Embed Size (px)

Citation preview

1

Institutional logic: the tale of overstatement of compliance with a corporate

governance guideline in a developing country, Bangladesh.

Abstract Manuscript Type: Empirical

Research Question/Issue: This study seeks to understand whether publicly listed companies in Bangladesh

overstate compliance with the Bangladesh Corporate Governance Guidelines-2006 (hereafter ‘the BCGG-2006’)

in annual reports.

Research Findings/Insights: This study conceptualized overstatement of compliance by the difference between

the compliance with the BCGG-2006 as reported in annual reports and the compliance with the BCGG-2006 as

stated in a confidential survey addressed to company secretaries. We found that there is a significant

overstatement of compliance with the BCGG-2006 in annual reports. We also found that overstatement of

compliance in annual reports is positively associated with control by sponsor family and is not associated with

control by institutional investors.

Theoretical/Academic Implications: This study provides empirical support for the theory of path dependence of

corporate governance and the neo-institutional theory rather than agency theory with respect to motivation for

overstatement of compliance with in annual reports in a developing country context. As such, this study

questions prior research on corporate governance in the context of developing countries that uses compliance

reported in annual reports to measure corporate governance variable.

PR actioners/Policy Implications: This study offers insights to international financial institutions and domestic

regulatory agencies in developing countries that advocate for corporate governance reform based on an Anglo-

American model. In addition, it provides a perspective for national and international investors to understand

corporate governance structure of companies in developing countries differently rather than solely relying on the

compliance reported in annual reports if they are considering making an investment in these companies.

INTRODUCTION

Corporate governance (CG) codes based on Anglo-American model have been adopted by

nations worldwide due to efficiency-based and legitimacy-based reasons (Zattoni and

Coumo, 2008). The legitimacy-based reasons have been particularly pronounced in

developing countries (Reed, 2002; Siddiqui, 2010; Cuervo, 2002; Reid, 2003). Depending on

the nature of issuing authority, the adoption of a CG code creates different types of pressures

for compliance, and non-compliance can result into a loss of external legitimacy (Aguilera &

Cuervo-Cazurra, 2004). However, CG practices are embedded in a country’s institutional

environment (e.g., Kim and Ozdemir, 2014; Khanna, Kogan & Palepu, 2006; Aguilera,

Filatotchev, Gospel & Jackson, 2008; Aguilera and Jackson, 2003; 2010) and compliance with

CG codes which are counter to the wider social values, existing rules and laws and cognitive

structures of the concerned country may discount legitimacy (Sanders and Tuschke,

2007:40). The institutional characteristics of developing countries are distinct from Anglo-

2

American countries (Claessens and Yurtoglu, 2013; Wanyama, Burton & Helliar, 2009; Khanna

and Palepu, 2004; Sing and Zammit, 2006; Pardes, 2004; Dela Rama 2012) and some

scholars have argued that Anglo-American model is ‘unsuitable for developing country

economies’ (Sing and Zammit, 2006:221). Moreover, compliance with new CG codes can be

resisted by a powerful interest group in fear of reduction in their private benefits of control

offered by existing CG practices (Bebchuk and Roe, 1999). Thus, firms’ responses toward

compliance with a CG code based on Anglo-American Model in the context of developing

countries are subject to conflicting institutional demands.

To date, there has been extensive descriptive research into compliance with CG codes both in

non-Anglo-American developed (v Werder, Talaulicar & Kolat, 2005; Akkermans, Van Ees,

Hermes, Hooghiemstra, Van der Laan, Postma, & Van Witteloostuijn, 2007; Talaulicar and V

Werder, 2008) and developing countries (e.g., Chen and Nowland, 2011; World Bank, 2009).

These researchers consistently found that majority of firms comply with the majority of the

provisions of the CG code. To illustrate, Talaulicar and V. Werder (2008) find that 96.81

percent of sample firms on average comply with 92.32 percent of ‘comply or explain’ based

recommendations of the German Corporate Governance Code. This high level of reported

compliance which are not consistent with the ‘comply or explain’ principle leads several

researchers (e.g., v. Werder et al., 2005; Akkermans et al., 2007:1109) to explicitly caution

that compliance rates based on public disclosures may overstate actual compliance.

Furthermore, researchers draw on interview and survey methods as the source of evidence on

compliance. These researchers found some evidence (e.g. Uddin and Choudhury 2008,

Wanyama et al. 2009) that where enforcement regimes are weak there may be undisclosed

failure to meet expected standards of CG. This suspicion regarding the level of compliance

with CG code reported in annual reports leads us to ask the main question of this study, does

3

compliance reported in annual reports overstate the reality of compliance with a CG code in a

developing country?

The widespread adoption of Anglo-American model has been frequently perceived as

evidence of institutionalization (Enrione, Mazza, & Zerboni, 2006). However, the conflict

between institutional characteristics of developing countries and Anglo-American model

poses threat to its taken-for-grantedness (Soederberg 2003: 17–18, 23; Sing and Zammit,

2006; Pardes, 2004). This implies that companies operating in developing countries face

conflicting institutional logics with regard to implementation of CG mechanisms. Thus, this

study used organisational responses to institutional change subject to competing institutional

logics framework as a theoretical framework. This framework has been used to investigate

diffusion of CG mechanisms (Chizema, 2008; Fiss and Zajak, 2004; Westphal and Zajak,

1998; Westphal and Zajak, 1994) and International Financial Reporting Standards (Alon,

2013) in environments where competing institutional logics exist. Most of these studies, due

to their reliance on public sources for data, took binary approach of either compliance/non-

compliance (e.g., Chizema, 2008) or substantial/ceremonial compliance (e.g., Westphal and

Zajak, 1994). However, theoretical development suggests that organizations use more than

these dichotomous strategic responses while they face competing institutional logics (Pache

and Santos, 2010; Kraatz and Block, 2008; Seo and Creed, 2002; Oliver, 1991; review by

Greenwood, Raynard, Kodeth, Micelotta and Lounsbury, 2011). We take this route of

theoretical development to generate hypothesis in order to understand: Does the level of

compliance with a CG code as reported in annual reports overstate the reality of compliance

with CG code? Moreover, how can the extent of overstatement of compliance with CG code

as reported in annual reports be explained?

To inform and support our hypotheses, we use data from a developing country, Bangladesh.

Data sources include a survey of actual practice and content analysis of annual reports.

4

Bangladesh is chosen because, although the Bangladesh Corporate Governance Guideline-

2006 is based on Anglo-American model and thus, draws on ‘comply or explain’ principle, a

compliance checklist is required by the Bangladesh Securities and Exchange Commission as

an item in the annual reports. This gives us an opportunity to more accurately measure

reported compliance. Furthermore, the BCGG-2006 is adopted to prove legitimacy of

government and regulatory agencies to international financial institutions (IFIs) but

institutional and firm characteristics of Bangladesh suggest that Anglo-American model is

not an appropriate model (Siddiqui, 2010). Given these, Bangladesh seems a potential

laboratory in which to investigate overstatement of compliance in annual reports.

We find supports in favour of our hypotheses. While prior researchers find that organisations

are complying with institutionally contested CG mechanisms either substantially or

ceremonially based on public disclosure (Westphal and Zajak, 1994; 1998; 2004), our paper

demonstrates that organizations seek legitimacy by disclosing compliance in annual reports

while disregard compliance in reality. We also make general contribution to institutional

literature. Further contribution is methodological, in distinguishing reported CG disclosure

from real CG compliance, and in corroborating empirical findings with interviews.

The remainder of the paper proceeds as follows. The next section discusses CG practices in

Bangladesh. In section three, we present our theoretical framework. Section 4 develops our

hypotheses. Section 5 outlines the research design while section 6 presents the findings of the

study. Section 7 concludes the paper and addresses the study’s limitations.

CORPORATE GOVERANNCE IN BANGLADESH

The importance of CG practices in Bangladesh attracted attention of the IFIs and the

domestic regulators after the stock-market crash in 1996. In November 1997, the Asian

Development Bank (ADB) funded an $80 million project to transform Bangladesh capital

markets toward an Anglo-American model (ADB, 1997). This programme consists of seven

5

technical assistances; one of them is Building Capacity of the Securities and Exchange

Commission and Selected Capital Market Institutions which costs $1.10 million. The first

objective of this technical assistance was to draft a comprehensive CG manual for public

limited companies and security issuers. This project was executed by the ADB with the help

of an USA consultant, The Aries Group Ltd., USA who formulated a CG guideline in line

with OECD’s Principles of CG (ADB, 2005). The Bangladesh Securities and Exchange

Commission (hereafter ‘the BSEC’) adopted the CG guideline in 2006 (hereafter ‘the BCGG-

2006’) (BSEC order No. SEC/CMRRCD/2006-158/Admin/02-08, dated 20 February 2006).

An earlier initiative was, however, taken by an IFIs-funded private-sector think-tank

organization, Bangladesh Enterprise Institute (BEI) toward improvement of CG. In 2003, BEI

conducted a comprehensive study on CG practices in Bangladesh funded by the IFIs. The

study found that the Bangladesh corporate sector lacked a sound CG structure due to country-

level institutional weaknesses such as lack qualified accounting and auditing profession,

ineffective and inefficient government-funded regulatory agencies and lack of effective

financial media and shareholder groups (BEI, 2003). This identification of weaknesses in CG

practices might be an initiative of the IFIs to create a normative isomorphism about Anglo-

American model of CG (c.f. Reed, 2002). In 2004, BEI issued a CG code (hereafter ‘the

voluntary BCGC-2004) in line with the OECD Principles of CG-1999. While developing the

CG code, BEI formed a taskforce on CG and a working group. The taskforce on CG included

a number of managing directors of local publicly listed companies and subsidiaries of foreign

multinational companies; a number of top officials from the Bangladesh government;

president and similar level officials from the professional accounting bodies and other

professional institutes; top officials of BSEC including chairman and CEO of a stock

exchange and president of foreign investors’ Chamber of Commerce. The working group

includes a number of foreign consultants, a number of Supreme Court advocates, an audit

6

partner from KPMG affiliated audit firm in Bangladesh and CEO of the first private sector

mutual fund company. The BEI might include the aforementioned group of professionals to

create normative, coercive and mimetic pressures on companies (c.f., Aguilera and Cuervo-

Cazurra, 2004; Seidl, 2007).

