Embed Size (px)

Citation preview

Confidential and Proprietary Innovation & Culture

www.jusung.com

240 Opo-ro, Opo-eup, Gwangju-si

Gyeonggi-do, Korea

World 1St Technology

Only 1 In The World

JUSUNG ENGINEERING

ASIA NDR

0

JUNE 13 ~ 16, 2016

Confidential and Proprietary Innovation & Culture

Disclaimer

All information regarding management performance and financial results of JUSUNG ENGINEERING (the “Company”)

during the 1st quarter of 2016 as contained herein has been prepared on a Non-consolidated basis in accordance with

International Financial Reporting Standards (“IFRS”).

The information regarding results of 1st quarter of 2016 has been prepared in advance, prior to being reviewed by

outside auditors, solely for the convenience of investors of the Company, and is subject to change in the process of

final reviewing by external auditors.

The information contained herein includes forward-looking statements in respect to future plans, prospects, and

performances of the Company. These forward-looking statements also refer to the Company’s performance on Non-

consolidated base, as indicated.

The aforementioned forward-looking statements are influenced by changes in the management environment and

relative events, and by their nature, these statements refer to uncertain circumstances. Consequently, due to these

uncertainties, the Company’s actual future results may differ materially from those expressed or implied by such

statements.

Please note that as the forward-looking statements contained herein are based on the current market situation and

the Company’s management direction, they are subject to change according to the changes in future market

environment and business strategy.

The information contained herein should not be utilized for any legal purposes in regards to investors’ investment

results. The Company hereby expressly disclaims any and all liability for any loss or damage resulting from the

investors’ reliance on the information contained herein.

1

Confidential and Proprietary Innovation & Culture 2

Table of Contents

1. Company Overview

2. Market Trend & Competitiveness

3. Financial Status

Confidential and Proprietary Innovation & Culture

1-1. Vision

Culture Spirit

Innovate Technology!

Create New Industry!

Make Happiness!

3

Confidential and Proprietary Innovation & Culture

1-2. Mission

First Mover & Market Developer

Semiconductor, Display, Solar Cell Technology Integration

World’s 1 Technology

Only 1 in the World

st

4

Confidential and Proprietary Innovation & Culture

1-3. Spirit & Culture

Think for the First !

Work for the No.1 !

Make New Records !

1. Creative · Innovative People

5

2. Success-Sharing Culture

Mutual Success of JUSUNG & Its

Customer

Confidential and Proprietary Innovation & Culture 6

1-4. Campus Map

Leading Korean Enterprise with Creative · Innovative Technology!

Confidential and Proprietary Innovation & Culture

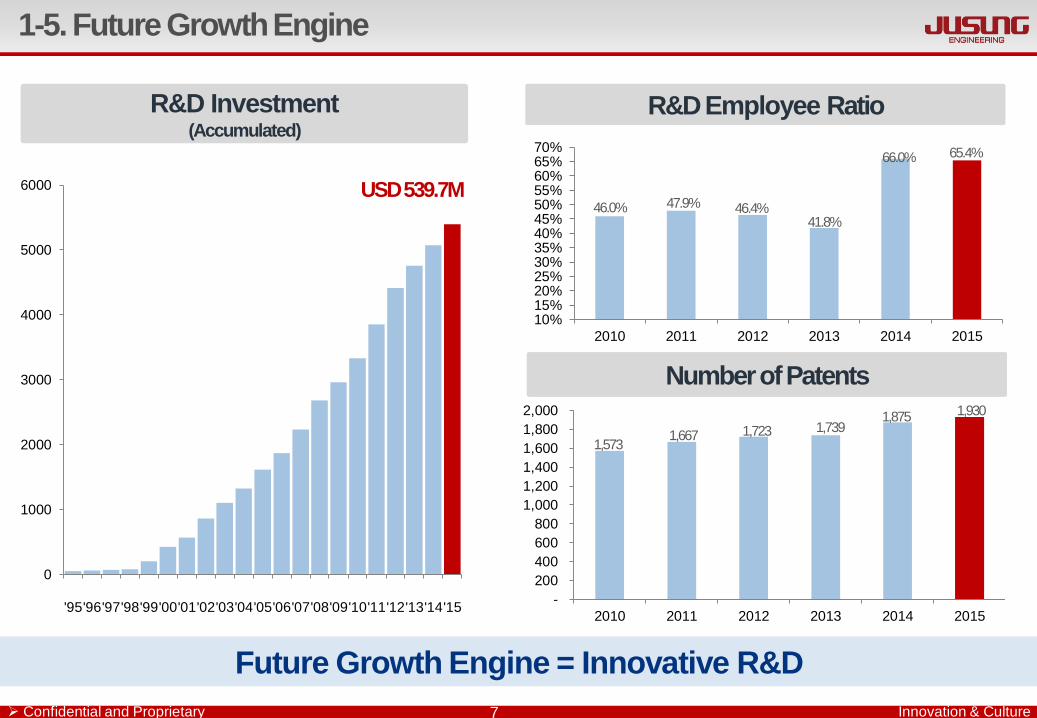

1-5. Future Growth Engine

Future Growth Engine = Innovative R&D

7

R&D Employee Ratio

USD 539.7M

Number of Patents

R&D Investment (Accumulated)

Number of Patents

0

1000

2000

3000

4000

5000

6000

'95'96'97'98'99'00'01'02'03'04'05'06'07'08'09'10'11'12'13'14'15

46.0% 47.9% 46.4% 41.8%

66.0% 65.4%

10%15%20%25%30%35%40%45%50%55%60%65%70%

2010 2011 2012 2013 2014 2015

1,573 1,667 1,723 1,739

1,875 1,930

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2010 2011 2012 2013 2014 2015

Confidential and Proprietary Innovation & Culture

1-6. Core Technology Competitiveness

Competency With Leading-Edge Technology in Core Industries

8

1. Semiconductor

(Core Technologies)

