Embed Size (px)

Citation preview

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 1/13

Please refer to important disclosures at the end of this report 1

Quarterly highlights – (Consolidated)

Particulars (` cr) 4QFY13 4QFY12 % chg (yoy) 3QFY13 % chg (qoq)

Net sales 12,609 10,763 17.2 10,692 17.9

EBITDA 3,307 2,705 22.2 2,327 42.1

% margin 26.2 25.1 109bp 21.8 446bp

Adjusted PAT 1,964 1,377 42.6 1,254 56.6

Source: Company, Angel Research

Sterlite Industries (Sterlite) reported better-than-expected 4QFY2013 results. Both,

the top-line as well as the net profit were above our expectations, mainly due to

better-than-expected performance from the Copper and Zinc segments.We

recommend Accumulate rating on the stock.

Top-line growth driven by all the segments: The company’s net sales grew 17.2%

yoy to ` 12,609cr. The growth was driven by increase in all the segments’

revenues. Aluminium, Copper and Zinc segment revenues grew 9.8%, 16.9 and

21.6% yoy to ` 954cr, ` 5,783cr and ` 4,950cr, respectively

Copper segment profitability surprises: On the operating front, Sterlite’s EBITDA

grew 22.2% yoy to ` 3,307cr and EBITDA margin improved by 109bp yoy to

26.2% (above our estimate of 23.1%) because of improved profitability across all

segments. Copper segment’s profitability was above our estimate as its EBIT

improved by 22.5% yoy due to higher volumes and power sales from the 80MW

captive power plant, although partially offset by higher costs of production).

Lower interest costs and higher other income boost PAT: Interest costs declined by

15.9% yoy to ` 276cr and other income grew by 13.5% yoy to ` 798cr. Tax rate

was also lower at 12.1% compared to 16.8% in 4QFY2012; hence, adjusted net

profit increased by 42.6% yoy to ` 1,964cr, which was above our estimate of

` 1,522cr.

Outlook and valuation: We expect Sterlite to benefit from the expansion of

Zinc-Lead smelting capacity during FY2014-15 although its Aluminium segment’s

profitability is expected to remain under pressure. Considering the ongoing process

of group restructuring by the promoter, Vedanta Resources, the valuation of Sterlite

will mirror the valuation of the consolidated company - Sesa Sterlite. We recommend

Accumulate rating on the stock.

Key financials (Consolidated)Y/E March ( ` cr) FY2012 FY2013E FY2014E FY2015E

Net sales 41,179 45,162 44,462 45,568

% chg 35.3 9.7 -1.5 2.5

Net profit 4,828 6,060 6,092 6,787

% chg -4.3 25.5 0.5 11.4

FDEPS (`) 15.5 18.3 18.1 20.2

OPM (%) 24.0 23.2 23.2 24.7

P/E(x) 6.1 5.2 5.2 4.7

P/BV(x) 0.7 0.6 0.6 0.5

RoE(%) 11.0 12.5 11.3 11.4RoCE(%) 11.3 10.2 8.4 8.5

EV/Sales (x) 0.7 0.6 0.6 0.5

EV/EBITDA (x) 2.8 2.5 2.4 2.0

Source: Company, Angel Research

ACCUMULATECMP ` 95

Target Price ` 100

Investment Period 12 months

Stock Info

Sector

Net Debt ( ` cr) (6,234)

Bloomberg Code

Shareholding Pattern (%)

Promoters 53.3

MF / Banks / Indian Fls 9.3

FII / NRIs / OCBs 27.6

Indian Public / Others 9.8

Abs. (%) 3m 1yr 3yr

Sensex (3.0) 13.5 11.1

STLT (16.3) (9.7) (53.9)

52 Week High / Low 123/83

Base Metals

Market Cap ( ` cr) 32,077

Beta 1.5

Avg. Daily Volume 615,888

Face Value ( ` ) 1

BSE Sensex 19,504

Nifty 5,930

Reuters Code STRL.BO

STLT@IN

Bhavesh Chauhan

Tel: 022- 39357600 Ext: 6821

Vinay Rachh

Tel: 022- 39357600 Ext: 6841

Sterlite Industries

Performance Highlights

4QFY2013 Result Update | Base Metals

April 30, 2013

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 2/13

Sterlite Industries | 4QFY2013 Result Update

April 30, 2013 2

Exhibit 1: 4QFY2013 Performance (Consolidated)

Y/E March (` cr) 4QFY13 4QFY12 % chg yoy 3QFY13 % chg qoq FY2013 FY2012 % chg yoy

Net Sales 12,609 10,763 17.2 10,692 17.9 44,922 40,967 9.7

- Consumption of Raw Material 5,772 4,854 18.9 5,023 14.9 20,883 18,832 10.9(% of Net Sales) 45.8 45.1 47.0 46.5 46.0

- Power& Fuel 1,081 991 9.1 1,008 7.3 4,420 4,040 9.4

(% of Net Sales) 8.6 9.2 9.4 9.8 9.9

- Staff Costs 503 415 21.3 475 6.1 1,880 1,612 16.6

(% of Net Sales) 4.0 3.9 4.4 4.2 3.9

- Other expenses 2,010 1,854 8.4 1,906 5.5 7,454 6,819 9.3

(% of Net Sales) 15.9 17.2 17.8 16.6 16.6

Total Expenditure 9,367 8,113 15.5 8,411 11.4 34,637 31,304 10.6

(% of Net Sales) 74.3 75.4 78.7 77.1 76.4

Other operating Income 65 56 15.1 45 43.2 240 212 13.4

EBITDA 3,307 2,705 22.2 2,327 42.1 10,469 9,863 6.1

EBITDA margin (%) 26.2 25.1 21.8 23.3 24.1

Interest 276 328 (15.9) 227 21.6 922 852 8.2

Depreciation 453 507 (10.6) 538 (15.8) 2,032 1,830 11.0

Other Income 798 704 13.5 859 (7.1) 3,453 3,163 9.2

Exceptional Items (40) (100) (63) (101) (473) (78.7)

Profit before Tax 3,454 2,905 18.9 2,358 46.5 10,867 9,872 10.1

(% of Net Sales) 27.4 27.0 22.1 24.2 24.1

Tax 418 487 (14.1) 356 17.6 1,618 2,111 (23.3)

(% of PBT) 12.1 16.8 15.1 14.9 21.4

Minority Interest 787 550 43.2 585.3 2,529 2,161 17.0

Share of profit/(loss) in associate (206) (160) (226.1) (660) (772) (14.6)

Reported PAT 1,925 1,277 50.7 1,191 61.5 6,060 4,828 25.5

Net income margin (%) 15.3 11.9 11.1 13.5 11.8

FDEPS 5.7 3.6 58.7 3.5 61.9 18.3 15.5 18.2

Adj. net profit 1,964 1,377 42.6 1,254 56.6 6,146 5,200 18.2

Source: Company, Angel Research

Exhibit 2: 4QFY2013 – Actual vs Angel estimates

(` cr) Actual Estimates Variation (%)

Net sales 12,609 11,334 11.3

EBITDA 3,307 2,618 26.3

EBITDA margin (%) 26.2 23.1 312bp

Adj. net profit 1,964 1,522 29.1

Source: Company, Angel Research

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 3/13

Sterlite Industries | 4QFY2013 Result Update

April 30, 2013 3

4QFY2013 result highlights

Sterlite reported stronger-than-expected 4QFY2013 results. Both, the top-line as

well as net profit were above our expectations mainly due to higher-than-expected

performance from the Copper segment. The company’s net sales grew 17.2% yoy

to ` 12,609cr. The growth was driven by increase in all the segments’ revenues.

