Embed Size (px)

Citation preview

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 1/30

Chapter 9Chapter 9

Strategic Control andStrategic Control and

Corporate GovernanceCorporate Governance

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 2/30

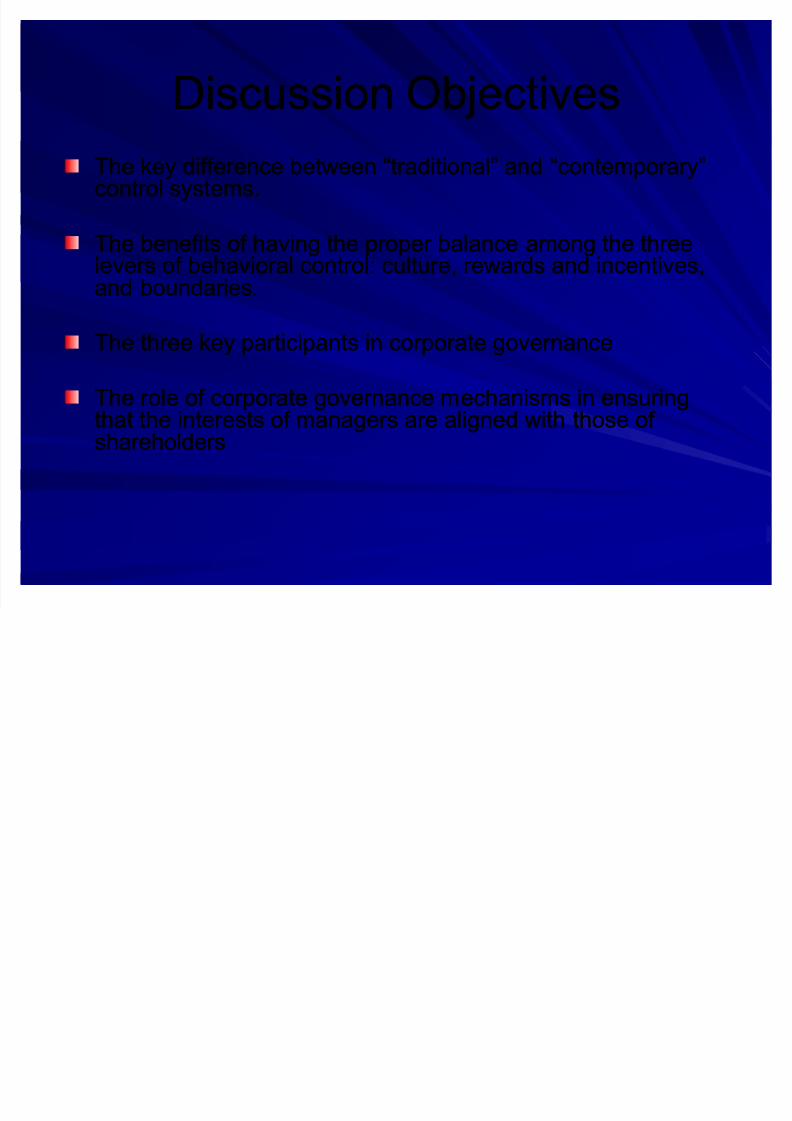

Discussion ObjectivesDiscussion Objectives

The key difference between ³traditional´ and ³contemporary´The key difference between ³traditional´ and ³contemporary´control systems.control systems.

The benefits of having the proper balance among the threeThe benefits of having the proper balance among the three

levers of behavioral control: culture, rewards and incentives,levers of behavioral control: culture, rewards and incentives,and boundaries.and boundaries.

The three key participants in corporate governanceThe three key participants in corporate governance

The role of corporate governance mechanisms in ensuringThe role of corporate governance mechanisms in ensuringthat the interests of managers are aligned with those of that the interests of managers are aligned with those of shareholdersshareholders

