Embed Size (px)

DESCRIPTION

Brief presentation and illustrative description on the prospects of oil palm plantation in Indonesia. Sustainability standards become an integral part in this growing industry.

Citation preview

INDONESIA’S PALM OIL OUTLOOK2011-2020

Suhardiyoto HaryadiSuhardiyoto Haryadi

INDONESIA’S PALM OIL OUTLOOK 2011-2020

12/6/2010Inonesia's Palm Oil Outlook 2011-20202

Edible Oil Market 3 Rising Global Demand 4 Indonesia’s Production 5 Indonesia Takes the Lead 6 World Supply and Demand 7 World Trade 8 Commodity Boom 9 Indonesia’s Major-

Producers 10

Corporate Performance 11 Indonesia’s 20 Richest 12 Promising Global-

Economy 13 Price Projection 2011-2020 14 Expansion Areas 15 Controversy and Solution 16 Conclusion: Sustainable

Palm Oil 17

TABLE OF CONTENTS

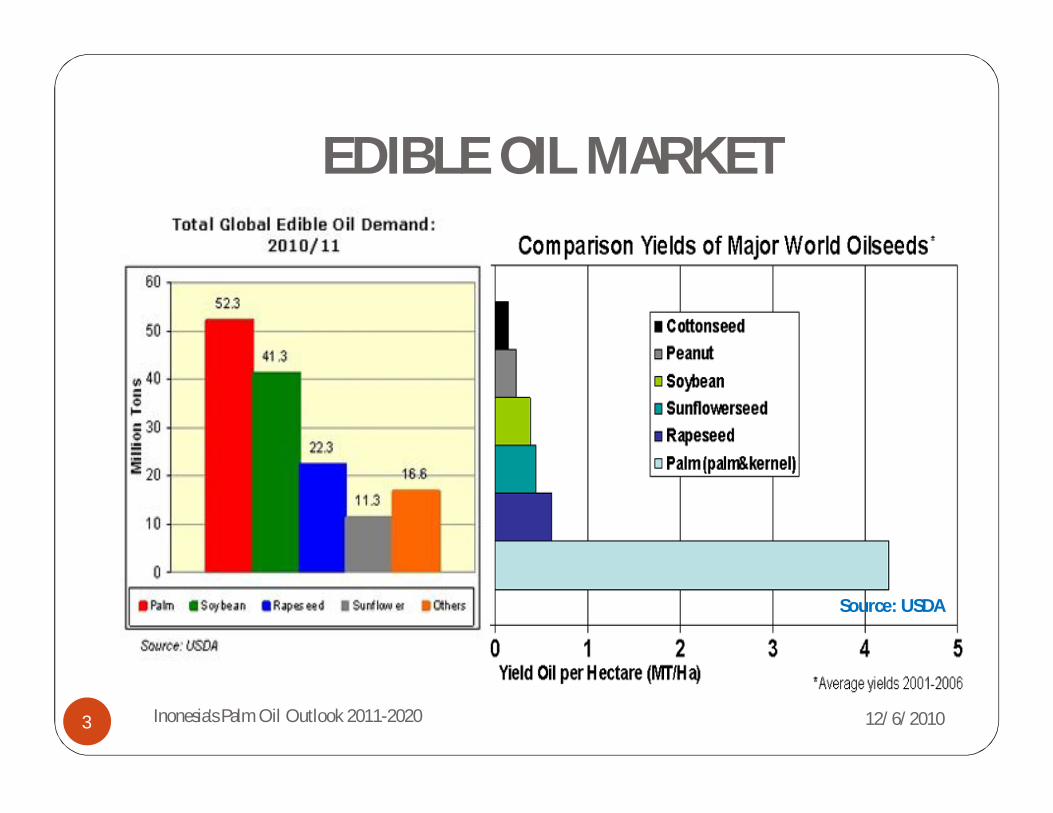

EDIBLE OIL MARKET

12/6/2010

Source: USDA

3 Inonesia's Palm Oil Outlook 2011-2020

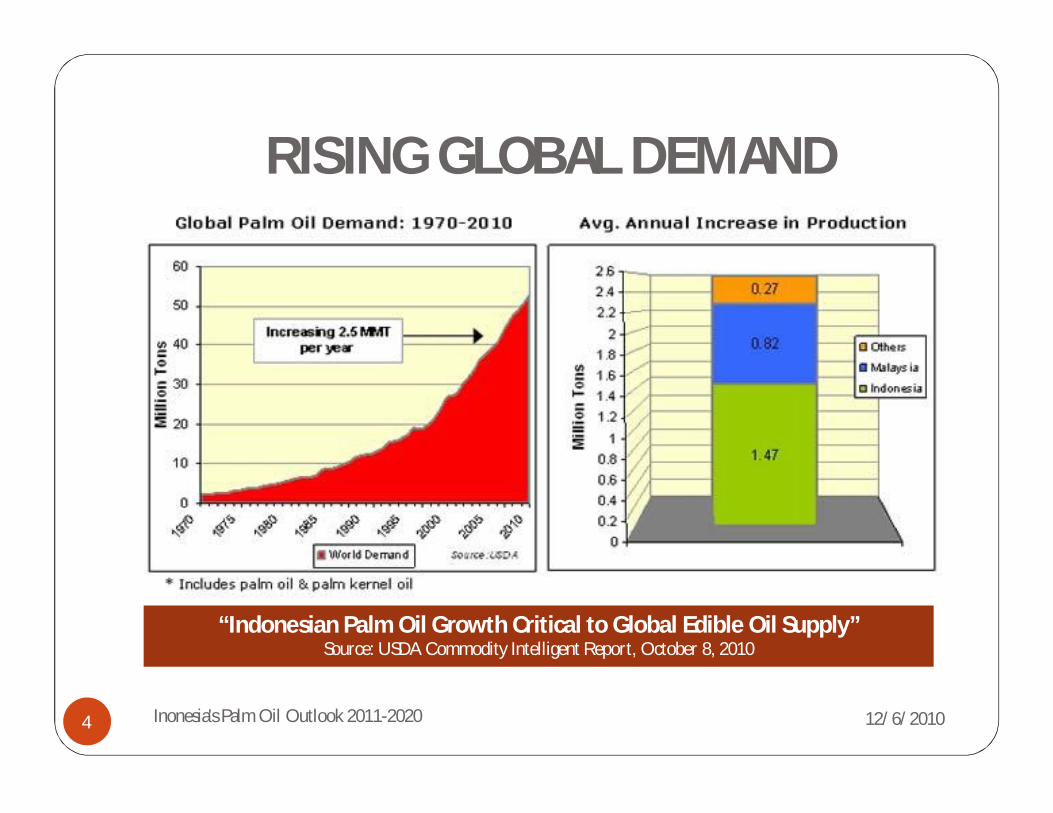

RISING GLOBAL DEMAND

12/6/2010

“Indonesian Palm Oil Growth Critical to Global Edible Oil Supply”Source: USDA Commodity Intelligent Report, October 8, 2010

4 Inonesia's Palm Oil Outlook 2011-2020

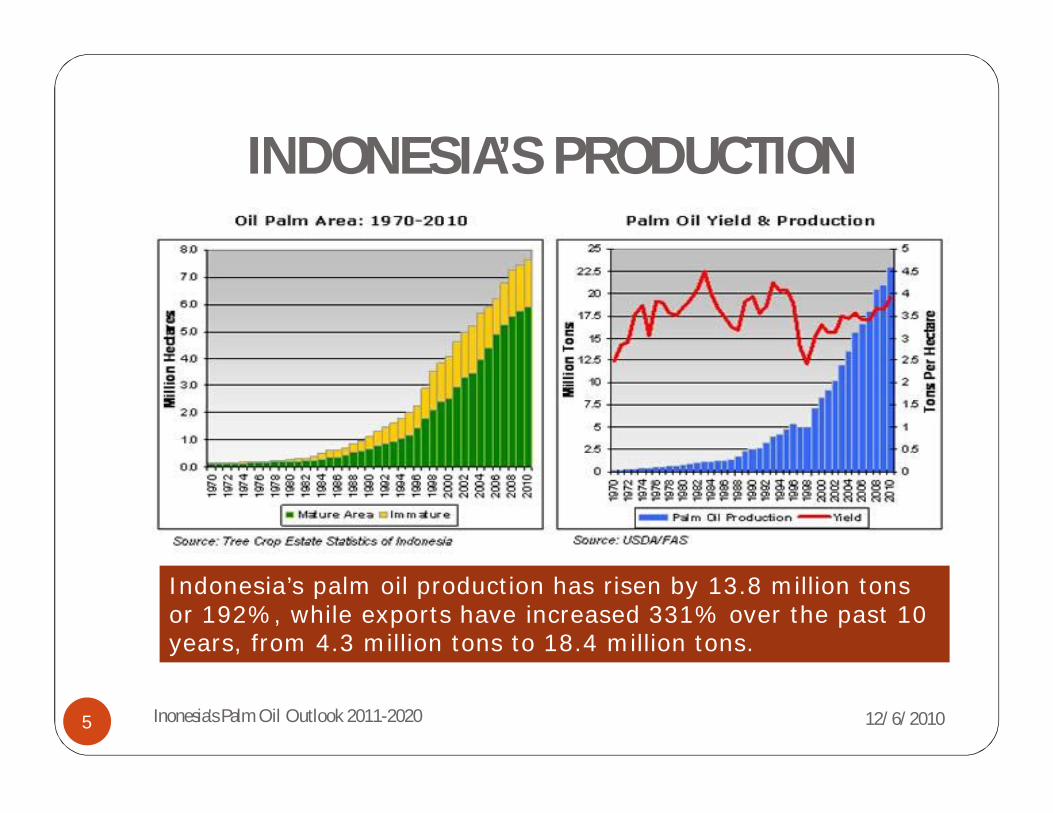

INDONESIA’S PRODUCTION

12/6/2010

Indonesia’s palm oil production has risen by 13.8 million tons or 192%, while exports have increased 331% over the past 10 years, from 4.3 million tons to 18.4 million tons.