Aluminium, Copper and Zinc segment revenues grew 9.8%, 16.9 and 21.6% yoy

to ` 954cr, ` 5,783cr and ` 4,950cr, respectively. On the operating front, Sterlite’s

EBITDA grew 22.2% yoy to ` 3,307cr and EBITDA margin improved by 109bp yoy

to 26.2% (above our estimate of 23.1%) because of improved profitability across

segments. Copper segment’s profitability was above our estimate as its EBIT

improved by 22.5% yoy due to higher volumes and power sales from the 80MW

captive power plant, although partially offset by higher costs of production. The

company reported a few exceptional items relating to forex gain, penalty levied by

Supreme Court on the Tuticorin smelter leaks and VRS scheme. The interest costsduring the quarter declined by 15.9% yoy to ` 276cr and other income grew by

13.5% yoy to ` 798cr. The tax rate was also lower at 12.1% compared to 16.8% in

4QFY2012 and therefore the adjusted net profit increased by 42.6% yoy to

` 1,964cr, which was above our estimate of ` 1,522cr. The reported net profit

increased 50.7% yoy to ` 1,925cr.

Segmental performance

Copper segment’s profitability rises on higher power sales

During 4QFY2012, copper cathode production at the Tuticorin smelter increased7.0% yoy to 86k tonne. Metal mined from the Australian mines increased by

28.0% yoy to 7k tonne. Copper segment revenues increased by 16.9% yoy to

` 5,783cr during the quarter.

Copper Tc/Rcs decreased by 3.0% yoy to USc14.8/lb. The company reported cost

of production of USc10.7lb in 4QFY2013 compared to USc4.1/lb in 4QFY2012.

The Copper business had an exceptional item of ` 100cr related to penalty by

Supreme Court on Tuticorin smelter gas leak. However the Copper segment’s PAT

increased by 203.0% yoy to ` 322cr in 4QFY2013, mainly due to higher power

sales from the fully commissioned 80MW power plant at Tuticorin.

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 4/13

Sterlite Industries | 4QFY2013 Result Update

April 30, 2013 4

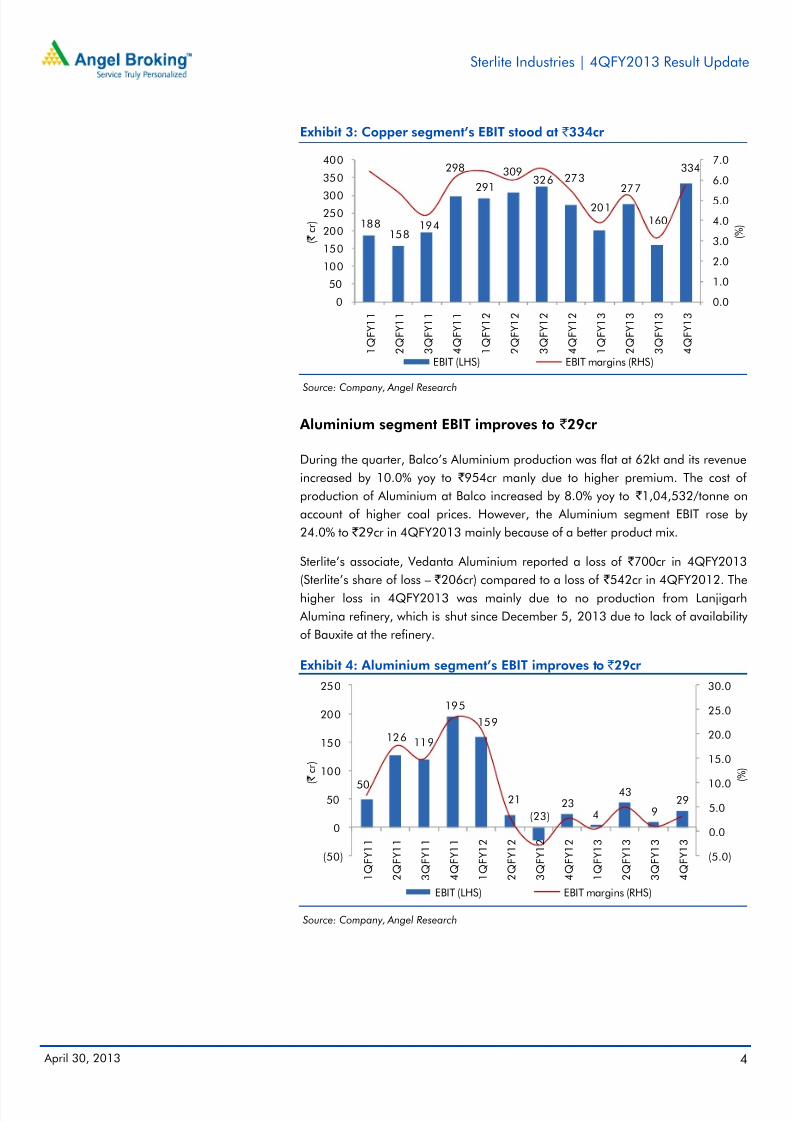

Exhibit 3: Copper segment’s EBIT stood at ` 334cr

Source: Company, Angel Research

Aluminium segment EBIT improves to ` 29cr

During the quarter, Balco’s Aluminium production was flat at 62kt and its revenue

increased by 10.0% yoy to ` 954cr manly due to higher premium. The cost of

production of Aluminium at Balco increased by 8.0% yoy to ` 1,04,532/tonne on

account of higher coal prices. However, the Aluminium segment EBIT rose by

24.0% to `29cr in 4QFY2013 mainly because of a better product mix.

Sterlite’s associate, Vedanta Aluminium reported a loss of ` 700cr in 4QFY2013

(Sterlite’s share of loss – ` 206cr) compared to a loss of ` 542cr in 4QFY2012. Thehigher loss in 4QFY2013 was mainly due to no production from Lanjigarh

Alumina refinery, which is shut since December 5, 2013 due to lack of availability

of Bauxite at the refinery.

