Embed Size (px)

Citation preview

KHALSACREDIT UNION

KCU, THE NAME YOU CAN BANK ON

Annual Report2014

Sowing For A Future Harvest

slwnW irport

Biv`K leI Psl bIjxI

Registration: 1:00 PM - 2:00 PMMeeting Agenda

Call To OrderArdas

1. Adoption of Agenda 2. Approval of Minutes of 2014 AGM 3. Business Arising Out of Minutes 4. Chairman’s Report 5. Chief Executive O�cer’s Report 6. Auditor’s Report 7. Approval of Financial Statements 8. Appointment of Auditors 9. Un�nished Business 10. New Business 11. Adjourn/Refreshments

DATED at Surrey, British Columbia,this 23rd day of March 2015

NOTICE OF MEETING

The twenty-ninth Annual General Meeting of Khalsa Credit Union will be held on Sunday, April 26, 2015 at 2:00 PM at the Crown Palace Banquet Hall located at 201-12025 Nordel Way, Surrey, B.C. V3W 1W1, Phone 604-591-8100, www.crownpalace.ca

Only members in good standing as at January 22, 2015will be entitled to vote at the Annual General Meeting.A member is in good standing if the member is not morethan 90 days delinquent in any of the member’sobligations to the Credit Union and has paid for andholds the respective number of membership equityshares as set out below and has attained the age of majority – 19 years of age: (a) 5 shares if the member is an individual; (b) in the case of a joint account; 5 shares for the �rst named and 1 for each additional named person; (c) 5 shares if the member is an incorporated company; (d) 5 shares per partner if the member is a partnership or (e) 5 shares if the member is an association.

1

PUNJABITRANSLATION

Crown Palace Banquet Hall201-12025 Nordel Way

Surrey, BC Canada

SundayApril 26, 2015

2:00 PM

Registration: 1:00 PM - 2:00 PMMeeting Agenda

Call To OrderArdas

1. Adoption of Agenda 2. Approval of Minutes of 2014 AGM 3. Business Arising Out of Minutes 4. Chairman’s Report 5. Chief Executive O�cer’s Report 6. Auditor’s Report 7. Approval of Financial Statements 8. Appointment of Auditors 9. Un�nished Business 10. New Business 11. Adjourn/Refreshments

DATED at Surrey, British Columbia,this 23rd day of March 2015

NOTICE OF MEETING

The twenty-ninth Annual General Meeting of Khalsa Credit Union will be held on Sunday, April 26, 2015 at 2:00 PM at the Crown Palace Banquet Hall located at 201-12025 Nordel Way, Surrey, B.C. V3W 1W1, Phone 604-591-8100, www.crownpalace.ca

Only members in good standing as at January 22, 2015will be entitled to vote at the Annual General Meeting.A member is in good standing if the member is not morethan 90 days delinquent in any of the member’sobligations to the Credit Union and has paid for andholds the respective number of membership equityshares as set out below and has attained the age of majority – 19 years of age: (a) 5 shares if the member is an individual; (b) in the case of a joint account; 5 shares for the �rst named and 1 for each additional named person; (c) 5 shares if the member is an incorporated company; (d) 5 shares per partner if the member is a partnership or (e) 5 shares if the member is an association.

1

PUNJABITRANSLATION

Crown Palace Banquet Hall201-12025 Nordel Way

Surrey, BC Canada

SundayApril 26, 2015

2:00 PM

iejlws dw noits

Kwlsw krYift XUnIAn dw aux`qIvW slwnW Awm iejlws AYqvwr, 26 AprYl 2015 nUM bwd dupihr 2:00 vjy krwaUn pYlys bYNkuiet hwl, #201-12025 nOrfl vyA, srI, bI.sI., vI3fbilaU 1fbilaU1, Pon 604-591-8100, www.crownpalace.ca ivKy hovygw[

rijstrySn: bwd dupihr 1:00 vjy qoN 2:00 vjy q`k

mIitMg dw eyjMfwSurUAwq dw bulwvw

Ardws 1. eyjMfw svIkwr 2. 2014 slwnW Awm iejlws dy kwrj vyrivAW dI mnzUrI 3. kwrj vyrivAW qoN auqpMn kMmkwr 4. cyArmYn dI irport 5. mu`K kwrj-swDk APsr dI irport 6. Awiftr dI irport 7. iv`qI stytmYNtW dI mnzUrI 8. AwiftrW dI inXukqI 9. Axmu`ikAw kMm kwr 10. nvW kMm kwr11. iejlws mulqvI/cwh pwxI

22 jnvrI 2015 nUM ijhVy mYNbr gu`f stYNifMg ’c sn kyvl auh hI slwnW Awm iejlws ’c vot pw skx dy Xog hoxgy[ koeI vI mYNbr gu`f stYNifMg ’c hY, jykr aus mYNbr ny krYift XUnIAn pRiq mYNbr dIAW iksy vI qrHW dIAW dyxdwrIAW leI 90 idnW qoN v`D dy smyN leI kuqwhI nhIN kIqI hoeI Aqy aus ny loVINdI igxqI dy mYNbriS`p AYkuietI SyArW leI AdwiegI kIqI hoeI hY Aqy SyAr r`Ky hoey hn, ijvyN ik hyTW id`qw igAw hY Aqy auh bwlg aumr dw – mqlb 19 swl dw ho igAw hY: (a) 5 SyAr jykr mYNbr iek ivAkqI hY; (A) sWJy Kwqy dI sUrq ’c, 5 SyAr pihly nW vwly ivAkqI leI Aqy 1 SyAr hryk vDIk nW vwly ivAkqI leI; (e) 5 SyAr jykr mYNbr iek ieMkwrporyt kMpnI hY; (s) 5 SyAr pRiq iBAwl jykr mYNbr iek BweIvwlI kMpnI hY jW (h) 5 SyAr jykr mYNbr iek AYsosIeySn hY[

23 mwrc 2015 nUM srI, ibRitS kulMbIAw ivKy qwrIkbD

2

BOARD OF DIRECTORS’ ELECTION – 2016

KCU is pleased to announce that we are seeking qualiedcandidates for the 2016 Directors Election. Three successfuldirectors will be elected for six (6) year terms and onesuccessful director will be elected for a four (4) year term.These directors will assume their responsibilities at the closeof the Annual General Meeting in April 2016.

The Board has identied these characteristics/qualications as those it is seeking in directors: Gursikh; nancially literate; leadership ability; geographic/gender diversity. At least one director should have an accounting background and at least one director should have a legal background. We are looking for directors who are consensus builders/team players, and are respectful, independent thinkers, creative, visionaries, negotiators and communicators.

Qualied candidates are invited to come forward. The requirements of candidates and the process of nominations are as follows: a candidate must be a member in good standing of KCU for a least twelve (12) consecutive months prior to the closing date for nominations which will be in the middle of February 2016. A candidate must qualify under Rule 4.26 1 of KCU respecting the Sikh religion. A candidate must not be disqualied under Rule 4.26 2 of the credit union due to, among other things,legislative prohibition and con�icts of employment. A copy of the Rules can be obtained from the Head O�ce of KCU.

As per current Honorarium Policy, directors are entitled to a meeting allowance of $250/$150 for attending Board/Committee meetings. Interested candidates are requested to contact the Chairperson of the Nominating Committee, Mr. Harinder Singh Sohi via telephone 604-417-9490 or email [email protected]

Please participate fully in your credit union and be part of the Khalsa spirit.

3

PUNJABITRANSLATION

2

BOARD OF DIRECTORS’ ELECTION – 2016

KCU is pleased to announce that we are seeking qualiedcandidates for the 2016 Directors Election. Three successfuldirectors will be elected for six (6) year terms and onesuccessful director will be elected for a four (4) year term.These directors will assume their responsibilities at the closeof the Annual General Meeting in April 2016.

The Board has identied these characteristics/qualications as those it is seeking in directors: Gursikh; nancially literate; leadership ability; geographic/gender diversity. At least one director should have an accounting background and at least one director should have a legal background. We are looking for directors who are consensus builders/team players, and are respectful, independent thinkers, creative, visionaries, negotiators and communicators.

Qualied candidates are invited to come forward. The requirements of candidates and the process of nominations are as follows: a candidate must be a member in good standing of KCU for a least twelve (12) consecutive months prior to the closing date for nominations which will be in the middle of February 2016. A candidate must qualify under Rule 4.26 1 of KCU respecting the Sikh religion. A candidate must not be disqualied under Rule 4.26 2 of the credit union due to, among other things,legislative prohibition and con�icts of employment. A copy of the Rules can be obtained from the Head O�ce of KCU.

As per current Honorarium Policy, directors are entitled to a meeting allowance of $250/$150 for attending Board/Committee meetings. Interested candidates are requested to contact the Chairperson of the Nominating Committee, Mr. Harinder Singh Sohi via telephone 604-417-9490 or email [email protected]

Please participate fully in your credit union and be part of the Khalsa spirit.

3

PUNJABITRANSLATION

fwierYktrW dy borf dI cox-2016

Kwlsw krYift XUnIAn ieh GoSxw kridAW KuSI mihsUs kr rhI hW ik AsIN 2016 dI fwierYktrW dI cox leI Xog aumIdvwrW dI Bwl kr rhy hW[ iqMn kwmXwb fwierYktr Cy (6) swlW dI imAwd leI Aqy iek kwmXwb fwierYktr cwr (4) swlW dI imAwd leI cuxy jwxgy[ ieh fwierYktr AprYl 2016 ‘c hox vwly slwnW Awm iejlws dy AMq ‘qy AwpxIAW izMmyvwrIAW sMBwlxgy[

borf nyy ienHW guxW/XogqwvW dI inSwndyhI kIqI hY ijhVIAW auh iek fwierYktr ‘c hox dI Bwl kr rhy hn; iv`qI jwxwkwr, AgvweI Xogqw; BUgoilk/ilMg iviBMnqw[ G`to G`t iek fwierYktr dw lyKwkwrI dw ipCokV hovy Aqy G`to G`t iek fwierYktr kol kwnUMnI ipCokV hovy[ AsIN aunHW fwierYktrW dI Bwl kr rhy hW ijhVy sihmqI bxw skx vwly/tIm Bwvnw vwly, Aqy AwdrkwrI, Awzwd soc vwly, rcnwqmk, dUrAMdyS, smJOqyXog g`lbwq kr skx vwly Aqy sMvwd kr skx vwly hox[

Xog aumIdvwrW nUM A`gy Awaux dw s`dw id`qw jWdw hY[ aumIdvwrW leI zrUrqW Aqy nwmzdgI dw Aml A`gy id`qy Anuswr hn: aumIdvwr zrUrI qOr ‘qy nwmzdgI bMd hox dI qrIk, ijhVI ik PrvrI 2016 dy m`D ivc hovygI, qoN G`to G`t bwrW (12) auproQlI mhIny pihlW q`k Kwlsw krYift XUnIAn dw mYNbr ieMn gu`f stYNifMg irhw hovy[ aumIdvwr zrUrI qOr ‘qy Kwlsw krYift XUnIAn dy is`K Drm dw siqkwr krn dy inXm 4.26 1 Anuswr Xog hovy[ aumIdvwr zrUrI qOr ‘qy krYift XUnIAn dy inXm 4.26 2 dy qihq, hornW qoN ielwvw ivDwnk mnwhI Aqy nOkrI dy pRspr ivroDW kwrn AwXog nw hoieAw hovy[ inXmW dI kwpI Kwlsw krYift XUnIAn dy m`uK dPqr qoN leI jw skdI hY[

mOzUdw AwnryrIAm pwilsI qihq fwierYktr borf/kmytI mIitMgW ‘c hwzr hox bdly 250/150 fwlr dy mIitMg AlwaUNs vwsqy h`kdwr hn[ idlcspI r`Kx vwly aumIdvwrW nUM bynqI kIqI jWdI hY ik auh nwmzdgI kmytI dy cyArprsn, sR hirMdr isMG sohI nwl 604-417-9490 ‘qy Pon duAwrw jW [email protected] rwhIN sMprk krn[

ikrpw krky AwpxI krYift XUnIAn nwl pUrI qrHW Swml hovo Aqy KwlsweI BwvnW dw Bwg bxo[

4

Respectively Submitted

Harinder Singh Sohi,Chairman

CHAIRMAN’S REPORT

The Canadian economy showed some signs of improvement in 2014, but the recent drop in the prime interest rate and oil �uctuations as well as a low loonie have created considerable angst among consumers. Closer to home, the good news is that the out�ow of workers to other provinces has reversed and BC is enjoying net migration growth for the rst time since 2010-11, and the population is predicted to grow by 1% in 2015.

With respect to nancial services, the continued low interest rate environment has shrunk margins to historic lows and created even more competition among nancial institutions for market share – even as families struggle with the burden of rising household debt. Mortgage and loan revenue lost due to narrow margins has not been replaced by fee income that has dwindled as the result of regulatory pressure and technological advances.

Despite all the challenges and our credit union‘s size and longevity compared to others, KCU continued to blossom and �ourish in 2014. Operating results were excellent, our ratios are among the best in BC and we were delighted to increase membership last year. Based on these results, the Board of Directors was pleased to declare a dividend of 3.25% on Class “A” Membership Shares and 5.0% on Class “B’ Equity Shares. In addition signi cant community contributions were made by way of scholarships and donations.

In 2014 we conducted a mail survey of over 5000 members and nearly 83% of respon-dents indicated they were very happy with the service provided by KCU and 56% had recommended the credit union to others during the previous six months. The board and management has reviewed the survey results and assessed the need for any changes. We expect to make this survey a regular yearly activity of KCU.

