Embed Size (px)

Citation preview

TPCC

Taiwan Prosperity Chemical Corporation

2Q/2013

Investors’ Conference

September 3, 2013

TPCC 2

Disclaimer

The forward-looking statements contained in this presentation are

subject to risks and uncertainties and actual results may differ

materially from those expressed or implied in these forward-looking

statements.

Taiwan Prosperity Chemical Corporation makes no representation or

warranty as to the accuracy or completeness of these forward-looking

statements and nor does Taiwan Prosperity Chemical Corporation

undertake any obligation to update any forward-looking statements,

whether as a result of new information or future events.

TPCC

Agenda

• Company Snapshot

• 2Q/2013 Financial Results

• Business Overview

• Capital Expenditure

• 2H/2013 Business Outlook

3

TPCC 4

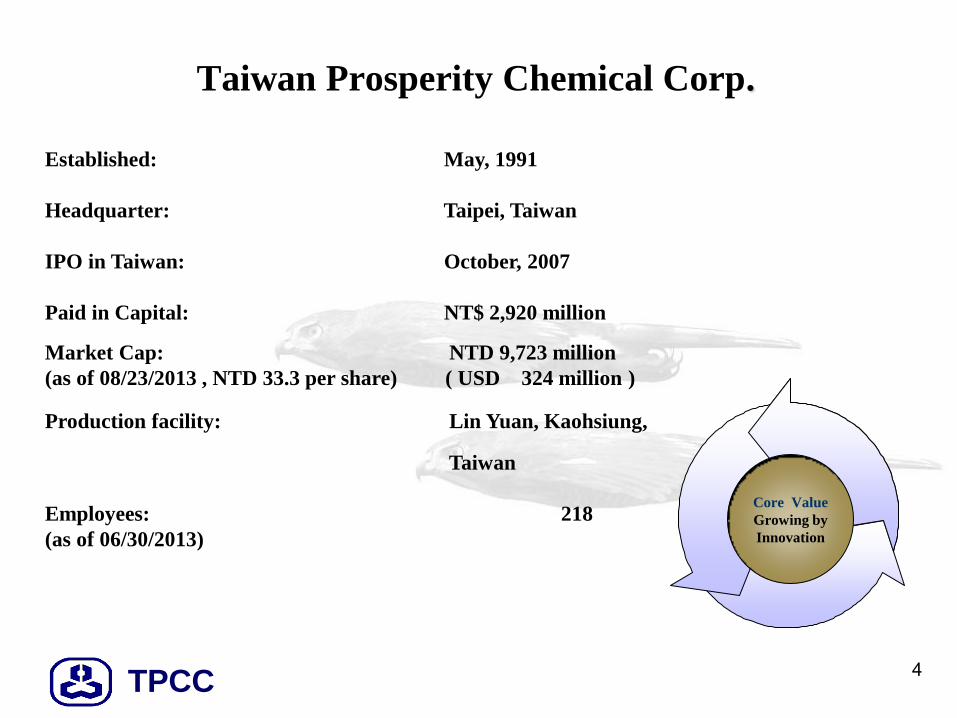

Taiwan Prosperity Chemical Corp.

Core Value

Growing by

Innovation

Established: May, 1991

Headquarter: Taipei, Taiwan

IPO in Taiwan: October, 2007

Paid in Capital: NT$ 2,920 million

Market Cap: NTD 9,723 million

(as of 08/23/2013 , NTD 33.3 per share) ( USD 324 million )

Production facility: Lin Yuan, Kaohsiung,

Taiwan

Employees: 218

(as of 06/30/2013)

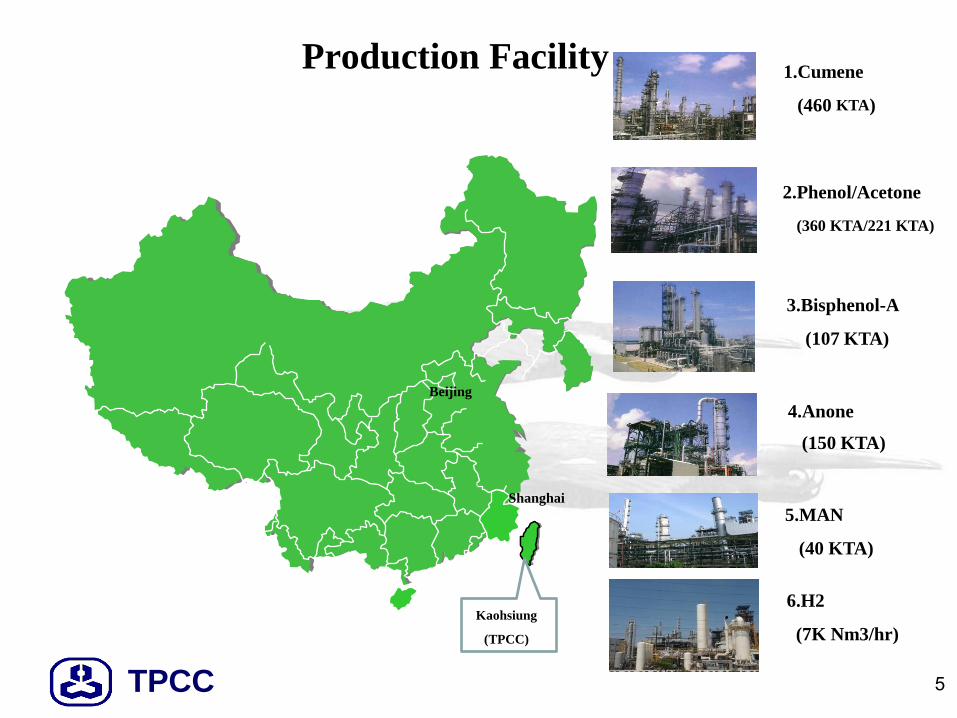

TPCC 5

Production Facility

Kaohsiung

(TPCC)

Beijing

Shanghai

1.Cumene

(460 KTA)

2.Phenol/Acetone

(360 KTA/221 KTA)

3.Bisphenol-A

(107 KTA)

4.Anone

(150 KTA)

5.MAN

(40 KTA)

6.H2

(7K Nm3/hr)

