Embed Size (px)

Citation preview

www.contrast.at

Datum:

Präsentation:

Strateški kontroling – Misija kontrolinga u vrijeme ekonomske krize

05. Studenog 2013

Denis Petrović, Mag. oec. ,MBA

Verteiler:

CONTROLLER_KONGRESS_ZAGREB_DPE.pptxCONTROLLER_KONGRESS_ZAGREB_DPE.pptxCONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 2|

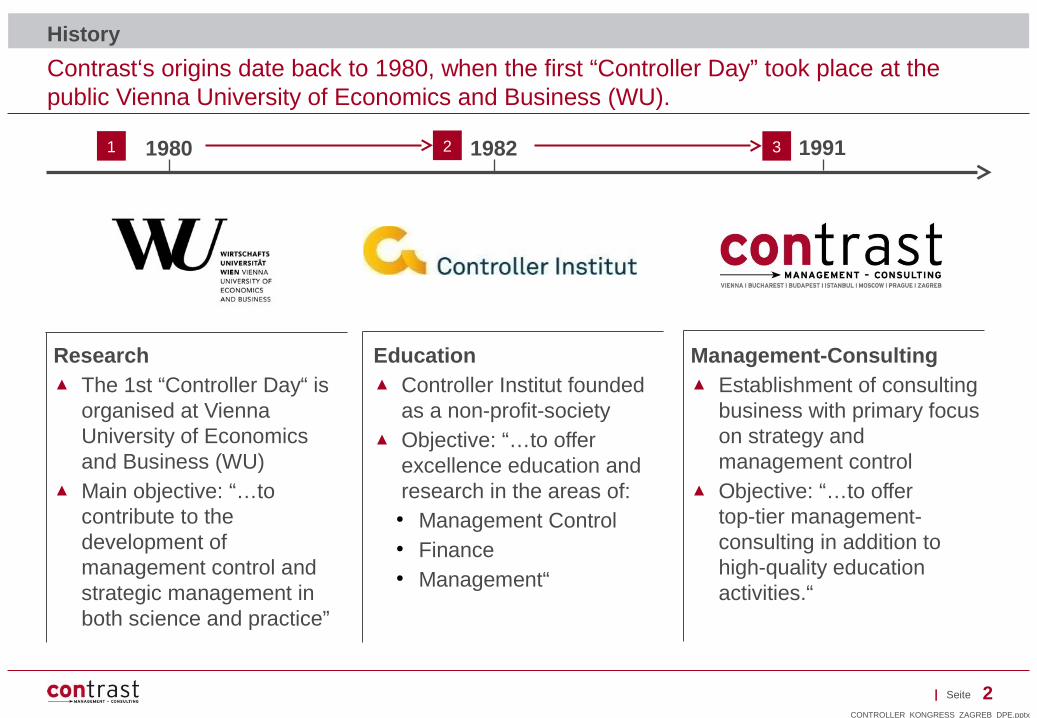

Contrast‘s origins date back to 1980, when the first “Controller Day” took place at the public Vienna University of Economics and Business (WU).

History

1 21980 1982 1991

Research▲ The 1st “Controller Day“ is

organised at Vienna University of Economics and Business (WU)

▲ Main objective: “…to contribute to the development of management control and strategic management in both science and practice”

Education▲ Controller Institut founded

as a non-profit-society▲ Objective: “…to offer

excellence education and research in the areas of:

● Management Control● Finance● Management“

Management-Consulting▲ Establishment of consulting

business with primary focus on strategy and management control

▲ Objective: “…to offer top-tier management- consulting in addition to high-quality education activities.“

3

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 3|

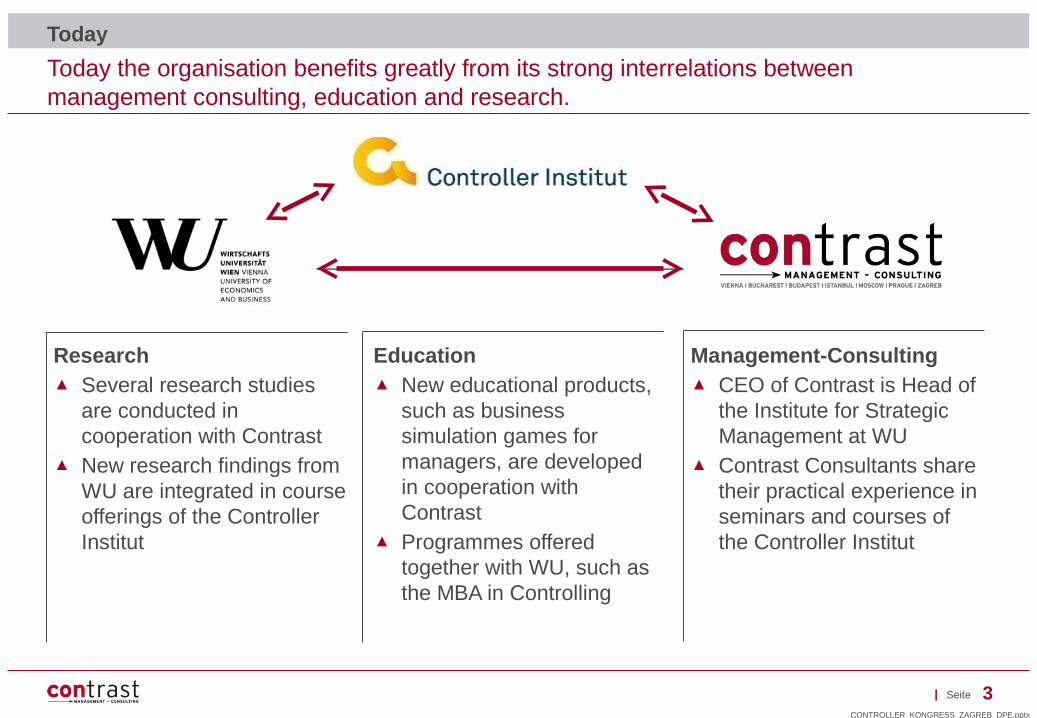

Today the organisation benefits greatly from its strong interrelations between management consulting, education and research.

Today

Research▲ Several research studies

are conducted in cooperation with Contrast

▲ New research findings from WU are integrated in course offerings of the Controller Institut

Education▲ New educational products,

such as business simulation games for managers, are developed in cooperation with Contrast

▲ Programmes offered together with WU, such as the MBA in Controlling

Management-Consulting▲ CEO of Contrast is Head of

the Institute for Strategic Management at WU

▲ Contrast Consultants share their practical experience in seminars and courses of the Controller Institut

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 4|

Studies about Controlling and CFO Roles1

Strategic Management in the Public Sector 6

Strategic Management 3

Strategy in the Time of Economic Crises4

The Role of Controlling 5

Role and Tools in the Future – Strategic Performance Management

2

Agenda

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 5|

Controlling according to IGC What does this mean

Controlling is a management activity that makes sure that companies reach their objectives.

As partners of management Controllers make a significant contribution to the sustainable success of the organization.

Controllers …▲ design and accompany the management

process of defining goals, planning and reviewing so that every decision maker can act in accordance with agreed objectives

▲ ensure that decision makers act with foresight and thus make it possible to take advantage of opportunities and manage risks.

▲ integrate an organization's plans into a cohesive whole

▲ ensure the quality of data and provide decision-relevant information.

▲ are an organizations economic conscience and thus committed to ensuring its success

Details:

http://www.igc-controlling.org/EN/_leitbild/leitbild.php

▲ Controller believe that clear and accepted objectives are at the core of management. By ensuring the definition of these objectives the controller substantially contributes to successful management.

▲ Controllers take care of planning and reporting.▲ The Controller has to use all his resources to

support management in achieving their objectives. The resources include financial know-how, fast and flexible information as well as constant reviews and checking. The sophisticated controller calls this sparring or consulting.

▲ To be efficient, the Controller needs to have his systems under control. This takes up a lot of her time.

▲ By strictly administering management processes, the Controller forces the company into a regular review cycle, thus making sure that problems and opportunities are being identified early on.

Definition of Controlling

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 6|

Recent developments influence the role of the CFO

Übersicht & zentrale Ergebnisse der Studie

▲ Financial crisis and high insecurity of the economic environement

▲ The challenges become more and more diverse and interdisciplinary

▲ Next to data integration, compliance and financing, including the CFO in strategy development becomes more and more important

▲ Time of crisis strenghten the position of the CFO

▲ The role of the CFO devlops towards the real strategist behind the board’s plans

▲ The CFO becomes challenger and sparring partner for management, also for strategic issues

Motivation for the Study

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 7|

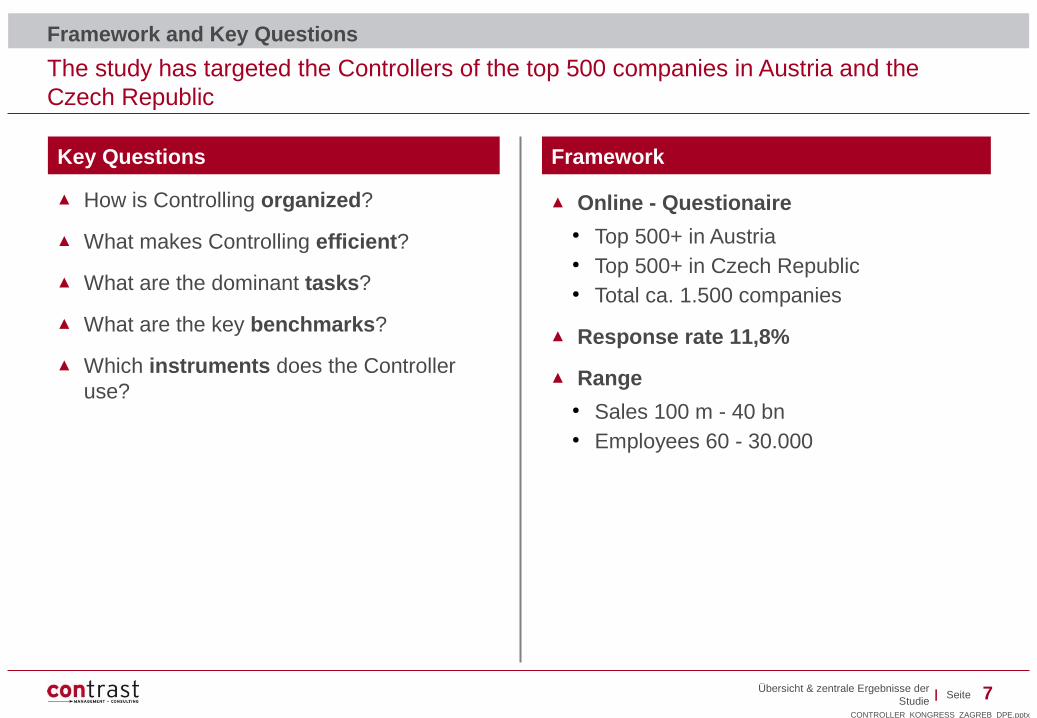

▲ How is Controlling organized?

▲ What makes Controlling efficient?

▲ What are the dominant tasks?

▲ What are the key benchmarks?

▲ Which instruments does the Controller use?

Übersicht & zentrale Ergebnisse der Studie

The study has targeted the Controllers of the top 500 companies in Austria and the Czech Republic

Framework and Key Questions

Key Questions Framework

▲ Online - Questionaire● Top 500+ in Austria● Top 500+ in Czech Republic● Total ca. 1.500 companies

▲ Response rate 11,8%

▲ Range● Sales 100 m - 40 bn● Employees 60 - 30.000

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 8|

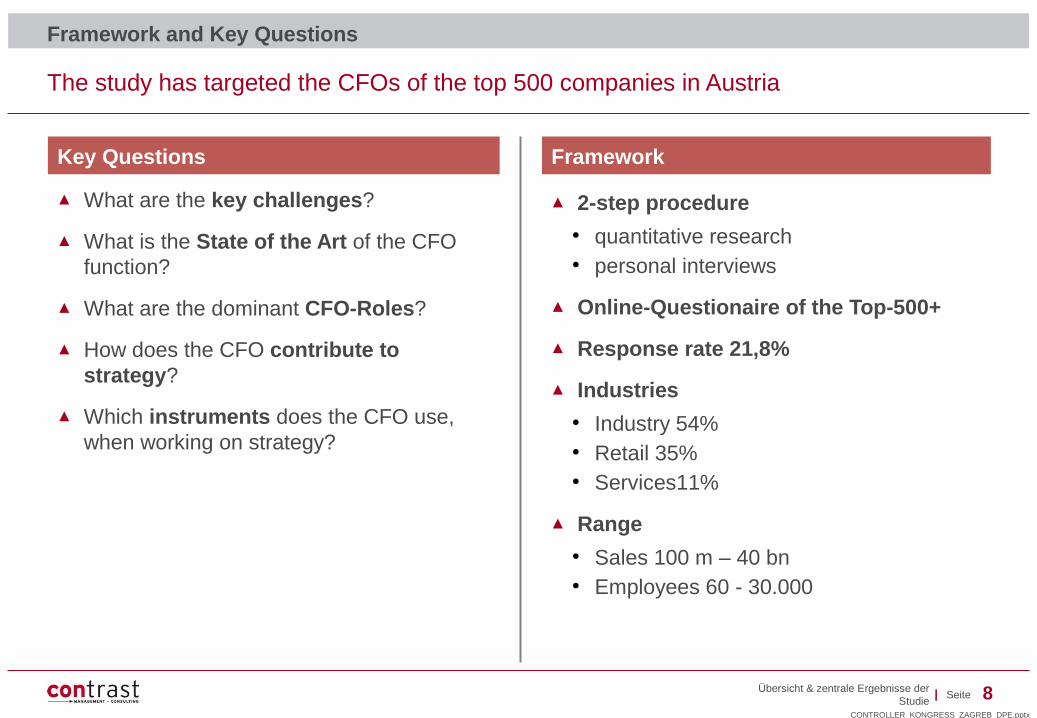

▲ What are the key challenges?

▲ What is the State of the Art of the CFO function?

▲ What are the dominant CFO-Roles?

▲ How does the CFO contribute to strategy?

▲ Which instruments does the CFO use, when working on strategy?

Übersicht & zentrale Ergebnisse der Studie

The study has targeted the CFOs of the top 500 companies in Austria

Framework and Key Questions

Key Questions Framework

▲ 2-step procedure● quantitative research● personal interviews

▲ Online-Questionaire of the Top-500+

▲ Response rate 21,8%

▲ Industries● Industry 54%● Retail 35%● Services11%

▲ Range● Sales 100 m – 40 bn● Employees 60 - 30.000

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 9|

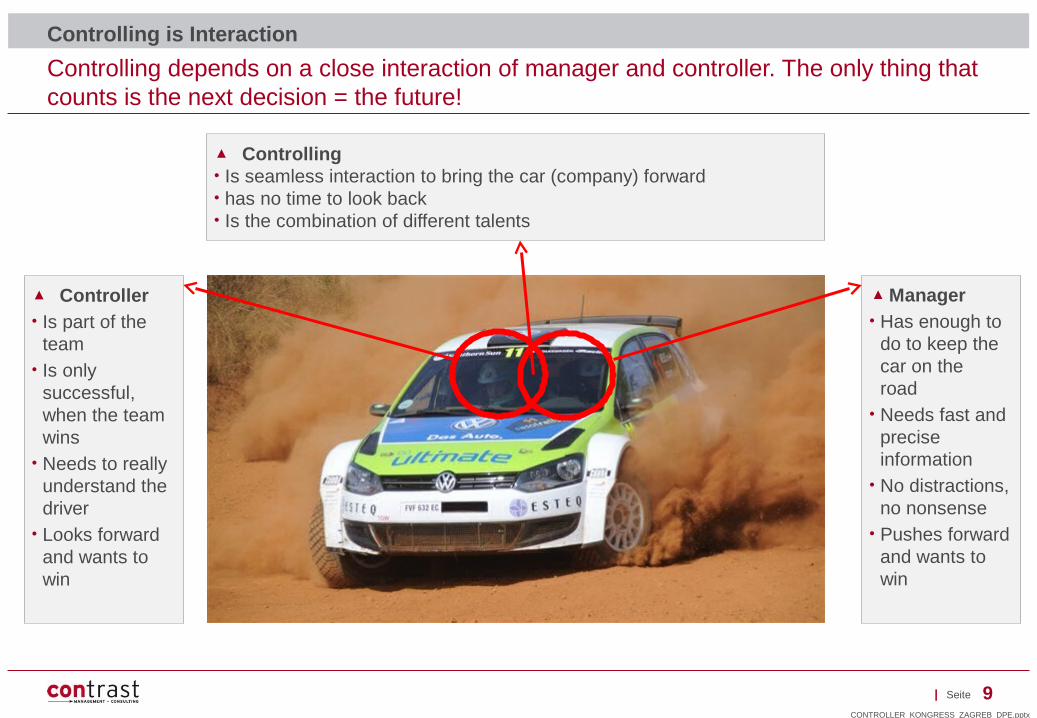

Controlling depends on a close interaction of manager and controller. The only thing that counts is the next decision = the future!