On behalf of your Board, I would like to pay tribute to and honour the memory of Sikh religious leader Bhai Sahib Bhai Jiwan Singh Ji who passed way earlier this year and who played a prominent role in the early development of this credit union.

We have come a long way since our founding in 1986 and our future remains bright with promise as we leverage our unique strengths as an ethnic-based nancial cooperative to grow healthy communities. I wish to convey my appreciation to our Chief Executive O�cer, his executive team, the branch managers and employees for their hard work and dedication to KCU. By cultivating the support of our members, we are indeed sowing the seeds of future success. We are successful because of your loyalty and ongoing support. On behalf of our Board of Directors and employees, I thank you for making KCU your own nancial institution. I invite you to contact us with any question/suggestion that you may have. I also welcome new Board members and look forward to their help in shaping the future of your credit union.

5

PUNJABITRANSLATION

CHAIRMAN’S REPORT

4

Respectively Submitted

Harinder Singh Sohi,Chairman

CHAIRMAN’S REPORT

The Canadian economy showed some signs of improvement in 2014, but the recent drop in the prime interest rate and oil �uctuations as well as a low loonie have created considerable angst among consumers. Closer to home, the good news is that the out�ow of workers to other provinces has reversed and BC is enjoying net migration growth for the rst time since 2010-11, and the population is predicted to grow by 1% in 2015.

With respect to nancial services, the continued low interest rate environment has shrunk margins to historic lows and created even more competition among nancial institutions for market share – even as families struggle with the burden of rising household debt. Mortgage and loan revenue lost due to narrow margins has not been replaced by fee income that has dwindled as the result of regulatory pressure and technological advances.

Despite all the challenges and our credit union‘s size and longevity compared to others, KCU continued to blossom and �ourish in 2014. Operating results were excellent, our ratios are among the best in BC and we were delighted to increase membership last year. Based on these results, the Board of Directors was pleased to declare a dividend of 3.25% on Class “A” Membership Shares and 5.0% on Class “B’ Equity Shares. In addition signi cant community contributions were made by way of scholarships and donations.

In 2014 we conducted a mail survey of over 5000 members and nearly 83% of respon-dents indicated they were very happy with the service provided by KCU and 56% had recommended the credit union to others during the previous six months. The board and management has reviewed the survey results and assessed the need for any changes. We expect to make this survey a regular yearly activity of KCU.

On behalf of your Board, I would like to pay tribute to and honour the memory of Sikh religious leader Bhai Sahib Bhai Jiwan Singh Ji who passed way earlier this year and who played a prominent role in the early development of this credit union.

We have come a long way since our founding in 1986 and our future remains bright with promise as we leverage our unique strengths as an ethnic-based nancial cooperative to grow healthy communities. I wish to convey my appreciation to our Chief Executive O�cer, his executive team, the branch managers and employees for their hard work and dedication to KCU. By cultivating the support of our members, we are indeed sowing the seeds of future success. We are successful because of your loyalty and ongoing support. On behalf of our Board of Directors and employees, I thank you for making KCU your own nancial institution. I invite you to contact us with any question/suggestion that you may have. I also welcome new Board members and look forward to their help in shaping the future of your credit union.

5

PUNJABITRANSLATION

CHAIRMAN’S REPORTcyArmYn dI irport

kYnyfw dI AwriQkqw ny 2014 ‘c qr`kI dy kuJ icMn ivKwey, pr pRweIm ivAwz drW ‘c qwzw igrwvt Aqy qyl dIAW kImqW ‘c auqrwA cVHwA dy nwl nwl ssqy hoey fwlr ny KpqkwrW ‘c kwPI bycYnI pYdw kIqI[ ieQoN bwry cMgI Kbr ieh hY ik kwimAW dw hor sUby v`l nUM jwx dw ruJwn aultw ho igAw hY Aqy bI sI 2010-11 qoN lY ky pihlI vwr hux Su`D Awvws vwDw vyK irhw hY Aqy 2015 ‘c v`soN 1% vwDw hox dw Anumwn lwieAw igAw hY[

iv`qI syvwvW dy sbMD ‘c, lgwqwr nIvIAW ivAwz drW dy vwqwvrx ny lwBW nUM ieiqhwsk invwxW q`k suMgyV id`qw hY Aqy iv`qI sMsQwvW drimAwn mwrkIt ‘c bxdw ih`sw pRwpq krn vwsqy hor vI vDyry mukwblw pYdw kIqw hY - jdoN ik pirvwr vD rhy GrylU krizAW dy Bwr nwl G`uL rhy hn[ mOrtgyj Aqy krizAW dI Awmdn nUM G`t lwBW krky jo nukswn hoieAw hY auh PIsW qoN huMdI Awmdn nwl BirAw nw jw sikAw, ikauNik ieh PIsW dI Awmdn ivinXmk dbwvW Aqy qknwlojI vwiDAW kwrn G`t cu`kI sI[

swrIAW cuxOqIAW Aqy horW dy mukwbly quhwfI krYift XUnIAn dw Awkwr qy AwXU dy bwvjUd Kwlsw krYift XUnIAn ny 2014 ‘c mOlxw qy vDxw Pu`lxw jwrI r`iKAw[ kMm-kwrI AmlW dy nqIjy kmwl dy sn, swfy Anupwq bI sI ‘c au~qm AnupwqW ‘coN iek sn Aqy AsIN ipCly swl ‘c AwpxI mYNbriSp vDwaux krky bVy KuS hW[ ieMnW nqIijAW dy AwDwr ‘qy fwierYktrW dy borf ny klws “ey” mYNbriSp SyArW ‘qy 3.25% Aqy klws “bI” AYkuietI SyArW ‘qy 5.0% ifvIfYNf dw AYlwn kridAW KuSI mihsUs kIqI[ ies qoN ielwvw vzIiPAW Aqy dwn dy rUp ‘c mh`qvpUrn kimaUintI Xogdwn pwey gey[

2014 ‘c AsIN 5000 qoN v`D mYNbrW dw iek fwk srvyKx krvwieAw Aqy jvwb dyx vwilAW ‘coN 83% dy nyVy Kwlsw krYift XUnIAn v`loN pRdwn kIqIAW jWdIAw syvwvW qoN bhuq KuS sn Aqy 56% ny ipCly Cy mhIinAW dOrwn krYift XUnIAn dI hornW nUM isPwirS kIqI[ boorf Aqy mYnyjmYNt ny srvyKx dy nqIijAW dI pVcol kIqI Aqy iksy vI qbdIlI dI loV nUM jWicAw[ AsIN ies srvyKx nUM Kwlsw krYift XUnIAn dI bwkwiedw slwnW kwrvweI bxwaux dI Aws r`Kdy hW[

quhwfy borf v`loN, mYN is`K Dwrimk AwgU BweI swihb BweI jIvn isMG jI, ijhVy ies swl dy SurU ‘c Akwl clwxw kr gey, Aqy ijMnHW ny ies krYift XUnIAn dy SurU dy ivkws ‘c mh`qvpUrn rol Adw kIqw, nUM SrDWjlI Aripq krdw Aqy aunHW dI Xwd nUM siqkwr pyS krdw hW[

AsIN 1986 ‘c AwpxI sQwpnW qoN lY ky hux q`k lMmW sPr qYA kIqw hY Aqy swfw Biv`K ies vwAdy nwl au~jlw rihMdw hY ik AsIN iek kOm-AwDwirq sihkwrI sMsQw vjoN Awpxw invyklw zor mzbUq kimaUintIAW dI auswrI ‘c lgwauNdy hW[ mYN Awpxy mu`K kwrj-swDk APsr, aunHW dI kwrj-swDk tIm, brWc mYnyjrW Aqy krmcwrIAW q`k aunHW dI sKq imhnq Aqy Kwlsw krYift XUnIAn pRiq lgn vwsqy AwpxI pRsMsw aunHW q`k pu`jdI krnI cwhuMdw hW[ Awpxy mYNbrW v`loN sihXog pRwpq kridAW AsIN byS`k Biv`K dI kwmXwbI vwsqy bIA bIj rhy hW[ quhwfI vPwdwrI Aqy lgwqwr iml rhy sihXog kwrn AsIN kwmXwb hW[ fwierYktrW dy borf Aqy krmcwrIAW v`loN mYN Kwlsw krYift XUnIAn nUM quhwfy duAwrw AwpxI Kud dI iv`qI sMsQw bxwaux vwsqy quhwfw DMnvwd krdw hW[ mYN quhwnUM Awpxy iksy vI svwl/suJwA, jo vI hox, bwry swfy nwl sMprk krn dw s`dw idMdw hW[ mYN nvyN borf mYNbrW nUM vI jI AwieAW AwKdw hW Aqy quhwfI krYift XUnIAn dw Biv`K aulIkx ‘c aunHW v`loN sihXog dI Aws krdw hW[

siqkwr sihq,

hirMdr isMG sohI, cyArmYn

6

Respectively Submitted

Dalbir Singh SohiChief Executive O�cer

CHIEF EXECUTIVE OFFICER’S REPORT

It was another good year for KCU. Assets grew to $321.6 million, an increase of 6.8% from the previous year. Loans were up by 6.7% while deposits climbed over $19 million. Our operating e�ciency is a cornerstone of KCU’s success and once again we outperformed the credit union system as a whole in most measurable categories.

On the product front, we were pleased to partner with Qtrade Investors, a leading online brokerage house, to provide members with access to discounted online investing services. As part of our support for youth, a Khalsa Student Line of Credit was introduced with no annual fees or standby charges. Students may borrow from $5,000 to $50,000 with interest only payments until graduation.

Free Chequing remains a popular product available to members under 25, new immigrants, mortgage holders and members with more than $50,000 on deposit with KCU. If you sign up for Direct Payroll Deposits then your chequing is also free. Our Verifast pin pad devices were upgraded in 2014. Also, the images and messages on our digital display screens were regularly rotated to keep members informed of interest rates, community events and product enhancements.

Expansion and upgrading of our branch network remains a priority for KCU. Extensive studies were conducted during 2014 as to possible branch sites in the interior of BC and a decision as to the location of our sixth branch is expected during 2015. Negotiations for a new site for our Vancouver o�ce have been concluded and the design and layout of the facility will commence shortly.

A sta� engagement survey was completed in 2014 and a new Manager, Human Resources was hired to work with employees and management on training and development programs and assess any changes identi�ed as a result of the survey. We also reviewed our policy with regard to new arrivals to Canada who haven’t yet established a credit rating in order to ease the transition to their adopted country.

I am constantly reminded of the enormous possibilities for growth at KCU and I am extremely grateful for the continuing support of the Board, management and the hard work of our employees. By working together, we can all enjoy a bountiful harvest.

7

PUNJABITRANSLATION

CHIEF EXECUTIVE OFFICER’S REPORT

6

Respectively Submitted

Dalbir Singh SohiChief Executive O�cer

CHIEF EXECUTIVE OFFICER’S REPORT

It was another good year for KCU. Assets grew to $321.6 million, an increase of 6.8% from the previous year. Loans were up by 6.7% while deposits climbed over $19 million. Our operating e�ciency is a cornerstone of KCU’s success and once again we outperformed the credit union system as a whole in most measurable categories.

On the product front, we were pleased to partner with Qtrade Investors, a leading online brokerage house, to provide members with access to discounted online investing services. As part of our support for youth, a Khalsa Student Line of Credit was introduced with no annual fees or standby charges. Students may borrow from $5,000 to $50,000 with interest only payments until graduation.

Free Chequing remains a popular product available to members under 25, new immigrants, mortgage holders and members with more than $50,000 on deposit with KCU. If you sign up for Direct Payroll Deposits then your chequing is also free. Our Verifast pin pad devices were upgraded in 2014. Also, the images and messages on our digital display screens were regularly rotated to keep members informed of interest rates, community events and product enhancements.

Expansion and upgrading of our branch network remains a priority for KCU. Extensive studies were conducted during 2014 as to possible branch sites in the interior of BC and a decision as to the location of our sixth branch is expected during 2015. Negotiations for a new site for our Vancouver o�ce have been concluded and the design and layout of the facility will commence shortly.

A sta� engagement survey was completed in 2014 and a new Manager, Human Resources was hired to work with employees and management on training and development programs and assess any changes identi�ed as a result of the survey. We also reviewed our policy with regard to new arrivals to Canada who haven’t yet established a credit rating in order to ease the transition to their adopted country.

I am constantly reminded of the enormous possibilities for growth at KCU and I am extremely grateful for the continuing support of the Board, management and the hard work of our employees. By working together, we can all enjoy a bountiful harvest.