TPCC

Agenda

6

• Company Snapshot

• 2Q/2013 Financial Results

• Business Overview

• Capital Expenditure

• 2H/2013 Business Outlook

TPCC 7

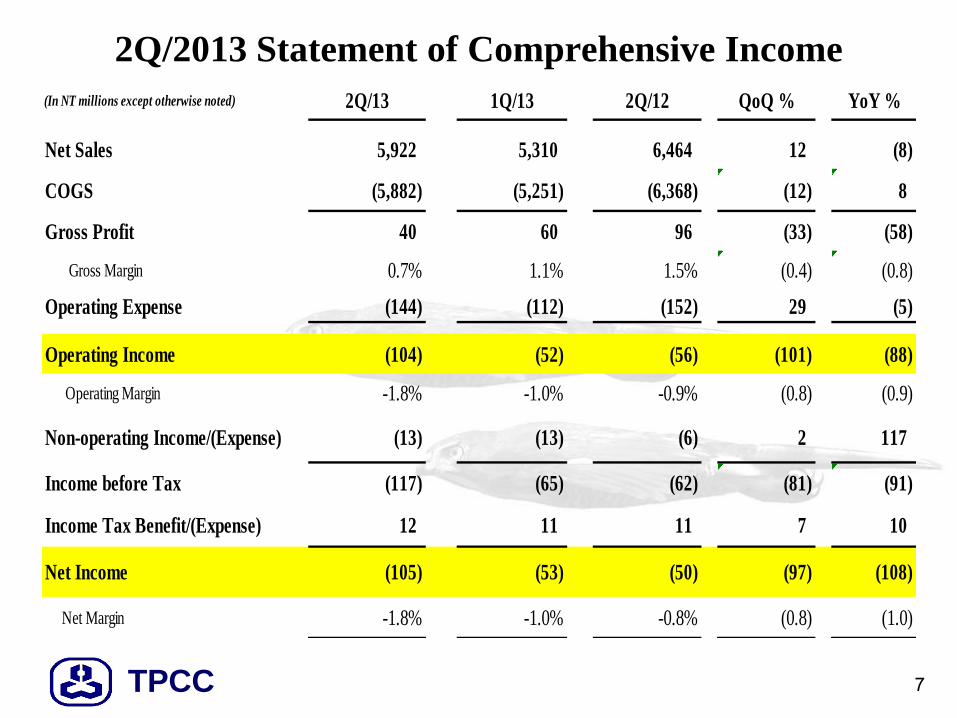

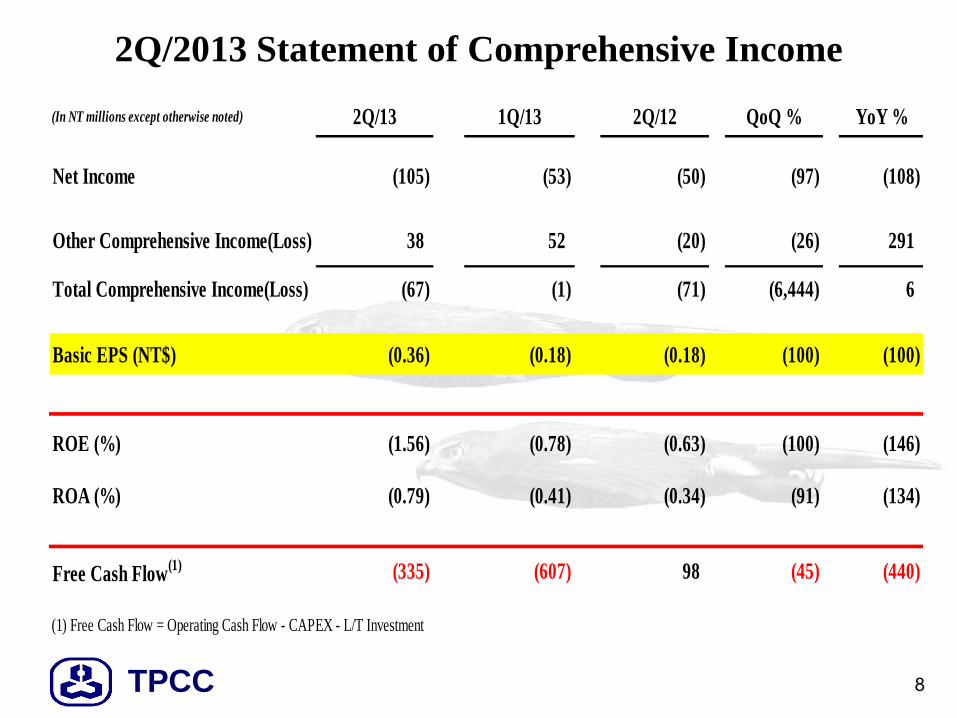

2Q/2013 Statement of Comprehensive Income

(In NT millions except otherwise noted) 2Q/13 1Q/13 2Q/12 QoQ % YoY %

Net Sales 5,922 5,310 6,464 12 (8)

COGS (5,882) (5,251) (6,368) (12) 8

Gross Profit 40 60 96 (33) (58)

Gross Margin 0.7% 1.1% 1.5% (0.4) (0.8)

Operating Expense (144) (112) (152) 29 (5)

Operating Income (104) (52) (56) (101) (88)

Operating Margin -1.8% -1.0% -0.9% (0.8) (0.9)

Non-operating Income/(Expense) (13) (13) (6) 2 117

Income before Tax (117) (65) (62) (81) (91)

Income Tax Benefit/(Expense) 12 11 11 7 10

Net Income (105) (53) (50) (97) (108)

Net Margin -1.8% -1.0% -0.8% (0.8) (1.0)

TPCC 8

2Q/2013 Statement of Comprehensive Income

(In NT millions except otherwise noted) 2Q/13 1Q/13 2Q/12 QoQ % YoY %

Net Income (105) (53) (50) (97) (108)

Other Comprehensive Income(Loss) 38 52 (20) (26) 291

Total Comprehensive Income(Loss) (67) (1) (71) (6,444) 6

Basic EPS (NT$) (0.36) (0.18) (0.18) (100) (100)

ROE (%) (1.56) (0.78) (0.63) (100) (146)

ROA (%) (0.79) (0.41) (0.34) (91) (134)

Free Cash Flow(1) (335) (607) 98 (45) (440)

(1) Free Cash Flow = Operating Cash Flow - CAPEX - L/T Investment

TPCC 9

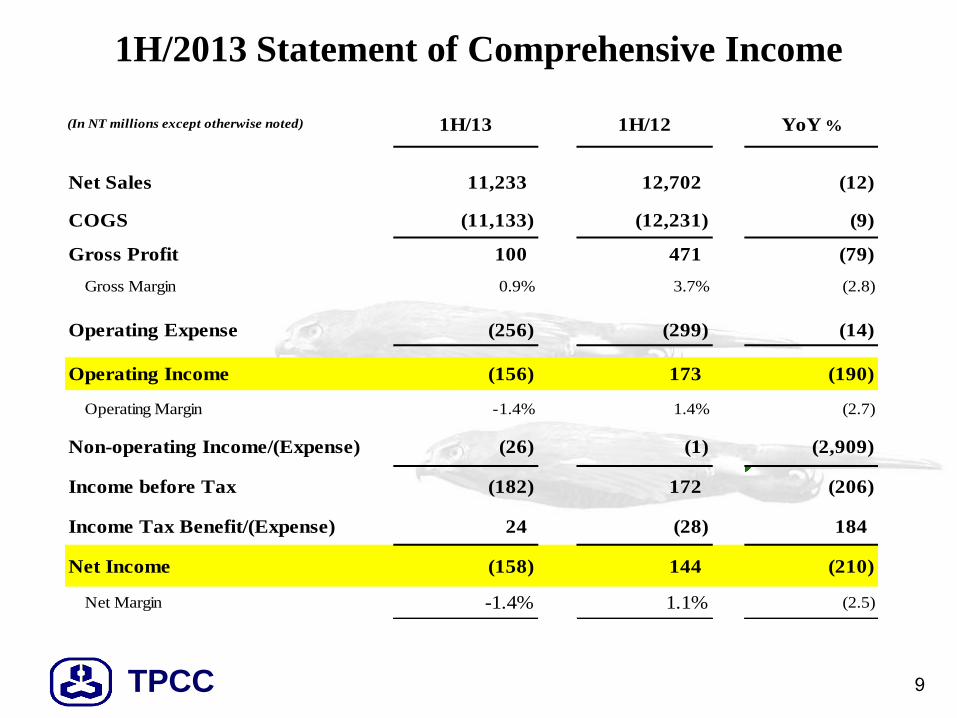

1H/2013 Statement of Comprehensive Income

(In NT millions except otherwise noted) 1H/13 1H/12 YoY %

Net Sales 11,233 12,702 (12)

COGS (11,133) (12,231) (9)

Gross Profit 100 471 (79)

Gross Margin 0.9% 3.7% (2.8)

Operating Expense (256) (299) (14)

Operating Income (156) 173 (190)

Operating Margin -1.4% 1.4% (2.7)

Non-operating Income/(Expense) (26) (1) (2,909)

Income before Tax (182) 172 (206)

Income Tax Benefit/(Expense) 24 (28) 184

Net Income (158) 144 (210)

Net Margin -1.4% 1.1% (2.5)