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 3/30

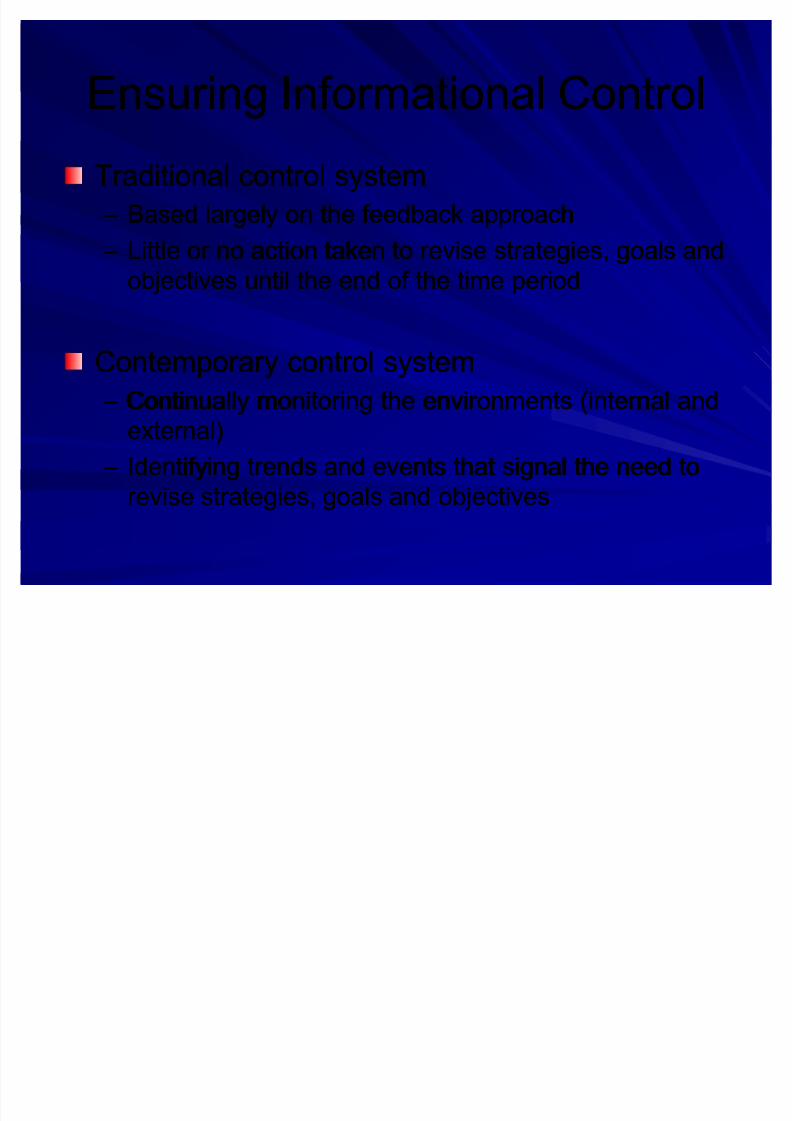

Ensuring Informational ControlEnsuring Informational Control

Traditional control systemTraditional control system

±± Based largely on the feedback approachBased largely on the feedback approach

±± Little or no action taken to revise strategies, goals andLittle or no action taken to revise strategies, goals and

objectives until the end of the time periodobjectives until the end of the time period

Contemporary control systemContemporary control system

±± Continually monitoring the environments (internal andContinually monitoring the environments (internal andexternal)external)

±± Identifying trends and events that signal the need toIdentifying trends and events that signal the need to

revise strategies, goals and objectivesrevise strategies, goals and objectives

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 4/30

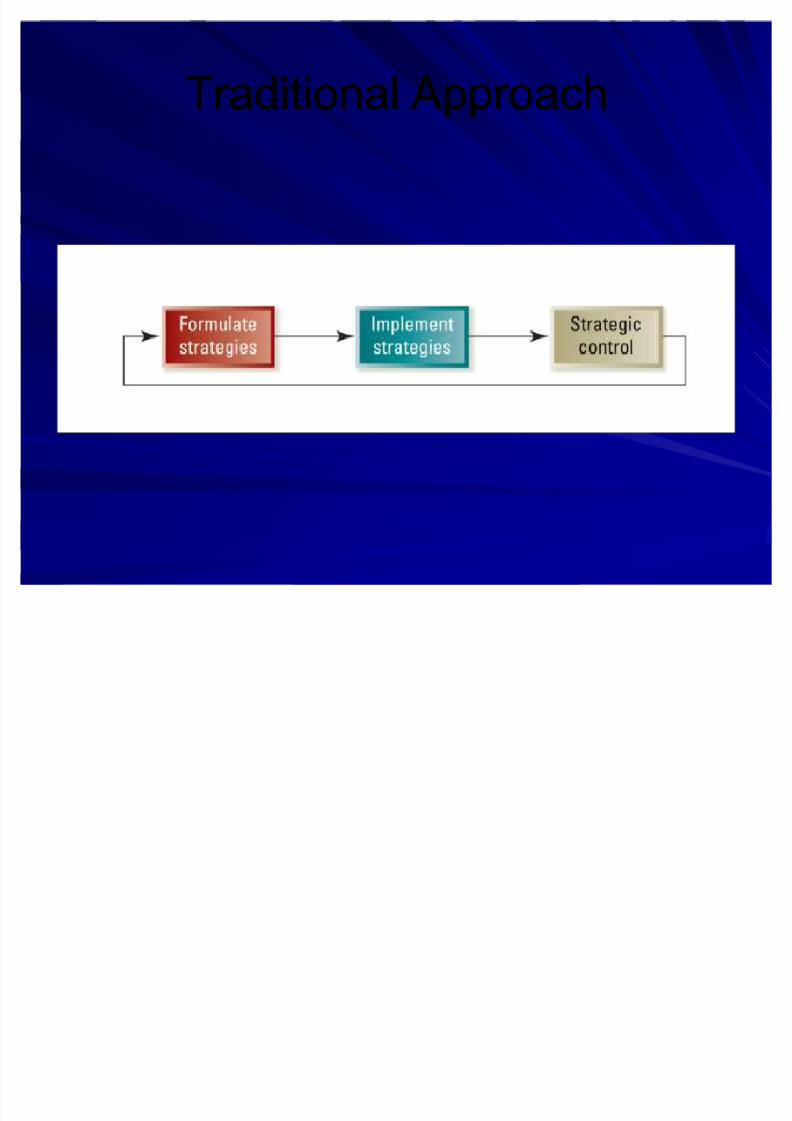

Traditional ApproachTraditional Approach

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 5/30

Traditional ApproachTraditional Approach

Traditional approach is sequentialTraditional approach is sequential

±± Strategies are formulated and topStrategies are formulated and top

management sets goalsmanagement sets goals

±± Strategies are implementedStrategies are implemented

±± Performance is measured against thePerformance is measured against the

predetermined goal setpredetermined goal set

±± Control is based on a feedback loop fromControl is based on a feedback loop fromperformance measurement to strategyperformance measurement to strategy

formulationformulation

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 6/30

Traditional Cont.Traditional Cont.