7

PUNJABITRANSLATION

CHIEF EXECUTIVE OFFICER’S REPORTmu`K kwrj-swDk APsr dI irport

Kwlsw krYift XUnIAn vwsqy ieh iek hor vDIAw vrHw sI[ kul sMpqI vD ky 321.6 imlIAn fwlr ho geI jo ipCly vrHy nwloN 6.8% dw v`D sI[ krzw rwSI 6.7% vDI jdoN ik ifpwizt 19 imlIAn qoN au~pr cly gey[ swfI kMm-kwrI kuSlqw Kwlsw krYift XUnIAn dI kwmXwbI dI AwDwriSlw hY Aqy iek vwr iPr AsIN bhuqIAW nwpxXog SRyxIAW ‘c pUry krYift XUnIAn isstm nUM mwq pwieAw hY[

pRwfktW dy morcy ‘qy AsIN Awpxy mYbrW nUM irAwieqI AwnlweIn pUMjI invyS syvwvW q`k phuMc muh`eIAw krn leI Qtrade Investors nwl BweIvwlI kridAW KuSI mihsUs kIqI[ nvXuvkW vwsqy swfI shwieqw dy iek ih`sy vjoN Kwlsw stUfYNt lweIn AwP krYift sQwipq kIqI geI ijsdI koeI slwnW PIs jW vDIk Krcy nhIN hn[ ividAwrQI 5,000 fwlr qoN lY ky 50,000 fwlr q`k AwpxI grYjUeySn q`k isrP ivAwj dIAW pymYNtW sihq auDwr lY skdy hn[

muPq cYikMg Kwqw iek hrmn ipAwrw pRwfkt bixAw rihMdw hY ijhVw 25 qoN G`t aumr dy mYNbrW, nvyN ieMmIgrYNtW, mOrtgyj r`Kx vwilAW Aqy aunHW mYNbrW leI auplbD hY ijhVy Kwlsw krYift XUnIAn ‘c 50,000 fwlr qoN v`D dI jmHW pUMjI r`Kdy hn[ jykr qusIN is`Dy pyrol ifpwizt vwsqy ilKqI iekrwr krdy ho qW quhwfw cYikMg Kwqw vI muPq hovygw[ swfy Verifast ipMn pYf XMqr 2014 ‘c A`pgryf kIqy gey sn Aqy Awpxy mYNbrW nUM ivAwj drW, kimaUintI pRogrwmW Aqy pRwfktW ‘c vwiDAW bwry sUicq r`Kx leI ifzItl ifsplyA skrInW au~prly swfy ic`qr Aqy sunyhy bwkwiedw bdldy/c`ldy r`Ky jWdy hn[

AwpxIAW brWcW dw pwswr Aqy aunHW nUM A`pgryf krnW Kwlsw krYift XUnIAn leI pihl dw kMm rihMdw hY[ bI sI dy Dur-AMdr brWc KolHx vwsqy sMBwvq jgh qYA krn leI 2014 ‘c ivsiqRq AiDAYn krvwey gey Aqy swfI CyvIN brWc dy sQwn dy sbMD ‘c 2015 ‘c PYslw ley jwx dI Aws kIqI jWdI hY[ swfy vYnkUvr dPqr leI nvIN jgh sbMDI swrI g`lbwq Kqm kr leI geI hY Aqy ies dPqr leI ifzwien Aqy lyAwaUt dw kMm jldI ArMB ho jwvygw[

stwP dI kMMmkwrI inpuMnqw bwry iek srvyKx 2014 ‘c krvwieAw igAw sI Aqy isKlweI qy ivkws pRogrwmW leI Aqy srvyKx dy nqIjy vjoN jWcI geI iksy qbdIlI sbMDI krmcwrIAW Aqy mYnyjmYNt nwl imlky kMm krn vwsqy iek nvW mwnvI sroq mYnyjr r`iKAw igAw hY[ kYnyfw ‘c nvyN AwauNx vwilAW, ijMnHW ny Ajy AwpxI koeI krYift ryitMg nhIN bxweI huMdI, aunHW v`loN Apxwey gey nvyN mulk ‘c aunHW dI qbdIlI nUM suKwilAW bxwaux vwsqy AsIN AwpxI sbMiDq pwilsI dw vI punr inrIKx kIqw hY[

myry mn ‘c lgwqwr AwauNdw hY ik Kwlsw krYift XUnIAn ‘c vwDy dIAW byAMq sMBwvnwvW hn Aqy mYN borf, mYnyjmYNt v`loN imldy lgwqwr sihXog Aqy Awpxy krmcwrIAW dI sKq imhnq vwsqy aunHW dw AiqAMq AwBwrI hW[ imlky kMm kridAW, AsIN swry BrvIN Psl dw AnMd mwx skdy hW[

Awdr sihq,

dlbIr isMG sohI mu`K kwrj-swDk APsr

8

SOWING AND REAPING, PLANTING AND HARVESTING

The ancestral home of Khalsa Credit Union is renowned for its rich, fertile soil that produces lush crops. Harvest is celebrated in the Land of Five Waters with numerous festivals and events. Since 1986 KCU has been planting the seeds for a successful future and is now reaping the rewards from its labour. Here are some of the crops to be planted in 2015:

Branching – The branch of the future will have a much smaller footprint and will utilize digital displays and technology to improve service. In 2015 we expect to �nalize the location of the next branch of KCU and begin planning for the re-location of our Vancouver branch. We will also work with our Branch Managers to optimize business within their units.

Branding – The KCU brand grows stronger and more in�uential every year and we will work to make it part of members daily lives and help to make their lives better, more interesting and more meaningful. Telling our story at every opportunity, including facebook and our website, will be a big part of our brand building and will attract new members and enhance the product share of existing ones.

Educating – KCU is a strong proponent of education and annually awards over $30,000 in scholarships and bursaries to deserving Grade 12 students. The credit union also advocates for �nancial literacy. A major initiative in 2015 is the launch of the Khalsa Junior Credit Union, which will mimic the operations of its sponsoring organization and help students to set goals, build self-esteem and understand the di�erence between credit unions and banks. We are excited about this development and believe it could become a model for others to tap youth membership growth.

Marketing – “Millenials”, also known as Generation Y or Echo Boomers, are the fastest growing generation of consumers in history. This group is driven by community-focused causes and is the most philanthropic generation yet. Because of their size and life stage (ages 19-37) Millenials currently represent the greatest potential lifetime value of any consumer segment. KCU will consider what additional products and services will be required to attract more Millennial members, including remote deposit capture.

Mining – Our DNA computer system contains extensive information about KCU but we need to �nd better ways to “mine” the data and add to it. With this in mind, we will conduct another member survey in 2015 and establish measurement metrics so we can focus on outcomes not just processes and establish benchmarks for service standards.

Modeling – Research by the Catalyst Group indicates that having women on corporate boards results in measurably increased performance for that organization. In recent years KCU has elected women to its Board of Directors, appointed female representa-tives as executives/managers and this gender modeling will continue as KCU attempts to attract more women to its membership rolls.

Planning – KCU devotes considerable energy to planning activities, both short and long-term, in order to service its three main publics: members; employees; and communities. Within each of these publics are sub groups such as senior members whose main focus is retirement planning. Succession planning is necessary for management continuity. Your credit union will continue to be diligent in all its planning e�orts and welcomes comments and suggestions from members as to how KCU can become an even better credit union.

Training – The training and development of KCU sta� is essential for the long-term success of KCU. Our addition of a Manager, Human Resources will greatly assist in the establishment of training programs to help our employees reach their career goals and potential while serving members con�dently.

NOTICE OF INSURANCEAll members are reminded that under the terms and conditions of their mortgages or chattel lien, they are required to maintain insurance to the full insurable value of their property and/or chattels, with loss, if any payable to Khalsa Credit Union as their interest may appear.

NOTICE OF PROPERTY TAXESMembers are reminded that, if you have a mortgage with Khalsa Credit Union, you are required to pay your full property tax every year.

9

SOWING AND REAPING, PLANTING AND HARVESTING

The ancestral home of Khalsa Credit Union is renowned for its rich, fertile soil that produces lush crops. Harvest is celebrated in the Land of Five Waters with numerous festivals and events. Since 1986 KCU has been planting the seeds for a successful future and is now reaping the rewards from its labour. Here are some of the crops to be planted in 2015:

Branching – The branch of the future will have a much smaller footprint and will utilize digital displays and technology to improve service. In 2015 we expect to �nalize the location of the next branch of KCU and begin planning for the re-location of our Vancouver branch. We will also work with our Branch Managers to optimize business within their units.

Branding – The KCU brand grows stronger and more in�uential every year and we will work to make it part of members daily lives and help to make their lives better, more interesting and more meaningful. Telling our story at every opportunity, including facebook and our website, will be a big part of our brand building and will attract new members and enhance the product share of existing ones.

Educating – KCU is a strong proponent of education and annually awards over $30,000 in scholarships and bursaries to deserving Grade 12 students. The credit union also advocates for �nancial literacy. A major initiative in 2015 is the launch of the Khalsa Junior Credit Union, which will mimic the operations of its sponsoring organization and help students to set goals, build self-esteem and understand the di�erence between credit unions and banks. We are excited about this development and believe it could become a model for others to tap youth membership growth.

Marketing – “Millenials”, also known as Generation Y or Echo Boomers, are the fastest growing generation of consumers in history. This group is driven by community-focused causes and is the most philanthropic generation yet. Because of their size and life stage (ages 19-37) Millenials currently represent the greatest potential lifetime value of any consumer segment. KCU will consider what additional products and services will be required to attract more Millennial members, including remote deposit capture.

Mining – Our DNA computer system contains extensive information about KCU but we need to �nd better ways to “mine” the data and add to it. With this in mind, we will conduct another member survey in 2015 and establish measurement metrics so we can focus on outcomes not just processes and establish benchmarks for service standards.

Modeling – Research by the Catalyst Group indicates that having women on corporate boards results in measurably increased performance for that organization. In recent years KCU has elected women to its Board of Directors, appointed female representa-tives as executives/managers and this gender modeling will continue as KCU attempts to attract more women to its membership rolls.

Planning – KCU devotes considerable energy to planning activities, both short and long-term, in order to service its three main publics: members; employees; and communities. Within each of these publics are sub groups such as senior members whose main focus is retirement planning. Succession planning is necessary for management continuity. Your credit union will continue to be diligent in all its planning e�orts and welcomes comments and suggestions from members as to how KCU can become an even better credit union.

Training – The training and development of KCU sta� is essential for the long-term success of KCU. Our addition of a Manager, Human Resources will greatly assist in the establishment of training programs to help our employees reach their career goals and potential while serving members con�dently.

NOTICE OF INSURANCEAll members are reminded that under the terms and conditions of their mortgages or chattel lien, they are required to maintain insurance to the full insurable value of their property and/or chattels, with loss, if any payable to Khalsa Credit Union as their interest may appear.

NOTICE OF PROPERTY TAXESMembers are reminded that, if you have a mortgage with Khalsa Credit Union, you are required to pay your full property tax every year.

8

SOWING AND REAPING, PLANTING AND HARVESTING

The ancestral home of Khalsa Credit Union is renowned for its rich, fertile soil that produces lush crops. Harvest is celebrated in the Land of Five Waters with numerous festivals and events. Since 1986 KCU has been planting the seeds for a successful future and is now reaping the rewards from its labour. Here are some of the crops to be planted in 2015:

Branching – The branch of the future will have a much smaller footprint and will utilize digital displays and technology to improve service. In 2015 we expect to �nalize the location of the next branch of KCU and begin planning for the re-location of our Vancouver branch. We will also work with our Branch Managers to optimize business within their units.

Branding – The KCU brand grows stronger and more in�uential every year and we will work to make it part of members daily lives and help to make their lives better, more interesting and more meaningful. Telling our story at every opportunity, including facebook and our website, will be a big part of our brand building and will attract new members and enhance the product share of existing ones.

Educating – KCU is a strong proponent of education and annually awards over $30,000 in scholarships and bursaries to deserving Grade 12 students. The credit union also advocates for �nancial literacy. A major initiative in 2015 is the launch of the Khalsa Junior Credit Union, which will mimic the operations of its sponsoring organization and help students to set goals, build self-esteem and understand the di�erence between credit unions and banks. We are excited about this development and believe it could become a model for others to tap youth membership growth.

Marketing – “Millenials”, also known as Generation Y or Echo Boomers, are the fastest growing generation of consumers in history. This group is driven by community-focused causes and is the most philanthropic generation yet. Because of their size and life stage (ages 19-37) Millenials currently represent the greatest potential lifetime value of any consumer segment. KCU will consider what additional products and services will be required to attract more Millennial members, including remote deposit capture.

Mining – Our DNA computer system contains extensive information about KCU but we need to �nd better ways to “mine” the data and add to it. With this in mind, we will conduct another member survey in 2015 and establish measurement metrics so we can focus on outcomes not just processes and establish benchmarks for service standards.

Modeling – Research by the Catalyst Group indicates that having women on corporate boards results in measurably increased performance for that organization. In recent years KCU has elected women to its Board of Directors, appointed female representa-tives as executives/managers and this gender modeling will continue as KCU attempts to attract more women to its membership rolls.

Planning – KCU devotes considerable energy to planning activities, both short and long-term, in order to service its three main publics: members; employees; and communities. Within each of these publics are sub groups such as senior members whose main focus is retirement planning. Succession planning is necessary for management continuity. Your credit union will continue to be diligent in all its planning e�orts and welcomes comments and suggestions from members as to how KCU can become an even better credit union.

Training – The training and development of KCU sta� is essential for the long-term success of KCU. Our addition of a Manager, Human Resources will greatly assist in the establishment of training programs to help our employees reach their career goals and potential while serving members con�dently.

NOTICE OF INSURANCEAll members are reminded that under the terms and conditions of their mortgages or chattel lien, they are required to maintain insurance to the full insurable value of their property and/or chattels, with loss, if any payable to Khalsa Credit Union as their interest may appear.

NOTICE OF PROPERTY TAXESMembers are reminded that, if you have a mortgage with Khalsa Credit Union, you are required to pay your full property tax every year.

9

SOWING AND REAPING, PLANTING AND HARVESTING

The ancestral home of Khalsa Credit Union is renowned for its rich, fertile soil that produces lush crops. Harvest is celebrated in the Land of Five Waters with numerous festivals and events. Since 1986 KCU has been planting the seeds for a successful future and is now reaping the rewards from its labour. Here are some of the crops to be planted in 2015:

Branching – The branch of the future will have a much smaller footprint and will utilize digital displays and technology to improve service. In 2015 we expect to �nalize the location of the next branch of KCU and begin planning for the re-location of our Vancouver branch. We will also work with our Branch Managers to optimize business within their units.

