Embed Size (px)

Citation preview

08/05/2014

1

N R id t T tNon-Resident TrustsThe Canadian Experience

Michael Cadesky, TEP, and Grace Chow, TEP(Cadesky and Associates, LLP)

Chair: Lorraine Wheeler (First Names Group)

Sponsored by:

Non‐Resident TrustsThe Canadian ExperienceThe Canadian Experience

MICHAEL CADESKY, TEPGRACE CHOW, TEP

2

CADESKY AND ASSOCIATES LLPTORONTO, CANADA

08/05/2014

2

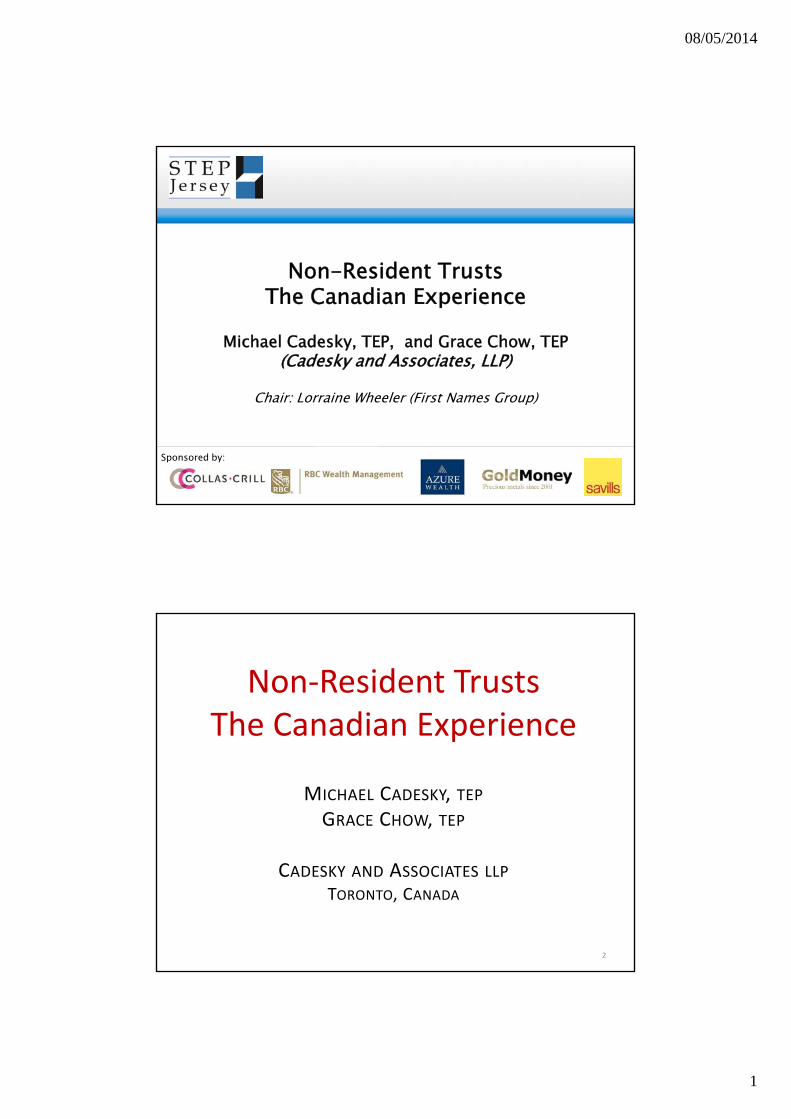

Chapter 1Good Old Days‐ 1972 – 1996Non‐resident trust not taxed unless:1. Canadian resident contribution (or resident in (

past 18 months)2. Canadian resident beneficiary3. Contributor and beneficiary related; and4. Canadian resident contributor was resident for

60 monthsN ti f ki dNo reporting of any kindTax‐free capital distributions Income becomes capital at December 31

3

Schematic

Trustees non‐resident

TRUST

Contributor

Beneficiaries

4

08/05/2014

3

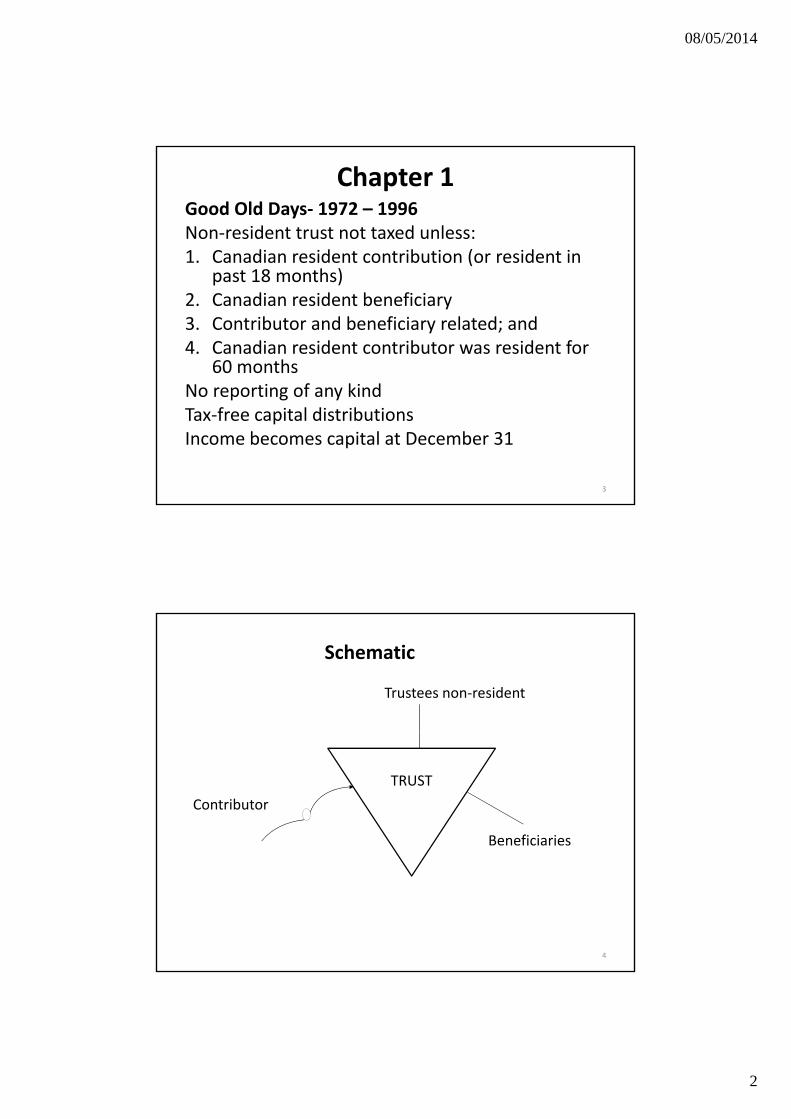

1. No Canadian Resident Contributor

TRUSTContributor(non‐resident)

Canadian Resident B fi i i

5

Beneficiaries

Trust not taxed Capital distribution tax‐free to Canadian resident beneficiaries

TRUST

1.(a) Freeze Structure Non‐Resident Contributor

Non‐resident Contributor

Canadian Resident Beneficiaries

Canadian Resident

commonPreferred shares

$100

6

CORPORATION

Nominal amount from non‐resident contributor for growth shares.

