Embed Size (px)

Citation preview

FC Research

March 2017

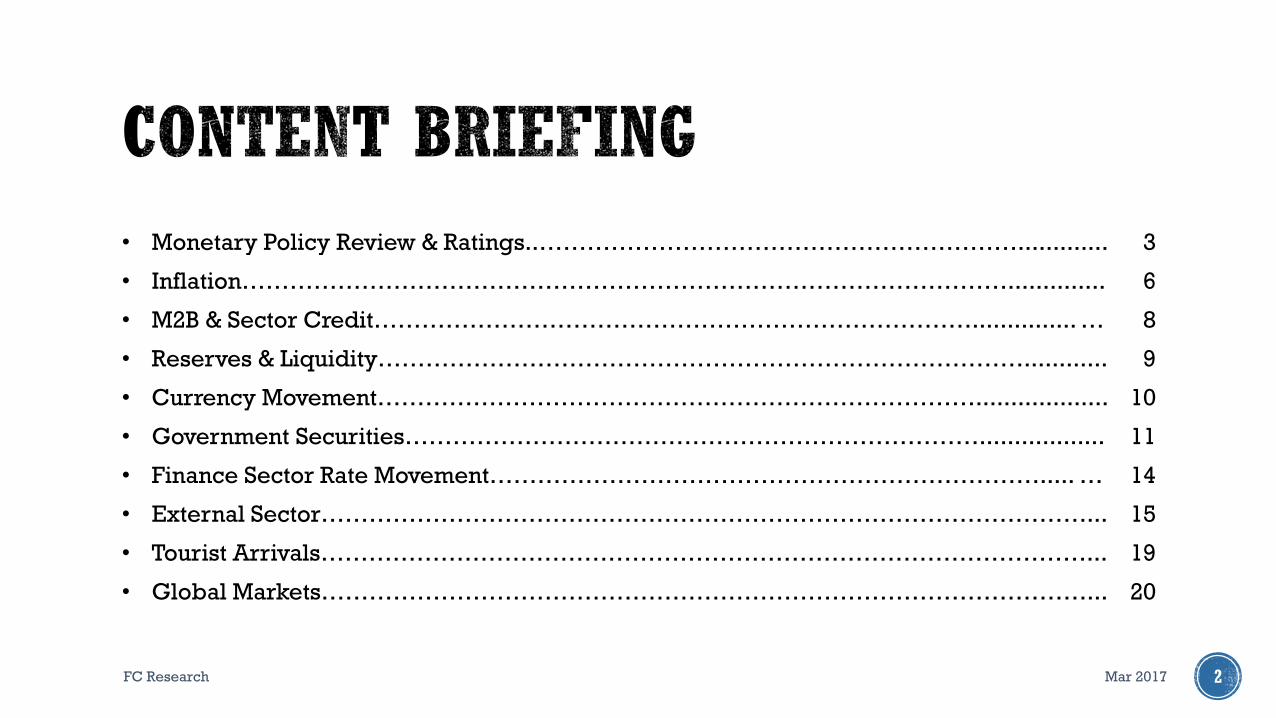

• Monetary Policy Review & Ratings..……………………………………………………............. 3

• Inflation…………………………………………………………………………………….............. 6

• M2B & Sector Credit…………………………………………………………………............... … 8

• Reserves & Liquidity………………………………………………………………………............ 9

• Currency Movement…………………………………………………………………................... 10

• Government Securities……………………………………………………………….................. 11

• Finance Sector Rate Movement……………………………………………………………..... … 14

• External Sector……………………………………………………………………………………... 15

• Tourist Arrivals……………………………………………………………………………………... 19

• Global Markets……………………………………………………………………………………... 20

Mar 2017FC Research 2

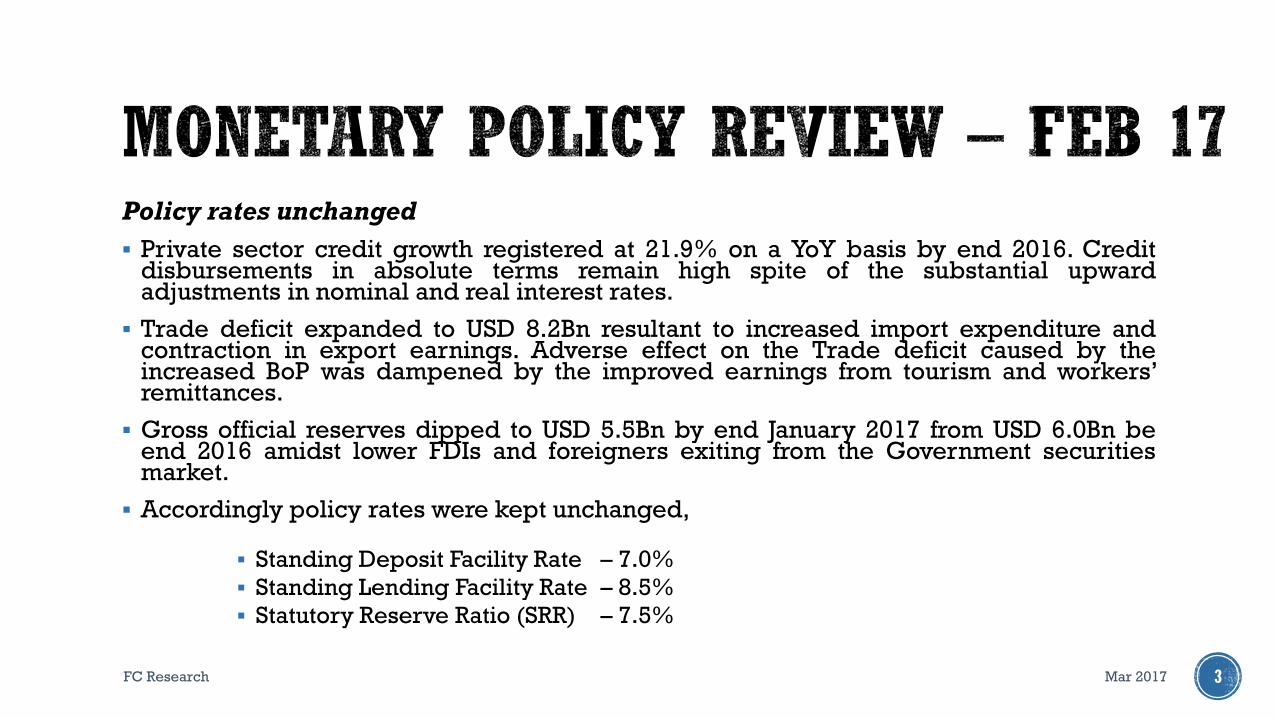

Policy rates unchanged

Private sector credit growth registered at 21.9% on a YoY basis by end 2016. Creditdisbursements in absolute terms remain high spite of the substantial upwardadjustments in nominal and real interest rates.

Trade deficit expanded to USD 8.2Bn resultant to increased import expenditure andcontraction in export earnings. Adverse effect on the Trade deficit caused by theincreased BoP was dampened by the improved earnings from tourism and workers’remittances.

Gross official reserves dipped to USD 5.5Bn by end January 2017 from USD 6.0Bn beend 2016 amidst lower FDIs and foreigners exiting from the Government securitiesmarket.

