Embed Size (px)

Citation preview

PENGUMUMAN

Equity Research PT Jasuindo Tiga Perkasa Tbk. (JTPE) (Tercatat Di Papan : Pengembangan) No.Peng-ER-00022/BEI.PPJ/09-2012

(dapat dilihat di laman: http://www.idx.co.id) PT Bursa Efek Indonesia pada tanggal 11 September 2012 telah menerima surat melalui email dari PT Pemeringkat Efek Indonesia dengan No. 1489/PEF-DIR/IX/2012 tanggal 10 September 2012 mengenai Publikasi Laporan Penilaian Target Harga Referensi Saham PT Jasuindo Tiga Perkasa Tbk. sebagaimana terlampir (22 lembar). Demikian untuk diketahui.

11 September 2012

Umi Kulsum Andre P.J. Toelle Kepala Divisi Penilaian Perusahaan Sektor Jasa Kepala Divisi Perdagangan Saham Tembusan: 1. Yth. Ketua Badan Pengawas Pasar Modal dan LK; 2. Yth. Kepala Biro Transaksi dan Lembaga Efek Bapepam dan LK; 3. Yth. Kepala Biro PKP Sektor Jasa Bapepam dan LK; 4. Yth. Direktur Indonesian Capital Market Electronic Library; 5. Yth. Pengurus Pusat Referensi Pasar Modal; 6. Yth. Direktur Indonesian Capital Market Electronic Library; 7. Yth. Direksi PT Jasuindo Tiga Perkasa Tbk.

psu_JTPE_er_20120911_22

PEFINDO CREDIT RATING INDONESIA

1489/PEF-DIR/IX/2012

Jakarta, 10 September 2012

Kepada Yth.1. PT Jasuindo Tiga Perkasa, Tbk

JI. Raya Betro No. 21, SedatiSidoarjo 61253Jawa Timur

u.p. Bapak Lukito Budiman, Direktur

2. PT Bursa Efek IndonesiaGedung Bursa Efek IndonesiaJI. Jend. Sudirman Kav 52-53Jakarta Selatan, 12190

u.p. Bapak Ito Warsito, Direktur UtamaBapak Hoesen, Direktur Penilaian Perusahaan

Perihal: Publikasi Laporan Penilaian Target Harga Referensi Saham PT Jasuindo TigaPerkasa Tbk.

Dengan hormat,

Sehubungan dengan penugasan yang kami peroleh untuk melakukan Penilaian Target HargaReferensi Saham, dengan ini kami sampaikan hasil penilaian kami atas saham PT Jasuindo TigaPerkasa Tbk (JTPE) dalam versi Bahasa Indonesia dan Bahasa Inggris.

Apabila masih ada hal-hal yang memerlukan penjelasan lebih lanjut, mohon agar menghubungi kami.Atas perhatian dan kerjasamanya, kami ucapkan terima kasih.

Hormat kami,

.~

SaIY~Direktur

Y e Rizalirektur

Tembusan: Bapak I Gede Nyoman Yetna, Kepala Divisi Pencatatan Sektor Riil, PT Bursa EfekIndonesia

/ms

-,

Halaman 1 dari 11

Kontak: Equity & Index Valuation Division Phone: (6221) 7278 2380 [email protected]

“Pernyataan disclaimer pada halaman akhir

merupakan bagian yang tidak terpisahkan dari

dokumen ini”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk Laporan Kedua

Equity Valuation

10 September 2012

Target Harga

Terendah Tertinggi 790 870

Dokumen Niaga

Kinerja Saham

0

50

100

150

200

250

300

350

400

450

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

Sep-11 Nov-11 Jan-12 Mar-12 May-12 Jul-12

JTPEIHSG

IHSG JTPE Sumber: Bloomberg

Informasi Saham Rp

Kode Saham JTPE

Harga Saham Per 7 September 2012 385

Harga Tertinggi 52 minggu terakhir 420

Harga Terendah 52 minggu terakhir 197

Kapitalisasi Pasar Tertinggi 52 minggu (miliar) 743

Kapitalisasi Pasar Terendah 52 minggu (miliar) 349

Penilaian Saham Sebelumnya Saat ini

Tertinggi 850 870

Terendah 770 790

Market Value Added & Market Risk

00

00

00

00

00

01

01

01

01

01

01

00

50

100

150

200

250

300

350

1H11 1H12

MVA Market risk

Sumber:Bloomberg, Pefindo Divisi Valuasi Saham & Indexing

Pemegang Saham

(%)

PT Jasuindo Multi Investama 65,67

Tn. Yongky Wijaya 4,38

Nyonya Oei, Melinda Poerwanto 2,19

Tn. Oei, Allan Wibisono 0,73

Publik (masing-masing dibawah 5% kepemilikan)

27,03

Memperluas Jalan untuk Pertumbuhan yang Lebih

Tinggi

v

PT Jasuindo Tiga Perkasa Tbk ("JTPE") adalah perusahaan yang bergerak di bidang dokumen niaga terintegerasi, yang mencakup Security Document, Non-Security Document dan Document Management. Beberapa produk JTPE antara lain: STNK, BPKB, cek, KTP, polis asuransi, faktur, voucher. Didirikan pada tanggal 10 Juli 1991 dan berdomisili di Sidoarjo, Jawa Timur. Saat ini, JTPE dianggap sebagai salah satu pemain utama dalam industri ini, didukung oleh keanggotaannya di Global

Printing Network, di mana satu negara diwakili oleh satu perusahaan

percetakan dokumen niaga. Dalam menjalani usahanya, JTPE memiliki beberapa segmen pelanggan, yaitu pemerintah, bank, manufaktur, maskapai penerbangan dan lain-lain. Selain mencetak Security Document, tahun ini, JTPE juga meluncurkan produk baru yaitu smart card. Sejak tahun lalu, JTPE sudah mendapat lisensi dari Visa dan MasterCard untuk memproduksi bank card (kartu kredit). Berkat kinerja

yang luar biasa, JTPE dianugerahi oleh majalah Forbes sebagai Asia 200 Best Under a Billion pada bulan Juli 2012. Mengingat penjualan kendaraan di Indonesia yang terus meningkat, pertumbuhan positif dari sektor perbankan, membuat kami percaya bahwa JTPE memiliki kesempatan yang luas untuk menikmati pertumbuhan yang lebih tinggi di tahun-tahun mendatang.

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

10 September 2012 Halaman 2 dari 11

Penyesuaian Target Harga Saham

Kami melakukan beberapa penyesuaian terhadap proyeksi kami sebelumnya dan menyesuaikan target harga saham JTPE menjadi pada kisaran Rp 790 – Rp 870 per saham, berdasarkan pertimbangan-pertimbangan berikut:

Mengingat sekitar 46% dari pendapatan JTPE di 1H12 berasal dari pencetakan STNK dan BPKB dan mengacu pada pertumbuhan yang stabil dari penjualan mobil serta sepeda motor di Indonesia yang tumbuh masing-masing sebesar 17% YoY dan 9 YoY%, membuat kami percaya bahwa pendapatan JTPE dapat meningkat sebesar 10% YoY, atau sekitar Rp 560 miliar di FY2012.

Kinerja penjualan JTPE di tahun 2011 berada di atas target kami

sebelumnya. JTPE mencatat pendapatan sebesar Rp 507 miliar, sedangkan proyeksi kami sebesar Rp 501 miliar. Meningkatnya penjualan yang memiliki margin lebih tinggi seperti security document

adalah penyebab utama bahwa kinerja baik JTPE.

Kemudian pada 1H12, JTPE juga mampu membukukan hasil menggembirakan dalam hal efisiensi, seperti yang digambarkan oleh

melonjaknya margin profitabilitas. Marjin laba kotor, operasi dan bersih mencapai 31%, 14% dan 10% di 1H12, lebih baik dari pada periode yang sama tahun lalu yang sebesar 27%, 12% dan 9%.

Asumsi risk free rate, equity premium dan beta masing-masing adalah sebesar 6,0%, 6,3% dan 0,9x.