Process typically involves lengthy time lags,Process typically involves lengthy time lags,

often tied to the annual planning cycleoften tied to the annual planning cycle

This ³singleThis ³single--loop´ learning control system simplyloop´ learning control system simply

compares actual performance to acompares actual performance to a

predetermined goalpredetermined goal

Most appropriate whenMost appropriate when

±±E

nvironment is stable and relatively simpleE

nvironment is stable and relatively simple±± Goals and objectives can be measured with certaintyGoals and objectives can be measured with certainty

±± Little need for complex measures of performanceLittle need for complex measures of performance

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 7/30

Contemporary ApproachContemporary Approach

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 8/30

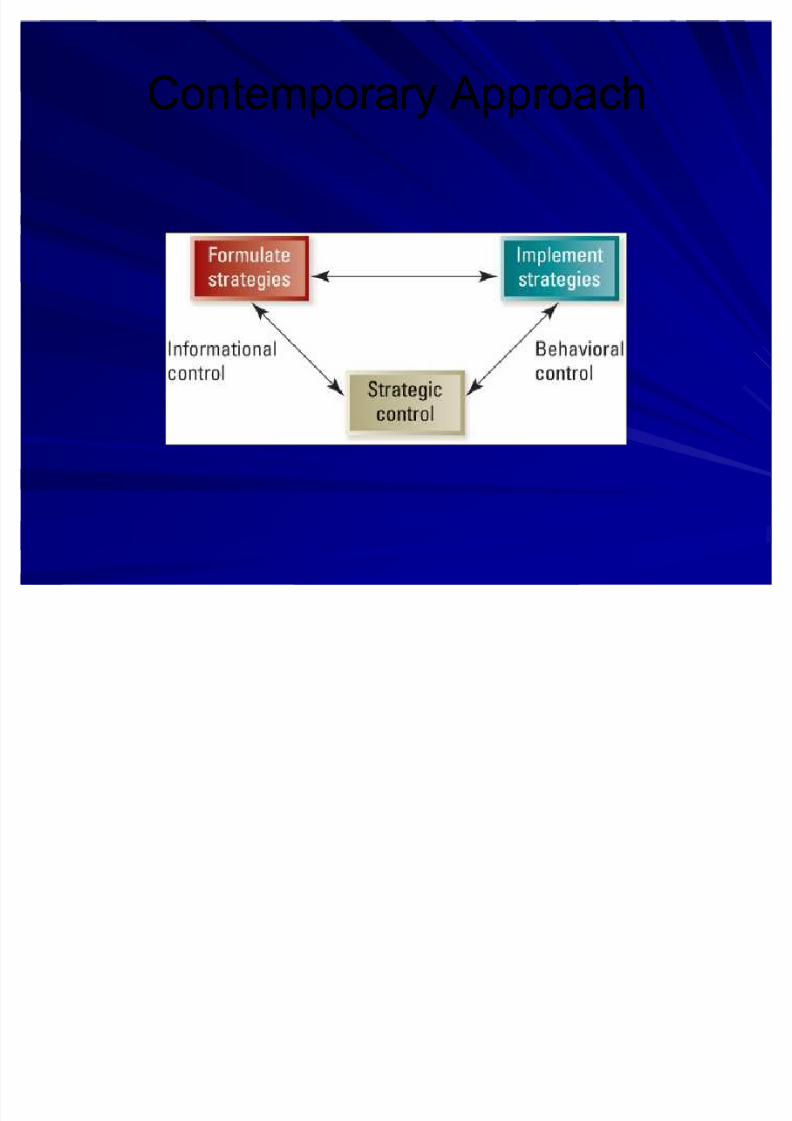

Contemporary Approach Cont.Contemporary Approach Cont.

Relationships between strategyRelationships between strategy

formulation, implementation and controlformulation, implementation and control

are highly interactiveare highly interactive

Two different types of controlTwo different types of control

±± Informational controlInformational control±± Behavioral controlBehavioral control

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 9/30

Contemporary Approach Cont.Contemporary Approach Cont.

BenefitsBenefits

±± Time lags are dramatically shortened,Time lags are dramatically shortened,

±± Changes in the competitive environment areChanges in the competitive environment are

detected earlier detected earlier

±± The organization¶s ability to respond withThe organization¶s ability to respond withspeed and flexibility is enhancedspeed and flexibility is enhanced

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 10/30

4 Key Issues4 Key IssuesContemporary control systems must have four characteristics to beContemporary control systems must have four characteristics to beeffective.effective.

1. They must focus on constantly changing information that top1. They must focus on constantly changing information that topmanagers identify as having potential strategic importance.managers identify as having potential strategic importance.

2.2. The information is important enough to demand frequent andThe information is important enough to demand frequent andregular attention from operating managers at all levels of theregular attention from operating managers at all levels of theorganization.organization.

3. The data and information generated by the control system are best3. The data and information generated by the control system are bestinterpreted and discussed in faceinterpreted and discussed in face--toto--face meetings.face meetings.

