Embed Size (px)

Citation preview

3/10/2010

1

Old Dominion University Hampton Roads Real Estate Market Review and Forecast

20102010

Presented by: E.V. Williams

Center for Real Estate and Economic Development John R. Broderick, President

Nancy Bagranoff, DBA; Dean, College of Business & Public Administration, Old Dominion University

Industry Professional Advisors to the Center (IPAC)

Honorary Member

Robert M. Stanton, CSM and CPM, Stanton Partners, Inc.

Jeff Ainslie, Ainslie Group

G. Robert Aston, Jr., TowneBank

Ramon W. Breeden, Jr., The Breeden Company

Sanford (Sandy) M. Cohen, Divaris Real Estate, Inc.

Michael Newsome, Clark Whitehill Enterprises, Inc.

Harrison J. Perrine, Perrine Investments

Don Perry, Continental Development

Victor L. Pickett, Grandbridge Real Estate Capital, LLC

Thomas E. Robinson, Robinson Development Group

Jim V. Rose, Rose & Womble Realty Co., LLC

Bradley R. Sanford, MAI, Dominion Realty AdvisorsCraig Cope, Liberty Property Trust

Cecil V. Cutchins, Olympia Development Corporation

Robert L. Dewey, Willcox & Savage, PC

Thomas M. Dillon, Fulton Bank

N. Joseph Dreps, BB&T

Pamela J. Faber, LeClair Ryan

Joel T. Flax, CPA, Goodman & Company

David M. Gianascoli, Gee's Group Real Estate Development

John L. Gibson, III, Ellis-Gibson Development Group

Warren Harris, City of Virginia Beach Economic Development

Aubrey L. Layne, Jr., Great Atlantic Management, LLC

Miles B. Leon, S. L. Nusbaum Realty Company

Michael W. McCabe, Harvey Lindsay Commercial Real Estate

y , , y

Burrell F. Saunders, CMSS Architects, PC

Reese Smith, Reese Smith & Associates

Tony Smith, Robinson Development Group

Deborah K. Stearns, CPM, SIOR, Harvey Lindsay Commercial Real Estate

Richard Thurmond, William E. Wood

Jon S. Wheeler, Wheeler Interests

Robert T. Williams, Tri City Developers, LLC

Rod Woolard, City of Norfolk Economic Development

Steven Wright, City of Chesapeake Economic Development

CREED CouncilJ. Scott Adams, CB Richard Ellis of Virginia, Inc.

Tom Atherton, MEB General Contractors

Jim Bradshaw, Woolpert LLP

Stewart Buckle, II, The Morgan Real Estate Group

M. Albert Carmichael, Harvey Lindsay Commercial Real Estate

W. Page Cockrell, Hurt & Proffitt

David Collier, First Atlantic Restoration

Lawrence J. Colorito, Jr., MAI, Axial Advisory Group, LLC

Hahns L. Copeland, DARVA Group LLC

Ann K. Crenshaw, Kaufman & Canoles, PC

Don Crigger, CCIM, CB Richard Ellis

Jon R. Crunkleton, Old Dominion University

Rennie Richardson, Richardson Real Estate Corporation

Maureen G. Rooks, Thalhimer/Cushman & Wakefield

Jim V. Rose, Rose & Womble Realty Company, LLC

J. Randy Royal, Kimley-Horn and Associates

Robert J. Ruhl, City of Virginia Beach Economic Development

Stephanie Sanker, S. L. Nusbaum Realty Co.

Paula J. Shendow, Wireless Capital Partners

Robert M. Sherman, III, CPM, Harrison & Lear Inc. Realtors

Kenneth Sisk, P.E., Bowman Consulting Group

Anthony W. Smith, Robinson Development Group

Dorcas T. Helfant-Browning, DTH Properties, LLC

Virginia P. Henderson, MAI, Commercial First Appraisers, LLC

Charles Hutchison, Vanasse Hangen Brustlin, Inc.

Michael A. Inman, Inman & Strickler, P.L.C.

Cherie James, Wall, Einhorn & Chernitzer, P.C.

Terry Johnson, Abbitt Realty

Mallory Kahler, City of Portsmouth Economic Development

E. Andrew Keeney, Kaufman & Canoles, P.C.

R.I. King, II, Thalhimer/Cushman & Wakefield

William E. King, SIOR, Harvey Lindsay Commerical Real Estate

Kim Curtis, Tidewater Home Funding

William G. Darden, Hearndon Construction Company

George C. Davis, West Neck Community Association

Laura B. de Graaf, Bank of America

Michael Divaris, Divaris Real Estate, Inc.

Helen Dragas, The Dragas Companies

Brian Dundon, Dundon & Associates

Frederick D. Facka, Tuckahoe Asset Management

Sandra Ferebee, GSH Residential Sales

Brian E. Gordineer, A.A.S., City of Hampton, Office of the Assessor

Howard E. Gordon, Williams Mullen

Dennis W. Gruelle, Appraisal Consultation Group

Jonathan S. Guion, SIOR, Jonathan Commercial Properties

Elizabeth O. Hancock, Office of Real Estate Assessor, City of Norfolk

Russell G. Hanson, Jr., Hanson Capital, LLC

Carl Hardee, Lawson Realty Corporation

John Harry, John C. Harry, Inc.

Anthony W. Smith, Robinson Development Group

Jeremy R. Starkey, Monarch Capital, LLC

Daniel R. Stegall, Daniel Richard Stegall, PC

Terrie L. Suit, Williams Mullen

Leo Sutton, Historic Ventures, LLC

Michael Sykes, Bank of America

Robert M. Thornton, CRE, CCIM, SIOR, Thalhimer/Cushman & Wakefield

William C. Throne, SIOR, CCIM, ALC, Thalhimer/Cushman & Wakefield

Jamie Tollenaere, Clancy & Theys Construction

Stewart Tyler, ASA, Righy of Way Acquisitions & Appraisals

George D. Vick, III, Harvey Lindsay Commercial Real Estate

Edward W. Ware, Norfolk Redevelopment & Housing

H. Mac Weaver, II, Wells Fargo Real Estate Group

Edward M. Williams, William E. Wood & Associates

F. Blair Wimbush, Norfolk Southern Corporation

Peter E. Winters, Jr., Axial Advisory Group, LLC

Chris Wood, JD & W

John Wright, Waverton Associates

Estate

April Koleszar, Koleszar Properties, Inc.

Barry M. Kornblau, Summit Realty Group, Inc.

Tyler Leinbach, Meredith Construction Company, Inc.

John R. (Jack) Lewis, II, ECS Mid-Atlantic, LLC

Harvey Lindsay, Jr., Harvey Lindsay Commercial Real Estate

Susan Long-Molnar, Managing Communications Consulting

Jeffrey R. Mack, The CIM Group

Lauren Marsh, Frye Properties

Mike Mausteller

G. Cliff Moore, Virtexco Corporation

Michael Nice, George Nice and Sons, Inc.

Thomas O'Grady, KBS, Inc.

James N. Owens, CCIM, Harvey Lindsay Commercial Real Estate

Robert L. Philips, Jr., Thalhimer/Cushman & Wakefield

Victor L. Pickett, Grandbridge Real Estate

Sandra Prestridge, City of Norfolk Economic Development

Chris Read, CB Richard Ellis

F. Craig Read, Read Commercial Properties

John C. Richards, Jr., CB Richard Ellis/Melody & Co.