08/05/2014

4

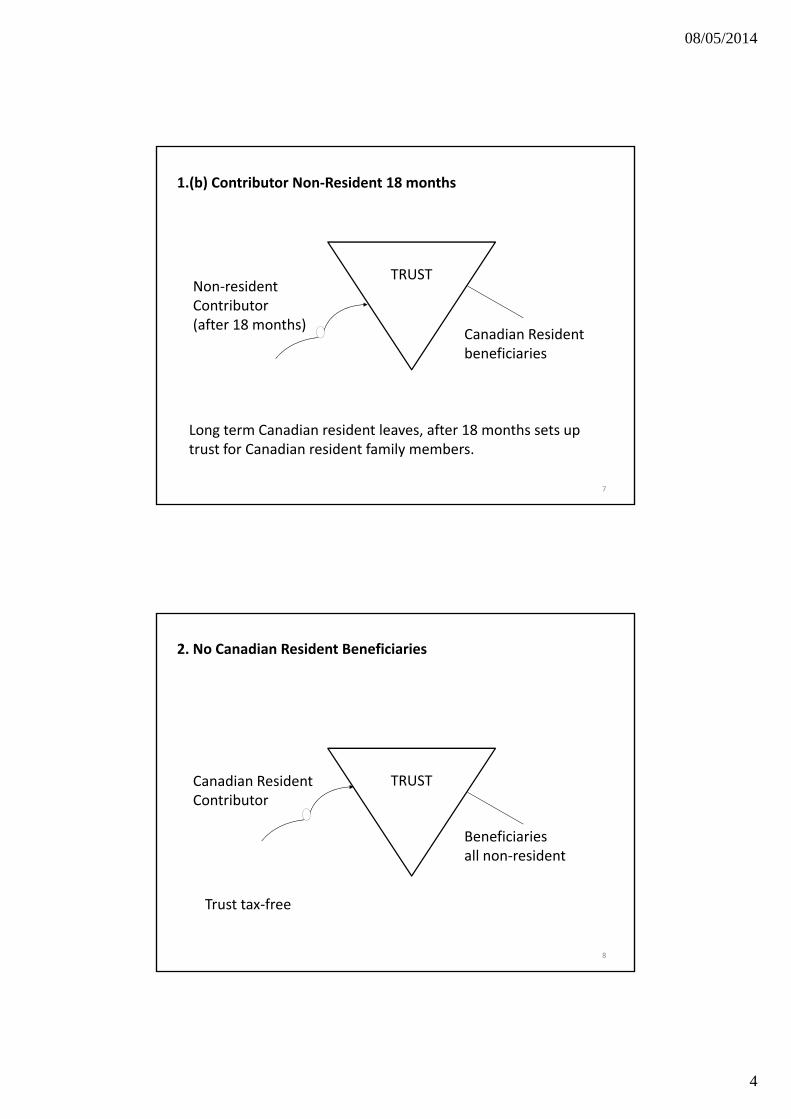

1.(b) Contributor Non‐Resident 18 months

TRUSTNon‐resident Contributor(after 18 months)

Canadian Resident beneficiaries

7

Long term Canadian resident leaves, after 18 months sets up trust for Canadian resident family members.

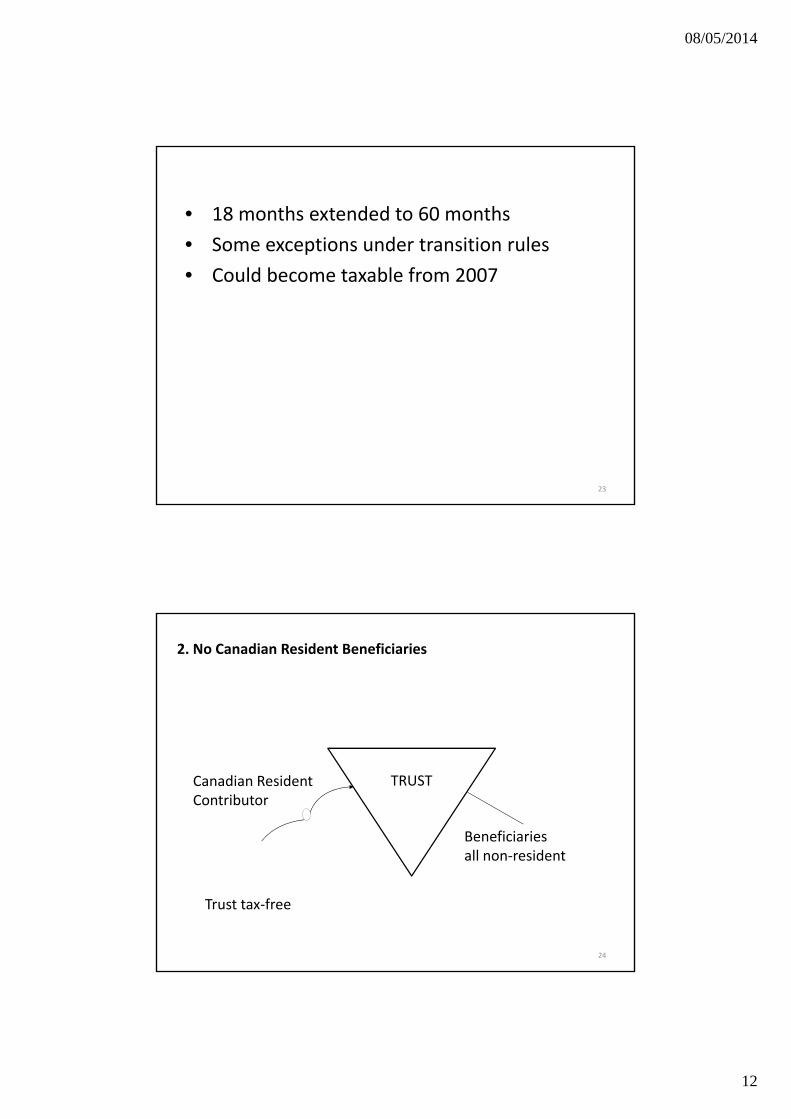

2. No Canadian Resident Beneficiaries

TRUSTCanadian Resident Contributor

Beneficiariesll id t

8

all non‐resident

Trust tax‐free

08/05/2014

5

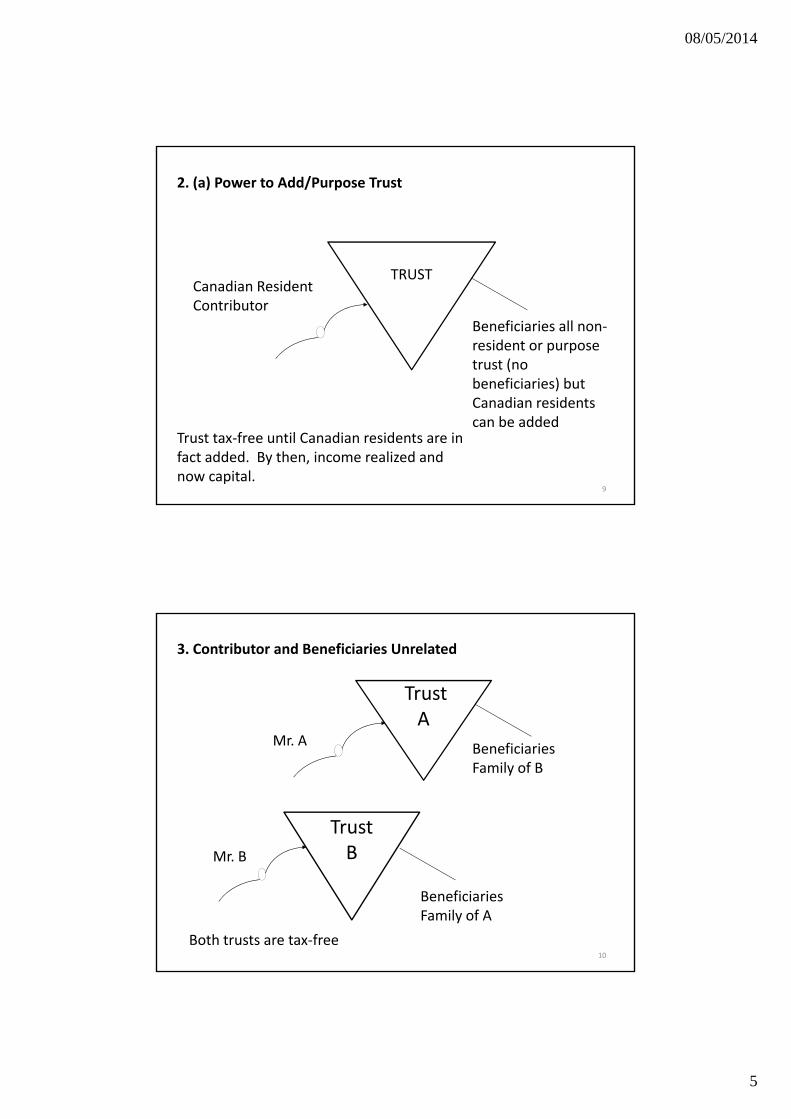

2. (a) Power to Add/Purpose Trust

TRUSTCanadian Resident Contributor

Beneficiaries all non‐resident or purpose trust (no beneficiaries) but

9

beneficiaries) but Canadian residents can be added

Trust tax‐free until Canadian residents are in fact added. By then, income realized and now capital.