4. The contemporary control system is a key catalyst for an ongoing4. The contemporary control system is a key catalyst for an ongoingdebate about underlying data, assumptions, and action plans.debate about underlying data, assumptions, and action plans.

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 11/30

Informational ControlInformational Control

Deals with internal environment and externalDeals with internal environment and external

strategic contextstrategic context

Key questionKey question

±± ³Do the organization¶s goals and strategies still µfit¶³Do the organization¶s goals and strategies still µfit¶

within the context of the current strategicwithin the context of the current strategic

environment?´environment?´

Two key issuesTwo key issues

±± Scan and monitor external environment (general andScan and monitor external environment (general and

industry)industry)

±± Continuously monitor the internal environmentContinuously monitor the internal environment

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 12/30

Behavioral ControlBehavioral Control

Behavioral control is focused onBehavioral control is focused on

implementationimplementation²²doing things rightdoing things right

Three key control ³levers´Three key control ³levers´

±± CultureCulture

±± RewardsRewards±± BoundariesBoundaries

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 13/30

2 Key Reasons to emphasize rewards and culture2 Key Reasons to emphasize rewards and culture

1.1. The competitive environment isThe competitive environment is

increasingly complex and unpredictable,increasingly complex and unpredictable,

demanding both flexibility and quickdemanding both flexibility and quick

response to its challenges.response to its challenges.

2.2. The implicit longThe implicit long--term contract betweenterm contract between

the organization and its key employeesthe organization and its key employees

has been eroded.has been eroded.

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 14/30

Organizational culture is a system of Organizational culture is a system of

±± Shared values (what is important)Shared values (what is important)

±± Beliefs (how things work)Beliefs (how things work)

Organizational culture shapes a firm¶sOrganizational culture shapes a firm¶s

±± PeoplePeople

±± Organizational structuresOrganizational structures

±± Control systemsControl systems

Organizational culture producesOrganizational culture produces

±± Behavioral norms (the way we do things around here)Behavioral norms (the way we do things around here)

Building a Strong and Effective CultureBuilding a Strong and Effective Culture

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 15/30

Motivating with Rewards and IncentivesMotivating with Rewards and Incentives

Rewards and incentive systemsRewards and incentive systems

±± Powerful means of influencing anPowerful means of influencing anorganization¶s cultureorganization¶s culture

±± Focuses efforts on highFocuses efforts on high--priority taskspriority tasks

±± Motivates individual and collective taskMotivates individual and collective task

performanceperformance±± Can be an effective motivator and controlCan be an effective motivator and control

mechanismmechanism

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 16/30

Motivation Cont.Motivation Cont.

Potential downsidePotential downside

±± Subcultures may arise in different businessSubcultures may arise in different business

units with multiple reward systemsunits with multiple reward systems

±± May reflect differences among functionalMay reflect differences among functional

areas, products, services and divisionsareas, products, services and divisions

±± Shared values may emerge in subculture inShared values may emerge in subculture in

opposition to patterns of the dominant cultureopposition to patterns of the dominant culture±± Reward systems may lead to informationReward systems may lead to information

hoarding, working at cross purposeshoarding, working at cross purposes

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 17/30

Motivation Cont.Motivation Cont.

Creating effective reward and incentiveCreating effective reward and incentiveprogramsprograms±± Objectives are clear, well understood and broadlyObjectives are clear, well understood and broadly

acceptedaccepted

±± Rewards are clearly linked to performance andRewards are clearly linked to performance anddesired behaviorsdesired behaviors

±± Performance measures are clear and highly visiblePerformance measures are clear and highly visible

±± Feedback is prompt, clear, and unambiguousFeedback is prompt, clear, and unambiguous

±± Compensation ³system´ is perceived as fair andCompensation ³system´ is perceived as fair and

equitableequitable±± Structure is flexible; it can adapt to changingStructure is flexible; it can adapt to changing

circumstancescircumstances

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 18/30

Boundaries and ConstraintsBoundaries and Constraints

RuleRule--based controls most appropriate in firmsbased controls most appropriate in firmswith the following characteristicswith the following characteristics±± Stable and predictable environmentsStable and predictable environments

±± Largely unskilled and interchangeable employeesLargely unskilled and interchangeable employees

±± Consistency in product and service is criticalConsistency in product and service is critical

±± Risk of malfeasance is extremely highRisk of malfeasance is extremely high

GuidelinesGuidelines

±± Can set spending limits and range of discretionCan set spending limits and range of discretion±± Can specify proper relationships with customers andCan specify proper relationships with customers and

supplierssuppliers

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 19/30

Situational EffectsSituational Effects

Not all organizations use the same types of controls.Not all organizations use the same types of controls.

In professional organizations, control comes fromIn professional organizations, control comes frominternalized norms, values, and cultureinternalized norms, values, and culture

When measurement of performance is straight forward,When measurement of performance is straight forward,control depends on granting or withholding rewards suchcontrol depends on granting or withholding rewards suchas compensationas compensation

Control in bureaucratic organizations comes from aControl in bureaucratic organizations comes from ahighly formalized set of rules and regulations.highly formalized set of rules and regulations.