Executive CommitteeExecutive Committee

Chair Brad Sanford

Director John Lombard

Program Chair Stephanie Sanker

Publications Chair Brian Dundon

Membership Chair Craig Cope

Curriculum Co‐Chairs Jon Crunkleton, Brad Sanford

Sponsorship Chair Fred Facka

By‐Laws Chair Andrew Keeney

Past Chair Tom Dillon

At‐Large Jonathan Guion

Billy King

Aubrey Layne

3/10/2010

2

Market Review CommitteeMarket Review Committee

Industrial Bill Throne and Stephanie Sanker

Office Scott Adams

Retail David Machupa and David ChapmanRetail David Machupa and David Chapman

Multi‐family Charles Dalton/Real Data

Residential Blair Hardesty and Van Rose

Investment Scott Adams

Publications Committee

Brian Dundon

Nancy Gossett

Elizabeth Hancock

Sandi Prestridge

Maureen Rooks

Brad SanfordElizabeth Hancock

Janice Hurley

Joy Learn

Brad Sanford

Lane Shea

Kristi Sutphin

Special thank you to

Inside Business

for their sponsorship

over the past seven years.

Program Moderator

Michael J. Seiler, Ph.D.Professor and

Robert M. Stanton Chair of Real Estate and Economic Development

Investment Market Review

Presented By:

J. Scott Adams, CCIMJ. Scott Adams, CCIMPresident, Mid-South Region

March 10, 2010

Investment Market Review

Trends in Property Sales (DOWN!)• Nationally• Hampton Roads

Trends in Distressed Assets (UP!)

TOPICS TO COVER

CB Richard Ellis | Page 12

The Lending Market Today (IT DEPENDS)

Commercial Real Estate as an Investment Class(A WINNER OVER THE LONG TERM)

3/10/2010

3

Trends in Property Sales Nationally

National Sales Transactions of $5 Million or Greater

$250,000,000

$300,000,000

$350,000,000

$400,000,000

$450,000,000

$500,000,000

$443.4 Billion

CB Richard Ellis | Page 13

$0

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

2007 2008 2009

$135.4 Billion

$51.1 Billion

Source: Real Capital Analytics

$600 000 000

$800,000,000

$1,000,000,000

$1,200,000,000

Local Sales Transactions of $5 Million or Greater

$602.3 Million

$1.083 Billion

Trends in Property Sales Hampton Roads

CB Richard Ellis | Page 14

$0

$200,000,000

$400,000,000

$600,000,000

2007 2008 2009

$139.5 Million

Source: CB Richard Ellis Market Research

2009 Top Local Sales Transactions: Multi-Family

Springhouse @ Newport The Townes @ Jones Run

CB Richard Ellis | Page 15

Woodshire Apartments

Harbour View East

2009 Top Local SalesTransactions: Retail

CB Richard Ellis | Page 16

London Bridge Shopping Center

2009 Top Local Sales Transactions: Retail

CB Richard Ellis | Page 17

2009 Top Local Sales Transaction: OfficeLynnwood Plaza

CB Richard Ellis | Page 18

3/10/2010

4

Trends in Distressed Assets

WHAT IS A “DISTRESSED ASSET”?

A loan default has occurred or is imminent

CB Richard Ellis | Page 19

and/or

The owner/sponsor of the asset is bankrupt or faces financial trouble

Trends in Distressed Assets

CB Richard Ellis | Page 20

The Lending Market TodayHOW IS THE LENDING MARKET TODAY?

It Depends!

1) By Property Type

Multi-Family vs. all other Property Types

2) By Asset StabilityStable Positive Cash Flow

CB Richard Ellis | Page 21

Stable Positive Cash Flow

vs.

Unstable Positive or Negative Cash Flow

3) By Investor Type (For Office and Industrial Assets)

Owner-Occupants vs. Traditional Investors

Commercial Real Estate vs. Stocks and BondsHigher Returns for real estate over a 5 and 10 year hold period

Commercial Real Estate as an Investment

CB Richard Ellis | Page 22

Source: NCREIF, Delta Associates; January 2010: for 12 month periods ending September 2009.

Commercial Real Estate as an Investment

CB Richard Ellis | Page 23

GAME PLAN FOR SUCCESSFOR SERVICE PROVIDERS

Be sensitive to the stress on real estate owners

Educate our clients with fresh, thorough information

Investment Market Review

CB Richard Ellis | Page 24

Seize every opportunity for our clients

Make a difference in our clients’ lives

3/10/2010

5

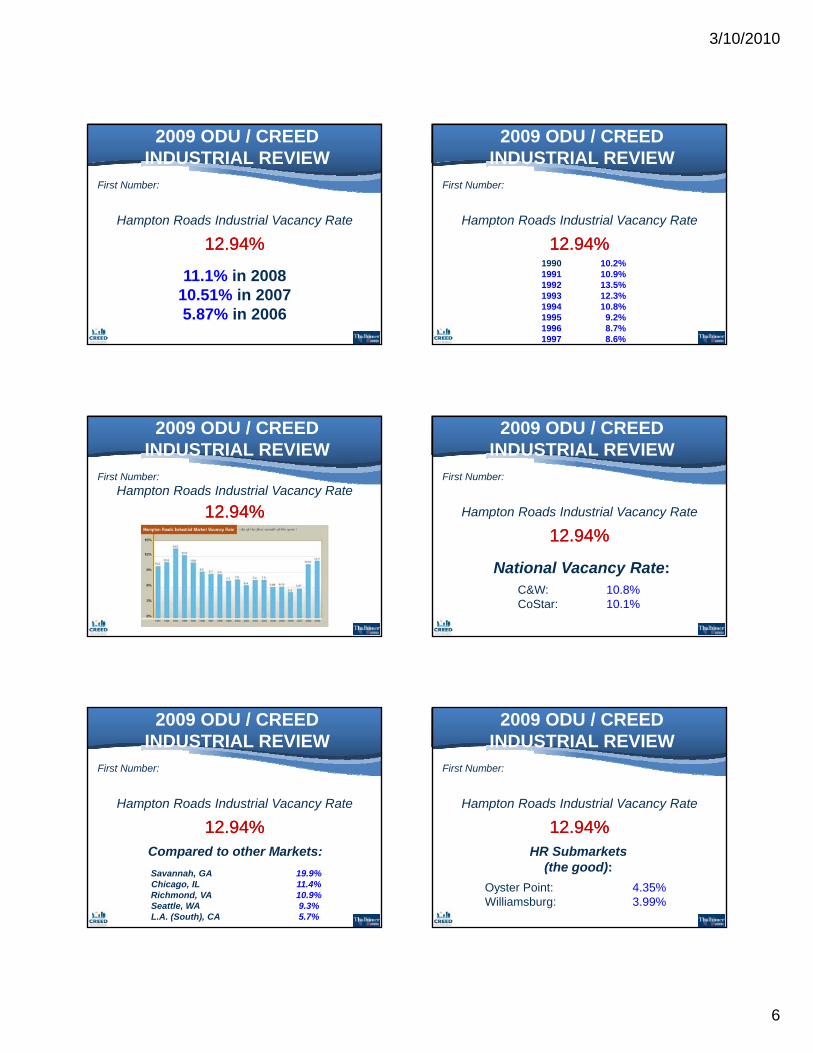

2009 ODU / CREED INDUSTRIAL REVIEW

Presented by:

William C. Throne, CCIM, SIOR, ALC

2009 ODU / CREED INDUSTRIAL REVIEW

3

NUMBERS

2009 ODU / CREED INDUSTRIAL REVIEW

12 9412 94

First Number:

12.9412.94

2009 ODU / CREED INDUSTRIAL REVIEW

Hampton Roads Industrial Vacancy Rate

First Number:

12.94%12.94%

2009 ODU / CREED INDUSTRIAL REVIEW

Hampton Roads Industrial Vacancy Rate

First Number:

87.06% occupied!