Accordingly policy rates were kept unchanged,

Standing Deposit Facility Rate – 7.0%

Standing Lending Facility Rate – 8.5%

Statutory Reserve Ratio (SRR) – 7.5%

Mar 2017FC Research 3

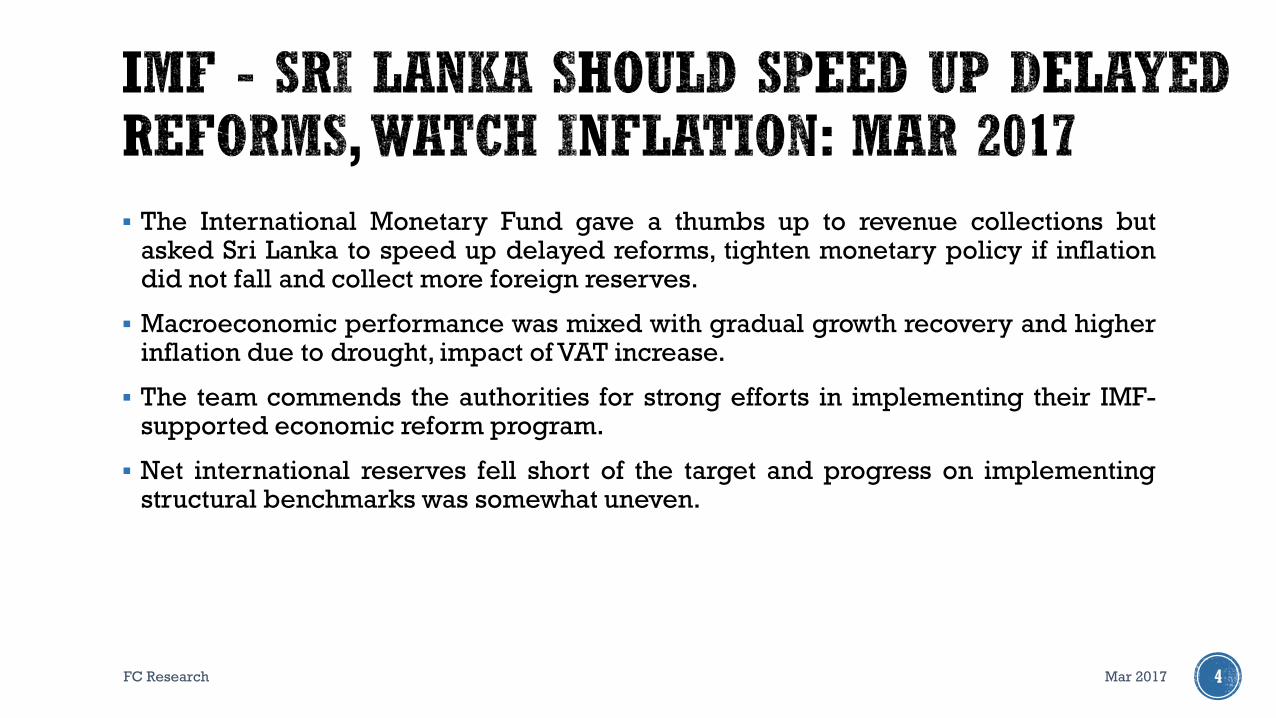

The International Monetary Fund gave a thumbs up to revenue collections butasked Sri Lanka to speed up delayed reforms, tighten monetary policy if inflationdid not fall and collect more foreign reserves.

Macroeconomic performance was mixed with gradual growth recovery and higherinflation due to drought, impact of VAT increase.

The team commends the authorities for strong efforts in implementing their IMF-supported economic reform program.

Net international reserves fell short of the target and progress on implementingstructural benchmarks was somewhat uneven.

Mar 2017FC Research 4

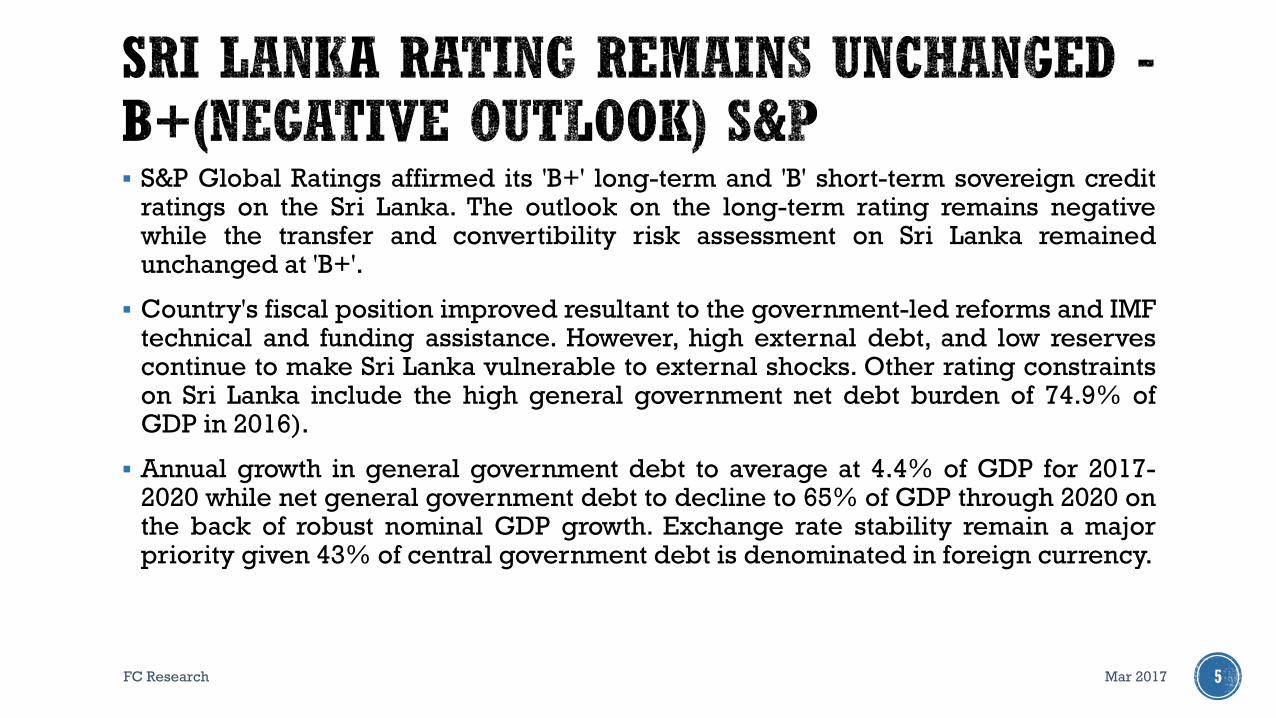

S&P Global Ratings affirmed its 'B+' long-term and 'B' short-term sovereign creditratings on the Sri Lanka. The outlook on the long-term rating remains negativewhile the transfer and convertibility risk assessment on Sri Lanka remainedunchanged at 'B+'.

Country's fiscal position improved resultant to the government-led reforms and IMFtechnical and funding assistance. However, high external debt, and low reservescontinue to make Sri Lanka vulnerable to external shocks. Other rating constraintson Sri Lanka include the high general government net debt burden of 74.9% ofGDP in 2016).

Annual growth in general government debt to average at 4.4% of GDP for 2017-2020 while net general government debt to decline to 65% of GDP through 2020 onthe back of robust nominal GDP growth. Exchange rate stability remain a majorpriority given 43% of central government debt is denominated in foreign currency.

Mar 2017FC Research 5

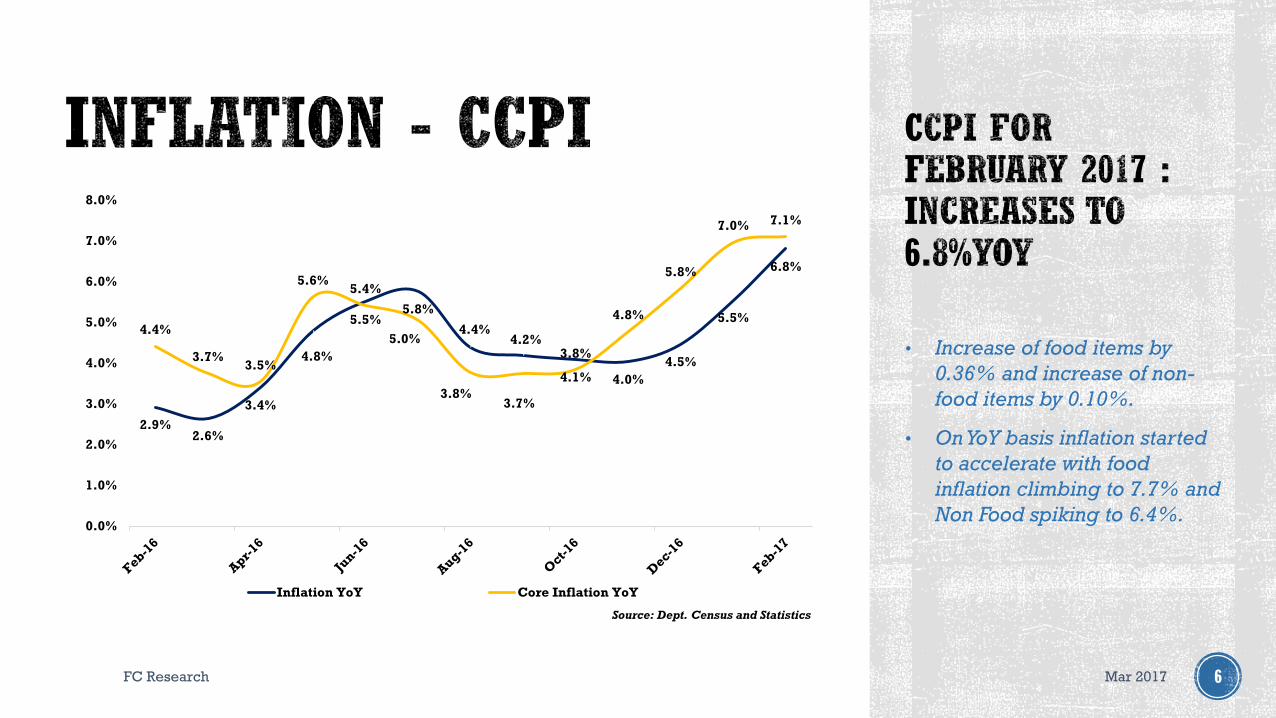

• Increase of food items by

0.36% and increase of non-

food items by 0.10%.

• On YoY basis inflation started

to accelerate with food

inflation climbing to 7.7% and

Non Food spiking to 6.4%.

Mar 2017FC Research 6

2.9%2.6%

3.4%

4.8%

5.5%5.8%

4.4%4.2%

4.1% 4.0%

4.5%

5.5%

6.8%

4.4%

3.7%3.5%

5.6%5.4%

5.0%

3.8%3.7%

3.8%

4.8%

5.8%

7.0% 7.1%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Inflation YoY Core Inflation YoY

Source: Dept. Census and Statistics

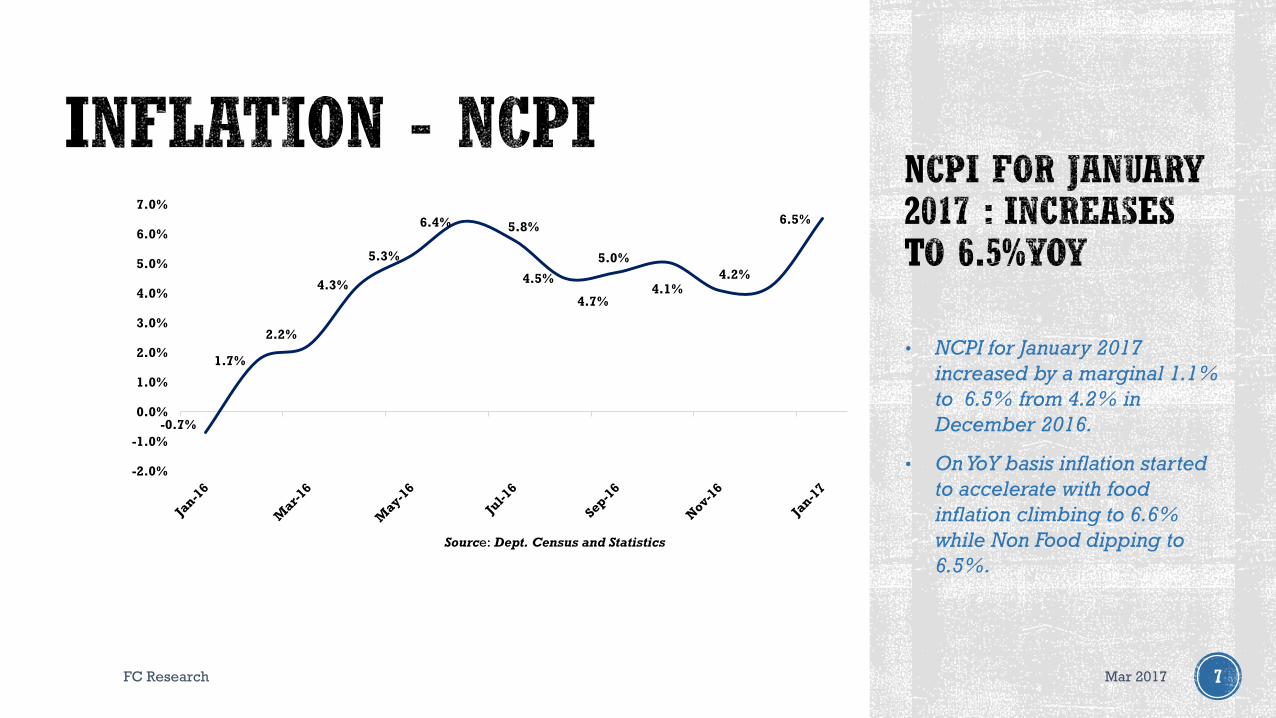

• NCPI for January 2017

increased by a marginal 1.1%

to 6.5% from 4.2% in

December 2016.

• On YoY basis inflation started

to accelerate with food

inflation climbing to 6.6%

while Non Food dipping to

6.5%.

Mar 2017FC Research 7

-0.7%

1.7%

2.2%

4.3%

5.3%

6.4% 5.8%

4.5%

4.7%

5.0%

4.1%4.2%

6.5%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Source: Dept. Census and Statistics

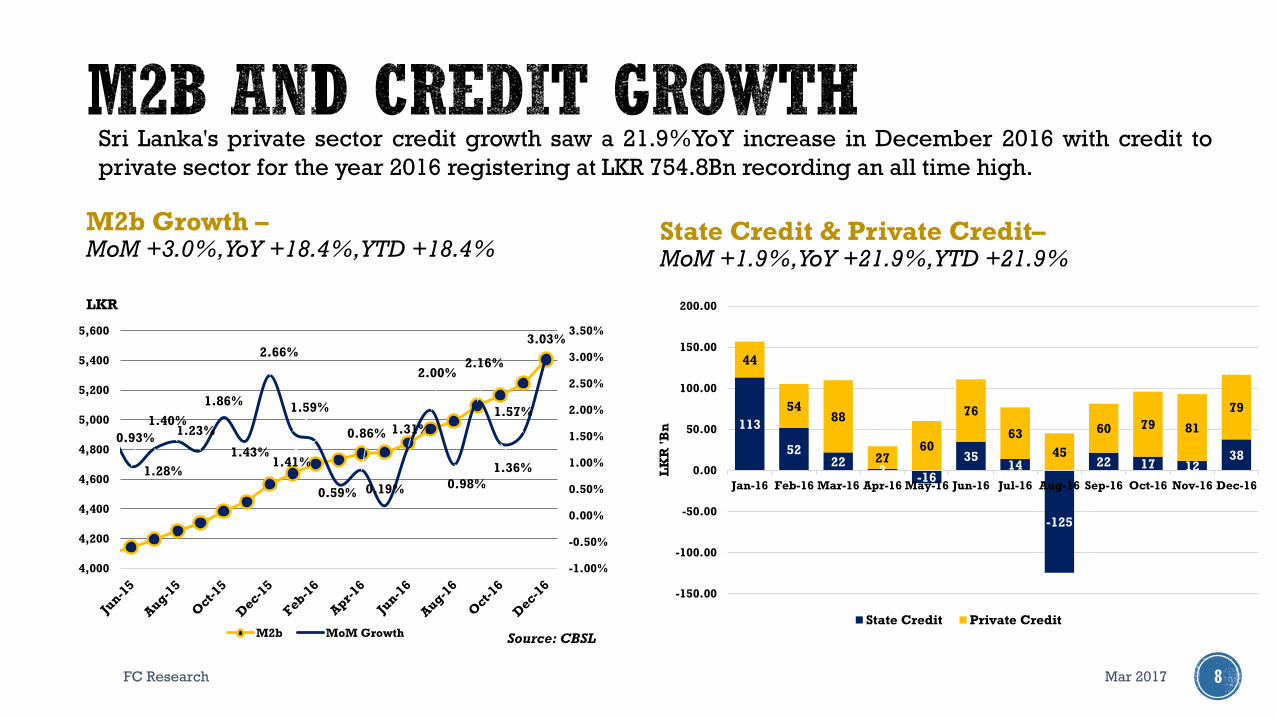

M2b Growth –MoM +3.0%, YoY +18.4%, YTD +18.4%

Mar 2017FC Research 8

Sri Lanka's private sector credit growth saw a 21.9%YoY increase in December 2016 with credit to

private sector for the year 2016 registering at LKR 754.8Bn recording an all time high.

0.93%

1.28%

1.40%1.23%

1.86%

1.43%

2.66%

1.59%

1.41%

0.59%

0.86%

0.19%

1.31%

2.00%

0.98%

2.16%

1.36%

1.57%

3.03%

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4,000

4,200

4,400

4,600

4,800

5,000

5,200

5,400

5,600

M2b MoM Growth Source: CBSL

LKR

State Credit & Private Credit–MoM +1.9%, YoY +21.9%, YTD +21.9%

113

5222

2-16

3514

-125

22 17 1238

44

5488

2760

76

63

45

60 79 81

79

-150.00

-100.00

-50.00

0.00

50.00

100.00

150.00

200.00

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16

LK

R '

Bn

State Credit Private Credit

Mar 2017FC Research 9

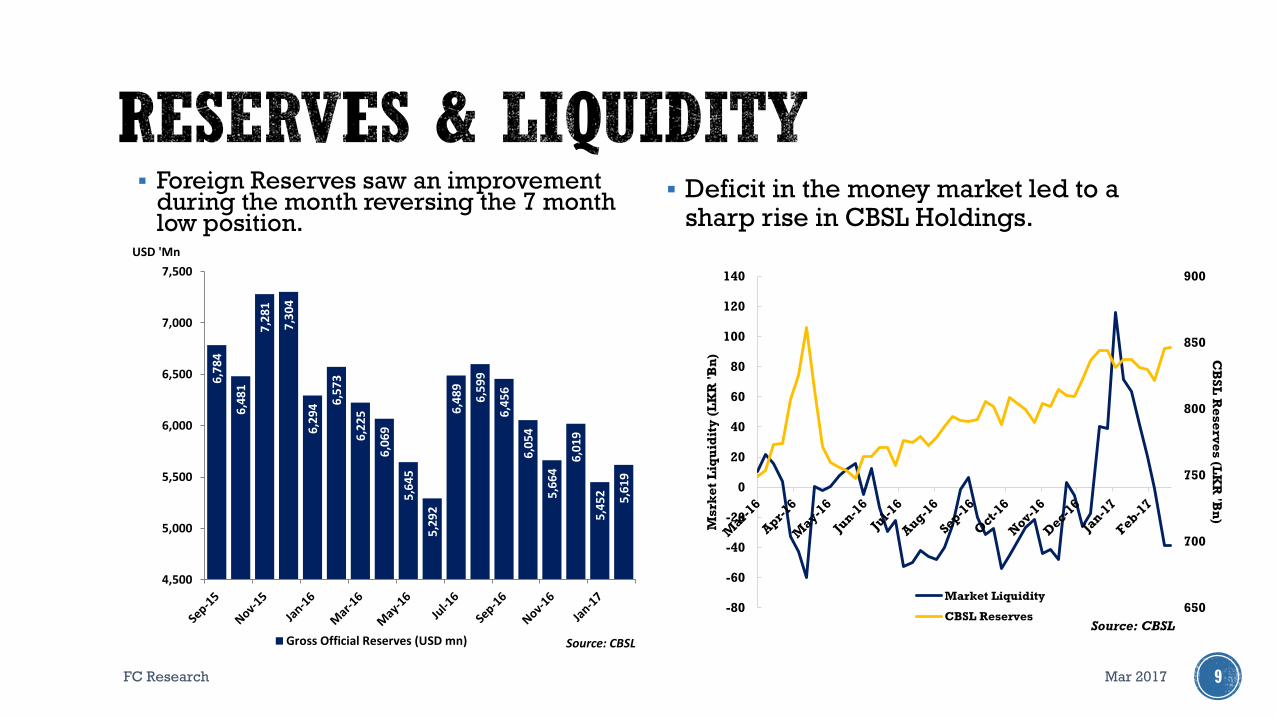

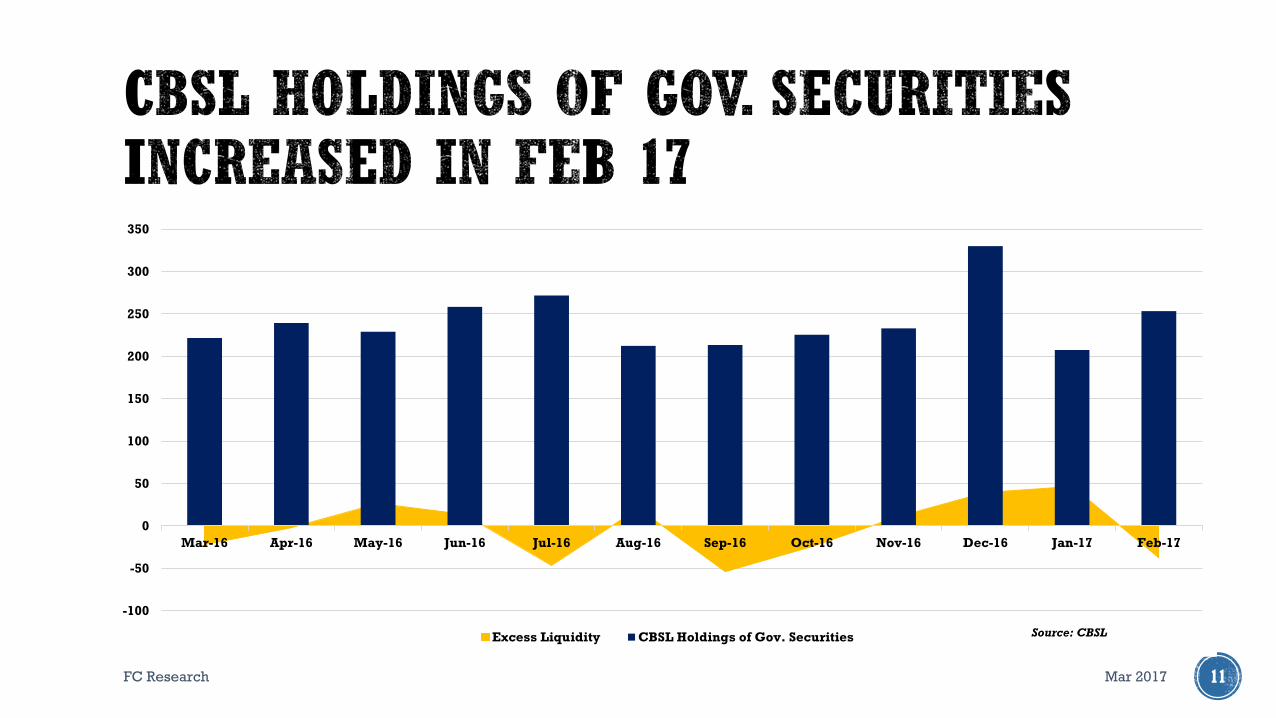

Foreign Reserves saw an improvement during the month reversing the 7 month low position.

Deficit in the money market led to a sharp rise in CBSL Holdings.

6,7

84

6,4

81

7,2

81

7,3

04

6,2

94 6

,57

3

6,2

25

6,0

69

5,6

45

5,2

92

6,4

89

6,5

99

6,4

56

6,0

54

5,6

64

6,0

19

5,4

52 5,6

19

4,500

5,000

5,500

6,000

6,500

7,000

7,500

USD 'Mn

Gross Official Reserves (USD mn) Source: CBSL

650

700

750

800

850

900

-80

-60

-40

-20

0

20

40

60

80

100

120

140

CB

SL

Re

se

rve

s (L

KR

'Bn

)

Ms

rke

t L

iqu

idit

y (

LK

R '

Bn

)

Market Liquidity

CBSL ReservesSource: CBSL

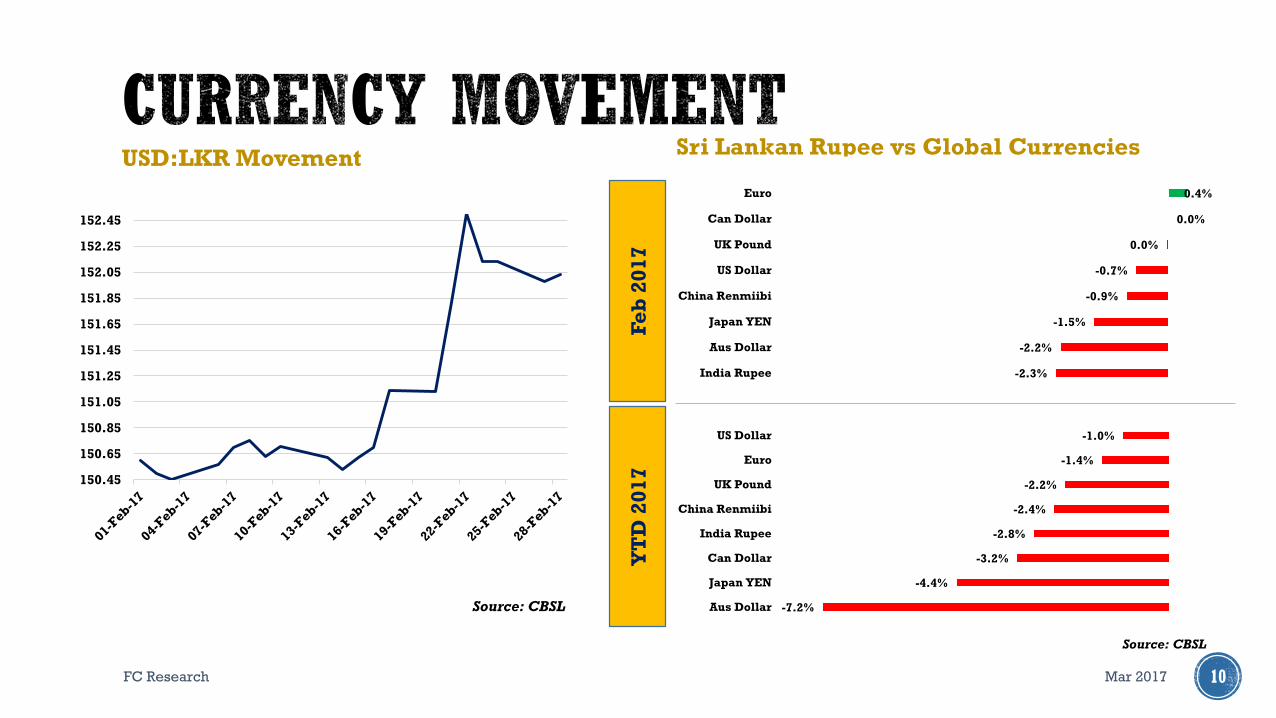

USD:LKR MovementSri Lankan Rupee vs Global Currencies

Mar 2017FC Research 10

Source: CBSL

Fe

b 2

01

7Y

TD

20

17

Source: CBSL

150.45

150.65

150.85

151.05

151.25

151.45

151.65

151.85

152.05

152.25

152.45

-2.3%

-2.2%

-1.5%

-0.9%

-0.7%

0.0%

0.0%

0.4%

India Rupee

Aus Dollar

Japan YEN

China Renmiibi

US Dollar

UK Pound

Can Dollar

Euro

-7.2%

-4.4%

-3.2%

-2.8%

-2.4%

-2.2%

-1.4%

-1.0%

Aus Dollar

Japan YEN

Can Dollar

India Rupee

China Renmiibi

UK Pound

Euro

US Dollar

Mar 2017FC Research 11

-100

-50

0

50

100

150

200

250

300

350

Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17

Excess Liquidity CBSL Holdings of Gov. Securities Source: CBSL

Mar 2017FC Research 12

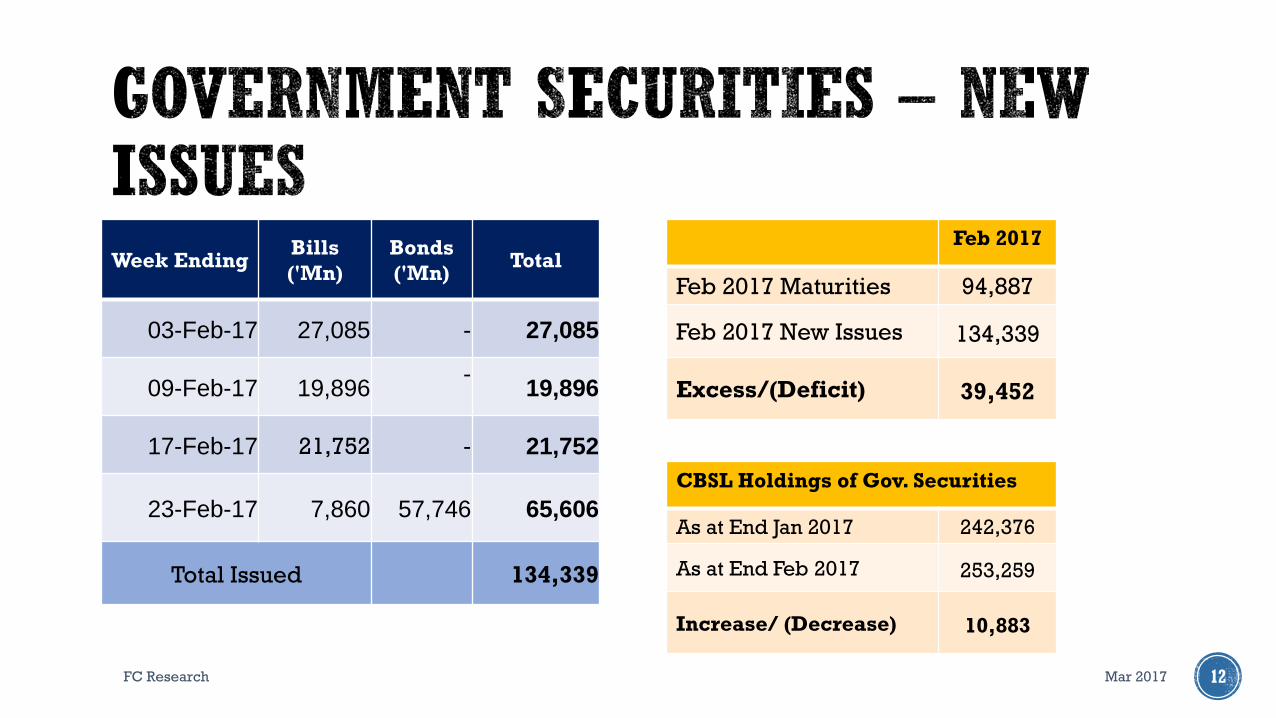

Week EndingBills

('Mn)

Bonds

('Mn)Total

03-Feb-17 27,085 - 27,085

09-Feb-17 19,896-

19,896

17-Feb-17 21,752 - 21,752

23-Feb-17 7,860 57,746 65,606

Total Issued 134,339

Feb 2017

Feb 2017 Maturities 94,887

Feb 2017 New Issues 134,339

Excess/(Deficit) 39,452

CBSL Holdings of Gov. Securities

As at End Jan 2017 242,376

As at End Feb 2017 253,259

Increase/ (Decrease) 10,883

Mar 2017FC Research 13

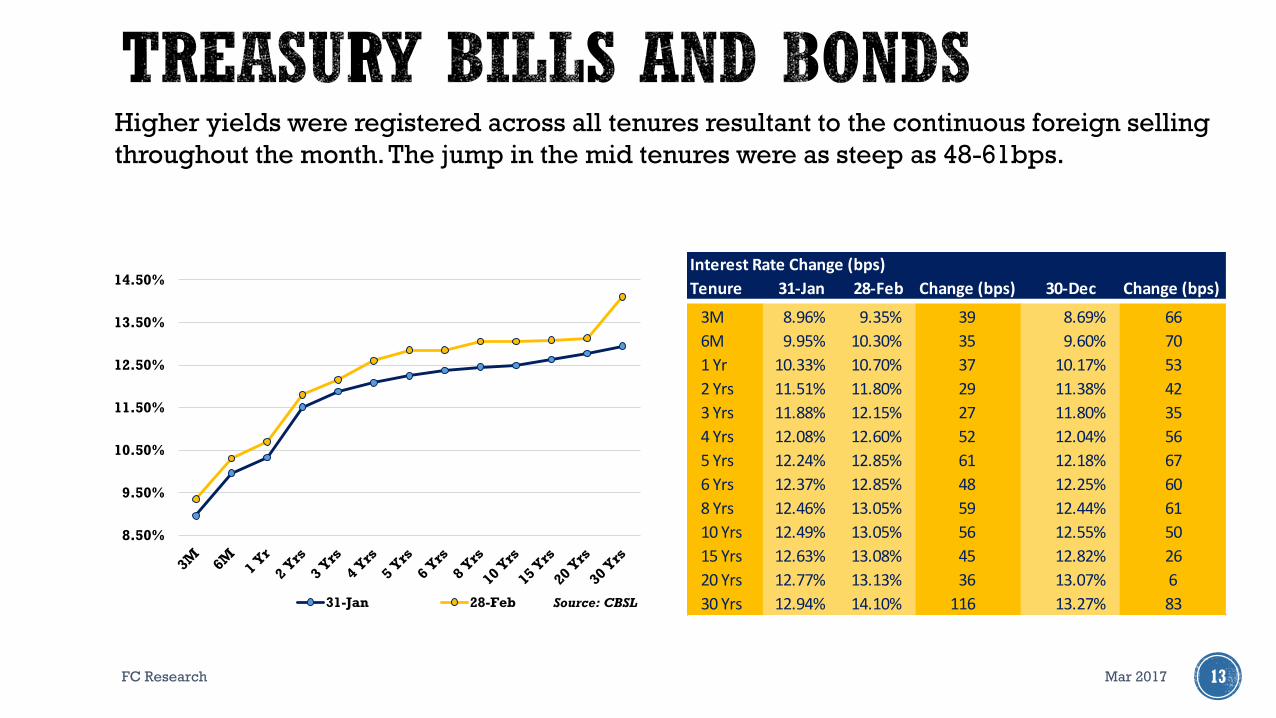

Higher yields were registered across all tenures resultant to the continuous foreign selling

throughout the month. The jump in the mid tenures were as steep as 48-61bps.

8.50%

9.50%

10.50%

11.50%

12.50%

13.50%

14.50%

31-Jan 28-Feb Source: CBSL

Interest Rate Change (bps)

Tenure 31-Jan 28-Feb Change (bps) 30-Dec Change (bps)

3M 8.96% 9.35% 39 8.69% 66

6M 9.95% 10.30% 35 9.60% 70

1 Yr 10.33% 10.70% 37 10.17% 53

2 Yrs 11.51% 11.80% 29 11.38% 42

3 Yrs 11.88% 12.15% 27 11.80% 35

4 Yrs 12.08% 12.60% 52 12.04% 56

5 Yrs 12.24% 12.85% 61 12.18% 67

6 Yrs 12.37% 12.85% 48 12.25% 60

8 Yrs 12.46% 13.05% 59 12.44% 61

10 Yrs 12.49% 13.05% 56 12.55% 50

15 Yrs 12.63% 13.08% 45 12.82% 26

20 Yrs 12.77% 13.13% 36 13.07% 6

30 Yrs 12.94% 14.10% 116 13.27% 83

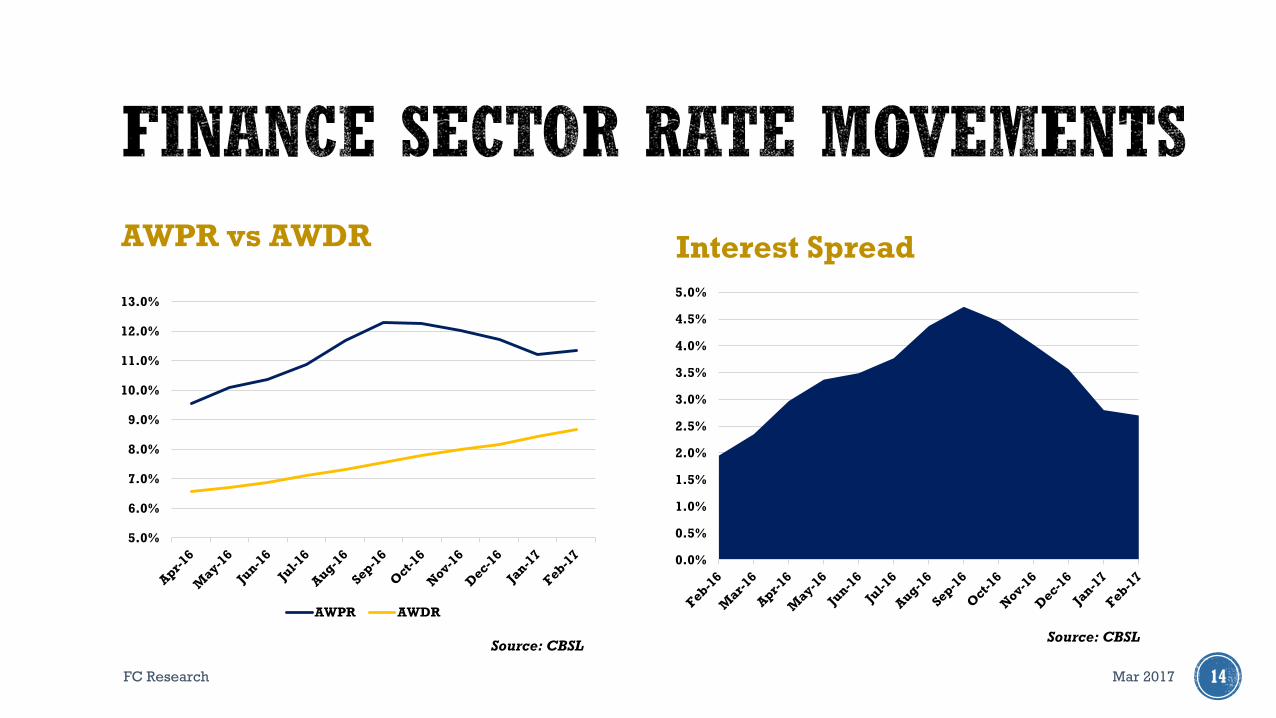

AWPR vs AWDR Interest Spread

Mar 2017FC Research 14

Source: CBSLSource: CBSL

Source: CBSL

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

AWPR AWDR

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Mar 2017FC Research 15

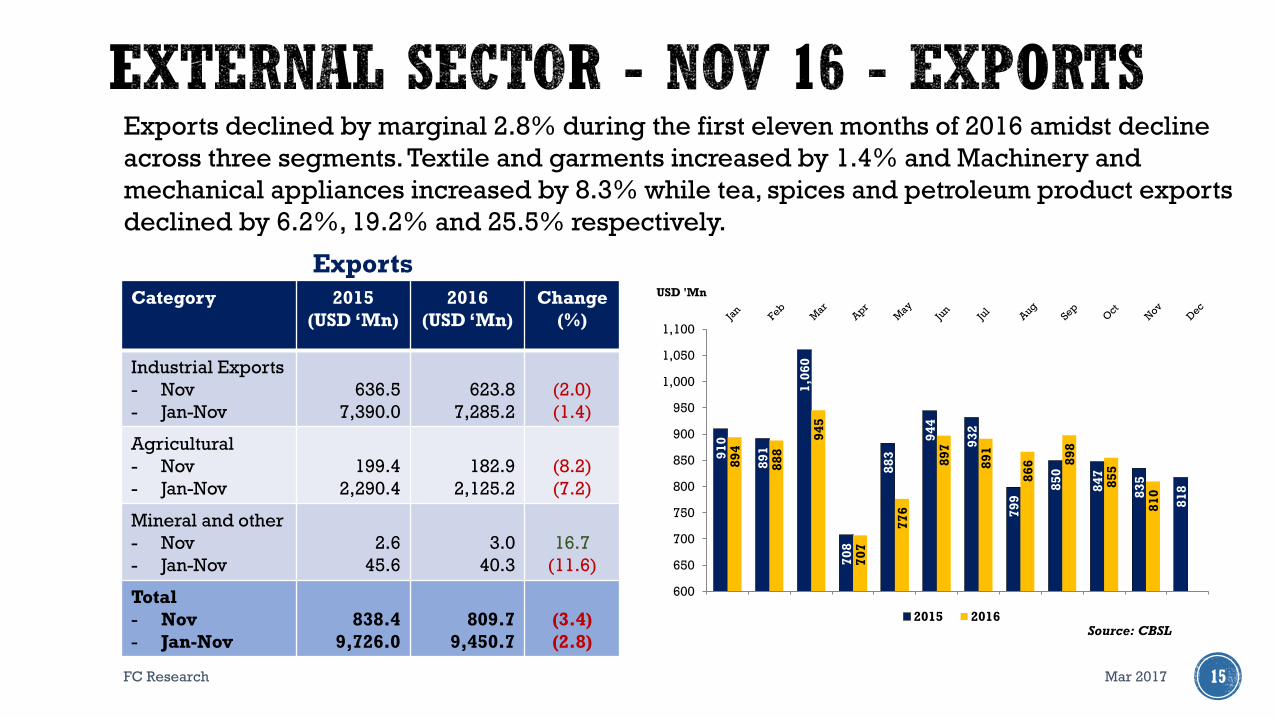

Exports declined by marginal 2.8% during the first eleven months of 2016 amidst decline

across three segments. Textile and garments increased by 1.4% and Machinery and

mechanical appliances increased by 8.3% while tea, spices and petroleum product exports

declined by 6.2%, 19.2% and 25.5% respectively.

Exports

Category 2015

(USD ‘Mn)

2016

(USD ‘Mn)

Change

(%)

Industrial Exports

- Nov

- Jan-Nov

636.5

7,390.0

623.8

7,285.2

(2.0)

(1.4)

Agricultural

- Nov

- Jan-Nov

199.4

2,290.4

182.9

2,125.2

(8.2)

(7.2)

Mineral and other

- Nov

- Jan-Nov

2.6

45.6

3.0

40.3

16.7

(11.6)

Total

- Nov

- Jan-Nov

838.4

9,726.0

809.7

9,450.7

(3.4)

(2.8)

91

0

89

1

1,0

60

70

8

88

3

94

4

93

2

79

9

85

0

84

7

83

5

81

8

89

4

88

8

94

5

70

7

77

6

89

7

89

1

86

6 89

8

85

5

81

0

600

650

700

750

800

850

900

950

1,000

1,050

1,100

USD 'Mn

2015 2016Source: CBSL

Imports

Mar 2017FC Research 16

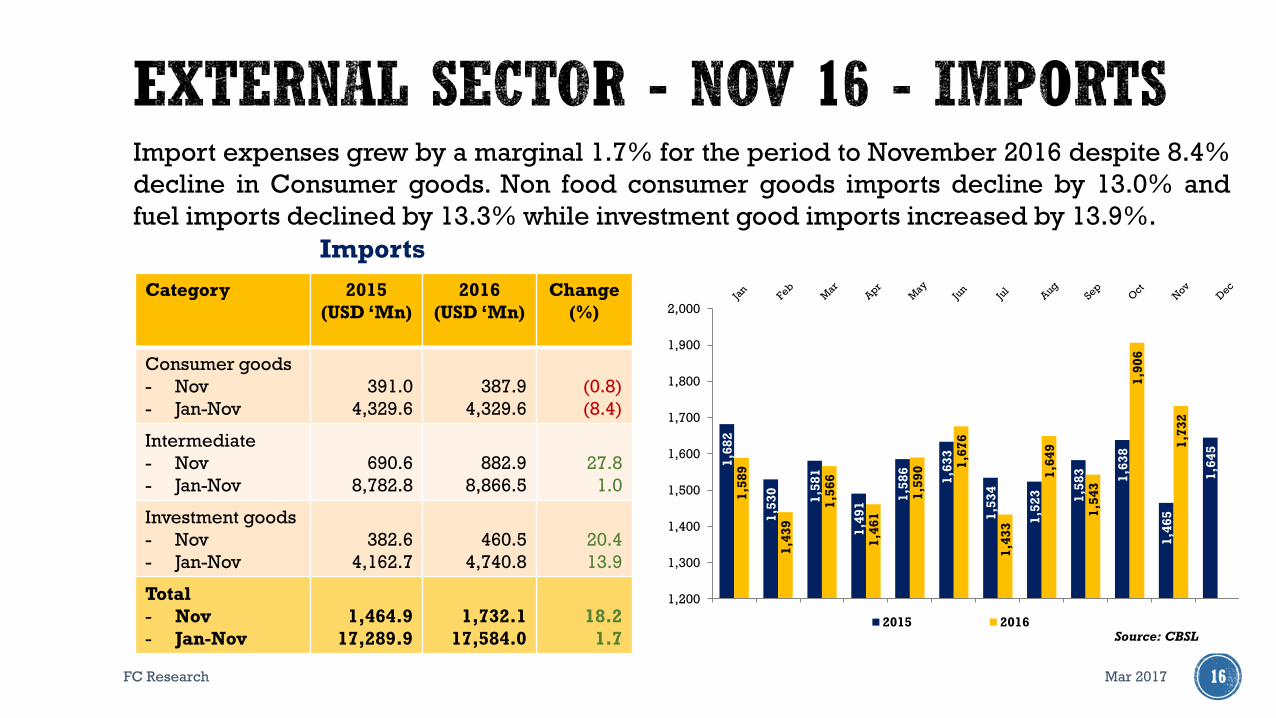

Import expenses grew by a marginal 1.7% for the period to November 2016 despite 8.4%

decline in Consumer goods. Non food consumer goods imports decline by 13.0% and

fuel imports declined by 13.3% while investment good imports increased by 13.9%.

Category 2015

(USD ‘Mn)

2016

(USD ‘Mn)

Change

(%)

Consumer goods

- Nov

- Jan-Nov

391.0

4,329.6

387.9

4,329.6

(0.8)

(8.4)

Intermediate

- Nov

- Jan-Nov

690.6

8,782.8

882.9

8,866.5

27.8

1.0

Investment goods

- Nov

- Jan-Nov

382.6

4,162.7

460.5

4,740.8

20.4

13.9

Total

- Nov

- Jan-Nov

1,464.9

17,289.9

1,732.1

17,584.0

18.2

1.7

1,6

82

1,5

30

1,5

81

1,4

91

1,5

86

1,6

33

1,5

34

1,5

23 1,5

83

1,6

38

1,4

65

1,6

45

1,5

89

1,4

39

1,5

66

1,4

61

1,5

90 1

,67

6

1,4

33

1,6

49

1,5

43

1,9

06

1,7

32

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2015 2016Source: CBSL

Mar 2017FC Research 17

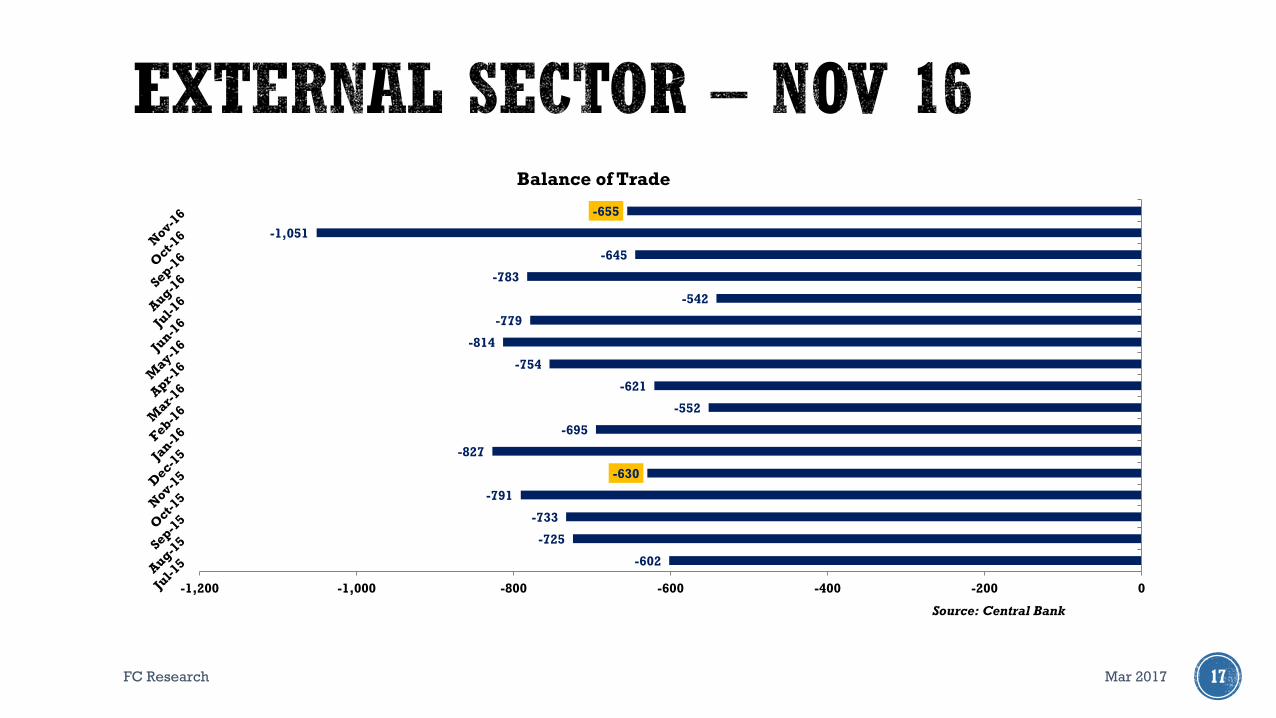

-602

-725

-733

-791

-630

-827

-695

-552

-621

-754

-814

-779

-542

-783

-645

-1,051

-655

-1,200 -1,000 -800 -600 -400 -200 0

Balance of Trade

Source: Central Bank

Nov

Trade Balance -13.2%

Mar 2017FC Research 18

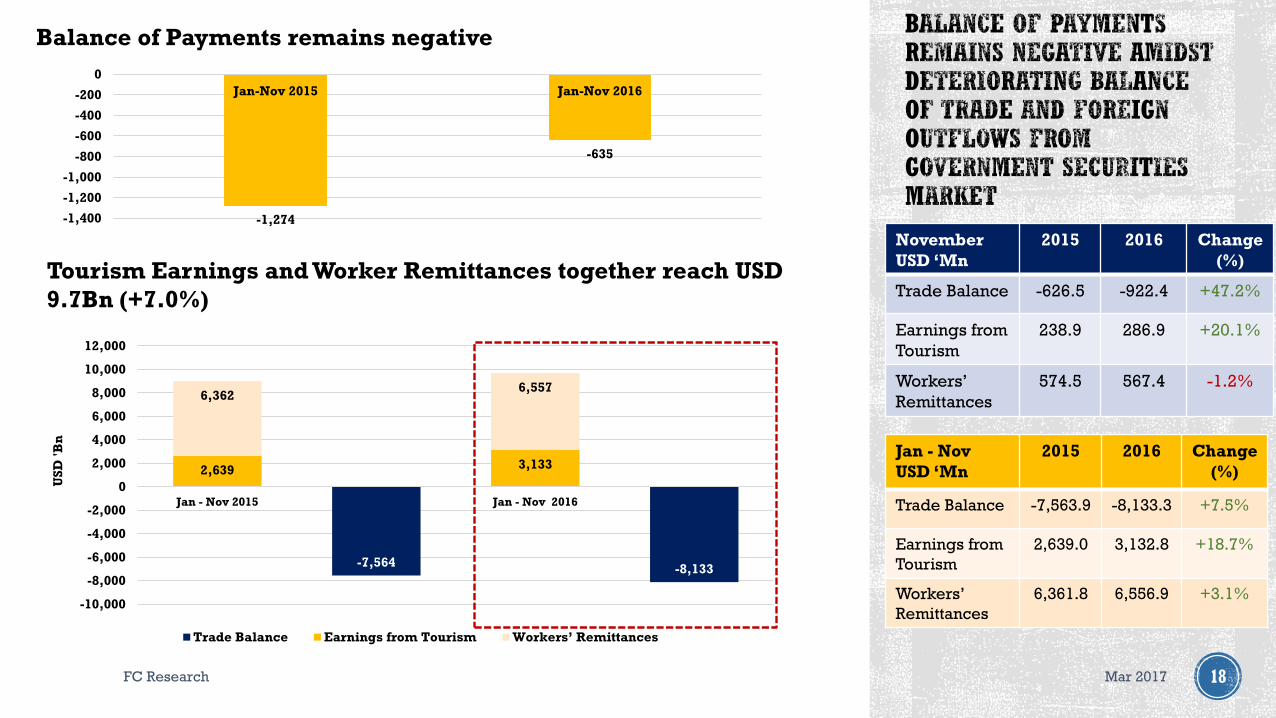

November

USD ‘Mn

2015 2016 Change

(%)

Trade Balance -626.5 -922.4 +47.2%

Earnings from

Tourism

238.9 286.9 +20.1%

Workers’

Remittances

574.5 567.4 -1.2%

Jan - Nov

USD ‘Mn

2015 2016 Change

(%)

Trade Balance -7,563.9 -8,133.3 +7.5%

Earnings from

Tourism

2,639.0 3,132.8 +18.7%

Workers’

Remittances

6,361.8 6,556.9 +3.1%

Balance of Payments remains negative

Tourism Earnings and Worker Remittances together reach USD

9.7Bn (+7.0%)

-1,274

-635

-1,400

-1,200

-1,000

-800

-600

-400

-200

0

Jan-Nov 2015 Jan-Nov 2016

-7,564-8,133

2,639 3,133

6,3626,557

-10,000

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

Jan - Nov 2015 Jan - Nov 2016

Trade Balance Earnings from Tourism Workers’ Remittances

US

D '

Bn

DOWN 0.1% UP 6.4%

Mar 2017FC Research 19

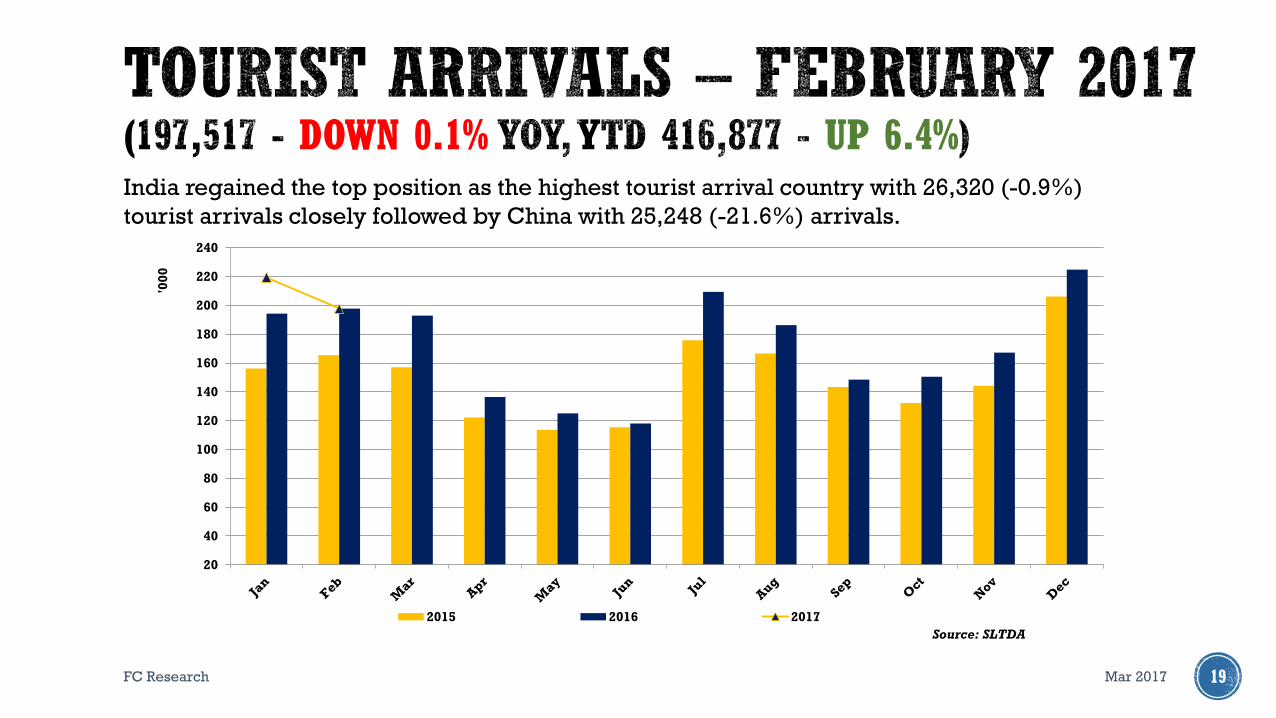

India regained the top position as the highest tourist arrival country with 26,320 (-0.9%)

tourist arrivals closely followed by China with 25,248 (-21.6%) arrivals.

20

40

60

80

100

120

140

160

180

200

220

240

'00

0

2015 2016 2017

Source: SLTDA

FC Research 20

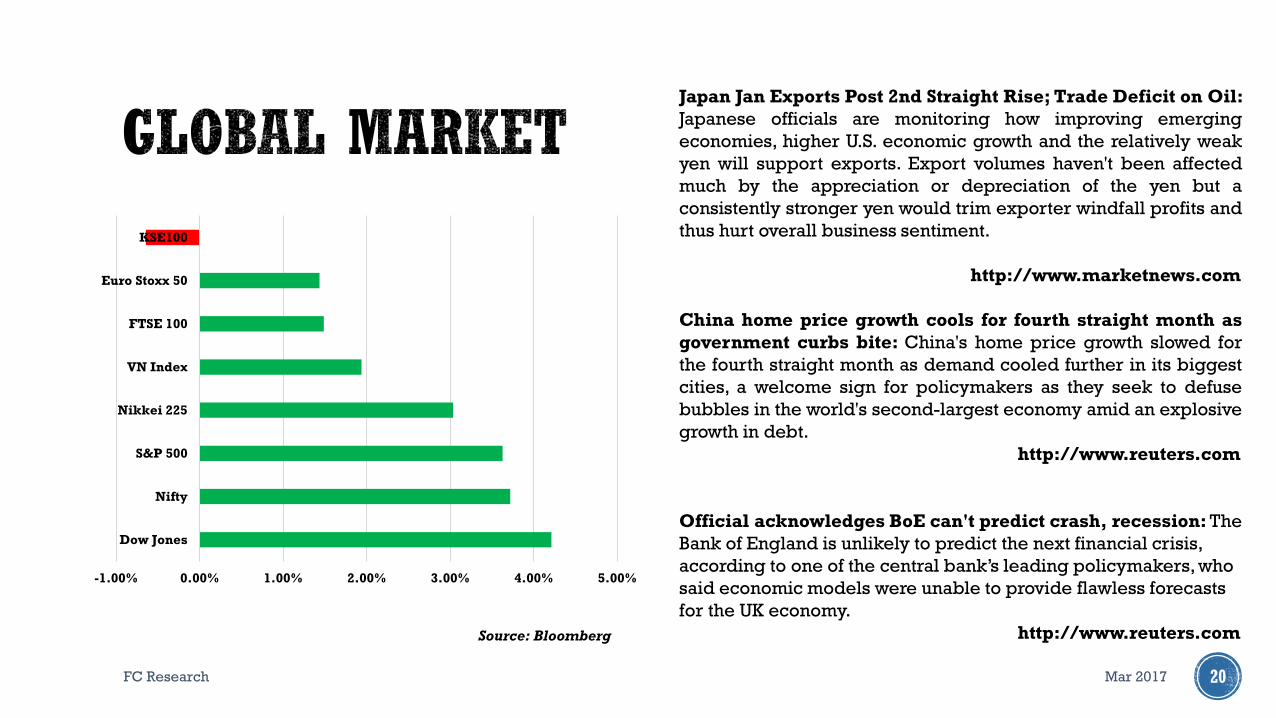

Japan Jan Exports Post 2nd Straight Rise; Trade Deficit on Oil:

Japanese officials are monitoring how improving emerging

economies, higher U.S. economic growth and the relatively weak

yen will support exports. Export volumes haven't been affected

much by the appreciation or depreciation of the yen but a

consistently stronger yen would trim exporter windfall profits and

thus hurt overall business sentiment.

http://www.marketnews.com

China home price growth cools for fourth straight month as

government curbs bite: China's home price growth slowed for

the fourth straight month as demand cooled further in its biggest

cities, a welcome sign for policymakers as they seek to defuse

bubbles in the world's second-largest economy amid an explosive

growth in debt.

http://www.reuters.com

Official acknowledges BoE can't predict crash, recession: The

Bank of England is unlikely to predict the next financial crisis,

according to one of the central bank’s leading policymakers, who

said economic models were unable to provide flawless forecasts

for the UK economy.

http://www.reuters.comSource: Bloomberg

Mar 2017

-1.00% 0.00% 1.00% 2.00% 3.00% 4.00% 5.00%

Dow Jones

Nifty

S&P 500

Nikkei 225

VN Index

FTSE 100

Euro Stoxx 50

KSE100

FC Research 21

This Review is prepared and issued by First Capital Equities (Pvt) Ltd. based on information in the public domain, internallydeveloped and other sources, believed to be correct. Although all reasonable care has been taken to ensure the contents ofthe review are accurate, First Capital Equities (Pvt) Ltd and/or its Directors, employees, are not responsible for thecorrectness, usefulness, reliability of same. First Capital Equities (Pvt) Ltd may act as a Broker in the investments which are thesubject of this document or related investments and may have acted on or used the information contained in this document, orthe research or analysis on which it is based, before its publication. First Capital Equities (Pvt) Ltd and/or its principal, theirrespective Directors, or Employees may also have a position or be otherwise interested in the investments referred to in thisdocument. This is not an offer to sell or buy the investments referred to in this document. This Review may contain data whichare inaccurate and unreliable. You hereby waive irrevocably any rights or remedies in law or equity you have or may haveagainst First Capital Equities (Pvt) Ltd with respect to the Review and agree to indemnify and hold First Capital Equities (Pvt)Ltd and/or its principal, their respective directors and employees harmless to the fullest extent allowed by law regarding allmatters related to your use of this Review. No part of this document may be reproduced, distributed or published in whole orin part by any means to any other person for any purpose without prior permission.

Mar 2017

CONTACT

FC Research +94 11 2639 898

• Amanda Lokugamage +94 11 2639 868

• Michelle Weerasinghe +94 11 2639 866

• Dimantha Mathew +94 11 2639 853

• Atchuthan Srirangan +94 11 2639 863

• Hansinee Beddage +94 11 2639 864

22