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 20/30

Evolving from Boundaries to Culture & RewardsEvolving from Boundaries to Culture & Rewards

Organizations should strive to haveOrganizations should strive to haveboundaries internalizedboundaries internalized

±± System of rewards and incentives coupledSystem of rewards and incentives coupled

with a strong culturewith a strong culture±± Hire the right people (already identify with theHire the right people (already identify with the

firm¶s dominant values)firm¶s dominant values)Train people in the dominant cultural valuesTrain people in the dominant cultural values

Have managerial role modelsHave managerial role modelsReward systems clearly aligned withReward systems clearly aligned withorganizational goals and objectivesorganizational goals and objectives

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 21/30

Role of Corporate GovernanceRole of Corporate Governance

Corporate governanceCorporate governance±± Relationship amongRelationship among

The shareholdersThe shareholders

The management (led by the Chief Executive Officer)The management (led by the Chief Executive Officer)

The board of directorsThe board of directors

Issue isIssue is±± How corporations can succeed (or fail) in aligningHow corporations can succeed (or fail) in aligning

managerial motives withmanagerial motives withThe interests of the shareholdersThe interests of the shareholders

The interests of the board of directorsThe interests of the board of directors

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 22/30

Role of Corporate GovernanceRole of Corporate Governance

Shareholders (investors)Shareholders (investors)

±± Limited liabilityLimited liability

±± Participate in the profits of the enterpriseParticipate in the profits of the enterprise

±± Limited involvement in the company¶s affairsLimited involvement in the company¶s affairs

ManagementManagement

±± Run the companyRun the company

±± Does not personally have to provide the fundsDoes not personally have to provide the funds

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 23/30

Role of Corporate GovernanceRole of Corporate Governance

Board of directorsBoard of directors

±± Elected by shareholdersElected by shareholders

±± Fiduciary obligation to protect shareholder Fiduciary obligation to protect shareholder

interestsinterests

What is the inherent Problem with thisWhat is the inherent Problem with this

relationship?relationship?

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 24/30

Agency TheoryAgency Theory

Deals with the relationship betweenDeals with the relationship between

PrincipalsPrincipals ±± who are owners of the firmwho are owners of the firm(stockholders), and the(stockholders), and the

AgentsAgents ±± who are the people paid bywho are the people paid byprincipals to perform a job on their behalf principals to perform a job on their behalf

(management)(management)

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 25/30

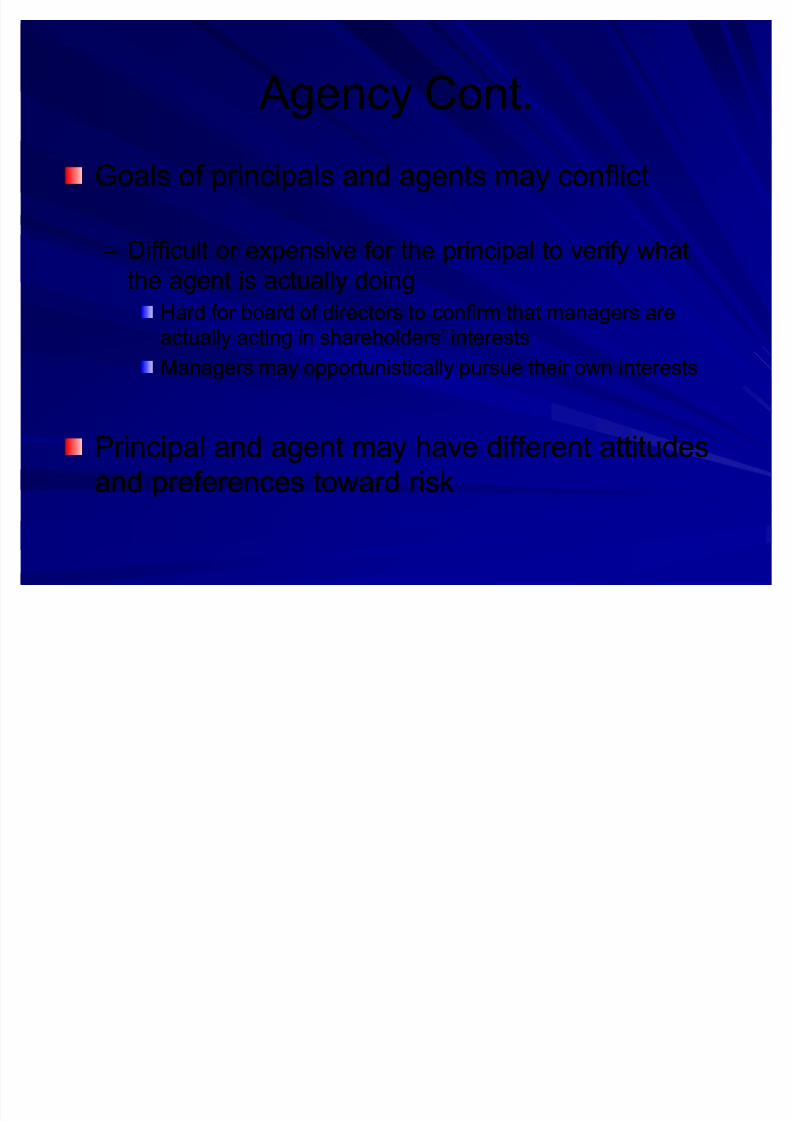

Agency Cont.Agency Cont.