Controlling is Interaction

▲ Manager• Has enough to

do to keep the car on theroad

• Needs fast and precise information

• No distractions, no nonsense

• Pushes forward and wants to win

▲ Controller• Is part of the

team• Is only

successful, when the team wins

• Needs to really understand the driver

• Looks forward and wants to win

▲ Controlling• Is seamless interaction to bring the car (company) forward• has no time to look back• Is the combination of different talents

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 10|

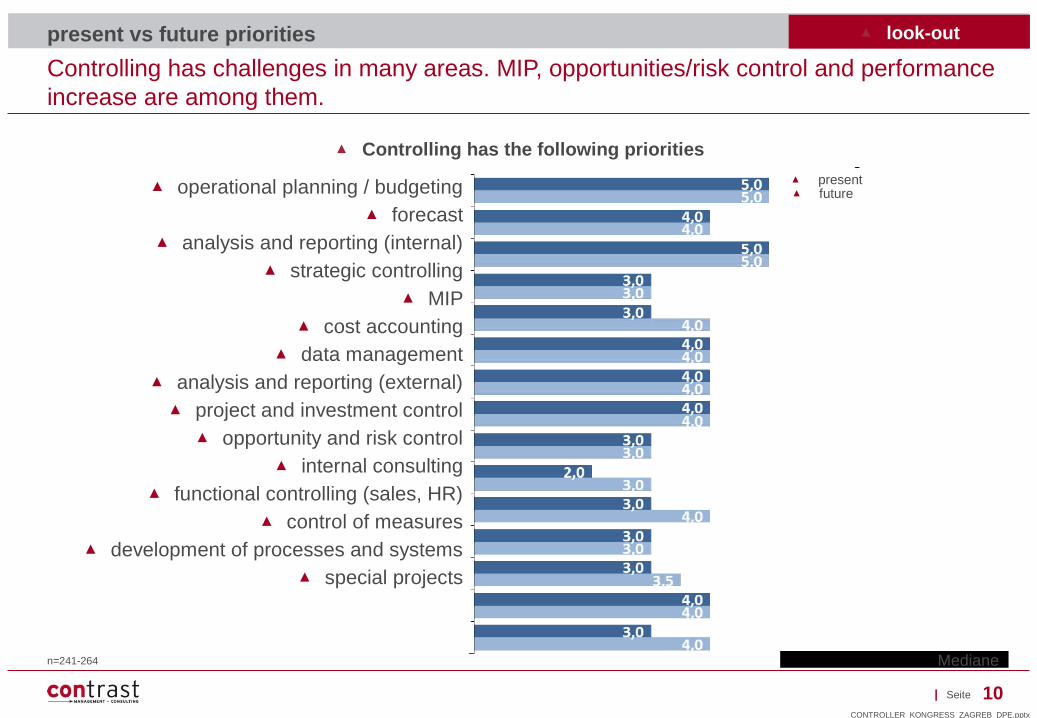

n=241-264

Controlling has challenges in many areas. MIP, opportunities/risk control and performance increase are among them.

present vs future priorities

Mediane

▲ look-out

▲ present▲ future

▲ Controlling has the following priorities

▲ operational planning / budgeting▲ forecast

▲ analysis and reporting (internal)▲ strategic controlling

▲ MIP▲ cost accounting

▲ data management▲ analysis and reporting (external)

▲ project and investment control▲ opportunity and risk control

▲ internal consulting▲ functional controlling (sales, HR)

▲ control of measures▲ development of processes and systems

▲ special projects

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 11|

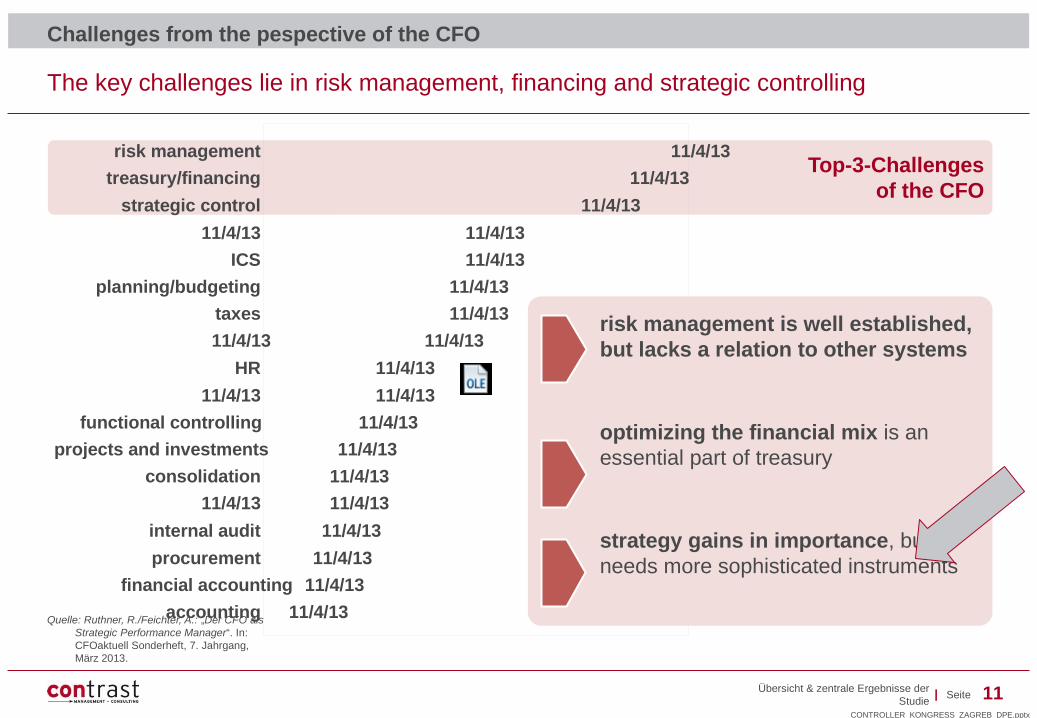

Quelle: Ruthner, R./Feichter, A.: „Der CFO als Strategic Performance Manager“. In: CFOaktuell Sonderheft, 7. Jahrgang, März 2013.

Übersicht & zentrale Ergebnisse der Studie

The key challenges lie in risk management, financing and strategic controlling

Challenges from the pespective of the CFO

accounting 11/4/13

financial accounting 11/4/13

procurement 11/4/13

internal audit

planning/budgeting 11/4/13

ICS 11/4/13

11/4/13 11/4/13

strategic control 11/4/13

treasury/financing 11/4/13

risk management 11/4/13

projects and investments 11/4/13

functional controlling 11/4/13

11/4/13 11/4/13

HR 11/4/13

11/4/13 11/4/13

taxes 11/4/13

11/4/13

consolidation 11/4/13

11/4/1311/4/13

Top-3-Challengesof the CFO

risk management is well established, but lacks a relation to other systems

optimizing the financial mix is an essential part of treasury

strategy gains in importance, but needs more sophisticated instruments

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 12|

Studies about Controlling and CFO Roles1

Strategic Management in the Public Sector 6

Strategic Management 3

Strategy in the Time of Economic Crises4

The Role of Controlling 5

Role and Tools in the Future – Strategic Performance Management

2

Agenda

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 13|

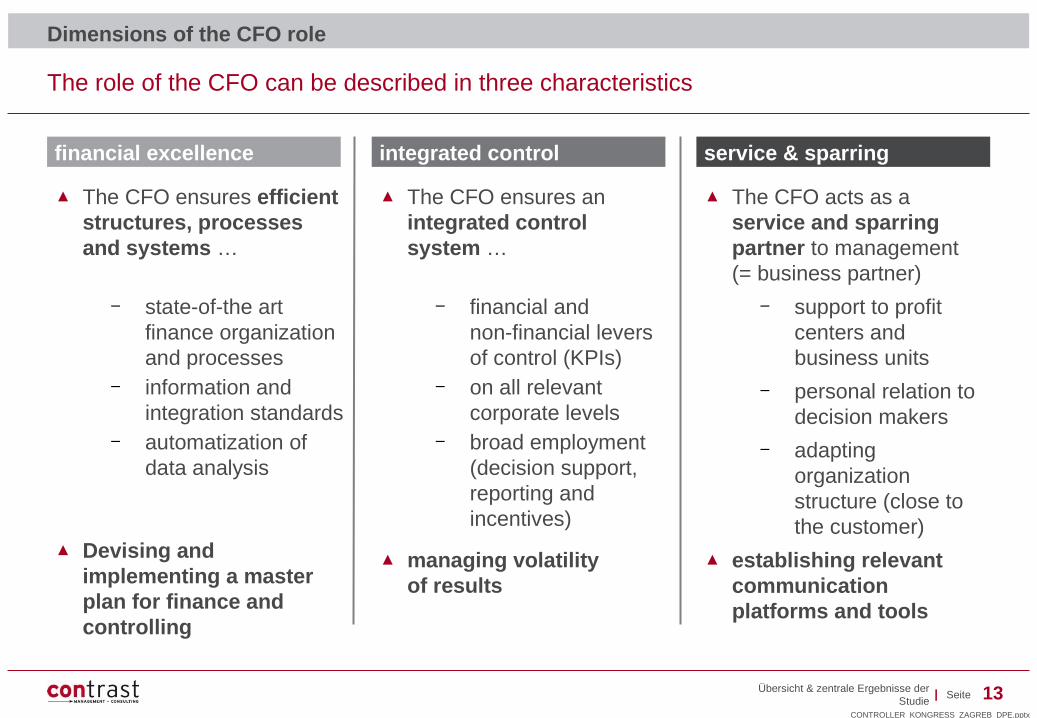

The role of the CFO can be described in three characteristics

Übersicht & zentrale Ergebnisse der Studie

integrated control

▲ The CFO ensures an integrated control system …

– financial and non-financial levers of control (KPIs)

– on all relevant corporate levels

– broad employment (decision support, reporting and incentives)

▲ managing volatility of results

financial excellence

▲ The CFO ensures efficient structures, processes and systems …

– state-of-the art finance organization and processes

– information and integration standards

– automatization of data analysis

▲ Devising and implementing a master plan for finance and controlling

Dimensions of the CFO role

service & sparring

▲ The CFO acts as a service and sparring partner to management (= business partner)

– support to profit centers and business units

– personal relation to decision makers

– adapting organization structure (close to the customer)

▲ establishing relevant communication platforms and tools

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 14|

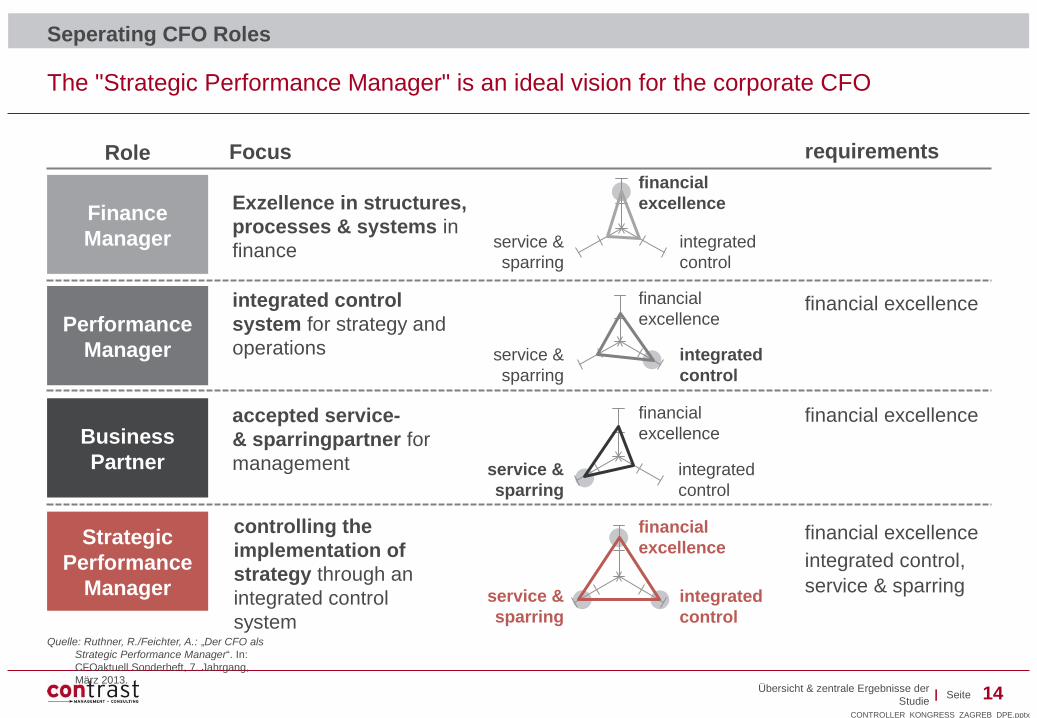

The "Strategic Performance Manager" is an ideal vision for the corporate CFO

Finance Manager

Strategic Performance

Manager

Performance Manager

Business Partner

Übersicht & zentrale Ergebnisse der Studie

Exzellence in structures, processes & systems in finance

Quelle: Ruthner, R./Feichter, A.: „Der CFO als Strategic Performance Manager“. In: CFOaktuell Sonderheft, 7. Jahrgang, März 2013.

Seperating CFO Roles

integrated control system for strategy and operations

financial excellence

Role Focus requirements

accepted service- & sparringpartner for management

financial excellence

controlling the implementation of strategy through an integrated control system

financial excellenceintegrated control,service & sparring

financial excellence

integrated control

service & sparring

financial excellence

integrated control

service & sparring

financial excellence

integrated control

service & sparring

financial excellence

integrated control

service & sparring

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 15|

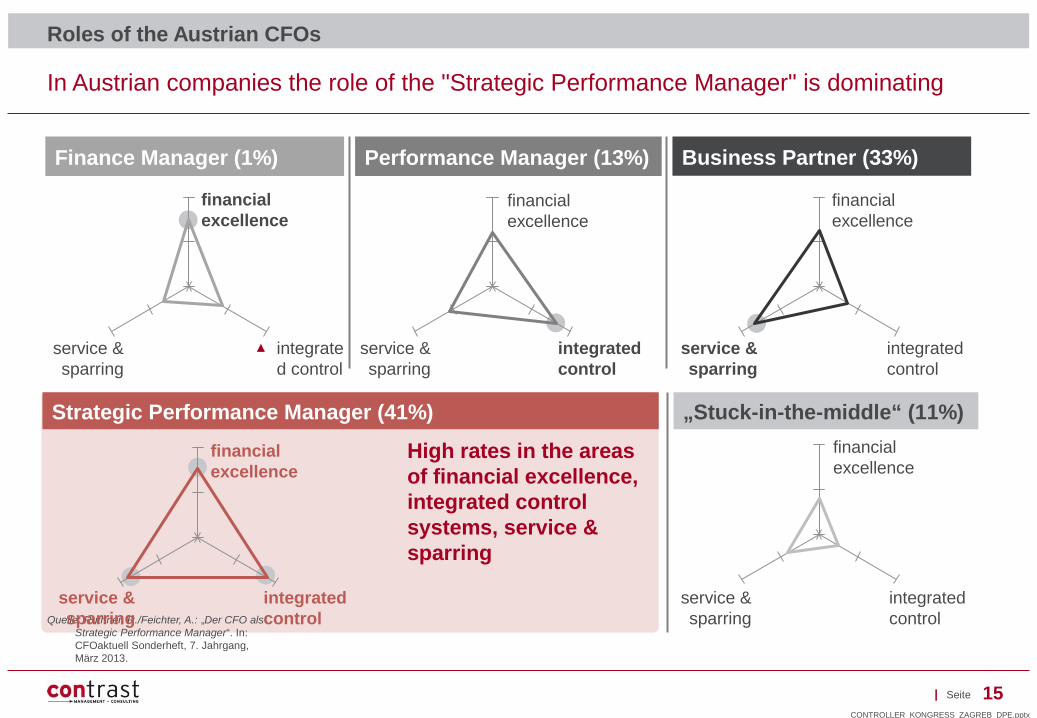

In Austrian companies the role of the "Strategic Performance Manager" is dominating

Roles of the Austrian CFOs

Finance Manager (1%) Performance Manager (13%) Business Partner (33%)

High rates in the areas of financial excellence, integrated control systems, service & sparring

„Stuck-in-the-middle“ (11%)

Quelle: Ruthner, R./Feichter, A.: „Der CFO als Strategic Performance Manager“. In: CFOaktuell Sonderheft, 7. Jahrgang, März 2013.