Exhibit 4: Aluminium segment’s EBIT improves to ` 29cr

Source: Company, Angel Research

188158

194

298

291

309326 273

201277

160

334

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

0

50

100

150

200

250

300

350

400

1 Q F Y 1 1

2 Q F Y 1 1

3 Q F Y 1 1

4 Q F Y 1 1

1 Q F Y 1 2

2 Q F Y 1 2

3 Q F Y 1 2

4 Q F Y 1 2

1 Q F Y 1 3

2 Q F Y 1 3

3 Q F Y 1 3

4 Q F Y 1 3

( % )

( `

c r )

EBIT (LHS) EBIT margins (RHS)

50

126 119

195

159

21

(23)23

4

43

929

(5.0)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

(50)

0

50

100

150

200

250

1 Q F Y 1 1

2 Q F Y 1 1

3 Q F Y 1 1

4 Q F Y 1 1

1 Q F Y 1 2

2 Q F Y 1 2

3 Q F Y 1 2

4 Q F Y 1 2

1 Q F Y 1 3

2 Q F Y 1 3

3 Q F Y 1 3

4 Q F Y 1 3

( %

)

( `

c r )

EBIT (LHS) EBIT margins (RHS)

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 5/13

Sterlite Industries | 4QFY2013 Result Update

April 30, 2013 5

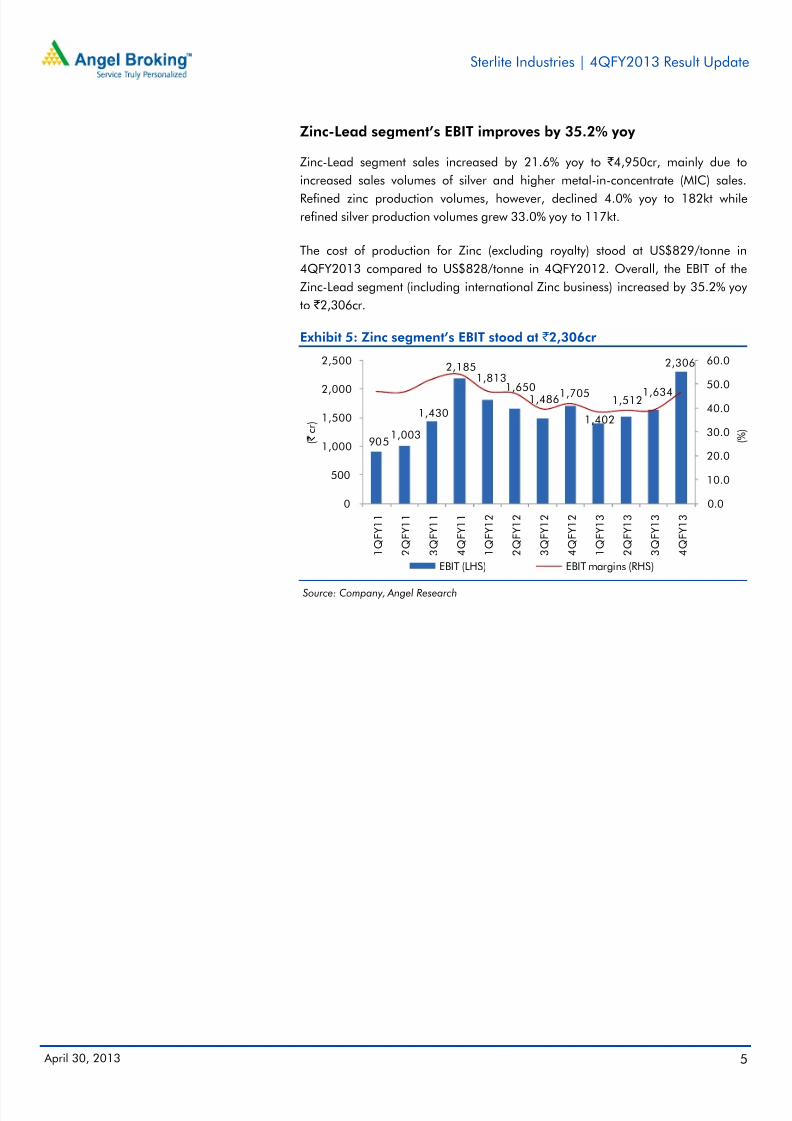

Zinc-Lead segment’s EBIT improves by 35.2% yoy

Zinc-Lead segment sales increased by 21.6% yoy to ` 4,950cr, mainly due to

increased sales volumes of silver and higher metal-in-concentrate (MIC) sales.

Refined zinc production volumes, however, declined 4.0% yoy to 182kt while

refined silver production volumes grew 33.0% yoy to 117kt.

The cost of production for Zinc (excluding royalty) stood at US$829/tonne in

4QFY2013 compared to US$828/tonne in 4QFY2012. Overall, the EBIT of the

Zinc-Lead segment (including international Zinc business) increased by 35.2% yoy

to ` 2,306cr.

Exhibit 5: Zinc segment’s EBIT stood at ` 2,306cr

Source: Company, Angel Research

9051,003

1,430

2,1851,813

1,6501,486

1,705

1,402

1,5121,634

2,306

0.0

10.0

20.0

30.0

40.0

50.0

60.0

0

500

1,000

1,500

2,000

2,500

1 Q F Y 1 1

2 Q F Y 1 1

3 Q F Y 1 1

4 Q F Y 1 1

1 Q F Y 1 2

2 Q F Y 1 2

3 Q F Y 1 2

4 Q F Y 1 2

1 Q F Y 1 3

2 Q F Y 1 3

3 Q F Y 1 3

4 Q F Y 1 3

( % )

( `

c r )

EBIT (LHS) EBIT margins (RHS)

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 6/13

Sterlite Industries | 4QFY2013 Result Update

April 30, 2013 6

Investment rationale

Zinc-Lead expansion to aid growth: Sterlite’s subsidiary, Hindustan Zinc (HZL) has

commenced work at its underground Kayar mine, which has 11mn tonne of high-

grade reserves (10-12% zinc content). The company expects to increase its capacity

from 1.0mn tonne to 1.2mn tonne. Moreover, given the cash-rich balance sheet,

HZL is actively exploring greenfield projects through prospecting licenses and

mining lease projects across different states.

Ban on Sesa Goa’s mines in Goa remains a concern: During 2QFY2013, the Goa

government had imposed a ban on iron ore mining in Goa until further review.

Later, the Ministry of Environment and Forest Clearances (MOEF) also suspended

environment clearances to all functional mining leases in Goa. Sesa Goa operated

several mines in the region with an annual production of 12mn tonne. While we

believe the ban could be temporary, there are chances of iron ore production cap

by the government/MOEF which could affect Sesa’s production going forward. This

is likely to be a key overhang on the stock in our view.

Outlook and Valuation

We expect Sterlite to benefit from the expansion of Zinc-Lead smelting capacity

during FY2014-15. While we expect the Aluminium segment’s profitability to

remain under pressure, the current stock price factors these concerns.

Considering the ongoing process of group restructuring by the promoter, Vedanta

Resources, the valuation of Sterlite will mirror the valuation of the consolidated

company - Sesa Sterlite. We value Sterlite at `100, based on the SOTP

methodology and recommend Accumulate rating on the stock.

