Embed Size (px)

Citation preview

Japan-Cambodia Association

Tokyo, Japan

February 08th, 2016

1

Investment Seminar

Economic Situation and

Investment Policy in Cambodia

Contents

2

1. Robust Economy

2. Strong FDIPerformance

3. Why Cambodia?

4. Ways forward

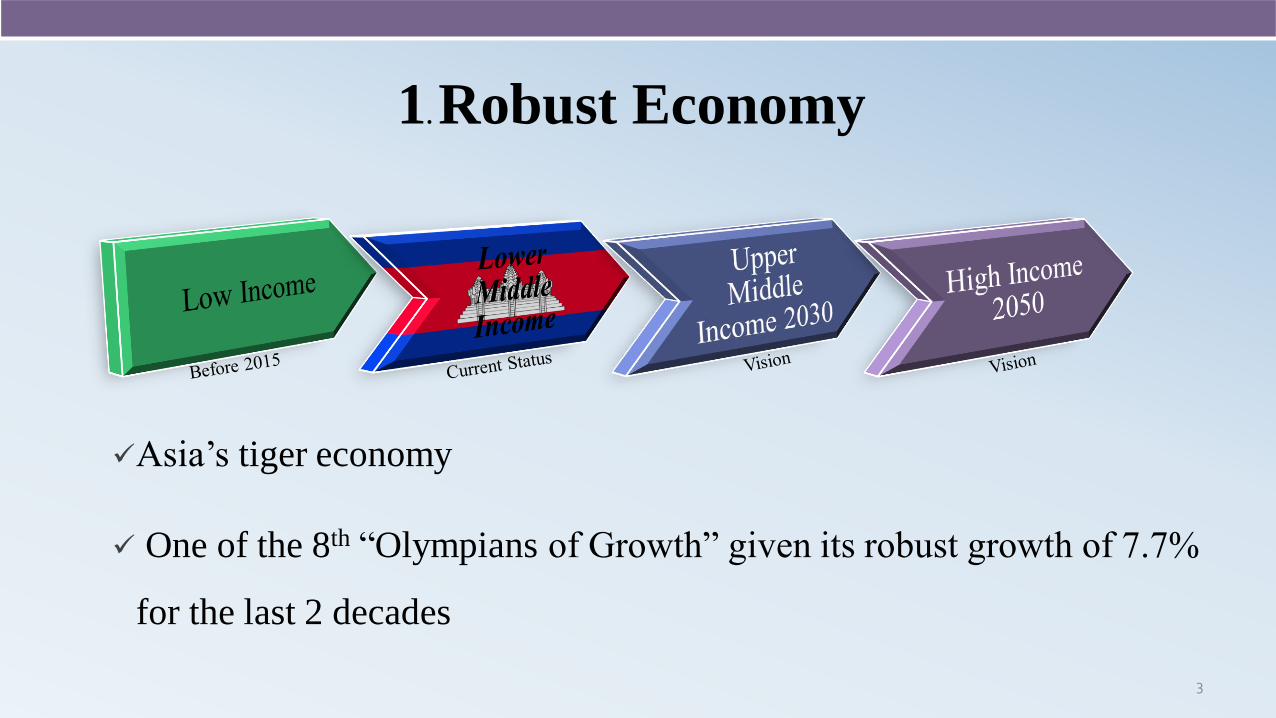

3

Asia’s tiger economy

One of the 8th “Olympians of Growth” given its robust growth of 7.7%

for the last 2 decades

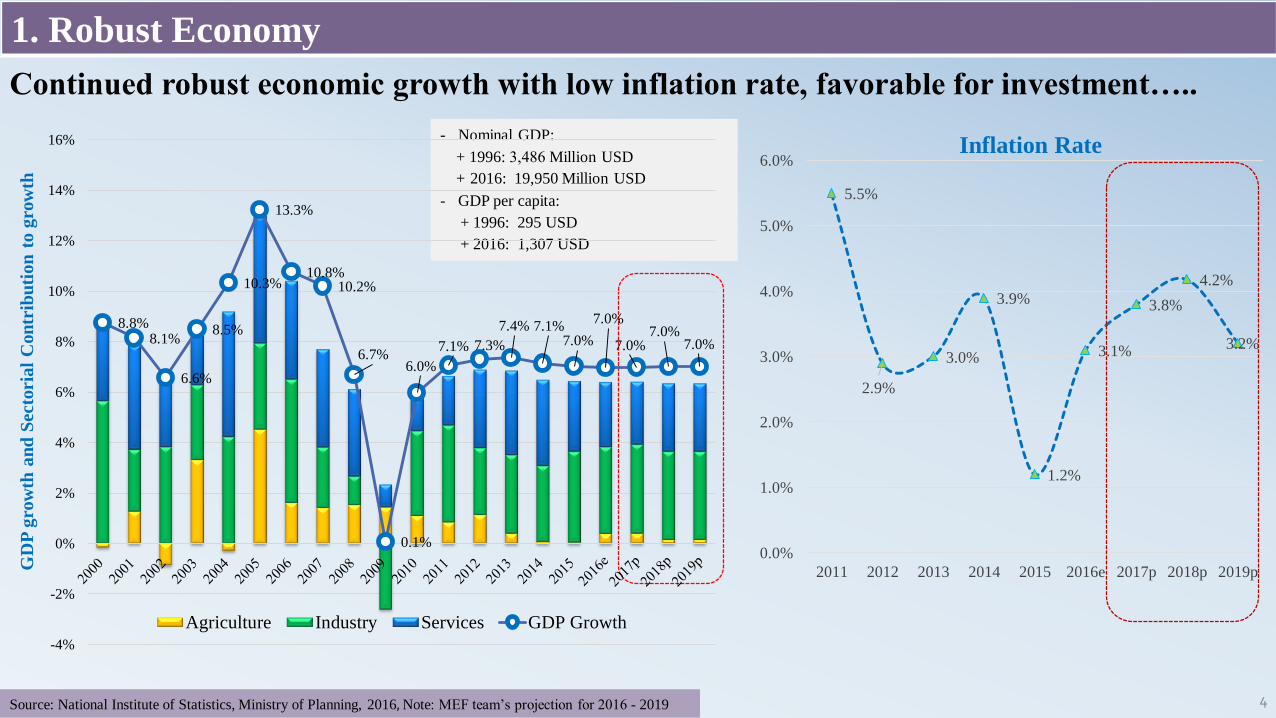

1. Robust Economy

Continued robust economic growth with low inflation rate, favorable for investment…..

Source: National Institute of Statistics, Ministry of Planning, 2016, Note: MEF team’s projection for 2016 - 2019

GD

P g

row

th a

nd

Secto

ria

l C

on

trib

uti

on

to g

row

th

- Nominal GDP:

+ 1996: 3,486 Million USD

+ 2016: 19,950 Million USD

- GDP per capita:

+ 1996: 295 USD

+ 2016: 1,307 USD

4

Inflation Rate

1. Robust Economy

5.5%

2.9%

3.0%

3.9%

1.2%

3.1%

3.8%

4.2%

3.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2011 2012 2013 2014 2015 2016e 2017p 2018p 2019p

8.8%8.1%

6.6%

8.5%

10.3%

13.3%

10.8%10.2%

6.7%

0.1%

6.0%

7.1% 7.3%

7.4% 7.1%7.0%

7.0%

7.0%7.0%

7.0%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Agriculture Industry Services GDP Growth