5 Inonesia's Palm Oil Outlook 2011-2020

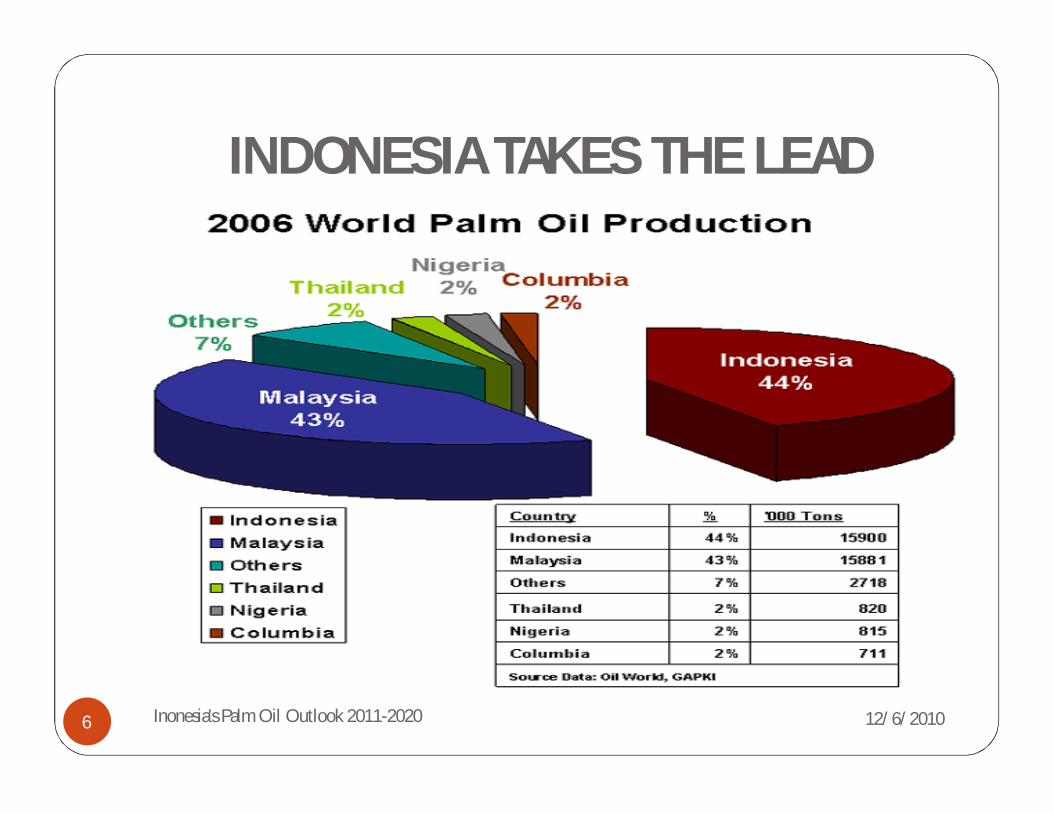

INDONESIA TAKES THE LEAD

12/6/20106 Inonesia's Palm Oil Outlook 2011-2020

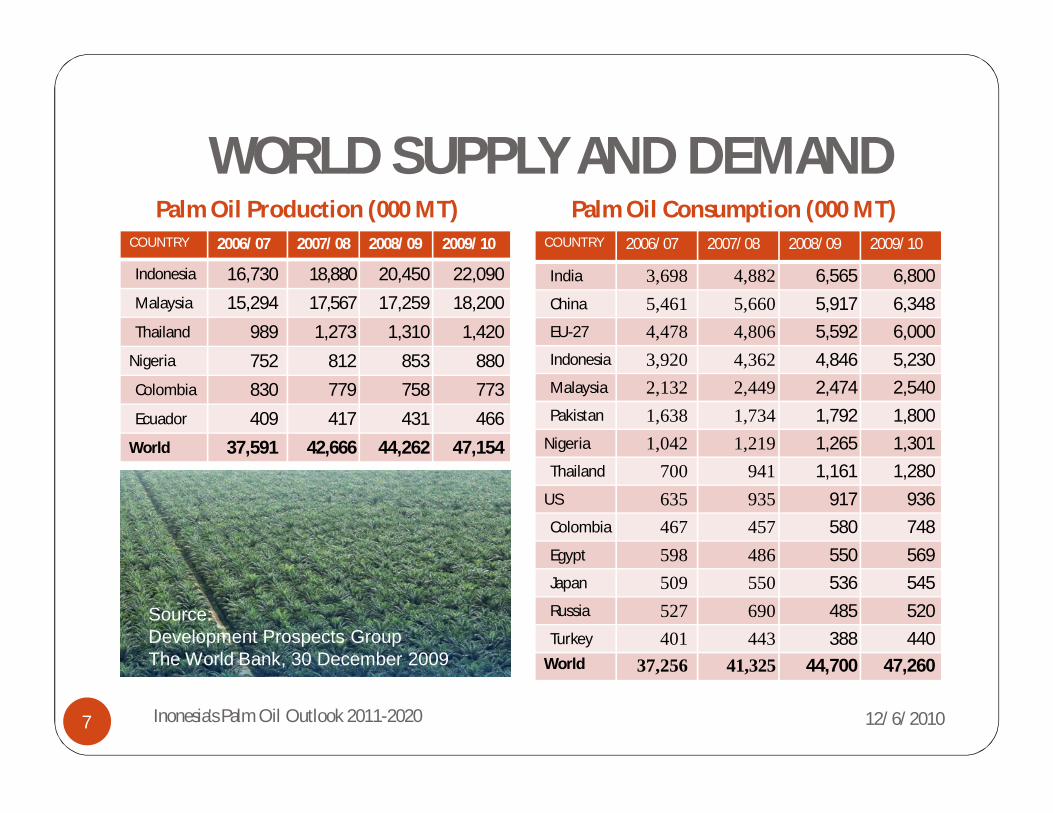

WORLD SUPPLY AND DEMANDPalm Oil Production (000 MT) Palm Oil Consumption (000 MT)