The BSEC adopted the BCGG-2006 on ‘comply or explain’ basis. Siddiqui (2010) argued

that by adopting the BCGG-2006 which is remarkably similar to the CG code of BEI, the

BSEC proved its legitimacy to the IFIs. The BCGG-2006 is subsequently considered as part

of the listing rules of both DSE and CSE. Several legal rules have also been enacted in line

with Anglo-American model making Bangladesh theoretically a country with an investor

protection index higher than OECD high income average (World Bank, 2013: 65). According

to the BCGG-2006, listed companies have to include a ‘comply box’ in their annual report or

otherwise explain the reason for non-compliance. An investigation of level of compliance

with the BCGG-2006 as reported in annual reports by World Bank found that reported

average compliance with the BCGG-2006 reached 82 percent in 2008 (World Bank, 2009;

p.41). Based on these findings, World Bank claimed that there has been a significant

improvement in CG practices of firms in Bangladesh.

Although the effort of IFIs, their funded local think-thank organization and regulatory

agencies have created normative, coercive and mimetic pressures on companies for

implementing CG practices similar to Anglo-American countries, wider social, regulatory,

political and cultural factors of Bangladesh limit legitimacy of Anglo-American-based CG

practices. At present, like many other developing countries (e.g., Claessens and Yurtoglu,

2013; Claessens, Djankov & Lang, 2000), the ownership of Bangladeshi companies are

concentrated in sponsor families and groups (Haque, Arun, & Kirkpatrick, 2011; Imam and

Malik, 2007). As in other developing countries (Claessens et al., 2000; Fan, Wei and Xu,

2011), the sponsor families also maintain significant control over their companies by

7

representing board and key management positions (Haque et al. 2011). Few families have

control over manufacturing, financial and service sectors (Nuruzzaman, 2004). Several

researchers maintained that Bangladesh is a decent example of family capitalism which it

developed due to the intervention of the IFIs into its development policies, and patronization

of own political alliances and corruption by the contemporary ruling parties since 1975 when

Bangladesh moved to market-based capitalism (Uddin, 2005; Uddin and Chowdhury, 2008;

Uddin and Hopper, 2001). At present, most of the industrial families are either directly or

indirectly politically connected with one of two major political parties (Jahan and Amundsen,

2012; Uddin, 2009) making them even more powerful. Consequently, sponsor families can

easily prevent general shareholders to publicly challenge CG practices in several means

(Uddin and Chowdhury, 2008). On the other hand, external stakeholders lack skills and

motivation to confront managers with respect to CG practices (BEI, 2003).

In spite of IFIs suggested significant economic and policy reforms since 1980s, capital

markets are still small and highly volatile (Chowdhury, 2013) and populated mostly by

poorly-literate ill-informed retail ‘momentum’ investors (The Aries Group Ltd, 2012).

Sponsors can easily manipulate stock price by several legal and illegal means (Khaled,

Chowdhury, Baree and Kabir, 2011). Moreover, inefficiency, corruption and politicization of

the regulatory agencies and the judicial systems still remain a critical issue (World Bank,

2009; 2011; The Aries Group Ltd, 2012). As a result, theoretically strong legal framework

fails to properly protect private property rights (World Heritage Foundation, 2014).

Consistent with wider socio-political environment such as corruption, dominance (Belal and

Cooper, 2011) and high power distance (Hofstede, Hofstede & Minkov, 2010), CG practices of

Bangladesh is inherently relation-based (Uddin and Chowdhury, 2008). Companies are

managed by appointing employees loyal to sponsor families in key management positions

and relying on ‘informal, familial and personal control’ (Uddin, 2009:791). As in other

8

relation-based systems (Li, 2013: 568), Bangladeshi firms need to bribe and make other off-

the-record payments to government officials and other regulatory authorities to obtain

business permits and necessary utilities (World Bank, 2013). Uddin (2009:789) maintained

that to conceal these irregular payments in external reports, firms prepare accounting

information under strong secrecy and control. External auditors lack independence and are

vulnerable to the power of sponsor families (Uddin and Chowdhury, 2008). Consequently,

published accounting reports do not properly comply with adopted IASs/IFRSs (Mir and

Rahaman. 2005; World Bank, 2003), disclose majority of items mandated by IASs/IFRSs

(Ahmed and Nicholls, 1994; Uddin and Hooper, 2003; Akhtaruddin, 2005) and provide

quality and reliable information (Wu, 2005). Outside stakeholders predominantly rely on

private relations with sponsor mangers for acquiring information and for protecting their

interests. For instance, Banks maintain close relationship with non-financial companies and

provide loans based on past relationship and collateral (BEI, 2003).

The high level of compliance with the BCGG-2006 as reported in annual reports (World

Bank, 2009) is doubtful given the above mentioned wider social, regulatory, political and

cultural environment. Indeed, research based on interview and survey method provided a

contradictory picture of CG practices (Uddin and Choudhury, 2008; Haque et al, 2011). For

instance, Uddin and Choudhury (2008, p.1045) found, by applying interview method, that

companies in Bangladesh fail to comply with basic corporate rules and regulations, with the

dominance of sponsor families weakening the state’s power in the enforcement of rules and

regulations. This is consistent with survey evidence of Haque et al. (2011) who found that

sponsor family and political affiliation of directors hinder improvement in CG in Bangladesh.

9

THEORITICAL FRAMEWORK

The adoption of a CG code, in general, creates different types of isomorphic pressures for

compliance with code provisions (Aguilera and Cuervo-Cazurra, 2004; Seidl, 2007; Zattoni

and Cuomo, 2008; p. 2). However, as CG practices are embedded in a country’s institutional

environment (e.g., Kim and Ozdemir, 2014; Khanna et al., 2006; Aguilera et al., 2008;

Aguilera and Jackson, 2003; 2010), national institutions and some of the stakeholders may

exert competing pressures for maintaining status quo (Lee and Yoo, 2008). Institutional

theorists have assimilated such situation with adoption of a new practice subject to competing

institutional logics within an institutional context (Sanders and Tuschke, 2007; Bates and

Hennessy, 2010).

Isomorphic pressures generate legitimacy discounts for organizations whose responses are

not satisfactory to constituents prescribing new practice (Deephouse and Carter, 2005:333;

Meyer and Rowan, 1977; DiMaggio and Powell, 1983). Some new-institutional scholars,

therefore, argued that all organisations inevitably comply with new practices (e.g., Scot,

2001; p.170) leading to homogenous organisational practices within an organizational field

(e.g., Strang and Soule, 1998). Recent neo-institutional scholarship has, however,

undermined the absolute role of isomorphic pressures and posited the role of institutional

logics in determining how organizations impliment new practices (Thornton and Ocasio,

1999; 2008; Kraatz and Block, 2008; Lounsburry, 2008; review by Greenwood et al., 2011).

Institutional logic approach acknowledges that organizational responses to institutional

pressures are rational behaviour which is shaped by field-level institutional processes,

organizational-level dynamics and individual-level experiences and identities (Pache &

Santos, 2010; Thornton and Ocasio, 2008; Greenwood and Hinings, 1996). To create a

context for our hypotheses, we discuss the concept of competing institutional logics and the

nature and role of organizational field, organizations and individuals in shaping

organizational responses to institutional pressures within institutional logics.

10

Institutional logics acknowledge that institutional pressures are often fragmented (Friedland

and Alford, 1991) and there exists conflict among external constituents (Briscoe and Murphy,

2012: 553; Kraatz and Block, 2008; Pache and Santos, 2010) as well as between external and

internal constituents (Westphal and Zajak, 2001; Fiss and Zajak, 2004). When competing

institutional demands exist, organizations need to maintain ‘pluralistic legitimacy’ (Kraatz

and Block, 2008:249) because organizational responses which may be perceived legitimate

by one constituent may be perceived illegitimate by another constituent (Pratt and Foreman,

2000; Stryker and Burke, 2000). Consequently, under condition of competing institutional

logics organizations can exercise some level of strategic choice to gain and maintain

legitimacy (Friedland and Alford, 1991; Sewell, 1992; Whittington, 1992; Clemens and

Cook, 1999; Dorado, 2005). Theoretical development suggests that organizations facing

competing institutional logics strategically choose either an individual or a combination of

alternatives among four types of strategic choices – compromise, avoidance, manipulation

and defiance - to gain and maintain legitimacy (Pache & Santos, 2010; Scherer, Palazzo and

Seidl, 2013; Oliver, 1991). Among these strategies, the avoidance strategy which includes

ceremonial window dressing to conceal non-conformity with institutional demands attracted

much empirical attention, especially with respect to study of formal compliance programs

(Hafner-Burton and Tsutsui, 2005; Cashmore, 2002; MacLean and Behnam, 2010; Maclean,

Litzky and Holderness, 2014). This may be because compromise involving balancing,

pacifying and bargaining with institutional referents, defiance involving rejecting institutional

demands, and manipulation involving attempt to control the source of content of the

institutional demands are difficult to exercise with respect to formal compliance program.

Ceremonial window dressing is analogous to the concept of decoupling in early neo-

institutional formulations (Westphal and Zajak, 1994; 2001; Elsbach and Sutton, 1992;

Hafner-Burton and Tsutsui, 2005; review by Bromley and Powell, 2012). For instance, by

11

decoupling Westphal and Zajak (1994) indicate a situation in which organizations declare

adoption of CEO long-term incentive plans without its actual implementation.

Institutional logic approach argues that organizational strategic responses are affected by

three levels – the organizational field, the organization and the individual - which are

practically and conceptually inseparable actors (Friedland and Alford, 1991: 242).