Melonjaknya Pemegang Kartu Kredit Diharapkan Mendongkrak

Pendapatan Smart Card JTPE telah meluncurkan produk barunya yaitu smart card. Smart card umumnya berukuran seperti kartu identitas (ID card) dan berisi chip yang dapat memberikan informasi dari pemegang kartu menjadi data yang lengkap. Penggunaan smart card adalah untuk kartu kredit, ID card dan kartu akses. Saat ini, JTPE sudah memegang lisensi dari Visa dan

MasterCard untuk menghasilkan bank card (kartu kredit). Hingga Juli

2012, rata-rata transaksi kartu kredit mencapai Rp 17,5 triliun. Transaksi yang tinggi tersebut disertai oleh pemegang kartu kredit yang meningkat di Indonesia. Pada FY2012, pemegang kartu kredit diperkirakan meningkat 10% YoY atau sekitar 15 juta, mengingat ada acara besar antara lain Idul Fitri, Hari Natal dan perayaan Tahun Baru di 3Q12 dan 4Q12. Seiring dengan itu, kami memperkirakan pendapatan dari divisi

smart card bisa mencapai Rp 28 miliar pada tahun 2012.

Prospek Usaha Didukung oleh pertumbuhan positif perekonomian Indonesia yang diperkirakan mencapai 6,2% YoY pada tahun 2012, inflasi terkendali sekitar 4,5% YoY dan pendapatan per kapita yang bisa melebihi USD 4.000 pada tahun 2012, kami percaya bahwa prospek industri percetakan

seperti JTPE akan tetap prospektif. Kondisi tersebut akan menguntungkan JTPE karena beberapa industri yang dilayani seperti perbankan,

manufaktur dan otomotif tumbuh positif. Selain itu, kami melihat bahwa ketidakpastian ekonomi global tidak akan menghambat kinerja JTPE karena seluruh produk yang dijual ke pasar dalam negeri. Berdasarkan pertimbangan di atas, kami percaya JTPE mampu mencetak pendapatan Rp 560 miliar pada 2012, mencerminkan pertumbuhan 10% YoY.

PARAMETER INVESTASI

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

10 September 2012 Halaman 3 dari 11

Tabel 1: Ringkasan Kinerja

2009 2010 2011 2012P 2013P

Penjualan [Rp Miliar] 271 446 507 560 620

Laba sebelum pajak [Rp miliar]

36 101 106 118 131

Laba bersih [Rp miliar] 25 76 80 90 100

EPS [Rp] 14 43 45 51 57

Pertumbuhan EPS [%] 2,2 2,0 0,1 0,1 0,1

P/E [x] 7,1 5,4 6,7 7,6* 6,8*

PBV [x] 2,0 2,7 3,4 2,5* 2 ,4* Sumber: PT Jasuindo Tiga Perkasa Tbk ., Estimasi Pefindo Divisi Valuasi Saham & Indexing Catatan: * Berdasarkan Harga Saham JTPE per 7 September 2012 – Rp 385/lembar *Asumsi Stok Split 1:5 terjadi pada 31 Desember 2008

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

10 September 2012 Halaman 4 dari 11

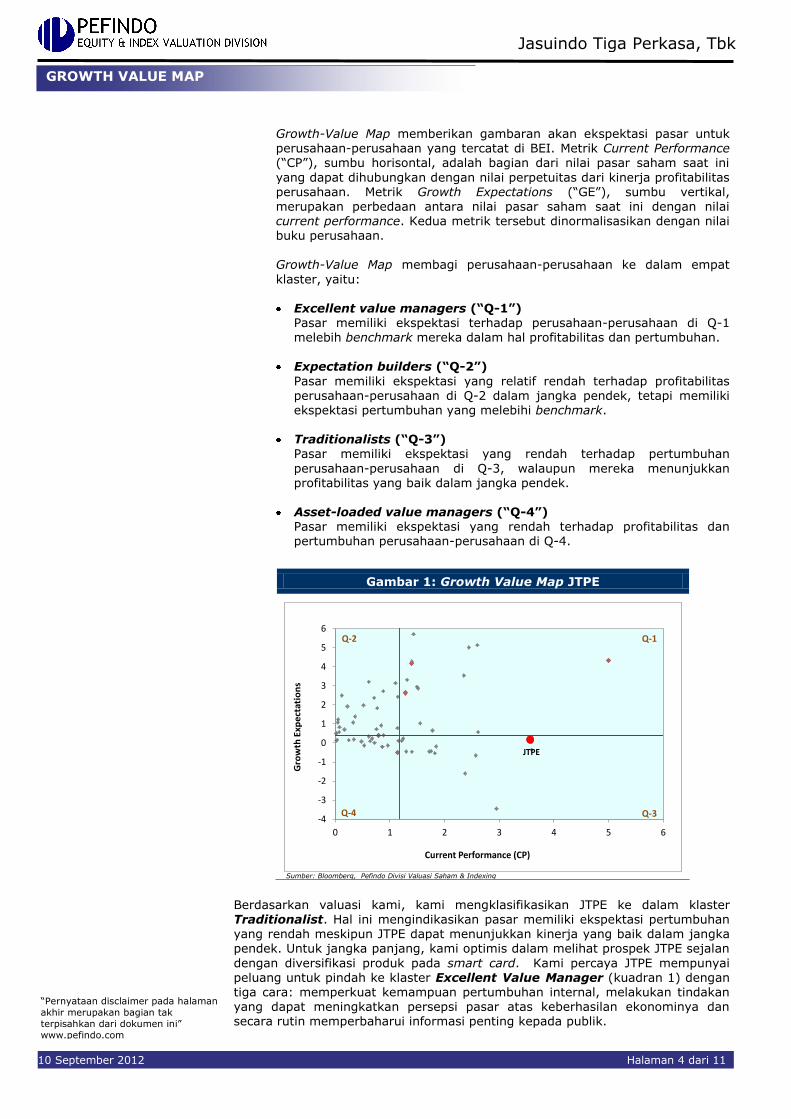

Growth-Value Map memberikan gambaran akan ekspektasi pasar untuk perusahaan-perusahaan yang tercatat di BEI. Metrik Current Performance (“CP”), sumbu horisontal, adalah bagian dari nilai pasar saham saat ini

yang dapat dihubungkan dengan nilai perpetuitas dari kinerja profitabilitas perusahaan. Metrik Growth Expectations (“GE”), sumbu vertikal, merupakan perbedaan antara nilai pasar saham saat ini dengan nilai current performance. Kedua metrik tersebut dinormalisasikan dengan nilai buku perusahaan. Growth-Value Map membagi perusahaan-perusahaan ke dalam empat

klaster, yaitu:

Excellent value managers (“Q-1”) Pasar memiliki ekspektasi terhadap perusahaan-perusahaan di Q-1 melebih benchmark mereka dalam hal profitabilitas dan pertumbuhan.

Expectation builders (“Q-2”)

Pasar memiliki ekspektasi yang relatif rendah terhadap profitabilitas perusahaan-perusahaan di Q-2 dalam jangka pendek, tetapi memiliki ekspektasi pertumbuhan yang melebihi benchmark.

Traditionalists (“Q-3”)

Pasar memiliki ekspektasi yang rendah terhadap pertumbuhan

perusahaan-perusahaan di Q-3, walaupun mereka menunjukkan profitabilitas yang baik dalam jangka pendek.

Asset-loaded value managers (“Q-4”)

Pasar memiliki ekspektasi yang rendah terhadap profitabilitas dan pertumbuhan perusahaan-perusahaan di Q-4.

Berdasarkan valuasi kami, kami mengklasifikasikan JTPE ke dalam klaster Traditionalist. Hal ini mengindikasikan pasar memiliki ekspektasi pertumbuhan yang rendah meskipun JTPE dapat menunjukkan kinerja yang baik dalam jangka pendek. Untuk jangka panjang, kami optimis dalam melihat prospek JTPE sejalan

dengan diversifikasi produk pada smart card. Kami percaya JTPE mempunyai peluang untuk pindah ke klaster Excellent Value Manager (kuadran 1) dengan tiga cara: memperkuat kemampuan pertumbuhan internal, melakukan tindakan yang dapat meningkatkan persepsi pasar atas keberhasilan ekonominya dan secara rutin memperbaharui informasi penting kepada publik.

