Embed Size (px)

Citation preview

ReportIn This Issue

• EOSRiSqiSanEquitybaSEdEuROpEanpaRtnERShip

• WEaREalEadingpROvidEROfinSuRancEbROkingandRiSkmanagEmEntcOnSultancytOEuROpEanandglObalEntERpRiSES

• cliEntSREcEivEaSERvicEWhichiStailOREdtOthEiRnEEdS

• intERnatiOnalSOlutiOnSaREOffEREdthROughlOcalapplicatiOn

• WESpEakyOuRlanguagEandundERStandyOuRcultuRE

• WEhavEanunRivallEdStRuctuREinthEEmERgingmaRkEtSOfcEE

• glObalviSiOn,lOcalpREciSiOn

copyright2006EOSRiSqn.v.allrightsreserved.alltrademarks,tradenamesorcompanynamesreferencedhereinareormaybethetrademarksorregisteredtrademarksoftheirrespectiveowners.anyrightsnotexpresslygrantedhereinarereserved.

For comments, questions or requests, please contact the editor at:

eos risq Belgium, Bert van roY, plantin en moretuslei 297, 2140 antwerp, Belgium

or e-mail [email protected] - www.eosrisq.com

volume 3, sprIng 2006

Introduction1 introduction

2 Riskmanagement–conceptsofimplementationfortheclinicalpractice

5 boomingchinachina’sEconomy–abriefOverview

8 impactofnewchinesebusinessinsurance

legislation

9 howcantheavianfluaffectyourbusiness?

11 prospectusliabilityandmergers&acquisitions

14 EOSRiSqopenscountryofficeintheRussianfederation–interviewwithgeneralmanagergleblobanovonthecurrentRussianinsurancemarket

17 Europeansprinklerregulation:rulesandnorms

We hope that you will enjoy this edition of the EOS RiSq report.We feature articles covering a wide range of topics all of whichrelatetotheincreasinglycomplexrisksthatfacebusinessesandtheopportunitiesthatthesecomplexitiescreateforbrokersasadvisorsandadvocatestotheirclients.

unlike the Wtc loss in 2001, the ferocious hurricanes that tookplace last year around the gulf of mexico and which caused suchwidespreaddevastationbothtopropertyandtothepopulationinthevicinity,havenotresultedinauniformincreaseinratesasoccurredafterWtcdespitetheaggregatequantumsoflossbeinghigherthanWtc.

the upward pressure on rates has been predominantly limited tocertain classes of insurance and reinsurance, in particular thosethatproducedthelossesandtocatastropheprogrammeswithhighwindstorm exposures. in most other classes and territories, clientscontinuetoachieveratereductionsandcapacity issufficient forallbutthelargestofrisks.

EOSRiSqhascontinueditsexpansionduringthepast6monthswiththeopeningofanofficeinRussiaandthisreportcarriesaprofileofthatnewinitiative.Welookforwardtoexpandingourpresenceinthisimportantworldeconomy.

the increasing tendency for corporations to expand theiractivities internationally is generating insurance needs and advicethat traditionally have only been required by the larger globalor international companies. the ability of corporations to gain acompetitive advantage by either outsourcing or relocating partsof their businesses to lower cost environments provide us ourinternational alliance with an opportunity to prove our value toour customers providing local knowledge and solutions under theumbrella of internationally agreed service standards and operatingprocedures.

WehopeyouenjoythisadditionoftheEOSRiSqreportandwillnothesitatetocontactusaroundanyriskissuesonwhichyouhaveanyconcern.

Wishingyouallthebest,

Johnpercy-davischairmanEOSRiSq

2Report

EOS RISQ Germany – Peter Gausmann

the quality of medical care in diagnostics, therapy andcare has been continuously improved in the course ofrecentyearsbyimplementationofmanifoldexternalandespecially internal measures. this is essential in timesof economisation, rationalisation and globalisation. thenumber of reported liability losses claimed by patientsagainst hospitals parallels the quality-improvementcampaignandestablishmentofcertificationprocedures,and reaches record level. today’s hospital patients areincreasingly informed and capable of criticism, and arenot willing to accept the outcomes of modern medicinescience as being fate. they articulate their expectationsfor medicine and care, and object alleged malfeasance.infuture,thesepatientswillreadupmoreonpreventivestandards, assumedly more than they will catch up onqualitymanagementandcertification.

thenumberofreportedliabilitylossesclaimedbypatientsagainsthospitalsparallels

thequality-improvementcampaignandestablishmentofcertificationprocedures,and

reachesrecordlevel.

theplayersinhealthcare-physiciansinthefirstinstance– ought to respond the claims development, whichconstitutes another trend causing concern, with theimplementation of prevention measures in terms of riskmanagement.Statisticsshowthatallegationsoferrorintreatment are without legal cause in many cases. Onethirdofclaimsissettled,twothirdsarefiledawaywithoutassuming any liability. this constant level extends overseveralyears.

nonetheless, each reported allegation involves time-consuming investigations, hearings and entailsanalysis efforts for the accused. the situation becomesparticularly tragic for clinics, if potential allegations oferror in treatment are passed to the blaze of publicityandthemediabecomesinterested.thiscouldnullifythelongstandingeffortstocreateapositiveimageinashorttime.therearenumerousexamplesofit–andareversalofthistrendisnotexpected.

Riskmanagement isnothingnew!daily teammeetings,ward rounds, mortality conferences etc. are measuresof prevention that belong in variable degrees to therepertoire of therapeutic teams in every specialistdepartment. methodical risk management surveysstructures, processes and results of medical and care

procedures from the perspective of former claims. itconcernsprophylacticstrategiesforerrorpreventionandthus, reduction of forensic risks by gathering existingweakpointsandpotentiallosses.

if not before, it is then, when losses occur, that risks ofclinics or specialist departments become known – itis easy to be wise after the event – but then it is toolate. professional risk management capitalises on anamplewealthofexperiencegatheredfromincidentsthatoccurredinothercomparablefacilities.theseexperiencesand their derivable prevention measures are passed onto the clinic staff during the implementation of riskmanagementprocesses.