TrustA

3. Contributor and Beneficiaries Unrelated

Mr. A Beneficiaries Family of B

TrustBM B

10

BMr. B

Beneficiaries Family of A

Both trusts are tax‐free

08/05/2014

6

IMMIGRANT

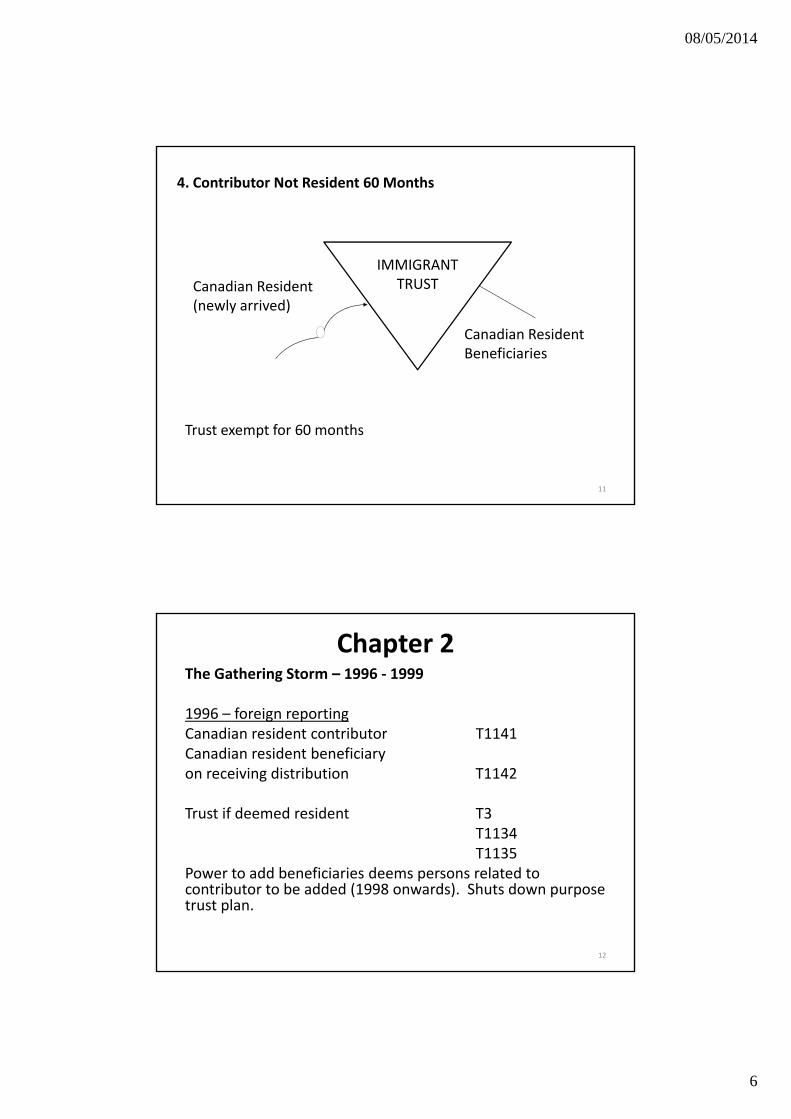

4. Contributor Not Resident 60 Months

IMMIGRANT TRUSTCanadian Resident

(newly arrived)

Canadian Resident Beneficiaries

11

Trust exempt for 60 months

Chapter 2The Gathering Storm – 1996 ‐ 1999

1996 – foreign reportingCanadian resident contributor T1141Canadian resident contributor T1141Canadian resident beneficiaryon receiving distribution T1142

Trust if deemed resident T3T1134T1135T1135

Power to add beneficiaries deems persons related to contributor to be added (1998 onwards). Shuts down purpose trust plan.

12

08/05/2014

7

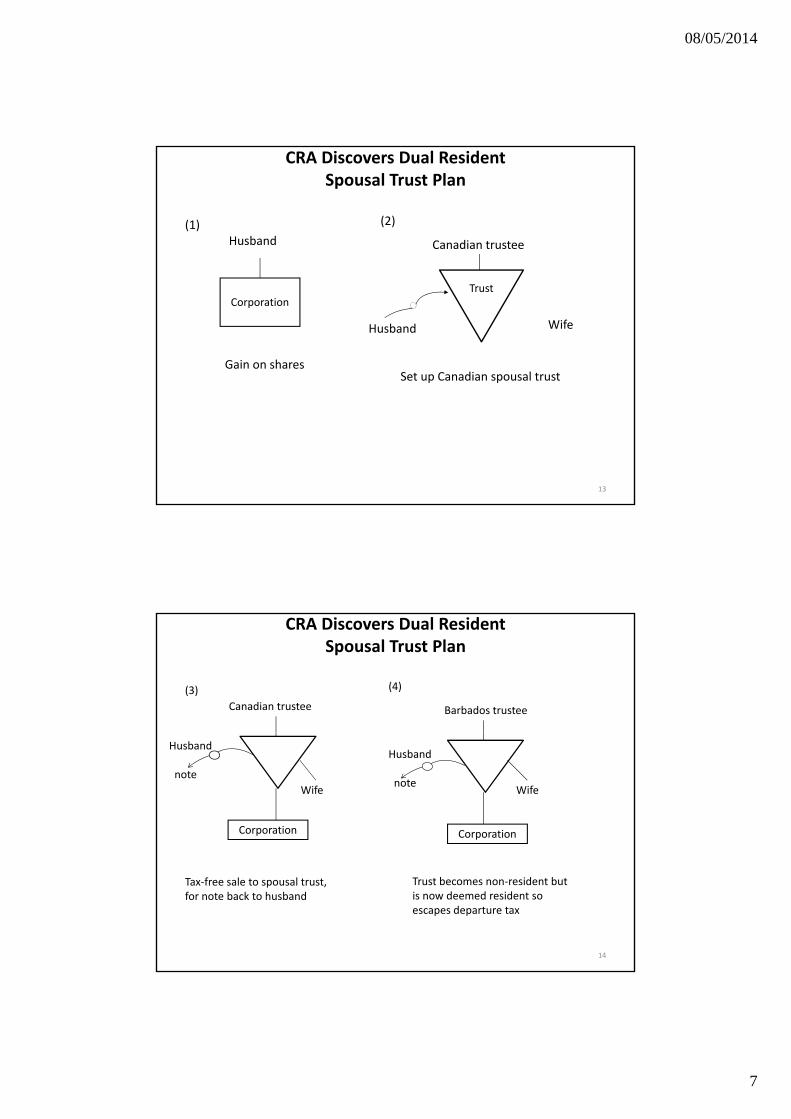

CRA Discovers Dual Resident Spousal Trust Plan

Canadian trusteeHusband(1) (2)

CorporationTrust

Gain on shares

WifeHusband

Set up Canadian spousal trust

13

CRA Discovers Dual Resident Spousal Trust Plan

Canadian trustee Barbados trustee

(3) (4)

Corporation Corporation

Wife Wife

Husband

note

Husband

note

14

Tax‐free sale to spousal trust, for note back to husband

Trust becomes non‐resident but is now deemed resident so escapes departure tax

08/05/2014

8

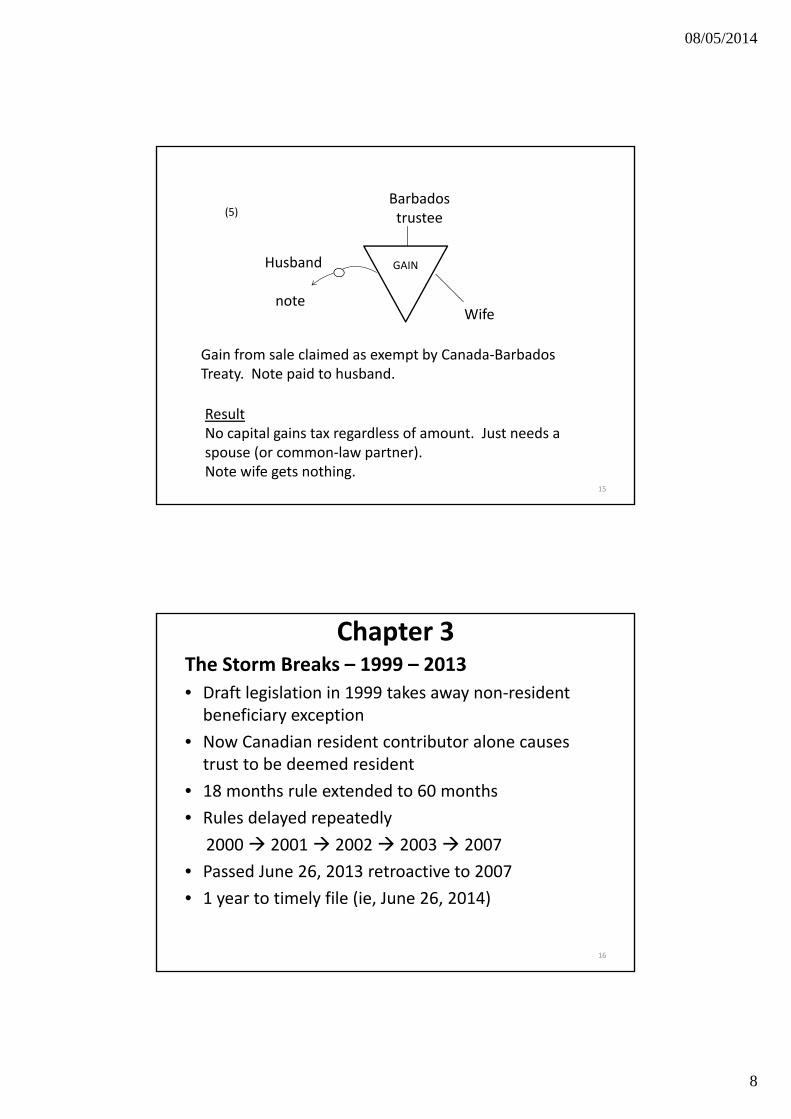

GAIN

Barbados trustee

Husband

(5)

GAIN

Wife

Husband

note

Gain from sale claimed as exempt by Canada‐Barbados Treaty. Note paid to husband.