Organizational field represents the cognitive-cultural, normative, and regulatory environment

in which organizations function (Scott, 1995, Kostova, Roth and Dacin, 2008) and

characterizes the power dynamics and coalitions among all referent audiences such as focal

organizations, regulatory agencies, key resource providers, professional associations

(DiMaggio and Powell, 1983; Scott, 1995). The central construct of competing institutional

logics is that organizational fields are fragmented in nature, less formalized (Meyer, Scott and

Strang, 1987) and there may be a lack of consensus among cognitive-cultural, normative, and

regulatory pressures (Greenwood and Hinings, 1996) and among referent audiences regarding

institutional prescriptions (Pache and Santos, 2010). This lack of consensus suggests that no

single prescription achieves a taken for granted status (Purdy and Gray, 2009) providing

discretion to organizational members regarding selection of responses to gain legitimacy

(Goodrick and Salancik, 1996). Decoupling enables organizations to deal with ambiguity in

heterogeneous environment (Christensen and Molin, 1995; Ruef and Scott, 1998; Kostova

and Roth, 2002). For instance, Kostova and Roth (2002) has demonstrated that organizations

more likely decouple a practice when the practice is recommended and enforced by

regulatory institutional profile but is less favoured by normative and cognitive institutional

profiles. Although the Anglo-American model is recommended by regulatory institutional

profile, it may be less favoured by normative and cognitive institutional profiles of

developing countries. A heterogeneous field further characterised with lack of professional

associations and social groups with power to enforce implementation of new practices may

12

encourage firms to decouple new practices further to gain and maintain legitimacy

(Greenwood, Suddaby and Hinings, 2002; Rao, Morrill and Zald, 2000). This is particularly

the case in respect of developing countries which lack strong association of shareholders and

mutual funds and financial media (Pardes, 2004).

Organizational field-level institutional logics provide a part understanding of organizational

responses to institutional pressures (Broadbent, Jacobs and Laughlin, 2001) because field-

level institutional logics are filtered through organizational-level dynamics (Boxenbaum and

Perderson, 2009; Greenwood and Hinings, 1996). Organizations are heterogeneous entities

composed of functionally differentiated groups pursuing goals and promoting interests

(Greenwood and Hinings, 1996). Hence, organizational field-level recommendations may

‘acquire different meaning when they are implemented in different organizational contexts’

(Boxenbaum and Perderson, 2009: 190). Research has shown that organizations that lack of

resources to implement new practice more likely use window dressing as a response

(Bromley, Hwang and Powell, 2012). Research has shown that corporations invest in new

practice and protect their legitimacy as long as benefits exceed or at least equal the costs

(Siegel, 2009; Sprinkle and Maines, 2010; Scherer at al., 2013). For instance, Scherer at al.

(2013) have shown that when cost of implementing corporate social responsibility strategy is

high, organizations adopts manipulation strategy to gain legitimacy when pressures arise

from sustainable development.

Central to competing institutional logics are social agents both internal and external to the

organization (Kostova et al., 2008; Thornton and Ocasio, 2008; Pache & Santos, 2010).

Individual-level experiences and identities of these social actors influence their cognitive

processes to their understanding of what is a legitimate organizational response under

conflicting institutional pressures (Aurini, 2006; George, Chattopadhyay, Sitkin, & Barden,

2006). The relative power and influence of social actors would create variation in

13

organizational responses since responses which protect the interest of one group of social

actors may hamper interest of another. Both theory and empirics suggest that when personal

interests of managers are potentially threatened by adoption of new practice (Pache and

Santos, 2010:465; Fiss and Zajak, 2004; Westphal and Zajak, 2001; Oliver, 1991), or when

managers lack rationale for implementation of a new practice (Sauder and Espeland, 2009:

63; Bromley et al., 2012), selection of avoidance strategy is more likely to maintain

legitimacy to external constituents. Westphal and Zajak (1994; 2001), for instance, have

shown that how potential threat on managers’ personal interests exerted by CEO long-term

incentive plans and stock repurchase programme let organizations declare adoption of the

plan and stock repurchase program without their actual implementation. Similarly, Bromley

et al. (2012) have demonstrated that window dressing with respect to strategic planning in

response to pressure from funding agencies is positively associated with the absence of

managerial rationale in non-profit organizations.

Finally, relative power of external constituents actively influence the organizational actions

as organizations depend on external constituents for resources and legitimacy provides access

to key resources (e.g., Pfeffer & Salancik, 1978). DiMaggio (1988: 14) argued that “new

institutions arise when organized actors with sufficient resources see in them an opportunity

to realize interests that they value highly.” Oliver (1991) support the above arguments and

argued that if the new practice is favoured by external constituents who are uniform in terms

of demand and powerful in term of source of resources, firms more likely acquiescence to the

demand of that constituent. Ultimate power over an organization lies with ownership if

sources of resource are considered. Among different ownership groups, institutional

blockholders are more powerful in terms of uniformity of demand. Westphal and Zajak

(2001) argued that the presence powerful of institutional investors reduces the gap between

espousal and implementation of CG mechanisms (Westphal and Zajak, 2001).

14

Statement on compliance with CG code provisions - A tool to seek legitimacy

CG code of a nation is generally a formal set of best practice recommendations regarding

characteristics of board and its sub-committees and other internal CG mechanisms (Chizema,

2008:360; Zattoni and Cuomo, 2008). Compliance with a corporate governance code follows,

in many cases, a ‘comply or explain’ principle. This principle recognizes that a ‘one size fits

all’ approach is not justified for CG (MacNeil and Li, 2006:486) and thus, permits firms to

non-comply with a specific provision of the code if firms cannot comply with it (Coombes

and Wong, 2004; Seidl, 2007). That is, compliance with a code provision is voluntary

(Zattoni and Cuomo, 2008; p. 2). However, a company subject to a code has to often issue a

statement on compliance and specially report and justify non-compliance. This requirement

makes compliance statement a key legitimacy seeking tool because by compliance statement

organizations seek approval about their CG structures (Seidl, Sanderson, and Roberts, 2013).

Compliance statement is extensively used by researchers to quantify compliance (von Werder

et al. 2005; Arcot, Bruno, and Faure-Grimaud, 2010; Seidl et al., 2013; Talaulicar and von

Werder, 2008; Akkermans et al., 2007). These researchers mostly look into compliance with

observable provisions, such as information on attendance at board meetings, composition of

the board of directors, or the proportion of independent non-executive directors. The results

of these studies indicate that majority of firms comply with the majority of the provisions of

the corporate governance code. Zattoni and Cuomo (2008) argued that this high level of

compliance reflects formal influence of CG codes on CG structures of listed companies.

Researchers who study level of compliance with CG code also speculate several reasons for

this seeming over-compliance with CG codes: pressures from capital markets (Arcot et al.,

2010; v. Werder et al., 2005; Akkermans et al., 2007) and peer companies (Wymeersch 2006;

Talaulicar and v. Werder, 2008); monitoring by regulatory authorities such as stock

exchanges and their regulators (Wymeersch 2006; Arcot et al., 2010; Burton, 2000; Aguilera

15

& Cuervo-Cazurra, 2004); pressures from spontaneous constituents such as academics,

consultancy firms and the media (Wymeersch, 2006; Akkermans et al., 2007); risks of

reputational damage arising from non-compliance (Wymeersch 2006; Hooghiemstra and van

Ees, 2011) indicating that compliance with CG codes help firms to gain legitimacy.

Next, the organizational response to new prescription subject to competing institutional logics

framework is applied to examine overstatement of compliance with the BCGG-2006 in

annual reports.

Conflicting institutional demands and overstatement of compliance with the BCGG-

2006 in annual reports:

We described CG practices in the Bangladeshi context and reviewed competing institutional

logic’s perspective on how the organizational field, organizational dynamics and individual-

level experiences and identities of social actors influence organizational responses to

institutional pressures. We observe that issuance of the BCGG-2006 by the BSEC, the main

regulatory agency for listed companies in Bangladesh, and subsequent inclusion of the

BCGG-2006 into listing rules of stock exchanges created coercive pressures (c.f. Wymeersch

2006; Arcot et al., 2010; Aguilera & Cuervo-Cazurra, 2004). Non-conformance to coercive

pressures created by regulatory agencies threatens a firm’s regulatory legitimacy (e.g.,

Aldrich & Fiol, 1994; Ruef & Scott, 1998). Research in developed countries validated this

threat to firm’s regulatory legitimacy by demonstrating that managers perceive the ‘comply

or explain’ based CG code as regulative as a hard law (Seidl, Sanderson & Roberts, 2009).

Managers in Bangladesh are relatively naïve and do not understand the idea of CG (Jabed and

Rahman 2003 cited in Rahim and Alam, 2014). Hence, it is more likely that they will fail to

distinguish between the BCGG-2006 and a hard law. They may perceive that declaration of

non-compliance with the BCGG-2006 may threaten regulatory legitimacy although non-

compliance with an appropriate explanation is legitimate under a ‘comply or explain’ regime.

16

However, normative and the cultural-cognitive structure of Bangladesh invoke limited

legitimacy threats for non-compliance with the BCGG-2006, as discussed below. Normative

legitimacy of the BCGG-2006 is tried to create by the IFIs and the private sector think-tank

organization funded by the IFIs, the BEI by identifying weaknesses in Bangladesh CG system

(c. f., Reed, 2002) and then by engaging a large number of practitioners and government-

officials in development of voluntary code (c. f., Seidle, 2007). Non-conformance to

normative pressures, however, threatens normative legitimacy when new institutional

prescription is consistent with wider social norms and values (Scott, 2001: 54). CG system of

Bangladesh is inherently relation-based (Uddin and Chowdhury, 2008). Firms in Bangladesh

need to bribe government officials for obtaining business permits and necessary utilities

(World Bank, 2013) and manage tax and custom related issues (Uddin, 2009). Johnson,

Kaufmann, and Zoido-Lobaton (1998) and Friedman, Johnson, Kaufmann, & Zoido-Lobaton,

(2000) asserted that high level of corruption motivates businesses to practice secretive

culture. Interview evidence of Uddin (2009) is consistent with aforesaid assertion. The

secretive culture is also reflected in inadequate development of accounting profession and

system in Bangladesh (Mir and Rahaman. 2005; World Bank, 2003). Consequently, banks,

main provider of finance, maintain close and long-term relationship with non-financial

companies and extend credit based on relationships and collateral (Siddique, 2010). This

suggests that larger belief-systems and experienced reality of the audience’s daily life of

Bangladesh are not consistent with Anglo-American model that asks for openness and

transparency. Thus, a firm’s normative legitimacy (Scott, 2001) in the Anglo-American

model is questioned. Firms’ poor compliance with the voluntary BCGC-2004 issued by the

BEI (World Bank, 2009) reflected this low normative legitimacy in Anglo-American model.