3. Solar Cell 2. Display(LCD & OLED)

Confidential and Proprietary Innovation & Culture

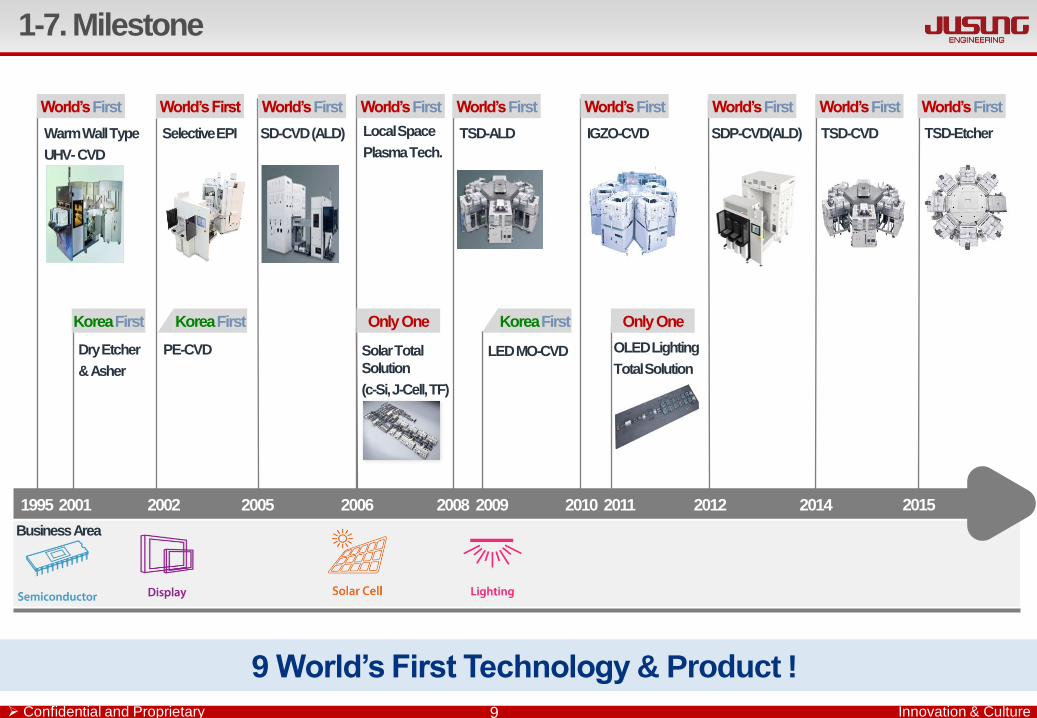

9 World’s First Technology & Product !

1-7. Milestone

9

Korea First

1995 2001 2002 2005 2006 2009 2010 2011 2012 2014

World’s First

Warm Wall Type

UHV- CVD

Korea First

Dry Etcher

& Asher

World’s First

Selective EPI

PE-CVD

World’s First

SD-CVD (ALD)

World’s First

Local Space

Plasma Tech.

Korea First

LED MO-CVD

World’s First

IGZO-CVD

OLED Lighting

Total Solution

World’s First

SDP-CVD(ALD)

World’s First

TSD-ALD

World’s First

TSD-CVD

Business Area

Solar Total

Solution

(c-Si, J-Cell, TF)