Gambar 1: Growth Value Map JTPE

-4

-3

-2

-1

0

1

2

3

4

5

6

0 1 2 3 4 5 6

Gro

wth

Exp

ect

atio

ns

Current Performance (CP)

JTPE

Q-1

Q-3

Q-2

Q-4

Sumber: Bloomberg, Pefindo Divisi Valuasi Saham & Indexing

GROWTH VALUE MAP

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

10 September 2012 Halaman 5 dari 11

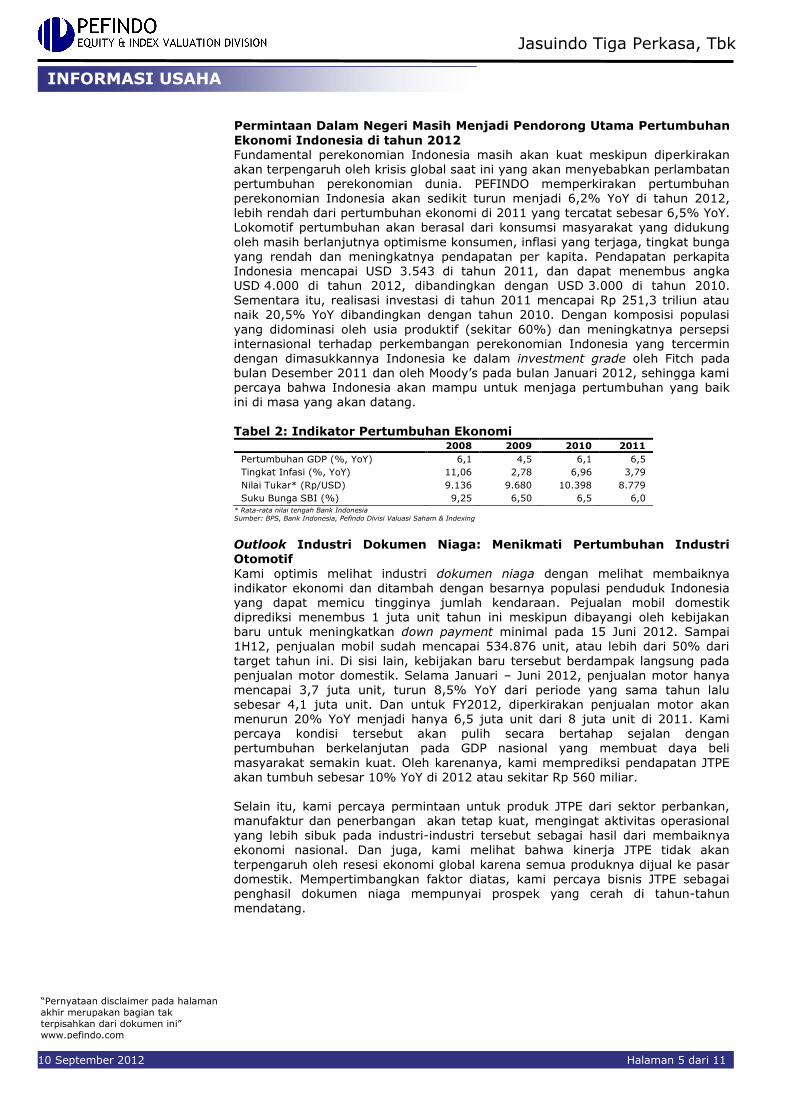

Permintaan Dalam Negeri Masih Menjadi Pendorong Utama Pertumbuhan

Ekonomi Indonesia di tahun 2012 Fundamental perekonomian Indonesia masih akan kuat meskipun diperkirakan akan terpengaruh oleh krisis global saat ini yang akan menyebabkan perlambatan pertumbuhan perekonomian dunia. PEFINDO memperkirakan pertumbuhan perekonomian Indonesia akan sedikit turun menjadi 6,2% YoY di tahun 2012, lebih rendah dari pertumbuhan ekonomi di 2011 yang tercatat sebesar 6,5% YoY. Lokomotif pertumbuhan akan berasal dari konsumsi masyarakat yang didukung

oleh masih berlanjutnya optimisme konsumen, inflasi yang terjaga, tingkat bunga yang rendah dan meningkatnya pendapatan per kapita. Pendapatan perkapita Indonesia mencapai USD 3.543 di tahun 2011, dan dapat menembus angka USD 4.000 di tahun 2012, dibandingkan dengan USD 3.000 di tahun 2010. Sementara itu, realisasi investasi di tahun 2011 mencapai Rp 251,3 triliun atau naik 20,5% YoY dibandingkan dengan tahun 2010. Dengan komposisi populasi

yang didominasi oleh usia produktif (sekitar 60%) dan meningkatnya persepsi internasional terhadap perkembangan perekonomian Indonesia yang tercermin

dengan dimasukkannya Indonesia ke dalam investment grade oleh Fitch pada bulan Desember 2011 dan oleh Moody’s pada bulan Januari 2012, sehingga kami percaya bahwa Indonesia akan mampu untuk menjaga pertumbuhan yang baik ini di masa yang akan datang.

Tabel 2: Indikator Pertumbuhan Ekonomi 2008 2009 2010 2011

Pertumbuhan GDP (%, YoY)

Tingkat Infasi (%, YoY)

Nilai Tukar* (Rp/USD)

Suku Bunga SBI (%)

6,1

11,06

9.136

9,25

4,5

2,78

9.680

6,50

6,1

6,96

10.398

6,5

6,5

3,79

8.779

6,0 * Rata-rata nilai tengah Bank Indonesia Sumber: BPS, Bank Indonesia, Pefindo Divisi Valuasi Saham & Indexing

Outlook Industri Dokumen Niaga: Menikmati Pertumbuhan Industri Otomotif

Kami optimis melihat industri dokumen niaga dengan melihat membaiknya indikator ekonomi dan ditambah dengan besarnya populasi penduduk Indonesia

yang dapat memicu tingginya jumlah kendaraan. Pejualan mobil domestik diprediksi menembus 1 juta unit tahun ini meskipun dibayangi oleh kebijakan baru untuk meningkatkan down payment minimal pada 15 Juni 2012. Sampai 1H12, penjualan mobil sudah mencapai 534.876 unit, atau lebih dari 50% dari

target tahun ini. Di sisi lain, kebijakan baru tersebut berdampak langsung pada penjualan motor domestik. Selama Januari – Juni 2012, penjualan motor hanya mencapai 3,7 juta unit, turun 8,5% YoY dari periode yang sama tahun lalu sebesar 4,1 juta unit. Dan untuk FY2012, diperkirakan penjualan motor akan menurun 20% YoY menjadi hanya 6,5 juta unit dari 8 juta unit di 2011. Kami percaya kondisi tersebut akan pulih secara bertahap sejalan dengan pertumbuhan berkelanjutan pada GDP nasional yang membuat daya beli

masyarakat semakin kuat. Oleh karenanya, kami memprediksi pendapatan JTPE akan tumbuh sebesar 10% YoY di 2012 atau sekitar Rp 560 miliar. Selain itu, kami percaya permintaan untuk produk JTPE dari sektor perbankan, manufaktur dan penerbangan akan tetap kuat, mengingat aktivitas operasional yang lebih sibuk pada industri-industri tersebut sebagai hasil dari membaiknya

ekonomi nasional. Dan juga, kami melihat bahwa kinerja JTPE tidak akan

terpengaruh oleh resesi ekonomi global karena semua produknya dijual ke pasar domestik. Mempertimbangkan faktor diatas, kami percaya bisnis JTPE sebagai penghasil dokumen niaga mempunyai prospek yang cerah di tahun-tahun mendatang.