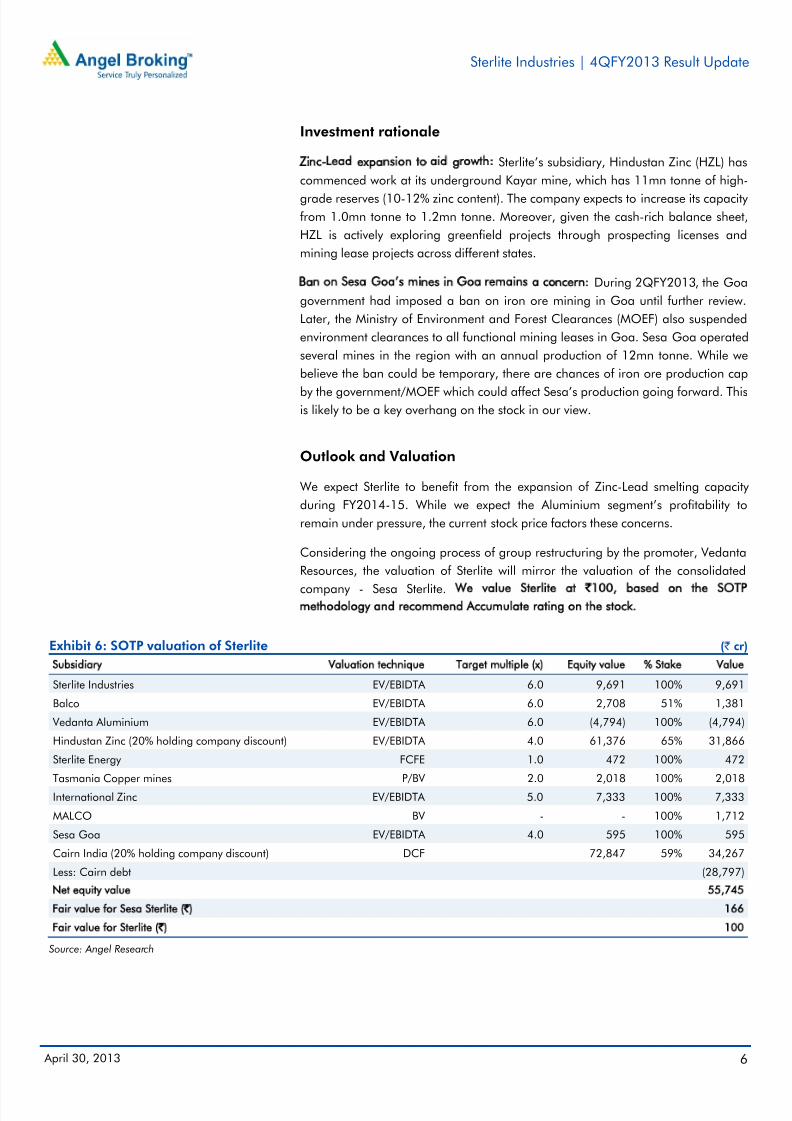

Exhibit 6: SOTP valuation of Sterlite ( ` cr)

Subsidiary Valuation technique Target multiple (x) Equity value % Stake Value

Sterlite Industries EV/EBIDTA 6.0 9,691 100% 9,691

Balco EV/EBIDTA 6.0 2,708 51% 1,381

Vedanta Aluminium EV/EBIDTA 6.0 (4,794) 100% (4,794)

Hindustan Zinc (20% holding company discount) EV/EBIDTA 4.0 61,376 65% 31,866

Sterlite Energy FCFE 1.0 472 100% 472

Tasmania Copper mines P/BV 2.0 2,018 100% 2,018

International Zinc EV/EBIDTA 5.0 7,333 100% 7,333

MALCO BV - - 100% 1,712

Sesa Goa EV/EBIDTA 4.0 595 100% 595

Cairn India (20% holding company discount) DCF 72,847 59% 34,267

Less: Cairn debt (28,797)

Net equity value 55,745

Fair value for Sesa Sterlite (`) 166

Fair value for Sterlite (`) 100

Source: Angel Research

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 7/13

Sterlite Industries | 4QFY2013 Result Update

April 30, 2013 7

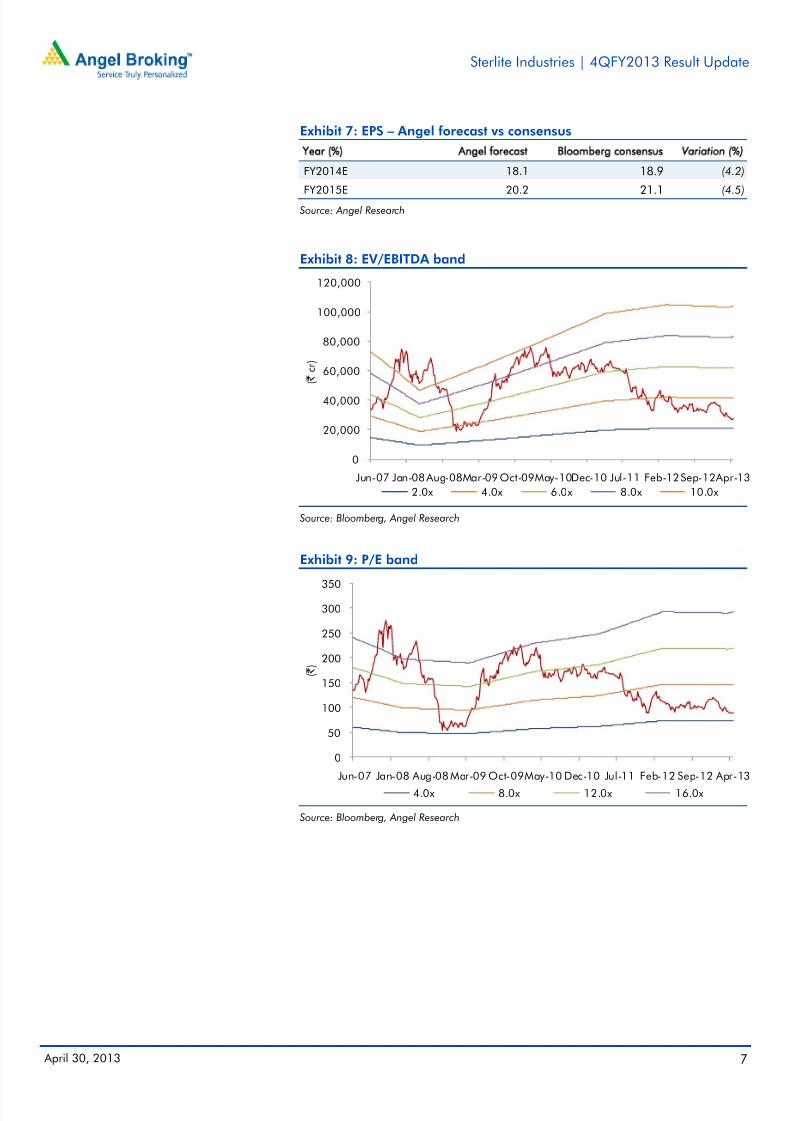

Exhibit 7: EPS – Angel forecast vs consensus

Year (%) Angel forecast Bloomberg consensus Variation (%)

FY2014E 18.1 18.9 (4.2)

FY2015E 20.2 21.1 (4.5) Source: Angel Research

Exhibit 8: EV/EBITDA band

Source: Bloomberg, Angel Research

Exhibit 9: P/E band

Source: Bloomberg, Angel Research

0

20,000

40,000

60,000

80,000

100,000

120,000

Jun-07 Jan-08Aug-08Mar-09Oct-09May-10Dec-10 Jul-11 Feb-12Sep-12Apr-13

( ` c r )