Strategic Performance Manager (41%)

financial excellence

▲ integrated control

service & sparring

financial excellence

integrated control

service & sparring

financial excellence

integrated control

service & sparring

financial excellence

integrated control

service & sparring

financial excellence

integrated control

service & sparring

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 16|Entwicklungsstand des Strategic Performance Managements

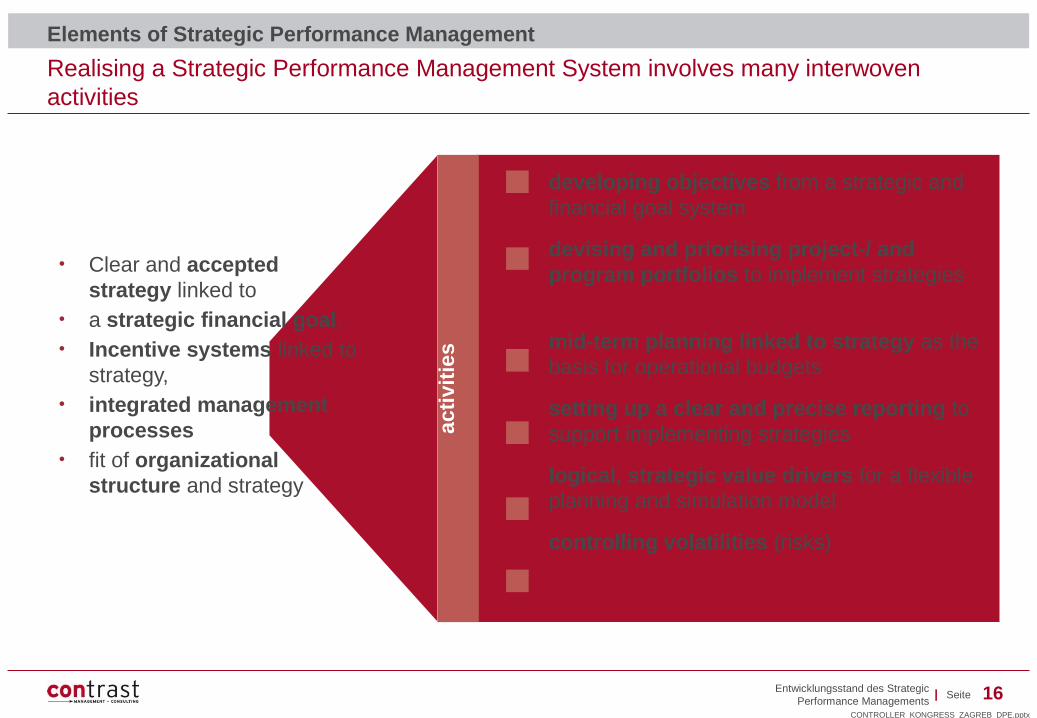

Realising a Strategic Performance Management System involves many interwoven activities

Elements of Strategic Performance Management

acti

viti

es

• Clear and accepted strategy linked to

• a strategic financial goal.• Incentive systems linked to

strategy, • integrated management

processes• fit of organizational

structure and strategy

developing objectives from a strategic and financial goal system

devising and priorising project-/ and program portfolios to implement strategies

mid-term planning linked to strategy as the basis for operational budgets

setting up a clear and precise reporting to support implementing strategies

logical, strategic value drivers for a flexible planning and simulation model

controlling volatilities (risks)

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 17|

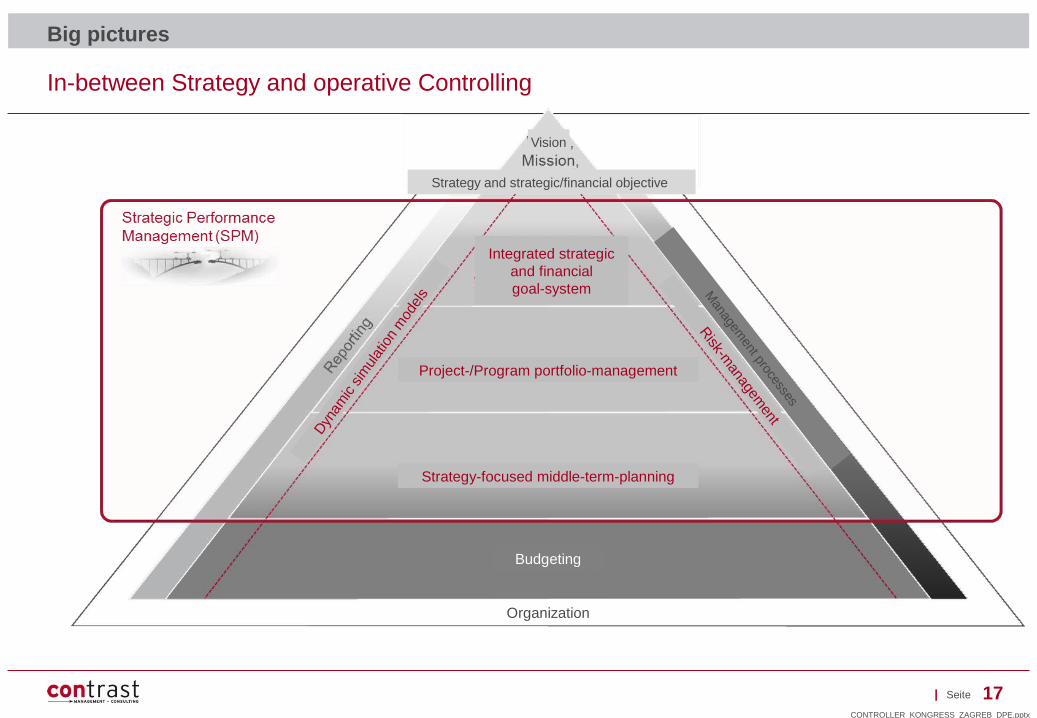

In-between Strategy and operative Controlling

Big pictures

Organization

Budgeting

Strategy-focused middle-term-planning

Project-/Program portfolio-management

Integrated strategic and financial goal-system

Risk-m

anagement

Dyn

amic

sim

ulat

ion

mod

els

Vision

Strategy and strategic/financial objective

Managem

ent processes

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 18|

CFOs of Austrian companies more and more become "Strategic Performance Managers" – financial excellence is an important basis for this development

Zusammenfassung & Handlungsempfehlungen

▲ The CFO is challenger & sparring partner of management and is an important player in corporate strategy

▲ The role of the CFO as a Strategic Performance Managers (41%) dominates in Austrian companies

▲ Financial excellence is an important condition for development in the dimensions integrated control and service & sparring

▲ In Strategic Performance Management more work is needed to ensure a forceful implementation of strategies

▲ The contributions of the CFO to corporate success are considerable and will increase in the future

CFO-Study 2012 „The CFO as Strategic Performance Manager“

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 19|

Studies about Controlling and CFO Roles1

Strategic Management in the Public Sector 6

Strategic Management 3

Strategy in the Time of Economic Crises4

The Role of Controlling 5

Role and Tools in the Future – Strategic Performance Management

2

Agenda

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 20|

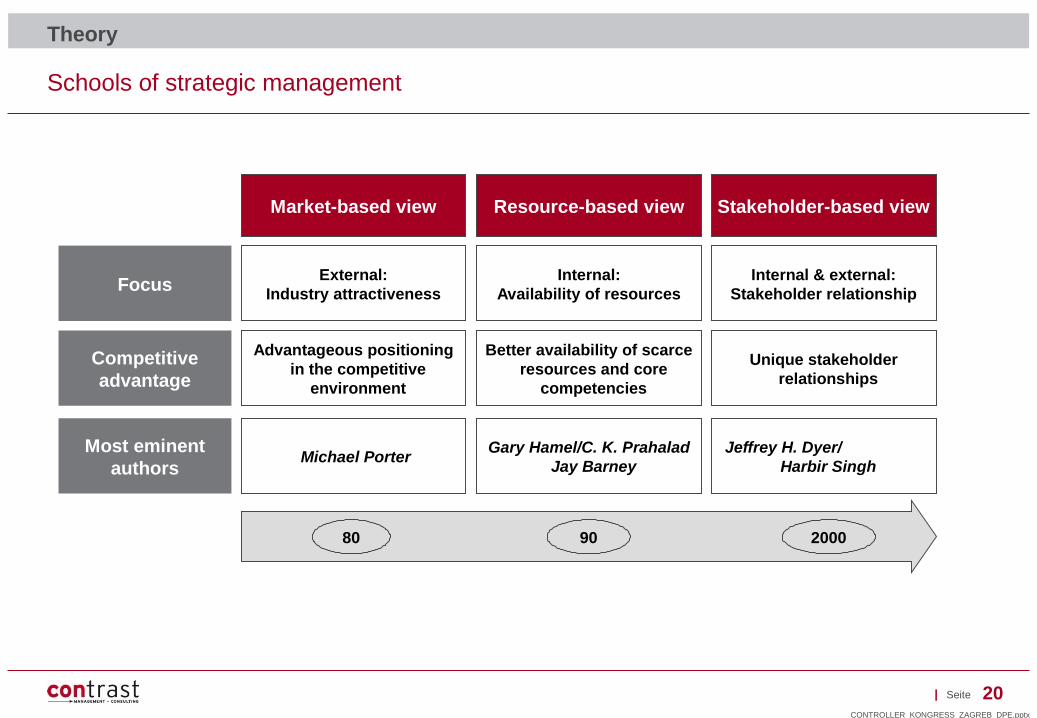

Schools of strategic management

Theory

External:Industry attractiveness

Market-based view

Advantageous positioning in the competitive

environment

Michael Porter

Stakeholder-based view

Internal & external:Stakeholder relationship

Unique stakeholder relationships

Jeffrey H. Dyer/ Harbir Singh

Resource-based view

Internal:Availability of resources

Better availability of scarce resources and core

competencies

Gary Hamel/C. K. PrahaladJay Barney

Competitive advantage

Focus

Most eminent authors

80 90 2000

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

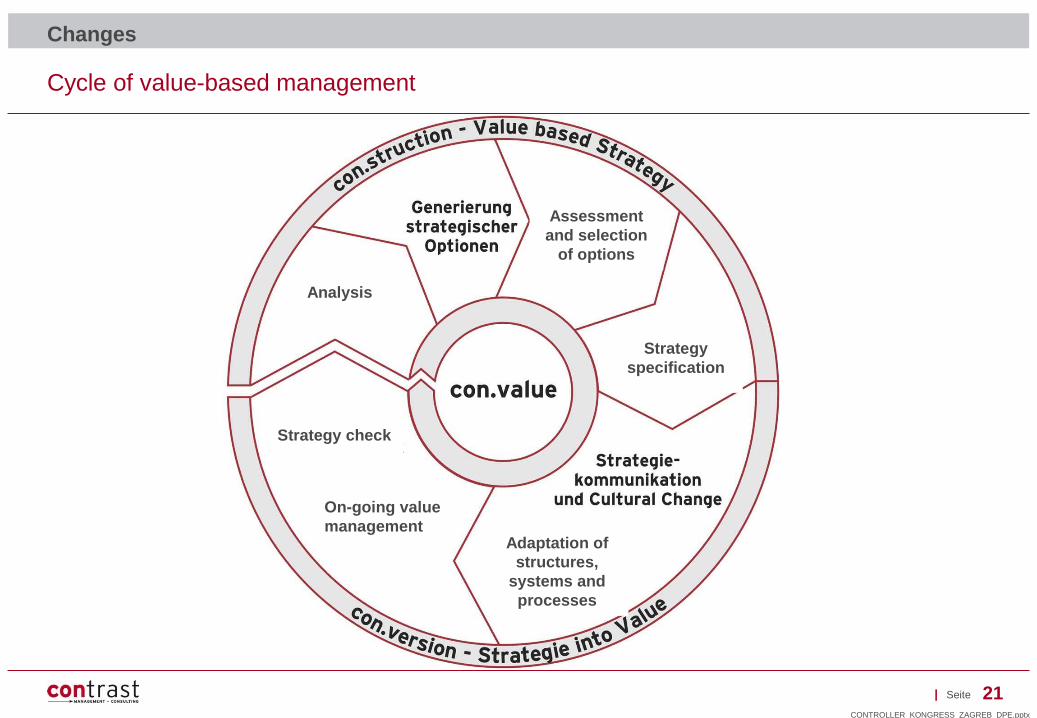

Seite 21|

Generation of strategic

option

Strategy communication and

cultural change

Cycle of value-based management

Changes

Analysis

Strategy check

On-going value management

Strategy specification

Adaptation of structures,

systems and processes

Assessment and selection

of options

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 22|

Four dimensions of strategic analysis and strategy conception

Strategic analysis

Financial performance / value creation

Processes / activities and company organization

Customer / market

Resources and potentials

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 23|

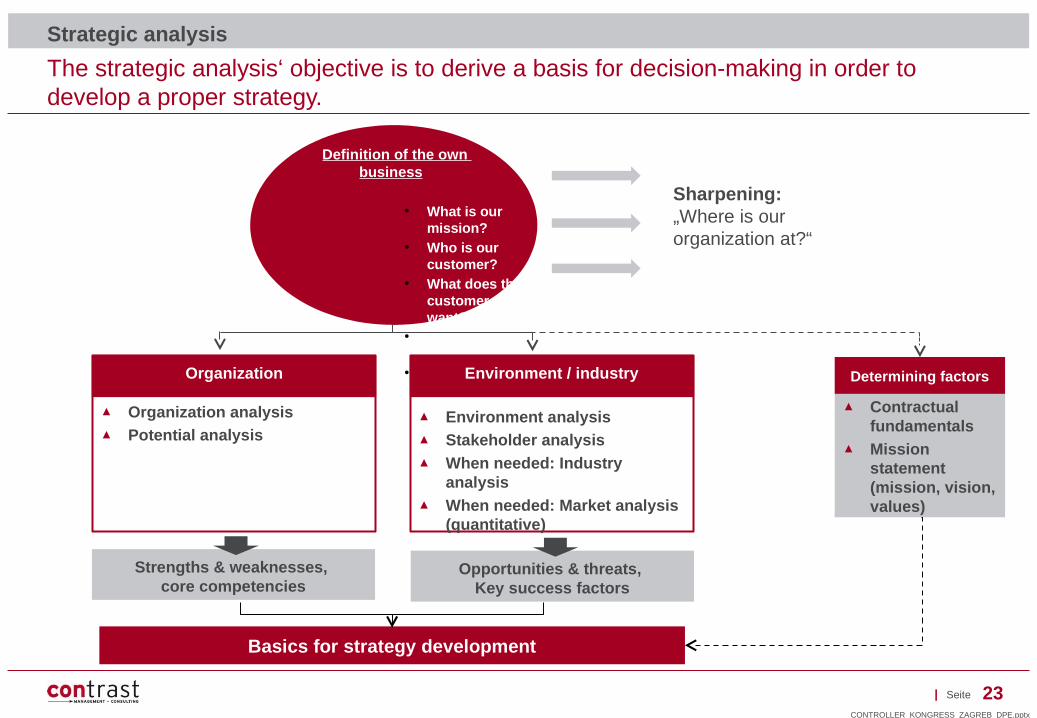

The strategic analysis‘ objective is to derive a basis for decision-making in order to develop a proper strategy.

Strategic analysis

Definition of the own business

● What is our mission?

● Who is our customer?

● What does the customer want?

● What are our results?

● What is our plan?