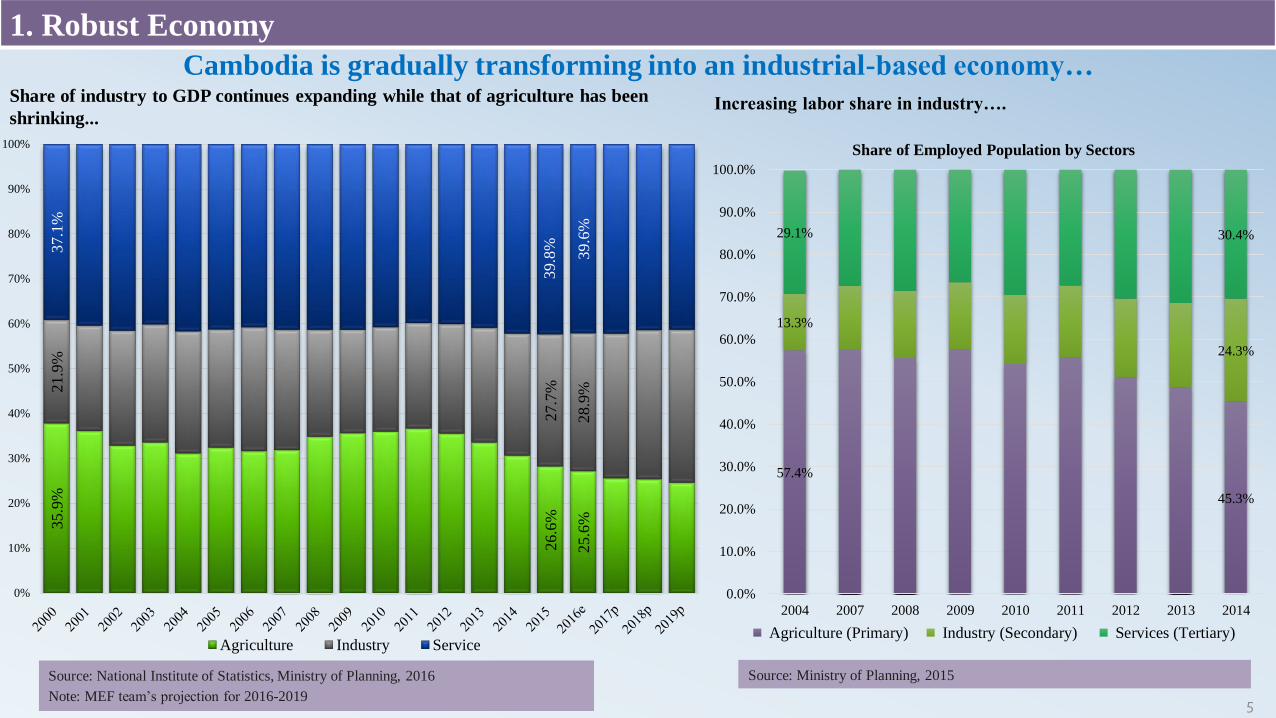

Cambodia is gradually transforming into an industrial-based economy…

Source: National Institute of Statistics, Ministry of Planning, 2016

Note: MEF team’s projection for 2016-2019

57.4%

45.3%

13.3%

24.3%

29.1% 30.4%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2004 2007 2008 2009 2010 2011 2012 2013 2014

Agriculture (Primary) Industry (Secondary) Services (Tertiary)

Share of Employed Population by Sectors

Increasing labor share in industry….

Source: Ministry of Planning, 2015

5

1. Robust Economy35.9

%

26.6

%

25.6

%

21

.9%

27.7

%

28.9

%

37.1

%

39.8

%

39.6

%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Agriculture Industry Service

Share of industry to GDP continues expanding while that of agriculture has been

shrinking...

Increased domestic production has been observed in sectors such as food, beverages, light manufacturing…

6Source: National Institute of Statistics, Ministry of Planning, 2016, Note: MEF team’s projection for 2016 - 2017

Gro

wth

in

Per

cen

t

1. Robust Economy

19

.9%

6.5

%

10

.7%

6.6

%

9.8

%

8.4

%

8.5

%

7.9%

18.2%

13.7%

21.4%

19.2%

15.9%

14.1%6

.2%

10

.2%

8.4

%

9.6

%

9.3

%

11

.6%

12

.3%

14.5%

9.3%10.7%

10.1%

11.7%10.7% 10.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2011 2012 2013 2014 2015 2016e 2017p

Garment Construction Other industry Industry Sector

Export Diversification: From garment to rice and others (electronic, bicycles...)

Source: Ministry of Economy and Finance, 2016

7

1. Robust Economy

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

88.8% 86.4% 82.0% 77.1% 73.5% 73.7% 73.1%

7.8% 7.4% 12.6% 16.6% 21.5% 21.1% 22.3%

Export by Products

Garment Rice Rubber Others (Electronic components, bicycles, etc.)

Source: Ministry of Economy and Finance, 2016

Export Diversification: From export to the US to export to EU, Japan,...

8

1. Robust Economy

4.5% 6.2% 7.2% 9.3% 11.7% 11.1% 10.3%

25.0%30.0% 32.1%

33.4%34.1% 37.9% 38.8%

52.3% 42.6% 36.7% 31.4% 26.7% 23.9% 20.9%

2.4%3.1%

3.5% 4.8% 5.7% 6.8%8.2%

15.7% 18.1% 20.5% 21.1% 21.8% 20.2% 21.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

Share of Export Value by Countries

ASEAN EU USA JAPAN Others

9

2. Strong FDI Performance

Robust Economy

Strong Policy

Support

Favorable Investment Condition

Source: National Bank of Cambodia, 2016

Strong FDI performance, on the back of sound macroeconomic environment, favorable investment climate and

supporting policies…….

10

2. Strong FDI Performance

31.2%

9.3%8.6%

7.4%

7.1%

5.0%

4.4%

4.3%

4.1%

2.7%

China

Vietnam

Korea

Malaysia

Taiwan

Singapore

Hong Kong

Japan

Thailand

UK

Top 10 Investors in 2015

15.4%

26.2%

18.9%

9.3%

3.6%

13.5%

Major Investment Sectors, in 2015

Agriculture Manufacturing Financial ActivitiesAccommodation Telecom Hydropower

o.w: Garment 22.2%

Sh

are

of

Tota

l In

ves

tmen

t In

flow

928

1,342 1,372

1,835 1,872

1,720 1,701

2,167

9.8%

44.6%

2.3%

33.7%

2.0%

-8.1%

-1.1%

27.4%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

-

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013 2014 2015 2016E

USD

Mill

ion

FDI Inflow Change in %

11

2. Strong FDI Performance

An increasing wave of Japanese Investment

into Special Economics Zone directly from

Japan and relocation from other countries.

Minebea is building its third factory for in-

house part production in addition to the

existing two factory, signify its operations

toward more value-added products.

Reflection

The effect of Economic Corridor (Myanmar,

Thailand and Vietnam) on regional connection

and integration.

Cambodia is becoming more conducive to

investment with the policy to reduce footloose

investment and move up the value chain.