Goals of principals and agents may conflictGoals of principals and agents may conflict

±± Difficult or expensive for the principal to verify whatDifficult or expensive for the principal to verify what

the agent is actually doingthe agent is actually doingHard for board of directors to confirm that managers areHard for board of directors to confirm that managers are

actually acting in shareholders¶ interestsactually acting in shareholders¶ interests

Managers may opportunistically pursue their own interestsManagers may opportunistically pursue their own interests

Principal and agent may have different attitudesPrincipal and agent may have different attitudes

and preferences toward riskand preferences toward risk

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 26/30

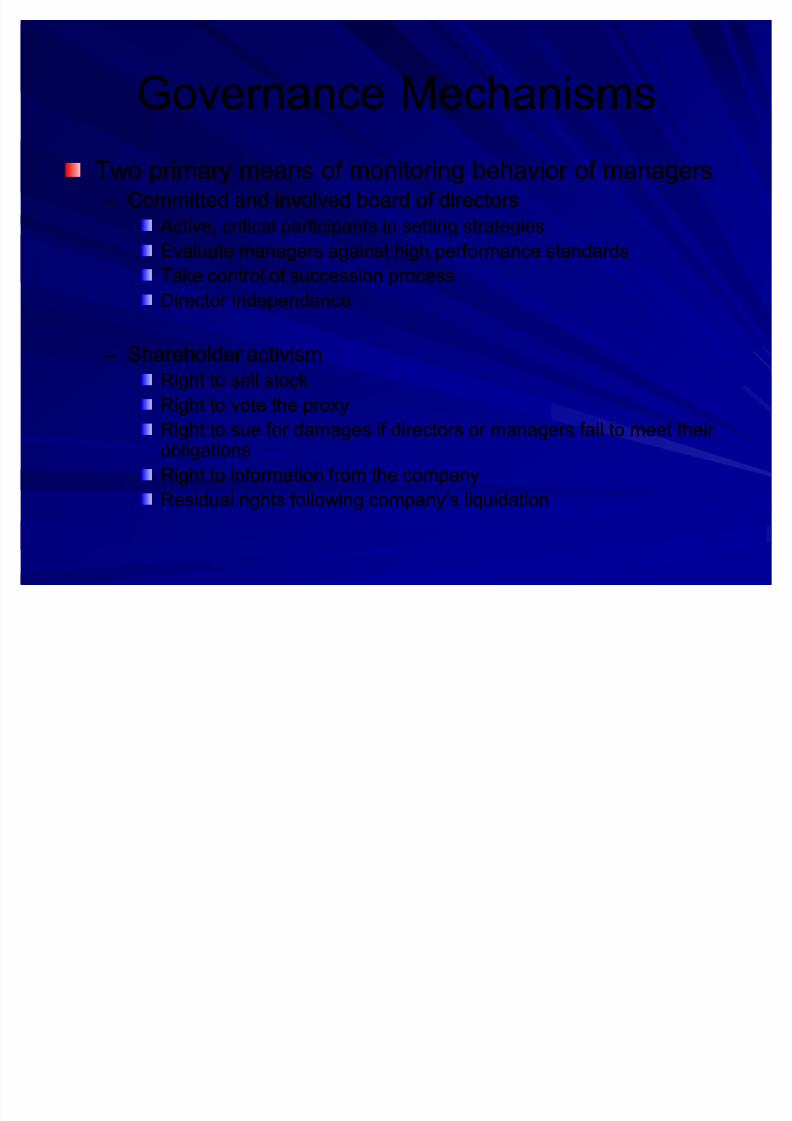

Governance MechanismsGovernance Mechanisms

Two primary means of monitoring behavior of managersTwo primary means of monitoring behavior of managers±± Committed and involved board of directorsCommitted and involved board of directors

Active, critical participants in setting strategiesActive, critical participants in setting strategies

Evaluate managers against high performance standardsEvaluate managers against high performance standards

Take control of succession processTake control of succession processDirector independenceDirector independence

±± Shareholder activismShareholder activism

Right to sell stockRight to sell stock

Right to vote the proxyRight to vote the proxy

Right to sue for damages if directors or managers fail to meet their Right to sue for damages if directors or managers fail to meet their obligationsobligations

Right to information from the companyRight to information from the company

Residual rights following company¶s liquidationResidual rights following company¶s liquidation