TPCC 10

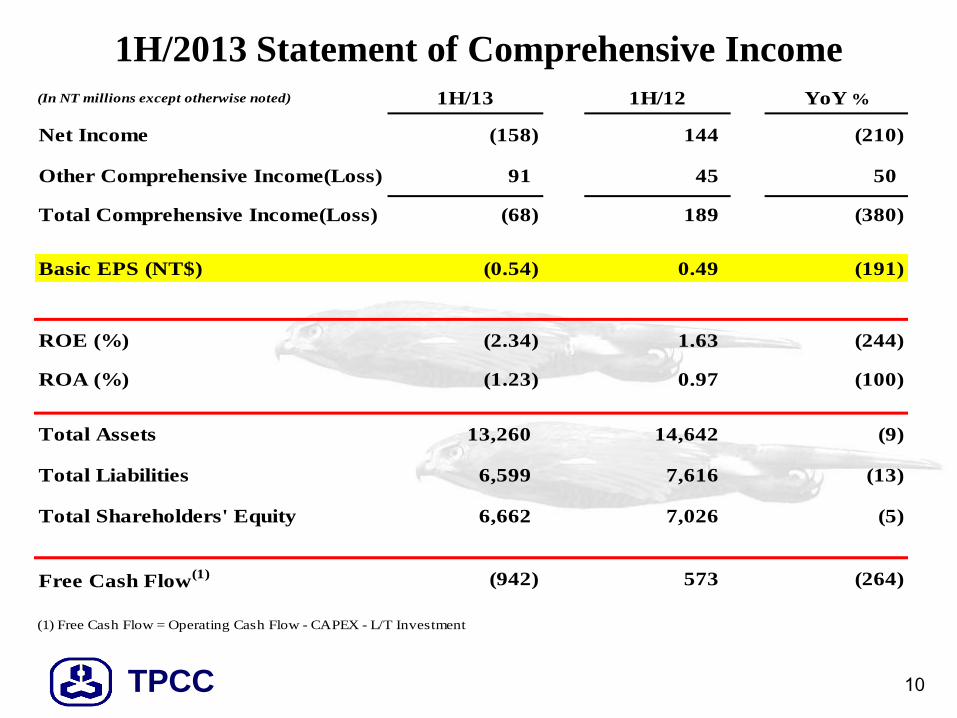

1H/2013 Statement of Comprehensive Income (In NT millions except otherwise noted) 1H/13 1H/12 YoY %

Net Income (158) 144 (210)

Other Comprehensive Income(Loss) 91 45 50

Total Comprehensive Income(Loss) (68) 189 (380)

Basic EPS (NT$) (0.54) 0.49 (191)

ROE (%) (2.34) 1.63 (244)

ROA (%) (1.23) 0.97 (100)

Total Assets 13,260 14,642 (9)

Total Liabilities 6,599 7,616 (13)

Total Shareholders' Equity 6,662 7,026 (5)

Free Cash Flow(1) (942) 573 (264)

(1) Free Cash Flow = Operating Cash Flow - CAPEX - L/T Investment

TPCC 11

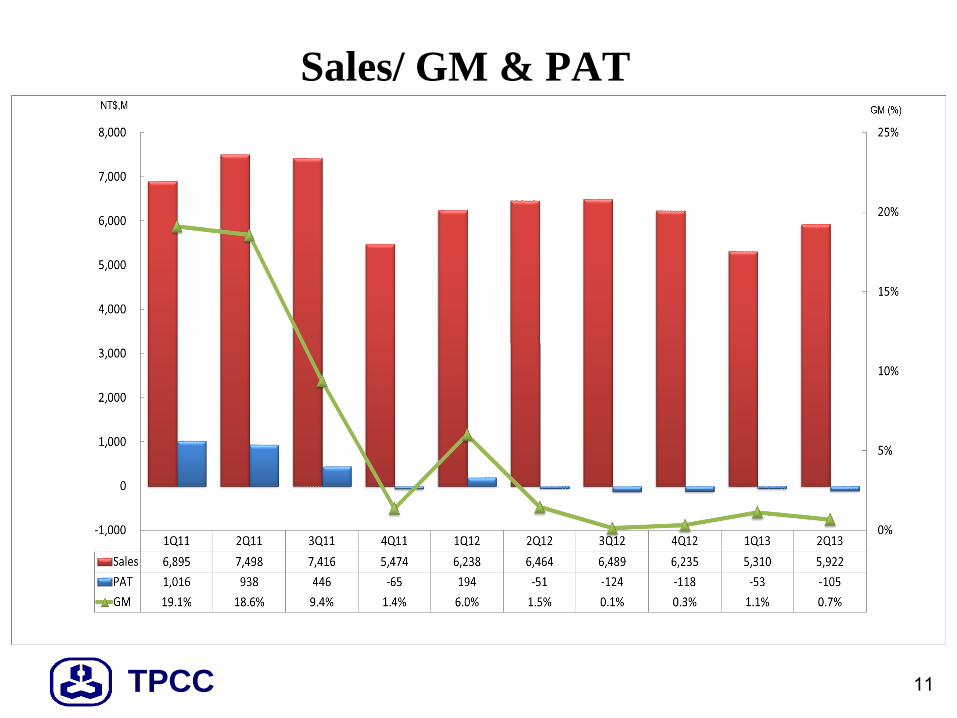

Sales/ GM & PAT

TPCC 12

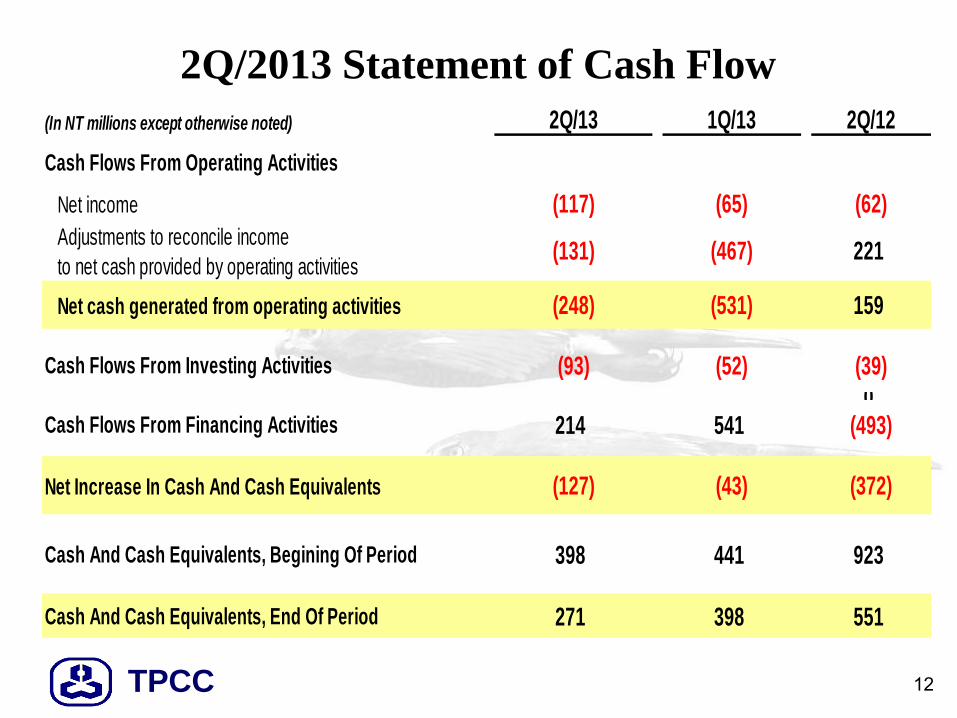

2Q/2013 Statement of Cash Flow

(In NT millions except otherwise noted) 2Q/13 1Q/13 2Q/12

Cash Flows From Operating Activities

Net income (117) (65) (62)

Adjustments to reconcile income

to net cash provided by operating activities(131) (467) 221

Net cash generated from operating activities (248) (531) 159

Cash Flows From Investing Activities (93) (52) (39)

0Cash Flows From Financing Activities 214 541 (493)

Net Increase In Cash And Cash Equivalents (127) (43) (372)