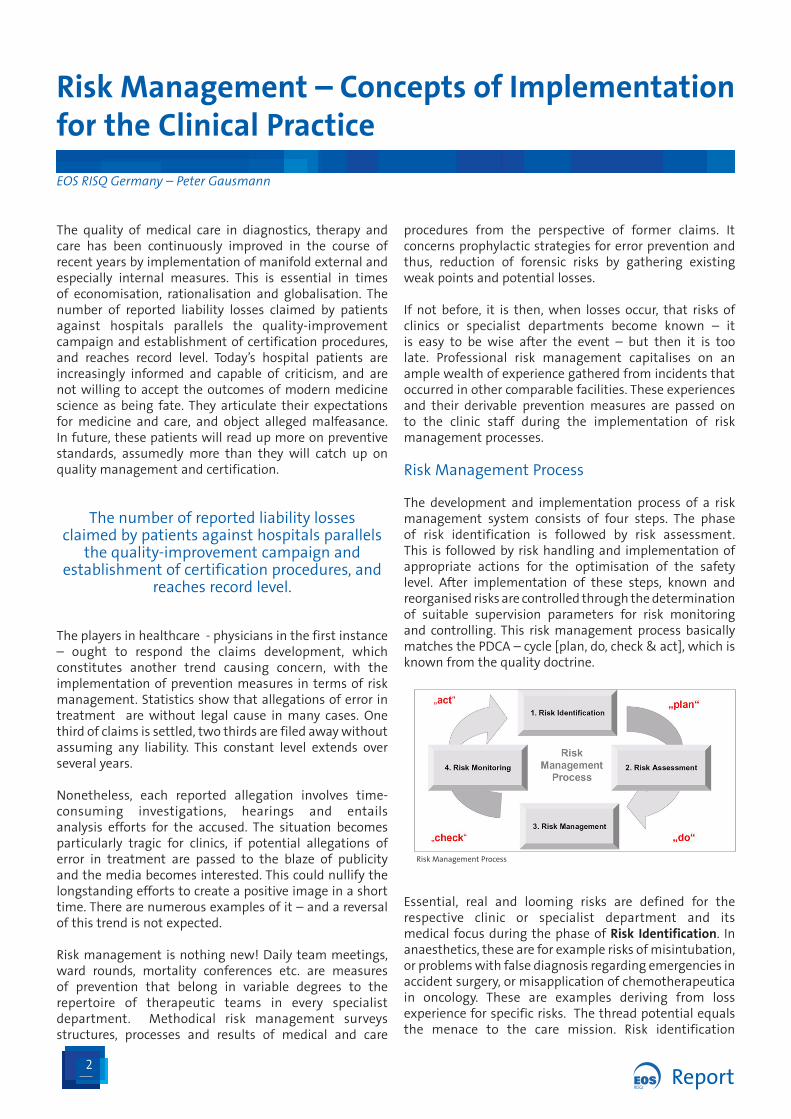

Riskmanagementprocess

the development and implementation process of a riskmanagement system consists of four steps. the phaseof risk identification is followed by risk assessment.this is followed by risk handling and implementation ofappropriate actions for the optimisation of the safetylevel. after implementation of these steps, known andreorganisedrisksarecontrolledthroughthedeterminationof suitable supervision parameters for risk monitoringand controlling. this risk management process basicallymatchesthepdca–cycle[plan,do,check&act],whichisknownfromthequalitydoctrine.

Essential, real and looming risks are defined for therespective clinic or specialist department and itsmedical focus during the phase of Risk Identification. inanaesthetics,theseareforexamplerisksofmisintubation,orproblemswithfalsediagnosisregardingemergenciesinaccidentsurgery,ormisapplicationofchemotherapeuticain oncology. these are examples deriving from lossexperienceforspecificrisks. thethreadpotentialequalsthe menace to the care mission. Risk identification

Risk Management – Concepts of Implementation for the Clinical Practice

Riskmanagementprocess

�volume 3

requires attentiveness, consciousness and sensitisation of all involved members of a therapeutic team; it is not only the responsibility of physicians, but also a task for the nursing care and medical assistance professions. Staff members usually know the thread potentials of their direct working area through their vocational education, further trainings, and last but not least through their work experience. However, risks seem to be controllable due to certain routine processes that emerge, especially, if risks have not resulted in losses in the past. Therefore, it is important to take the opportunity for unreserved and self-critical reflection, which is offered during the phase of risk identification. It must not be affected by hierarchic structures and other disruptive factors.

Potential consequences of identified risks are quantified in the Risk Assessment phase. The degree of risk is assessed by quantifying the probability of occurrence and the size of potential loss involved. The outcome is shown in a simple two-dimensional risk-portfolio-scheme, for example:

The area between the opposing poles of loss potential and occurrence probability shows the therapeutic team the need for action. The assessment of identified risks ignites a fruitful interaction process, and mostly a practicable solution is being elaborated at its final stage.

Risk Handling constitutes phase � of the risk management process. The task is to draw consequences from the risks that were previously identified and assessed.

Manifold measures, which have been defined in line with risk identification and assessment, become effective as risk handling strategies:

Examples for department-specific risks in

...surgical care Development and implementation of requirements-

oriented, pre-operative preparation standards.Continuous medical device-related training and

instruction.

...in-patient care Establishment of scoring systems for the risk of patient

fall and decubitus ulcer.Development of interdisciplinary treatment paths.

...emergency care Resuscitation trainings for all therapeutic team

members and interactive CRM measures (Crew Resource Management).

Continuous critical retrospective analyses of emergency missions.

... anaesthetics Provision of centrally available material sets for

complicated intubations, and training of employees.Development of interdisciplinary association /

enlistment rules.

•

•

•

•

•

•

•

•

From medical everyday life it is known that sources of incidents, complications and losses are multifactorial. Misinterpretations, lacks of attention and misunderstandings add up to a constellation, that overrides the established safety barriers. The meanwhile well-known ‘Swiss-Cheese-Scheme’ adapted from Reason, illustrates, that single holes in a multifaceted safety net are non-effective, but that holes fatefully correspondent to one another will cause the unintentional result. This visualization may be employed in a useful way in order to create risk awareness and to control risks and hazards in the risk management process.

Considering, for example the problem of wrong-side surgery in surgical care, safety barriers are established in all clinics; however, in a differently developed manner and pervasion. In risk management it is to question for example, whether:

the surgeon knows the patient to be operated on;the surgical area is adequately marked where

appropriate;the patient is adequately interviewed before

anaesthesia;a suitable identification system is provided.

Clinic-wide Risks

Not only discipline-specific risks, but also perils that are irrespective of specialist departments and which require a preventive concept for the entire clinic, are revealed by each analysis performed on risk management grounds. Over the past years, media have shown a continuously growing interest in the topic ‘medical malpractice in hospitals’. This has brought vexatious experiences to some clinics that have been through the mills of journalism without chance of an unbiased, objective statement.

••

•

•

�Report

Risk management also provides preventive training measures for this purpose, such as:

writing press releases;simulation of press conferences;creation of a code of practice for the ‘case of media

emergency’;pre-test interviews for live performances;clinic-internal information activities.

A strength and weakness analysis of the hospital’s public relations section is required in the course of the risk management process implementation. The phase of risk monitoring completes the risk management process. The effectiveness of newly defined safety measures is to be monitored continuously, and as the case may be modifications have to be accomplished where necessary. To do so, appropriate instruments are inevitable. This particularly comprises a continuous loss monitoring including causation assessment and return information to the persons involved.

A sustainable consciousness for risks and perils has to be achieved in clinical care.

A CIRS (Critical Incident Reporting System) should be installed and trained, as it is an effective instrument, that allows for identification of known and unknown risks. This procedure gathers near losses, i.e. incidents, which had the potential to lead to an undesirable outcome if left to progress (e.g. malfunction of an alerting system and as a consequence thereof, physician was not reached). The awareness that critical incidents, slight and severe complications, as well as serious losses are associated with each other, forms the basis of such a system. The systematic examination of critical incidents without consequences of loss and identification of its causation may help prevent potential real losses by introduction of adequate prevention measures. A comprehensive risk survey and reorganisation, i.e. implementation of the entire risk management process is inevitable, as otherwise the introduction of a CIRS may be ineffective. Initially, a process of growing consciousness has to be started. Members of the therapeutic team screen their respective

•••

••

fields of activities under the aspect of risks, and introduce preventive measures during this process. The process of growing consciousness may be followed by CIRS for stabilisation and completion purposes.

Conclusion

Staff members of clinics have to keep pace with the rapid development of medical science, but their possibilities are restricted by legal practice and claims settlement. Moving within this field of tension requires medical and legal expertise.

Risk management is based on four pillars: efficient documentation on services rendered in

diagnostics, therapy and care; extensive patient education and information;organisation of work flow; proper and professional treatment.

A sustainable consciousness for risks and perils has to be achieved in clinical care. A comprehensive approach, which embraces all occupational groups beyond hierarchy levels, and the understanding for risk reduction, which was elaborated in these groups lead to the fact, that sensitive work processes are not only eyed from the medical and economic perspective, but also from the liability- relevant point of view. Normally, clinics dispose of a tight network of safety barriers, and of a critical incident instrument by implementing a house risk managment system (e.g. the software riskop).

Liability insurers of hospitals increasingly ask for evidence of prevention measures for the elevation of patient safety, as precondition for risk coverage.