Environment / industry

▲ Environment analysis▲ Stakeholder analysis▲ When needed: Industry

analysis▲ When needed: Market analysis

(quantitative)

Organization

▲ Organization analysis▲ Potential analysis

Strengths & weaknesses, core competencies

Opportunities & threats, Key success factors

Sharpening: „Where is our organization at?“

▲ Contractual fundamentals

▲ Mission statement (mission, vision, values)

Determining factors

Basics for strategy development

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 24|

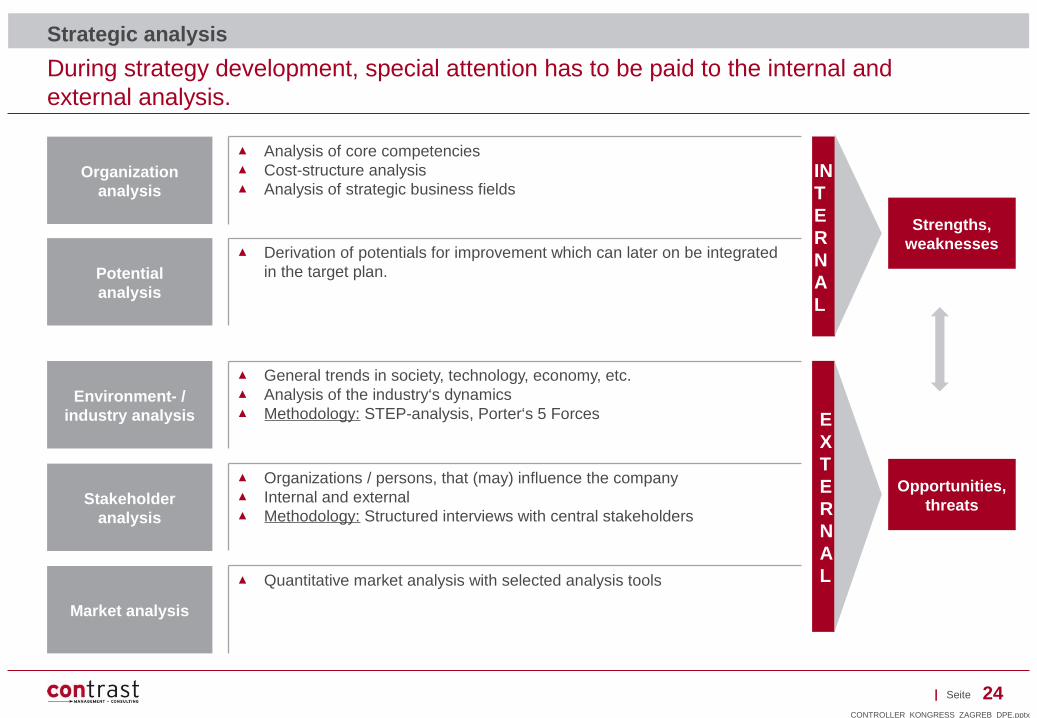

During strategy development, special attention has to be paid to the internal and external analysis.

Strategic analysis

Organization analysis

Potential analysis

▲ Analysis of core competencies▲ Cost-structure analysis▲ Analysis of strategic business fields

▲ Derivation of potentials for improvement which can later on be integrated in the target plan.

Environment- / industry analysis

Stakeholder analysis

▲ General trends in society, technology, economy, etc.▲ Analysis of the industry‘s dynamics ▲ Methodology: STEP-analysis, Porter‘s 5 Forces

▲ Organizations / persons, that (may) influence the company▲ Internal and external▲ Methodology: Structured interviews with central stakeholders

INTERNAL

EXTERNAL

Market analysis

▲ Quantitative market analysis with selected analysis tools

Opportunities, threats

Strengths, weaknesses

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 25|

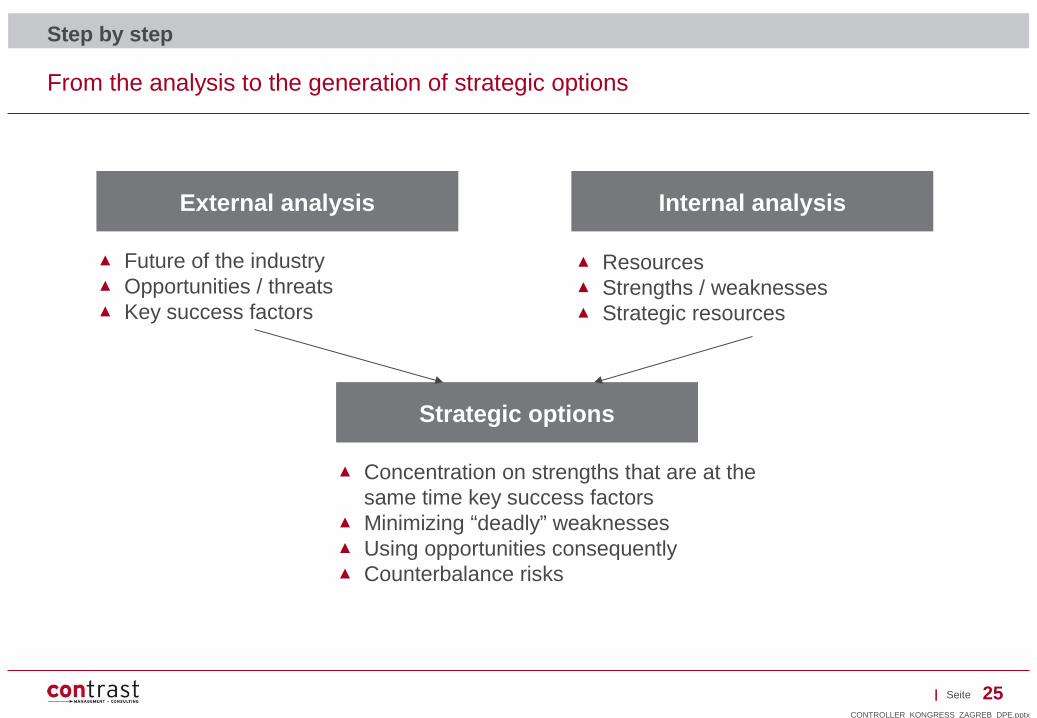

From the analysis to the generation of strategic options

Step by step

External analysis Internal analysis

Strategic options

▲ Future of the industry▲ Opportunities / threats▲ Key success factors

▲ Resources▲ Strengths / weaknesses▲ Strategic resources

▲ Concentration on strengths that are at the same time key success factors

▲ Minimizing “deadly” weaknesses▲ Using opportunities consequently ▲ Counterbalance risks

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

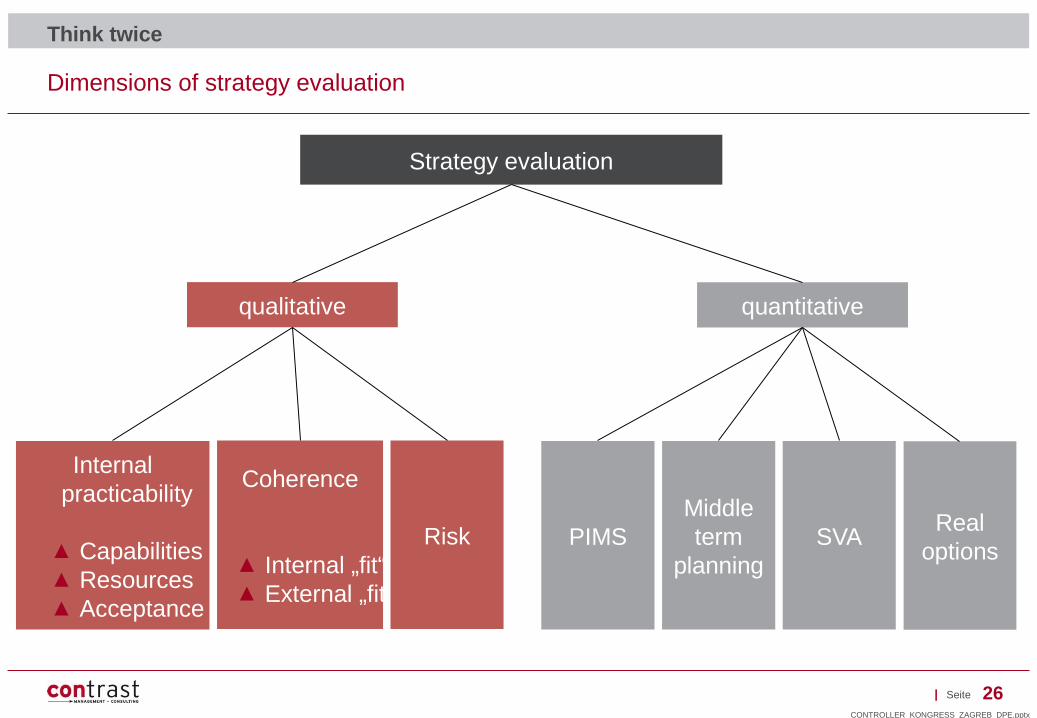

Seite 26|

Dimensions of strategy evaluation

Think twice

Strategy evaluation

qualitative quantitative

Internalpracticability

▲ Capabilities▲ Resources▲ Acceptance

Coherence

▲ Internal „fit“▲ External „fit“

Risk PIMS SVAReal

options

Middleterm

planning

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

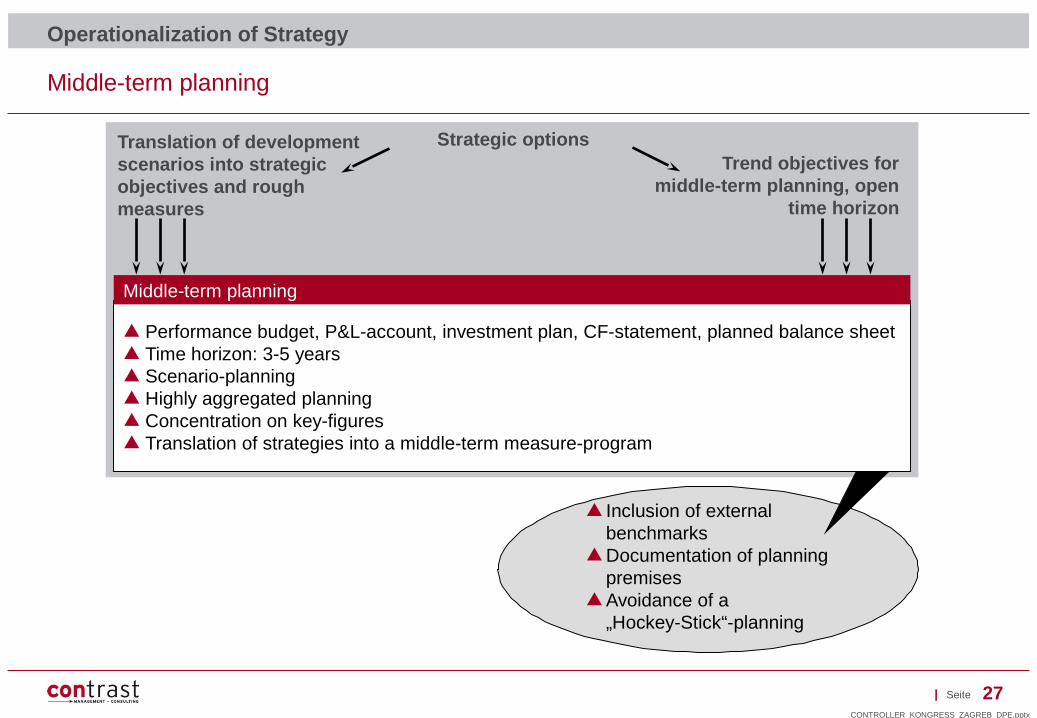

Seite 27|

Middle-term planning

Operationalization of Strategy

▲ Inclusion of external benchmarks

▲ Documentation of planning premises

▲ Avoidance of a „Hockey-Stick“-planning

▲ Performance budget, P&L-account, investment plan, CF-statement, planned balance sheet ▲ Time horizon: 3-5 years▲ Scenario-planning▲ Highly aggregated planning▲ Concentration on key-figures▲ Translation of strategies into a middle-term measure-program

Middle-term planning

Strategic optionsTranslation of developmentscenarios into strategic objectives and rough measures

Trend objectives for middle-term planning, open

time horizon

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 28|

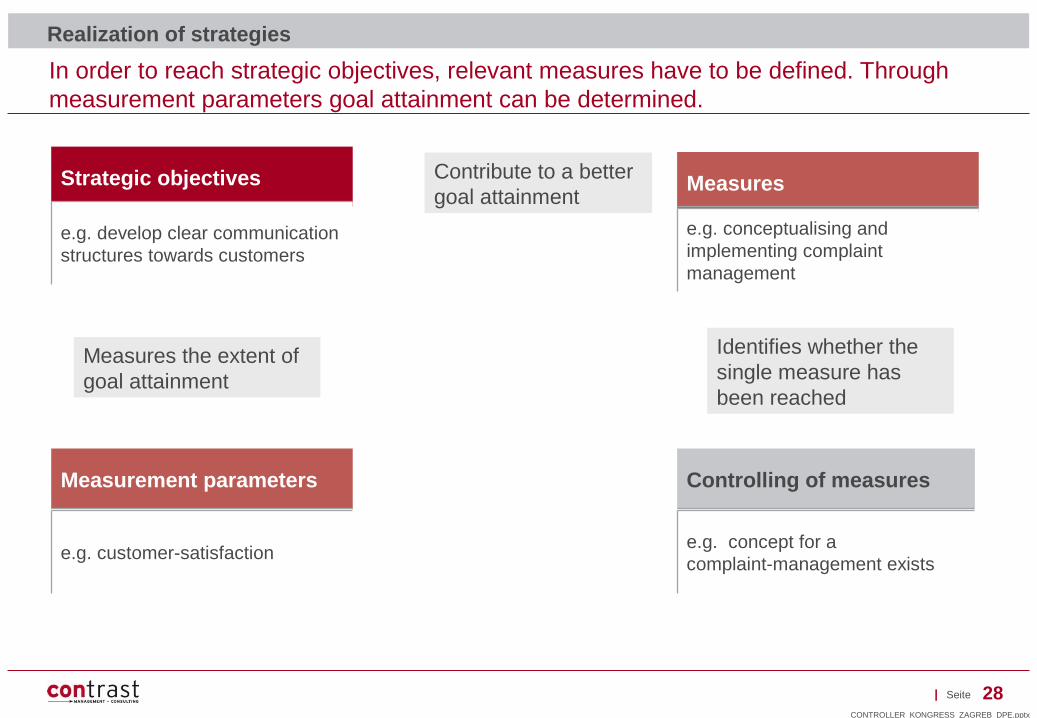

Realization of strategies

Measurement parameters

Measures

Controlling of measures

e.g. customer-satisfaction

e.g. conceptualising and implementing complaint management

e.g. concept for a complaint-management exists

Strategic objectives

e.g. develop clear communication structures towards customers

Measures the extent of goal attainment

Identifies whether the single measure has been reached

Contribute to a better goal attainment

In order to reach strategic objectives, relevant measures have to be defined. Through measurement parameters goal attainment can be determined.

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 29|

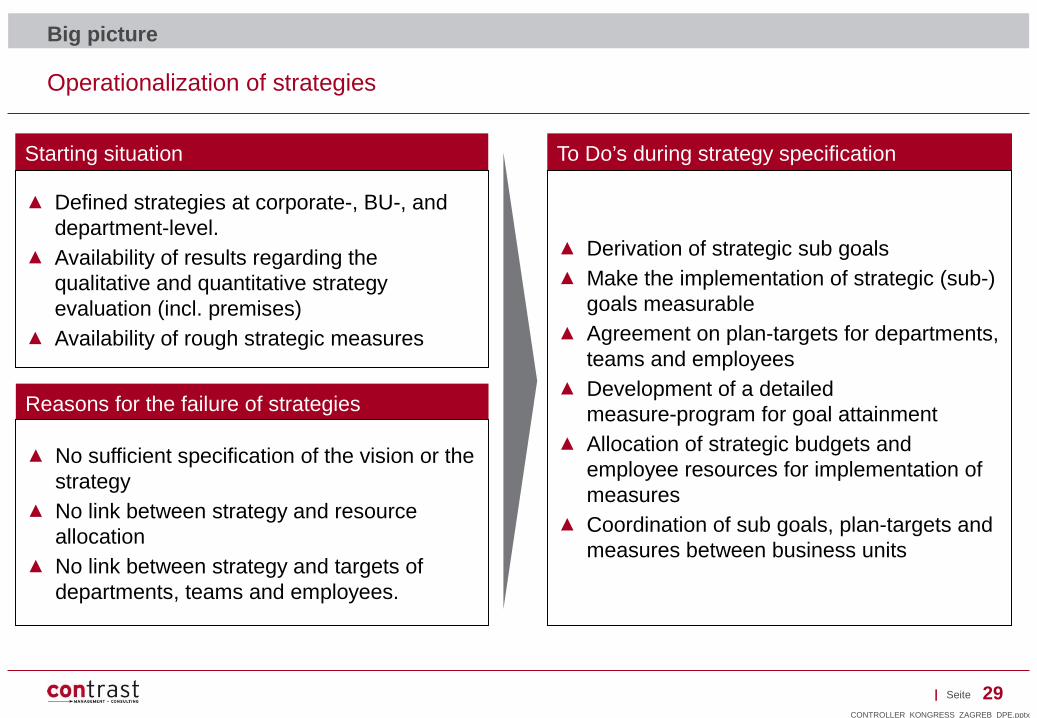

Operationalization of strategies

Big picture

Reasons for the failure of strategies

▲ No sufficient specification of the vision or the strategy

▲ No link between strategy and resource allocation

▲ No link between strategy and targets of departments, teams and employees.