INFORMASI USAHA

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

10 September 2012 Halaman 6 dari 11

Gambar 2: Pendapatan JTPE dan Penjualan Kendaraan di Indonesia

271

446

507

560

0

100

200

300

400

500

600

2009 2010 2011 2012P

da

lam

Rp

mil

iar

Pendapatan JTPE

486.088,00

764.710,00

894.164,00 950.000,00

0

2.000.000

4.000.000

6.000.000

8.000.000

0

200.000

400.000

600.000

800.000

1.000.000

2009 2010 2011 2012P

da

lam

un

it

da

lam

un

it

Penjualan Mobil Penjualan Motor

Sumber: PT Jasuindo Tiga Perkasa Tbk., dan berbagai sumber diolah oleh Pefindo Divisi Valuasi Saham & Indexing

Terpercaya karena Memiliki Lisensi

Pada 1996, JTPE medapat lisensi dari Badan Pemberantasan Uang Palsu. Kemudian di 1997, JTPE mulai memproduksi produk security document. Saat ini, terdapat sekitar 36 perusahaan yang bergerak di industri ini, sementara hanya 8 (termasuk JTPE) yang mempunyai lisensi dari Bank Indonesia untuk mencetak

cek, polis asuransi dan deposito. Dan berkat memegang lisensi tersebut, JTPE dipercaya oleh pemerintah untuk mencetak security document seperti STNK dan BPKB serta kartu identitas. Sampai saat ini, sektor pemerintah mempunyai kontribusi terbesar terhadap total pendapatan JTPE. Selain Badan Pemberantasan Uang Palsu dan Bank Indonesia, JTPE juga telah mengantongi lisensi dari Visa dan MasterCard untuk memproduksi kartu untuk bank (kartu kredit). Di 2011,

JTPE telah mengalokasikan sekitar Rp 720 juta untuk lisensi tersebut dan kami mengharapkan pendapatan dari divisi smart card dapat mencapai Rp 28 miliar di 2012.

Menyediakan Produk yang Beragam dan Berkualitas Untuk melayani permintaan yang beragam dari pelanggannya, JTPE menyediakan produk yang beragam dan terintegerasi yaitu Security Document, Non-Security

Document dan Document Management. Produk-produk yang termasuk dalam produk Security Document antara lain: cek, kartu identitas, polis asuransi, doumen negara. Sementara Non-Security Document seperti: faktur, EDC slip, direct mail, voucher dan billing statement. Dalam hal volume penjualan, Security Document mempunyai andil terbesar atau setara 86% dari 385.754 kotak di 2011. Dan di 2012, kami memperkirakan volume penjualan dari Security Document dapat tumbuh 10% YoY atau sekitar 426.200 kotak. Di sisi lain, kami

percaya pada kualitas produk-produk JTPE karena diawasi langsung oleh Institusi Pemerintah.

Gambar 3: Beberapa Produk JTPE

Sumber: PT Jasuindo Tiga Perkasa Tbk., Pefindo Divisi Valuasi Saham & Indexing

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

10 September 2012 Halaman 7 dari 11

Efisiensi Membuat Marjin Lebih Tinggi

Selama 1H12, JTPE mencatat penurunan pertumbuhan penjualan sebesar 27% YoY atau setara dengan Rp 106 miliar. Hal ini terutama karena penjualan ke pemerintah, kontributor utama pendapatan JTPE, turun 44% YoY di periode itu menjadi Rp 49 miliar dari Rp 88 miliar di 1H11. Meskipun menghadapi penurunan penjualan, JTPE dapat menunjukkan efisiensinya pada HPP yang kemudian meningkatkan marjin profitabilitasnya. Marjin laba kotor, laba operasi dan laba bersih JTPE mencapai 31%, 14% dan 10% di 1H12, lebih baik dari periode yang

sama tahun lalu yaitu masing-masing 27%, 12% dan 9%. Kami percaya JTPE akan tetap dapat membukukan pertumbuhan positif di FY12 mengingat pertumbuhan pada penjualan kendaraan dan sebagian besar order pemerintah datang di 3Q dan 4Q.

Gambar 4: Marjin Laba Kotor, Laba Operasi dan Laba Bersih JTPE

26%

34%32%

27%

31%

14%

23%21%

12%14%

9%

17% 16%

9% 10%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2009 2010 2011 1H11 1H12

Marjin Laba Kotor Marjin Laba Operasi Marjin Laba Bersih

Sumber: PT Jasuindo Tiga Perkasa Tbk., Pefindo Divisi Valuasi Saham & Indexing

Pemegang Kartu Kredit Terus Meningkat Berdasarkan data dari Bank Indonesia, pemegang kartu kredit tetap tumbuh

dalam 5 tahun terakhir. Di 2008, pemegang kartu kredit sejumlah 11,5 juta. Di 2009, tumbuh 6% YoY mencapai 12,2 juta. Sementara di 2010 dn 2011 naik

sebesar 11% YoY dan 9% YoY atau masing-masing mencapai 13,5 juta dan 14,7 juta. Meskipun terdapat peraturan baru dari Bank Indonesia untuk membatasi jumlah kartu kredit, akan tetapi, kami percaya lebih tingginya pendapatan masyarakat Indonesia dan konsumsi domestik yang kuat dapat memicu pertumbuhan positif sektor perbankan terutama kartu kredit. Untuk 2012, kami memperkirakan pemegang kartu kredit akan bertambah 10% YoY atau sekitar 15 juta.

Gambar 5: Jumlah Pemegang Kartu Kredit di Indonesia

11,512,2

13,5

14,7 15

0

2

4

6

8

10

12

14

16

2008 2009 2010 2011 2012P

da

lam

ju

ta

Pemegang Kartu Kredit

Sumber: Berbagai sumber diolah oleh Pefindo Divisi Valuasi Saham & Indexing

KEUANGAN

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

10 September 2012 Halaman 8 dari 11

Prospek Usaha JTPE Didukung oleh pertumbuhan positif perekonomian Indonesia yang diperkirakan mencapai 6,2% YoY pada tahun 2012, inflasi dikelola sekitar 4,5% YoY dan

pendapatan per kapita yang bisa melebihi USD 4.000 pada tahun 2012, kami

percaya bahwa prospek industri percetakan seperti JTPE akan tetap prospektif. Kondisi tersebut akan menguntungkan JTPE karena beberapa industri yang dilayani seperti perbankan, manufaktur dan otomotif tumbuh positif. Selain itu, kami melihat bahwa ketidakpastian ekonomi global tidak akan menghambat kinerja JTPE karena seluruh produk yang dijual ke pasar dalam negeri. Berdasarkan pertimbangan di atas, kami percaya JTPE mampu mencetak pendapatan Rp 560 miliar pada 2012, mencerminkan pertumbuhan 10% YoY.

.

Gambar 6: Estimasi Pendapatan JTPE

0

100

200

300

400

500

600

700

800

2012P 2013P 2014P 2015P 2016P

560620

679716 756

da

lam

Rp

mil

iar

Pendapatan JTPE

Sumber: PT Jasuindo Tiga Perkasa Tbk., Pefindo Divisi Valuasi Saham & Indexing

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

10 September 2012 Halaman 9 dari 11

VALUASI

Metodologi

Kami mengaplikasikan metode discounted cash flow (DCF) sebagai metode penilaian utama dengan pertimbangan bahwa pertumbuhan pendapatan adalah merupakan faktor yang sangat mempengaruhi nilai (value driver) bagi JTPE jika dibandingkan dengan pertumbuhan aset.

Kami tidak mengkombinasikan perhitungan DCF ini dengan metode Guideline

Company Method (GCM) di dalam valuasi ini, disebabkan tidak terdapat peers yang benar-benar dapat diperbandingkan dengan JTPE di Bursa Efek Indonesia.

Penilaian ini berdasarkan pada nilai 100% saham JTPE per 7 September 2012, menggunakan laporan keuangan JTPE per 30 Juni 2012 sebagai dasar dilakukannya analisa fundamental.

Estimasi Nilai

Kami menggunakan Cost of Capital sebesar 10,7% dan Cost of Equity sebesar 11,5% berdasarkan asumsi-asumsi berikut:

Tabel 3: Asumsi

Risk free rate [%]* 6,0 Risk premium [%]* 6,3

Beta [x]* 0,9 Cost of Equity [%] 11,5 Marginal tax rate [%] 25,0 Debt to Equity Ratio [x] 0,34 WACC [%] 10,7

Sumber: Bloomberg, Estimasi Pefindo Divisi Valuasi Saham & Indexing *Catatan: Per 7 September 2012

Estimasi target harga saham untuk 12 bulan berdasarkan posisi penilaian

pada tanggal 7 September 2012, dengan menggunakan metode DCF dan asumsi tingkat diskonto 10,7%, adalah sebesar Rp 790 hingga Rp 870 per saham.