2.0x 4.0x 6.0x 8.0x 10.0x

0

50

100

150

200

250

300

350

Jun-07 Jan-08 Aug-08 Mar-09 Oct-09May-10 Dec-10 Jul-11 Feb-12 Sep-12 Apr-13

( ` )

4.0x 8.0x 12.0x 16.0x

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 8/13

Sterlite Industries | 4QFY2013 Result Update

April 30, 2013 8

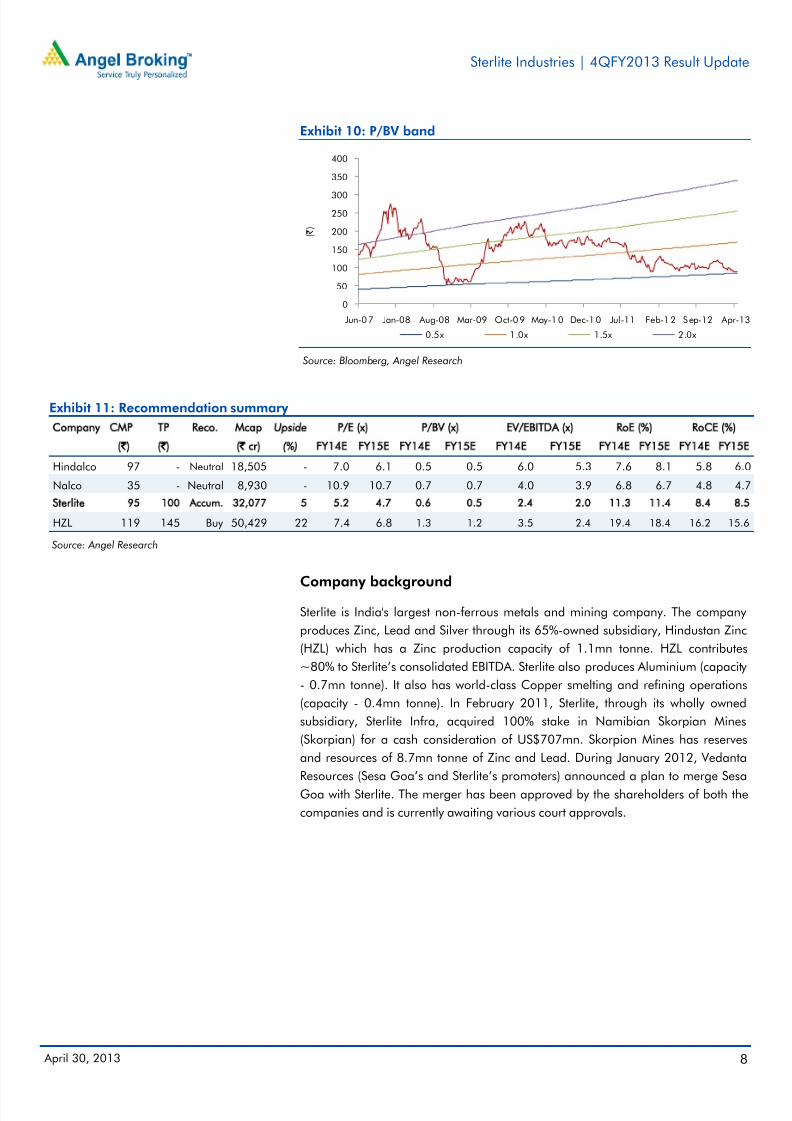

Exhibit 10: P/BV band

Source: Bloomberg, Angel Research

Exhibit 11: Recommendation summary

Company CMP TP Reco. Mcap Upside P/E (x) P/BV (x) EV/EBITDA (x) RoE (%) RoCE (%)

(`) (`) (` cr) (%) FY14E FY15E FY14E FY15E FY14E FY15E FY14E FY15E FY14E FY15E

Hindalco 97 - Neutral 18,505 - 7.0 6.1 0.5 0.5 6.0 5.3 7.6 8.1 5.8 6.0

Nalco 35 - Neutral 8,930 - 10.9 10.7 0.7 0.7 4.0 3.9 6.8 6.7 4.8 4.7

Sterlite 95 100 Accum. 32,077 5 5.2 4.7 0.6 0.5 2.4 2.0 11.3 11.4 8.4 8.5

HZL 119 145 Buy 50,429 22 7.4 6.8 1.3 1.2 3.5 2.4 19.4 18.4 16.2 15.6

Source: Angel Research

Company background

Sterlite is India's largest non-ferrous metals and mining company. The company

produces Zinc, Lead and Silver through its 65%-owned subsidiary, Hindustan Zinc

(HZL) which has a Zinc production capacity of 1.1mn tonne. HZL contributes

~80% to Sterlite’s consolidated EBITDA. Sterlite also produces Aluminium (capacity

- 0.7mn tonne). It also has world-class Copper smelting and refining operations

(capacity - 0.4mn tonne). In February 2011, Sterlite, through its wholly owned

subsidiary, Sterlite Infra, acquired 100% stake in Namibian Skorpian Mines

(Skorpian) for a cash consideration of US$707mn. Skorpion Mines has reserves

and resources of 8.7mn tonne of Zinc and Lead. During January 2012, Vedanta

Resources (Sesa Goa’s and Sterlite’s promoters) announced a plan to merge SesaGoa with Sterlite. The merger has been approved by the shareholders of both the

companies and is currently awaiting various court approvals.

0

50

100

150

200

250

300

350

400

Jun-07 Jan-08 Aug-08 Mar-09 Oct-09 May-10 Dec-10 Jul-11 Feb-12 Sep-12 Apr-13

( ` )