Cash And Cash Equivalents, Begining Of Period 398 441 923

Cash And Cash Equivalents, End Of Period 271 398 551

TPCC 13

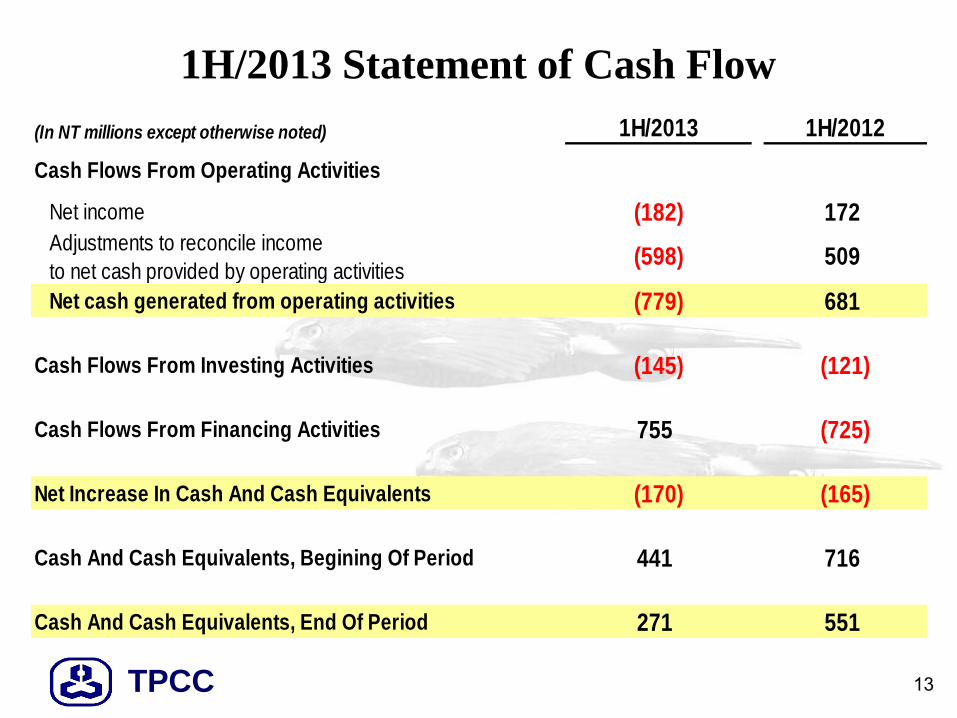

1H/2013 Statement of Cash Flow

(In NT millions except otherwise noted) 1H/2013 1H/2012

Cash Flows From Operating Activities

Net income (182) 172

Adjustments to reconcile income

to net cash provided by operating activities(598) 509

Net cash generated from operating activities (779) 681

Cash Flows From Investing Activities (145) (121)

Cash Flows From Financing Activities 755 (725)

Net Increase In Cash And Cash Equivalents (170) (165)

Cash And Cash Equivalents, Begining Of Period 441 716

Cash And Cash Equivalents, End Of Period 271 551

TPCC

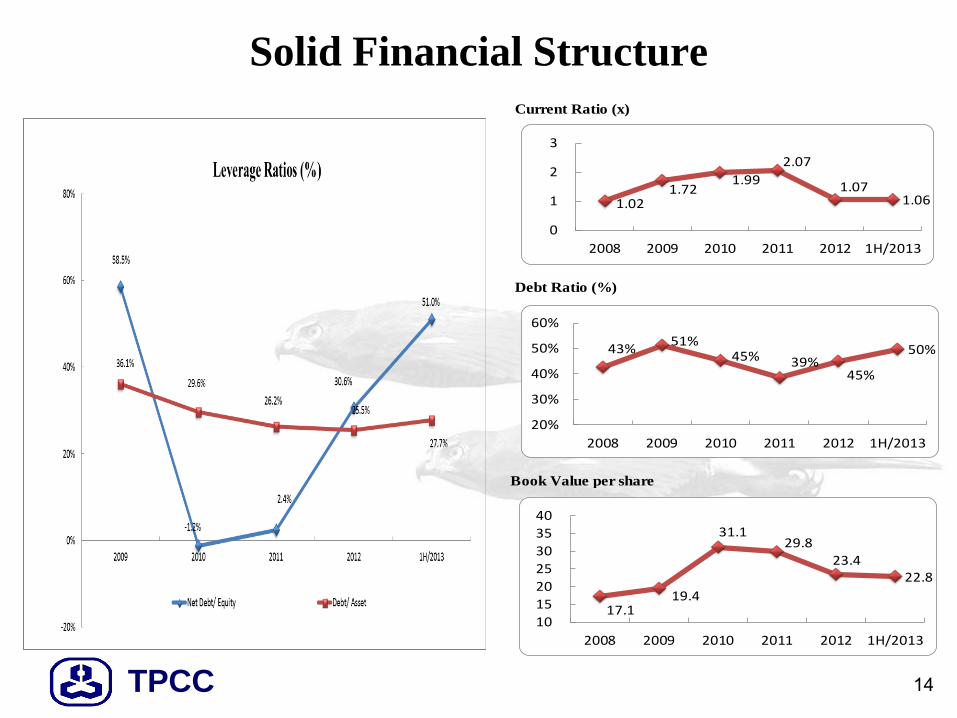

Solid Financial Structure

14

28 26 24

19 27

33

0

10

20

30

40

2007Y 2008Y 2009Y 2010Y 2011Y 1H/12

2.26

1.02

1.72 1.99

2.08

1.28

0.00

0.50

1.00

1.50

2.00

2.50

2007Y 2008Y 2009Y 2010Y 2011Y 1H/12

34% 43%

51% 45%

38%

52%

0%

20%

40%

60%

2007Y 2008Y 2009Y 2010Y 2011Y 1H/12

24.8

17.1 19.5

31.1 29.8

24.1

10.0

20.0

30.0

40.0

2007Y 2008Y 2009Y 2010Y 2011Y 1H/12

Current Ratio (x)

Debt Ratio (%)

Book Value per share

1.02 1.72

1.99

2.07

1.07 1.06

0

1

2

3

2008 2009 2010 2011 2012 1H/2013

43%51%

45% 39%45%

50%

20%

30%

40%

50%

60%

2008 2009 2010 2011 2012 1H/2013

17.119.4

31.129.8

23.422.8

10

15

20

25

30

35

40

2008 2009 2010 2011 2012 1H/2013

TPCC

Agenda

15

• Company Snapshot

• 2Q/2013 Financial Results

• Business Overview

• Capital Expenditure

• 2H/2013 Business Outlook

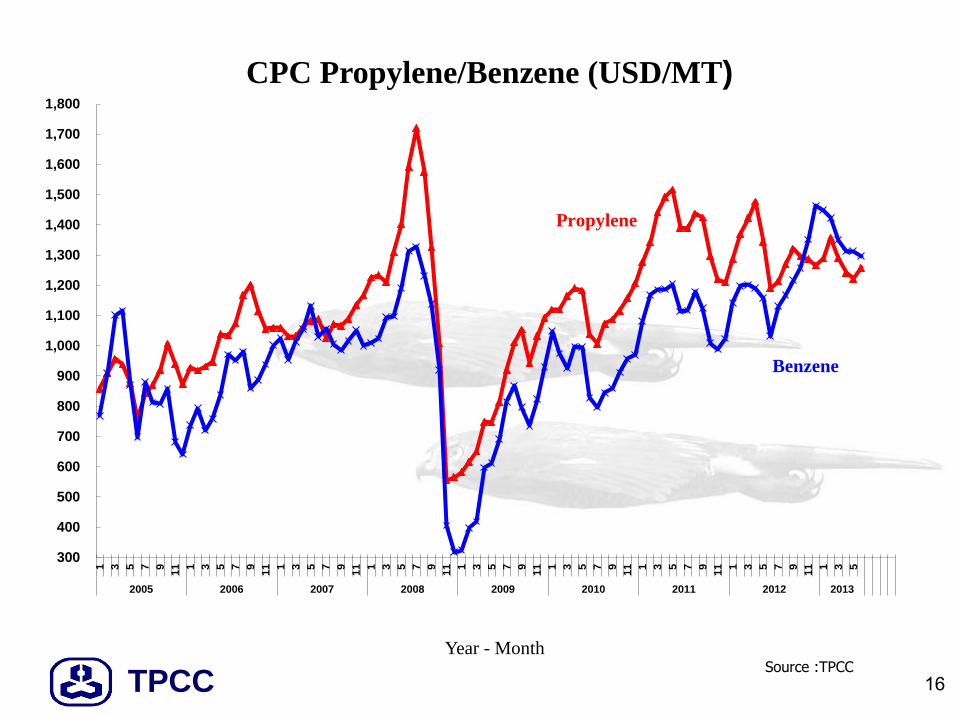

TPCC 16 Source :TPCC

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,8001 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5

2005 2006 2007 2008 2009 2010 2011 2012 2013

Year - Month

CPC Propylene/Benzene (USD/MT)