Branding – The KCU brand grows stronger and more in�uential every year and we will work to make it part of members daily lives and help to make their lives better, more interesting and more meaningful. Telling our story at every opportunity, including facebook and our website, will be a big part of our brand building and will attract new members and enhance the product share of existing ones.

Educating – KCU is a strong proponent of education and annually awards over $30,000 in scholarships and bursaries to deserving Grade 12 students. The credit union also advocates for �nancial literacy. A major initiative in 2015 is the launch of the Khalsa Junior Credit Union, which will mimic the operations of its sponsoring organization and help students to set goals, build self-esteem and understand the di�erence between credit unions and banks. We are excited about this development and believe it could become a model for others to tap youth membership growth.

Marketing – “Millenials”, also known as Generation Y or Echo Boomers, are the fastest growing generation of consumers in history. This group is driven by community-focused causes and is the most philanthropic generation yet. Because of their size and life stage (ages 19-37) Millenials currently represent the greatest potential lifetime value of any consumer segment. KCU will consider what additional products and services will be required to attract more Millennial members, including remote deposit capture.

Mining – Our DNA computer system contains extensive information about KCU but we need to �nd better ways to “mine” the data and add to it. With this in mind, we will conduct another member survey in 2015 and establish measurement metrics so we can focus on outcomes not just processes and establish benchmarks for service standards.

Modeling – Research by the Catalyst Group indicates that having women on corporate boards results in measurably increased performance for that organization. In recent years KCU has elected women to its Board of Directors, appointed female representa-tives as executives/managers and this gender modeling will continue as KCU attempts to attract more women to its membership rolls.

Planning – KCU devotes considerable energy to planning activities, both short and long-term, in order to service its three main publics: members; employees; and communities. Within each of these publics are sub groups such as senior members whose main focus is retirement planning. Succession planning is necessary for management continuity. Your credit union will continue to be diligent in all its planning e�orts and welcomes comments and suggestions from members as to how KCU can become an even better credit union.

Training – The training and development of KCU sta� is essential for the long-term success of KCU. Our addition of a Manager, Human Resources will greatly assist in the establishment of training programs to help our employees reach their career goals and potential while serving members con�dently.

NOTICE OF INSURANCEAll members are reminded that under the terms and conditions of their mortgages or chattel lien, they are required to maintain insurance to the full insurable value of their property and/or chattels, with loss, if any payable to Khalsa Credit Union as their interest may appear.

NOTICE OF PROPERTY TAXESMembers are reminded that, if you have a mortgage with Khalsa Credit Union, you are required to pay your full property tax every year.

SOWING AND REAPING, PLANTING AND HARVESTING

10

PUNJABITRANSLATION

NOTICE OF INSURANCE

NOTICE OF PROPERTY TAX (PUNJABI)

11

PUNJABITRANSLATION

bIjxw Aqy v`Fxw

Kwlsw krYift XUnIAn dw ipqrI Gr AwpxI zrKyj aupjwaU BUMmI krky mShUr hY ijhVI BUMmI hrIAW BrIAW PslW pYdw krdI hY[ pMj pwxIAW dI DrqI ‘qy Psl v`Fx nwl sbMDq keI swry iqauhwr Aqy pRogrwm mnwey jWdy hn[ 1986 qoN lY ky Kwlsw krYift XUnIAn iek sPl Biv`K vwsqy bIj bIjdI Aw rhI sI Aqy hux AwpxI imhnq dy Pl nUM v`F rhI hY[ ie`Qy kuJ ku KyqIAW d`sIAW hn jo 2015 ‘c bIjIAW jwxIAW hn:

brwcW KolHxw - Biv`K dI brWc dy pd-icMnH kwPI Coty hoxgy pRMqU ieh AwpxI syvw ‘c qr`kI ilAwaux leI ifzItl ifsplyA Aqy qknwlojI vrqoN ivc ilAwvygI[ 2015 ‘c AsIN Kwlsw krYift XUnIAn dI AglI brWc dy sQwn bwry qYA kr lYx dI Aqy AwpxI vYnkUvr brWc nUM nvyN sQwn ‘qy iljwx dI Aws krdy hW[ AsIN mYnyjrW nwl vI imlky kMm krWgy qW jo aunHW dIAW brWcW ivc ibzns nUM hor vDwieAw jw sky[

brWf bxwauxw - Kwlsw krYift XUnIAn dw brWf hr vrHy mzbUq Aqy pRBwvSwlI bxdw jWdw hY Aqy AsIN iesnUM Awpxy mYNbrW dIAW rozwnW izMdgIAW dw ih`sw bxwaux Aqy aunHW dIAW izMdgIAW nUM cMgyrIAW, vDyry ijaUxXog Aqy ArQpUrn bxwaux ‘c mdd krWgy[ Pys bu`k Aqy Awpxy vY~bsweIt smyq hwsl huMdy hryk mOky ‘qy AwpxI khwxI d`sxw swfy brWf auswrI dy pRogrwm dw iek v`fw ih`sw hovygw Aqy ieh nvyN mYNbrW nUM iK`cygw qy mOzUdw mYNbrW dy pRwfkt ih`sy nUM vDweygw[

is`iKAw - Kwlsw krYift XUnIAn is`iKAw dI qkVI smrQk hY Aqy gryf 12 dy Xog ividAwrQIAW nUM vwriSk AwDwr ‘qy vzIiPAW Aqy brsrIAW dy rUp ‘c 30,000 fwlr qoN v`D dy ienwm idMdI hY[ krYift XUnIAn iv`qI is`iKAw dI vI vkwlq krdI hY[ 2015 ivc iek v`fw au~dm Kwlsw jUnIAr krYift XUnIAn dw pRwrMB hovygw, ijhVI AwpxI pRwXojk sMsQw dy kMm-kwrI Aml Anuswr c`lygI Aqy ividAwrQIAW nUM Awpxy inSwny qYA krn, svY-mwx auswrn Aqy krYift XUnIAn Aqy bYNkW drimAwn Prk nUM smJx ‘c mdd krygI[ AsIN ies qr`kI bwry bVy auqSwhpUrn hW Aqy XkIn r`Kdy hW ik nvXuvkW ‘c mYNbriS`p vDwaux leI ieh hornW leI mwfl bxygI[

mwrkIitMg - “imlynIAlz” ijMnHW nUM jYnrySn vweI jW eIko bUmrz vjoN vI jwixAW jWdw hY, ieiqhws ‘c KpqkwrW dI sB qoN qyzI nwl vDx vwlI pIVHI hY[ ieh gru`p kimaUintI-kyNdirq kwrnW duAwrw sMcwilq hY Aqy Ajy q`k dI sB qoN v`D pRaupkwrI pIVHI hY[ Awpxy Awkwr Aqy aumr dy pVwA (19-37 dI aumr) krky imlynIAlz mOzUdw smyN iksy vI Kpqkwr gru`p nwloN sB qoN v`D sMBwvI jIvn-kwl mu`l dI pRqIinDqw krdy hn[ Kwlsw krYift XUnIAn, irmot-ifpwizt kr skx smyq ies g`l au~pr ivcwr krygI ik hor vDyry imlynIAlz mYNbrW nUM Awpxy v`l iK`cx leI ikhVy vDIk pRwfkt Aqy syvwvW dI zrUrq hovygI[

SOWING AND REAPING, PLANTING AND HARVESTING

10

PUNJABITRANSLATION

NOTICE OF INSURANCE

NOTICE OF PROPERTY TAX (PUNJABI)

11

PUNJABITRANSLATION

mweIinMg - swfy fI AYn ey kMmipaUtr isstm ‘c Kwlsw krYift XUnIAn bwry ivsiqRq pRkwr dI jwxkwrI peI hoeI hY[ prMqU swnUM fYtw “Koj k`Fx” Aqy hor pwaux leI izAwdw cMgy qrIky l`Bx dI loV hY[ ies g`l nUM iDAwn ‘c r`KidAW AsIN 2015 ‘c iek hor mYNbr srvyKx krvwvWgy Aqy imxqI dy qrIky sQwpq krWgy qW ik AsIN kyvl FMg-qrIikAW ‘qy hI nhIN sgoN nqIijAW ‘qy kyNdirq hoeIey Aqy Awpxy syvw dy drizAW nUM im`Qx leI mwpdMf sQwpq kr skIey[

mwfilMg - kYtwilst gru`p v`loN kIqI iek Koj drswauNdI hY ik kwrporyt borfW ‘c AOrqW nUM r`Kx dy nqIjy aus sMsQw dI kwrguzwrI ‘c izkrXog vwDy vjoN inkldy hn[ bIqy qwzw virHAW ‘c Kwlsw krYift XUnIAn ny Awpxy fwierYktrW dy borf ‘c AOrqW nUM cuixAw hY, kwrjswDkW/mYnyjrW vjoN AOrq pRiqinDW nUM inXukq kIqw hY Aqy ieh ilMg mwfilMg jwrI rhygI, jdoN ik Kwlsw krYift XUnIAn AwpxI mYNbriS`p sUcI ‘c hor vDyry AOrqW nUM iK`cx dy Xqn krygI[

XojnWbMdI - Kwlsw krYift XUnIAn iqMn mu`K pRkwr dy lokW; mYNbrW; krmcwrIAW Aqy kimaUintIAW nUM syvwvW dyx leI QoVH-icrIAW Aqy lMmyN smyN dIAW kwrvweIAW dI XojnWbMdI ‘qy izkrXog SkqI lgwauNdI hY[ ieMnHW iqMnW pRkwr dy lokW ‘c au`p-gru`p hn ijvyN sInIAr mYNbr, ijMnHW dw mu`K iDAwn irtwiermYNt dI XojnwbMdI ‘qy huMdw hY[ au~qrwiDkwr bwry XojnW bxwauxw pRbMD nUM jwrI r`Kx vwsqy zrUrI huMdw hY[ quhwfI krYift XUnIAn XojnWbMdI dy Awpxy XqnW nUM lgwqwr imhnq sihq jwrI r`KygI Aqy Kwlsw krYift XUnIAn hor cMgyrI krYift XUnIAn ikvyN bx skdI hY, ies bwry mYNbrW dIAW it`pxIAW Aqy suJwvW nUM jI AwieAW AwKdI hY[

tryinMg - Kwlsw krYift XUnIAn dI lMmyry smyN dI kwmXwbI leI Kwlsw krYift XUnIAn dy stwP dI tryinMg Aqy ivkws zrUrI hY[ Awpxy mYNbrW dI ivSvwS sihq syvw kridAW hoieAW, swfy kmrcwrIAW leI mYnyjr, mwnvI sroq dw r`iKAw jwxw krmcwrIAW nUM Awpxy ik`qy sbMDI inSwinAW Aqy sMBwvnwvW dIAW pRwpqIAW leI loVINdy tryinMg pRogrwmW dI sQwpqI ‘c bVw shweI hovygw[

bImyN dw noitsswry mYˆbrW ƒ Xwd idvwieAw jWdw hY ik aunHW dIAW mwrtgyjW jW cYtl lIAn dIAW SrqW qy zrUrqW dy qihq aunWH ƒ zrUrq hY ik auh AwpxIAW pRwprtIAW Aqy/jW cYtlW dy ku`l bImw Xog mu`l vwsqy aunHW dw bImw krvw ky r`Kx ijs ’c ieh hovy ik aunHW dw koeI nukswn ho jwx dI sUrq ’c bImy dI rkm Kwlsw krYift XUnIAn ƒ imlx Xog hovy[

pRwprtI tYks dw noitsmYNbrW nUM Xwd idvwieAw jWdw hY ik, jykr quhwfI mOrtgyj Kwlsw krYift XUnIAn nwl hY, qW quhwnUM hr swl Awpxw pUrw pRwprtI tYks Adw krn dI zrUrq hY[

12

Report of the Independent Auditor on the Summary Financial Statements

To the Members ofKhalsa Credit Union

The accompanying summary financial statements which comprise the Summary Statement of FinancialPosition as at December 31, 2014, the Summary Statements of Comprehensive Income, Changes inMembers' Equity and Cash Flows for the year ended December 31, 2014. We expressed an unmodifiedaudit opinion on those financial statements in our report dated March 1, 2015. Those financialstatements, and the summary financial statements, do not reflect the effects of events that occurredsubsequent to the date of our report on those financial statements.

The summary financial statements do not contain all the disclosures required by International FinancialReporting Standards. Reading the summary financial statements, therefore, is not a substitute forreading the audited financial statements of Khalsa Credit Union.

Management's Responsibility for the Summary Financial Statements

Management is responsible for the preparation of the summary of the audited financial statements.

Auditor's Responsibility

Our responsibility is to express an opinion on the summary financial statements based on ourprocedures, which were conducted in accordance with Canadian Auditing Standard (CAS) 810,"Engagements to Report on Summary Financial Statements."

Opinion

In our opinion, the summary financial statements derived from the audited financial statements ofKhalsa Credit Union for the year ended December 31, 2014 are a fair summary of those financialstatements.

Chartered Accountants

Vancouver, British ColumbiaMarch 1, 2015

Tel: 604 688 5421 Fax: 604 688 5132 [email protected] www.bdo.ca

BDO Canada LLP 600 Cathedral Place 925 West Georgia Street Vancouver BC V6C 3L2 Canada

13

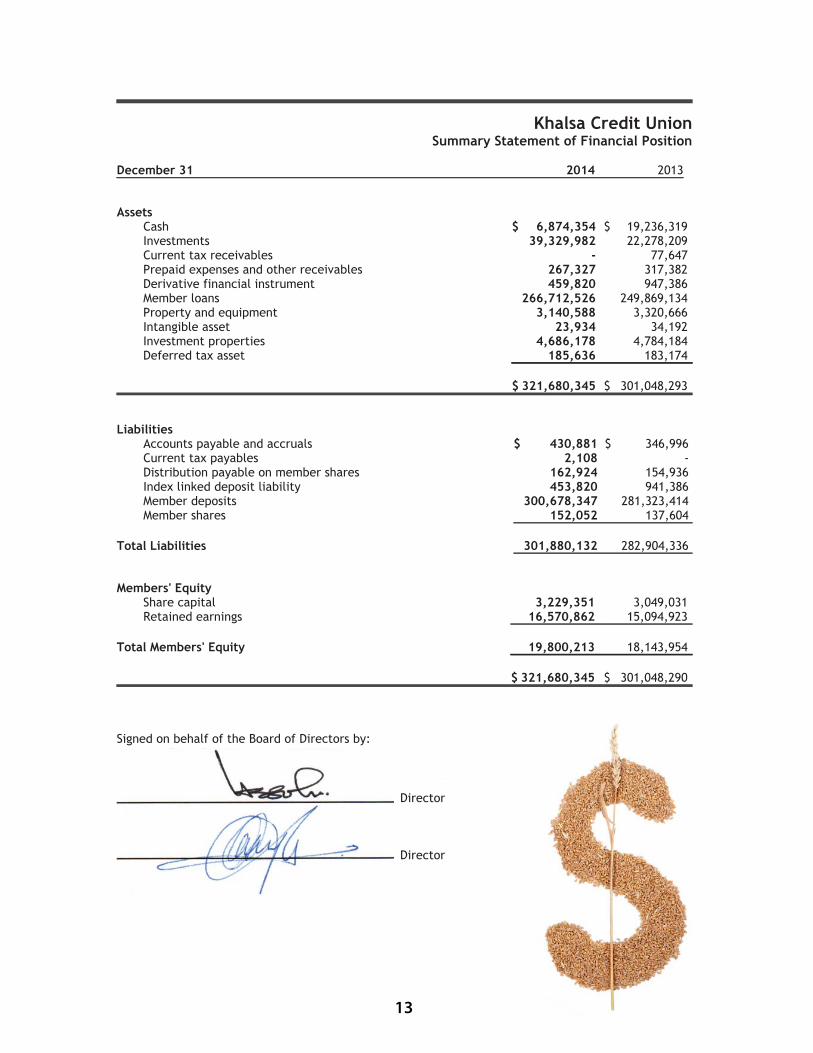

Khalsa Credit UnionSummary Statement of Financial Position

410213 rebmeceD 2013

AssetsCash $ 6,874,354 $ 19,236,319Investments 39,329,982 22,278,209Current tax receivables - 77,647Prepaid expenses and other receivables 267,327 317,382Derivative financial instrument 459,820 947,386Member loans 266,712,526 249,869,134Property and equipment 3,140,588 3,320,666Intangible asset 23,934 34,192Investment properties 4,686,178 4,784,184Deferred tax asset 185,636 183,174

$ 321,680,345 $ 301,048,293

LiabilitiesAccounts payable and accruals $ 430,881 $ 346,996Current tax payables 2,108 -Distribution payable on member shares 162,924 154,936Index linked deposit liability 453,820 941,386Member deposits 300,678,347 281,323,414Member shares 152,052 137,604

Total Liabilities 301,880,132 282,904,336

Members' EquityShare capital 3,229,351 3,049,031Retained earnings 16,570,862 15,094,923

Total Members' Equity 19,800,213 18,143,954

$ 321,680,345 $ 301,048,290

Signed on behalf of the Board of Directors by:

Director

Director

12

Report of the Independent Auditor on the Summary Financial Statements

To the Members ofKhalsa Credit Union

The accompanying summary financial statements which comprise the Summary Statement of FinancialPosition as at December 31, 2014, the Summary Statements of Comprehensive Income, Changes inMembers' Equity and Cash Flows for the year ended December 31, 2014. We expressed an unmodifiedaudit opinion on those financial statements in our report dated March 1, 2015. Those financialstatements, and the summary financial statements, do not reflect the effects of events that occurredsubsequent to the date of our report on those financial statements.

The summary financial statements do not contain all the disclosures required by International FinancialReporting Standards. Reading the summary financial statements, therefore, is not a substitute forreading the audited financial statements of Khalsa Credit Union.

Management's Responsibility for the Summary Financial Statements

Management is responsible for the preparation of the summary of the audited financial statements.

Auditor's Responsibility

Our responsibility is to express an opinion on the summary financial statements based on ourprocedures, which were conducted in accordance with Canadian Auditing Standard (CAS) 810,"Engagements to Report on Summary Financial Statements."

Opinion

In our opinion, the summary financial statements derived from the audited financial statements ofKhalsa Credit Union for the year ended December 31, 2014 are a fair summary of those financialstatements.

Chartered Accountants

Vancouver, British ColumbiaMarch 1, 2015

Tel: 604 688 5421 Fax: 604 688 5132 [email protected] www.bdo.ca

BDO Canada LLP 600 Cathedral Place 925 West Georgia Street Vancouver BC V6C 3L2 Canada

13

Khalsa Credit UnionSummary Statement of Financial Position

410213 rebmeceD 2013

AssetsCash $ 6,874,354 $ 19,236,319Investments 39,329,982 22,278,209Current tax receivables - 77,647Prepaid expenses and other receivables 267,327 317,382Derivative financial instrument 459,820 947,386Member loans 266,712,526 249,869,134Property and equipment 3,140,588 3,320,666Intangible asset 23,934 34,192Investment properties 4,686,178 4,784,184Deferred tax asset 185,636 183,174

$ 321,680,345 $ 301,048,293

LiabilitiesAccounts payable and accruals $ 430,881 $ 346,996Current tax payables 2,108 -Distribution payable on member shares 162,924 154,936Index linked deposit liability 453,820 941,386Member deposits 300,678,347 281,323,414Member shares 152,052 137,604

Total Liabilities 301,880,132 282,904,336

Members' EquityShare capital 3,229,351 3,049,031Retained earnings 16,570,862 15,094,923

Total Members' Equity 19,800,213 18,143,954

$ 321,680,345 $ 301,048,290

Signed on behalf of the Board of Directors by:

Director

Director

14

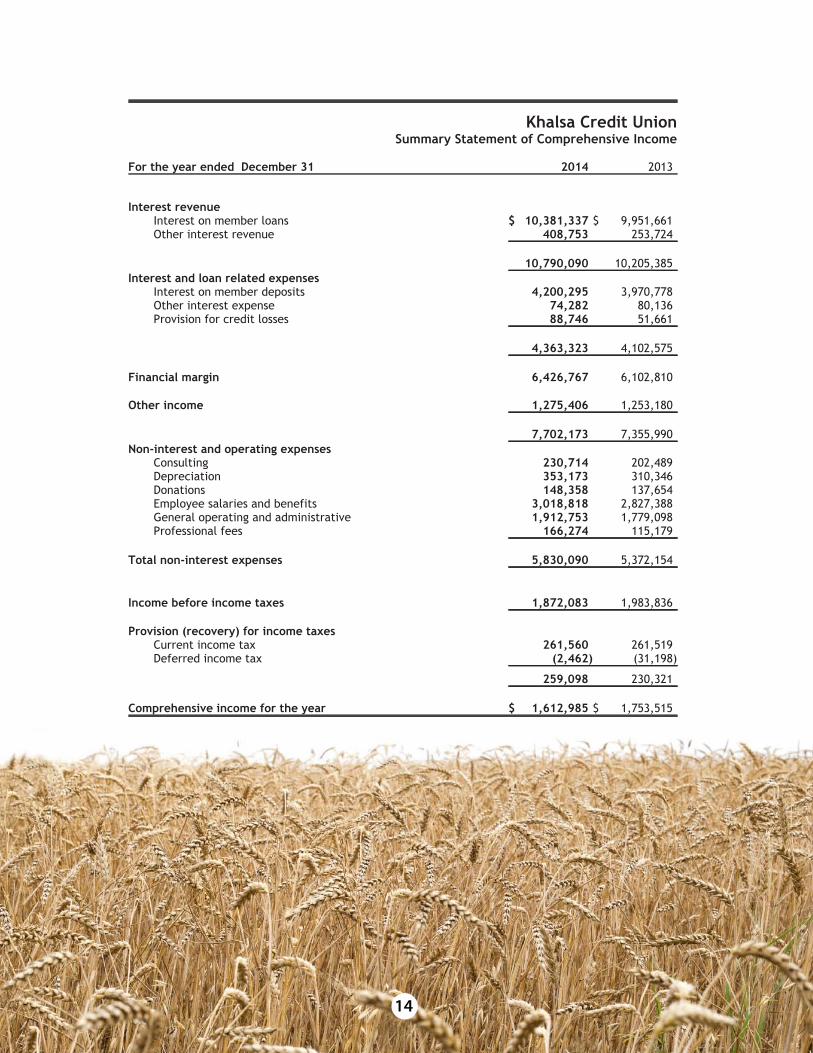

Khalsa Credit UnionSummary Statement of Comprehensive Income

410213 rebmeceD dedne raey eht roF 2013

Interest revenueInterest on member loans $ 10,381,337 $ 9,951,661Other interest revenue 408,753 253,724

10,790,090 10,205,385Interest and loan related expenses

Interest on member deposits 4,200,295 3,970,778Other interest expense 74,282 80,136Provision for credit losses 88,746 51,661

4,363,323 4,102,575

Financial margin 6,426,767 6,102,810

604,572,1 emocni rehtO 1,253,180

7,702,173 7,355,990Non-interest and operating expenses

Consulting 230,714 202,489Depreciation 353,173 310,346Donations 148,358 137,654Employee salaries and benefits 3,018,818 2,827,388General operating and administrative 1,912,753 1,779,098Professional fees 166,274 115,179

Total non-interest expenses 5,830,090 5,372,154

380,278,1sexat emocni erofeb emocnI 1,983,836

Provision (recovery) for income taxesCurrent income tax 261,560 261,519Deferred income tax (2,462) (31,198)

259,098 230,321

Comprehensive income for the year $ 1,612,985 $ 1,753,515

15

For the year ended December 31

Balance at January 1, 2013

Balance on December 31, 2013

Balance on December 31, 2014

Operating Activities

Adjustments for non-cash items:

investment propertyProvision for credit lossesDeferred tax asset

Changes in member activitiesNet increase in member loansNet increase in deposits

Investing Activities

Purchases of property and equipmentAdditions to investment properties

Financing ActivitiesNet increase in equity shares

Net increase (decrease) in cash

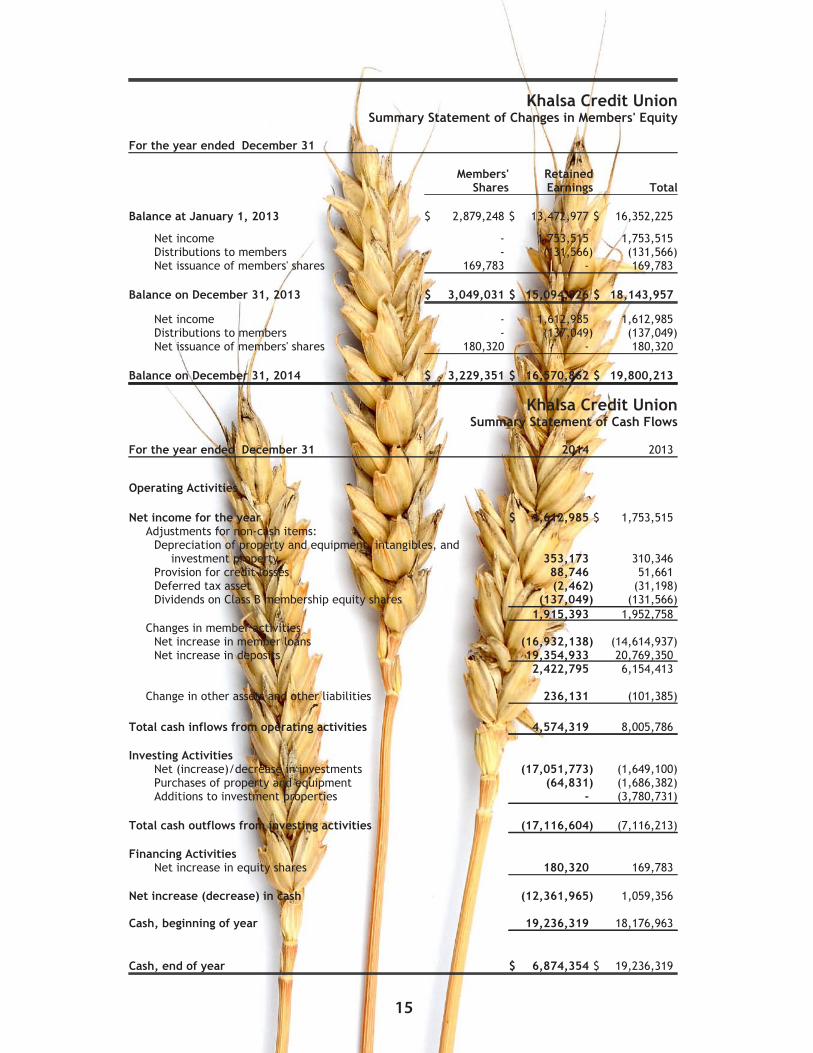

Khalsa Credit UnionSummary Statement of Changes in Members' Equity

Members'Shares

RetainedEarnings Total

$ 2,879,248 $ 13,472,977 $ 16,352,225

515,357,1515,357,1-emocni teN)665,131()665,131(- srebmem ot snoitubirtsiD

387,961-387,961serahs 'srebmem fo ecnaussi teN

$ 3,049,031 $ 15,094,926 $ 18,143,957

589,216,1589,216,1-emocni teN)940,731()940,731(- srebmem ot snoitubirtsiD

023,081-023,081serahs 'srebmem fo ecnaussi teN

$ 3,229,351 $ 16,570,862 $ 19,800,213

Khalsa Credit UnionSummary Statement of Cash Flows

4102 13 rebmeceD dedne raey eht roF 2013

589,216,1$raey eht rof emocni teN $ 1,753,515

Depreciation of property and equipment, intangibles, and353,173 310,34688,746 51,661(2,462) (31,198)