An increasing wave of Japanese investment, reflecting the increased investor confidence in Cambodia …

12

3. Why Cambodia?

Open Economy with Sound Macroeconomic Environment

Competitive Investment Conditions

Market access

Strategic location

Attractive FDI Promotion Policies

Open Economy with Sound Macroeconomic Environment

- Robust GDP growth

- Low inflation rate

- Fast growing middle class

Low Labor Cost

US$ 153 in 2017

Demographic Dividend

- Young and dynamic labor force

(median age 24 years old)

- 60% of population under 30 years

in 2015

High Market Access

- MFN/GSP: from major trading partners

such as EU, the USA, Japan, Canada and

Australia

- Market access to EU: “Everything But

Arms (EBA)”

- Member of ASEAN, RCEP and WTO

Very Competitive and Favorable Investment Conditions…

13

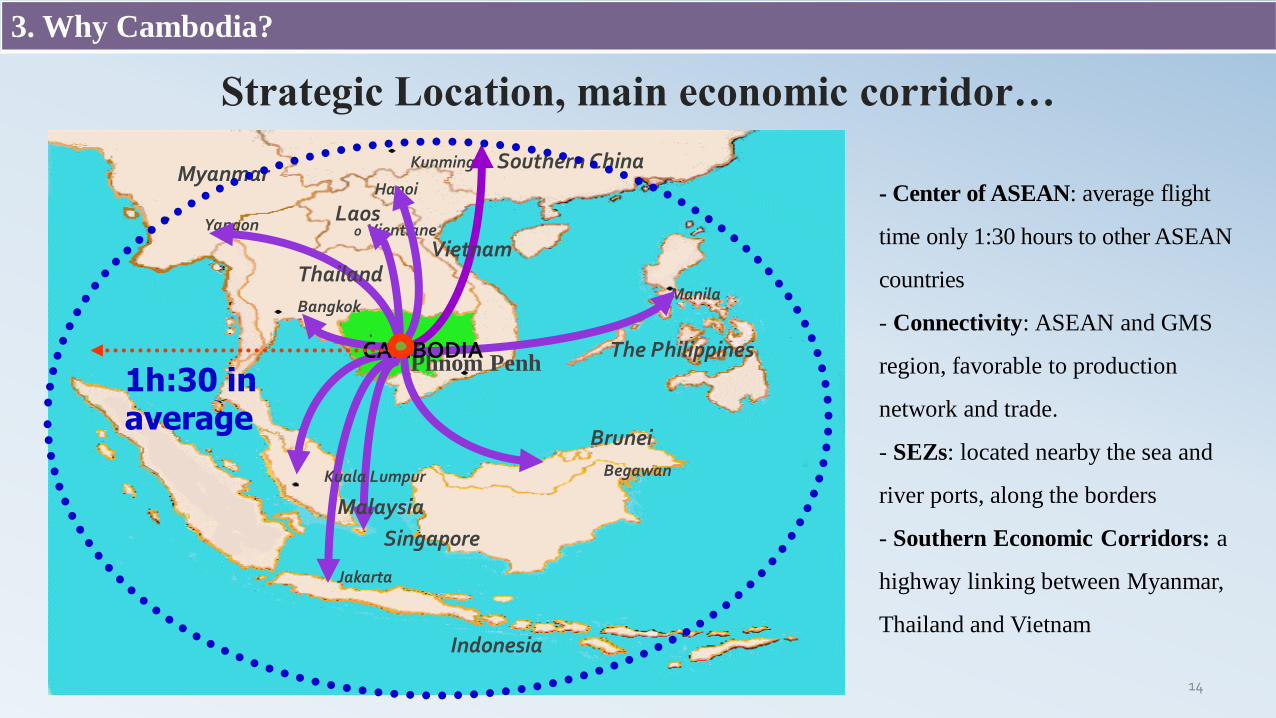

3. Why Cambodia?

.

Phnom PenhThe Philippines

Singapore

Indonesia

MyanmarSouthern China

ManilaBangkok

Kunming

Yangon

Brunei

Jakarta

Begawan

Hanoi

Laoso Vientiane

CAMBODIA

Malaysia

Kuala Lumpur

ThailandVietnam

1h:30 in average

Strategic Location, main economic corridor…

14

- Center of ASEAN: average flight

time only 1:30 hours to other ASEAN

countries

- Connectivity: ASEAN and GMS

region, favorable to production

network and trade.

- SEZs: located nearby the sea and

river ports, along the borders

- Southern Economic Corridors: a

highway linking between Myanmar,

Thailand and Vietnam

3. Why Cambodia?

3. Why Invest in Cambodia?

Investment and Trade Facilitation

- One Stop Service: CDC, sole organization for investment activities

- Fast track investment approval within 28 days

- National Single Window: Trade and transport with a single entry points

- Japanese Desk: Special service for the rising of Japanese Investors

- Authorized Economic Operators

Investment Guarantee

- Equal Treatment of All Investors

- No Requirement of Local Equity Participation

- No Price Controls on Products or Services

- No Restriction on Forex Convertibility

- Free Remittance of Foreign Currencies Abroad

Investment Incentive

- 20% Corporate Tax : Lower than regional average

-Tax holidays up to 9 years

- Full Import Duty Exemption

- Repatriation of profit/Reinvestment of earning

- 100% exemption of export tax

- Loss carried Forward up to 5 years.

