Embed Size (px)

Citation preview

Welcome

Little Rock Commercial Loan Servicing Center and

Fresno Commercial Loan Servicing Center

Overview of the Express Purchase Process when it arrives

Screening

Review

Legal

Approval

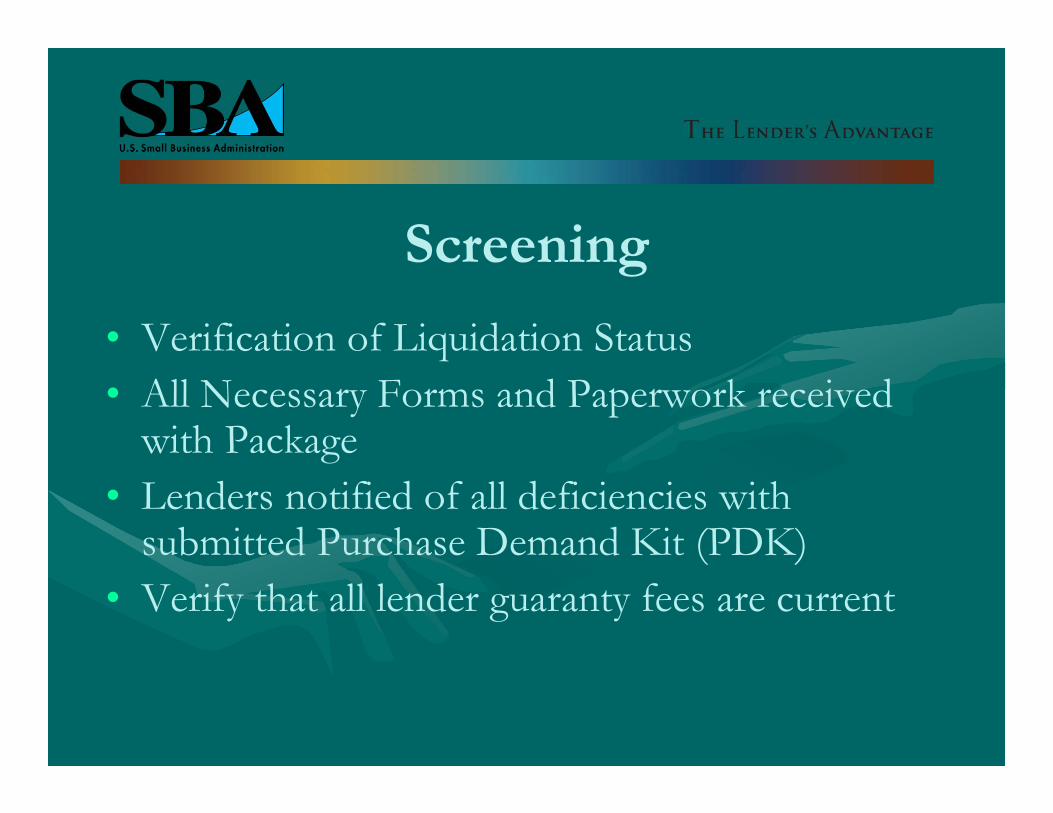

Screening

• Verification of Liquidation Status• All Necessary Forms and Paperwork received

with Package• Lenders notified of all deficiencies with

submitted Purchase Demand Kit (PDK)• Verify that all lender guaranty fees are current

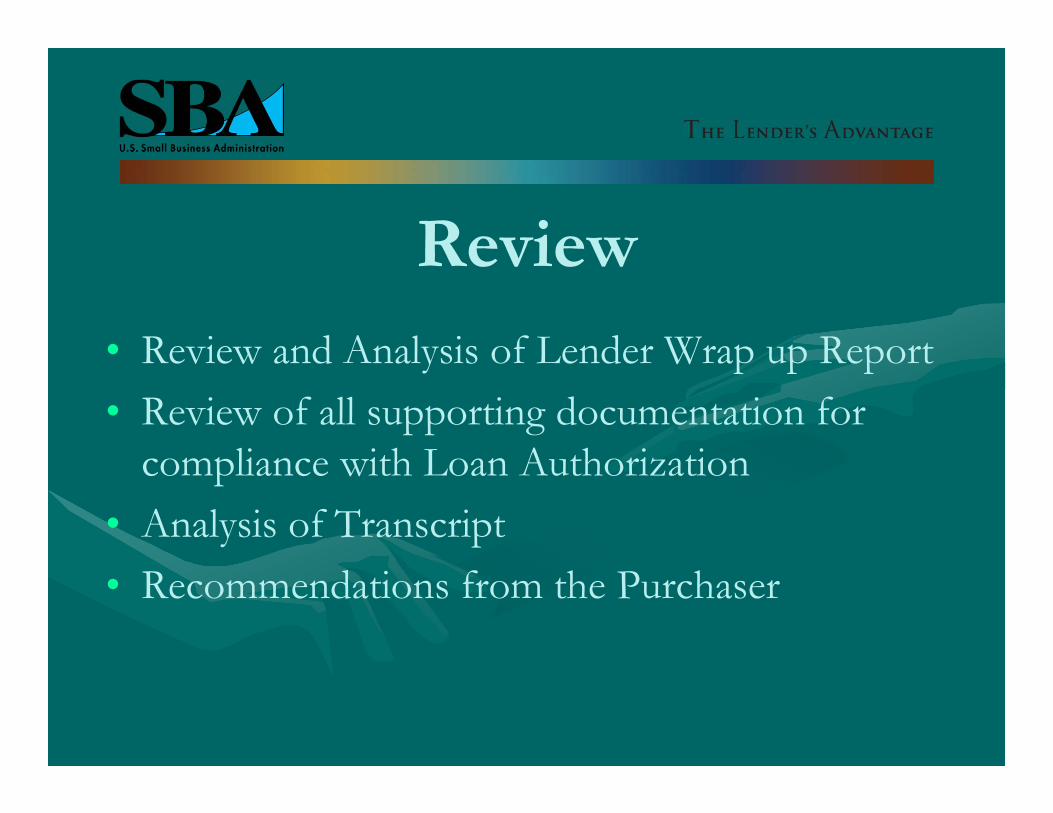

Review• Review and Analysis of Lender Wrap up Report • Review of all supporting documentation for

compliance with Loan Authorization• Analysis of Transcript• Recommendations from the Purchaser

Legal

• Review of Process Notes and Summary• Verification of Eligibility• Review of Loan Authorization; i.e., Use of

Proceeds and Collateral Conditions• Review of Bankruptcy Information• Recommendation of Purchase based on Legal

Review

Approval

• Review of Purchaser’s Recommendations• Approval of Purchase and/or change of• Review and Confirmation of Purchase Amounts• Verification that purchase complies with SBA

Rules and Regulations

The New Express Purchase Demand Kit

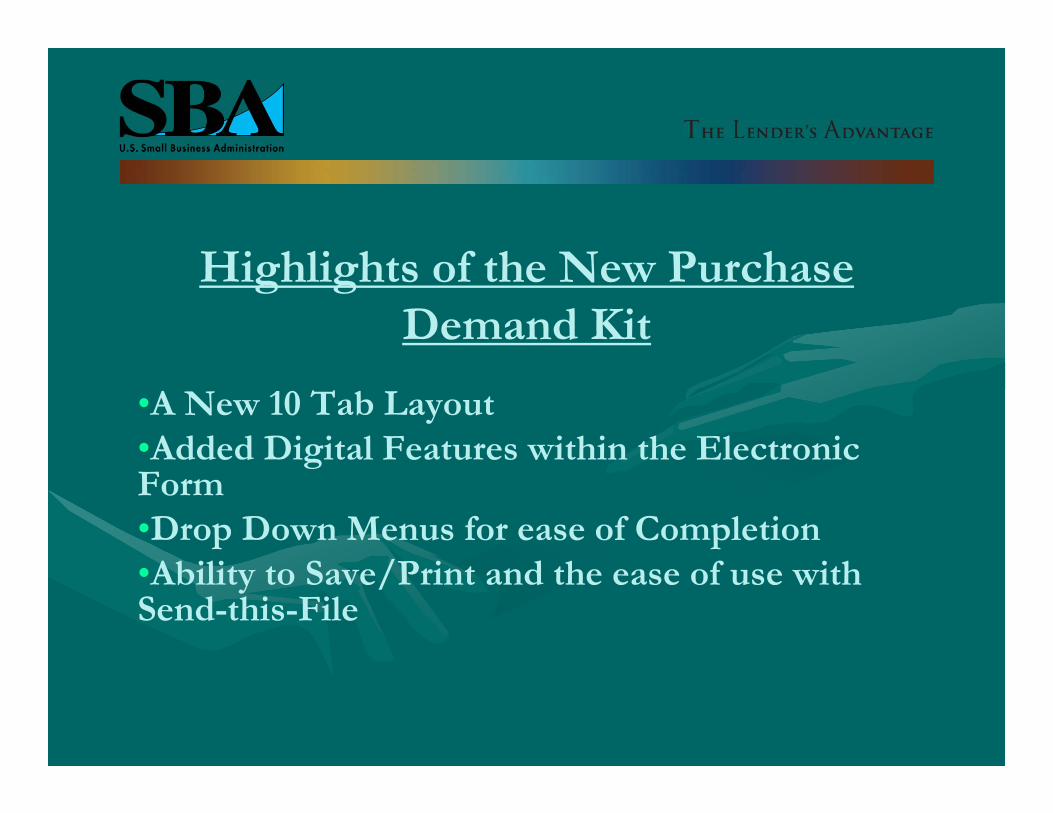

Highlights of the New Purchase Demand Kit

•A New 10 Tab Layout•Added Digital Features within the Electronic Form•Drop Down Menus for ease of Completion•Ability to Save/Print and the ease of use with Send-this-File

• The “Tab Pages” were designed to help you assemble your guaranty purchase request package.

• The Tab Pages are mandatory for all guaranty purchase packages. Help us help you to receive your guaranty funds timely by following ALL requirements outlined in organizing your purchase package

Where do I start?The process begins when you notify SBA to reclassify a loan into liquidation

status. Therefore, before any action can be done the loan will have to be transferred into liquidation status.

Little Rock CLSC2120 Riverfront Dr. Suite 100Little Rock, AR 72202(501)-324-5871(202) 292-3877 [email protected]

Fresno CLSC2719 N. Air Fresno Drive, Suite 107Fresno, CA 93727(559) 487-5136 559) 487-5009 [email protected]

To email secure files or packages to the Little Rock Service Center

Send this File - SBA's new File Transfer Service *Secure transmission method for files over 2.5 MB

Express Loan Guaranty Purchase

The SBA Express program has several unique features that make it different from other 7a loans.

One of the most important differences is the requirement that all liquidation or collection

activity must be completed before the demand for purchase is submitted unless the Expedited

Demand Procedure is utilized.

(SBA Procedural Notice 5000-803)

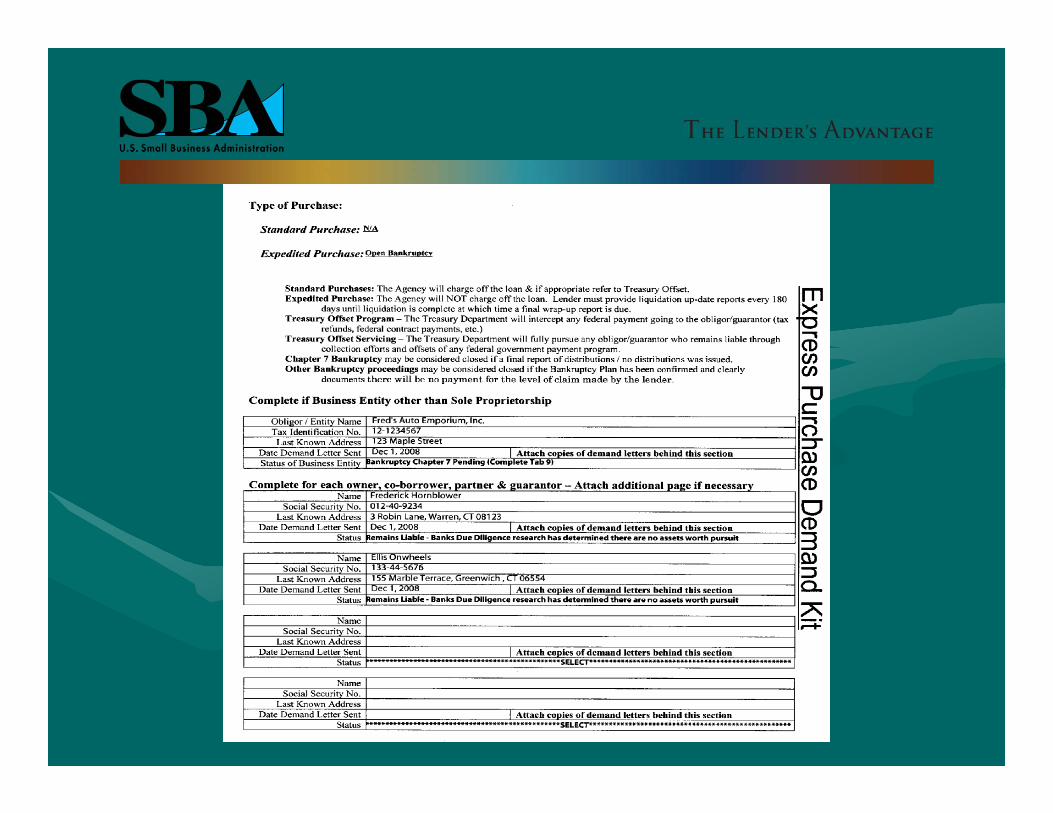

Expedited Purchases

• SBAExpress or Community Express loan which had an original balance of $50,000 or Less or Export Express loans, regardless of size (no substantiation of disposition of business assets required)

• Cases involving probate, bankruptcy, judicial foreclosure, litigation, or other unusual liquidation circumstances *

• Purchase request for loans over $50,000, Lender must explain why liquidation process is expected to be protracted but not required to submit a liquidation plan

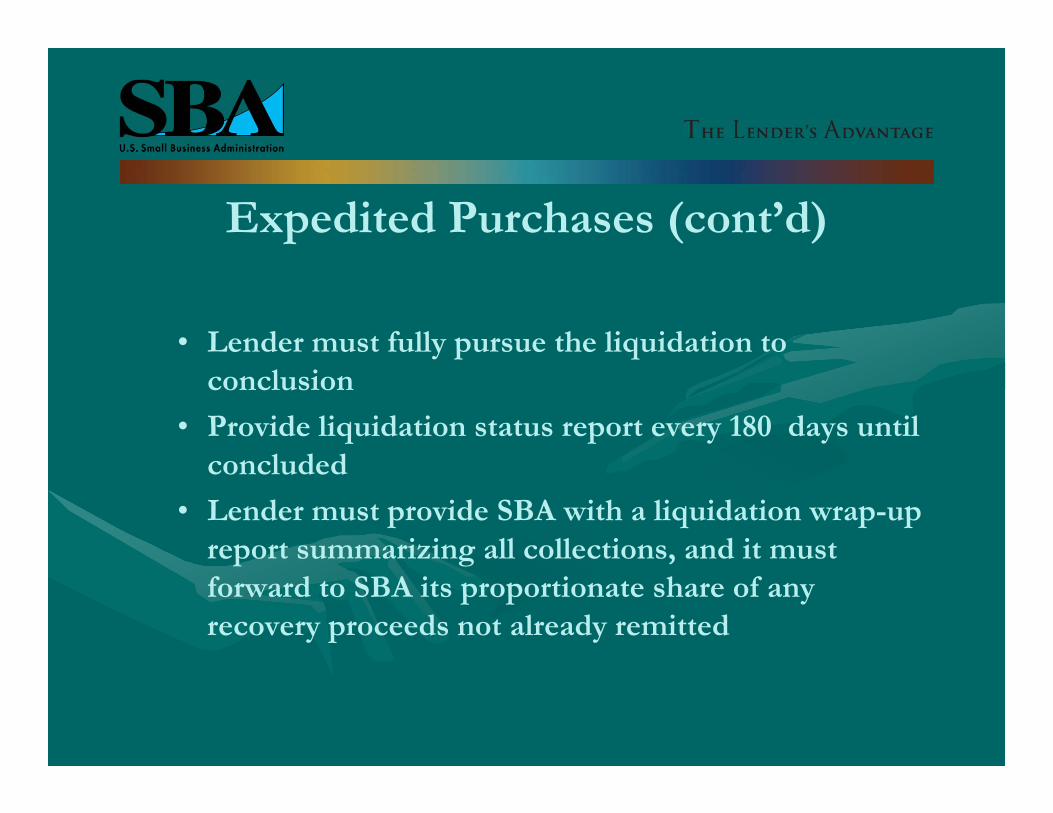

Expedited Purchases (cont’d)

• Lender must fully pursue the liquidation to conclusion

• Provide liquidation status report every 180 days until concluded

• Lender must provide SBA with a liquidation wrap-up report summarizing all collections, and it must forward to SBA its proportionate share of any recovery proceeds not already remitted

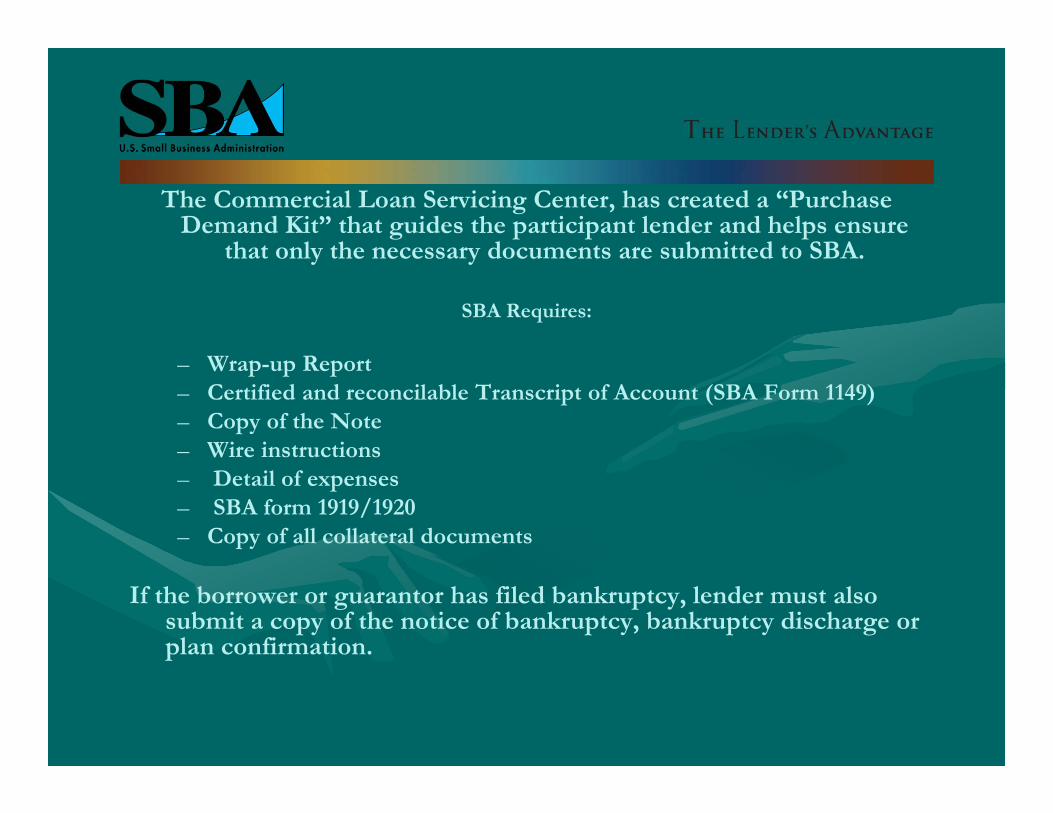

The Commercial Loan Servicing Center, has created a “Purchase Demand Kit” that guides the participant lender and helps ensure

that only the necessary documents are submitted to SBA.

SBA Requires:

– Wrap-up Report– Certified and reconcilable Transcript of Account (SBA Form 1149)– Copy of the Note– Wire instructions– Detail of expenses– SBA form 1919/1920– Copy of all collateral documents

If the borrower or guarantor has filed bankruptcy, lender must also submit a copy of the notice of bankruptcy, bankruptcy discharge or plan confirmation.

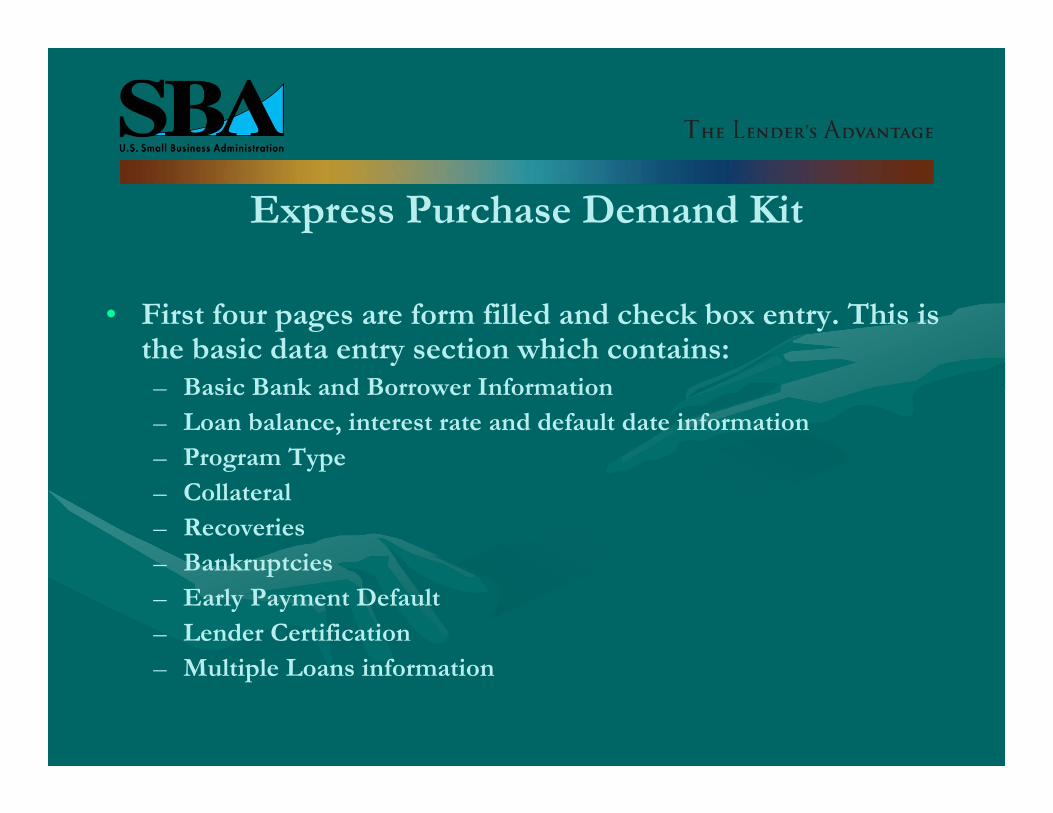

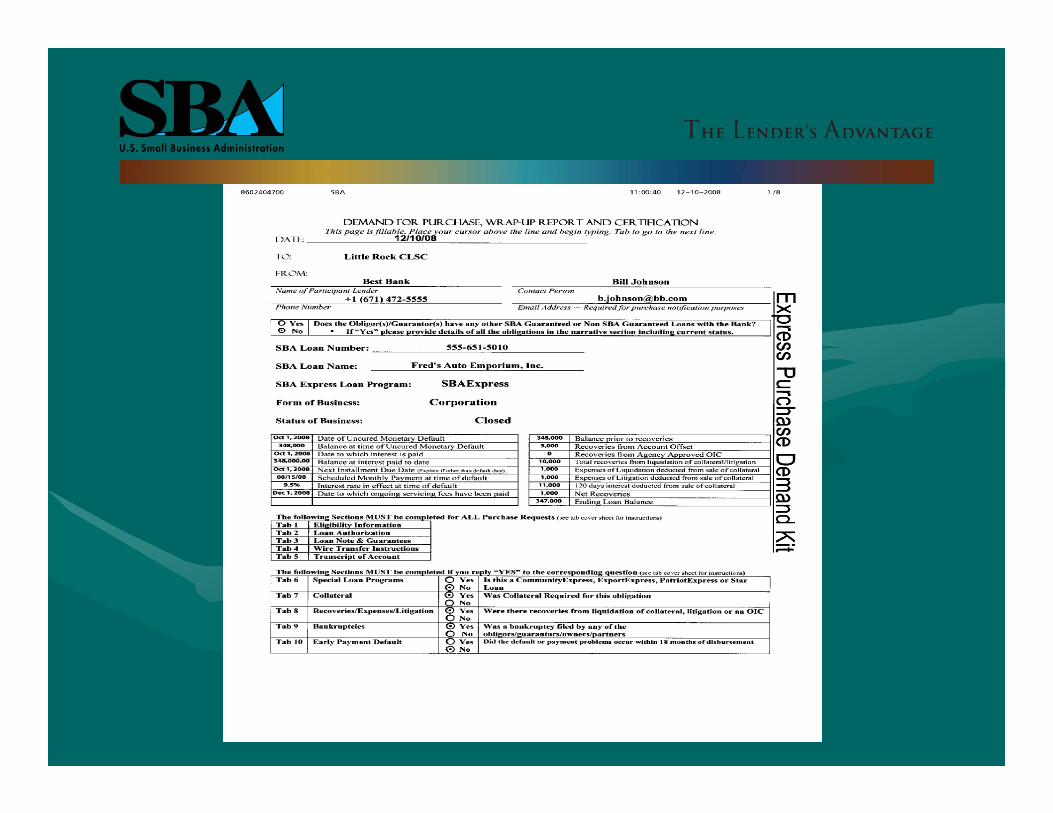

Express Purchase Demand Kit

• First four pages are form filled and check box entry. This is the basic data entry section which contains:– Basic Bank and Borrower Information– Loan balance, interest rate and default date information– Program Type – Collateral – Recoveries– Bankruptcies– Early Payment Default – Lender Certification– Multiple Loans information

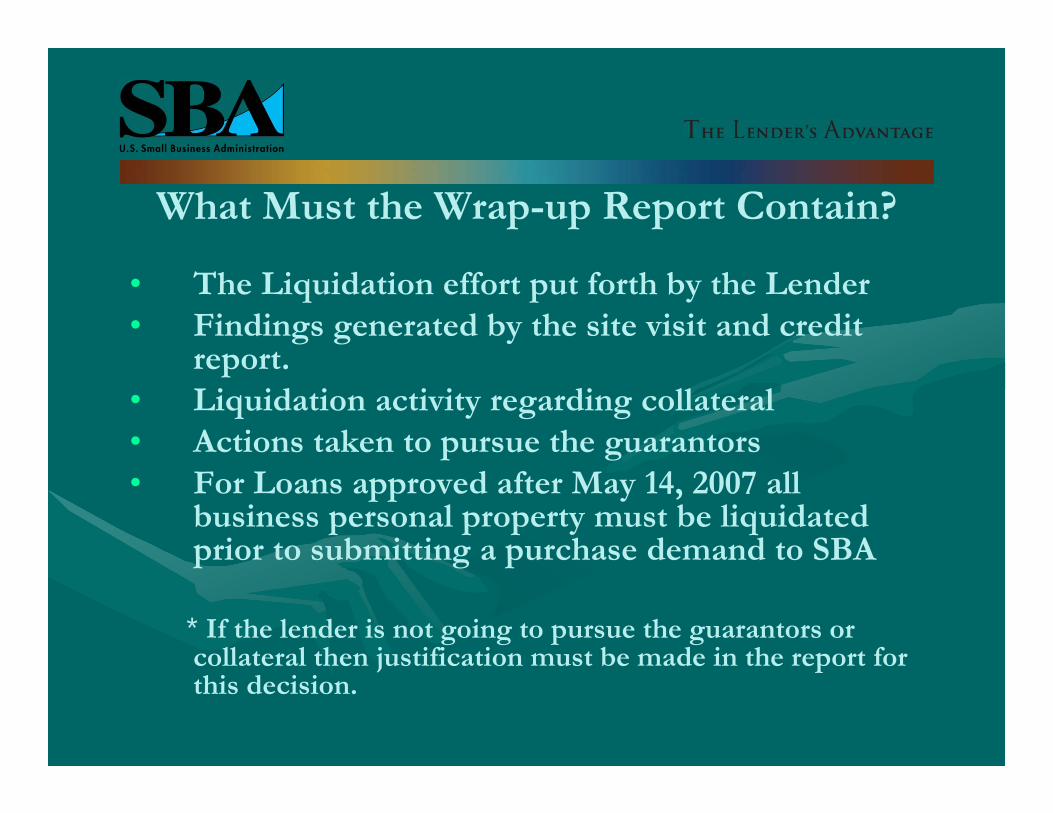

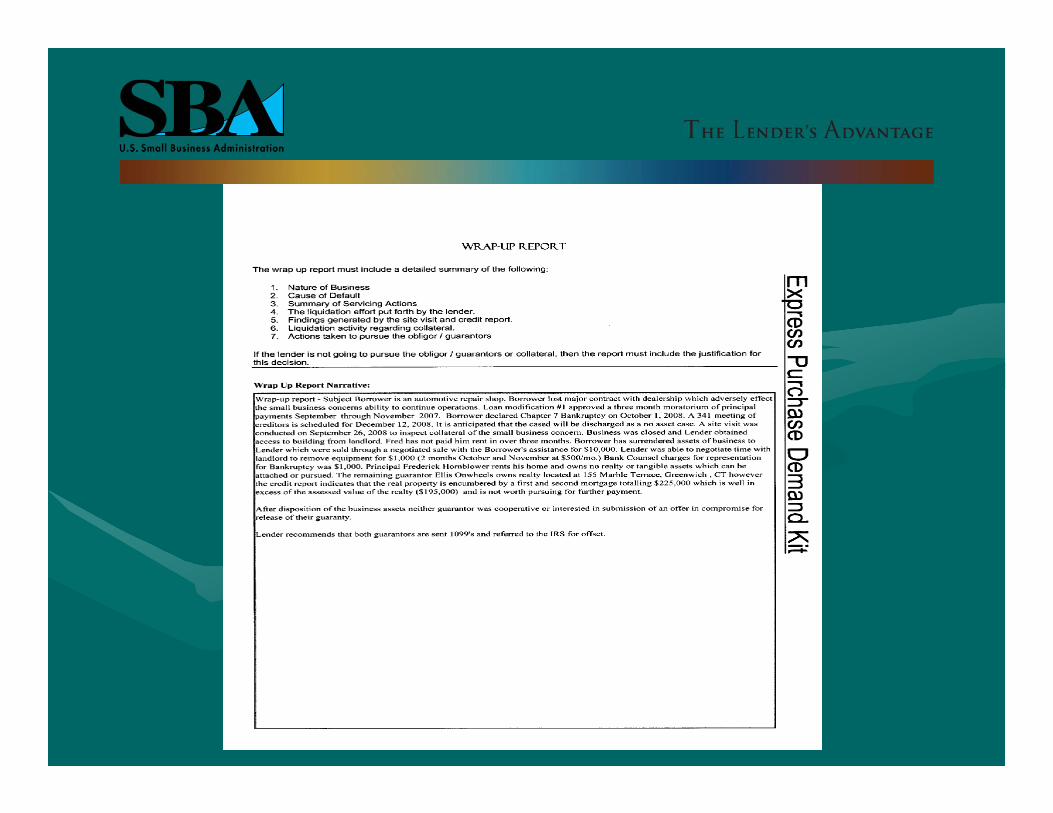

What Must the Wrap-up Report Contain?

• The Liquidation effort put forth by the Lender• Findings generated by the site visit and credit

report.• Liquidation activity regarding collateral• Actions taken to pursue the guarantors• For Loans approved after May 14, 2007 all

business personal property must be liquidated prior to submitting a purchase demand to SBA

* If the lender is not going to pursue the guarantors or collateral then justification must be made in the report for this decision.

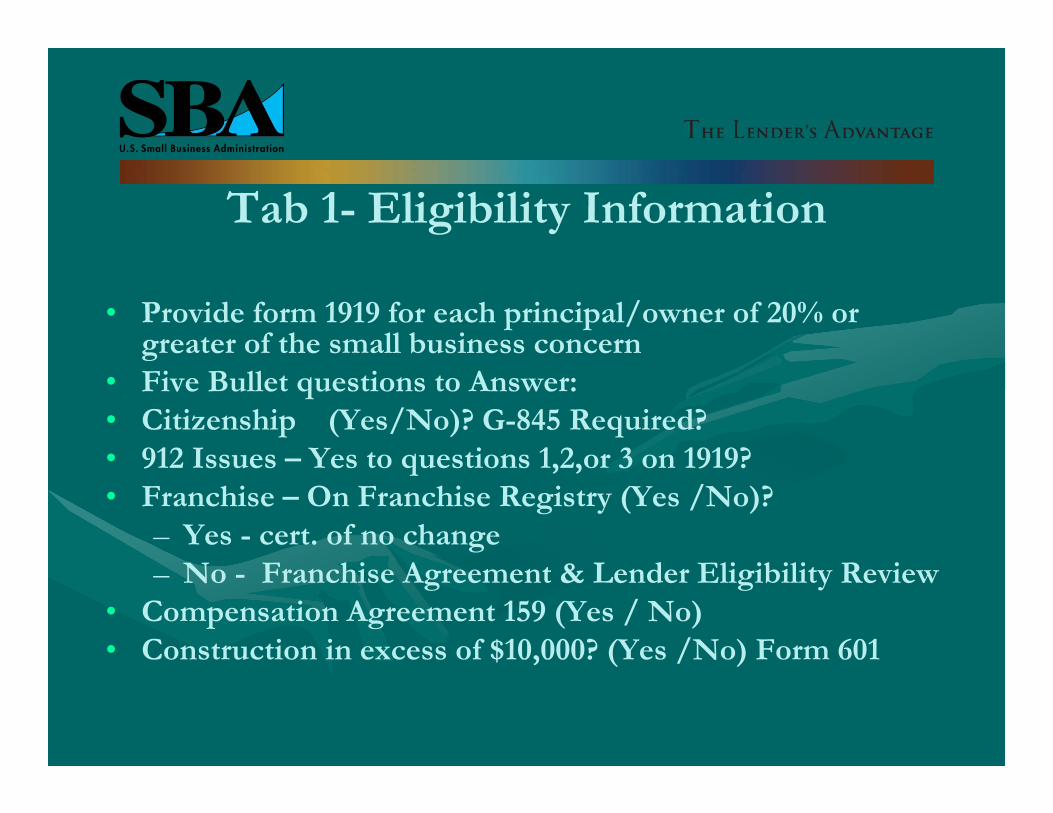

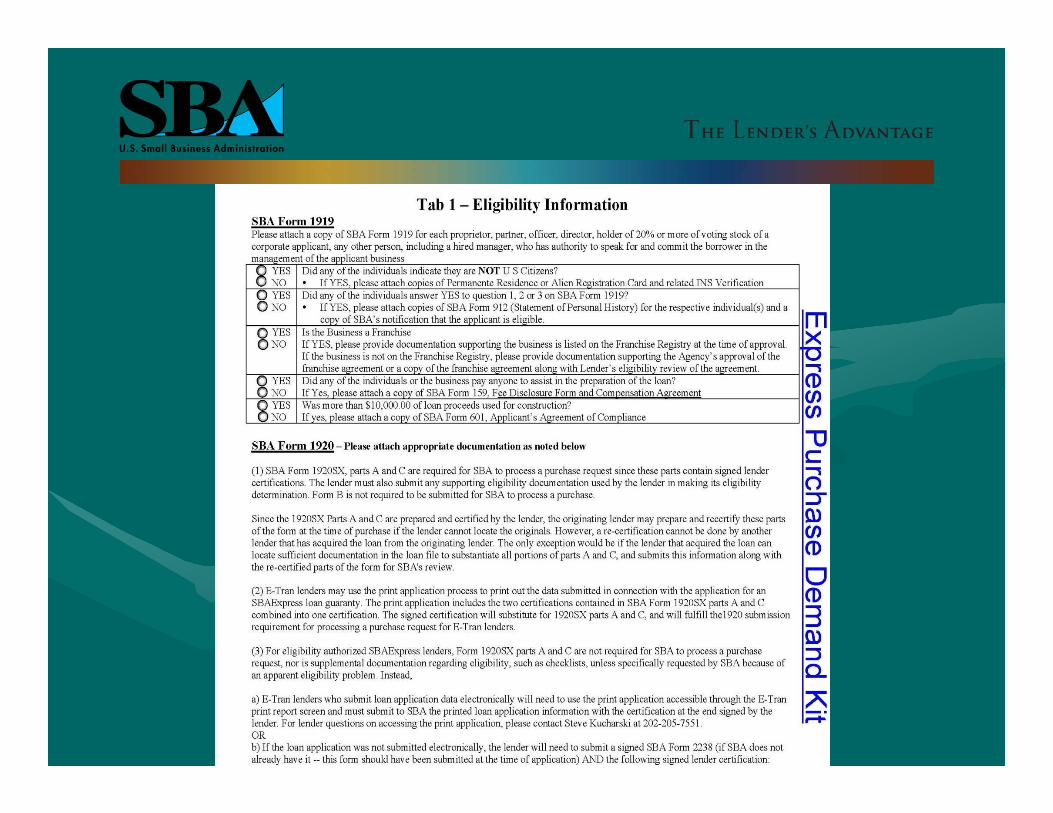

Tab 1- Eligibility Information

• Provide form 1919 for each principal/owner of 20% or greater of the small business concern

• Five Bullet questions to Answer:• Citizenship (Yes/No)? G-845 Required?• 912 Issues – Yes to questions 1,2,or 3 on 1919?• Franchise – On Franchise Registry (Yes /No)?

– Yes - cert. of no change– No - Franchise Agreement & Lender Eligibility Review

• Compensation Agreement 159 (Yes / No)• Construction in excess of $10,000? (Yes /No) Form 601

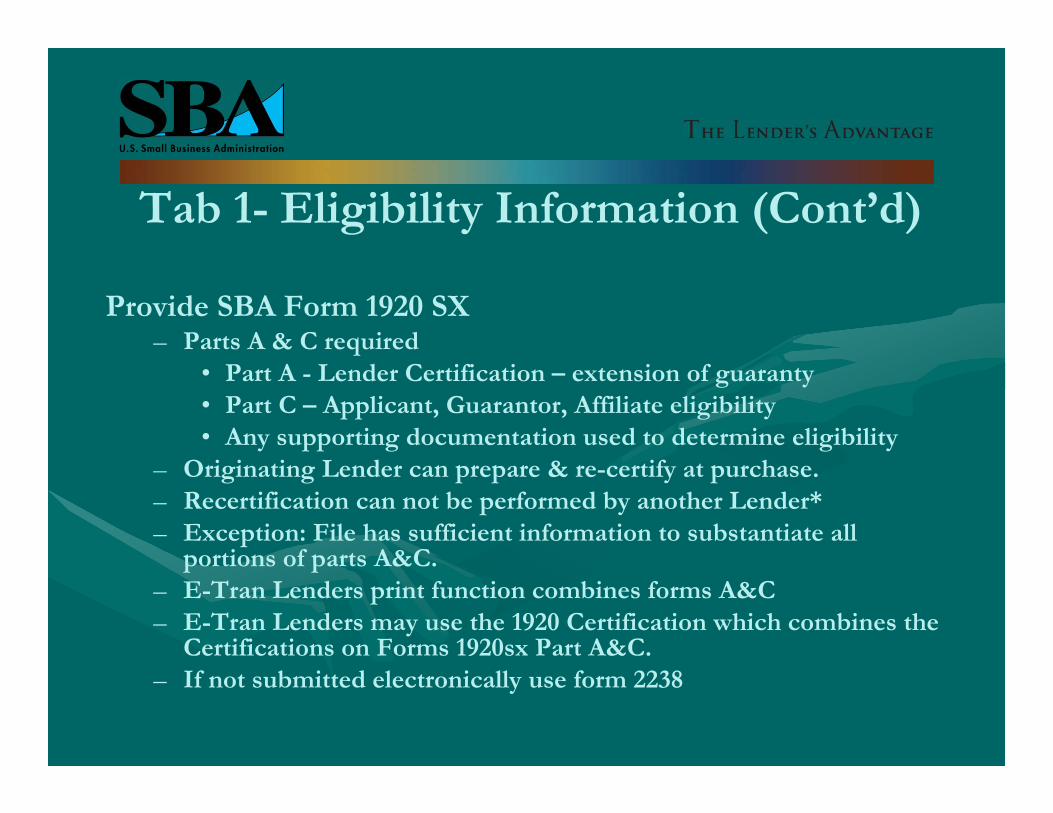

Tab 1- Eligibility Information (Cont’d)

Provide SBA Form 1920 SX– Parts A & C required

• Part A - Lender Certification – extension of guaranty• Part C – Applicant, Guarantor, Affiliate eligibility• Any supporting documentation used to determine eligibility

– Originating Lender can prepare & re-certify at purchase.– Recertification can not be performed by another Lender*– Exception: File has sufficient information to substantiate all

portions of parts A&C.– E-Tran Lenders print function combines forms A&C– E-Tran Lenders may use the 1920 Certification which combines the

Certifications on Forms 1920sx Part A&C.– If not submitted electronically use form 2238

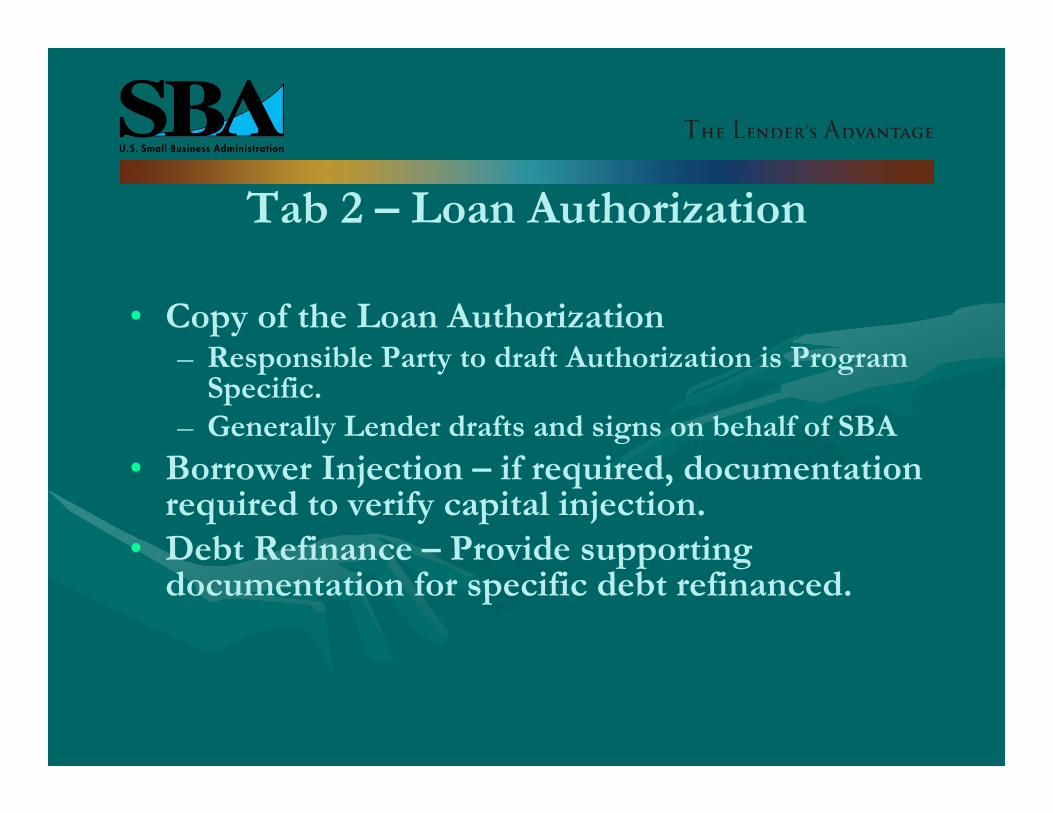

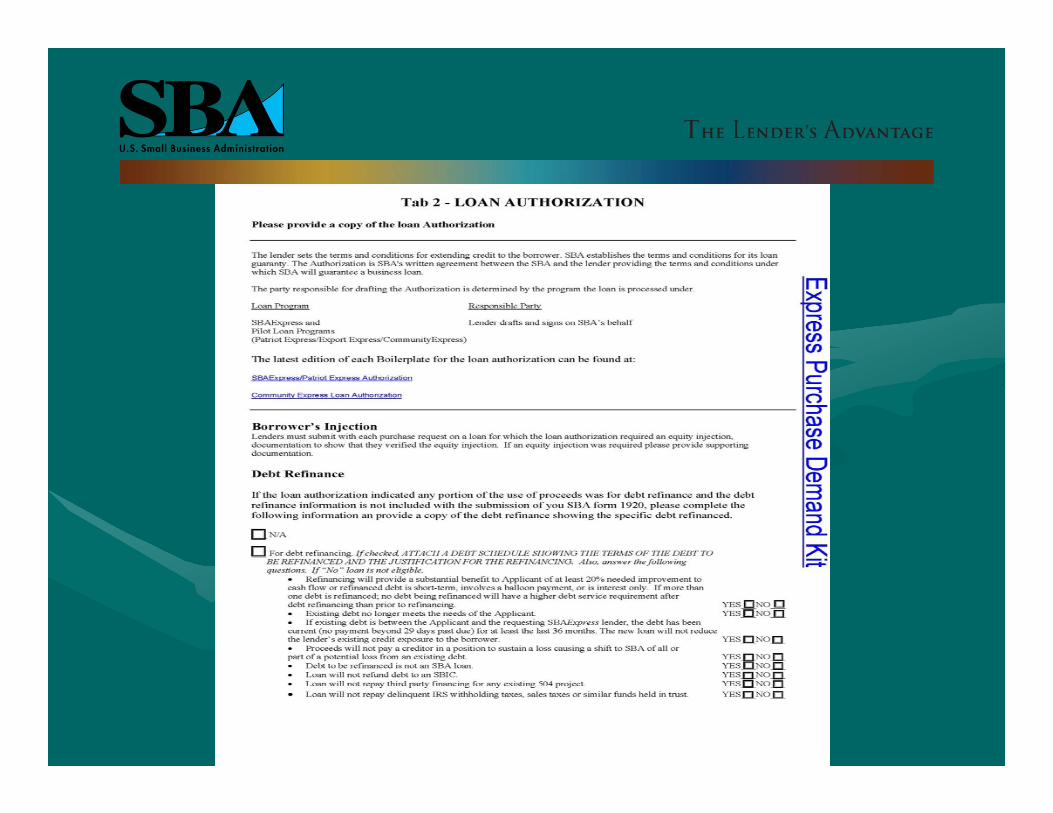

Tab 2 – Loan Authorization

• Copy of the Loan Authorization– Responsible Party to draft Authorization is Program

Specific.– Generally Lender drafts and signs on behalf of SBA

• Borrower Injection – if required, documentation required to verify capital injection.

• Debt Refinance – Provide supporting documentation for specific debt refinanced.

Tab 3 Loan Note & Guaranties• SBA Express & Pilot Programs – Lender must use same

closing procedures as for non-SBA loans • Note must be in an assignable form• Must also submit copies of any Note Modifications,

Amendments, Deferments, and Workout Agreements (include all revised repayment terms including dates, interest rate adjustments, and payment revisions)

• For Secondary Market loans, lender must provide evidence of investor's approval of modifications, as applicable

• Copies of Corporate and Personal Guaranties (SBA Form 148)

• Guarantor consent to material changes to loan terms

Tab 4 – Wire Transfer Instructions• Complete form with all applicable data.• Bank to receive wire transfer for amounts over $5,000

– Banker, Name, address, telephone– Wire Transfer #– Direct Deposit Account #

• Bank to receive ACH for amounts under $5,000– Banker, Name, address, telephone– ACH Routing #– ACH Checking Account # or ACH Savings Account #

• Colson Information if Sold on Secondary Market– Date of default– Interest “Paid-to” date– Principal Balance– Interest rate at time of default

• Choices C&D on the form if payment recipient different

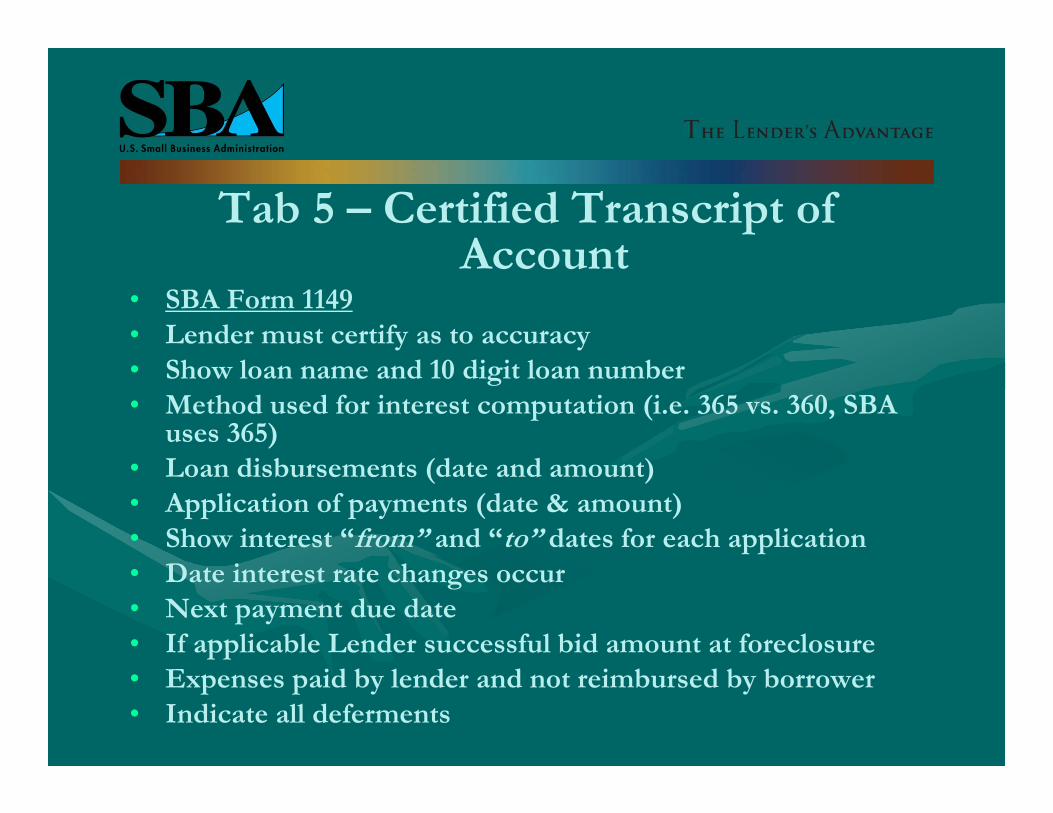

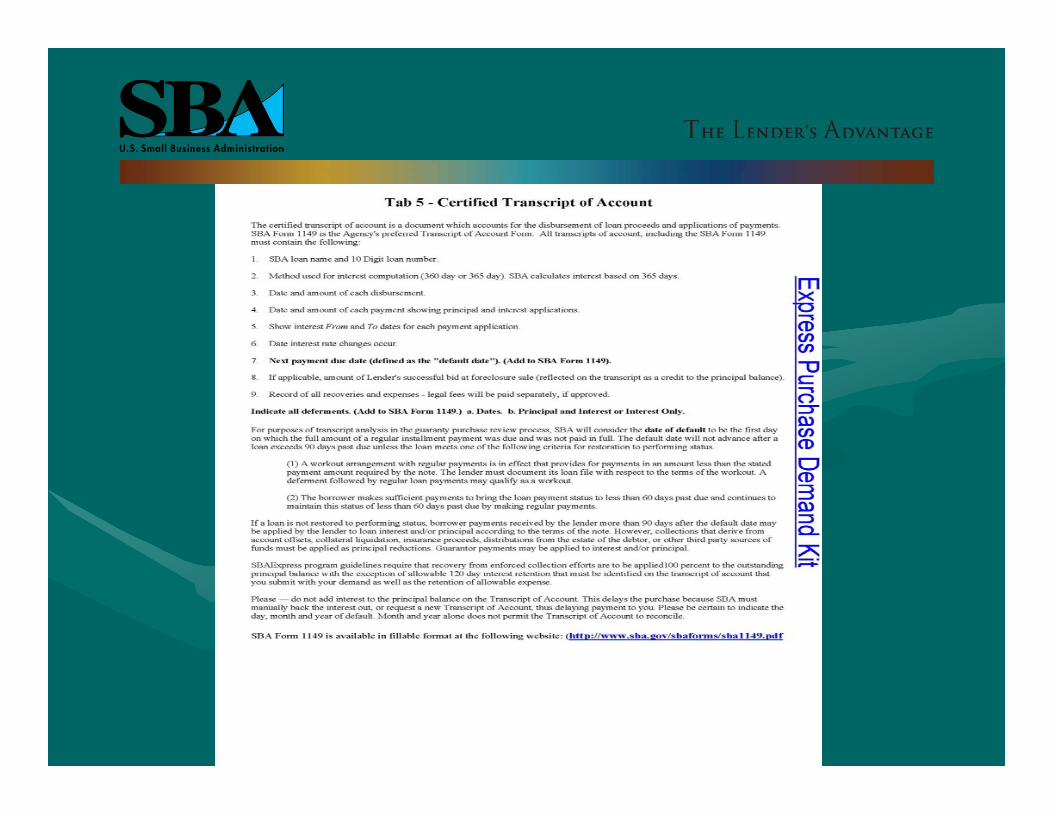

Tab 5 – Certified Transcript of Account

• SBA Form 1149• Lender must certify as to accuracy• Show loan name and 10 digit loan number• Method used for interest computation (i.e. 365 vs. 360, SBA

uses 365) • Loan disbursements (date and amount)• Application of payments (date & amount) • Show interest “from” and “to” dates for each application• Date interest rate changes occur• Next payment due date• If applicable Lender successful bid amount at foreclosure• Expenses paid by lender and not reimbursed by borrower• Indicate all deferments

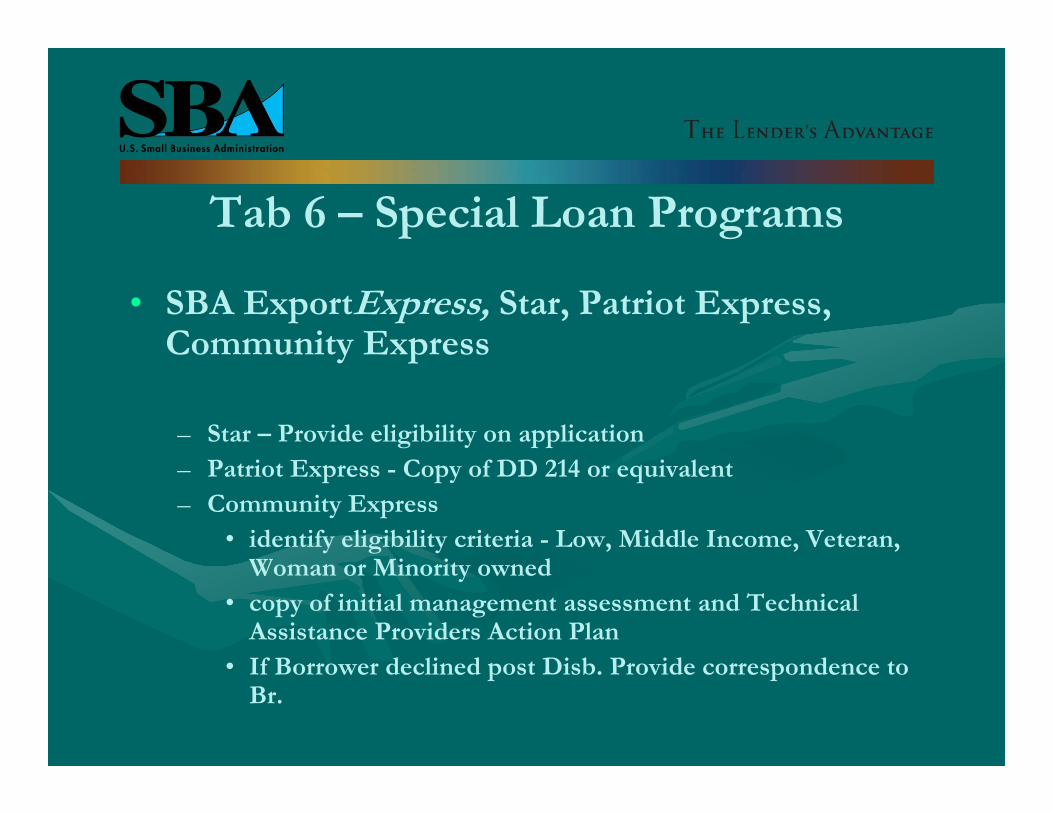

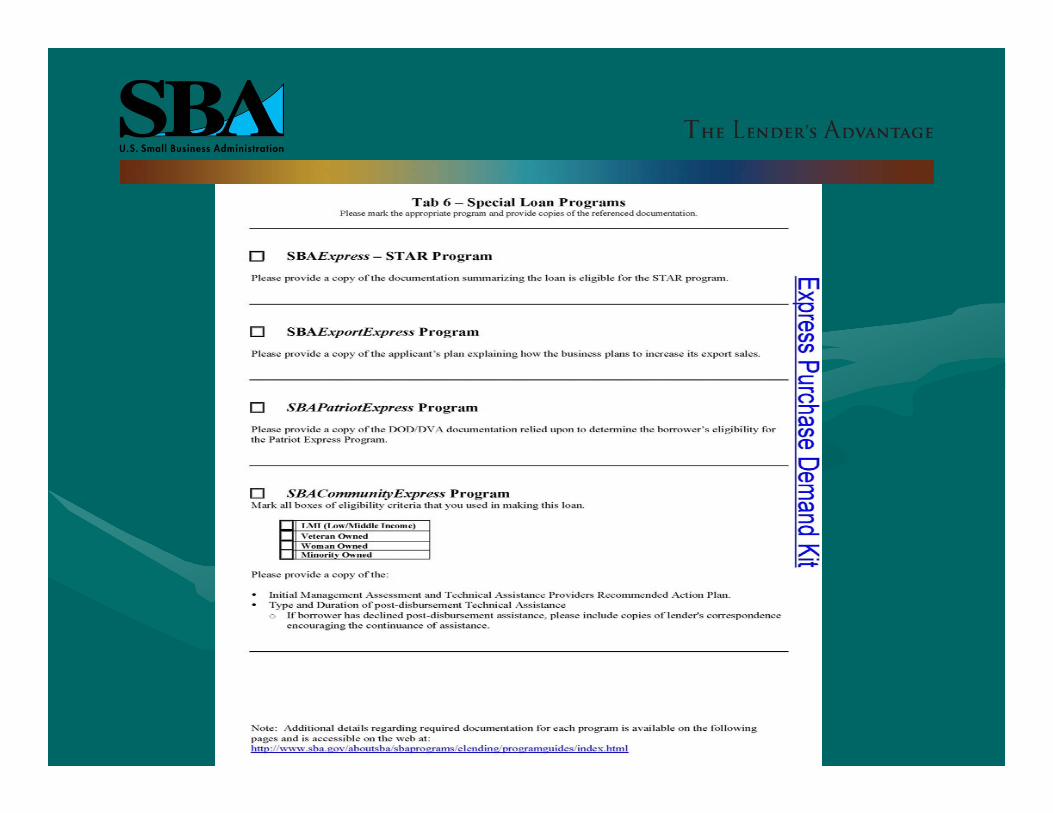

Tab 6 – Special Loan Programs

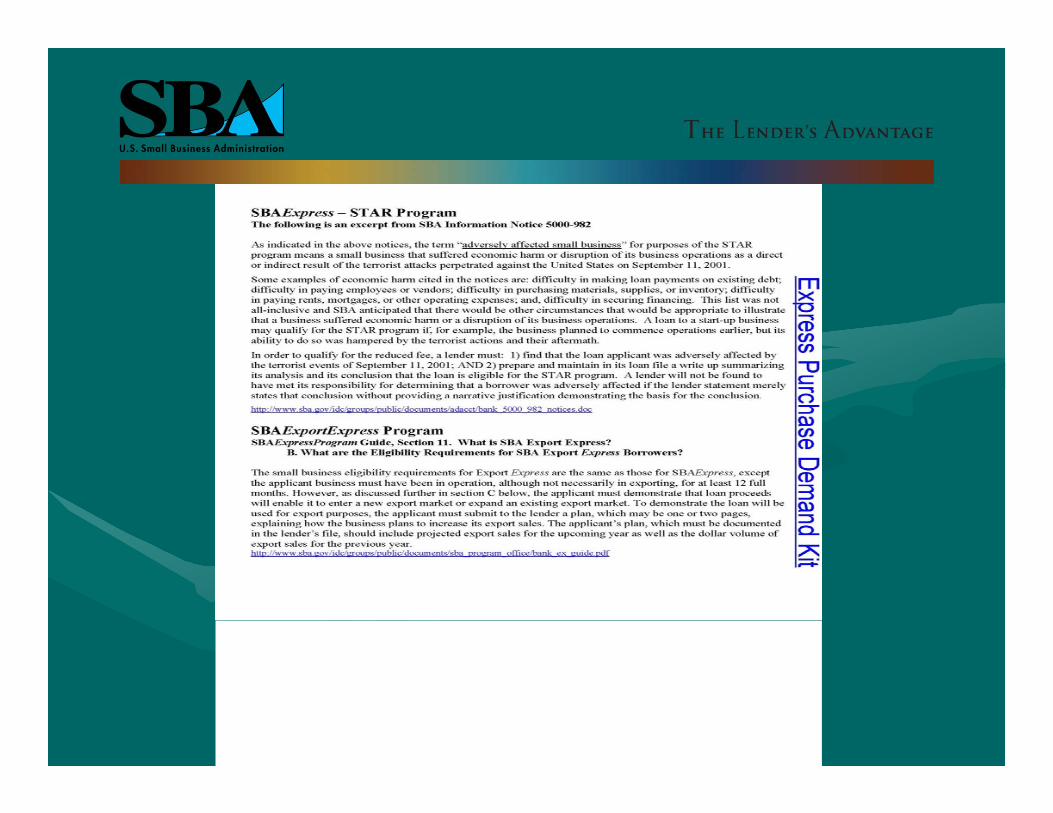

• SBA ExportExpress, Star, Patriot Express, Community Express

– Star – Provide eligibility on application– Patriot Express - Copy of DD 214 or equivalent – Community Express

• identify eligibility criteria - Low, Middle Income, Veteran, Woman or Minority owned

• copy of initial management assessment and Technical Assistance Providers Action Plan

• If Borrower declined post Disb. Provide correspondence to Br.

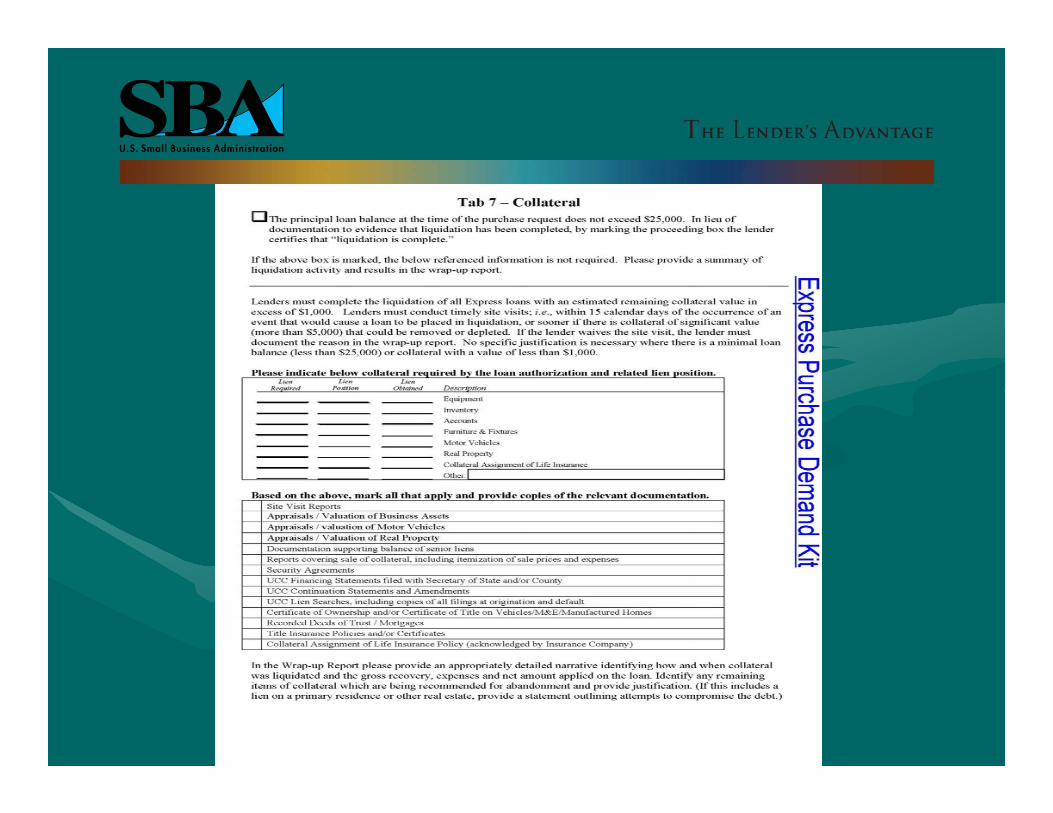

Tab 7 – Collateral

• Check Box if Principal Balance < $25.0K – need only summary of liquidation efforts in wrap up report

• Site Visit required within 15 days of triggering event• Liquidation of all assets in excess of $1,000• Identify collateral and lien priority• Provide documentation to support collateral

requirements• Detailed liquidation information identify- How, When

& How much gross recovery, expenses & net recovery applied to loan in wrap-up report.

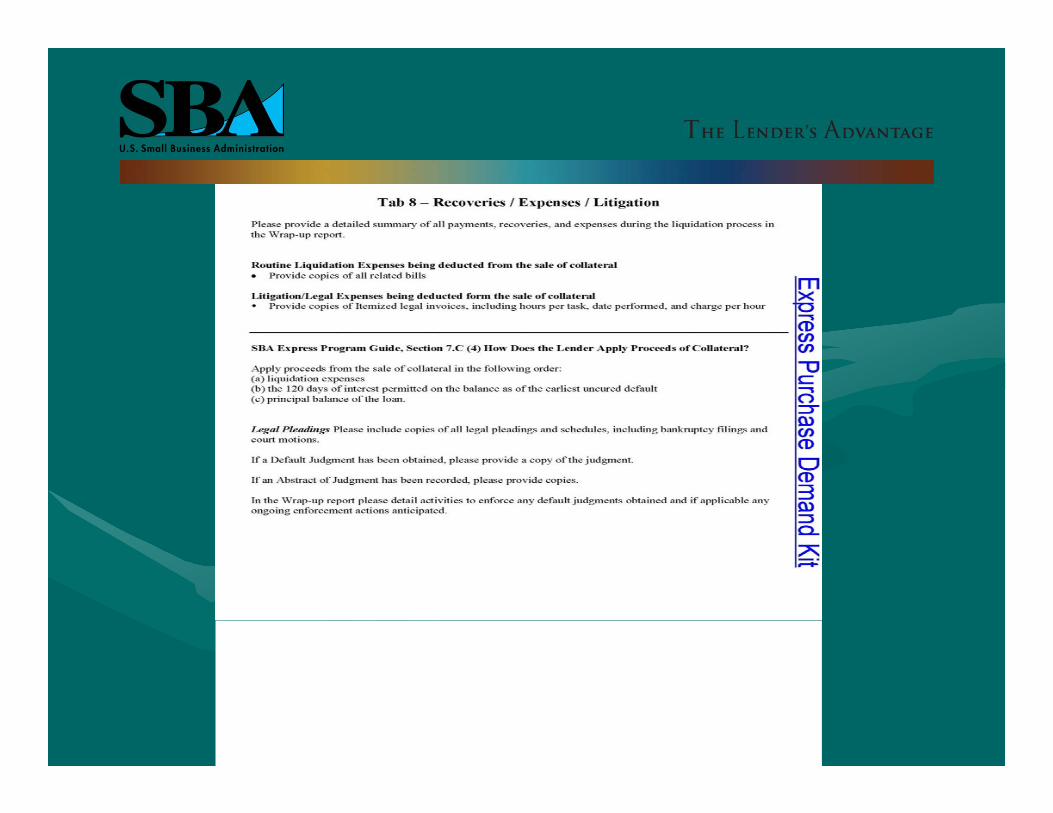

Tab 8 – Recoveries / Expenses / Litigation

• Provide copies invoices of all liquidation expenses deducted from sale of assets

• Provide copies of all litigation/ legal expenses being deducted from the sale of collateral (i.e. itemized legal invoice, hrs./task, date performed, hourly rate)

• Application of proceeds from sale of collateral in order of priority:

– Liquidation Expenses– 120 days interest on balance as of earliest uncured default date– Principal balance of the loan

• Provide copies of all legal pleadings, schedules and files

• Copy of default or abstract of judgment if applicable

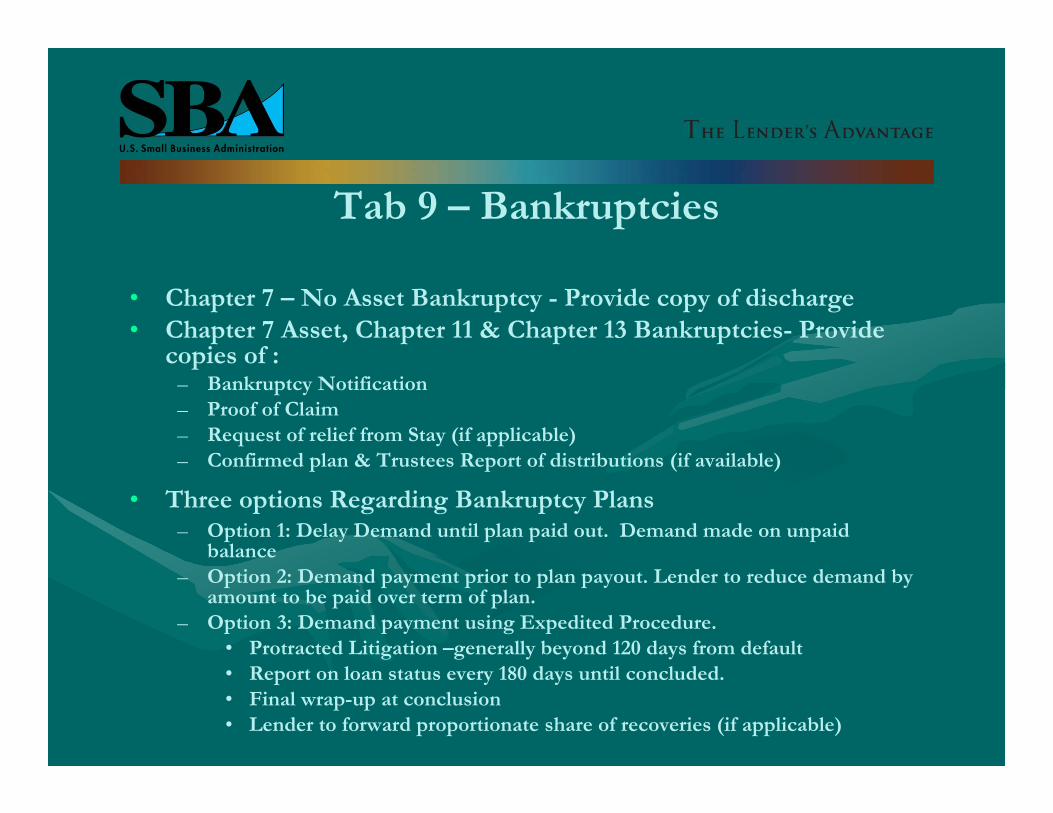

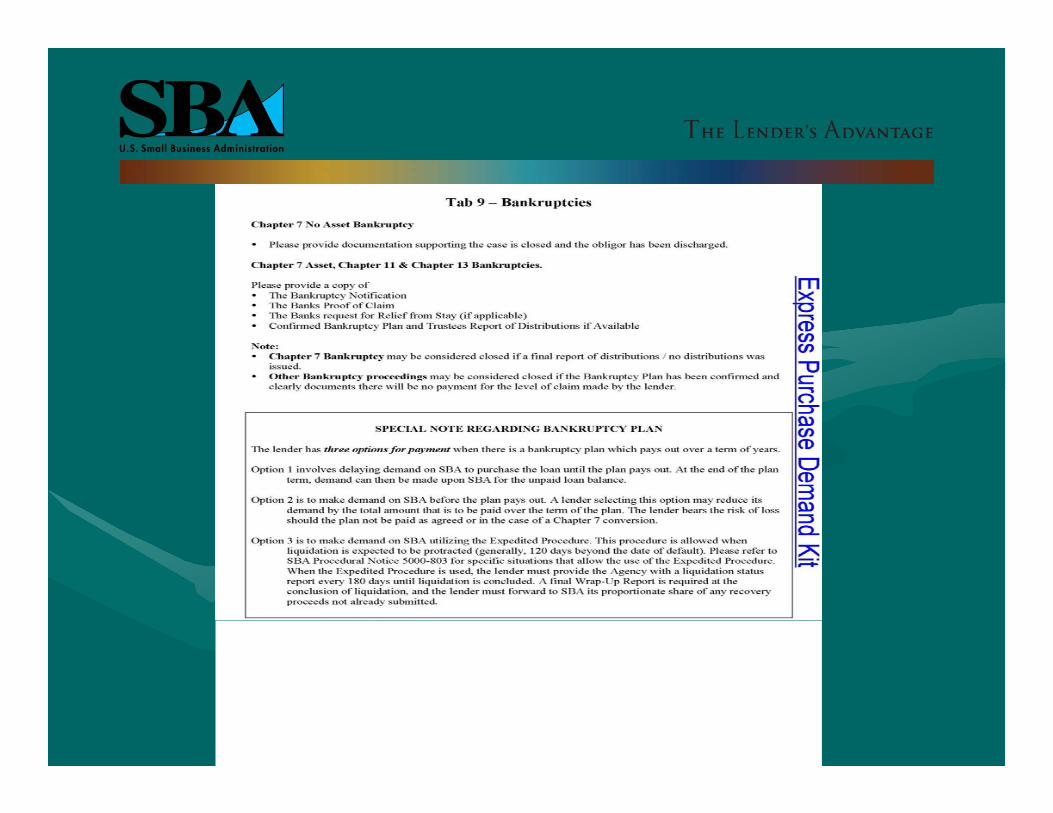

Tab 9 – Bankruptcies

• Chapter 7 – No Asset Bankruptcy - Provide copy of discharge• Chapter 7 Asset, Chapter 11 & Chapter 13 Bankruptcies- Provide

copies of :– Bankruptcy Notification– Proof of Claim– Request of relief from Stay (if applicable)– Confirmed plan & Trustees Report of distributions (if available)

• Three options Regarding Bankruptcy Plans– Option 1: Delay Demand until plan paid out. Demand made on unpaid

balance– Option 2: Demand payment prior to plan payout. Lender to reduce demand by

amount to be paid over term of plan.– Option 3: Demand payment using Expedited Procedure.

• Protracted Litigation –generally beyond 120 days from default• Report on loan status every 180 days until concluded.• Final wrap-up at conclusion • Lender to forward proportionate share of recoveries (if applicable)

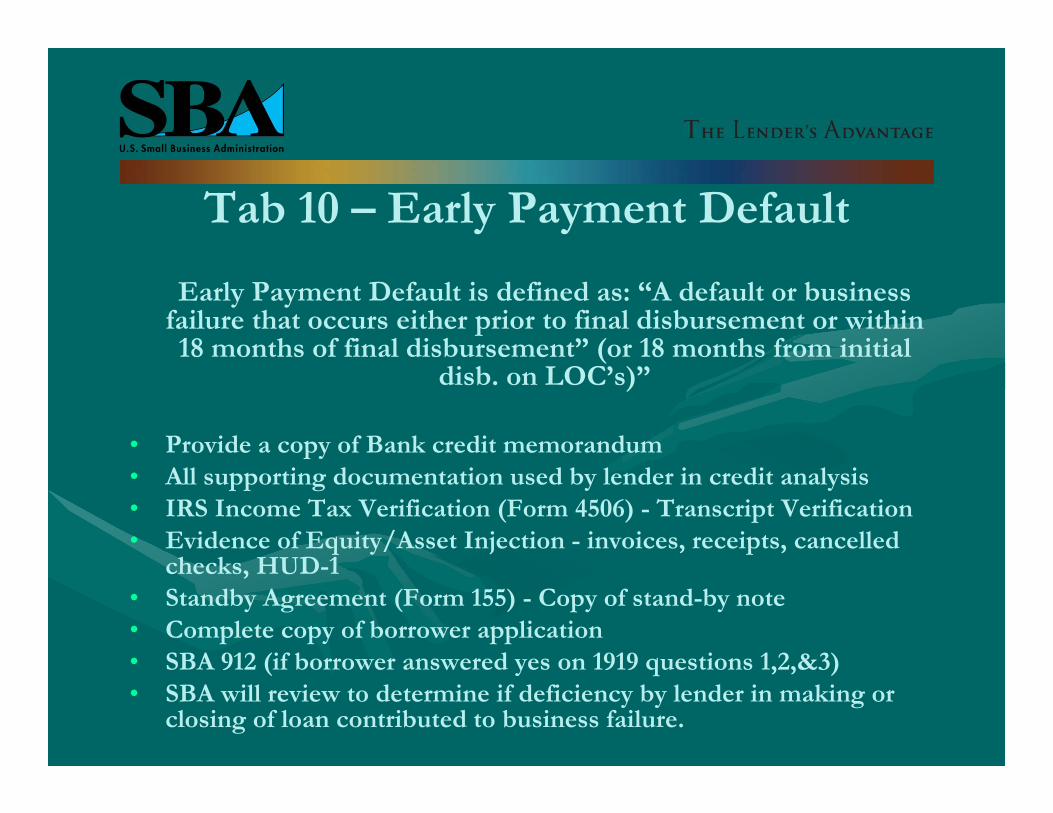

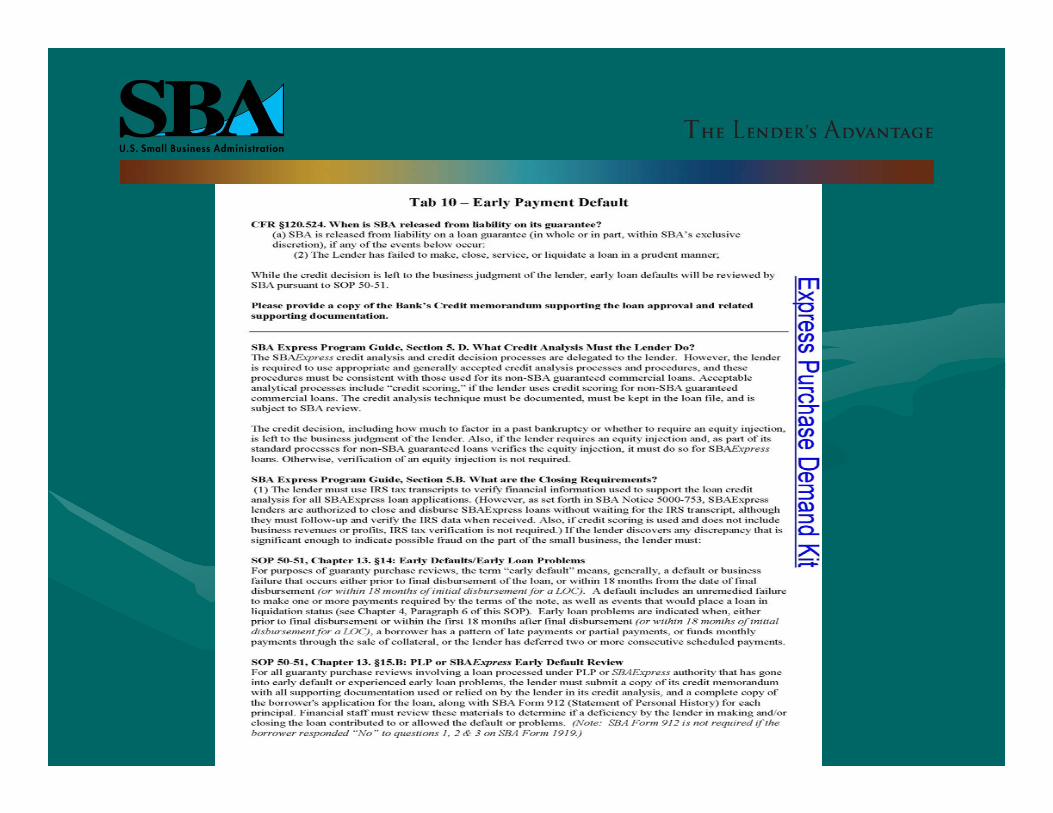

Tab 10 – Early Payment Default

Early Payment Default is defined as: “A default or business failure that occurs either prior to final disbursement or within 18 months of final disbursement” (or 18 months from initial

disb. on LOC’s)”

• Provide a copy of Bank credit memorandum• All supporting documentation used by lender in credit analysis• IRS Income Tax Verification (Form 4506) - Transcript Verification• Evidence of Equity/Asset Injection - invoices, receipts, cancelled

checks, HUD-1• Standby Agreement (Form 155) - Copy of stand-by note• Complete copy of borrower application• SBA 912 (if borrower answered yes on 1919 questions 1,2,&3) • SBA will review to determine if deficiency by lender in making or

closing of loan contributed to business failure.

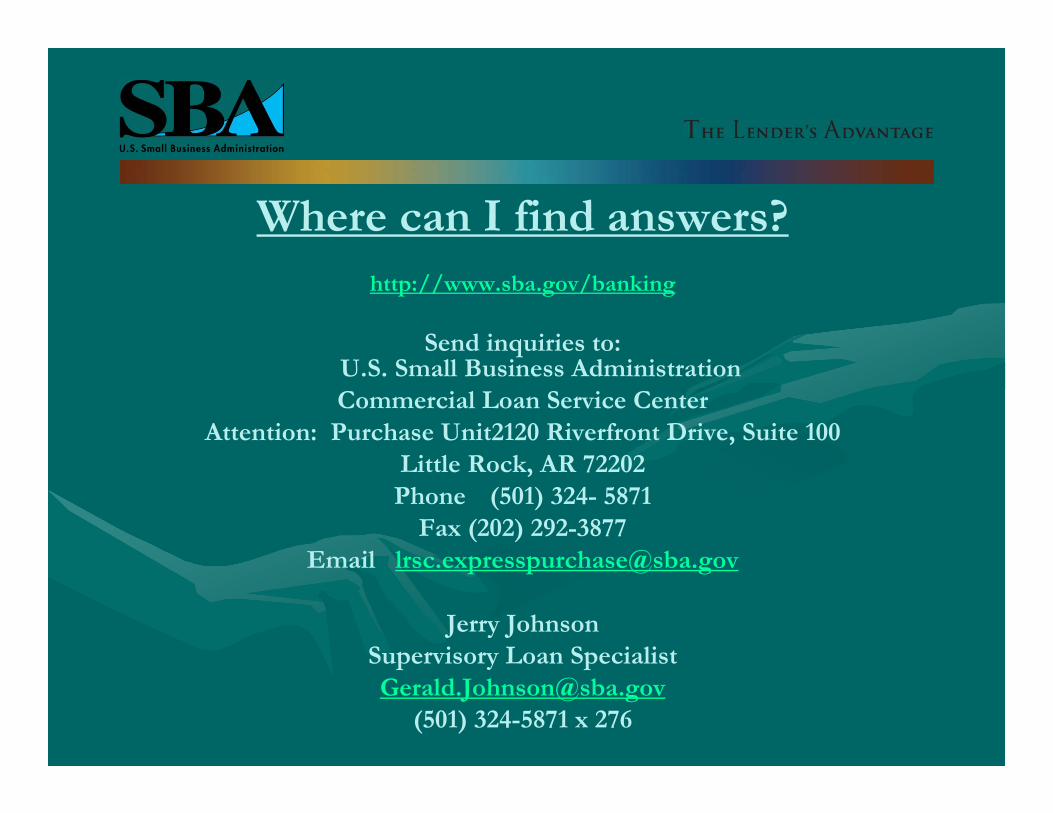

Where can I find answers?http://www.sba.gov/banking

Send inquiries to: U.S. Small Business AdministrationCommercial Loan Service Center

Attention: Purchase Unit2120 Riverfront Drive, Suite 100Little Rock, AR 72202Phone (501) 324- 5871

Fax (202) 292-3877Email [email protected]

Jerry JohnsonSupervisory Loan [email protected]

(501) 324-5871 x 276

Questions?

Thank you for your time

This Concludes our Presentation