilitation Funds

IFRIC 6 Liabilities arising from Participating in a Specific Market – Waste Electrical and Electronic Equipment

IFRIC 7 Applying the Restatement Approach under IAS 29, Financial Reporting in Hyperinflationary Economies

IFRIC 8 Scope of IFRS 2

IFRIC 9 Reassessment of Embedded Derivatives

IFRIC 10 Interim Financial Reporting and Impairment

IFRIC 11 IFRS 2 - Group and treasury transactions

16

Key IFRS issues for the life sciences sector

Your IFRS contacts

Clive BirchPartner, Life Sciences Sector LeaderTel: 0122� ��2�0�Email: [email protected]

Ian DixonDirector, Life Sciences SectorTel: 0122� ��2�09Email: [email protected]

Stephen WybornManager, Life Sciences SectorTel: 0122� ��2270Email: [email protected]

17

www.pwc.com/uk/lifesciences

This article has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this article without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this article, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents accept no liability, and disclaim all responsibility, for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this article or for any decision based on it.

The firms of the PricewaterhouseCoopers global network (www.pwc.com) provide industry-focused assurance, tax and advisory services to build public trust and enhance value for clients and their stakeholders. More than 140,000 people in 149 countries across our network share their thinking, experience and solutions to develop fresh perspectives and practical advice.

© 2007 PricewaterhouseCoopers LLP. All rights reserved. ‘PricewaterhouseCoopers’ refers to PricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom) or, as the context requires, the PricewaterhouseCoopers global network or other member firms of the network, each of which is a separate and

independent legal entity. Ref 2006BHM21891.