FDI Promotion

Policies

15

0 5 10 15 20 25 30 35

Customs and trade regulations

Courts

Crime, theft and disorder

Business licensing and permits

Electricity

Corruption

Access to finance

Biggest obstacle to operate in Cambodia, in % of firms

2016 2013 2007

Source: Enterprise Surveys, World Bank

Business environment has been greatly improved……

16

3. Why Invest in Cambodia?

17

4. Ways Forward

18

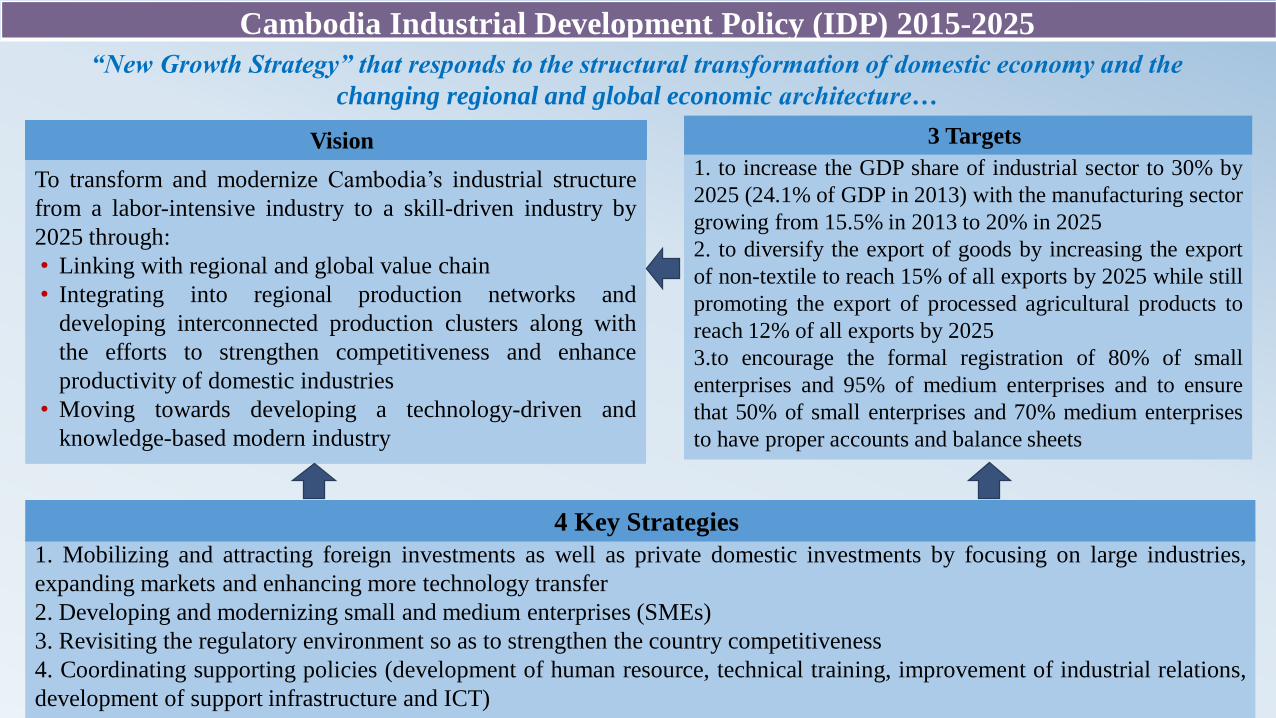

Vision

StrategiesTo transform and modernize Cambodia’s industrial structure

from a labor-intensive industry to a skill-driven industry by

2025 through:

• Linking with regional and global value chain

• Integrating into regional production networks and

developing interconnected production clusters along with

the efforts to strengthen competitiveness and enhance

productivity of domestic industries

• Moving towards developing a technology-driven and

knowledge-based modern industry

Vision

1. Mobilizing and attracting foreign investments as well as private domestic investments by focusing on large industries,

expanding markets and enhancing more technology transfer

2. Developing and modernizing small and medium enterprises (SMEs)

3. Revisiting the regulatory environment so as to strengthen the country competitiveness

4. Coordinating supporting policies (development of human resource, technical training, improvement of industrial relations,

development of support infrastructure and ICT)