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 27/30

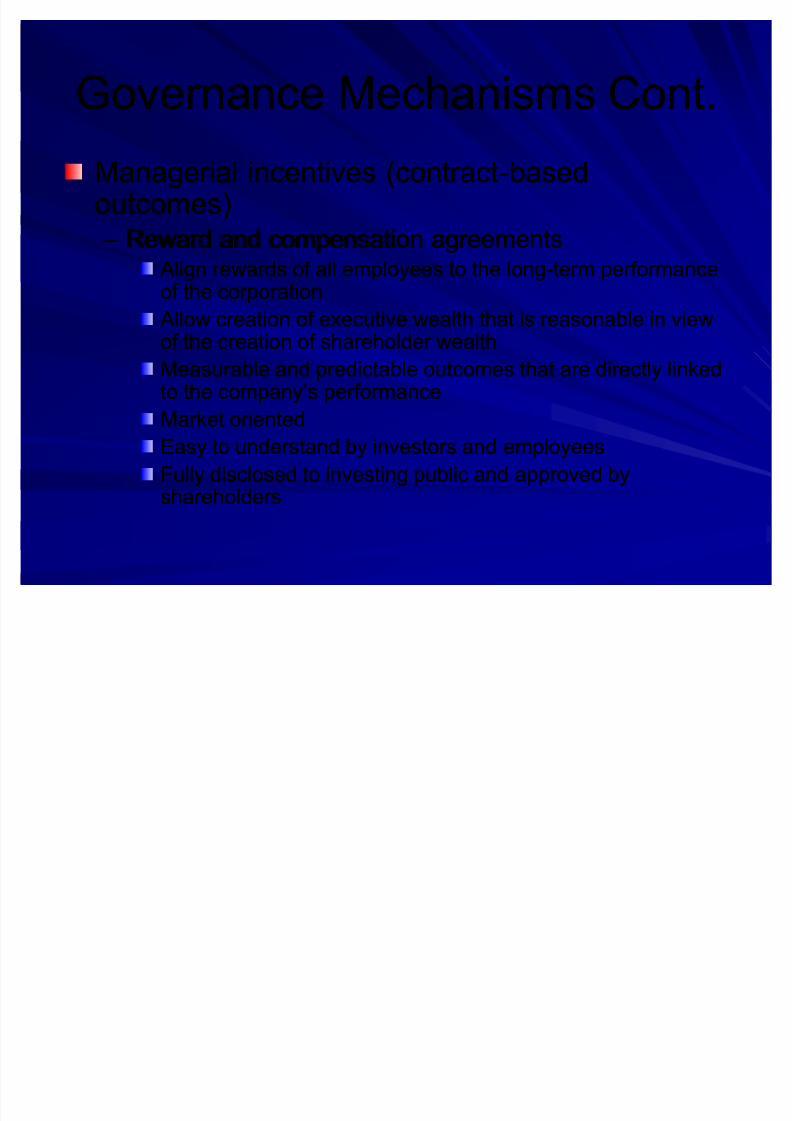

Governance Mechanisms Cont.Governance Mechanisms Cont.

Managerial incentives (contractManagerial incentives (contract--basedbasedoutcomes)outcomes)±± Reward and compensation agreementsReward and compensation agreements

Align rewards of all employees to the longAlign rewards of all employees to the long--term performanceterm performanceof the corporationof the corporation

Allow creation of executive wealth that is reasonable in viewAllow creation of executive wealth that is reasonable in viewof the creation of shareholder wealthof the creation of shareholder wealth

Measurable and predictable outcomes that are directly linkedMeasurable and predictable outcomes that are directly linkedto the company¶s performanceto the company¶s performance

Market orientedMarket orientedEasy to understand by investors and employeesEasy to understand by investors and employees

Fully disclosed to investing public and approved byFully disclosed to investing public and approved byshareholdersshareholders

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 28/30

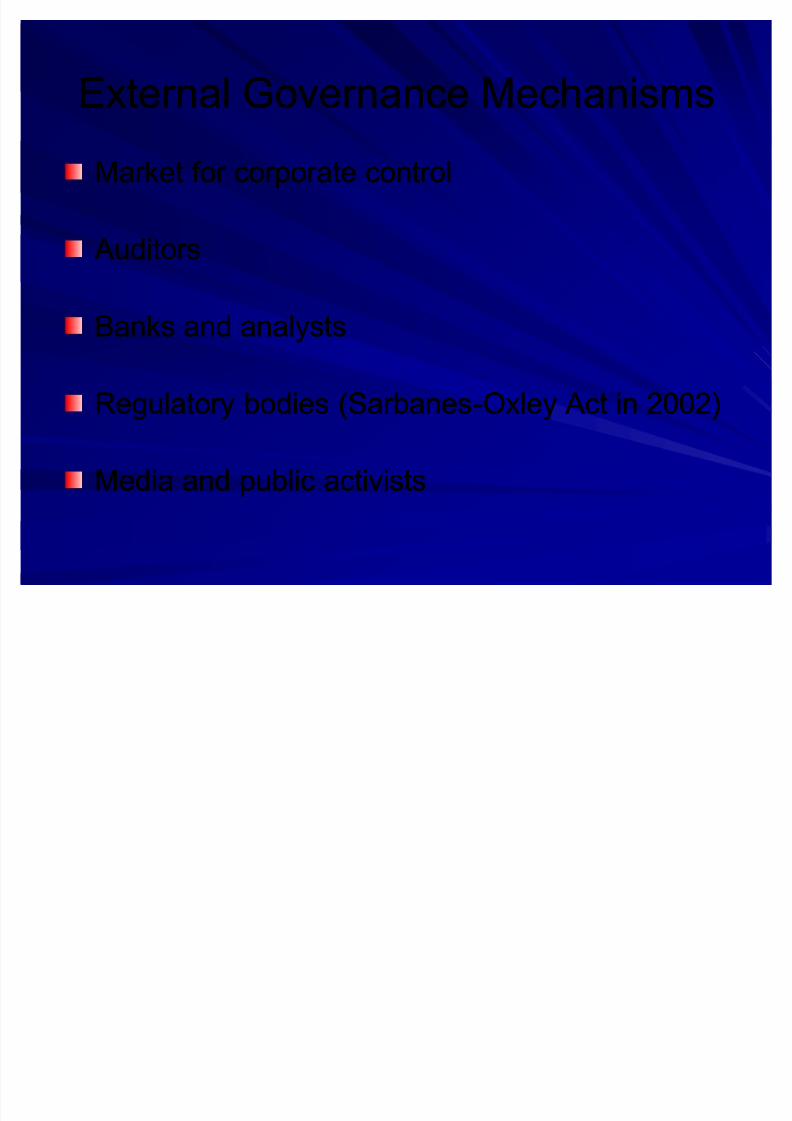

External Governance MechanismsExternal Governance Mechanisms

Market for corporate controlMarket for corporate control

AuditorsAuditors

Banks and analystsBanks and analysts

Regulatory bodies (SarbanesRegulatory bodies (Sarbanes--Oxley Act in 2002)Oxley Act in 2002)