15

ResultNo capital gains tax regardless of amount. Just needs a spouse (or common‐law partner). Note wife gets nothing.

Chapter 3The Storm Breaks – 1999 – 2013• Draft legislation in 1999 takes away non‐resident beneficiary exception

• Now Canadian resident contributor alone causes trust to be deemed resident

• 18 months rule extended to 60 months

• Rules delayed repeatedly

2000 2001 2002 2003 2007

• Passed June 26, 2013 retroactive to 2007

• 1 year to timely file (ie, June 26, 2014)

16

08/05/2014

9

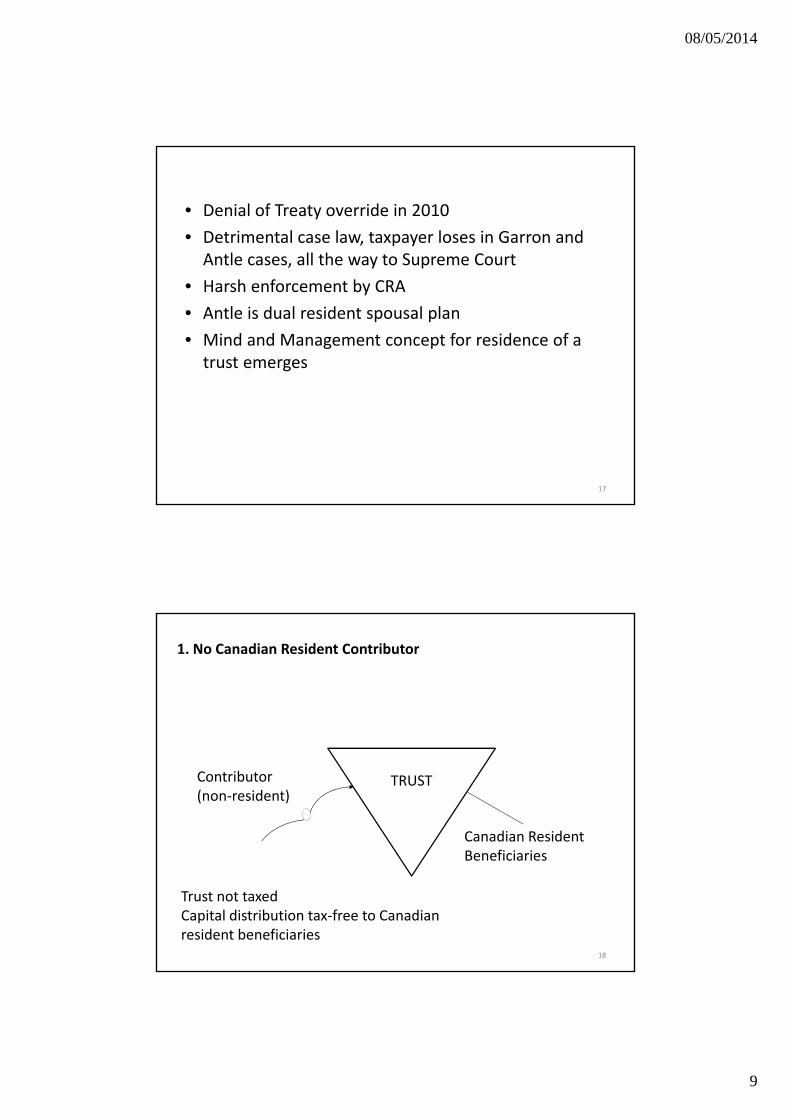

• Denial of Treaty override in 2010

• Detrimental case law, taxpayer loses in Garron and Antle cases, all the way to Supreme Court, y p

• Harsh enforcement by CRA

• Antle is dual resident spousal plan

• Mind and Management concept for residence of a trust emerges

17

1. No Canadian Resident Contributor

TRUSTContributor(non‐resident)

Canadian Resident B fi i i

18

Beneficiaries

Trust not taxed Capital distribution tax‐free to Canadian resident beneficiaries

08/05/2014

10

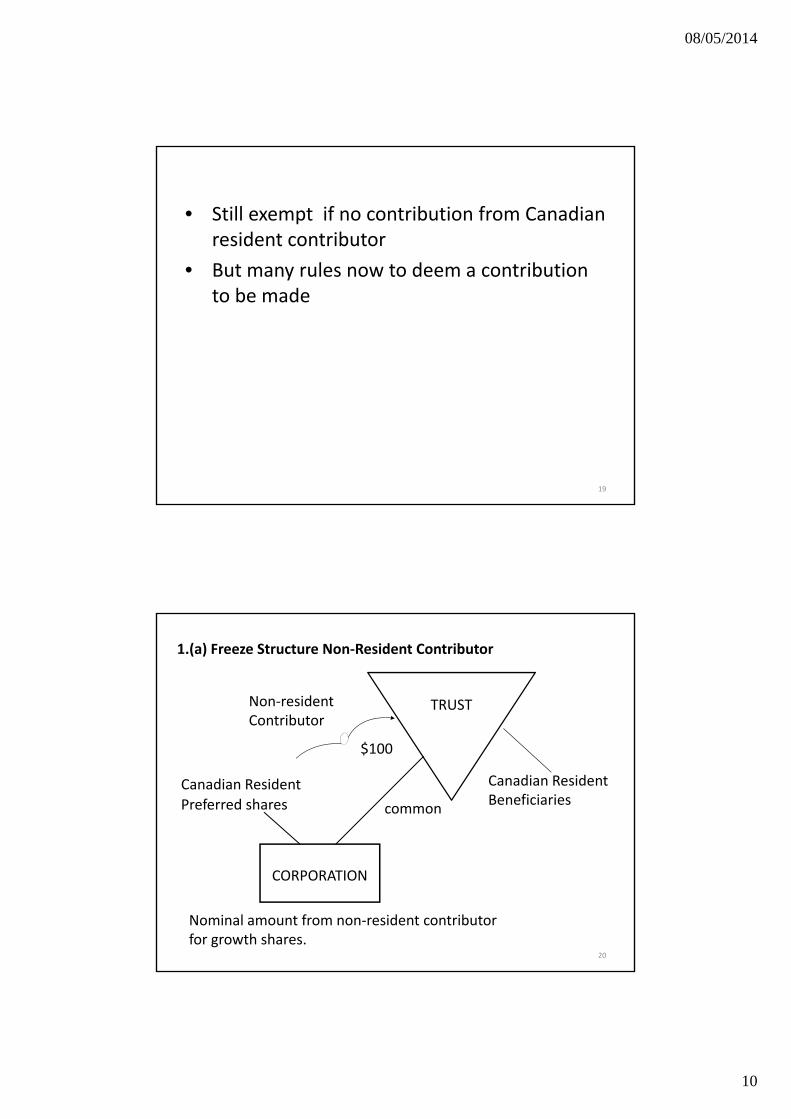

• Still exempt if no contribution from Canadian resident contributor

B t l t d t ib ti• But many rules now to deem a contribution to be made

19

TRUST

1.(a) Freeze Structure Non‐Resident Contributor

Non‐resident Contributor

Canadian Resident Beneficiaries

Canadian Resident

commonPreferred shares

$100

20

CORPORATION

Nominal amount from non‐resident contributor for growth shares.