Only One Only One

2015

World’s First

TSD-Etcher

2008

Confidential and Proprietary Innovation & Culture

1-8. Mutual Success of JUSUNG & Its Customers

■ 78 Worldwide Customers with World’s Best Product & Technology

Outstanding

Contribution Award Best Partner Award Best Supplier

Award Outstanding

Contribution Award

◆

◆

◆

10

Headquarter

Subsidiary

Local Office

Sales Agent

Appreciation

Plaque Appreciation

Plaque

Appreciation

Plaque Best Supplier

Award

Confidential and Proprietary Innovation & Culture 11

Table of Contents

1. Company Overview

2. Market Trend & Competitiveness

3. Financial Status

Confidential and Proprietary Innovation & Culture

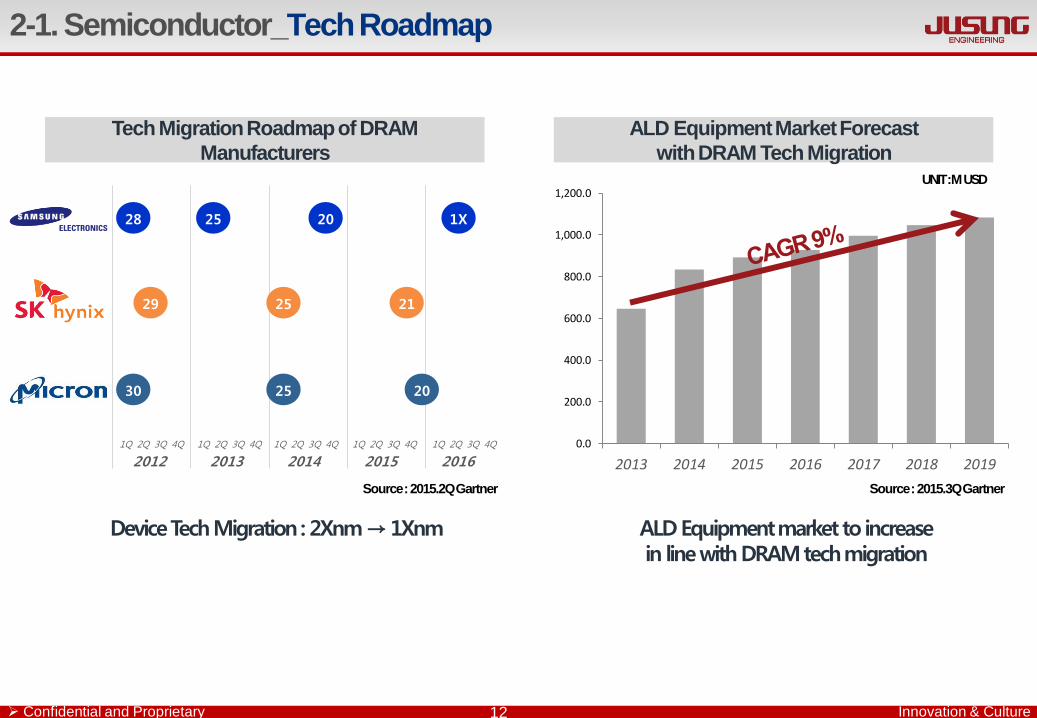

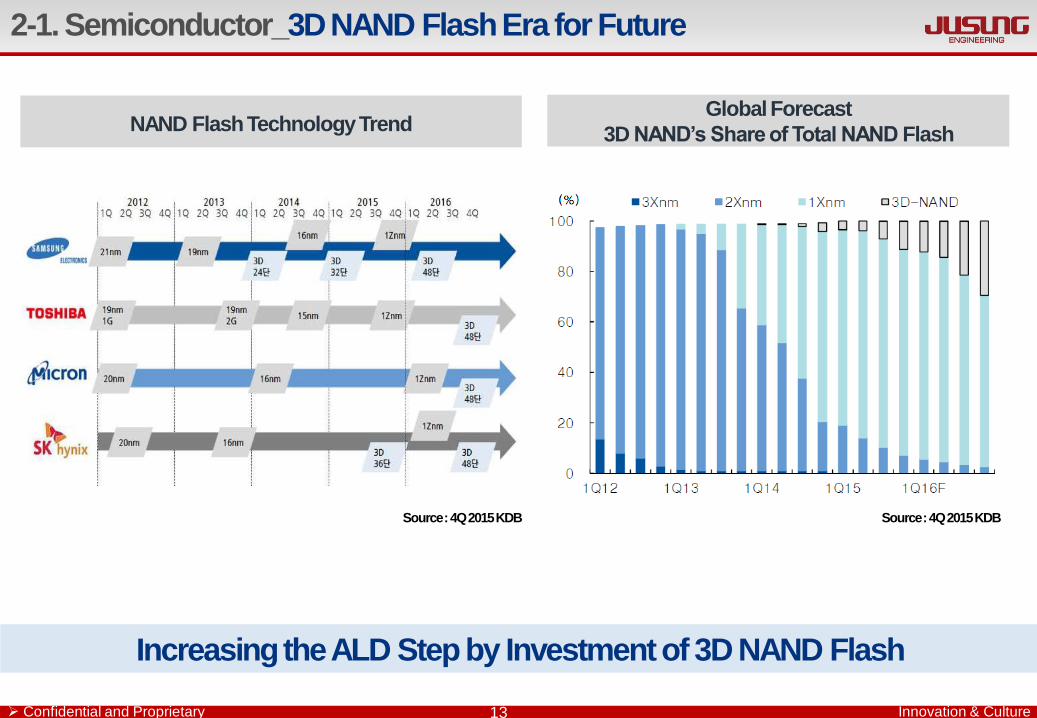

2-1. Semiconductor_Tech Roadmap

12

Tech Migration Roadmap of DRAM

Manufacturers

ALD Equipment market to increase in line with DRAM tech migration

Device Tech Migration : 2Xnm → 1Xnm

2012 2013 2014 2015 2016

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

28 25 20 1X

29 25 21

30 25 20

ALD Equipment Market Forecast

with DRAM Tech Migration

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

2013 2014 2015 2016 2017 2018 2019

UNIT : M USD

Source : 2015.3Q Gartner Source : 2015.2Q Gartner

Confidential and Proprietary Innovation & Culture

Increasing the ALD Step by Investment of 3D NAND Flash

2-1. Semiconductor_3D NAND Flash Era for Future

NAND Flash Technology Trend Global Forecast

3D NAND’s Share of Total NAND Flash

13

Source : 4Q 2015 KDB Source : 4Q 2015 KDB

Confidential and Proprietary Innovation & Culture

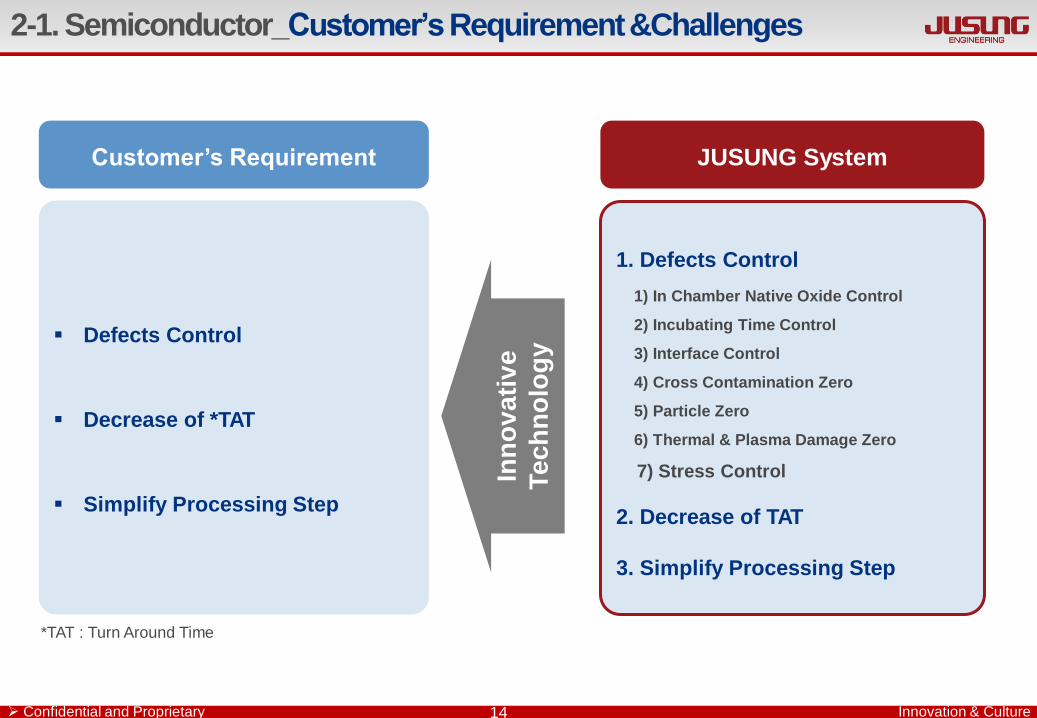

Defects Control

Decrease of *TAT

Simplify Processing Step

Customer’s Requirement JUSUNG System

1. Defects Control

1) In Chamber Native Oxide Control

2) Incubating Time Control

3) Interface Control

4) Cross Contamination Zero

5) Particle Zero

6) Thermal & Plasma Damage Zero

7) Stress Control

2. Decrease of TAT

3. Simplify Processing Step

Inn

ov

ati

ve

Tech

no

log

y

2-1. Semiconductor_Customer’s Requirement &Challenges

*TAT : Turn Around Time

14

Confidential and Proprietary Innovation & Culture 15

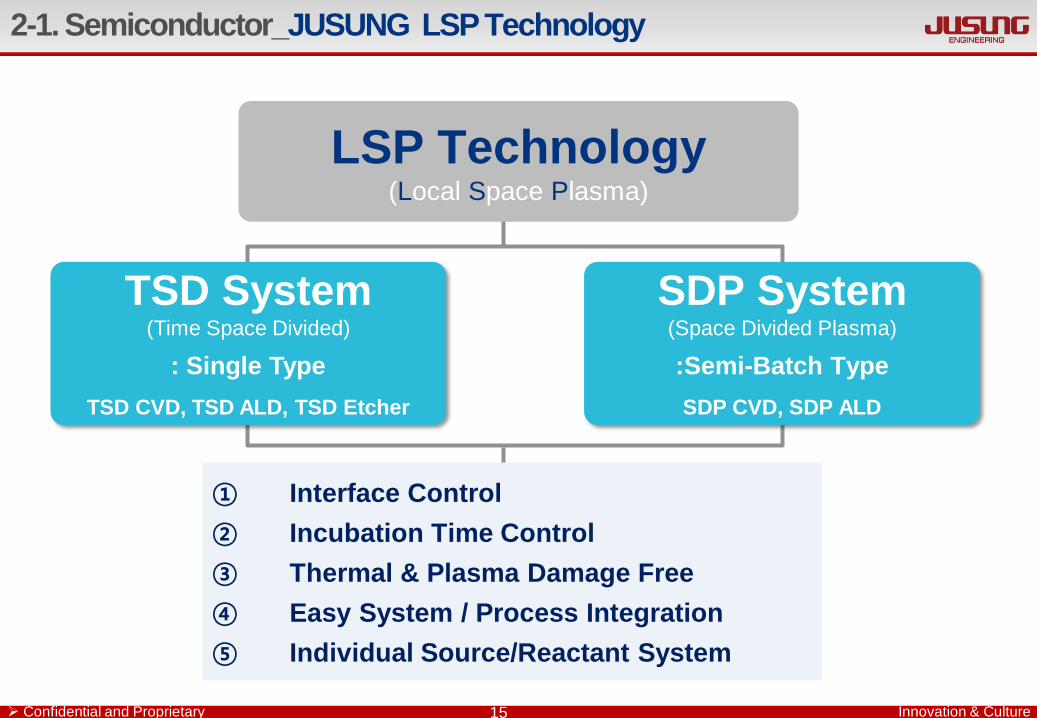

2-1. Semiconductor_JUSUNG LSP Technology

LSP Technology (Local Space Plasma)