Tabel 4: Ringkasan Penilaian dengan Metode DCF

Konservatif Moderat Agresif

PV of Free Cash Flows [Rp miliar] 370 390 409 PV Terminal Value [Rp miliar] 1.074 1.131 1.187 Non-Operating Asset [Rp miliar] 10 10 10 Net Debt [Rp miliar] (66) (66) (66) Total Equity Value [Rp miliar] 1.388 1.464 1.540 Number of Share [juta saham] 1.770 1.770 1.770 Fair Value per Share [Rp] 790 830 870

Sumber: Estimasi Pefindo Divisi Valuasi Saham & Indexing

TARGET HARGA

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

10 September 2012 Halaman 10 dari 11

Tabel 5: Laporan Laba Rugi Komprehensif

Konsolidasian

[dalam Rp Miliar] 2009 2010 2011 2012P 2013P

Penjualan 271 446 507 560 620

Harga Pokok Penjualan (199) (295) (344) (379) (419)

Laba Kotor 72 151 163 181 201

Beban Operasi (34) (48) (56) (62) (68)

Laba Operasi 38 103 107 119 133

Pendapatan [Beban] lain-lain (2) (2) (1) (1) (2)

Laba Sebelum Pajak 36 101 106 118 131

Pajak (12) (25) (26) (28) (31)

Laba Bersih 25 76 80 90 100

Sumber: PT Jasuindo Tiga Perkasa Tbk, Estimasi Pefindo Divisi Valuasi Saham & Indexing

Tabel 6: Laporan Posisi Keuangan Konsolidasian

[dalam Rp Miliar] 2009 2010 2011 2012P 2013P

Aset

Aset Lancar

Kas dan Setara Kas 44 79 83 97 89

Piutang Usaha 31 16 16 39 44

Persediaan 12 8 15 23 25

Aset lain-lain 10 28 52 64 71

Total Aset Lancar 97 131 166 223 229

Aset Tetap 63 104 145 185 201

Aset lainnya 1 1 2 2 2

Total Aset 161 236 313 410 432

Kewajiban

Hutang Usaha 24 25 76 79 87

Hutang Jk, Pendek 27 2 5 13 14

Hutang Jk, Pendek

lainnya 18 30 30 33 37

Hutang Jk, Panjang 4 25 17 10 5

Total Kewajiban 73 82 128 135 143

Total Ekuitas 88 154 185 275 289

Sumber: PT Jasuindo Tiga Perkasa Tbk, Estimasi Pefindo Divisi Valuasi Saham & Indexing

Gambar 7: P/E dan P/BV Historis

0,00

0,50

1,00

1,50

2,00

2,50

3,00

3,50

4,00

0,00

1,00

2,00

3,00

4,00

5,00

6,00

7,00

8,00

2009 2010 2011

P/BVP/E

P/E

P/BV

Gambar 8: ROA, ROE dan TAT Historis

01

02

02

02

02

02

02

02

02

02

02

00

10

20

30

40

50

60

2009 2010 2011

TATROA & ROE

ROA

ROE

TAT

Tabel 7: Rasio Penting

Rasio 2009 2010 2011 2012P 2013P

Pertumbuhan [%]

Penjualan 69,9 64,6 13,8 10,4 10,8

Laba Operasi 171,0 173,7 4,5 10,8 11,9

EBITDA 135,5 154,5 9,4 9,1 11,7

Laba Bersih 215,9 197,9 5,5 12,6 11,8

Profitabilitas [%]

Marjin Laba Kotor 26,5 33,8 32,2 32,2 32,5

Marjin Laba Operasi 13,8 23,0 21,1 21,2 21,4

Marjin EBITDA 15,9 24,6 23,7 23,4 23,6

Marjin Laba Bersih 9,4 16,9 15,7 16,0 16,2

ROA 15,8 32,0 25,6 21,9 23,2

ROE 28,7 49,1 43,0 32,6 34,6

Solvabilitas [X]

Rasio Kewajiban Terhadap Ekuitas 0,8 0,5 0,7 0,5 0,5

Rasio KewajibanTerhadap Aset 0,4 0,3 0,4 0,3 0,3

Likuiditas[X]

Rasio Lancar 1,4 2,3 1,5 1,8 1,7

Rasio Cepat 1,1 1,7 0,9 1,1 1,0

Sumber: PT Jasuindo Tiga Perkasa Tbk, Estimasi Pefindo Divisi Valuasi Saham & Indexing

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

10 September 2012 Halaman 11 dari 11

DISCLAIMER

Laporan ini dibuat berdasarkan sumber-sumber yang kami anggap terpercaya dan dapat diandalkan, Namun kami tidak menjamin kelengkapan, keakuratan atau kecukupannya , Dengan demikian kami tidak bertanggung jawab atas segala keputusan investasi yang diambil berdasarkan laporan ini, Adapun asumsi, opini, dan perkiraan merupakan hasil dari pertimbangan internal kami per tanggal penilaian (cut-off date), dan kami dapat mengubah pertimbangan diatas sewaktu-waktu tanpa pemberitahuan terlebih dahulu.

Kami tidak bertanggung jawab atas kekeliruan atau kelalaian yang terjadi akibat penggunaan laporan ini, Kinerja dimasa lalu tidak selalu dapat dijadikan acuan hasil masa depan , Laporan ini bukan merupakan rekomendasi penawaran, pembelian atau menahan suatu saham tertentu, Laporan ini mungkin tidak sesuai untuk beberapa investor, Seluruh opini dalam laporan ini telah disampaikan dengan itikad baik, namun sewaktu-waktu dapat berubah tanpa pemberitahuan terlebih dahulu, dan disajikan dengan benar per tanggal diterbitkan laporan ini , Harga, nilai,

atau pendapatan dari setiap saham Perseroan yang disajikan dalam laporan ini kemungkinan dapat lebih rendah dari harapan pemodal, dan pemodal juga mungkin mendapatkan

pengembalian yang lebih rendah dari nilai investasi yang ditanamkan, Investasi didefinisikan sebagai pendapatan yang kemungkinan besar diterima dimasa depan, namun nilai dari pendapatan yang akan diterima tersebut kemungkinan besar juga akan berfluktuasi , Untuk saham Perseroan yang penyajian laporan keuangannya didenominasi dalam mata uang selain Rupiah, perubahan nilai tukar mata uang tersebut kemungkinan dapat menurunkan nilai, harga,

atau pendapatan investasi pemodal, Informasi dalam laporan ini bukan merupakan pertimbangan pajak dalam mengambil suatu keputusan investasi . Target harga saham dalam Laporan ini merupakan nilai fundamental, bukan merupakan Nilai Pasar Wajar, dan bukan merupakan harga acuan transaksi yang diwajibkan oleh peraturan perundang-undangan yang berlaku.

Laporan target harga saham yang diterbitkan oleh Pefindo Divisi Valuasi Saham dan Indexing bukan merupakan rekomendasi untuk membeli, menjual, atau menahan suatu saham tertentu, dan tidak dapat dianggap sebagai nasehat investasi oleh Pefindo Divisi Valuasi Saham dan Indexing yang behubungan dengan cakupan Jasa Pefindo kepada, atau kaitannya kepada, beberapa pihak, termasuk emiten, penasehat keuangan, pialang saham, investment banks,

institusi keuangan dan perantara keuangan, dalam kaitannya menerima imbalan atau

keuntungan lainnya dari pihak tersebut. Laporan ini tidak ditujukan untuk pemodal tertentu dan tidak dapat dijadikan bagian dari tujuan investasi terhadap suatu saham dan juga bukan merupakan rekomendasi investasi terhadap suatu saham tertentu atau suatu strategi investasi, Sebelum melakukan tindakan dari hasil laporan ini, pemodal disarankan untuk mempertimbangkan terlebih dahulu kesesuaian situasi dan kondisi dan, jika dibutuhkan, mintalah bantuan penasehat keuangan.

PEFINDO memisahkan kegiatan Valuasi Saham dengan kegiatan Pemeringkatan untuk menjaga independensi dan objektivitas dari proses dan produk kegiatan analitis , PEFINDO telah menetapkan kebijakan dan prosedur untuk menjaga kerahasiaan informasi non-publik tertentu yang diterima sehubungan dengan proses analitis, Keseluruhan proses, metodologi dan database yang digunakan dalam penyusunan Laporan Target Harga Referensi Saham ini secara

keseluruhan adalah berbeda dengan proses, metodologi dan database yang digunakan PEFINDO dalam melakukan pemeringkatan.