Starting situation

▲ Defined strategies at corporate-, BU-, and department-level.

▲ Availability of results regarding the qualitative and quantitative strategy evaluation (incl. premises)

▲ Availability of rough strategic measures

To Do’s during strategy specification

▲ Derivation of strategic sub goals▲ Make the implementation of strategic (sub-)

goals measurable ▲ Agreement on plan-targets for departments,

teams and employees ▲ Development of a detailed

measure-program for goal attainment ▲ Allocation of strategic budgets and

employee resources for implementation of measures

▲ Coordination of sub goals, plan-targets and measures between business units

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 30|

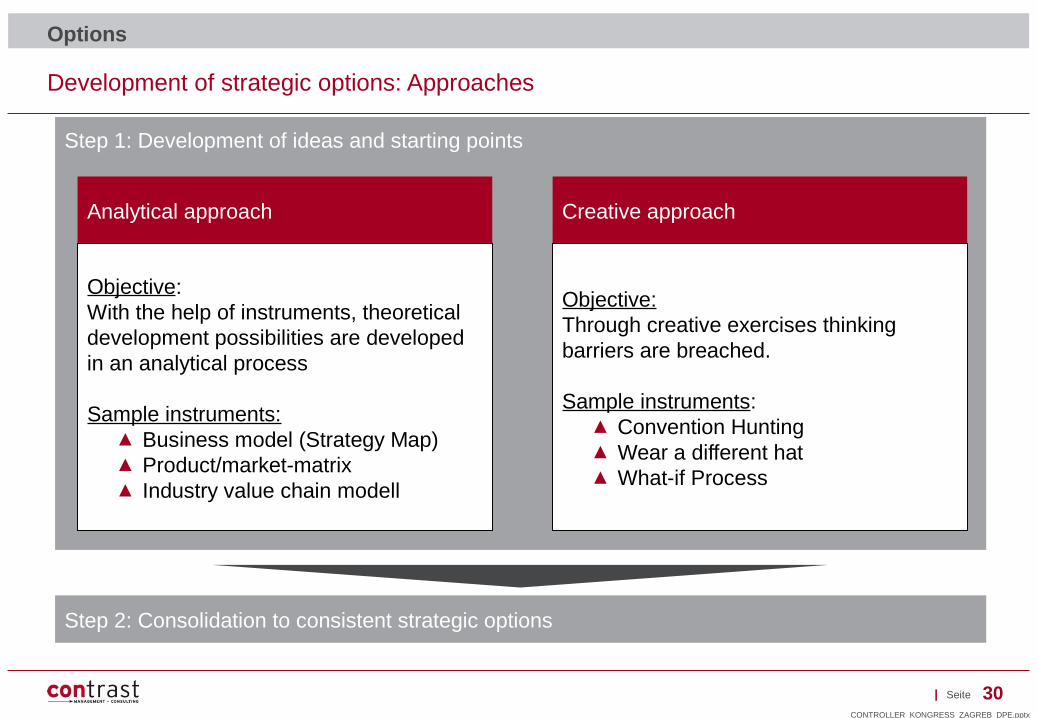

Development of strategic options: Approaches

Options

Step 1: Development of ideas and starting points

Analytical approach Creative approach

Step 2: Consolidation to consistent strategic options

Objective:With the help of instruments, theoretical development possibilities are developed in an analytical process

Sample instruments:▲ Business model (Strategy Map)▲ Product/market-matrix▲ Industry value chain modell

Objective:Through creative exercises thinking barriers are breached.

Sample instruments:▲ Convention Hunting▲ Wear a different hat▲ What-if Process

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 31|

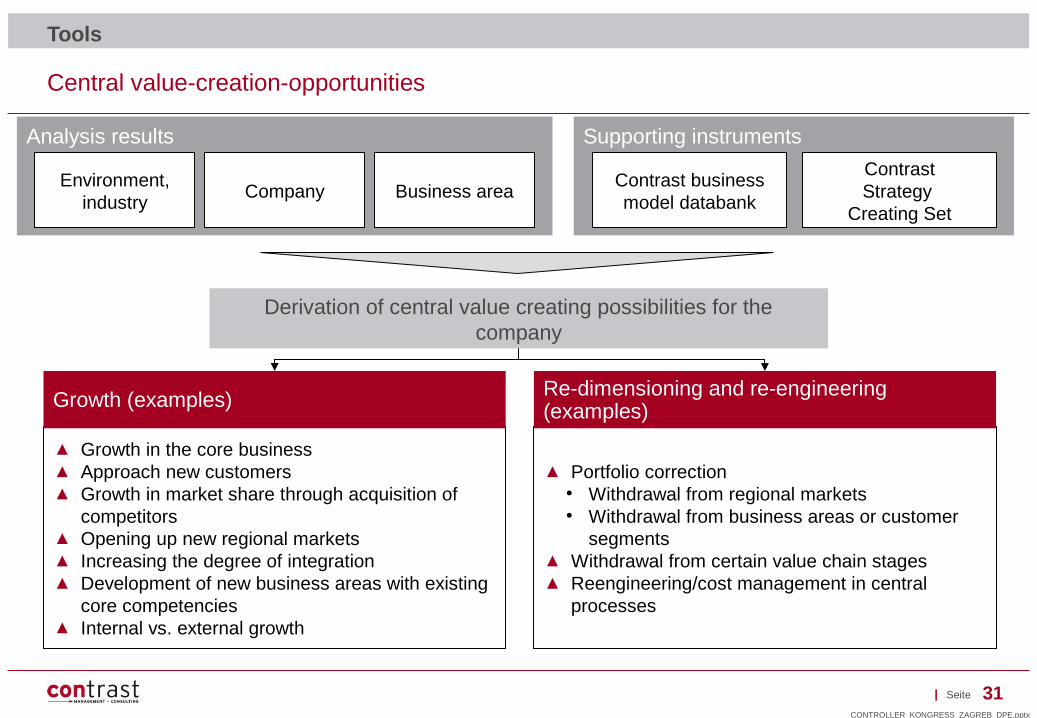

Central value-creation-opportunities

Tools

▲ Portfolio correction● Withdrawal from regional markets● Withdrawal from business areas or customer

segments▲ Withdrawal from certain value chain stages▲ Reengineering/cost management in central

processes

▲ Growth in the core business▲ Approach new customers▲ Growth in market share through acquisition of

competitors▲ Opening up new regional markets▲ Increasing the degree of integration▲ Development of new business areas with existing

core competencies ▲ Internal vs. external growth

Growth (examples)

Derivation of central value creating possibilities for the company

Re-dimensioning and re-engineering (examples)

Analysis results Supporting instruments

Contrast business model databank

ContrastStrategy

Creating Set

Environment, industry

Company Business area

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 32|

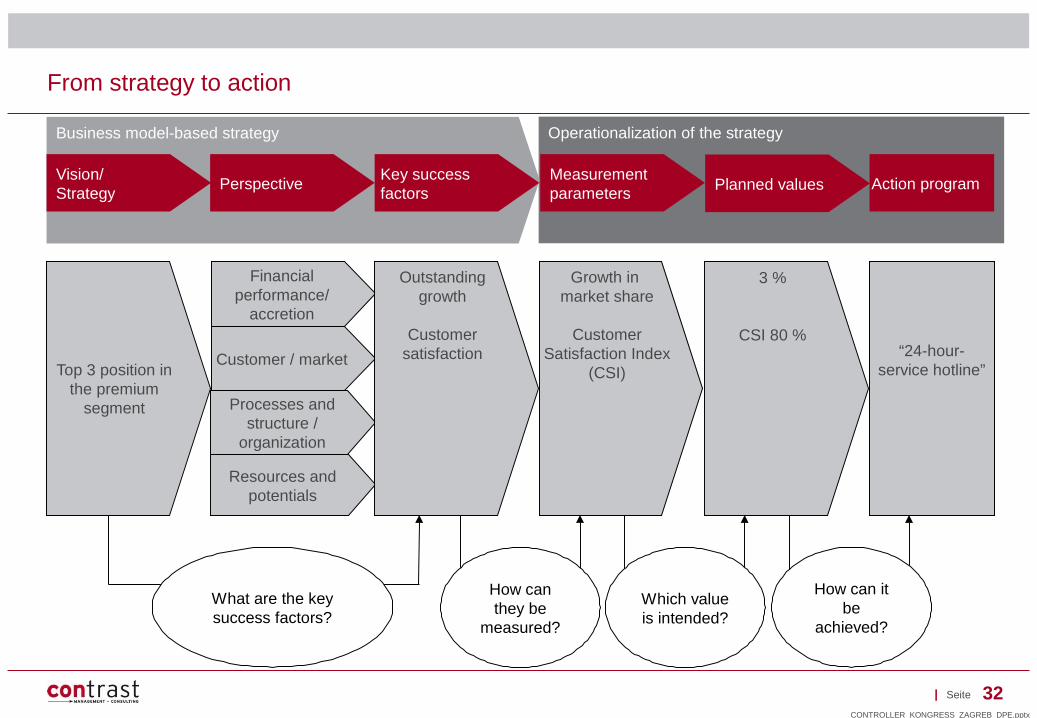

From strategy to action

Operationalization of the strategyBusiness model-based strategy

“24-hour-service hotline”

Action programVision/ Strategy

PerspectiveKey success factors

Measurementparameters

Planned values

How can they be

measured?

Which value is intended?

How can it be

achieved?

What are the key success factors?

Financial performance/

accretion

Customer / market

Processes and structure /

organization

Resources and potentials

Top 3 position in the premium

segment

Outstanding growth

Customer satisfaction

Growth in market share

Customer Satisfaction Index

(CSI)

3 %

CSI 80 %

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 33|

Studies about Controlling and CFO Roles1

Strategic Management in the Public Sector 6

Strategic Management 3

Strategy in the Time of Economic Crises4

The Role of Controlling 5

Role and Tools in the Future – Strategic Performance Management

2

Agenda

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 34|

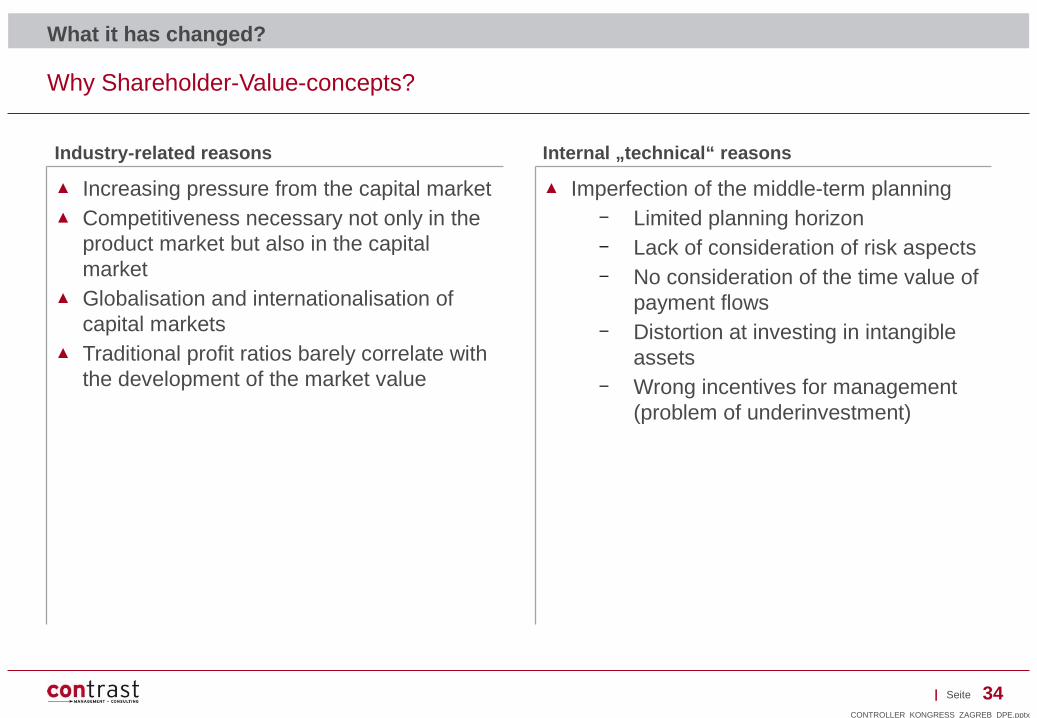

Industry-related reasons Internal „technical“ reasons

Why Shareholder-Value-concepts?

▲ Increasing pressure from the capital market▲ Competitiveness necessary not only in the

product market but also in the capital market

▲ Globalisation and internationalisation of capital markets

▲ Traditional profit ratios barely correlate with the development of the market value

▲ Imperfection of the middle-term planning– Limited planning horizon– Lack of consideration of risk aspects– No consideration of the time value of

payment flows– Distortion at investing in intangible

assets– Wrong incentives for management

(problem of underinvestment)

What it has changed?

