Embed Size (px)

Citation preview

SUR 826 Financial Management in Construction

UK Construction Healthcare Sector Market

Analysis by

Sandeep Naik Vaigankar

Contents

The UK Market Sector Overview Market sector drivers Procurement practice and pipeline SWOT Analysis of UK Healthcare Construction Stakeholders’ Strategic Pathways Conclusions and Recommendations

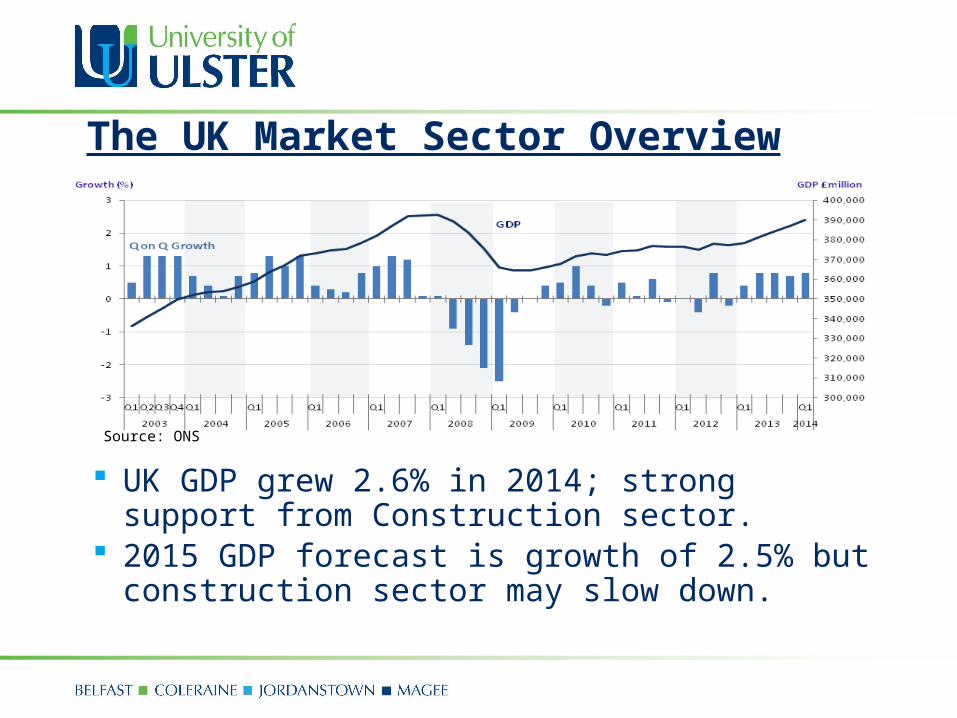

The UK Market Sector Overview

UK GDP grew 2.6% in 2014; strong support from Construction sector.

2015 GDP forecast is growth of 2.5% but construction sector may slow down.

Source: ONS

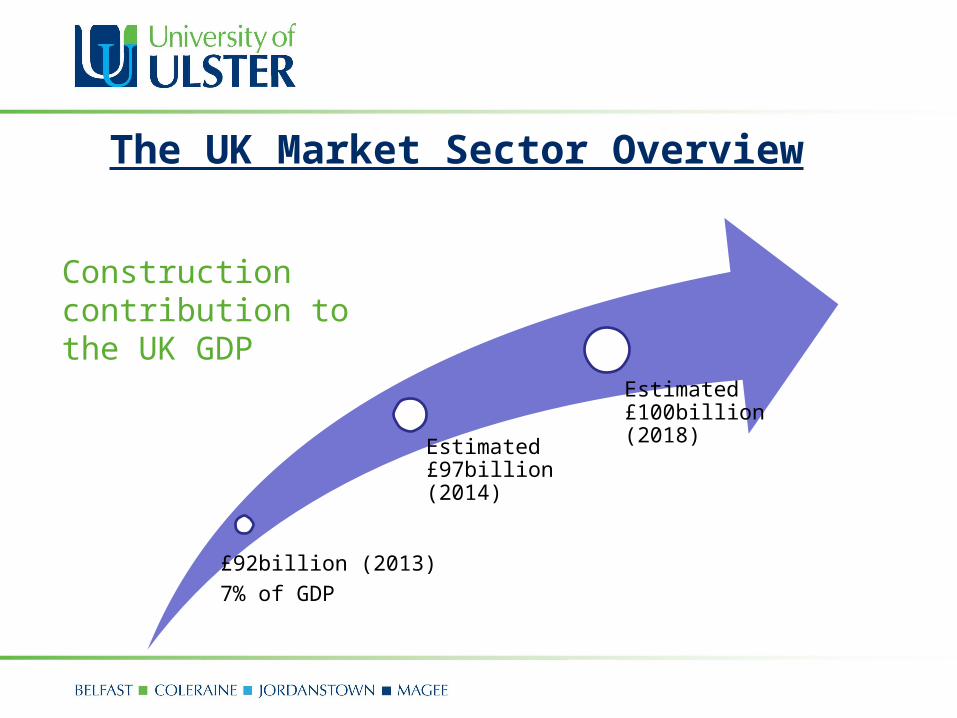

£92billion (2013)

7% of GDP

Estimated £97billion (2014)

Estimated £100billion (2018)

Construction contribution to the UK GDP

The UK Market Sector Overview

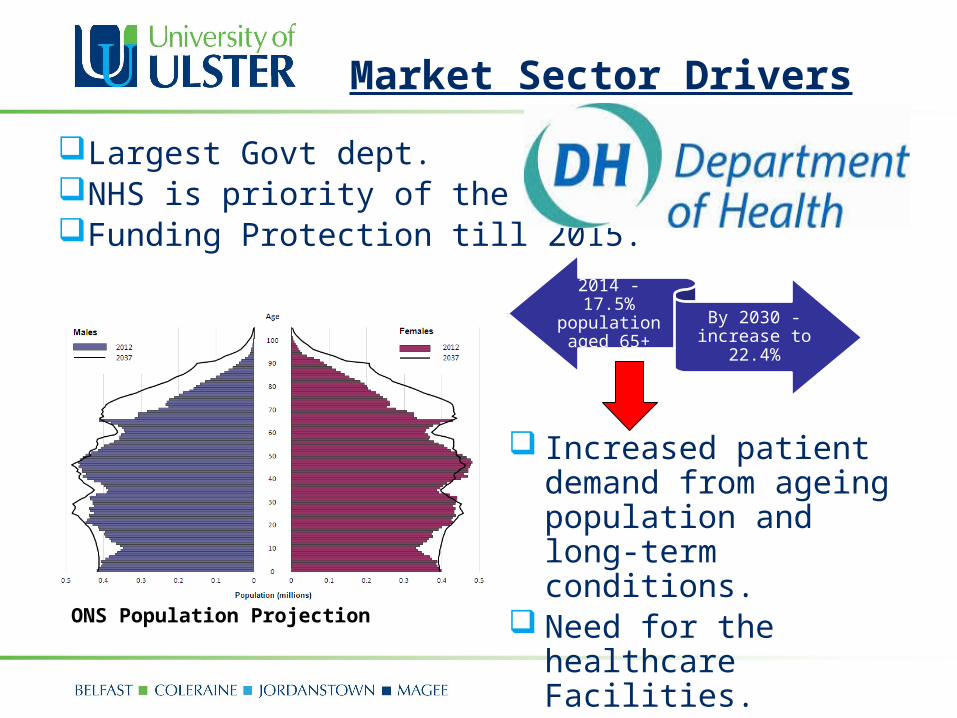

Largest Govt dept.NHS is priority of the Govt.Funding Protection till 2015.

ONS Population Projection

2014 - 17.5% population aged 65+ By 2030 -

increase to 22.4%

Increased patient demand from ageing population and long-term conditions.

Need for the healthcare Facilities.

Market Sector Drivers

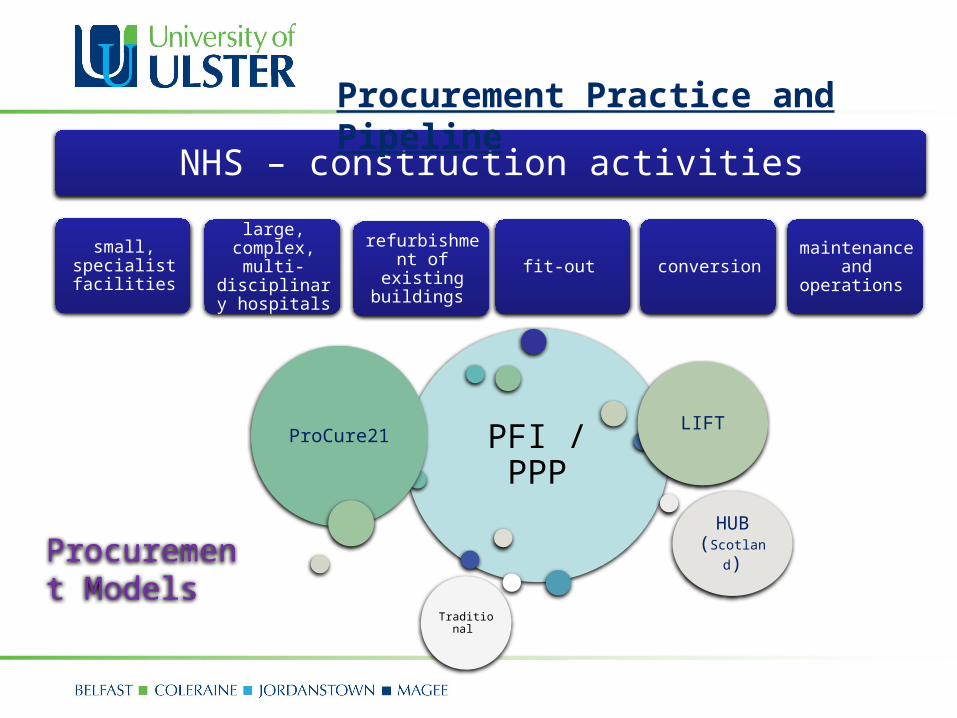

NHS – construction activities

small, specialist facilities

large, complex, multi-

disciplinary hospitals

refurbishment of existing buildings

fit-out conversion maintenance and operations

PFI / PPPProCure21

LIFT

HUB (Scotland)

Traditional

Procurement Models

Procurement Practice and Pipeline

Procurement Practice and Pipeline

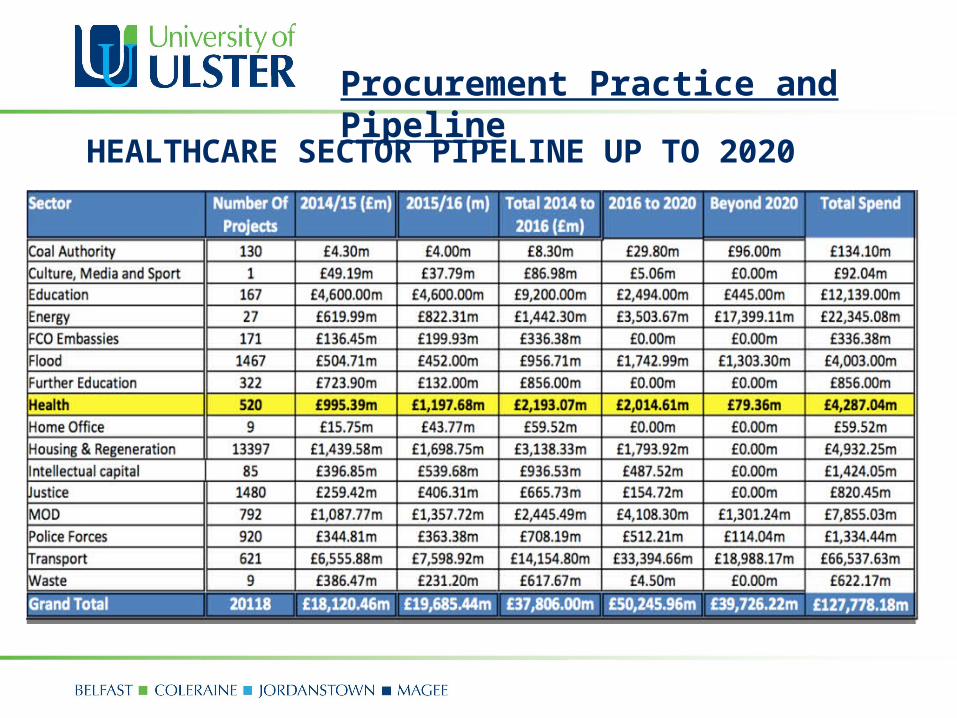

HEALTHCARE SECTOR PIPELINE UP TO 2020

Procurement Practice and Pipeline

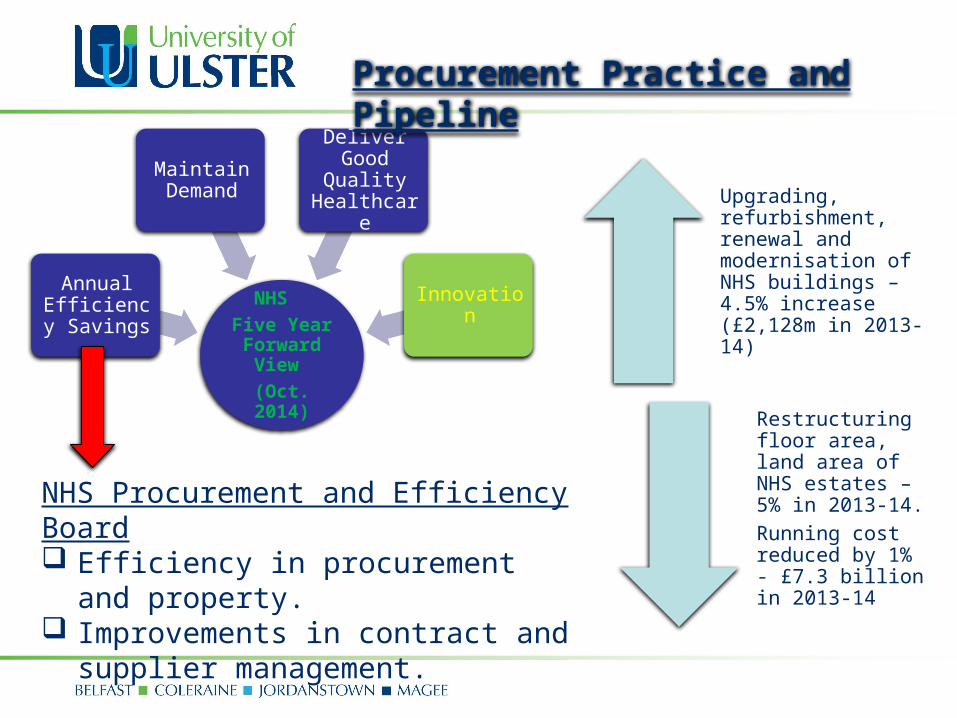

NHS

Five Year Forward

View

(Oct. 2014)

Annual Efficiency Savings

Maintain Demand

Deliver Good

Quality Healthcare

Innovation

NHS Procurement and Efficiency Board Efficiency in procurement and

property. Improvements in contract and

supplier management.

Upgrading, refurbishment, renewal and modernisation of NHS buildings – 4.5% increase (£2,128m in 2013-14)

Restructuring floor area, land area of NHS estates – 5% in 2013-14.

Running cost reduced by 1% - £7.3 billion in 2013-14

Procurement Practice and Pipeline

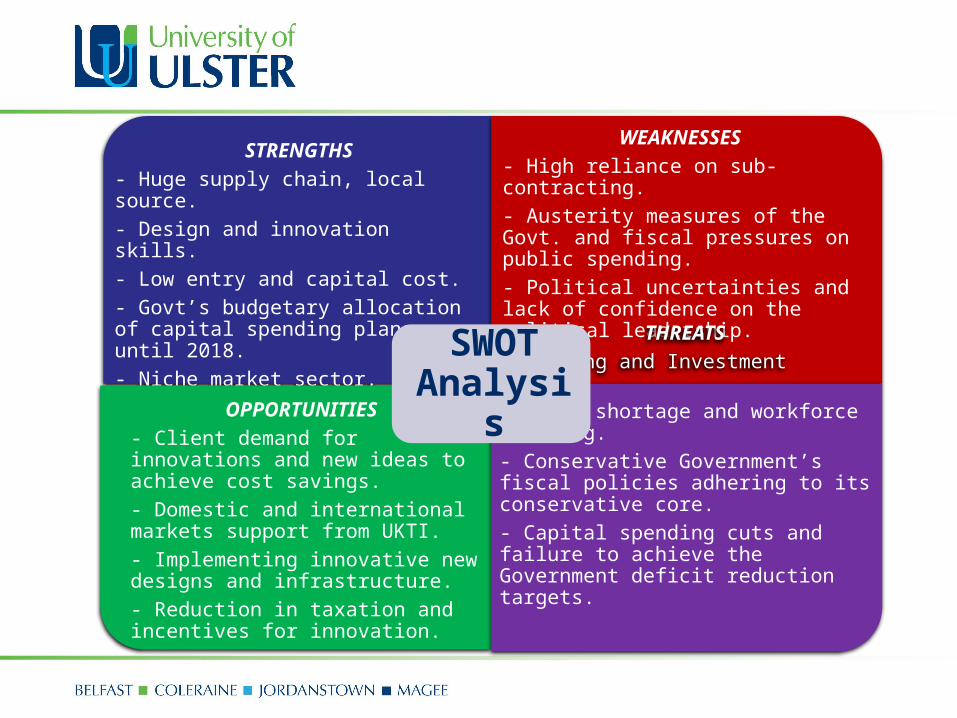

STRENGTHS

- Huge supply chain, local source.

- Design and innovation skills.

- Low entry and capital cost.

- Govt’s budgetary allocation of capital spending plans until 2018.

- Niche market sector.

WEAKNESSES

- High reliance on sub-contracting.

- Austerity measures of the Govt. and fiscal pressures on public spending.

- Political uncertainties and lack of confidence on the political leadership.

OPPORTUNITIES

- Client demand for innovations and new ideas to achieve cost savings.

- Domestic and international markets support from UKTI.

- Implementing innovative new designs and infrastructure.

- Reduction in taxation and incentives for innovation.

THREATS

- Funding and Investment inflow.

- Skill shortage and workforce training.

- Conservative Government’s fiscal policies adhering to its conservative core.

- Capital spending cuts and failure to achieve the Government deficit reduction targets.

SWOT Analysis

Stakeholders’ Strategic Pathway PFI funding model, a preferred route by NHS. Health and Social Care Bill reduced the number of health

bodies and abolished Primary Care Trusts and Strategic Health Authorities.

Need for the designs that help healthcare clients to cut costs by reducing staff numbers and shorten the processes of the health care service delivery.

Construction healthcare CEOs think most of their future growth will come from mature markets, and 22% are also looking to China (PwC, 2015).

There is a growing concern of the risk of over-regulation, indebted government’s ability to handle huge fiscal deficits and the availability of key skills

Stakeholders’ Strategic Pathway

The lower productivity output would stretch the austerity beyond the targeted years and deficit would continue to grow putting pressure on public finances enforcing further spending cuts.

The Healthcare UK is actively involved in sourcing the international business opportunities in healthcare with 82 leads of £10.8bn in 2013-14 exceeded the targeted £1.5bn; and has set up the annual target of £1.5bn business wins internationally up to 2020.

Construction healthcare sector is very competitive. The healthcare sector is demanding the efficiency and

affected by the spending cuts. The public demand on the health service delivery is ever

increasing, that will create demand for the infrastructure. The companies with unique selling point and competitive

advantage would create business opportunities in this sector.

Significant cost savings can be made by applying the economies of scale and reviewing the estates of the NHS in the areas of facilities management and operations by efficiently programming the servicing.

Conclusions and Recommendations

The UK has a large stock of ageing hospital facilities, which provides opportunities for the maintenance and refurbishment of medical buildings.

There is a huge potential in this segment with limited competition for the companies to provide retrofit and regeneration services to update the existing healthcare facilities and equip them for new clinical services.

The construction companies wanting to enter this market sector should create the long term competitive advantage by either reducing the costs or offering something unique by reconfiguring the value chain management.

Conclusions and Recommendations

The public sector client’s tender selection is based on value for money approach and not on the lowest tender; hence can not compete only on the lower cost.

The companies involved in this sectors are vastly experienced, has access to expertise and are huge, backed by the financial and technological capabilities, difficult to compete against.

Innovation is one of the key issues in creating and sustaining the competitive advantage.

organisations with innovative design and technological ideas to improve efficiency in service delivery would be successful in securing long-term business.

Conclusions and Recommendations

The entry and sustaining the business in the healthcare construction sector is very challenging:

1. PFI model would need strong financial reserves with the company to support the contracts.

2. Framework procurement routes requires strength in the tender bids supported by the skills, expertise and experience.

3. Competitors in this sector are big companies with strong financial, experience and expertise such as Belfour Beatty, Kier etc.

4. Innovation is the key competitive edge but difficult to realise in short term to gain entry, requires through research and development with technological support.

Conclusions and Recommendations