Propylene

Benzene

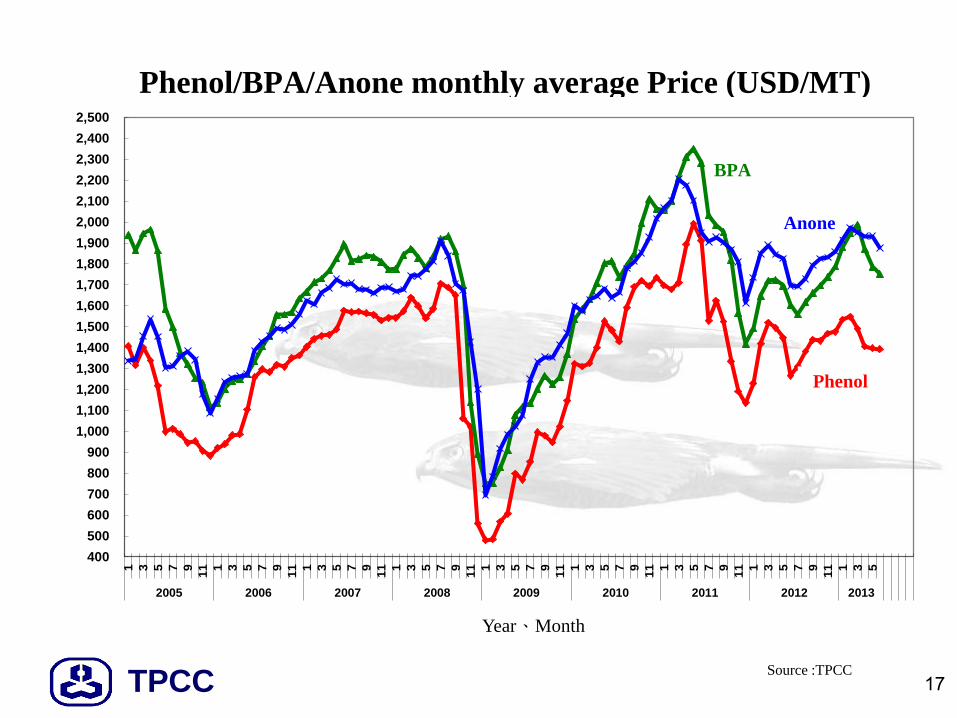

TPCC 17 Source :TPCC

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2,5001 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5 7 9

11 1 3 5

2005 2006 2007 2008 2009 2010 2011 2012 2013

Year、Month

BPA

Phenol

Anone

Phenol/BPA/Anone monthly average Price (USD/MT)

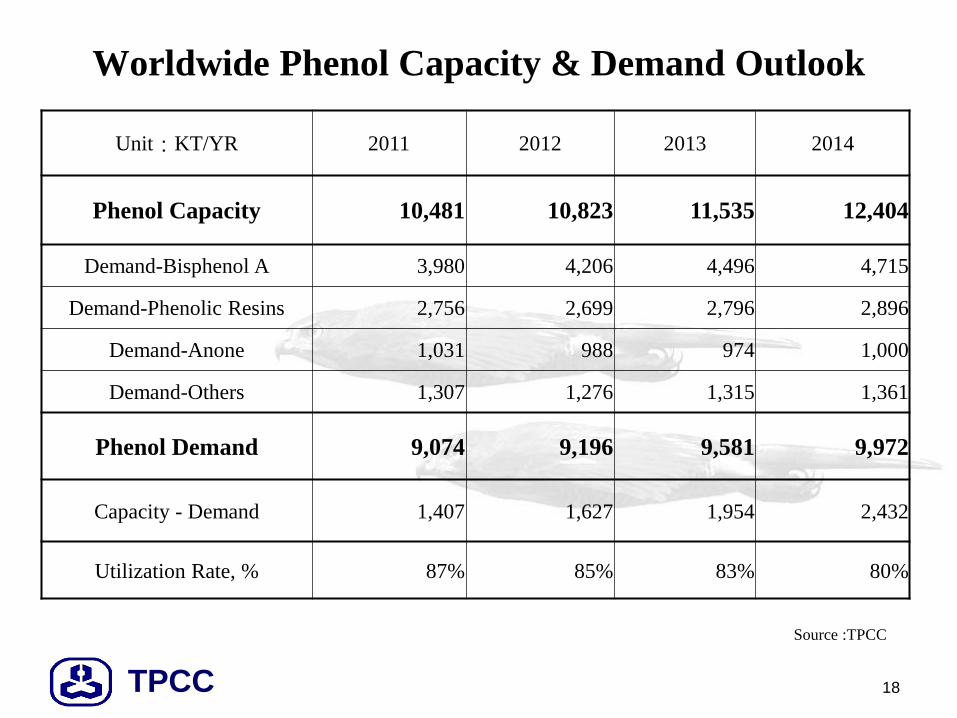

TPCC 18

Worldwide Phenol Capacity & Demand Outlook

Source :TPCC

Unit:KT/YR 2011 2012 2013 2014

Phenol Capacity 10,481 10,823 11,535 12,404

Demand-Bisphenol A 3,980 4,206 4,496 4,715

Demand-Phenolic Resins 2,756 2,699 2,796 2,896

Demand-Anone 1,031 988 974 1,000

Demand-Others 1,307 1,276 1,315 1,361

Phenol Demand 9,074 9,196 9,581 9,972

Capacity - Demand 1,407 1,627 1,954 2,432

Utilization Rate, % 87% 85% 83% 80%

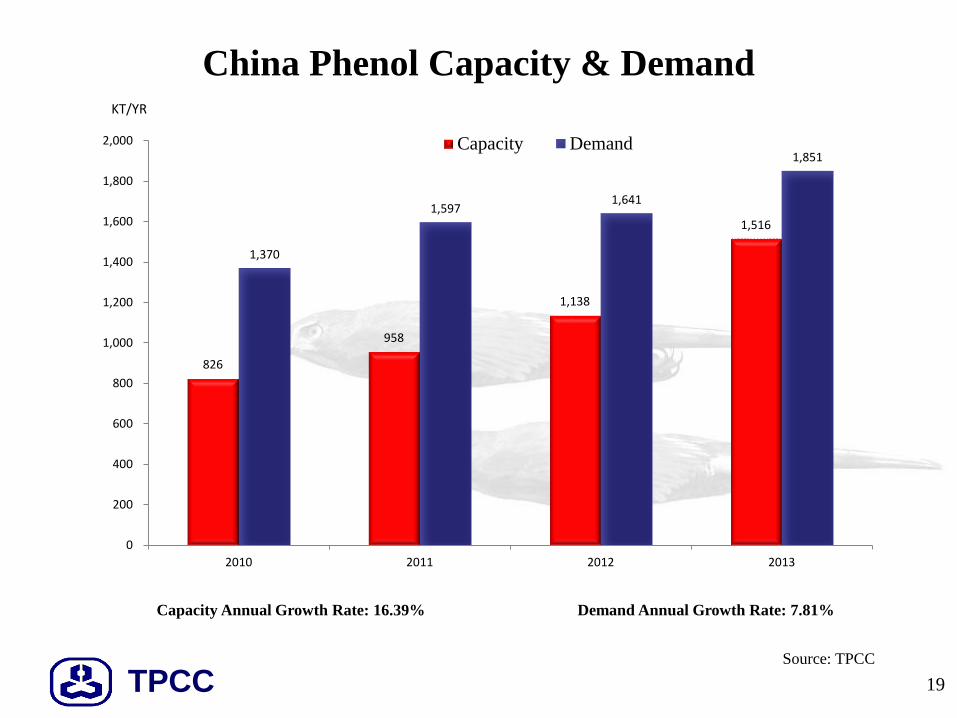

TPCC

826

958

1,138

1,516

1,370

1,597 1,641

1,851

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2010 2011 2012 2013

Capacity Demand

KT/YR

19

China Phenol Capacity & Demand

Source: TPCC

Capacity Annual Growth Rate: 16.39% Demand Annual Growth Rate: 7.81%

TPCC 20

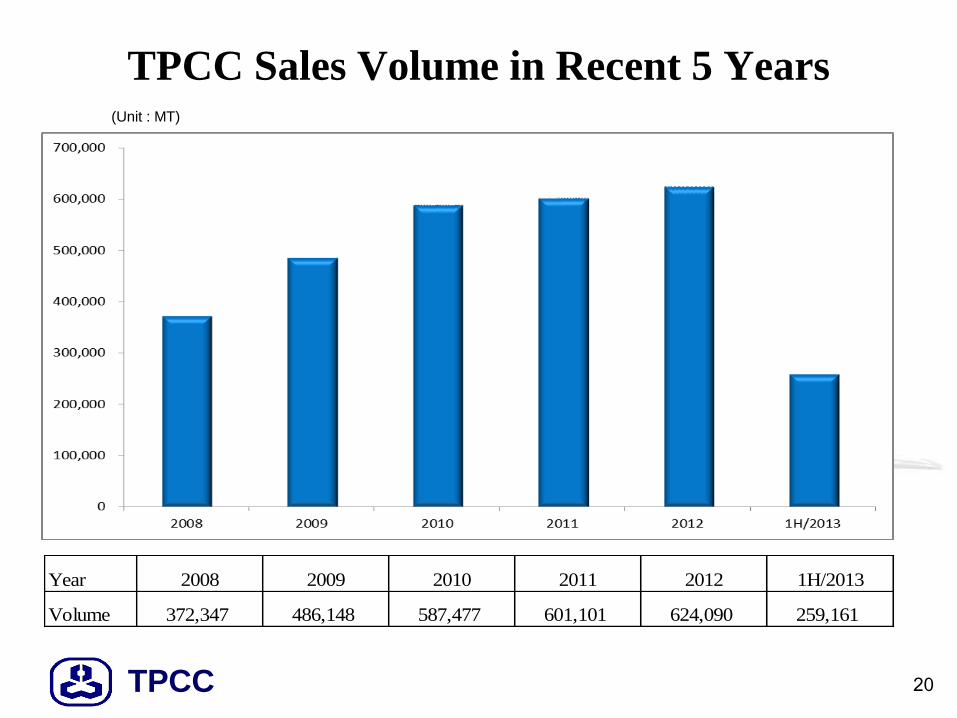

TPCC Sales Volume in Recent 5 Years (Unit : MT)