A clinic-wide risk management concept that is integrated into the quality management structures, offers a distinguished chance to visualise measures of risk prevention and, last but not least, its demonstration to patients.

•

•••

Contact

Peter GausmannKlingenbergstraße ��2758 DetmoldGermanyE-mail: [email protected]

5volume 3

Booming China

gdp–SizeandgrowthRate

One of the biggest questions absorbing the minds oftoday’s economists is: “When will china’s economybe as big as that of the united States?” based uponavailablehistoricaleconomicdataandpatternsofpeopledevelopment, itmight reasonablybeestimatedthat thechinese economy will achieve this sometime between2012and2016.percapitagdp,however,itisnotlikelytoapproachthatoftheuSuntildecadeslater.

these projections may be somewhat on the optimisticside because they take no account of the potentiallynegative impact of constraints in resources such asenergy, clean water supply and improved air quality.Without proper management of these fundamentals,economicgrowthwillarguablyfaileconomists’brightestexpectations.indeed,manychinesebusinessmenbelievethat environmental issues will ultimately prove to bechina’sachillesheel.

frompublisheddata,china’scumulativegdpgrowthovertheperiod1978to2002was814%.Extrapolatingthisdatausingvarioustriedandtestedeconomicmodelsproducesanaverageannualgrowthrateingdpofbetween6%and10%fortheperiod200�to2025.iftrue,thismeansthatby2025,china’seconomywillbeninetimesaslargeasitistoday.

manychinesebusinessmenbelievethatenvironmentalissueswillultimatelyproveto

bechina’sachillesheel.

thereare,however,lessoptimisticviewsoutthere.Someeconomists predict average annual gdp growth duringthe next ten years to be less than 5%, although thiscan probably be considered the worst-case scenario.these observers cite the accumulation of inventory andtransitionfromexport-orientedtodomesticconsumption-basedgrowthasthemainissuesforchinatosuccessfullymanage.

howevereventhepessimists,whilstpredictingaslowdownintheshortterm,stillconsider longertermprospectstobegood,dueprincipallytothecontinuedsupplyofcheaplabour and the existence and further development offirst-worldinfrastructuresuchastransportationandportfacilities.

StructureoftheEconomy

“China’s economy is not booming – the world economy is booming in China.”

foreignparticipationinthechineseeconomyisremarkablyhigh,despitethefactthatcommonwisdomwouldsuggestthat it has long been closed to foreign participation.considerthefollowingOEcdfigures,givingtheshareofthe three sectors in china’s economy, and ask yourselfhowtheywouldhavecomparedwithsimilaranalysesatthesamestagesofdevelopmentof,say,theJapaneseandkoreaneconomies:

Participation in PRC Economy

Sector 1998 2003 2005 (est)

State 47% �6% �1%

privatedomestic

�5% 42% 45%

foreign 18% 22% 24%

[itshouldhoweverberememberedthattaiwanandhongkong are considered foreign in this analysis and thatalmost half the foreign participation described wouldrelatetoinvestmentfromthesetwosources.]

foreigncompaniesoperatinginchinatodayproduce87%of the country’s high-tech exports and 60% of exportsoverall. Whereas in terms of industrial manufacturingforeign participation appears to have reached a plateau(duelargelytotheriseofprivatedomesticmanufacturing),foreign-producedexportsfromchinaarestillgrowinginabsolute terms. this suggests they must be movingupwardsintohigher-valueproductsandservices.

the above data also tell us that domestically there hasbeenareversalofthebalancebetweenstateandprivatesectorparticipationintheeconomy,whichhasresultedinincreasedproductivity.thereisstillhoweveranenormousamountofstate-ownedenterprisethatcouldbeprivatized,withconsequentimprovementsinefficiency.

China’s Economy – A Brief OverviewEOS RISQ UK – Kirk Austin

6Report

futuregrowthareasofthechineseEconomy“Willtheworldcontinuetoabsorbchina-madeproducts?”there is currently such a huge stockpile of unsold pRcmanufacturesthatarguablytheworldhasalreadyreachedsaturationpoint.

china’s mushrooming inventories, the product ofgovernment-sponsoredoverproductionaimedarguablyatbolsteringgdpatallcosts,areestimatedtorepresentone-quarterofgdpgrowthinrecentyears.theirdistribution“could cause one or two quarters of negative growth inthenearfuture,”accordingtooneeconomistrecently.

china'sfutureliesinthedevelopmentofnon-industrial,highervalueproductsandservices

suchashealthandmedical,technologydevelopmentandmoneymanagement.

all of this nonetheless belies a temptation for us tocontinuethinkingas ifweare living inthe19thcentury;whereas china’s future, even in the relatively mediumterm, almost certainly lies in the development of non-industrial, higher value products and services such ashealthandmedical,technologydevelopmentandmoneymanagement.

impactofchina’sgrowthontheWorldEconomy

china’sentry intotheglobaleconomyasamajorsourceof low-cost manufacturing is a continuing threat toother countries whose economies likewise rely uponindustrialmanufacturing. henceJapan,koreaandpartsofcontinentalEuropesuchasgermanyandfrancewillbeamongthosemostaffected.downglobally(theso-called‘chinaprice’)andthroughincreasingdemandpushesupthepriceofrawmaterials.

themoreservice-orientedeconomiessuchasuSandukare to some extent lessaffected bychina’s phenomenalgrowth. however, in the final analysis china may stillbe judged guilty of a global erosion of manufacturingprofitability.

thesecountriesfacea‘triplewhammy’aschinaimportslessoftheirproducts,pushesthepriceofmanufactures

for asian countries, many of which are raw-materialssuppliers,china’smoveintoexport-orientedmanufacturehasbeenbeneficial.infact,two-thirdsofchina’simportsare sourced from within asia and its growth has helped‘pullalong’asia’sdevelopingeconomiessuchasindonesiaandvietnam.

globalprofitWarning?

“China will drive a slowdown in global profits.”

China’s Share of World Manufacturing

1800 ��%

1950 <1%

2005 9%

20�0 20%?

china’s share of global manufacturing will, by someestimates, more than double in the next 25 years.Some economists believe that this growth is ‘virtuallyunstoppable’asapackageofthird-worldlabourcostsandfirst-world infrastructure combine to deliver unbeatablevaluetoglobalconsumers.

asever,therearealternativeviewsonhowchina’splaceintheworldeconomywilldevelopandnotallpredictsucharosyfuture.forexample,ifthechineseyen–orRenminbi– is allowed to find its own value, then some of china’scomparative advantage, such as cheap labour costs, willlikelybeeroded.inthewordsofoneeconomist:

“China’s competitive advantage arises because it is the cheapest place on earth to make things at the moment. The emerging platform companies are well-equipped to move their manufacturing at a stroke to the world’s latest, cheapest place…”

humanResources

there are many who believe that china’s continuedeconomic growth will be a function of ‘people

China’s ‘Triple Whammy’

Cause Effect Impact

domesticoversupplyofindustrialmanufactures

Reducedrequirementforforeignimports

foreignmanufacturersexportlessproducttochina

domesticmanufacturersseektoincreaseexportsaslocalconsumptionreachessaturation

globalpricespusheddownaschinesemanufacturesfloodmarket–theso-called‘chinaprice’

profitabilitydeclinesastheglobalmarkettriestocompetewithchineseproduct

growthindemandforrawmaterialstosupportincreasedexport-orientedproduction

priceofrawmaterialsincreases profitabilityfurtherdeclines

7volume 3

development’. the simple fact is that the huge numberofpeopleinthismostpopulousofnationshaslongbeenhypnotictooutsiders.

however, the population of china is aging rapidly:throughouttheworld,onlyJapanhasanolderpopulation.therapiddeclineinthebirthrateinchinaisnotsomethingthatwillbeeasytoreverse.

china’s population data, of which the year 2000 censuswould be the latest example, suggeststhat there are on average 17 millionnewbirthsperannum.however,recentministry of education data supports agrowing suspicion that there has beenarapiddeclineinthebirthrateinrecentyears.

trendsintheavailabledataalsosuggestthefollowing:

for the last ten years there have been, on average, an additional 8 million new workers entering the marketeachyear;

forthenexttenyears,onaverage,therewillbenonet growth;

china’s population will continue to grow until 2015, fromwhenitwillstabilizeandthendiminish;

itslabourforcewillbeindeclinefrom2009.

inshort, therefore, thesetrends indicatethatwithinthenext quarter century, the number of educated peopleentering the workforce will diminish, as will the size ofchina’slabourforceoverall.Withit,alargepartofchina’scomparativeadvantagewillbeeroded.

