Embed Size (px)

DESCRIPTION

PPT

Citation preview

English for Finance and Banking 1

The presentation

Sai Gon UniversityEnglish for Finance and BankingLecturer: Mrs. Doan Thi Thuy Lieu

Group

Members: 1. D ng Th Maiươ ị2. D ng Th Th yươ ị ủ3. Ph m Th Tuy t Nhungạ ị ế4. Lê Th Tuy t Nhiị ế

English for Finance and Banking 2

Topic: Interest Rate

1. What is the interest rate?

2. Reasons for interest rate changes• Your text to explain this label• Your text to explain this label

• Your text to explain this label• Your text to explain this label

3. Different Rate

4. Interest Rate in Viet Nam• Your text to explain this label• Your text to explain this label

• Your text to explain this label• Your text to explain this label

English for Finance and Banking 3

1. What is the Interest Rate?

• For example, if one holds a bond with a face value of $1,000 and a 3% interest rate payable each quarter, one receives $30 each quarter.

• The Interest Rate is the percentage of the value of a balance or debt that one pays or is paid each time period.

English for Finance and Banking 4

• For example, if one pays off part of the principal on a loan each month, the amount one pays in interest decreases even though the rate remains the same. See also: Time Value of Money .

• The percentage of the interest rate remains constant (usually), but the amount one pays or is paid changes according to the amount of the balance or debt

English for Finance and Banking 5

• Interest-rate targets are a vital tool of monetary policy and are taken into account when dealing with variables like investment, inflation, and unemployment.

The central banks of countries generally tend to reduce interest rates when they wish to increase investment and consumption in the country's economy.

6

Historical interest rates

In the past two centuries, interest rates have been variously set either by national governments or central banks. For example, the Federal Reserve federal funds rate in the United States has varied between about 0.25% to 19% from 1954 to 2008, while the Bank of England base rate varied between 0.5% and 15% from 1989 to 2009,