Year 2008 2009 2010 2011 2012 1H/2013

Volume 372,347 486,148 587,477 601,101 624,090 259,161

TPCC 21

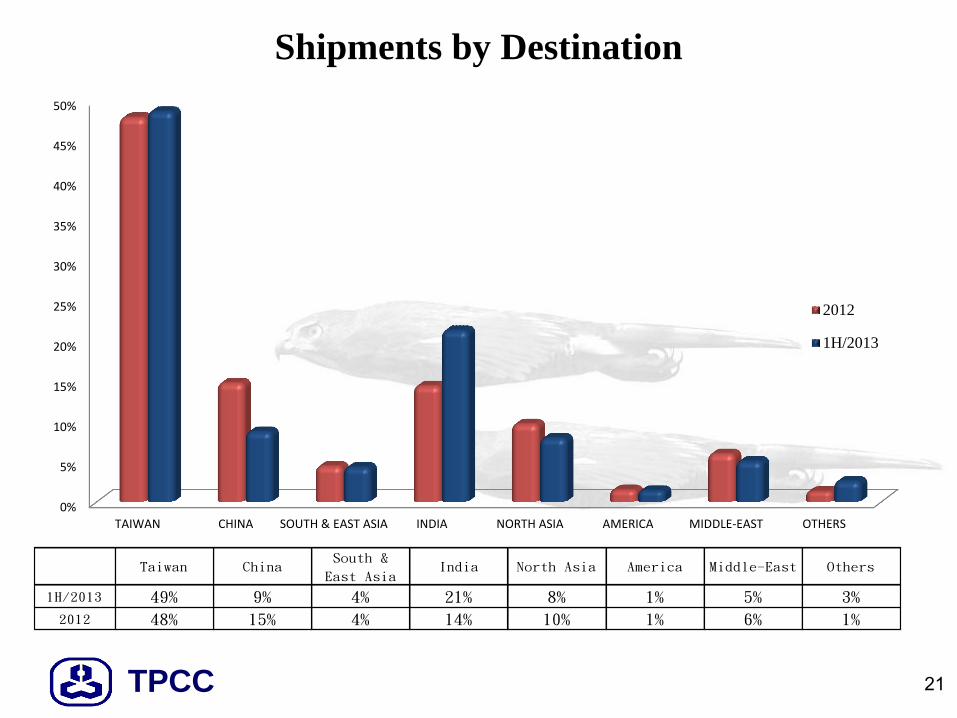

Shipments by Destination

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

TAIWAN CHINA SOUTH & EAST ASIA INDIA NORTH ASIA AMERICA MIDDLE-EAST OTHERS

2012

1H/2013

Taiwan ChinaSouth &

East AsiaIndia North Asia America Middle-East Others

1H/2013 49% 9% 4% 21% 8% 1% 5% 3%

2012 48% 15% 4% 14% 10% 1% 6% 1%

TPCC 22

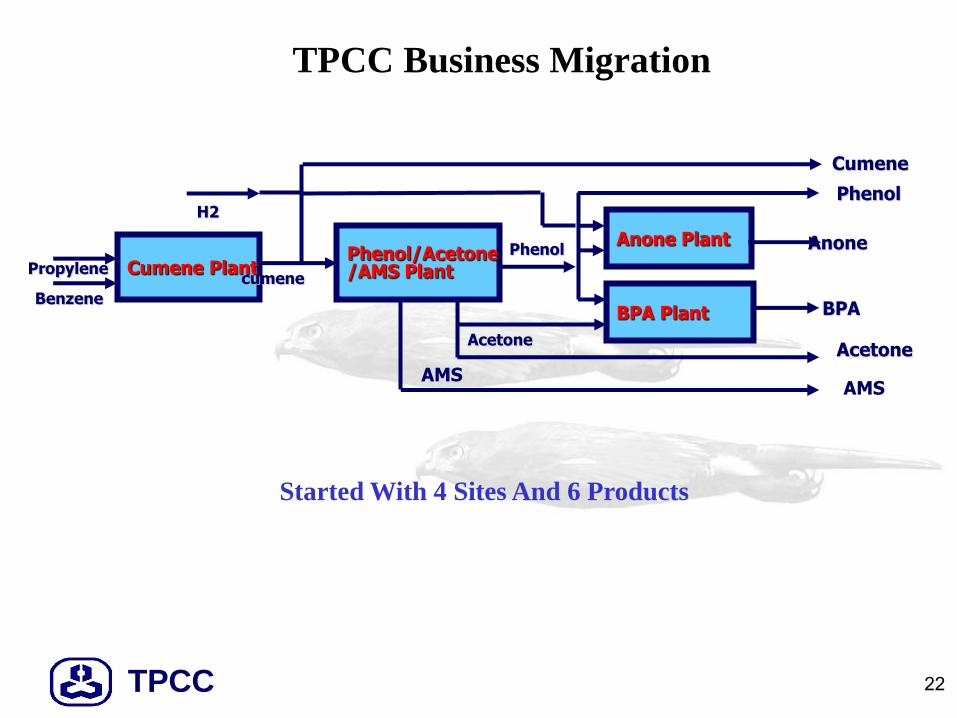

TPCC Business Migration

Cumene Plant Phenol/Acetone /AMS Plant

Anone Plant

BPA Plant

Propylene

Benzene

cumene

Phenol

Acetone

Anone

BPA

Acetone

Phenol

Cumene

AMS AMS

H2

Started With 4 Sites And 6 Products

TPCC 23

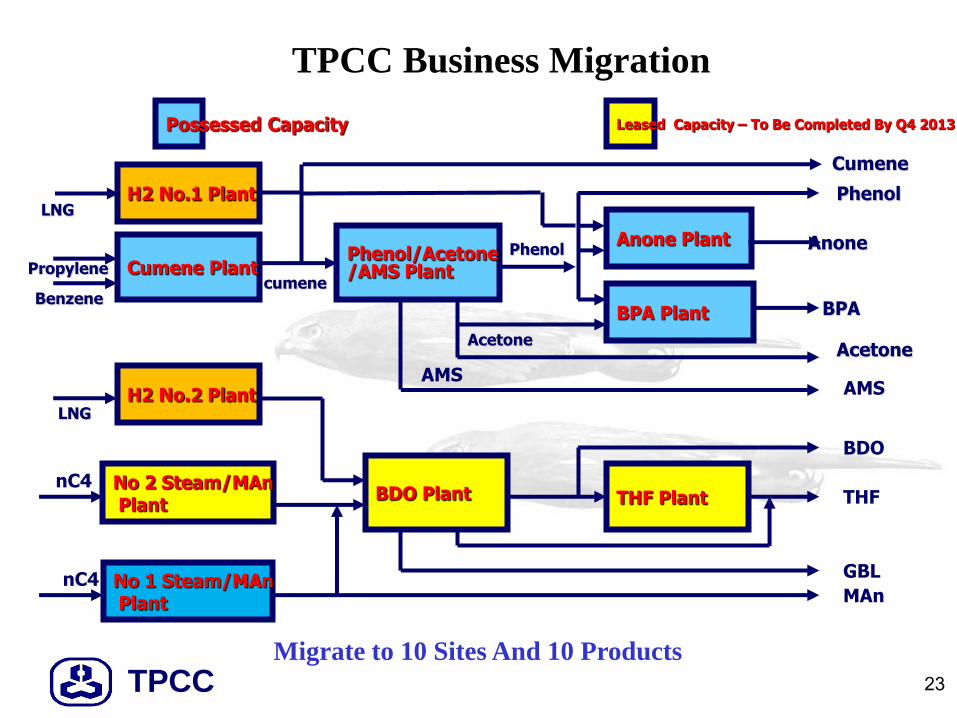

TPCC Business Migration

Cumene Plant Phenol/Acetone /AMS Plant

Anone Plant

BPA Plant

Propylene

Benzene cumene

Phenol

Acetone

Anone

BPA

Acetone

Phenol

Cumene

AMS AMS

H2 No.1 Plant

H2 No.2 Plant

No 2 Steam/MAn Plant

No 1 Steam/MAn Plant

BDO Plant THF Plant

LNG

BDO

THF

GBL

MAn

LNG

nC4

nC4

Migrate to 10 Sites And 10 Products

Possessed Capacity Leased Capacity – To Be Completed By Q4 2013

TPCC

BDO PLANT

24

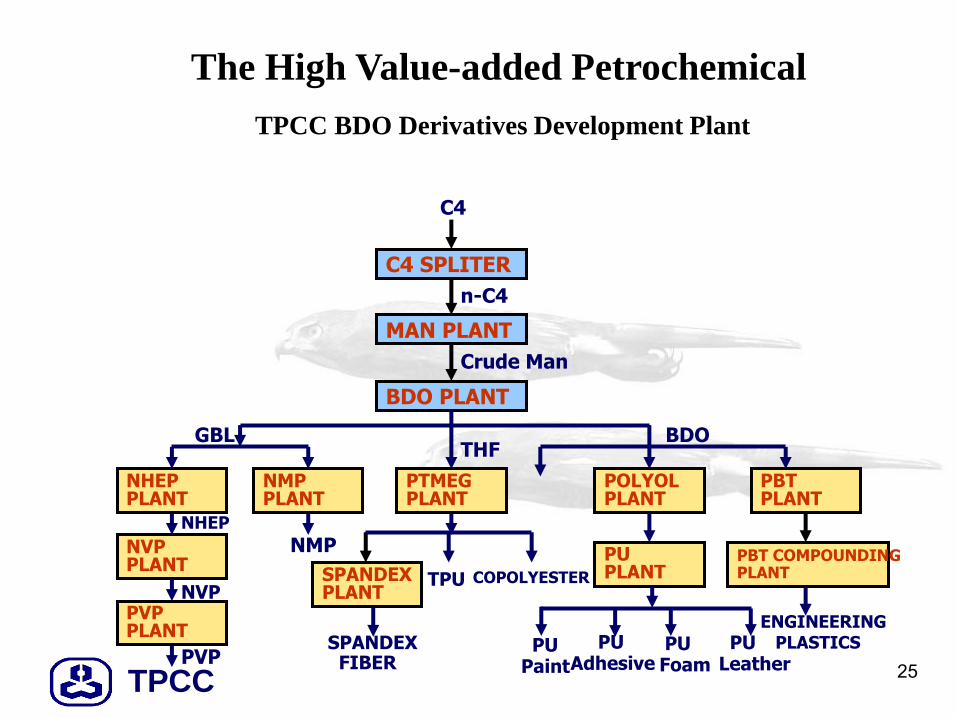

TPCC 25

TPCC BDO Derivatives Development Plant

C4 SPLITER

MAN PLANT

BDO PLANT

PTMEG PLANT

NMP PLANT

NHEP PLANT

POLYOL PLANT

PBT PLANT

C4

n-C4

Crude Man

GBL THF

BDO

NVP PLANT

PVP PLANT

PVP

NHEP

NVP

NMP

SPANDEX PLANT

TPU COPOLYESTER

SPANDEX FIBER

PU PLANT

PU Paint

PU Foam

PU Adhesive

PU Leather

PBT COMPOUNDING PLANT

ENGINEERING PLASTICS

The High Value-added Petrochemical

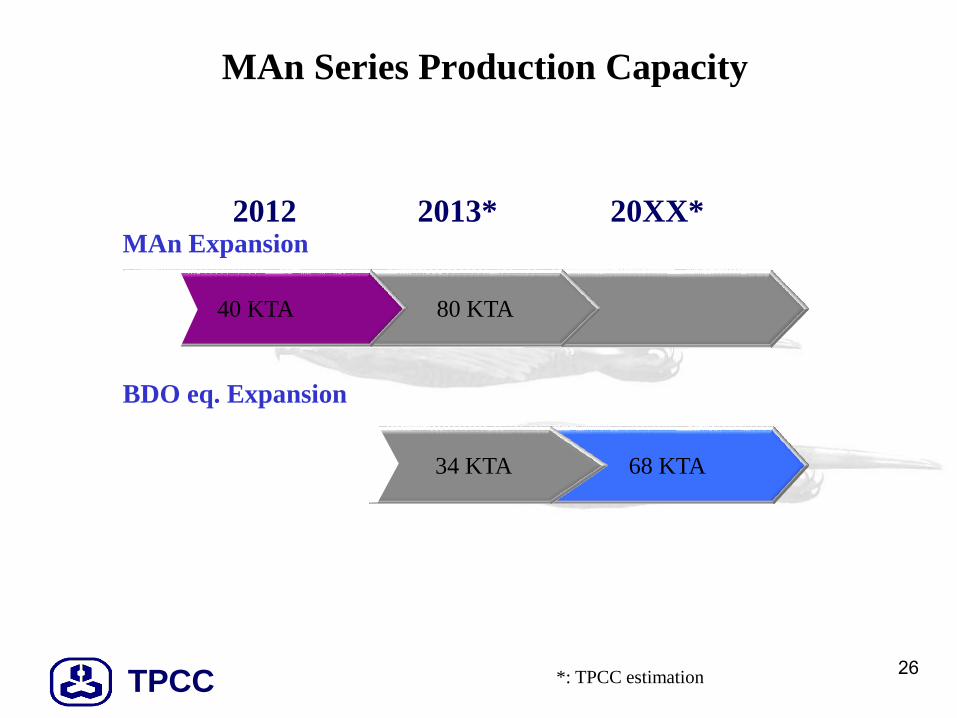

TPCC 26

MAn Series Production Capacity

2013* 2012 20XX*

80 KTA 40 KTA

BDO eq. Expansion

68 KTA 34 KTA

MAn Expansion

*: TPCC estimation

TPCC

Agenda

27

• Company Snapshot

• 2Q/2013 Financial Results

• Business Overview

• Capital Expenditure

• 2H/2013 Business Outlook

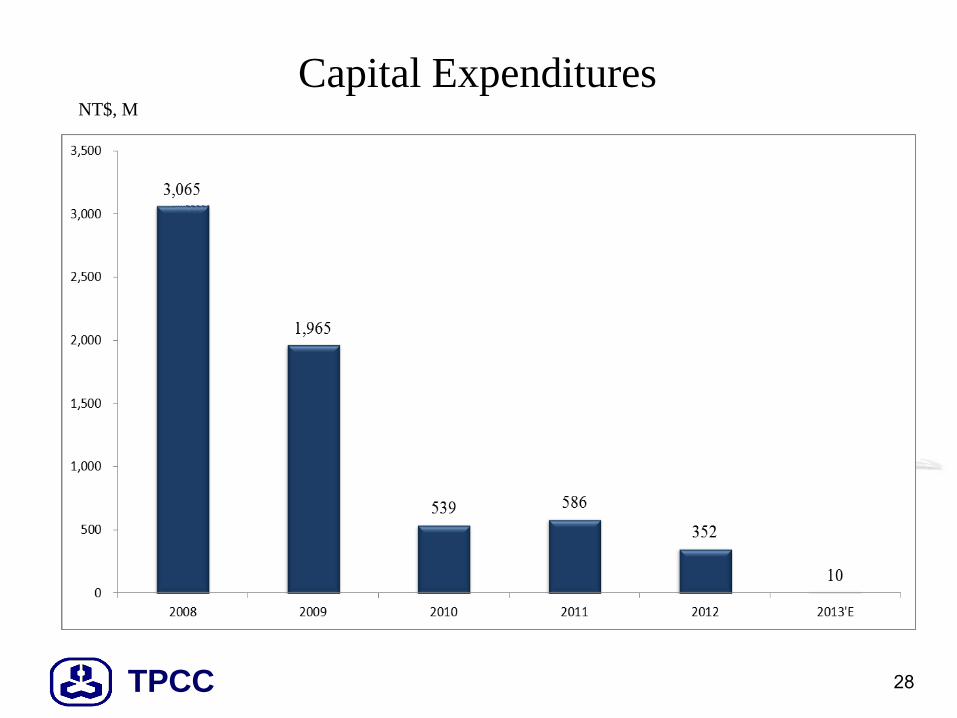

TPCC

Capital Expenditures

28

NT$, M

TPCC

Agenda

29

• Company Snapshot

• 2Q/2013 Financial Results

• Business Overview

• Capital Expenditure

• 2H/2013 Business Outlook

TPCC 30

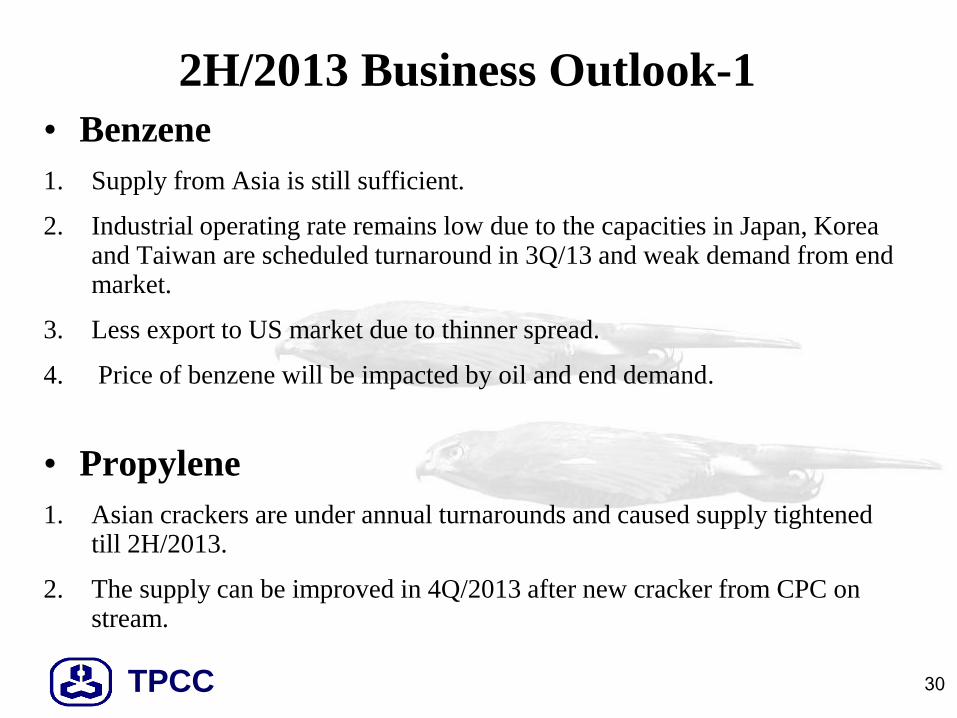

2H/2013 Business Outlook-1

• Benzene

1. Supply from Asia is still sufficient.

2. Industrial operating rate remains low due to the capacities in Japan, Korea and Taiwan are scheduled turnaround in 3Q/13 and weak demand from end market.

3. Less export to US market due to thinner spread.

4. Price of benzene will be impacted by oil and end demand.

• Propylene

1. Asian crackers are under annual turnarounds and caused supply tightened till 2H/2013.

2. The supply can be improved in 4Q/2013 after new cracker from CPC on stream.

TPCC 31

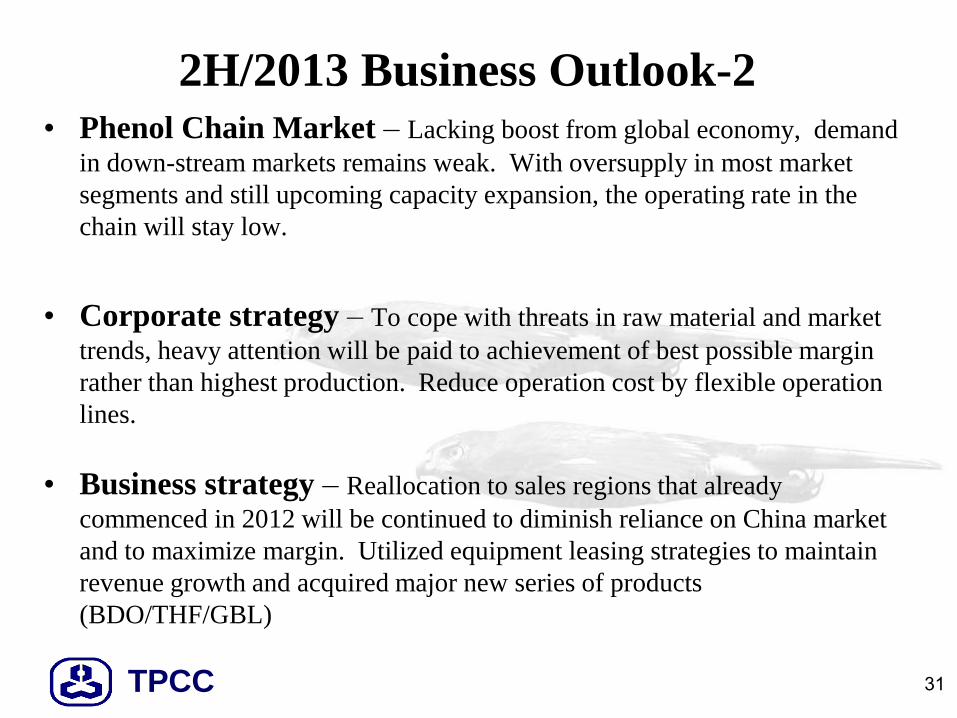

2H/2013 Business Outlook-2 • Phenol Chain Market – Lacking boost from global economy, demand

in down-stream markets remains weak. With oversupply in most market

segments and still upcoming capacity expansion, the operating rate in the

chain will stay low.

• Corporate strategy – To cope with threats in raw material and market

trends, heavy attention will be paid to achievement of best possible margin

rather than highest production. Reduce operation cost by flexible operation

lines.

• Business strategy – Reallocation to sales regions that already

commenced in 2012 will be continued to diminish reliance on China market

and to maximize margin. Utilized equipment leasing strategies to maintain

revenue growth and acquired major new series of products

(BDO/THF/GBL)

TPCC

Thank You

32