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 35|

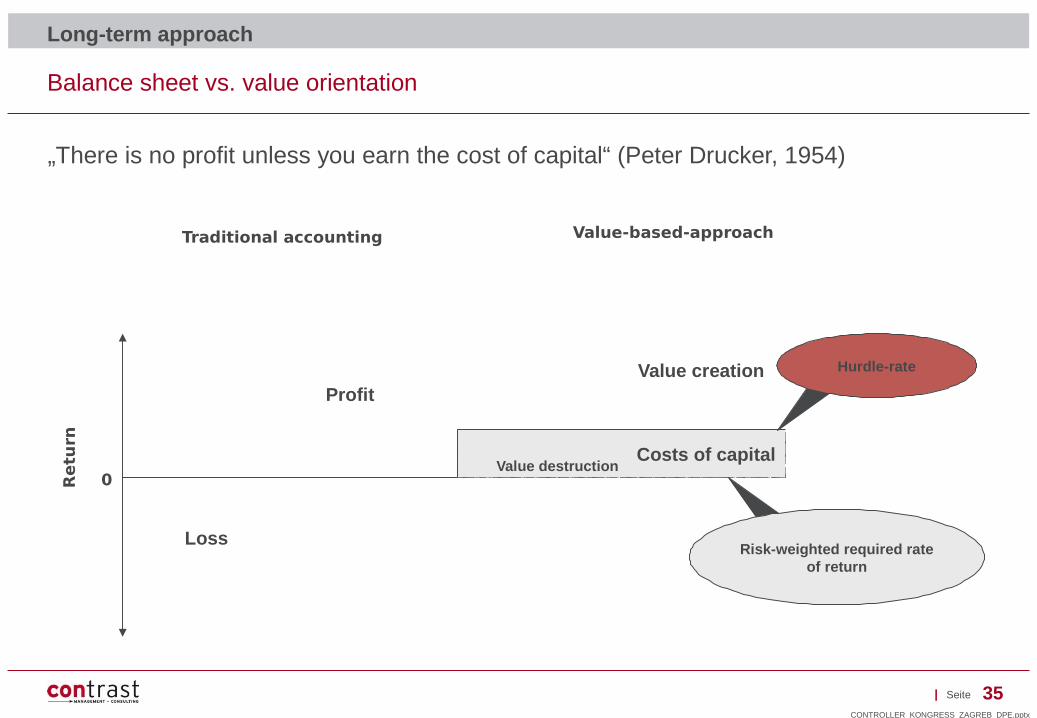

Balance sheet vs. value orientation

Long-term approach

„There is no profit unless you earn the cost of capital“ (Peter Drucker, 1954)

Traditional accounting Value-based-approach

0Retu

rn

Loss

Value creationProfit

Costs of capitalValue destruction

Hurdle-rate

Risk-weighted required rate of return

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 36|

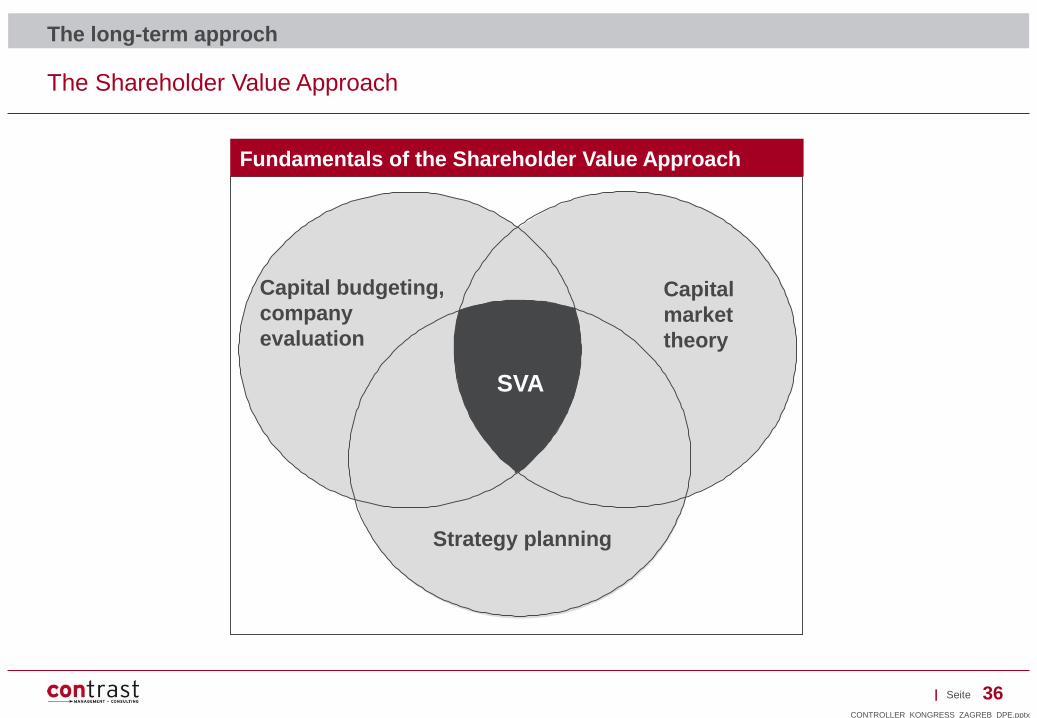

The Shareholder Value Approach

The long-term approch

Capital budgeting, company evaluation

Capital markettheory

Strategy planning

SVA

Fundamentals of the Shareholder Value Approach

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 37|

Initial situation I

▲ Insufficient specification of strategic objectives and strategies▲ Missing quantification of strategic objectives and strategies▲ Performance Measurement is only concentrated on operative financial indicators▲ Market-based and financial planning- and management systems are not sufficiently integrated ▲ Measures in order to optimize market performance and financial performance are not

sufficiently coordinated ▲ Profound understanding of value- and cost-drivers is often missing in the management team

Linking financial and strategic values

„Strategy world“ and „financial world“ often co-exist and are most of the time not linked systematically

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 38|

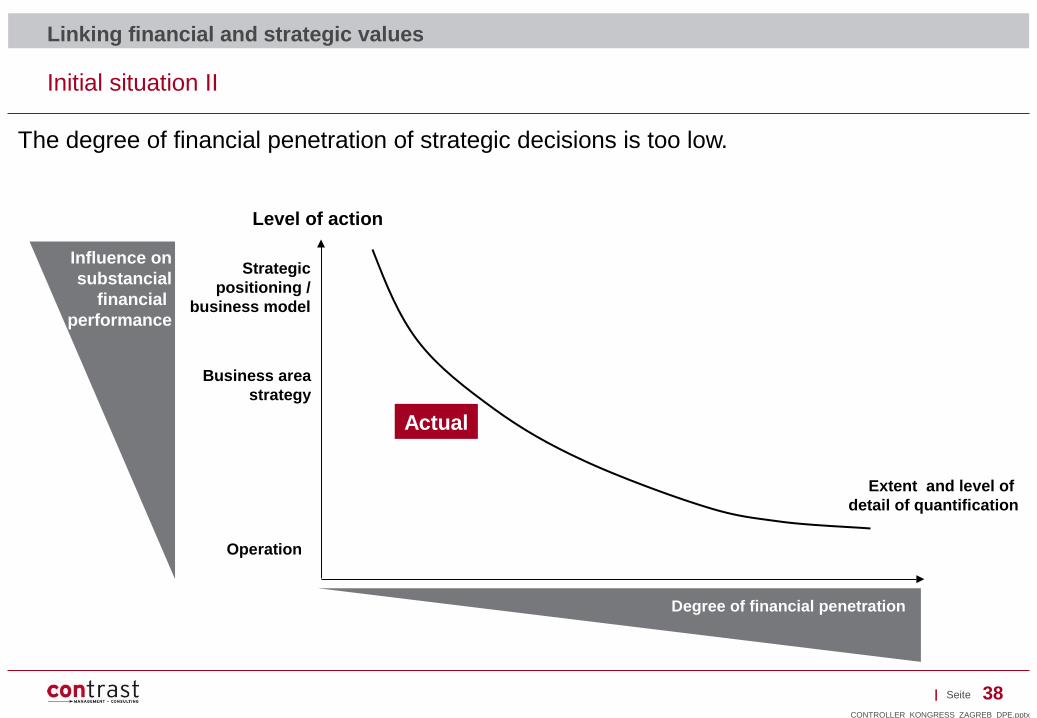

Initial situation II

Linking financial and strategic values

The degree of financial penetration of strategic decisions is too low.

Influence on substancial

financial performance

Level of action

Strategic positioning /

business model

Business area strategy

Operation

Degree of financial penetration

Extent and level of detail of quantification

Actual

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 39|

Challenges I

▲ Specification and quantification of strategic objectives and strategies

▲ Supplementation of performance-measurement through strategic pre-control measures

▲ Integration of market- and financial-based planning and controlling systems

▲ Missionizing the company for financial performance targets

Linking financial and strategic values

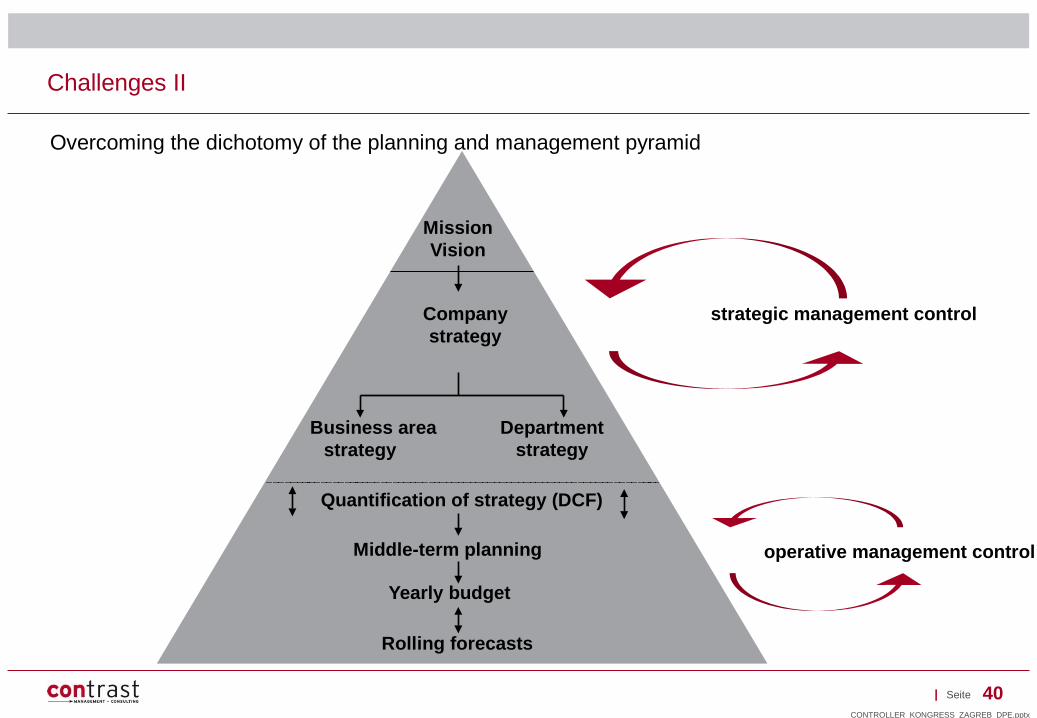

Contentual business planning and business controlling as well as financial planning and financial controlling have to be systematically linked between all levels of action.

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 40|

Challenges II

Overcoming the dichotomy of the planning and management pyramid

strategic management control

operative management control

Departmentstrategy

Business areastrategy

Quantification of strategy (DCF)

MissionVision

Companystrategy

Middle-term planning

Yearly budget

Rolling forecasts

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 41|

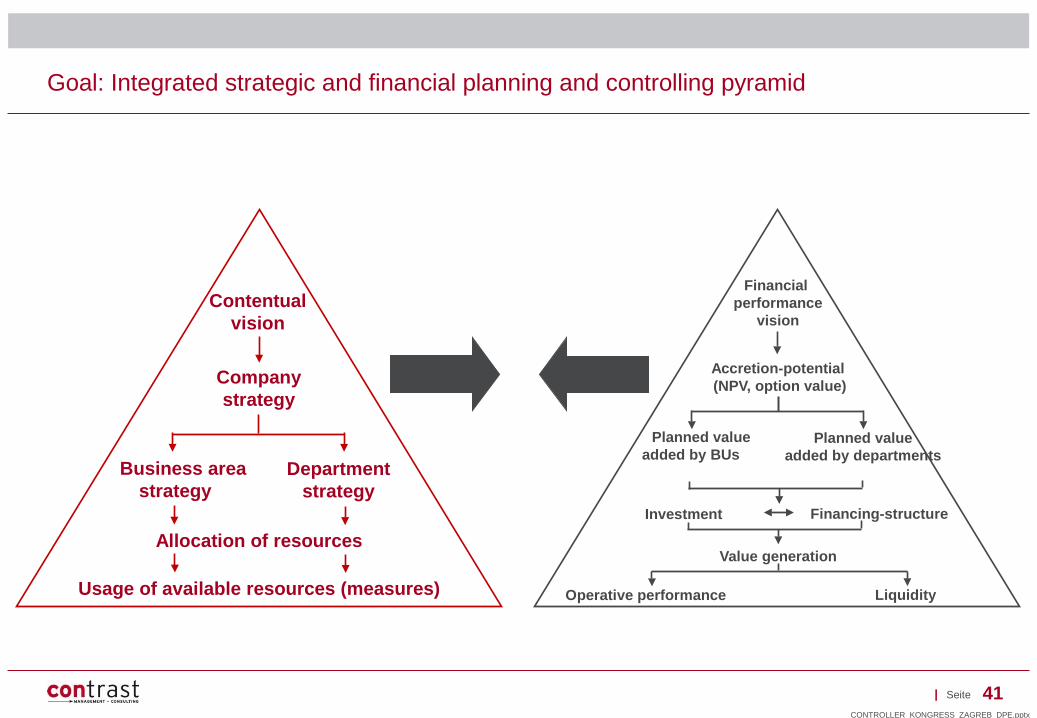

Goal: Integrated strategic and financial planning and controlling pyramid

Companystrategy

Contentualvision

Business areastrategy

Allocation of resources

Departmentstrategy

Usage of available resources (measures)

Accretion-potential (NPV, option value)

Financial performance

vision

Planned valueadded by BUs

Value generation

Planned valueadded by departments

Operative performance Liquidity

Investment Financing-structure

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 42|

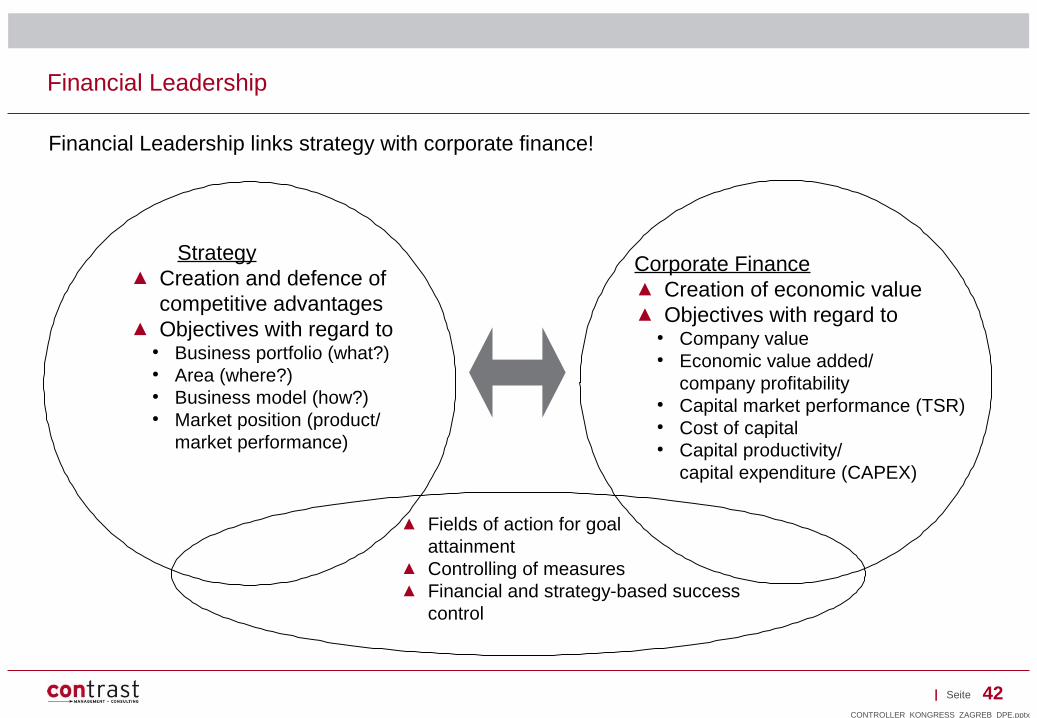

Financial Leadership

▲ Fields of action for goal attainment

▲ Controlling of measures▲ Financial and strategy-based success

control

Strategy▲ Creation and defence of

competitive advantages▲ Objectives with regard to

● Business portfolio (what?)● Area (where?)● Business model (how?)● Market position (product/

market performance)

Corporate Finance▲ Creation of economic value▲ Objectives with regard to

● Company value● Economic value added/

company profitability● Capital market performance (TSR)● Cost of capital● Capital productivity/

capital expenditure (CAPEX)

Financial Leadership links strategy with corporate finance!

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 43|

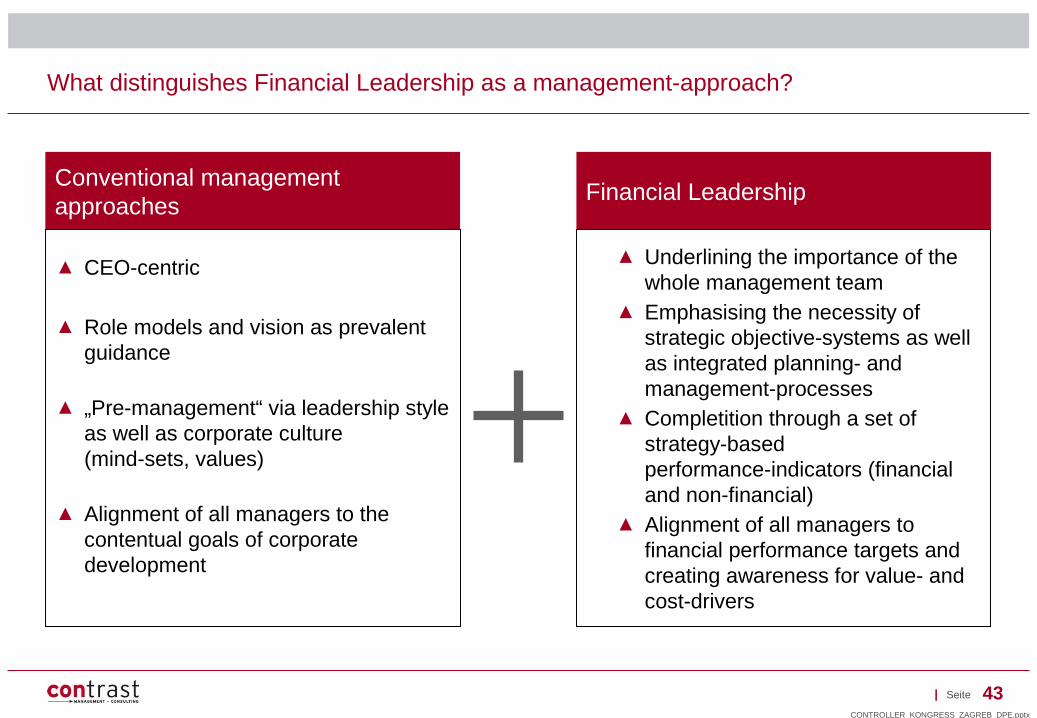

What distinguishes Financial Leadership as a management-approach?

▲ CEO-centric

▲ Role models and vision as prevalent guidance

▲ „Pre-management“ via leadership style as well as corporate culture (mind-sets, values)

▲ Alignment of all managers to the contentual goals of corporate development

Conventional management approaches

▲ Underlining the importance of the whole management team

▲ Emphasising the necessity of strategic objective-systems as well as integrated planning- and management-processes

▲ Completition through a set of strategy-based performance-indicators (financial and non-financial)

▲ Alignment of all managers to financial performance targets and creating awareness for value- and cost-drivers

Financial Leadership

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 44|

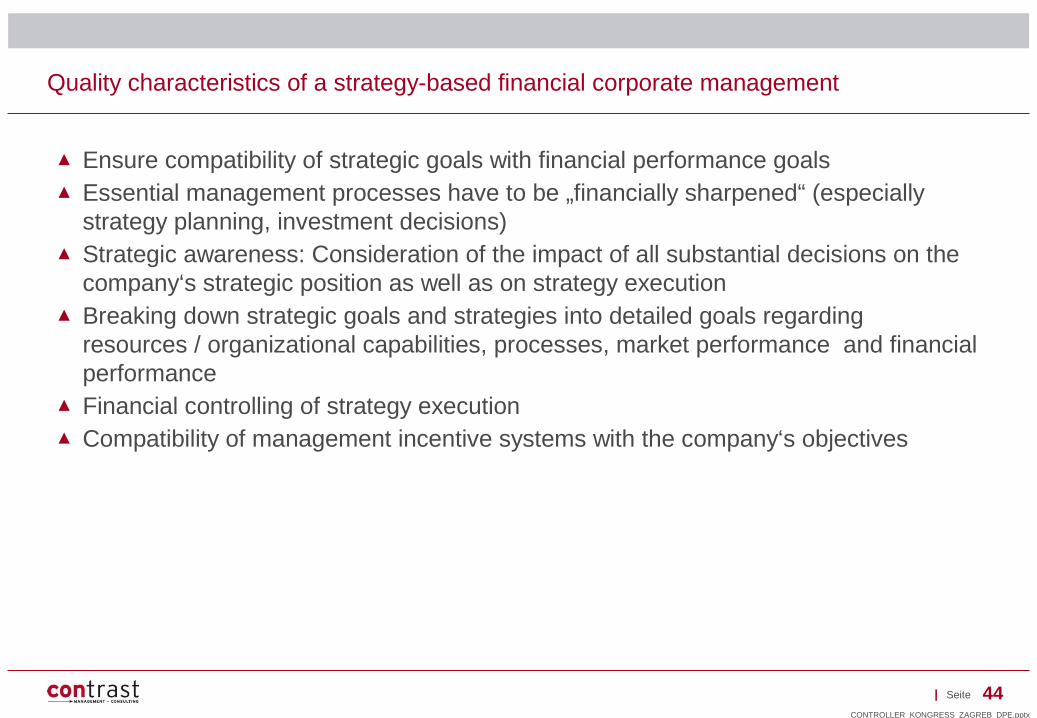

Quality characteristics of a strategy-based financial corporate management

▲ Ensure compatibility of strategic goals with financial performance goals▲ Essential management processes have to be „financially sharpened“ (especially

strategy planning, investment decisions)▲ Strategic awareness: Consideration of the impact of all substantial decisions on the

company‘s strategic position as well as on strategy execution▲ Breaking down strategic goals and strategies into detailed goals regarding

resources / organizational capabilities, processes, market performance and financial performance

▲ Financial controlling of strategy execution▲ Compatibility of management incentive systems with the company‘s objectives

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 45|

Studies about Controlling and CFO Roles1

Strategic Management in the Public Sector 6

Strategic Management 3

Strategy in the Time of Economic Crises4

The Role of Controlling 5

Role and Tools in the Future – Strategic Performance Management

2

Agenda

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 46|

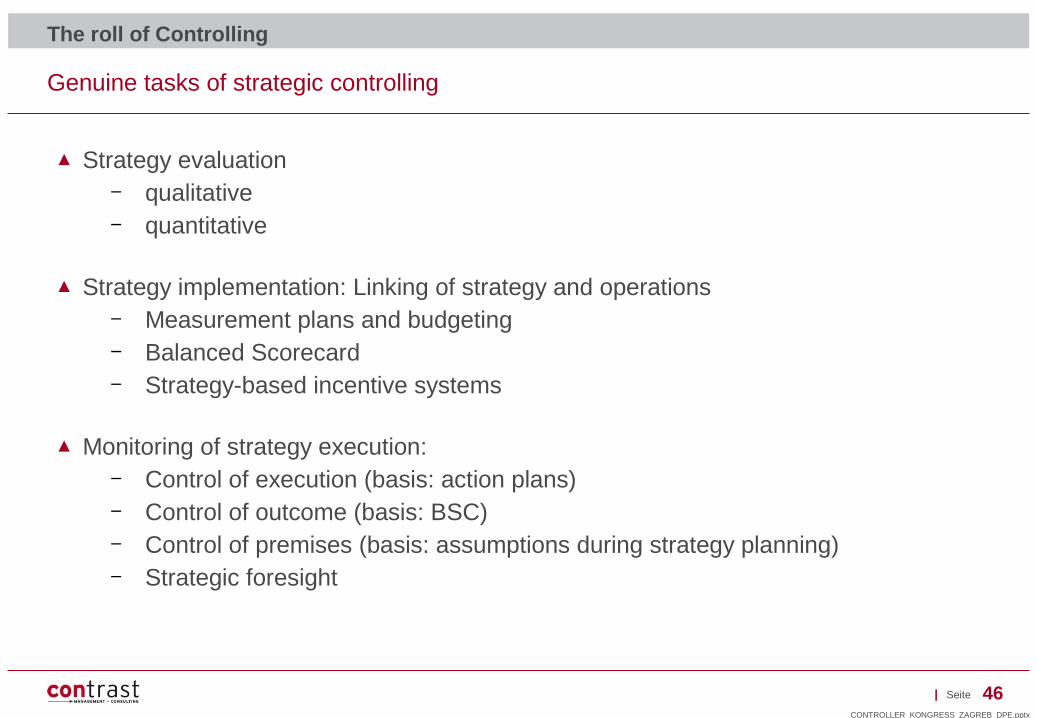

Genuine tasks of strategic controlling

▲ Strategy evaluation– qualitative– quantitative

▲ Strategy implementation: Linking of strategy and operations– Measurement plans and budgeting– Balanced Scorecard– Strategy-based incentive systems

▲ Monitoring of strategy execution:– Control of execution (basis: action plans)– Control of outcome (basis: BSC)– Control of premises (basis: assumptions during strategy planning)– Strategic foresight

The roll of Controlling

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 47|

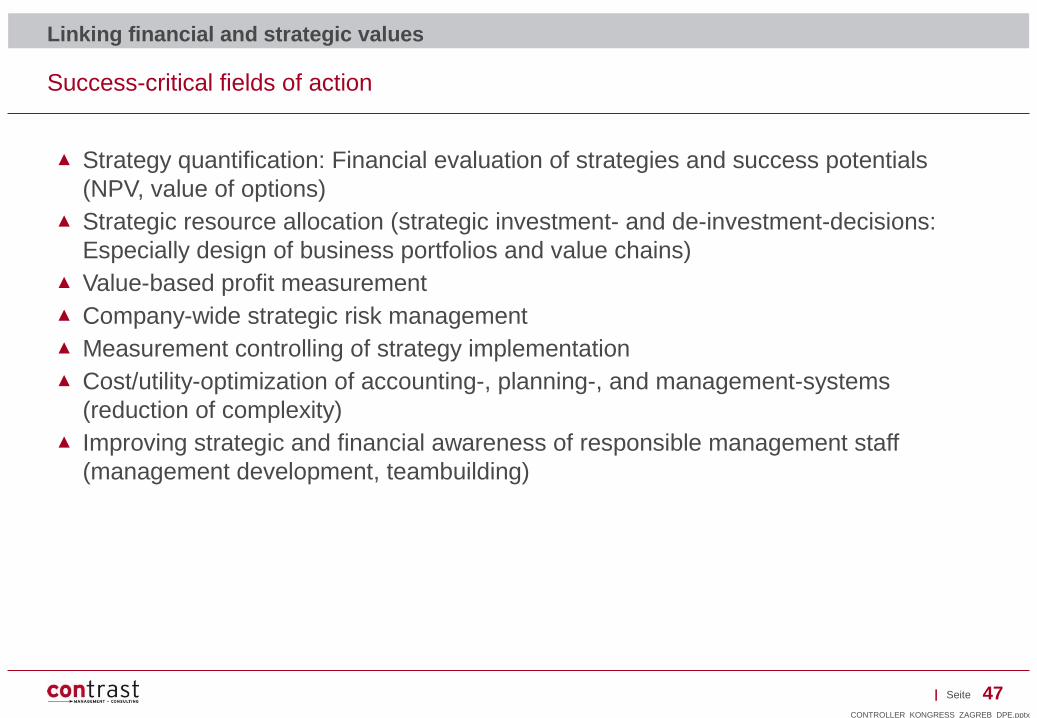

Success-critical fields of action

▲ Strategy quantification: Financial evaluation of strategies and success potentials (NPV, value of options)

▲ Strategic resource allocation (strategic investment- and de-investment-decisions: Especially design of business portfolios and value chains)

▲ Value-based profit measurement ▲ Company-wide strategic risk management▲ Measurement controlling of strategy implementation▲ Cost/utility-optimization of accounting-, planning-, and management-systems

(reduction of complexity)▲ Improving strategic and financial awareness of responsible management staff

(management development, teambuilding)

Linking financial and strategic values

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 48|

Studies about Controlling and CFO Roles1

Strategic Management in the Public Sector 6

Strategic Management 3

Strategy in the Time of Economic Crises4

The Role of Controlling 5

Role and Tools in the Future – Strategic Performance Management

2

Agenda

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

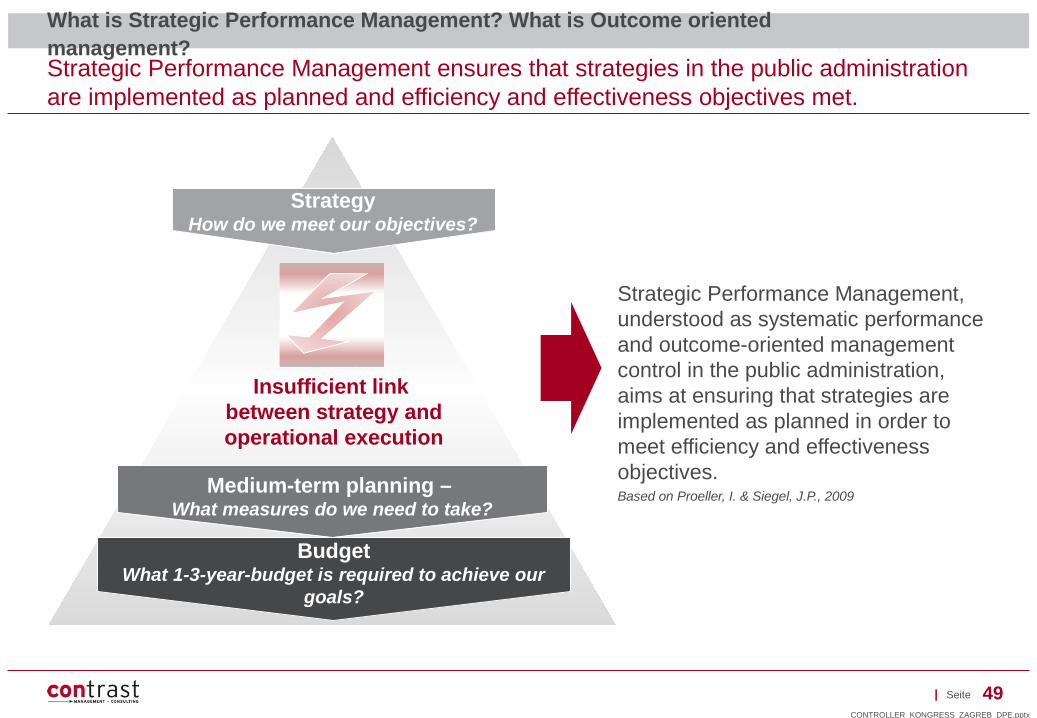

Seite 49|

Strategic Performance Management ensures that strategies in the public administration are implemented as planned and efficiency and effectiveness objectives met.

What is Strategic Performance Management? What is Outcome oriented management?

BudgetWhat 1-3-year-budget is required to achieve our

goals?

Medium-term planning – What measures do we need to take?

Insufficient link between strategy andoperational execution

StrategyHow do we meet our objectives?

Strategic Performance Management, understood as systematic performance and outcome-oriented management control in the public administration, aims at ensuring that strategies are implemented as planned in order to meet efficiency and effectiveness objectives.Based on Proeller, I. & Siegel, J.P., 2009

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 50|

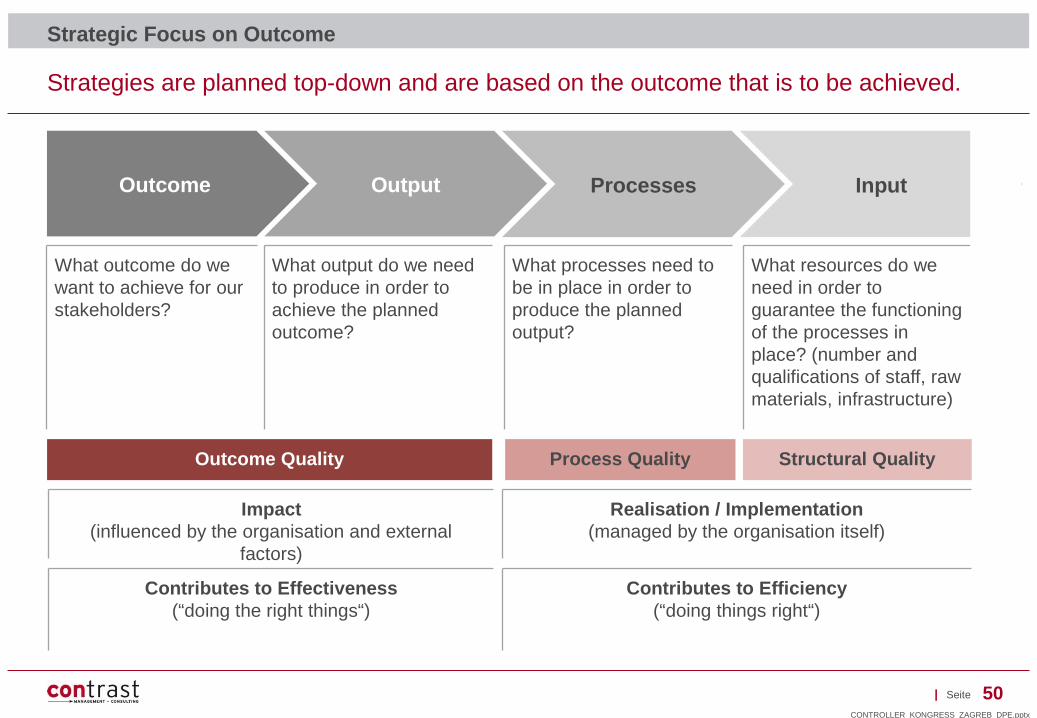

Strategies are planned top-down and are based on the outcome that is to be achieved.

Strategic Focus on Outcome

Outcome Output Processes Input

What outcome do we want to achieve for our stakeholders?

What processes need to be in place in order to produce the planned output?

What output do we need to produce in order to achieve the planned outcome?

What resources do we need in order to guarantee the functioning of the processes in place? (number and qualifications of staff, raw materials, infrastructure)

Outcome Quality Process Quality Structural Quality

Impact(influenced by the organisation and external

factors)

Realisation / Implementation(managed by the organisation itself)

Contributes to Effectiveness(“doing the right things“)

Contributes to Efficiency(“doing things right“)

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 51|

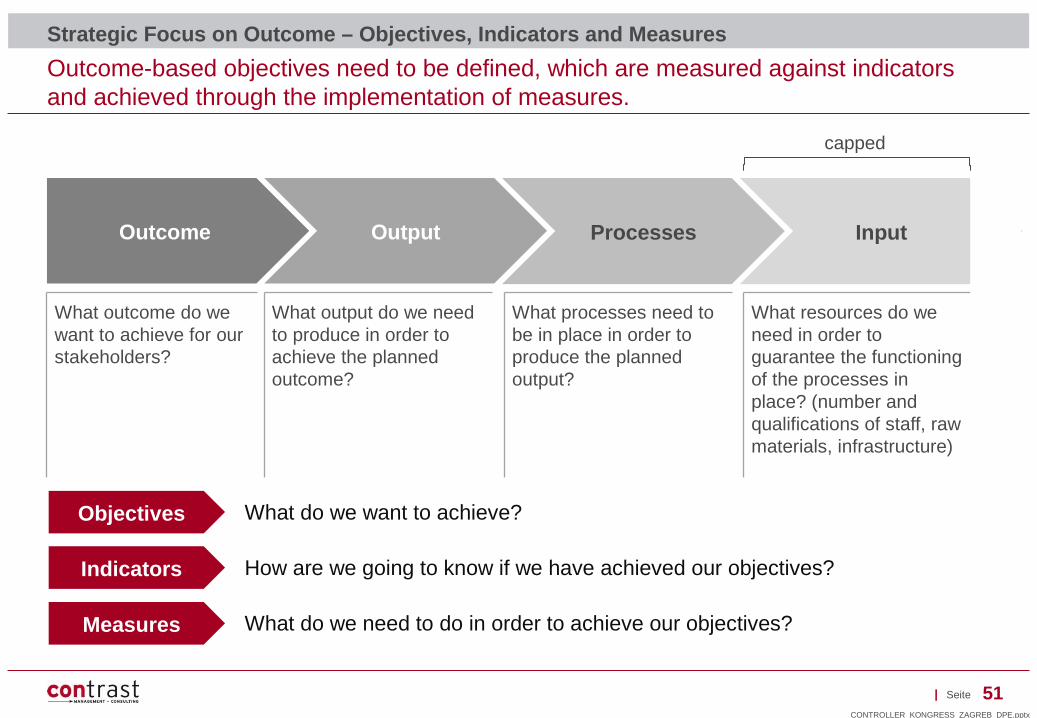

Outcome-based objectives need to be defined, which are measured against indicators and achieved through the implementation of measures.

Strategic Focus on Outcome – Objectives, Indicators and Measures

Outcome Output Processes Input

What outcome do we want to achieve for our stakeholders?

What processes need to be in place in order to produce the planned output?

What output do we need to produce in order to achieve the planned outcome?

What resources do we need in order to guarantee the functioning of the processes in place? (number and qualifications of staff, raw materials, infrastructure)

What do we want to achieve?

How are we going to know if we have achieved our objectives?

What do we need to do in order to achieve our objectives?

Objectives

Measures

Indicators

capped

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 52|

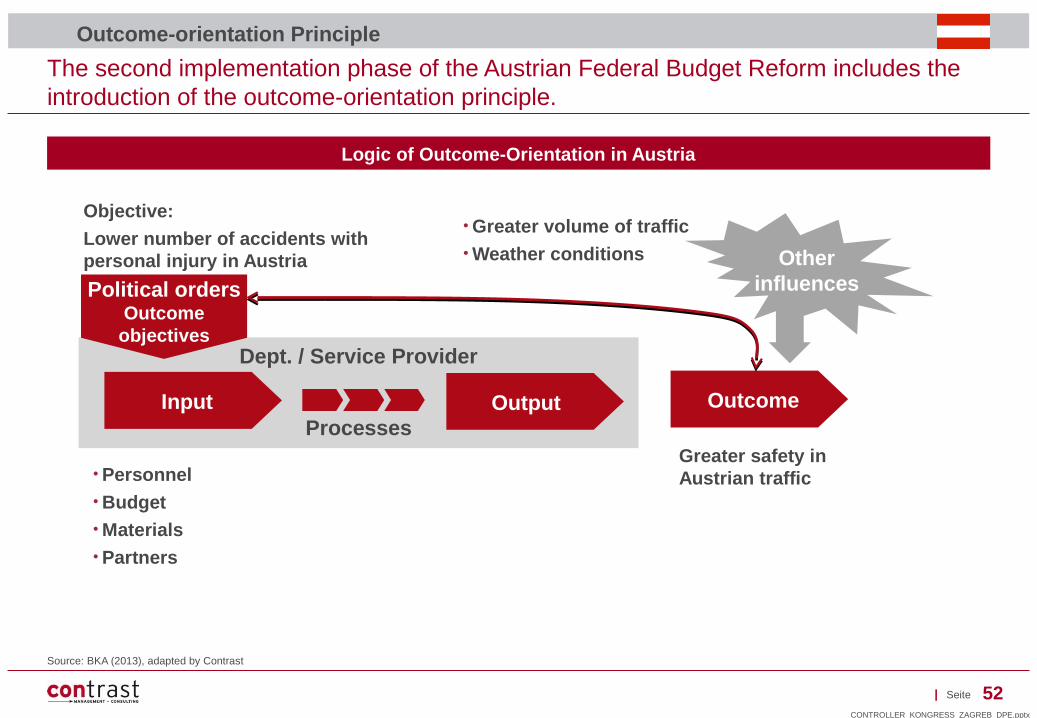

The second implementation phase of the Austrian Federal Budget Reform includes the introduction of the outcome-orientation principle.

Source: BKA (2013), adapted by Contrast

Outcome-orientation Principle

Dept. / Service Provider

Input Output Outcome

Political ordersOutcome

objectives

Processes

• Personnel• Budget• Materials• Partners

Greater safety in Austrian traffic

Objective:

Lower number of accidents with personal injury in Austria

• Greater volume of traffic• Weather conditions Other

influences

Logic of Outcome-Orientation in Austria

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 53|

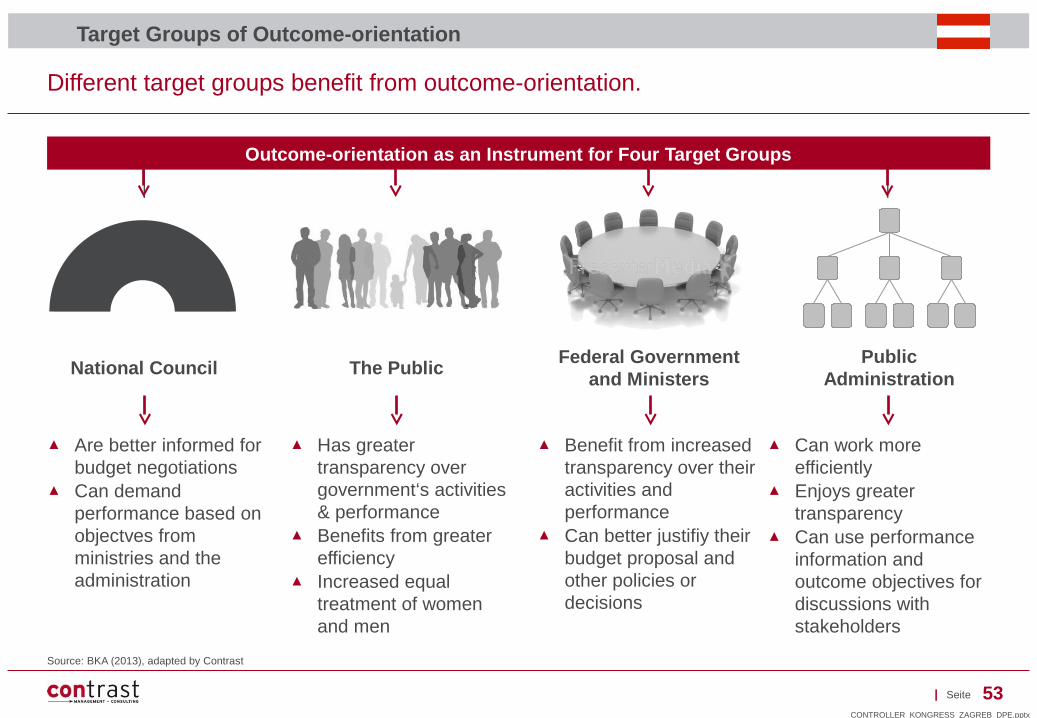

Different target groups benefit from outcome-orientation.

Source: BKA (2013), adapted by Contrast

Target Groups of Outcome-orientation

Outcome-orientation as an Instrument for Four Target Groups

National CouncilFederal Government

and MinistersPublic

AdministrationThe Public

▲ Are better informed for budget negotiations

▲ Can demand performance based on objectves from ministries and the administration

▲ Has greater transparency over government‘s activities & performance

▲ Benefits from greater efficiency

▲ Increased equal treatment of women and men

▲ Benefit from increased transparency over their activities and performance

▲ Can better justifiy their budget proposal and other policies or decisions

▲ Can work more efficiently

▲ Enjoys greater transparency

▲ Can use performance information and outcome objectives for discussions with stakeholders

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 54|

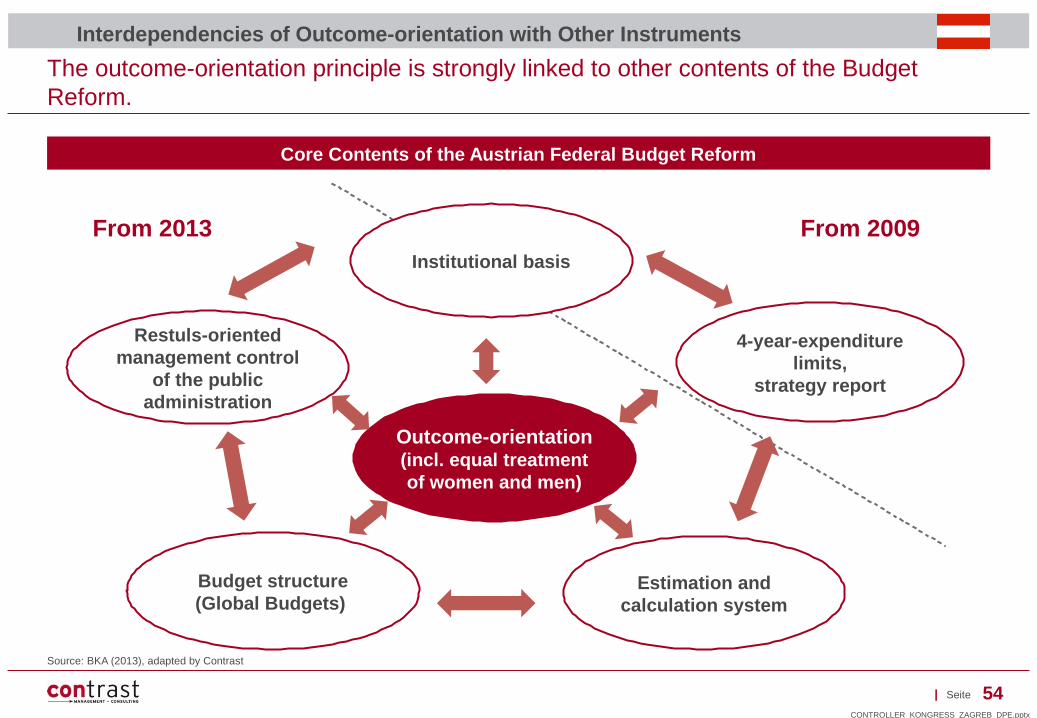

The outcome-orientation principle is strongly linked to other contents of the Budget Reform.

Source: BKA (2013), adapted by Contrast

Interdependencies of Outcome-orientation with Other Instruments

From 2009

Budget structure (Global Budgets)

Estimation and calculation system

Restuls-oriented management control

of the public administration

Outcome-orientation (incl. equal treatment of women and men)

4-year-expenditure limits,

strategy report

Institutional basis

From 2013

Core Contents of the Austrian Federal Budget Reform

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx

Seite 55|

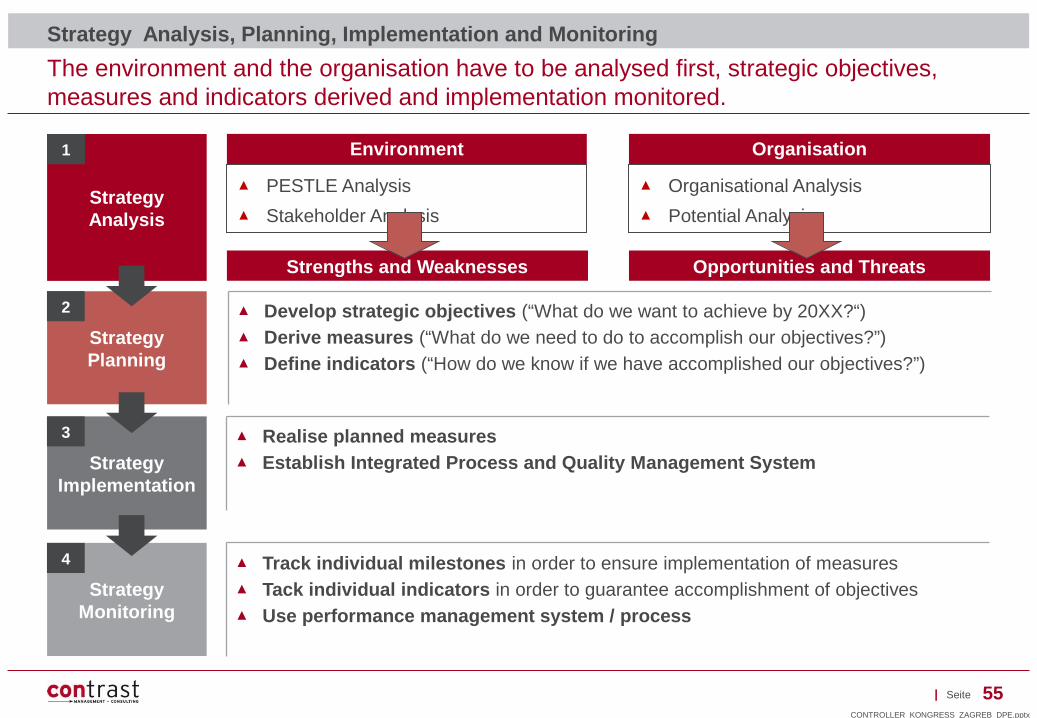

The environment and the organisation have to be analysed first, strategic objectives, measures and indicators derived and implementation monitored.

Strategy Analysis, Planning, Implementation and Monitoring

Strengths and Weaknesses Opportunities and Threats

Environment Organisation

▲ PESTLE Analysis

▲ Stakeholder Analysis

▲ Organisational Analysis

▲ Potential Analysis

▲ Develop strategic objectives (“What do we want to achieve by 20XX?“)▲ Derive measures (“What do we need to do to accomplish our objectives?”)▲ Define indicators (“How do we know if we have accomplished our objectives?”)

Strategy Analysis

Strategy Planning

Strategy Monitoring

▲ Track individual milestones in order to ensure implementation of measures▲ Tack individual indicators in order to guarantee accomplishment of objectives▲ Use performance management system / process

Strategy Implementation

▲ Realise planned measures▲ Establish Integrated Process and Quality Management System

1

2

3

4

CONTROLLER_KONGRESS_ZAGREB_DPE.pptx