•

•

•

•

Summary–china’sgrowthWilldecelerate

Sowhatdoesthefuturehold?

“There are many things that cannot be imagined, but there is nothing that may not happen,” isperhapsanappropriatechinesesaying,forevenapanelofinformedeconomistswouldfinddifficultyagreeingonchina’slikelypositionintheworldeconomy20yearsfromnow.

but there are some common areas ofthinking:

economic growth will increasinglybedrivenbydomesticconsumptionand no longer rely almost entirelyuponexport-orientedinvestment;however, accumulation of

inventory(domesticoversupply)willpersist;there will be a tightening of money supply with

chinese companies having to adapt to a scenario wherebythecostofcapitalishigher;

chinawillcontinuetodrivedownglobalprofitability;china’s population and workforce will peak at some

pointbetween2009and2015,thendiminish;china’s growth will begin to decelerate, sometime

soon.

•

•

•

••

•

Withinthenextquartercentury,thenumberof

educatedpeopleenteringtheworkforcewilldiminish,as

willthesizeofchina’slabourforceoverall.

8Report

Effective 1 december 2005, the new legislation governsthe way in which domestic insurance companies mayreinsureandseekstorestrict theoutflowof reinsurancepremiums abroad. through this the chinese insuranceregulator, ciRc, aims to assist the development of thelocalreinsuranceindustry.

thenewrulesapplyequallytolocalchinesedirectwriters,Sino-foreignjointventuresandsubsidiariesandbranchesofforeigninsurancecompanies.allmodesofreinsurancebusiness fall within its scope, including facultativeplacementsandtreatyreinsurancearrangements.

newlegislationgovernsthewayinwhichdomesticinsurancecompaniesmayreinsure

andseekstorestricttheoutflowofreinsurancepremiumsabroad.

thesalientfeaturesofthenewlegislationareasfollows:

direct insurers are instructed to give priority tochina-domiciled reinsurers when entering intoreinsurancearrangements.at leasttwodomesticcompaniesmustbe invitedtoparticipateinanyreinsuranceoffering.atleast50%ofanyreinsuranceplacementshouldbeeffectedwithchina-domiciledreinsurers.

•

•

•

no more than 80% of any reinsurance placementmaybeeffectedwiththesamereinsurer.no more than 20% of any reinsurance placementmay be effected with a reinsurer that is affiliated tothecedant.

Whatthismeansforthechina-basedoperationsofclientsof the EOS RiSq network is that they will now haveless flexibility over the design and control of their riskfinancingarrangements.forexample,cessionstocaptiveinsurance companies through fronting agreements willhenceforth come under close scrutiny and may well berestricted. there may also be security (rating) issues,whichweareevaluating.

thepenaltiesfornon-compliancewiththenewdirectiveinclude, in extreme cases, withdrawal of licence andsuspensionofbusinessactivitiesandasaresultdomesticinsurers have initially indicated to EOS RiSq that theyintendtofullycomplywiththelegislation.

however, we have yet to see in practice how chineseinsurers will react in relation to their future handling ofglobal insuranceprogrammesandwillkeepournetworkpartners informed of developments in the comingmonths.

•

•

newinsurancebusinesslegislationhasrecentlybeenenactedinchinathathasimplicationsforclientsoftheEOSRiSqnetworkandotherpartnerbrokers.

Booming China

Impact of new Chinese Business Insurance LegislationEOS RISQ UK – Kirk Austin

9volume 3

How can the avian flu affect your business?

EOS RISQ Italy – Marketing and Communication Division

anavianflupandemiccouldleaveemployerswithdecimatedworkforcesandahostofinsurancecoveragequestions,whileinsurerscouldsufferbillionsofdollarsinlosses.thisisoneofthealarmingconclusionsofaninquiryofEOSRiSqitalyoninsuranceconsequencesofanavianflupandemic.

Whatisavianflu?

avian influenza, or “bird flu” is a contagious disease ofanimalscausedbyvirusesthatnormallyinfectonlybirdsand, less commonly, pigs. the most important controlmeasures of avian influenza are rapid destruction of allinfectedorexposedbirds.

particularlyalarming,intermsofrisksforhumanhealth,is the detection of a highly pathogenic strain, known as“h5n1”,asthecauseofmostoftheseoutbreaks.h5n1hasa unique capability to jump the species barrier, causingseveredisease,withhighmortality,inhumans.

avian and human influenza viruses can exchange geneswhen a person is simultaneously infected with virusesfrombothspecies.

anew ‘mixed’virus isdifferent fromeitherparentvirus,and humans may have no immunity to it. and if thenewviruscontainssufficienthumangenes,transmissiondirectly from one person to another (instead of frombirdstohumanonly)couldoccur.Whenthishappens,theconditionsofthestartofanewinfluenzapandemicwillhavebeenmet.

there were three influenza pandemics in the 20thcentury:

1918Spanishflu-20-40milliondeathsworldwide;1957asianflu-70,000deathsintheu.S.alone;1968hongkongflu-�4,000deathsintheu.S.alone.

both1957and1968pandemicviruseswerearesultofthere-assortmentofahumanvirus withan avian influenzavirus.theoriginofthe1918pandemicvirusisnotclear.

asreportedbyWorldhealthOrganisation(WhO),publichealthpreparednessactivitiesare:

officials from the WhO are working across asia to assist in establishing an extensive surveillance networktoprovideearlywarning;

fewerthan10countriesareworkingonvaccines;Roche has committed to give WhO three million

antiviraldrugdoses(tamiflu);2� countries have ordered drug stockpiles: delivery

willtakeuptoayear;abouthalfofallcountriesnowhaveaformalpandemic

controlplan.