Dividends on Class B membership equity shares (137,049) (131,566)1,915,393 1,952,758

(16,932,138) (14,614,937)19,354,933 20,769,3502,422,795 6,154,413

Change in other assets and other liabilities 236,131 (101,385)

913,475,4seitivitca gnitarepo morf swolfni hsac latoT 8,005,786

Net (increase)/decrease in investments (17,051,773) (1,649,100)(64,831) (1,686,382)

- (3,780,731)

Total cash outflows from investing activities (17,116,604) (7,116,213)

180,320 169,783

(12,361,965) 1,059,356

913,632,91raey fo gninnigeb ,hsaC 18,176,963

453,478,6$raey fo dne ,hsaC $ 19,236,319

14

Khalsa Credit UnionSummary Statement of Comprehensive Income

410213 rebmeceD dedne raey eht roF 2013

Interest revenueInterest on member loans $ 10,381,337 $ 9,951,661Other interest revenue 408,753 253,724

10,790,090 10,205,385Interest and loan related expenses

Interest on member deposits 4,200,295 3,970,778Other interest expense 74,282 80,136Provision for credit losses 88,746 51,661

4,363,323 4,102,575

Financial margin 6,426,767 6,102,810

604,572,1 emocni rehtO 1,253,180

7,702,173 7,355,990Non-interest and operating expenses

Consulting 230,714 202,489Depreciation 353,173 310,346Donations 148,358 137,654Employee salaries and benefits 3,018,818 2,827,388General operating and administrative 1,912,753 1,779,098Professional fees 166,274 115,179

Total non-interest expenses 5,830,090 5,372,154

380,278,1sexat emocni erofeb emocnI 1,983,836

Provision (recovery) for income taxesCurrent income tax 261,560 261,519Deferred income tax (2,462) (31,198)

259,098 230,321

Comprehensive income for the year $ 1,612,985 $ 1,753,515

15

For the year ended December 31

Balance at January 1, 2013

Balance on December 31, 2013

Balance on December 31, 2014

Operating Activities

Adjustments for non-cash items:

investment propertyProvision for credit lossesDeferred tax asset

Changes in member activitiesNet increase in member loansNet increase in deposits

Investing Activities

Purchases of property and equipmentAdditions to investment properties

Financing ActivitiesNet increase in equity shares

Net increase (decrease) in cash

Khalsa Credit UnionSummary Statement of Changes in Members' Equity

Members'Shares

RetainedEarnings Total

$ 2,879,248 $ 13,472,977 $ 16,352,225

515,357,1515,357,1-emocni teN)665,131()665,131(- srebmem ot snoitubirtsiD

387,961-387,961serahs 'srebmem fo ecnaussi teN

$ 3,049,031 $ 15,094,926 $ 18,143,957

589,216,1589,216,1-emocni teN)940,731()940,731(- srebmem ot snoitubirtsiD

023,081-023,081serahs 'srebmem fo ecnaussi teN

$ 3,229,351 $ 16,570,862 $ 19,800,213

Khalsa Credit UnionSummary Statement of Cash Flows

4102 13 rebmeceD dedne raey eht roF 2013

589,216,1$raey eht rof emocni teN $ 1,753,515

Depreciation of property and equipment, intangibles, and353,173 310,34688,746 51,661(2,462) (31,198)

Dividends on Class B membership equity shares (137,049) (131,566)1,915,393 1,952,758

(16,932,138) (14,614,937)19,354,933 20,769,3502,422,795 6,154,413

Change in other assets and other liabilities 236,131 (101,385)

913,475,4seitivitca gnitarepo morf swolfni hsac latoT 8,005,786

Net (increase)/decrease in investments (17,051,773) (1,649,100)(64,831) (1,686,382)

- (3,780,731)

Total cash outflows from investing activities (17,116,604) (7,116,213)

180,320 169,783

(12,361,965) 1,059,356

913,632,91raey fo gninnigeb ,hsaC 18,176,963

453,478,6$raey fo dne ,hsaC $ 19,236,319

16

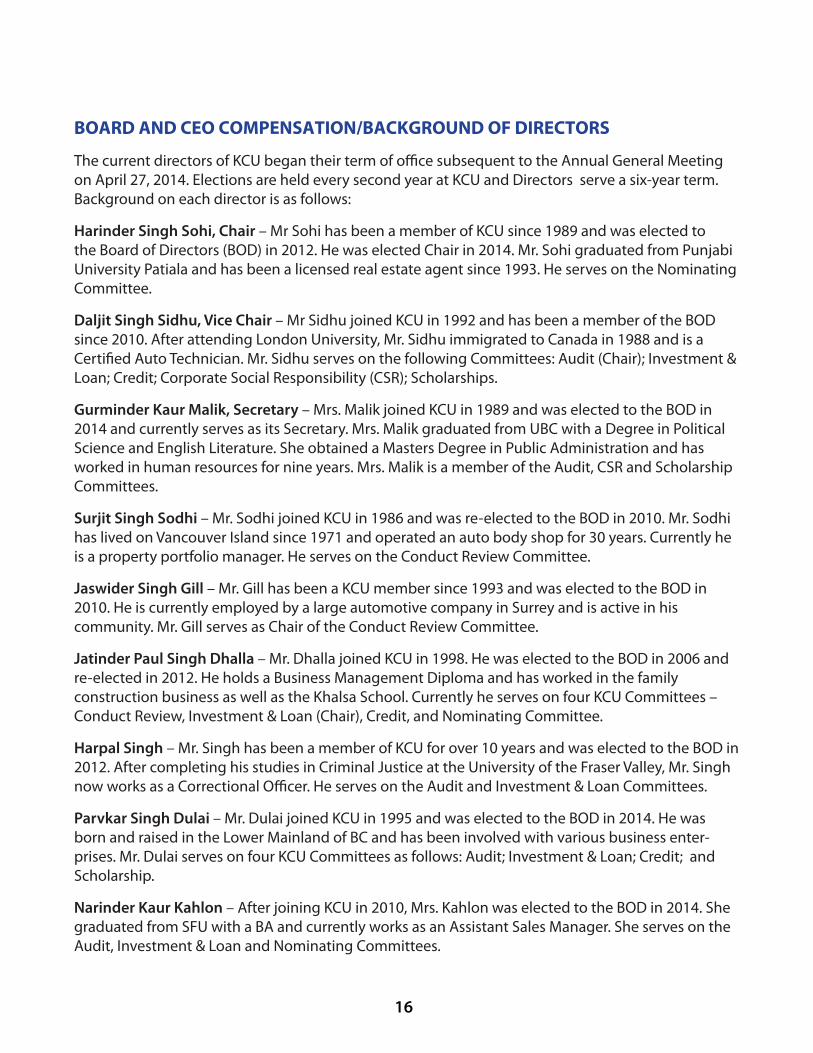

BOARD AND CEO COMPENSATION/BACKGROUND OF DIRECTORS

The current directors of KCU began their term of oce subsequent to the Annual General Meeting on April 27, 2014. Elections are held every second year at KCU and Directors serve a six-year term. Background on each director is as follows:

Harinder Singh Sohi, Chair – Mr Sohi has been a member of KCU since 1989 and was elected to the Board of Directors (BOD) in 2012. He was elected Chair in 2014. Mr. Sohi graduated from Punjabi University Patiala and has been a licensed real estate agent since 1993. He serves on the Nominating Committee.

Daljit Singh Sidhu, Vice Chair – Mr Sidhu joined KCU in 1992 and has been a member of the BOD since 2010. After attending London University, Mr. Sidhu immigrated to Canada in 1988 and is a Certi�ed Auto Technician. Mr. Sidhu serves on the following Committees: Audit (Chair); Investment & Loan; Credit; Corporate Social Responsibility (CSR); Scholarships.

Gurminder Kaur Malik, Secretary – Mrs. Malik joined KCU in 1989 and was elected to the BOD in 2014 and currently serves as its Secretary. Mrs. Malik graduated from UBC with a Degree in Political Science and English Literature. She obtained a Masters Degree in Public Administration and has worked in human resources for nine years. Mrs. Malik is a member of the Audit, CSR and Scholarship Committees.

Surjit Singh Sodhi – Mr. Sodhi joined KCU in 1986 and was re-elected to the BOD in 2010. Mr. Sodhi has lived on Vancouver Island since 1971 and operated an auto body shop for 30 years. Currently he is a property portfolio manager. He serves on the Conduct Review Committee.

Jaswider Singh Gill – Mr. Gill has been a KCU member since 1993 and was elected to the BOD in 2010. He is currently employed by a large automotive company in Surrey and is active in his community. Mr. Gill serves as Chair of the Conduct Review Committee.

Jatinder Paul Singh Dhalla – Mr. Dhalla joined KCU in 1998. He was elected to the BOD in 2006 and re-elected in 2012. He holds a Business Management Diploma and has worked in the family construction business as well as the Khalsa School. Currently he serves on four KCU Committees – Conduct Review, Investment & Loan (Chair), Credit, and Nominating Committee.

Harpal Singh – Mr. Singh has been a member of KCU for over 10 years and was elected to the BOD in 2012. After completing his studies in Criminal Justice at the University of the Fraser Valley, Mr. Singh now works as a Correctional Ocer. He serves on the Audit and Investment & Loan Committees.

Parvkar Singh Dulai – Mr. Dulai joined KCU in 1995 and was elected to the BOD in 2014. He was born and raised in the Lower Mainland of BC and has been involved with various business enter-prises. Mr. Dulai serves on four KCU Committees as follows: Audit; Investment & Loan; Credit; and Scholarship.

Narinder Kaur Kahlon – After joining KCU in 2010, Mrs. Kahlon was elected to the BOD in 2014. She graduated from SFU with a BA and currently works as an Assistant Sales Manager. She serves on the Audit, Investment & Loan and Nominating Committees.

17

BOARD AND CEO COMPENSATION/BACKGROUND OF DIRECTORS

PUNJABITRANSLATION

16

BOARD AND CEO COMPENSATION/BACKGROUND OF DIRECTORS

The current directors of KCU began their term of oce subsequent to the Annual General Meeting on April 27, 2014. Elections are held every second year at KCU and Directors serve a six-year term. Background on each director is as follows:

Harinder Singh Sohi, Chair – Mr Sohi has been a member of KCU since 1989 and was elected to the Board of Directors (BOD) in 2012. He was elected Chair in 2014. Mr. Sohi graduated from Punjabi University Patiala and has been a licensed real estate agent since 1993. He serves on the Nominating Committee.

Daljit Singh Sidhu, Vice Chair – Mr Sidhu joined KCU in 1992 and has been a member of the BOD since 2010. After attending London University, Mr. Sidhu immigrated to Canada in 1988 and is a Certi�ed Auto Technician. Mr. Sidhu serves on the following Committees: Audit (Chair); Investment & Loan; Credit; Corporate Social Responsibility (CSR); Scholarships.

Gurminder Kaur Malik, Secretary – Mrs. Malik joined KCU in 1989 and was elected to the BOD in 2014 and currently serves as its Secretary. Mrs. Malik graduated from UBC with a Degree in Political Science and English Literature. She obtained a Masters Degree in Public Administration and has worked in human resources for nine years. Mrs. Malik is a member of the Audit, CSR and Scholarship Committees.

Surjit Singh Sodhi – Mr. Sodhi joined KCU in 1986 and was re-elected to the BOD in 2010. Mr. Sodhi has lived on Vancouver Island since 1971 and operated an auto body shop for 30 years. Currently he is a property portfolio manager. He serves on the Conduct Review Committee.

Jaswider Singh Gill – Mr. Gill has been a KCU member since 1993 and was elected to the BOD in 2010. He is currently employed by a large automotive company in Surrey and is active in his community. Mr. Gill serves as Chair of the Conduct Review Committee.

Jatinder Paul Singh Dhalla – Mr. Dhalla joined KCU in 1998. He was elected to the BOD in 2006 and re-elected in 2012. He holds a Business Management Diploma and has worked in the family construction business as well as the Khalsa School. Currently he serves on four KCU Committees – Conduct Review, Investment & Loan (Chair), Credit, and Nominating Committee.

Harpal Singh – Mr. Singh has been a member of KCU for over 10 years and was elected to the BOD in 2012. After completing his studies in Criminal Justice at the University of the Fraser Valley, Mr. Singh now works as a Correctional Ocer. He serves on the Audit and Investment & Loan Committees.

Parvkar Singh Dulai – Mr. Dulai joined KCU in 1995 and was elected to the BOD in 2014. He was born and raised in the Lower Mainland of BC and has been involved with various business enter-prises. Mr. Dulai serves on four KCU Committees as follows: Audit; Investment & Loan; Credit; and Scholarship.

Narinder Kaur Kahlon – After joining KCU in 2010, Mrs. Kahlon was elected to the BOD in 2014. She graduated from SFU with a BA and currently works as an Assistant Sales Manager. She serves on the Audit, Investment & Loan and Nominating Committees.