08/05/2014

11

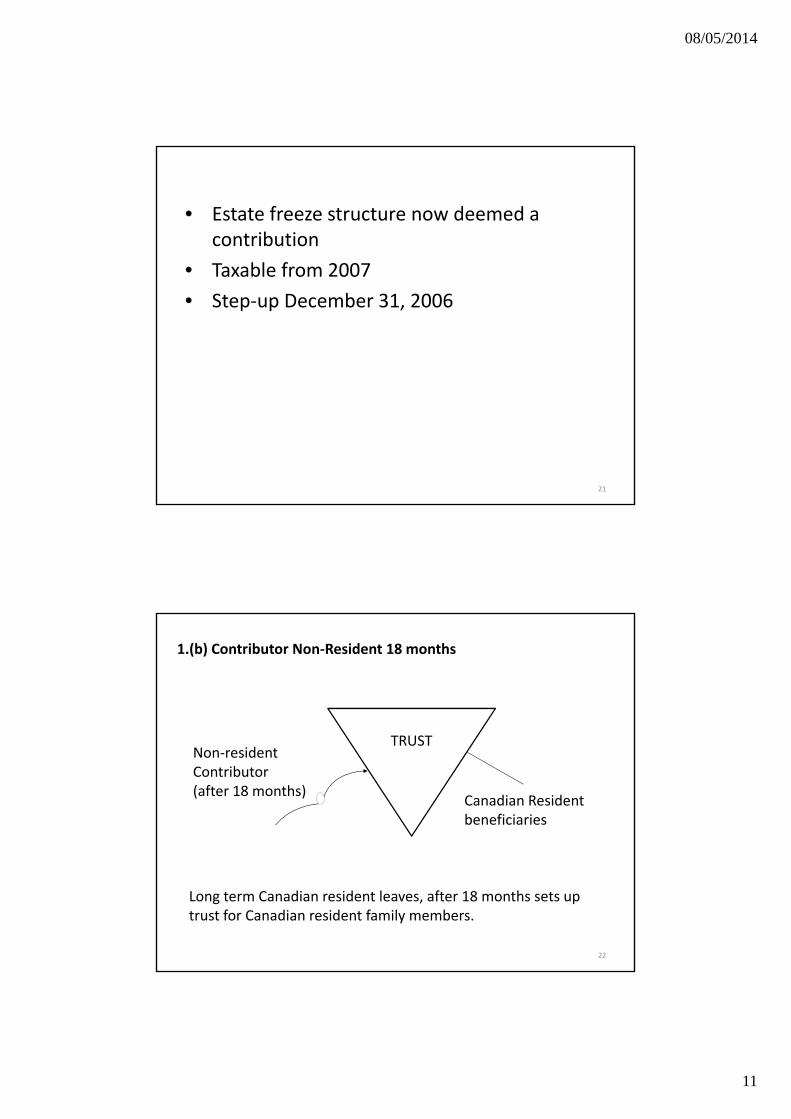

• Estate freeze structure now deemed a contribution

T bl f 2007• Taxable from 2007

• Step‐up December 31, 2006

21

1.(b) Contributor Non‐Resident 18 months

TRUSTNon‐resident Contributor(after 18 months)

Canadian Resident beneficiaries

22

Long term Canadian resident leaves, after 18 months sets up trust for Canadian resident family members.

08/05/2014

12

• 18 months extended to 60 months

• Some exceptions under transition rules

• Could become taxable from 2007

23

2. No Canadian Resident Beneficiaries

TRUSTCanadian Resident Contributor

Beneficiariesll id t

24

all non‐resident

Trust tax‐free

08/05/2014

13

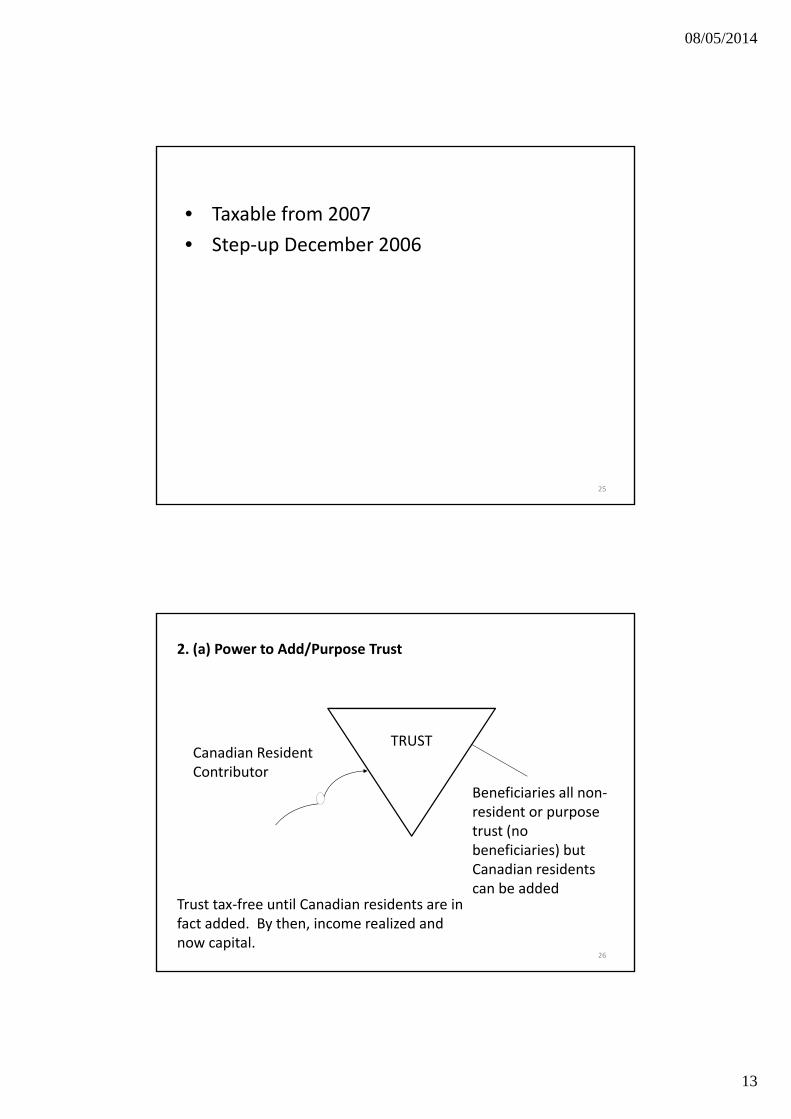

• Taxable from 2007

• Step‐up December 2006

25

2. (a) Power to Add/Purpose Trust

TRUSTCanadian Resident Contributor

Beneficiaries all non‐resident or purpose trust (no beneficiaries) but

26

beneficiaries) but Canadian residents can be added

Trust tax‐free until Canadian residents are in fact added. By then, income realized and now capital.