Laporan ini dibuat dan disiapkan Pefindo Divisi Valuasi Saham & Indexing dengan tujuan untuk meningkatkan transparansi harga saham yang tercatat di Bursa Efek Indonesia , Laporan ini juga bebas dari pengaruh tekanan atau paksaan dari Bursa maupun Perseroan yang dinilai, Pefindo Divisi Valuasi Saham & Indexing akan menerima imbalan sebesar Rp. 20.000.000,-

masing-masing dari Bursa Efek Indonesia dan Perseroan yang dinilai untuk 2 (dua) kali pelaporan per tahun, Untuk keterangan lebih lanjut, dapat mengunjungi website kami di http://www,pefindo,com Laporan ini dibuat dan disiapkan oleh Pefindo Divisi Valuasi Saham dan Indexing , Di Indonesia Laporan ini dipublikasikan pada website kami dan juga pada website Bursa Efek Indonesia.

Page 1 of 10

Contact: Equity & Index Valuation Division Phone: (6221) 7278 2380 [email protected]

“Disclaimer statement in the last page is an

integral part of this report”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk Secondary Report

Equity Valuation

September 10th, 2012

Target Price

Low High 790 870

Security Document

Historical Chart

0

50

100

150

200

250

300

350

400

450

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

Sep-11 Nov-11 Jan-12 Mar-12 May-12 Jul-12

JTPEJCI

JCI JTPE Source: Bloomberg

Stock Information Rp

Ticker code JTPE

Market price as of September 7th 2012 385

Market price – 52 week high 420

Market price – 52 week low 197

Market cap – 52 week high (bn) 743

Market cap – 52 week low (bn) 349

Stock Valuation Last Current

High 850 870

Low 770 790

Market Value Added & Market Risk

00

00

00

00

00

01

01

01

01

01

01

00

50

100

150

200

250

300

350

1H11 1H12

MVA Market risk

Source: Bloomberg, Pefindo Equity & Index Valuation Division

Shareholders (%)

PT Jasuindo Multi Investama 65.67

Tn. Yongky Wijaya 4.38

Nyonya Oei, Melinda Poerwanto 2.19

Tn. Oei, Allan Wibisono 0.73

Public (each below 5% ownership) 27.03

Broadening Ways for Higher Growth

PT Jasuindo Tiga Perkasa Tbk (“JTPE”) is a company that engages in integrated commercial documents, namely Security Document, Non-Security Document and Document Management. Some of JTPE’s products are vehicle registration certificate and proof of vehicle ownership (STNK and BPKB), check, ID card, insurance policy, invoice, and voucher. It was established on July 10th, 1991 and domiciled in Sidoarjo, East Java. Currently, JTPE is considered as one of the main players in this industry,

underpinned by its membership in Global Printing Network, in which one

country is represented by one security printing company. In doing its business, JTPE has several customer segments, namely government, bank, manufacture, airline and others. Besides printing security documents, this year, JTPE also launched new product namely smart card. Since last year, JTPE already got license from Visa and MasterCard to produce bank card (credit card). Thanks to its superb performance,

JTPE was awarded by Forbes magazine as Asia 200 Best Under a Billion in July 2012. Considering the vehicle sales in Indonesia which continues to rise, positive growth of banking sector, thus makes us believe that JTPE has wide opportunity to enjoy higher growth in the years ahead.

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

September 10th, 2012 Page 2 of 10

Target Price Adjustment We made some adjustments to our previous forecast and adjust our Target Price to the range of Rp 790 - Rp 870 per share, based on the following

considerations:

Due to around 46% of JTPE’s revenue in 1H12 came from printing of vehicle registration certificate and proof of vehicle ownership (STNK and BPKB) and referring to steady growth of car sales as well as motorcycle in Indonesia which grew by 17% YoY and 9% YoY, respectively, makes us believe that

JTPE’s revenue could soar by 10% YoY, or around Rp 560 billion in FY2012. JTPE’s sales performance in 2011 was above our previous target. JTPE

recorded revenue of Rp 507 billion, while our projection was Rp 501 billion. Increasing sales of higher margin products such as security document was the main cause of that JTPE’s great performance.

Later in 1H12, JTPE was also able to book encouraging result in term of efficiency, as depicted by soaring profitability margins. Gross, operating and

net margin reached 31%, 14% and 10% in 1H12, better than in the same period last year which was 27%, 12% and 9%, respectively.

Assumption of risk free rate, equity premium and beta reach 6.0%, 6.3% and 0.9x, respectively.

Soaring of Credit Card Holder is expected to Boost Smart Card Revenue JTPE has launched its new product namely smart card. Smart card is generally

sized like identity card (ID card) and contains of chip which can proceed the information of card holder to become complete data. The usage of smart card are for credit card, ID card and access card. Currently, JTPE has already hold the licence from Visa and MasterCard to produce the bank card (credit card). Up to July 2012, the average transaction of credit card reached Rp 17.5 trillion. Such high transaction is accompanied by the increasing of credit card holder in

Indonesia. In FY2012, the credit card holder is predicted to increase by 10% YoY or around 15 million, citing there are several big events such as Eid al-Fitr, Christmas Day and New Year celebration in 3Q12 and 4Q12. Along with that, we

estimate the revenue from smart card division could reach Rp 28 billion in 2012. Business Prospects Supported by positive growth of Indonesian economy which is predicted to hit

6.2% YoY in 2012, manageable inflation at around 4.5% YoY and income per capita that may break over USD 4,000 in 2012, we believe that outlook for printing industry such as JTPE will remain prospective. Such conditions will much benefit JTPE since some industries that being served such as banking, manufacture and automotive grows positively. Besides that, we view that the global economic uncertainty will not hamper JTPE’s performance since its entire products are sold to domestic market. Based on above consideration, we believe

JTPE is able to record Rp 560 billion of revenue in 2012, or reflecting 10% YoY growth.

Table 1: Performance Summary

2009 2010 2011 2012P 2013P

Revenue (Rp bn) 271 446 507 560 620

Pre-tax Profit (Rp bn) 36 101 106 118 131

Net Profit (Rp bn) 25 76 80 90 100

EPS (Rp) 14 43 45 51 57

EPS Growth (%) 2.2 2.0 0.1 0.1 0.1

P/E (x) 7.1 5.4 6.7 7.6* 6.8*

PBV (x) 2.0 2.7 3.4 2.5* 2 .4* Source: PT Jasuindo Tiga Perkasa Tbk ., Pefindo Equity and Index Valuation Division Estimates Notes: * Based on Share Price as of September 7

th, 2012 – Rp 385/share

*Assumed Stock Split 1:5 occurred as of December 31st, 2008

INVESTMENT PARAMETERS

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

September 10th, 2012 Page 3 of 10

Growth-Value Map provides overview of market expectations for the companies

listed on IDX. Current Performance (“CP”) metric, running along the horizontal axis, is a portion of current stock market value that can be linked to the perpetuity of current company’s performance in profitability. Growth Expectations (“GE”) metric, plotted on the vertical axis, is the difference between current stock market value and the value of current performance. Both metrics are normalized by the company’s book value.

Growth-Value Map divides companies into four clusters, they are:

Excellent Value Managers (“Q-1”) Market expects companies in Q-1 to surpass their benchmark in profitability and growth.

Expectation Builders (“Q-2”) Market has relatively low expectations of profitability from companies in Q-2 in the short term, but has growth expectations exceed the benchmark.

Traditionalists (“Q-3”)

Market has low growth expectations of companies in the Q-3, although they showed a good profitability in the short term.

Asset-loaded Value Managers (“Q-4”) Market has low expectations in terms of profitability and growth for companies in Q-4.