① Interface Control

② Incubation Time Control

③ Thermal & Plasma Damage Free

④ Easy System / Process Integration

⑤ Individual Source/Reactant System

SDP System (Space Divided Plasma)

:Semi-Batch Type

SDP CVD, SDP ALD

TSD System (Time Space Divided)

: Single Type

TSD CVD, TSD ALD, TSD Etcher

Confidential and Proprietary Innovation & Culture

Hidden Champion First Mover

2-1. Semiconductor_Product & Technology

16

Future Transistor Tech.

• Si SEG ; Elevated

Source Drain

• SiGe, SiC

• a-Si, Poly Si

• OEC

(Oxide Elimination

Chamber)

UHV-CVD & OEC

(Warm Wall Type )

LSP Technology

• High-K

• Metal

• ULTO

Defect Free Tech.

• High-K

• Metal

• SiO / SiOC / SiON

• SiN / SiBN

• Oxidation

• Nitridation

• High-K

• Metal

ICP Etcher SDP-CVD/ALD TSD-CVD/ALD

Defect Free Tech.

• High-K

• Metal

• SiO / SiOC / SiON

• SiN / SiBN

• Oxidation

• Nitridation

SD-CVD/ALD MO-CVD/ALD TSD-Etcher

Defect Free Tech.

• DPT Partition Etch

• STI & Gate Etch

• Hard Mask Etch

• Poly Etch Back

• MTJ Etch

Defect Free Tech.