08/05/2014

14

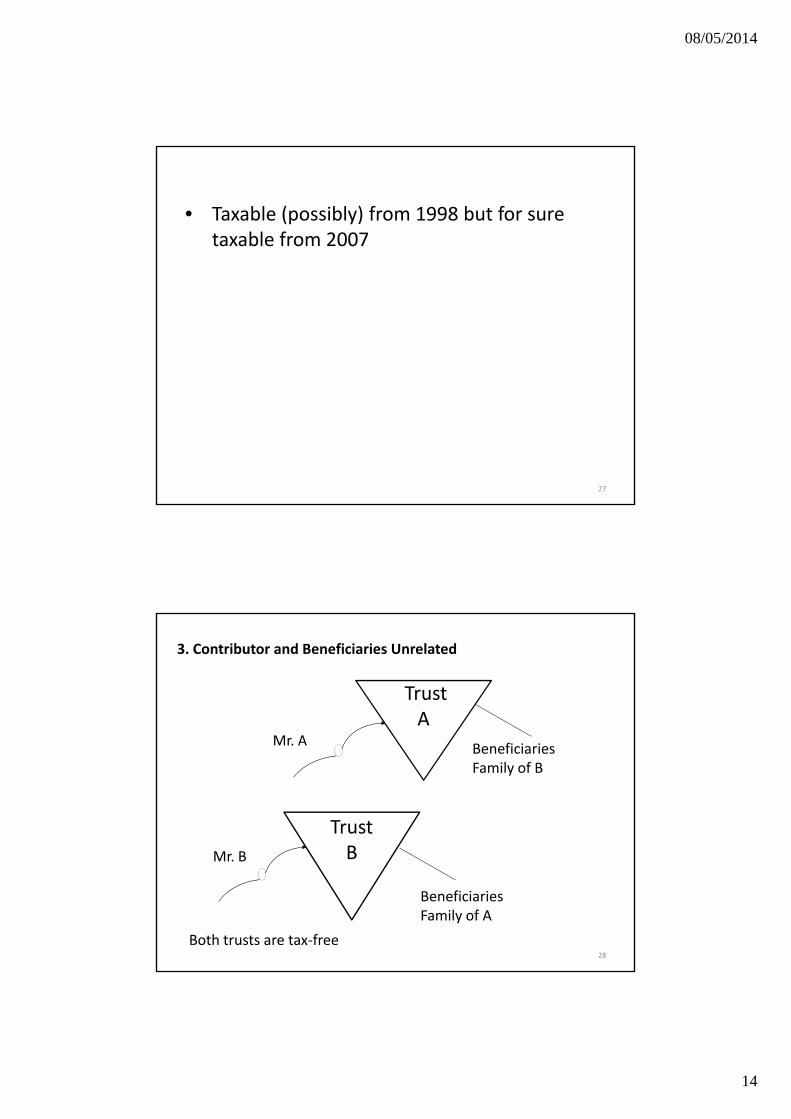

• Taxable (possibly) from 1998 but for sure taxable from 2007

27

TrustA

3. Contributor and Beneficiaries Unrelated

Mr. A Beneficiaries Family of B

TrustBM B

28

BMr. B

Beneficiaries Family of A

Both trusts are tax‐free

08/05/2014

15

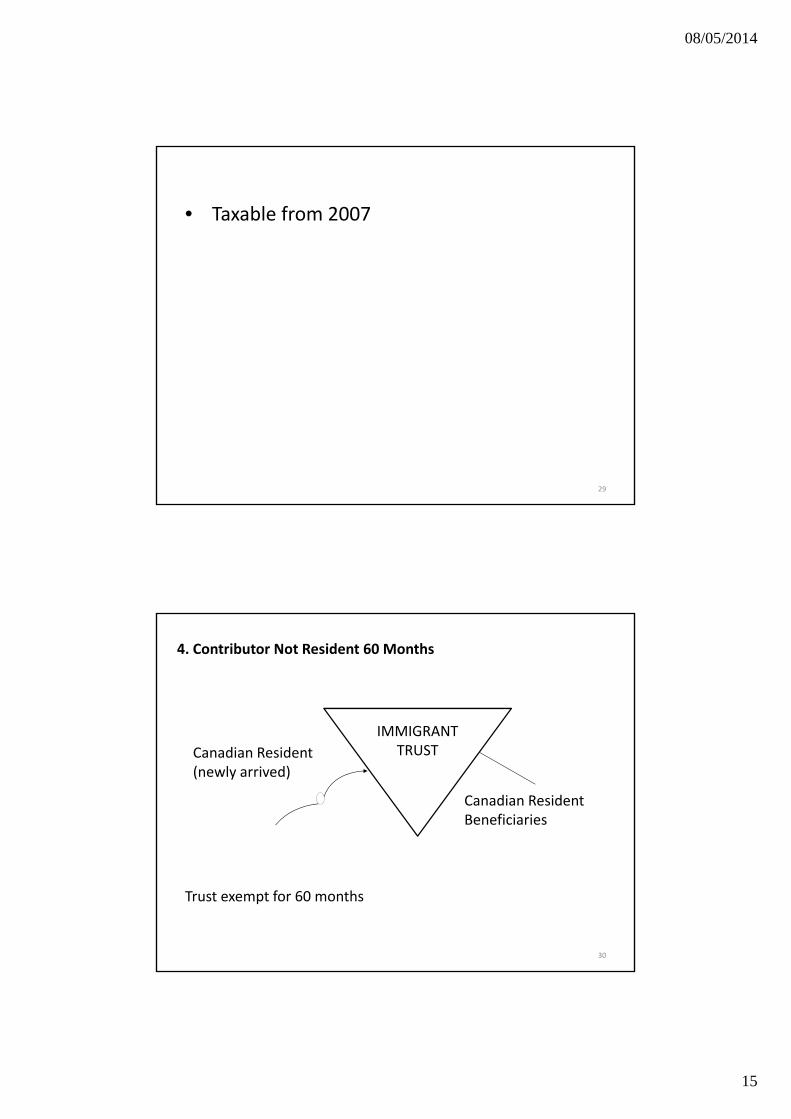

• Taxable from 2007

29

IMMIGRANT

4. Contributor Not Resident 60 Months

IMMIGRANT TRUSTCanadian Resident

(newly arrived)

Canadian Resident Beneficiaries

30

Trust exempt for 60 months

08/05/2014

16

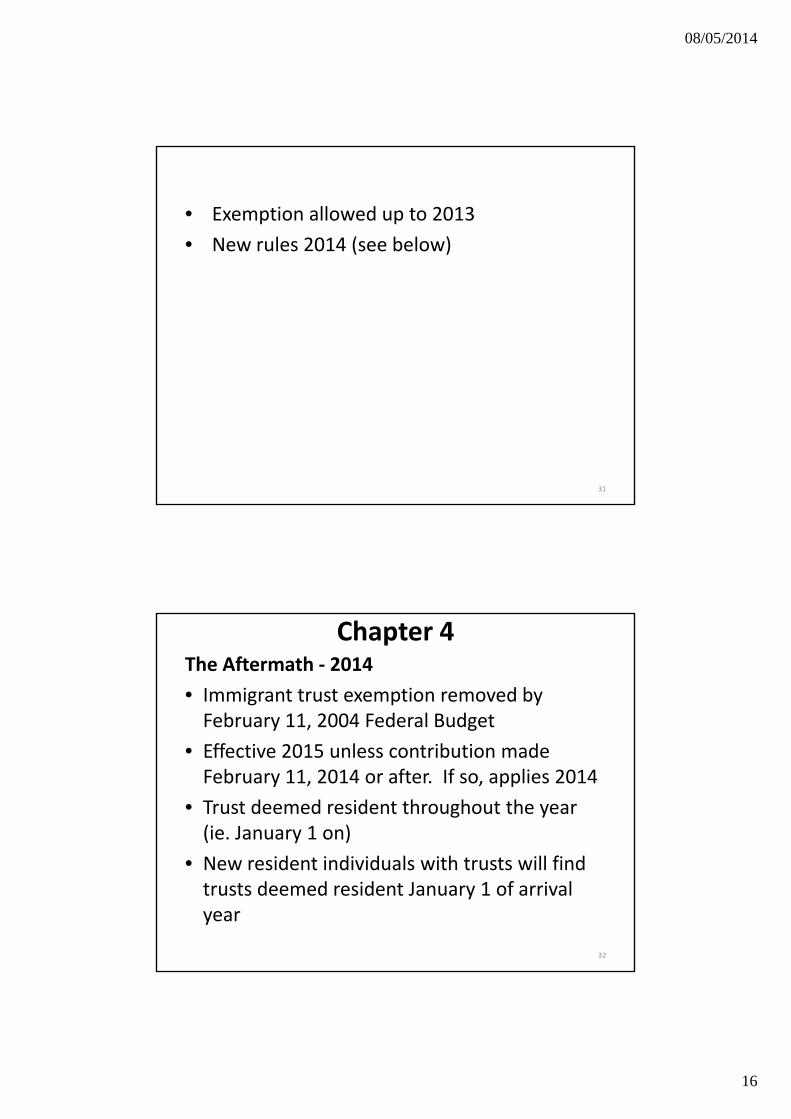

• Exemption allowed up to 2013

• New rules 2014 (see below)

31

Chapter 4The Aftermath ‐ 2014

• Immigrant trust exemption removed by February 11, 2004 Federal Budget

• Effective 2015 unless contribution made February 11, 2014 or after. If so, applies 2014

• Trust deemed resident throughout the year (ie. January 1 on)

• New resident individuals with trusts will find trusts deemed resident January 1 of arrival year