Figure 1: Growth-Value Map of JTPE

-4

-3

-2

-1

0

1

2

3

4

5

6

0 1 2 3 4 5 6

Gro

wth

Exp

ect

atio

ns

Current Performance (CP)

JTPE

Q-1

Q-3

Q-2

Q-4

Source: Bloomberg, Pefindo Equity & Index Valuation Division

Based on our valuation, we classify JTPE in Traditionalist cluster. It indicates market has low growth expectation although JTPE’s is able to show good

performance in short term. And in long term, we are positive to view JTPE’s prospect in line with its product diversification on as smart card. We believe JTPE has opportunity to move to Excellent Value Managers’ cluster (quadrant 1) by

three ways: strengthen their internal growth capabilities, doing actions to drive market perceptions of their economic success and regularly update their significant information to public.

GROWTH VALUE MAP

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

September 10th, 2012 Page 4 of 10

Domestic Demand Remains the Main Engine for Indonesia Economic

Growth in 2012 Indonesia’s economic fundamentals will remain strong despite expected effect of current global crisis that may cause world economic slowdown. PEFINDO estimates that Indonesia’s economic growth will slightly down to 6.2% YoY in 2012, as in 2011, it was recorded of 6.5% YoY. The growth locomotive would be contributed from private consumption with the support of continued consumers’ optimism, manageable inflation, lower interest rate, and increasing per capita

income. Indonesia per capita income reached USD 3,543 in 2011, and may break USD 4,000 in 2012, compared to USD 3,000 in 2010. Meanwhile, investment realization in 2011 reached Rp 251.3 trillion or rose by 20.5% YoY compared to 2010’s. With population composition is dominated by productive age population (around 60%) and increasing international perception of Indonesia’s economy development that reflected from the inclusion of Indonesia into investment grade

by Fitch on December 2011 and by Moody’s on January 2012, then we believe that Indonesia will able to maintain its favorable growth in the coming years.

Table 2: Indonesia Economic Indicator 2008 2009 2010 2011

GDP Growth (%, YoY)

Inflation rate (%, YoY)

Exchange rate* (Rp/USD)

SBI rate (%)

6.1

11.06

9,136

9.25

4.5

2.78

9,680

6.50

6.1

6.96

10,398

6.5

6.5

3.79

8,779

6.0 * Bank Indonesia middle rate average Source: BPS, Bank Indonesia, Pefindo Equity & Index Valuation Division

Outlook of Security Document Industry: Enjoying Automotive Industry Growth We are positive to view security document industry by looking at better economic indicator and augmented with huge population in Indonesia which can trigger high number of vehicle. The car sales in domestic are predicted to break 1 million units this year although shadowed by the new policy to increase minimal down

payment in June 15th, 2012. Up to 1H12, the car sales already hit 534,876 units, or more than 50% from the target this year. On the other hand, such new policy

directly impacts to motorcycle sales in domestic. During January – June 2012, motorcycle sales only reached 3.7 million units, dropped by 8.5% YoY from the same period last year which hit 4.1 million units. And for FY2012, it is estimated that motorcycle sales will fall by 20% YoY to only 6.5 million units, from 8.0

million units in 2011. We believe that condition will gradually recover along with the continued growth of national GDP which leads stronger people purchasing power. Accordingly, we predict JTPE’s revenue will be able to grow by 10% YoY in 2012 or around Rp 560 billion. Besides that, we believe the demand for JTPE’s products from banking, manufacture, and airlines industry will remain robust, citing busier operational

activities from those industries as a result of better national economy. Also, we view that JTPE’s performance will not be affected by global economy woes since all of its products are sold in domestic market. Considering above factors, we are confident that JTPE’s business as security document producer has bright prospect in the years ahead.

BUSINESS INFORMATION

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

September 10th, 2012 Page 5 of 10

Figure 2: JTPE’s Revenue and Vehicle Sales in Indonesia

271

446

507

560

0

100

200

300

400

500

600

2009 2010 2011 2012P

in R

p b

illi

on

JTPE's Revenue

486,088

764,710

894,164 950,000

-

2,000,000

4,000,000

6,000,000

8,000,000

-

200,000

400,000

600,000

800,000

1,000,000

2009 2010 2011 2012P

in u

nit

s

in u

nit

s

Car Sales Motorcycle Sales

Source: PT Jasuindo Tiga Perkasa Tbk, and various source processed by Pefindo Equity & Index Valuation Division

Reliable due to Holding License

In 1996, JTPE received license from Indonesian Agency for Eradication Money Counterfeiting. Later in 1997, JTPE started to produce security document products. Currently, there are around 36 companies that engage in this industry, while only 8 companies (including JTPE) that hold the license from Bank of

Indonesia to print check, insurance policy and deposit. And thanks to holding the license, JTPE is trusted by government to produce security documents such as registration certificate and proof of vehicle ownership (STNK and BPKB) as well as ID card. Up to now, government sector takes major contribution to JTPE’s total revenue. Besides Indonesian Agency for Eradication Money Counterfeiting and Bank of Indonesia, JTPE also has pocketed license from Visa and MasterCard to produce bank card (credit card). In 2011, JTPE has invested around Rp 720

million to get such license and we expect the revenue from smart card division could hit Rp 28 billion in 2012. Providing Diverse and High-Quality Products To serve the varying demand from its customers, JTPE provide diverse and

integrated product namely Security Document, Non-Security Document and

Document Management. The products that include in Security Documents are: check, ID card, insurance policy, state document. While Non-Security Documents such as: invoice, EDC slip, direct mail, voucher and billing statement. In term of sales volume, Security Document took a major part or equivalent to 86% from 385,754 boxes in 2011. And for 2012, we estimate the sales volume of Security Document could grow by 10% YoY or around 426,200 boxes. On the other hand, we believe in JTPE’s products quality since it is directly supervised by

Government Institution.

Figure 3: Some of JTPE’s Products

Source: PT Jasuindo Tiga Perkasa Tbk., Pefindo Equity & Index Valuation Division

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

September 10th, 2012 Page 6 of 10

Efficiency Leads to Higher Margins

During 1H12, JTPE recorded decreasing sales growth by 27% YoY or equivalent to

Rp 106 billion. It was mainly due sales to government, the main contributor to JTPE’s total revenue, dropped by 44% YoY at the period to Rp 49 billion from Rp 88 billion in 1H11. Despite facing sales drop, JTPE could perform efficiency in COGS which further cascaded its profitability margins. JTPE’s gross, operating and net margin reached 31%, 14% and 10% in 1H12, better than in the same period last year which was 27%, 12% and 9%, respectively. We believe JTPE is still able to book positive growth in FY12 considering the growing of vehicle sales

and most of government order come up in 3Q and 4Q.

Figure 4: JTPE’s Gross, Operating and Net Margin

26%

34%32%

27%

31%

14%

23%21%

12%14%

9%

17% 16%

9% 10%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2009 2010 2011 1H11 1H12

Gross Margin Operating Margin Net Margin

Source: PT Jasuindo Tiga Perkasa Tbk., Pefindo Equity & Index Valuation Division

Credit Card Holder Continues to Rise According to the data from Bank of Indonesia, credit card holder remains growing in the last five years. In 2008, credit card holder was 11.5 million. In 2009, it grew by 6% YoY to reach 12.2 million. While in 2010 and 2011, it climbed by

11% YoY and 9% YoY or reached 13.5 million and 14.7 million, respectively.

Despite the fact that there is a new regulation from Central Bank to restrict the number of credit card, however, we believe higher income per capita of Indonesian and strong domestic consumption could trigger positive growth in banking sector particularly in credit card. For 2012, we estimate credit card holder will increase by 10% YoY or around 15 million.

Figure 5: Number of Credit Card Holder in Indonesia

11,512,2

13,5

14,7 15

0

2

4

6

8

10

12

14

16

2008 2009 2010 2011 2012P

in m

illi

on

Credit Card Holder

Source: Various source proceed by Pefindo Equity & Index Valuation Division

FINANCE

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

September 10th, 2012 Page 7 of 10

JTPE Business Prospect Supported by positive growth of Indonesian economy which is predicted to hit 6.2% YoY in 2012, manageable inflation at around 4.5% YoY and income per

capita that may break over USD 4,000 in 2012, we believe that outlook for

printing industry such as JTPE will remain prospective. Such conditions will much benefit JTPE since some industries that being served such as banking, manufacture and automotive grows positively. Besides that, we view that the global economic uncertainty will not hamper JTPE’s performance since its entire products are sold to domestic market. Based on above consideration, we believe JTPE is able to record Rp 560 billion of revenue in 2012, or reflecting 10% YoY growth.