12/6/2010

COUNTRY 2006/07 2007/08 2008/09 2009/10

Indonesia 16,730 18,880 20,450 22,090

Malaysia 15,294 17,567 17,259 18,200

Thailand 989 1,273 1,310 1,420

Nigeria 752 812 853 880

Colombia 830 779 758 773

Ecuador 409 417 431 466

World 37,591 42,666 44,262 47,154

COUNTRY 2006/07 2007/08 2008/09 2009/10

India 3,698 4,882 6,565 6,800

China 5,461 5,660 5,917 6,348

EU-27 4,478 4,806 5,592 6,000

Indonesia 3,920 4,362 4,846 5,230

Malaysia 2,132 2,449 2,474 2,540

Pakistan 1,638 1,734 1,792 1,800

Nigeria 1,042 1,219 1,265 1,301

Thailand 700 941 1,161 1,280

US 635 935 917 936

Colombia 467 457 580 748

Egypt 598 486 550 569

Japan 509 550 536 545

Russia 527 690 485 520

Turkey 401 443 388 440World 37,256 41,325 44,700 47,260

Source: Development Prospects Group The World Bank, 30 December 2009

7 Inonesia's Palm Oil Outlook 2011-2020

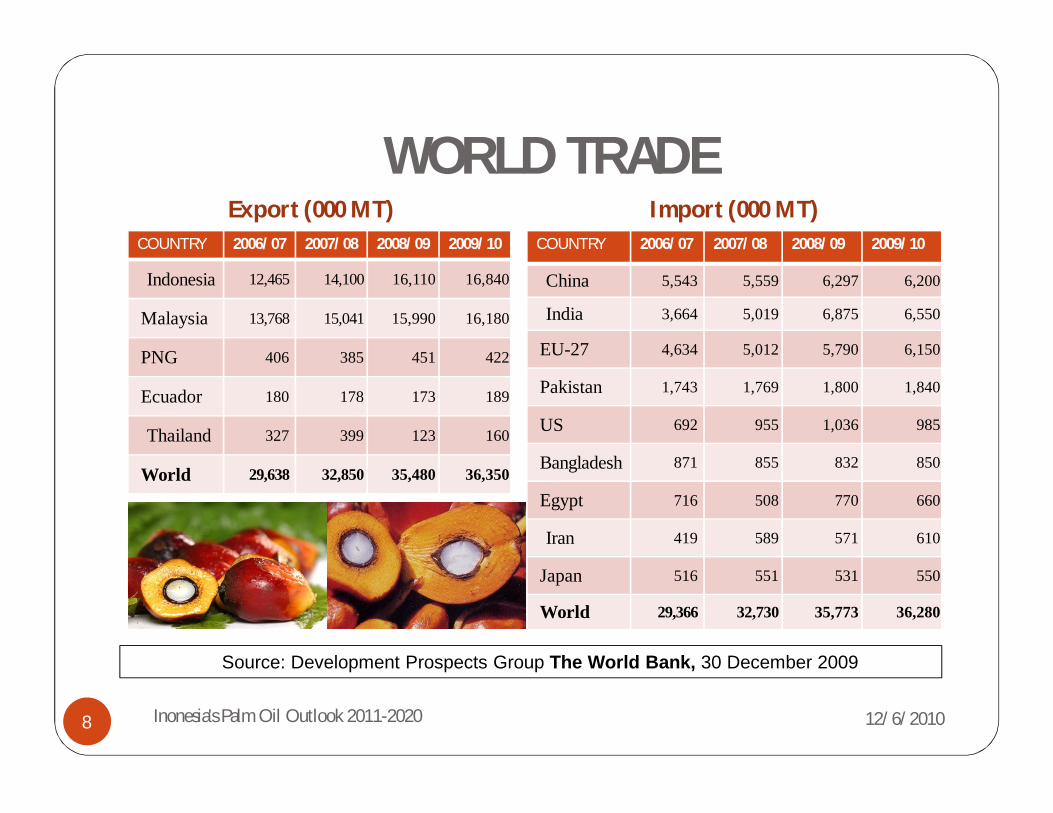

WORLD TRADEExport (000 MT) Import (000 MT)

12/6/2010

COUNTRY 2006/07 2007/08 2008/09 2009/10

Indonesia 12,465 14,100 16,110 16,840

Malaysia 13,768 15,041 15,990 16,180