32

08/05/2014

17

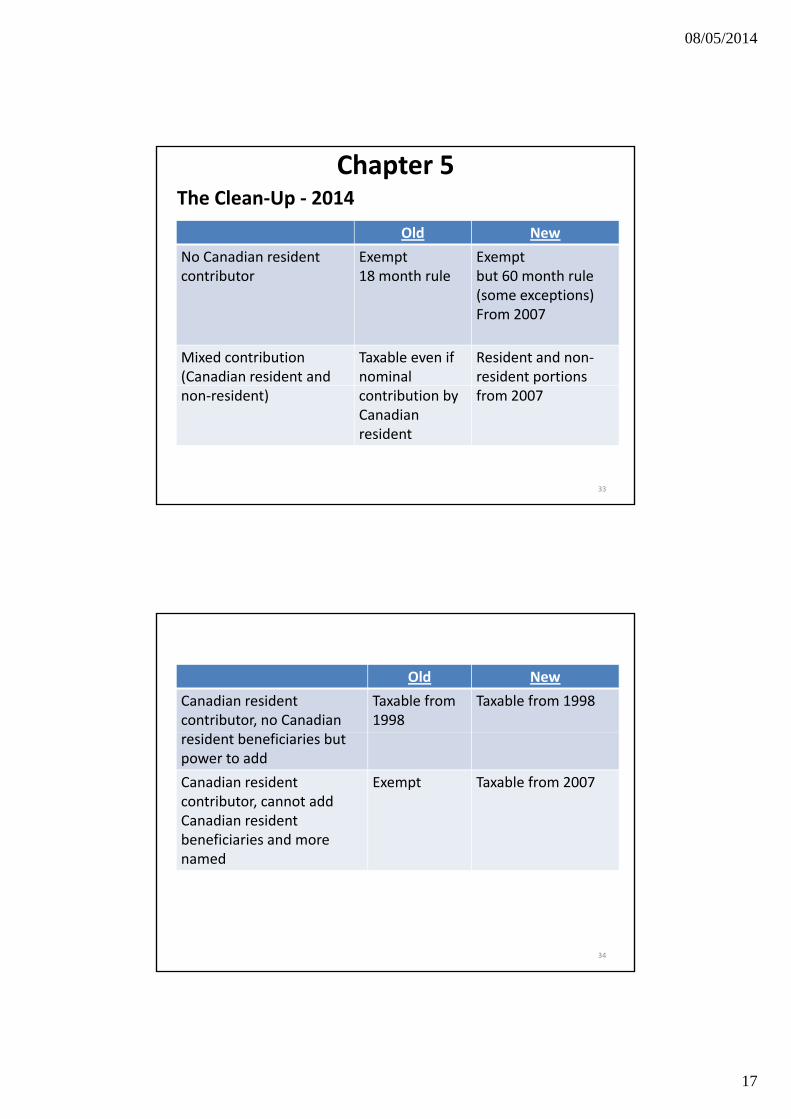

The Clean‐Up ‐ 2014

Old New

No Canadian resident Exempt Exempt

Chapter 5

contributor 18 month rule but 60 month rule(some exceptions) From 2007

Mixed contribution(Canadian resident and

Taxable even if nominal

Resident and non‐resident portions

33

non‐resident) contribution by Canadian resident

from 2007

Old New

Canadian resident contributor, no Canadian

Taxable from 1998

Taxable from 1998

resident beneficiaries but power to add

Canadian residentcontributor, cannot add Canadian resident beneficiaries and more

Exempt Taxable from 2007

34

named

08/05/2014

18

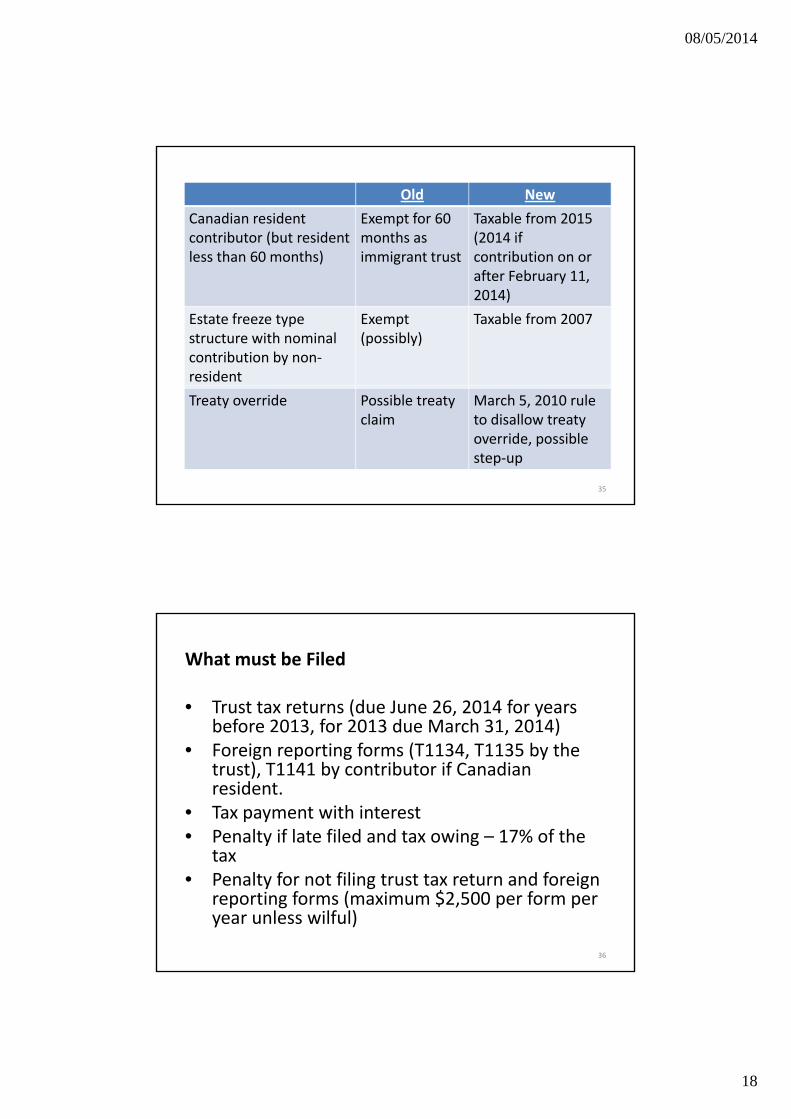

Old New

Canadian residentcontributor (but resident less than 60 months)

Exempt for 60 months as immigrant trust

Taxable from 2015 (2014 ifcontribution on or after February 11, 2014)

Estate freeze type structure with nominal contribution by non‐resident

Exempt (possibly)

Taxable from 2007

35

Treaty override Possible treaty claim

March 5, 2010 rule to disallow treaty override, possible step‐up

What must be Filed

• Trust tax returns (due June 26, 2014 for years before 2013, for 2013 due March 31, 2014)before 0 3, for 0 3 due March 3 , 0 4)

• Foreign reporting forms (T1134, T1135 by the trust), T1141 by contributor if Canadian resident.

• Tax payment with interest• Penalty if late filed and tax owing – 17% of the

ttax• Penalty for not filing trust tax return and foreign

reporting forms (maximum $2,500 per form per year unless wilful)

36

08/05/2014

19

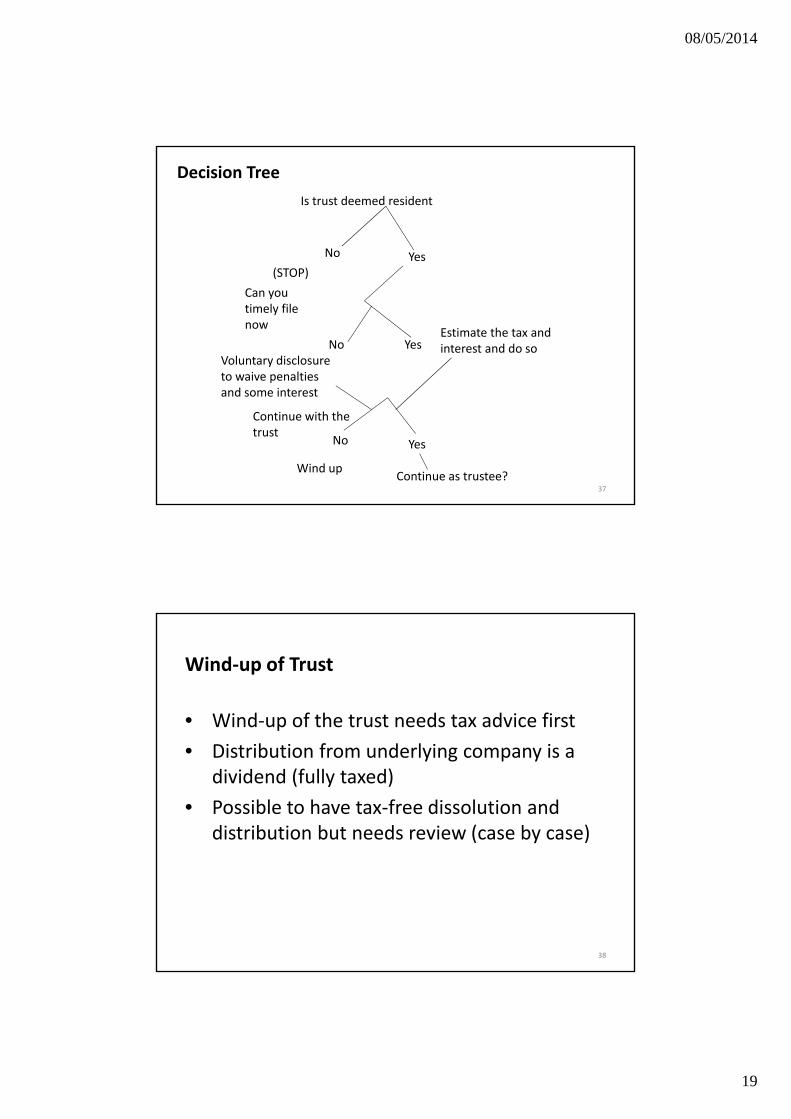

Decision Tree

Is trust deemed resident

No Yes

Can you timely file now

(STOP)

YesNoEstimate the tax and interest and do so

Voluntary disclosure to waive penalties

37

Yes

and some interest

Continue with the trust

No

Wind upContinue as trustee?