• DPT Partition Etch

• STI & Gate Etch

• Hard Mask Etch

• Poly Etch Back

• MTJ Etch

Confidential and Proprietary Innovation & Culture

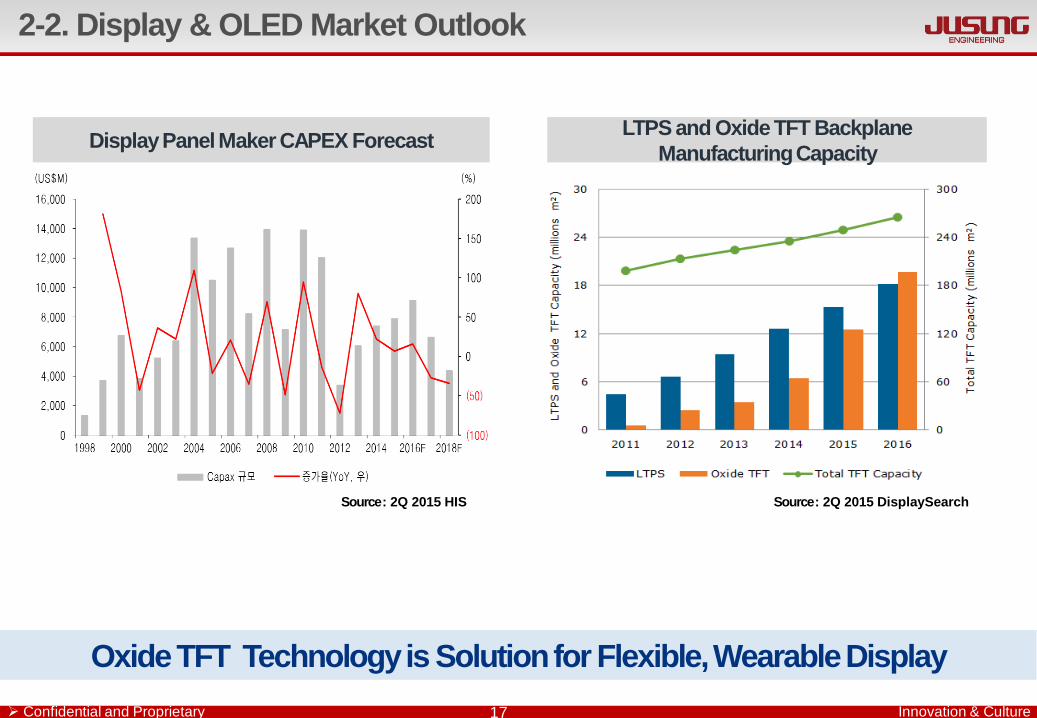

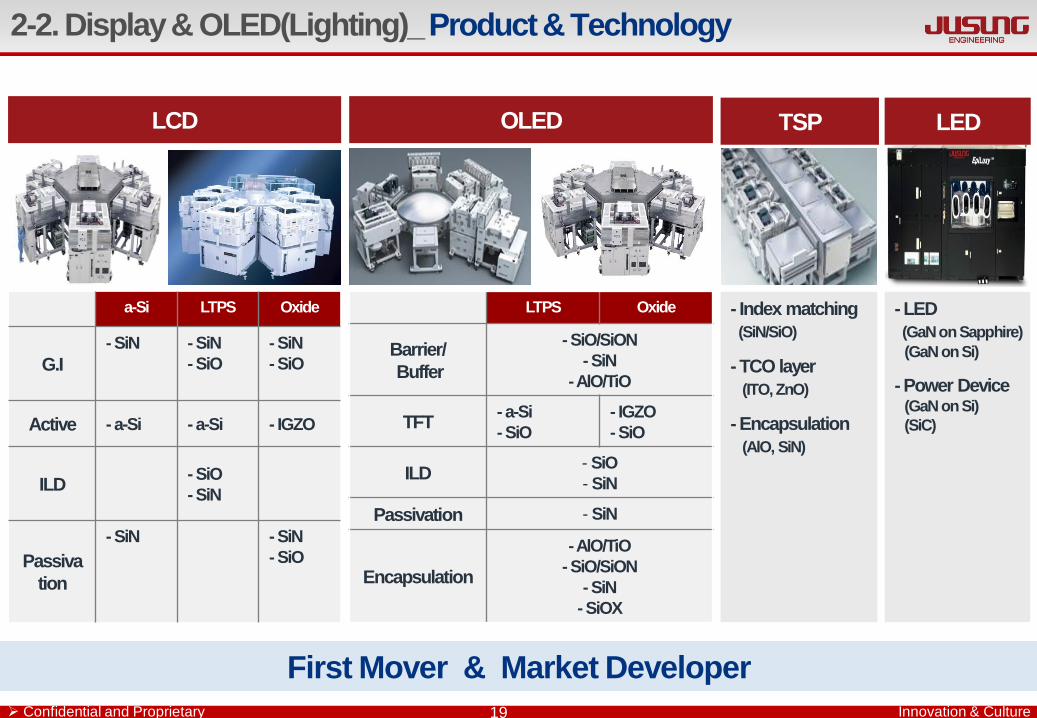

2-2. Display & OLED Market Outlook

17

Oxide TFT Technology is Solution for Flexible, Wearable Display

LTPS and Oxide TFT Backplane

Manufacturing Capacity Display Panel Maker CAPEX Forecast

Source : 2Q 2015 HIS Source : 2Q 2015 DisplaySearch

Confidential and Proprietary Innovation & Culture

Realizing Next-Gen. of Display via TSD-CVD/ALD

a-Si TFT LCD IGZO TFT LCD IGZO

AMOLED

Bendable/ Flexible

AMOLED

Transparency

AMOLED

Tech.

Trend

KPI

LTPS

AMOLED

1. Mobility 0.5cm2/Vs 2. Well Known

1. Mobility >50cm2/Vs 2. Anneal Unif.

3. Cost Reduction

4. Scale Up

1. Mobility >50cm2/Vs 2. Reliability

3. Repeatability

4. Stability

1. Mobility >50cm2/Vs 2. Encap Reliability

3. Repeatability

4. Stability

1. Mobility > 50cm2/Vs 2. Isolated Thin Film

3. Encap Reliability

4. Repeatability

5. Stability

1. Mobility >50cm2/Vs 2. Black Light Unit Control 3. Transparency

4. Reliability

5. Repeatability

6. Stability

2-2. Display & OLED_ Trend vs. JUSUNG

18

JUSUNG

Tech.

a-Si, SiN, SiO

OLED Encapsulation : Thin Film Encap. (SiN, SiO, SiON, SiOC, Al2O3)

Touch panel sensor : Insulator, TCO, Index matching (Al2O3, BZO, SiN/SiO)

LSP Tech.

TSD CVD/ALD

( Up to 11G)

CCP Tech.

CVD ( Up to 8G)

Thin Film Transistor : Active, GI, ESL, PAS (a-Si, IGZO, SiO, SiN, Al2O3)

Plastic OLED : Barrier (SiN, SiO, Al2O3)

Confidential and Proprietary Innovation & Culture

First Mover & Market Developer

2-2. Display & OLED(Lighting)_ Product & Technology

19

First Mover & Market Developer

OLED TSP LED

- Index matching

(SiN/SiO)

- TCO layer

(ITO, ZnO)

- Encapsulation

(AlO, SiN)

- LED

(GaN on Sapphire)

(GaN on Si)

- Power Device (GaN on Si)

(SiC)

LTPS Oxide

Barrier/

Buffer

- SiO/SiON

- SiN

- AlO/TiO

TFT - a-Si

- SiO

- IGZO

- SiO

ILD - SiO

- SiN

Passivation - SiN

Encapsulation

- AlO/TiO

- SiO/SiON

- SiN

- SiOX

LCD

a-Si LTPS Oxide

G.I

- SiN - SiN

- SiO

- SiN

- SiO

Active - a-Si - a-Si - IGZO

ILD - SiO

- SiN

Passiva

tion

- SiN - SiN

- SiO

Confidential and Proprietary Innovation & Culture 20

Table of Contents

1. Company Overview

2. Market Trend & Competitiveness

3. Financial Status

Confidential and Proprietary Innovation & Culture

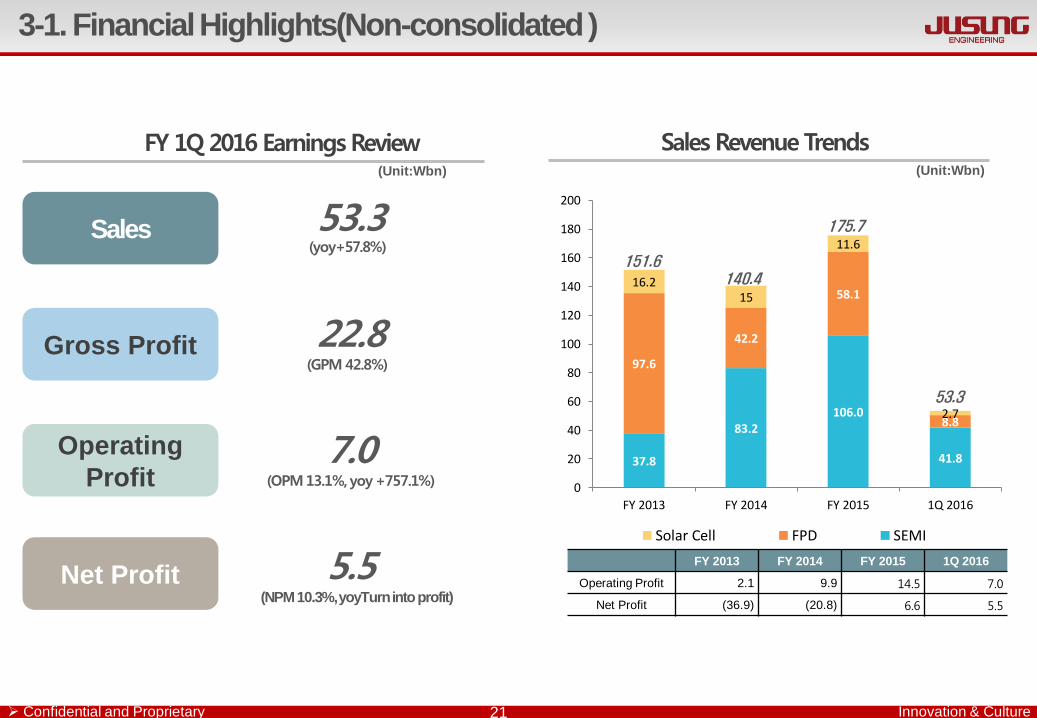

3-1. Financial Highlights(Non-consolidated )

21

Sales

Gross Profit

Operating

Profit

Net Profit

(Unit:Wbn)

Sales Revenue Trends (Unit:Wbn)

FY 2013 FY 2014 FY 2015 1Q 2016

Operating Profit 2.1 9.9 14.5 7.0

Net Profit (36.9) (20.8) 6.6 5.5

408

76.8

37.8

83.2 106.0

41.8

97.6

42.2

58.1

8.8

16.2 15

11.6

2.7

0

20

40

60

80

100

120

140

160

180

200

FY 2013 FY 2014 FY 2015 1Q 2016

Solar Cell FPD SEMI

151.6 140.4

175.7

53.3

FY 1Q 2016 Earnings Review

53.3 (yoy+57.8%)

22.8 (GPM 42.8%)

7.0 (OPM 13.1%, yoy +757.1%)

5.5 (NPM 10.3%, yoyTurn into profit)

Confidential and Proprietary Innovation & Culture 22

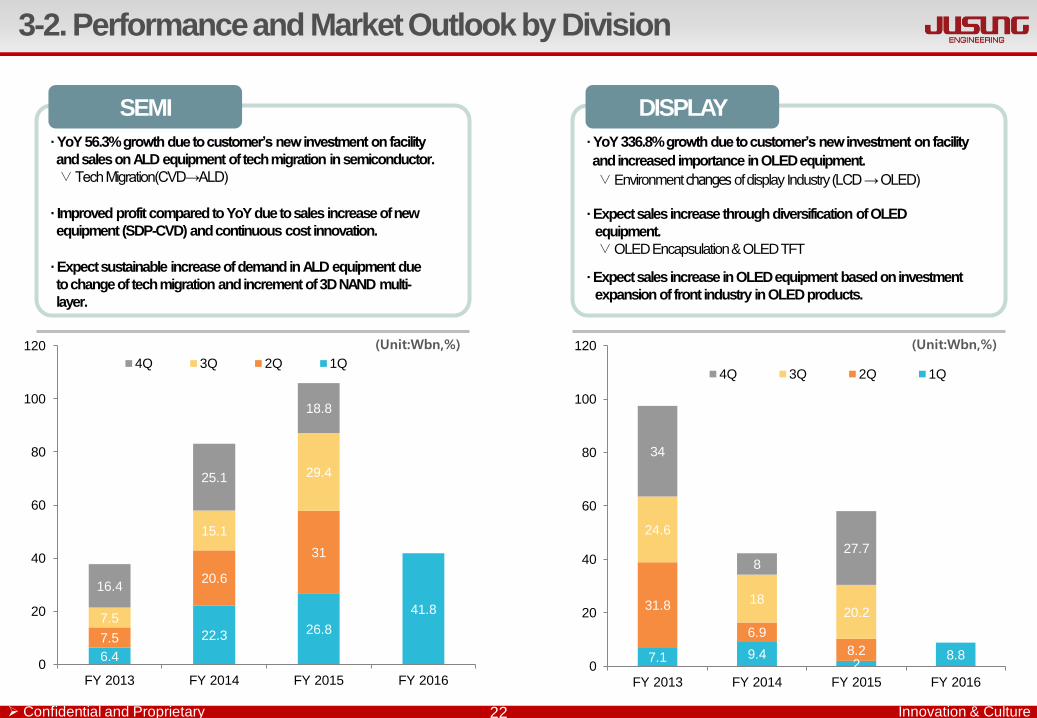

3-2. Performance and Market Outlook by Division

· YoY 56.3% growth due to customer’s new investment on facility

and sales on ALD equipment of tech migration in semiconductor.

∨ Tech Migration(CVD→ALD)

· Improved profit compared to YoY due to sales increase of new

equipment (SDP-CVD) and continuous cost innovation.

SEMI

· Expect sustainable increase of demand in ALD equipment due

to change of tech migration and increment of 3D NAND multi-

layer.

· YoY 336.8% growth due to customer’s new investment on facility

and increased importance in OLED equipment. ∨ Environment changes of display Industry (LCD → OLED)

· Expect sales increase through diversification of OLED

equipment.

∨ OLED Encapsulation & OLED TFT

· Expect sales increase in OLED equipment based on investment

expansion of front industry in OLED products.

DISPLAY

(Unit:Wbn,%) (Unit:Wbn,%)

6.4

22.3 26.8

41.8

7.5

20.6

31

7.5

15.1

29.4

16.4

25.1

18.8

0

20

40

60

80

100

120

FY 2013 FY 2014 FY 2015 FY 2016

4Q 3Q 2Q 1Q

7.1 9.4 2

8.8

31.8

6.9

8.2

24.6

18 20.2

34

8

27.7

0

20

40

60

80

100

120

FY 2013 FY 2014 FY 2015 FY 2016

4Q 3Q 2Q 1Q

Confidential and Proprietary Innovation & Culture

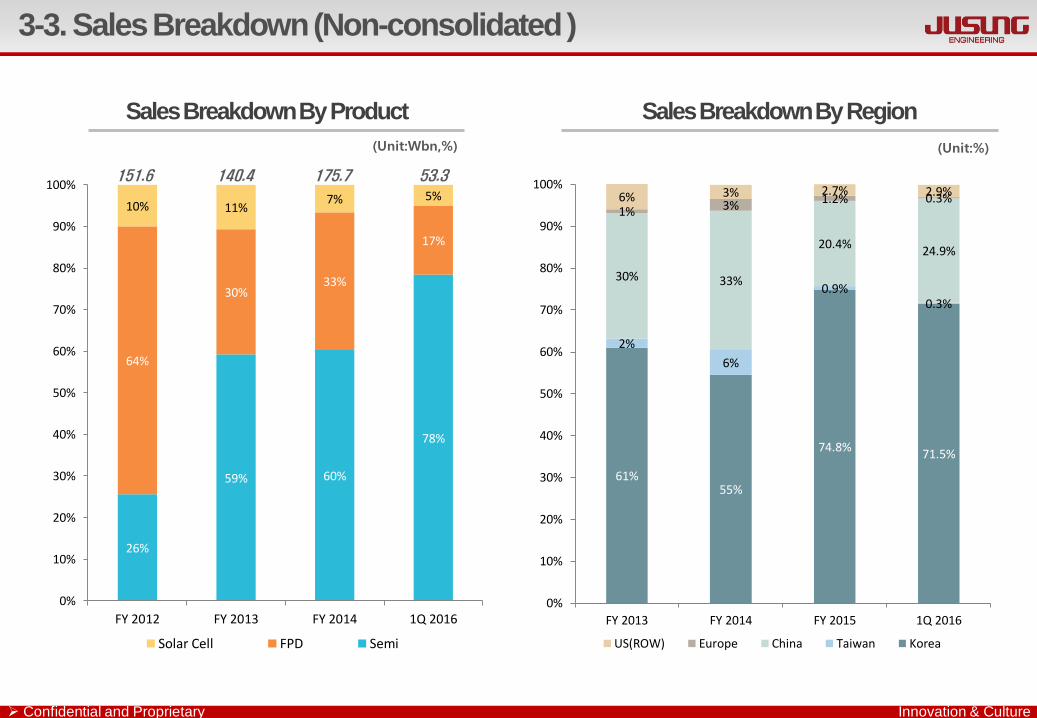

3-3. Sales Breakdown (Non-consolidated )

(Unit:Wbn,%)

Sales Breakdown By Product Sales Breakdown By Region

(Unit:%)