•••

•

••

•

•

WhOactivitiesinEurope

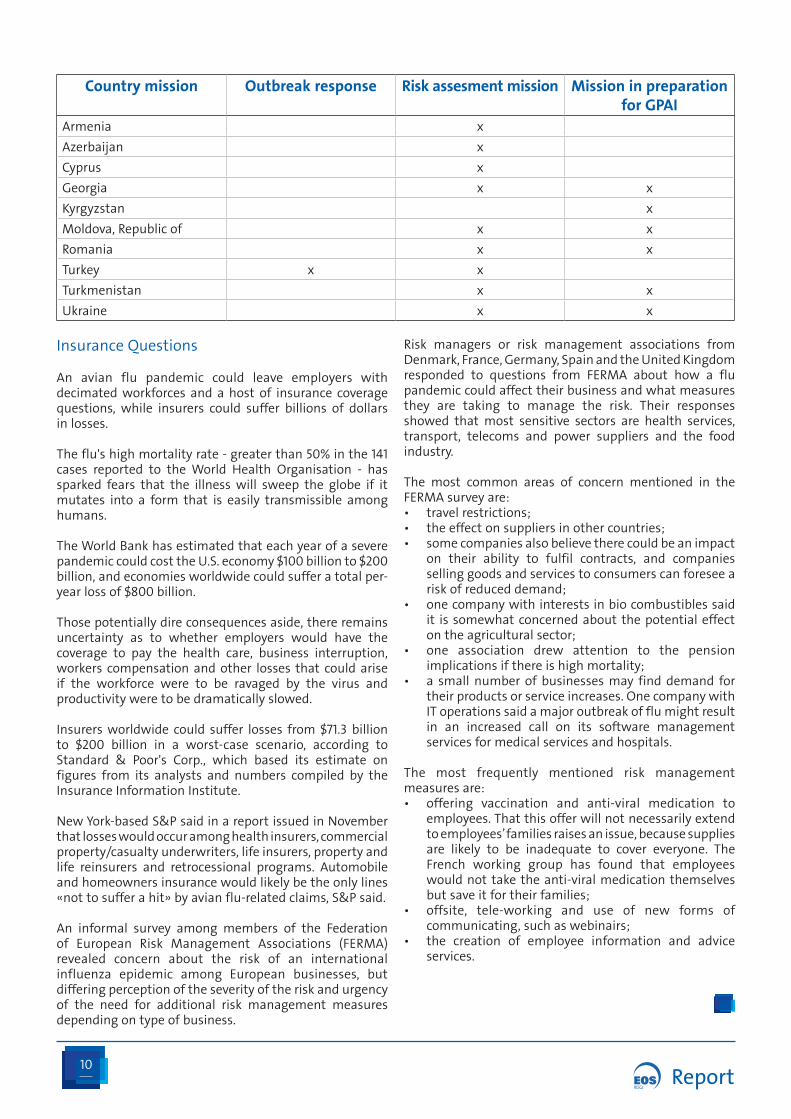

as of 4 march 2006, sixteen countries within the WhOEuropeanRegionhavereportedconfirmedcasesofavianinfluenza h5n1 in birds to the World Organisation foranimalhealth(OiE):austria,azerbaijan,bulgaria,croatia,france, germany, greece, hungary, italy, kazakhstan,Romania, Russia, Slovakia, Slovenia, turkey and ukraine.three European countries have reported avian influenzah5inbirdstotheOiE:bosniaandherzegovina,SerbiaandmontenegroandSwitzerland.

WhO experts are contributing to preparing integratedproject proposals for the global programme for avianinfluenza and human pandemic preparedness andResponse (gpai), which provides financial and technicalassistance to individual countries. gpai is funded bylines-of-credit from the World bank and is coordinatedwith many other partners, including uSaid, unicEf, OiEandthefoodandagricultureOrganisationoftheunitednations(faO).

anavianflupandemiccouldleaveemployerswithdecimatedworkforcesandahostof

insurancecoveragequestions,whileinsurerscouldsufferbillionsofdollarsinlosses.

WhO has collaborated with the European commission(Ec) and the European centre for disease preventionand control (Ecdc) to assess the national pandemicpreparedness plans in the following countries: france,greece, italy, kazakhstan, poland, the former yugoslavRepublic of macedonia, turkey, ukraine and unitedkingdom. missions to other European countries are alsobeingplanned.

all52memberStatesoftheWhOEuropeanRegionhavebeen invited to attend workshops to review nationalpandemicpreparednessplans,heldincollaborationwithEcandEcdc.thefirstpandemicinfluenzapreparednessplanning workshop took place in luxemburg in march2005, the second workshop in copenhagen, denmark,in October 2005, and the third workshop will be held inStockholm,Sweden,inmay2006.

10Report

Country mission Outbreak response Risk assesment mission Mission in preparation for GPAI

armenia x

azerbaijan x

cyprus x

georgia x x

kyrgyzstan x

moldova,Republicof x x

Romania x x

turkey x x

turkmenistan x x

ukraine x x

insurancequestions

an avian flu pandemic could leave employers withdecimated workforces and a host of insurance coveragequestions, while insurers could suffer billions of dollarsinlosses.

theflu'shighmortalityrate-greaterthan50%inthe141cases reported to the World health Organisation - hassparked fears that the illness will sweep the globe if itmutates into a form that is easily transmissible amonghumans.

theWorldbankhasestimatedthateachyearofaseverepandemiccouldcosttheu.S.economy$100billionto$200billion,andeconomiesworldwidecouldsufferatotalper-yearlossof$800billion.

thosepotentiallydireconsequencesaside,thereremainsuncertainty as to whether employers would have thecoverage to pay the health care, business interruption,workers compensation and other losses that could ariseif the workforce were to be ravaged by the virus andproductivityweretobedramaticallyslowed.

insurers worldwide could suffer losses from $71.� billionto $200 billion in a worst-case scenario, according toStandard & poor's corp., which based its estimate onfigures from its analysts and numbers compiled by theinsuranceinformationinstitute.

newyork-basedS&psaidinareportissuedinnovemberthatlosseswouldoccuramonghealthinsurers,commercialproperty/casualtyunderwriters,lifeinsurers,propertyandlife reinsurers and retrocessional programs. automobileandhomeownersinsurancewouldlikelybetheonlylines«nottosufferahit»byavianflu-relatedclaims,S&psaid.

an informal survey among members of the federationof European Risk management associations (fERma)revealed concern about the risk of an internationalinfluenza epidemic among European businesses, butdifferingperceptionoftheseverityoftheriskandurgencyof the need for additional risk management measuresdependingontypeofbusiness.

Risk managers or risk management associations fromdenmark,france,germany,Spainandtheunitedkingdomresponded to questions from fERma about how a flupandemiccouldaffecttheirbusinessandwhatmeasuresthey are taking to manage the risk. their responsesshowed that most sensitive sectors are health services,transport, telecoms and power suppliers and the foodindustry.

the most common areas of concern mentioned in thefERmasurveyare:

travelrestrictions;theeffectonsuppliersinothercountries;somecompaniesalsobelievetherecouldbeanimpact

on their ability to fulfil contracts, and companies sellinggoodsandservicestoconsumerscanforeseea riskofreduceddemand;

onecompanywithinterestsinbiocombustiblessaid it is somewhat concerned about the potential effect ontheagriculturalsector;

one association drew attention to the pension implicationsifthereishighmortality;

a small number of businesses may find demand for theirproductsorserviceincreases.Onecompanywith itoperationssaidamajoroutbreakofflumightresult in an increased call on its software management servicesformedicalservicesandhospitals.

the most frequently mentioned risk managementmeasuresare:

offering vaccination and anti-viral medication to employees.thatthisofferwillnotnecessarilyextend toemployees’familiesraisesanissue,becausesupplies are likely to be inadequate to cover everyone. the french working group has found that employees wouldnot take the anti-viral medication themselves butsaveitfortheirfamilies;

offsite, tele-working and use of new forms of communicating,suchaswebinairs;

the creation of employee information and advice services.

•••

•

•

•

•

•

•

11volume 3

EOS RISQ Belgium – Jan Van Hecke

havingrecoursetopublicorprivatesavingsinvolvesrisks.theEuropeanandbelgianinsurancemarkethasalreadycomeupwithsolutionsinthepast.fewpoliciesweretakenoutforvariousreasons.thischangedin2005whensupplyanddemandstartedtorise.theinsurancemarketwillbecomeafullydevelopedmarketforsuchrisksin2006.

EOSRiSqbelgiumhasalwaysfollowedthismarketcloselyandofferedinsurancesolutionswherepossible.forthisreason,wecannowanticipatecompanyneedsinamorefullydevelopedinsurancemarket.inthiscase,wemakeuseoftheexperienceofourpartnerswithintheEOSRiSqnetwork.