Media and public activistsMedia and public activists

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 29/30

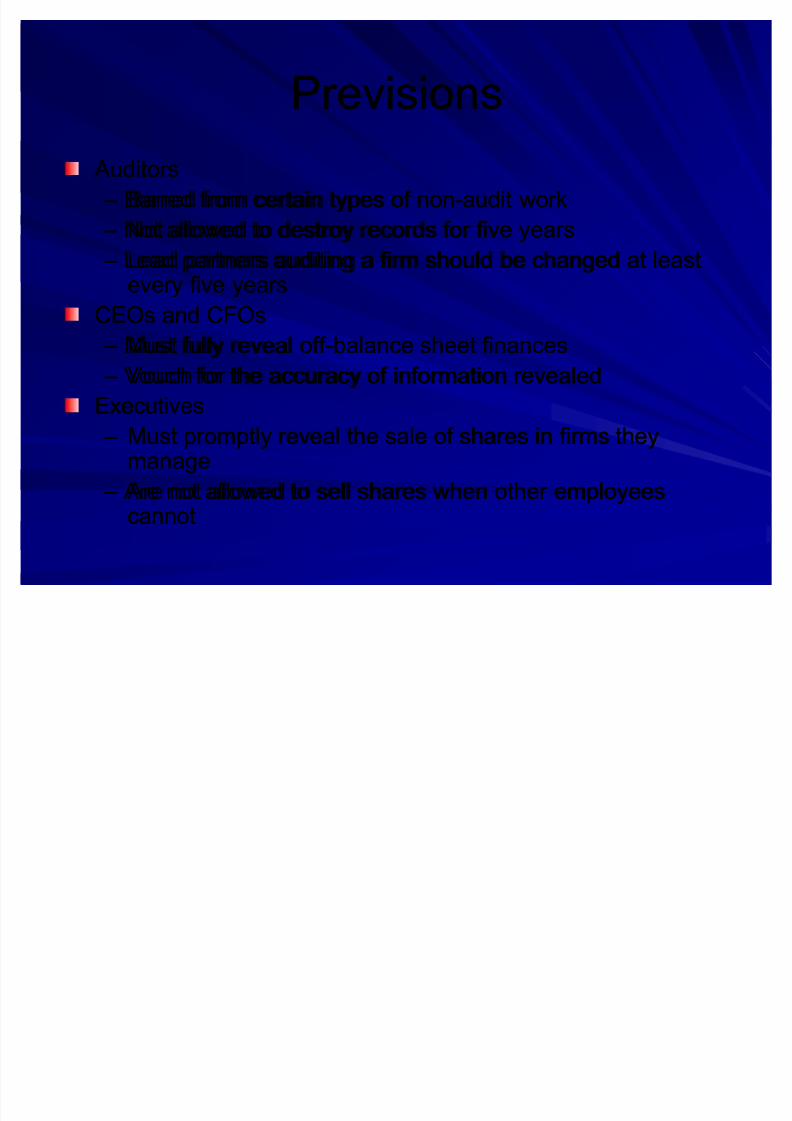

PrevisionsPrevisions

AuditorsAuditors

±± Barred from certain types of nonBarred from certain types of non--audit workaudit work

±± Not allowed to destroy records for five yearsNot allowed to destroy records for five years

±± Lead partners auditing a firm should be changed at leastLead partners auditing a firm should be changed at least

every five yearsevery five yearsCEOs and CFOsCEOs and CFOs

±± Must fully reveal off Must fully reveal off--balance sheet financesbalance sheet finances

±± Vouch for the accuracy of information revealedVouch for the accuracy of information revealed

ExecutivesExecutives

±± Must promptly reveal the sale of shares in firms theyMust promptly reveal the sale of shares in firms theymanagemanage

±± Are not allowed to sell shares when other employeesAre not allowed to sell shares when other employeescannotcannot

8/7/2019 strategy slides ch 09 (2)

http://slidepdf.com/reader/full/strategy-slides-ch-09-2 30/30

Discussion ObjectivesDiscussion Objectives

The key difference between ³traditional´ and ³contemporary´The key difference between ³traditional´ and ³contemporary´control systems.control systems.

The benefits of having the proper balance among the threeThe benefits of having the proper balance among the threelevers of behavioral control: culture, rewards and incentives,levers of behavioral control: culture, rewards and incentives,and boundaries.and boundaries.

The three key participants in corporate governanceThe three key participants in corporate governance

The role of corporate governance mechanisms in ensuringThe role of corporate governance mechanisms in ensuring

that the interests of managers are aligned with those of that the interests of managers are aligned with those of shareholdersshareholders