53.3 151.6 140.4 175.7

26%

59% 60%

78%

64%

30% 33%

17%

10% 11% 7% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY 2012 FY 2013 FY 2014 1Q 2016

Solar Cell FPD Semi

61% 55%

74.8% 71.5%

2%

6%

0.9% 0.3%

30% 33%

20.4% 24.9%

1% 3% 1.2% 0.3% 6% 3% 2.7% 2.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY 2013 FY 2014 FY 2015 1Q 2016

US(ROW) Europe China Taiwan Korea

Confidential and Proprietary Innovation & Culture 24

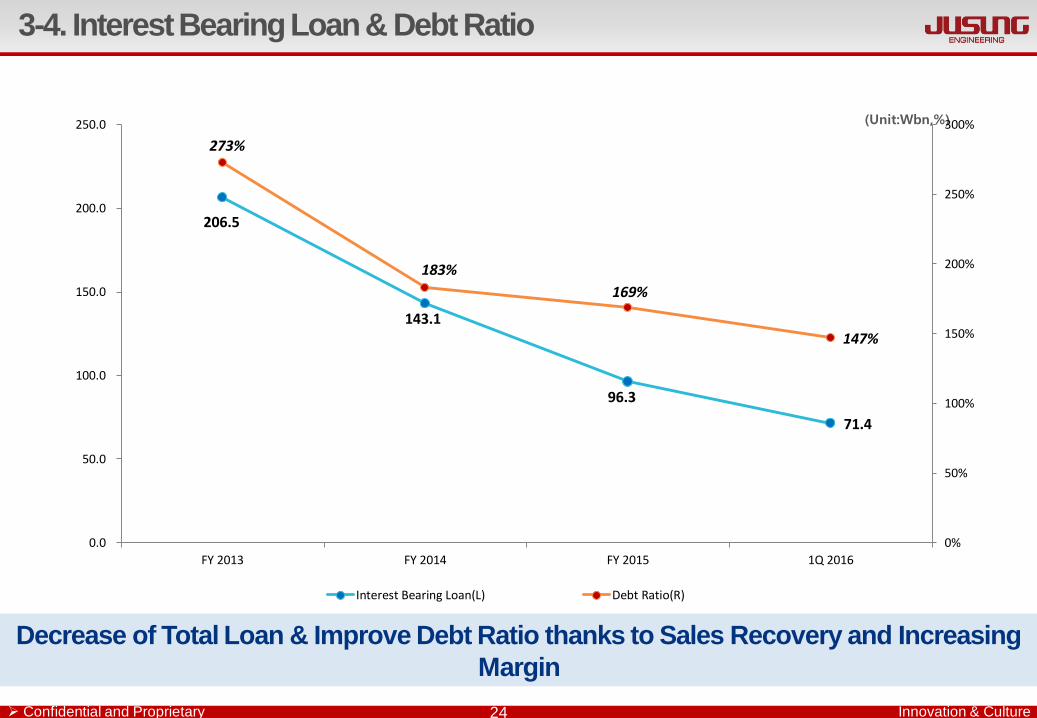

Decrease of Total Loan & Improve Debt Ratio thanks to Sales Recovery and Increasing

Margin

(Unit:Wbn,%)

3-4. Interest Bearing Loan & Debt Ratio

206.5

143.1

96.3

71.4

273%

183%

169%

147%

0%

50%

100%

150%

200%

250%

300%

0.0

50.0

100.0

150.0

200.0

250.0

FY 2013 FY 2014 FY 2015 1Q 2016

Interest Bearing Loan(L) Debt Ratio(R)

Confidential and Proprietary Innovation & Culture

World 1st Technology Only

www.jusung.com

1 in the World

Confidential and Proprietary Innovation & Culture 26

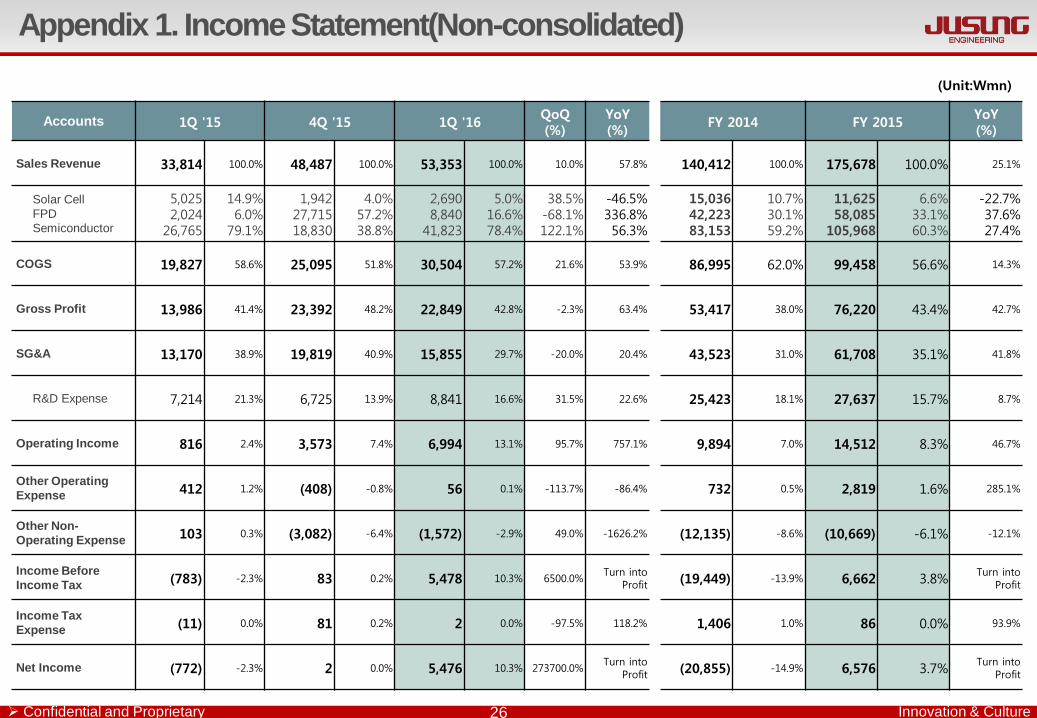

Accounts 1Q '15 4Q '15 1Q '16 QoQ (%)

YoY (%)

FY 2014 FY 2015 YoY (%)

Sales Revenue 33,814 100.0% 48,487 100.0% 53,353 100.0% 10.0% 57.8% 140,412 100.0% 175,678 100.0% 25.1%