Prospectus Liability and Mergers & Acquisitions

1.havingrecoursetopublicsavings:prospectusliability-trends

for the first time since 2000, a major increase of initialpublicofferingsinEuropefor2004hasbeennoted.Withjust twoofferings,belgiumcamethird in2004after theukwith191offeringsandfrancewith24offerings.

the reason for this high ranking was the initial publicofferingofbelgacom,whichamountedto$4,�99million.thiswas4%oftheoverallcapitalattractedworldwideviainitial public Offerings, abbreviated as ipO. the trend ofthepreviousyearcontinuedin2005.

Overthepasttwoyears,Europeanandbelgian companies did not only haverecourse to public savings via an ipO.Wehavealsonoted(secondary)capitalincreases, debenture emissions andpublictake-overbids.

acontinuationoftrendsofthepasttwoyearsarepredictedfor2006.

1.1.Riskslinkedtohavingrecoursetopublicsavings

thelegalbasisoftheserisks liesmainly inthelawof22april200�.thislawconcernsthepublicofferofsecurities.this law is not limited to the public offering of shares,including ipO and (secondary) capital increase, but alsofocuses on the public issue of debentures, real estatecertificates, interest instalment contracts, interest andcurrencyswaps,rightuptothepublictake-overbid.

accordingtothelawof22april200�,applyingaEuropeandirective to belgian legislation, a public offer of stocksmayonlybemadeafteraprospectushasbeenpublishedthat has been approved by the cbfa (belgian financialbankingandinsurancecommission).theprospectusmust

include data of the public needs to take considereddecisions regarding the investment offer. it must alsoincludethenamesofthoseresponsibleforthecontentoftheprospectus,usuallymanagers.theyarejointlyobligedto rectify any disadvantage that may be the immediateanddirectconsequenceofthelackoforinaccuratenatureof statements in the prospectus, its supplements orupdates.

in addition, the law states that the issuer, the bidderand the intermediary are always jointly liable for thecontent of the prospectus, as well as for reports, meansof advertising or other documents relating to the publicoffer. this can be, for example, press announcements

androadshowsaccompanyingthepublic offer and the issue of theprospectus.

the issuer is the company whosestocks are the subject of a publicoffer.thebidderisthepersonwho

makes a public bid, as with a public take-over bid. theintermediary is the financial institute that guides theissuerorbidder.

apartfromthelawof22april200�othersectionsofthelaw,onwhosebasisapersoncanbeheldliable,continuetoapply.thisincludescompanylegislationandcivilcodearticles on whose basis managers and companies canbe held liable. if managers are not mentioned in theprospectusthisdoesnotmeanthattheyareintheclear.

1.2.insurancefacilities

the insurance facility we can offer depends on thecoverageyouareseekingandontheextentandnatureofthepublicbid.doyouwishtoonly insurethemanagersor should the company (issuer/bidder) also be includedin the coverage? What about protection for the benefitof the intermediary? an ipO with limited capital needsa different insurance solution than an ipO with a largecapital,adebentureemissionoranOpa.

theinsurancefacilitywecanofferdependsonthecoverageyouare

seekingandontheextentandnatureofthepublicbid.

12Report

the insurance solution consists of either an extension ofthe existing policy manager liability or a separate policythatonlycoverstherisksofthepublicbid.aseparatepolicyonlygrantsyouadepositfortheserisks.Suchpoliciesareusuallytakenoutforaperiodofthreetofiveyears.

2.havingrecoursetoprivatecapital:mergersandacquisitions(m&a)-trends

mergers and acquisitions remain numerous. 2005 was agood year for mergers and acquisitions. 2006 promisesmore of the same. these days, many private equitycompanies and venture capitalists want to buy and sell.the insurance world is responding to these increasedactivities.

We note that both sellers and buyers are currentlyinterested inan insurancesolution for the risks involvedin an m&a deal. in turn, insurers respond with flexibleunderwritingandfeasible(premium)conditions.however,theminimumpremiumsremainconsiderable,soinsurancepoliciestakenouttodayaremoreaboutm&adealswitha high transaction value. the European m&a insurancemarketwillbeafactfromthisyearon.

2.1.Risksrelatedtohavingrecoursetoprivatecapital

in a private take-over bid, the seller has recourse to theprivate capital of the buyer. in a private merger, bothpartiesaresellerandbuyer.asthesecasesdonotconcern“usingpublicsavings”,thelawof2�april200�doesnotapply. this entails no prospectus or prospectus liability.however,thebuyerwantstobeinformedaboutwhathebuys,justlikethegeneralpublic.

this is why a company that wishes to sell one of itsbranches writes a memorandum that includes data thepotentialbuyerneedstomakeapurchasingdecision.

the memorandum can be compared to the brochure.the layout and the issue of the memorandum are doneinthedisclosurephase.adataroomistheninstalledona regular basis. here candidate buyers can consult evenmoredata.thisphaseiscalledthe“buyersduediligence”.thedisclosurephaseandthebuyerduediligenceresultsina“Sharepurchaseagreement”,abbreviatedasSpa.

thisagreementbetweenthesellerandthe(prospective)buyer mentions several securities, known as warrantiesandindemnities.

Someexamples:the sellerdeclares that hewillpay theunpaidsocial

securitydebt;thesellerdeclaresthatthependingdamageclaimwill

never amount to more than 10,000 EuR for the company.

•

•

When these warranties and indemnities are taken up,thisentailsariskfortheseller.hemustcompensate.thebuyer also runs the risk if the seller cannot or will notcompensate.

amuch-usedsolutionistheuseofan“escrowaccount”;thebuyerblocksasumonanaccountthatisusedeverytimewarrantiesandindemnitiesaretakenup.

both the seller and the buyer are increasingly on thelookoutforinsurancesolutionsforthefollowingreasons:

the seller wishes to give as few guarantees aspossible, while the buyer would benefit from highguarantees. the difference can be bridged by aninsurance contract. for example, if the seller wantsto provide securities up to 1,000,000 EuR, while thebuyer wants to increase this amount to 11,000,000EuR.theinsurancepolicytheninsuresthedifferenceof10,000,000EuR;the seller recently bought the company he wants to

sell, which makes it almost impossible for him to provide the requested securities. the insurance contract can again take over the value of the securities;

the seller cannot block a large sum of money on an account for a longer period for financial reasons. here the insurancecontractcanbeanalternative to the“escrowaccount”;

if the seller falls under a different jurisdiction than the buyer, this can result in uncertainties regarding the value of set warranties and indemnities. What is the value of warranties underwritten by a seller fromRussiawhowishestosellaRomanianbranchto a belgian company? an insurance policy may solve thisproblem;

the prospective buyer wants to distinguish himself fromhiscompetitors.hedoesnotrequestwarranties or indemnities from the seller, who is covered by an“escrowaccount”.hehascoveredthisviahisown insurancepolicy.

thesuccessoftheinsurancecontractnotonlydependsonthepricetagandthe

coverage,butalsoonthespeedandflexibilityofunderwriting.

2.2.insurancefacilities

thesuccessoftheinsurancecontractnotonlydependsonthepricetagandthecoverage,butalsoonthespeedandflexibilityofunderwriting.thisriskanalysisbytheinsurercan run smoothly and quickly through our mediation.as soon as we receive a memorandum, we organisea conference call with the insurers and the client. anindicativeofferfollowswithintwoworkingdaysthatcanbe adjusted in the light of new additional information.however, in practice the indicative offer usually remains

•

•

•

•

•

1�volume 3

the same. if changes need to be made to the first offer,theyareusuallytotheadvantageoftheclient.

boththesellerandthebuyercanunderwritethepolicy.

ifthesellerunderwritesthepolicy,thenitcoversliabilityresulting from given warranties and indemnities in theSpa. it then concerns liability insurance which excludesdeliberate action by the seller and excludes errorscommited by the seller of which he should have beenaware on the day the policy was signed. in professionaljargon, this second major exclusion is called “priorknowledgeexclusion”.if the seller underwrites the policy, then this does notcover liability insurance.thisentailsnodeliberateactionexclusionbytheselleror“priorknowledgeexclusion”.thispolicy ismoreexpensive,butcoversa lotmorethantheabove-mentionedliabilityinsurance.

Weusuallystartnegotiationsaboutaninsurancesolutionwiththeseller,as the layoutstageof thememorandumoftendoesnotconcernabuyer.Oncethebuyerisknown,furthernegotiationsoftentakeplacewiththebuyerwhothentakesoutthepolicy.

14Report

EOS RISQ opens country office in the Russian Federation – Interview with General Manager Gleb Lobanov on the current Russian insurance market

the opening of the moscow office enables EOS RiSq toprovide an expanded level of service to both Russia andthefSu.thenewoffice,whichhasstaffdedicatedsolelyto operations in the Russian federation, will strengthenEOSRiSq’spositions incentralandEasternEurope (cEE)andfSu.

Shavkat mingaliev, Regional manager for cEE and ciSnoted,"thecountryofficewillimprovetheresponsivenessof our Russian operations and strengthen our clientorientationbyestablishingastreamlinedandcoordinatedteam of insurance specialists in Russia. Establishing apermanent presence in the region will provide us withgreatercontroloverboththeglobalandlocaldeliveryofourservices."

"thecountryofficewillimprovetheresponsivenessofourRussianoperationsandstrengthenourclientorientationby

establishingastreamlinedandcoordinatedteamofinsurancespecialistsinRussia."

EOS RiSq is, and has been, involved in a wide rangeof projects across fSu, from providing western firmswith locally admitted insurance solutions to offeringreinsurance and risk management services to a largenumber of Russian insurance companies and otherclients.

EOS RiSq <s team in Russia will be headed up by gleblobanov. mr. lobanov has over 12 years experience ininsurancebrokingandriskmanagementandranksasoneof the Russian insurance broking industry's preeminentleadersintheEnergyandindustrysectors.

Mr. Lobanov, as you are in the insurance business for over 12 years now, can you please give us an update on the Russian insurance market?

Recently there have been changes to the insurance lawwhich will be fully implemented by 2007. the law hasintroduced new, higher capital requirements for bothlocalandforeigninsurers.Wecouldexpectthenumberofcompaniestobereducedheavilyasaresultofit.

toughatpresentthenumberoflocalinsurersisveryhigh(a few hundreds), in reality we have about 20 seriousplayers in the market who are buying very substantialreinsurance treaty protection from western companies.local capacity of property treaties is about half a billionuSdon probablemaximumlossbasisandthisamountkeepsgrowingasmorecompaniesarebecomingpreparedto increase their limits. here i would name ingosstrakh($150mln),Sogaz($100mln)–captiveofgazprom,Rosno($75mln). in marine, theRussianmarketcanonlycoversumsupto$100mln.

figures produced by the ministry of finance in 2005suggestthereal insurancemarket isarounduSd115mningrosspremiumsforlife,uSd�.6�bningrosspremiumsfornon-life.

a legal requirement to have motor third party liabilityinsurance was introduced as of 1 July 200� and becamefullycompulsoryasof1January2004.

How is the Russian insurance market regulated?

until2004underexistinglegislationinsurancecompaniescould be composite, that is they could transact bothlife and non-life insurances. changes to the law in

EOS RISQ Austria – Walter Schenk, Shavkat Mingaliev and Petra Steininger

EOS RiSq, Europe’s leading provider of insurance broking and risk management services, has officiallyopenedanewRussiancompanyinmoscow-ZaO“EOSRiSqciS”toconsolidateadecadeofservingclientsintheRussianfederationandtotakeadvantageofthegrowingmarketfortheinsurancesectorinthatcountry,andtherestoftheformerSovietunion(fSu).EOSRiSq’steaminRussiawillbeheadedupbygleblobanov,whohasover12yearsexperienceininsurancebrokingandriskmanagement.aninterviewwithoneoftheRussianinsurancebrokingindustry'spreeminentleadersintheEnergyandindustrysectors.

15volume 3

2004 introduced a separation between life and non-lifeinsurance, and insurers have until July 2007 to comply.life insurers are able to offer personal accident andmedicalexpensesinsurances,whichareregardedasnon-lifeclasses,inadditiontolifeproducts.allinsurershavetobelicensedforeachclassofinsurancetransacted,butforreinsuranceonlyasinglelicenseisneeded.

the statutory insurance supervisory authority in Russiais the federal agency for insurance Supervision (fSSn)knownasRosstrakhnadzor.Rosstrakhnadzor’sstatuswasupgraded in 2004 and it is no longer a department oftheministryoffinance,butanindependentgovernmentbody.

What are the current solvency margins applicable to insurers operating in the Russian market?

the solvency margin is established through a set ratioof assets and liabilities, with the company required tocomparetheactualratiooffreeassetstoliabilitiestotheratio laid down by Rosstrakhnadzor, but the principlesfollowEustandards.

companiesareobligedtoformpremiumandoutstandingclaims reserves and should create ibnR reserves ifnecessary.companiesmayalsoformanequalisationfundtocoverfluctuationsinresults.

Reinsurers’ share in the premium reserves of Russianinsurers is limited and the percentages changed in thesecond half of 2005 to a maximum of 25% each ratedReinsurer(regardlessofwhetherlocalorforeign)and15%foralocal,unratedcompany.althoughtheseregulationsprovokedanadversereactionwhenfirstintroduced,theyare understood not to cause any undue difficulties tocompaniesoperatinginthemarket.

Rosstrakhnadzor has the authority to order remedialaction in the event of the law being breached and thesuspension,restrictionorultimaterevocationoflicenses,ifnecessary. ifan insurer repeatedly infringes insurancelegislation, Rosstrakhnadzor has the power to bringit before the courts and also to instigate liquidationproceedingsagainstunlicensedinsurers.Otherwise,thereisnospecialinsolvencysystem.

What international insurers are present on the market?there are five international insurers present at themoment:

allianz – 100% subsidiary of allianz ag, germany. Registered in Russia in 1990 and offers industrial, Engineering,marineinsurance;

aig-aigRussia insurancecompanywas licensedtooperate in 1994 with headquarters in moscow. in1997 aig Russia insurance company received its life

•

•

insurance license and opened its life division inmoscow. as a result of the amendments to theinsurance law about composite companies, therewas a spilt into two companies: specialist generalinsurance company - aig insurance and Reinsurancecompany(whollyownedsubsidiaryofaigEurope,S.a.)andaigRussia(life,accidentandpension).Zurich–100%subsidiaryofZurichfinancialServices.

Registeredin1992;ERgO–operatesaspartofERgOgroupsince2002;acE – was set up in October 2004 to providecommercial property & casualty insurance servicesin Russia. the company’s insurance and reinsurancelicense for 15 product lines was received in march2005. the 100% shareholder of the company is acEEuropeanmarketsinsuranceltd.

We experienced in other CEE countries that many companies very often stick to the former monopoly insurer and do not use their competitors. What is the situation in the Russian Federation?the situation is not the same. two former monopolyinsurers Rosgosstrakh and ingosstrakh have been soldto different industrial companies and though theyremained market insurers their names are connected totheowners.

What is the common standard for insurance - book value or replacement cost value?dependingonspecificprovisionsoftheinsurancecontract,the property appraisal methods used, the actual value ofproperty at the moment of conclusion of the insurancecontractmaycorrespondto:

fullreplacementvalue;book(depreciated)value;thesalesvalue.

common standard is full replacement value, thoughotherscanbeappliedalso.