17

BOARD AND CEO COMPENSATION/BACKGROUND OF DIRECTORS

PUNJABITRANSLATION

borf Aqy m`uK kwrj-swDk APsr dy muAwvzy/fwierYktrW dI ip`T BUMmI

Kwlsw krYift XUnIAn dy mOzUdw fwierYktrW ny 27 AprYl 2014 dy slwnW Awm iejlws qoN auprMq Awpxy AhuidAW dI imAwd SurU kIqI[ krYift XUnIAn dy cuxwau hryk dUsry vrHy huMdy hn Aqy fwierYktr 6 virHAW dI imAwd leI syvw inBwauNdy hn[ hryk fwierYktr dI ip`TBUMmI hyTW ilKy dI qrHW hY:

hirMdr isMG sohI, cyArmYn - sR. sohI 1989 qoN Kwlsw krYift XUnIAn dy mYNbr cly Aw rhy hn Aqy auh 2012 ‘c fwierYktrW dy borf (BOD) vwsqy cuxy gey[ sR. sohI ny pMjwbI XUnIvristI pitAwlw qoN grYjUeySn kIqI Aqy 1993 qoN lwiesYNsSudw rIAl iestyt eyjMt cly Aw rhy hn[ auh nwmInyitMg kmytI ‘qy syvw inBwA rhy hn[

dljIq isMG is`DU, aup-cyArmYn - sR. is`DU 1992 ‘c Kwlsw krYift XUnIAn ‘c Swml hoey Aqy 2010 qoN fwierYktrW dy borf dy mYNbr cly Aw rhy hn[ lMfn XUnIvristI qoN pVHweI Kqm krn mgroN sR. is`DU 1988 ‘c kYnyfw Aw gey Aqy auh srtIPweIf Awto tYknISIAn hn[ sR. is`DU A`gy id`qIAW kmytIAW ‘c syvwvW inBwA rhy hn: Awift (cyAr); ieMnvYstmYNt AYNf lon; krYift; kwrporyt soSl irspWisibiltI (CSR); skwlriS`p[

gurimMdr kOr milk, sk`qr - srdwrnI milk 1989 ‘c Kwlsw krYift XUnIAn ‘c Swml hoey Aqy 2014 ‘c auh fwierYktrW dy borf leI cuxy gey sn Aqy mOzUdw smyN iesdy sk`qr vjoN syvw inBwA rhy hn[ srdwrnI milk XU bI sI dy grYjUeyt hn Aqy aunHW ny rwjnIqI SwSqr Aqy AMgryzI swihq ‘c ifgrI hwsl kIqI[ aunHW ny pbilk pRSwsn ‘c mwstr ifgrI leI Aqy nON swl mwnvI sroq ivBwg ‘c kMm kIqw[ srdwrnI milk Awift, kwrporyt soSl irspWisibiltI Aqy skwlriS`p kmytIAW dy mYNbr hn[

surjIq isMG soFI - sR. soFI 1986 ‘c Kwlsw krYift XUnIAn ‘c Swml hoey Aqy 2010 ‘c fwierYktrW dy borf leI muV cuxy gey[ sR. soFI vYnkUvr AweIlYNf ‘qy rihMdy rhy Aqy aunHW ny 30 virHAW q`k Awto bwfI Swp clweI[ mOzUdw smyN auh pRwprtI potrPolIau mYnyjr hn[ auh kMfkt rIivaU kmytI ‘qy syvw inBwA rhy hn[

jsivMdr isMG ig`l - sR. ig`l 1993 qoN Kwlsw krYift XUnIAn dy mYNbr hn Aqy auh 2010 ‘c fwierYktrW dy borf vwsqy cuxy gey[ mOzUdw smy auh srI ‘c v`fI Awtomoitv kMpnI ‘c nOkrI krdy hn Aqy AwpxI kimaUintI ‘c srgrm hn[ sR. ig`l kMfkt rIivaU kmytI dy cyArmYn vjoN syvw inBwA rhy hn[

jiqMdr pwl isMG Fwlw - sR. Fwlw 1998 ‘c Kwlsw krYift XUnIAn ‘c Swml hoey[ auh 2006 ‘c fwierYktrW dy borf leI cuxy gey Aqy 2012 ‘c auh muV cuxy gey[ aunHW pws ibzns mYnyjmYNt ‘c ifplomw hY Aqy aunHW ny auswrI dy pirvwrk kwrobwr Aqy nwl hI Kwlsw skUl ‘c kMm kIqw[ mOzUdw smyN auh Kwlsw krYift XUnIAn dIAW cwr kmytIAW-kMfkt rIivaU, ieMnvYstmYNt AYNf lon (cyAr), krYift Aqy nwmInyitMg kmytI ‘qy syvw inBwA rhy hn[

hrpwl isMG - sR. isMG 10 swlW qoN vDyry smyN qoN Kwlsw krYift XUnIAn dy mYNbr hn Aqy auh 2012 ‘c fwierYktrW dy borf vwsqy cuxy gey[ XUnIvristI AwP id Pryzr vYlI qoN ikRmInl jsits ‘c AwpxI ifgrI Kqm krn mgroN, sR. isMG hux iek kurYkSn APsr vjoN kMm kr rhy hn[ auh Awift Aqy ieMnvYstmYNt AYNf lon kmytIAW ‘qy syvw inBwA rhy hn[

prvkwr isMG dUly - sR. dUly 1995 ‘c Kwlsw krYift XUnIAn ‘c Swml hoey Aqy auh 2014 ‘c fwierYktrW dy borf vwsqy cuxy gey[ auh bI sI dI loAr mynlYNf ‘c jMmy, pLy Aqy auh v`K v`K kwrobwrW ‘c Swml cly Aw rhy hn[ sR. dUly Kwlsw krYift XUnIAn dIAW A`gy id`qIAW geIAW cwr kmytIAW ‘c syvwvW inBwA rhy hn: Awift; ieMnvYstmYNt AYNf lon; krYift Aqy skwlriS`p[

nirMdr kOr kwhloN - 2010 ‘c Kwlsw krYift XUnIAn ‘c Swml hox mgroN srdwrnI kwhloN 2014 fwierYktrW dy borf leI cuxy gey[ auh AY~s AY~P XU qoN bI ey krky grYjUeyt hoey Aqy mOjUdw smyN auh AisstYNt sylz mYnyjr vjoN kMm krdy hn[ auh Awift, ieMnvYstmYNt AYNf lon Aqy nwmInyitMg kmytIAW ‘qy syvw inBwA rhy hn[

18

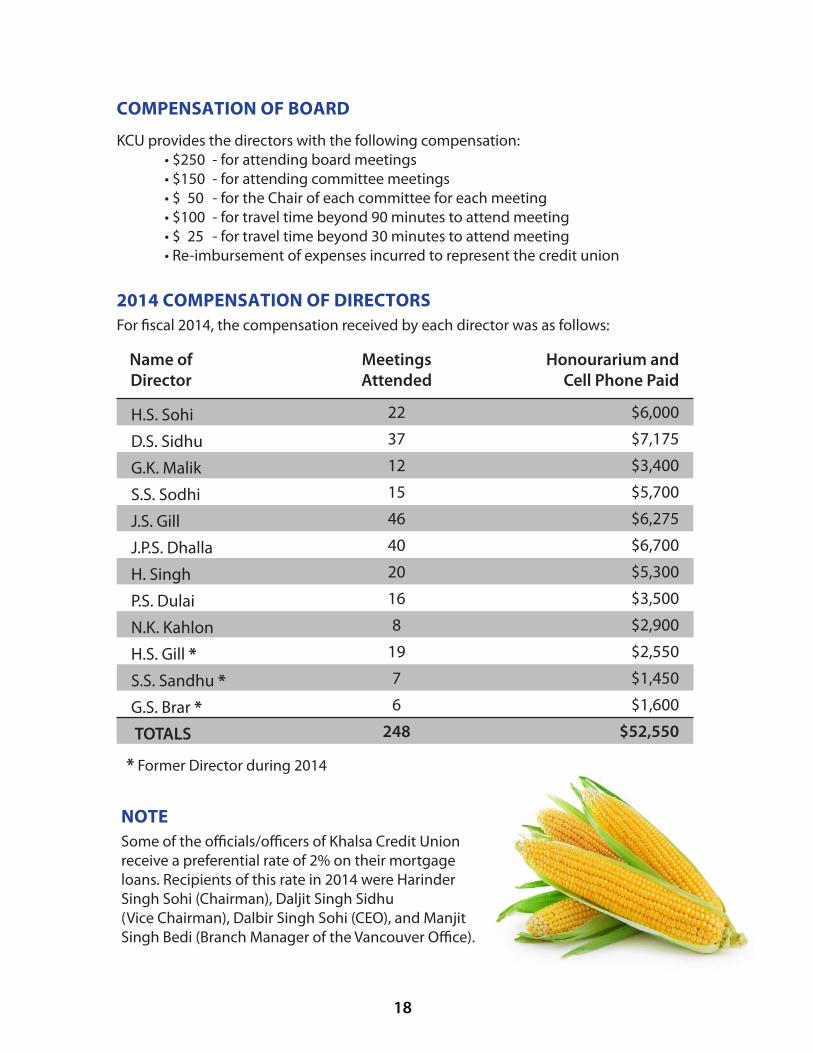

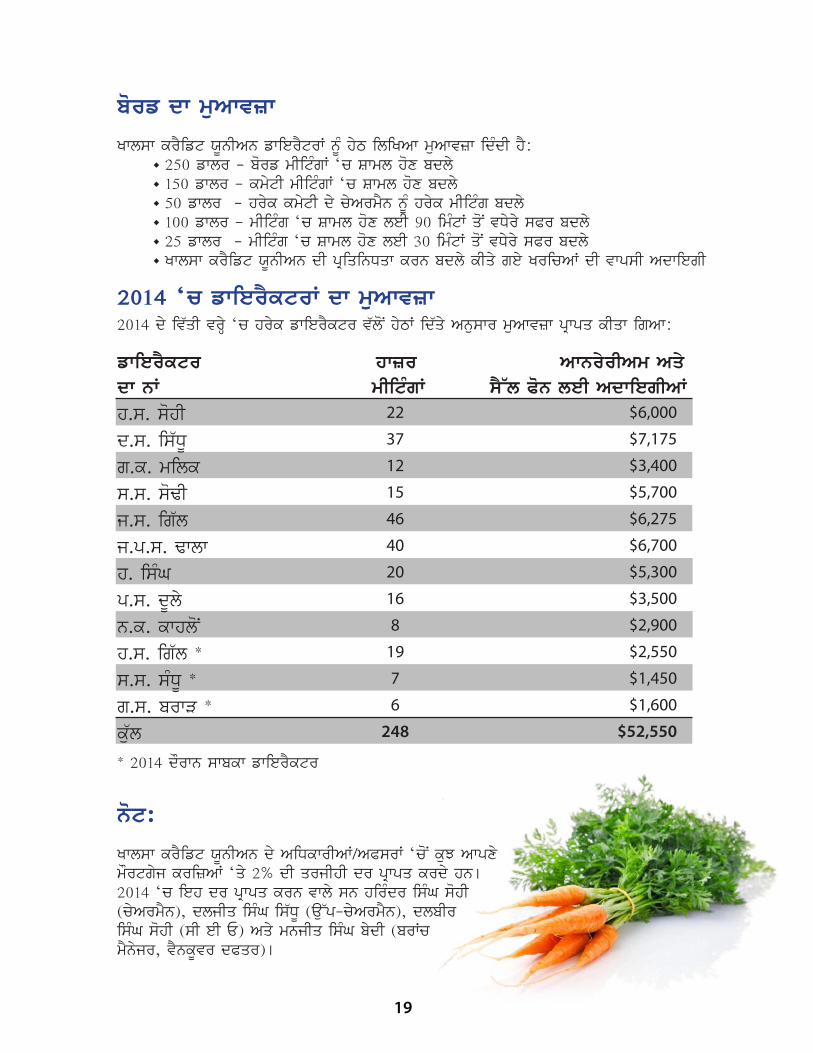

COMPENSATION OF BOARD

KCU provides the directors with the following compensation: • $250 - for attending board meetings • $150 - for attending committee meetings • $ 50 - for the Chair of each committee for each meeting • $100 - for travel time beyond 90 minutes to attend meeting • $ 25 - for travel time beyond 30 minutes to attend meeting • Re-imbursement of expenses incurred to represent the credit union

2014 COMPENSATION OF DIRECTORS For �scal 2014, the compensation received by each director was as follows:

22

37

12

15

46

40

20

16

8

19

7

6

248

$6,000

$7,175

$3,400

$5,700

$6,275

$6,700

$5,300

$3,500

$2,900

$2,550

$1,450

$1,600

$52,550

Honourarium andCell Phone Paid

Name ofDirector

MeetingsAttended

H.S. Sohi

D.S. Sidhu

G.K. Malik

S.S. Sodhi

J.S. Gill

J.P.S. Dhalla

H. Singh

P.S. Dulai

N.K. Kahlon

H.S. Gill * S.S. Sandhu * G.S. Brar * TOTALS

* Former Director during 2014

NOTESome of the o�cials/o�cers of Khalsa Credit Unionreceive a preferential rate of 2% on their mortgageloans. Recipients of this rate in 2014 were HarinderSingh Sohi (Chairman), Daljit Singh Sidhu(Vice Chairman), Dalbir Singh Sohi (CEO), and ManjitSingh Bedi (Branch Manager of the Vancouver O�ce).

PUNJABITRANSLATION

19

22

37

12

15

46

40

20

16

8

19

7

6

248

$6,000

$7,175

$3,400

$5,700

$6,275

$6,700

$5,300

$3,500

$2,900

$2,550

$1,450

$1,600

$52,550

18

COMPENSATION OF BOARD

KCU provides the directors with the following compensation: • $250 - for attending board meetings • $150 - for attending committee meetings • $ 50 - for the Chair of each committee for each meeting • $100 - for travel time beyond 90 minutes to attend meeting • $ 25 - for travel time beyond 30 minutes to attend meeting • Re-imbursement of expenses incurred to represent the credit union

2014 COMPENSATION OF DIRECTORS For �scal 2014, the compensation received by each director was as follows:

22

37

12

15

46

40

20

16

8

19

7

6

248

$6,000

$7,175

$3,400

$5,700

$6,275

$6,700

$5,300

$3,500

$2,900

$2,550

$1,450

$1,600

$52,550

Honourarium andCell Phone Paid

Name ofDirector

MeetingsAttended

H.S. Sohi

D.S. Sidhu

G.K. Malik

S.S. Sodhi

J.S. Gill

J.P.S. Dhalla

H. Singh

P.S. Dulai

N.K. Kahlon

H.S. Gill * S.S. Sandhu * G.S. Brar * TOTALS

* Former Director during 2014

NOTESome of the o�cials/o�cers of Khalsa Credit Unionreceive a preferential rate of 2% on their mortgageloans. Recipients of this rate in 2014 were HarinderSingh Sohi (Chairman), Daljit Singh Sidhu(Vice Chairman), Dalbir Singh Sohi (CEO), and ManjitSingh Bedi (Branch Manager of the Vancouver O�ce).

PUNJABITRANSLATION

19

22

37

12

15

46

40

20

16

8

19

7

6

248

$6,000

$7,175

$3,400

$5,700

$6,275

$6,700

$5,300

$3,500

$2,900

$2,550

$1,450

$1,600

$52,550

borf dw muAwvzw

Kwlsw krYift XUnIAn fwierYtrW nUM hyT iliKAw muAwvzw idMdI hY:• 250 fwlr - borf mIitMgW ‘c Swml hox bdly• 150 fwlr – kmytI mIitMgW ‘c Swml hox bdly• 50 fwlr - hryk kmytI dy cyArmYn nUM hryk mIitMg bdly• 100 fwlr – mIitMg ‘c Swml hox leI 90 imMtW qoN vDyry sPr bdly• 25 fwlr - mIitMg ‘c Swml hox leI 30 imMtW qoN vDyry sPr bdly• Kwlsw krYift XUnIAn dI pRiqinDqw krn bdly kIqy gey KricAW dI vwpsI AdwiegI

2014 ‘c fwierYktrW dw muAwvzw2014 dy iv`qI vrHy ‘c hryk fwierYktr v`loN hyTW id`qy Anuswr muAwvzw pRwpq kIqw igAw:

not:

Kwlsw krYift XUnIAn dy AiDkwrIAW/APsrW ‘coN kuJ Awpxy mOrtgyj krizAW ‘qy 2% dI qrjIhI dr pRwpq krdy hn[ 2014 ‘c ieh dr pRwpq krn vwly sn hirMdr isMG sohI (cyArmYn), dljIq isMG is`DU (au~p-cyArmYn), dlbIr isMG sohI (sI eI E) Aqy mnjIq isMG bydI (brWc mYnyjr, vYnkUvr dPqr)[

fwierYktr hwzr AwnryrIAm Aqy dw nW mIitMgW sY~l Pon leI AdwiegIAWh.s. sohId.s. is`DUg.k. milk s.s. soFIj.s. ig`l j.p.s. Fwlw h. isMGp.s. dUly n.k. kwhloN h.s. ig`l * s.s. sMDU * g.s. brwV * ku`l * 2014 dOrwn swbkw fwierYktr

MISSIONTo be the most successful Sikh Credit Union. To care about our community and

contribute to Sikh education, culture and religion. To be an environmentallyconscious and committed organization that is responsive to member-owners.

VISIONTo be the Sikh community’s �rst choice for �nancial services.

20

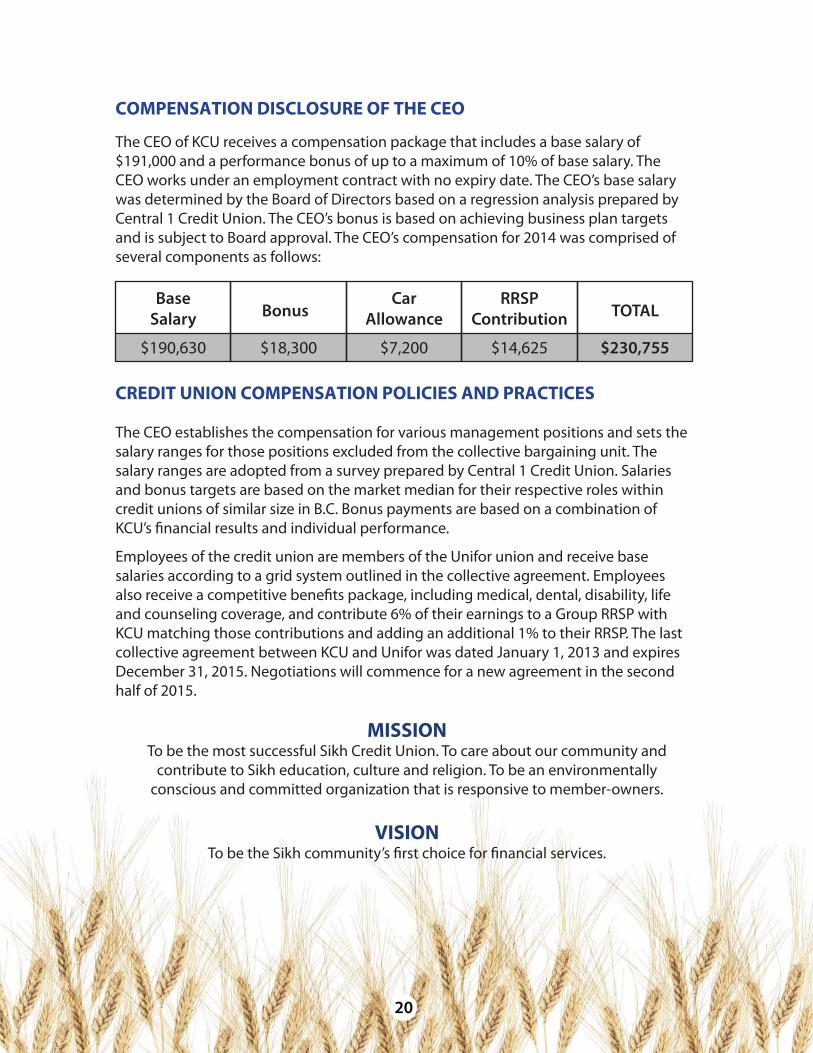

COMPENSATION DISCLOSURE OF THE CEO

The CEO of KCU receives a compensation package that includes a base salary of $191,000 and a performance bonus of up to a maximum of 10% of base salary. The CEO works under an employment contract with no expiry date. The CEO’s base salary was determined by the Board of Directors based on a regression analysis prepared by Central 1 Credit Union. The CEO’s bonus is based on achieving business plan targets and is subject to Board approval. The CEO’s compensation for 2014 was comprised of several components as follows:

CREDIT UNION COMPENSATION POLICIES AND PRACTICES

The CEO establishes the compensation for various management positions and sets the salary ranges for those positions excluded from the collective bargaining unit. The salary ranges are adopted from a survey prepared by Central 1 Credit Union. Salaries and bonus targets are based on the market median for their respective roles within credit unions of similar size in B.C. Bonus payments are based on a combination of KCU’s �nancial results and individual performance.

Employees of the credit union are members of the Unifor union and receive base salaries according to a grid system outlined in the collective agreement. Employees also receive a competitive bene�ts package, including medical, dental, disability, life and counseling coverage, and contribute 6% of their earnings to a Group RRSP with KCU matching those contributions and adding an additional 1% to their RRSP. The last collective agreement between KCU and Unifor was dated January 1, 2013 and expires December 31, 2015. Negotiations will commence for a new agreement in the second half of 2015.

BaseSalary Bonus

CarAllowance

RRSPContribution TOTAL

$190,630 $18,300 $7,200 $14,625 $230,755

PUNJABITRANSLATION

imSnsB qoN v`D kwmXwb is`K krYift XUnIAn bxnW[ AwpxI kimaUintI v`l iDAwn dyxw Aqy is`K ividAw, s`iBAwcwr Aqy Drm vwsqy Xogdwn pwauxw[ vwqwvrxk qOr ‘qy sucyq Aqy

iek pRiqbD sMsQw bxnW ijhVI Awpxy mYNbr-mwlkW pRiq auqrdweI hY[

dUrAMdySIiv`qI syvwvW leI is`K kimaUintI dI pihlI cox bxnW

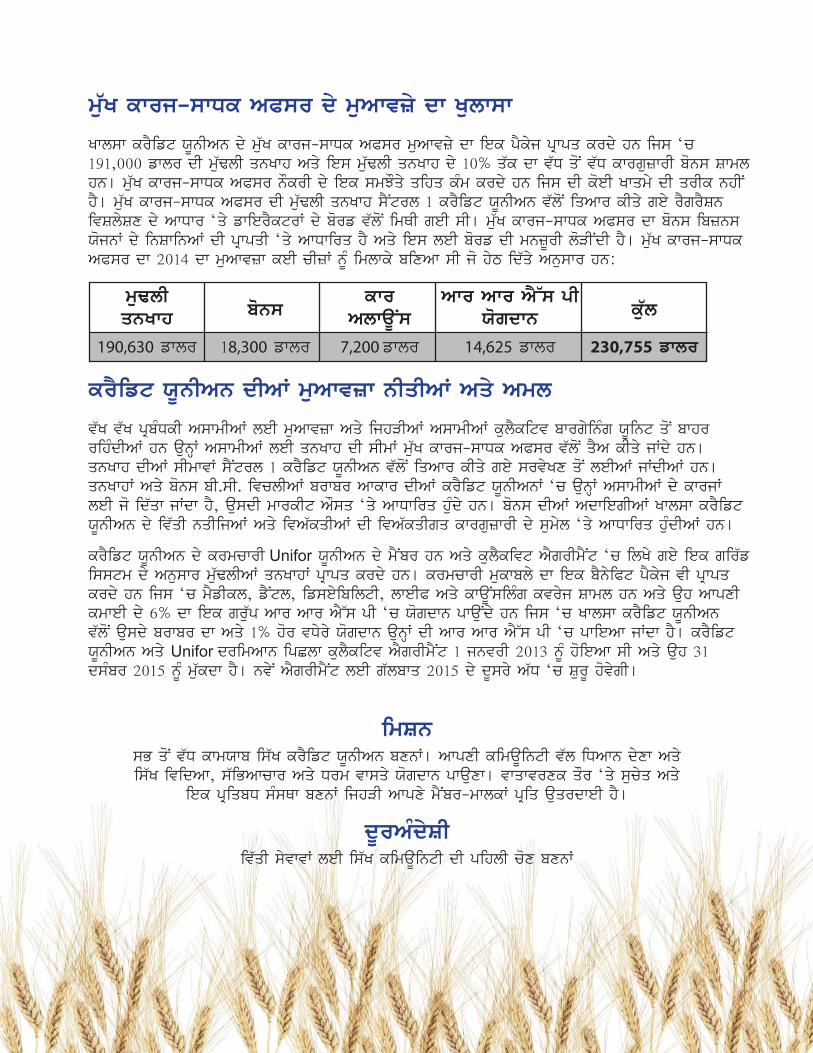

mu`K kwrj-swDk APsr dy muAwvzy dw Kulwsw

Kwlsw krYift XUnIAn dy m`uK kwrj-swDk APsr muAwvzy dw iek pYkyj pRwpq krdy hn ijs ‘c 191,000 fwlr dI mu`FlI qnKwh Aqy ies mu`FlI qnKwh dy 10% q`k dw v`D qoN v`D kwrguzwrI bons Swml hn[ m`uK kwrj-swDk APsr nOkrI dy iek smJOqy qihq kMm krdy hn ijs dI koeI Kwqmy dI qrIk nhIN hY[ mu`K kwrj-swDk APsr dI mu`FlI qnKwh sYNtrl 1 krYift XUnIAn v`loN iqAwr kIqy gey rYgrYSn ivSlySx dy AwDwr ‘qy fwierYktrW dy borf v`loN imQI geI sI[ m`uK kwrj-swDk APsr dw bons ibzns XojnW dy inSwinAW dI pRwpqI ‘qy AwDwirq hY Aqy ies leI borf dI mnzUrI loVINdI hY[ mu`K kwrj-swDk APsr dw 2014 dw muAwvzw keI cIzW nUM imlwky bixAw sI jo hyT id`qy Anuswr hn:

krYift XUnIAn dIAW muAwvzw nIqIAW Aqy Aml

v`K v`K pRbMDkI AswmIAW leI muAwvzw Aqy ijhVIAW AswmIAW kulYkitv bwrgyinMg XUint qoN bwhr rihMdIAW hn aunHW AswmIAW leI qnKwh dI sImW m`uK kwrj-swDk APsr v`loN qYA kIqy jWdy hn[ qnKwh dIAW sImwvW sYNtrl 1 krYift XUnIAn v`loN iqAwr kIqy gey srvyKx qoN leIAW jWdIAW hn[ qnKwhW Aqy bons bI.sI. ivclIAW brwbr Awkwr dIAW krYift XUnIAnW ‘c aunHW AswmIAW dy kwrjW leI jo id`qw jWdw hY, ausdI mwrkIt AOsq ‘qy AwDwirq huMdy hn[ bons dIAW AdwiegIAW Kwlsw krYift XUnIAn dy iv`qI nqIijAW Aqy ivA`kqIAW dI ivA`kqIgq kwrguzwrI dy sumyl ‘qy AwDwirq huMdIAW hn[