English for Finance and Banking

English for Finance and Banking 7

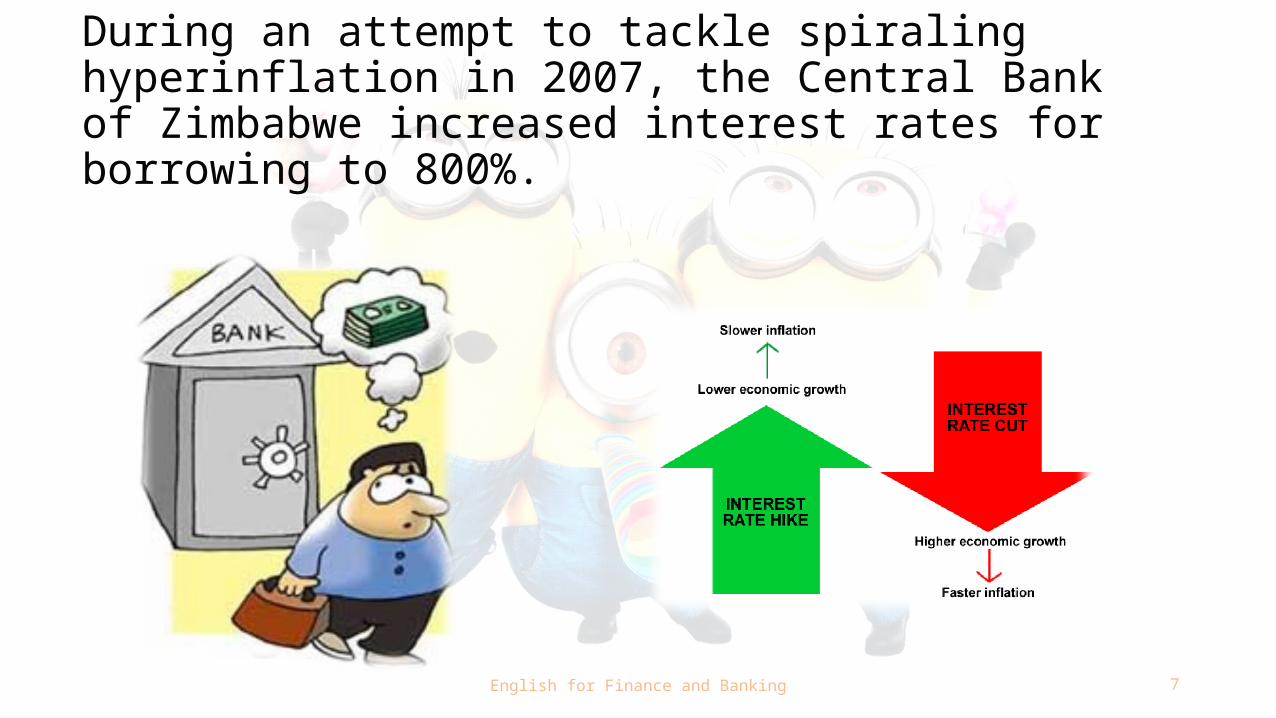

During an attempt to tackle spiraling hyperinflation in 2007, the Central Bank of Zimbabwe increased interest rates for borrowing to 800%.

English for Finance and Banking 8

2. Reasons for interest rate changes

The first: Supply and Demand for Funds: Interest rates move up and down, reflecting many factors. The most important among these is the supply of funds, available for loans from lenders, and the demand, from borrowers.

For example, take the mortgage market. In a period when many people are borrowing money to buy houses, banks and trust companies need to have the funds available to lend.

English for Finance and Banking 9

If the demand for borrowing is higher than the funds they have available, they can raise their rates or borrow money from other people by issuing bonds to institutions in the “wholesale market”.

The trouble is, this source of funds is more expensive. Therefore, interest rates go up!.

English for Finance and Banking 10

Click to edit Master title style

The second: Monetary PolicyAnother major factor in looking at an interest rate change is the monetary policy of governments. If a government loosens monetary policy, this means that it has “printed more money.” The Central Bank creates more money by printing it.This makes interest rates lower, because more money is available to lenders and borrowers alike

English for Finance and Banking 11

If the supply of money is lowered, this tightens monetary policy and causes interest rates to rise. Governments alter the money supply to try and manage the economy.

The trouble is, no one is quite sure how much money is necessary and how it is actually used once it is available.

English for Finance and Banking 12

The third: Inflation

• Another very important factor in answer why interest rates change is a consideration of inflation. Investors want to preserve the “purchasing power” of their money. If inflation is high and risks going higher, investors will need a higher interest rate to consider lending their money for more than the shortest term.

English for Finance and Banking 13

• After the very high inflation years of the 1970s and early 1980s, lenders had to receive a very high interest rate compared to inflation to lend their money. As inflation dropped, investors then demanded lower rates, as their expectations become lower. Imagine the plight of the long-term bond investor in the high inflation period.

English for Finance and Banking 14

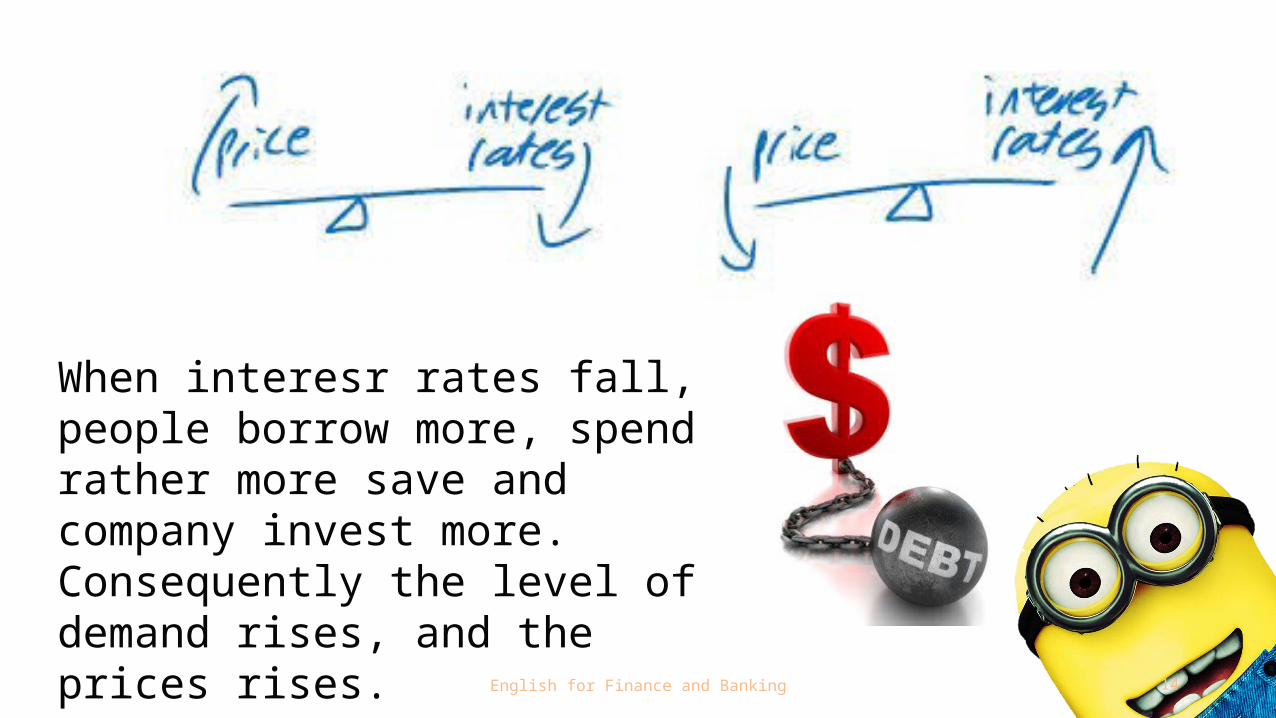

When interesr rates fall, people borrow more, spend rather more save and company invest more. Consequently the level of demand rises, and the prices rises.

English for Finance and Banking 15

3. Different Interest Rate

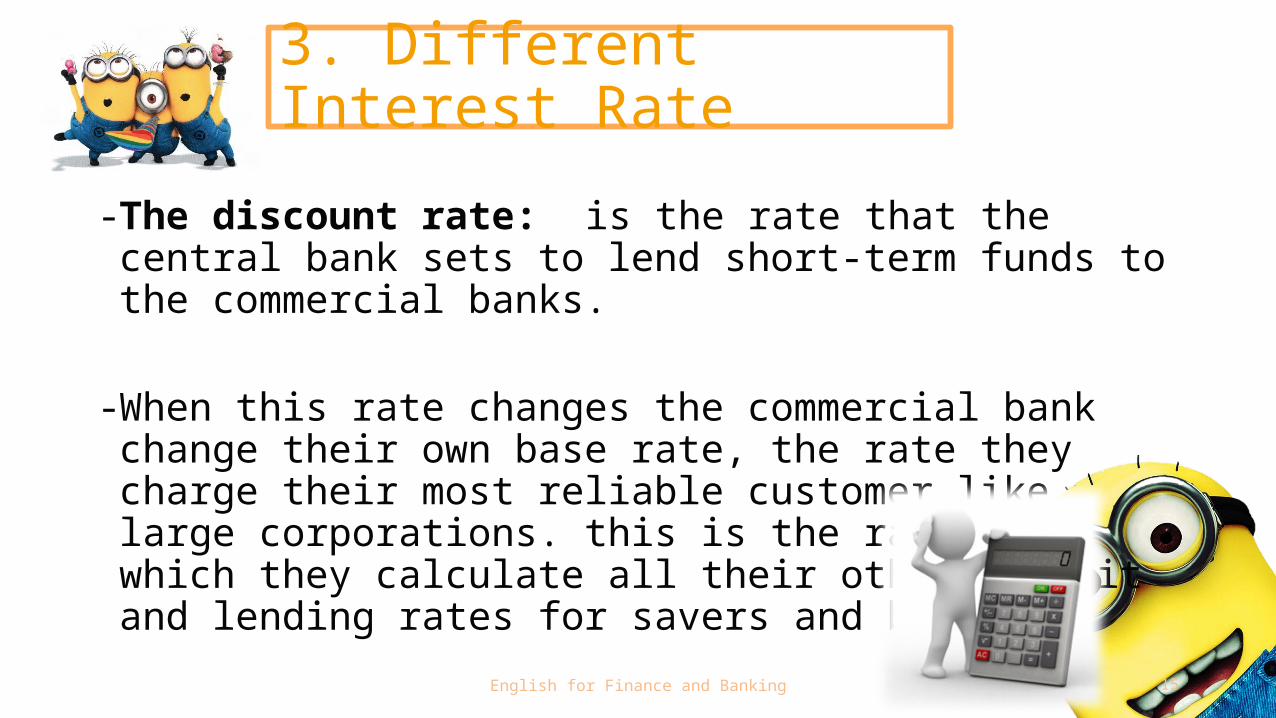

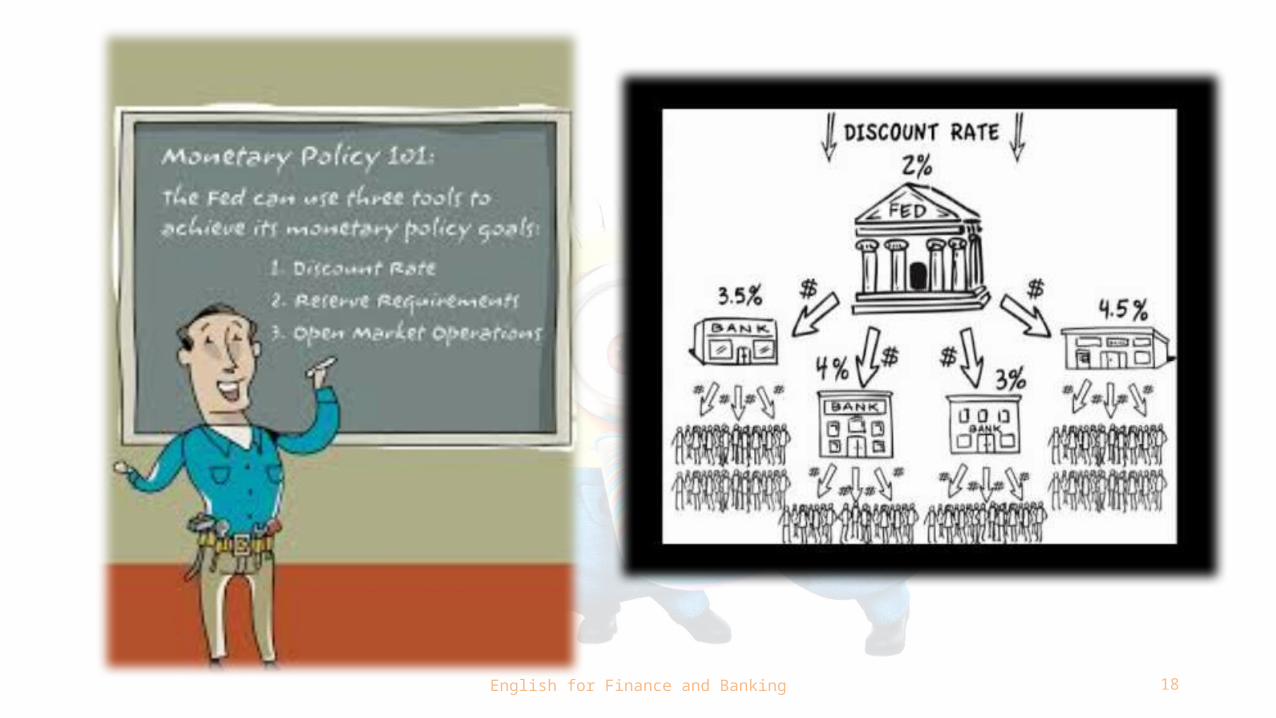

- The discount rate: is the rate that the central bank sets to lend short-term funds to the commercial banks.

-When this rate changes the commercial bank change their own base rate, the rate they charge their most reliable customer like large corporations. this is the rate from which they calculate all their other deposit and lending rates for savers and borrower

English for Finance and Banking 16

The estimation of a suitable discount rate is often the most difficult and uncertain part of a DCF. This is only worsened by the fact that the final result is very sensitive to the choice of discount rate — a small change in the discount rate causes a large change in the value.

For listed securities the discount rate is most often calculated using CAPM. The availability of both data to calculate betas and of services that provide beta estimates make this convenient.

English for Finance and Banking 17

In Viet Nam (March,2013), The central bank said in a statement that has asked bankers will VND short-term deposit interest rate ceiling, down 0.5 percentage points to 7.5%.

Prior to that, out of the need to stimulate the domestic economy, the Vietnamese government ordered the central bank to take interest rate cuts, so the decline in the cost of corporate finance, financing needs to meet. While the banking sector, but they still need to cope with high non-performing loan ratio.

English for Finance and Banking 18

English for Finance and Banking 19

• Hire purchase (HP) or leasing : is a type of asset finance that allow firms or individuals to possess and control an asset during an agreed term, while paying rent or instalments covering depreciation of the asset, and interest to cover capital cost.

- agreements have higher interest rate than bank loans and overdraft. - interest rate is high as there is little security for the lender

English for Finance and Banking 20

Advantages•HP or leasing allows companies to control and deploy assets without significant drain on working capital• fixed-rate funding makes budgeting easy as the lessee has clear sight of future expenditures• leasing prevents the risk of an asset’s value depreciating quickly and provides flexibility to enter into a new contract at the end of the original lease’s fixed term

English for Finance and Banking 21

Disadvantages• Total sum of capital payments for HP or leasing will be higher than the full payment on the asset purchase• Administrative complexity and costs will be greater if any covenants are applied to the arrangement. For example, updates on change of equipment locations• If the business changes its strategy, resulting in the leased asset no longer being useful, there can be early termination charges or

restrictions on subleasing.

English for Finance and Banking 22

4. The interest Rate in Viet Nam

Deposit Rates in VietnamIn recent years, interest rates on deposits in Vietnam has many changes due to fluctuations in the economy. Interest rate increases because of inflation. Economic difficulties. In 2013 the bank has many policies to stabilize interest rates.

English for Finance and Banking 23

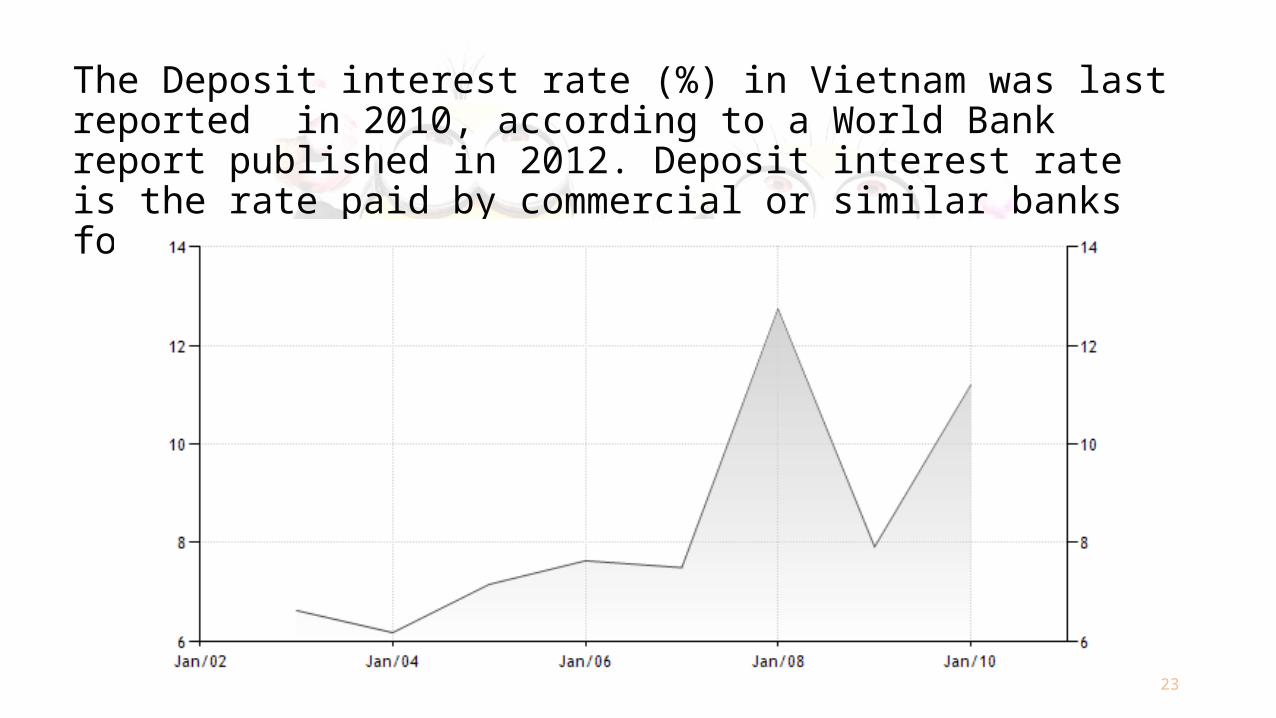

The Deposit interest rate (%) in Vietnam was last reported in 2010, according to a World Bank report published in 2012. Deposit interest rate is the rate paid by commercial or similar banks for demand, time, or savings

English for Finance and Banking 24

English for Finance and Banking 25

Lending Interest Rate

Commercial banks have kicked off a new interest rate race. However, they don’t scramble for depositors by offering high interest rates any more, but try to find as many borrowers as possible.

Though the lending interest rates have decreased significantly from the last year, the credit growth rate remains modest.

English for Finance and Banking 26

A report of the State Bank showed that by the end of August 2013, the growth rate of the whole banking system had reached 6.45 percent only, while it hoped the figure would be 12 percent this year.

Therefore, analysts believe that the interest rate downward tendency would continue, and the only solution for banks to boost lending is to increase the disbursement of consumer loans.

English for Finance and Banking 27

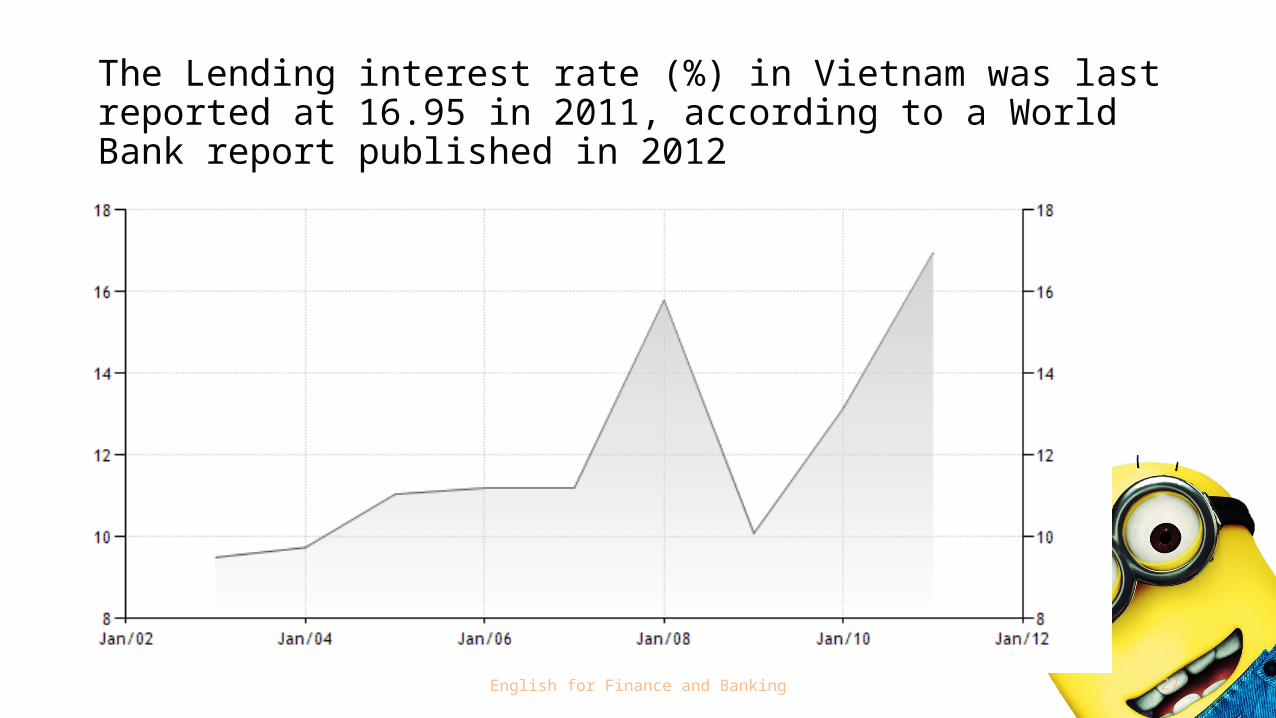

The Lending interest rate (%) in Vietnam was last reported at 16.95 in 2011, according to a World Bank report published in 2012

English for Finance and Banking 28

Thanks for your listening !

![Nuttenverschnitt (aus dem autobiografischen Roman „Mau-Mau“]](https://img.pdfslide.tips/doc/110x75/577cd7f11a28ab9e78a00aa4/nuttenverschnitt-aus-dem-autobiografischen-roman-mau-mau.jpg)