PNG 406 385 451 422

Ecuador 180 178 173 189

Thailand 327 399 123 160

World 29,638 32,850 35,480 36,350

COUNTRY 2006/07 2007/08 2008/09 2009/10

China 5,543 5,559 6,297 6,200

India 3,664 5,019 6,875 6,550

EU-27 4,634 5,012 5,790 6,150

Pakistan 1,743 1,769 1,800 1,840

US 692 955 1,036 985

Bangladesh 871 855 832 850

Egypt 716 508 770 660

Iran 419 589 571 610

Japan 516 551 531 550

World 29,366 32,730 35,773 36,280

Source: Development Prospects Group The World Bank, 30 December 2009

8 Inonesia's Palm Oil Outlook 2011-2020

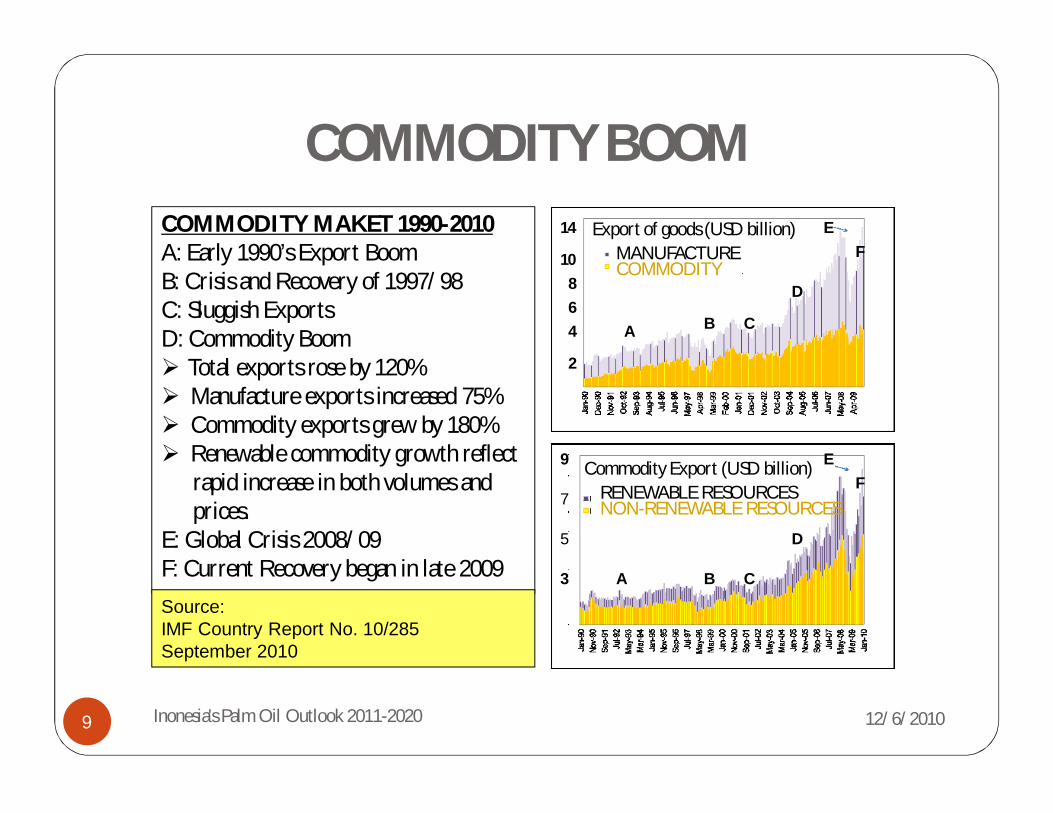

COMMODITY BOOM

12/6/2010

A B C

D

EF

Export of goods (USD billion)MANUFACTURECOMMODITY

Commodity Export (USD billion)RENEWABLE RESOURCESNON-RENEWABLE RESOURCES

COMMODITY MAKET 1990-2010A: Early 1990’s Export BoomB: Crisis and Recovery of 1997/98 C: Sluggish ExportsD: Commodity Boom Total exports rose by 120% Manufacture exports increased 75% Commodity exports grew by 180% Renewable commodity growth reflect

rapid increase in both volumes andprices.