Solar Cell

FPD

Semiconductor

5,025 2,024

26,765

14.9% 6.0%

79.1%

1,942 27,715 18,830

4.0% 57.2% 38.8%

2,690 8,840

41,823

5.0% 16.6% 78.4%

38.5% -68.1% 122.1%

-46.5% 336.8% 56.3%

15,036 42,223 83,153

10.7% 30.1% 59.2%

11,625 58,085

105,968

6.6% 33.1% 60.3%

-22.7% 37.6% 27.4%

COGS 19,827 58.6% 25,095 51.8% 30,504 57.2% 21.6% 53.9% 86,995 62.0% 99,458 56.6% 14.3%

Gross Profit 13,986 41.4% 23,392 48.2% 22,849 42.8% -2.3% 63.4% 53,417 38.0% 76,220 43.4% 42.7%

SG&A 13,170 38.9% 19,819 40.9% 15,855 29.7% -20.0% 20.4% 43,523 31.0% 61,708 35.1% 41.8%

R&D Expense 7,214 21.3% 6,725 13.9% 8,841 16.6% 31.5% 22.6% 25,423 18.1% 27,637 15.7% 8.7%

Operating Income 816 2.4% 3,573 7.4% 6,994 13.1% 95.7% 757.1% 9,894 7.0% 14,512 8.3% 46.7%

Other Operating

Expense 412 1.2% (408) -0.8% 56 0.1% -113.7% -86.4% 732 0.5% 2,819 1.6% 285.1%

Other Non-

Operating Expense 103 0.3% (3,082) -6.4% (1,572) -2.9% 49.0% -1626.2% (12,135) -8.6% (10,669) -6.1% -12.1%

Income Before

Income Tax (783) -2.3% 83 0.2% 5,478 10.3% 6500.0%

Turn into Profit (19,449) -13.9% 6,662 3.8%

Turn into Profit

Income Tax

Expense (11) 0.0% 81 0.2% 2 0.0% -97.5% 118.2% 1,406 1.0% 86 0.0% 93.9%

Net Income (772) -2.3% 2 0.0% 5,476 10.3% 273700.0% Turn into

Profit (20,855) -14.9% 6,576 3.7% Turn into

Profit

Appendix 1. Income Statement(Non-consolidated)

(Unit:Wmn)

Confidential and Proprietary Innovation & Culture

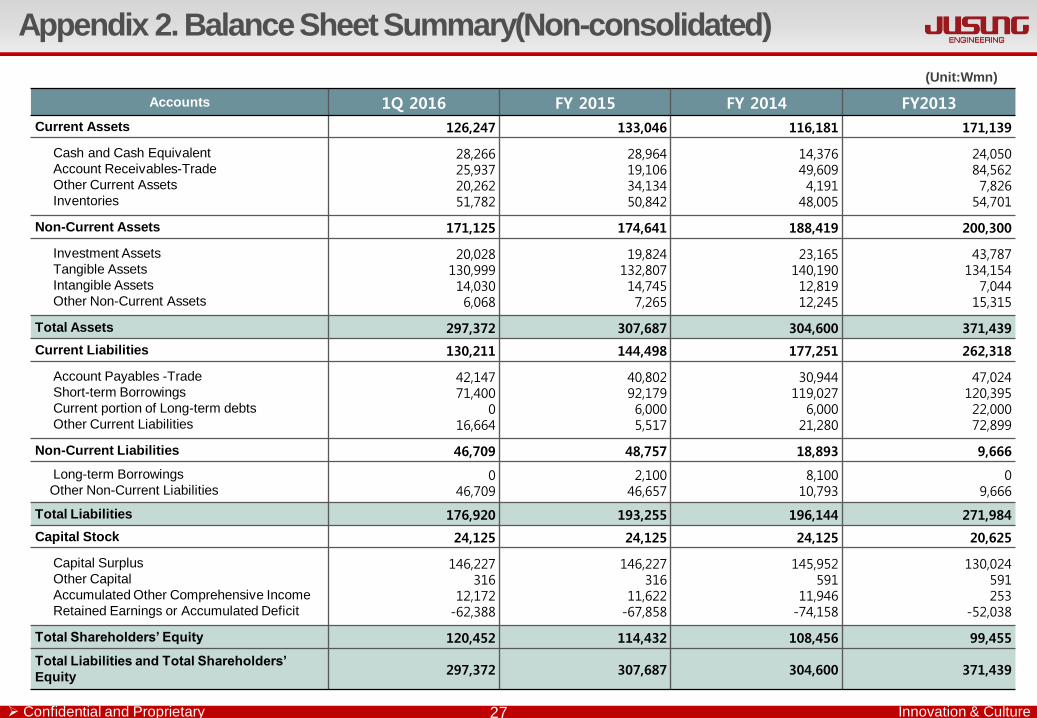

Accounts 1Q 2016 FY 2015 FY 2014 FY2013

Current Assets 126,247 133,046 116,181 171,139

Cash and Cash Equivalent

Account Receivables-Trade

Other Current Assets

Inventories

28,266 25,937 20,262 51,782

28,964 19,106 34,134 50,842

14,376 49,609 4,191

48,005

24,050 84,562

7,826 54,701

Non-Current Assets 171,125 174,641 188,419 200,300

Investment Assets

Tangible Assets

Intangible Assets

Other Non-Current Assets

20,028 130,999 14,030 6,068

19,824 132,807 14,745 7,265

23,165 140,190 12,819 12,245

43,787 134,154 7,044 15,315

Total Assets 297,372 307,687 304,600 371,439

Current Liabilities 130,211 144,498 177,251 262,318

Account Payables -Trade

Short-term Borrowings

Current portion of Long-term debts

Other Current Liabilities

42,147 71,400

0 16,664

40,802 92,179 6,000 5,517

30,944 119,027

6,000 21,280

47,024 120,395 22,000

72,899

Non-Current Liabilities 46,709 48,757 18,893 9,666

Long-term Borrowings

Other Non-Current Liabilities 0

46,709 2,100

46,657 8,100

10,793 0

9,666

Total Liabilities 176,920 193,255 196,144 271,984

Capital Stock 24,125 24,125 24,125 20,625

Capital Surplus

Other Capital

Accumulated Other Comprehensive Income

Retained Earnings or Accumulated Deficit

146,227 316

12,172 -62,388

146,227 316

11,622 -67,858

145,952 591

11,946 -74,158

130,024 591 253

-52,038

Total Shareholders’ Equity 120,452 114,432 108,456 99,455

Total Liabilities and Total Shareholders’

Equity 297,372 307,687 304,600 371,439

27

(Unit:Wmn)

Appendix 2. Balance Sheet Summary(Non-consolidated)

![AMOLED TV 기술itfind.or.kr/COMIN/file55584-AMOLED TV 기술.pdf · 2012-06-14 · AMOLED TV 기술 2011년 제12권 제4호 7 [그림 2] 출시된 OLED TV 제품 [그림 3] Fine](https://img.pdfslide.tips/doc/110x75/5e8f531e3d26c532e81ac0d9/amoled-tv-e-tv-epdf-2012-06-14-amoled-tv-e-2011e-oe12eoe.jpg)