0.5x 1.0x 1.5x 2.0x

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 9/13

Sterlite Industries | 4QFY2013 Result Update

April 30, 2013 9

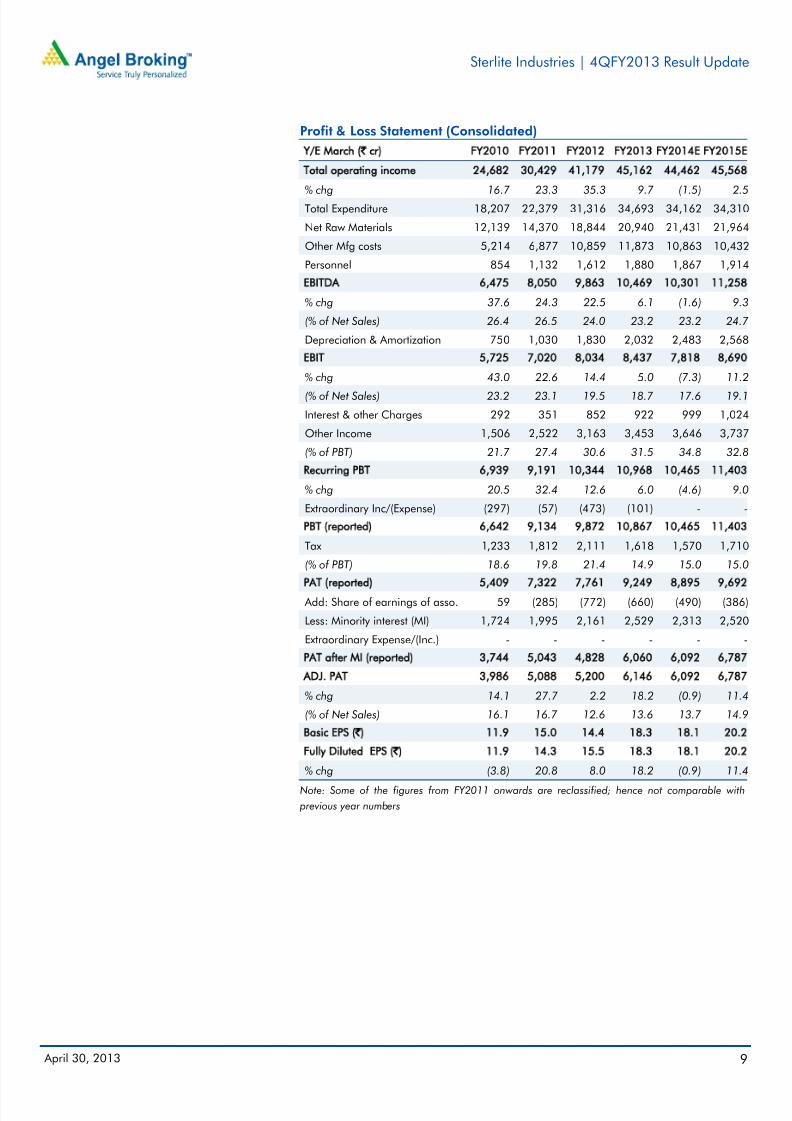

Profit & Loss Statement (Consolidated)

Y/E March (` cr) FY2010 FY2011 FY2012 FY2013 FY2014E FY2015E

Total operating income 24,682 30,429 41,179 45,162 44,462 45,568

% chg 16.7 23.3 35.3 9.7 (1.5) 2.5Total Expenditure 18,207 22,379 31,316 34,693 34,162 34,310

Net Raw Materials 12,139 14,370 18,844 20,940 21,431 21,964

Other Mfg costs 5,214 6,877 10,859 11,873 10,863 10,432

Personnel 854 1,132 1,612 1,880 1,867 1,914

EBITDA 6,475 8,050 9,863 10,469 10,301 11,258

% chg 37.6 24.3 22.5 6.1 (1.6) 9.3

(% of Net Sales) 26.4 26.5 24.0 23.2 23.2 24.7

Depreciation & Amortization 750 1,030 1,830 2,032 2,483 2,568

EBIT 5,725 7,020 8,034 8,437 7,818 8,690

% chg 43.0 22.6 14.4 5.0 (7.3) 11.2

(% of Net Sales) 23.2 23.1 19.5 18.7 17.6 19.1

Interest & other Charges 292 351 852 922 999 1,024

Other Income 1,506 2,522 3,163 3,453 3,646 3,737

(% of PBT) 21.7 27.4 30.6 31.5 34.8 32.8

Recurring PBT 6,939 9,191 10,344 10,968 10,465 11,403

% chg 20.5 32.4 12.6 6.0 (4.6) 9.0

Extraordinary Inc/(Expense) (297) (57) (473) (101) - -

PBT (reported) 6,642 9,134 9,872 10,867 10,465 11,403

Tax 1,233 1,812 2,111 1,618 1,570 1,710

(% of PBT) 18.6 19.8 21.4 14.9 15.0 15.0

PAT (reported) 5,409 7,322 7,761 9,249 8,895 9,692

Add: Share of earnings of asso. 59 (285) (772) (660) (490) (386)

Less: Minority interest (MI) 1,724 1,995 2,161 2,529 2,313 2,520

Extraordinary Expense/(Inc.) - - - - - -

PAT after MI (reported) 3,744 5,043 4,828 6,060 6,092 6,787

ADJ. PAT 3,986 5,088 5,200 6,146 6,092 6,787

% chg 14.1 27.7 2.2 18.2 (0.9) 11.4

(% of Net Sales) 16.1 16.7 12.6 13.6 13.7 14.9

Basic EPS (`) 11.9 15.0 14.4 18.3 18.1 20.2

Fully Diluted EPS (̀ ) 11.9 14.3 15.5 18.3 18.1 20.2

% chg (3.8) 20.8 8.0 18.2 (0.9) 11.4

Note: Some of the figures from FY2011 onwards are reclassified; hence not comparable with

previous year numbers

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 10/13

Sterlite Industries | 4QFY2013 Result Update

April 30, 2013 10

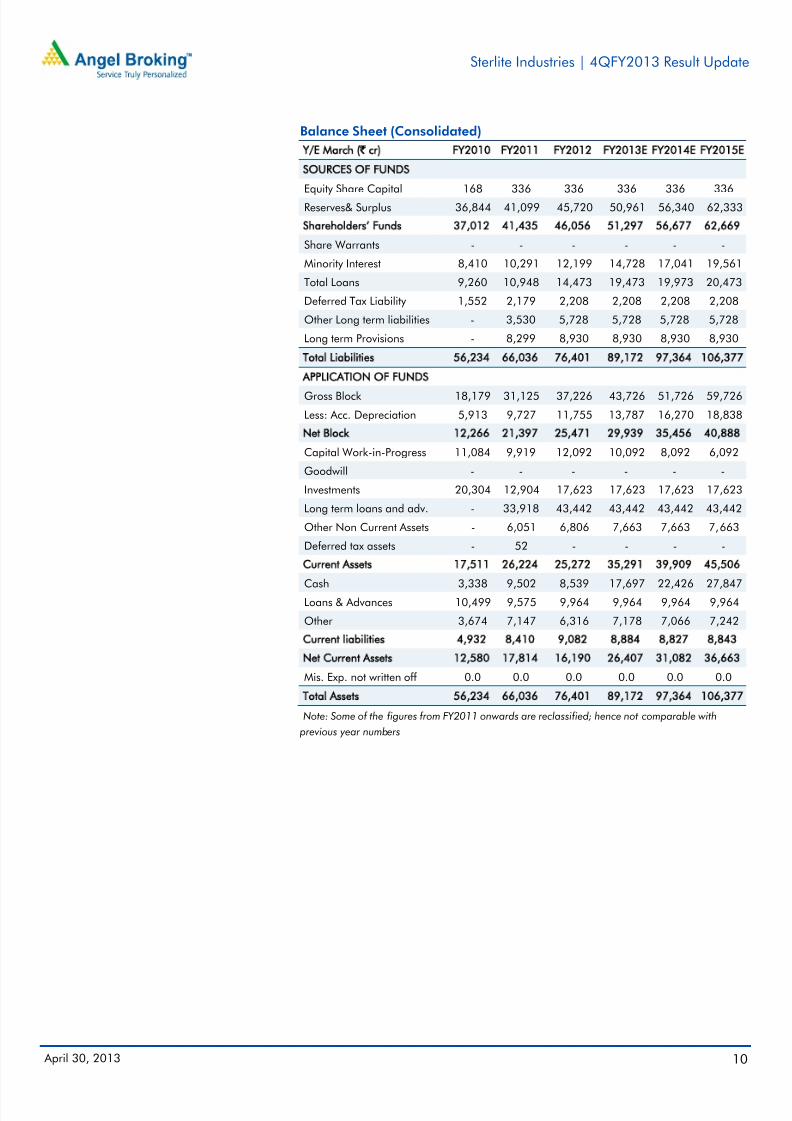

Balance Sheet (Consolidated)

Y/E March (` cr) FY2010 FY2011 FY2012 FY2013E FY2014E FY2015E

SOURCES OF FUNDS

Equity Share Capital 168 336 336 336 336 336Reserves& Surplus 36,844 41,099 45,720 50,961 56,340 62,333

Shareholders’ Funds 37,012 41,435 46,056 51,297 56,677 62,669

Share Warrants - - - - - -

Minority Interest 8,410 10,291 12,199 14,728 17,041 19,561

Total Loans 9,260 10,948 14,473 19,473 19,973 20,473

Deferred Tax Liability 1,552 2,179 2,208 2,208 2,208 2,208

Other Long term liabilities - 3,530 5,728 5,728 5,728 5,728

Long term Provisions - 8,299 8,930 8,930 8,930 8,930

Total Liabilities 56,234 66,036 76,401 89,172 97,364 106,377

APPLICATION OF FUNDS

Gross Block 18,179 31,125 37,226 43,726 51,726 59,726

Less: Acc. Depreciation 5,913 9,727 11,755 13,787 16,270 18,838

Net Block 12,266 21,397 25,471 29,939 35,456 40,888

Capital Work-in-Progress 11,084 9,919 12,092 10,092 8,092 6,092

Goodwill - - - - - -

Investments 20,304 12,904 17,623 17,623 17,623 17,623

Long term loans and adv. - 33,918 43,442 43,442 43,442 43,442

Other Non Current Assets - 6,051 6,806 7,663 7,663 7,663

Deferred tax assets - 52 - - - -

Current Assets 17,511 26,224 25,272 35,291 39,909 45,506

Cash 3,338 9,502 8,539 17,697 22,426 27,847

Loans & Advances 10,499 9,575 9,964 9,964 9,964 9,964

Other 3,674 7,147 6,316 7,178 7,066 7,242

Current liabilities 4,932 8,410 9,082 8,884 8,827 8,843

Net Current Assets 12,580 17,814 16,190 26,407 31,082 36,663

Mis. Exp. not written off 0.0 0.0 0.0 0.0 0.0 0.0

Total Assets 56,234 66,036 76,401 89,172 97,364 106,377

Note: Some of the figures from FY2011 onwards are reclassified; hence not comparable with

previous year numbers

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 11/13

Sterlite Industries | 4QFY2013 Result Update

April 30, 2013 11

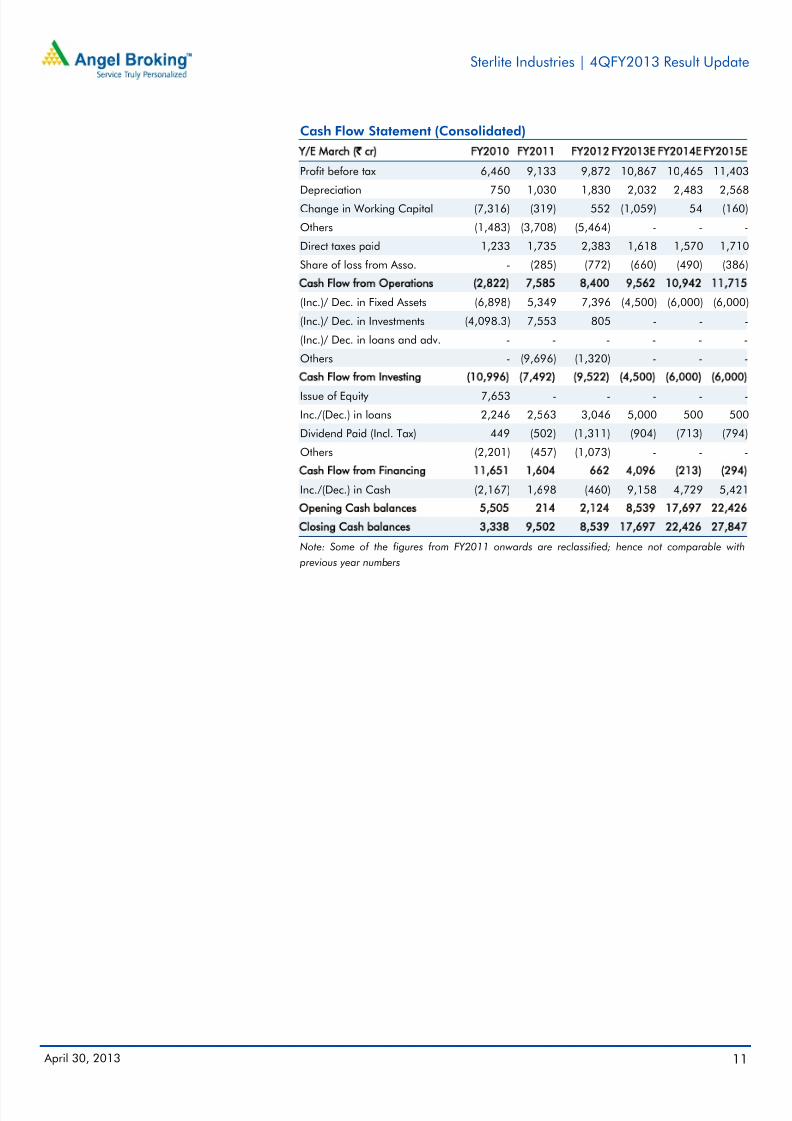

Cash Flow Statement (Consolidated)

Y/E March (` cr) FY2010 FY2011 FY2012FY2013EFY2014EFY2015E

Profit before tax 6,460 9,133 9,872 10,867 10,465 11,403

Depreciation 750 1,030 1,830 2,032 2,483 2,568Change in Working Capital (7,316) (319) 552 (1,059) 54 (160)

Others (1,483) (3,708) (5,464) - - -

Direct taxes paid 1,233 1,735 2,383 1,618 1,570 1,710

Share of loss from Asso. - (285) (772) (660) (490) (386)

Cash Flow from Operations (2,822) 7,585 8,400 9,562 10,942 11,715

(Inc.)/ Dec. in Fixed Assets (6,898) 5,349 7,396 (4,500) (6,000) (6,000)

(Inc.)/ Dec. in Investments (4,098.3) 7,553 805 - - -

(Inc.)/ Dec. in loans and adv. - - - - - -

Others - (9,696) (1,320) - - -

Cash Flow from Investing (10,996) (7,492) (9,522) (4,500) (6,000) (6,000)

