Embed Size (px)

Citation preview

Salomon Smith Barney Financial Services Conference

Global Institutional & Investment Banking –

Strong & consistent earnings growth

Dr Bob EdgarAustralia and New Zealand Banking Group Limited

4th March 2003

2 Global Institutional & Investment Banking

Outline

• Our business today– Definition– Performance– Credit Quality

• Why we are successful

• Strategy

• Outlook

3 Global Institutional & Investment Banking

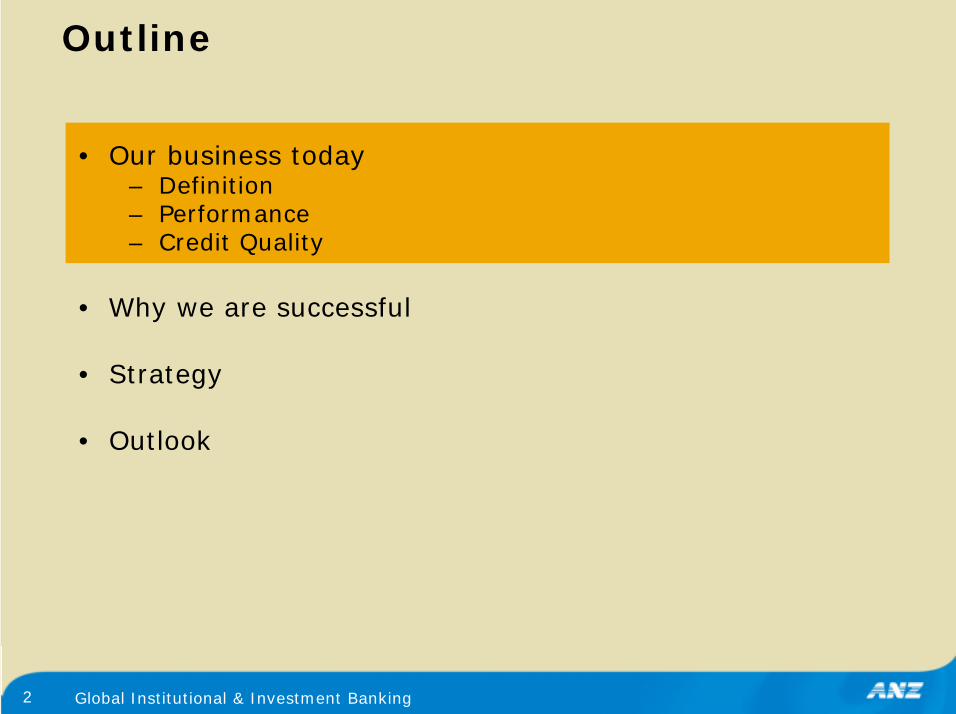

Corporate Units – business relationships overview

Corporate Cards

Merchant acquiring

Wealth

Corporate Superannuation & risk

Mortgages

Consumer Banking

Foreign Exchange

(GFX)

Capital Markets (GCM)

Transaction Services (GTS)

Structured Finance (GSF)

Corporate Finance & Advisory

(CF&A)

Corporate Product Businesses

Customer Segments Personal Products Businesses

Global Institutional

Banking (incl Asia, North

America, Europe)

Corporate Banking

Small Medium Business

Micro-Business

4 Global Institutional & Investment Banking

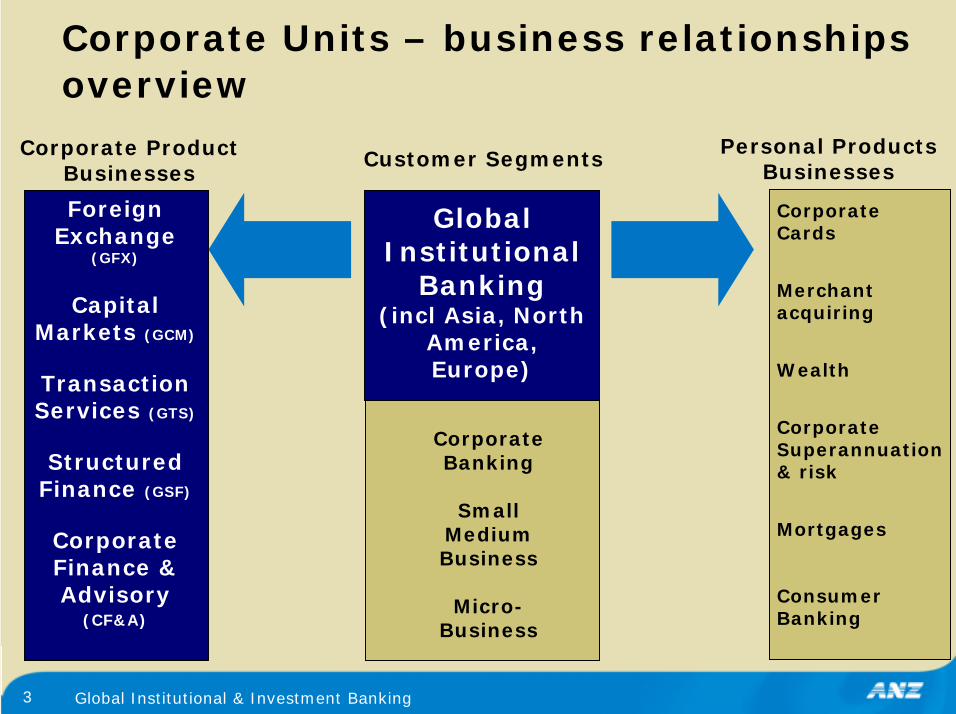

GI & IB – delivering consistent profit growth across the franchise

95 106 115 128

6670 74

762429

3133

4246

4143

3938

4143

3834

4138

0

50

100

150

200

250

300

350

400

Mar-01 Sep-01 Mar-02 Sep-02

Institutional GTS GCM GFX GSF CFA

304323

343361

6%6%

5%

$m13%

12%

One third

ofANZ’s2002 NPAT

5 Global Institutional & Investment Banking

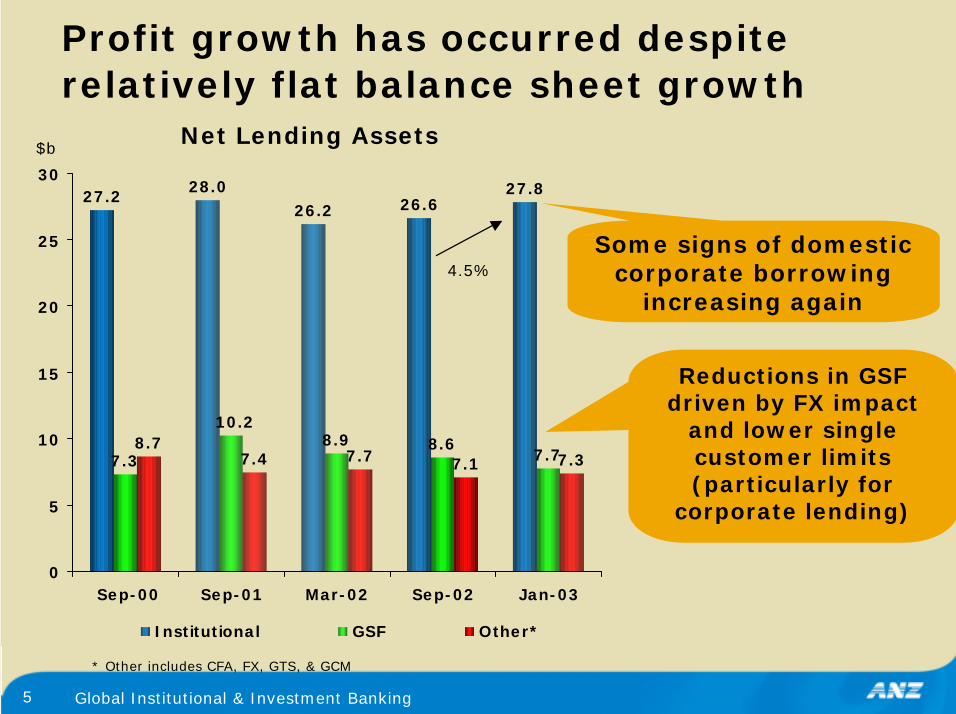

Profit growth has occurred despite relatively flat balance sheet growth

27.228.0

26.2 26.627.8

7.38.9 8.6

7.78.7

7.4 7.7 7.1 7.3

10.2

0

5

10

15

20

25

30

Sep-00 Sep-01 Mar-02 Sep-02 Jan-03

Institutional GSF Other*

Net Lending Assets$b

4.5%

* Other includes CFA, FX, GTS, & GCM

Some signs of domestic corporate borrowing

increasing again

Reductions in GSF driven by FX impact

and lower single customer limits (particularly for

corporate lending)

6 Global Institutional & Investment Banking

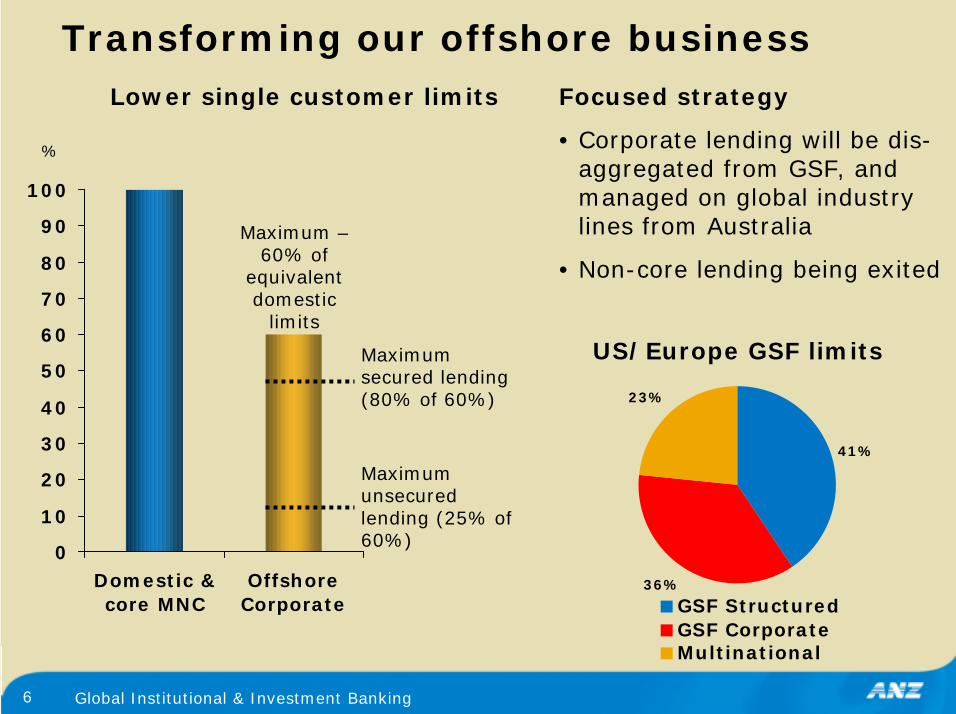

Transforming our offshore business

0

10

20

30

40

50

60

70

80

90

100

Domestic &core MNC

OffshoreCorporate

%

Lower single customer limits Focused strategy

• Corporate lending will be dis-aggregated from GSF, and managed on global industry lines from Australia

• Non-core lending being exited

41%

36%

23%

GSF StructuredGSF CorporateMultinational

Maximum unsecured lending (25% of 60%)

Maximum secured lending (80% of 60%)

Maximum –60% of

equivalent domestic

limits

US/Europe GSF limits

7 Global Institutional & Investment Banking

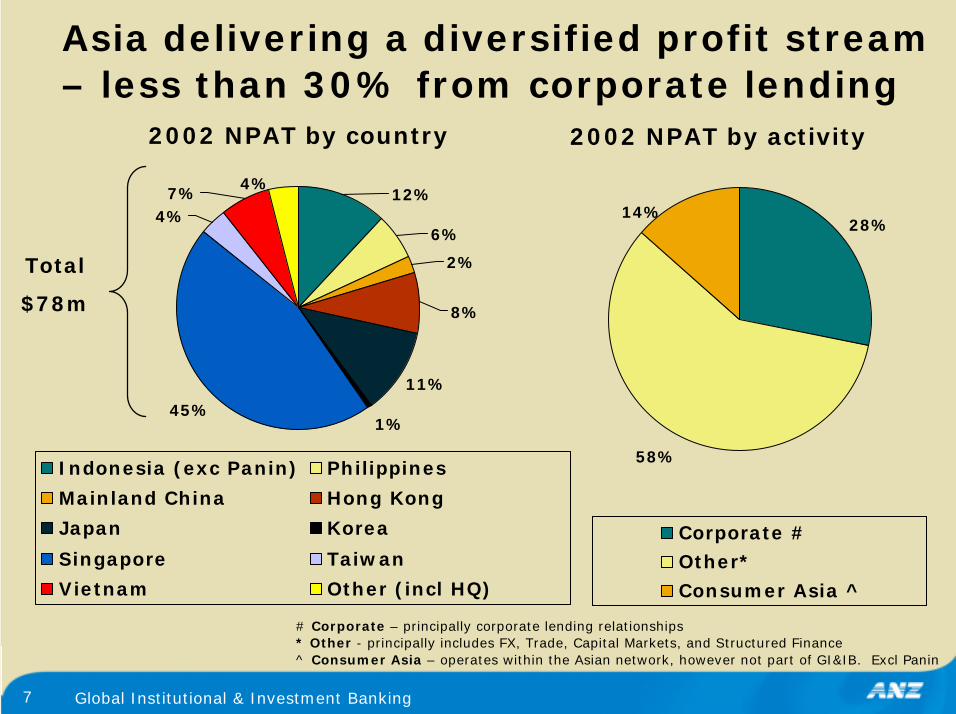

Asia delivering a diversified profit stream – less than 30% from corporate lending

# Corporate – principally corporate lending relationships* Other - principally includes FX, Trade, Capital Markets, and Structured Finance^ Consumer Asia – operates within the Asian network, however not part of GI&IB. Excl Panin

11%

1%

4%7%

4%

45%

12%

6%

2%

8%

Indonesia (exc Panin) Philippines

Mainland China Hong Kong

Japan Korea

Singapore Taiwan

Vietnam Other (incl HQ)

28%

58%

14%

Corporate #

Other*

Consumer Asia ^

2002 NPAT by country 2002 NPAT by activity

Total

$78m

8 Global Institutional & Investment Banking

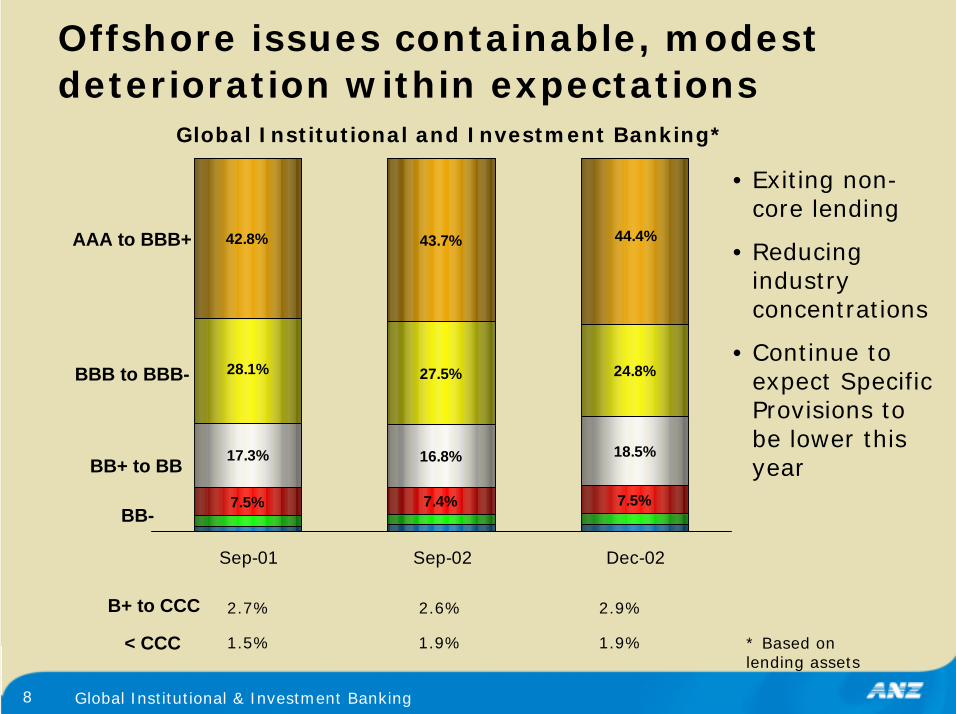

Offshore issues containable, modest deterioration within expectations

7.5% 7.4% 7.5%

17.3% 16.8% 18.5%

27.5% 24.8%

43.7%

28.1%

42.8% 44.4%

Sep-01 Sep-02 Dec-02

AAA to BBB+

BBB to BBB-

BB+ to BB

BB-

Global Institutional and Investment Banking*

B+ to CCC

< CCC

2.7% 2.6% 2.9%

1.5% 1.9% 1.9%

• Exiting non-core lending

• Reducing industry concentrations

• Continue to expect Specific Provisions to be lower this year

* Based on lending assets

9 Global Institutional & Investment Banking

Outline

• Our business today

• Why we are successful– A strong franchise– Sophisticated MIS– Our customer proposition

• Strategy

• Outlook

10 Global Institutional & Investment Banking

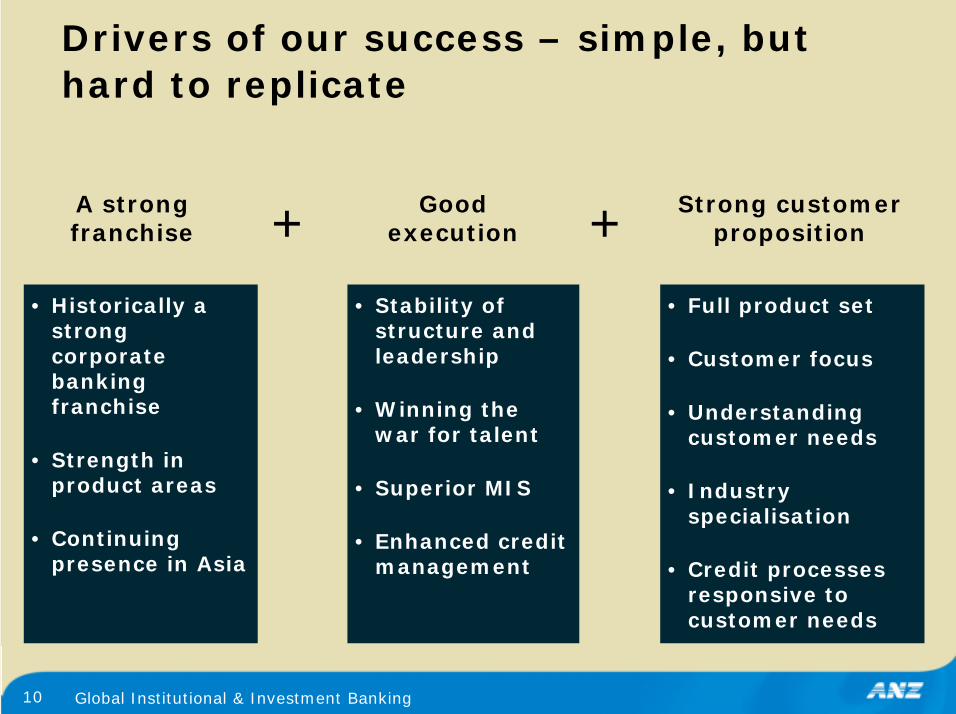

Drivers of our success – simple, but hard to replicate

• Historically a strong corporate banking franchise

• Strength in product areas

• Continuing presence in Asia

A strong franchise

• Stability of structure and leadership

• Winning the war for talent

• Superior MIS

• Enhanced credit management

Good execution+

• Full product set

• Customer focus

• Understanding customer needs

• Industry specialisation

• Credit processes responsive to customer needs

Strong customer proposition+

11 Global Institutional & Investment Banking

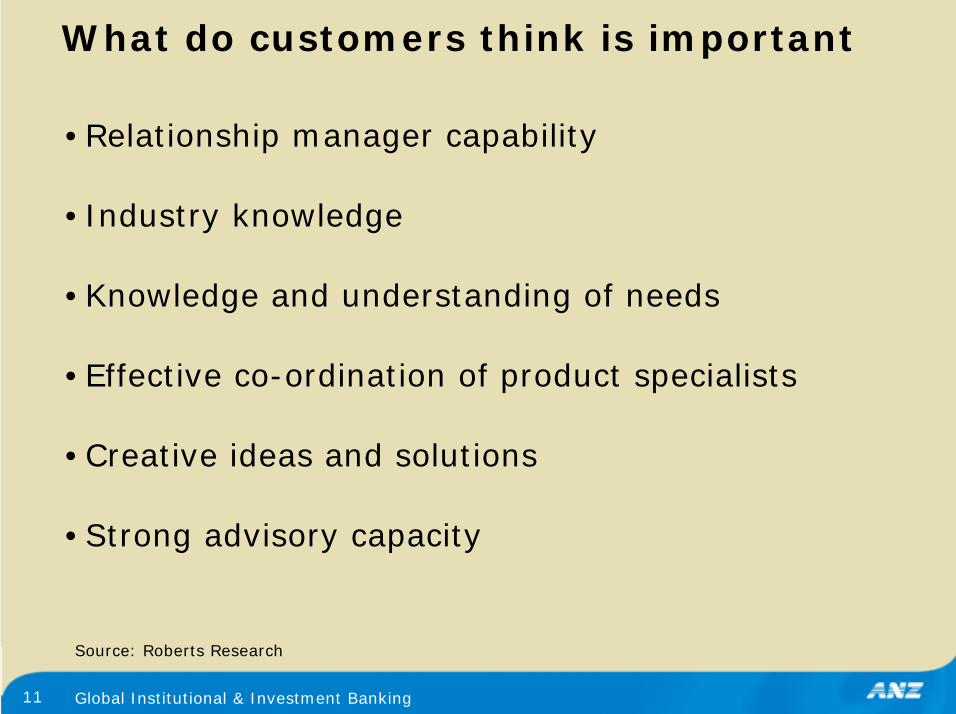

What do customers think is important

•Relationship manager capability

•Industry knowledge

•Knowledge and understanding of needs

•Effective co-ordination of product specialists

•Creative ideas and solutions

•Strong advisory capacity

Source: Roberts Research

12 Global Institutional & Investment Banking

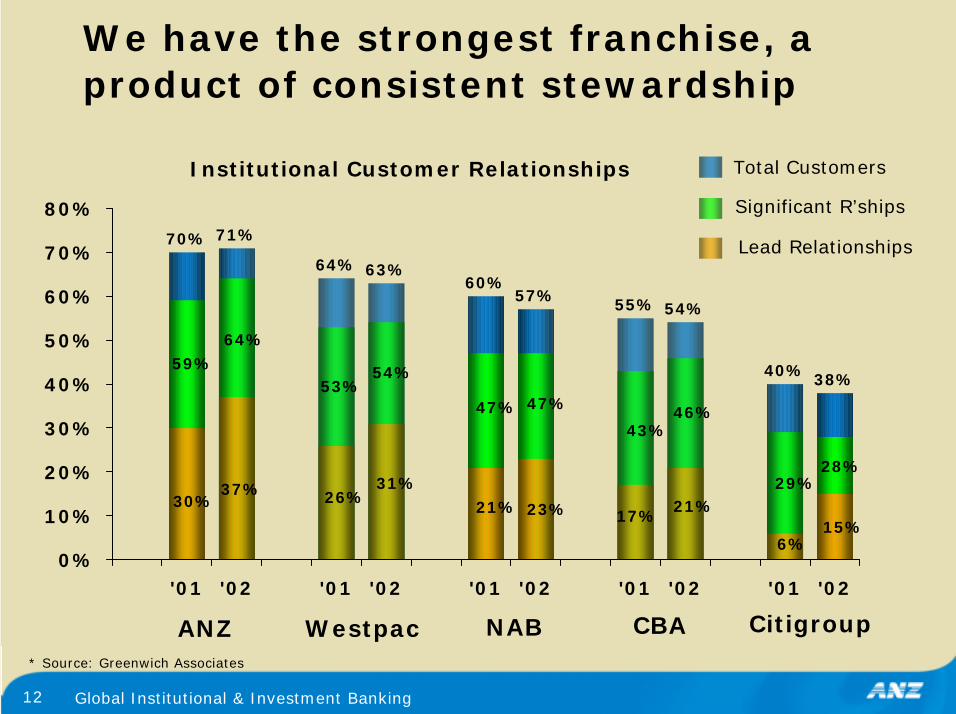

ANZ Westpac NAB CBA Citigroup* Source: Greenwich Associates

Total Customers

Significant R’ships

Lead Relationships

We have the strongest franchise, a product of consistent stewardship

70% 71%

64% 63%60%

57% 55% 54%

40% 38%

28%29%

46%43%

47%47%

54%53%

64%59%

15%6%

21%17%23%21%

31%26%37%

30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

'01 '02 '01 '02 '01 '02 '01 '02 '01 '02

Institutional Customer Relationships

13 Global Institutional & Investment Banking

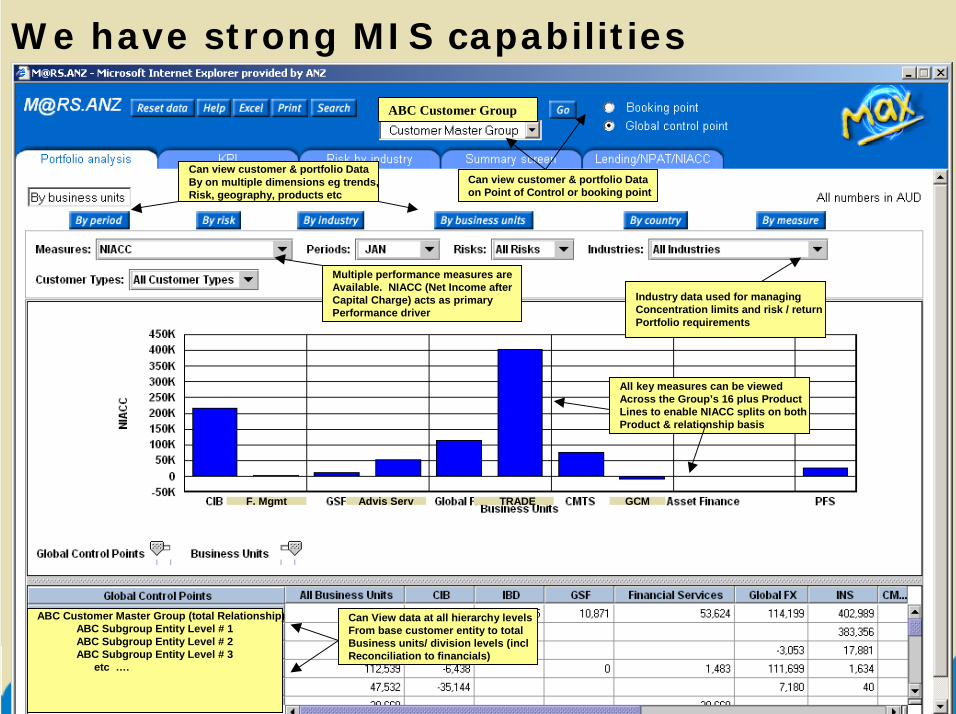

We have strong MIS capabilities

F. Mgmt Advis Serv TRADE GCM

Can view customer & portfolio Dataon Point of Control or booking point

Can view customer & portfolio DataBy on multiple dimensions eg trends,Risk, geography, products etc

Multiple performance measures areAvailable. NIACC (Net Income after Capital Charge) acts as primary Performance driver

Industry data used for managingConcentration limits and risk / returnPortfolio requirements

Can View data at all hierarchy levelsFrom base customer entity to totalBusiness units/ division levels (inclReconciliation to financials)

All key measures can be viewedAcross the Group’s 16 plus ProductLines to enable NIACC splits on bothProduct & relationship basis

ABC Customer Group

ABC Customer Master Group (total Relationship)ABC Subgroup Entity Level # 1 ABC Subgroup Entity Level # 2ABC Subgroup Entity Level # 3

etc ….

14 Global Institutional & Investment Banking

+19+10+10

+2+2-8

+35

+1

+ 64

+ 37

-40

-20

0

20

40

60

80

'01 '02 '01 '02 '01 '02 '01 '02 '01 '02ANZ Westpac NAB CBA Citigroup

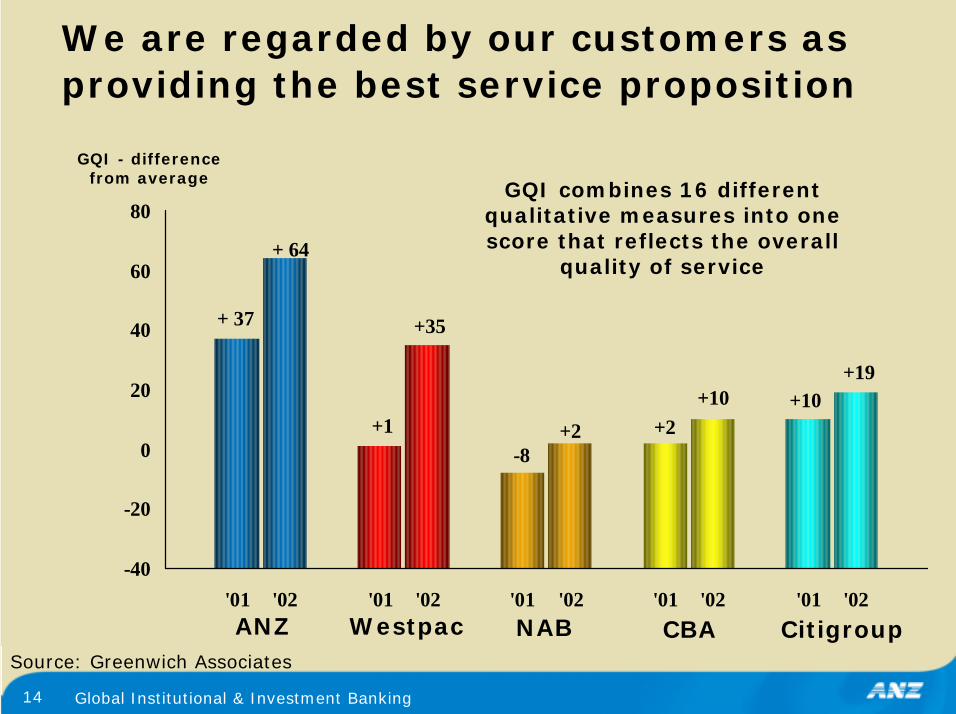

GQI - difference from average

GQI combines 16 different qualitative measures into one score that reflects the overall

quality of service

Source: Greenwich Associates

We are regarded by our customers as providing the best service proposition

15 Global Institutional & Investment Banking

Outline

• Our business today

• Why we are successful

• Strategy– Extending our business model

• Outlook

16 Global Institutional & Investment Banking

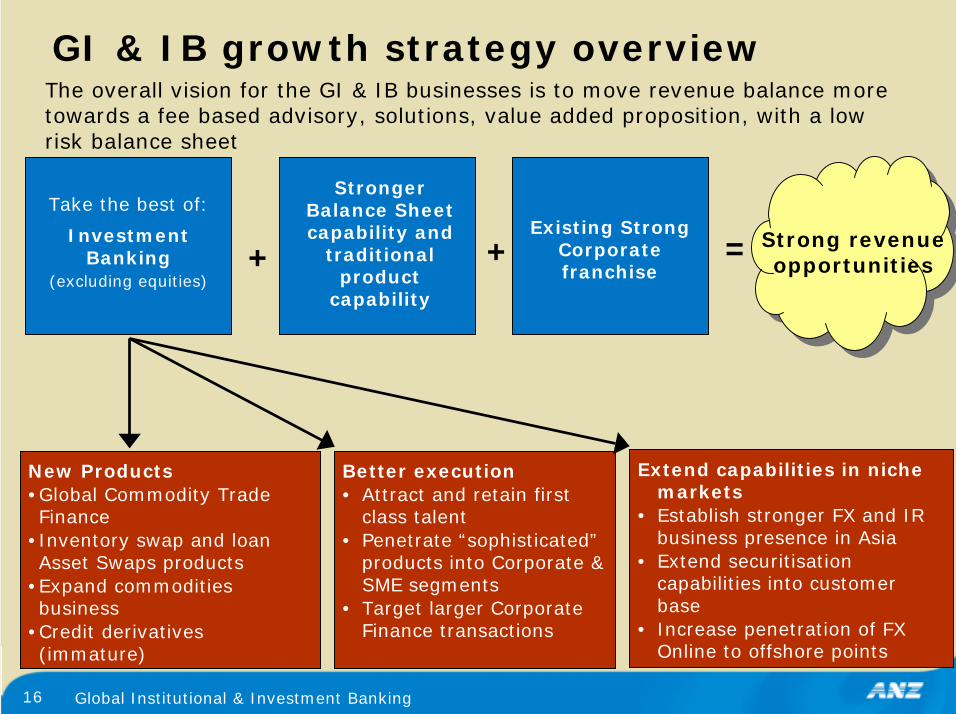

GI & IB growth strategy overviewThe overall vision for the GI & IB businesses is to move revenue balance more towards a fee based advisory, solutions, value added proposition, with a low risk balance sheet

Strong revenue opportunities

New Products•Global Commodity Trade Finance

•Inventory swap and loan Asset Swaps products

•Expand commodities business

•Credit derivatives (immature)

Take the best of:

Investment Banking

(excluding equities)

Stronger Balance Sheet capability and

traditional product

capability

Better execution• Attract and retain first

class talent• Penetrate “sophisticated”

products into Corporate & SME segments

• Target larger Corporate Finance transactions

Existing Strong Corporate franchise

Extend capabilities in niche markets

• Establish stronger FX and IR business presence in Asia

• Extend securitisation capabilities into customer base

• Increase penetration of FX Online to offshore points

+ + =

17 Global Institutional & Investment Banking

Summary

• We are performing well, and continue to target double digit earnings growth

• Credit quality in good shape, international energy/telco issues containable

• We have a very strong franchise in the corporate market

• Our customers confirm that we have the no. 1 service proposition

• We will extend our capabilities further into ANZ’s customer base and other niche markets, with some further rationalisation of offshore operations

GI & IB will continue to

deliver strong, stable earnings growth for ANZ

18 Global Institutional & Investment Banking

Supplementary information

19 Global Institutional & Investment Banking

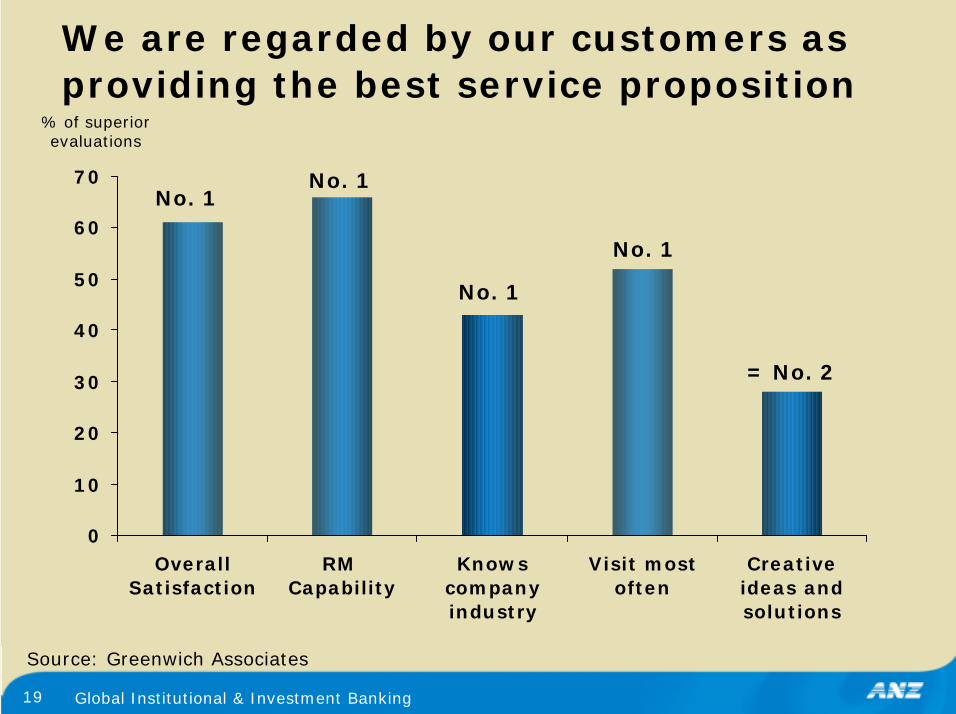

We are regarded by our customers as providing the best service proposition

0

10

20

30

40

50

60

70

OverallSatisfaction

RM Capability

Knowscompanyindustry

Visit mostoften

Creativeideas andsolutions

No. 1

= No. 2

No. 1

No. 1

No. 1

Source: Greenwich Associates

% of superior evaluations

20 Global Institutional & Investment Banking

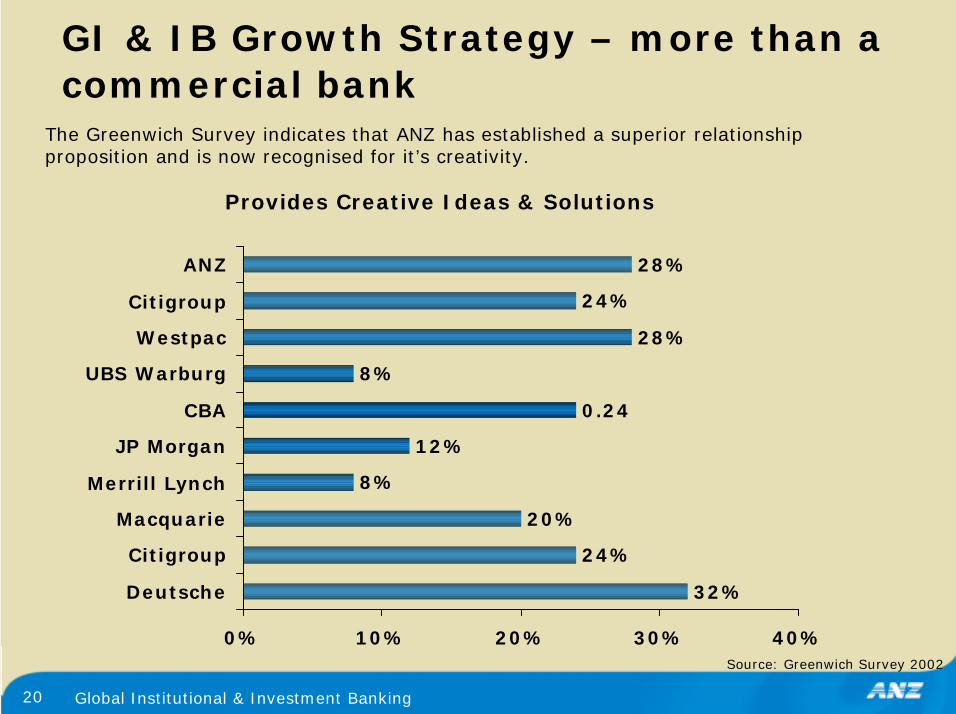

GI & IB Growth Strategy – more than a commercial bank

The Greenwich Survey indicates that ANZ has established a superior relationship proposition and is now recognised for it’s creativity.

32%

24%

20%

8%

12%

0.24

8%

28%

24%

28%

0% 10% 20% 30% 40%

Deutsche

Citigroup

Macquarie

Merrill Lynch

JP Morgan

CBA

UBS Warburg

Westpac

Citigroup

ANZ

Provides Creative Ideas & Solutions

Source: Greenwich Survey 2002

21 Global Institutional & Investment Banking

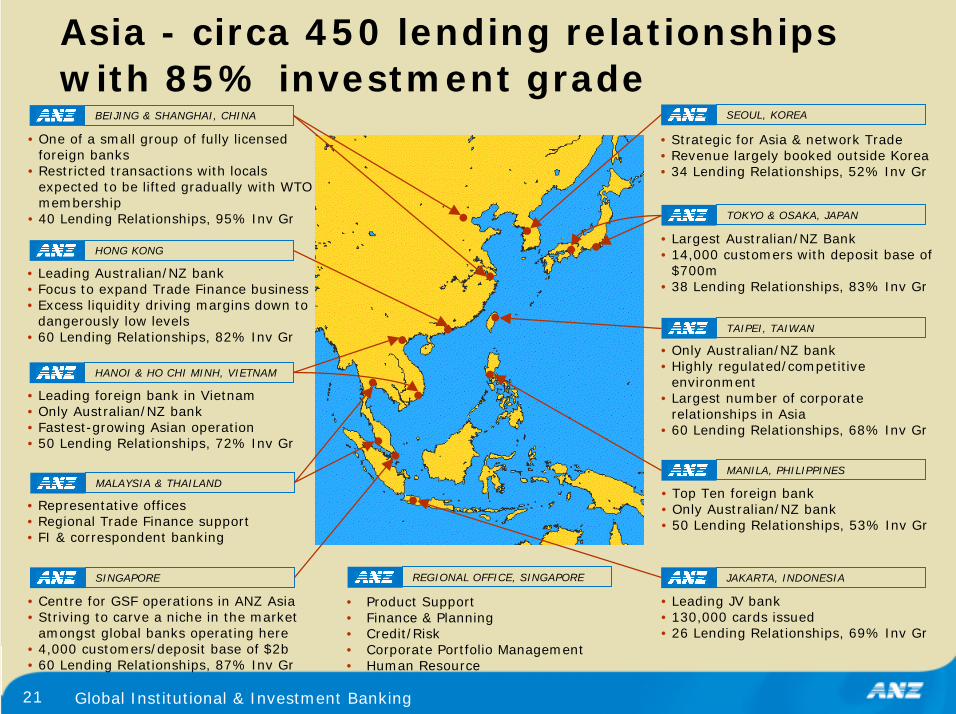

• Top Ten foreign bank• Only Australian/NZ bank• 50 Lending Relationships, 53% Inv Gr

• Only Australian/NZ bank• Highly regulated/competitive

environment• Largest number of corporate

relationships in Asia• 60 Lending Relationships, 68% Inv Gr

• Largest Australian/NZ Bank• 14,000 customers with deposit base of

$700m• 38 Lending Relationships, 83% Inv Gr

• Strategic for Asia & network Trade• Revenue largely booked outside Korea• 34 Lending Relationships, 52% Inv Gr

• Leading JV bank• 130,000 cards issued• 26 Lending Relationships, 69% Inv Gr

• One of a small group of fully licensed foreign banks

• Restricted transactions with locals expected to be lifted gradually with WTO membership

• 40 Lending Relationships, 95% Inv Gr

• Leading foreign bank in Vietnam• Only Australian/NZ bank• Fastest-growing Asian operation• 50 Lending Relationships, 72% Inv Gr

• Representative offices• Regional Trade Finance support• FI & correspondent banking

• Centre for GSF operations in ANZ Asia• Striving to carve a niche in the market

amongst global banks operating here• 4,000 customers/deposit base of $2b• 60 Lending Relationships, 87% Inv Gr

• Leading Australian/NZ bank• Focus to expand Trade Finance business• Excess liquidity driving margins down to

dangerously low levels• 60 Lending Relationships, 82% Inv Gr

• Product Support• Finance & Planning• Credit/Risk• Corporate Portfolio Management• Human Resource

Asia - circa 450 lending relationships with 85% investment grade

BEIJING & SHANGHAI, CHINA

HONG KONG

HANOI & HO CHI MINH, VIETNAM

SEOUL, KOREA

TOKYO & OSAKA, JAPAN

TAIPEI, TAIWAN

MANILA, PHILIPPINESMALAYSIA & THAILAND

REGIONAL OFFICE, SINGAPORESINGAPORE JAKARTA, INDONESIA

22 Global Institutional & Investment Banking

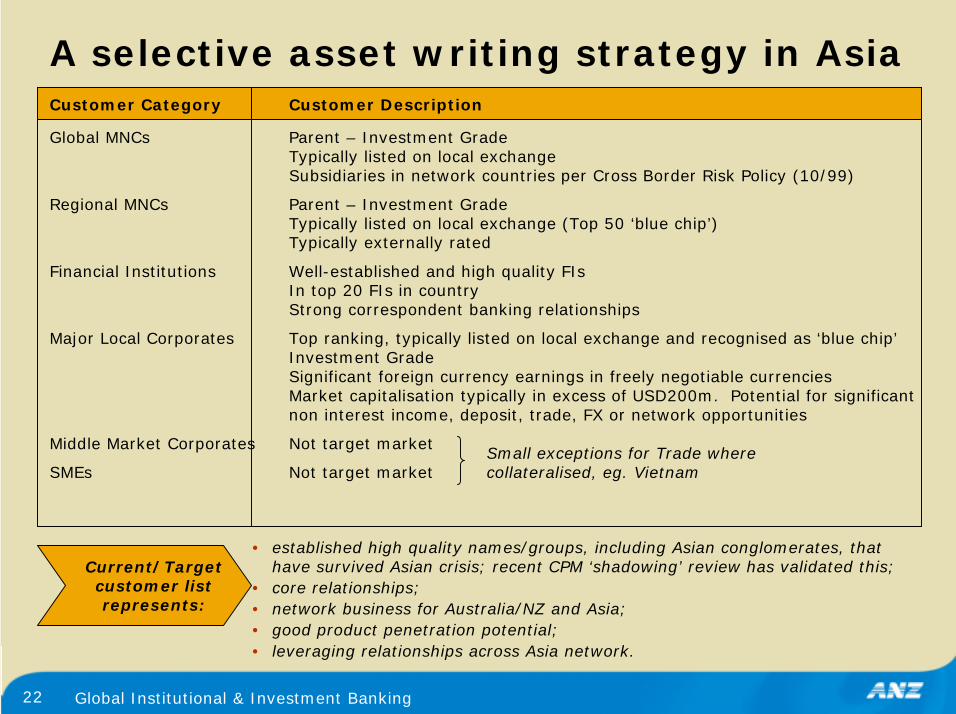

A selective asset writing strategy in AsiaCustomer Category Customer Description

Global MNCs Parent – Investment GradeTypically listed on local exchangeSubsidiaries in network countries per Cross Border Risk Policy (10/99)

Regional MNCs Parent – Investment GradeTypically listed on local exchange (Top 50 ‘blue chip’)Typically externally rated

Financial Institutions Well-established and high quality FIsIn top 20 FIs in countryStrong correspondent banking relationships

Major Local Corporates Top ranking, typically listed on local exchange and recognised as ‘blue chip’Investment Grade Significant foreign currency earnings in freely negotiable currenciesMarket capitalisation typically in excess of USD200m. Potential for significant non interest income, deposit, trade, FX or network opportunities

Middle Market Corporates Not target market

SMEs Not target market

• established high quality names/groups, including Asian conglomerates, that have survived Asian crisis; recent CPM ‘shadowing’ review has validated this;

• core relationships;• network business for Australia/NZ and Asia;• good product penetration potential;• leveraging relationships across Asia network.

Current/Target customer list represents:

Small exceptions for Trade where collateralised, eg. Vietnam

23 Global Institutional & Investment Banking

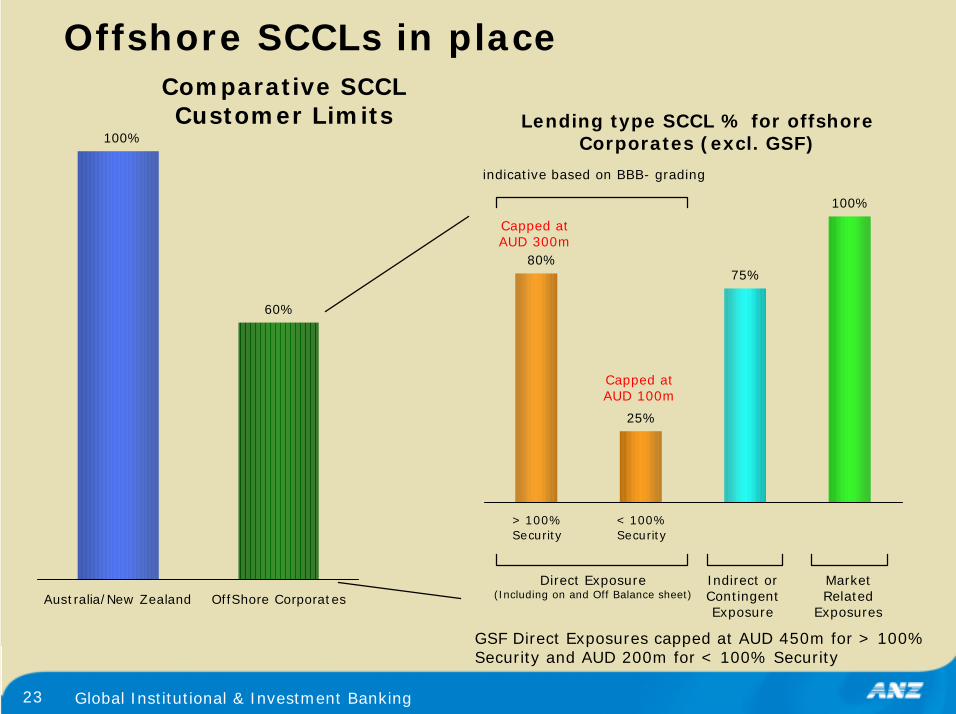

Offshore SCCLs in place

60%

100%

Australia/New Zealand OffShore Corporates

Comparative SCCL Customer Limits

25%

75%

100%

80%

> 100%Security

< 100%Security

Lending type SCCL % for offshoreCorporates (excl. GSF)

indicative based on BBB- grading

Direct Exposure(Including on and Off Balance sheet)

Indirect or Contingent Exposure

Market Related

Exposures

Capped at AUD 300m

Capped at AUD 100m

GSF Direct Exposures capped at AUD 450m for > 100% Security and AUD 200m for < 100% Security

24 Global Institutional & Investment Banking

The material in this presentation is general background information about the Bank’s activities current at the date of the presentation. It is information given in summary

form and does not purport to be complete. It is not intended to be relied upon as advice to investors or potential investors and does not take into account the

investment objectives, financial situation or needs of any particular investor. These should be considered, with or without professional advice when deciding if an

investment is appropriate.

For further information visit

www.anz.comor contact

Philip GentryHead of Investor Relations

ph: (613) 9273 4185 fax: (613) 9273 4091

mob: (61) 411 125 474 e-mail: [email protected]