Corporate ownership in Bangladesh is concentrated in families and complex in nature (Haque

et al. 2011; Imam and Malik, 2007). It has been argued that Anglo-American model, as it is

17

designed for dispersed ownership companies, is not effective for concentrated-ownership

companies of developing countries (Jiang and Peng, 2011; Young, Peng, Ahlstrom, Bruton and

Jiang, 2008). Empirical evidence in developing countries with similar ownership

characteristics has demonstrated that board independence maintain no relationship with

market-based performance of firms (Connelly, Limpaphayom and Nagarajan, 2012; Black,

Carvalho, and Gorga, 2012; Chen, Li, and Shapiro, 2011). This evidence may imply that CG

mechanisms suggested by Anglo-American model are not ‘understood, recognizable and

located within the set of the widely held cognitive structures’ (Sanders and Tuschke,

2007:33) of market participants of developing countries, such as Bangladesh.

The effective implementation of the BCGG-2006 can create uncertainty for firms by

revealing illegal practices such as illicit payments to government officials. To avoid this

uncertainty, firms can engage in ‘window dressing’ to conceal their non-conformity with the

BCGG-2006 and prove their legitimacy to the BSEC and the stock exchanges. Window

dressing can be easily used given the relatively small, illiquid and inefficient stock markets of

Bangladesh and inefficiency and corruption of regulatory agencies which indicate that there

is a lack of strong collective action to reveal underlying non-conformity. Previous research on

reliability of accounting reports (Wu, 2005) and corporate social responsibility (Belal and

Cooper, 2011) indeed suggests that Bangladeshi firms used ‘window dressing’ in a routinized

manner to reduce tax and to gain legitimacy, respectively. For instance, Belal and Cooper

(2011) report the opinion of one of the company secretaries they interviewed:

We don’t have any written equal opportunity policy. But in our job advert we do say

that we’re an equal opportunity employer (Belal and Cooper, 2011; p. 663).

A logical extension of these findings on CSR to reporting compliance with BCGG-2006

indicates that Bangladeshi companies may overstate compliance in annual reports. Hence,

following hypotheses follow:

18

H1: There is a significant level overstatement of compliance with the BCGG-2006 as

reported in annual reports.

Legitimacy is determined by mutual observations between managers and external

constituents who recommend institutional change and observe managers actions (Seidl,

2007). Meyer and Rowan (1977) maintained that in order to gain legitimacy, organizations

change more visible and formal structure while ‘decouple’ internal structures in order to

maintain autonomy. Decoupling of internal structures is also less risky for organizations

because internal practices are less transparent to outsiders and thus, attract less negative

publicity, even if decoupling is revealed, and consequently cause less reputational damage

(Briscoe and Murphy, 2012). With respect to CG codes, Seidle (2007:713) hypothesised that

conformance between compliance with CG codes declared by managers and actually put into

action depends considerably on the extent to which external constituents are able to assess the

conformance. Specific empirical evidence also exists that organisations legitimate their CG

structures by appointing outside directors who have formal independence but not social

independence from CEOs as external constituents can more easily observe and monitor

formal independence than social independence (Westphal and Graebner, 2010). This follows

that organizations confirm better between disclosed compliance and actual compliance of

code provisions whose actual implementation are more observable by external constituents.

Alternatively, managers confirm less between disclosed compliance and actual

implementation of code provisions whose actual implementation are difficult to assess by

external constituents.

The BCGG-2006 contains provisions that can be divided into more observable and less

observable provisions. Hence, the second hypothesis is:

H2: The extent of overstatement of compliance with the BCGG-2006 is higher with

respect to the provisions of the BCGG-2006 which are less observable by outsiders.

19

The perceived legitimacy gain is not solely determined by how external constituents perceive

the new practice (Crilly, Zollo & Hansen, 2012) but also by how insiders perceive it as a

source of opportunity or threat for their organizational and personal interests (George et al.,

2006). One of the important characteristics of companies in Bangladesh is family-ownership

and control. Family companies differ from management-controlled companies in terms of CG

structure and strategic decision making process (review by Gomez-Mejia, Cruz, Berrone, and

De Castro, 2011). The CG structure of family-controlled firms is more informal and

centralized in nature than that of non-family firms. The existing CG structures of these

family-controlled firms may not be consistent with CG structures suggested by the BCGG-

2006. The inconsistency between internal structure and external pressure has been identified

as one of the reasons for window dressing of compliance. Moreover, family-controlled firms

requires less monitoring and extra-monitoring suggested by the BCGG-2006 may be counter-

productive. Indeed, evidence in a developing country has shown that extra-monitoring of

family-controlled firms often leads to lower-level financial performance (Chen and Nowland,

2010). Furthermore, effective implementation of the BCGG-2006 may require changing

existing CG structure and thus, incurrence of significant amount of costs, exceeding the

expected benefits of CG as stock market is small and these firms are reluctant to raise funds

from stock markets.

Moreover, family-affiliated managers have different normative believe structures

which often maintain that long-term capital investment, survival of the firm, and the intention

of passing the firm on to descendants are main goals of firms (Casson, 1999). Gomez-Mejia

and colleagues labelled it as desire for protection of socio-emotional wealth (Gomez-Mejia,

Haynes, Nuñez-Nickel, Jacobson, and Moyano-Fuentes, 2007; Gomez-Mejia, Makri, and

Kintana, 2010; Gomez-Mejia et al., 2011). The underlying rationale of Anglo-American

20

model, the maximisation of shareholder wealth in short-term (Porter, 1992), contradicts with

the above normative believe structures of family-affiliated managers. Interview and survey

research has, indeed, suggested that family-affiliated managers in Bangladesh maintain the

aforesaid substantive rationalities for compliance (Uddin, 2009: 785) and thus, resist

implementation of the BCGG-2006 (Uddin and Chowdhury, 2008:1030; Haque et al., 2011).

However, family-controlled companies are equally under regulative pressure either to comply

or explain non-compliance with the BCGG-2006 in order to maintain their listing status.

Furthermore, the pressures from the IFIs, local research organizations funded by the IFIs,

regulators is not lower for family-controlled firms. Indeed, the IFIs and their supporters have

long argued that family-control is the cause of poor corporate governance (e.g., Morck and

Yeung. 2004). By disclosing compliance with the BCGG-2006 in annual reports, family-

controlled firms can alleviate pressures from the IFIs and their supporters. Hence, third

testable hypothesis follows:

H3: Overstatement of compliance with the BCGG- 2006 as reported in annual reports

is positively associated with family control.

While our discussion so far suggests that outside shareholder interests are poorly

protected in Bangladesh, one uniform and important resource provider to organizations in

Bangladesh can be institutional blockholders who are independent of controlling families.

Prior interview evidence provided by Uddin and Chowdhury (2008) has indicated that

presence of representative of institutional investors on board of directors improves CG

practices. Empirical evidence has also shown that existence of outside blockers is positively

associated with firm performance, indicating that outside blockholders play monitoring roles

(Farooque, Zijl, Dunstan and Karim, 2007). Hence, the fourth testable hypothesis is:

H4: Overstatement of compliance with the BCGG- 2006 as reported in annual reports

is negatively associated with control by institutional blockholders.

21

RESEARCH DESIGN

Sample and data collection

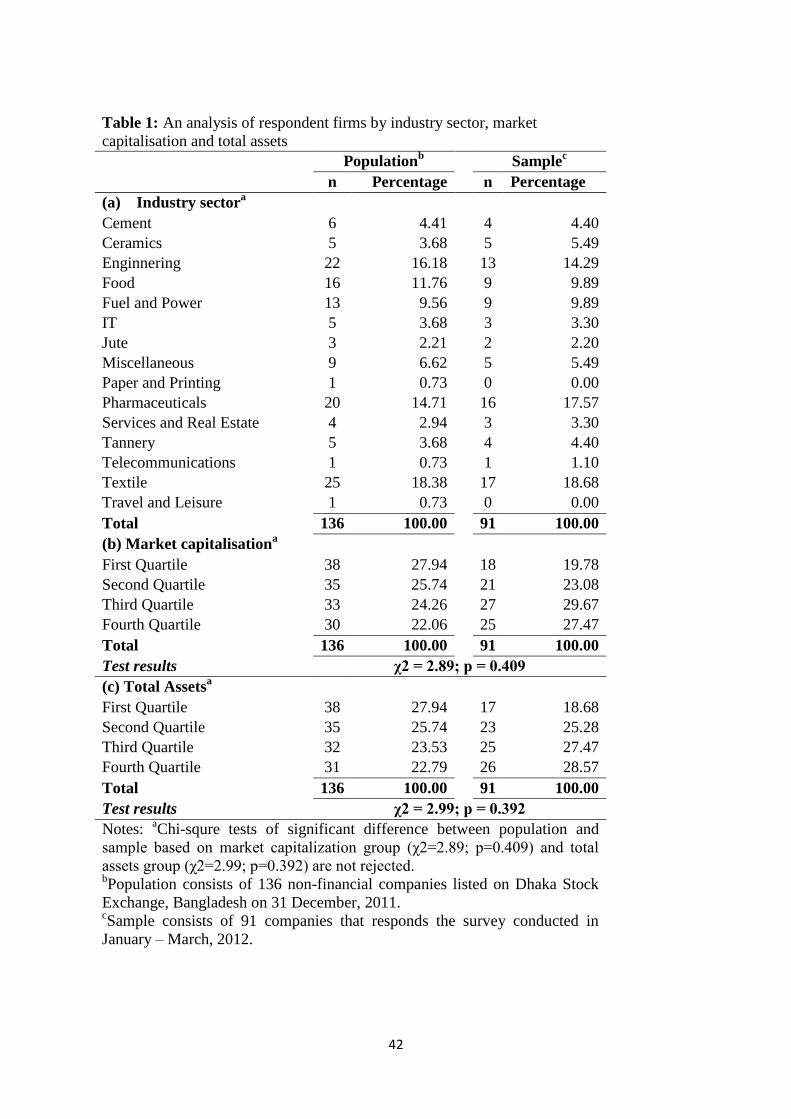

The sample of this study consists of 91 non-financial companies that responded in a

self-explanatory questionnaire survey. The survey was conducted during January – March,

2012 and addressed to company secretaries or CFO. The survey was designed to collect

detailed data on compliance with the provisions of the BCGG-2006, family relationship

among directors, composition of board of directors and the ownership structure of the

company. With respect to compliance with the BCGG-2006, the questionnaire emphasises on

20 easily comparable provisions which can be compared with compliance reported in annual

reports without ambiguity. The questionnaire includes both open and closed questions. The

introductory letter of the survey describes that the purpose of the survey is to understand

underlying level of compliance with the provisions of the BCGG-2006 (Diamond, 2000),

promises confidentiality by ensuring anonymity of the respondents and his organisation (Van

der Stede et al., 2005) and provides an assurance that the outcome of the survey will not be

published in Bangladesh. This assurance was added to increase the reliability of the survey

responses. The questionnaire was pre-tested in person with a number of company secretaries

of local privately-owned companies. Based on the feedback of the pre-test, we deleted all

questions related to remuneration committee and nomination committee because these

questions are not applicable to Bangladesh yet.

The survey instrument (Appendix one) was mailed to all 136 non-financial companies

listed on the Dhaka Stock Exchange, Bangladesh as at 31 December, 2011. The names of the

company secretaries and the addresses of headquartersi of companies were retrieved from

Central Depository Bangladesh Limited. Banks and financial institutions were excluded

because they are subject to different governance rules under the regulatory authorities. One of

22

the researchers physically visited companies whose registered offices are situated in Dhaka

and personally persuaded the company secretaries or CFOs to take part in the survey in a

structured interview manner. He often used his alumni connections to reach the respondents.

By the end of March 2012, he ended up with 91 usable responses, a response rate of 66.91%.

In order to test for response bias, responders are compared with the population on the basis of

industry sectors, market capitalization and total assets (Wallace and Mellor, 1988). As shown

in Table 1, a chi-square test indicated no significant difference in the distribution of

companies across any of these categories.

<Insert table 1 here>

In order to have available the most recent accounting information at the date of the

survey, annual reports were collected for the full population of 136 non-financial companies,

for the financial year 2011 Reports are available in printed format, at the Bangladesh

Securities and Exchange Commission and Dhaka Stock Exchange Library. Year ends were

31 December (44 companies) or 30 June (47 companies). Relevant regulations were

unchanged over this period.

Data Analysis

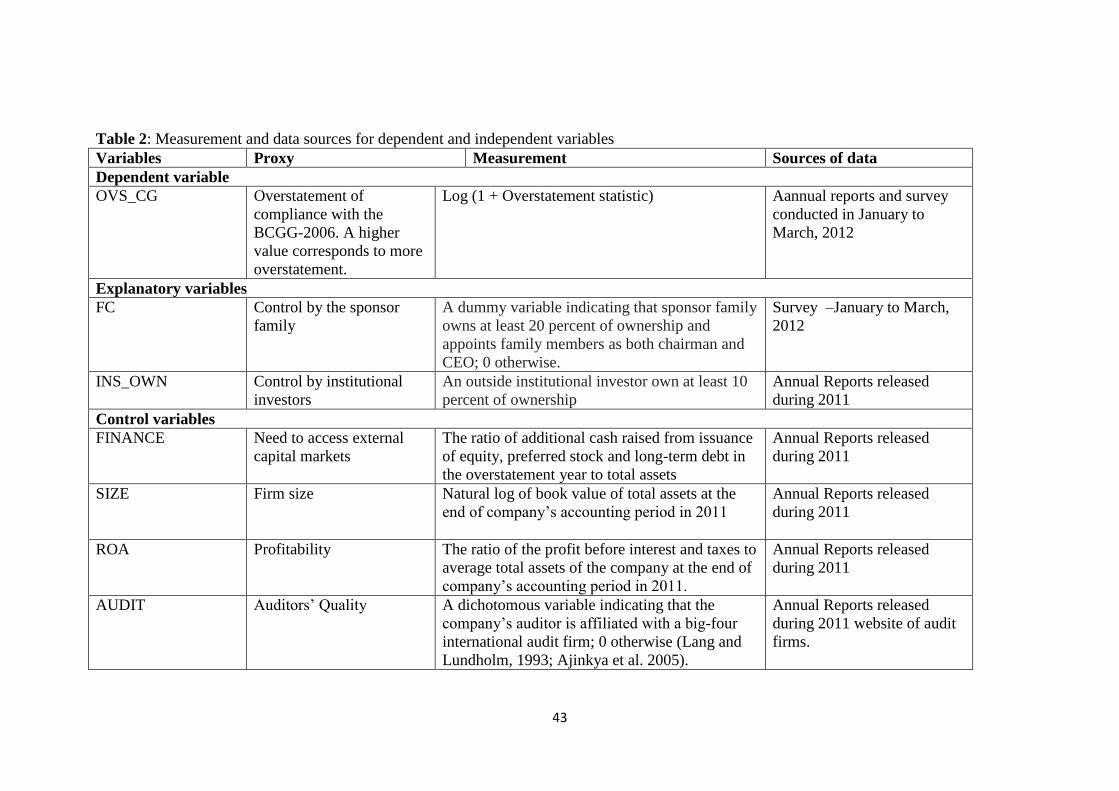

We construct two measures of compliance [one for compliance as reported in annual reports

(ReportedCG) and one for compliance as stated in the survey (SurveyCG)] with the BCGG-

2006 for each company. The ReportedCG and SurveyCG are measured using a binary

indicator [1 for compliance and 0 for non-compliance] separately for compliance as reported

in annual reports and as stated in the survey by each company. The value of binary indicators

are added together to derive company-specific values of ReportedCG and SurveyCG. This

method of measuring corporate governance is based on Gompers, Ishii, & Metriek (2003)

which extensively used by subsequent researchers (see, e.g., Ammann, Oesch, & Schmid, 2011;

Bebchuk, Cohen & Ferrell, 2009; Cremers and Nair, 2005; Brown and Caylor, 2006). The

23

theoretical minimum and maximum value of both ReportedCG and SurveyCG are 0 and 20

respectively as compliance with 20 provisions of the BCGG-2006 is used.

Alternative methods of measuring corporate governance index are assignment of unequal

weight for different mechanisms depending on the importance of the mechanisms (Bhagat,

Bolton & Romano, 2008) and Principal Component Analysis (Larcker, Richardson & Tuna,

2007). However, the purpose of this study is to measure overstatement of compliance with the

BCGG-2006 in annual reports rather than to measure the strength of CG of companies

implying that measuring CG index by assigning unequal weight or using Principal

Component Analysis is less appropriate. Hence, measuring corporate governance index by

assigning weight is avoided.

We define overstatement as the extent to which the reported corporate governance

compliance overstates the admitted compliance as revealed in the survey. It is measured by

calculating the difference between ReportedCG and SurveyCG, scaling the difference by

ReportedCG.

Overstatement statistic = (ReportedCG – SurveyCG)/ ReportedCG expressed as a

percentage

ReportedCG is a corporate governance compliance index based on disclosure in annual

reports of 20 main provisions of the BCGG-2006. SurveyCG is a corporate governance

compliance index of the same 20 provisions, as revealed by a survey.

We then classify the aforesaid 20 provisions into observable and less observable. Observable

provisions are easily verifiable or are subject to strong monitoring by regulatory authorities

such as the BSEC and the DSE. Observable provisions, thus, include nine provisions such as

the number of board members, separation of the chairman and CEO, formation of an audit

24

committee etc. as well as at least four board meetings per year. Board meetings are

categorized as an observable provision because companies are under an obligation to

announce the time, date and venue of the meeting before, and the decisions of board meeting

after, the meeting is held through the DSE website. Less observable provisions are related to

the internal practices of the company and thus, are relatively less visible to an outside

individual or organization. Less observable provisions, hence, include 11 provisions such as

defining the roles and responsibilities of the chairman and CEO, having a written audit

committee charter etc. Based on this classification of provisions, four composite corporate

governance sub-indices based on (1) compliance with observable provisions as reported in

annual reports (observable CG_AR); (2) compliance with observable provisions as stated in

the survey (observable CG_SR); (3) compliance with less observable provisions as reported

in annual reports (less observable CG_AR): and (4) compliance with non-observable

provisions as stated in the survey (less observable CG_SR) are constructed.

Then we determine two new distributions: overstatement in observable CG and

overstatement in less observable CG using method we apply for defining overstatement

statistic and the values of observable CG_AR, observable CG_SR, less observable CG_AR,

and less observable CG_SR.

Our dependent variable to investigate the relationship of overstatement of compliance with

the provision of the BCGG-2006 with control by family is ‘overstatement of compliance’.

Because overstatement statistic was truncated at the lower bound of zero, we used Tobit

regression model. In order to use tobit regression model, we performed a logarithmic

transformation of overstatement statistic (after adding 1). Formally, the overstatement index

can be expressed in this way:

Overstatement index = ln [1+ {(ReportedCG – SurveyCG)/ ReportedCG}]

25

We defined family control, coded 1, if an individual member and members of the founding

family either directly or indirectly own at least 20 percent of ownership and an individual

member of the founding family occupy the position of chairman and CEO, or two members

of the founding family occupy the position of chairman and CEO; 0 otherwise. This

definition of control by family is more aligned with Villalonga and Amit (2006) who argue

that family nature of firms depends on three aspects: ownership, control and management.

We argue that the capture of ownership, key control (i.e., chairman of board) and key

management (i.e., CEO) by sponsor family makes family powerful. In case of Bangladesh,

ownership is concentrated and sponsor family holds the key management positions

frequently. Hence, we combine control in terms of ownership, control and management.

Similar definition of family control is used by Luo and Chung (2013) and Jara‐Bertin,

López‐Iturriaga, & López‐de‐Foronda (2008).

We defined presence of blockholder, coded 1, if at least one of the outside institutional

investors own at least 10 percent of outstanding shares at the end of a company’s accounting

period in 2011; 0 otherwise. This variable captures concentration of institutional ownership

and thus, indicates resource dependence of the firm on institutional ownership. Alternatively,

it indicates power of institutional ownership. This variable is consistent with Hartzell and

Starks (2003).

We assume that external pressures for legitimacy will increase overstatement. Due to lack of

prior research related to overstatement of compliance with corporate governance, we draw

control variables from evidence in prior literature on associations of firm characteristics with

compliance with formal compliance program we control for firm size measured by logarithm

of total assets (Cao, Myers & Omer, 2012), profitability measured by ROA (e.g., Dechow et al.

1995; 1996; Beneish, 1999; Richardson, Tuna, and Wu, 2003; Burns and Kedia, 2006), audit

26

quality measured by audit firm’s affiliation with international big four and requirement to

raise funds from external capital markets measured by the ratio of additional cash raised from

issuance of equity, preferred stock and long-term debt in the overstatement year to total assets

(Richardson et al., 2003).

To compare compliance as reported in annual reports and compliance as stated in the survey,

we used t-test on the means and a Mann-Whitney U-test on the medians. We apply same tests

compare extent of overstatement with respect to observable and non-observable provisions.

To examine the association between overstatement of compliance and family control,

we used a Tobit regression. We used a Tobit regression because the distribution of

overstatement statistic is truncated at the lower bound of zero. Tobit regression is more

appropriate than ordinary least square (OLS) to predict a truncated dependent variable

because the use of OLS provides inconsistent estimates of the parameters (Woolridge, 2002;

p. 668). Tobit regression is used censoring the dependent variable at zero, as presented in the

following equations1:

OVS_G* = β0 + β1FC + β2INS_OWN + γi Controls + εi

OVS_G=0 if OVS_G* ≤ 0

OVS_G= OVS_G* if OVS_G≥ 0

OVS_G = ln (1+ overstatement statistic) ………….. (1)

Where

FC, a dichotomous variable indicating presence of both chairman and CEO from the

sponsor family or an individual member of the sponsor family holding both the position of

chairman and CEO; 0 otherwise;

INS_OWN, percentage of outstanding shares owned by institutional investors at the

end of a company’s accounting period in 2011;

1 See Wooldridge (2002) p. 670-71 for an exposition of Tobit regression model.

27

Control variables include following:

MB, ratio of the firm’s market value of common equity to book value of common

equity at the end of company’s accounting period in 2011;

ROA, the ratio of the profit before interest and taxes to average total assets of the

company at the end of company’s accounting period in 2011;

SIZE, natural log of book value of total assets at the end of company’s accounting

period in 2011;

AUDIT, a dichotomous variable indicating that a company’s auditor is affiliated with

a big-four international audit firms; 0 otherwise.

The measurement of variables and method required for testing H3 and H4 are detailed in

table 2.

<Insert table 2 here>

RESULTS

Overstatement of compliance with the BCGG-2006 in annual reports

The minimum and maximum values of both ReportedCG and SurveyCG are 3 and 20

respectively. One company has a ReportedCG value 3. Although this company does not

include the ‘comply box’ in its annual report, disclosures about the board of directors and

external auditors in annual reports indicate compliance with three provisions of the BCGG-

2006. On the other hand, one other company has a SurveyCG value 3. This additional

company also does not actually comply with the BCGG-2006 but scores three because it has

a board of directors which complies with three provisions of the BCGG-2006. With respect to

the maximum values of ReportedCG and SurveyCG, eight and five companies have a

maximum ReportedCG and SurveyCG score respectively. The ReportedCG and SurveyCG

values of the other companies remain within the range of 3 - 20. Although no company has a

28

SurveyCG value greater than ReportedCG, detailed analysis shows that a few companies

state compliance in the survey only with respect to few individual provisions.

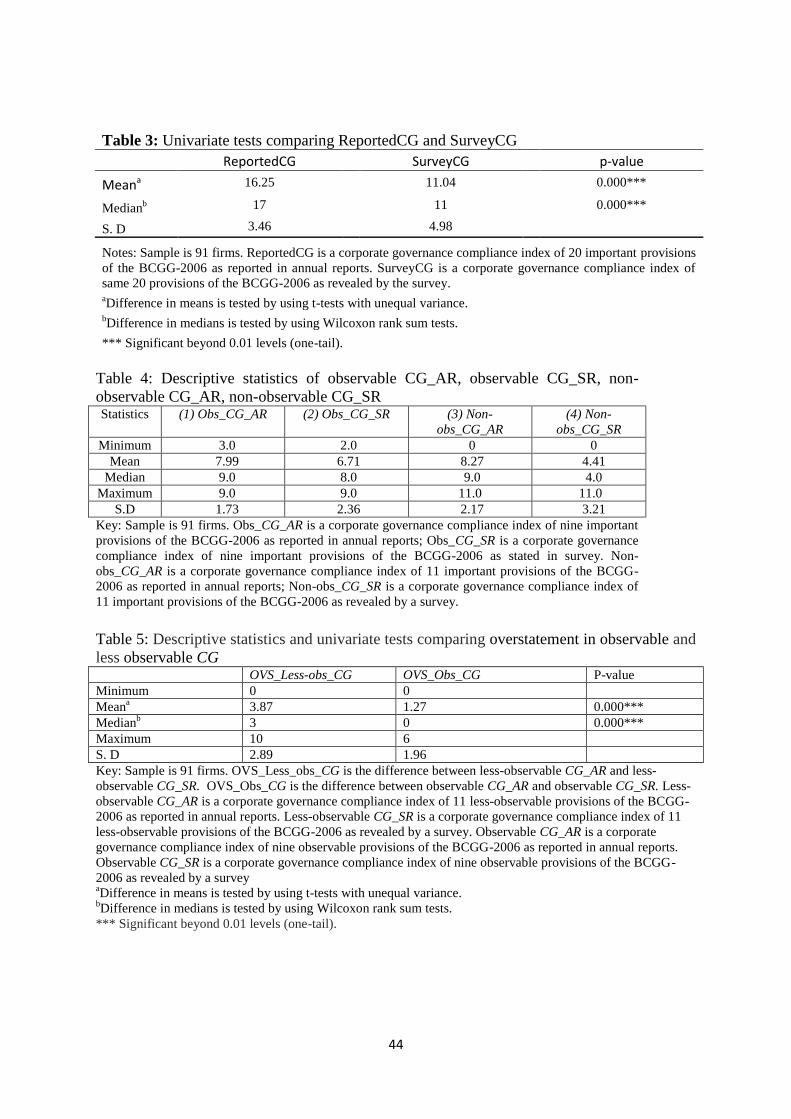

We tested the difference between ReportedCG and SurveyCG using a t-test on the

means and a Wilcoxon rank-sum test on the medians (see Table 3). Our results show that the

mean (median) of ReportedCG is significantly greater than the mean (median) of SurveyCG

at less than 0.01 level. Our results, thus, support H1.

<Insert table 3 here>

Overstatement of compliance with the BCGG-2006 in annual reports is more

pronounced with respect to less observable provisions

Table 4 presents descriptive statistics of observable CG_AR, less observable CG_AR,

observable CG_SR and less observable CG_SR. The mean (median) values of less

observable CG and observable CG based on as reported in annual reports and as stated in the

survey indicates that the gap between less observable CG as reported in annual reports and as

stated in the survey is higher than the gap between observable CG as reported in annual

reports and as stated in the survey.

<Insert table 4 here>

The result of tests comparing overstatement with respect to less observable and

observable provisions of the BCGG-2006 is presented in Table 5.

<Insert table 5 here>

Table 5 shows that the mean and median of overstatement in non-observable CG are

significantly higher than that of overstatement in observable CG at the 0.01 level. This

evidence provides support for Hypothesis 2 that overstatement of compliance in annual

reports is more pronounced with respect to less observable provisions.

Association of overstatement of compliance with the BCGG-2006 in

annual reports with family control and presence of blockholders

The value of the overstatement statistic

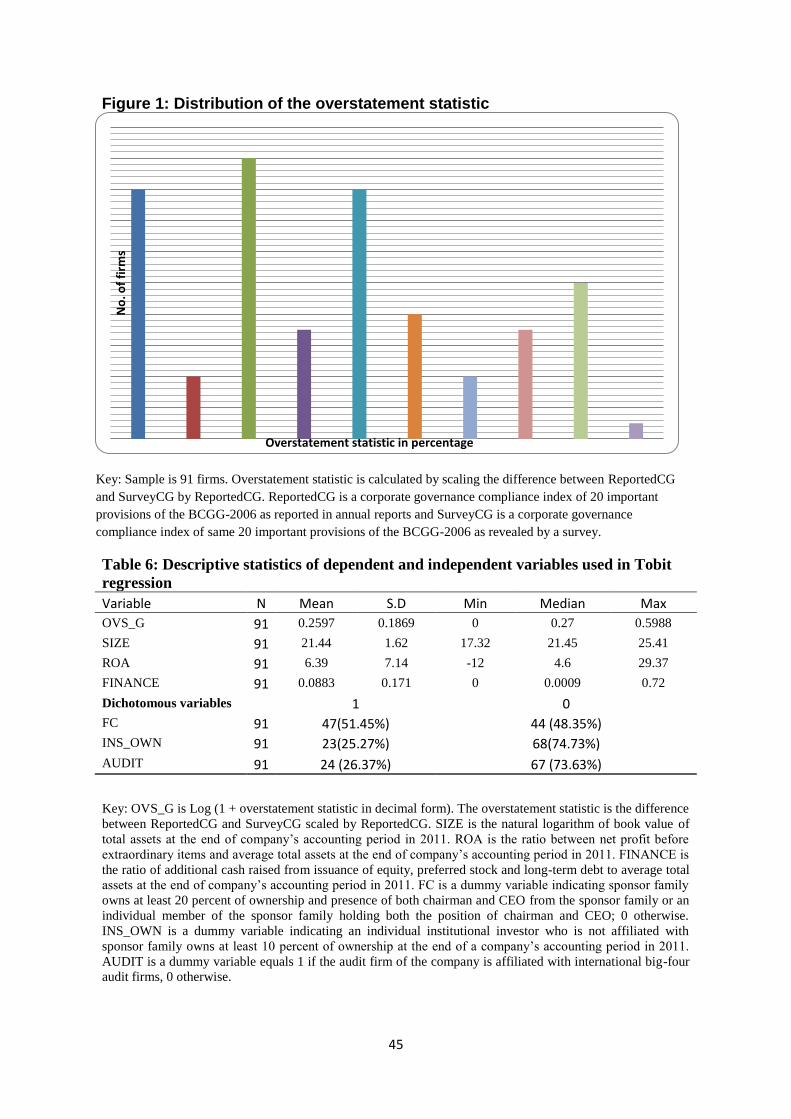

The value of the overstatement statistic as a percentage is presented in a bar diagram

in Figure 1. Figure 1 show that 16 firms do not overstate compliance in their annual reports

and have an overstatement statistic of equal to zero. However, the remaining 75 companies

29

have a positive overstatement statistic. The mean (median) of the overstatement statistic is

31.92 (31.25) per cent and standard deviation is 24.87 per cent. This result suggests that, on

average, the level of compliance reported in the annual reports is not a very good reflection of

underlying compliance with the BCGG-2006. The maximum value of the overstatement

statistic is 82.352 per cent. The distribution of the overstatement statistic is truncated at the

lower bound of zero and is not symmetric. Hence, for incorporation in statistical tests, 1 is

added to the overstatement statistic in decimal form and then log is taken on the resulting

variable3. This log (1+ overstatement statistic in decimal form) (OVS_G) is used as the

dependent variable in Tobit model.

<Insert figure 1 here>

Descriptive statistics

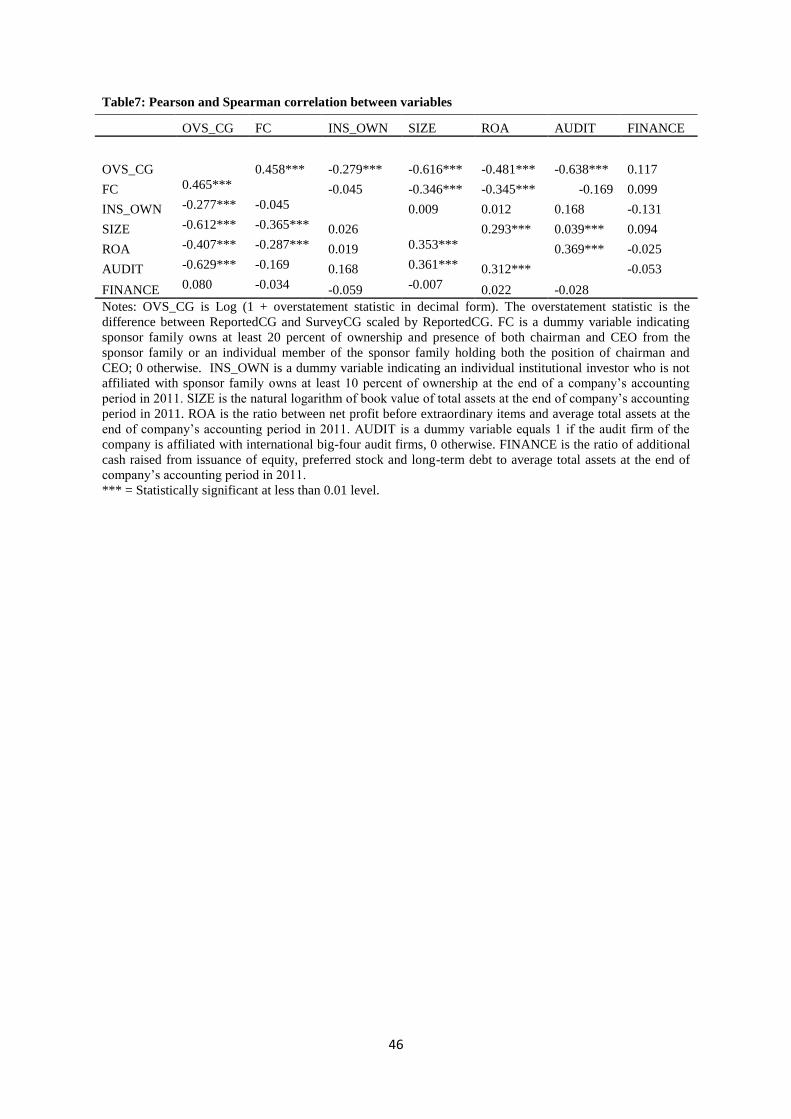

Table 6 presents descriptive statistics for OVS_CG and independent variables used in

Tobit regression. Table 6 shows that the mean (median) of OVS_CG is 0.2597 (0.2700). The

sponsor family owns at least 20 per cent of shares and sponsor family members occupy both

the positions of chairman and CEO in the case of 51.45 percent of sample firms. An

institutional investor owns at least 10 percent of ownership in 25.27 percent of sample

companies. The mean (median) size of firms is 21.44 (21.45). The mean (median)

profitability of firms is 6.39 (4.60) percent. The mean (median) FINANCE is 0.0883 (0.0009)

indicating that sample firms raise minimum percentage of funds by issuing equity, preference

shares and long-term debt. Finally, 26.37 percent of sample firms are audited by audit firms

affiliated with an international big-four audit firm.

<Insert table 6 here>

Correlation analysis

Table 7 presents the correlation coefficients between variables used in Tobit

regression. OVS_CG is positively correlated with FC. The correlation coefficient is

significant at the 0.01 level. This result provides initial evidence for H3. OVS_CG is

negatively correlated with INS_OWN at the 0.01 level. This evidence provides preliminary

supports for H4. SIZE, ROA and AUDITOR are negatively correlated with OVS_CG and all

2 The overstatement statistic cannot be 1 because it is obvious for firms to report several items of the BCGG-

2006 such as name of the chairman, CEO and members of board which indicates compliance with provisions

related to separation of CEO, board size and composition. 3 See Woolridge (2002) p. 671 on linearization of a truncated distribution.

30

coefficients are significant at the 0.01 level. FINANCE does not have any significant

correlation with OVS_CG. Among the independent variables, FC is significantly negatively

correlated with SIZE and ROA. This is in line with prior research and suggests that family

controlled firms are on average small in size and less profitable (Faccio et al., 2001).

Furthermore, there are significant correlations between ROA and SIZE; ROA and AUDIT;

and SIZE and AUDIT which is consistent with prior studies (Abbott and Parker, 2000;

Johansen et al., 2013). However, none of the correlation coefficients between independent

variables is greater than (the absolute value of) 0.40. This indicates that multicolinearity is

not a serious issue here.

<Insert table 6 here>

Multiple regression

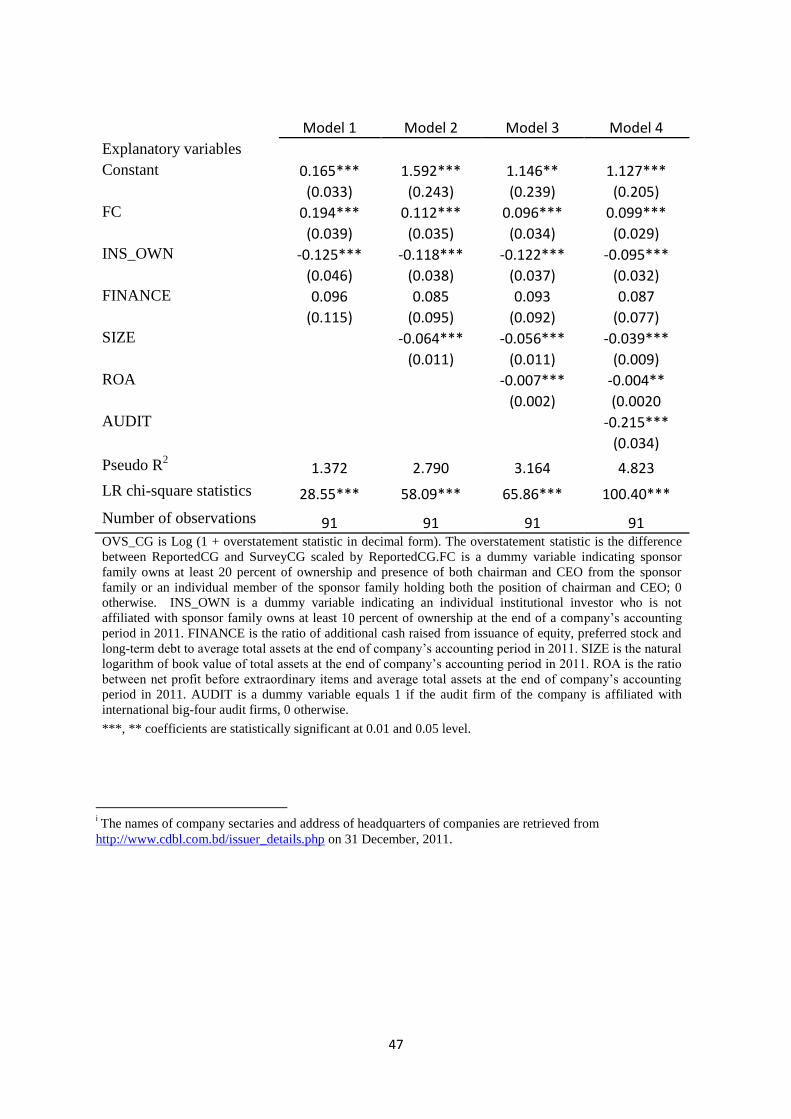

Table 7 shows the results of the analysis of the influence of control by sponsor family

and control by institutional investors on overstatement of compliance with the BCGG-2006 in

annual reports. As FC is significantly correlated with SIZE and ROA and there are significant

correlations between ROA and SIZE; ROA and AUDIT; and SIZE and AUDIT, we estimate

four different versions of tobit model with varying explanatory variables.

<Insert table 7 here>

The results in Model 1 show that the coefficient of FC is positive and significant at less

than the 0.01 level, indicating that control by sponsor family is positively associated with the

overstatement of compliance with the BCGG-2006 in annual reports. This result provides

support for H3. The results in Model 1 also reveal that the coefficient of INS_OWN is

negative and significant at less than the 0.01 level. This result supports H4ly. The coefficient

of FINACE is not significant at 0.10 level. This evidence suggests that companies that raise

cash by issuing equity, preference shares and long-term debt do not overstate compliance

with the BCGG-2006 more than other firms.

In Model 2, we further control for SIZE. There is no change in sign and significance of

coefficients of FC and INS_OWN. The coefficient on SIZE is negative and significant at the

31

0.01 level. This is not surprising given that larger firms are subject to closer scrutiny by

investment community (Richarson et al., 2003), media (Miller, 2006) and regulators (Reverte,

2009) and larger firms more likely provide credible and trustworthy accounting reports in

order to maintain their reputation (Cao et al., 2012).

In Model 3, when ROA is included as a control variable, there is again no change in sign

and significance of coefficients of FC and INS_OWN. The coefficient of ROA is negative

and significant at 0.01 level. This is consistent with previous evidence that profitable firms

have better CG structure in place (Linck, Netter & Yang, 2008; Coles, Daniel & Naveen, 2008)

and better accounting reporting quality (Cheng and Courtenay, 2006). In model 4, we add

AUDIT as a control variable. Again there is no change in sign and significance of

coefficients of FC and INS_OWN. The coefficient of AUDIT is negatively significant at 0.01

level. This is consistent with prior evidence that large audit firms plays strong CG role (e.g.,

Gul, Kim, & Qiu, 2010) and quality of auditor is positive related with the quality of accounting

disclosure (e.g., Bassett, Koh and Tutticci, 2007).

Four models with different control variables in table 7 provide consistent evidence that

FC is positively and INS_OWN is negatively significantly associated with OVS_CG. These

results provide support for H3 and H4.

8.6 Summary and concluding remarks

This study focuses on the overstatement of compliance with the BCGG-2006 as

reported in annual reports and the association between the extent of this overstatement and

firms’ control characteristics. This study finds that compliance with the BCGG-2006 as

reported in annual reports is significantly higher than the compliance as stated in a survey.

Moreover, this study finds that the overstatement of compliance with the BCGG-2006 in

annual reports is more pronounced with respect to non-observable provisions than observable

provisions. This is probably because firms cannot easily change their internal authority

relationship but are aware of the consequences of disclosure of non-compliance such as

regulatory pressures from the BSEC and stock exchanges. The results indicate that firms

report compliance with the BCGG-2006 in annual reports without actual implementation.

This is consistent with our argument that regulatory pressures for improving CG without

changing other related institutional factors lead to overstatement of compliance. Thus, users

cannot rely solely on the disclosures of compliance in annual reports to evaluate whether the

companies are actually complying with the provisions of the BCGG-2006 and have a sound

CG structure in place.

32

Furthermore, this study finds that overstatement of compliance in annual reports is

positively associated with control by sponsor family. These results hold after taking into

consideration a number of control variables. The firms under control of sponsor families may

find it legitimate not to comply with specific provisions of the BCGG-2006 on the grounds of

protection of organization interest and protection of socio-political wealth of the family.

However, in order to avoid undesirable consequences (e.g., delisting from stock exchanges)

of non-compliance, firms under control of sponsor families report compliance with the

provisions of the BCGG-2006 in annual reports. The positive association between

overstatement of compliance in annual reports and control by sponsor family is in line with

previous findings that family controlled companies maintain a weaker CG structure

(Anderson and Reeb, 2004; Chen, Chen and Cheng, 2008; Chen and Nowland, 2010).

Finally, this study finds that overstatement of compliance in annual reports is

negatively significantly associated with institutional ownership. This result is consistent with

prior research on institutional investors in developed countries (Elyasiani and Jia, 2010;

Solomon and Solomon, 2006; Hartzell and Starks, 2003). In respect of Bangladesh, this result

supports Farooque et al. (2007) that institutional owner owning significant ownership can

exert pressure for better governance.

An important limitation of the results showing an association between overstatement

of compliance with the BCGG-2006 and control by sponsor family is the likely endogeneity

of control by the sponsor family. This study does not address the issue of causality directly

because it uses survey data. Survey data by nature are cross-sectional (Van der Stede, 2013).

Hence, several econometric tests of causality (e.g., the effect of change in control by sponsor

families on change in overstatement of compliance with the BCGG-2006 in annual reports

(Woodward, 2003, pp. 35-36) cannot be performed. Furthermore, there is no plausible

instrument for control by sponsor families. However, control by the sponsor families is

unlikely to be endogenous because family control is a general pattern of control in

Bangladesh (Haque et al., 2011). Moreover, the BCGG-2006 was introduced in 2006,

indicating that overstatement of compliance with the BCGG-2006 in annual reports is not the

cause of control by sponsor families.

We further acknowledge that there may be number of additional logics that can affect

the extent of overstatements such as directors’ training and educational qualifications.

However, given the data availability, we cannot test that impact. Finally, arguments behind

33

some of our hypotheses are consistent with agency theory, but none of these arguments

contradicts with institutional logic approach.

References

ADB. 1997. Report and recommendation of the president to the board of directors on a

proposed loan and technical assistance grants to the People’s Republic of Bangladesh

for the capital market development program. The Asian Development Bank.

ADB. 2005. Program performance audit report, capital market development program (Loan

1580-BAN [SF]) in Bangladesh. The Asian Development Bank. Available at

http://www.adb.org/sites/default/files/ppar-ban-24103.pdf (accessed January 30,

2012)

Aguilera, R. V. & Cuervo-Cazurra, A. 2004. Codes of good governance worldwide: What is

the trigger?. Organization Studies, 25(3): 415-443.

Aguilera, R. V., Filatotchev, I., Gospel, H., & Jackson, G. 2008. An organizational approach

to comparative corporate governance: Costs, contingencies, and complementarities.

Organization Science, 19(3), 475-492.

Aguilera, R. V. & Jackson, G. 2003. The cross-national diversity of corporate governance:

Dimensions and determinants. Academy of Management Review, 28(3): 447-465.

Aguilera, R. V. & Jackson, G. 2010. Comparative and international corporate governance.

The Academy of Management Annals, 4(1): 485-556.

Ahmed, K. & Nicholls, D. 1994. The impact of non-financial company characteristics on

mandatory disclosure compliance in developing countries: The case of Bangladesh,

The International Journal of Accounting, 29(3): 62-77.

Akhtaruddin, M. 2005. Corporate mandatory disclosure practices in Bangladesh. The

International Journal of Accounting, 40(4): 399-422.

Akkermans, D., Van Ees, H., Hermes, N., Hooghiemstra, R., Van der Laan, G., Postma, T., &

Van Witteloostuijn, A. 2007. Corporate governance in the Netherlands: An overview

of the application of the Tabaksblat Code in 2004. Corporate Governance: An

International Review, 15(6): 1106-1118.

Aldrich, H. E. & Fiol, C. M. 1994. Fools rush in? The institutional context of industry

creation. Academy of Management Review, 19(4): 645-670.

Alon, A. 2013. Complexity and dual institutionality: The case of IFRS adoption in Russia.

Corporate Governance: An International Review, 21(1): 42-57.

Ammann, M., Oesch, D., & Schmid, M. M. 2011. Corporate governance and firm value:

International evidence, Journal of Empirical Finance, 18(1):36-55.

Anderson, R.C. & Reeb, D.M. 2004. Board composition: Balancing family influence in

S&P 500 firms, Administrative Science Quarterly, 49(2): 209-237.

Arcot, S., Bruno, V., & Faure-Grimaud, A. 2010. Corporate governance in the UK:

Is the comply or explain approach working? International Review of Law and

Economics, 30(2): 193–201.

Aurini, J. 2006. Crafting legitimation projects: An institutional analysis of private education

businesses. Sociological Forum, 21(1): 83-111.

Bassett, M., Koh, P., & Tutticci, I. 2007. The association between employee stock option

disclosures and corporate governance: Evidence from an enhanced disclosure regime,

The British Accounting Review, 39(4): 303–322.

Bates, K. & Hennessy, D. 2010. Tilting at windmills or contested norms? Dissident proxy

initiatives in Canada. Corporate Governance: An International Review, 18(4): 360-

375.

34

Bebchuk, L. A., Cohen, A., & Ferrell, A. 2009. What matters in corporate governance? The

Review of Financial Studies, 22(2): 783-827.

Bebchuk, L. A. & Roe, M. J. 1999. A theory of path dependence in corporate ownership and

governance. Stanford Law Review, 52(1): 127-170.

BEI. 2003. Comparative analysis of corporate governance in South Asia: Charting a roadmap

for Bangladesh, Bangladesh Enterprise Institute. Available at

http://www.bei-bd.org/downloadreports/publicationdownload/67/download (accessed

11 February, 2011).

BEI, 2004. 2004. The code of corporate governance for Bangladesh, Bangladesh Enterprise

Institute. Available at http://www.ecgi.org/codes/documents/code.pdf (accesses 11

February, 2011).

Belal, A.R. & Cooper, S. 2011. The absence of corporate social responsibility reporting in

Bangladesh, Critical Perspectives on Accounting, 22(7): 654– 667.

Beneish, M. 1999. Incentives and penalties related to earnings overstatements that violate

GAAP. The Accounting Review, 74(4): 425–457.

Bhagat, S., Bolton, B., & Romano, R. 2008. The promise and peril of corporate governance

indices, Columbia Law Review, 108(8): 1803-1882.

Black, B.S., De Carvalho, A.G. and Gorga. 2012. What matters and for which firms for

corporate governance in emerging markets? Evidence from Brazil (and other BRIK

Countries), Journal of Corporate Finance, 18(4): 934-952.

Boxenbaum, E., & Pedersen, S. J. 2009. Scandinavian institutionalism – a case of

institutional work. In T. B. Lawrence, R. Suddaby & B. Leca (Eds.), Institutional

work: 178–204. Cambridge, UK: Cambridge University Press.

Briscoe, F. & Murphy, C. 2012. Sleight of hand? Practice opacity, third-party responses, and

the interorganizational diffusion of controversial practices. Administrative Science

Quarterly, 57(4): 553-584.

Broadbent, J., Jacobs, K., & Laughlin, R. 2001. Organisational resistance strategies to

unwanted accounting and finance changes: the case of general medical practice in the

UK. Accounting, Auditing & Accountability Journal, 14(5): 565-586.

Bromley, P., Hwang, H., & Powell, W. W. 2013. Decoupling revisited: Common pressures,

divergent strategies in the US nonprofit sector. M@ n@ gement, 15(5): 469-501.

Burns, N. & Kedia, S. 2006. The impact of performance-based compensation on

misreporting.

Journal of Financial Economics, 79(), 35–67.

Cao, Y., Myers, L. A., & Omer, T. C. 2012. Does company reputation matter for financial