Issue of Equity 7,653 - - - - -

Inc./(Dec.) in loans 2,246 2,563 3,046 5,000 500 500

Dividend Paid (Incl. Tax) 449 (502) (1,311) (904) (713) (794)

Others (2,201) (457) (1,073) - - -

Cash Flow from Financing 11,651 1,604 662 4,096 (213) (294)

Inc./(Dec.) in Cash (2,167) 1,698 (460) 9,158 4,729 5,421

Opening Cash balances 5,505 214 2,124 8,539 17,697 22,426

Closing Cash balances 3,338 9,502 8,539 17,697 22,426 27,847

Note: Some of the figures from FY2011 onwards are reclassified; hence not comparable with

previous year numbers

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 12/13

Sterlite Industries | 4QFY2013 Result Update

April 30, 2013 12

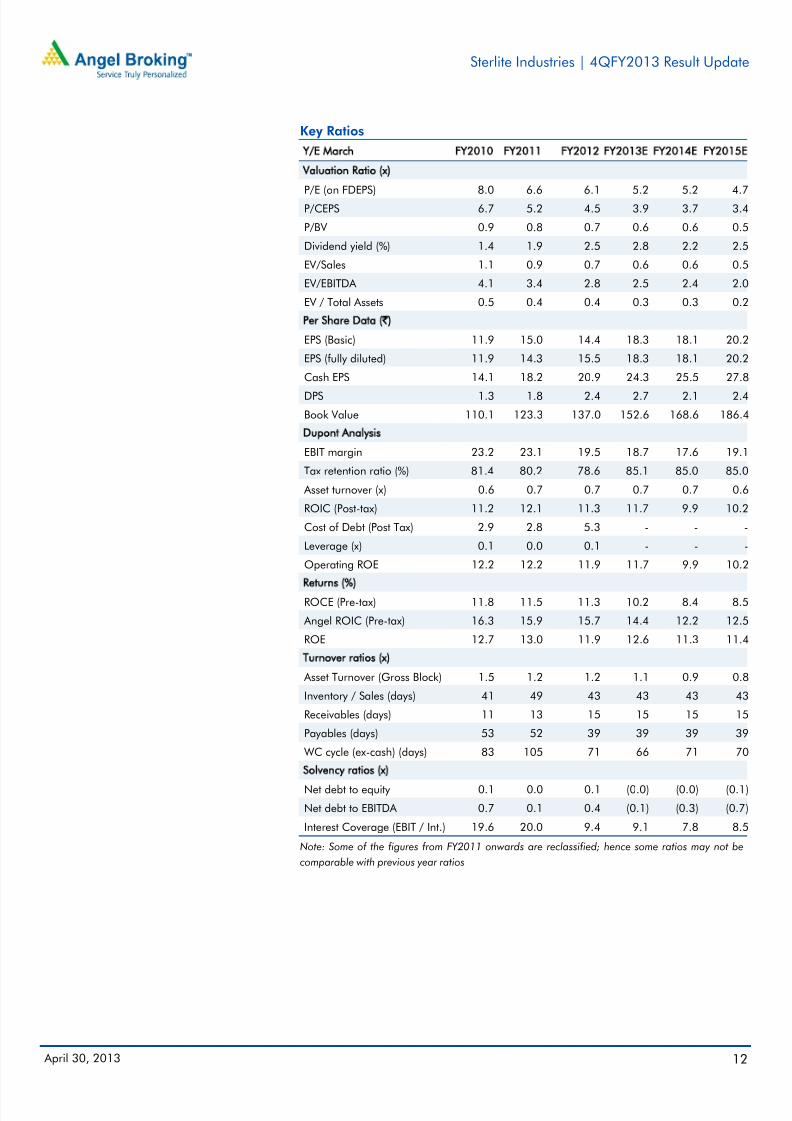

Key Ratios

Y/E March FY2010 FY2011 FY2012 FY2013E FY2014E FY2015E

Valuation Ratio (x)

P/E (on FDEPS) 8.0 6.6 6.1 5.2 5.2 4.7P/CEPS 6.7 5.2 4.5 3.9 3.7 3.4

P/BV 0.9 0.8 0.7 0.6 0.6 0.5

Dividend yield (%) 1.4 1.9 2.5 2.8 2.2 2.5

EV/Sales 1.1 0.9 0.7 0.6 0.6 0.5

EV/EBITDA 4.1 3.4 2.8 2.5 2.4 2.0

EV / Total Assets 0.5 0.4 0.4 0.3 0.3 0.2

Per Share Data (`)EPS (Basic) 11.9 15.0 14.4 18.3 18.1 20.2

EPS (fully diluted) 11.9 14.3 15.5 18.3 18.1 20.2

Cash EPS 14.1 18.2 20.9 24.3 25.5 27.8

DPS 1.3 1.8 2.4 2.7 2.1 2.4

Book Value 110.1 123.3 137.0 152.6 168.6 186.4

Dupont Analysis

EBIT margin 23.2 23.1 19.5 18.7 17.6 19.1

Tax retention ratio (%) 81.4 80.2 78.6 85.1 85.0 85.0

Asset turnover (x) 0.6 0.7 0.7 0.7 0.7 0.6

ROIC (Post-tax) 11.2 12.1 11.3 11.7 9.9 10.2

Cost of Debt (Post Tax) 2.9 2.8 5.3 - - -

Leverage (x) 0.1 0.0 0.1 - - -

Operating ROE 12.2 12.2 11.9 11.7 9.9 10.2

Returns (%)

ROCE (Pre-tax) 11.8 11.5 11.3 10.2 8.4 8.5

Angel ROIC (Pre-tax) 16.3 15.9 15.7 14.4 12.2 12.5

ROE 12.7 13.0 11.9 12.6 11.3 11.4

Turnover ratios (x)

Asset Turnover (Gross Block) 1.5 1.2 1.2 1.1 0.9 0.8

Inventory / Sales (days) 41 49 43 43 43 43

Receivables (days) 11 13 15 15 15 15

Payables (days) 53 52 39 39 39 39

WC cycle (ex-cash) (days) 83 105 71 66 71 70

Solvency ratios (x)Net debt to equity 0.1 0.0 0.1 (0.0) (0.0) (0.1)

Net debt to EBITDA 0.7 0.1 0.4 (0.1) (0.3) (0.7)

Interest Coverage (EBIT / Int.) 19.6 20.0 9.4 9.1 7.8 8.5

Note: Some of the figures from FY2011 onwards are reclassified; hence some ratios may not be

comparable with previous year ratios

7/30/2019 Sterlite 4Q FY 2013

http://slidepdf.com/reader/full/sterlite-4q-fy-2013 13/13

Sterlite Industries | 4QFY2013 Result Update

A il 30 2013 13

Disclosure of Interest Statement Sterlite Industries

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)Reduce (-5% to -15%) Sell (< -15%)

Research Team Tel: 022 – 3935 7800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.The information in this document has been printed on the basis of publicly available information, internal data and other reliablesources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as thisdocument is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report .

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking orother advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important ` Stock Holding Disclosure' report on the Angel website (Research Section). Also, pleaserefer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited andits affiliates may have investment positions in the stocks recommended in this report.