Figure 6: JTPE Revenue Estimation

0

100

200

300

400

500

600

700

800

2012P 2013P 2014P 2015P 2016P

560620

679716 756

in R

p b

illi

on

JTPE's Revenue

Source: PT Jasuindo Tiga Perkasa Tbk ., Pefindo Equity and Index Valuation Division

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

September 10th, 2012 Page 8 of 10

VALUATION

Methodology

We apply Discounted Cash Flow (DCF) method as the main valuation approach considering the income growth is a value driver in JTPE instead of asset growth. We do not combine DCF method with Guideline Company Method (GCM) as there are no similar companies eligible to be compared with JTPE in the IDX.

This valuation is based on 100% JTPE’s shares price as of September 7th, 2012, using JTPE’s financial report as of June 30th, 2012 for our fundamental analysis.

Value Estimation

We use Cost of Capital of 10.7% and Cost of Equity of 11.5% based on the

following assumption:

Table 3: Assumption

Risk free rate [%]* 6.0 Risk premium [%]* 6.3 Beta [x]* 0.9 Cost of Equity [%] 11.5 Marginal tax rate [%] 25.0

Debt to Equity Ratio [x] 0.34 WACC [%] 10.7

Source: Bloomberg, Pefindo Equity & Index Valuation Division Estimates Notes: *As of September 7

th, 2012

The target price for 12 months based on Valuation as of September 7th, 2012 using DCF method with an assumption of 10.7% discount rate is ranging

between Rp 790 to Rp 870 per share. Table 4: Summary of DCF Method Valuation

Conservative Moderate Aggressive

PV of Free Cash Flows [Rp bn] 370 390 409 PV Terminal Value [Rp bn] 1,074 1,131 1,187 Non-Operating Assets- [Rp bn] 10 10 10 Net Debt [Rp bn] (66) (66) (66) Total Equity Value [Rp bn] 1,388 1,464 1,540 Number of Share [mn shares] 1,770 1,770 1,770 Fair Value per Share [Rp] 790 830 870 Source: Pefindo Equity & Index Valuation Division Estimates

TARGET PRICE

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

September 10th, 2012 Page 9 of 10

Table 5: Income Statement

Income Statement

(in Rp bn) 2009 2010 2011 2012P 2013P

Sales 271 446 507 560 620

COGS (199) (295) (344) (379) (419)

Gross Profit 72 151 163 181 201

Operating Expense (34) (48) (56) (62) (68)

Operating Profit 38 103 107 119 133

Other Income (Charges) (2) (2) (1) (1) (2)

Pre-tax Profit 36 101 106 118 131

Tax (12) (25) (26) (28) (31)

Net Profit 25 76 80 90 100

Source: PT Jasuindo Tiga Perkasa Tbk ., Pefindo Equity and Index Valuation Division Estimates

Table 6: Balance Sheet Balance Sheet

(in Rp bn) 2009 2010 2011 2012P 2013P

Assets

Current Assets

Cash & cash equivalents 44 79 83 97 89

Receivables 31 16 16 39 44

Inventory 12 8 15 23 25

Other Assets 10 28 52 64 71

Total Current Assets 97 131 166 223 229

Fixed Assets 63 104 145 185 201

Other Assets 1 1 2 2 2

Total Assets 161 236 313 410 432

Liabilities

Trade liabilities 24 25 76 79 87

Short-term liabilities 27 2 5 13 14

Other Short-term liabilities

18 30 30 33 37

Long-term liabilities 4 25 17 10 5

Total Liabilities 73 82 128 135 143

Total Equity 88 154 185 275 289

Source: PT Jasuindo Tiga Perkasa Tbk ., Pefindo Equity and Index Valuation Division Estimates

Figure 7: Historical P/E and P/BV

0,00

0,50

1,00

1,50

2,00

2,50

3,00

3,50

4,00

0,00

1,00

2,00

3,00

4,00

5,00

6,00

7,00

8,00

2009 2010 2011

P/BVP/E

P/E

P/BV

Figure 8: Historical ROA, ROE and TAT

01

02

02

02

02

02

02

02

02

02

02

00

10

20

30

40

50

60

2009 2010 2011

TATROA & ROE

ROA

ROE

TAT

Table 7: Key Ratio

Ratio 2009 2010 2011 2012P 2013P

Growth (%)

Sales 69.9 64.6 13.8 10.4 10.8

Operating Profit 171.0 173.7 4.5 10.8 11.9

EBITDA 135.5 154.5 9.4 9.1 11.7

Net Profit 215.9 197.9 5.5 12.6 11.8

Profitability (%)

Gross Margin 26.5 33.8 32.2 32.2 32.5

Operating Margin

13.8 23.0 21.1 21.2 21.4

EBITDA Margin 15.9 24.6 23.7 23.4 23.6

Net Margin 9.4 16.9 15.7 16.0 16.2

ROA 15.8 32.0 25.6 21.9 23.2

ROE 28.7 49.1 43.0 32.6 34.6

Solvability (X)

Debt to Equity 0.8 0.5 0.7 0.5 0.5

Debt to Asset 0.4 0.3 0.4 0.3 0.3

Liquidity (X)

Current Ratio 1.4 2.3 1.5 1.8 1.7

Quick Ratio 1.1 1.7 0.9 1.1 1.0

Source: PT Jasuindo Tiga Perkasa Tbk ., Pefindo Equity and Index Valuation Division Estimates

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Jasuindo Tiga Perkasa, Tbk

September 10th, 2012 Page 10 of 10

DISCLAIMER

This report was prepared based on the trusted and reliable sources. Nevertheless, we do not

guarantee its completeness, accuracy and adequacy. Therefore we do not responsible of any

investment decision making based on this report. As for any assumptions, opinions and predictions were solely our internal judgments as per reporting date, and those judgments are subject to change without further notice. We do not responsible for mistake and negligence occurred by using this report. Last performance could not always be used as reference for future outcome. This report is not an offering recommendation, purchase or holds particular shares. This report might not be suitable

for some investors. All opinion in this report has been presented fairly as per issuing date with good intentions; however it could be change at any time without further notice. The price, value or income from each share of the Company stated in this report might lower than the investor expectation and investor might obtain lower return than the invested amount. Investment is defined as the probable income that will be received in the future; nonetheless such return may possibly fluctuate. As for the Company which its share is denominated other than Rupiah, the

foreign exchange fluctuation may reduce the value, price or investor investment return. This report does not contain any information for tax consideration in investment decision making .

The share price target in this report is a fundamental value, not a fair market value nor a transaction price reference required by the regulations. The share price target issued by Pefindo Equity & Index Valuation Division is not a

recommendation to buy, sell or hold particular shares and it could not be considered as an investment advice from Pefindo Equity & Index Valuation Division as its scope of service to, or in relation to some parties, including listed companies, financial advisor, broker, investment bank, financial institution and intermediary, in correlation with receiving rewards or any other benefits from that parties. This report is not intended for particular investor and cannot be used as part of investment

objective on particular shares and neither an investment recommendation on particular shares or an investment strategy. We strongly recommended investor to consider the suitable situation and condition at first before making decision in relation with the figure in this report. If i t is necessary, kindly contact your financial advisor.

PEFINDO keeps the activities of Equity Valuation separate from Ratings to preserve

independence and objectivity of its analytical processes and products. PEFINDO has established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process. The entire process, methodology and the database used in the preparation of the Reference Share Price Target Report as a whole is different from the processes, methodologies and databases used PEFINDO in doing the rating. This report was prepared and composed by Pefindo Equity & Index Valuation Division with the

objective to enhance shares price transparency of listed companies in Indonesia Stock Exchange (IDX). This report is also free of other party’s influence, pressure or force either from IDX or the listed company which reviewed by Pefindo Equity & Index Valuation Division. Pefindo Equity & Index Valuation Division will earn reward amounting to Rp 20 mn each from IDX and the reviewed company for issuing report twice per year. For further information, please visit our website at http://www.pefindo.com This report is prepared and composed by Pefindo Equity & Index Valuation Division. In

Indonesia, this report is published in our website and in IDX website .