12.94%12.94%

2009 ODU / CREED INDUSTRIAL REVIEW

Hampton Roads Industrial Vacancy Rate

First Number:

11.1% in 2008

12.94%12.94%

3/10/2010

6

2009 ODU / CREED INDUSTRIAL REVIEW

Hampton Roads Industrial Vacancy Rate

First Number:

12.94%12.94%

11.1% in 200810.51% in 20075.87% in 2006

2009 ODU / CREED INDUSTRIAL REVIEW

Hampton Roads Industrial Vacancy Rate

First Number:

1990 10.2%1991 10.9%1992 13.5%1993 12.3%1994 10.8%1995 9.2%1996 8.7%1997 8.6%

12.94%12.94%

2009 ODU / CREED INDUSTRIAL REVIEW

12.94%12.94%Hampton Roads Industrial Vacancy Rate

First Number:

2009 ODU / CREED INDUSTRIAL REVIEW

Hampton Roads Industrial Vacancy Rate

First Number:

National Vacancy Rate:C&W: 10.8%CoStar: 10.1%

12.94%12.94%

2009 ODU / CREED INDUSTRIAL REVIEW

Hampton Roads Industrial Vacancy Rate

First Number:

Compared to other Markets:

Savannah, GA 19.9%Chicago, IL 11.4%Richmond, VA 10.9%Seattle, WA 9.3%L.A. (South), CA 5.7%

12.94%12.94%

2009 ODU / CREED INDUSTRIAL REVIEW

Hampton Roads Industrial Vacancy Rate

First Number:

HR Submarkets (the good):

Oyster Point: 4.35%Williamsburg: 3.99%

12.94%12.94%

3/10/2010

7

2009 ODU / CREED INDUSTRIAL REVIEW

Hampton Roads Industrial Vacancy Rate

First Number:

HR Submarkets (the good):

Peninsula: 9.49%

12.94%12.94%

2009 ODU / CREED INDUSTRIAL REVIEW

Hampton Roads Industrial Vacancy Rate

First Number:

HR Submarkets (the good):

Lowered Vacancy in 2009:

*Bainbridge *Lynnhaven *Portsmouth*Copeland *Oakland *Williamsburg

12.94%12.94%

2009 ODU / CREED INDUSTRIAL REVIEW

Hampton Roads Industrial Vacancy Rate

First Number:

HR Submarkets (the not-so-good):

Norfolk Commerce Park: 38.41%Isle of Wight: 28.45%Suffolk: 19.13%

12.94%12.94%

2009 ODU / CREED INDUSTRIAL REVIEW

44

Second Number:

44

2009 ODU / CREED INDUSTRIAL REVIEW

Rental Rate a Landlord would love to get fordistribution space

Second Number:

$4.00 NNN $4.00 NNN psfpsf/yr/yr

distribution space

2009 ODU / CREED INDUSTRIAL REVIEW

Rental Rate a Landlord would love to get fordistribution space

Second Number:

*This will remain something of a benchmark for warehouse space.

*Market rents for other subgroups will cluster around:

$4.75-$5.75 NNN for general industrial$5.50-$6.50 NNN for higher rent submarkets

$4.00 NNN $4.00 NNN psfpsf/yr/yr

distribution space

3/10/2010

8

2009 ODU / CREED INDUSTRIAL REVIEW

44

Second Number:

44

2009 ODU / CREED INDUSTRIAL REVIEW

The number of predictionsI got wrong last year:

Second Number:

44

I got wrong last year:

2009 ODU / CREED INDUSTRIAL REVIEW

The number of predictionsI got wrong last year:

Second Number:

44

I got wrong last year:

1. GVA Advantis is bullish for 2009.

2009 ODU / CREED INDUSTRIAL REVIEW

The number of predictionsI got wrong last year:

Second Number:

44

I got wrong last year:

1. GVA Advantis is bullish for 2009.2. There are two big deals about to be announced in the market.

2009 ODU / CREED INDUSTRIAL REVIEW

The number of predictionsI got wrong last year:

Second Number:

44

I got wrong last year:

1. GVA Advantis is bullish for 2009.2. There are two big deals about to be announced in the market.3. The local industrial market is healthy with a modestly successful

2009.

2009 ODU / CREED INDUSTRIAL REVIEW

The number of predictionsI got wrong last year:

Second Number:

44

I got wrong last year:

1. GVA Advantis is bullish for 2009.2. There are two big deals about to be announced in the market.3. The local industrial market is healthy with a modestly successful

2009.4. Vacancy rates are not expected to rise.

3/10/2010

9

2009 ODU / CREED INDUSTRIAL REVIEW

The number of ‘big’ deals in the market this year:

Second Number:

44

this year:

1. Virginia Beach2. Chesapeake3. Norfolk4. Suffolk

2009 ODU / CREED INDUSTRIAL REVIEW

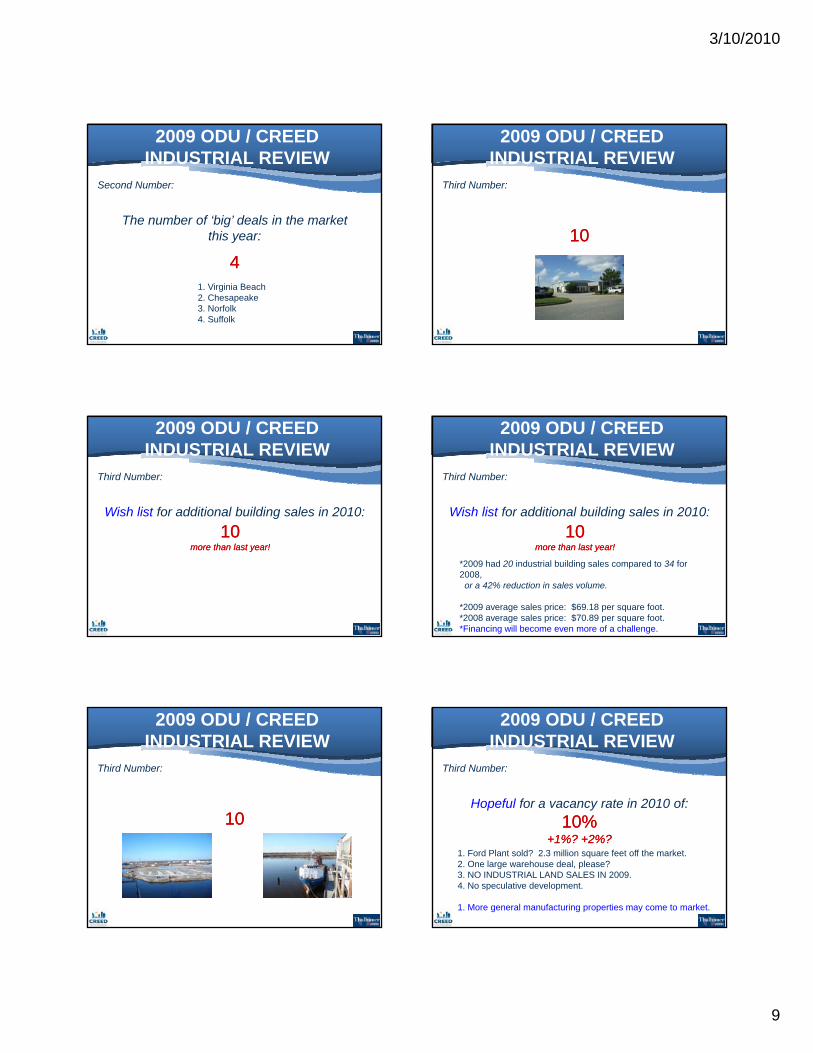

1010

Third Number:

1010

2009 ODU / CREED INDUSTRIAL REVIEW

Wish list for additional building sales in 2010:

Third Number:

101010 10 more than last year!more than last year!

2009 ODU / CREED INDUSTRIAL REVIEW

1010Wish list for additional building sales in 2010:

Third Number:

10 10 more than last year!more than last year!

*2009 had 20 industrial building sales compared to 34 for 2008,or a 42% reduction in sales volume.

*2009 average sales price: $69.18 per square foot.*2008 average sales price: $70.89 per square foot.*Financing will become even more of a challenge.

2009 ODU / CREED INDUSTRIAL REVIEW

1010

Third Number:

1010

2009 ODU / CREED INDUSTRIAL REVIEW

10%10%Hopeful for a vacancy rate in 2010 of:

Third Number:

10% 10% +1%? +2%?+1%? +2%?

1. Ford Plant sold? 2.3 million square feet off the market.2. One large warehouse deal, please?3. NO INDUSTRIAL LAND SALES IN 2009.4. No speculative development.

1. More general manufacturing properties may come to market.

3/10/2010

10

2009 ODU / CREED INDUSTRIAL REVIEW

1010

Third Number:

1010

2009 ODU / CREED INDUSTRIAL REVIEW

How can I be successful in:

Third Number:

202010?10?1. You have to search for the hard-to-find eggs…

2009 ODU / CREED INDUSTRIAL REVIEW

How can I be successful in:

Third Number:

202010?10?1. You have to search for the hard-to-find eggs…2. Get your equity piece secure.

2009 ODU / CREED INDUSTRIAL REVIEW

How can I be successful in:

Third Number:

202010?10?1. You have to search for the hard-to-find eggs…2. Get your equity piece secure.3. Treat good tenants like the partners they are.

2009 ODU / CREED INDUSTRIAL REVIEW

How can I be successful in:

Third Number:

202010?10?1. You have to search for the hard-to-find eggs…2. Get your equity piece secure.3. Treat good tenants like the partners they are.4. Stay in touch with your lenders.

2009 ODU / CREED INDUSTRIAL REVIEW

How can I be successful in:

Third Number:

202010?10?1. You have to search for the hard-to-find eggs…2. Get your equity piece secure.3. Treat good tenants like the partners they are.4. Stay in touch with your lenders.5. Keep your sense of humor.

3/10/2010

11

2009 ODU / CREED INDUSTRIAL REVIEW

How can I be successful in:

Third Number:

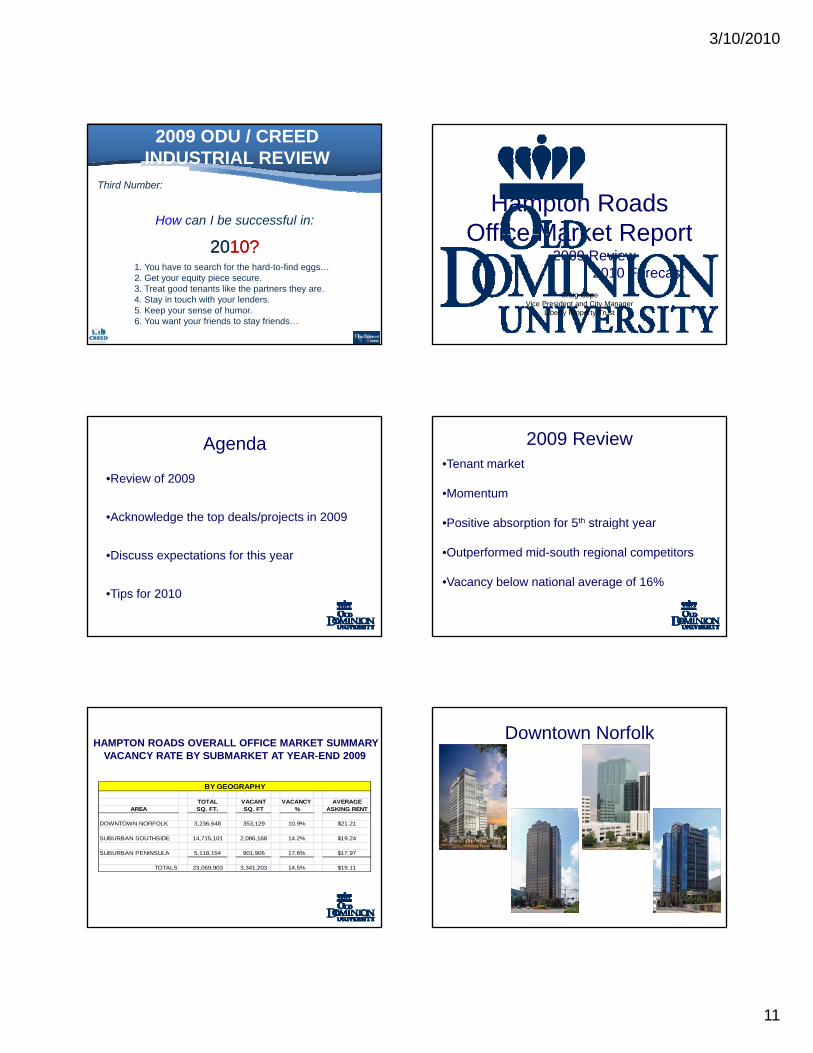

202010?10?1. You have to search for the hard-to-find eggs…2. Get your equity piece secure.3. Treat good tenants like the partners they are.4. Stay in touch with your lenders.5. Keep your sense of humor.6. You want your friends to stay friends…

Hampton Roads Office Market ReportOffice Market Report

2009 Review2010 Forecast

Craig CopeVice President and City Manager

Liberty Property Trust

•Review of 2009

•Acknowledge the top deals/projects in 2009

Agenda

•Discuss expectations for this year

•Tips for 2010

•Tenant market

•Momentum

•Positive absorption for 5th straight year

2009 Review

Positive absorption for 5 straight year

•Outperformed mid-south regional competitors

•Vacancy below national average of 16%

TOTAL VACANT VACANCY AVERAGEAREA SQ. FT. SQ. FT % ASKING RENT

BY GEOGRAPHY

HAMPTON ROADS OVERALL OFFICE MARKET SUMMARY VACANCY RATE BY SUBMARKET AT YEAR-END 2009

DOWNTOWN NORFOLK 3,236,648 353,129 10.9% $21.21

SUBURBAN SOUTHSIDE 14,715,101 2,086,168 14.2% $19.24

SUBURBAN PENINSULA 5,118,154 901,906 17.6% $17.97

TOTALS 23,069,903 3,341,203 14.5% $19.11

Downtown Norfolk

3/10/2010

12

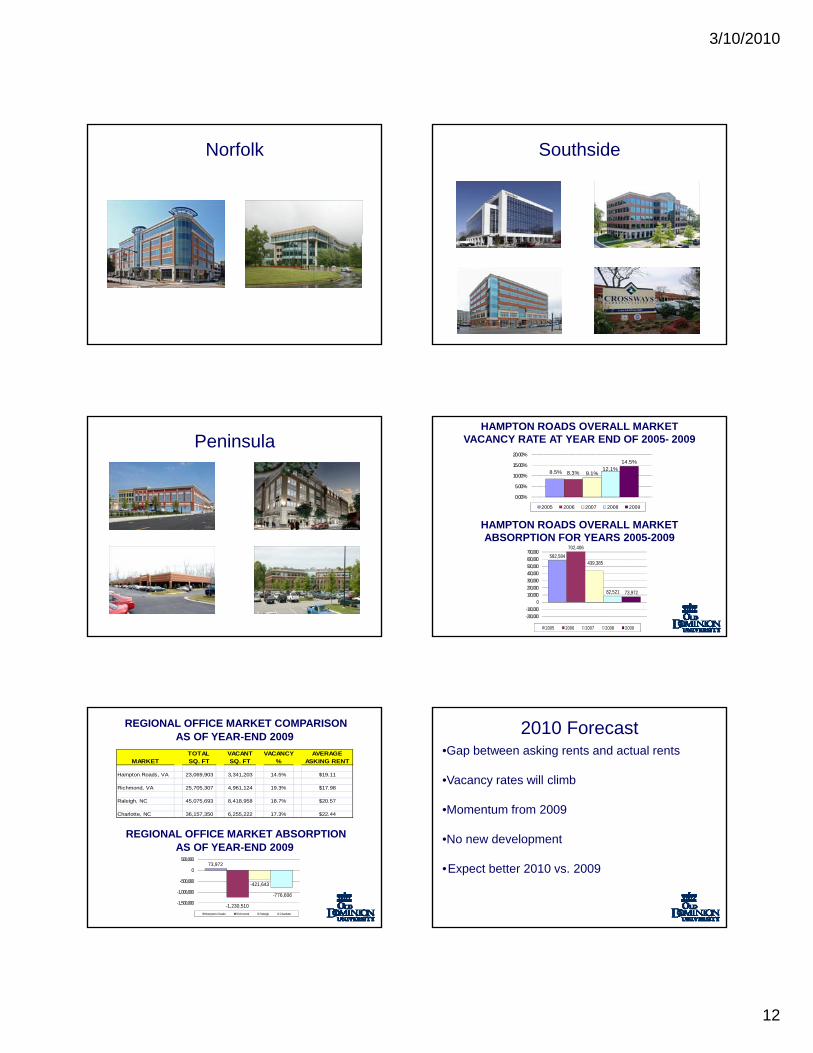

Norfolk Southside

Peninsula

8.5% 8.3% 9.1%12.1%

14.5%

0.00%

5.00%

10.00%

15.00%

20.00%

2005 2006 2007 2008 2009

HAMPTON ROADS OVERALL MARKET VACANCY RATE AT YEAR END OF 2005- 2009

HAMPTON ROADS OVERALL MARKET

582,584

702,406

439,385

82,521 73,972

-200,000-100,000

0100,000200,000300,000400,000500,000600,000700,000

2005 2006 2007 2008 2009

HAMPTON ROADS OVERALL MARKET ABSORPTION FOR YEARS 2005-2009

TOTAL VACANT VACANCY AVERAGEMARKET SQ. FT SQ. FT % ASKING RENT

Hampton Roads, VA 23,069,903 3,341,203 14.5% $19.11

Richmond, VA 25,705,307 4,961,124 19.3% $17.98

Raleigh, NC 45,075,693 8,418,958 18.7% $20.57

Charlotte, NC 36,157,350 6,255,222 17.3% $22.44

REGIONAL OFFICE MARKET COMPARISONAS OF YEAR-END 2009

REGIONAL OFFICE MARKET ABSORPTIONAS OF YEAR-END 2009

73,972

-1,230,510

-421,643

-776,606

-1,500,000

-1,000,000

-500,000

0

500,000

Hampton Roads Richmond Raleigh Charlotte

2010 Forecast•Gap between asking rents and actual rents

•Vacancy rates will climb

•Momentum from 2009

•No new development

•Expect better 2010 vs. 2009

3/10/2010

13

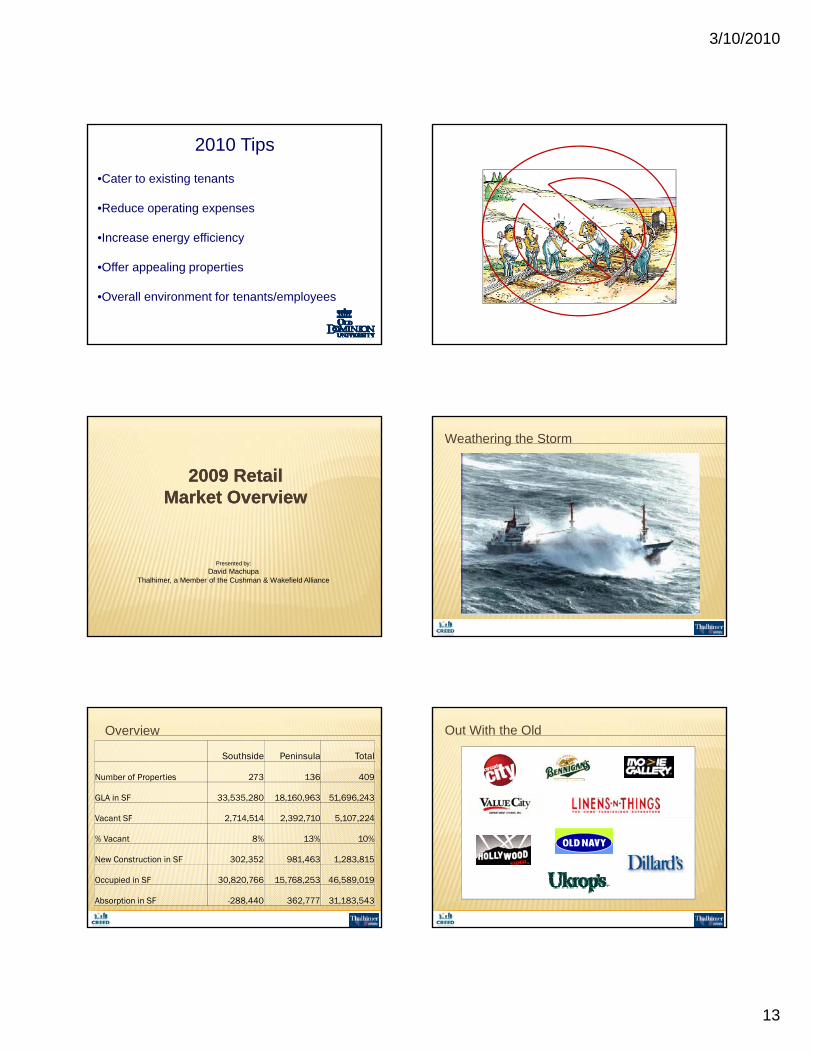

2010 Tips

•Cater to existing tenants

•Reduce operating expenses

I ffi i•Increase energy efficiency

•Offer appealing properties

•Overall environment for tenants/employees

2009 Retail 2009 Retail Market OverviewMarket Overview

Presented by:

David MachupaThalhimer, a Member of the Cushman & Wakefield Alliance

Weathering the Storm

Overview

Southside Peninsula Total

Number of Properties 273 136 409

GLA in SF 33,535,280 18,160,963 51,696,243

Vacant SF 2 714 514 2 392 710 5 107 224Vacant SF 2,714,514 2,392,710 5,107,224

% Vacant 8% 13% 10%

New Construction in SF 302,352 981,463 1,283,815

Occupied in SF 30,820,766 15,768,253 46,589,019

Absorption in SF -288,440 362,777 31,183,543

Out With the Old

3/10/2010

14

Harbour View Marketplace In With the New

Six and Counting Peninsula Towne Center

Peninsula Towne Center Pub Time

3/10/2010

15

Presented By:

William H. HalprinSenior Vice President

Director of Operations, Multifamily Property ManagementS.L. Nusbaum Realty Co.

Stronger demand and a slower pace of construction improvedthe region’s average vacancy rate to 6.9%

During the 4th quarter of 2009, just 463 new units werecompleted and 813 units absorbed in the Hampton Roadsmarket.

There were 1,753 units under construction and an additional1,522 units proposed.

Based on the development pipeline, vacancy rates will movecloser to 8% in 2010.

Average rents are expected to remain flat.

3/10/2010

16

MSOffice1

Slide 91

MSOffice1 Susan Childress, 2/17/2010

3/10/2010

17

RESIDENTIALRESIDENTIALMARKET UPDATEMARKET UPDATE

20102010Van Rose, MIRMVan Rose, MIRM

President, Rose and President, Rose and WombleWomble New HomesNew Homes

2005 2007

200915 Year Closing15 Year Closing

New Construction & Resale HistoryNew Construction & Resale History

20,000

25,000

30,000

4,000

5,000

6,000

Source:

0

5,000

10,000

15,000

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

0

1,000

2,000

3,000

Existing Homes New Construction

3/10/2010

18

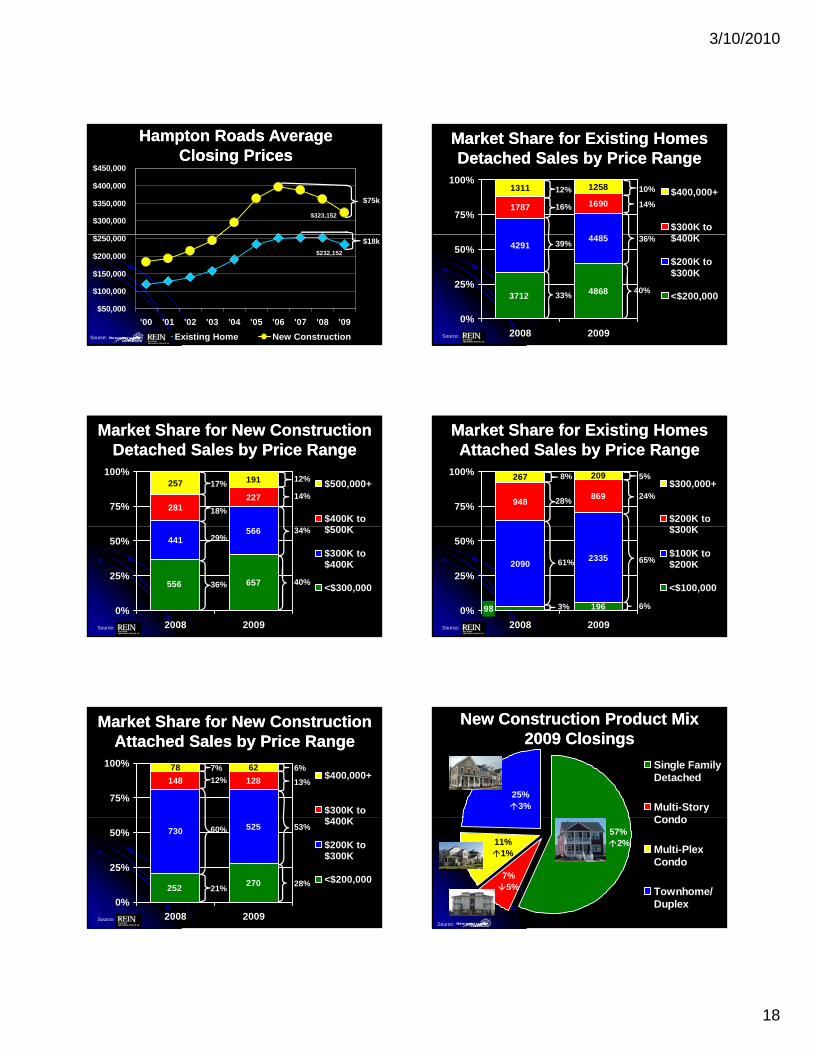

$323,152 $300,000

$350,000

$400,000

$450,000

Hampton Roads Average Hampton Roads Average Closing PricesClosing Prices

$75k

$232,152

$50,000

$100,000

$150,000

$200,000

$250,000

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09

Existing Home New ConstructionSource:

$18k

Market Share for Existing Homes Market Share for Existing Homes Detached Sales by Price RangeDetached Sales by Price Range

1787 1690

1311 1258

75%

100%$400,000+

$300K to$400K

16%

12% 10%

14%

Source:

4868

42914485

3712

0%

25%

50%

2008 2009

$400K

$200K to$300K

<$200,00033%

39%36%

40%

Market Share for New Construction Market Share for New Construction Detached Sales by Price RangeDetached Sales by Price Range

281227

257 191

75%

100%$500,000+

$400K to$500K

18%

17%12%

14%

Source:

657

441566

556

0%

25%

50%

2008 2009

$500K

$300K to$400K

<$300,00036%

29%34%

40%

Market Share for Existing Homes Market Share for Existing Homes Attached Sales by Price RangeAttached Sales by Price Range

948869

267 209

75%

100%$300,000+

$200K to$300K

28%

8% 5%

24%

Source:

196

20902335

980%

25%

50%

2008 2009

$300K

$100K to$200K

<$100,000

3%

61% 65%

6%

Market Share for New Construction Market Share for New Construction Attached Sales by Price RangeAttached Sales by Price Range

148 128

78 62

75%

100%$400,000+

$300K to$400K

12%

7% 6%

13%

Source:

270

730 525

252

0%

25%

50%

2008 2009

$400K

$200K to$300K

<$200,00021%

60% 53%

28%

New Construction Product MixNew Construction Product Mix2009 Closings2009 Closings

25%3%

Single FamilyDetached

Multi-StoryCondo

Source:

57% 2%

7%5%

11% 1%

Condo

Multi-PlexCondo

Townhome/Duplex

3/10/2010

19

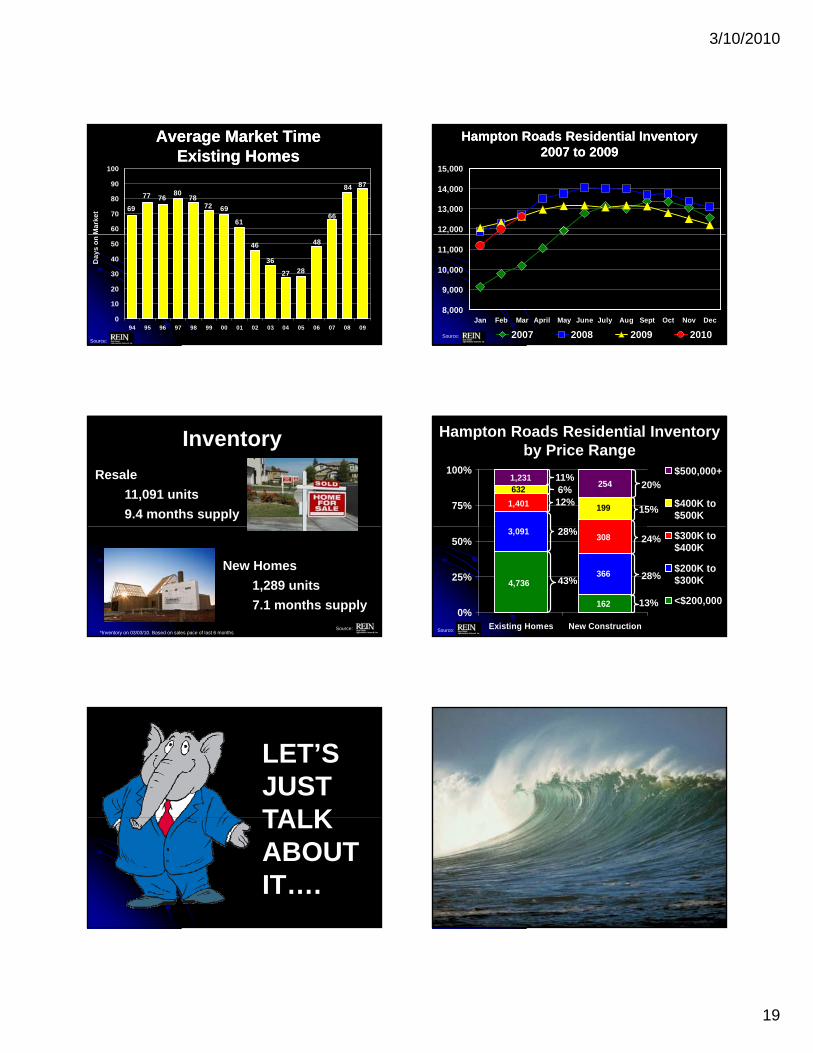

Average Market Time Average Market Time Existing HomesExisting Homes

87

69

77 7680

7872 69

6166

84

60

70

80

90

100

Ma

rke

t

Source:

46

36

27 28

48

0

10

20

30

40

50

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Da

ys

on

12,000

13,000

14,000

15,000

Hampton Roads Residential InventoryHampton Roads Residential Inventory2007 to 20092007 to 2009

Source:

8,000

9,000

10,000

11,000

Jan Feb Mar April May June July Aug Sept Oct Nov Dec

2007 2008 2009 2010

Resale

11,091 units

9.4 months supply

Inventory

New Homes

1,289 units

7.1 months supply

Source: *Inventory on 03/03/10. Based on sales pace of last 6 months

Hampton Roads Residential Inventory by Price Range

1,231254

1,401

632

19975%

100% $500,000+

$400K to$500K

12%

11%20%

15%

6%

Source:

4,736

162

3,091

366

308

0%

25%

50%

Existing Homes New Construction

$300K to$400K

$200K to$300K

<$200,000

43%

28%24%

13%

28%

LET’S JUST TALKTALK ABOUT IT….

3/10/2010

20

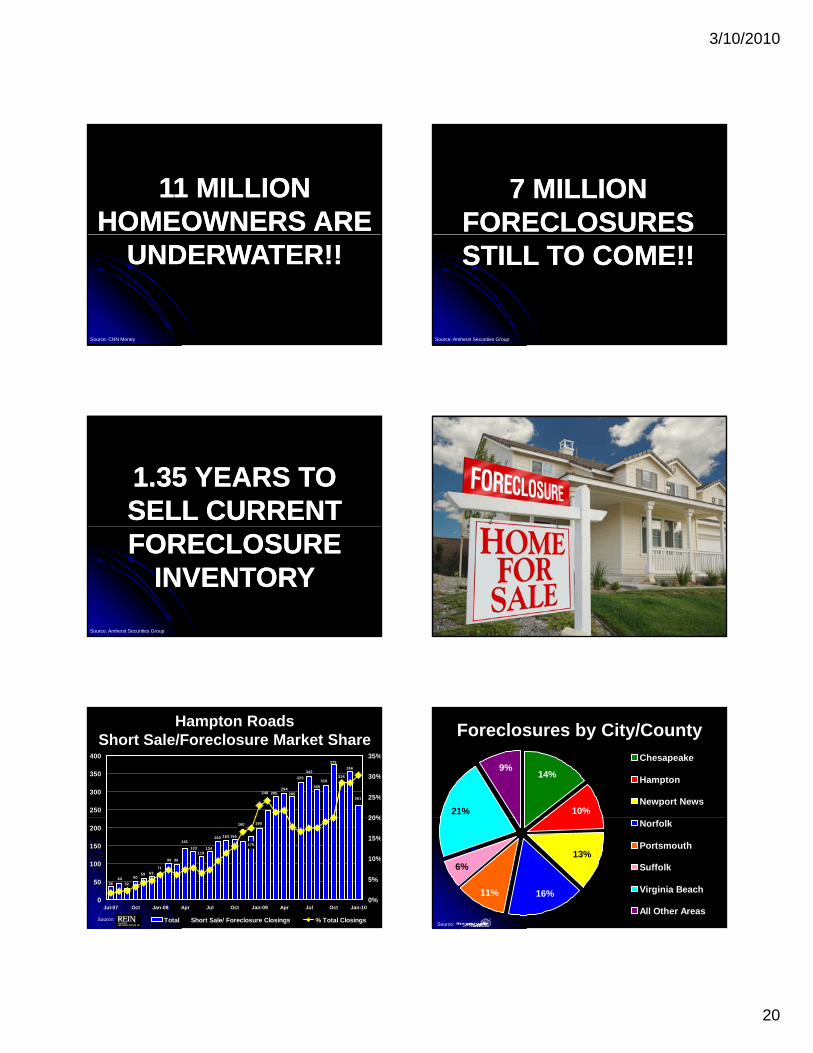

11 MILLION 11 MILLION HOMEOWNERS ARE HOMEOWNERS ARE

UNDERWATER!!UNDERWATER!!

Source: CNN Money

7 MILLION 7 MILLION FORECLOSURES FORECLOSURES STILL TO COME!!STILL TO COME!!

Source: Amherst Securities Group

1.35 YEARS TO 1.35 YEARS TO SELL CURRENT SELL CURRENT FORECLOSURE FORECLOSURE

INVENTORYINVENTORY

Source: Amherst Securities Group

294

342

261

356

326

375

318

305

325

285285248

250

300

350

400

20%

25%

30%

35%

Hampton Roads Short Sale/Foreclosure Market Share

Source:

3644

32

5059 63

71

99 96

141

133119

134

160 163 166

160

176

198

0

50

100

150

200

Jul-07 Oct Jan-08 Apr Jul Oct Jan-09 Apr Jul Oct Jan-100%

5%

10%

15%

20%

Total Short Sale/ Foreclosure Closings % Total Closings

Foreclosures by City/County

21%

9%14%

10%

Chesapeake

Hampton

Newport News

Source:

16%11%

6%13%

Norfolk

Portsmouth

Suffolk

Virginia Beach

All Other Areas

3/10/2010

21

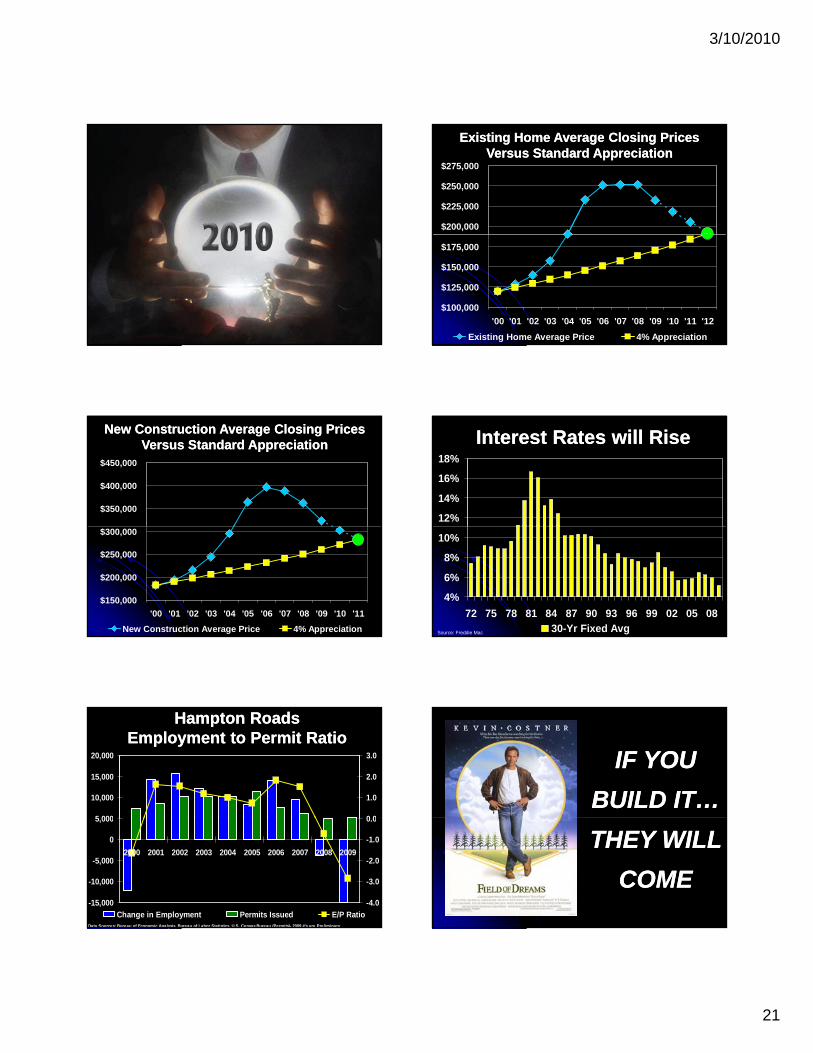

$200,000

$225,000

$250,000

$275,000

Existing Home Average Closing PricesExisting Home Average Closing PricesVersus Standard AppreciationVersus Standard Appreciation

$100,000

$125,000

$150,000

$175,000

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

Existing Home Average Price 4% Appreciation

$350,000

$400,000

$450,000

New Construction Average Closing PricesNew Construction Average Closing PricesVersus Standard AppreciationVersus Standard Appreciation

$150,000

$200,000

$250,000

$300,000

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

New Construction Average Price 4% Appreciation

12%

14%

16%

18%

Interest Rates will RiseInterest Rates will Rise

4%

6%

8%

10%

72 75 78 81 84 87 90 93 96 99 02 05 0830-Yr Fixed AvgSource: Freddie Mac

Hampton Roads Hampton Roads Employment to Permit RatioEmployment to Permit Ratio

5 000

10,000

15,000

20,000

0 0

1.0

2.0

3.0

-15,000

-10,000

-5,000

0

5,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

-4.0

-3.0

-2.0

-1.0

0.0

Change in Employment Permits Issued E/P RatioData Sources: Bureau of Economic Analysis, Bureau of Labor Statistics U.S. Census Bureau (Permits)- 2009 #'s are Preliminary

IF YOU IF YOU

BUILD IT…BUILD IT…

THEY WILL THEY WILL

COMECOME

3/10/2010

22

33

$368,048

# 5

45

$237,438

# 4 Riverwalk Townes

46

$252,617

# 3

62

$382,456

# 2

83

$180,506

# 1

92

$208,695

3/10/2010

23

AND THEAND THE

Hampton Roads

Top 5 Builders

WINNERS WINNERS

ARE……..ARE……..

Source:

# 5

93

# 4

98

# 3

133

# 2

154

# 1

233

3/10/2010

24

Closing

Bradley R. Sanford, MAI

Ch i E ti C ittChair, Executive Committee

E. V. Williams Center for

Real Estate and Economic Development

CREED Membership

Interested???

Please send a note of interest to thePlease send a note of interest to the Membership Chair, Craig Cope ([email protected])

Old Dominion University Hampton Roads Real Estate

Thank you for attending!Thank you for attending!

Please Join Us for the ReceptionPlease Join Us for the Reception

pMarket Review and Forecast

Presented by: E.V. Williams

Center for Real Estate and Economic Development

![Shehabi - OPTIMAL AEROELASTIC VEHICLE SENSOR PLACEMENT FOR ROOT MIGRATION FLIGHT CONTROL APPLICATIONS [Old dominion univ. 2001] Arabic V](https://img.pdfslide.tips/doc/110x75/58ceeaa11a28ab333d8b5ceb/shehabi-optimal-aeroelastic-vehicle-sensor-placement-for-root-migration-flight.jpg)