E: Global Crisis 2008/09F: Current Recovery began in late 2009Source:IMF Country Report No. 10/285September 2010

A B C

D

EF

14

10864

2

9

7

5

3

9 Inonesia's Palm Oil Outlook 2011-2020

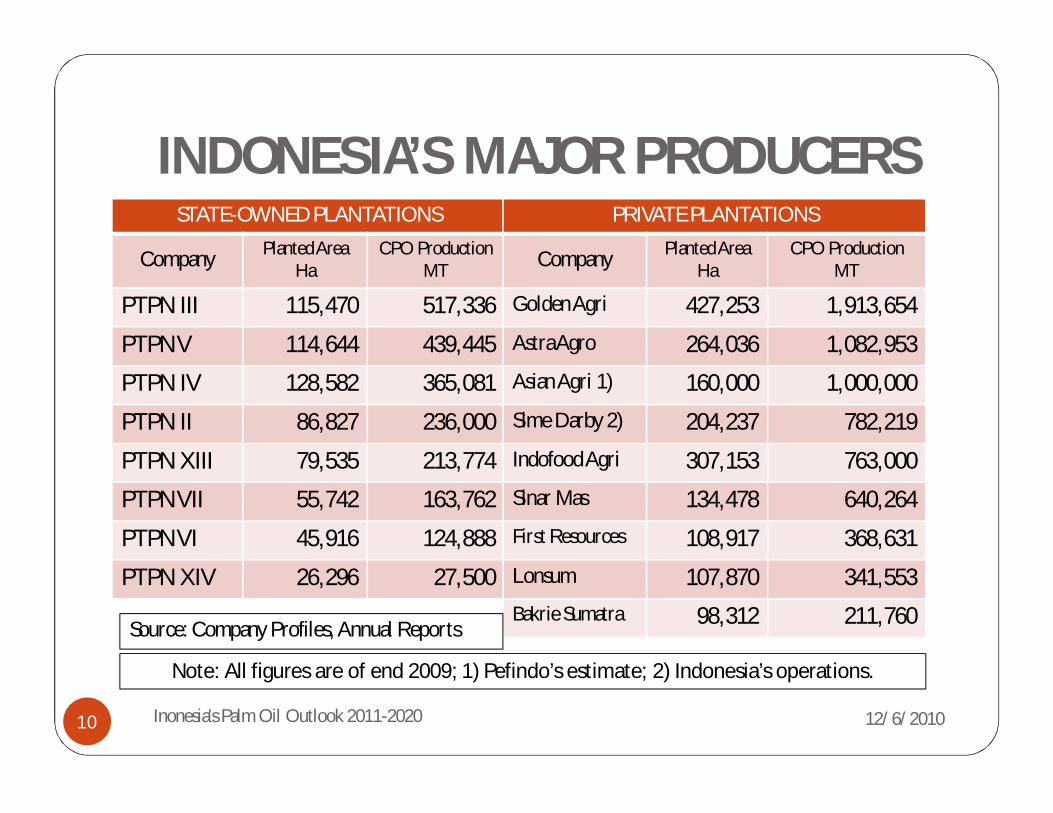

INDONESIA’S MAJOR PRODUCERS

12/6/2010

STATE-OWNED PLANTATIONS

Company Planted Area Ha

CPO Production MT

PTPN III 115,470 517,336

PTPN V 114,644 439,445

PTPN IV 128,582 365,081

PTPN II 86,827 236,000

PTPN XIII 79,535 213,774

PTPN VII 55,742 163,762

PTPN VI 45,916 124,888

PTPN XIV 26,296 27,500

PRIVATE PLANTATIONS

Company Planted Area Ha

CPO Production MT

Golden Agri 427,253 1,913,654

Astra Agro 264,036 1,082,953Asian Agri 1) 160,000 1,000,000

Sime Darby 2) 204,237 782,219

Indofood Agri 307,153 763,000Sinar Mas 134,478 640,264First Resources 108,917 368,631

Lonsum 107,870 341,553Bakrie Sumatra 98,312 211,760

Note: All figures are of end 2009; 1) Pefindo’s estimate; 2) Indonesia’s operations.

Source: Company Profiles, Annual Reports

10 Inonesia's Palm Oil Outlook 2011-2020

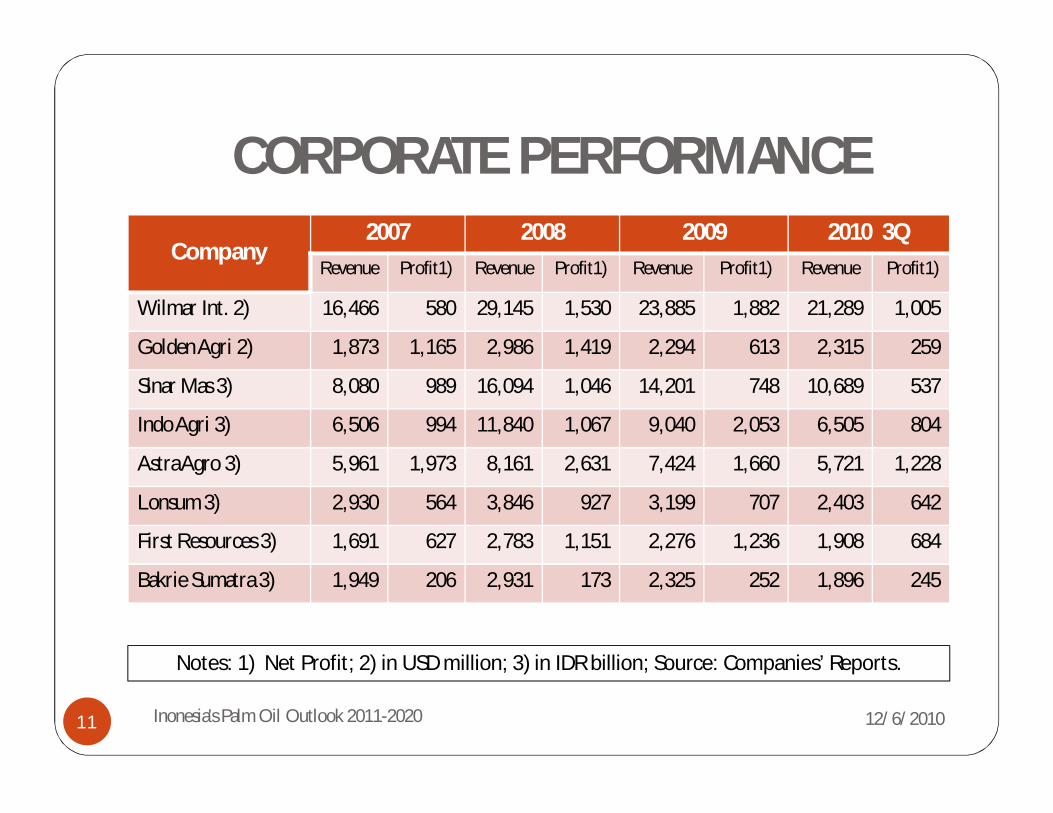

CORPORATE PERFORMANCE

12/6/2010

Company2007 2008 2009 2010 3Q

Revenue Profit1) Revenue Profit1) Revenue Profit1) Revenue Profit1)

Wilmar Int. 2) 16,466 580 29,145 1,530 23,885 1,882 21,289 1,005

Golden Agri 2) 1,873 1,165 2,986 1,419 2,294 613 2,315 259

Sinar Mas 3) 8,080 989 16,094 1,046 14,201 748 10,689 537

Indo Agri 3) 6,506 994 11,840 1,067 9,040 2,053 6,505 804

Astra Agro 3) 5,961 1,973 8,161 2,631 7,424 1,660 5,721 1,228

Lonsum 3) 2,930 564 3,846 927 3,199 707 2,403 642

First Resources 3) 1,691 627 2,783 1,151 2,276 1,236 1,908 684

Bakrie Sumatra 3) 1,949 206 2,931 173 2,325 252 1,896 245

Notes: 1) Net Profit; 2) in USD million; 3) in IDR billion; Source: Companies’ Reports.

11 Inonesia's Palm Oil Outlook 2011-2020

INDONESIA’S 20 RICHEST

12/6/2010Inonesia's Palm Oil Outlook 2011-202012

Rank Name Net Worth (USD mil) Rank Name Net Worth

(USD mil)

1 R. Budi & Michael Hartono 11,000 11 Kiki Barki 1,700

2 Susilo Wonowidjojo 8,000 12 Eddy William Katuari 1,650

3 Eka Tjipta Widjaja 6,000 13 Edwin Soeryadjaya 1,600

4 Martua Sitorus 3,200 14 Boenyamin Setiawan 1,500

5 Anthony Salim 3,000 15 Garibaldi Thohir 1,450

6 Sri Prakash Lohia 2,650 16 Sukanto Tanoto 1,400

7 Low Tuck Kwong 2,600 17 Theodore Rachmat 1,350

8 Peter Sondakh 2,400 18 Chairul Tanjung 1,250

9 Putera Sampoerna 2,300 19 Murdaya Poo 1,150

10 Aburizal Bakrie 2,100 20 Ciliandra Fangiono 1,100

Most of the country’s wealthiest reap their fortune in the renewable resources sector, notably palm oil. Source: Forbes Indonesia 3 December 2010.

PROMISING GLOBAL ECONOMY

12/6/2010

Country 2008 2009 2010 e

2011 f

2012 f

World 1.7 -2.1 3.3 3.3 3.5

OECD 0.3 -3.4 2.2 2.3 2.6

Brazil 5.1 -0.2 6.4 4.5 4.1

Russia 5.6 -7.9 4.5 4.8 4.7

India 5.1 7.7 8.2 8.7 8.2

China 9.6 8.7 9.5 8.5 8.2

Indonesia 6.0 4.5 5.9 6.2 6.3

Real GDP Growth (%)

Source: WB, Global Economic Outlook 2010

13 Inonesia's Palm Oil Outlook 2011-2020

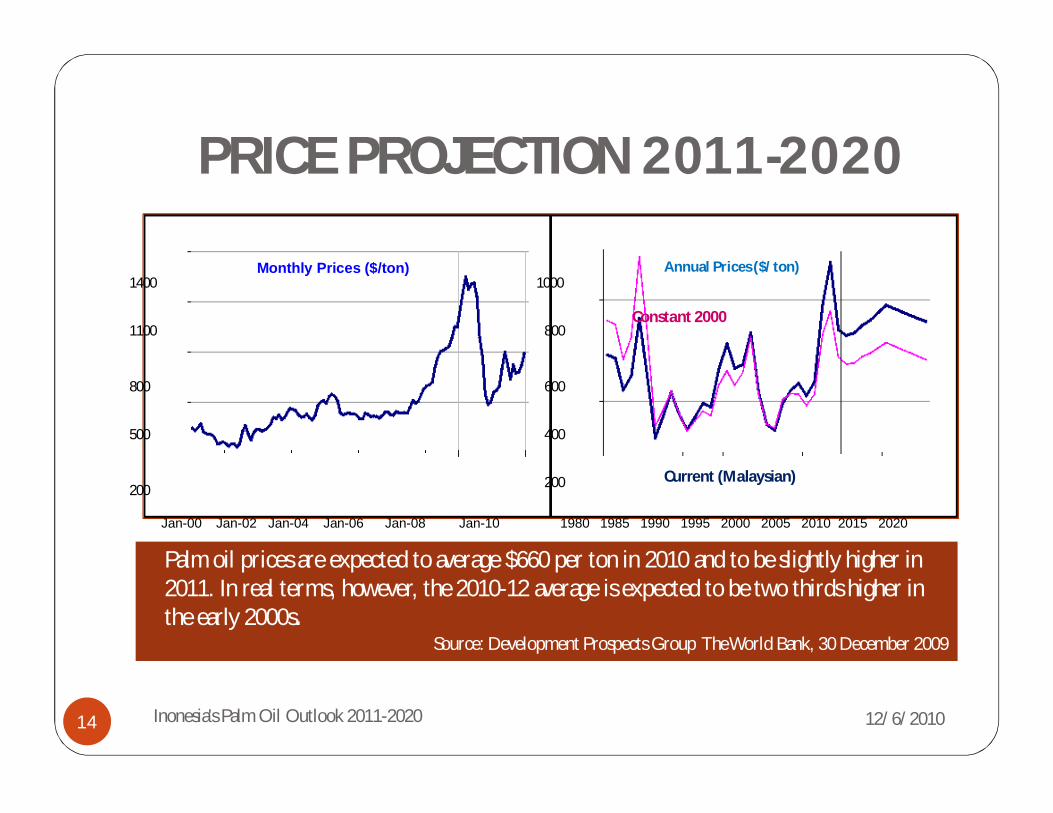

PRICE PROJECTION 2011-2020

12/6/2010

1980 1985 1990 1995 2000 2005 2010 2015 2020Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10

Monthly Prices ($/ton) Annual Prices ($/ton)

200

400

600

800

1000

200

500

800

1100

1400

Palm oil prices are expected to average $660 per ton in 2010 and to be slightly higher in 2011. In real terms, however, the 2010-12 average is expected to be two thirds higher inthe early 2000s.

Source: Development Prospects Group The World Bank, 30 December 2009

Constant 2000

Current (Malaysian)

14 Inonesia's Palm Oil Outlook 2011-2020

EXPANSION AREAS

12/6/2010Inonesia's Palm Oil Outlook 2011-202015

Potential 24.5 million Ha

CONTROVERSY AND SOLUTION

12/6/2010

CONTROVERSY PROPONENTS SOLUTION

Saturated fat content Competitors from other vegetable oil industry

Joint campaign by government and industry associations

Deforestation and biodiversity degradation

International interest groups High Conservation Value (HCV) assessment and management

Marginalization of local population

Local interest groups Social Impact Assessment and CSR programs; and smallholder (plasma) scheme

16 Inonesia's Palm Oil Outlook 2011-2020