Wind‐up of Trust

• Wind‐up of the trust needs tax advice first

• Distribution from underlying company is a dividend (fully taxed)

• Possible to have tax‐free dissolution and distribution but needs review (case by case)

38

08/05/2014

20

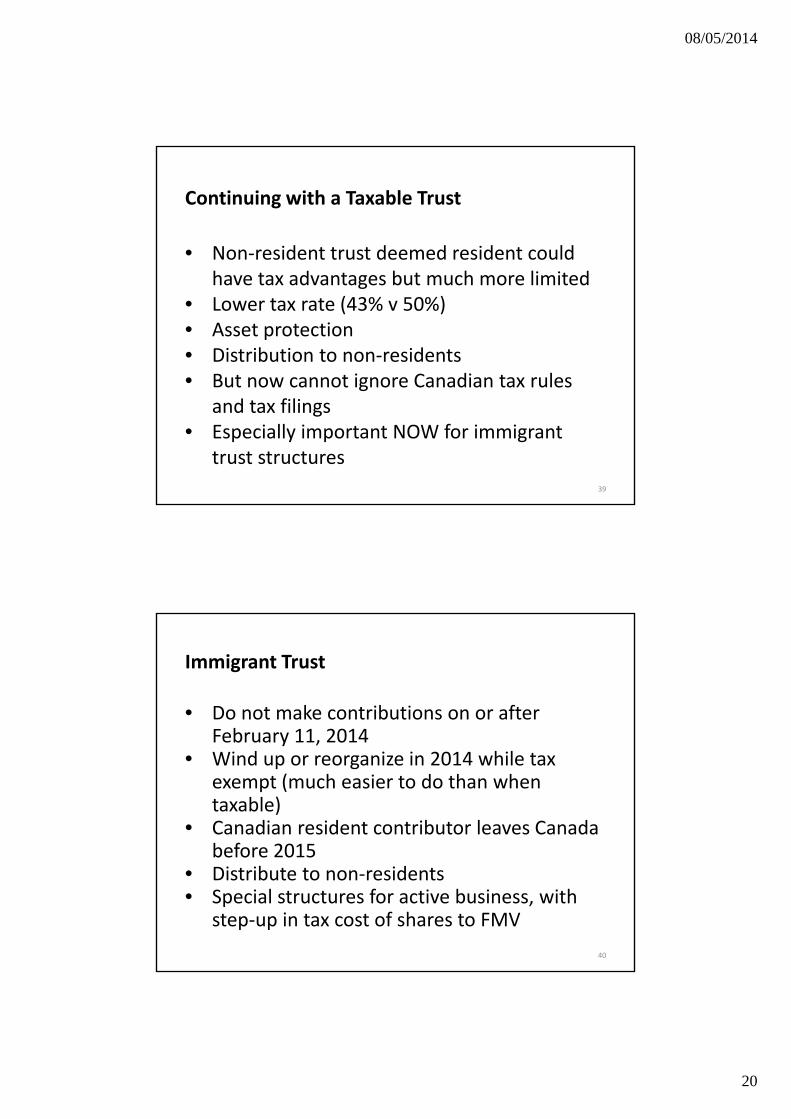

Continuing with a Taxable Trust

• Non‐resident trust deemed resident could have tax advantages but much more limited

• Lower tax rate (43% v 50%)• Asset protection• Distribution to non‐residents• But now cannot ignore Canadian tax rulesBut now cannot ignore Canadian tax rules

and tax filings• Especially important NOW for immigrant

trust structures39

Immigrant Trust

• Do not make contributions on or after Febr ar 11 2014February 11, 2014

• Wind up or reorganize in 2014 while tax exempt (much easier to do than when taxable)

• Canadian resident contributor leaves Canada before 2015before 2015

• Distribute to non‐residents• Special structures for active business, with

step‐up in tax cost of shares to FMV

40

08/05/2014

21

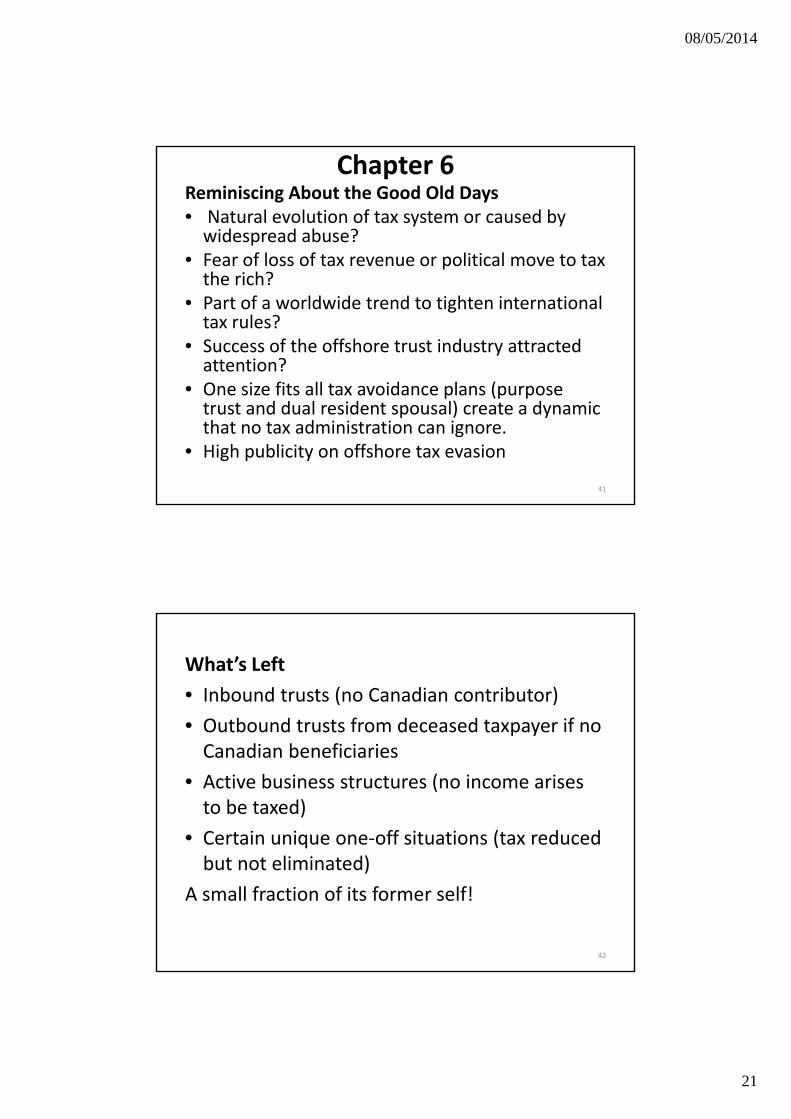

Chapter 6Reminiscing About the Good Old Days• Natural evolution of tax system or caused by widespread abuse?

• Fear of loss of tax revenue or political move to tax Fear of loss of tax revenue or political move to tax the rich?

• Part of a worldwide trend to tighten international tax rules?

• Success of the offshore trust industry attracted attention?O i fit ll t id l (• One size fits all tax avoidance plans (purpose trust and dual resident spousal) create a dynamic that no tax administration can ignore.

• High publicity on offshore tax evasion

41

What’s Left

• Inbound trusts (no Canadian contributor)

• Outbound trusts from deceased taxpayer if no Outbou d t usts o deceased ta paye oCanadian beneficiaries

• Active business structures (no income arises to be taxed)

• Certain unique one‐off situations (tax reduced but not eliminated)

A small fraction of its former self!

42

08/05/2014

22

Thank you for your attendance

Sponsored by: