Embed Size (px)

Citation preview

Predicciones de Tecnología, Medios y Telecomunicaciones2015

Craig WiggintonNelson ValeroCraig WiggintonNelson Valero

#PrediccionesTMT

Sobre las predicciones

2© 2015. Deloitte & Touche Ltda.

Descubra lo que viene en Tecnología, Medios y Telecomunicaciones

3© 2015. Deloitte & Touche Ltda.

3. La impresión 3D es una revolución, pero no la revolución que imaginamos

5. Videos de corta duración: un futuro, pero no el futuro de la televisión

4. Las baterías de los smartphones sin grandes avances

6. La “generación que no gasta” está gastando mucho en contenidos

1. Internet de las cosas es para las cosas no para las personas

2. Drones: perfil elevado y de nicho

7. El papel está vivo y coleando – al menos en el caso de los libros

8. Mil millones de reposiciones de smartphones

9. El cisma de la conectividad se agranda: la creciente brecha en las velocidades de la banda ancha

10. Los pagos con el móvil “sin contacto” (por fin) toman impulso.

Predicciones de Tecnología2015

4© 2015. Deloitte & Touche Ltda.

Internet de las cosas es para las cosas, no para las personas

5© 2015. Deloitte & Touche Ltda.

6© 2015. Deloitte & Touche Ltda.

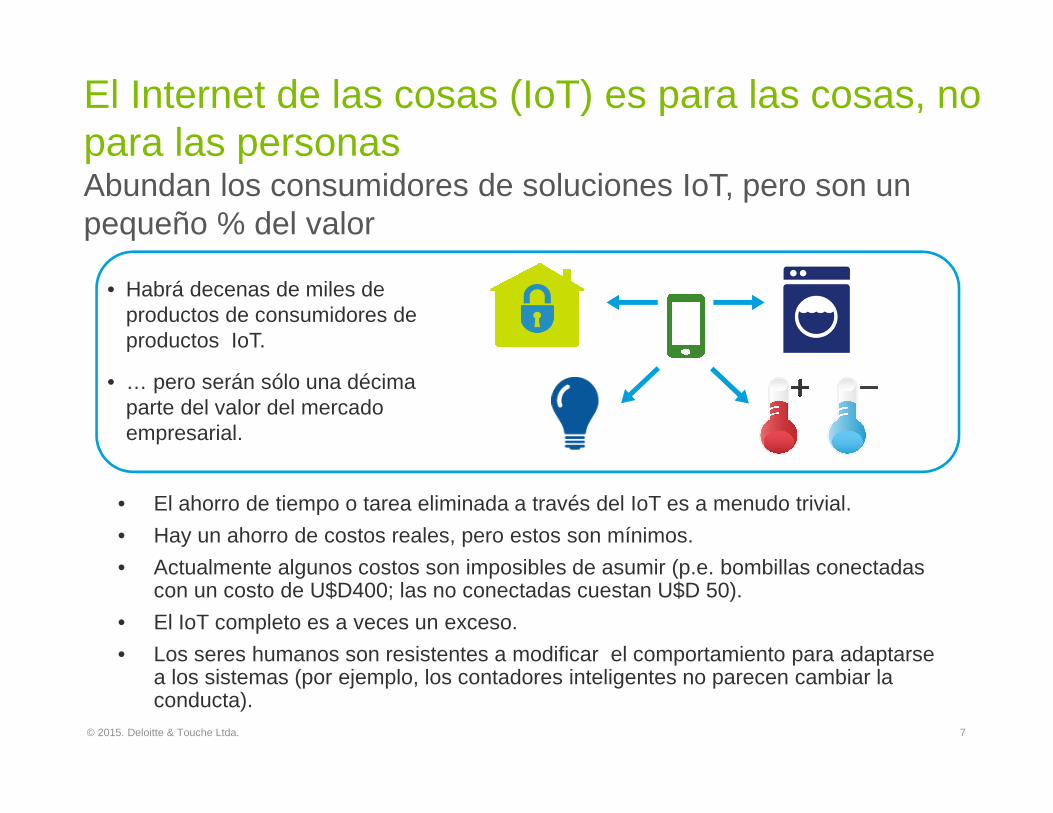

El Internet de las cosas (IoT) es para las cosas, no para las personas

• El ahorro de tiempo o tarea eliminada a través del IoT es a menudo trivial.

• Hay un ahorro de costos reales, pero estos son mínimos.

• Actualmente algunos costos son imposibles de asumir (p.e. bombillas conectadas con un costo de U$D400; las no conectadas cuestan U$D 50).

• El IoT completo es a veces un exceso.

• Los seres humanos son resistentes a modificar el comportamiento para adaptarse a los sistemas (por ejemplo, los contadores inteligentes no parecen cambiar la conducta).

El Internet de las cosas (IoT) es para las cosas, no para las personasAbundan los consumidores de soluciones IoT, pero son un pequeño % del valor

• Habrá decenas de miles de productos de consumidores de productos IoT.

• … pero serán sólo una décima parte del valor del mercado empresarial.

7© 2015. Deloitte & Touche Ltda.

Drones: perfil elevado y de nicho

8© 2015. Deloitte & Touche Ltda.

El valor total del mercado de aviones no tripulados será equivalente al de un jet de pasajeros

de tamaño medio9© 2015. Deloitte & Touche Ltda.

Drones: perfil elevado y de nicho

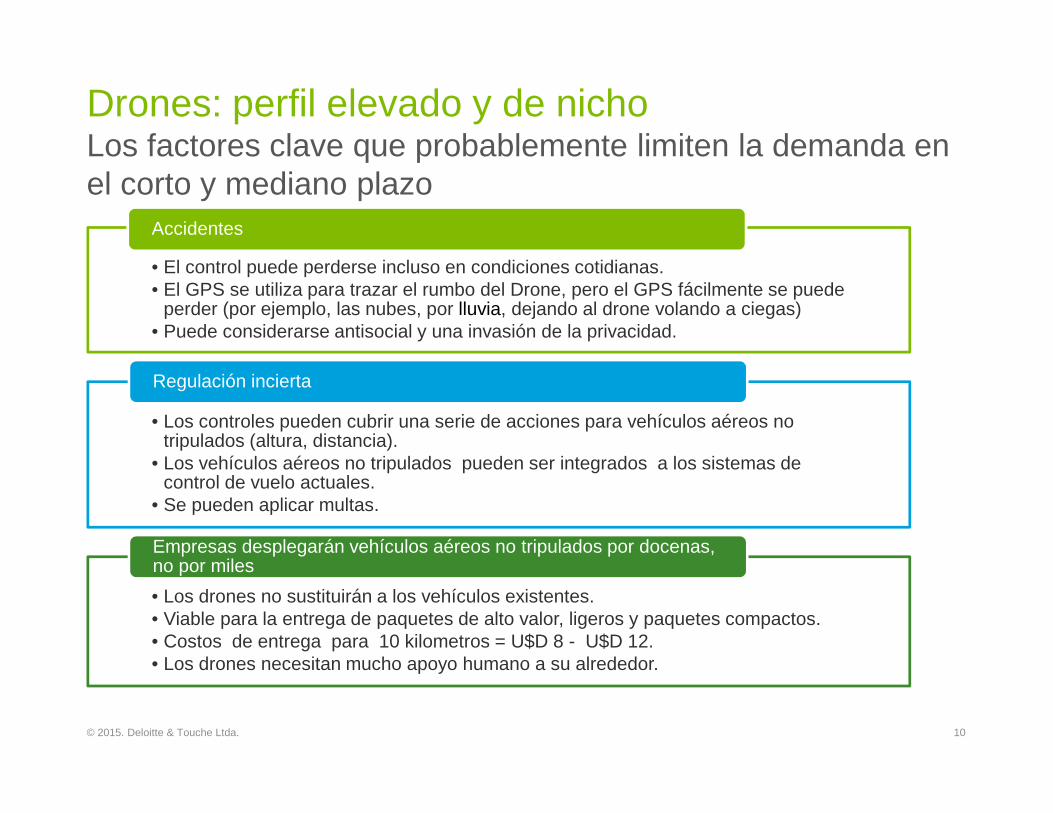

Drones: perfil elevado y de nichoLos factores clave que probablemente limiten la demanda en el corto y mediano plazo

• El control puede perderse incluso en condiciones cotidianas.• El GPS se utiliza para trazar el rumbo del Drone, pero el GPS fácilmente se puede

perder (por ejemplo, las nubes, por lluvia, dejando al drone volando a ciegas)• Puede considerarse antisocial y una invasión de la privacidad.

Accidentes

• Los controles pueden cubrir una serie de acciones para vehículos aéreos no tripulados (altura, distancia).

• Los vehículos aéreos no tripulados pueden ser integrados a los sistemas de control de vuelo actuales.

• Se pueden aplicar multas.

Regulación incierta

• Los drones no sustituirán a los vehículos existentes.• Viable para la entrega de paquetes de alto valor, ligeros y paquetes compactos.• Costos de entrega para 10 kilometros = U$D 8 - U$D 12.• Los drones necesitan mucho apoyo humano a su alrededor.

Empresas desplegarán vehículos aéreos no tripulados por docenas, no por miles

10© 2015. Deloitte & Touche Ltda.

Las baterías de los smartphones sin grandes avances

11© 2015. Deloitte & Touche Ltda.

12© 2015. Deloitte & Touche Ltda.

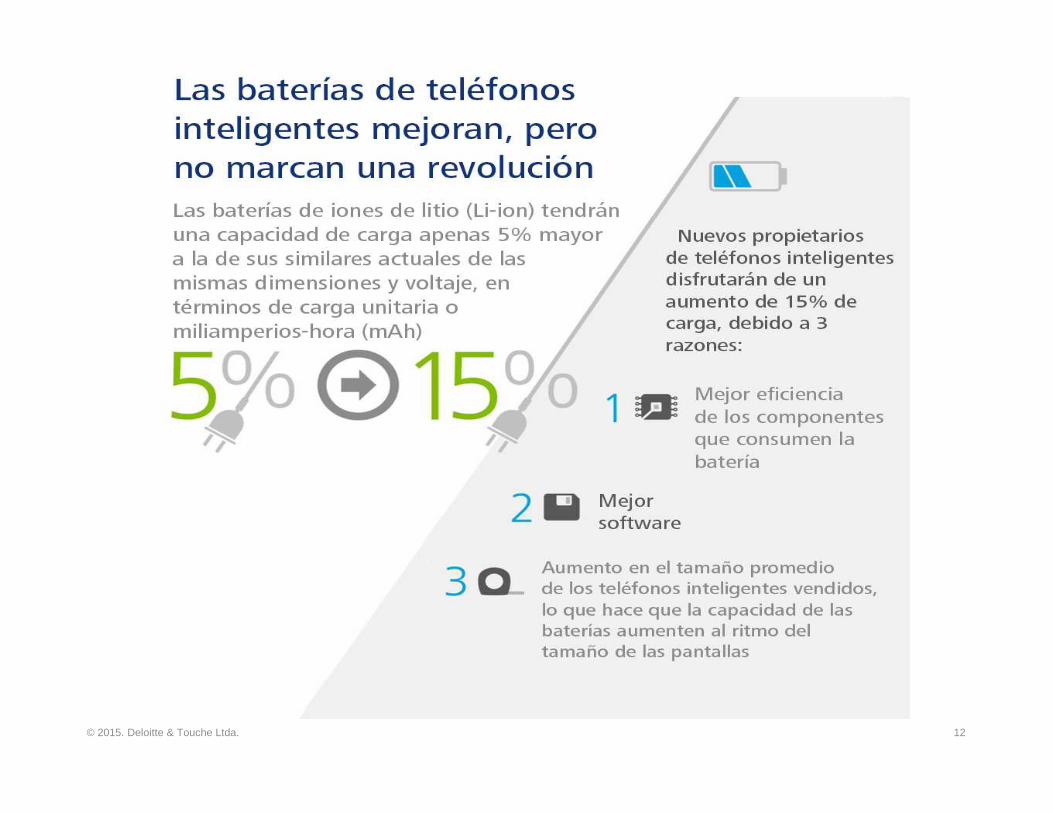

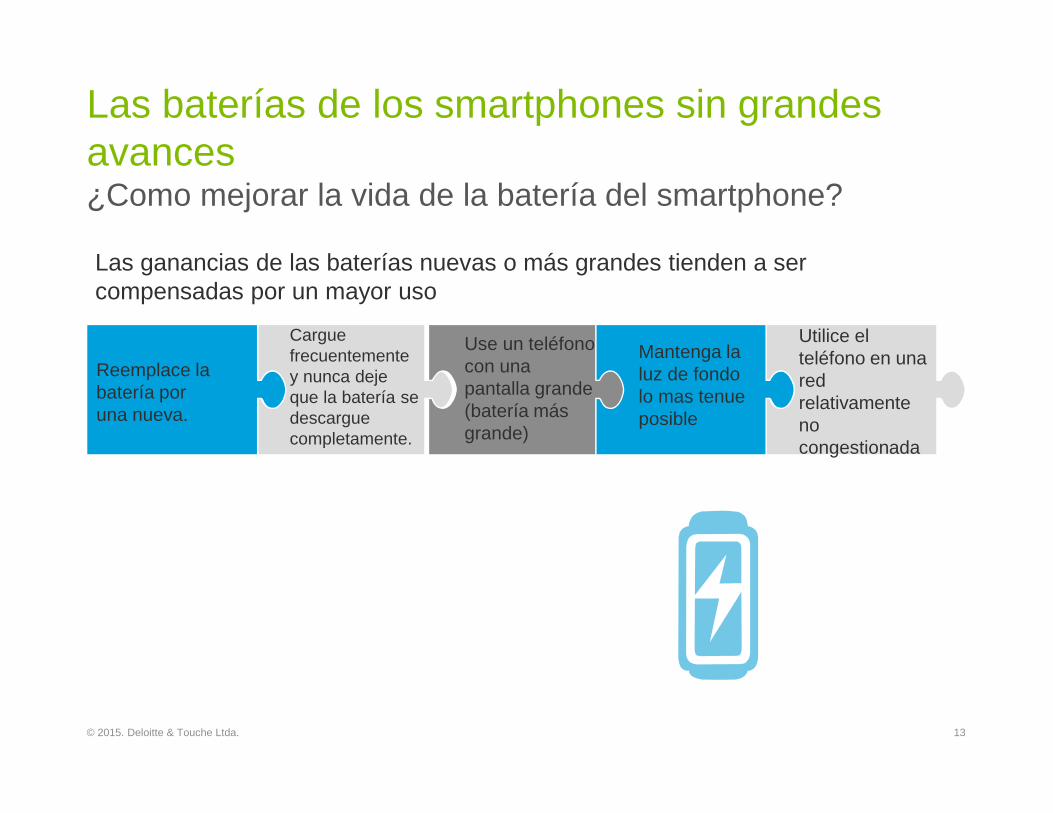

Las ganancias de las baterías nuevas o más grandes tienden a ser compensadas por un mayor uso

Las baterías de los smartphones sin grandes avances ¿Como mejorar la vida de la batería del smartphone?

13© 2015. Deloitte & Touche Ltda.

Use un teléfono con una pantalla grande (batería más grande)

Cargue frecuentemente y nunca deje que la batería se descargue completamente.

Reemplace la batería por una nueva.

Mantenga la luz de fondo lo mas tenue posible

Utilice el teléfono en una red relativamente no congestionada

Predicciones de Medios2015

14© 2015. Deloitte & Touche Ltda.

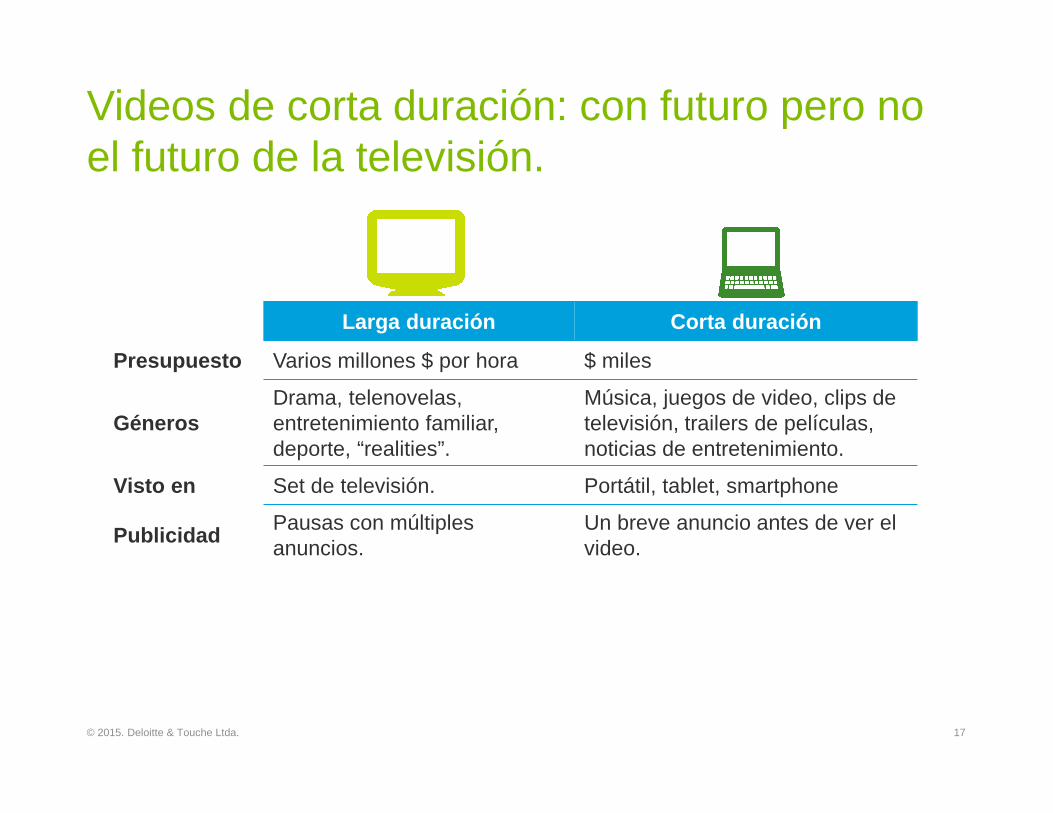

Videos de corta duración: con futuro, pero no el futuro de la televisión.

15© 2015. Deloitte & Touche Ltda.

16© 2015. Deloitte & Touche Ltda.

Videos de corta duración: con futuro pero no el futuro de la televisión.

Videos de corta duración: con futuro pero no el futuro de la televisión.

Larga duración Corta duración

Presupuesto Varios millones $ por hora $ miles

GénerosDrama, telenovelas, entretenimiento familiar, deporte, “realities”.

Música, juegos de video, clips de televisión, trailers de películas, noticias de entretenimiento.

Visto en Set de televisión. Portátil, tablet, smartphone

PublicidadPausas con múltiples anuncios.

Un breve anuncio antes de ver el video.

17© 2015. Deloitte & Touche Ltda.

El impreso sigue vivo ycoleando; al menos en elcaso de los libros.

18© 2015. Deloitte & Touche Ltda.

El impreso sigue vivo y coleando; al menos en el caso de los libros

La impresión dominará las ventas de libros, incluso en mercados con alta penetración de dispositivos digitales.

eReaders

16%

Tablets Smartphones Portátil.

P: En su caso, cuales de las opciones usted posee y a cuales tiene acceso inmediato?

19© 2015. Deloitte & Touche Ltda.

44% 74% 79%

En algunos mercados de impresión, comolos periódicos, la mayor parte de demandaes impulsada por los antiguos consumidoresque crecieron en el mundo de la impresión.

Este no es el caso de los libros , la aversión de lageneración del milenio a los CD, DVD, periódicosimpresos y revistas no se extiende a la impresión delibros.

El impreso sigue vivo y coleando; al menos en el caso de los librosLos jóvenes lectores aún están leyendo, en impresos; y lo están haciendo con gran intensidad. En una encuesta realizada en Estados Unidos en septiembre de 2013, del 16 al 34% dijo que esto es lo que les apasiona:

25% 38% 25% 16%3%

Casi el 50% de la generación del milenio, coincide en que los libros electrónicos

nunca tomarán el lugar de los impresos.

20© 2015. Deloitte & Touche Ltda.

También puede ser el caso deque los libros físicos sonsuperiores cuando se trata deretención de la información.

Telecoms Predictions2015

21© 2015. Deloitte & Touche Ltda.

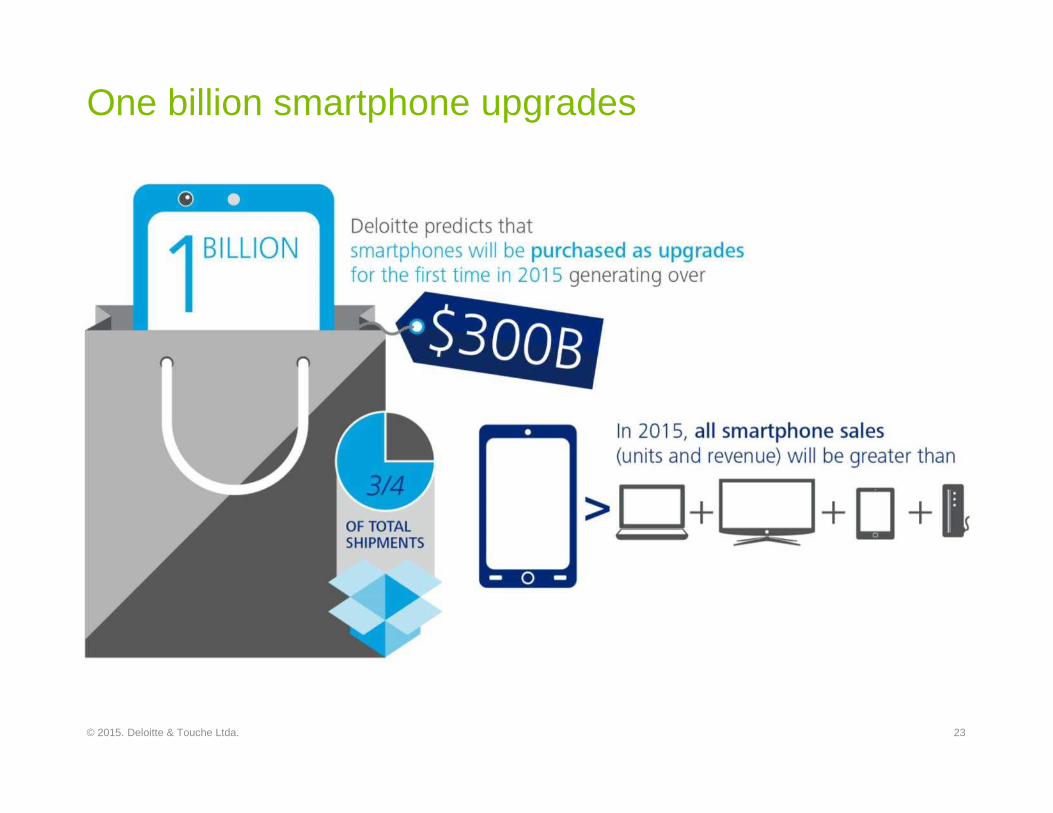

One billion smartphone upgrades

22© 2015. Deloitte & Touche Ltda.

One billion smartphone upgrades

23© 2015. Deloitte & Touche Ltda.

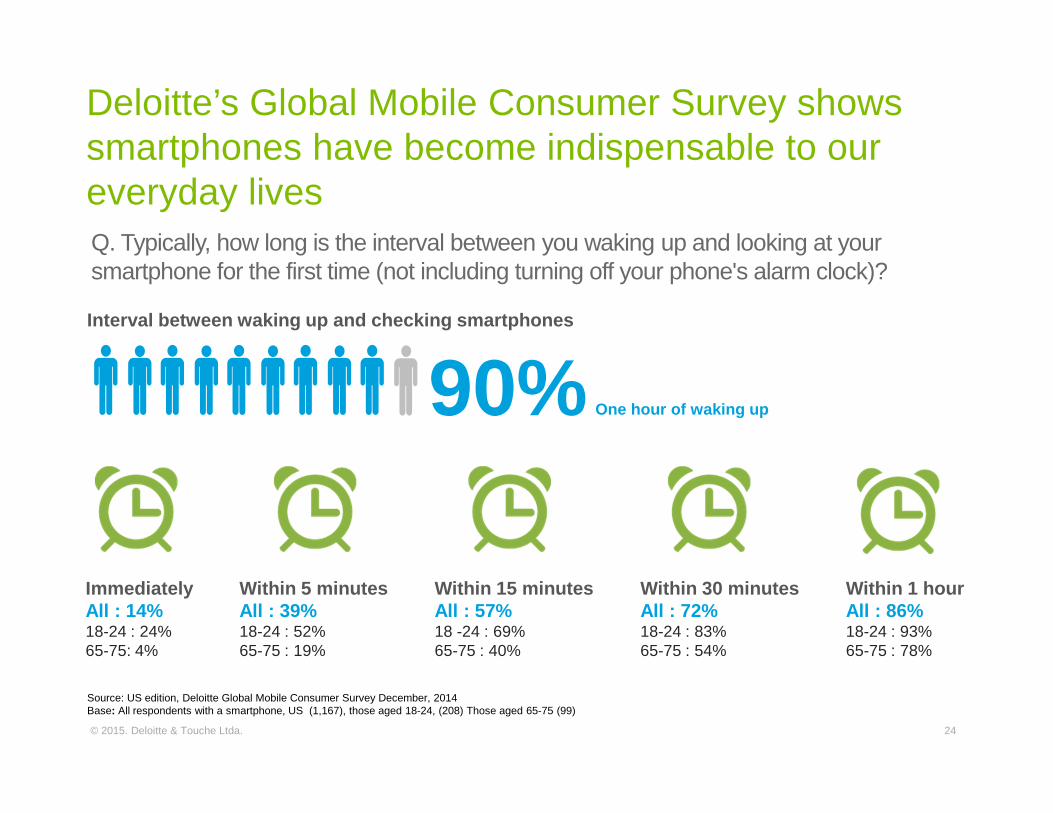

Deloitte’s Global Mobile Consumer Survey shows smartphones have become indispensable to our everyday livesQ. Typically, how long is the interval between you waking up and looking at your smartphone for the first time (not including turning off your phone's alarm clock)?

Interval between waking up and checking smartphones

90%

ImmediatelyAll : 14% 18-24 : 24%65-75: 4%

Within 5 minutesAll : 39%18-24 : 52%65-75 : 19%

Within 30 minutesAll : 72%18-24 : 83%65-75 : 54%

Within 1 hourAll : 86%18-24 : 93%65-75 : 78%

Within 15 minutesAll : 57%18 -24 : 69%65-75 : 40%

One hour of waking up

Source: US edition, Deloitte Global Mobile Consumer Survey December, 2014Base: All respondents with a smartphone, US (1,167), those aged 18-24, (208) Those aged 65-75 (99)

24© 2015. Deloitte & Touche Ltda.

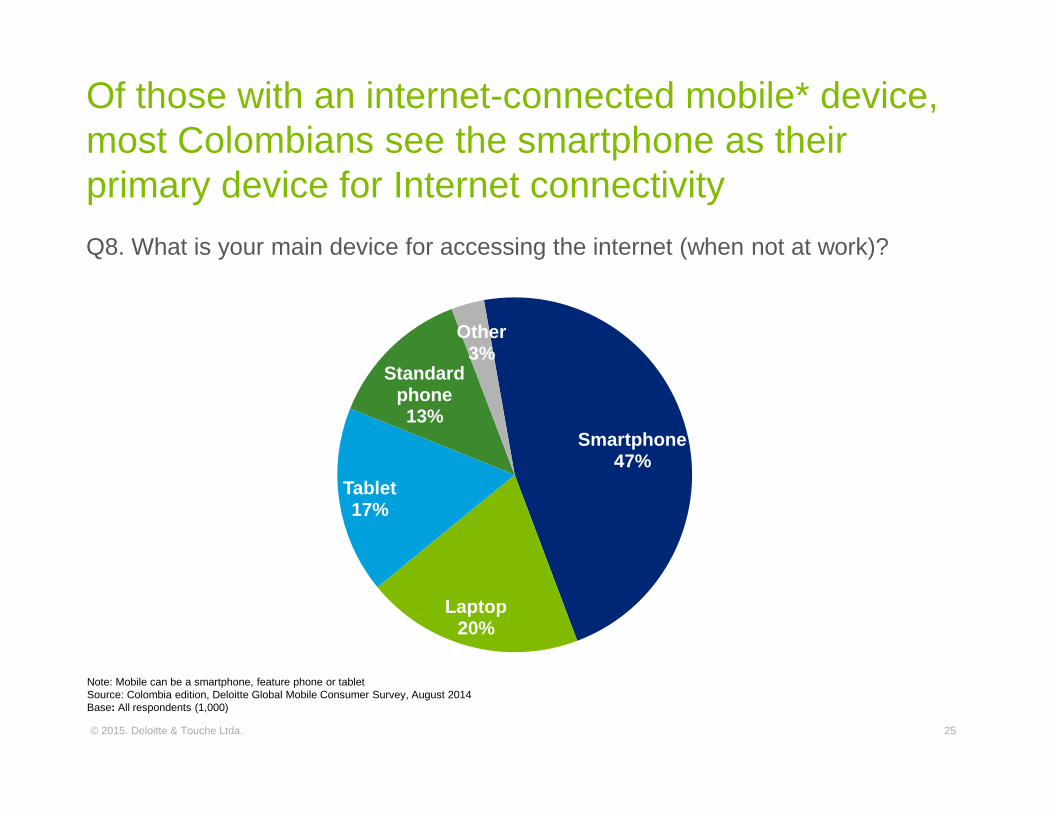

Q8. What is your main device for accessing the internet (when not at work)?

Smartphone47%

Laptop20%

Tablet17%

Standard phone13%

Other3%

Note: Mobile can be a smartphone, feature phone or tabletSource: Colombia edition, Deloitte Global Mobile Consumer Survey, August 2014Base: All respondents (1,000)

Of those with an internet-connected mobile* device, most Colombians see the smartphone as their primary device for Internet connectivity

25© 2015. Deloitte & Touche Ltda.

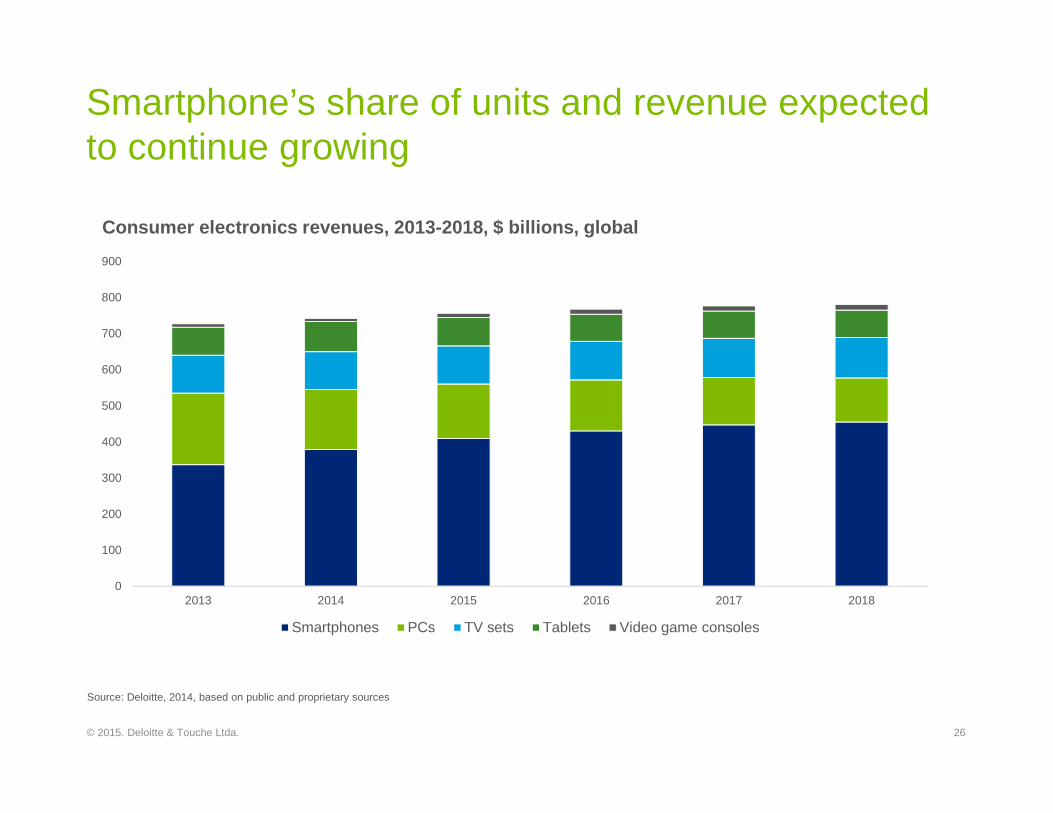

Smartphone’s share of units and revenue expected to continue growing

0

100

200

300

400

500

600

700

800

900

2013 2014 2015 2016 2017 2018

Smartphones PCs TV sets Tablets Video game consoles

Consumer electronics revenues, 2013-2018, $ billion s, global

Source: Deloitte, 2014, based on public and proprietary sources

26© 2015. Deloitte & Touche Ltda.

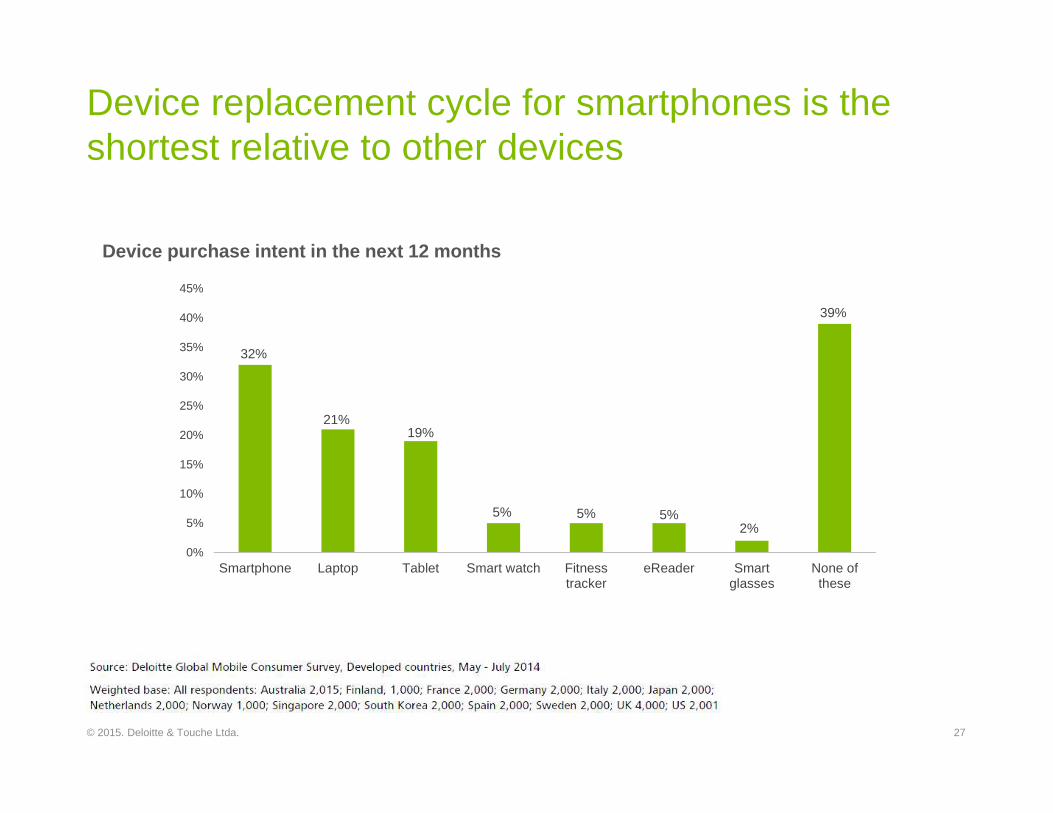

Device purchase intent in the next 12 months

32%

21%19%

5% 5% 5%2%

39%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Smartphone Laptop Tablet Smart watch Fitnesstracker

eReader Smartglasses

None ofthese

Device replacement cycle for smartphones is the shortest relative to other devices

27© 2015. Deloitte & Touche Ltda.

Bottom line

The smartphone is the most successful consumer device ever.

Challenges for smartphone vendors: retaining loyalty, taking share in a mature market, maintaining margin, determining which functionality their customers want.

Vendors will need to:

• Increment the range of intangible factors used to enhance their devices appeal: technical support, data transfer, perceived security of client data, caliber of app store.

• Ensure that all functionality addresses current needs and anticipates latent ones.

• Continue to work closely with carriers.

The selection process for enterprise smartphones can be more complex than for consumers:

• Some functionality may be not considered relevant from the COI point of view, but it is of interest to the HR department.

• Some phones may be of particular interest to different companies with different needs (waterproof devices for field workers, fingerprint readers and NFC chips for additional security).

One billion smartphone upgrades

28© 2015. Deloitte & Touche Ltda.

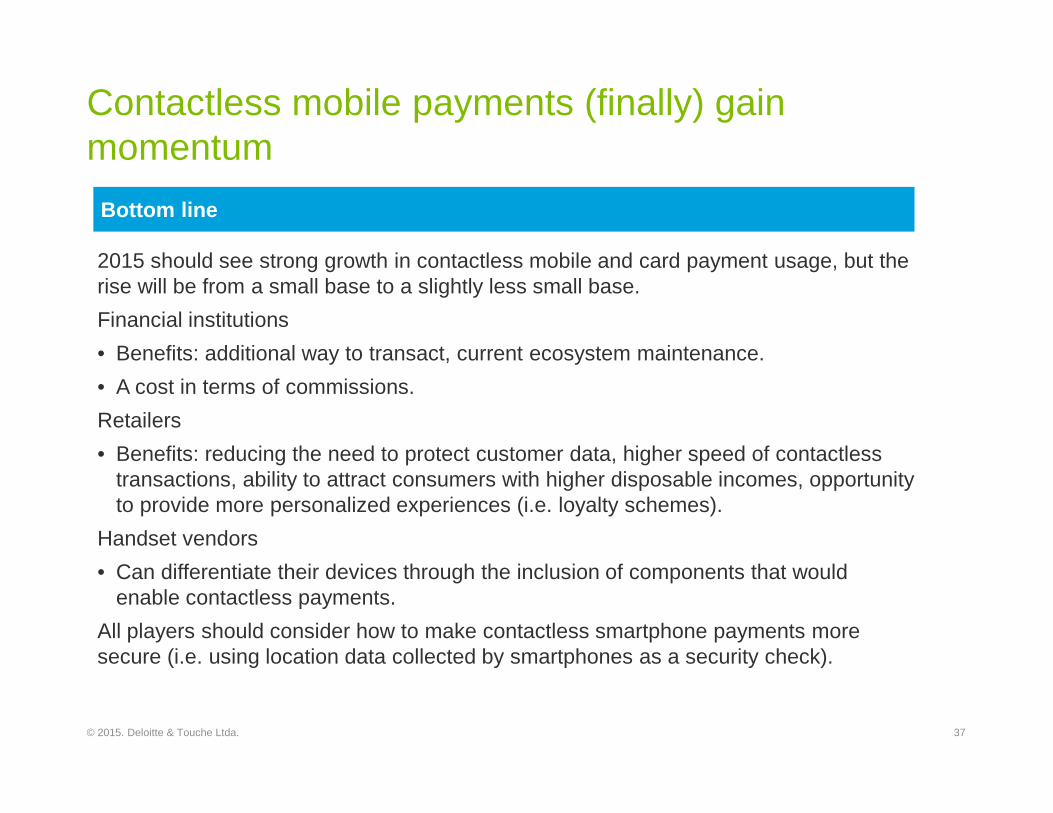

Contactless mobile payments (finally) gain momentum

29© 2015. Deloitte & Touche Ltda.

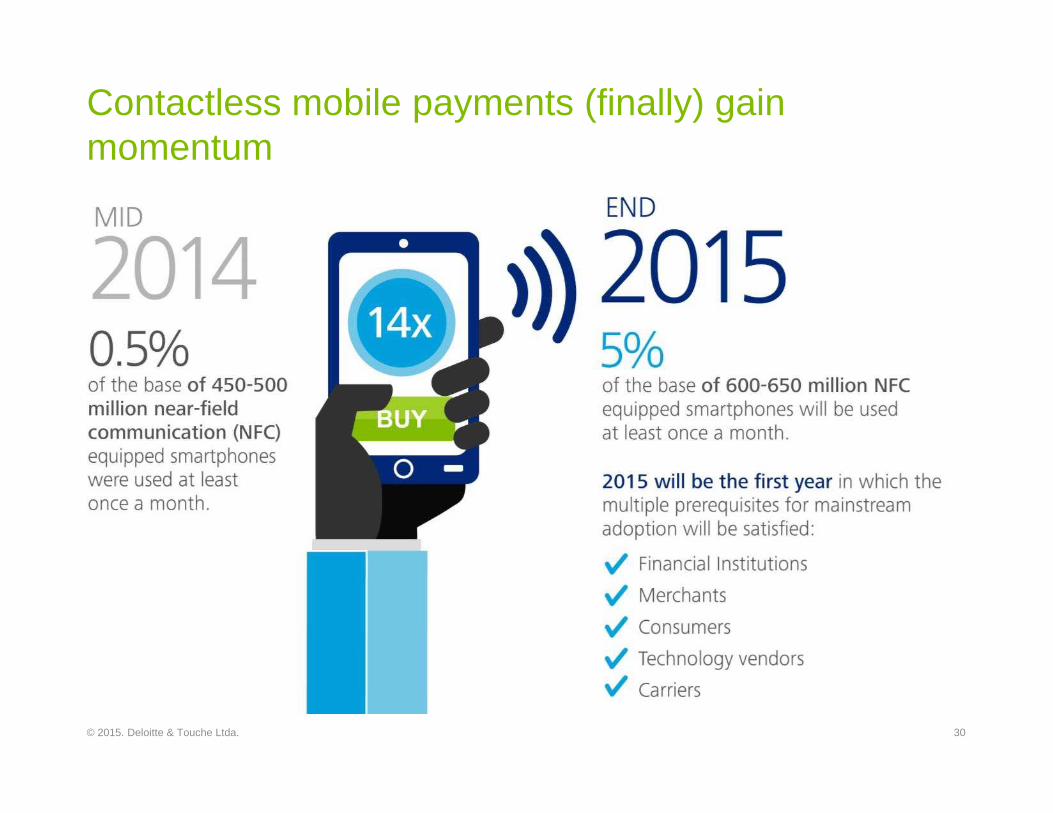

Contactless mobile payments (finally) gain momentum

30© 2015. Deloitte & Touche Ltda.

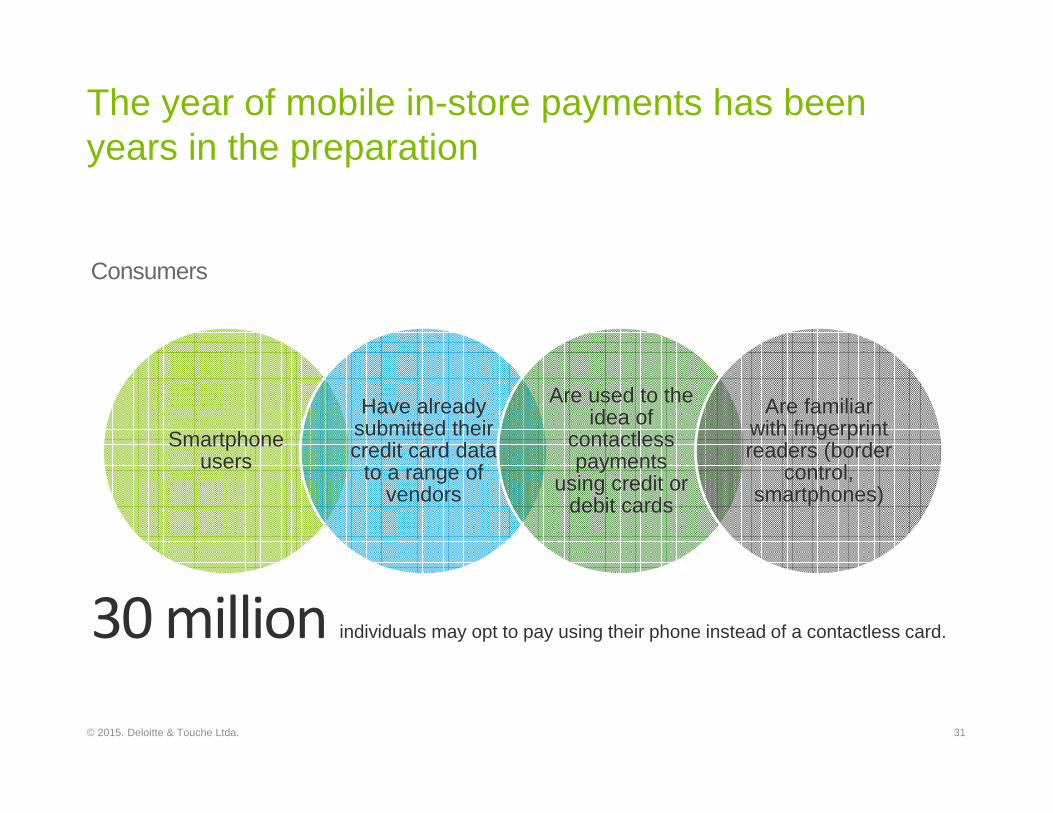

Consumers

30 million individuals may opt to pay using their phone instead of a contactless card.

The year of mobile in-store payments has been years in the preparation

Smartphone users

Have already submitted their credit card data

to a range of vendors

Are used to the idea of

contactless payments

using credit or debit cards

Are familiar with fingerprint readers (border

control, smartphones)

31© 2015. Deloitte & Touche Ltda.

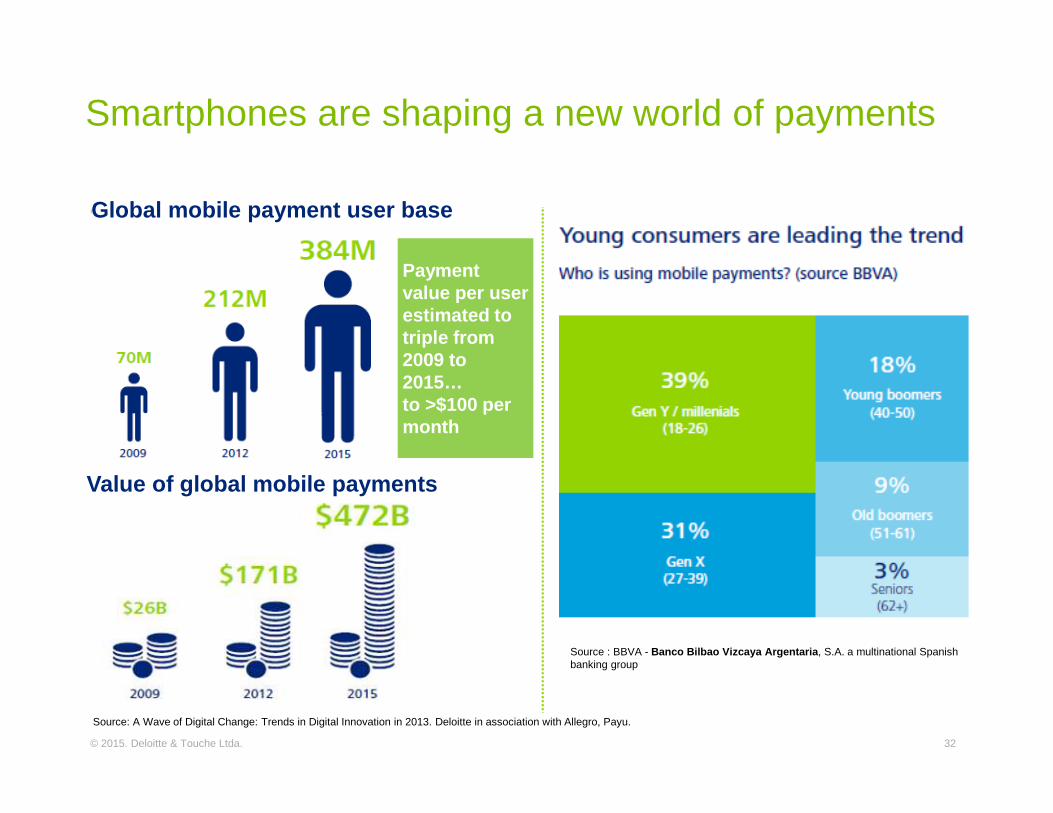

Source: A Wave of Digital Change: Trends in Digital Innovation in 2013. Deloitte in association with Allegro, Payu.

Source : BBVA - Banco Bilbao Vizcaya Argentaria, S.A. a multinational Spanish banking group

Payment value per user estimated to triple from 2009 to 2015…to >$100 per month

Value of global mobile payments

Smartphones are shaping a new world of payments

Global mobile payment user base

32© 2015. Deloitte & Touche Ltda.

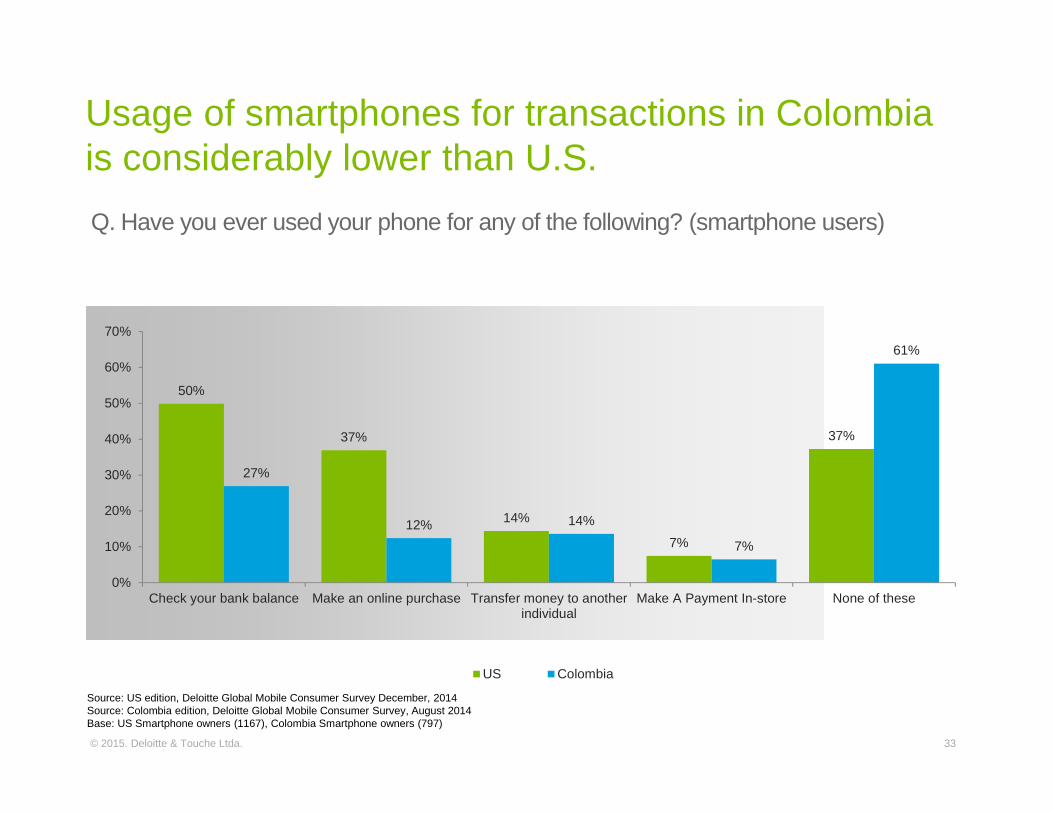

Usage of smartphones for transactions in Colombia is considerably lower than U.S.

50%

37%

14%

7%

37%

27%

12% 14%

7%

61%

0%

10%

20%

30%

40%

50%

60%

70%

Check your bank balance Make an online purchase Transfer money to anotherindividual

Make A Payment In-store None of these

US Colombia

Q. Have you ever used your phone for any of the following? (smartphone users)

Mobile-oriented

Source: US edition, Deloitte Global Mobile Consumer Survey December, 2014 Source: Colombia edition, Deloitte Global Mobile Consumer Survey, August 2014Base: US Smartphone owners (1167), Colombia Smartphone owners (797)

33© 2015. Deloitte & Touche Ltda.

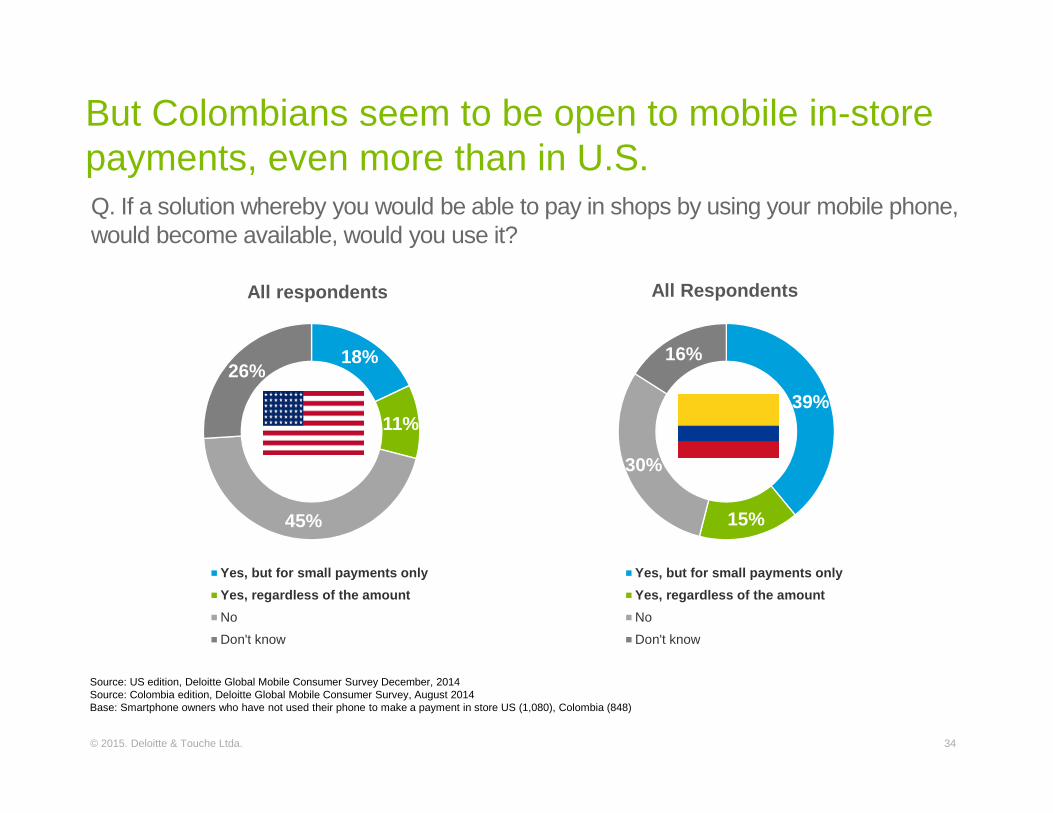

But Colombians seem to be open to mobile in-store payments, even more than in U.S.Q. If a solution whereby you would be able to pay in shops by using your mobile phone, would become available, would you use it?

18%

11%

45%

26%

Yes, but for small payments only

Yes, regardless of the amount

No

Don't know

All respondents

Source: US edition, Deloitte Global Mobile Consumer Survey December, 2014Source: Colombia edition, Deloitte Global Mobile Consumer Survey, August 2014Base: Smartphone owners who have not used their phone to make a payment in store US (1,080), Colombia (848)

39%

15%

30%

16%

All Respondents

Yes, but for small payments only

Yes, regardless of the amount

No

Don't know

34© 2015. Deloitte & Touche Ltda.

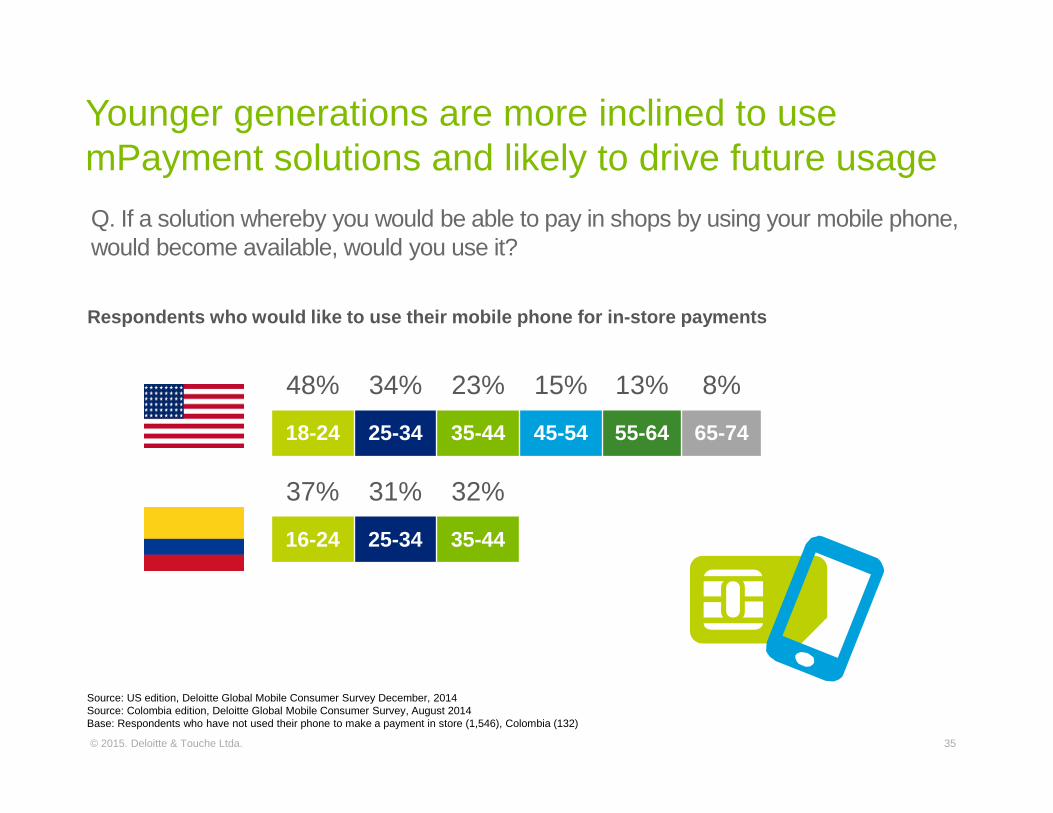

Younger generations are more inclined to use mPayment solutions and likely to drive future usage

Q. If a solution whereby you would be able to pay in shops by using your mobile phone, would become available, would you use it?

48% 34% 23% 15% 13% 8%

18-24 25-34 35-44 45-54 55-64 65-74

Respondents who would like to use their mobile phon e for in-store payments

Source: US edition, Deloitte Global Mobile Consumer Survey December, 2014Source: Colombia edition, Deloitte Global Mobile Consumer Survey, August 2014Base: Respondents who have not used their phone to make a payment in store (1,546), Colombia (132)

37% 31% 32%

16-24 25-34 35-44

35© 2015. Deloitte & Touche Ltda.

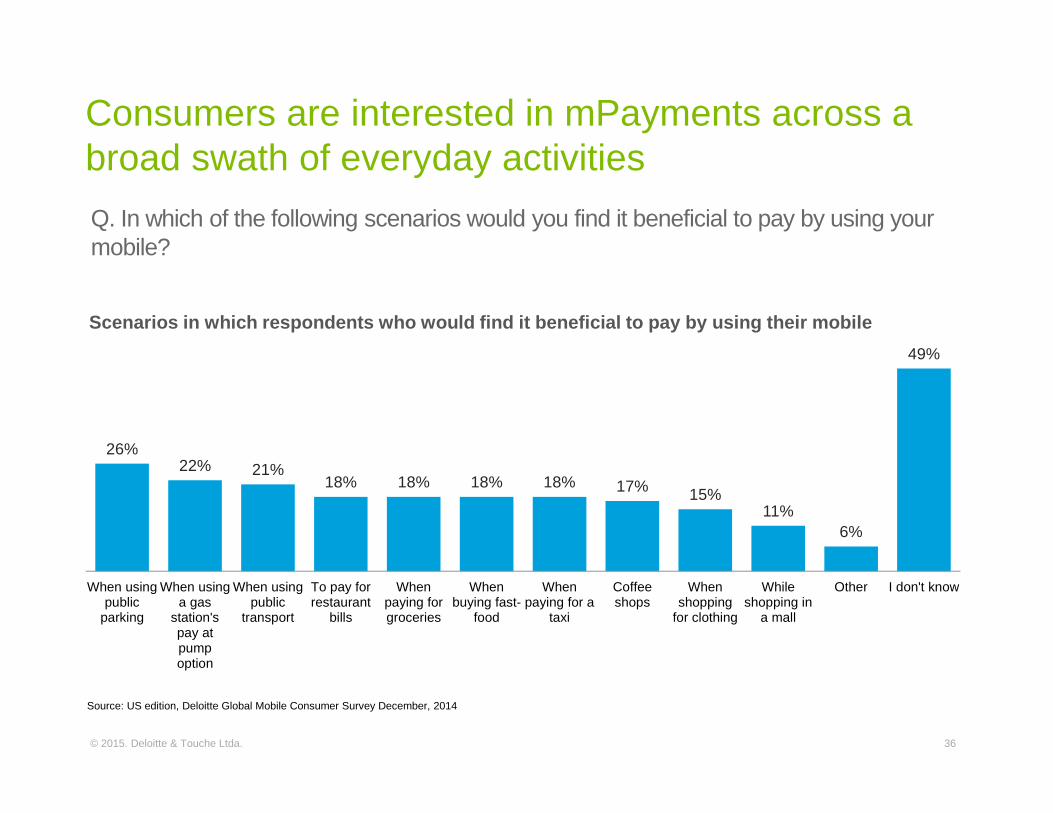

Consumers are interested in mPayments across a broad swath of everyday activities

26%22% 21%

18% 18% 18% 18% 17% 15%11%

6%

49%

When usingpublic

parking

When usinga gas

station'spay atpumpoption

When usingpublic

transport

To pay forrestaurant

bills

Whenpaying forgroceries

Whenbuying fast-

food

Whenpaying for a

taxi

Coffeeshops

Whenshopping

for clothing

Whileshopping in

a mall

Other I don't know

Q. In which of the following scenarios would you find it beneficial to pay by using your mobile?

Scenarios in which respondents who would find it be neficial to pay by using their mobile

Source: US edition, Deloitte Global Mobile Consumer Survey December, 2014

36© 2015. Deloitte & Touche Ltda.

Contactless mobile payments (finally) gain momentum

Bottom line

2015 should see strong growth in contactless mobile and card payment usage, but the rise will be from a small base to a slightly less small base.

Financial institutions

• Benefits: additional way to transact, current ecosystem maintenance.

• A cost in terms of commissions.

Retailers

• Benefits: reducing the need to protect customer data, higher speed of contactless transactions, ability to attract consumers with higher disposable incomes, opportunity to provide more personalized experiences (i.e. loyalty schemes).

Handset vendors

• Can differentiate their devices through the inclusion of components that would enable contactless payments.

All players should consider how to make contactless smartphone payments more secure (i.e. using location data collected by smartphones as a security check).

37© 2015. Deloitte & Touche Ltda.

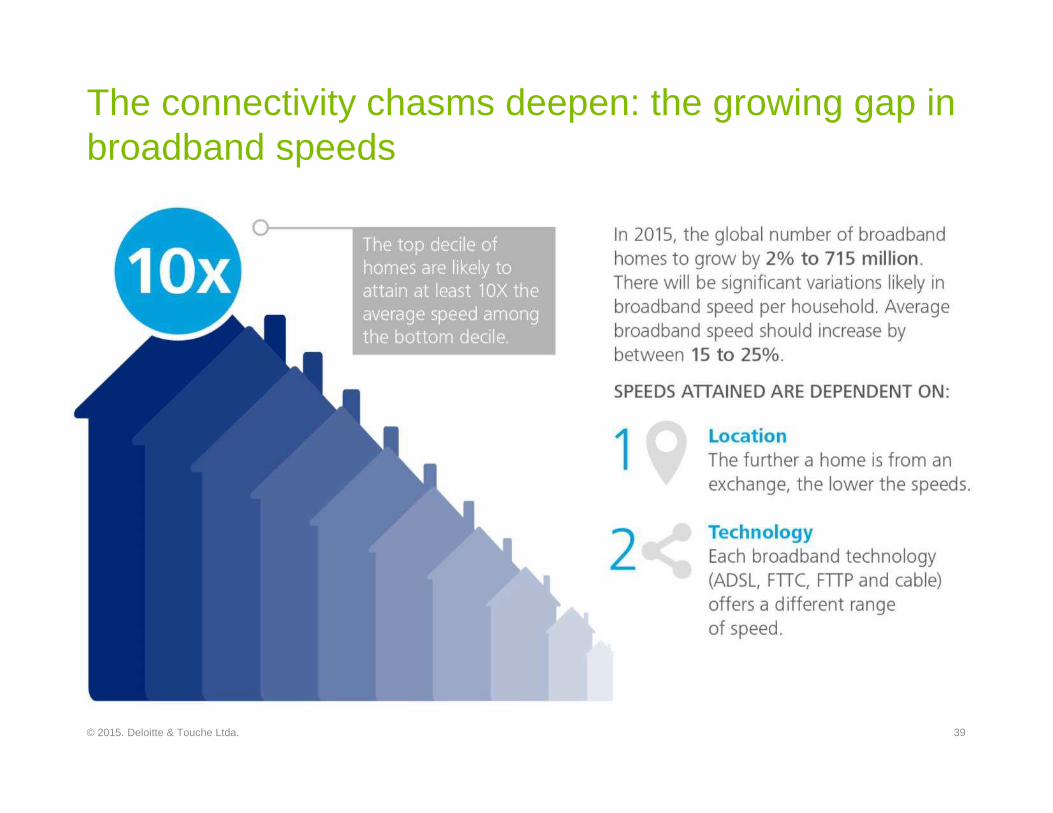

The connectivity chasms deepen: the growing gap in broadband speeds

38© 2015. Deloitte & Touche Ltda.

The connectivity chasms deepen: the growing gap in broadband speeds

39© 2015. Deloitte & Touche Ltda.

-

20

40

60

80

100

120

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Ave

rage

dow

nstr

eam

ban

dwid

th,

Mbi

t/s

Axis Title

Fibre DSL Cable

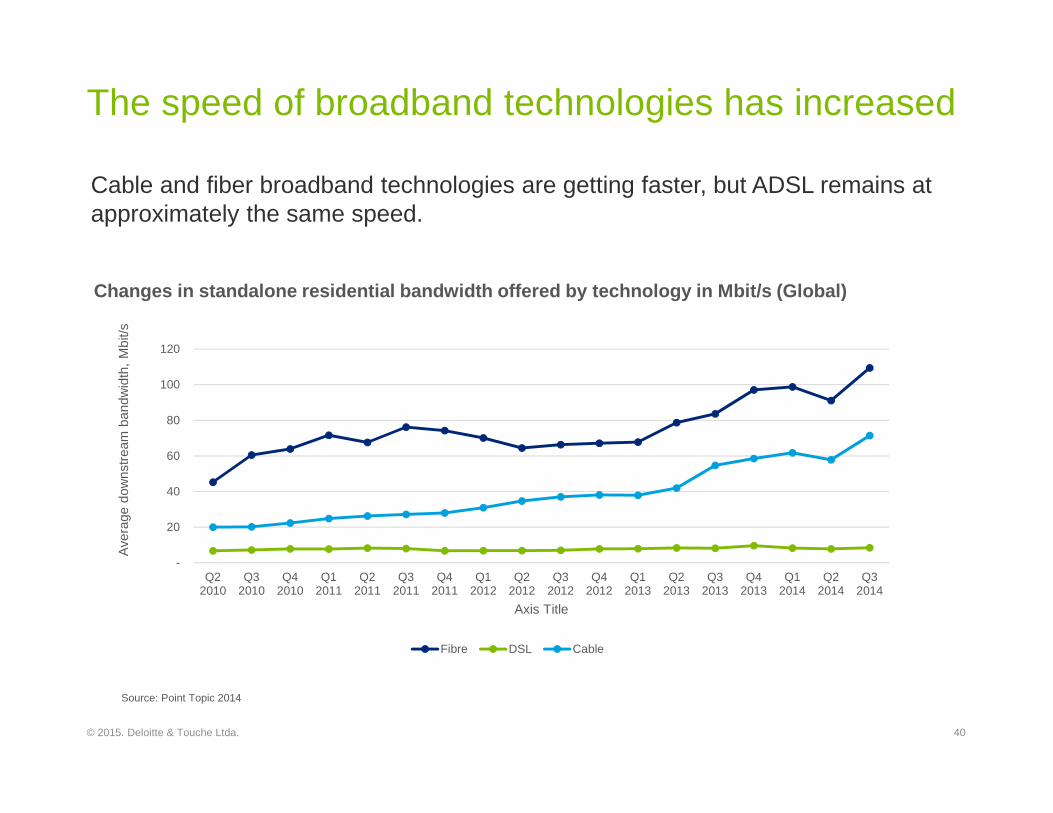

Cable and fiber broadband technologies are getting faster, but ADSL remains at approximately the same speed.

The speed of broadband technologies has increased

Changes in standalone residential bandwidth offered by technology in Mbit/s (Global)

Source: Point Topic 2014

40© 2015. Deloitte & Touche Ltda.

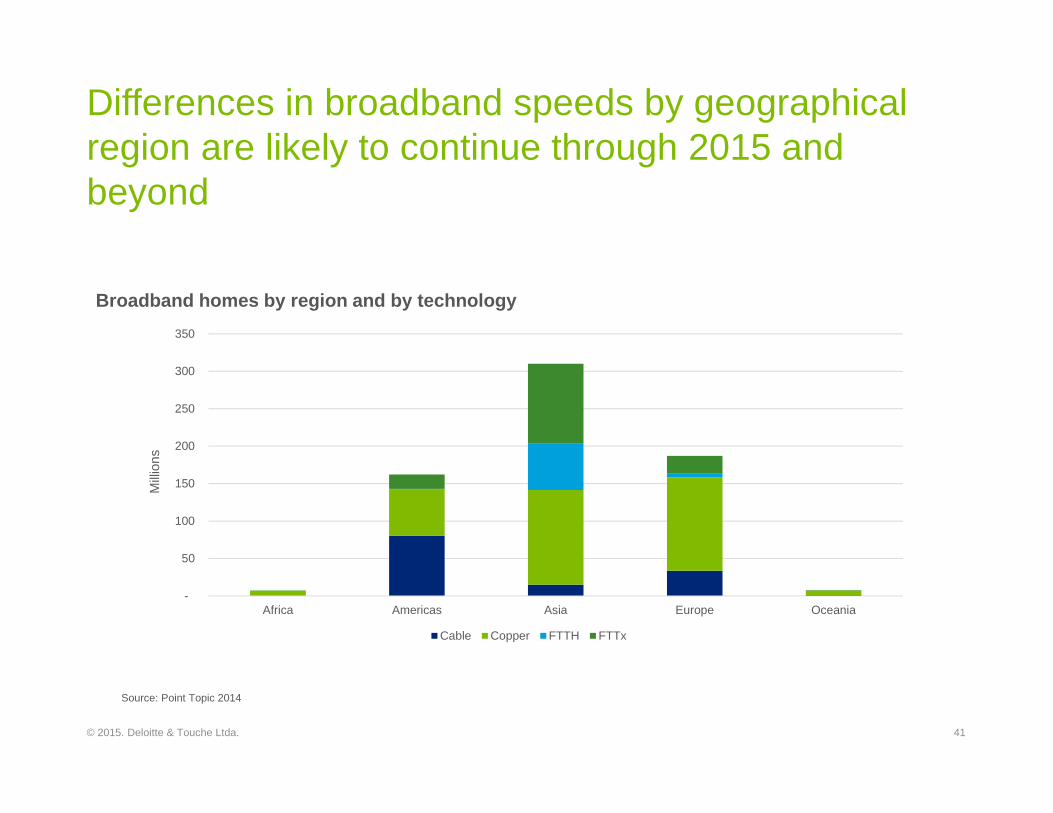

Differences in broadband speeds by geographical region are likely to continue through 2015 and beyond

41© 2015. Deloitte & Touche Ltda.

-

50

100

150

200

250

300

350

Africa Americas Asia Europe Oceania

Mill

ions

Cable Copper FTTH FTTx

Broadband homes by region and by technology

Source: Point Topic 2014

The connectivity chasms deepen: the growing gap in broadband speeds

Bottom line

The gulf between those with access to the fastest broadband speeds and those on basic speeds has widened over recent years; and in the near term looks likely to increase further.

Regulators should:

• Update the definition of broadband regularly. In the future, speed will still be key, but upstream speed will become increasingly important as broadband usage evolves.

• Consider how price per megabit is affected by technology. ADSL households have lower speed and pay more per Mbit/s.

Any private or public entity looking to deliver OTT services should consider what ranges of broadband speeds households are able to get:

• Households wishing to have on-demand video service may need to be offered alternative approaches.

• The richest online shopping experiences require fast broadband connections.

In the long-term there is ample opportunity for more disruptive innovation with broadband delivery, including hot air balloons to deliver high speed connections to rural areas (3G type speed).

42© 2015. Deloitte & Touche Ltda.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, consulting, financial advisory, risk management, tax, and related services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 210,000 professionals are committed to becoming the standard of excellence.

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this publication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication.

© 2015. Deloitte & Touche Ltda. 43© 2015. Deloitte & Touche Ltda.

ERROR: syntaxerror

OFFENDING COMMAND: --nostringval--

STACK:

/Title

()

/Subject

(D:20150524210830-05’00’)

/ModDate

()

/Keywords

(PDFCreator Version 0.9.5)

/Creator

(D:20150524210830-05’00’)

/CreationDate

(NVALERO)

/Author

-mark-

![PREDICCIONES 2014 -[Revisadas]](https://img.pdfslide.tips/doc/110x75/577cd31a1a28ab9e7896b288/predicciones-2014-revisadas.jpg)