4 Key Strategies

1. to increase the GDP share of industrial sector to 30% by

2025 (24.1% of GDP in 2013) with the manufacturing sector

growing from 15.5% in 2013 to 20% in 2025

2. to diversify the export of goods by increasing the export

of non-textile to reach 15% of all exports by 2025 while still

promoting the export of processed agricultural products to

reach 12% of all exports by 2025

3.to encourage the formal registration of 80% of small

enterprises and 95% of medium enterprises and to ensure

that 50% of small enterprises and 70% medium enterprises

to have proper accounts and balance sheets

3 Targets

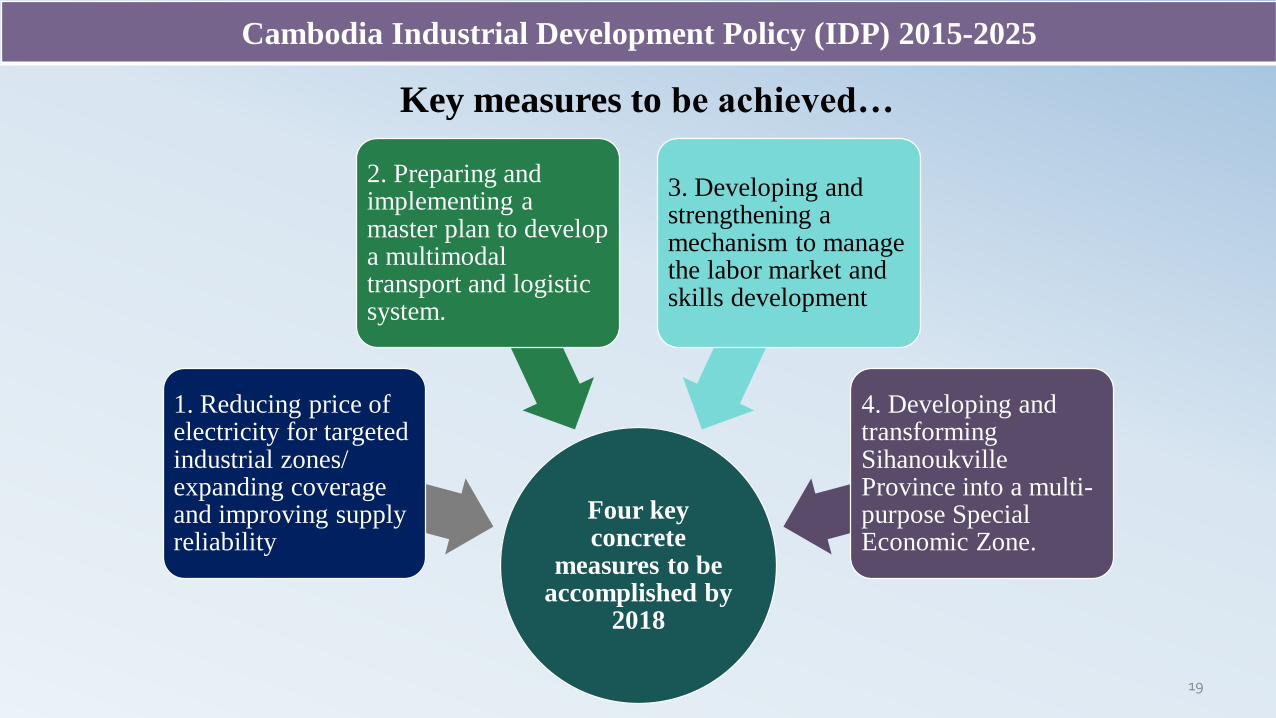

Cambodia Industrial Development Policy (IDP) 2015-2025

“New Growth Strategy” that responds to the structural transformation of domestic economy and the