What are the most important issues for an international investor when it comes to their insurance needs when entering Russia?

these are the points which may differentiate RussianenvironmentfromWesternapproaches.

Only admitted insurance companies are allowed toinsureRussianrisks.despitetheexistenceofaconsumers’lawandrightsanddutiesclearlysetoutinthecivilcode,litigiousnessisverylowandgeneralthirdpartyliability insuranceisthereforeoneoftheweakestclassesinthemarket.a certain group of activities are defined as beingparticularly dangerous and those carrying out theseactivitiesarestrictlyliableforanydamagetheycauseaccordingtotheindustrialSafetylawpassedin1997.

•

••

•••

•

•

16Report

this also provides for the compulsory third partyliability insurance of enterprises involved in thesehazardousactivities(whichincludeoperatingalift).the civil code places a duty on employers toindemnify employees who are injured as a resultof an employer’s negligence and, as compensationpayable to an injured employee is not necessarilylimitedtopaymentsfromtheSocial insurancefund,this means that employers could have a greatertheoreticalexposurethantheyrealise.atthepresenttime,asstatebenefitsareconsideredtobesufficientlyhigh,courtsarethoughtunlikelytoinsistonanyextracompensationfromtheemployer.Employers’liabilityinsurance (El) is available but for the above reasonsverylittleisactuallybought.Whenitis,itisboughtbyforeign and joint venture companies which are usedtobuyingthiscoverelsewhere.

What do you expect from the Russian insurance market in the future?

We have a few types of insurance which have growthpotential. it is long term life insurance inclusive withinvestment program (as an alternative to differentforms of investments), motor insurance, various typesof liabilities ,mediumsizeandsmallbusiness.Economicgrowthandstrongcompetitionwilldefinitelysupportthegrowth of property and liability insurance of companiesincreasing the demand of industrial, construction andtradingenterprisesforinsurance.

•

alsotherecouldbearise inproperty insurance;aboominconstruction,mortgagedevelopmentandlivingqualityimprovementwillbepromotingthistrend.

Oneofthemostprospectivegrowthsectorsispiinsurance.Withthedevelopmentoflitigationwewillfacemoresuitsfordamagescompensationforfaultygoodsandservices.pi of auditors, bookkeepers, valuers, doctors, lawyers,brokers,builderswillbedevelopingveryfast.

contactdetails

gleblobanovdirectorgeneralEOSRiSqc.i.S.

12krasnopresnenskayaEmbankment,Worldtradecenter,office1101,moscow,Russianfederation,12�610

tel/fax:+74952581205mobile:+7495768�845E-mail:[email protected]

17volume 3

European sprinkler regulation: rules and norms

EOS RISQ France – Gilles Lefrand and Guy Massart

On 16 march 2006, EOS RiSq france (diOt) organised a debate on European sprinkler regulations in theprestigiouslutetiapalace (paris).this debate, conductedbychantaldelverdier,director ofdiOtpropertydepartment, gathered Risk managers, loss control Officers, directors of insurances, etc. of the localmarket.

considering all sprinkler standards which appeared few years ago, it seemed interesting to draw up acomparison. during the first part of the debate, gilles lefrand and guy massart, diOt loss preventionEngineers,compareddifferentsprinklerregulationsandstandardsincludingthenewEuropeannormn°En12845(alsoknownasfrenchreference.nfEn12845).

Sprinklerrulesandnorms

availableregulations,rulesandstandardscanbesummedupasfollows:

theycanalsobedistinguishedasfollows:

infrance:the french rule R1 apSad (assemblée pleinière des

Sociétés d’assurances dommages), last edition in October200�,ongoingadjustments;

theEuropeanrulenfEn12845(december2004);theamericanstandardsnfpa(nationalfireprotection

association);private standards: factory mutual, motor and

aeronauticmanufacturers;livedatatestsachievedbyindustrials(storageoftires,

storageofcasessprays…).

in france, all these regulations are recognised.the mostfrequentlyusedistheinsuranceruleR1fromtheapSad.

however, the new European norm En 12845 shouldchange the habits as it is going to become the requiredreference forpublicpremises (shoppingmalls, centresofexhibition…).

•

••

•

•

inEurope:the European insurance committee rules (cEa 4001

–edition200�)and/ornationalinsurancerules(vaS, lpc,Sbf…),conceivedinthesamewayastheEn12845 norm,butwithinsurancespecificities(choiceofwater sourcesforinstance…).

Whydospecificinsuranceregulationsexistforsprinklerinstallations?

the insurancerules forsprinkler installationsarethe oldest(1898fortheruleR1apSad);

the constant evolution of sprinkler systems and the change in risks has forced the construction of a commonbase;

theintegrationofspecialsprinklers(EarlySuppression fastResponse-ESfR,largedrop…);

rules are thoroughly investigated by third parties (vdS,anpi,cnpp…) to interpretparticularcasesand tovalidateconformity;

rulesdonotpertaintotheinstallationofthesystems, buttheyadvisetoenrolinaglobalsystemwith:

acertificationoftheinstallers;criteriaforthedefinitionofthewatersources;afollow-upintimebyperiodiccontrol;maintenance criteria and a life span of the

system.

Whatarethecommonpointsandthetechnicalparticularities?

theprinciplesaresimilarwithregardstotheregulationoftheactivitiesandtheproducts;the next edition of the rule cEa 4001 (1st quarter

2006) will introduce an important evolution (aggravation) of the regulation of the activities and theproducts;

thenormnfEn12845remainedgloballydemanding intermsofregulationofactivitiesandgoods.asimilar

•

•

•

•

•

•

••••

•

•

•

Europe

France

International

R1apSad nfEn12845

nationalrules

En12845 cEa4001

nfpa dataSheetfm

18Report

evolution to the cEa’s is foreseen subsequently.this normdoesnotintegratethenewtechnologies(ESfR);

for the regulation of the given risk, all rules and European norms give a same density and a same demandarea.

Wehavecompareddifferentmainstandardsfordifferentbusinessstreams,dependingonthe:

density;demandarea;flowrateofthefirepump;autonomyofthewatersources.

actually, for ‘classic’ activities, there are not a lot ofdifferencesbetweenallthestandards.thedifferencesaremoremeaningfulinindustrialactivities.

conclusion

industrials have a variety of standards at their disposaland, in agreement with their insurers, can choose themostsuitabletomeettheoptimalsecuritylevelfortheiractivities.

at a European level, the forthcoming regulations willenableaharmonisationofallcurrentinstallationrules.

Oneofthemostimportantissuesregardingthesprinklersysteminstallationisthequestionconcerningtheperiodicrevision. On one hand, the European regulations are notsufficientlyclearonthis topic.Ontheotherhand,a few

•

••••

national regulations are very demanding, such as the R1ruleoftheapSad.

EOS RiSq france suggests the ‘progressive steps’developedforthisperiodicreviewofthecurrentsprinklerinstallations. this action, including the latest Europeanregulations, is essentially based on an actual analysiswhichwillalsointegratetheuseofnewtechnologiessuchasendoscopiesandultrasonicsounds.

the goal is to ensure durability for the good operationof the installations, working closely with insurers onan objective and technical argumentation, to achievesubstantialsavingsbyminimizingtherepairworks.

contactdetails

chantaldElvERdiER,[email protected]:(��)144796204

gilleslEfRand,[email protected]:(��)144796267

guymaSSaRt,lpEngineer–[email protected]:(��)144796261

global vision, local precision

Europe's leading insurance broking and risk management

consultancy, providing practical solutions for our clients.

Offering know-how and expertise, together with quick,

personal and flexible service.

Check www.eosrisq.com for your local EOS RISQ office.