changing regional and global economic architecture…

Key measures to be achieved…

Four key concrete

measures to be accomplished by

2018

1. Reducing price of electricity for targeted industrial zones/ expanding coverage and improving supply reliability

2. Preparing and implementing a master plan to develop a multimodal transport and logistic system.

3. Developing and strengthening a mechanism to manage the labor market and skills development

4. Developing and transforming SihanoukvilleProvince into a multi-purpose Special Economic Zone.

19

Cambodia Industrial Development Policy (IDP) 2015-2025

Priority Investment Opportunities

20

New Industries

• Electronic assembly

• Natural resources processing

• High Valued Added Garment Products

• Industrial equipment assembly

Supporting Industry

• SMEs Supporting Industry

• Light Manufacturing

• Construction materials

• Food and Beverage

• Packaging equipment for export

• Transport and Logistic

Agro-Industrial

• For Export and Domestic Market

Other Sectors

• Tourism sector

• Human Resource Development

• Information technology and telecommunication

• Energy Development

• Furniture manufacturing

• Traditional Handicraft

Cambodia Industrial Development Policy (IDP) 2015-2025

21

Strategic Development by Region…

Cambodia Industrial Development Policy (IDP) 2015-2025

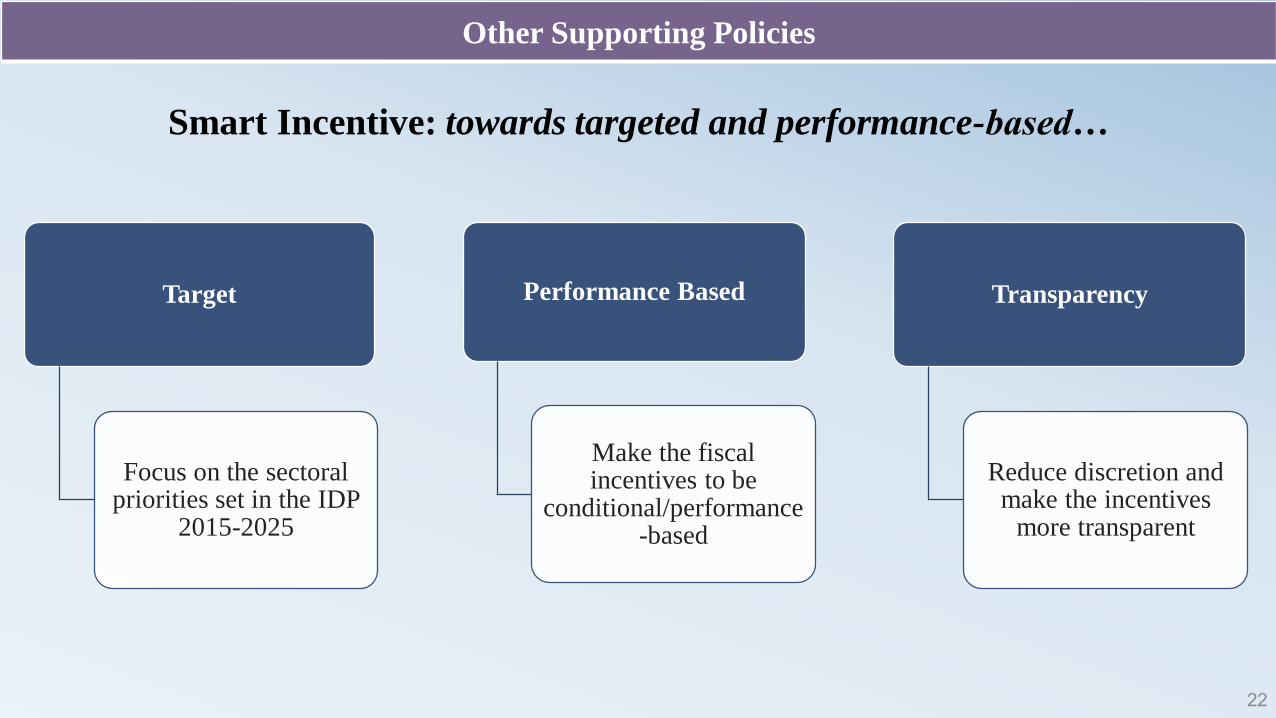

Smart Incentive: towards targeted and performance-based…

22

Other Supporting Policies

Target

Focus on the sectoral priorities set in the IDP

2015-2025

Performance Based

Make the fiscal incentives to be

conditional/performance-based

Transparency

Reduce discretion and make the incentives

more transparent

23

• Amendment of Law on Investment

• Master Plan on Infrastructure Development

• Financial Investment: derivative trading has been executed.

• Law on Government Securities is already in place.

• Bond market is being developed.

• T-bill is another long-term policy under consideration

• Promoting Authorized Economic Operator (AEO): for easier passage of products across the country’s borders.

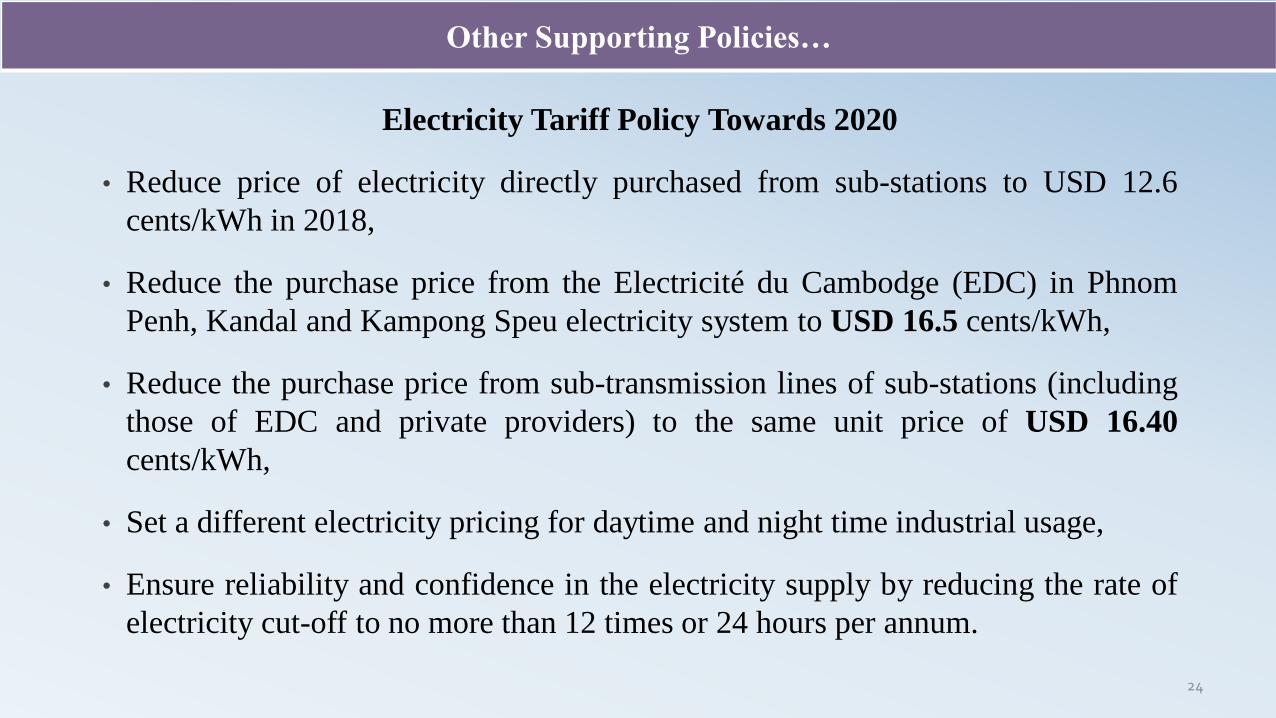

Other Supporting Policies…

Electricity Tariff Policy Towards 2020

• Reduce price of electricity directly purchased from sub-stations to USD 12.6

cents/kWh in 2018,

• Reduce the purchase price from the Electricité du Cambodge (EDC) in Phnom

Penh, Kandal and Kampong Speu electricity system to USD 16.5 cents/kWh,

• Reduce the purchase price from sub-transmission lines of sub-stations (including

those of EDC and private providers) to the same unit price of USD 16.40

cents/kWh,

• Set a different electricity pricing for daytime and night time industrial usage,

• Ensure reliability and confidence in the electricity supply by reducing the rate of

electricity cut-off to no more than 12 times or 24 hours per annum.

24

Other Supporting Policies…

Thank You!25

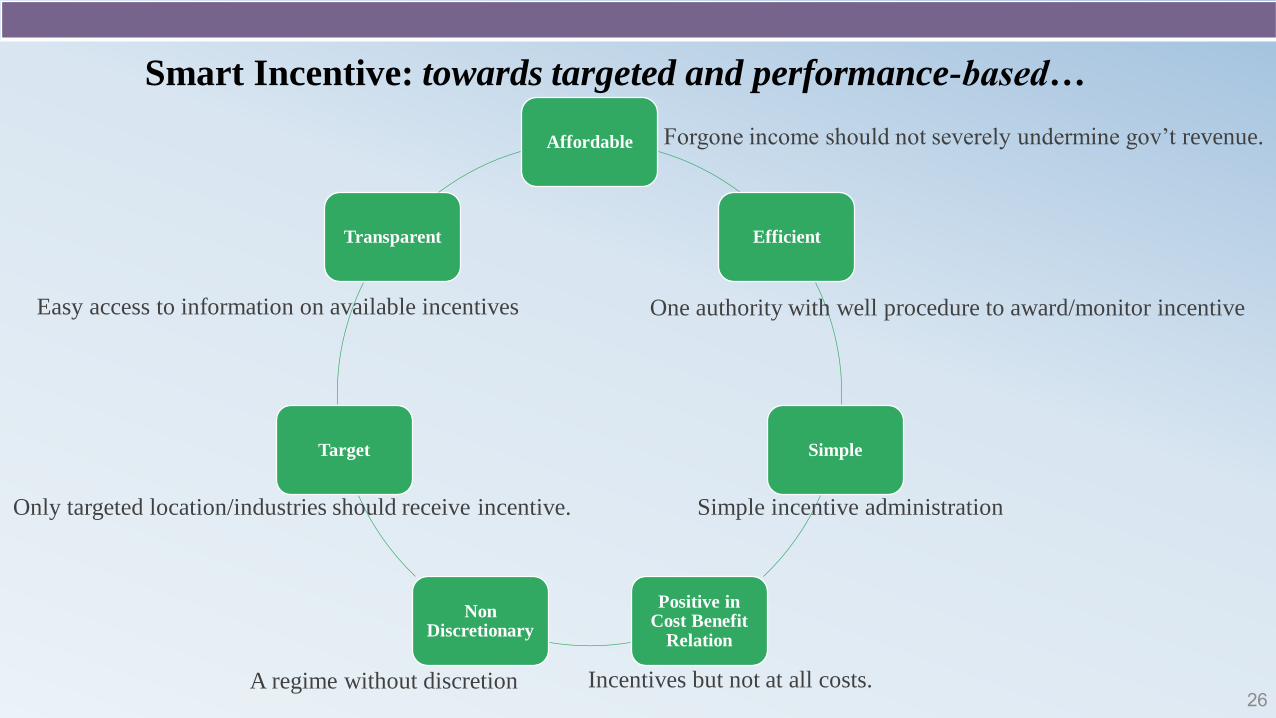

Smart Incentive: towards targeted and performance-based…

26

Affordable

Efficient

Simple

Positive in Cost Benefit

Relation

Non Discretionary

Target

Transparent

Forgone income should not severely undermine gov’t revenue.

Easy access to information on available incentives One authority with well procedure to award/monitor incentive

Only targeted location/industries should receive incentive. Simple incentive administration

A regime without discretion Incentives but not at all costs.